Embed Size (px)

Citation preview

©The McGraw-Hill Companies, Inc.,2001

17- 1

Irwin/McGraw-HillIrwin/McGraw-HillIrwin/McGraw-Hill

Institute of Internaitonal Politics and Economics

Prof. dr Hasiba Hrustić

FOREIGN DEBT

OF SERBIA AND ITS

NEIGHBORS

©The McGraw-Hill Companies, Inc.,2001

17- 2

Irwin/McGraw-Hill

SERBIA AND ITS NEIGHBORS

NEIGHBOR COUNTRIES: Hungary Romania Bulgaria

Macedonia Albania Montenegro Bosnia and Herzegovina

Croatia

©The McGraw-Hill Companies, Inc.,2001

17- 3

Irwin/McGraw-Hill

Main Macroeconomic Indicators

GDP

General

government

debt

Inflation

Unmployment

Current account

balance

General government balance

Foreign loan

©The McGraw-Hill Companies, Inc.,2001

17- 4

Irwin/McGraw-Hill

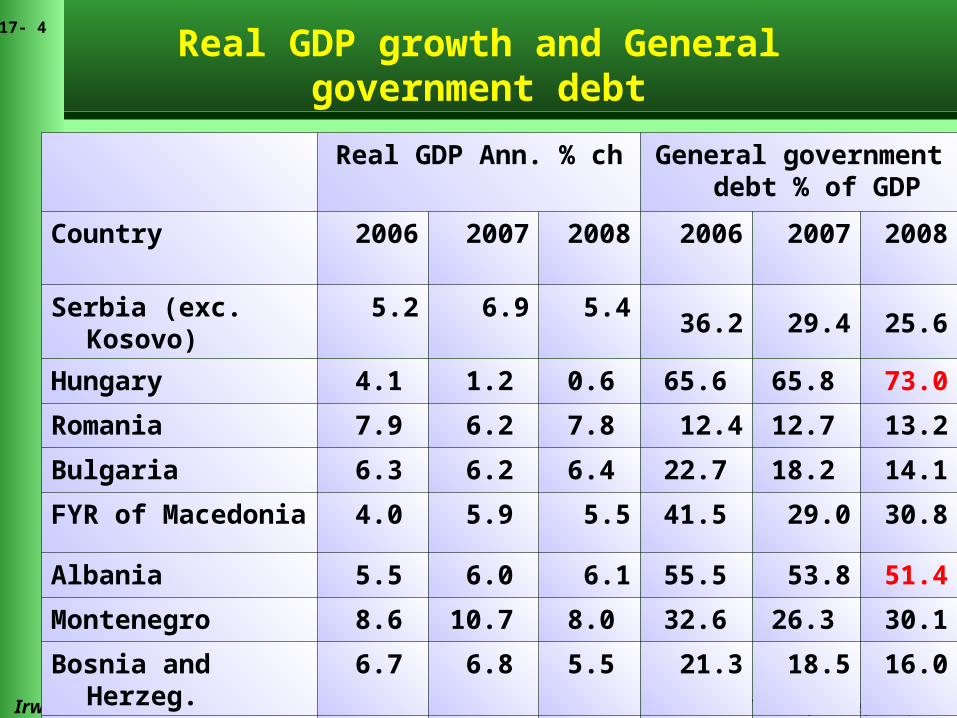

Real GDP growth and General government debt

Real GDP Ann. % ch General government debt % of GDP

Country 2006 2007 2008 2006 2007 2008

Serbia (exc. Kosovo) 5.2 6.9 5.4 36.2 29.4 25.6

Hungary 4.1 1.2 0.6 65.6 65.8 73.0

Romania 7.9 6.2 7.8 12.4 12.7 13.2

Bulgaria 6.3 6.2 6.4 22.7 18.2 14.1

FYR of Macedonia 4.0 5.9 5.5 41.5 29.0 30.8

Albania 5.5 6.0 6.1 55.5 53.8 51.4

Montenegro 8.6 10.7 8.0 32.6 26.3 30.1

Bosnia and Herzeg. 6.7 6.8 5.5 21.3 18.5 16.0

Croatia 4.8 5.6 2.4 40.8 37.7 47.8

©The McGraw-Hill Companies, Inc.,2001

17- 5

Irwin/McGraw-Hill

Inflation and Unemployment rate

Inflation Ann. % ch Unemployment rate %

Country 2006 2007 2008 2006 2007 2008

Serbia (exc. Kosovo) 12.7 11.0 8.6 21.6 18.8 14.7

Hungary 4.0 7.9 6.1 7.5 7.4 7.7

Romania 9.1 6.6 4.9 12.4 22.4 22.5

Bulgaria 7.4 7.6 12.0 9.0 6.9 6.0

FYR Macedonia 3.2 2.3 8.3 36.0 34.9 33.0

Albania 2.4 2.9 3.0 13.9 13.4 12.6

Montenegro 3.0 4.3 9.2 14.7 11.9 10.7

