Embed Size (px)

Citation preview

COMPANY NAME : Banque de l’Habitat

HEAD OFFICE ADDRESS : 18, avenue Mohamed V 1080 Tunis

BOX OFFICE : 242 Cédex 1080

PHONE : +216 71 126 000

FAX : +216 71 337 957

SWIFT ADDRESS : BHBKTNTT

E-MAIL : [email protected]

WEBSITE : www.bh.com.tn

CALL CENTER : 1800 (from abroad : +216 71 001 800)

VOCAL SERVER : 88 401 421

BH SMS : 87 987

CAPITAL : 90 000 000 dinars

Quantity Amount : TD Percentage

Tunisian State 5 872 427 29 362 135 32.62%

Public 4 140 571 20 702 855 23.00%

Para public 255 306 1 276 530 1.42%

Private business 1 387 401 6 937 005 7.71%

Private individuals 4 485 283 22 426 415 24.92%

Foreigners 1 852 446 9 262 230 10.29%

Staff 5 826 29 130 0.03%

Free unconfirmed 740 3 700 0.004%

Total 18 000 000 90 000 000 100.00%

generalpresentation on the BH

PAGE 02

Structure of the capital as of 31/12/2010

banque de l’habitat • ANNUAL REPORT 2010

PAGE 03

SUMMARY

PAGE 04

08

16

46

1 0

24

Speech of the Chairman and Managing Director

National economic situation

Assessment of undertaken actions in 2010

International environment

The activities of the Bank

banque de l’habitat • ANNUAL REPORT 2010

PAGE 05

54

76

102

58

86

Future prospects

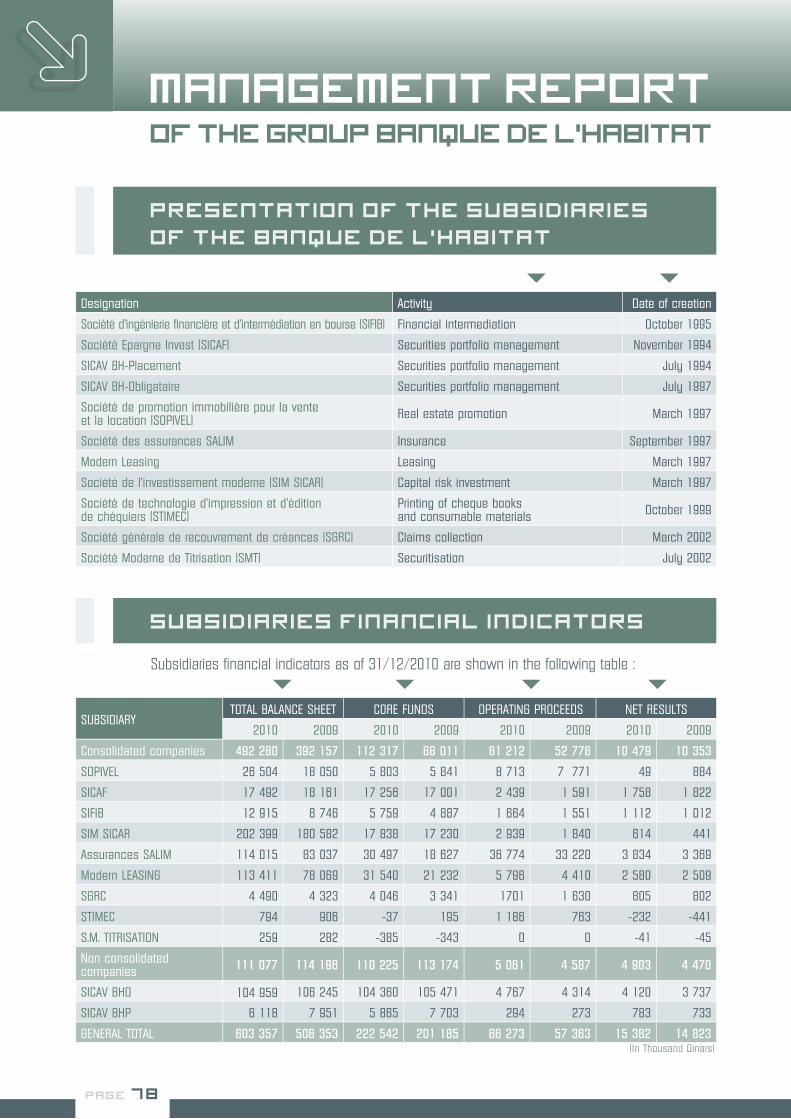

Management report of the Group Banque de l’Habitat

Resolutions

Financial statements

Consolidated financial statements

executive board

PAGE 06

Public sector

Mr Brahim HAJJI

Chairman and Managing Director

Mrs Fawzia Moussa SAAYID

Director representing the State

Mrs Souhir TAKTAK

Director respresenting the State

Mr Jalel CHOUIHI

Director representing the State

Mr Habib TOUMI

Director representing the State

Mr Ettajouri FATNASSI

Director representing the State

banque de l’habitat • ANNUAL REPORT 2010

PAGE 07

Private sector

Mr Ahmed TRABELSI

Mr Mohamed Sadok DRISS

Mr Rached EL HORCHANI

Mr Mohamed Taoufik DRISS

General Manager Assistant in

charge of facility management

Mr Adel ZARROUK

Mr Néjib

BEN Laaroussi MARZOUGUI

Mr Mahmoud

Montacer MANSOUR

State Controller

Mr Chihab GHANMI

Auditor

Mr Cherif BEN ZINA

Auditor

SPEECHOF THE CHAIRMAN

AND MANAGING DIRECTOR

Ladies and gentlemen shareholders,

I have the honor of presenting to you the annual report of the Bank’s activity as well as the financial statements and the main indicators trends during the fiscal year 2010.

Dear shareholders,

Dignity and freedom are universal values appreciated at the expense of priceless sacrifices. The Tunisian people and the youth offered them to Tunisia on January 14, 2011 our revolution day, May God all the mighty award to our martyrs his infinite forgiveness and may this revolution offer a better future to our youth and people.

Though the events that accompanied the 14 January revolution concern the year 2011, the fiscal year 2010 has been affected by the classification of the commitments of the deposed president. In effect, the Bank in a reasoning of preventing and preserving its financial balances and its shareholders, customers and staff interests constituted sound additional provisions.

Had it not been for this special circumstance, the Bank net result would have been at the expected level and we are confident in your comprehension and support in this exceptional situation.

At the level of risks management, the Bank proceeded during 2010 to the setting up of a set of measures related to the standardization of concepts tied to risks in order to control them in their different aspects: credit, rate, liquidity… thanks to committees that see to the good governance of these new practices.

At the activity level, the Bank’s results are satisfying on the whole. In effect, the year 2010 was marked by the 118.8 MTD (+2.3%) assets progress rising to 5 295.7 MTD, the increase in financing the economy by 527.6 MTD (+12.7%) and the raising of additional resources of 162.8 MTD (+3.3%).

Customers depos i ts were marked by an inc rease o f 1 08 .8 MTD (+3 .3%) to amount to 3 363.9 MTD.

As far as uses are concerned, the Bank managed during 2010 to maintain the revival of real estate activity achieving one of its strategic objectives namely the recovery of its market share in this activity sector. In effect, real estate loans to property providers went up by 98.4 MTD (+30.2%). Concurrently, the Bank continued to consolidate its core trade, buyers loans, in spite of increased competition in this field.

Totaling 3 680.4 MTD as of 31/12/2010 vs. 3 342.5 MTD a year before, productive claims went up by 437.9 MTD.

As for classified claims, they accounted for 10.8% of total loans and were covered at 68.9% by provisions and reserved charges.

PAGE 08

banque de l’habitat • ANNUAL REPORT 2010

Concerning operating results, net banking proceed came in at 194.6 MTD and operating gross result at 128.3 MTD, up respectively by 8.1 MTD (+4.4%) and 5.1 MTD (+4.1%). Net result of the fiscal year amounted to 32.6 MTD as of 31/12/2010.

As for regulatory ratios, the liquidity ratio and the solvency ratio reached respectively 111.94% and 9.95% at the end of 2010.

Concerning the group BH, the different subsidiaries of the Bank registered satisfying results on the whole helping to register a group’s net profit of 38.3 MTD at the end of the fiscal year 2010.

On the other hand, the Bank undertook several actions dealing with improvements in files processing delays and services quality; these measures dealt with sales points organizational procedures and the setting up of controller position.

Concerned with offering better quality services and in order to be close to its customers, the Bank extended branches network to 93 through the opening of 4 new sales points in Rawabi Bizerte, Moulares, Korba and northern urban zone.

As for prospects, the Bank intends to pursue its development process during 2011 by seeing to consolidating and preserving its financial balances and a better appropriateness between uses and resources. In effect, the Bank views to issue a 150 MTD debenture loan at conditions that will be set later taking into account the trends in financial market situation.

Thus, the Bank will strive to reinforce its information system through notably the system of exchanging information with the Central Bank, the system of combating money laundering and all mechanisms likely to reinforce surveillance and reduce risks in particular those related to daily operations and transactions and new products and services development…

Finally, I would like to take this opportunity to express my most profound thanks to the Bank’s staff for their effort and the spirit of enterprise that they showed; I also express my gratitude to the members of the executive board for their contribution to ensure the good governance of the Bank and our kind clientele for their loyalty.

PAGE 09

PAGE 11

INTERNATIONAL

ENVIRONMENT

World economic activity progress came in at around 5% in 2010, showing that world economy

recovered from financial crisis effects.

Should many countries overcome economic difficulties, it should be outlined that not all of them

are shielded from a possible shock. It is the case for most developed countries : some of them are facing

high levels of unemployment and others trade and / or budget imbalances.

In the United States , annual economic activity would register a 2.9% growth in 2010. In 2010

last quarter its GDP progressed by 3.2% vs. 2.6% in the third quarter. This performance is tied to household

consumption which went up by 4.4% and investments in facilities and softwares (+ 5.8%).

In 2010 second half, the euro zone experienced turbulences linked to countries indebtedness

crisis such as Greece, Ireland and at a lesser extent Spain and Portugal. This situation has an impact on this

zone growth level which would come in at 1.8%. As for emerging countries such as China, India and Brazil ,

they keep on registering a sound growth between 7.5% and 10.3%.

Japan found its growth path again 4.3% in 2010 after experiencing one of its serious recessions

in 2009 (-6.3%). This country’s exports soared in 2010 second half particularly in December 2010 (+5.7%).

Concurrently, it should be noted a decrease in imports because of domestic demand drop.

In emerging countries , economic activity was sound throughout 2010. The Chinese economy

was the strongest with a growth rate of 10.3% vs. 9.2% in 2009. It took advantage of an increasing

international demand and a growing domestic demand.

India , Asia’s third economic power would register a 9.7% growth rate in 2010.

INTERNATIONALENVIRONMENT

PAGE 12

World growth

INTERNATIONAL ENVIRONMENT • ANNUAL REPORT 2010

PAGE 13

At the end of 2010, commodities international prices registered an increase for most foodstuffs

under the effect notably of unfavorable climatic conditions having affected many agricultural crops such as

cereals in many producing countries like Brazil , Australia and China. In particular, prices rise reached at

the end of 2010 compared to the end of the previous year 46.2% for wheat and 18.9% for sugar against

20.1% and 2.2% respectively at the end of November. Also, industrial raw materials kept on increasing

reaching at the same date 89.4% for cotton and 32.6% for copper against 80.4% and 14% at end November.

