Embed Size (px)

Citation preview

________________________________

Prepared by Joseph S.Samaha (CPA)

1

Hospitals Financial Accounting Basics

Presentation prepared by

Joseph S.SamahaMember of The AICPA-IIA-IMA-LACPA-AOCPA

Quality Management Systems – Internal Auditing

Sworn by Lebanese Courthouses since 1984

To the LACPA CPE program – April 2007

________________________________

Prepared by Joseph S.Samaha (CPA)

2

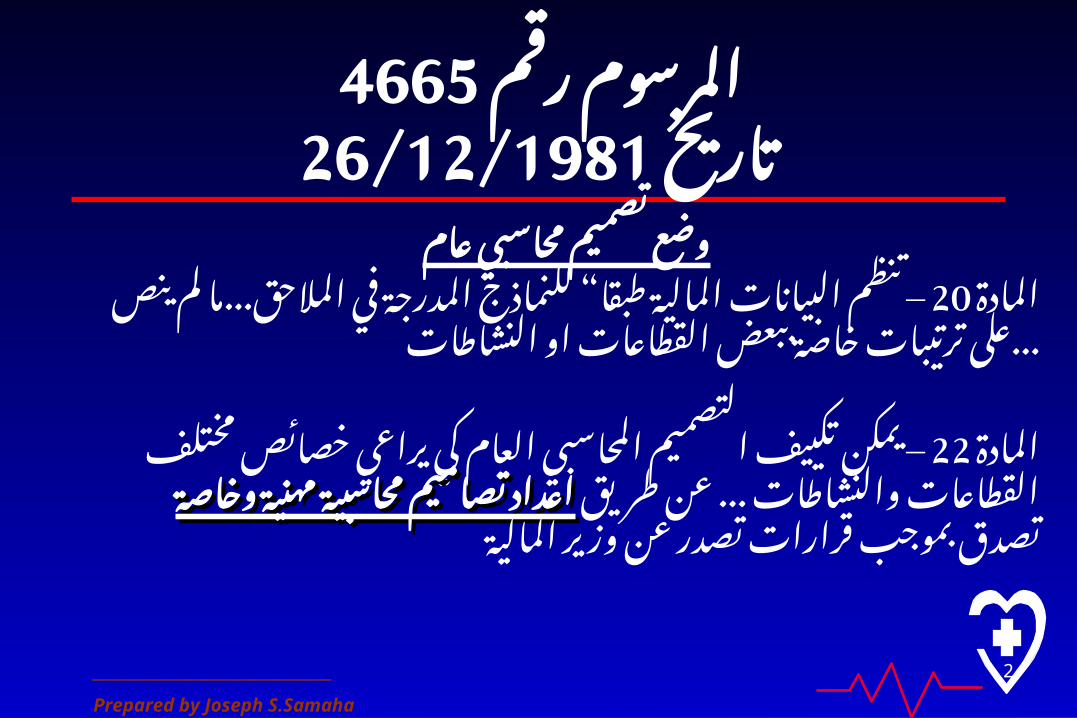

رقم 4665المرسوم26/12/1981تاريخ

عام محاسبي تصميم وضع“ 20المادة في – المدرجة للنماذج طبقا المالية البيانات تنظم

او... القطاعات ببعض خاصة ترتيبات على ينص لم ما المالحق...النشاطات

يراعي – 22المادة كي العام المحاسبي التصميم تكييف يمكنطريق ... عن والنشاطات القطاعات مختلف اعداد اعداد خصائص

وخاصة مهنية محاسبية وخاصة تصاميم مهنية محاسبية تصدر تصاميم قرارات بموجب تصدقالمالية وزير عن

________________________________

Prepared by Joseph S.Samaha (CPA)

3

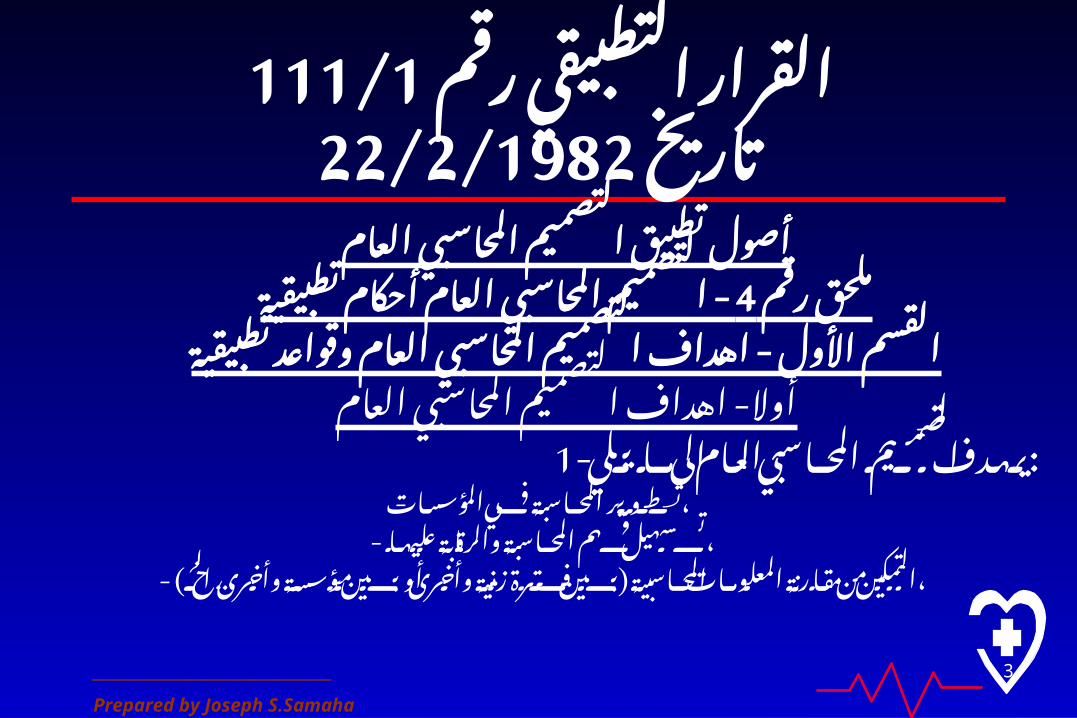

رقم التطبيقي 111/1القرار22/2/1982تاريخ

العام المحاسبي التصميم تطبيق أصولرقم تطبيقية - 4ملحق أحكام العام المحاسبي التصميم

وقواعد - العام المحاسبي التصميم اهداف األول القسمتطبيقية

العام- المحاسبي التصميم اهداف أواليلي -1 ما الى العام المحاسبي التصميم :يهدف

المؤسسات - في المحاسبة ،تطويرعليها - والرقابة المحاسبة فهم ،تسهيل

- ) ... الخ ) وأخرى مؤسسة بين أو وأخرى زمنية فترة بين المحاسبية المعلومات مقارنة من ،التمكين

________________________________

Prepared by Joseph S.Samaha (CPA)

4

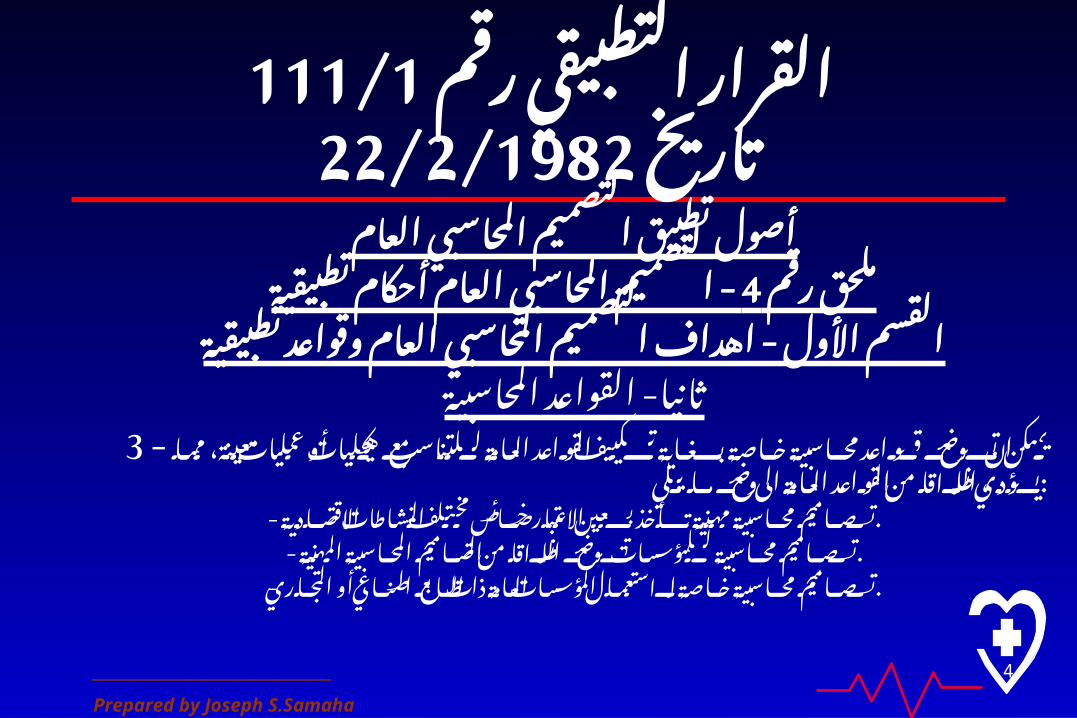

رقم التطبيقي 111/1القرار22/2/1982تاريخ

العام المحاسبي التصميم تطبيق أصولرقم تطبيقية - 4ملحق أحكام العام المحاسبي التصميم

وقواعد - العام المحاسبي التصميم اهداف األول القسمتطبيقية

المحاسبية- القواعد ثانياأو - 3 هيكليات مع للتناسب العامة القواعد تكييف بغاية خاصة محاسبية قواعد توضع ان يمكن

يلي ما وضع الى العامة القواعد من انطالقا يؤدي، مما معينة، :عملياتاالقتصادية - النشاطات مختلف خصائص االعتبار بعين تأخذ مهنية محاسبية .تصاميم

المهنية - المحاسبية التصاميم من انطالقا توضع للمؤسسات محاسبية .تصاميمالتجاري - أو الصناعي الطابع ذات العامة المؤسسات الستعمال خاصة محاسبية .تصاميم

________________________________

Prepared by Joseph S.Samaha (CPA)

