Embed Size (px)

Citation preview

Gilles BogaertManaging Director, Finance

Pierre PringuetChief Executive Offi cer

Dear colleagues,

Performance management has always been a key element in Pernod Ricard’s culture, decentralized business model and way of working. It has allowed to deliver consistently strong results over time, with a good level of predictability.

That said, it has been mainly focused on profi t. We need to enlarge our P&L culture to a true cash and value creation culture, among the whole group, beyond the fi nance function. Clearly, the best way to generate cash is to grow the top line and then the bottom line. But there are many other parameters that also have to be monitored.

Cash generation is the main criteria used by investors for the valuation of our company. It is also required to reduce the debt (still at a high level), ease our refi nancing needs and generate the headroom to allow investments and, in the future, potential acquisitions.

We are clearly not starting from scratch. But there is signifi cant room for improvement in cash forecasts accuracy, in cash performance monitoring and, above all, in the activation of the cash levers at all levels and in all areas of the organization.

As a consequence, cash management has been one of the key projects among the Agility global initiative. one of the deliverables is the cash toolkit, a good practices handbook (prepared by people from all areas) that will allow all functions to better understand cash generation cycles and drivers to boost our performance.

A cash toolkit by function has been sent to all CEos with a guideline to cascade it down to the respective functional departments.

As CFos, you will play a key role to drive these initiatives in your respective businesses, educate people on cash and make sure the cash toolkit is actually used by all departments. You will benefi t from the support of the International Treasury Department.

We are now at the end of the second phase of Agility 2, delivering the tools to you to raise our game in our approach to cash generation. The key to success is now to ensure a closer link to the business and your active involvement in pursuing the implementation of the recommendations and good practices you will fi nd in the cash toolkit.

Best wishes

Edito

Pernod Ricard / Cash Management / 1

Why ?The Cash Toolkit was created to meet two key objectives:

• improve commitment to cash generation across pernod ricard and make cash a subject shared and understood by all company functions,

• activate cash optimization levers and monitor improvements with relevant kpis.

What ? The Cash Toolkit is a cross-functional good practices handbook that links each company function with related cycles that have a direct impact on cash generation. It includes a checklist of operating levers that can be activated to stimulate cash generation, as well as relevant KPIs to monitor changes over time.In order to facilitate the use of the Cash Toolkit, two versions have been prepared, including the same good practices, but presented differently.

• The Cash Toolkit by function => sub-booklets “Purchasing / Marketing”, “Sales”, “Supply Chain" and “Finance” to be distributed separately to the corresponding departments.

• The Cash Toolkit by process cycle => full Cash Toolkit presenting the entire process cycles perspective "Purchase to Pay", "order to Cash", "Forecast to Fulfill" and "Treasury operations".

Cash Toolkitby function

Cash Toolkitby process cycle

(for CFOs)

Pernod Ricard / Cash Management / 2

CashToolKitCash Management

Fin

an

CE

April 2011

EX

EC

uT

ivE

su

mm

ar

y

CashToolKitCash Management

April 2011

su

pp

ly C

ha

in

CashToolKitCash Management

April 2011

sa

lE

s

CashToolKitCash Management

April 2011

April 2011

pu

rC

ha

sin

g /

ma

rk

ET

ing

CashToolKitCash Management

CashToolKitCash Management

April 2011

Pernod Ricard / Cash optimization / 4

ExEcutivE summarythE cash ToolkiT

in three keys questions

Pernod Ricard / Cash Management / 3

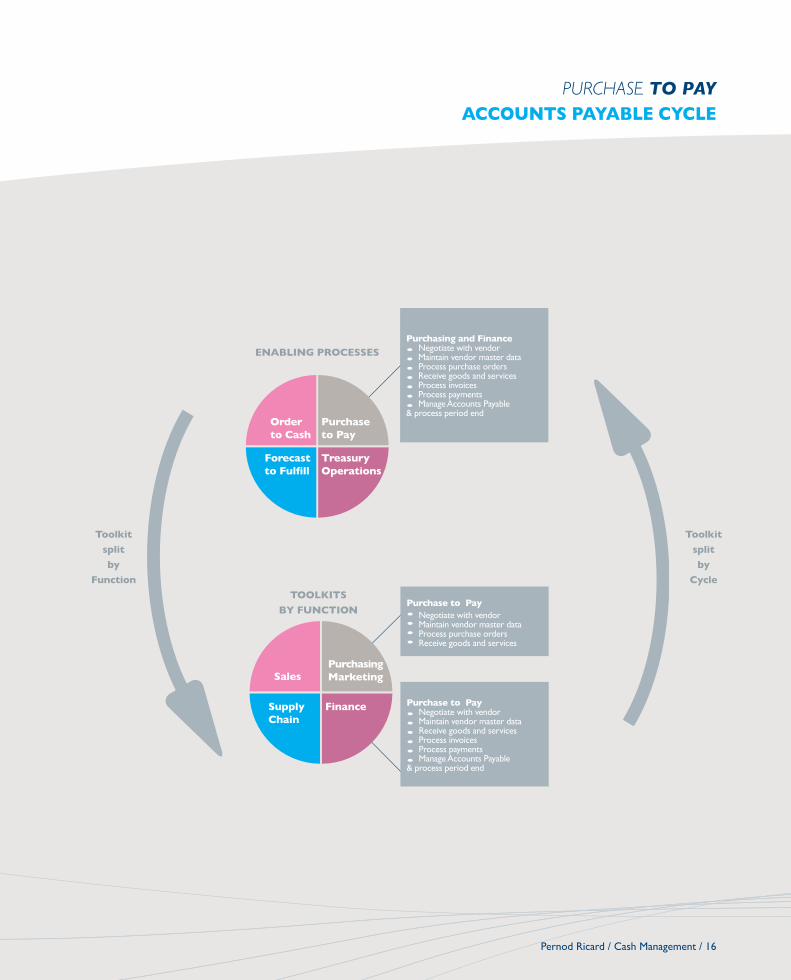

Who ?Cash Toolkit by function

CEos of all Pernod Ricard affiliates receive a Cash Toolkit by function and are responsible for its deployment to the relevant departments: the CEo is the sponsor of this project within the affiliate. Practically, the CEo cascades the appropriate section of the Cash Toolkit to his Management Committee. Each Management Committee member is then expected to push down the document into his team, enabling the good practices to be spread and become part of the normal way of working.

The Cash Toolkit by process cycle

CFos of all Pernod Ricard affiliates receive a Cash Toolkit by process cycle and are responsible for ensuring that the relevant operating levers are properly activated across the different departments. The CFo coordinates the implementation of local initiatives, assists and supports the other departments: the CFo is the driver of this project within the affiliate.

Pernod Ricard / Cash Management / 4

how ?The Cash Toolkit is structured according to two different perspectives:

The process view (e.g. “Purchase to Pay”, “order to Cash”, “Forecast to Fulfill”, “Treasury operations”) to show how the different company functions should work together to achieve high level targets.

Cash Toolkit process cycle structure

Detailed good practices

Pernod Ricard / Cash Management / 23PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYDiversify supplier relationship

based on risk and impact

oBJECTivEs

• Increase profits and cash flow for non critical items

• Diversify supply risk

kEy pErFormanCE inDiCaTors OR aNaLYsis

Definition: The quadrants of the kraljic matrix can be described as follows

• Non-critical items: small quantity baseline, wide supplier range

• Leverage items: small quantity baseline, many suppliers, big order quantity / volume

• Bottleneck items: multiple suppliers, critical for value chain / production

• Strategic items: few suppliers, own business depends on them

gooD praCTiCEs

Classify supplier relationship ◗ analyze your relationship with each of your suppliers and classify this relationship in terms of impact on profit and supply risk ◗ Give each supplier a classification and fill in the purchase portfolio matrix (Kraljic Matrix) ◗ implement and monitor the portfolio matrix

Take appropriate action with regards to each quadrant ◗ Non-critical items: optimize the processing of purchasing and exploit the competition between your suppliers ◗ Leverage item: use your purchasing power and competition to optimize purchase terms ◗ Bottleneck items: define and manage safety stock level, manage proper delivery frequency, identify suppliers for item substitution ◗ Strategic items: optimize the relationship with those suppliers and consider strategic partnerships as well as back-up

solutions to ensure availability of critical items

non-critical items

Effi cient processing

Bottleneck items

Volume assurance

leverage items

Exploitation of purchasing power

strategic items

Diversify, balance or exploit

Impa

ct o

n pr

ofi t

Supply risk

Purchase portfolio matrix (Kraljix Matrix)

Pernod Ricard / Cash Management / 22PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYperform a/B/C purchases

category optimization

oBJECTivEs

• Assess cash opportunities to partner efficiently with your purchasing team (tariffs, rebates, payment terms, etc.)

