Embed Size (px)

Citation preview

1

Reinsurance Market Outlook:Value Creating Capital

Azerbaijan International Insurance Forum - AIIF 2012Baku, 04th – 05th July, 2012

2

Contents

I. Who is Aon Benfield

II. Setting the Scene

3

Who is Aon Benfield

4

About Aon

Aon plc (NYSE: AON) is the leading global provider of risk management services, insurance and reinsurance brokerage, and human resource consulting and outsourcing.

Aon plc

Aon Risk Solutions Aon Benfield Aon Hewitt

Retail Brokerage Reinsurance Human Capital Consulting

Proprietary & Confidential

$ 6.0 billion

$ 78 billion

~28,000

$ 3.8 billion

~30,000

$ 1.5 billion

$ 29 billion

~3,000

Commissions & Fees

Premium

Colleagues

$ 11.3 billion

$ 107 billion

~61,000

Total 2011

5

Aon Benfield

Aon Benfield is world’s No.1:

Treaty

Facultative

Investment bank exclusively focused in (re)insurance

Why is Aon Benfield No.1:

Experience and knowledge about each country and region

– offices in more than 50 countries

Unrivalled investments in Analytics – Over US$ 120m invested annually– Over 500 in analytics– 16 partner universities globally

Best Transactional team

Widest Market Access

Global Reach

Trusted Advisor

Numbers for 2010, Source: Business Insurance 24th October 2011

Aon Benfield CEE team

All part of ONE CEE Team with 87 members

The most experienced team in the region

27 Analytics dedicated to the region

6Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Aon Benfield CEE Business

127 direct cedents

In CEE

Placing business with 163

reinsurers.

EUR 428m ceded premium

7

Setting the Scene

Full year ended December 31, 2011

8

Economic Climate

Main issues for insurance and reinsurance market:

9Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Reinsurer Capital Change (USD Billions)

Reinsurance capacity ended 2011 down 3 percent over FY 2010 despite nearly USD113 billion in insured catastrophe losses during 2011

Reinsurers covered a higher proportion of losses in 2011 than in prior major catastrophe years because affected insurers generally held lower retentions and utilized substantial proportional contracts

Source: Individual Company Reports, Aon Benfield Analytics

10Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Aon Benfield Aggregate Combined Ratio Comparison

Source: Individual Company Reports, Aon Benfield Analytics

The ABA combined ratio increased to 108.2 percent, an increase of 13.5 percentage points compared to 2010 with a 14.1 percentage point increase in natural catastrophe losses

Reinsurer returns on equity in 2011 dropped to 3 percent due to catastrophe losses and lower investment yields; Analyst consensus earnings for public reinsurers show returns on equity rebounding to the 10 percent range for 2012 and 2013

11Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Shareholders’ funds development – FY 2011 vs FY 2010

246.6 1.6

11.7 -9.6

-0.8 5.0 -4.10.5 250.8

200

210

220

230

240

250

260

270

FY 2010SHF

Additionalcapital

Netincome

Dividends FX Investmentgains

Sharebuybacks

Other FY 2011SHF

US

D (b

illio

ns)

209.7

24.7

23.6 -7.4-1.8

8.4 -10.2

-0.5 246.6

200

210

220

230

240

250

260

270

FY 2009SHF

Additionalcapital

Netincome

Dividends FX Investmentgains

Sharebuybacks

Other FY 2010SHF

US

D (b

illio

ns)

12Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

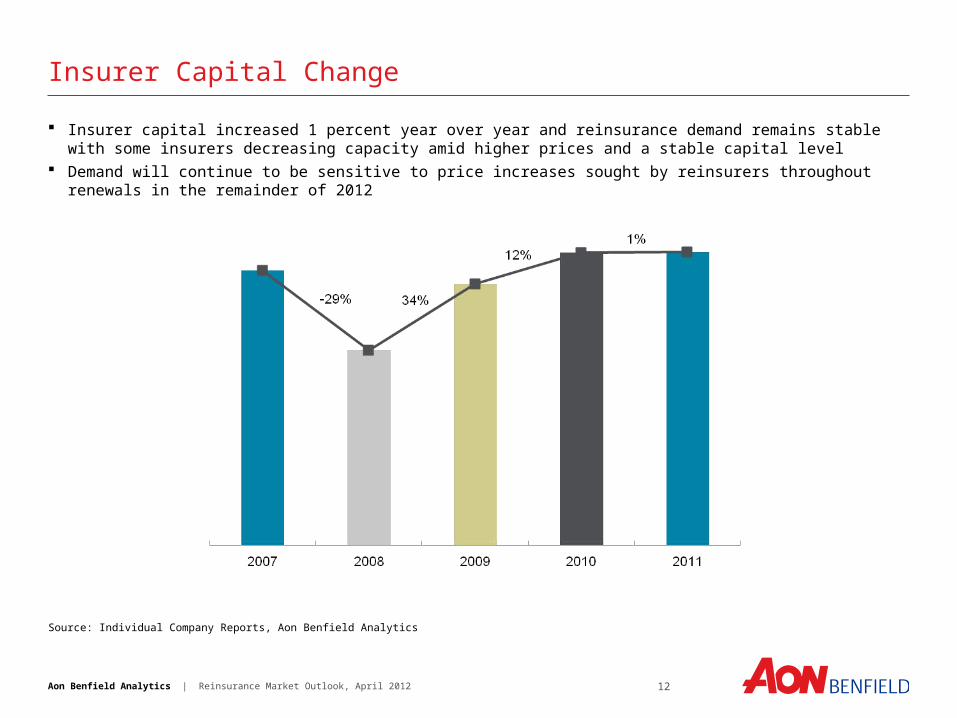

Insurer Capital Change

Source: Individual Company Reports, Aon Benfield Analytics

Insurer capital increased 1 percent year over year and reinsurance demand remains stable with some insurers decreasing capacity amid higher prices and a stable capital level

Demand will continue to be sensitive to price increases sought by reinsurers throughout renewals in the remainder of 2012

13Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Impact Forecasting Economic Loss Estimates

Source: Impact Forecasting

Global losses for 2011 are currently estimated at USD 434 billion

-

50

100

150

200

250

300

350

400

450

500

2004 2005 2006 2007 2008 2009 2010 2011

Bill

ion

s

Winter Weather

Wind

Wildfires

Tropical Cyclone

Severe Weather

Other

Hurricane/Typhoon

Flood

Earthquake

14Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

2011 Economic Loss versus Recent Years’ Average

Losses in Asia alone accounted for 65 percent of total losses for 2011, more than six times the average annual economic loss in that region in recent years

Higher insurance penetration in the regions with loss in 2011 increased total loss covered by insurance to approximately 25 percent (USD 106 billion), up from 15 percent in 2010.

Source: Impact Forecasting

$0

$50

$100

$150

$200

$250

$300

Africa Asia Europe NorthAmerica(excl US)

Oceania SouthAmerica

US

Bill

ion

s

Average 2004-2010 2011

15Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

3 of Top 10 Events in the past 30 Years Occurred in 2011

•The New Zealand government has only released a combined USD 30 billion economic loss total for the September 2010, February 2011 and June 2011 EQ Events.•Sources: Impact Forecasting, Insurance Information Institute, National Hurricane Center, National Climatic Data Center, USGS

16Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

2011 Catastrophe Losses as Percent of FY 2010 Shareholders’ Funds

*Includes other major events, additions/releases from previous quarter(s) loss estimates (when not split by event), reinstatements, FX reconciliations, etc.Splits by event are shown as latest reported, i.e. could be from Q1, Q2, Q3 or FY 2011 results. Some Thai flood loss estimates are from preliminary announcementsAll losses are assumed pre-taxAll losses are net of reinstatement premiums except for Validus and ACEAll losses converted to USD at 2011 full year average FX ratesUS tornadoes includes Hurricane Irene for Argo, Ariel and NovaeSource: Individual company reports, Aon Benfield Analytics

The impact of the 2011 catastrophes varied widely by reinsurer Catastrophe losses in Q1 2012 were significantly less than in 2011; 2012 has resulted in

approximately USD10 billion in economic loss and nearly USD3 billion in insured loss compared to USD270 billion in economic loss in Q1 2011 and almost USD53 billion in insured loss

49%

38%

30%

27%25% 25% 24% 23%

22%21% 20% 20%

20%20% 20%

17% 17% 17% 16% 16% 16% 15% 15% 15%13% 13% 13%

12% 12%

9% 9% 9%7%

6%

4%2%

1%

-5%

5%

15%

25%

35%

45%

Adjustments / Other*

Thai Floods

Hurricane Irene

US Tornadoes

Japan Earthquake & Tsunami

New Zealand Earthquakes

Australia

17Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Timeline of 2011 Industry Events