5

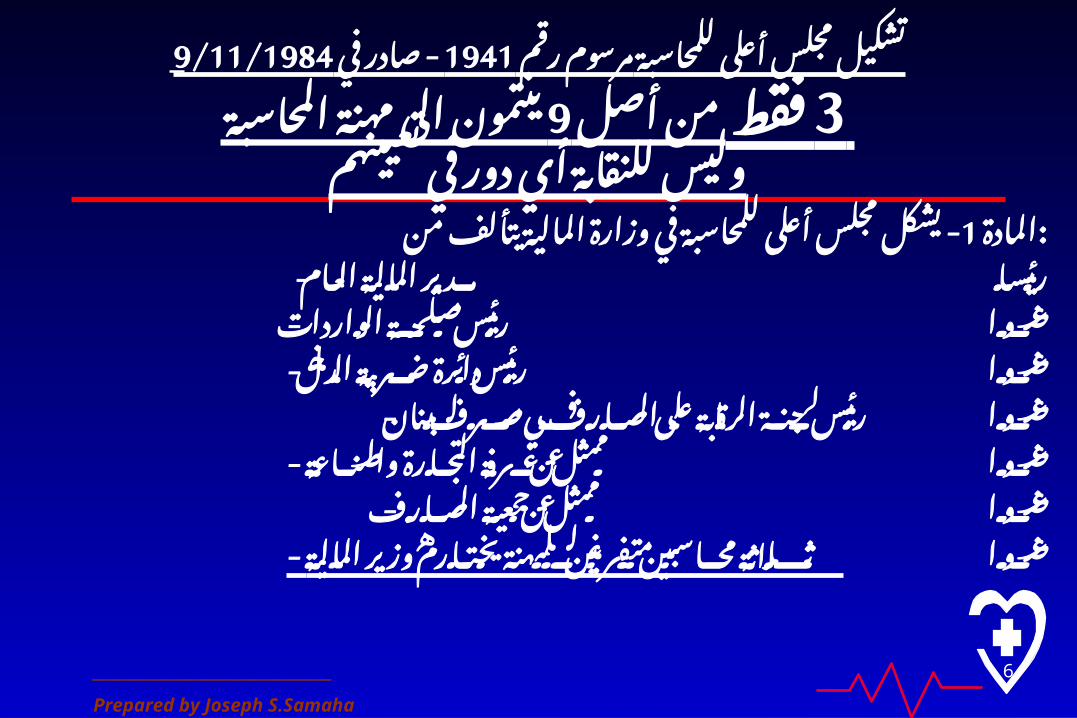

للمحاسبة مجلسأعلى رقم تشكيل صادر - 1941مرسوم 9/11/1984في

قطاعي لبرنامج توصية المجلسأي يصدر لملتاريخه

التالية- 2المادة المهمات المجلساالعلى يتولى :والوضعيات - المالية البيانات ونماذج المحاسبية القواعد وضع على االشراف

واالنظمة القوانين مختلف في المنصوصعنها والحسابية .االحصائيةالعام - المحاسبي التصميم على دوريا ادخالها الواجب التعديالت اقتراح

القانون التطور مع لتتوافق والمهنية القطاعية المحاسبية والتصاميم.والتقني

النشاطات - خصائصبعض مع تتناسب فرعية محاسبية تصاميم وضع اقتراحالعام المحاسبي للتصميم األساسي االطار .ضمن

كفاءة - ورفع المحاسبة مهنة لتنظيم الالزمة والتوصيات االقتراحات تقديمالمحاسبي .العمل

________________________________

Prepared by Joseph S.Samaha (CPA)

6

للمحاسبة مجلسأعلى رقم تشكيل صادر - 1941مرسوم 9/11/1984في

أصل فقط 3 مهنة 9من الى ينتمونالمحاسبة

تعيينهم في دور أي للنقابة وليس يتألفمن- 1المادة المالية وزارة في للمحاسبة مجلسأعلى يشكل :

العام - المالية مدير رئيساالواردات - رئيسمصلحة عضواالدخل - ضريبة رئيسدائرة عضوا

لبنان - مصرف المصارففي على الرقابة رئيسلجنة عضواوالصناعة - التجارة غرفة عن ممثل عضواالمصارف - جمعية عن ممثل عضوا

المالية - وزير يختارهم للمهنة متفرغين محاسبين ثالثةعضوا

________________________________

Prepared by Joseph S.Samaha (CPA)

7

والقرارات المراسيم الئحةالمتعلقة

الحسابات بتصميم

________________________________

Prepared by Joseph S.Samaha (CPA)

8

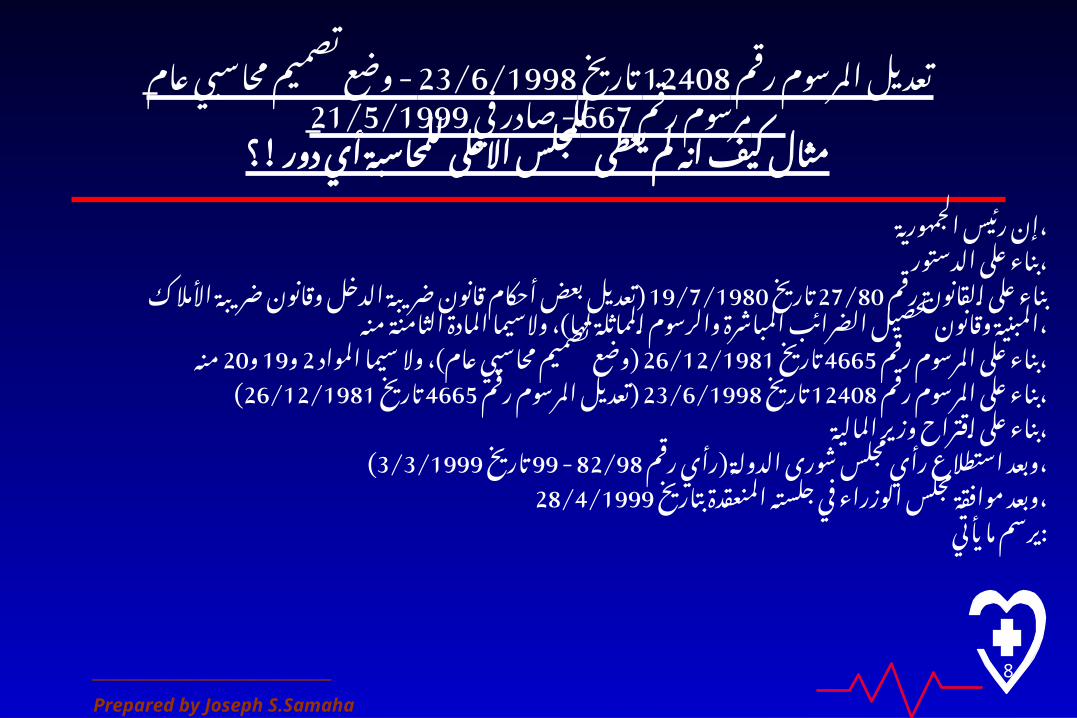

رقم المرسوم محاسبي - 23/6/1998تاريخ 12408تعديل تصميم وضع عام

رقم في - 667مرسوم 21/5/1999صادرأي للمحاسبة للمجلساالعلى يعطى لم انه كيف مثال

؟ ! دورالجمهورية رئيس ،إنالدستور على ،بناء

رقم القانون على وقانون ) 19/7/1980تاريخ 27/80بناء الدخل ضريبة قانون أحكام بعض تعديل ) المادة والسيما ، لها المماثلة والرسوم المباشرة الضرائب تحصيل وقانون المبنية األمالك ضريبة

منه ،الثامنةرقم المرسوم على ( 26/12/1981تاريخ 4665بناء المواد ) سيما وال ، عام محاسبي تصميم وضع

منه 20و 19و 2 ،رقم المرسوم على رقم ) 23/6/1998تاريخ 12408بناء المرسوم (26/12/1981تاريخ 4665تعديل ،

المالية وزير اقتراح على ،بناءرقم ) رأي الدولة مجلسشورى رأي استطالع (3/3/1999تاريخ 99 - 82/98وبعد ،

بتاريخ المنعقدة جلسته في الوزراء مجلس موافقة 28/4/1999وبعد ،يأتي ما :يرسم

________________________________

Prepared by Joseph S.Samaha (CPA)

9

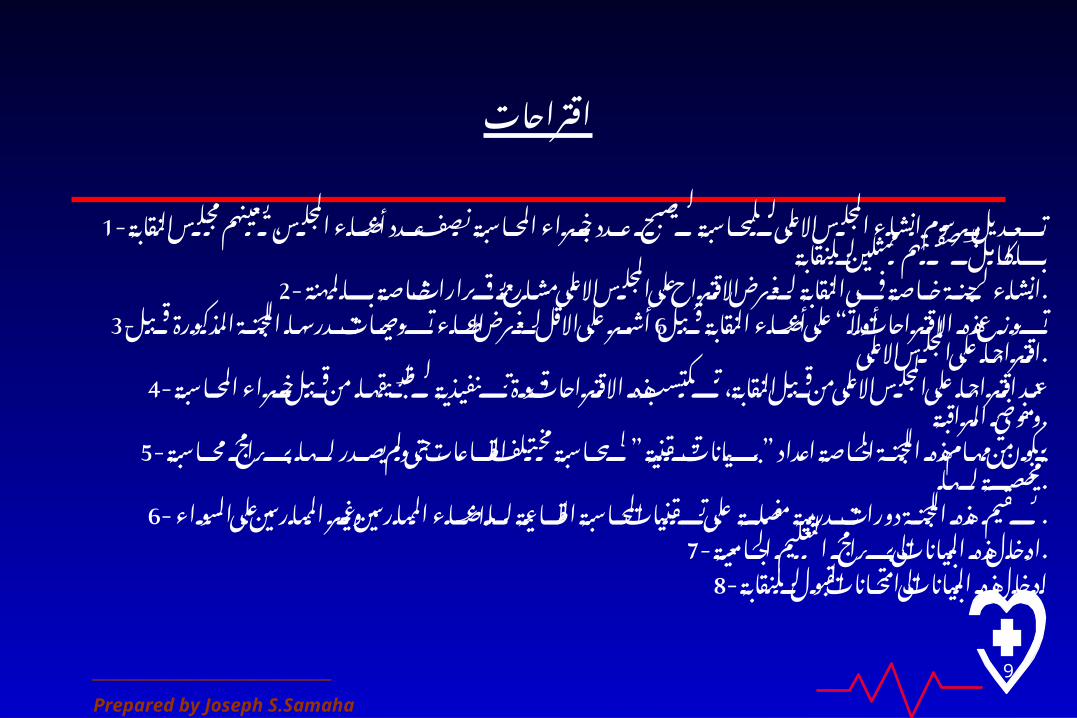

اقتراحات

المجلس، -1 أعضاء عدد نصف المحاسبة خبراء عدد ليصبح للمحاسبة االعلى المجلس انشاء مرسوم تعديلللنقابة ممثلين بصفتهم بالكامل النقابة مجلس يعينهم

بالمهنة -2 خاصة قرارات مشاريع االعلى المجلس على االقتراح لغرض النقابة في خاصة لجنة .انشاء3- “ قبل النقابة أعضاء على أوال االقتراحات هذه تدرسها 6توزع توصيات اعطاء لغرض االقل على أشهر

االعلى المجلس على اقتراحها قبل المذكورة .اللجنةمن -4 لتطبيقها تنفيذية قوة االقتراحات هذه تكتسب النقابة، قبل من االعلى المجلس على اقتراحها عند

