Embed Size (px)

Citation preview

1 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

TThe Financial System:he Financial System:Institutions, Loanable Funds,Institutions, Loanable Funds,

and the Impact of Deficits and the Impact of Deficits

Introduction to Political Economy: Introduction to Political Economy: MacroeconomicsMacroeconomicsWashington University – St. LouisWashington University – St. Louis

Mark VaughanMark VaughanFall 2008Fall 2008

2 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Lecture OutlineLecture Outline

• Overview of the U.S. Financial System

• Important Identities about Saving and Investment

• The Loanable Funds Market

• Pro-Growth Policies and the Loanable Funds Market Economic Impact of tax breaks for private saving Economic Impact of tax breaks for private investment

• Economic Impact of Government Deficits

3 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

U.S. Financial SystemU.S. Financial System

• Consists of institutions in the economy that match savers and borrowers.

• Can be decomposed into two categories: Financial markets Financial intermediaries

.

4 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

• Financial markets: channel funds directly from savers to borrowers. Equity Market Debt Market

• Financial intermediaries: channel funds indirectly from savers to borrowers. Depository institutions Mutual funds Other non-depository institutions

(pension funds, insurance companies, etc.)

U.S. Financial SystemU.S. Financial System

5 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Financial Markets: Financial Markets: Debt MarketDebt Market

• A debt security is a loanloan.• Debt market largerlarger than equity market.• Characteristics of debt securities:

- Term: Length of time until maturity- Cash Flows: Periodic interest + principal at maturity- Credit Risk: Probability interest or principal will not be repaid- Liquidity Risk: Probability of significant “Fire Sale” loss- Tax Treatment: Municipal bonds exempt from federal taxes

• Types of debt securities:- Money market: (maturity ≤ 1 year)- Bond market: (maturity > 1 year)

• Bond prices change when:- Opportunity cost of invested funds changes (↑ causes prices to ↓)- Perceived default or liquidity risk changes (↑ causes prices to ↓)

6 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Financial Markets: Financial Markets: Equity MarketEquity Market

• Equity – Ownership stake- Preferred stock – no voting rights, dividend paid first- Common stock – voting rights, dividends paid last

• Compared to debt securities, stocks offer potentially higher returns but with more risk

• Stock prices change when: - Opportunity cost of invested funds changes (↑ causes prices to ↓)(↑ causes prices to ↓)

- Expected dividends changes (↑ causes prices to (↑ causes prices to ↓)↓)

• Important U.S. Stock Markets: - New York Stock Exchange- American Stock Exchange- NASDAQ (over the counter)

7 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Financial Intermediaries:Financial Intermediaries:Depository InstitutionsDepository Institutions

• Take deposits and funds loans (i.e., intermediate)(i.e., intermediate)

- Profit chiefly from spread between interest on deposits and (higher) interest on loans.

• Help create medium of exchangemedium of exchange by allowing checks to be written against deposits.

• Types (as of 6/30/08)(as of 6/30/08)

- Banks: 7,203 holding $11.4 trillion in assets- Thrifts: 1,208 holding $1.9 trillion in assets- Credit Unions: 8,101 holding $753.5 billion in assets

Source: FDIC, NCUA

8 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Financial Intermediaries:Financial Intermediaries:Mutual FundsMutual Funds

• Sell shares to public, buy portfolios of debt & equity securities• Industry size / scope (year-end 2007):

- ≈8,000 U.S. funds with ≈$12 trillion in assets.- ≈66,000 funds worldwide with ≈$66 trillion in assets

• Permit small investors to diversify cheaply

• Types (by portfolio, U.S., year-end 2007):- Equity = 54.3 % (of $12 trillion in assets)- Bond = 14.0%- Money Market = 25.8%- Hybrid = 5.9%

• Types (by fund strategies)- Actively managed- Index funds (11% of total assets, year-end 2007)

Source: 2008 Investment Company Fact Book

9 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Financial Intermediaries:Financial Intermediaries:Mutual FundsMutual Funds