On the other hand, crude oil prices have exceeded 90 dollars the barrel since the beginning of

December 2010 along with world demand revival, stocks decrease and the ongoing cold wave that hit

the United States and Europe. Thus, the barrel price amounted at the end 2010 to 94.75 dollars for the Brent

and 91.38 dollars for American light oil that is an increase by 21.6% and 15.1% respectively compared to the

end of the previous year.

As far as inflation is concerned, consumer prices registered some acceleration during December

2010 in the main industrialized countries following notably an increase in energy prices. In terms of annual

slide, inflation rate reached 1.5% in the United States vs. 1.1% the previous month and 2.2% in the Euro

zone vs. 1.9%.

As for unemployment, employment situation registered some improvement in industrial countries

with an unemployment rate regressing to 9.4% in the United States in December 2010 vs. 9.8% the previous

month. Moreover, the unemployment rate stabilized at 10.1% in November of the same year in the Euro zone

and at 5.1% in Japan.

Inflation

Employment

Commodities world market

Foreign Exchange markets and

monetary policies

On international foreign exchange markets , the euro decreased against the dollar in 2010 mainly

because of the fallouts of sovereign debt crisis in some European countries and the risks of its spread

to other countries of the Euro zone. The European currency ended the year 2010 at 1.3386 dollar registering

a drop by 6.6% against the dollar from the end of a year to another.

On the contrary, the yen appreciated in 2010 against the dollar taking advantage of its choice as

a safe currency by investors against turmoils experienced by international financial markets following notably

sovereign debt crisis. Then it reached at the end of the year 80.915 yens for a dollar, a 13.1% appreciation

from one end of the year to another.

On the other hand, Central banks in many industrialised countries have kept on softening

their monetary policies during 2010 through notably non conventional measures in the form of programmes

of assets purchase such as treasury bonds and treasury bills following the example of the American Federal

Reserve and the Bank of Japan which intervened for respective amounts of 600 billion dollars

and 5 000 billion yens (about 43 billion Euros). On the other hand, central banks in some industrialised

countries and emerging countries have started to apply restrictive monetary policies to lighten pressures on

the economy. In particular the Bank of China rose its key interest rate twice during 2010 and six times

the rate of reserve requirements in the same year.

INTERNATIONALENVIRONMENT

INTERNATIONAL ENVIRONMENT • ANNUAL REPORT 2010

PAGE 14 PAGE 15

International stock markets indexes

INTERNATIONALENVIRONMENT

INTERNATIONAL ENVIRONMENT • ANNUAL REPORT 2010

PAGE 14 PAGE 15

On another level, the trend of main international stock markets diverged during 2010. In particular,

the American stock market registered positive results taking advantage of important interventions

of the Federal Reserve to support the economy revival and the improvement in economic indicators

in the United States at the end of the year. In this context, the Dow Jones and Nasdaq went up respectively

by 11% and 16.9% from one end of the year to another.

On the contrary, many European stock markets registered a decrease because of sovereign debt

crisis. The CAC 40 in particular went down by 3.3% between end 2009 and end 2010. Also, Tokyo stock

market recorded a decrease under the effect of the yen’s appreciation which affected exports

and consequently the financial results of Japanese businesses. The Nikkei drop reached 3.3% from one end

of year to another.

PAGE 17

NATIONAL ECONOMIC

SITUATION

NATIONALECONOMIC SITUATION

NATIONAL ECONOMIC SITUATION • ANNUAL REPORT 2010

PAGE 18 PAGE 19

The Tunisian economy recorded satisfying results on the whole during 2010 and was able

to register an improvement compared to the previous year. Thus, and in spite of a relatively modest agricultural

campaign, these results have been obtained thanks to production progress the trend in some manufacturing

industries activities notably with world economic growth revival and a slight increase in tourism and transport

sectors.

In 2010, the agricultural sector registered a decrease in its added value estimated at 8.8%

in constant prices against a 6% progress in 2009 following notably a regress in cereals and olive oil

productions.

In effect, cereals production of the 2009-2010 campaign came in at 10.8 million quintals against

25.3 million in 2008 - 2009 campaign.

As for olive oil production of 2010 – 2011 campaign, it is estimated at 120 thousand tonnes

against 150 thousand tonnes in the previous campaign.

However, dates and citrus fruits productions went up respectively by 7.4% and 13.9% compared

to the previous campaign reaching 174 and 352 thousand tonnes.

As for the sector of breeding, fresh milk production progressed by 2.3% in 2010 which helped

increase collected quantities intended to dairy industry.

Economic growth rate came in at 3.8% in 2010 against 3.1% in the previous year.

This progress is ascribable to the recovery in manufacturing industries thanks to the net

improvement in external demand. Like mechanical and electrical industries, the service sector was also

characterized by a positive trend of indicators pertaining to tourism and air transport activities.

Growth

Agriculture and Fishing

NATIONALECONOMIC SITUATION

NATIONAL ECONOMIC SITUATION • ANNUAL REPORT 2010

PAGE 18 PAGE 19

Concerning the sector of fish and fish farming , the production stabilized during the first eleven

months of 2010 at the level of the same period in 2009 that is 93 thousand tonnes.

On the level of trade transactions of agricultural and food products with abroad, cereals imports

went up by about 65% in quantity in 2010 and by 78% in value reaching 3 234 thousand tonnes for a value

of 1 087 MTD following the decrease in production and prices increase on world market.

As for exports, olive oil exported quantities reached 110 thousand tonnes in 2010 for a value

of 444 MTD against about 142 thousand tonnes and 533 MTD the previous year.

Concerning dates , their exports have reached since the beginning of the current trading campaign

and till January 24, 2011, a level similar to the one registered during the same period of the previous

campaign that is about 25 thousand tonnes. These exports value rose by 3.7% reaching 85 MTD following

an improvement in prices average level.

Sea products exports went up by 3.7% in quantity in 2010 and by 1.6% in value to reach about

17 thousand tonnes and 185 MTD.

Thus, the food trade balance showed a deficit of about 557 MTD in 2010 against a 38 MTD

surplus the year before because of imports increase by 38.6% against exports slight increase by 1.2%.

It resulted a decrease in the rate of coverage of food products imports by exports which

regressed from 102.4% to 74.8% from one year to another.

NATIONALECONOMIC SITUATION

NATIONAL ECONOMIC SITUATION • ANNUAL REPORT 2010

PAGE 20 PAGE 21

During 2010, industrial production general index rose by 7.8% against a 4.5% decrease

the previous year following production revival in the manufacturing industries (9.3% vs. -6% a year earlier) as

well as in mining sector (15.4% vs. -2.8%) while production registered a virtual stagnation in energy sector

(0.6% vs. 1.7% a year earlier) .

Manufacturing industries production progress concerned all sectors in particular mechanical

and electrical industries (25.2% vs. -8.3% in 2009) and chemical industries (6.9% vs. 2.3%) which took

advantage of external demand rise. Also, the production in the sector of textile, clothing, leather, and footwear

went up by 4.2% against a 14.8% decrease a year earlier.

As for trade transactions with abroad, manufacturing industries exports other than foodstuffs

registered a net revival in 2010 (22.1% vs. - 13.4% the year before).

Also, chemical industries exports registered a revival (23.1% vs. -43% a year earlier) following

essentially phosphate by products exports revival and prices rise on world market.

Concerning clothing and textile sector exports , they progressed by 6.8% vs. a 8.7% drop

in 2009 along with the sector progressive activity revival.

Energy sector trade balance showed a deficit of 484 MTD vs. a 152 MTD deficit a year earlier

because of imports which exceeded exports notably for oil products along with prices rise on world markets

and the break in Bizerte refinery.

Industrial activity

During 2010, passengers air traffic rose by 5.5% after regressing by 5.4% in the previous year

to amount to 11.2 million passengers. This trend concerned international flights (5.4% against a drop

at the same rate in 2009), notably regular flights (12.2%) as well as domestic flights (9.8%).

In terms of trade transactions with abroad, exports and imports went up respectively by 20.8%

and 23% during 2010 against respective drops of 17.6% and 14.4% in 2009 which meant a widening

of the trade deficit by 1 889.7 MTD and a decrease in the coverage rate which went down from 75.2%

to 73.9% from one period to another.

Current deficit accounted for 4.8% of GDP in 2010 against 2.8% in 2009.

Net assets in foreign currencies amounted to 13 003 MTD at end 2010 corresponding to

147 days of imports against 13 353 MTD and 186 days at the same date in 2009.

NATIONALECONOMIC SITUATION

NATIONAL ECONOMIC SITUATION • ANNUAL REPORT 2010

PAGE 20 PAGE 21

The number of foreign tourists stagnated in 2010 after decreasing by 2.1% the previous year

reaching 6.9 million tourists. This situation is explained by the regress in Maghreb tourists flows (-2.4%) while

the number of European tourists went up by (1.9% vs. an 8.8% decrease a year earlier) .

On the other hand, overall tourist bednights rose by 4.3% in 2010 against a 9.2% drop a year

earlier to reach 36.2 million units.

As for the occupancy rate of used accommodation capacity , it came in at 50.3% and varied

between 17.5% in the zone of Gabès and 60.3% in the one of Djerba-Zarzis.

Regarding tourism earnings in foreign currencies in 2010, they rose by 1.2% (-1.2% excluding

foreign exchange effect) against a 2.4% progress the previous year reaching 3513 MTD which accounts

for about 10% of current receipts of the balance of payments against 11.6% in 2009.

Tourism activity

Air transport

External trade

NATIONALECONOMIC SITUATION

NATIONAL ECONOMIC SITUATION • ANNUAL REPORT 2010

PAGE 22 PAGE 23

The increase in the supply of banks the liquidity of which is in excess and more important than

the one of banks showing a deficit during the last quarter of 2010, meant a decrease in banks needs

in liquidity on the money market.

The year 2010 was also characterized by :

• An increase in money supply M3 by 11.1% vs. 13% in 2009.

• The decrease in net claims on abroad by 482 MTD compared to their level of the previous year

reflecting essentially the shrinking in net assets in foreign currencies (-350 MTD).

• The decrease in net claims on the State by 168 MTD against a 953 MTD increase a year before

under the effect mainly of the decrease in the outstanding balance of treasury bonds in banks portfolio

(-111 MTD) and the increase in treasury current account balance (+ 209 MTD).

• The performance of financing the economy (19.2% or 6 934 MTD) against (10.3% or 3 371 MTD)

during the previous fiscal year. This increase reflects the one of loans granted on ordinary resources (20.6%

vs. 11%). However, the outstanding balance of loans on special resources kept on decreasing but at a lesser

pace than the one of the previous year (-1% vs. -3.3%).

• At the end of 2010 and compared to its level at end 2009, the rate of the dinar on interbank

market registered a respective decrease by 19.4% against the Japanese yen, 8.4% against the American

dollar, 2.3% against the Moroccan dirham but a virtual stability against the euro (-1.2%).

Monetary policy

The inflation rate came in at 4.4% during 2010 against 3.5% in 2009.

This is ascribable essentially to the rise in imported products world prices mainly foodstuffs

and energy in addition to the impact of foreign exchange rate fluctuations and in particular the euro

appreciation against the Tunisian dinar.

