Embed Size (px)

Citation preview

1Presentation prepared forPublic Finance Headquarters

1400 Wewatta Street, Suite 800 • Denver, CO 80202 • (800) 722-1670

Single-Family Financing Essentials, Part 2: Securing the Best Price

MRB, Mortgage Market or Both?

January 2015

JIM STRETZSenior Vice [email protected]

2Presentation prepared for

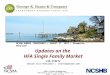

Who is Doing What?

U.S. Bank MS – 3rd Party Hedge

U.S. Bank MS – Self Hedge w/ 3rd Party Advice

U.S. Bank MS – Non TBA

Idaho MS – 3rd Party Hedge

Idaho MS – Self Hedge Alabama MS – Self Hedge

Alabama MS – 3rd Party Hedge

Self Servicing – Self Hedge

Multiple Servicers – Non-TBA

Rhode Island

Connecticut

New Jersey

Delaware

Maryland

Washington, D.C.

Self Servicing – Non-TBA

3Presentation prepared for

Reserve Requirements

Lower Requirements (0% - 3%)

Higher Requirements (5% - 7%)

Ratings Rating Higher thanWhole Loans with Similar Parity

Rating Influenced by PMI Providers & Reserve Investments

Risk No exposure to PMI Credit Exposure to PMI Providers’ Credit

Cash Flow Timing

Predictable, Scheduled/Scheduled

Less Predicable, Actual/Actual

Optimal Structure

Lowest Cost Possible with Pass-Through Structure

Pass-Through is 50 to 100 bps Higher in Rate

Portfolio Data

Information Standardized & Available by Third Party

Information Produced by HFA and Different from Issuer to Issuer

Mortgage Costs

Higher Costs with GSE Guaranty& Adverse Market Fees

NoneNone

MRB Cost Considerations

M B S Whole LoansConsideration

4Presentation prepared for

HFA Mortgage Market Cost Considerations

Different HFA strategies listed from lowest estimated net cost to highest.

1) In-house hedging, using TBA or window

2) In-house hedging, using Broker Dealer as Advisor

3) Hedging using Financial Advisor to run the program

4) Third Party Hedge Provider for a fee less any shared profits on the back-end for benefits received by early delivery, specified pools and CRA motivated investors

5) Third Party Hedge Provider for a set fee

Defined: MBS Sale to Third Party or Whole Loan Sale to GSE Window, Hedging Rate Risk in TBA Market or GSE Window

Note: In 1 – 3, the HFA takes

all the risk.

