Embed Size (px)

Citation preview

1

CIFP Annual National Conference 20041 - Capital Markets Overview - Second Quarter 20042 – Investing for Income3 – Asian Exposure

Tuesday June 15, 2004Tuesday June 15, 2004

2

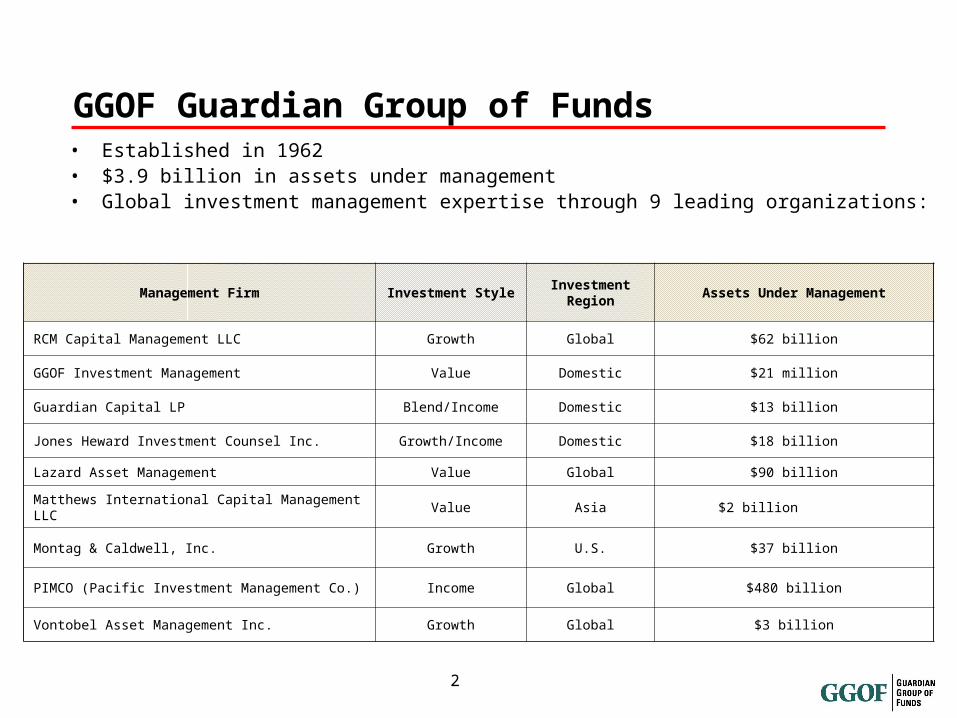

GGOF Guardian Group of Funds• Established in 1962• $3.9 billion in assets under management• Global investment management expertise through 9 leading organizations:

Management Firm Investment StyleInvestment

RegionAssets Under Management

RCM Capital Management LLC Growth Global $62 billion

GGOF Investment Management Value Domestic $21 million

Guardian Capital LP Blend/Income Domestic $13 billion

Jones Heward Investment Counsel Inc. Growth/Income Domestic $18 billion

Lazard Asset Management Value Global $90 billion

Matthews International Capital Management LLC Value Asia $2 billion

Montag & Caldwell, Inc. Growth U.S. $37 billion

PIMCO (Pacific Investment Management Co.) Income Global $480 billion

Vontobel Asset Management Inc. Growth Global $3 billion

3

A New Era of Single-Digit Returns

• Moderate growth and inflation looking forward

• Single-digit return expectations for most Canadian asset classes in the next few years

• Stock market leadership requires powerful earnings momentum

• Current income a much larger portion of total returns

4

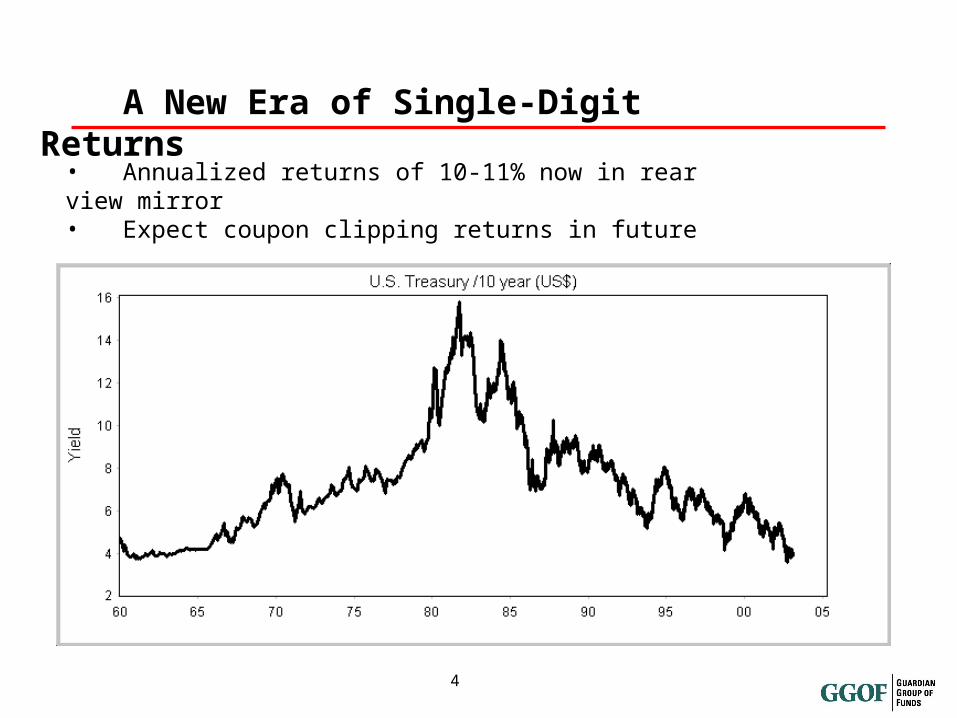

A New Era of Single-Digit Returns

• Annualized returns of 10-11% now in rear view mirror• Expect coupon clipping returns in future

5

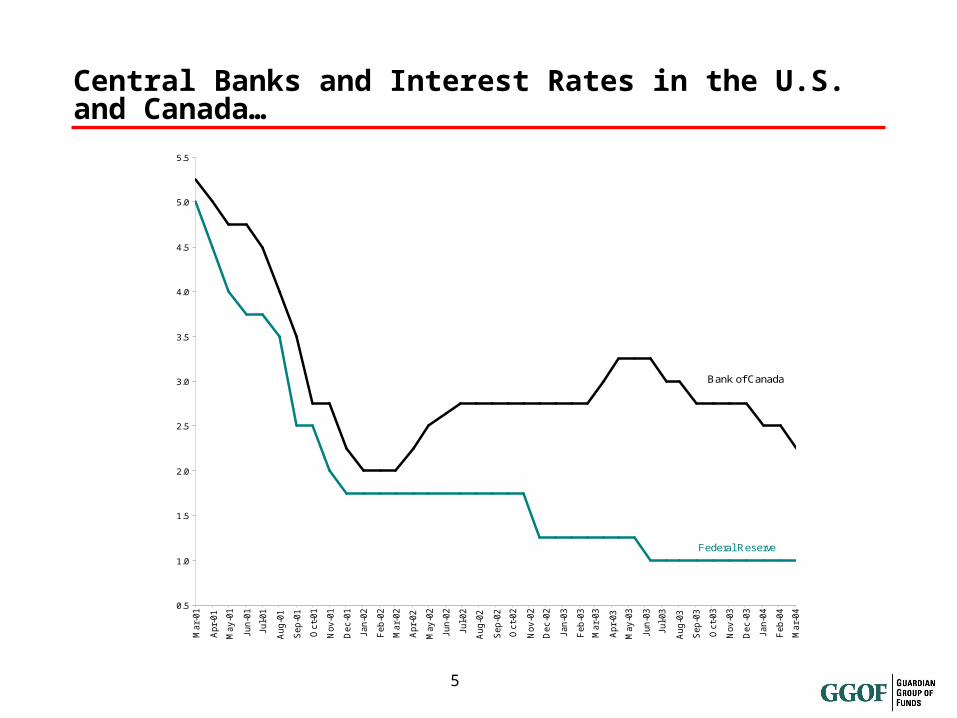

Central Banks and Interest Rates in the U.S. and Canada…

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Mar-

01

Apr-

01

May-0

1

Jun-0

1

Jul-01

Aug-0

1

Sep-0

1

Oct-

01

Nov-0

1

Dec-0

1

Jan-0

2

Feb-0

2

Mar-

02

Apr-

02

May-0

2

Jun-0

2

Jul-02

Aug-0

2

Sep-0

2

Oct-

02

Nov-0

2

Dec-0

2

Jan-0

3

Feb-0

3

Mar-

03

Apr-

03

May-0

3

Jun-0

3

Jul-03

Aug-0

3

Sep-0

3

Oct-

03

Nov-0

3

Dec-0

3

Jan-0

4

Feb-0

4

Mar-

04

Federal Reserve

Bank of Canada

6

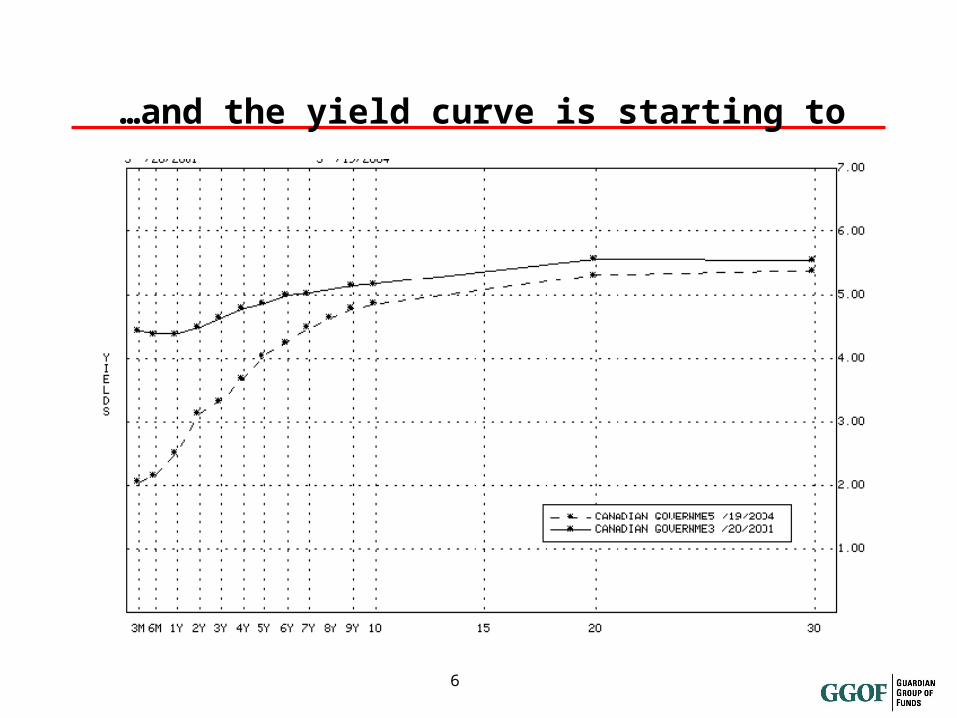

…and the yield curve is starting to steepen again.