Bosnia and Herzeg. 6.1 1.5 9.4 44.2 42.9 40.5

Croatia 3.2 2.9 7.4 11.1 9.6 12.4

EU -27 2.3 2.4 3.7 8.2 7.1 7.0

©The McGraw-Hill Companies, Inc.,2001

17- 6

Irwin/McGraw-Hill

Current account balance and

General government balance Current account balance % of GDP

General government balance % of GDP

Country 2006 2007 2008 2006 2007 2008

Serbia (exc. Kosovo) -11,5 15,9 -17,9 1,6 -1,9 -2.3

Hungary -7.5 -6.4 -7.2 -9.3 -5.0 -3.3

Romania -10.6 -13.6 -12.9 -2.2 -2.5 -5.2

Bulgaria -11.5 -18.6 -22.5 3.0 0.1 -3.2

FYR Macedonia -0.9 -3.0 -12.9 -0.5 0.6 -3.0

Albania -6.5 -10.5 -13.2 -3.3 -3.5 -5.2

Montenegro -24.7 -29.4 -35.4 2.7 6.4 4.3

Bosnia and Herzegovina -7.8 -7.8 -12.6 2.9 1.3 -2.0

Croatia -7.9 -8.7 -10.9 -2.2 -1.8 -2.8

©The McGraw-Hill Companies, Inc.,2001

17- 7

Irwin/McGraw-Hill

FOREIGN DEBT

the foreign loan is partly financed by incomes from foreign direct investments (FDI) attained in the process of privatization

- remittances from abroad

- foreign private lending

Rapid credit growth has been one of the main drivers of growth in the region in recent years

The rapid credit growth in the region in recent years has boosted domestic consumption

©The McGraw-Hill Companies, Inc.,2001

17- 8

Irwin/McGraw-Hill

The impact of the global international crisis and external financing

reduced economic activityenhanced foreign loan and trade deficitsimport dependencysignificant declined in foreign trade and

industrial productionoutput reduction this yearhigh levels of unemployment

©The McGraw-Hill Companies, Inc.,2001

17- 9

Irwin/McGraw-Hill

External Debt of Serbia and its Neighbors, 2008

Country External Debt

(bn USD) External Debt

Per Capita (USD)1 External debt (% of GDP)