It should be mentioned that the increase in consumer prices general index has been slowering

from one month to another compared to the start of the previous year going down from a 4.9% peak

in February 2010 to 4.4% in December 2010.

INFLATION

NATIONALECONOMIC SITUATION

NATIONAL ECONOMIC SITUATION • ANNUAL REPORT 2010

PAGE 22 PAGE 23

Tunis stock market ended 2010 with a Tunindex annual yield of 19% vs. 48.4% a year before

registering its eighth increase in a row. It should be mentioned that the last quarter was characterized

by a drop in transactions following the announcement of taxing added values on stock markets.

Stock market indexes have been as follows :

• Tunindex capitalization index ended the year 2010 on 19.1% profit at 5 681.39 points against

4 291.72 points; a satisfying performance compared to the record yield of 48.4% registered a year earlier.

• Stock market capitalization came in at 15 282 MTD at end 2010 against 12 227 MTD in 2009,

a 25% increase compared to its 2009 level.

This increase is the combined effect of a record number of introductions on the stock market

(5 companies: Salim, Tunis Re, Carthage Cement, Ennakl and Modern Leasing) bringing the number of listed

companies to 56 and the four capital increase of listed companies.

• Annual transactions on the cotation reached 2 702 MTD against 1 814 MTD during 2009,

a 49% increase showing an improvement in liquidity with a daily average volume of 10.4 MTD against

6.8 MTD a year before.

This dynamism is due to investors infatuation for newly introduced securities and some financial

securities which captured about 50% of transactions overall volume.

• Annual yields of sector related indexes were positive except for the index “services

to consumers” (-0.01% vs. +60.8% in 2009) led by the decrease in the security “Tunisair” (-18.9%).

These positive yields varied between 3.2% for the index “Distribution” and 38.6% for the index

“financial services” with an increase in the index “Tunbank” of 19.6% against 49.7% in 2009.

• Foreign investors share in stock market capitalization came in at 20.16% at end December

2010 against 21.92% in 2009 and against 19.97% in September 2010, an increase ascribable

to the comeback of these investors to the Tunisian market for a 22 MTD balance on the stock market cotation

(that is purchases for 71 MTD and sales for 49 MTD).

It should be noted that “Modern Leasing” security newly introduced at end 2010 registered

the highest increase of the year that is 40.8%.

Financial market

THE ACTIVITIES

OF THE BANK

PAGE 25

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 26 PAGE 27

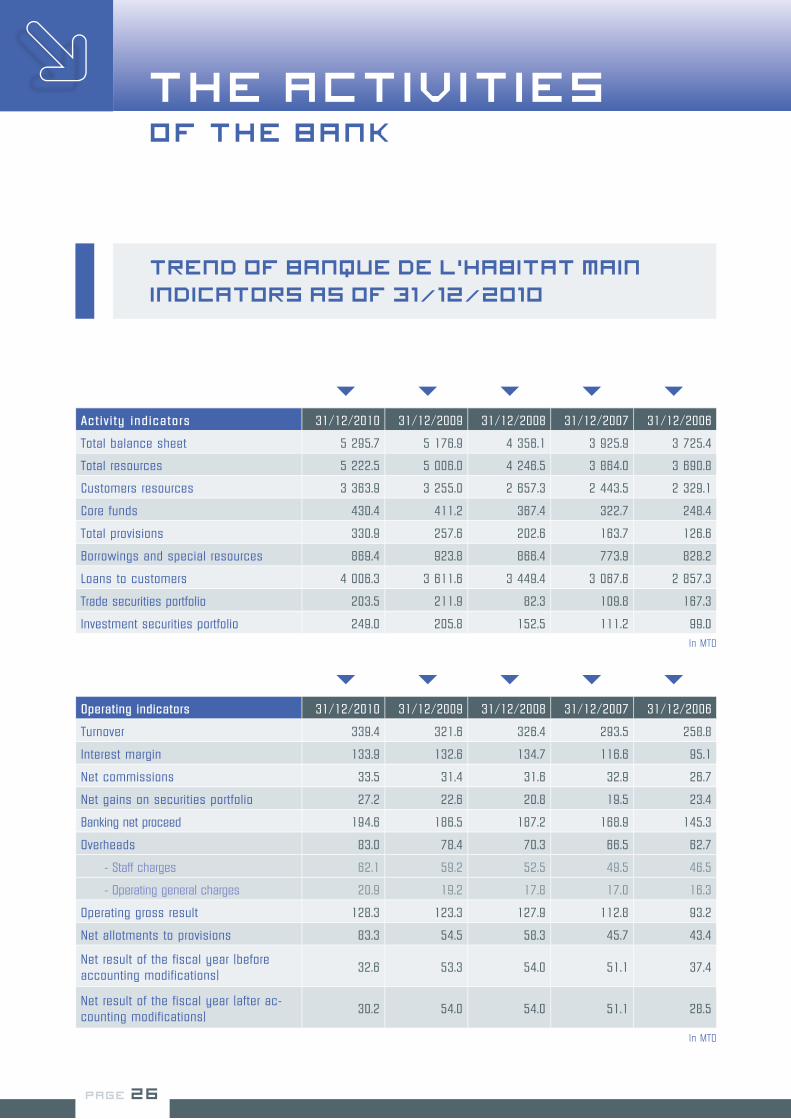

Act i v i ty ind ica to rs 31/12/2010 31/12/2009 31/12/2008 31/12/2007 31/12/2006

Total balance sheet 5 295.7 5 176.9 4 356.1 3 925.9 3 725.4

Total resources 5 222.5 5 006.0 4 246.5 3 864.0 3 690.8

Customers resources 3 363.9 3 255.0 2 657.3 2 443.5 2 329.1

Core funds 430.4 411.2 367.4 322.7 248.4

Total provisions 330.9 257.6 202.6 163.7 126.6

Borrowings and special resources 869.4 923.8 866.4 773.9 828.2

Loans to customers 4 006.3 3 611.6 3 449.4 3 067.6 2 857.3

Trade securities portfolio 203.5 211.9 82.3 109.8 167.3

Investment securities portfolio 249.0 205.8 152.5 111.2 99.0

Operating indicators 31/12/2010 31/12/2009 31/12/2008 31/12/2007 31/12/2006

Turnover 339.4 321.6 326.4 293.5 258.8

Interest margin 133.9 132.6 134.7 116.6 95.1

Net commissions 33.5 31.4 31.6 32.9 26.7

Net gains on securities portfolio 27.2 22.6 20.8 19.5 23.4

Banking net proceed 194.6 186.5 187.2 168.9 145.3

Overheads 83.0 78.4 70.3 66.5 62.7

- Staff charges 62.1 59.2 52.5 49.5 46.5

- Operating general charges 20.9 19.2 17.8 17.0 16.3

Operating gross result 128.3 123.3 127.9 112.8 93.2

Net allotments to provisions 83.3 54.5 58.3 45.7 43.4

Net result of the fiscal year (before accounting modifications)

32.6 53.3 54.0 51.1 37.4

Net result of the fiscal year (after ac-counting modifications)

30.2 54.0 54.0 51.1 28.5

Trend of Banque de l’Habitat main

indicators as of 31/12/2010

In MTD

In MTD

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 26 PAGE 27

Rat ios 31/12/2010 31/12/2009 31/12/2008 31/12/2007 31/12/2006

• PROFITABILITY RATIOS

Net profit / Core funds (ROE) 7.57% 12.95% 14.70% 15.85% 11.47%

Net profit / Total assets (ROA) 0.62% 1.03% 1.24% 1.30% 0.76%

Banking Net proceeds / Total balance sheet

3.68% 3.60% 4.30% 4.30% 3.90%

Banking Net proceeds / turnover 57.34% 57.99% 57.34% 57.57% 56.12%

Banking Net proceeds / Total loans 4.86% 5.16% 5.43% 5.51% 5.08%

• OPERATING RATIOS

Encashed commissions / staff costs 63.00% 59.20% 66.68% 71.38% 62.33%

Operating ratios(Overheads / Banking net proceeds)

42.63% 42.03% 37.57% 39.38% 43.18%

Net commissions / Banking net proceeds

17.19% 16.81% 16.88% 19.45% 18.39%

Staff costs / Banking net proceeds 31.91% 31.74% 28.07% 29.31% 31.99%

• STRUCTURE RATIOS

Loans to customers/ Deposits to customers 119.10% 110.95% 129.81% 125.54% 122.68%

• REGULATORY RATIOS

Cooke ratio 9.95% 10.16% 10.44% 11.36% 8.17%

Liquidity ratio 111.94% 129.55% 114.06% 115.0% 123.13%

• NPL COVERAGE 68.9% 70.0% 63.5% 72.3% 71.2%

NPL / Total commitments 10.8% 8.7% 8.3% 7.3% 7.7%

Resources costs 3.27% 3.46% 4.15% 4.11% 4.0%

Uses yield 6.08% 6.48% 7.49% 7.17% 6.9%

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 28 PAGE 29

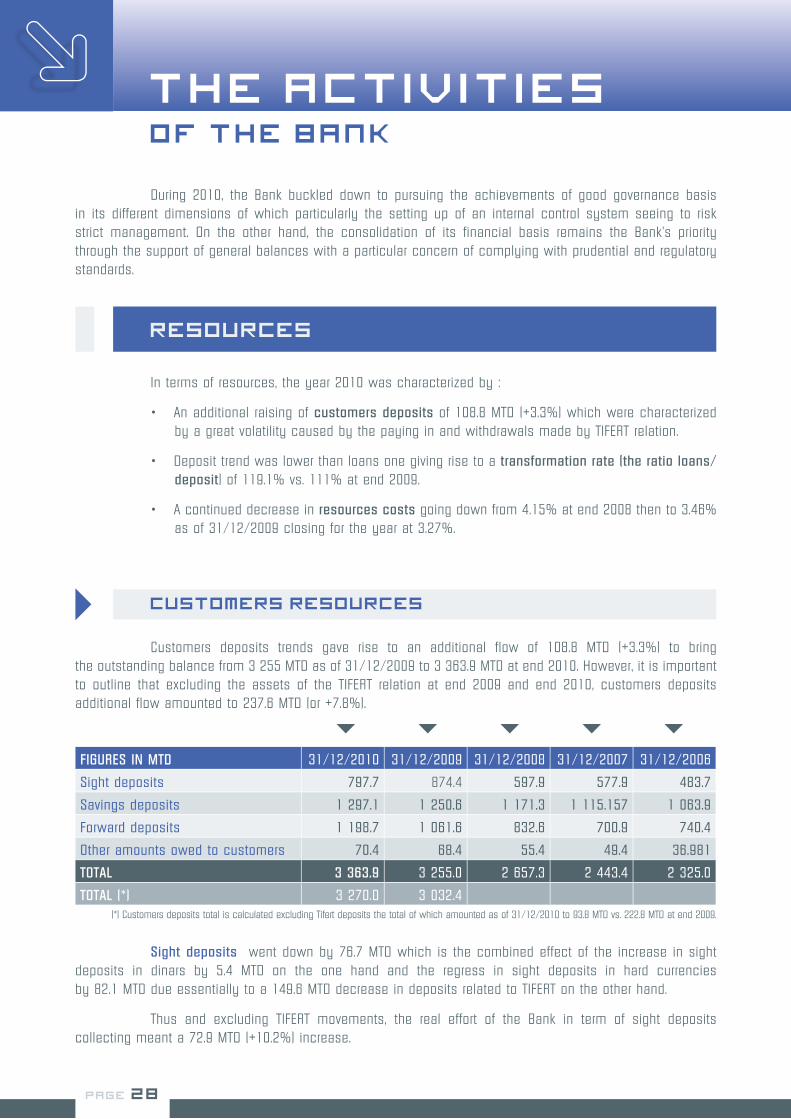

In terms of resources, the year 2010 was characterized by :

An additional raising of • customers deposits of 108.8 MTD (+3.3%) which were characterized by a great volatility caused by the paying in and withdrawals made by TIFERT relation.