7

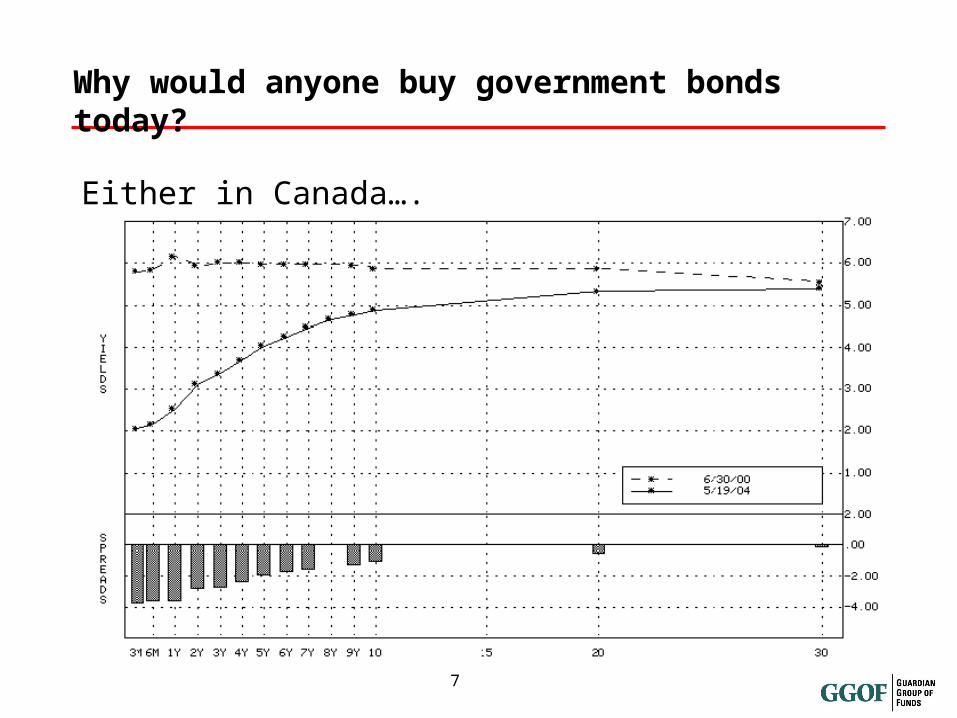

Why would anyone buy government bonds today?

Either in Canada….

8

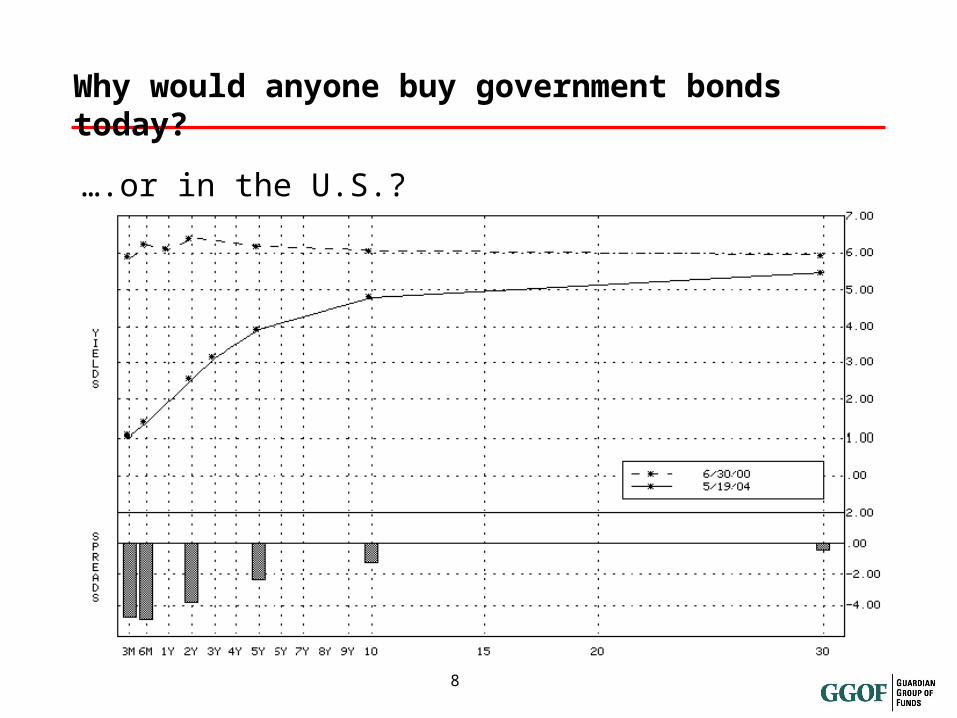

Why would anyone buy government bonds today?

….or in the U.S.?

9

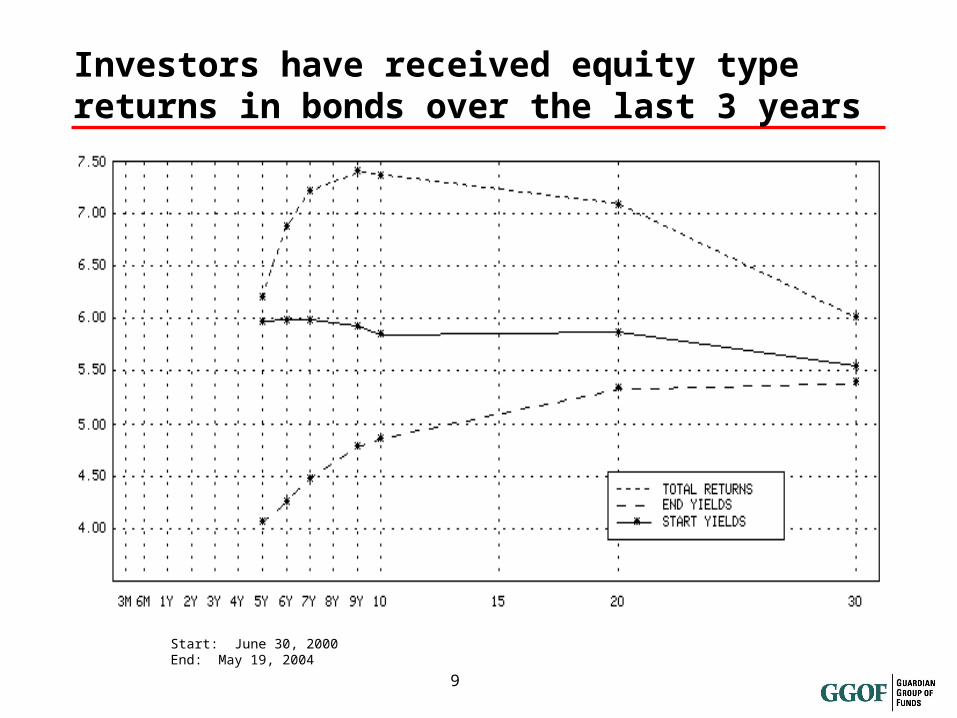

Investors have received equity type returns in bonds over the last 3 years

Start: June 30, 2000End: May 19, 2004

10

Reasons to Consider ‘Non-Traditional’ Income Alternatives

• Coupon returns for traditional income products

• Promising outlook for income products with equity-like characteristics

• Well-developed markets now for ‘non-traditional’ income products

• Value of low or non-correlated asset classes

11

Non-traditional Income Alternatives

• Preferred shares

• High yield bonds

• Income trusts

• Dividend-paying common shares

12

Preferred Shares

• Exchangeable, retractable and floating rate preferred shares provide:

• stable, tax-effective income

• low volatility

• $1.00 of dividend income and $1.25 - $1.30 of interest income both produce the same after-tax income

• Dividends provide yield support, which contributes to price stability

• High quality (P1/P2) preferred share market shrinking

• Be careful: Know what you are buying because issue features vary greatly

13

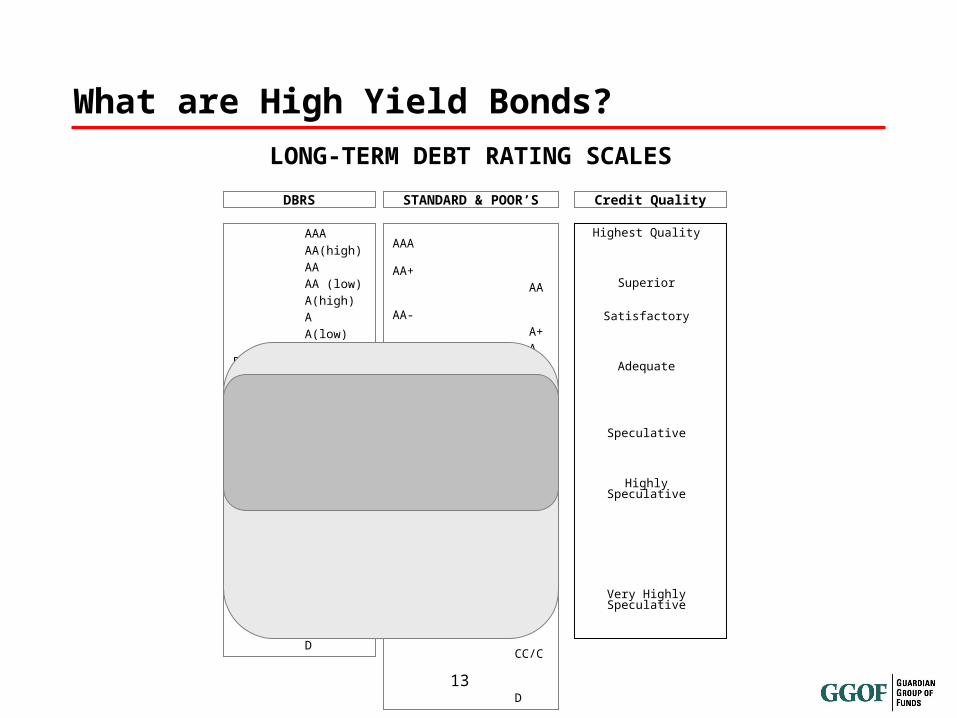

What are High Yield Bonds?

LONG-TERM DEBT RATING SCALES

STANDARD & POOR’SDBRS

Highest Quality

Superior

Satisfactory

Adequate

Speculative

Highly Speculative

Very Highly Speculative

Credit Quality

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB-

BB+ BB BB- B+ B B-

CCC+ CCC CCC- CC/C D

AAA AA(high) AA AA (low) A(high) A A(low) BBB(high) BBB BBB(low)

BB(high) BB BB(low) B(high) B B(low) CCC

CC/C

D

14

* ScotiaCapital BBB Index prior to inception of High Yield Index December 31/1994

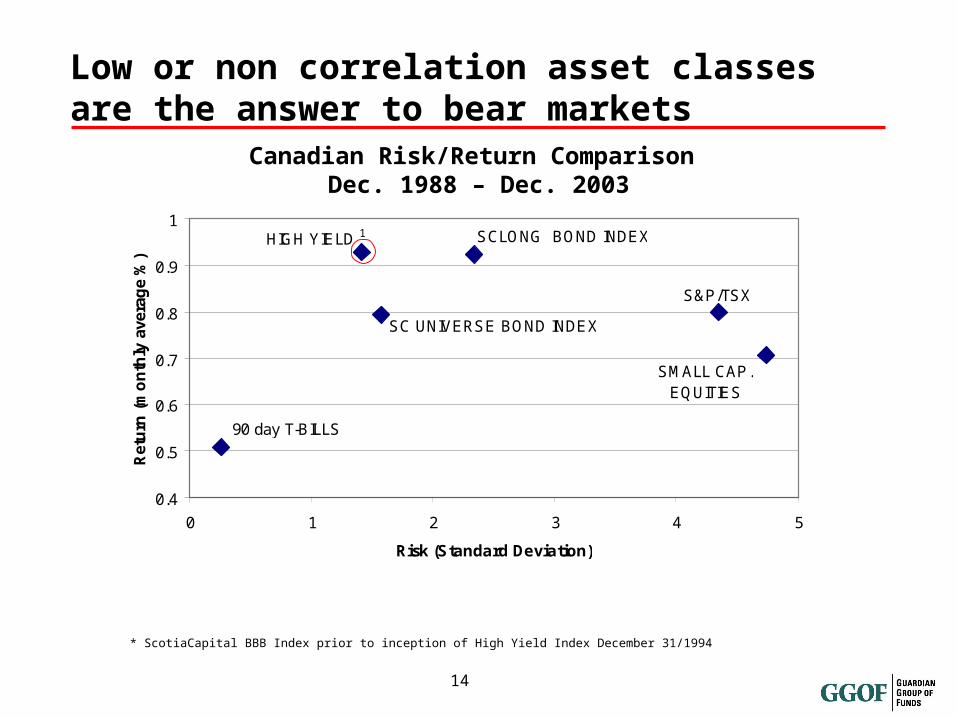

Low or non correlation asset classes are the answer to bear markets

Canadian Risk/Return Comparison Dec. 1988 – Dec. 2003

0.4

0.5

0.6

0.7

0.8

0.9

1

0 1 2 3 4 5

Risk (Standard Deviation)