• Standardize payment terms to optimize working capital

• Streamline suppliers portfolio

kEy pErFormanCE inDiCaTors OR aNaLYsis

kpi: a/B/C analysis example

• Weight of the top 350 vs. low 1,500 suppliers in 8mFY10 (total suppliers: 2,912)

Definition: The a/B/C categories are defined as follows A: 80% purchases from 20% of all suppliersB: 15% from 30% C: 5% from 50%

gooD praCTiCEs

Ensuring efficiency of supplier base ◗ Perform a/B/c purchases analysis to determine potential optimization of the supplier / purchases base

(see KPi box for further explanation) ◗ Ensure that your purchasing team is involved in order to

• provide expertise in the sourcing and procurement processes for category a and B• negotiate proper payment terms

◗ assess the opportunity to streamline the category c supplier portfolio ◗ Ensure that budget holders apply to standard terms for all category c suppliers

top 350 suppliersRemaining supplierssmallest 1,500 suppliers

9%

1%

90%

16%

29%

55%Top 350 suppliersRemaining suppliersSmallest 1,500 suppliers

Weight of the top 350 vs. Low 1,500 suppliers in 8mFY10 (total suppliers: 2,912)

Share of the €79.9m purchase Share of 15,972 invoices received

Share of the €79.9m purchasesin value

Share of 15,972 invoices receivedin number of invoices

Pernod Ricard / Cash Management / 21PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYregister and control contractual

terms in vendor master data

oBJECTivEs • Ensure that suppliers contractual terms recorded in ERP system are updated to reflect the real contractual payment terms

• optimize cash flow forecast

• Reduce risk of automatic early payment or cash payment

• Align payment date versus due date

• Reduce cost of payment processing by higher standardization

kEy pErFormanCE inDiCaTors OR aNaLYsis

• Number and share of supplier master data with an incomplete set of contract terms

• structure of contractual payment terms (see example chart):

• % of payment terms structure < 30 days in ERP or procurement tool

gooD praCTiCEs

use one single supplier database ◗create one single supplier database and one account set up per vendor ◗Define a procedure to create and to update master data related to the vendor: contact details, payment terms, etc. ◗consider using a workflow when creating or updating vendor master data involving relevant departments (i.e. finance, legal, marketing) ◗ Establish Electronic Data interchange (EDi) with major suppliers wherever possible with access to suppliers’ product references and tariffs ◗create a vendor portal for vendor to access own account

Ensuring all payment terms are set in your system ◗ Once a year, run a report to determine that all payment terms are set in your system and perform test to ensure that they

are in line with actual contractual terms and conditions negotiated with suppliers ◗ On a yearly basis the contracts terms registered in the vendor master should be reviewed and different payment terms

compared to standard payment terms should received and approval from the purchasing and financial department ◗ Proper categorization of supplier type (e.g., cash vs. negotiated.)

Cash payment exposure ◗ at the beginning of each semester, run a report focused on suppliers with “cash” contractual terms and perform test to

avoid cash payments by default whereas delay of payment where negotiated with suppliers

Nb of invoices 8mFY10

Nb of invoices FY09

Cumulated value 8mFY10

Cumulated value FY09

NB

of in

voic

es

€ in

mill

ions

Others EOM

45 days EOM

60 days 60 days

10th EOM on 31 days

EOM 30 days

net net 30 days Cash

8000 7000 6000 5000 4000 3000 2000 1000

0

60

50

40

30

20

10

0

cumulated value FY09 cumulated value 8mFY10Nb of invoices FY09 Nb of invoices 8mFY10

overview of purchase invoices by contractual term

of payment over FY09 and 8mFY10

EnaBling proCEssEs anD sysTEms

• Negotiate with vendor

• Maintain vendor master data

• Process purchase orders

• Receive goods and services

• Process invoices

• Process payments

• Manage AP & process period end

• Negotiate with customers orders

• Manage credit

• Maintain customer master data

• Process orders

• Process invoices

• Process receipts

• Manage collection & disputes

• Manage AR & process period end

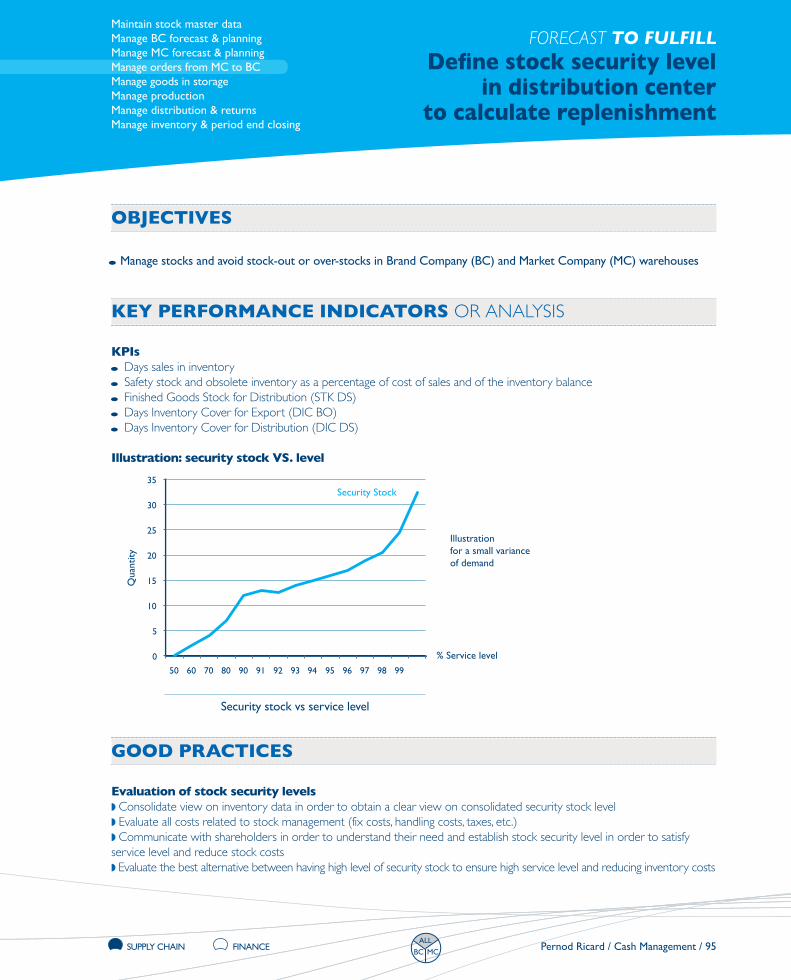

• Maintain stock master data

• Manage Brand Company forecast & planning

• Manage Market Company forecast & planning

• Manage orders from Market Companies to Brand Companies

• Manage goods in storage

• Manage production

• Manage distribution & returns

• Manage inventory & period end closing

orderto Cash

Treasuryoperations

purchaseto pay

Forecast to Fulfill

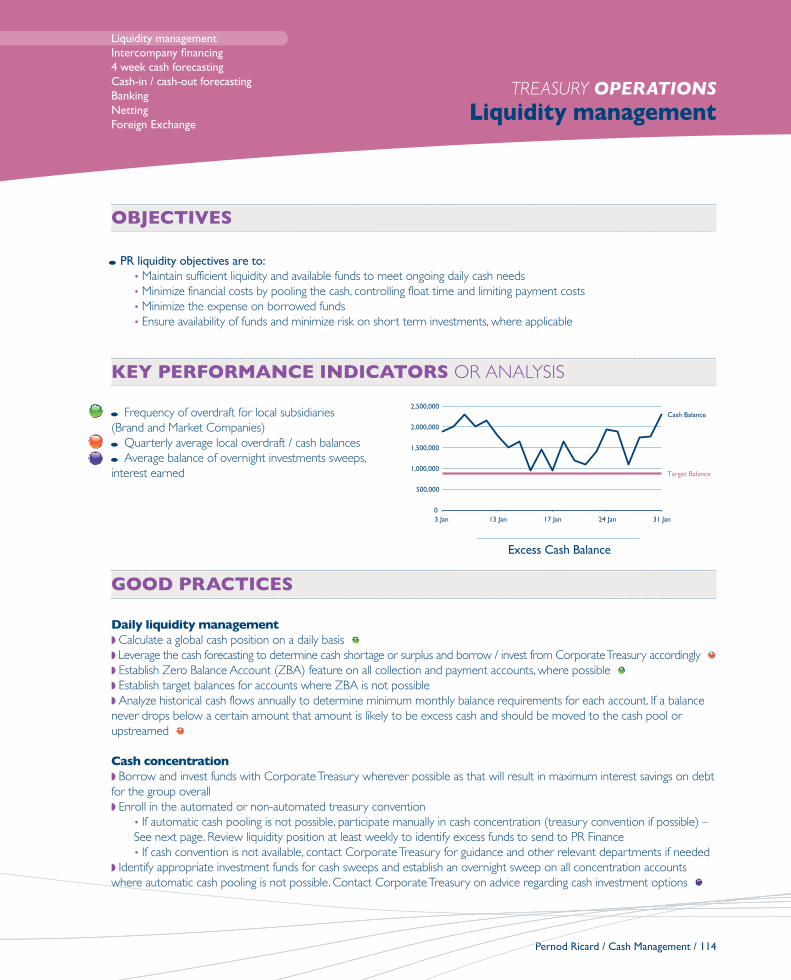

• Liquidity management

• Intercompany financing

• 4 week cash forecasting

• Cash-in / Cash-out forecasting

• Banking

• Netting

• Foreign Exchange

Pernod Ricard / Cash Management / 5

process cycle

Pernod Ricard / Cash Management / 17Pernod Ricard / Cash Management / 17

PURCHASE To pay

Table of contents

• PURCHASING • FINANCE • MARKETING

negotiate with vendor

• Consider the scope of the purchasing function, and relevant rules and procedures (e.g. bidding, contracts, etc.)