Deposit trend was lower than loans one giving rise to a • transformation rate (the ratio loans/ deposit) of 119.1% vs. 111% at end 2009.

A continued decrease in • resources costs going down from 4.15% at end 2008 then to 3.46% as of 31/12/2009 closing for the year at 3.27%.

Resources

Customers deposits trends gave rise to an additional flow of 108.8 MTD (+3.3%) to bring the outstanding balance from 3 255 MTD as of 31/12/2009 to 3 363.9 MTD at end 2010. However, it is important to outline that excluding the assets of the TIFERT relation at end 2009 and end 2010, customers deposits additional flow amounted to 237.6 MTD (or +7.8%).

Sight deposits went down by 76.7 MTD which is the combined effect of the increase in sight deposits in dinars by 5.4 MTD on the one hand and the regress in sight deposits in hard currencies by 82.1 MTD due essentially to a 149.6 MTD decrease in deposits related to TIFERT on the other hand.

Thus and excluding TIFERT movements, the real effort of the Bank in term of sight deposits collecting meant a 72.9 MTD (+10.2%) increase.

(*) Customers deposits total is calculated excluding Tifert deposits the total of which amounted as of 31/12/2010 to 93.8 MTD vs. 222.8 MTD at end 2009.

Customers resources

FIGURES IN MTD 31/12/2010 31/12/2009 31/12/2008 31/12/2007 31/12/2006

Sight deposits 797.7 874.4 597.9 577.9 483.7

Savings deposits 1 297.1 1 250.6 1 171.3 1 115.157 1 063.9

Forward deposits 1 198.7 1 061.6 832.6 700.9 740.4

Other amounts owed to customers 70.4 68.4 55.4 49.4 36.981

TOTAL 3 363.9 3 255.0 2 657.3 2 443.4 2 325.0

TOTAL (*) 3 270.0 3 032.4

During 2010, the Bank buckled down to pursuing the achievements of good governance basis in its different dimensions of which particularly the setting up of an internal control system seeing to risk strict management. On the other hand, the consolidation of its financial basis remains the Bank’s priority through the support of general balances with a particular concern of complying with prudential and regulatory standards.

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 28 PAGE 29

Savings deposits continued their upward trend but at a lesser pace than the one of 2009, progressing by 46.5 MTD (+3.7%) vs. 79.3 MTD (+6.8%) in 2009.

Increasing by 50.2 MTD free savings deposits remain the exclusive boost of savings deposits which were impacted by the downward trend of housing savings deposits (-6.7 MTD). As for Eljadid savings deposits and studies savings deposits, they went up respectively by 1.5 MTD and 1.4 MTD.

Maturities deposits i l lustrated a 137 MTD trend favored by a progress of forward deposits by 186.8 MTD against a decrease in deposit certificates by 52 MTD.

TREND OF CUSTOMERS DEPOSITS 2006-2010 :

2 32

5.0

2 44

3.5

2 65

7.3

3 25

5.0

3 36

3.9

3

032.

4

3

270.

0

2 000

2 400

2 800

3 200

3 600

2006 2007 2008 2009 2010

Customers deposits

deposits excluding TIFERT

- Figures in MTD -

CUSTOMERS RESOURCES ADDITIONAL FLOWS IN 2010 :

Sight deposit

Savings deposits

Maturities deposits

- Figures in MTD -

-76.7

46.5

137.0

- Figures in MTD -

STRUCTURE OF CUSTOMERS DEPOSITS AS OF 31/12/2010 :

Saving deposits

Maturities deposits

24%

40%

36%

Sight deposits

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 30 PAGE 31

TREND OF CUSTOMERS DEPOSITS 2006-2010 :

Borrowings and special resources

Core funds

As for borrowings , 2010 was characterized by a reimbursement pace that was higher than the one of encashment; in effect the Bank made the following paying out:

The first portion of a subordinated loan of 14 MTD.•

The whole last year’s borrowing from Nefzoua clinic (4.6 MTD)•

Maturities regarding first lines pertaining to ADB borrowing (3.5 MTD), EIB (0.6 MTD) and FDA (0.9 MTD).•

The second lines pertaining to borrowings from ADB (11.7 MTD) and EIB (0.9 MTD).•

The third line of EIB borrowings (2.6 MTD).•

And the second portion of HG 004C borrowing (0.4 MTD)•

On the other hand and dur ing 2010, the sole drawing is the f i f th of E IB bor rowing for an amount of 7 MTD.

Core funds reached 430.4 MTD vs. 411.2 MTD a year before meaning a consolidation of 19.1 MTD (+4.7%) led mainly by the strengthening of reserves by 43 MTD.

Taking advantage of provisions reinforcement by 73.3 MTD (+28.4%), these resources went up by 24% that is +89.2 MTD with reserved agios contribution by 12.4 MTD (+17.8%).

Other resources

2006 2007 2008 2009 2010

Savings deposits

Maturities deposits

Sight deposits

1063.9

1115.5

1171.3 1250.6

1297.1

740.4

700.9

832.6 1061.6 1198.7

483.7

578.0

597.9

874.4

797.7

- Figures in MTD -

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 30 PAGE 31

Provisions

Reserved agios

126.

6 163.

7 202.

6

257.

6

330.

9

59.8

65.5

64.2

69.7

82.1

2006 2007 2008 2009 2010

- Figures in MTD -

At the level of uses, the year 2010 was marked by:

Intensifying the Bank’s intervention in financing the economy which meant an additional flow • going up from 284.6 MTD (7.4%) in 2009 to 527.6 MTD (+12.7%) in 2010.

Diversifying the activity while maintaining a structure that supports the predominance of real • estate loans (prefinancing and buyers) the outstanding balance of which accounts for 48.2% of productive claims.

THE USES

Accounting for the dominating item of financing the economy, loans on core funds went up by 487 MTD, more than the double of achievements at the end of 2009 (+ 227.6 MTD).

Securities portfolio rose by 49.1 MTD fed by the increase of participation portfolio by 32.3 MTD of which 21.7 MTD coming to the Bank’s additional participation in the capital of Foreign Tunisian Bank (former UTB). The Bank also invested 12.8 MTD in 2010 in its subsidiary SIM-SICAR.

Loans on special resources pursued their 2009 decrease (-0.9 MTD) going down by 8.6 MTD.

These trends combining generated a volume of financing the economy going up by 527.6 MTD closing for the year 2010 at 4 680.1 MTD.

Financing the economy

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 32 PAGE 33

STRUCTURE OF PRODUCTIVE CLAIMS IN 2010 :

37 %

8 %

11 %

12 %

32 %

Buyers real estate loans

Consumer loans

Loans to individuals

Loans to real estate property developers

Customers debtor accounts

66%

Crédits Epargne Eljadid

Crédits Epargne Logement

Crédits Directs

32%

2%

FIGURES IN MTD 31/12/2010 31/12/2009 31/12/2008 31/12/2007 31/12/2006

Total loans/core funds 3 973.9 3 486.8 3 259.2 2 851.7 2 504.6

Customers debtors accounts 299.7 267.1 297.2 235.9 195.9

Loans to individuals 444.0 385.8 363.9 323.5 226.6

Consumer loans 1 162.4 941.4 834.8 561.3 417.3

Loans to real estate property developers

424.7 326.3 255.5 267.6 254.2

Loans to real estate buyers 1 349.6 1 321.8 1 272.1 1 224.9 1 195.4

Total produtives claims 3 680.4 3 242.5 3 023.4 2 613.2 2 289.4

Total undue payments 293.5 244.3 235.8 238.6 215.2

Total loans / special resources 419.4 428.0 428.9 423.6 418.2

Total loans to customers (1) 4 393.3 3 914.8 3 688.1 3 275.4 2 922.8

Total securities portfolio (2) 286.8 237.7 179.8 132.2 119.0

Financing of the economy(1)+(2) 4 680.1 4 152.5 3 867.9 3 407.6 3 041.8

The following table shows the trend of financing the economy during the period 2006-2010 :

TREND OF FINANCING THE ECONOMY AND PRODUCTIVE CLAIMS 2006-2010 :

4500

4000

3500

3000

2500

2000

1500

2006 2007 2008 2009 2010

4680

.1

3143

.5 3407

.7 3867

.7 4152

.5

Productive claimsFinancing of the economy

2364

.5

2613

.2 3023

.4

3242

.5 3680

.4

- Figures in MTD -

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 32 PAGE 33

Debtor accounts were characterized

by a non linear trend. In effect during the first half,

these claims went up by 28.6 MTD then

by 23.5 MTD during their third quarter closing for

the last three months at a downward trend (-18.5

MTD). Consequently, debtor accounts closed for

the year 2010 at a 32.6 MTD increase bringing

their outstanding balance to 299.7 MTD against

267.1 MTD a year before.

TREND IN DEBTOR ACCOUNTS(IN OUTSTANDING BALANCE AND IN FLOWS) 2006-2010 :

2006 2007 2008 2009 2010

400

300

200

100

0

80.0

60.0

40.0

20.0

0.0

-20.0

-40.0

177.

7

235.

9

297.

2

267.

1

299.

7

39.4

58.2

61.3

-30.

0

32.6

- Figures in MTD -

Outstanding balance Additional flow

Loan to customers

Personal loans were characterized by

a new boost progressing by 58.2 MTD, an additional

flow exceeding the registered amounts in 2009

and 2008 (+49.9 MTD). This boost was led mainly by

the trend in medium term loans rising by 98.8 MTD

partially slowered by consumer loans (-43.2 MTD).

Loans intended to cars purchases went up

by 2.6 MTD.

Thus, the outstanding balance rose by

15.1% to 444 MTD at end 2010.

TREND IN PERSONAL LOANS(IN OUTSTANDING BALANCE AND IN FLOWS) 2006-2010

2006 2007 2008 2009 2010

500

400

300

200

100

80.0

70.0

60.0

50.0

40.0

30.0

20.0

Outstanding balance Additional flow

259.

1

335.

9

363.

9

385.

8 444.

0

76.8

69.0

28.0

21.9

58.2

- Figures in MTD -

Almost all forms of loans showed a double digit positive variation with a net acceleration of pace

trend. Thus productive claims rose by 437.9 MTD corresponding to 13.5% increase against 7.2% in 2009.

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 34 PAGE 35

Short term consumer loans showed

an 82.2 MTD increase against a 4.6 MTD decrease

a year before. The outstanding balance registered

a 17.6% increase bringing it to 549.9 MTD as of

31/12/2010.

Medium term consumer loans

progressed at an annual average rate of 28%;

the outstanding balance having increased from

225 MTD as of 31/12/2006 to 607 MTD

at end 2010.