المراقبة ومفوضي المحاسبة خبراء .قبليصدر ” ” -5 ولم حتى ، القطاعات مختلف لمحاسبة تقنية بيانات اعداد الخاصة اللجنة هذه مهام من يكون

لها مخصصة محاسبة برامج .لهاوغير -6 الممارسين لالعضاء القطاعية المحاسبة تقنيات على مفصلة تدريبية دورات اللجنة هذه تقيم

السواء على . الممارسينالجامعية -7 التعليم برامج الى البيانات هذه .ادخالللنقابة -8 القبول امتحانات الى البيانات هذه ادخال

________________________________

Prepared by Joseph S.Samaha (CPA)

10

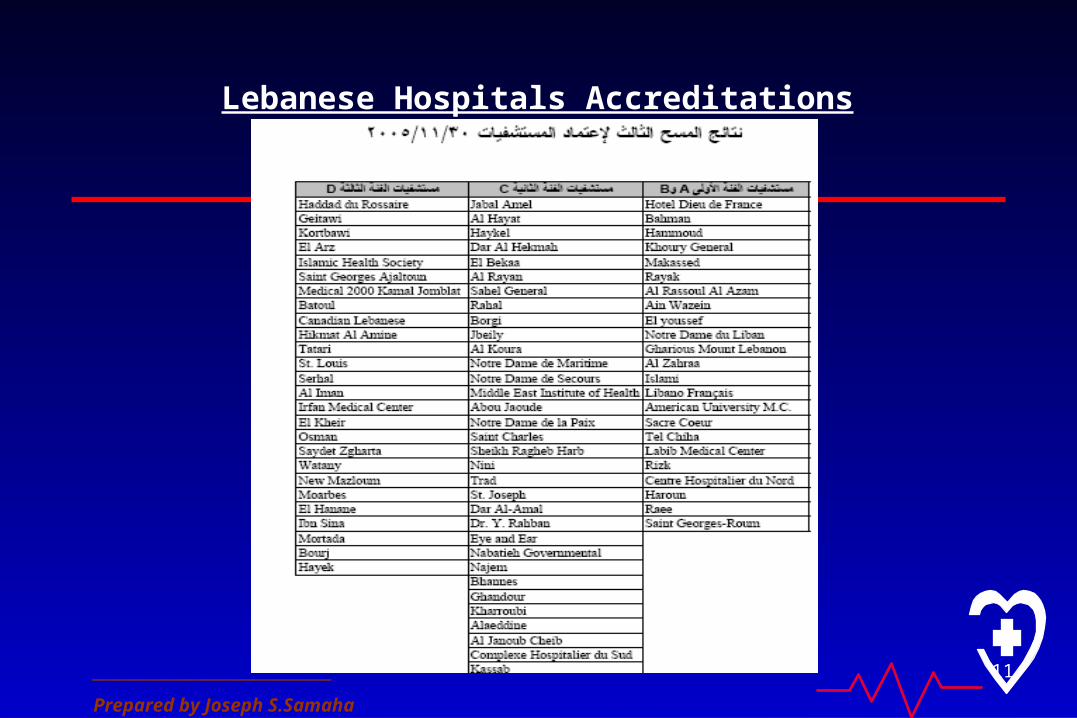

لبنان في المستشفيات تصنيف جدول مقدمةالعامة الصحة وزارة عام مدير كتبها

المستشفيات اعتماد المتقدمة Accreditationان الدول في المعتمدة المشاريع من واحد هو . لمشروع الوحيدة الغاية يشكل الجودة فضمان االستشفائية الخدمات جودة لضمان

مراكز. أم مختبرات أم مستشفيات، أكانت المعنية المؤسسات ان c دوليا المعروف ومن االعتماد . ان d إال منه األول المستفيد كونها اإلعتماد بعملية تقوم التي هي غيرها أم طبي تصوير

بهذا القيام الى تبادر لم لبنان في اإلستشفائي القطاع معظم تشكل التي الخاصة المؤسساتالصحة. وزارة اخذت المواطنين، صحة على مباشرة ينعكس الجودة ضمان ان وبما المشروع

. بأن لنا تبين ان بعد وذلك المسؤولية هذه الراهنة المرحلة في عاتقها على القطاع العامة هائلة وبشرية مادية قدرات يملك هذه اإلستشفائي مع c أبدا تتناسب ال الخدمات نوعية وبأن

بأن. الخبراء يفيد بحيث االعتماد، تجربة برهنته ما وهذا حققت القدرات اإلستشفائية الخدماتسنوات خمس تتعدى ال وجيزة بفترة هائلة نوعية c قفزة ممكنا كان ما السريع التطور هذا وان ،

. لذلك الالزمة المقومات األساس من تمتلك المؤسسات هذه تكن لم حقيقة لو يؤكد وهذاالمستشفيات عدم لموارد الرشيد تعانيه االستعمال كانت الذي والتراخي

السابق في المؤسسات بأنها. هذه يعني ال فذلك المبادرة زمام اخذت قد الوزارة كانت واذااعطاء الى هدفت انها بل تكاليفها، وتحمل االعتماد بعملية بالقيام مسمى غير أجل الى ستستمر

. هذه ترى وعندما بالمتابعة المعنية المؤسسات تقوم ان بانتظار االتجاه بهذا قوية دفعةوتكتفي بذلك الوزارة ترحب سوف المشروع هذا استكمال على قادرة نفسها المؤسسات

. التنفيذ حسن بمراقبة

________________________________

Prepared by Joseph S.Samaha (CPA)

11

Lebanese Hospitals Accreditations

________________________________

Prepared by Joseph S.Samaha (CPA)

12

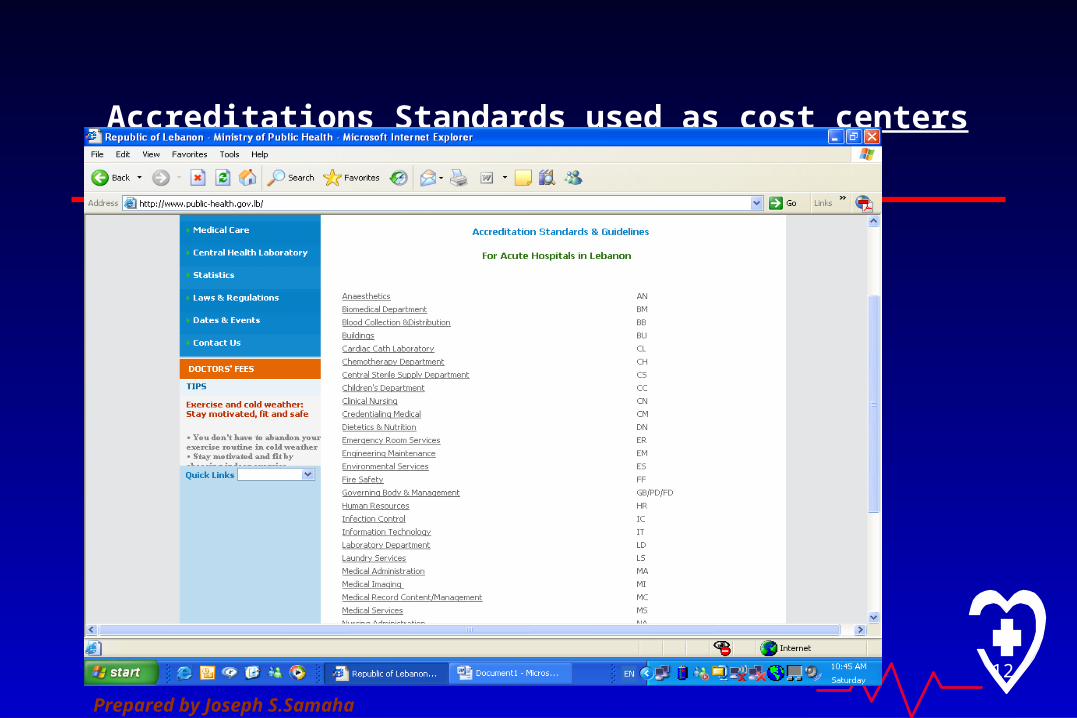

Accreditations Standards used as cost centers

________________________________

Prepared by Joseph S.Samaha (CPA)

13

رقم التعميم من وزارة 56فقرات عام مدير عن الصادرالصحة

10/5/2005بتاريخ

:\ إحترام أوال على السهر المالي إن مع السقف بالعقد المحدد . يوجب ذلك أن i إال المراقب الطبيب عمل في أولوية يعتبر المستشفى

خارج معالجتها يمكن حاالت إدخال على الموافقة عدم c أوالأكثر المستشفى داخل المرضى بإبقاء السماح عدم c وثانيا المستشفى،

. التدابير هذه إن الصحي وضعهم يستدعيها التي الضرورية الفترة منالمخصص اإلعتماد وتوفير المجدي غير اإلنفاق من الحد شأنها من

منها الطارئ وخاصة الضرورية الحاالت .لمعالجة:\ ووضعه ثانيا المريض هوية من التأكد المراقب الطبيب على يتوجب

. توقيع عدم عليه كما المناسب الطبي والعمل التشخيص ودقة الصحيالملف في الملحوظة العالجات تلقي حقيقة من التثبت قبل الجداول

بالفواتير والواردة .الطبي

________________________________

Prepared by Joseph S.Samaha (CPA)

14

اقتراحات

بالمستشفيات خاص محاسبة برنامج اصدار بعدالخيرية -1 والمنظمات للجمعيات التابعة المستشفيات اخضاع

مراقبة مفوضي تعيين وجوب الى الحكومية .وتلك

الضامنة -2 الرسمية والهيئات الصحة وزارة الى اقتراح تقديمهذه حسابات صحة لتدقيق محاسبة خبراء مع بالتعاقد االخرى

المستشفيات لدى .الهيئاتSpecial Assignment/Attestation Function

االولى -3 الفئة من المستشفيات على داخلية رقابة انشاء .ضرورة

Internal Audit Dept.

________________________________

Prepared by Joseph S.Samaha (CPA)

15

Hospital Main Functions 1/2

Hospitals generally have three main functions: patient care, teaching, and research.

The most important of these is patient care.

Patient care comprises all activities involving the provision of care to patients who arrive at the hospital or are treated elsewhere by the

hospital staff.Patient care itself has three main components – outpatient, day care and

inpatient care.Further subdivisions can be made according to clinical area

________________________________

Prepared by Joseph S.Samaha (CPA)

16

Hospital Main Functions 2/2

Patient care services are supported by several important intermediary medical functions (notably pharmaceutics and diagnostic facilities).

And patient care, research, and training all need the back-up of administrative and logistical support.

Services such as laundry, catering, maintenance, transport, and personnel management are essential to the smooth running of the hospital.

Some activities do not fit neatly into these categories and some (such as the emergency department services) cut across all the subclasses.

________________________________

Prepared by Joseph S.Samaha (CPA)

17

Measures of Service Output

Many different kinds of indicators can be used to measure the output or volume of services provided.