Ret

urn

(m

on

thly

ave

rag

e %

)

SC UNIVERSE BOND INDEX

90 day T-BILLS

HIGH YIELD 1

S&P/TSX

SMALL CAP.EQUITIES

SCLONG BOND INDEX

15

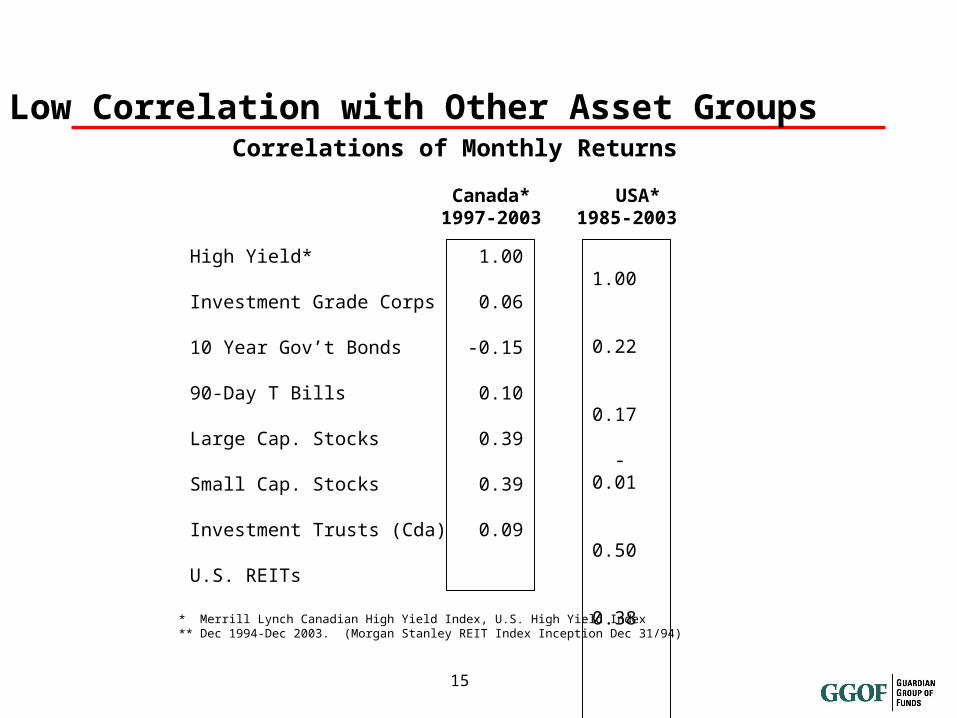

High Yield*

Investment Grade Corps

10 Year Gov’t Bonds

90-Day T Bills

Large Cap. Stocks

Small Cap. Stocks

Investment Trusts (Cda)

U.S. REITs

1.00

0.06

-0.15

0.10

0.39

0.39

0.09

Correlations of Monthly Returns

* Merrill Lynch Canadian High Yield Index, U.S. High Yield Index** Dec 1994-Dec 2003. (Morgan Stanley REIT Index Inception Dec 31/94)

1.00

0.22

0.17

-0.01

0.50

0.38

0.31**

Canada*1997-2003

USA*1985-2003

Low Correlation with Other Asset Groups

16

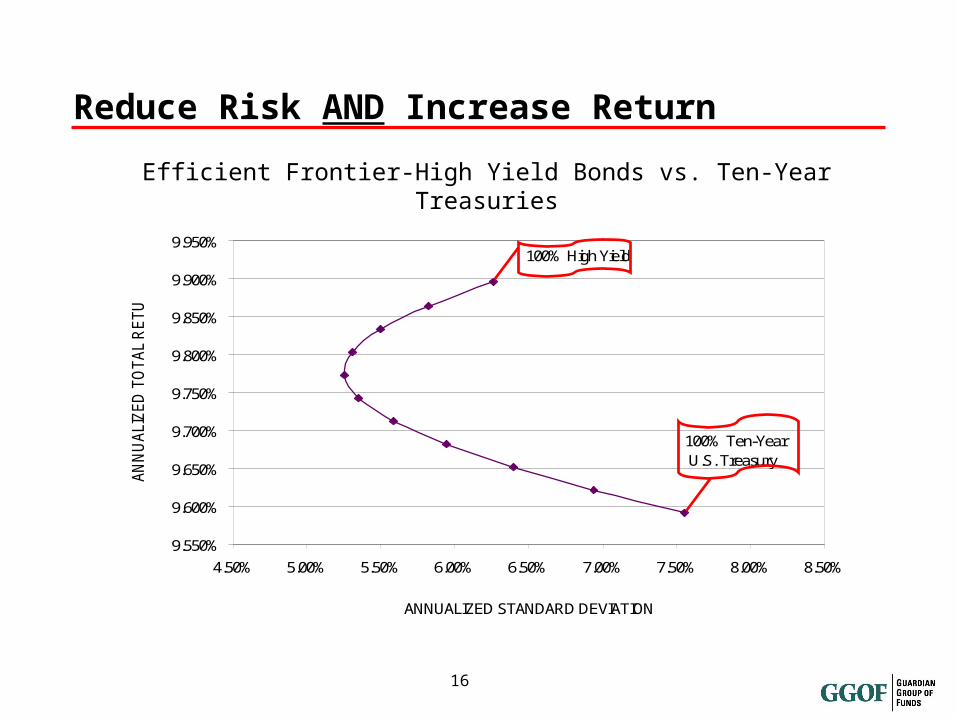

Reduce Risk AND Increase Return

Efficient Frontier-High Yield Bonds vs. Ten-Year Treasuriesmonthly, 1985 - Q1 2003

Source: Merrill Lynch & Co.

9.550%

9.600%

9.650%

9.700%

9.750%

9.800%

9.850%

9.900%

9.950%

4.50% 5.00% 5.50% 6.00% 6.50% 7.00% 7.50% 8.00% 8.50%

ANNUALIZED STANDARD DEVIATION

AN

NU

ALI

ZE

D T

OT

AL

RE

TU

RN

100% Ten-Year U.S. Treasury

100% High Yield

17

High Yield Bonds

• Dual nature helps performance in all market environments

• Interest-sensitive nature causes price appreciation when interest rates fall

• Stronger economies that produce rising rates also benefit high yield issuer companies

• Low correlation with other asset classes provides diversification benefits

• Total returns driven by income, not capital gains

• Keys are credit analysis and issuer knowledge

• Fund eliminates most of the single issuer risk

18

Income Trusts

• Power and Pipeline Trusts utility type income

• Real Estate Investment Trusts (REITs) produce rental income

• Royalty Trust Units (RTUs) produce resource royalty income

• Business Trust Units (BTUs) produce business income

• Return of Capital (ROC) is very tax-efficient

• Tax liability is deferred

• Ultimately paid at lower capital gains rate

• Can act as an inflation hedge

• Low correlation with other asset classes provides diversification

19

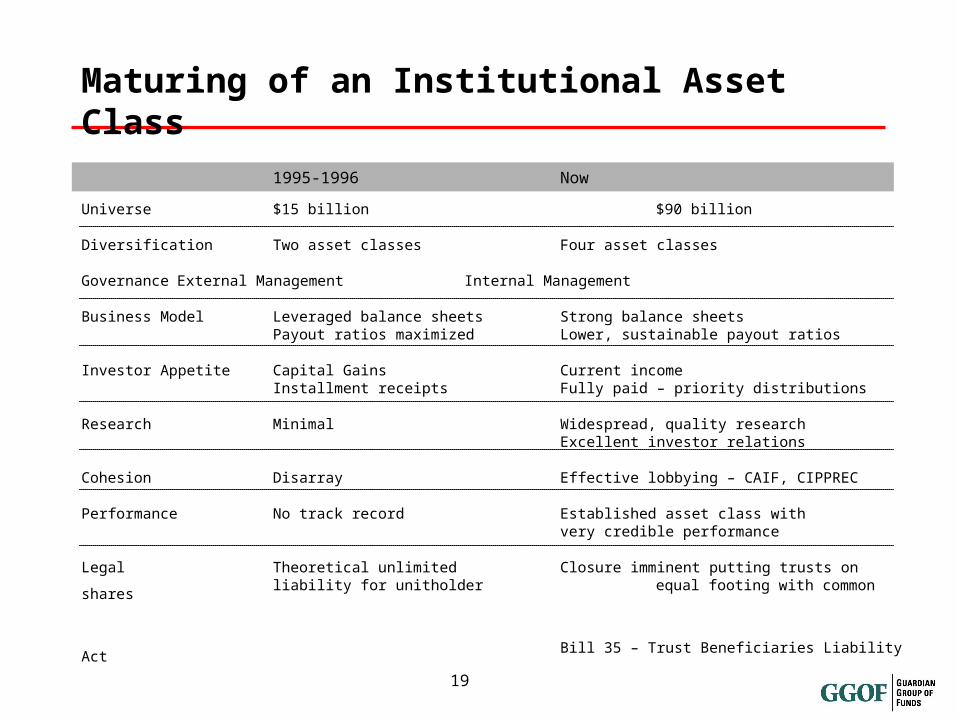

Maturing of an Institutional Asset Class

1995-1996 Now

Universe $15 billion $90 billion

Diversification Two asset classes Four asset classes

Governance External Management Internal Management

Business Model Leveraged balance sheets Strong balance sheetsPayout ratios maximized Lower, sustainable payout ratios

Investor Appetite Capital Gains Current incomeInstallment receipts Fully paid – priority distributions

Research Minimal Widespread, quality researchExcellent investor relations

Cohesion Disarray Effective lobbying – CAIF, CIPPREC

PerformanceNo track record Established asset class with very credible performance

Legal Theoretical unlimited Closure imminent putting trusts onliability for unitholder equal footing with common shares