5Presentation prepared for

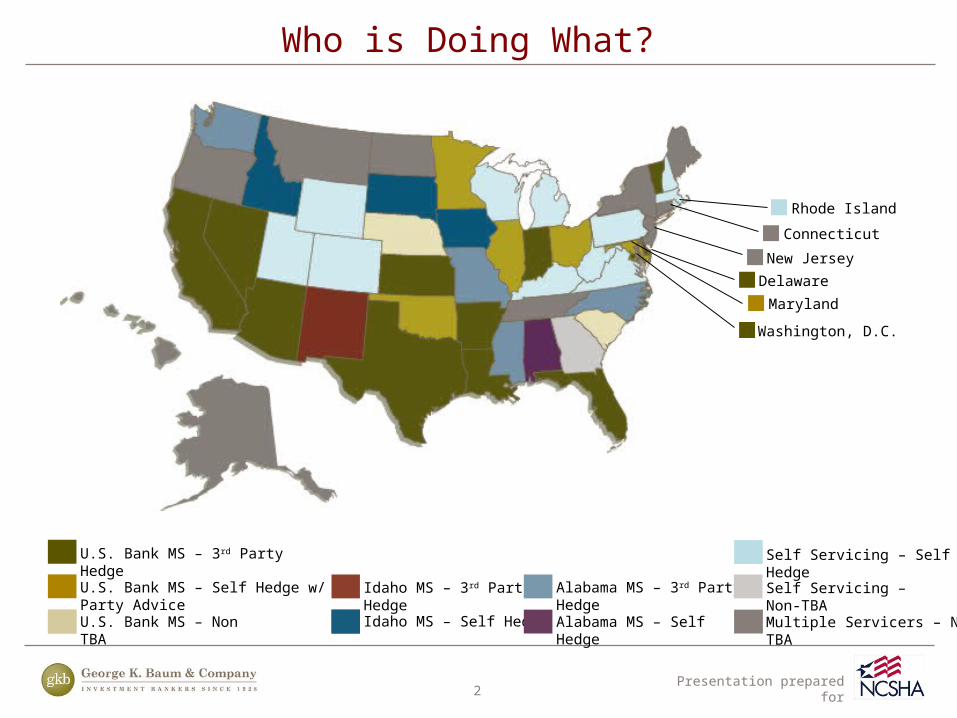

MRB or Mortgage Market

Comparison using rates as of Jan 5, 2015. Assuming $20 Million Portfolio 4% Ginnie Mae MBS

Estimated Net Return after Down Payment & Expense Reimbursement

Structure 100% PSA 200% PSA 300% PSA

Pass-Through 105.4 103.8 102.9

Traditional 104.3 102.7 101.7

MBS Sale 105.0 Paid Upfront at SaleMortgageMarket

Mortgage Revenue Bonds

6Presentation prepared for

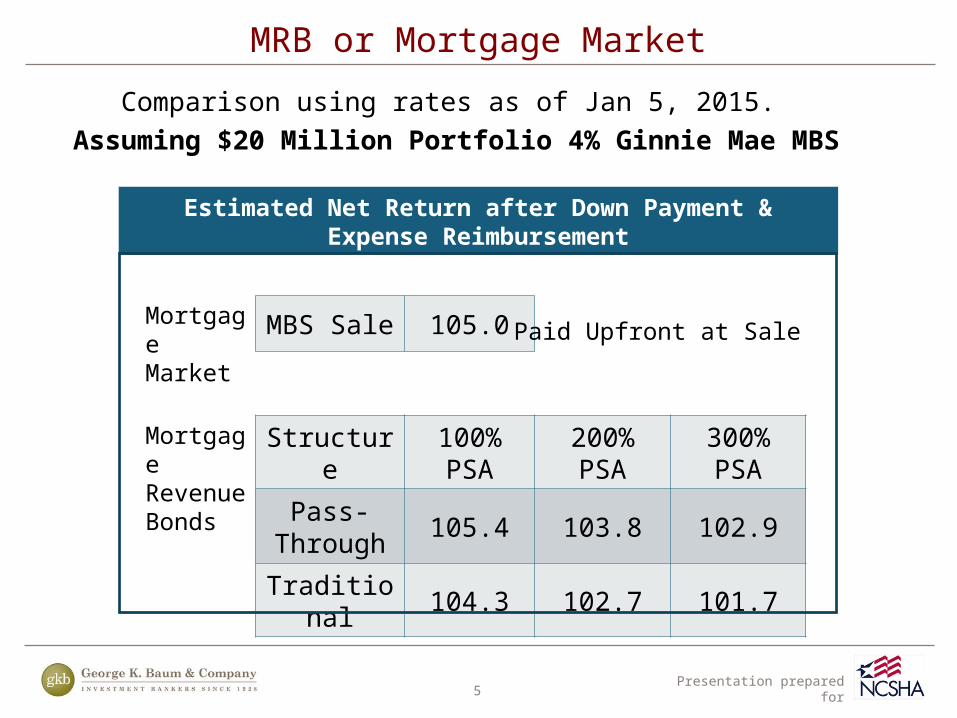

2006 2015(estimated)

Whole Loan 30 6

MBS 18 29

Mixed 3 16

MCC 14 33

Changing HFA Strategies

HFA’s switching to (or including) MBS’s are also selling into the cash or TBA market using their balance sheets, “zeros” or TBA as a rate hedge.

7Presentation prepared for

0.000%

0.500%

1.000%

1.500%

2.000%

2.500%

3.000%

3.500%

4.000%

4.500%

5.000%

5.500%Ne

bras

ka D

L*C

onne

cticu

t D M

Min

neso

ta D

M L

Ore

gon

DSo

uth

Dako

ta D

MW

yom

ing

DD.