They can be broad and general (e.g., number of patients admitted to hospital) or quite precise (e.g., the number of brain surgeries

performed). The general indicators have the advantage that they can be used to

measure the output from a number of different centers. The more precise indicators can be tailored to particular centers, much depends on how detailed the costing exercise and management analysis

is and whether comparisons between different centers are required.

________________________________

Prepared by Joseph S.Samaha (CPA)

18

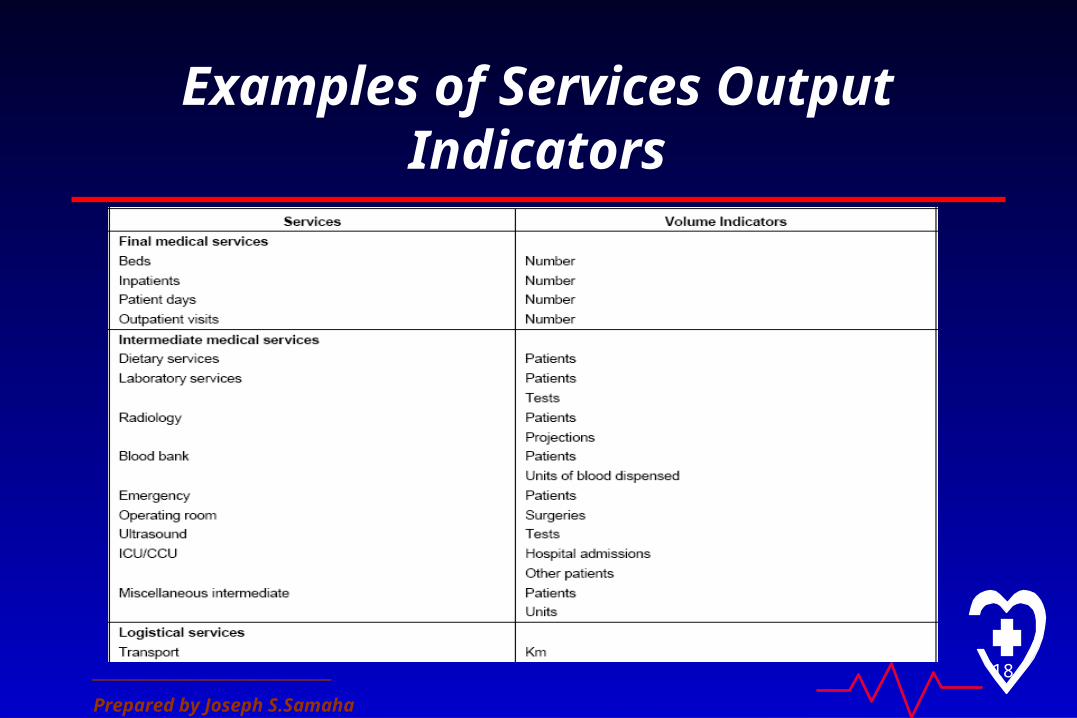

Examples of Services Output Indicators

________________________________

Prepared by Joseph S.Samaha (CPA)

19

A Cost Center

A cost center is a unit that creates one product or a range of similar services or products using common mixes of

resources and production methods.

The operating room is one example. The outpatient clinic, blood bank, clinical laboratory, and inpatient care

department are others.

________________________________

Prepared by Joseph S.Samaha (CPA)

20

Principles for identifying Cost Centers1/3

There are no hard and fast rules about defining cost centers but there are some useful principles to bear in mind.

A single classification system will require some compromise, because not all these principles can be addressed simultaneously.

The exercise should be useful to managers and evaluators. For this to be the case, cost centers should group together activities that have

some kind of management autonomy and common inputs including designated staff and space.

________________________________

Prepared by Joseph S.Samaha (CPA)

21

Principles for identifying Cost Centers2/3

Cost centers should be defined in such a way as to capitalize on an existing sense of identify among hospital workers.

This makes it easier to generate a collaborative response to a cost-relatedproblem and any proposed improvement plan.

Similarly, taking account of the way the hospital is defined or identified by patients, the community, and payers, and the kind of services likely to attract the attention of any of these groups makes the management accounting system more responsive to issues

that might arise.Cost centers should be associated with a single product or service. This principle

allows for an average cost per unit of service to be calculated in a given clinical department by dividing the full departmental costs by the total number of output

units.

________________________________

Prepared by Joseph S.Samaha (CPA)

22

Principles for identifying Cost Centers3/3

Cost centers should usually match an entity on the hospital organizational chart.

But if the hospital organizational structure integrates broad functions it may be necessary to split one department into several cost centers.

Increasing the number of cost centers in an individual hospital allows for more accurate accounting of services and costs. But it also requires

additional time and effort. How detailed the breakdown into cost centers should be is a judgement that needs to be made based on how valuable additional detail might be

and how costly.

________________________________

Prepared by Joseph S.Samaha (CPA)

23

Classification of Cost Centers1/3

Cost centers should be classified broadly into either final or intermediate cost centers.

The Finals are those cost centers directly involved in the production of services for which the hospital is budgeted or reimbursed. They are sometimes called revenue-earning cost centers.

The Intermediates provide support services for the final cost centers but are not, by definition, revenue-earning centers.

________________________________

Prepared by Joseph S.Samaha (CPA)

24

Classification of Cost Centers2/3

This distinction is important because costs are handled differently.

Final cost centers are reimbursed directly for their services.

Intermediate cost centers have to cover their costs by allocating or mapping them appropriately among revenue-earning (or final) cost

centers.

Centers which offer support services and would normally be considered intermediate should be classified as final cost centers if their costs are reimbursed by paying customers or third-party payers.

________________________________

Prepared by Joseph S.Samaha (CPA)

25

Classification of Cost Centers3/3

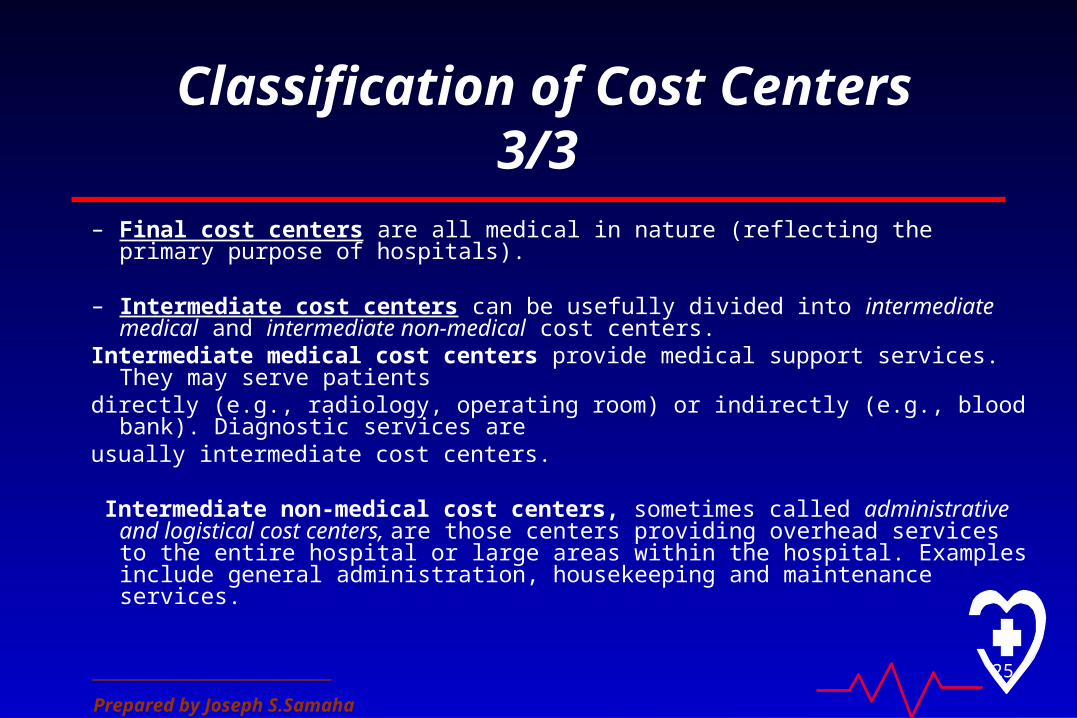

– Final cost centers are all medical in nature (reflecting the primary purpose of hospitals).

– Intermediate cost centers can be usefully divided into intermediate medical and intermediate non-medical cost centers.

Intermediate medical cost centers provide medical support services. They may serve patientsdirectly (e.g., radiology, operating room) or indirectly (e.g., blood bank). Diagnostic services areusually intermediate cost centers.

Intermediate non-medical cost centers, sometimes called administrative and logistical cost centers, are those centers providing overhead services to the entire hospital or large areas within the hospital. Examples include general administration, housekeeping and maintenance services.

________________________________

Prepared by Joseph S.Samaha (CPA)

26

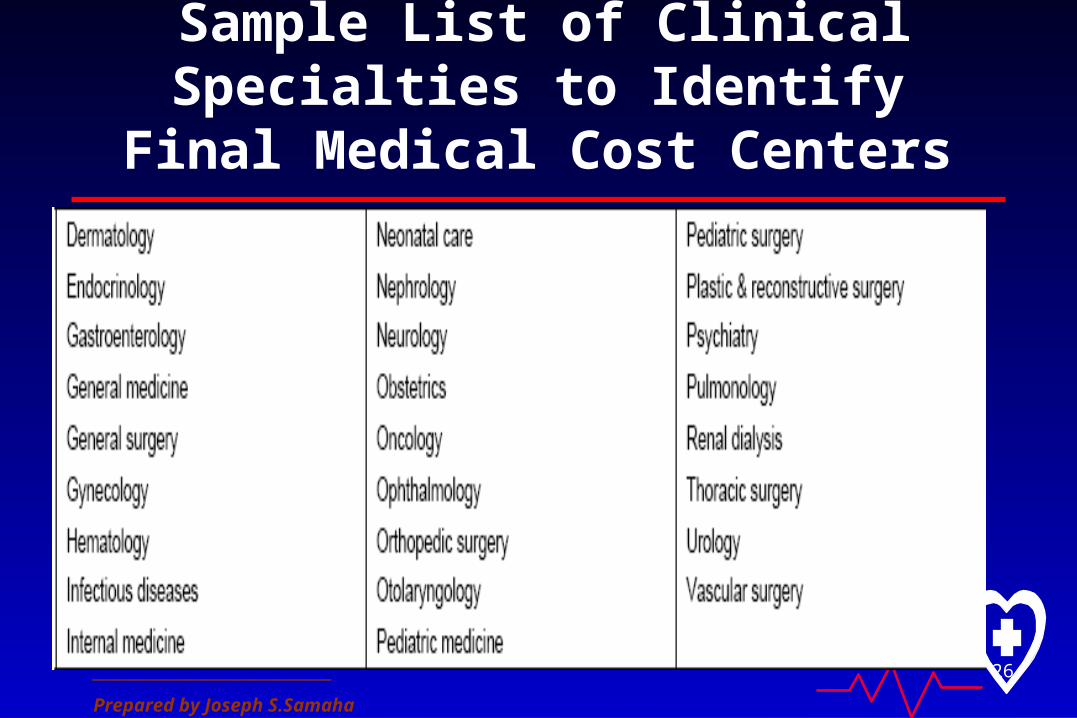

Sample List of Clinical Specialties to Identify Final Medical Cost Centers

________________________________

Prepared by Joseph S.Samaha (CPA)