Serbia (exc. Kosovo) 30,7 4,175 64.4

Hungary 164,2 15,728 108.9

Romania 99,1 4,609 49.5

Bulgaria 33,7 4,434 67.5

Macedonia 4,3 2,182 22.8

Albania 1,5 547 7.4

Montenegro 0,6 45 10.9

Bosnia and Herzegovina

7,6 1,667 25.3

Croatia 55,0 12,224 67.0

©The McGraw-Hill Companies, Inc.,2001

17- 10

Irwin/McGraw-Hill

Foreign-denominated loans

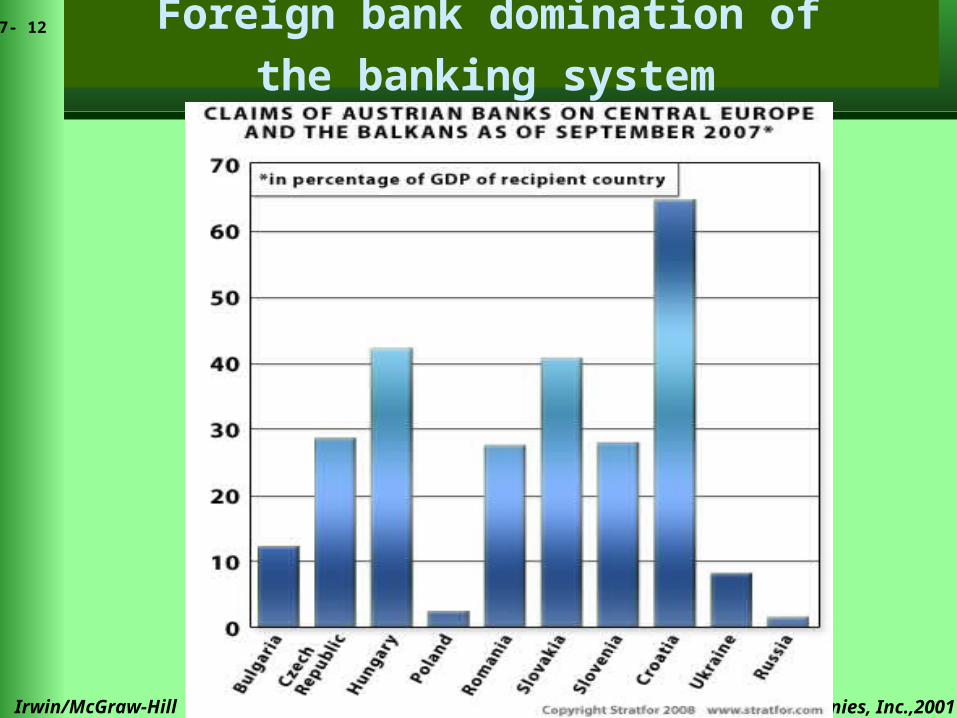

The combination of foreign bank domination of the banking system and weak fundamentals plaguing in region is definitely an issue in this region as well

©The McGraw-Hill Companies, Inc.,2001

17- 11

Irwin/McGraw-Hill

©The McGraw-Hill Companies, Inc.,2001

17- 12

Irwin/McGraw-Hill

Foreign bank domination of

the banking system

©The McGraw-Hill Companies, Inc.,2001

17- 13

Irwin/McGraw-Hill

Foreign-denominated loans

Foreign-denominated loans allow potential homeowners to take out a loan originally denominated in low-interest-rate Swiss francs or euros instead of the high-interest-rate domestic currencies.

Due to the instability of the region’s currencies, foreign-denominated lending was popular with business lenders and other consumer lenders.

At the onset of the current finansial crisis, foreign banks operating started to repay loans from private companies, putting pressure on the exchange rate and creating an outflow of foreign currency

©The McGraw-Hill Companies, Inc.,2001

17- 14

Irwin/McGraw-Hill

Foreign bank domination of the banking system

As a result, about 1 billion exited Serbia between November 2008 and January 2009

Also, one of the effects of the crisis was that banks increased their spreads to a high extent; they doubled spreads, not only in Serbia, but also in other Eastern European countries.

©The McGraw-Hill Companies, Inc.,2001

17- 15

Irwin/McGraw-Hill

©The McGraw-Hill Companies, Inc.,2001

17- 16

Irwin/McGraw-Hill

Short Macroeconomic Profile

strengths and weaknesses

©The McGraw-Hill Companies, Inc.,2001

17- 17

Irwin/McGraw-Hill

GDP Per Capita

Country GDP (nominal )Per Capita (USD)