• use standardized payment terms and align multiple payment terms from a single supplier

• optimize payments cycle by negotiating longer payment terms or early payment discounts based on business needs

maintain vendor master data

• register and control contractual terms in vendor master data

• perform a/B/C purchases category optimization

• Diversify supplier relationship based on risk and impact

process purchase orders

• ask the supplier to indicate the purchase order number as well as a breakdown of services on the invoice

• manage a maximum number of purchases orders in procurement tool or Enterprise resource planning (Erp)

• automate purchase order processing and use enabling technologies

receive goods and services

• integration between procurement tool and accounting system

• only accept goods / services receipt corresponding to an outstanding purchase order

process invoices

• manage a single entry point for invoices

• Ensure supply has corresponding purchase order to match the invoice

• Consider more effective billing mechanisms

process payments

• plan periodic payment campaigns (use a payment schedule) to optimize Days payable outstanding (Dpo)

• implement controls to prevent early payments

• integrate accounts payable system with banking system

manage a/p & process period end

• perform inventory and valuation of claims for provisions

• perform an annual review of actual payment terms versus contract payment terms

• monitor accounts payable (a/p) ageing balance

• Compare actual with target Dpo

good practices for marketing

• negotiate with vendors and formalize of the business relationship

• implement follow-up and monitor procedures regarding budget versus actual spend

••

•

•

•••

••

process step

responsible company function(recipient of the good practice)

list of good practices per process step

ExEcutivE summarythE cash ToolkiT

how is it structured?

The company function view (e.g. “Purchasing/Marketing”, “Sales”, “Supply Chain”, “Finance”) to emphasize whose is the responsibility for the management of the Good Practice. Each department receives only the related section of Cash Toolkit.

Example of a table of contents for one process cycle

Pernod Ricard / Cash Management / 6

thE cash ToolkiThow is a good practice presented?

Each page presents one good practice and provides (1) information on the objectives, (2) a detailed description of activities to be performed when implementing, (3) corresponding Key Performance Indicators (KPIs) to assess the impact over the time.

Example of a good practice

Pernod Ricard / Cash Management / 18PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

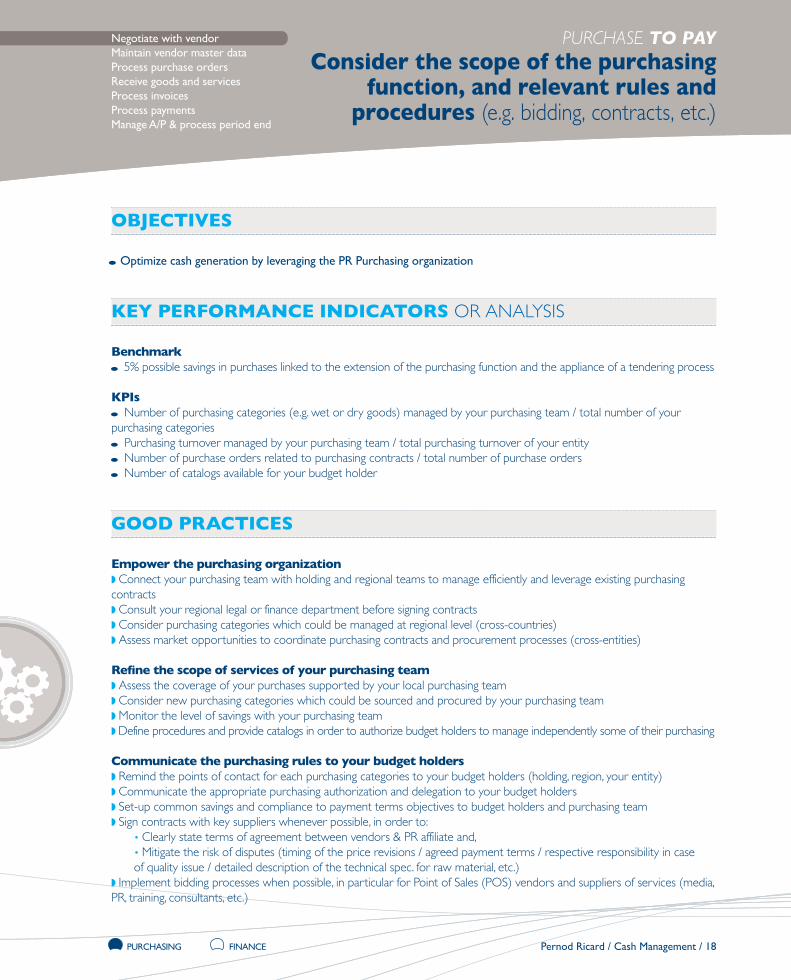

PURCHASE TO PAYConsider the scope of the purchasing

function, and relevant rules and procedures (e.g. bidding, contracts, etc.)

oBJECTivEs

• optimize cash generation by leveraging the PR Purchasing organization

kEy pErFormanCE inDiCaTors OR aNaLYsis

Benchmark

• 5% possible savings in purchases linked to the extension of the purchasing function and the appliance of a tendering process

kpis

• Number of purchasing categories (e.g. wet or dry goods) managed by your purchasing team / total number of your purchasing categories

• Purchasing turnover managed by your purchasing team / total purchasing turnover of your entity

• Number of purchase orders related to purchasing contracts / total number of purchase orders

• Number of catalogs available for your budget holder

gooD praCTiCEs

Empower the purchasing organization ◗ connect your purchasing team with holding and regional teams to manage efficiently and leverage existing purchasing

contracts ◗ consult your regional legal or finance department before signing contracts ◗ consider purchasing categories which could be managed at regional level (cross-countries) ◗ assess market opportunities to coordinate purchasing contracts and procurement processes (cross-entities)

refine the scope of services of your purchasing team ◗ assess the coverage of your purchases supported by your local purchasing team ◗ consider new purchasing categories which could be sourced and procured by your purchasing team ◗ Monitor the level of savings with your purchasing team ◗ Define procedures and provide catalogs in order to authorize budget holders to manage independently some of their purchasing

Communicate the purchasing rules to your budget holders ◗ Remind the points of contact for each purchasing categories to your budget holders (holding, region, your entity) ◗ communicate the appropriate purchasing authorization and delegation to your budget holders ◗ set-up common savings and compliance to payment terms objectives to budget holders and purchasing team ◗ sign contracts with key suppliers whenever possible, in order to:

• clearly state terms of agreement between vendors & PR affiliate and,• Mitigate the risk of disputes (timing of the price revisions / agreed payment terms / respective responsibility in case of quality issue / detailed description of the technical spec. for raw material, etc.)

◗ implement bidding processes when possible, in particular for Point of sales (POs) vendors and suppliers of services (media, PR, training, consultants, etc.)

good practice

objectives of the particular good practice

recommended list of kpis

Detailed activitiesto be performed

process step of each good practice is highlighted

responsible Company Function(recipient of the good practice)

Chivas

The purpose of the Executive Summary is to provide CEos and CFo a simplified checklist of the key good practices to be implemented for every process cycle, as well as a suggestion of the main Key Performance Indicators (KPIs).

We recommend that CEos, CFos and other involved departments periodically review the implementation status of the good practices and monitor the KPIs.

Implementation of the relevant good practices contributes to optimization of the affiliate cash generation, and therefore to a continuous improvement in the group Net Debt / EBITDA ratio.

Working CapiTal lEvErs

DrivE opTimal Cash ConvErsion CyClE

Procurement of services, and the payment of those services (The Accounts Payable Cycle)

Functions:• Purchasing

• Marketing

• Budget holders in other departments

• Finance

Sales cycle, from the development of customer relationships to the receipt of cash (The Accounts Receivable Cycle)

ordering raw materials and inventory to fulfill product demand, to the management, and reporting of inventory

orderto Cash

purchaseto pay

Forecast to Fulfill

Cash optimization and the best utilization of working capital that considers the impact of the cycles on Purchase to Pay, order to Cash, Forecast to Fulfill, plus a strong centralized treasury process that facilitates debt minimization

Functions:• account Management

• Field Management

• sales administration

• Finance

Functions:• Demand Planning

• Logistics

• industrial

• Finance

Functions:• Finance

ExEcutivE summaryoverview

Pernod Ricard / Cash Management / 8

Treasuryoperations

ExEcutivE summarypurchase to pay (accounts payable Cycle)

• optimize payments cycle to maximize your business liquidity: - Negotiate longer payment terms or early payment discounts based on business needs - Plan periodic payment campaigns (use a payment schedule)

• Maintain vendor master data by ensuring that contractual terms are current

• Ensure that all invoices have one single point of entry

• Monitor accounts payable (A/P) ageing balance

• Compare actual with target Days Payable out-standing (DPo)