27

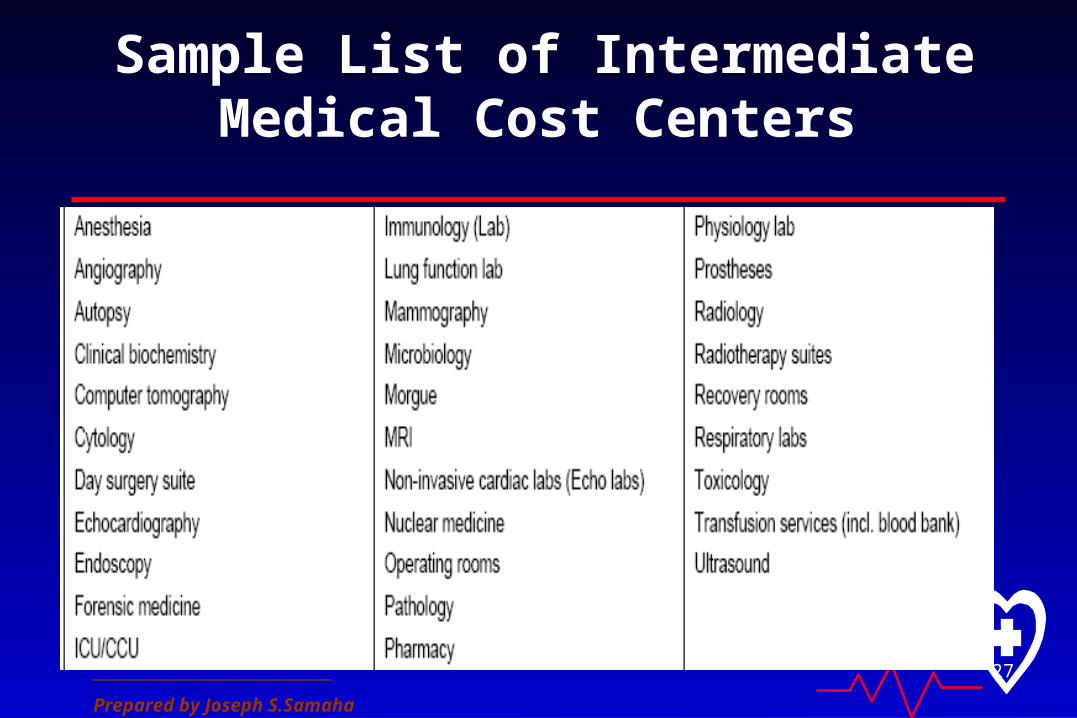

Sample List of Intermediate Medical Cost Centers

________________________________

Prepared by Joseph S.Samaha (CPA)

28

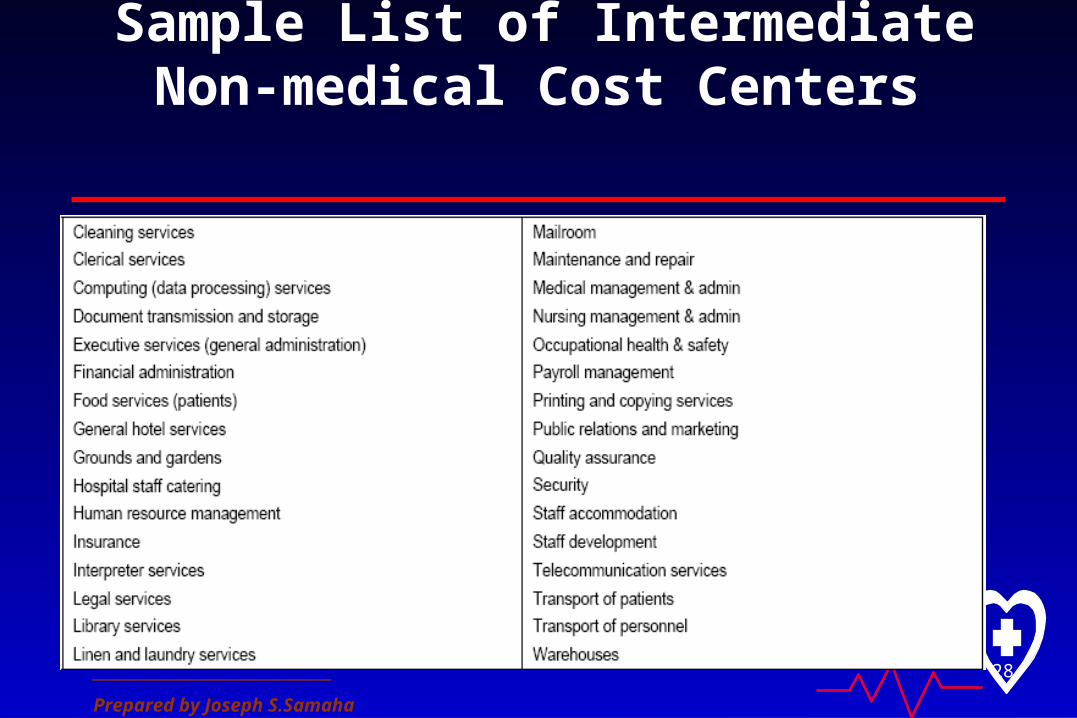

Sample List of Intermediate Non-medical Cost Centers

________________________________

Prepared by Joseph S.Samaha (CPA)

29

Nature of Costs

Hospital resources are central to cost accounting. Resources used in the production of hospital services – as in any production effort – include labor (human resources), material and

supplies, equipment, and other assets, including buildings and land. Knowing the quantity of resources is often an important first step in costing. Quantities of resources can also serve as proxy variables for

allocating shared costs . Because costs are usually estimated over a defined one-year period, an important distinction needs to be made between those resources which are consumed within the year (recurrent) and those which are longer-

lived (capital goods or fixed assets).

________________________________

Prepared by Joseph S.Samaha (CPA)

30

Recurrent Costs

Recurrent costs include costs of labor, pharmaceuticals and medical supplies, meals, linen and clothing, utilities (water, gas, heat, electricity), maintenance and repair of buildings and equipment, laundry, cleaning, business travel, office

supplies, communication, and transportation services.

Annual accounting of recurrent costs is conceptually straightforward.

________________________________

Prepared by Joseph S.Samaha (CPA)

31

Capital Costs

Capital costs include the costs of larger office equipment and medical equipment and vehicles that are usually incurred through a one-time payment even though the items are used over a considerably longer period.

Annual accounting requires the transformation of these capital cost into a regular stream of equivalent annual or recurrent costs over the life of the asset. This is done by a process called “depreciation” that estimates how much of an asset is used up each

year. An organization that annually puts aside the sum calculated through depreciation should

have enough funds by the end of the asset’s useful life to be able to replace the worn out asset with a new one.

________________________________

Prepared by Joseph S.Samaha (CPA)

32

Categories of Costs

Direct Costs: Costs that can be easily attributed to a particular cost center are termed “direct costs.”

Indirect Costs :Some resources are shared between cost centers in a way that cannot be easily teased out. They can only be allocated (i.e., shared out) to a particular cost center indirectly, using some kind of proxy variable (or cost driver). Costs calculated in this way are termed “indirect costs.”

The cost driver might be a measure of resources (e.g., number of staff, area covered) or of outputs (e.g., number of patients treated) or even of other costs (indirect costs are

sometimes allocated in proportion to direct costs). The crucial feature of the cost driver is that it should mirror as closely as possible the amount of activity being

costed indirectly.

________________________________

Prepared by Joseph S.Samaha (CPA)

33

Categories of Costs

Direct Costs: Costs that can be easily attributed to a particular cost center are termed “direct costs.”

Indirect Costs :Some resources are shared between cost centers in a way that cannot be easily teased out. They can only be allocated (i.e., shared out) to a particular cost center indirectly, using some kind of proxy variable (or cost driver). Costs calculated in this way are termed “indirect costs.”

The cost driver might be a measure of resources (e.g., number of staff, area covered) or of outputs (e.g., number of patients treated) or even of other costs (indirect costs are

sometimes allocated in proportion to direct costs). The crucial feature of the cost driver is that it should mirror as closely as possible the amount of activity being

costed indirectly.

________________________________

Prepared by Joseph S.Samaha (CPA)

34

Principles for Calculation of Costs 1/3

Costs are a function of the number of resources and their unit value. There are many different ways to calculate costs. For example, you might have access to expenditure records that have exactly the costs you are looking for. Or you may need to combine data on quantities of resources and their prices. You may have access to an average

(or typical) cost and have to employ it to estimate the costs of more units. The resource may have a simple, single cost or a variety of different elements

(e.g., labor costs include allowances of various sorts). The way you perform the calculations will depend on how the available data is

organized and the extent to which you have the capacity to collect additional primary data yourself.

Whatever procedure is used to calculate costs, there are some important principles that must be followed :

________________________________

Prepared by Joseph S.Samaha (CPA)

35

Principles for Calculation of Costs 2/2

1-Costing Should Be Comprehensive:• All costs incurred should be accurately accounted for,• All costs should be included even if money doesn’t change hands.

2-Costs Should Be Attributed as Precisely as Possible to Specific Cost Centers:Where possible, costs should be traced directly to a specific cost center.