Serbia (exc. Kosovo) 6,782

Hungary 15,542

Romania 9,291

Bulgaria 6,857

Macedonia 4,656

Albania 4,073

Montenegro 7,702

Bosnia and Herzegovina 4,625

Croatia 15,628

©The McGraw-Hill Companies, Inc.,2001

17- 18

Irwin/McGraw-Hill

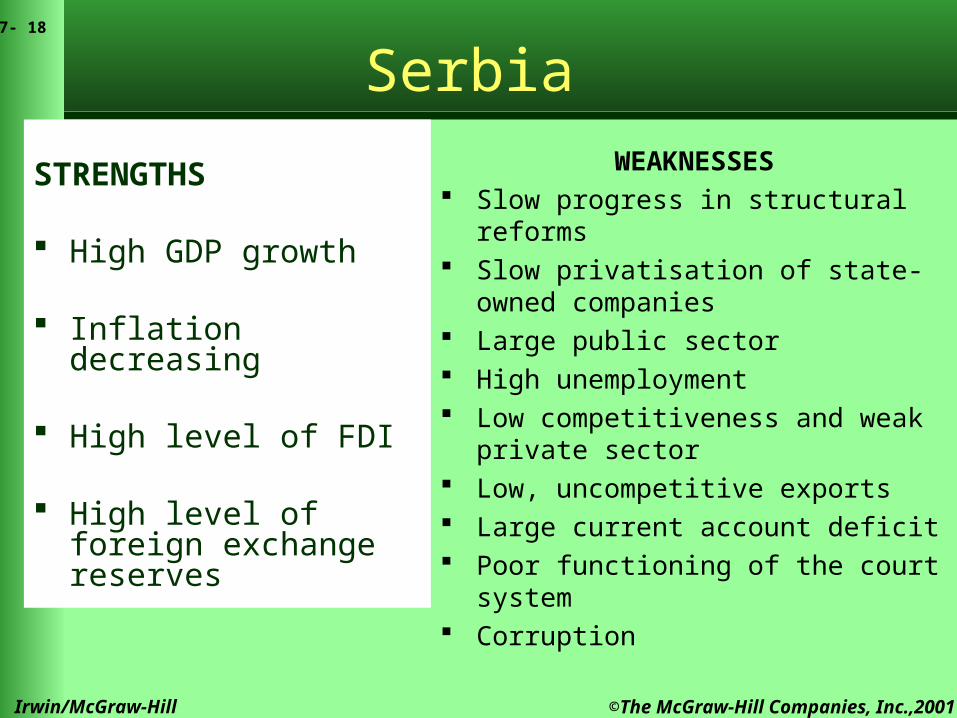

Serbia

STRENGTHS

High GDP growth

Inflation decreasing

High level of FDI

High level of foreign exchange reserves

WEAKNESSES Slow progress in structural

reforms Slow privatisation of state-

owned companies Large public sector High unemployment Low competitiveness and weak

private sector Low, uncompetitive exports Large current account deficit Poor functioning of the court

system Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 19

Irwin/McGraw-Hill

HUNGARY

STRENGTHSEU Member Preparations for euro membership under way

Budget deficit Declining inflatory pressures

Rising FDI and improving investment climate

WEAKNESSES

Large public debt

trade deficit

current account deficit

external debt increasing

©The McGraw-Hill Companies, Inc.,2001

17- 20

Irwin/McGraw-Hill

RomaniaSTRENGTHS

EU MemberHigh GDP growthBooming economyInflation decreasingHigh level of FDIHigh level of foreign exchange reserves

WEAKNESSES

Unemployment Weak private sector Fiscal loosening and rising

budget deficit Rapid credit growth Large trade deficit Large current account deficit Poor functioning of the court

system Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 21

Irwin/McGraw-Hill

BulgariaSTRENGTHS

EU Member

High GDP growth Low public debt Preparations for euro membership under way

Declining inflatory pressures

Rising FDI and improving investment climate

WEAKNESSES

Large trade deficit Large current account

deficit external debt

increasing Private sector

external debt increasing

Poor functioning of the court system

Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 22

Irwin/McGraw-Hill

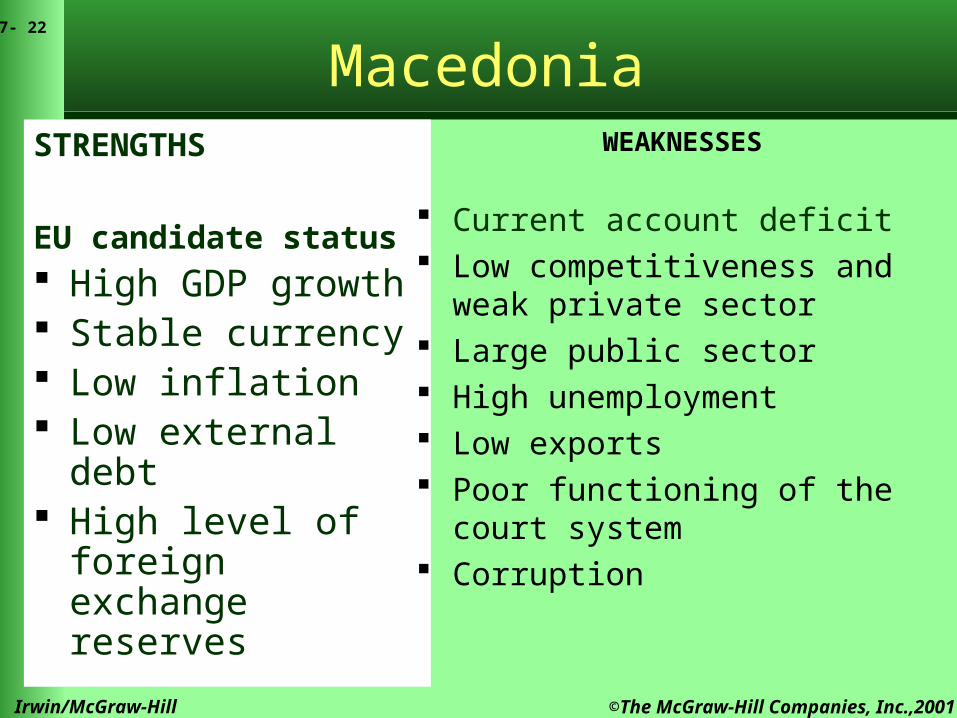

STRENGTHS

EU candidate status High GDP growth Stable currency Low inflation Low external debt High level of foreign

exchange reserves

WEAKNESSES

Current account deficit Low competitiveness and weak private sector

Large public sector High unemployment Low exports Poor functioning of the court system

Corruption

Macedonia

©The McGraw-Hill Companies, Inc.,2001

17- 23

Irwin/McGraw-Hill

Albania

STRENGTHS

SAA signed Progress in privatisation High GDP growth Low inflation Unemployment decreasing Low external debt and low