• Consider the scope of the purchasing function and its impact on working capital needs

• Manage a maximum number of purchase orders in procurement tool or Enterprise Resource Planning (ERP)

DirECT Cash impaCT inDirECT Cash impaCT

+180 days90-180 days0-90 daysnot impaired and not due

Payable vs. DPO

DPO Non group FY 10/11

DPO Non group FY 09/10

Trade payables Non group FY 10/11

Trade payables Non group FY 09/10

EUR

mill

ion

Day

s

Aug Sep

Oct

Nov Dec

BUD D

ec Jan Feb

Mar Apr May Jun

LE Ju

nBU

D Jun

90

80

70

60

50

40

30

20

10

0

140

120

100

80

60

40

20

0

Payables vs. DPo

not impaired and not due

0-90 days

90-180 days

+180 days

'000

EU

R

BUD

FC

Jun

10

May

10

Apr

10

Mar

10

Feb

10

Jan

10

Dec

10

Nov

10

Oct

10

Sep

10

Aug

10

Jun

09

May

09

Apr

09

Mar

09

Feb

09

Jan

09

Dec

08

Nov

08

Oct

08

Sep

08

Aug

08

Jun

08

May

08

Apr

08

1000

900

800

700

600

500

400

300

200

100

0

Aged Accounts Payables

significant kpis

Pernod Ricard / Cash Management / 9

trade payables Non group FY 10/11 trade payables Non group FY 09/10 DPO Non group FY 09/10DPO Non group FY 10/11

ExEcutivE summaryorder to Cash (accounts receivable Cycle)

Pernod Ricard / Cash Management / 10

• optimize receipts cycle to maximize your business liquidity: - Standardize and renegotiate payment terms with customers - Consider factoring to manage cash vs. working capital

• Analyze aged accounts receivables

• Implement formal dispute resolution mechanism

• Compare actual versus target Receivables & Days Sales outstanding (DSo)

• Partner with (larger) customers to streamline ordering, receipt and payment process

• Set-up credit policies and define credit limits for all customers

• Create effective automated controls to prevent staff from overriding set credit limits

• Register customer master data in your sales & distribution tool or Enterprise Resource Planning (ERP)

• Manage 100% of orders in Sales Administration tool or ERP

DirECT Cash impaCT inDirECT Cash impaCT

significant kpis

+180 days90-180 days0-90 daysnot impaired and not due

Receivables vs. DSo

Aged Accounts Receivable

not impaired and not due

0-90 days

90-180 days

+180 days

'000

EU

R

BUD

FC

Jun

10

May

10

Apr

10

Mar

10

Feb

10

Jan

10

Dec

10

Nov

10

Oct

10

Sep

10

Aug

10

Jun

09

May

09

Apr

09

Mar

09

Feb

09

Jan

09

Dec

08

Nov

08

Oct

08

Sep

08

Aug

08

Jun

08

May

08

Apr

08

1000

900

800

700

600

500

400

300

200

100

0

Receivables vs. DSO

DSO (before Factoring) Non group FY 10/11

DSO (before Factoring)Non group FY 09/10

Trade receivables (before Factoring)Non group FY 10/11

Trade receivables (before Factoring)Non group FY 09/10

EUR

mill

ion

Day

s

Aug Sep

Oct

Nov Dec

BUD D

ec Jan Feb

Mar Apr May Jun

LE Ju

nBU

D Jun

50

40

45

35

30

25

20

15

10

5

0

30

25

20

15

10

5

0

trade receivables (before Factoring) Non group FY 10/11trade receivables (before Factoring) Non group FY 09/10 DsO (before Factoring) Non group FY 09/10DsO (before Factoring) Non group FY 10/11

ExEcutivE summaryForecast to Fulfi ll (inventory management)

Pernod Ricard / Cash Management / 11

• Standardize and rationalize product portfolio

• Calculate seasonality influences

• Develop policies and procedures for goods storage and handling

• Perform regular physical inventory count and ensure the posting of inventory differences in your warehouse/inventory management and accounting

• Compare actual versus target Days Inventory on-hand (DIo)

• Calculate and monitor inventory carrying/ holding costs

• Maintain stock master data

• Design and deploy processes to manage stock and forecast for new products or end of life products

• Coordinate large promotion orders from retailer to Market Company (MC) and Brand Company (BC)

• Use an inventory tracking process

DirECT Cash impaCT inDirECT Cash impaCT

• Value of slow moving inventory including obso-lescence

• Evolution of number of Stock Keeping Units (SKUs)

other kpis

EUR

mill

ion

days

BUDLE

Oct

11

BUD D

ec 1

1

Sep

11

Aug 1

1

Jun 1

1

May

11

Apr 1

1

Mar

11

Feb

11

Jan 1

1

Dec 1

0

Nov

10

Oct

10

40

35

30

25

20

15

10

5

0

30

25

20

15

10

5

0

Inventory vs. DIO

Trade goods - non group

Trade goods - group

Finished goods

Other inventories

Non aged wet goods

Dry goods

significant kpi

Inventory vs. DIo

trade goods - non group trade goods - group Finished goodsOther inventoriesNon aged wet goodsDry goods

ExEcutivE summaryTreasury operations

Pernod Ricard / Cash Management / 12

• Concentrate cash with Corporate Treasury as soon as possible

• Calculate a global cash position on a daily basis

• Perform cash-in / cash-out forecasting

• Make every effort to join the netting system, and utilize it to offset all agreed intercompany balances each month

• No external borrowing facilities are to be established without approval from Corporate Treasury

• Bank only with the core financing banks for cash management purposes

• Entities should investigate how to integrate the group financing process (cash pool, treasury convention, etc.)

• Communicate immediately all non-functional currency invoices above €350k (outside of net-ting system) to Corporate Treasury front-office via e-Treasury

DirECT Cash impaCT inDirECT Cash impaCT

• Cash Forecast vs. Actual

• Foreign Exchange (FX) results on current op-erations

other kpis

significant kpi

Cash Position

cash - Non GroupGross Debt - Non GroupDebt/cash GroupNet Debt total

300

200

100

0

-100

-200

-300

-400

-500

-600

-700

Aug 08

Sep 0

8

Oct 08

Nov 08

Dec 08

Jan 09

Feb 0

9

Mar 09

Apr 09

Aug 09

Sep 0

9

Oct 09

Nov 09

Dec 09

Jan 10

Feb 1

0

Mar 10

Apr 10

May 09

Jun 09

Cash Position

Cash - Non GroupGross Debt - Non GroupDebt/Cash GroupNet Debt Total

ExEcutivE summarynotes

Pernod Ricard / Cash Management / 13

PURCHASE to PAYProcurement of services, and the payment of those services (The Accounts Payable Cycle)

Ricard

EnAbling ProcEssEs Purchasing and Finance• Negotiate with vendor• Maintain vendor master data• Process purchase orders• Receive goods and services• Process invoices• Process payments• Manage Accounts Payable & process period end

orderto cash

treasury operations

Purchaseto Pay

Forecast to Fulfill

toolkits

bY FunctionPurchase to Pay • Negotiate with vendor• Maintain vendor master data• Process purchase orders• Receive goods and services

sales

Financesupply chain

Purchase to Pay • Negotiate with vendor• Maintain vendor master data• Receive goods and services• Process invoices• Process payments• Manage Accounts Payable & process period end

toolkit

split

by

cycle

toolkit

split

by

Function

PURCHASE TO PAYAccounts PAYAblE cYclE

Pernod Ricard / Cash Management / 16

PurchasingMarketing

Pernod Ricard / Cash Management / 17Pernod Ricard / Cash Management / 17

PURCHASE to PAY

table of contents

• PURCHASING • FINANCE • MARKETING

negotiate with vendor

• consider the scope of the purchasing function, and relevant rules and procedures (e.g. bidding, contracts, etc.)