3-Allocation of Indirect Costs Should Be Done in a Way that Reflects as Closely as Possible the True Incidence of Those Costs

4-Costs Incurred by One Service Should Never Be Attributed to Another Service

________________________________

Prepared by Joseph S.Samaha (CPA)

36

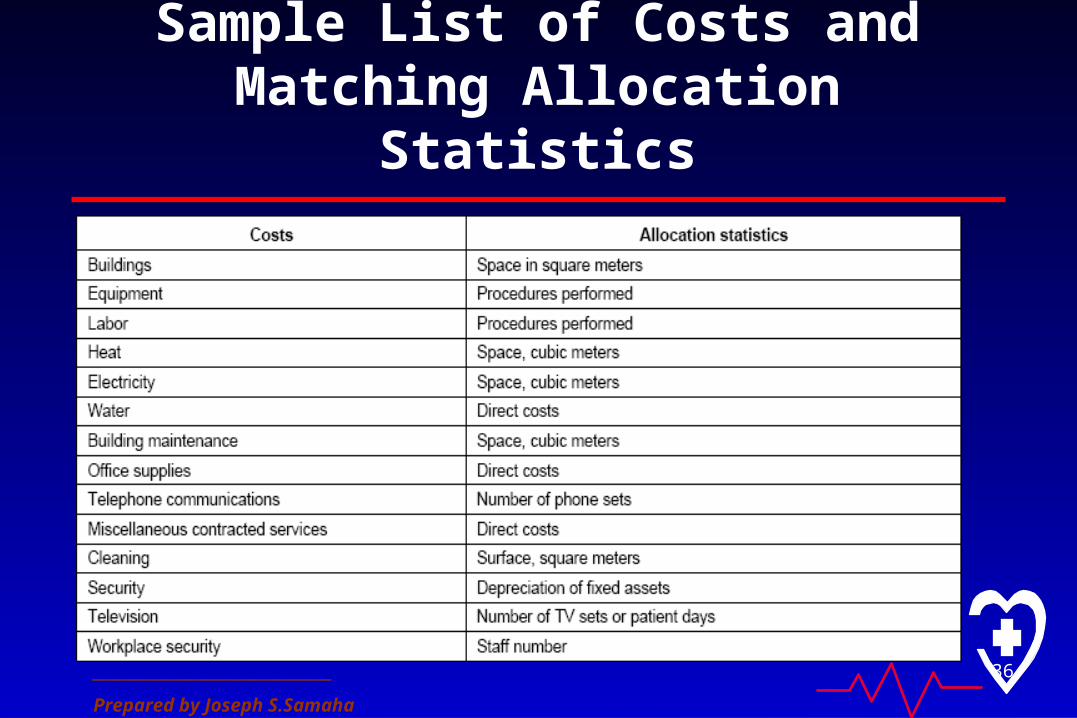

Sample List of Costs and Matching Allocation Statistics

________________________________

Prepared by Joseph S.Samaha (CPA)

37

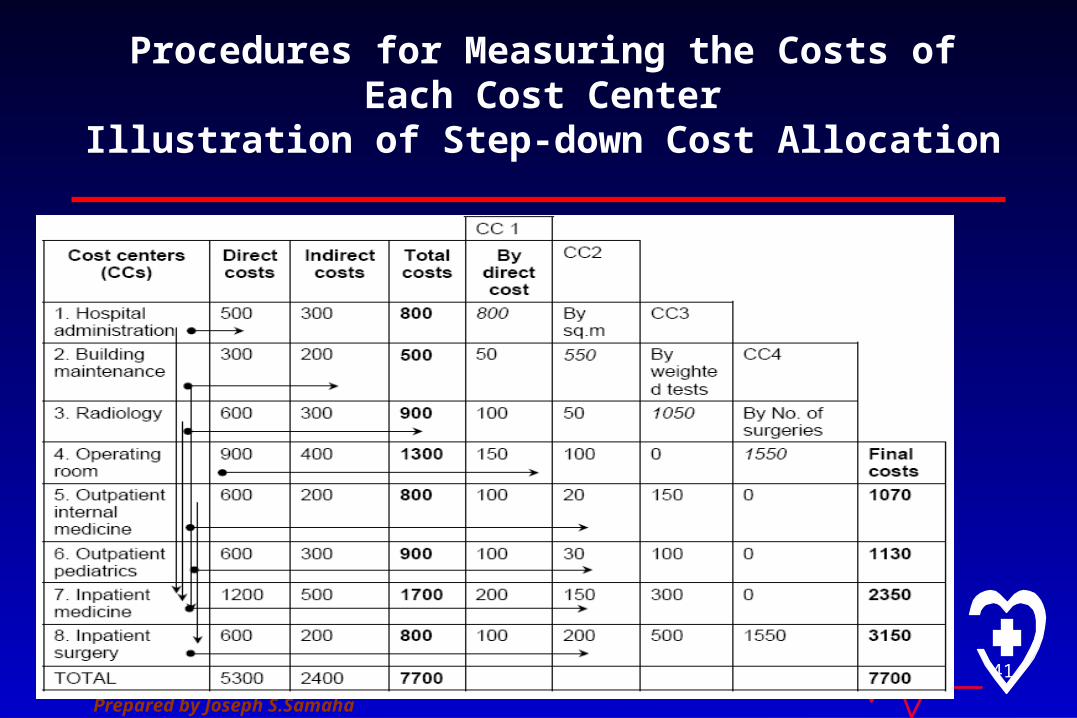

Procedures for Measuring the Costs of Each Cost Center

In measuring costs it is useful to start by consulting expenditure records. Usually this will not be enough either because data are insufficiently disaggregated or because expenditure is not equivalent to annual costs (e.g., with equipment and buildings) and it will be

necessary also to collect information on the quantity and cost per unit of resources. Sometimes the cost per unit is a relatively straight forward measure (e.g., for pharmaceuticals),

and sometimes it is a complex set of different elements (e.g., in the case of labor where allowances, bonuses, and compensations of different kinds complicate the picture).

It is important to collect data on the quantity of resources, not only because it can be used (together with unit prices) to calculate costs but also because they can function as cost drivers. Human resources (e.g., numbers of staff) and physical plant (e.g., square meters of space)

both serve as important cost drivers for indirect costing and for step-down allocationof costs to revenue-earning cost centers .

________________________________

Prepared by Joseph S.Samaha (CPA)

38

Procedures for Measuring the Costs of Each Cost CenterExample : Labor Cost

1/3

1. Identify all the staff employed in the hospital. Include:clinical staff such as physicians, pharmacologists, nurses, midwives, or pharmacists; andnon-clinical staff such as engineers and technicians, administrative personnel,

office/clerical and other administrative personnel, or ancillary medical and technical staff.

2. Classify these staff into full-time and part-time workers. For those who work part time estimate annual work hours or workdays. These estimates can be later translated into fulltime equivalent (FTE) labor.

3. Consider classifying hospital staff by qualification and other categories to provide additional information for hospital resource management and analyses.

4. For each staff member or group of staff whose labor is being costed, track down all the different elements that contribute to the cost of that person or group of persons. These

________________________________

Prepared by Joseph S.Samaha (CPA)

39

Procedures for Measuring the Costs of Each Cost CenterExample :Labor Cost

2/3

1. Identify all the staff employed in the hospital. Include:clinical staff such as physicians, pharmacologists, nurses, midwives, or pharmacists; andnon-clinical staff such as engineers and technicians, administrative personnel,

office/clerical and other administrative personnel, or ancillary medical and technical staff.

2. Classify these staff into full-time and part-time workers. For those who work part time estimate annual work hours or workdays. These estimates can be later translated into fulltime equivalent (FTE) labor.

3. Consider classifying hospital staff by qualification and other categories to provide additional information for hospital resource management and analyses.

4. For each staff member or group of staff whose labor is being costed, track down all the different elements that contribute to the cost of that person or group of persons. These

________________________________

Prepared by Joseph S.Samaha (CPA)

40

Procedures for Measuring the Costs of Each Cost CenterExample : Labor Cost

3/3

These elements, whose records are often kept somewhat separately, include:

– Standard wages and salaries– Additional compensation for such things as extra-hours and night shifts; work in,… – Work-related allowances (e.g., commuter subsidies, car allowances)– Cash and in-kind income supplementation (e.g., housing and utility allowances,…)– Vacations, sick leave, and other off-time payments– Educational stipends– Performance bonuses and miscellaneous rewards– Workers’ compensations– Severance packages– Labor surcharges, such as NSSF charges or payroll taxes.

________________________________

Prepared by Joseph S.Samaha (CPA)

41

Procedures for Measuring the Costs of Each Cost CenterIllustration of Step-down Cost Allocation

________________________________

Prepared by Joseph S.Samaha (CPA)

42

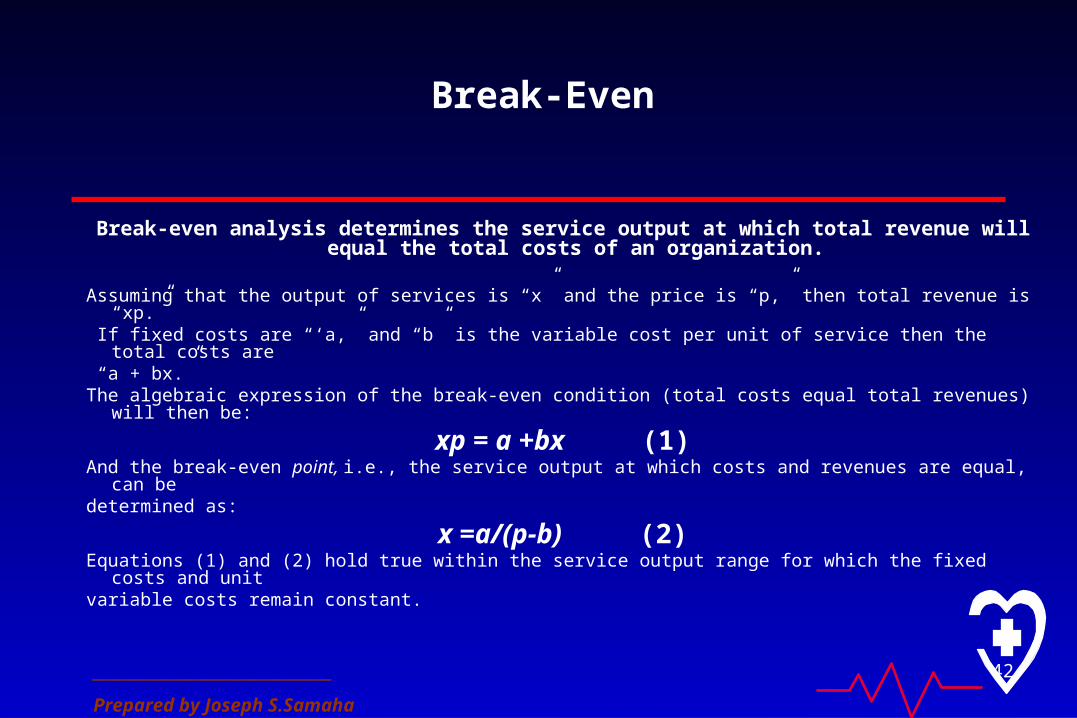

Break-Even

Break-even analysis determines the service output at which total revenue will equal the total costs of an organization.

Assuming that the output of services is “x” and the price is “p,” then total revenue is “xp.” If fixed costs are “‘a,” and “b” is the variable cost per unit of service then the total costs are “a + bx.”The algebraic expression of the break-even condition (total costs equal total revenues) will then be:

xp = a +bx (1)And the break-even point, i.e., the service output at which costs and revenues are equal, can bedetermined as:

x =a/(p-b) (2)Equations (1) and (2) hold true within the service output range for which the fixed costs and unitvariable costs remain constant.