C. D

Idah

o D

MIo

wa D

MM

issou

ri D

M*O

klaho

ma

D M

Dela

ware

D M

Mai

ne D

Mon

tana

D M

New

Mex

ico D

North

Car

olin

a D

M*Il

linoi

s D

M L

*Miss

issip

pi M

*Wes

t Virg

inia

D L

Ohi

o D

M L

North

Dak

ota

D L

*Ala

bam

a D

M*M

aryla

nd D

M*R

hode

Isla

nd D

M*S

outh

Car

olin

a D

LCa

liforn

ia D

MCo

lora

do D

M L

Kent

ucky

D M

Mich

igan

D M

New

Ham

pshi

re D

M L

Verm

ont D

M*U

tah

D M

Alas

ka D

*Ten

ness

ee D

MG

eorg

ia D

LNe

w Yo

rk D

M L

*Flo

rida

D M

*Wisc

onsin

D M

LNe

w Je

rsey

D*L

ouisi

ana

D*N

evad

a D

M*W

ashi

ngto

n D

M L

*Ariz

ona

D M

L*T

exas

D M

HFA Rates as of January 9, 2015

Freddie Mac Primary Mortgage Market Rate 3.73%

Rates shown above are for unassisted loans. HFAs that do not have a posted rate on their website include: Arkansas, Hawaii, Indiana, Massachusetts Pennsylvania, and Virginia. (*) denotes HFAs with no difference between the DPA and no DPA rate,

(D) denotes a DPA program, (M) an MCC program and (L) a local premium priced DPA program as competition.

8Presentation prepared for

0.000%

0.500%

1.000%

1.500%

2.000%

2.500%

3.000%

3.500%

4.000%

4.500%

5.000%

5.500%O

rego

n D

Conn

ectic

ut D

MId

aho

D M

Neb

rask

a D

Nor

th D

akot

a D

Calif

orni

a D

Mai

ne D

Mon

tana

Sout

h D

akot

a D

MW

yom

ing

DAl

aska

DM

ichi

gan

D M

Min

neso

ta D

MCo

lora

do D

MD

.C. D

Del

awar

e D

MIo

wa

D M

New

Ham

pshi

re D

MN

ew Y

ork

D M

Nor

th C

arol

ina

D M

Ohi

o D

MPe

nnsy

lvan

ia D

MU

tah

DVe

rmon

t D M

Geo

rgia

DM

isso

uri D

MRh

ode

Isla

nd D

Tenn

esse

e M

Alab

ama

D M

Flor

ida

DIll

inoi

s D

MM

aryl

and

Nev

ada

DW

est V

irgin

ia D

Wis

cons

in D

MAr

izon

a D

MKe

ntuc

ky D

Loui

sian

aO

klah

oma

DW

ashi

ngto

n D

MSo

uth

Caro

lina

DTe

xas

D M

New

Jers

ey D

New

Mex

ico

D

HFA Rates as of January 13, 2014

HFAs that do not have a posted rate on their website include: Arkansas, Hawaii, Indiana, Massachusetts, Mississippi and Virginia. (D) denotes rates that include DPA, (M) denotes HFAs advertising an MCC program on their website.

