Embed Size (px)

DESCRIPTION

Â

Citation preview

Retail Bulletin

Featured in this issue:Our latest news 2

Central London Retail Development Map 3

Where is the intrinsic value from a good tenant mix? 4

Pop-up retail trend 5

It’s the people, stupid! 6

The National Planning Practice Guidance 7

MUD glorious MUD 8

Retail statistics 10

Jason SibthorpeSenior DirectorHead of Retail+44 (0) 20 7911 [email protected]

Spring 2014

As the retail market continues to be challenging with footfall down over the important Easter trading period it remains fundamental for retailers to implement robust and innovative portfolio solutions to respond to operational pressures. Failure to be proactive and effective can cause catastrophic consequences.

GVA is delighted to be able to offer holistic service capabilities to all of our occupier clients with a focus on some herein. In this bulletin we cover a number of topics including the increasing relevance of pop-ups, securing the right tenant mix and developers responding to personalised shopping experience via mixed-use development.

We hope you find all the features of interest and look forward to doing business with you.

To kick-start the arrival of Spring, GVA Retail is attending ‘Completely Retail Marketplace’ on the 29th April.

Come and meet us at stand 60 to see how we can help you with your next steps in the UK retail market. If you wish to arrange a specific meeting, please do not hesitate to contact us.

1

We are pleased to have selected GVA as our property advisers going forward, in what will be a busy and interesting 12-18 months for the Auntie Anne’s brand in the UK and have already seen a positive insight in to GVA’s approach and capabilities. We look forward to working with GVA to develop this exciting, unique brand into all corners of the UK.

Max Burton, Head of Property,

Auntie Anne’s Pretzels

Cattlegrid RestaurantsGVA has let a unit adjacent to Earlsfield Station in London to Cattlegrid Restaurants. The deal comprises a 25 year lease for a 2,900 sq ft unit at a rent of £90,000 per annum, bringing high quality casual dining to this affluent South West London suburb.

The Master & MargaritaFollowing an extensive marketing effort GVA concluded a 5,700 sq ft letting to contemporary Indian restaurant and cocktail bar The Master & Margarita in The Cube, Birmingham. The rent is £69,000 per annum on a new lease.

Premier InnGVA has exchanged an Agreement for Lease for a 100 room Premier Inn Hotel in our client’s mixed-use development in Addlestone, Surrey. With a rent of £4,500 per annum per room.

SeasaltGVA has been instructed to assist Seasalt with new store acquisitions in coastal locations and affluent market towns. This lifestyle fashion chain, established in Cornwall, already has stores trading in Cornwall, Guernsey, the Isles of Scilly and West Sussex.

Help for HeroesGVA is instructed to assist with a national store acquisition programme for Help for Heroes. The charity has reinvented the definition of “charity shop”, opening up unique bright, colourful and friendly shops selling Help for Heroes new branded clothing, accessories and gifts. Stores already trade in St David’s, Cardiff, Lakeside, Essex and Meadowhall, Sheffield.

HavaianasTrading their third season in mid-mall kiosks and pop-ups, GVA has acquired 17 new locations for Havaianas. New stores include sites in Westfield London and Stratford, Bluewater, Lakeside, Meadowhall, Kingston, Bromley, Watford and Brighton.

Mint VelvetFollowing recent acquisitions for Mint Velvet, GVA has secured new shops in Berkhamsted and Cambridge with a further two locations to complete shortly.

Musto GVA has acquired a new store for Musto, the outdoor and sailing clothing company, in Clarks Village Street, Somerset.

PorcelanosaGVA has been instructed to acquire at least three new stores for Porcelanosa in the South East region of the UK. Porcelanosa currently has 22 existing stores across the UK, but are now looking to expand and acquire new units on a leasehold basis.

Carluccio’sGVA has advised Carluccio’s on their recent opening at 9-11 Station Square, Harrogate, 12 months after a change of use application was originally rejected.

Trespass Following recent acquisitions, GVA has secured further stores in Lincoln, Buxton, Warrington Newport Retail Park, Parc Trostre Llanelli, High Wycombe and Stevenage on behalf of Trespass.

Gregory Property Group We have secured lettings to Aldi and Iceland at Great Eastern Way Rotherham, a development on behalf of Gregory Property Group.

CBRE Global InvestorsGVA has secured a letting to Farmfoods at Pellon Lane Retail Park, Halifax on behalf of the landlord CBRE Global Investors.

Patisserie ValerieGVA has secured a prominent corner unit of approx. 1,600 sq. ft ground floor in Cheltenham at 208 High Street for Patisserie Valerie.

Auntie Anne’s Pretzels We have been selected by the worlds’ largest soft pretzel retailer Auntie Anne’s Pretzels as sole UK property adviser. Auntie Anne’s currently trade from approximately 30 UK sites with over 1,400 international sites and are part of the larger Focus Brands Group. Plans remain on-going to expand the UK portfolio seeking prime kiosk and small in-line units in shopping centres, high streets, stations and transport hubs.

