Embed Size (px)

Citation preview

© Steven J. Willis 2001 1

Methods of Accounting

• IRC § 446– Permitted methods

• Cash• Accrual• Other

– Farming (447)– Inventory (472)– Installment (453)– Percentage of completion (460)– Subscriptions (455)

• Hybrid

– Change of Method (446(e)/481)• Need permission• Must make adjustments

• IRC § 448– Limitation on the use of the cash method

© Steven J. Willis 2001 2

Role of generally accepted accounting principles

GAAP– “A method of accounting which reflects the consistent

application of generally accepted accounting principles in a particular trade or business in accordance with accepted conditions or practices in that trade or business will ordinarily be regarded as clearly reflecting income, provided all items of gross income and expense are treated consistently from year to year. “ Treas. Reg. 1.446-1(a)(2).

– See, Thor Power Tools, 439 U.S. 522 (1979).

© Steven J. Willis 2001 3

Year of Inclusion

• Cash– “The amount of any item of gross income shall be included

in the gross income for the taxable year in which received by the taxpayer, unless, under the method of accounting used in computing taxable income, such amount is to be properly accounted for as of a different period.” IRC § 451(a).

• Accrual– “Under an accrual method of accounting, income is

includible in gross income when all the events have occurred which fix the right to receive such income and the amount thereof can be determined with reasonable accuracy.” Treas. Reg. § 1.451-1(a).

© Steven J. Willis 2001 4

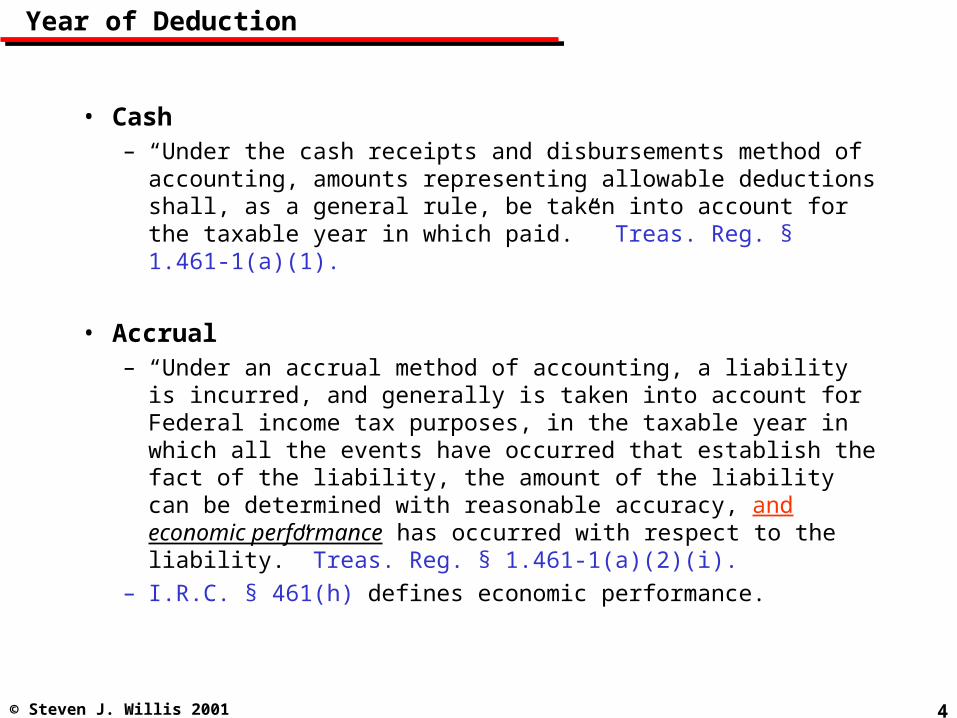

Year of Deduction

• Cash– “Under the cash receipts and disbursements method of

accounting, amounts representing allowable deductions shall, as a general rule, be taken into account for the taxable year in which paid.” Treas. Reg. § 1.461-1(a)(1).

• Accrual– “Under an accrual method of accounting, a liability is

incurred, and generally is taken into account for Federal income tax purposes, in the taxable year in which all the events have occurred that establish the fact of the liability, the amount of the liability can be determined with reasonable accuracy, and economic performance has occurred with respect to the liability.” Treas. Reg. § 1.461-1(a)(2)(i).

– I.R.C. § 461(h) defines economic performance.

![Accrual Methods[1]](https://img.pdfslide.net/doc/110x75/577ccf761a28ab9e788fc3c2/accrual-methods1.jpg)