In 2010, the additional flow amounted

to 136.8 MTD

600

500

400

300

200

100

200

100

300

400

500

600

Outstanding balance

70.5

62.5

166.

2

-4.6

82.1

-10

10

30

50

70

90

110

130

150

170

2006 2007 2008 2009 2010

- Figures in MTD -

additional flow

243.

6

306.

1

472.

3

467.

7

549.

8

TREND IN SHORT TERM CONSUMER LOANS (IN OUTSTANDING BALANCE AND IN FLOWS) 2006-2010

225.

0

252.

2

358.

9

470.

2 607.

0

44.0

27.3

106.

6

111.

3

136.

8

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

100

200

300

400

500

600

2006 2007 2008 2009 2010

- Figures in MTD -

Outstanding balance additional flow

TREND IN MEDIUM TERM CONSUMER LOANS (IN OUTSTANDING BALANCE AND IN FLOWS) 2006-2010

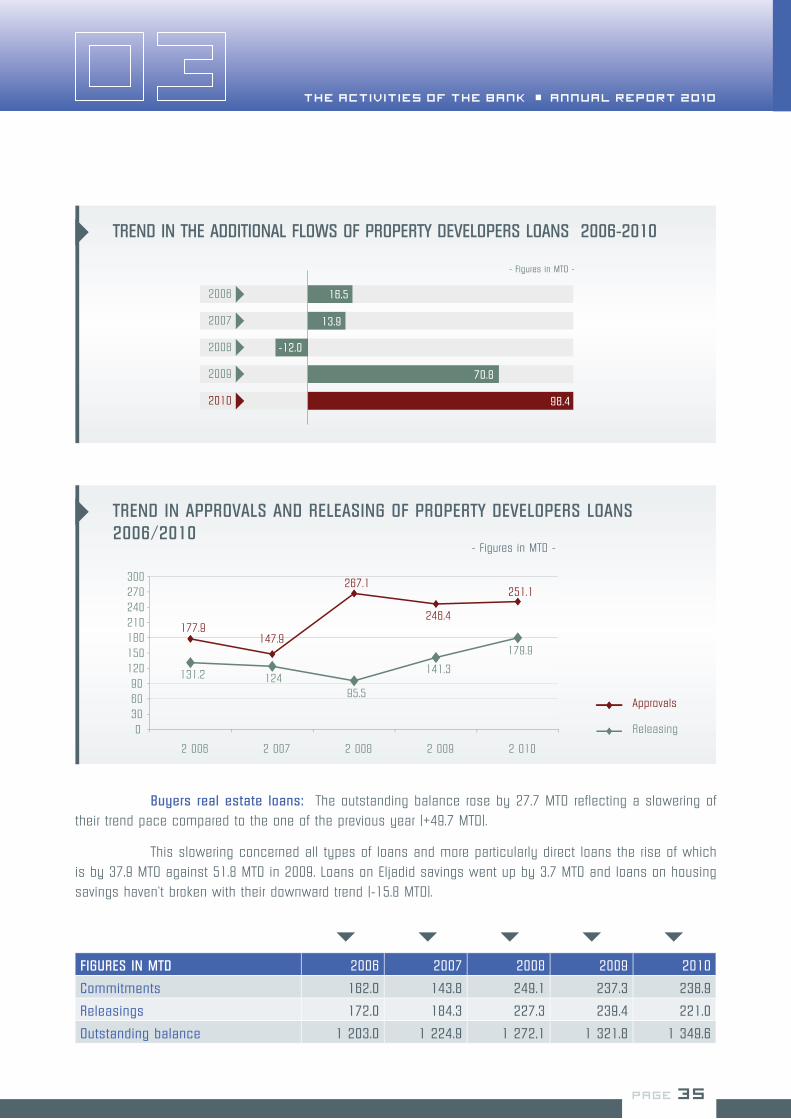

Prefinancing loans registered the highest growth rate of productive claims (+30.1%) going

up by 98.4 MTD feeding thus these claims total increase by 24%.

This growth is favored by a released package amounting to 179.9 MTD up by 27.4% compared

to the one used in 2009. Private real estate providers absorbed 78.3% of this package, an amount

of 140.8 MTD. Releasings in favor of public real estate providers came in at 39.1 MTD against 21.6 MTD

in 2009 showing an 81% increase.

As for authorizations, loans granted to real estate providers totaled 251.1 MTD intended

to the achievement of 3 672 lodgings against 3 251 in 2009.

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 34 PAGE 35

TREND IN THE ADDITIONAL FLOWS OF PROPERTY DEVELOPERS LOANS 2006-2010

16.5

13.9

-12.0

70.8

98.4

2006

2007

2008

2009

2010

- Figures in MTD -

TREND IN APPROVALS AND RELEASING OF PROPERTY DEVELOPERS LOANS 2006/2010

177.9 147.9

267.1

246.4

251.1

131.2 124 95.5

141.3

179.9

0 30 60 90

120 150 180 210 240 270 300

2 006 2 007 2 008 2 009 2 010

Approvals

Releasing

- Figures in MTD -

Buyers real estate loans: The outstanding balance rose by 27.7 MTD reflecting a slowering of

their trend pace compared to the one of the previous year (+49.7 MTD).

This slowering concerned all types of loans and more particularly direct loans the rise of which

is by 37.9 MTD against 51.8 MTD in 2009. Loans on Eljadid savings went up by 3.7 MTD and loans on housing

savings haven’t broken with their downward trend (-15.8 MTD).

FIGURES IN MTD 2006 2007 2008 2009 2010

Commitments 162.0 143.8 249.1 237.3 238.9

Releasings 172.0 184.3 227.3 239.4 221.0

Outstanding balance 1 203.0 1 224.9 1 272.1 1 321.8 1 349.6

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 36 PAGE 37

STRUCTURE OF HOUSING LOANS

Y E A R 2 0 0 6

Y E A R 2 0 1 0

Eljadid savings loans 2%

Direct loans 66%

Housing savings loans 32%

Direct loans 70%

Eljadid savings loans 4%

Housing savings loans 26%

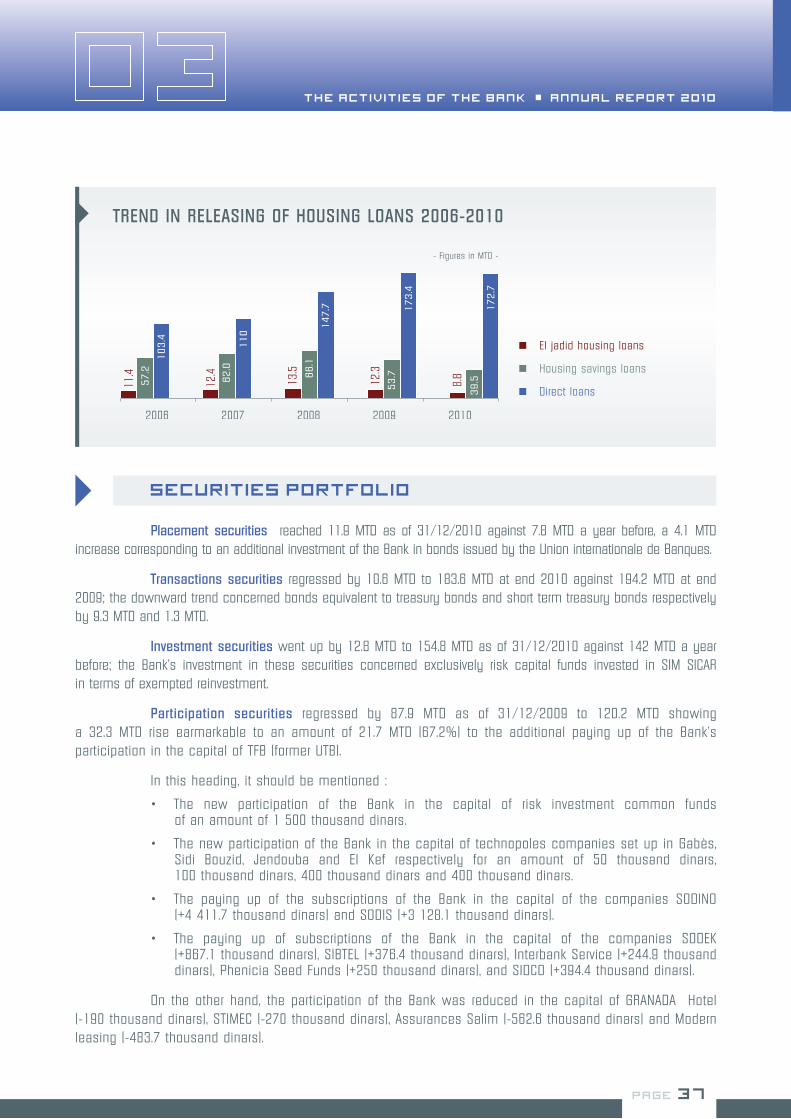

Releasing went down by 18.4 MTD of which 14.2 MTD coming to the released amount in favor of housing savings loans.

At a lesser extent, releasings regarding Eljadid housing savings went down by 3.5 MTD, on the other hand, releasings in favor of direct loans almost stagnated at the 2009 same level closing for the year 2010 with a package of 172.7 MTD.

FIGURES IN MTD

RELEASINGS 2006 2007 2008 2009 2010

Loans/ housing savings 57.2 62.0 66.1 53.7 39.5

Direct loans 103.4 110.0 147.7 173.4 172.7

Loans/ Eljadid savings 11.4 12.4 13.5 12.3 8.8

In 2010, the Bank granted 5 754 housing loans to private individuals of which 1 406 loans on housing savings, 4 028 direct loans and 320 loans on Eljadid resources. The total package of these approvals amounted to 238.9 MTD against 237.2 MTD a year before.

788.8 804.5 844.7

896.5

934.4

386.3 381 376.4 363.6

347.8

600

650

700

750

800

850

900

950

1 000

2006 2007 2008 2009 2010

Direct loans

Housing savings loans

- Figures in MTD -

250

300

350

400

450

500

550

600

TREND OF THE OUTSTANDING BALANCE OF HOUSING SAVINGS LOANS AND DIRECT LOANS 2006-2010

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 36 PAGE 37

TREND IN RELEASING OF HOUSING LOANS 2006-2010

11.4

12.4

13.5

12.3

8.8

57.2

62.0

66.1

53.7

39.5

103.4

110 1

47.7

173.4

172.7

El jadid housing loans

Housing savings loans

Direct loans

2006 2007 2008 2009 2010

- Figures in MTD -

Placement securities reached 11.9 MTD as of 31/12/2010 against 7.8 MTD a year before, a 4.1 MTD increase corresponding to an additional investment of the Bank in bonds issued by the Union internationale de Banques.

Transactions securities regressed by 10.6 MTD to 183.6 MTD at end 2010 against 194.2 MTD at end 2009; the downward trend concerned bonds equivalent to treasury bonds and short term treasury bonds respectively by 9.3 MTD and 1.3 MTD.

Investment securities went up by 12.8 MTD to 154.8 MTD as of 31/12/2010 against 142 MTD a year before; the Bank’s investment in these securities concerned exclusively risk capital funds invested in SIM SICAR in terms of exempted reinvestment.

Participation securities regressed by 87.9 MTD as of 31/12/2009 to 120.2 MTD showing a 32.3 MTD rise earmarkable to an amount of 21.7 MTD (67.2%) to the additional paying up of the Bank’s participation in the capital of TFB (former UTB).