Freddie Mac Primary Mortgage Market Rate 4.510%

9Presentation prepared for

Minimize Rate Risk with Third Party

No Opportunity with 3rd Party except forward

swaps or TBA

TBA & GSE Window Hedge

Reserves Reserve Requirements per Indenture Minimal

Hedging Balance Sheet Hedging and TBA TBA & GSE Window

Revenue Annuity Paid Upfront

Tax Status Tax Exempt Taxable

MRB v Mortgage Market Cost Considerations

M R Bs Mortgage MarketConsiderations

10Presentation prepared for

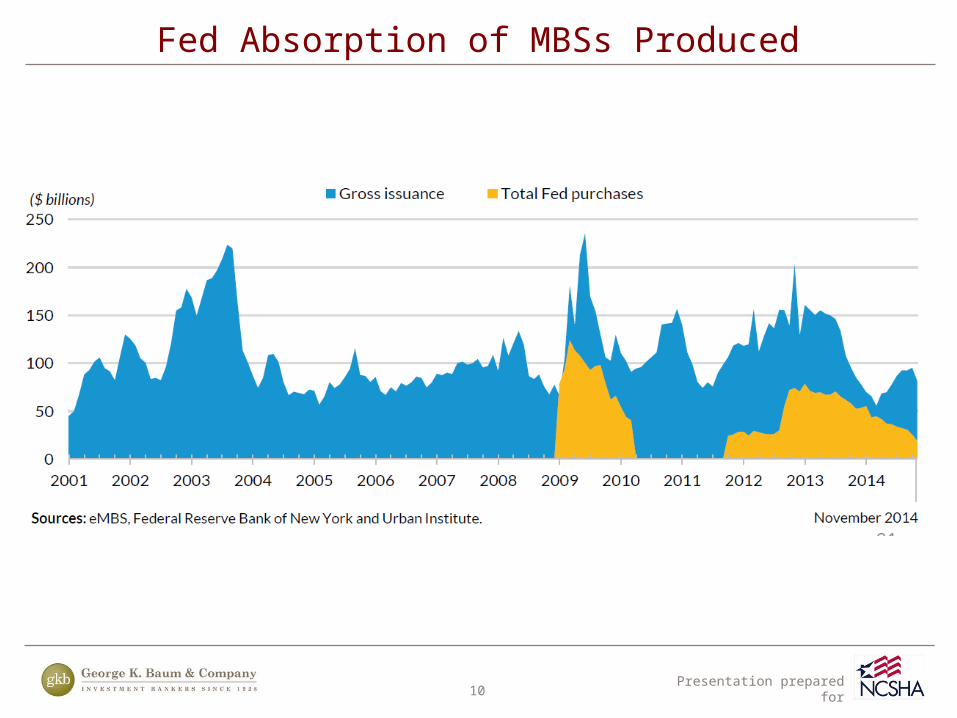

Fed Absorption of MBSs Produced

11Presentation prepared for

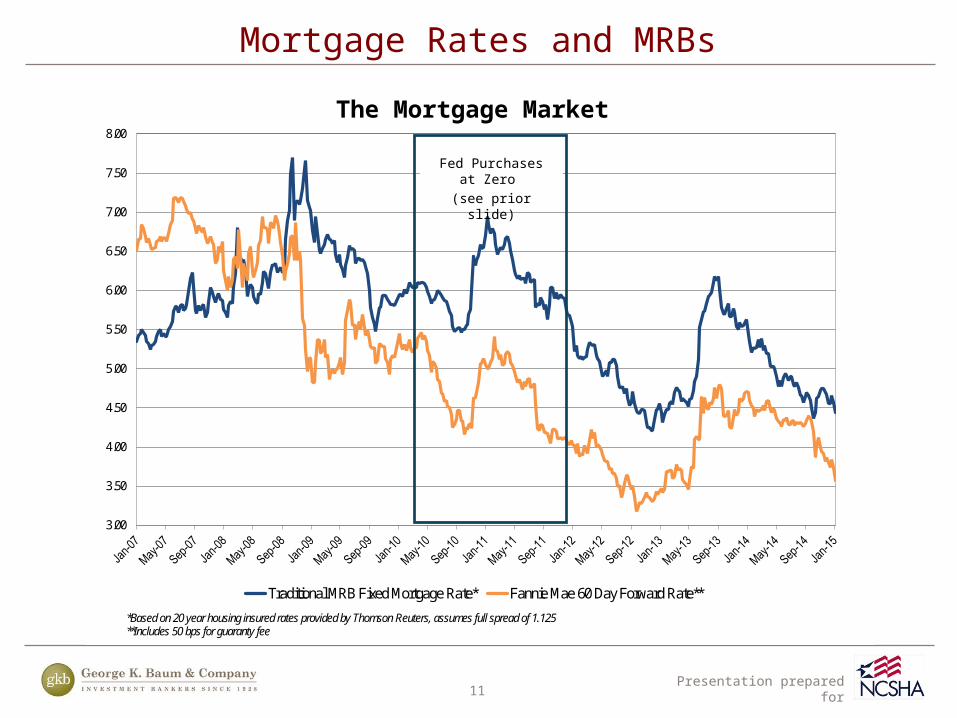

Mortgage Rates and MRBs

The Mortgage Market

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Traditional MRB Fixed Mortgage Rate* Fannie Mae 60 Day Forward Rate**