servicing costs High level of foreign exchange

reserves

WEAKNESSES

Low competitiveness and weak private sector

High general government debt

Rapid credit growth Low exports Large current account

deficit Budget deficit Poor functioning of

the court system Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 24

Irwin/McGraw-Hill

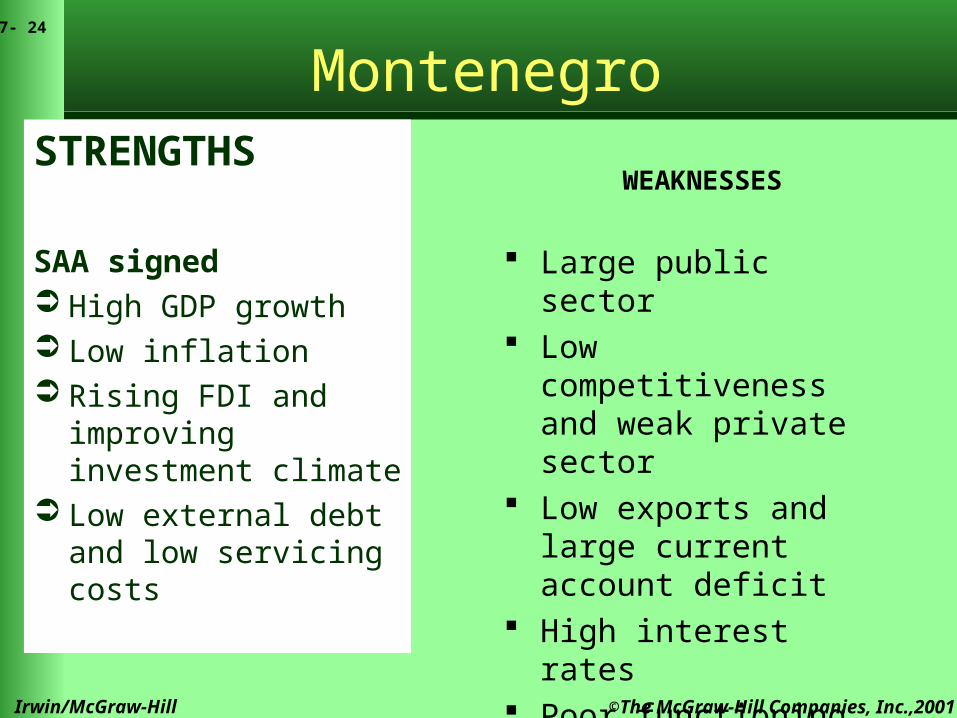

MontenegroSTRENGTHS

SAA signed High GDP growth Low inflation Rising FDI and

improving investment climate

Low external debt and low servicing costs

WEAKNESSES

Large public sector Low competitiveness and

weak private sector Low exports and large

current account deficit High interest rates Poor functioning of the

court system Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 25

Irwin/McGraw-Hill

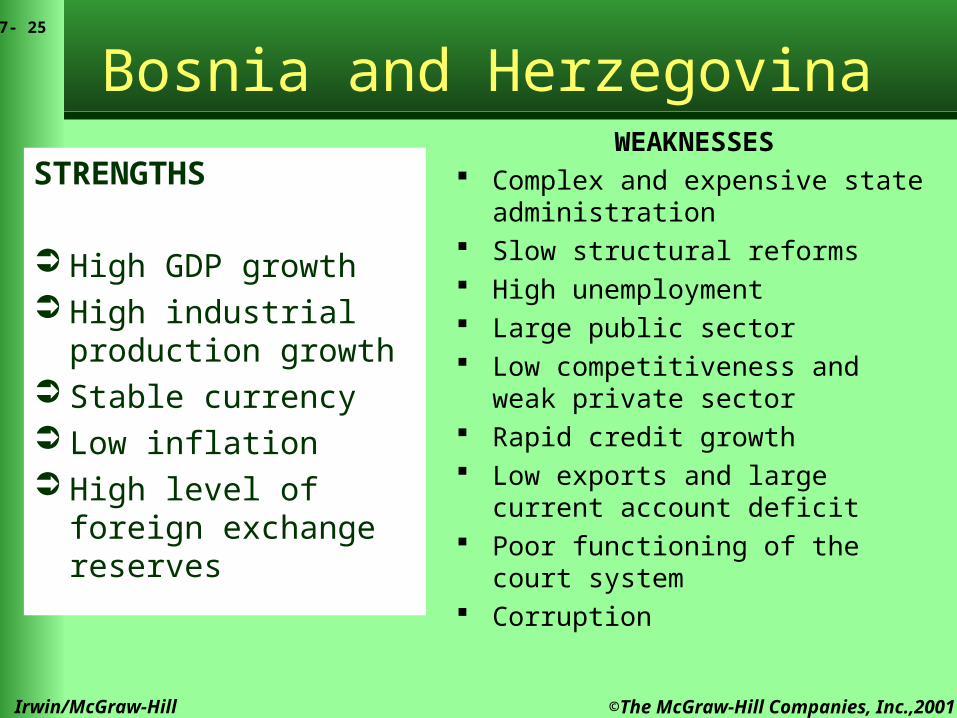

Bosnia and Herzegovina

STRENGTHS

High GDP growth High industrial production

growth Stable currency Low inflation High level of foreign

exchange reserves

WEAKNESSES Complex and expensive state

administration Slow structural reforms High unemployment Large public sector Low competitiveness and weak private

sector Rapid credit growth Low exports and large current account

deficit Poor functioning of the court system Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 26