Bill 35 – Trust Beneficiaries Liability Act

20

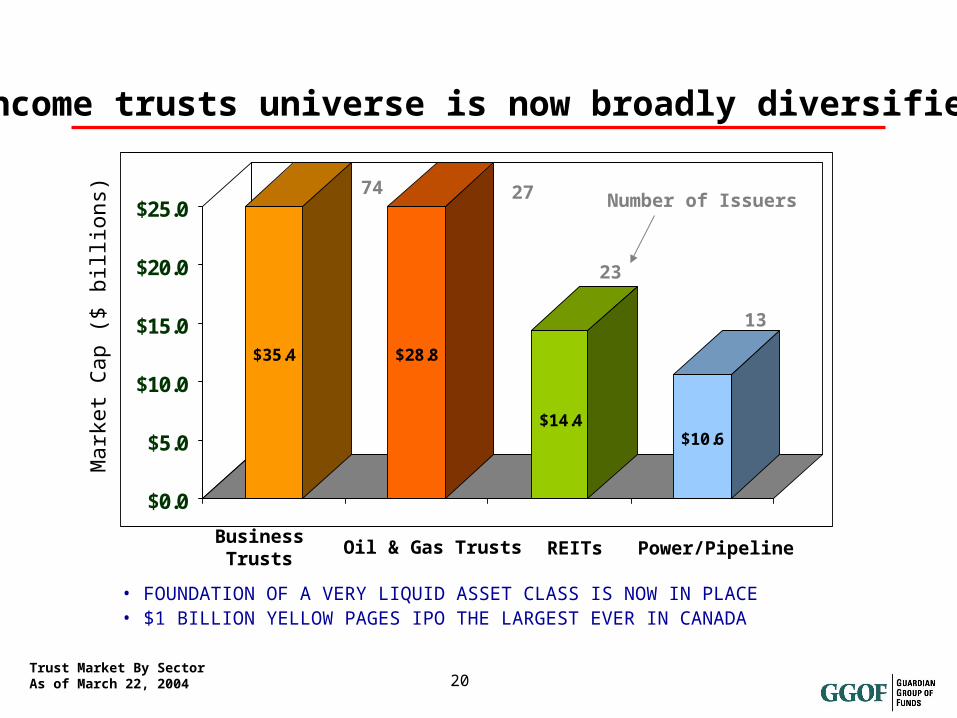

$35.4 $28.8

$14.4$10.6

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

Oil & Gas TrustsBusiness Trusts REITs Power/Pipeline

Mark

et

Cap

($

bill

ions)

74 27

23

13

Income trusts universe is now broadly diversified

Trust Market By SectorAs of March 22, 2004

• FOUNDATION OF A VERY LIQUID ASSET CLASS IS NOW IN PLACE• $1 BILLION YELLOW PAGES IPO THE LARGEST EVER IN CANADA

Number of Issuers

21

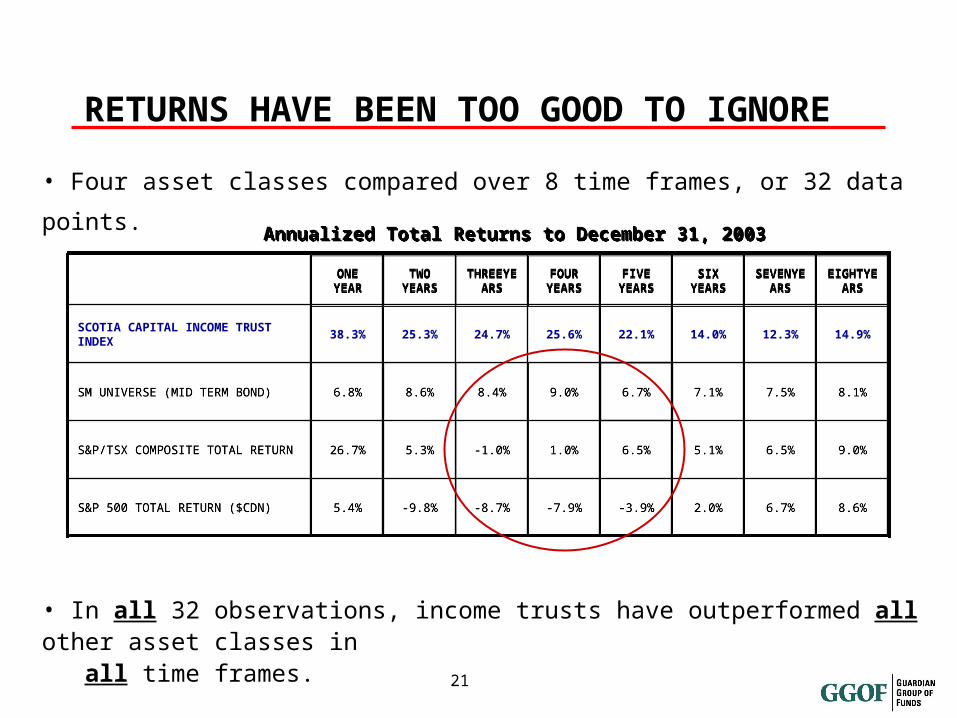

RETURNS HAVE BEEN TOO GOOD TO IGNORE

Annualized Total Returns to December 31, 2003Annualized Total Returns to December 31, 2003

• Four asset classes compared over 8 time frames, or 32 data points.

• In all 32 observations, income trusts have outperformed all other asset classes in all time frames.

5.4%5.4%

26.7%26.7%

6.8%6.8%

38.3%

ONE YEARONE

YEAR

8.6%8.6%6.7%6.7%2.0%2.0%-3.9%-3.9%-7.9%-7.9%-8.7%-8.7%-9.8%-9.8%S&P 500 TOTAL RETURN ($CDN)S&P 500 TOTAL RETURN ($CDN)

9.0%9.0%6.5%6.5%5.1%5.1%6.5%6.5%1.0%1.0%-1.0%-1.0%5.3%5.3%S&P/TSX COMPOSITE TOTAL RETURNS&P/TSX COMPOSITE TOTAL RETURN

8.1%8.1%7.5%7.5%7.1%7.1%6.7%6.7%9.0%9.0%8.4%8.4%8.6%8.6%SM UNIVERSE (MID TERM BOND)SM UNIVERSE (MID TERM BOND)

14.9%12.3%14.0%22.1%25.6%24.7%25.3%SCOTIA CAPITAL INCOME TRUST INDEX

EIGHTYEARS

EIGHTYEARS

SEVENYEARS

SEVENYEARS

SIX YEARS

SIX YEARS

FIVE YEARS

FIVE YEARS

FOUR YEARSFOUR

YEARSTHREEY

EARSTHREEY

EARSTWO

YEARSTWO

YEARS

22

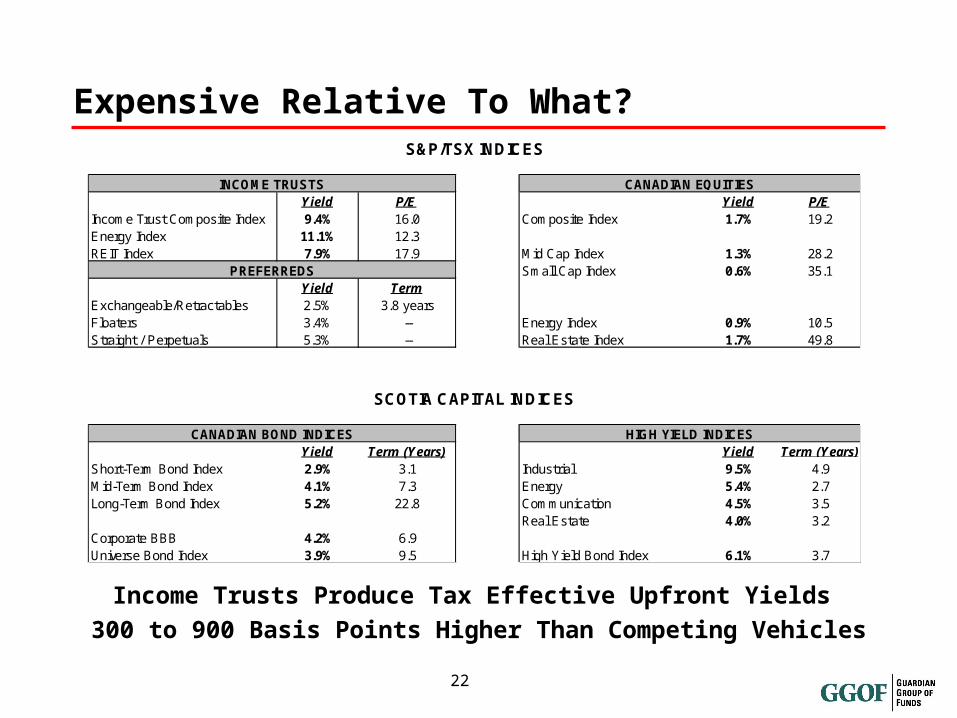

Expensive Relative To What?

Income Trusts Produce Tax Effective Upfront Yields 300 to 900 Basis Points Higher Than Competing Vehicles

Yield P/E Yield P/EIncome Trust Composite Index 9.4% 16.0 Composite Index 1.7% 19.2Energy Index 11.1% 12.3REIT Index 7.9% 17.9 Mid Cap Index 1.3% 28.2

Small Cap Index 0.6% 35.1Yield Term

Exchangeable/Retractables 2.5% 3.8 yearsFloaters 3.4% -- Energy Index 0.9% 10.5Straight / Perpetuals 5.3% -- Real Estate Index 1.7% 49.8

Yield Term (Years) Yield Term (Years)Short-Term Bond Index 2.9% 3.1 Industrial 9.5% 4.9Mid-Term Bond Index 4.1% 7.3 Energy 5.4% 2.7Long-Term Bond Index 5.2% 22.8 Communication 4.5% 3.5

Real Estate 4.0% 3.2Corporate BBB 4.2% 6.9Universe Bond Index 3.9% 9.5 High Yield Bond Index 6.1% 3.7