________________________________

Prepared by Joseph S.Samaha (CPA)

43

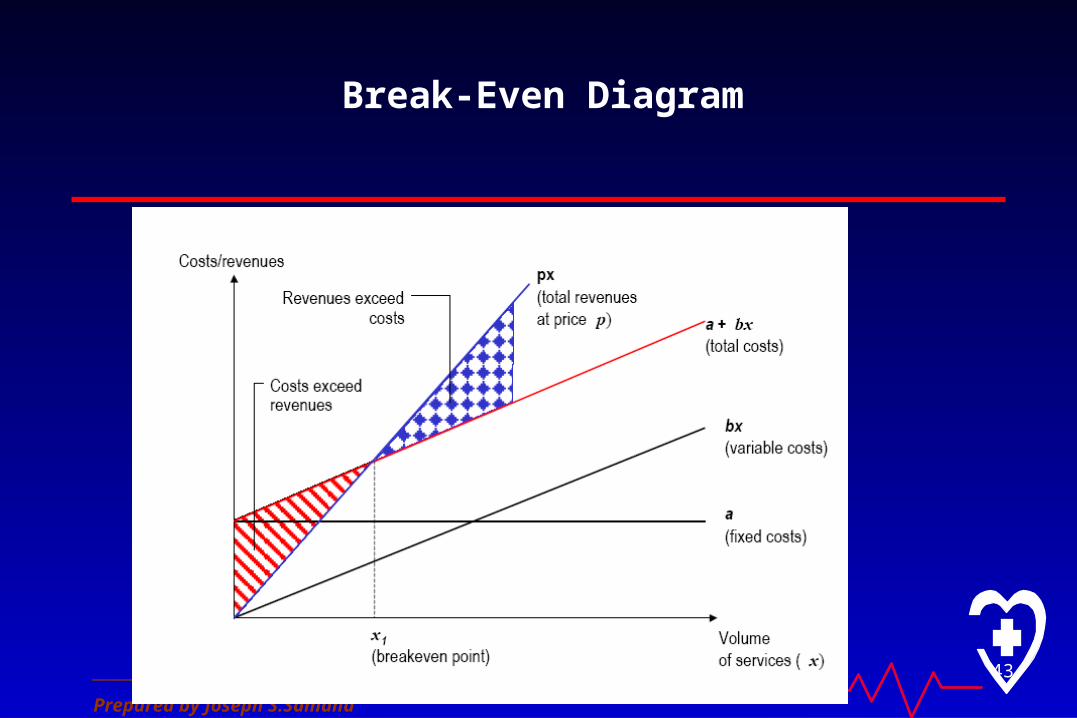

Break-Even Diagram

________________________________

Prepared by Joseph S.Samaha (CPA)

44

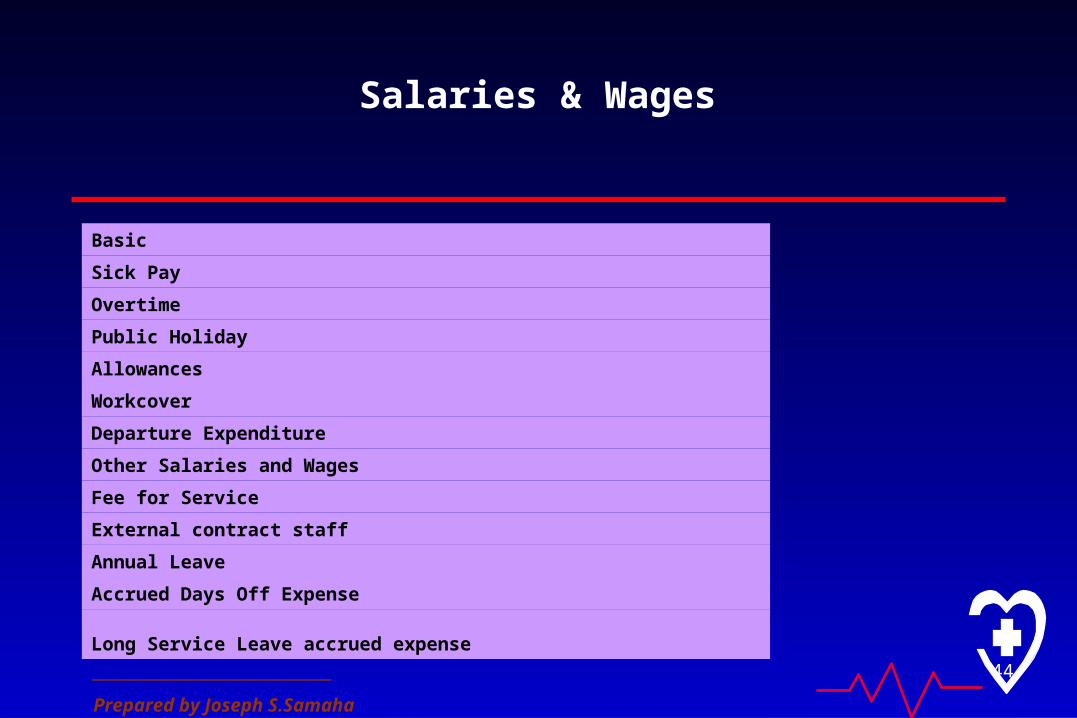

Salaries & Wages

Basic

Sick Pay

Overtime

Public Holiday

Allowances

Workcover

Departure Expenditure

Other Salaries and Wages

Fee for Service

External contract staff

Annual Leave

Accrued Days Off Expense

Long Service Leave accrued expense

________________________________

Prepared by Joseph S.Samaha (CPA)

45

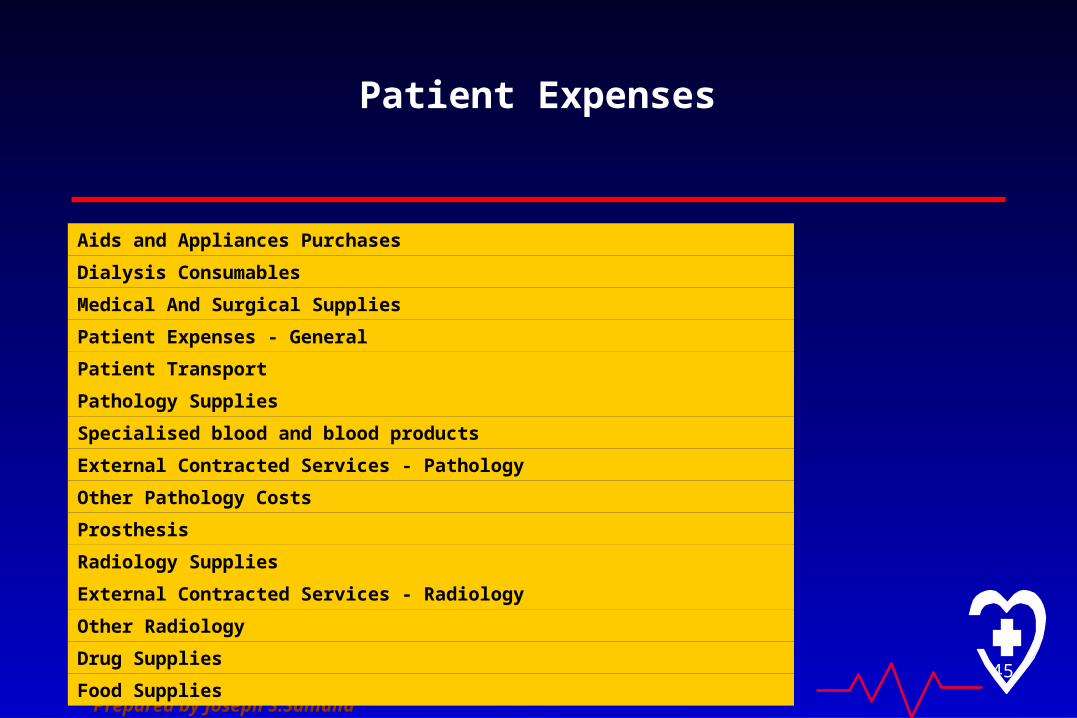

Patient Expenses

Aids and Appliances Purchases

Dialysis Consumables

Medical And Surgical Supplies

Patient Expenses - General

Patient Transport

Pathology Supplies

Specialised blood and blood products

External Contracted Services - Pathology

Other Pathology Costs

Prosthesis

Radiology Supplies

External Contracted Services - Radiology

Other Radiology

Drug Supplies

Food Supplies

________________________________

Prepared by Joseph S.Samaha (CPA)

46

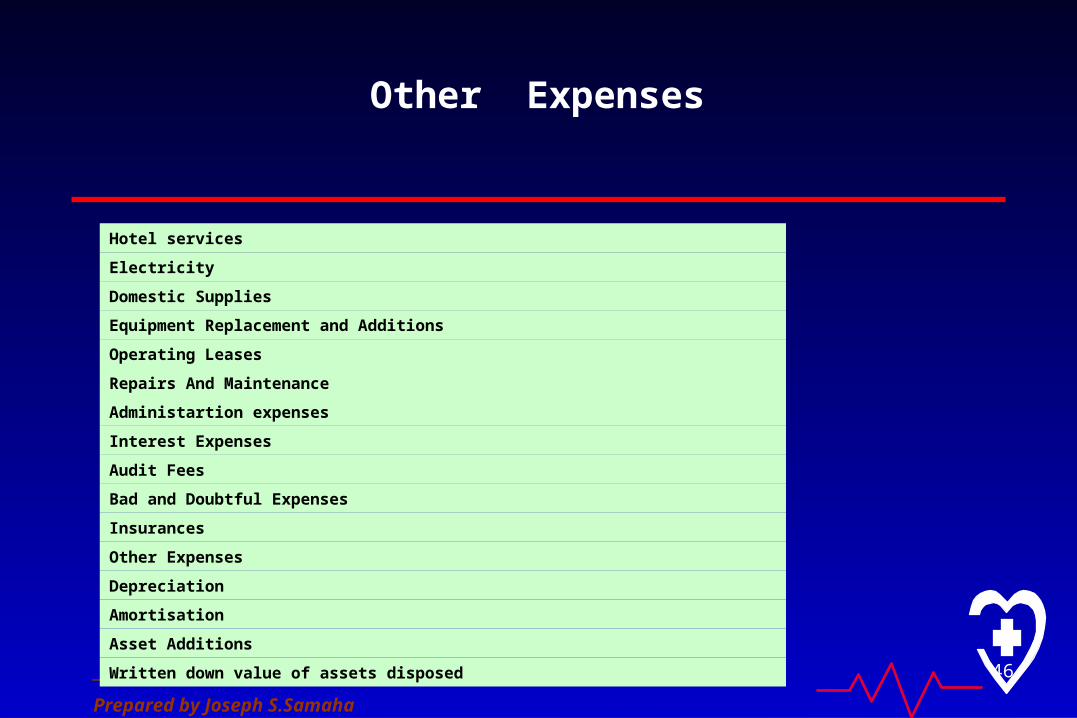

Other Expenses

Hotel services

Electricity

Domestic Supplies

Equipment Replacement and Additions

Operating Leases

Repairs And Maintenance

Administartion expenses

Interest Expenses

Audit Fees

Bad and Doubtful Expenses

Insurances

Other Expenses

Depreciation

Amortisation

Asset Additions

Written down value of assets disposed

________________________________

Prepared by Joseph S.Samaha (CPA)