Source: Aon Benfield Analytics

2011 was an eventful year with elevated catastrophe losses, volatile stock market conditions, record low investment yields and downgrade of U.S. debt and the European sovereign debt crisis

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Joplin Tornado Outbreak ~

$6.5B

Winter storms hit Midwest & Northeast

~ $1.0B

Birmingham Tornado Outbreak ~ $7.3B

Hurricane Irene ~ $4.3B

TX Wildfires ~ $.5B

A.M. Best places 6 Euro groups

"under review"

S&P warns of downgrades for 15 Euro nations

Snowstorm hits northeast

~ $.6B

10yr Treasury yield hits historical low

(1.72%)

S&P 500 down 19% from 2011

peak

S&P downgrades US

debt

Japan Earthquake and Tsunami

~ $23.5B

New Zealand Earthquake ~ $13.5B

Thailand Floods ~ $10B

18Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Lessons Learned from Observed Events

Source: Aon Benfield Analytics

Loss events in 2011 brought interesting tests of coverage, deductibles, policyholder co-participations and government / private insurer partnerships

Event Issue Observed Event Coverage Issues to ConsiderJapan Earthquake and Tsunami

Overwhelming debris created by tsunami

No coverage for debris removal by Japanese insurers

Large scale debris removal operations in many nations will require a coordination of the insurance policy coverage for debris with the need for extensive government involvement in the debris removal process.

Minority of homes and businesses purchased earthquake insurance

Banks do not require earthquake insurance in Japan

The impact on communities that did not have sufficient insurance was clear in New Orleans after Hurricane Katrina and it is clearly going to be an issue in Japan. Insurers and reinsurers have capacity to provide more coverage should governments recognize the inadequacy of banking policies. These policies place undue catastrophe burdens on financial systems and consequently destroy communities when the known catastrophic risks eventually occur.

50% co-participations for all homeowners

Coverage for earthquake in Japan is viewed as financial assistance after an event rather than indemnity coverage

While a 50% co-participation is substantially larger than the deductibles in place in most other nations there appear to be no signs of policyholder unrest with this form of coverage. Would co-participations be more useful to policyholders than large deductibles? Would insurance take-up rates improve if co-participations were used rather than deductibles?

New Zealand Earthquake and Liquefaction

Severe liquefaction combined with low levels of shake related damage to homes and businesses

Government underlying and private insurer excess coverage combine to insure homes and businesses

Liquefaction can affect very large areas and the decisions about relocating homes and businesses are made by governments, not private insurers. Insurers may need to reconsider whether excess coverage can include coverage for government requirements to relocate homes.

United States Tornado and Hail Missouri and Alabama

Nature's most powerful winds affecting high concentrations of insured values

Tornado and hail losses are covered under substantially all property policies

Very high level of damage can occur as a percentage of total insured values. Some of the highest levels of insured damage to insured values ever observed in tornado and hail losses occurred in these events. Concentration risk is real everywhere. Some of the debris removal coordination issues mentioned above were also revealed in these events.

United States Hurricane Irene

Non-uniform deductibles required or allowed in multiple states affected by the same event

Varying deductibles state to state and coastal versus inland in the same state

Consistency of deductibles may be more important than previously considered and the pressure from individual state insurance regulators for extra contractual allowances to policyholders may have been underappreciated.

19Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Impact of 2011 Cat losses

Economic losses of USD438bn made 2011 the costliest natural disaster year on record

Insured losses of USD112bn are second only to 2005’s USD120bn (KRW: USD90bn)

Reinsurers’ assumed losses in 2010/2011 are now likely to exceed those in 2004/2005

Compared with 2005

– industry capital is much stronger (near peak levels)

– risk modelling is much improved

– risk management is more robust

– risk tolerance is generally lower

Capital has been impacted but

– widespread capital raising is not required

– total capitalisation remains high

– the rating impact has been limited

20Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Financial strength ratings: negative action

Source: A.M. Best, S&P (ratings as at April 11, , 2012)

Allianz SE A+ Stable A+ Watch Neg AA Stable AA Negative

Ariel Reinsurance Co. Ltd. A- Stable A- Stable NR NR NR Withdrawn

Asia Capital Reinsurance Group Pte Ltd. A- Stable A- Stable A- Stable A- Negative