Traditional MRB Mortgage Rates vs. FNMA 60 Day Forward

*Based on 20 year housing insured rates provided by Thomson Reuters, assumes full spread of 1.125**Includes 50 bps for guaranty fee

Fed Purchases at Zero (see prior slide)

12Presentation prepared for

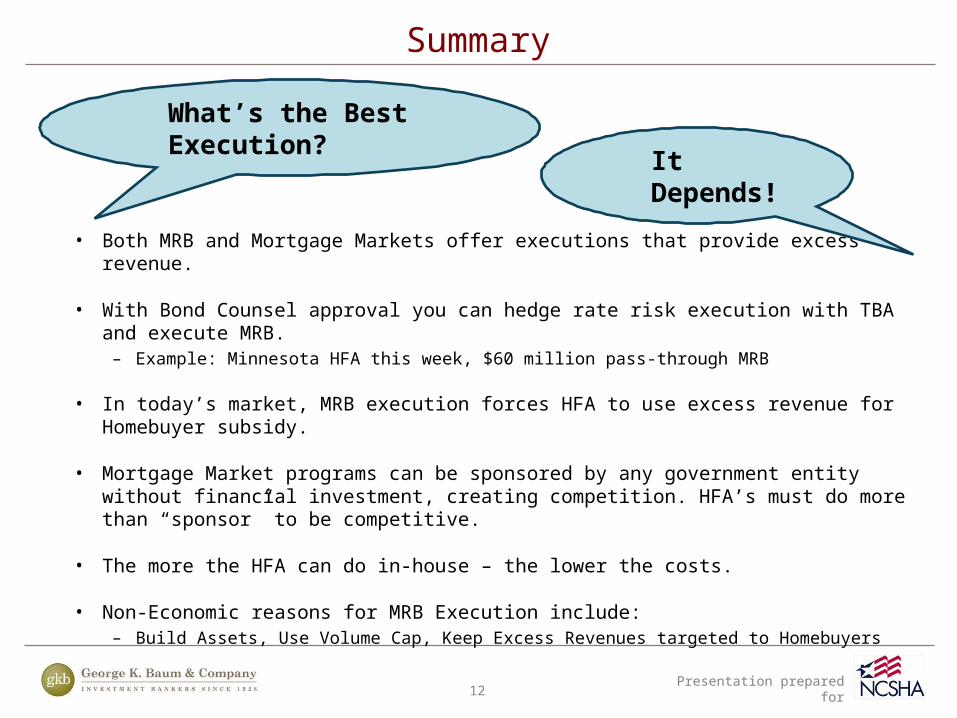

• Both MRB and Mortgage Markets offer executions that provide excess revenue.

• With Bond Counsel approval you can hedge rate risk execution with TBA and execute MRB.– Example: Minnesota HFA this week, $60 million pass-through MRB

• In today’s market, MRB execution forces HFA to use excess revenue for Homebuyer subsidy.

• Mortgage Market programs can be sponsored by any government entity without financial investment, creating competition. HFA’s must do more than “sponsor” to be competitive.

• The more the HFA can do in-house – the lower the costs.

• Non-Economic reasons for MRB Execution include:– Build Assets, Use Volume Cap, Keep Excess Revenues targeted to Homebuyers

Summary

What’s the Best Execution?

It Depends!

13Presentation prepared for

This report was prepared from data believed to be reliable but not guaranteed by us without further verification or investigation, and does not purport to be complete. It is not to be considered as an offer to sell or a solicitation of an offer to buy the securities of the entities covered by this report. Opinions expressed are subject to change without notice. George K. Baum & Company may act as a principal for its own account or as agent for another person, in connection with the sale or purchase of any security which is subject in this report.

Disclaimer