Embed Size (px)

Citation preview

Supply- How much of a good will be supplied at a particular price.

Demand- How much of a good will be demanded at a particular price.

Equilibrium price- The price at which the producer is willing to sell their product and the price at which consumers will buy them.

Substitute goods- Goods that can be used in place of one another. Ex: McDonald’s & Burger King, Margarine & Butter

Complimentary goods- Goods that work together. Ex: DVD & DVD Player, Computer & Software, Baseball glove & Ball

Personal income- All of the money received by a household.

Disposable income- Income that is left after paying taxes. This is spent on out needs. Ex: Mortgage

Discretionary income- Income that is leftover after meeting our needs. This may be spent on our wants. Ex: ipods

Shortage- When demand for a good exceeds supply. Surplus- When the supply of a good exceeds demand. Inflation- A general rise in prices. Interest rate- The amount of money paid to a lender in

exchange for the use of the lenders money. Ex: Mortgage, credit cards

What three elements depend on one another for economic interdependance?

What role do households play in the economy?

What role do firms play in the economy? What role does the government play in

the economy? What type of economic system does the

Island of Mocha have?

EQ: HOW DO CONSUMERS AND MARKETS REACT TO SHORTAGES AND SURPLUSES?

In the circular flow of the economy in which market do people sell their labor?

1. What are the 3 major economic actors in the U.S. economy?

A. Gov’t, market, entrepreneursB. Land, labor, capitalC. Households, businesses, gov’tD. Consumers, producers, businesses

2. The fact that these 3 actors need each other in order for the economy to function smoothly is referred to as what?

A. Circular relianceB. Economic needC. Economic interdependenceD. Product and factor markets

Supply How much a certain

good is available to consumers.

As price increases…supply is increased

Demand How much consumers

want the particular good.

As price decreases…demand increases

Law of Supply and Demand Producers will only supply a product that will…

Make a profit Consumers will only demand a product for

which they need or want at a price they can afford.

Supply will be determined by what is demanded. Producers will supply goods as long as they can

make a profit.

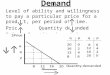

• Supply curve (supply schedule)– Shows how much of the

product that sellers are willing to sell at various price levels.

• Demand curve (demand schedule)– Shows how much of the

product buyers are willing to purchase at various price levels.

• Equilibrium (market) price– The point at which the

supply and demand curves meet.

– The price at which producers are willing to sell their products and the price at which consumers will buy those products.

Price

Quantity

Demand

Supply

Personal income All of the money received by

a household Disposable income

All of the income a household has after paying taxes.

Spent on needs (mortgage, electrical bills)

Discretionary income The income left after paying

for “necessities” . Spent on our wants Impacts supply and demand

The more suppliers there are, the more options for consumers. The more options for

consumers, the more producers must compete for business.

In order to compete, producers must either lower prices while still making a profit, or quit producing the good.

Substitute goods Goods that can be used

in place of other goods. Ex: McDonald’s, Burger

King, & Wendy’s Increases competition

Complimentary goods Goods that work

together to fulfill a certain need. Ex: DVDs and DVD players

are both useless unless used together.

1. When what is produced will be determined by what consumers want, provided they are willing to pay enough is called what?

A. The marketB. The law of demandC. The law of supply and demandD. The influence of disposable income

2. The price at which total supply equals total demand it known as what?

A. The middle priceB. The consumer priceC. Consumer demandD. Equilibrium price

On the island of Mocha, what was caused by the storm and the war? Shortage of wood

What is a shortage? When there is not enough of a product

What is a surplus? When there is too much of a product

Shortage When supply of a good

falls short of the demand. A price below equilibrium

results in a shortage Prices increase

Surplus When supply of a good

exceeds the demand. A price above equilibrium

results in a surplus. Prices decrease

Price

Quantity

Demand

Supply

Shortage

Surplus

Consumer tastes refers to individual consumers’ preferences. What is desirable to one

consumer may not be desirable to another.

Inflation A general rise in prices for

products.

Deflation A general fall in prices for

products. Gasoline

Stagflation When prices rise and

employment/wages fall at the same time.

Interest rates The amount paid to a lender in

exchange for the use of that lender’s money.

Higher interest rates = save Low interest rates = spend

Minimum wage Supporters argue that anything less

would not provide an adequate standard of living.

Opponents argue that it creates a surplus of labor that leaves many unemployed.

Price floors Minimum price below which the price

of a good is not permitted to drop.

Price ceilings Maximum price above which the

price of a good is not permitted to rise.

Fiscal policy Deficit spending (FDR) Supply-side economics (Reagan)

Cut corporate taxes so that businesses can have more money to spend on production and labor.

“Trickle down effect”

EQ: HOW DO CONSUMERS AND MARKETS REACT TO SHORTAGES AND SURPLUSES?

SUMMARIZE THE LAW OF SUPPLY AND DEMAND AND CREATE A DEMAND AND SUPPLY SCHEDULE

EXPLAIN WHAT IS THE EQUILIBRIUM PRICE? IDENTIFY SOME OF THE INFLUENCES ON SUPPLY AND

DEMAND? INTERPRET THE IMPACT OF COMPETITION ON SUPPLY AND

DEMAND? COMPARE AND CONTRAST SUBSTITUTE GOODS AND

COMPLIMENTARY GOODS IDENTIFY FACTORS THAT AFFECT PRICES? EXPLAIN THE DIFFERENCE BETWEEN INFLATION AND

DEFLATION? EVALUATE HOW INTEREST RATES CAN IMPACT PRICES

AND AFFECT SPENDING? IDENTIFY WAYS THE GOVERNMENT IMPACT PRICES?

What is the Equilibrium Price? The Equilibrium Price is the price

producers sell their product and the price consumers pay for the product.

Using pictures from the magazines and what you just learned create a collage of complimentary and substitute goods. Divide your poster board in half to separate each type

of good. Answer the following question on your collage:

What will happen to demand if the price rises for a substitute/complimentary good?

OR Complete the Supply/Demand donut fundraiser

packet

![Telly (n) television [ โทรทัศน์ ] addict (n) someone who likes a particular activity very much and spends as much time as they can doing it [ ผู้ที่หมกมุ่นกับสิ่งใดสิ่ง](https://img.pdfslide.net/doc/110x75/56649dc35503460f94ab56e3/telly-n-television-addict-n-someone-who-likes.jpg)