S&P/TSX INDICES

INCOME TRUSTS

CANADIAN BOND INDICES

CANADIAN EQUITIES

HIGH YIELD INDICES

PREFERREDS

SCOTIA CAPITAL INDICES

23

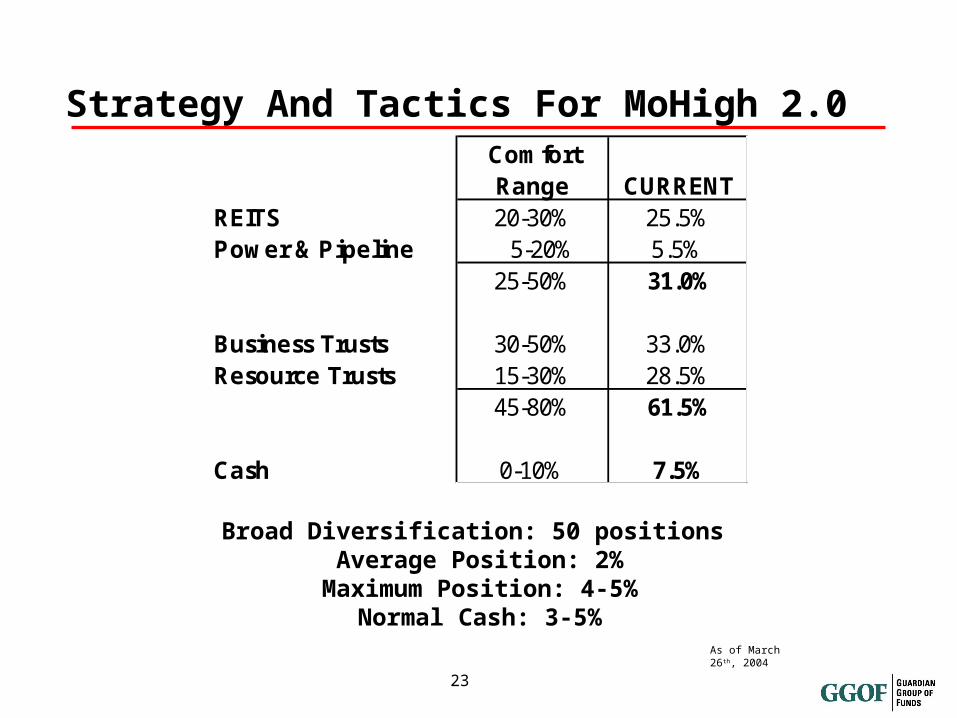

Strategy And Tactics For MoHigh 2.0

Broad Diversification: 50 positions Average Position: 2%

Maximum Position: 4-5%Normal Cash: 3-5%

ComfortRange CURRENT

REITS 20-30% 25.5%Power & Pipeline 5-20% 5.5%

25-50% 31.0%

Business Trusts 30-50% 33.0%Resource Trusts 15-30% 28.5%

45-80% 61.5%

Cash 0-10% 7.5%

As of March 26th, 2004

24

RETURN

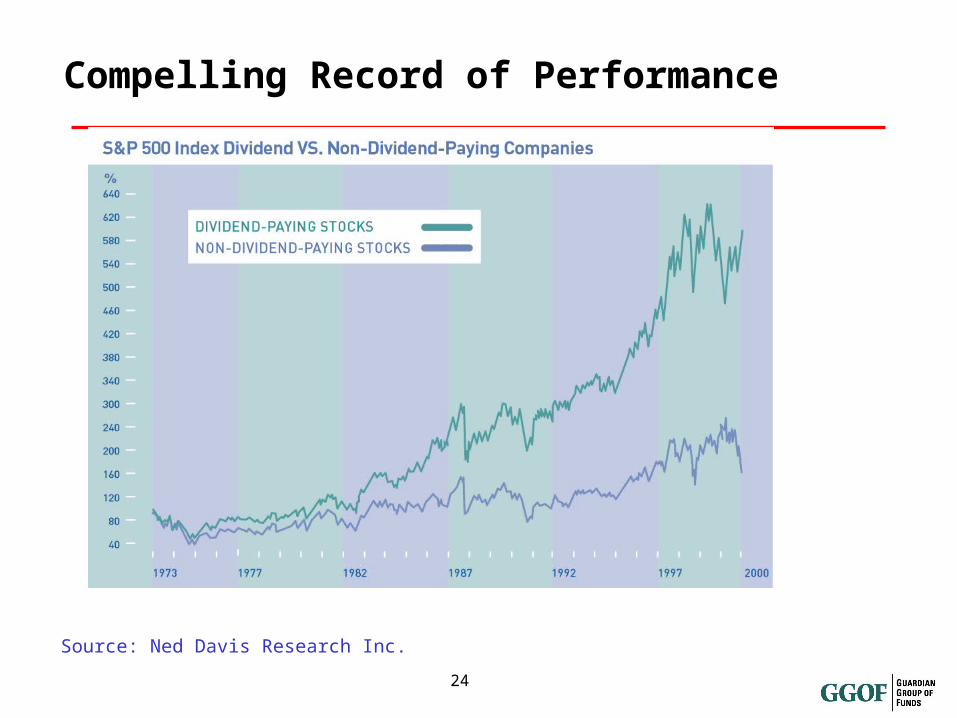

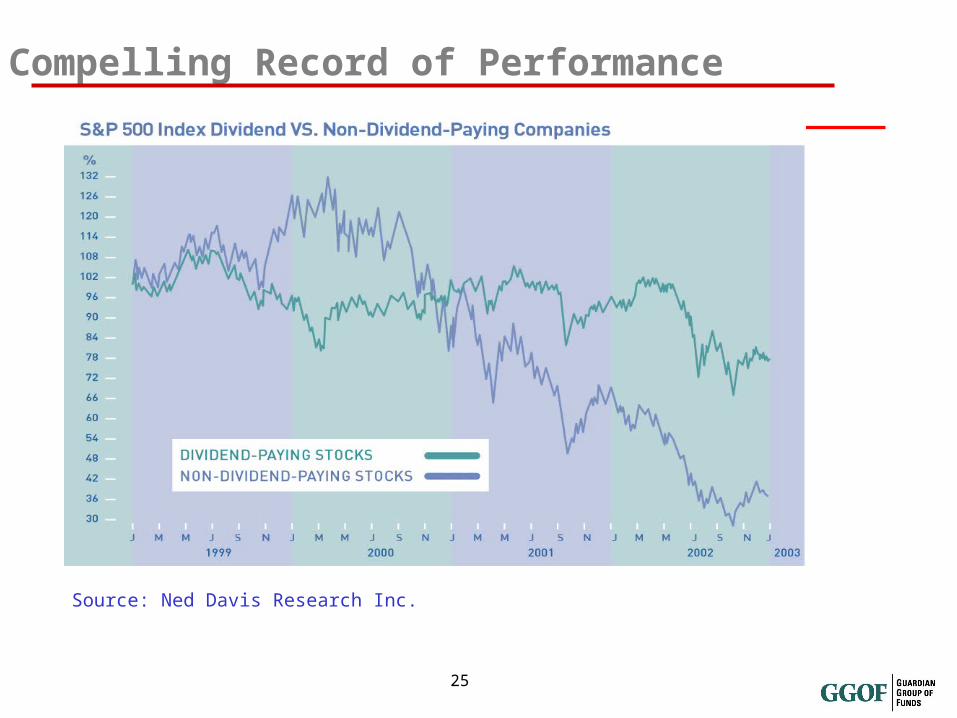

Compelling Record of Performance

Source: Ned Davis Research Inc.

25

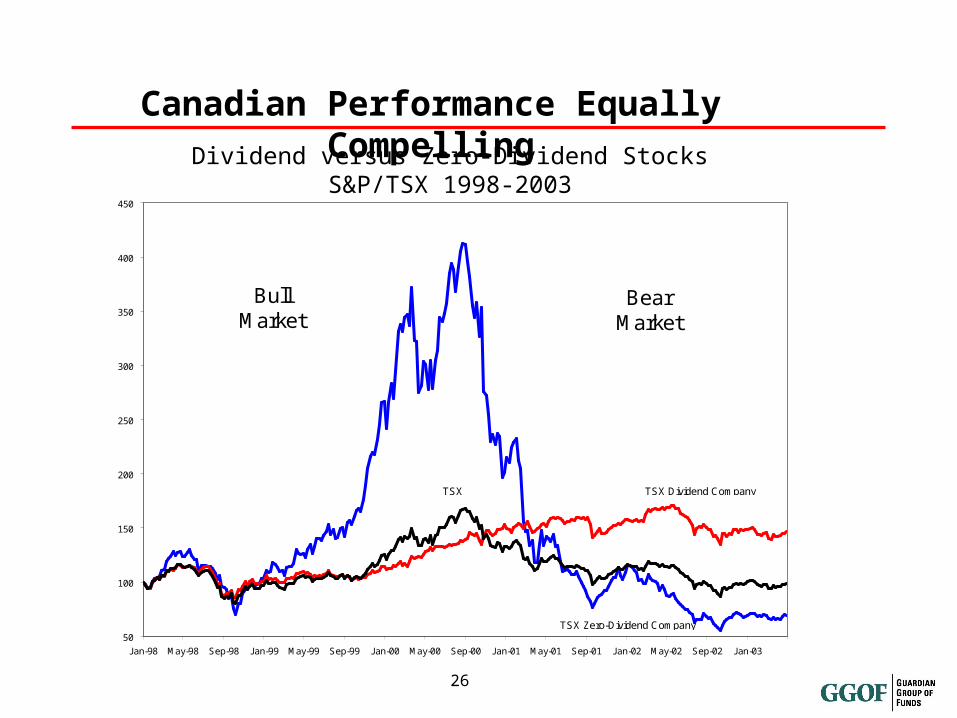

Source: Ned Davis Research Inc.

Compelling Record of Performance

26

50

100

150

200

250

300

350

400

450

Jan-98 May-98 Sep-98 Jan-99 May-99 Sep-99 Jan-00 May-00 Sep-00 Jan-01 May-01 Sep-01 Jan-02 May-02 Sep-02 Jan-03

Bull Market

Bear Market

TSX Dividend Company

TSX Zero-Dividend Company

TSX

Canadian Performance Equally Compelling

Dividend versus Zero-Dividend StocksS&P/TSX 1998-2003

27

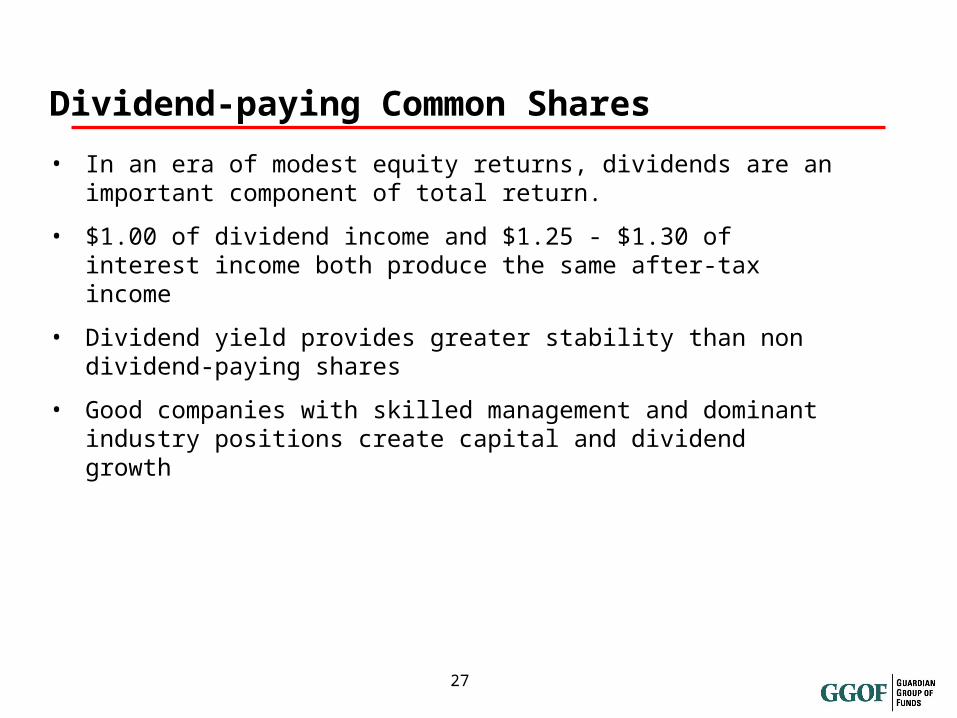

• In an era of modest equity returns, dividends are an important component of total return.