In this heading, it should be mentioned :

The new participation of the Bank in the capital of risk investment common funds • of an amount of 1 500 thousand dinars.

The new participation of the Bank in the capital of technopoles companies set up in Gabès, • Sidi Bouzid, Jendouba and El Kef respectively for an amount of 50 thousand dinars, 100 thousand dinars, 400 thousand dinars and 400 thousand dinars.

The paying up of the subscriptions of the Bank in the capital of the companies SODINO • (+4 411.7 thousand dinars) and SODIS (+3 128.1 thousand dinars).

The paying up of subscriptions of the Bank in the capital of the companies SODEK • (+867.1 thousand dinars), SIBTEL (+376.4 thousand dinars), Interbank Service (+244.9 thousand dinars), Phenicia Seed Funds (+250 thousand dinars), and SIDCO (+394.4 thousand dinars).

On the other hand, the participation of the Bank was reduced in the capital of GRANADA Hotel (-190 thousand dinars), STIMEC (-270 thousand dinars), Assurances Salim (-562.6 thousand dinars) and Modern leasing (-483.7 thousand dinars).

Securities portfolio

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 38 PAGE 39

Gross fixed assets totaled 117 MTD at end 2010 against 107 MTD as of 31/12/2009 corresponding to a 10 MTD increase resulting mainly from increases in the headings equipment and office furniture (+3.4 MTD) and lay out, fitting up and installations (+1.5 MTD). Amounts regarding plots of land and computer softwares went up respectively by 1 MTD and 0.6 MTD.

Fixed assets

Undue payments and matters in dispute

The overall volume of undue payments as of 31/12/2010 went up by 49.1 MTD of which 62% (+30.2 MTD) coming to claims in dispute. At a lesser extent, undue payments regarding consumer and industrial loans worsened by 10 MTD.

ASSETS QUALITY

Collection

Non performing loans

Efforts made by the Bank in 2010 in order to reduce the volume of undue payments as of 31/12/2009 helped to recover 71.1 MTD, a 29.1% rate of undue payments resumption. Recoveries on unsafe claims regarding prefinancing loans amounted to 7.3 MTD.

The works of classifying the Bank’s commitments taking into account those related to Ben Ali and Trabelsi families the amount of which comes in at 69.5 MTD show a total NPL of 550.3 MTD.

NPL portfolio related to consumer, industrial and prefinancing loans shows a volume of 473.4 MTD. Classified claims on loans to private individuals and housing loans to buyers amount respectively to 9.5 MTD and 67.4 MTD.

TREND IN UNDUE PAYMENTS 2006-2010

3.7 5.7 7.9 9.8 13

.4

51.3

54.7

55.5

55.4

60.7

36.4

38.1

49.5

51.2

61.2

150.

9

140.

0

122.

8

127.

9 158.

2

Undue payments/ personal loans

Undue payments/ housing loans

Undue payments/ consumer and industrial loans

Claims in dispute2006 2007 2008 2009 2010

- Figures in MTD -

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 38 PAGE 39

Thus, the rate of NPL with respect to the Bank’s total commitments accounts for 10.8%, the lowest rate of public banks below the estimated 13.2% of the sector’s rate.

The trend in NPL during the last five years is illustrated in the following table:

FIGURES IN THOUSAND DINARS 31/12/2006 31/12/2007 31/12/2008 31/12/2009 31/12/2010

Class 2 38 352 34 494 101 458 72 209 49 161

Class 3 13 141 19 367 38 681 74 020 137 085

Class 4 210 384 227 752 224 803 276 396 364 041

TOTAL 261 877 281 613 364 969 422 625 550 287

FIGURES IN MTD 31-12-2006 31-12-2007 31-12-2008 31-12-2009 31-12-2010

Provisions 126.593 138.1 167.4 226.077 297.218

Provisions + Reserved charges 186.369 203.6 231.7 295.782 379.328

Provisions + Reserved charges / Classified claims

71.17% 72.28% 63.50% 70% 68.9%

As for risks coverage, the Bank pursued its provisions consolidation effort and the coverage rate comes in at 68.9%.

TREND IN CLASSIFIED CLAIMS/RISK COVERAGE RATE 2006-2010

261.

9

281.

6

365.

0

422.

6

550.

3

71.2

%

72.3

%

63.5

%

70.0

%

68.9

%

60%

65%

70%

75%

100

150

200

250

300

350

400

450

500

550

2006 2007 2008 2009 2010

- Figures in MTD -

Classified claims Coverage rate

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 40 PAGE 41

During 2010, the Bank’s activity generated a banking net proceed of 194.6 MTD improving by 8.1 MTD (+4.4%) against 0.6 MTD decrease in 2009. All these headings participated at different degrees to this improvement; the interest margin progressed by 1.4 MTD, net commissions by 2.1 MTD and net gains on securities portfolio contributed to this improvement by 57.3% with a 4.7 MTD strengthening.

Operating charges totaled 83 MTD against 78.4 MTD a year before, up 4.6 MTD of which 2.9 MTD ascribable to staff costs; the general operating charges went up by 1.7 MTD.

Thus, Gross operating result strengthened by 5.1 MTD (+4.1%) to 128.3 MTD.

Having earmarked an additional net allocation for provisions of 28.7 MTD, the Bank registered a net result of 30.2 MTD.

BANK’S RESULTS

STATEMENT OF RESULT 2010 2009 2008 2007 2006

Interest margin 133.9 132.6 134.7 116.6 95.1

Net commissions 33.5 31.4 31.6 32.9 26.7

Net gains on securities portfolio 27.2 22.6 20.8 19.5 23.4

Net banking proceed 194.6 186.5 187.2 168.9 145.3

Banking operating other proceeds 16.7 15.1 11.0 10.4 10.7

Staff costs 62.1 59.2 52.5 49.5 46.5

General operating charges 20.9 19.2 17.8 17.0 16.3

Gross operating result 128.3 123.3 127.9 112.8 93.2

Allocations for provisions 72.8 55.6 52.1 41.4 38.8

Allocations for amortization 4.3 2.9 2.6 2.5 2.5

Allocations for provisions / Investment portfolio

10.5 -1.1 6.1 4.3 4.6

Operating result 40.7 65.8 67.07 64.6 47.4

Gains / ordinary elements 0.1 0.0 0.4 0.1 0.1

Loss / ordinary elements 0.3 0.0 0.00 0.0 0.00

Before tax result 40.6 65.8 67.4 64.7 47.4

Tax on profit 8.0 12.5 13.4 13.6 9.9

Effects of accounting modifications -2.4 0.8 0.000 0.0 -8.9

Net result of the fiscal year 30.2 53.3 53.9 51.1 28.5

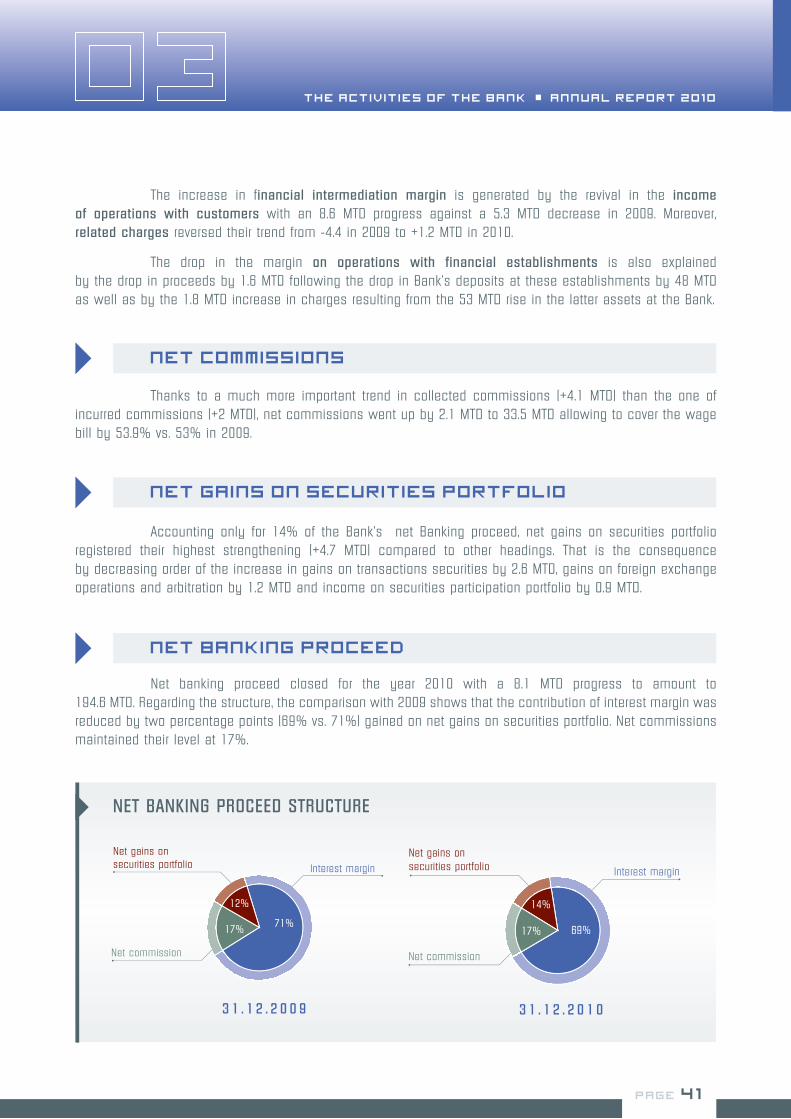

At end 2010, banking intermediation activity displayed a 1.4 MTD progress showing a net margin of 133.9 MTD against 132.6 MTD a year before. Interest margin was characterized mainly by an increase in financial intermediation margin by 7.5 MTD slowered in part by margin on transactions with financial establishments of 3.5 MTD.

Interest margin

Figures in MTD

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 40 PAGE 41

The increase in financial intermediation margin is generated by the revival in the income of operations with customers with an 8.6 MTD progress against a 5.3 MTD decrease in 2009. Moreover, related charges reversed their trend from -4.4 in 2009 to +1.2 MTD in 2010.

The drop in the margin on operations with financial establishments is also explained by the drop in proceeds by 1.6 MTD following the drop in Bank’s deposits at these establishments by 48 MTD as well as by the 1.8 MTD increase in charges resulting from the 53 MTD rise in the latter assets at the Bank.

Thanks to a much more important trend in collected commissions (+4.1 MTD) than the one of incurred commissions (+2 MTD), net commissions went up by 2.1 MTD to 33.5 MTD allowing to cover the wage bill by 53.9% vs. 53% in 2009.

Net commissions

Net gains on securities portfolio

Accounting only for 14% of the Bank’s net Banking proceed, net gains on securities portfolio registered their highest strengthening (+4.7 MTD) compared to other headings. That is the consequence by decreasing order of the increase in gains on transactions securities by 2.6 MTD, gains on foreign exchange operations and arbitration by 1.2 MTD and income on securities participation portfolio by 0.9 MTD.