Special Type of Actively Managed Mutual Fund: Hedge FundHedge FundCaters to wealthy, sophisticated investorsSeek high returns with advanced strategies (misnomer)Employs significant leverageRequires large initial minimum investment (illiquid)Faces minimal regulationUnfairly blamed for torpedoing companies by short selling

Economically Important

≈ 10,000 active funds with $2 trillion in assets (worldwide estimates)

10 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Some Important IdentitiesSome Important Identities

• Recall GDP is both total income and expenditure in the economy:

YY = = CC + + II + + GG + + NX (1)NX (1)

• Assume a closed economy – no international trade:

Y = C + I + G (2)Y = C + I + G (2)

• Now, subtract CC and GG from both sides of (2):

Y – C – G = I (3)Y – C – G = I (3)

• Left side of (3) is total income after consumption expenditure and government purchases – i.e., national saving or just saving ((SS).).

• Substituting SS for Y – C – GY – C – G, (2) can be rewritten as:

S = I S = I (4)(4)

11 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Some Important IdentitiesSome Important Identities

• National savingNational saving, or savingsaving, is equal to:

SS = = I I (4)(4)

SS = = YY – – CC – – G G (5)(5)

• Now, adding and subtracting taxes net of transfers from right side of (5) yields:

SS = ( = (YY – – TT – – CC) + () + (TT – – GG) ) (6)(6)

Private Saving Public Saving

12 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Government Deficits and SurplusesGovernment Deficits and Surpluses

• If TT > > GG, government runs budget surplusbudget surplus because more is collected in net tax revenue than spent. (T – G) represents public saving.

• If GG > > TT, government runs budget deficitbudget deficit because more is spent than collected in net tax revenue. (G – T) represents deficit (public dissaving)

• Accumulation of past budget deficits is called government (or national) debt.

13 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Loanable Funds MarketLoanable Funds Market

• Links suppliers & demanders of loanable funds.

• Supply of loanable funds by savers (mostly households)

• Demand for loanable funds by borrowers (households and firms).

• Interest rate:- Price of borrowing, return to saving- Equilibrates quantity supplied /quantity demanded

of loanable funds.

- Real (not nominal) interest rate is key rate.

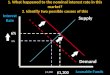

In Pictures: The Loanable Funds Market

Loanable Funds(in billions of dollars)

0

InterestRate

Supply

Demand

5%

$1,200

Real

Shifts caused by non-interest-rate determinants of

Demand for/Supply of Loanable Funds.

15 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Policy 1: Saving IncentivesPolicy 1: Saving Incentives

• Taxes on interest income substantially reduce payoff from current saving (reduce incentive to save).

• Relatively high U.S. taxes on saving lower U.S. productivity and real GDP growth.

• Reduction in tax on savings (revenue neutral) increases incentive to save at every real interest rate(rightward shift in supply of loanable-funds curve).(rightward shift in supply of loanable-funds curve).

Impact of Savings IncentivesImpact of Savings Incentives::

Lowers equilibrium real interest rate & increases equilibrium quantity of loanable funds

Increases spending on physical capital(and spending on consumer durables, too)

Raises future productivity & real GDP per capita

In Pictures: Impact of Savings Incentives

Loanable Funds(billions of dollars)

0

Supply, S1 S2

Demand

1. Tax incentives for saving increasesupply of loanablefunds…

5%

$1,200

4%

$1,600

InterestRate

Real

3. and raises equilibrium quantity of loanable funds.

2. which reducesequilibriumreal interestrate…

17 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Policy 2: Investment IncentivesPolicy 2: Investment Incentives

• Investment tax credit (ITC) is tax break for firmspurchasing new physical capital

• Increase in ITC increases incentive to borrow.