• $1.00 of dividend income and $1.25 - $1.30 of interest income both produce the same after-tax income

• Dividend yield provides greater stability than non dividend-paying shares

• Good companies with skilled management and dominant industry positions create capital and dividend growth

Dividend-paying Common Shares

28

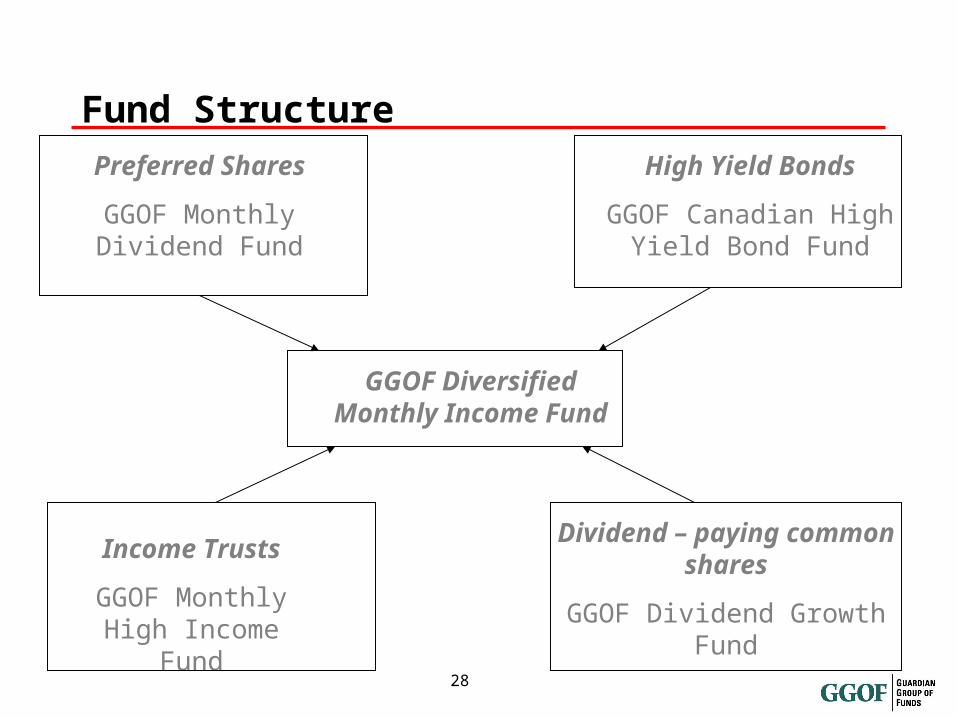

Fund Structure

Preferred Shares

GGOF Monthly Dividend Fund

High Yield Bonds

GGOF Canadian High Yield Bond Fund

GGOF Diversified Monthly Income Fund

Income Trusts

GGOF Monthly High Income Fund

Dividend – paying common shares

GGOF Dividend Growth Fund

29

Fund Benefits

• Provides tax-advantaged monthly income of 3.5 cents

• Comprised of four separate asset classes – 25% in each asset class

• Asset classes show little correlation with each other, ensuring superior diversification benefits

• Provides an easy, convenient way to invest in one product based on 4 successful GGOF funds

• Managers among the best in Canada

• John Priestman/Kevin Hall (Guardian Capital)

• Steve Kearns (Guardian Capital)

• Michael Stanley (Jones Heward)

30

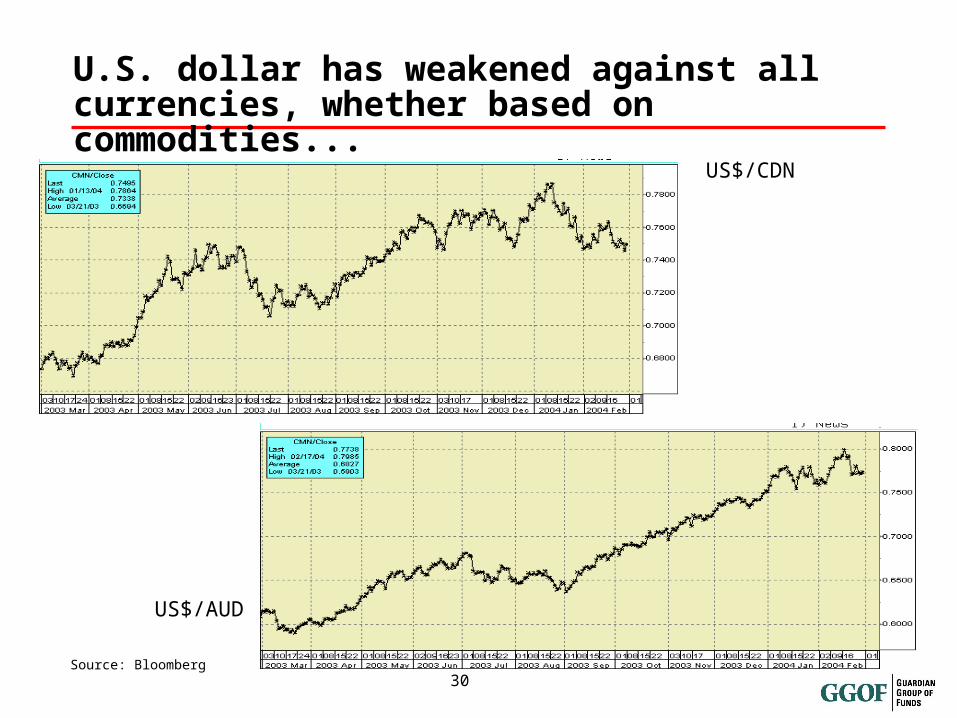

U.S. dollar has weakened against all currencies, whether based on commodities...

Source: Bloomberg

US$/AUD

US$/CDN

31

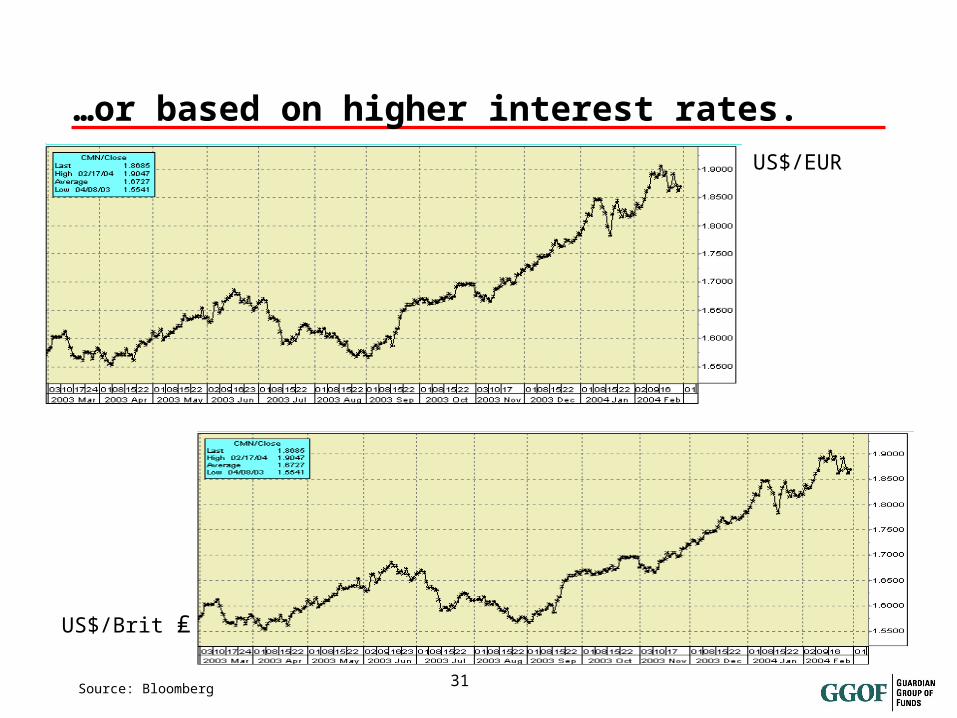

…or based on higher interest rates.

Source: Bloomberg

US$/EUR

US$/Brit ₤

32

CDN:USD

Source: Bloomberg

Over the long-term, this is the reasonfor foreign investing

U.S./Canada Exchange Rate

0.6

0.7

0.8

0.9

1

1.1

Dec-7

1

Dec-7

3

Dec-7

5

Dec-7

7

Dec-7

9

Dec-8

1

Dec-8

3

Dec-8

5

Dec-8

7

Dec-8

9

Dec-9

1

Dec-9

3

Dec-9

5

Dec-9

7

Dec-9

9

Dec-0

1

Dec-0

3

Year

$US

33

ASIA

The Case for Asia

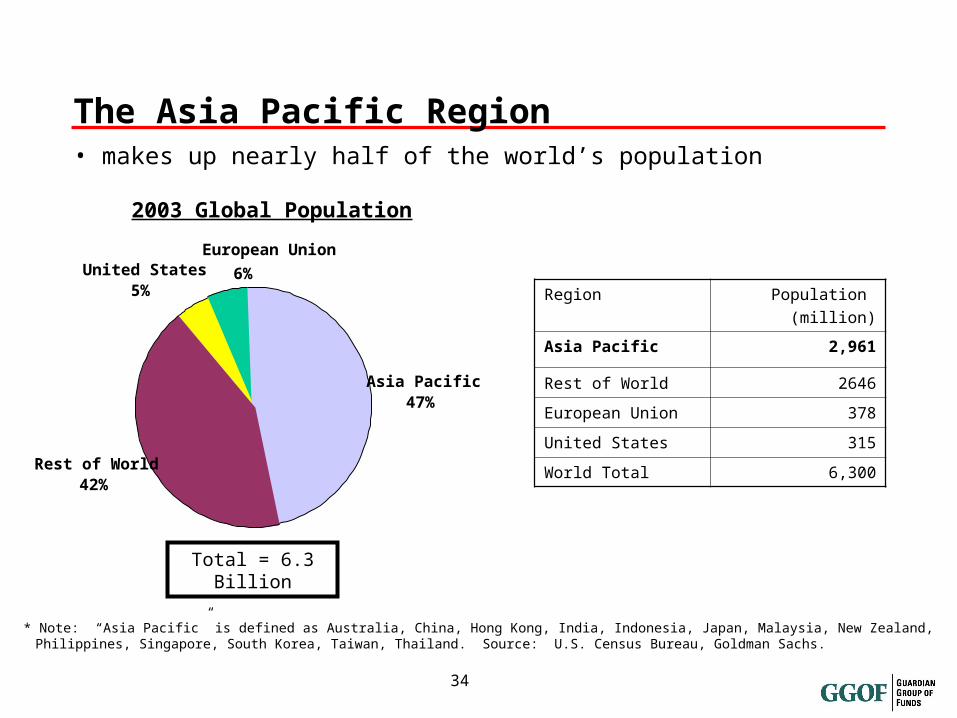

34

2003 Global Population

United States5%

Asia Pacific47%

Rest of World42%

European Union

6%

Total = 6.3 Billion

* Note: “Asia Pacific” is defined as Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand. Source: U.S. Census Bureau, Goldman Sachs.

• makes up nearly half of the world’s population

Region Population

(million)

Asia Pacific 2,961

Rest of World 2646

European Union 378

United States 315

World Total 6,300

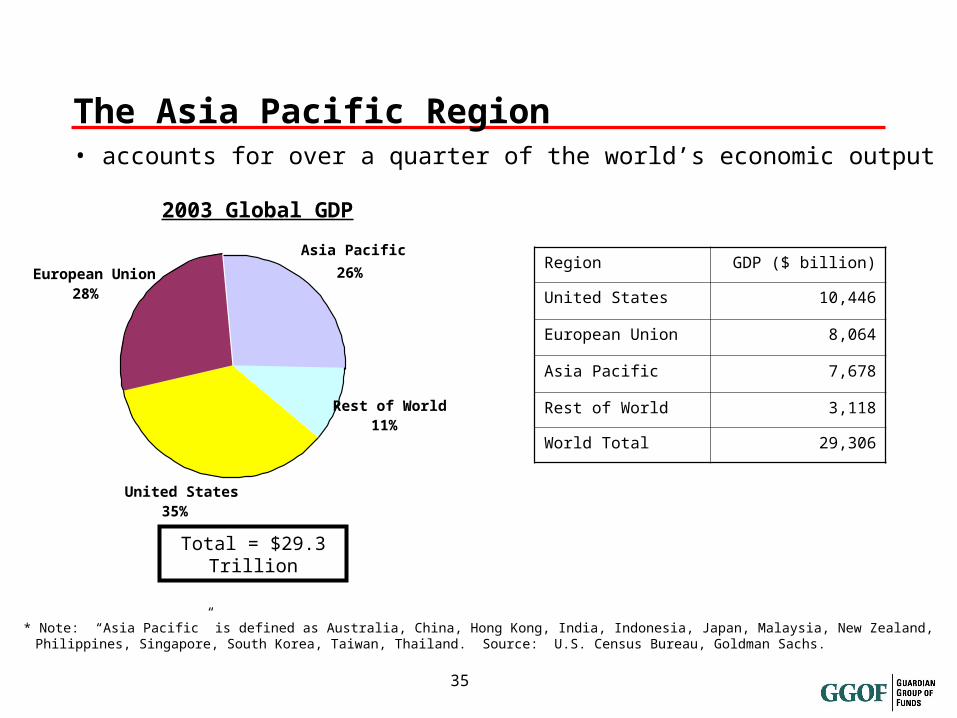

The Asia Pacific Region

35

2003 Global GDP

United States35%

European Union28%

Asia Pacific

26%

Rest of World11%

Total = $29.3 Trillion

* Note: “Asia Pacific” is defined as Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand. Source: U.S. Census Bureau, Goldman Sachs.