• use standardized payment terms and align multiple payment terms from a single supplier

• optimize payments cycle by negotiating longer payment terms or early payment discounts based on business needs

Maintain vendor master data

• register and control contractual terms in vendor master data

• Perform A/b/c purchases category optimization

• Diversify supplier relationship based on risk and impact

Process purchase orders

• Ask the supplier to indicate the purchase order number as well as a breakdown of services on the invoice

• Manage a maximum number of purchases orders in procurement tool or Enterprise resource Planning (ErP)

• Automate purchase order processing and use enabling technologies

receive goods and services

• integration between procurement tool and accounting system

• only accept goods / services receipt corresponding to an outstanding purchase order

Process invoices

• Manage a single entry point for invoices

• Ensure supply has corresponding purchase order to match the invoice

• consider more effective billing mechanisms

Process payments

• Plan periodic payment campaigns (use a payment schedule) to optimize Days Payable outstanding (DPo)

• implement controls to prevent early payments

• integrate accounts payable system with banking system

Manage A/P & process period end

• Perform inventory and valuation of claims for provisions

• Perform an annual review of actual payment terms versus contract payment terms

• Monitor accounts payable (A/P) ageing balance

• compare actual with target DPo

good Practices for Marketing

• negotiate with vendors and formalize of the business relationship

• implement follow-up and monitor procedures regarding budget versus actual spend

••

•

•

•••

••

Pernod Ricard / Cash Management / 18PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYconsider the scope of the purchasing

function, and relevant rules and procedures (e.g. bidding, contracts, etc.)

obJEctiVEs

• Optimize cash generation by leveraging the PR Purchasing organization

kEY PErForMAncE inDicAtors OR ANALYSIS

benchmark

• 5% possible savings in purchases linked to the extension of the purchasing function and the appliance of a tendering process

kPis

• Number of purchasing categories (e.g. wet or dry goods) managed by your purchasing team / total number of your purchasing categories

• Purchasing turnover managed by your purchasing team / total purchasing turnover of your entity

• Number of purchase orders related to purchasing contracts / total number of purchase orders

• Number of catalogs available for your budget holder

gooD PrActicEs

Empower the purchasing organization ◗ Connect your purchasing team with holding and regional teams to manage efficiently and leverage existing purchasing

contracts ◗ Consult your regional legal or finance department before signing contracts ◗ Consider purchasing categories which could be managed at regional level (cross-countries) ◗ Assess market opportunities to coordinate purchasing contracts and procurement processes (cross-entities)

refine the scope of services of your purchasing team ◗ Assess the coverage of your purchases supported by your local purchasing team ◗ Consider new purchasing categories which could be sourced and procured by your purchasing team ◗ Monitor the level of savings with your purchasing team ◗ Define procedures and provide catalogs in order to authorize budget holders to manage independently some of their purchasing

communicate the purchasing rules to your budget holders ◗ Remind the points of contact for each purchasing categories to your budget holders (holding, region, your entity) ◗ Communicate the appropriate purchasing authorization and delegation to your budget holders ◗ Set-up common savings and compliance to payment terms objectives to budget holders and purchasing team ◗ Sign contracts with key suppliers whenever possible, in order to:

• Clearly state terms of agreement between vendors & PR affiliate and,• Mitigate the risk of disputes (timing of the price revisions / agreed payment terms / respective responsibility in case of quality issue / detailed description of the technical spec. for raw material, etc.)

◗ Implement bidding processes when possible, in particular for Point of Sales (POS) vendors and suppliers of services (media, PR, training, consultants, etc.)

Pernod Ricard / Cash Management / 19PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYuse standardized payment terms and align multiple payment terms

from a single supplier

obJEctiVEs

• Monitor and align trade terms

• Optimize working capital and cash conversion

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number of payment terms (see example chart)

63%

16%

30 days net

Immediatelydue net

5%: 256 suppliers

15%: 96 suppliers

80% of volume34 suppliers

Target group forrenegotiation

• Number of payment terms per supplier and potential opportunities for improvement via negotiations

gooD PrActicEs

standardize and align payment terms ◗ Analyze at least once a year the number of payment terms per supplier and the reason for different payment terms ◗ Ensure that standard terms are stored centrally ◗ Determine the potential working capital improvement ◗ Define and communicate standard terms of payment ◗ Renegotiate the payment terms starting with suppliers promising the biggest improvement potential and negotiate towards

the favorable payment term ◗ Purchasing and accounting systems apply to standard terms

Pernod Ricard / Cash Management / 20PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYoptimize payments cycle by negotiating longer payment terms or early payment

discounts based on business needs

obJEctiVEs

• Optimize payments cycle

• Improve payment terms

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number and purchase volume of suppliers with whom longer payment terms by paying a premium makes sense (see example chart)

gooD PrActicEs

consider the payment terms before ordering and include finance in the discussions

consider negotiation of longer payment terms by paying a premium or early payment with a respective discount, based on the optimal terms for your business ◗ Identify suppliers with whom longer payment terms (by paying a premium) or early payment discounts can be negotiated ◗ Select items for which a premium could be paid to obtain longer payment terms ◗ Assess / consider the trade-off regarding Earnings Before Interest and Taxes (EBIT) vs. the cost of working capital ◗ Negotiate longer payment terms or early payment with selected vendors

Opportunity in [Currency]sOpportunity in [Currency]

Val

ue

Supp

lier

5

Supp

lier

4

Supp

lier

3

Supp

lier

2

Supp

lier

1

20000

15000

10000

5000

0

Pernod Ricard / Cash Management / 21PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYregister and control contractual

terms in vendor master data

obJEctiVEs • Ensure that suppliers contractual terms recorded in ERP system are updated to reflect the real contractual payment terms

• Optimize cash flow forecast

• Reduce risk of automatic early payment or cash payment

• Align payment date versus due date

• Reduce cost of payment processing by higher standardization

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number and share of supplier master data with an incomplete set of contract terms

• Structure of contractual payment terms (see example chart):

• % of payment terms structure < 30 days in ERP or procurement tool

gooD PrActicEs

use one single supplier database ◗Create one single supplier database and one account set up per vendor ◗Define a procedure to create and to update master data related to the vendor: contact details, payment terms, etc. ◗Consider using a workflow when creating or updating vendor master data involving relevant departments (i.e. finance, legal, marketing) ◗ Establish Electronic Data Interchange (EDI) with major suppliers wherever possible with access to suppliers’ product references and tariffs ◗Create a vendor portal for vendor to access own account

Ensuring all payment terms are set in your system ◗ Once a year, run a report to determine that all payment terms are set in your system and perform test to ensure that they

are in line with actual contractual terms and conditions negotiated with suppliers ◗ On a yearly basis the contracts terms registered in the vendor master should be reviewed and different payment terms

compared to standard payment terms should received and approval from the purchasing and financial department ◗ Proper categorization of supplier type (e.g., cash vs. negotiated.)

cash payment exposure ◗ At the beginning of each semester, run a report focused on suppliers with “cash” contractual terms and perform test to

avoid cash payments by default whereas delay of payment where negotiated with suppliers

Nb of invoices 8mFY10

Nb of invoices FY09

Cumulated value 8mFY10

Cumulated value FY09

NB

of in

voic

es

€ in

mill

ions

Others EOM

45 days EOM

60 days 60 days

10th EOM on 31 days

EOM 30 days

net net 30 days Cash

8000 7000 6000 5000 4000 3000 2000 1000

0

60

50

40

30

20

10

0

Cumulated value FY09 Cumulated value 8mFY10Nb of invoices FY09 Nb of invoices 8mFY10

Overview of purchase invoices by contractual term

of payment over FY09 and 8mFY10

Pernod Ricard / Cash Management / 22PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYPerform A/b/c purchases

category optimization

obJEctiVEs

• Assess cash opportunities to partner efficiently with your purchasing team (tariffs, rebates, payment terms, etc.)

• Standardize payment terms to optimize working capital

• Streamline suppliers portfolio

kEY PErForMAncE inDicAtors OR ANALYSIS

kPi: A/b/c analysis example

• Weight of the top 350 vs. low 1,500 suppliers in 8mFY10 (total suppliers: 2,912)

Definition: the A/b/c categories are defined as follows A: 80% purchases from 20% of all suppliersB: 15% from 30% C: 5% from 50%

gooD PrActicEs

Ensuring efficiency of supplier base ◗ Perform A/B/C purchases analysis to determine potential optimization of the supplier / purchases base

(see KPI box for further explanation) ◗ Ensure that your purchasing team is involved in order to

• provide expertise in the sourcing and procurement processes for category A and B• negotiate proper payment terms

◗ Assess the opportunity to streamline the category C supplier portfolio ◗ Ensure that budget holders apply to standard terms for all category C suppliers

Top 350 suppliersRemaining suppliersSmallest 1,500 suppliers

9%

1%

90%

16%

29%

55%Top 350 suppliersRemaining suppliersSmallest 1,500 suppliers

Weight of the top 350 vs. Low 1,500 suppliers in 8mFY10 (total suppliers: 2,912)

Share of the €79.9m purchase Share of 15,972 invoices received

Share of the €79.9m purchasesin value

Share of 15,972 invoices receivedin number of invoices

Pernod Ricard / Cash Management / 23PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYDiversify supplier relationship

based on risk and impact

obJEctiVEs

• Increase profits and cash flow for non critical items

• Diversify supply risk

kEY PErForMAncE inDicAtors OR ANALYSIS

Definition: the quadrants of the kraljic Matrix can be described as follows

• Non-critical items: small quantity baseline, wide supplier range

• Leverage items: small quantity baseline, many suppliers, big order quantity / volume

• Bottleneck items: multiple suppliers, critical for value chain / production

• Strategic items: few suppliers, own business depends on them

gooD PrActicEs

classify supplier relationship ◗ Analyze your relationship with each of your suppliers and classify this relationship in terms of impact on profit and supply risk ◗ Give each supplier a classification and fill in the purchase portfolio matrix (Kraljic Matrix) ◗ Implement and monitor the portfolio matrix

take appropriate action with regards to each quadrant ◗ Non-critical items: optimize the processing of purchasing and exploit the competition between your suppliers ◗ Leverage item: use your purchasing power and competition to optimize purchase terms ◗ Bottleneck items: define and manage safety stock level, manage proper delivery frequency, identify suppliers for item substitution ◗ Strategic items: optimize the relationship with those suppliers and consider strategic partnerships as well as back-up

solutions to ensure availability of critical items

non-critical items

Efficient processing

bottleneck items

Volume assurance

leverage items

Exploitation of purchasing power

strategic items

Diversify, balance or exploit

Impa

ct o

n pr

ofit

Supply risk

Purchase portfolio matrix (Kraljix Matrix)