Irwin/McGraw-Hill

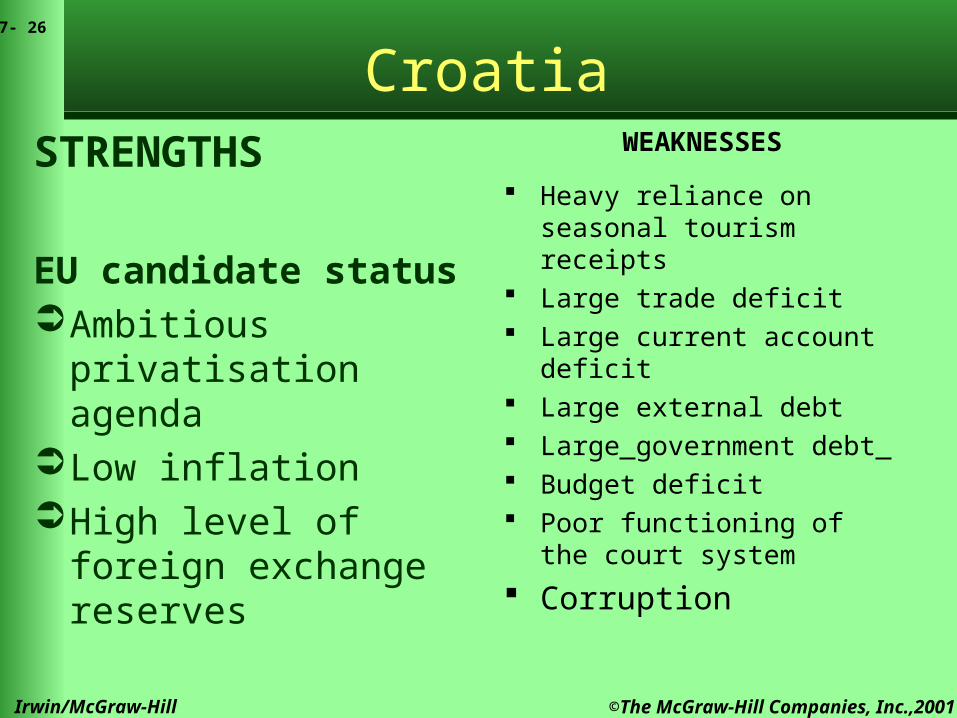

CroatiaSTRENGTHS

EU candidate status Ambitious privatisation agenda

Low inflationHigh level of foreign exchange reserves

WEAKNESSES

Heavy reliance on seasonal tourism receipts

Large trade deficit Large current account

deficit Large external debt Large government debt Budget deficit Poor functioning of

the court system

Corruption

©The McGraw-Hill Companies, Inc.,2001

17- 27

Irwin/McGraw-Hill

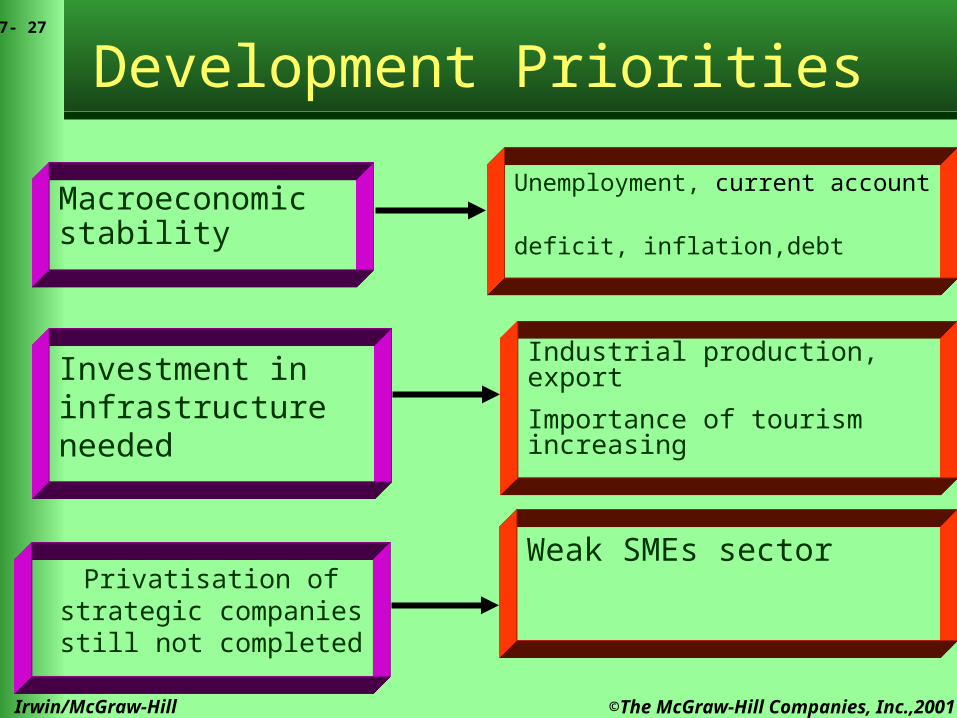

Development Priorities

Macroeconomic stability

Privatisation of strategic companies still not completed

Investment in infrastructure needed

Unemployment, current account

deficit, inflation,debt

Industrial production, export

Importance of tourism increasing

Weak SMEs sector