• accounts for over a quarter of the world’s economic output

Region GDP ($ billion)

United States 10,446

European Union 8,064

Asia Pacific 7,678

Rest of World 3,118

World Total 29,306

The Asia Pacific Region

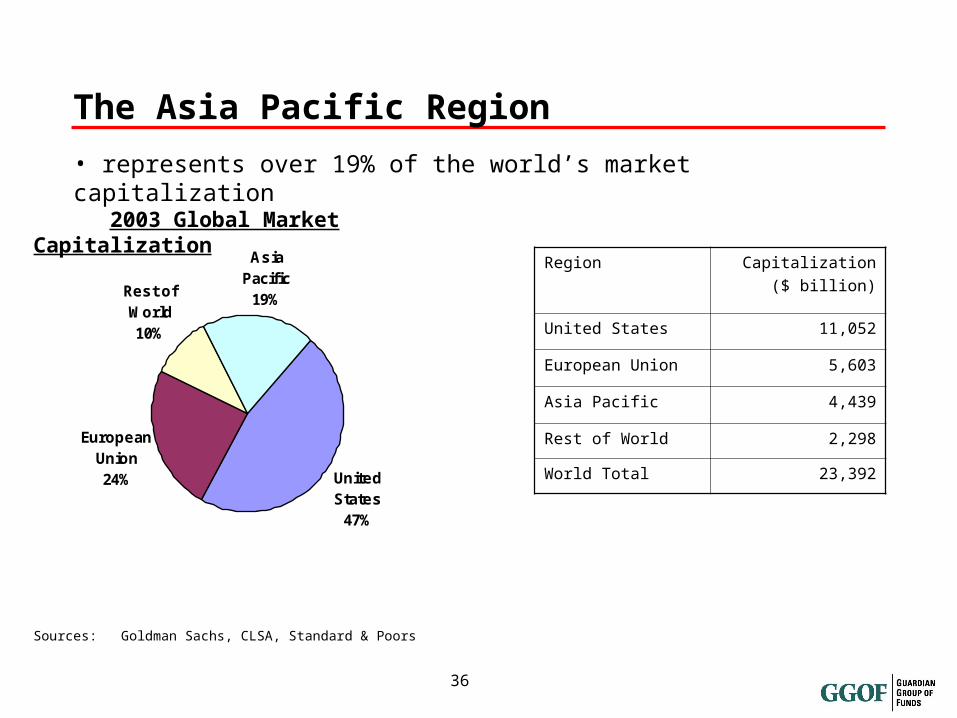

36

Sources: Goldman Sachs, CLSA, Standard & Poors

• represents over 19% of the world’s market capitalization

Region Capitalization

($ billion)

United States 11,052

European Union 5,603

Asia Pacific 4,439

Rest of World 2,298

World Total 23,392United States

47%

European Union24%

Rest of World10%

Asia Pacific

19%

2003 Global Market Capitalization

The Asia Pacific Region

37

0

1

2

3

4

5

6

7

8

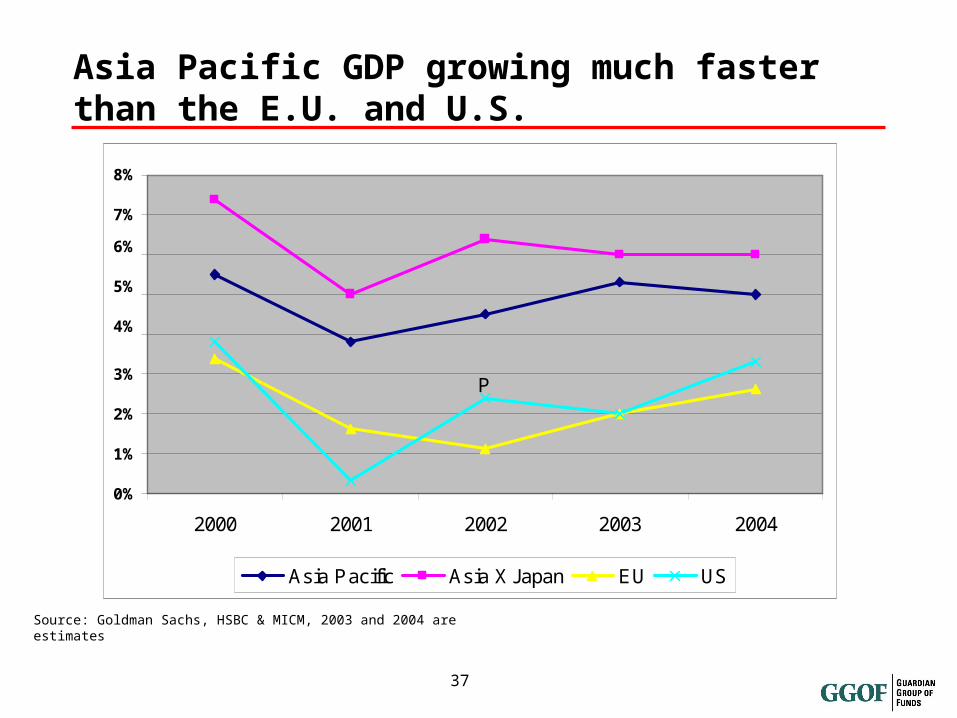

2000 2001 2002 2003 2004

Asia Pacific Asia X Japan EU US

P

Asia Pacific GDP growing much faster than the E.U. and U.S.

Source: Goldman Sachs, HSBC & MICM, 2003 and 2004 are estimates

8%

6%

5%

4%

3%

2%

1%

0%

7%

38

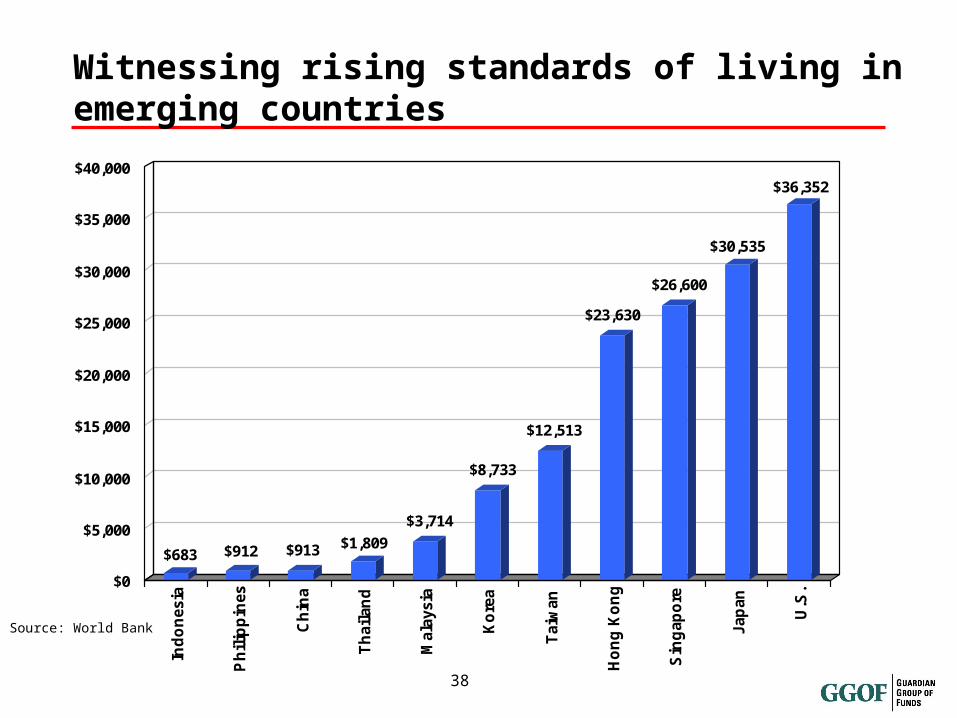

$683 $912 $913 $1,809

$3,714

$8,733

$12,513

$23,630

$26,600

$30,535

$36,352

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000In

do

nesia

Ph

ilip

pin

es

Ch

ina

Th

ail

an

d

Mala

ysia

Ko

rea

Taiw

an

Ho

ng

Ko

ng

Sin

gap

ore

Jap

an

U.S

.