Pernod Ricard / Cash Management / 24PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYAsk the supplier to indicate the

purchase order number as well as a breakdown of services on the invoice

obJEctiVEs

• Increase control on purchase orders

• Increase efficiency of accounts payable (A/P) process

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number and share of invoices i.e. open items that could not be matched to a purchase order (see example chart)

Invoices matched

Invoices not matched

Vol

umes

Apr Mar Feb Jan

20000

15000

10000

5000

0

• Number and share of items posted to a suspense account

gooD PrActicEs

contact suppliers ◗ Contact every supplier not indicating the purchase order number on the invoice and communicate the wish for indication ◗ Ensure that the format can be recognized ◗ Consider refusing the payment if the supplier does not cooperate

breakdown of services on the invoice ◗ Ask the supplier to provide a breakdown of services (e.g. per service type, progress) or cost types (e.g. fees, traveling costs,

etc.) on the invoice in order to properly match the service performed to the invoice. This reduces the risk of overpayment or fraud

Invoices not matchedInvoices matched

Pernod Ricard / Cash Management / 25PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYManage a maximum number

of purchase orders in procurement tool or ErP

obJEctiVEs

• Ensure that purchase orders are compliant with purchasing terms and conditions

• Ensure the completeness of commitments to improve cash forecasting

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number of requisitions approved vs. number of purchase orders (see example chart)

40%60%

10% requisitions, not approved

90% requisitions, approved

• Number of requisitions approved vs. total number of requisitions

• Number of blanket orders

gooD PrActicEs

set-up requisition approval levels ◗ Define rules & responsibilities with regards to requisitions

integration of materials management ◗ Integrate purchasing with materials management to improve inventory levels

blanket orders ◗ Make proper use of blanket orders with key suppliers

Monitoring and controlling purchase orders ◗ Ensure that 80% to 90% of your purchase orders are recorded in your procurement tool / Enterprise Resource Planning

(ERP) to obtain a clear view of the overall number and value of purchase commitments

Purchase orders with approved requisitionPurchasee orders without requisition

Pernod Ricard / Cash Management / 26PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYAutomate purchase order processing

and use enabling technologies

obJEctiVEs

• Increase control on purchases orders

• Efficient purchase order process

• Increase profits and cash

kEY PErForMAncE inDicAtors OR ANALYSIS

Definition

• Electronic Data Interchange (EDI) can be formally defined as ‘the transfer of structured data, by agreed message standards, from one computer system to another without human intervention'

• E-ordering: electronic ordering is the sending of purchase orders ‘by electronic means’, i.e. transmission or making available to the recipient and storage using electronic equipment for processing (including digital compression) and storage of data

kPis

• Time spent to approve purchase orders

• Number of people with authorization to approve purchase orders

• Share of purchase orders being transferred electronically

• Number of suppliers using EDI

• Number of available online catalogues

gooD PrActicEs

Automate purchase orders processing ◗ Define the scope of employees being able to create and approve purchase orders ◗ Define the workflow and authorization limits ◗ Consider workflow functionalities of your procurement tool or Enterprise Resource Planning (ERP) to support

the approval process

consider the use of enabling technologies ◗ Encourage the use of EDI with key suppliers to accelerate the processing time ◗ Consider e-ordering for remaining suppliers ◗ Implement online catalog for key suppliers to allow more informed purchasing decisions to be taken

Pernod Ricard / Cash Management / 27PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYintegration between

procurement tool and accounting system

obJEctiVEs

• Ensure the completeness of accruals to improve the accuracy of cash forecasting

kEY PErForMAncE inDicAtors OR ANALYSIS

• Purchase orders receipt of the period vs. total number of purchases orders in progress (see example chart)

Vol

umes

Total PO in progress

PO receivedfor the period

200

150

100

50

0

gooD PrActicEs

Accruals ◗ Ensure that goods or services receipt is evaluated in the procurement tool and updates the accounting system ◗ Ensure that a procedure for the posting of accruals exists ◗ Consider configuring your systems to create an accrual automatically at the goods / services receipt

Pernod Ricard / Cash Management / 28PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYonly accept goods / services

receipt corresponding to an outstanding purchase order

obJEctiVEs

• Ensure that receipt of goods or services are compliant with the purchase order

• Increase accuracy of accruals and cash forecasting

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number of rejected deliveries (see example chart)

rejected deliveries

Num

ber

Q4 2010

Q3 2010

Q2 2010

Q1 2010 2009 2008

2500

2000

1500

1000

500

0

• Number, value and share of approved variances, purchase order vs. goods/services receipt

gooD PrActicEs

Match the goods/services receipt to an open purchase order ◗ Ensure that deliveries (in terms of quantity) have been ordered and requisitioned ◗ Consider configuring your system to require an open purchase order to post the goods / services receipt ◗ Reject deliveries where no corresponding purchase order exists

tolerance limits ◗ Define tolerance limits for quantities and prices to prohibit unreasonable variances

Approval ◗ Create an automatic workflow for the approval of variances and posting with a missing purchase order

Rejected deliveries

Pernod Ricard / Cash Management / 29PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYManage a single

entry point for invoices

obJEctiVEs

• Ensure the completeness of reception, storage and entry of all invoices

• Prohibit duplicate invoice processing and payments

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number of locations / departments being able to post invoices

• Invoices processed per day

gooD PrActicEs

single entry point ◗ Define, construct and communicate a single entry point, managed by the accounts payable department ◗ Ensure that a delivery address and a unique invoice address is communicated while ordering ◗ Identify suppliers not indicating the purchase order number on their invoice and communicate the matter to your purchasing

function

Define approval process ◗ Define the scope of employees being able to approve invoices ◗ Implement a formal communications process (workflow) of invoices across multiple departments such as finance, legal

and marketing ◗ Define the authorization approach ◗ Apply escalation procedures or guidelines around payment limits

Assess the opportunity to use enabling technology ◗ Consider scanning invoices to manage invoice processing and archiving and to maintain one repository for paper invoices ◗ Consider an automatic workflow to process (scanned) invoices to reduce the time spent until the invoice is approved

and posted in the system with respect to your approval process

Avoid double payment ◗ Verify if your accounts payable system has a facility to recognize duplicate invoices to prevent duplicate payment

Pernod Ricard / Cash Management / 30PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYEnsure supply has corresponding

purchase order to match the invoice

obJEctiVEs

• Increase control on purchasing process

• Improve cash flow forecasting

kEY PErForMAncE inDicAtors OR ANALYSIS

Definition

• 2-way-match describes the process of verifying that purchase order and invoice information matches within accepted tolerance levels. The two-way match is based on the following criteria matching: invoice price = order price and quantity billed = quantity ordered

• 3-way-match verifies additionally to the 2-way-match if the quantity billed is equal to the quantity received

kPi

• Number and share of invoices• without goods / services receipt• without purchase order• without goods / services receipt and missing purchase order

gooD PrActicEs

Match the incoming invoice to… ◗ the purchase order and compare quantity and prices (2-way-match) and ◗ to the goods / services receipt and compare its quantities (3-way-match)

consider implementing preventive and/or detective controls ◗ Configure your procurement tool or Enterprise Resource Planning (ERP) to require an open purchase order to post the

goods / services received ◗ Monitor cases where the 2 or 3-way match was not possible and analyse root causes

Pernod Ricard / Cash Management / 31PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYconsider more effective

billing mechanisms

obJEctiVEs

• Streamline invoicing and payment process

• Optimize payment terms negotiation outcome

• Improve operational expenditure benefits (e-invoicing avoids some costs: paper, mailing etc.)

kEY PErForMAncE inDicAtors OR ANALYSIS

Definition

• Electronic invoicing is the sending of invoices ‘by electronic means’ so that the recipient can read, store or process within their system

kPi

• Number of invoices received per supplier (see example chart)

Number of invoices

Num

ber

of in

voic

es

Supp

lier 1

1

Supp

lier 1

0

Supp

lier 9

Supp

lier 8

Supp

lier 7

Supp

lier 6

Supp

lier 5

Supp

lier 4

Supp

lier 3

Supp

lier 2

Supp

lier 1

400

350

300

250

200

150

100

50

0

Most invoices are received from supplier 6 and 9: E-invoicing from these suppliers would bring the most advantages

gooD PrActicEs

consider electronic invoicing ◗ Analyze which suppliers could be suitable to request e.g. suppliers from whom the most invoices are received ◗ Consider the possibility to implement e-invoicing between affiliates ◗ Contact these suppliers and discuss the possibility for e-invoicing ◗ Make sure to consider relevant legal and tax requirements for e-invoicing ◗ In case of implementation, ensure that e-invoices are properly archived

consider self-billing ◗ Analyze which suppliers could be suitable for self billing; the most trusted and long-term suppliers are eligible for this ◗ Ensure that the reception area works properly in terms of incoming goods inspection ◗ Contact these suppliers and negotiate agreements on self billing, point out the advantages for suppliers ◗ If possible, combine self billing with e-ordering to fully automate the process (even less handling and less errors)