NET BANKING PROCEED STRUCTURE

3 1 . 1 2 . 2 0 0 9

Net commission

Interest margin

Net gains on securities portfolio

12%

71%17%

70%

Net commission

Interest margin

Net gains on securities portfolio

14%

17% 69%

3 1 . 1 2 . 2 0 1 0

Net banking proceed closed for the year 2010 with a 8.1 MTD progress to amount to 194.6 MTD. Regarding the structure, the comparison with 2009 shows that the contribution of interest margin was reduced by two percentage points (69% vs. 71%) gained on net gains on securities portfolio. Net commissions maintained their level at 17%.

Net banking proceed

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 42 PAGE 43

2010 2009 2008 2007 2006

Net banking proceed/total loans 4.86% 5.16% 5.42% 5.5% 5.08%

Staff costs/net banking proceed 31.91% 31.74% 28.07% 29.31% 31.99%

Overheads/net banking proceed 42.63% 42.03% 37.57% 39.38% 43.18%

NBP / staff (thousand dinars) 104.9 100.5 100.5 89.7 76.4

Gross operating result

Overheads

With an 8.6 MTD improvement in net banking proceed and 1.5 MTD increase in other products of banking operating absorbed in part by the 4.6 MTD rise in overheads, the gross operating result went up by 5.1 MTD closing for the year 2010 at 128.3 MTD.

Overheads rose by 6% from 78.4 MTD in 2009 to 83 MTD at end 2010, up by 4.6 MTD vs. 8 MTD a year before. This rise is ascribable to the wage bill by 2.9 MTD (+4.9%); as for operating overheads, they rose by 1.7 MTD (+9%).

FIGURES IN MTD 2010 2009 2008 2007 2006

Net bankig proceed 194 .6 186 .5 187.2 168.9 145.3

Other operating proceeds 16.7 15.1 11.0 10.4 10.6

Staff costs 62.1 59.2 52.5 49.5 46.5

overall operating charges 20.9 19.2 17.9 17.0 16.2

Operating gross result 128.3 123.3 127.9 112.8 93.2

TREND IN NET BANKING PROCEED AND OPERATING GROSS RESULT 2006-2010

93.2

112.

8

127.

9

123.

3

128.

3

220

200

180

160

140

120

100

80

60

145.3

168.9

187.2

186.5

194.6

2006 2007 2008 2009 2010

Operatinggrossresult

Netbankingproceed

220 - Figures in MTD -

The contribution of each agent kept on improving from 100.5 thousand dinars at end 2009 to 104.9 thousand dinars at end 2010.

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 42 PAGE 43

The Bank’s provisioning effort is noticeable through the 30.2 MTD provisions constituting on the whole ventured commitments towards the former president family. Net allocations totaled 83.3 MTD at end 2010 against 54.5 MTD a year before, an additional allotment of 28.7 MTD.

Allocations for provisions

FIGURES IN MTD 2010 2009 2008 2007 2006

Net allocations for provisions 83.3 54.5 58.3 45.7 43.4

Following an intensification of the provisioning effort, the net result came in at 30.2 MTD.

Net result of the financial year

Financial profitability expressed by ROE came in at 7.57% and assets profitability expressed by ROA at 0.62%.

Operating efficiency calculated by the operating ratio accounts for 42.63% rating the bank fourth in the sector in terms of productivity.

As for regulatory ratios, the solvency ratio came in at 9.95% and the liquidity ratio closed for the year 2010 at 111.94% against 129.55% at end 2009.

TREND IN MAIN RATIOS

31.12.2010 31.12.2009

ROE 7.57% 12.95%

ROA 0.62% 1.03%

Operating ratio 42.63% 42.03%

Solvency ratio 9.95% 10.16%

Liquidity ratio 111.94% 129.55%

Resources cost 3.27% 3.46%

Total loans/ total deposits 119.10% 110.95%

Ratios

Taking advantage of world economy revival in 2010, foreign exchange activity resumed its upward trend after a net slackening in 2009. In effect, generated proceeds went up by 1.2 MTD (+5.5%) against a drop by 3.9 MTD (-15.2%) in 2009 rising then from 21.7 MTD in 2009 to 22.9 MTD in 2010.

FOREIGN EXCHANGE ACTIVITY

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 44 PAGE 45

In 2010, the dealing room made the most important progress (+0.8 MTD) feeding the total increase

in proceeds generated by foreign exchange activity by almost 70%. At a lesser extent, foreign exchange

and transfer operations showed a slight progress by 0.3 MTD to 2.6 MTD.

On the other hand, income from external trade transactions almost stabilized at 3.6 MTD.

The following table shows the trend in proceeds related to foreign exchange different activities :

FIGURES IN THOUSAND DINARS 31/12/2010 31/12/2009 Variation 12.10/12.09

Foreign exchange and transfers 2 552 2 247 305 13.6%

Transfers 1 981 1 650 331 20.1%

Payment means 572 598 - 26 -4.3%

External trade 3 574 3 609 - 35 -1.0%

Import documentary credit 2 459 1 919 540 28.2%

Import documentary remittances 264 397 - 133 -33.5%

Export documentary credits 481 750 - 269 -35.9%

Export documentary remittances 370 543 - 173 -31.9%

Dealing room in currencies 16 258 15 434 824 5.3%

Cash foreign exchange 7 561 6 902 659 9.5%

Forward foreign exchange 4 111 3 728 383 10.3%

Money market in currencies 4 586 4 804 - 218 -4.5%

Foreign exchange bureau 545 440 105 23.8%

General total 22 929 21 731 1 199 5.5%

In terms of issue, the Bank’s effort in 2010 meant the creation of 30 082 cards against 26 859

cards in 2009, up by 12%.

On the other hand, the total value of cards in circulation regressed slightly from 161 728 at end

2009 to 156 688 as of 31/12/2010 following essentially the increase in cards cancelling pace which reached

37 536 against 21 000 in 2009 and 10 000 in 2008.

Re fe r red to the ove ra l l number o f accounts , the number o f ca rds obta ins a ra te o f

coverage of 66.3 %.

MONETICS

Issue of banking cards

In spite of the decrease in cards, the overall operating volume made by BH cards holders grew

substantially compared to 2009, rising by 6% in number and 11% in amount to reach 5 217 thousand

operations for a 654 thousand dinars turnover.

Operating volume of BH cards

THE ACTIVITIESOF THE BANK

THE ACTIVITIES OF THE BANK • ANNUAL REPORT 2010

PAGE 44 PAGE 45

At end 2010, affiliated network totaled 780 traders against 729 a year before. The number of

affiliated traders equipped with electronic payment terminal amounted to 448, an equipment rate of 57%

against 53% as of 31/12/2009. Also, processed transactions went up in volume and in amount as well

respectively by 12% and 7%.

The network of ATMS reached 101 as of 31/12/2010 of which 11 ATMS off site and 90 ATMS

in branches. As far as ATMS performance is concerned, the operating volume improved, the number of transactions

rose by 9% generating a turnover rising by 15% rating the Bank first in the sector.

Affiliated traders

Automated Teller machines

During 2010, the Bank’s share led to a volume of transactions totaling 47.9 MTD dealing with

the negotiation of 1 633 065 shares.

Closing for the year at 29.460 dinars, stock market capitalization amounted to 530.3 MTD, up by

6.5% compared to the year 2009

SHAREHOLDING AND TREND OF THE BANK’S

SHARE

31/12/2010 31/12/2009

Number of processed securities 1 633 065 3 213 126

Volume of traded assets (in MTD) 47.933 83.393

Stock market capitalization (in MTD) 530.280 497.700

During 2010, the trend in the rate of the bank’s share was characterized by an upward trend, its rate

oscillating between 26.300 dinars and 34.100 dinars, displaying an average of 28.689 dinars against 26.659 dinars

a year before.

Foreign investors interest to the Bank’s share rose and the share of the latter in the capital

of the Bank went up from 8.73% in 2009 to 10.29% as of 31/12/2010 with a 9.3 MTD participation.

FIGUERS IN DINARS 31/12/2010 31/12/2009

Start of period rate 27.650 23.290

End of period rate 29.460 27.650

Period highest rate 34.100 29.310

Period lowest rate 26.300 23.290

Period average rate 28.689 26.659

ASSESSMENT

OF UNDERTAKEN

ACTIONS IN 2010

PAGE 47

PAGE 48

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010 • ANNUAL REPORT 2010

The Banque de l’Habitat has always pursued its efforts in order to consolidate its results, improve

its services quality and reinforce its market share.

In 2010, these efforts have been materialized through a set of actions:

In the framework of extending its branches network and in order to be closer to its customers and to

ensure better services quality to its customers, the Bank opened 4 new sales points in 2010 bringing to 93

the number of sales points. These are Bizerte Erraouabi, Moulares, Korba and Northern Urban Centre in Tunis.

The Bank has also fit out 3 sales points: Charguia, Bizerte Thâalbi and Hammamet.

As for sales points transfer, they concerned Sfax Jadida, Kram and Ben Arous that are being fit out.

Finally, the Bank opened two foreign exchange bureau at Hammamet Enfidha airport.

In the second half 2010, the Bank experienced a major event namely the transfer to the new

head office in Avenue Mohamed V while maintaining the operating continuity of its services and its informatics

infrastructures.

This great achievement experienced by the site, infrastructure, functionality and modernity

of the head off ice wil l contr ibute to improve working condit ions and the qual i ty of offer ing services

and the influence of the Bank.

In the framework of diversifying and developing bank insurance products and in order to offer to

its customers a range of comprehensive and personalized product, the Bank finalized in 2010 the prerequisites

of the starting up of its new products “Dhamen Epargne retraite” (Guaranteeing retirement savings)

that is expected to be put on the market in the first quarter 2011.

COMMERCIAL DEVELOPMENT

OPENING AND TRANSFER OF SALES POINTS

BANK INSURANCE DEVELOPMENT

TRANSFER OF THE HEAD OFFICE KHEIREDDINE PACHA

TO THE NEW HEAD OFFICE IN AVENUE MOHAMED V

PAGE 49

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010 • ANNUAL REPORT 2010

With the objective of getting further close to its customers, the Bank pursued in 2010

the development of d istance serv ices mainly the package mobi le banking that wi l l be put on

the market in 2011.

This new package mobile banking will help customers carry out account management through

mobile phone.

Besides communications campaigns intended to residents and Tunisians living abroad, the Bank

participated to the following actions:

Carthage 2010 exhibition.•

Creation and technological development of business exhibition 2010.•

Sitap 2010 exhibition•

Lunch-debate with property developers.•

It is a retirement savings contract in favor of the Bank’s customers wishing to constitute

an additional retirement in the form of capital or life annuity.

It should be noted that the advantages of this product focus on:

The deduction from taxable income of the subscriptions paid with respect to the contract •

in the limit of regulatory ceilings.

The capitalization of net subscriptions at the minimum guaranteed rate with a profit making •

participation calculated on the basis of Salim insurance financial results.

Exemption of management and acquisition fees during the first year of subscription.•

Development of products and services

tied to new technologies

Participation to fairs exhibitions

and advertisement campaigns

PAGE 50 PAGE 51

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010 • ANNUAL REPORT 2010

In the framework of applying the circular of the Central Bank of Tunisia n°19/2006 of November

28, 2006 regarding internal control, it has been decided to create three committees during 2010 :

Security committee:• It is in charge of validating and approving the security policy of banking

operations as well as the follow up of security procedures and means to be implemented.

It sees to the integration of security concepts in the bank operating.