Witnessing rising standards of living in emerging countries

Source: World Bank

39

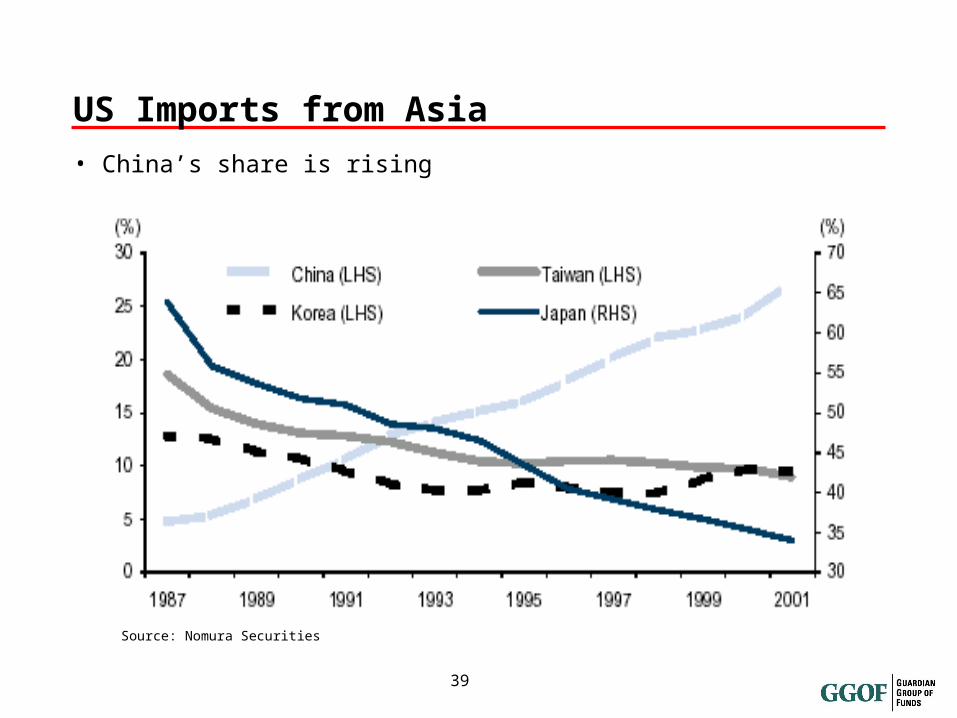

US Imports from Asia

Source: Nomura Securities

• China’s share is rising

40

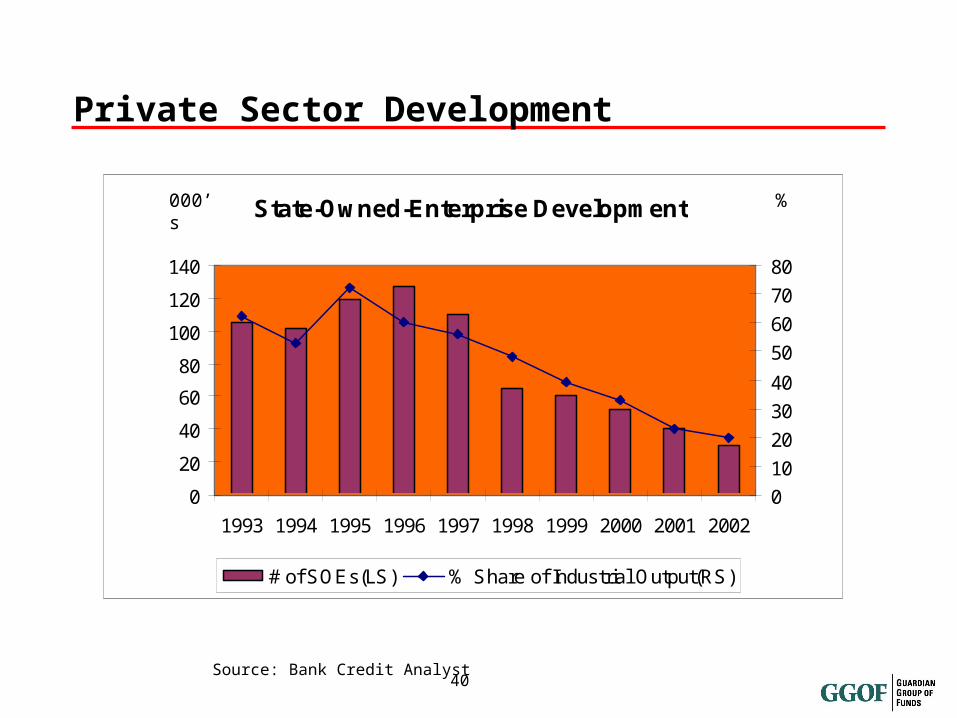

Private Sector Development

Source: Bank Credit Analyst

State-Owned-Enterprise Development

0

20

40

60

80

100

120

140

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

0

10

20

30

40

50

60

70

80

# of SOEs(LS) % Share of Industrial Output(RS)

000’s %

41

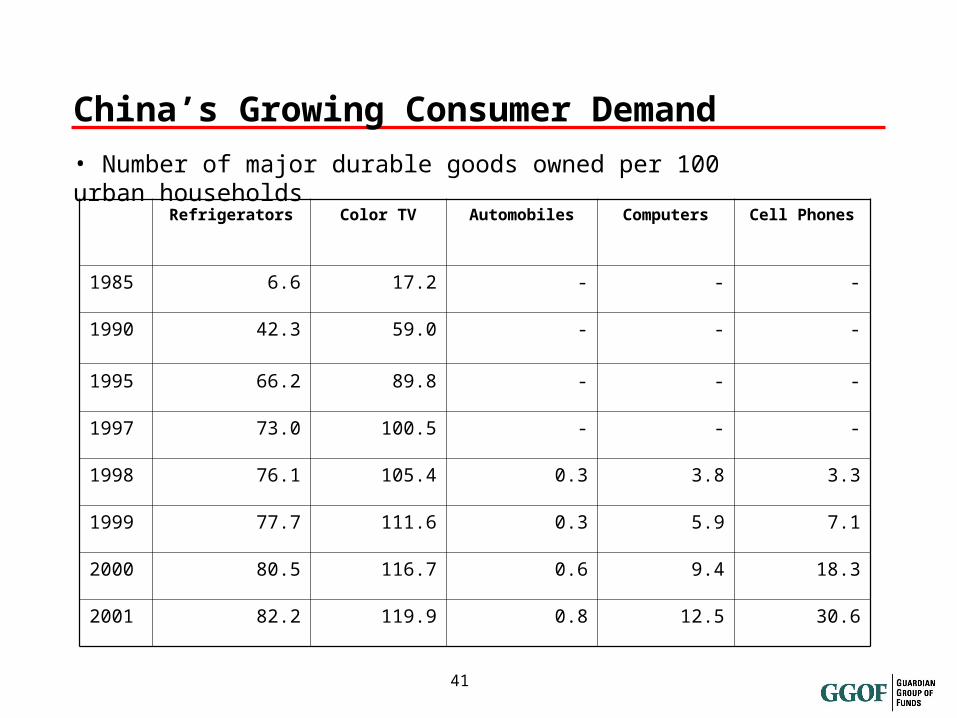

China’s Growing Consumer Demand

Refrigerators Color TV Automobiles Computers Cell Phones

1985 6.6 17.2 - - -

1990 42.3 59.0 - - -

1995 66.2 89.8 - - -

1997 73.0 100.5 - - -

1998 76.1 105.4 0.3 3.8 3.3

1999 77.7 111.6 0.3 5.9 7.1

2000 80.5 116.7 0.6 9.4 18.3

2001 82.2 119.9 0.8 12.5 30.6

• Number of major durable goods owned per 100 urban households

42

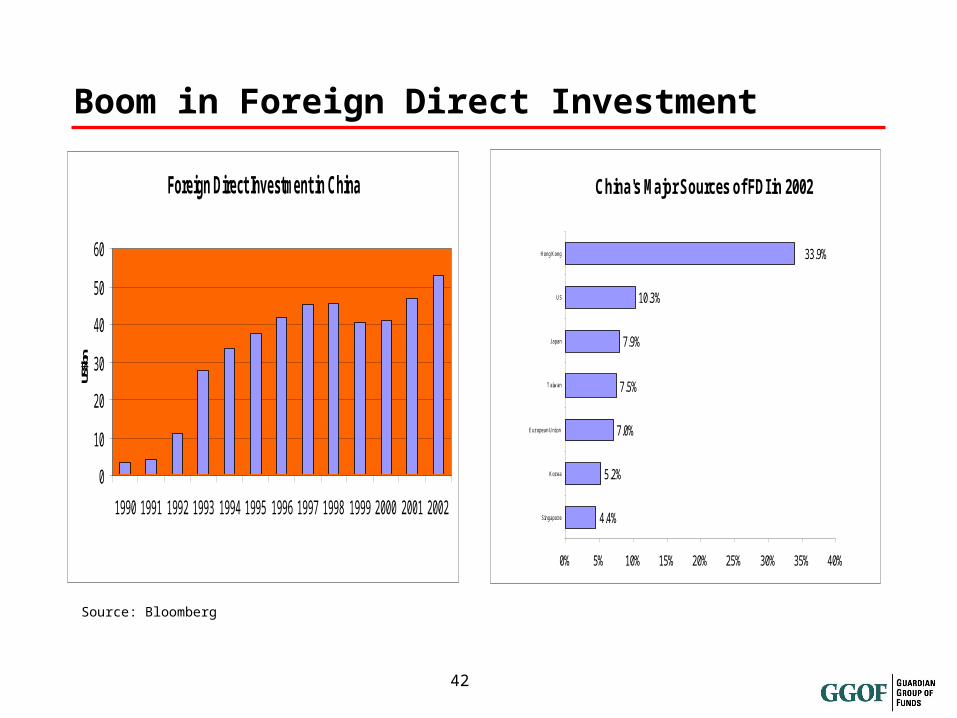

Boom in Foreign Direct Investment

Foreign Direct Investment in China

0

10

20

30

40

50

60

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

US$ b

n

Source: Bloomberg

China's Major Sources of FDI in 2002

5.2%

7.0%

7.5%

7.9%

10.3%

4.4%

33.9%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Singapor e

Kor ea

E ur opean Union

T aiwan

J apan

US

Hong Kong

43

GGOF Asian Growth and Income Fund

• Diversified exposure to Asian Tiger countries – China, Hong Kong, Thailand, Malaysia, Taiwan, Singapore, Indonesia, the Philippines and South Korea.

• Portfolio is concentrated among these countries, which have a combined population of 2.9 billion.

• Portfolio of 40 to 75 dividend-paying stocks and U.S. dollar-denominated convertible bonds

• Primary goal is to provide investors with capital growth and moderate income

44

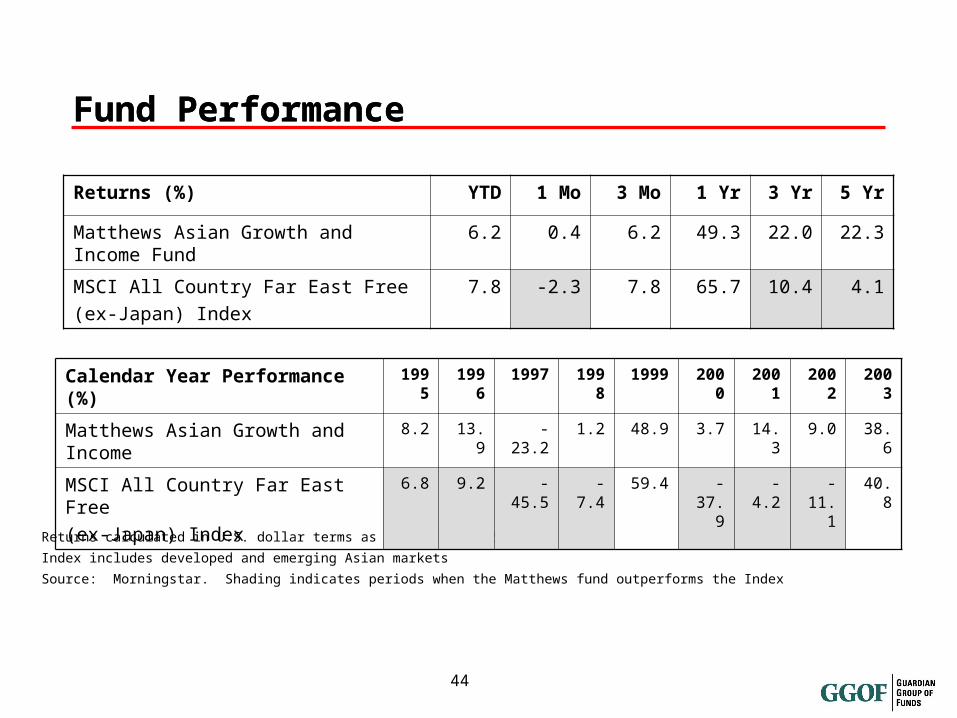

Fund PerformanceFund Performance

Returns calculated in U.S. dollar terms as of March 31, 2004

Index includes developed and emerging Asian markets

Source: Morningstar. Shading indicates periods when the Matthews fund outperforms the Index

Returns (%) YTD 1 Mo 3 Mo 1 Yr 3 Yr 5 Yr

Matthews Asian Growth and Income Fund 6.2 0.4 6.2 49.3 22.0 22.3

MSCI All Country Far East Free

(ex-Japan) Index

7.8 -2.3 7.8 65.7 10.4 4.1

Calendar Year Performance (%) 1995 1996 1997 1998 1999 2000 2001 2002 2003

Matthews Asian Growth and Income 8.2 13.9 -23.2 1.2 48.9 3.7 14.3 9.0 38.6

MSCI All Country Far East Free

(ex-Japan) Index

6.8 9.2 -45.5 -7.4 59.4 -37.9 -4.2 -11.1 40.8

45

Conclusion

• Single digit returns for most Canadian asset classes over the next 12 – 24 months

• Current income a much larger portion of total return.

• High yield bonds and more trusts good compliment to equities and government bonds (low correlation)

• The investment for Asia remains very positive.

46

Sales commissions, service fees, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return include changes in unit value and assume reinvestment of all distributions, and do not take into account sales, redemption or optional charges or income taxes payable by any securityholders, which would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Disclaimer