Number of invoices

Most invoices are received from supplier 6 and 9: E-invoicing from these suppliers would bring the most advantages

Pernod Ricard / Cash Management / 32PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYPlan periodic payment campaigns

(use a payment schedule) to optimize Days Payable outstanding (DPo)

obJEctiVEs

• Smooth and optimize cash outflows and forecasting

• Use favorable payment methods

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number, share and volume of payments per period that• are paid according to its due date• could be grouped and paid according to a defined schedule

gooD PrActicEs

Define payment campaigns ◗ Define a schedule for payment campaigns (twice a month) ◗ Negotiate periodic invoicing (e.g. blanket order), combining various orders received ◗ Analyze the breakdown of the different payment methods

Monitor results of payment campaigns ◗ Monitor the impact on the DPO and cash flow forecast ◗ Monitor and inform the payment method used after every campaign

Analyze current status of used payment methods ◗ Create a list of all payment methods in use ◗ Analyze which suppliers can be paid by using a favorable payment method

negotiate towards favorable payment methods ◗ Reduce check payments and negotiate towards electronic payments processing ◗ Avoid petty cash payments to reduce administration costs and potential fraud ◗ Negotiate the favorable payment method ◗ Monitor on a regular basis if favorable payment methods are used

Pernod Ricard / Cash Management / 33PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYimplement controls

to prevent early payments

obJEctiVEs

• Optimize cash flow and forecasting

• Control payment process

kEY PErForMAncE inDicAtors OR ANALYSIS

• Actual amount of early payments

• Early payments value and early volume in terms of number of invoices to be managed on a monthly basis

• Example of process:

gooD PrActicEs

Analyze existing controls (measures / activities) to prevent early payments ◗ Analyze the early payment purchase value and volume and identify root causes to determine if the amount could be

decreased in the future ◗ Analyze existing controls such as segregation of duties or system configurations

implement controls to prevent early payments, e.g. ◗ Ensure segregation of duties between the accounts payable (A/P) department (invoice processing) and Treasury or other

departments processing the payment, e.g. access or change of A/P master data files should not be permitted for employees processing payments ◗ Ensure that the accounts payable system determines the due date automatically according to the payment terms ◗ Analyze on a regular basis if early payments still occur and find root causes ◗ Formalize the controls by communicating them internally with clear roles & responsibilities and automating them in your

systems

Authorize and execute

payment

Preparepayment

Purchase order (Po) available ?

contact Administrator

goods received and same as Po ?

contact Administrator

invoice received and same as Po ?

contact Administrator

Payment date same as invoice ?

contact Administrator

Y Y Y Y

Adm

inis

trat

orC

ashi

er

N N N N

Pernod Ricard / Cash Management / 34PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYintegrate accounts payable system

with the banking system

obJEctiVEs

• Increase transparency over payments processing

• Reduce the risk of manipulation and fraud

• Automatic balancing of open items

kEY PErForMAncE inDicAtors OR ANALYSIS

• Time spent to balance open items after the receipt of the bank statement

• Example of an in-house regional payment factory:

PaymentsCompany

SystemBanking

Operating Parameters

Reporting

Corporate Treasury

In-HouseBank

Reporting

External Payments

Remittance Info

Bank(s)

Suppliers

Reporting

Cash Settlements Centre

gooD PrActicEs

interface your accounts payable systems with the banking system regarding the in- and outflow of information ◗ Streamline the format and process of your electronic payments processing ◗ Interface the two systems to avoid the usage of portable drives/discs ◗ Consider processing the electronic bank statement ◗ Analyze if your system can process an electronic bank statement to balance open accounts payable items automatically

Workflow for payment authorization ◗Create an automatic workflow for the authorization of payments to reduce the time spent until the payment is processed at the bank ◗ Depending on the payment volume, define authorization limits and configure your workflow system accordingly ◗ Limit the number of people having access to that system

Payment factory ◗ Consider building regional payment factories allowing to net and bundle payments, lowering the number of transactions and

related transaction costs as well as to streamline the payment process

Pernod Ricard / Cash Management / 35PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYPerform inventory and valuation

of claims for provisions

obJEctiVEs

• Improve cash flow management and forecasting

• Improve closing process

kEY PErForMAncE inDicAtors OR ANALYSIS

• Number, share and value of claims per supplier (see example chart)

Number of Claims

Number of PO

Num

ber

of

Supplier 6 Supplier 5 Supplier 4 Supplier 3 Supplier 2 Supplier 1

150

100

50

0

• Development of provisions

• Time to prepare the period-end closing

gooD PrActicEs

Estimation of provisions (managed by accounting) ◗ Perform inventory and valuation of claims for provisions ◗ Analyze root causes to reduce the number of claims ◗ Ensure all goods and services received are invoiced and accrued (e.g. enter all receipts to enable accounts payable to match

all outstanding invoices)

Number of PONumber of Claims

Pernod Ricard / Cash Management / 36PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYPerform an annual review

of actual payment terms versus contract payment terms

obJEctiVEs

• Reduce risk of early payment

• Optimize payment date vs. due date

kEY PErForMAncE inDicAtors OR ANALYSIS

• Actual Days Payable Outstanding (DPO) vs. master date, target DPO and working capital potential (see example chart)

Master data DPO/Target DPO

Actual DPO

Potential WC

W/C

Impr

ovem

ent

('000

EU

R) D

PO (D

ays)

Supp

lier 1

0

Supp

lier 9

Supp

lier 8

Supp

lier 7

Supp

lier 6

Supp

lier 5

Supp

lier 4

Supp

lier 3

Supp

lier 2

Supp

lier 1

100 90 80 70 60 50 40 30 20 10 0

100 90 80 70 60 50 40 30 20 10 0

30

60 60 60 60

90

60 60 60 60

29 22 15

12

50 52

9

43

28

4 7 8 9 9 9 14

16

28

48

97

gooD PrActicEs

Periodically analyze payment terms ◗ Make sure the actual invoice terms are aligned with the terms as stated in the contract ◗ Register contract terms in the supplier master data (refer to: "Register contract terms in vendor master data") ◗ Make a periodic analysis (minimum once a year) of actual invoice terms versus contract terms (for example: see chart) ◗ Determine how many invoices (and at which value) have been paid before the standard terms due date ◗ Determine the working capital improvement potential ◗ Take appropriate action (e.g. by registering schedule payment terms in the master data)

Potential WCActual DPO Master data DPO/ Target DPO

Pernod Ricard / Cash Management / 37PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYMonitor accounts payable (A/P)

ageing balance

obJEctiVEs

• Improve cash flow management and forecasting

• Improve closing process

kEY PErForMAncE inDicAtors OR ANALYSIS

• A/P ageing balance (see example chart)

gooD PrActicEs

Ageing balance ◗ Ensure that due dates are derived or entered when an invoice is posted ◗ Configure your system to be able to retrieve an ageing balance for accounts payable ◗ Analyze the root causes for items that have not been paid in a reasonable time frame ◗ Monitor the A/P ageing balance on a regular basis

Aged Accounts Payable

not impaired and not due

0-90 days

90-180 days

+180 days

'000

EU

R

BUD

FC

Jun

10

May

10

Apr

10

Mar

10

Feb

10

Jan

10

Dec

10

Nov

10

Oct

10

Sep

10

Aug

10

Jun

09

May

09

Apr

09

Mar

09

Feb

09

Jan

09

Dec

08

Nov

08

Oct

08

Sep

08

Aug

08

Jun

08

May

08

Apr

08

1000

900

800

700

600

500

400

300

200

100

0

+180 days90-180 days0-90 daysNot impaired and not due

Pernod Ricard / Cash Management / 38PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYcompare actual vs. target

Days Payable outstanding (DPo)

obJEctiVEs

• Monitor the DPO trend to ensure that targets are met

• Optimize working capital

kEY PErForMAncE inDicAtors OR ANALYSIS

• Payables vs. DPO (see example chart)

gooD PrActicEs

cash Dashboard ◗ Issue a Cash Dashboard in each reporting period ◗ Compare the actual vs. target accounts payable balance & DPO ◗ Analyze the reasons of changing A/P balance compared to last month ◗ Determine whether differences can be optimized ◗ Take appropriate action if targets cannot be met

Payables vs. DPO

Trade payables Non group FY 10/11 Trade payables Non group FY 09/10 DPO Non group FY 09/10DPO Non group FY 10/11

Payable vs. DPO

DPO Non group FY 10/11

DPO Non group FY 09/10

Trade payables Non group FY 10/11

Trade payables Non group FY 09/10

EUR

mill

ion

Day

s

Aug Sep

Oct

Nov Dec

BUD D

ec Jan Feb

Mar Apr May Jun

LE Ju

nBU

D Jun

90

80

70

60

50

40

30

20

10

0

140

120

100

80

60

40

20

0

Pernod Ricard / Cash Management / 39PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYnegotiate with vendors

and formalize the business relationship

obJEctiVEs

• Provide Marketing team with some key and simplified guidelines in order to ensure a purchasing process (media, PR event, etc.) consistent with the company policy exists