• Increase in ITC (revenue neutral) increases demandfor loanable funds at every real interest rate(rightward shift in demand curve)(rightward shift in demand curve)

Impact of Investment IncentiveImpact of Investment Incentive:: Lowers equilibrium real interest rate &

raises equilibrium quantity of loanable funds

Increases spending on physical capital(and spending on consumer durables, too)

Raises future productivity & real GDP per capita

In Pictures: Impact of Investment Incentives

Loanable Funds(in billions of dollars)

0

Supply

Demand, D1

D2

5%

$1,200

6%

$1,400

InterestRate

Real

1. Tax incentives for investment increases demand for loanable funds…

2. which raisesequilibriumreal interestrate…

3. and raises equilibrium quantity of loanable funds.

19 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Equity – Efficiency TradeoffEquity – Efficiency Tradeoff

• Tax breaks for savings and investment will increase future productivity and real GDP per capita.

• But such tax breaks could disproportionately benefit wealthy in the short run.

20 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Policy 3: Budget DeficitsPolicy 3: Budget Deficits

• Government borrowing to finance deficits reduces supply of loanable funds available to borrowers (crowding out). (crowding out).

• Graphically: Increase in deficit decreases supply of (private) loanable funds at every real interest rate(shifts curve to left)(shifts curve to left).

Impact of Increase in Budget DeficitImpact of Increase in Budget Deficit::

Raises equilibrium real interest rate & lowers equilibrium quantity of loanable funds

Lowers spending on physical capital (and consumer durables, too)

Lowers future productivity & real GDP per capita- real cost of deficits

In Pictures: Impact of Increase in Budget Deficit

Loanable Funds(billions of dollars)

0

S2 Supply, S1

Demand

$1,200

5%

$800

6%

InterestRate

Real

1. Increase in deficit decreases (private) supply of loanable funds…

2. which raisesequilibriumreal interestrate…

3. and lowers equilibrium quantity of loanable funds.

22 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Should We Worry about Deficits?Should We Worry about Deficits?

Depends on: • How big the deficits are, relatively speaking:

Nominal Federal Deficit / GDP Nominal Federal Debt / GDP

• When deficits are incurred:• Recession (good) vs. boom (bad)• Cut in taxes (could be good) in government spending (could be bad)

• Why deficits are being incurred: Public investment or war (good) vs. consumption (bad)

• What impact deficits have on private investment: Small (good) vs. large (bad)

(High ratios are bad)(High ratios are bad)

23 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Causes of Recent DeficitsCauses of Recent Deficits

Deficits incurred for sensible reasons (for the most part)!Deficits incurred for sensible reasons (for the most part)!

24 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Deficits Not LargeDeficits Not LargeAs a Percentage of GDPAs a Percentage of GDP

Deficits averaged 22.2% of GDP during World War II!Deficits averaged 22.2% of GDP during World War II!

U.S. Government Debt in Long-Run Historical Perspective

Percentof GDP

1790 1810 1830 1850 1870 1890 1910 1930 1950 1970 1990

RevolutionaryWar

2010

CivilWar World War I

World War II

0

20

40

60

80

100

120

Even with recent run-up, Debt/GDP ratio is not

high by historical standards.

26 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

How Important is Crowding Out?How Important is Crowding Out?

Evidence points to modest “crowding out” effect in U.S.: Deficits do not raise real interest rates that much. Increases in real interest rate attracts foreign savings. Private investment spending more sensitive to current state

of the economy than real interest rates.

Upshot: Even at current levels, impact of U.S government budget deficits on future productivity and real GDP growth is likely to be small.

27 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

Bottom Line on DeficitsBottom Line on Deficits

• At current levels, “much ado about nothing”

• Focus should be on government spending (represents public sector’s claim on private resources)(represents public sector’s claim on private resources)

• How that spending is financed (taxes, borrowing, money (taxes, borrowing, money

creation)creation) is second order.

28 - 27Presentation Last Edited: 04/18/23

Vaughan–104/Fall 2008The Financial System

TThe Financial System:he Financial System:Institutions, Loanable Funds,Institutions, Loanable Funds, and the Impact of Deficits??? and the Impact of Deficits???

Introduction to Political Economy: Introduction to Political Economy: MacroeconomicsMacroeconomicsWashington University – St. LouisWashington University – St. Louis

Mark VaughanMark VaughanFall 2008Fall 2008

Questions over