47

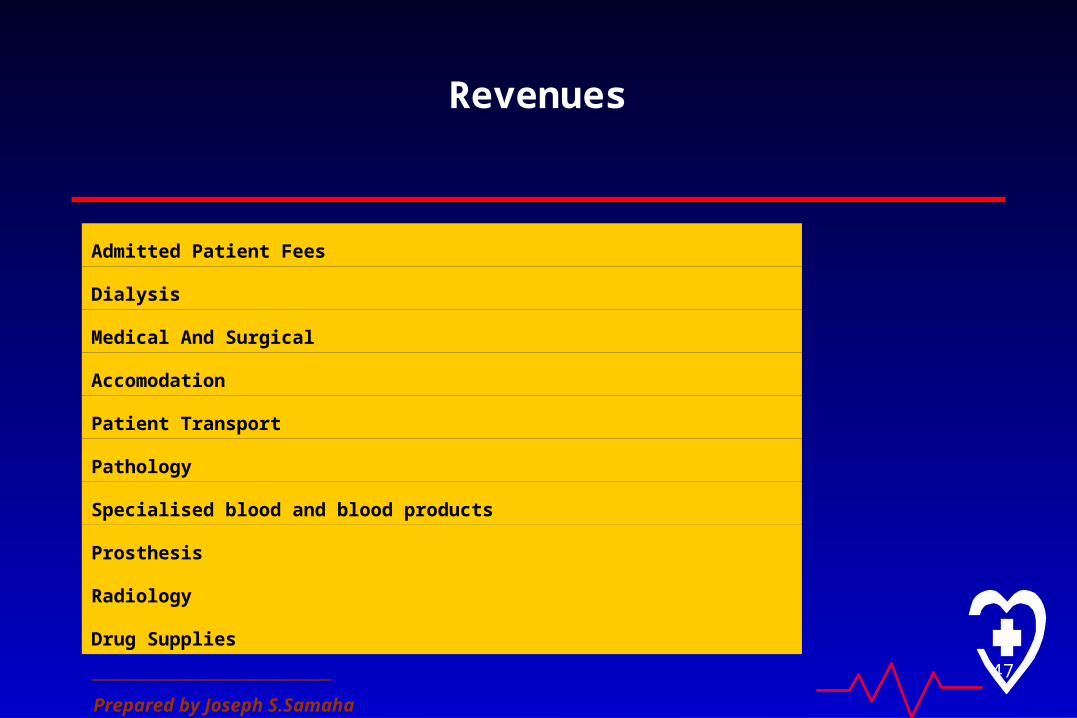

Revenues

Admitted Patient Fees

Dialysis

Medical And Surgical

Accomodation

Patient Transport

Pathology

Specialised blood and blood products

Prosthesis

Radiology

Drug Supplies

________________________________

Prepared by Joseph S.Samaha (CPA)

48

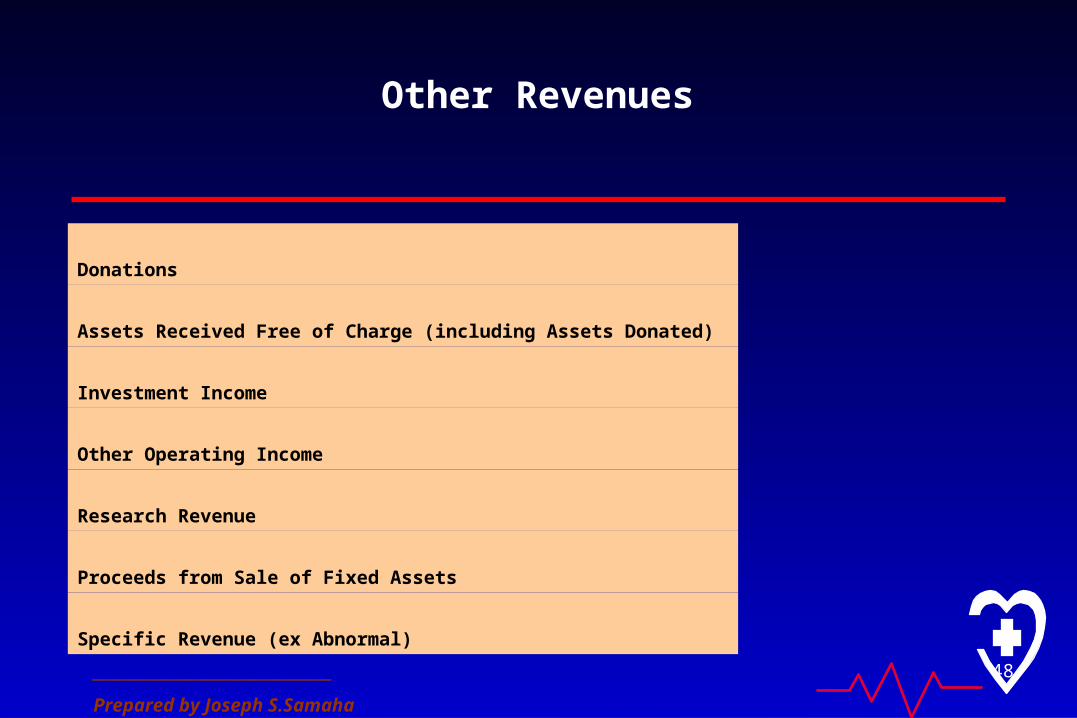

Other Revenues

Donations

Assets Received Free of Charge (including Assets Donated)

Investment Income

Other Operating Income

Research Revenue

Proceeds from Sale of Fixed Assets

Specific Revenue (ex Abnormal)

________________________________

Prepared by Joseph S.Samaha (CPA)

49

Leverage

Leverage indicates the importance of debt in financing the hospital, and the ability to incur additional debt.

These ratios are usually closely monitored by creditors and may ultimately determine the amount of borrowing available

for future capital projects.

Two statistics are to be considered:

Debt to Capitalization, and Debt Service Coverage.

________________________________

Prepared by Joseph S.Samaha (CPA)

50

Debt to Capitalization

measures the importance of debt in the hospital’s

permanent capital structure . Lower values

are preferred because they indicate less financial leverage (i.e., less reliance on borrowing) and because these

expenses are ‘fixed’ in that they are long livedand do not vary with volume.

________________________________

Prepared by Joseph S.Samaha (CPA)

51

Debt Service Coverage

Debt Service Coverage is a key leverage ratio,equating the available cash flow to the principal

and interest obligation on the debt .Lenders & Banks use this ratio to examine thesecurity of the debt, because it examines both a

source and a use of revenue. Higher valuesboth over time and in relation to the benchmarks are preferred.

________________________________

Prepared by Joseph S.Samaha (CPA)

52

Profitability

Profitability measures examine the generation of net income, and the creation of wealth.

Profitability is key to a hospital’s long-term survival because excessive reliance on philanthropy is risky.

Hospitals that are consistently unprofitable will have insufficient funds to meet current requirements, to replace aging plants or to invest in new

technologies.Two profitability statistics are presented: Profit Margin, and Equity Growth Rates

________________________________

Prepared by Joseph S.Samaha (CPA)

53

Profit Margin

Profit Margins are the bottom-line profits from hospital operations and non-operations alike . It reflects all realized gains and losses for the

year.

All organizations need to operate profitably in order to remain viable, so higher values are always preferred. Traditionally, lower comparative

Profit Margins usually indicate poor expense management.

However, the other variable often overlooked in the profitability equation is revenue, primarily patient reimbursement.

________________________________

Prepared by Joseph S.Samaha (CPA)

54

Equity Growth Rate

measures what is happening to the net worth of a hospital, or the percentage by which it is growing or shrinking.

Ideally, healthy organizations are expected to increase in value over time. Any combination of three factors may affect a hospital’s Equity

Growth Rate: profitability, fundraising, and market returns.

Any loss in equity is undesirable so higher values are always preferred. Technically, an organization is considered insolvent when its net worth

becomes negative.

________________________________

Prepared by Joseph S.Samaha (CPA)

55

Liquidity

Liquidity measures examine the ability of a hospital to meet its short-term obligations (i.e., to pay its bills), and the

timing of cash into the facility. Most organizations experience a financial problem because of

a liquidity crisis, and deterioration in these measures may presage future insolvency.

Two liquiditystatistics are examined: Current Ratio and Days in Patients’ Accounts Receivable.

________________________________

Prepared by Joseph S.Samaha (CPA)

56

Current Ratio

The Current Ratio evaluates the amount of current assets available to pay off each dollar in obligations coming due within the year.

It is a fairly stringent measure of liquidity as it includes only assets that are, or readily convertible to cash, in the numerator.

This metric is one in which higher values are preferred, but those values shouldn’t be ‘excessive’. Hospitals must strike a balance between

maintaining enough liquid assets for operations, but not so much as to affect profitability (i.e., Profit Margin).

The return on short-term investments is generally less than that of monies invested longer, so there is an opportunity cost in maintaining liquidity.

________________________________

Prepared by Joseph S.Samaha (CPA)

57

Days in Patients’Accounts Receivables

measures the average time receivables are outstanding . Lower values on this measure are favored. Patient care is the

primary source of operating revenue, so prompt collection of these bills is critical.

Increases in this measure can create cash-flow problems that usually cause a hospital to extend its own payables.

________________________________

Prepared by Joseph S.Samaha (CPA)

58

Activity

Activity refers to how productively a hospital uses its assets to generate revenue. Hospital revenue consists mostly of patient reimbursement

and some other minor sources (e.g., endowment transfers, other operating revenue, etc.).

Therefore, the numerator in these ratios is a proxy for output (i.e., services provided) and the denominator is a measure of input (i.e., the

investment is some category of assets). Two efficiency measures are examined:

Total Asset Turnover and Fixed Asset Turnover.

________________________________

Prepared by Joseph S.Samaha (CPA)

59

Total Asset Turnover

The Total Asset Turnover is a comprehensive asset efficiency measure. It analyzes the productivity of the entire asset base .

Higher ratio values are preferred and may reflect any combination of superior reimbursement, greater utilization,

or a more favorable mix of assets.

________________________________

Prepared by Joseph S.Samaha (CPA)

60

Fixed Asset Turnover

The Fixed Asset Turnover is another activity ratio, measuring the number of dollars generated from each dollar invested in property, plant and

equipment . Again, higher values are preferred.

The importance in maintaining a high Fixed Asset Turnover is that these investments are fixed (independent of patient volume), longlived

(useful lives in years), and for most part, illiquid (not easily sold or converted to other uses).

The Fixed Asset Turnover, and to some extent the previous measure, favor older facilities because of understated historical book values of

the property, plant and equipment.

________________________________

Prepared by Joseph S.Samaha (CPA)

61

Hospital Ranking

To determine overall financial performance for the hospitals, the indices in the four ratio categories were weighted

40% for profitability, 25% for leverage, 20% for liquidity, and 15% for activity.

Those weighted averages were then standardized to arrive at a single overall performance index for each hospital.

Again, higher index values are preferred.

________________________________

Prepared by Joseph S.Samaha (CPA)

62

End Slide

For any inquiries and feedback

Please send an email to :