• Mentioned good practices apply also to all other budget holders (budget in structure costs) who can engage the company resources directly (training, consultant fees, PR, etc.)

kEY PErForMAncE inDicAtors OR ANALYSIS

• N/A

gooD PrActicEs

negotiate with vendors and formalize the business relationship ◗ Implement a bidding process when the negotiation with the vendors is local (challenge your vendors even though the

relationship has existed for a long time) ◗ Ask your finance department some guidance regarding the payment terms before making an agreement with the supplier

(advance payments should be limited to very specific situations) ◗ Formalize the key partnerships with contracts and involve your legal department ◗ Follow the rules and approval process of your business when creating and/or updating master data related to the vendors

(name, address, contact point, payment term, etc.) ◗ Establish some clear and objective criteria for accepting the rendered services

Follow-up ◗ Prepare and communicate every quarter a summary of the next 3 months activities / action plans and related budgets for

all the brands (timeline) ◗ Monitor your Advertising & Promotion (A&P) budget by project (budget / schedule / progress) and appoint one single

responsible person for every project even though the project is cross-functional (e.g. marketing + trade marketing) ◗ The internal rules of the game to reallocate the saving at the end of a given project to another project should be discussed

and agreed with your finance department ◗ For the in progress action plans, liaise with your finance department to make sure the end of month accruals are consistent

with the real progress ◗ Make sure the received invoices are communicated to the accounting department in a timely manner. Posting the invoices

does not prevent from blocking the payment (in that case an information to your accounting / treasury department is needed) ◗ Ask the supplier to provide a breakdown of services (e.g. per service type, progress, etc.) or cost types (e.g. fees, traveling

costs) on the invoice and ask for back-up if needed (e.g. travel & expenses spending) ◗ Point of Sales material should be followed as an inventory (at least in quantity)

MARKETING

Pernod Ricard / Cash Management / 40PURCHASING FINANCE

Negotiate with vendorMaintain vendor master dataProcess purchase ordersReceive goods and servicesProcess invoicesProcess paymentsManage A/P & process period end

PURCHASE TO PAYimplement follow-up

and monitor procedures regarding budget versus actual spend

obJEctiVEs

• Provide the on-trade team with some key and simplified guidelines in order to ensure that the cash impact of the busi-ness decision to support iconic / image venues or outlets are considered in the business decision

kEY PErForMAncE inDicAtors OR ANALYSIS

• Return On Invesment (ROI) analysis

gooD PrActicEs

negotiation ◗ When a decision to support an iconic / image venue or outlet is made, assess the opportunity of drafting a contract

mentioning the expected counterparty for your entity (volumes target, listing new products, party sponsorships, bar styling, etc.) with the support of your legal counsel or team ◗ If the support is granted through the payment of a dedicated Trade Advertising & Promotion (A&P) budget, the cash-out

should be phased as much as possible (e.g. payment in one single exhibition at the beginning of a 1 year engagement should be avoided) ◗ If the support is granted through some longer payments terms (in case of direct sales to venues / outlets), your internal

credit policy rules apply ◗ When the counterpart is tangible and measurable, a Return On Investment (ROI) style analysis is needed (ask your finance

team to support you) ◗ Prior to beginning the negotiation process regarding payment terms with new or ongoing vendors, make sure you are

compliant with your entity's internal policy. If an exception exists, follow the proper approval process

Follow-up ◗ The progress of the commitments of the venue / outlet should be monitored on a regular basis till the termination of

the contract or the agreement

MARKETING

PURCHASE TO PAYnotes

Pernod Ricard / Cash Management / 41

Jameson

Order to CashSales cycle, from the development of customer relationships to the receipt of cash (The Accounts Receivable Cycle)

toolkit

split

by

Function

Pernod Ricard / Cash Management / 44

ORDER TO CASHaCCounts ReCeivable CyCle

enabling pRoCesses

sales and Finance• Negotiate with client• Manage credit• Maintain client master data• Process orders• Process invoices• Process receipts• Manage collection & disputes• Manage AR & process period end

orderto Cash

treasury operations

purchaseto pay

Forecast to Fulfill

toolkits

by FunCtion

order to Cash • Negotiate with client• Manage credit• Maintain client master data• Process orders• Process invoices• Manage collection & disputes

sales

Finance

purchasingMarketing

supply Chain

order to Cash • Negotiate with client• Manage credit• Maintain client master data• Process receipts• Manage collection & disputes• Manage AR & process period end

toolkit

split

by

Cycle

Pernod Ricard / Cash Management / 45• SALES • FINANCE

••••••

••••

••

•

•

••

•

Order to Cash

table of contents

negotiate with customers

• Minimize the total of payment terms and conditions offered• Offer differentiated payment methods• Negotiate automated remittance• Align payment terms with customer importance• Renegotiate payment terms with small customers• Partner with (larger) customers to streamline ordering, receipt and payment process

Manage credit order

• Set-up credit policies and define credit limits per customer category• Create effective automated controls to prevent staff from overriding set credit limits• Relate payment terms with credit rating

• Consider accounts receivable credit insurance

Maintain customer master data

• Register customer master data in your sales & distribution tool or ERP

• Analyze customer portfolio

process orders

• Provide electronic and/or automate ordering• Manage 100% of orders in Sales Administration tool or ERP• Offer Automatic Stock Replenishment (ASR) or Vendor Managed Inventory (VMI) to key customers

• Hold repeat orders (or block deliveries) if invoices are more then X days overdue

process invoices

• Consider electronic data interchange (EDI) to invoice key customers

• Send invoice early in the process (at order receipt or confirmation)

process receipts

• Automate reconciliation of payments with invoices

• Consider providing online access to customer accounts and invoices in order to ease and accelerate payments

Manage collection & disputes

• Diversify your follow-up procedures• Implement formal dispute resolution• Assign collectors to specific customers

• Provide collection and operations staff incentives for collection / dunning

Manage a/R & process period end

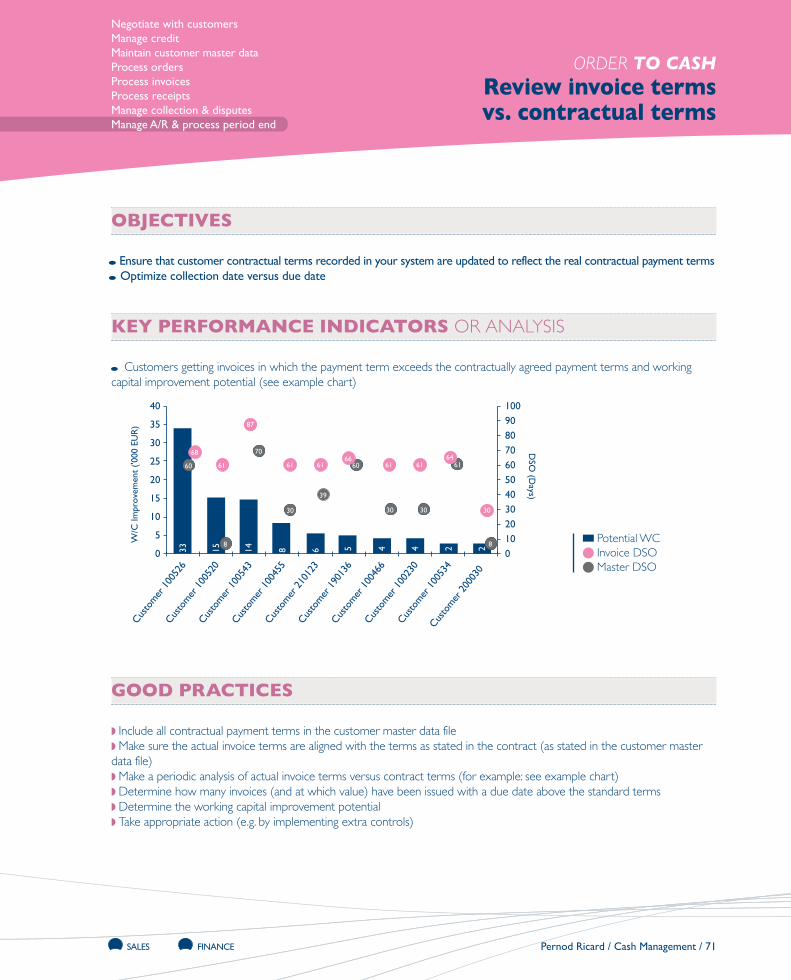

• Consider bad debts write-off and related tax reimbursement• Review invoice terms versus contractual terms• Analyze suspense accounts to ensure all received payments are allocated and to be invoiced orders are invoiced• Analyze ageing accounts receivable• Compare actual versus target receivables & Days Sales Outstanding (DSO)

Pernod Ricard / Cash Management / 46SALES FINANCE

Negotiate with customersManage creditMaintain customer master dataProcess ordersProcess invoicesProcess receiptsManage collection & disputesManage A/R & process period end