Risk committee:• It is in charge of ensuring that the risks generated by the activity of the

bank and its subsidiaries notably in the field of credit, market, the global rate of interests,

liquidity, settlement as well as operating risks are identified, covered and compatible with

profitability policies and objectives set by the executive board.

Risk technical committee:• It is in charge of identifying, analyzing and supervising risks

generated by the Bank activity in the field of credit, market, global rate of interests, liquidity,

settlement as well as operating risks.

During March 2010, the Bank implemented the organization chart started in 2007 through

the nomination of managers of submanagement and departments.

In order to improve the quality of its services, the Bank has :

Updated the memorandum dealing with the missions and attributions of the sales point •

director.

Implemented the position of sales point controller.•

ORGANIZATIONAL

AND PROCEDURAL ACTIONS

Organization Chart of the Bank

Creation of committees in the framework of

the setting up of an internal control system

Updating missions and attributions of sales

points.

PAGE 50 PAGE 51

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010 • ANNUAL REPORT 2010

In the framework of its mission, the body of compliance control carried out the following

actions in 2010 :

Identifying the situations of non compliance thanks to collected information from reports of •

the General supervision and internal audit following missions carried out in different

departments.

Follow up of auditors recommendations related to the fiscal year 2009.•

Steering jointly with the legal department of operations of files preparation to be conveyed to •

the National authority for the protection of personal data (INPDCP) pursuant to law 2004-63

of July 27, 2004 and subsequent decrees 3003-2007 and 3004-2007.

Widening conditions of granting loans to individuals by reconsidering management rules •

and granting consumer loans to individuals.

Decentralizing the issue of mortgage release on loans to individuals specifically those related •

to loans to individuals having financed non professional needs.

Decentralizing files processing of FOPROLOS loans•

Setting up the processing of “Dhamen Finance” through the setting of intervention conditions •

of the Fund of guaranteeing exports financing prior to shipment in the collection of loans

prefinancing exports with respect to the non carrying out of exporting business production.

Compliance control

Implementing operations control

at the level of sales points

PAGE 52 PAGE 53

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010 • ANNUAL REPORT 2010

Starting the setting up of 24 hours

electronic clearing

INFORMATION SYSTEM

The 24 H electronic clearing version regarding the transfer value has started since •

November 22, 2010.

The 24H electronic clearing version regarding the standing order value has started •

December 13, 2010.

The 24H electronic clearing version regarding the inter branch transfer value has started since •

December 13, 2010.

Processing and reporting on loans granting to individuals to the central Bank of Tunisia:

A procedure memorandum on the operating of loans to individuals unit through the system of

units of data exchange and its relation with the Central Bank of Tunisia has been set up.

The unit of loans to individuals processes the risks incurred by lending institutions

on private individuals.

After 4 months of centering the project, the Bank started adapting and delivering the solution.

This stage started on July 1, 2010. The achievement requires 10 months (validation delays of works

by the Bank excluded). It consists in achieving adaptations arising from the centering stage as well

as the parameters of core banking and its integration to current profession applications.

This operation was stopped in November 2010 in the framework of the former project of merging

Banque de l’Habitat with the Société Tunisienne de Banque.

Banking core

Progress report on the setting up of units

of data exchange with the Central Bank of

Tunisia

PAGE 52 PAGE 53

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010

ASSESSMENT OF UNDERTAKEN ACTIONS IN 2010 • ANNUAL REPORT 2010

HUMAN RESOURCES AND TRAINING

Concerned with better serving its customers, the Bank initiated :

The training of its sales points staff through diversified actions on many topics of banking •

practices.

The rationalization of human resources allocation at the level of sales points through •

the assignment of positions according to the sales point category. The use of resources new

employment when opening new sales points.

In the framework of applying law n°2003-75 of December 10, 2003 related to the support of

international efforts combating terrorism and money laundering, the set up of the organization memorandum

was repealed in order to ensure better actions of detecting unusual or suspicious operations.

Combating money laundering

FUTURE

PROSPECTS

PAGE 55

PAGE 56 PAGE 57

FUTUREPROSPECTS

FUTURE PROSPECTS • ANNUAL REPORT 2010

Human resources and training

The year 2011 looks like an exceptional year taking into account the economic, social and political situation: The Bank aware of its role of financing the economy is going to keep on improving its financial performance and consolidating its position in the banking sector.

Thus, the Bank is going to pursue its development through the consolidation of its core trade and the improvement of its services quality .

At the level of resources and more particularly customers resources, the Bank targets raising less costly resources.

The Bank sees to accompany its relations in developing their activities and deploy its commercial activity in cohesion with national policy financing of jobs creating projects.

Collection continues to appear amongst the Bank’s priorities taking into account its impact on its liquidity and profitability through the adoption of a sustained collection policy while being available to customers. The Bank ensures the control of the level of unproductive claims and of the compliance with regulatory ratios in terms of coverage of classified claims and NPL which remain among its priorities.

In order to secure the success of these objectives, the Bank is going to undertake actions regarding the information system , organization , human resources as well as the upgrading of infrastructure development .

Taking into account its need of commercial development and the necessity for the Bank to reinforce and upgrade its human resources, the Bank is going to undertake on 2011 a recruitment scheme and a set of training actions.

These recruitments come within the scope of national policy in the field of employment.

On the other hand, the training actions will take into consideration the new trades.

Started in 2010, some projects of acquisitions and setting up of management systems of banking trades are going to take shape in 2011 :

The management of foreign exchange operation and the dealing room•

The management of combating money laundering•

The continued development of ATMS network of the renewal off cost of equipments•

The management of human resources•

The Bank’s central computer site•

Information system and

infrastructure

PAGE 56 PAGE 57

FUTUREPROSPECTS

FUTURE PROSPECTS • ANNUAL REPORT 2010

The development of the network

Products launching

Organization

The Bank intends to reinforce its presence throughout the Tunisian territory through

the development of the network with the opening of 10 new sales points.

On the other hand and in order to position oneself in the region while ensuring better conditions

of customers welcome and service, the Bank intends to upgrade some existing sales points.

The Bank aware of improving its risks management in all its kinds, is going to buckle down to

the optimization of internal controls and working procedures while ensuring an increased reactivity to

its customers needs.

In this regard, the Bank is going to pursue its policy through the adoption of some measures

for the reinforcement of prudential ratios, the setting up and/ or optimization of tools of internal control

and risks supervision.

Through the launching of a Gold Card intended to top of the range customers and targeting

a niche of customers with adapted services to their needs. In effect, this product will have many advantages

in terms of ceilings and insurance and assistance package.

The Bank is going to keep on its strategy of diversifying products of Bank insurance to •

ensure to its customers an overall and personalized better offer.

Thus, the Bank intends to put on the market its new product “Dhamen Epargne retraite”

(ensuring retirement savings).

The Bank sticks the national strategy aiming at facilitating services access through new •

technologies with the setting up of a package of products and services helping its customers

getting a multi channel banking space using communications and technologies information.

Mobile banking service is on top of these products allowing customers to carry out account

management operations through mobile phone.

FINANCIAL

STATEMENTS

PAGE 59

PAGE 60 PAGE 61

FINANCIAL STATEMENTS

FINANCIAL STATEMENTS • ANNUAL REPORT 2010

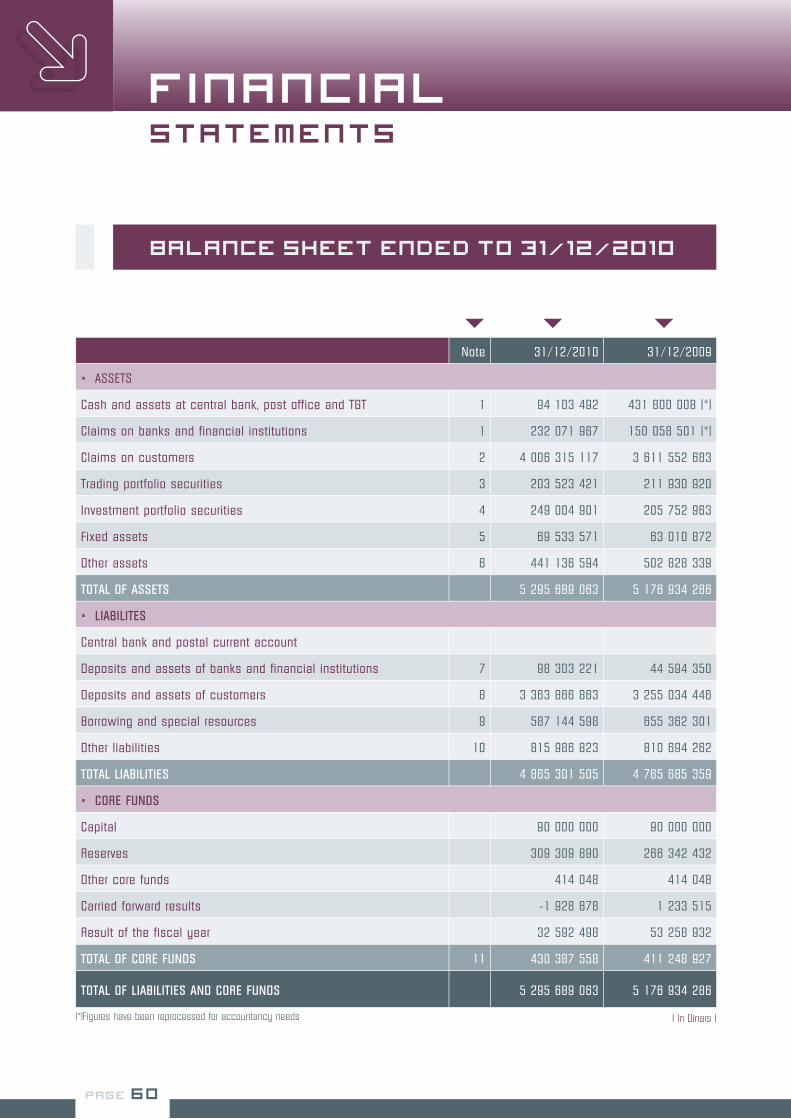

Balance Sheet Ended to 31/12/2010

Note 31/12/2010 31/12/2009

• ASSETS

Cash and assets at central bank, post office and TGT 1 94 103 492 431 800 008 (*)

Claims on banks and financial institutions 1 232 071 967 150 058 501 (*)

Claims on customers 2 4 006 315 117 3 611 552 683

Trading portfolio securities 3 203 523 421 211 930 920

Investment portfolio securities 4 249 004 901 205 752 963

Fixed assets 5 69 533 571 63 010 872

Other assets 6 441 136 594 502 828 339

TOTAL OF ASSETS 5 295 689 063 5 176 934 286

• LIABILITES

Central bank and postal current account

Deposits and assets of banks and financial institutions 7 98 303 221 44 594 350

Deposits and assets of customers 8 3 363 866 863 3 255 034 446

Borrowing and special resources 9 587 144 598 655 362 301

Other liabilities 10 815 986 823 810 694 262

TOTAL LIABILITIES 4 865 301 505 4 765 685 359

• CORE FUNDS

Capital 90 000 000 90 000 000

Reserves 309 309 890 266 342 432

Other core funds 414 048 414 048

Carried forward results -1 928 878 1 233 515

Result of the fiscal year 32 592 498 53 258 932

TOTAL OF CORE FUNDS 11 430 387 558 411 248 927

TOTAL OF LIABILITIES AND CORE FUNDS 5 295 689 063 5 176 934 286