Caisse Centrale de Reassurance A++ Stable A++ Negative AAA Stable AA+ Negative

Flagstone Reassurance Suisse SA A- Stable A- Negative NR NR NR NR

General Reinsurance Corp. A++ Stable A++ Stable AA+ Stable AA+ Negative

Labuan Reinsurance (L) Ltd A- Stable A- Watch Neg - - - -

Mapfre Re, Compania de Reaseguros, S.A. A Stable A Watch Neg AA Negative A Negative

MS Frontier Reinsurance Ltd. A Stable A Stable AA- Stable A+ Stable

National Indemnity Co. A++ Stable A++ Stable AA+ Stable AA+ Negative

Partner Reinsurance Co. Ltd. A+ Stable A+ Negative AA- Negative A+ Stable

Platinum Underwriters Bermuda Ltd. A Stable A Stable A Stable A- Stable

Sompo Japan Insurance Inc. A+ Stable A+ Stable AA- Stable A+ Stable

Thai Reinsurance Public Co. Ltd. NR NR A- Stable BBB+ Stable

Toa Reinsurance Co. A+ Stable A+ Watch Neg A+ Stable A+ Stable

Main Operating CompanyA.M. Best S&P

January 1, 2011 Current January 1, 2011 Current

21Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

Financial strength ratings: positive action

Allied World Assurance Co. Ltd. A Stable A Stable A- Positive A Stable

Arch Reinsurance Ltd. A Stable A+ Stable A+ Stable A+ Stable

AXIS Specialty Ltd. A Stable A Positive A+ Stable A+ Stable

Lancashire Insurance Co. Ltd. A- Positive A Stable A- Stable A- Stable

Montpelier Reinsurance Ltd. A- Stable A- Positive A- Stable A- Stable

Odyssey Reinsurance Co. A Stable A Stable A- Stable A- Positive

Swiss Reinsurance Co. Ltd. A Positive A+ Stable A+ Positive AA- Stable

Validus Reinsurance Ltd A- Positive A Stable A- Stable A- Stable

Mixed Messages

Alterra Bermuda Ltd. A Stable A Negative A- Positive A Stable

Tokio Millennium Re Ltd. A+ Stable A++ Stable AA Negative AA- Negative

S&P

January 1, 2011 Current January 1, 2011 Current

Main Operating Company

Main Operating Company

A.M. Best S&PJanuary 1, 2011 Current January 1, 2011 Current

A.M. Best

Source: A.M. Best, S&P (ratings as at April 11, , 2012)

22Aon Benfield Analytics | Reinsurance Market Outlook, April 2012

January 2012 Property Catastrophe Renewals Recap

Results are summarized for contracts that did not cede material losses to the expiring reinsurance program. Rate changes are based on exposure neutral pricing and measured from the expiring January 2011 terms. Source: Aon Benfield Analytics

ROL Change Capacity Change Retention Change

U.S. (accounts with Loss) +5% to +40% Stable to -5% Stable to +5%

U.S. +5% to +10% Stable to -5% Stable to +5%

ROL Change Capacity Change Retention Change

Asia PacificAustralia +40% to +75% Stable Stable to +25%China +10% to +20% Stable +10% to +15%

Hong Kong +10% -30% to -40% Stable

Indonesia -5% to +5% Stable Stable

Malaysia +5% to +10% -5% to Stable Stable

Pakistan +5% to +10% Stable Stable

Philippines +5% to +10% Stable Stable

Singapore Flat Stable Stable

Taiwan +5% to +25% -5% to -10% Stable to +5%

Thailand +100% to +600% +20% to +50% +10% to +100%

EMEANorthern (wind dominating) Flat to +5% Stable to +2.5% Flat

Southern (quake dominating) Flat to +10% Stable Flat

Americas – Non U.S.Chile Flat Stable Stable

Canada +5% to +15% -5% to-10% +5% to +15%

Brazil Flat Abundant Stable

South Africa +10% to +25% Stable Varies

U.S. Property Catastrophe January 1, 2012 Recap

Rest of the World: Property Catastrophe January 1, 2012 Recap

Aon Benfield · Vaclavske namesti 19 · 110 00 Prague 1 · Czech Republic

www.aonbenfield.com

Published by Aon Limited trading as Aon BenfieldRegistered office: 8 Devonshire Square, London EC2M 4PL.

Aon Limited is authorised and regulated by the Financial Services Authority in respect of insurance mediation activities only.