Lush GVA has acquired a highly prominent unit in Tunbridge Wells for retained client, Lush. A new lease was agreed with landlord Hermes for a unit on the main entrance to the Royal Victoria Place scheme, which also benefits from frontage to Calverley Road.

EDG PropertyGVA has secured a new lease on Unit 2 the School Yard, Harborne, a mixed-use redevelopment of a former Grade II listed Victorian school, to Boston Tea Party, who has agreed to take a new 15 year lease. We acted on behalf of the landlord, EDG Property.

GVA retail news

2

Taking inspiration from the GVA’s London Offices Development Map, GVA’s Retail team has produced a similar map illustrating where future developments with retail and/or leisure elements will take place within London’s West End. Stretching from Marble Arch to Covent Garden, the map also contains spot Zone A values for the major retail pitches, customer exit figures for all the tube stations and the locations of all the best hotels, from where many of London’s luxury consumers emanate. In addition, there is a weighted footfall index, a breakdown of how shopper spend is allocated between residents, workers and tourists and the ownerships of some of London’s biggest retail landlords is highlighted.

Furthermore, the units in all the major retail streets are labeled with their occupiers.

The aim of the map is to help retailers, particularly foreign operators, to get a good overview of the different West End retail pitches. If you do not know London well you may think that walking from Tottenham Court Road tube station to Covent Garden is quite onerous, when in fact it is only half a mile. The map also contains a footfall index, which illustrates, for example, that the footfall in Oxford Street, west of the Circus, is twice as high as it is near Marble Arch. When the second edition of the map is released in the autumn it will be fascinating to compare how rents have changed over the last 12 months in each location, how many new retailers have opened in London’s prime pitches, and where they come from. Certainly foreign retailers’ appetite for London representation shows no signs of abating.

GVA will also be releasing an Occupier’s Guide to accompany the map which will give retailers a full information pack helping them not only to decide where to locate but the necessary steps required to secure and open a store in the UK. This will not only encompass the property challenges but those of shop fitting and staffing as well. As a result, GVA can provide a turnkey service if required.

Since the launch of our retail development map, we have delivered numerous presentations to our clients which have received positive feedback. If you would like to know more or arrange a presentation, please do not hesitate to contact us and we would be delighted to present our findings to you.

Central London Retail Development MapHelping retailers understand the West End market

James BurtDirectorRetail Agency+44 (0) 20 7911 [email protected]

P

P

P

P

P

P

P

P

P

PO

PO

PO

PO

Underground

Underground

Underground

Underground

Underground

Underground

Underground

Underground

Underground

Under ground

Underground

Underground

RATHBONE STREET

CHARLOTTESTREET

TOTTENHAM STREET

MORWELL STREET

PERCY STREET

SCALA STREET

NEWM

ANSTREET

BAYLEY STREET

TOTTENHAMCOURT

ROAD

CHARLOTTESTREET

GOODGE STREET

KIRKMAN PLACE

ALFREDPLACE

WINDMILL STREET

COLVILLE PLACE

WHITFIELD

STREET

SOUTH CRESCENT

GOODGE STREET

STORE STREET

STRATFORD

PLACE

GILBERT

STREET

BINNEYSTREET

WEST ONE

SHOPPING CENTRE

WEIGHHOUSE STREET

AVERY ROW

BROOK STREET

STCHRISTO

PHERPLACE

GEES

COURT

PICKERING

PLACE

WEIGHHOUSE STREET

BINNEYSTREET

GILBERT

STREET

THREEKING

SYARD

BROOK STREET

VERESTREET

GROSVENOR SQUARE

BARRETT STREET

BROOKS MEWS

OXFORD STREET

TENTERDEN STREET

THREE KINGS YARD

LANCASHIRE COURT

NEWBOND

STREET

NEWBOND

STREET

DUKES YARD

BROOK STREET

OXFORD STREET

MARYLEBONE LANE

GROSVENOR STREET

NEWBOND

STREET

JAMES

STREET

LANCASHIRE COURT

BROOK STREET

HAMILTO

NPLACE

OLD

CAVENDISHSTREET

BLENHEIMSTREET

WOODSTOCK

STREET

DAVIESSTREET

DERING STREET

SEDLEYPLACE

DAVIES MEWS

OXFORD STREET

DERINGSTREET

DAVIESSTREET

DUKESTREET

SOUTH MOLTON LANE

HOLLES

STREET

HANOVER SQUARE

SOUTH MOLTON STREET

ST ANSELMS PLACE

MARSHALL

STREET

GREAT

TITCHFIELDSTREET

GREEN STREET

CULROSS STREET

OXFORD STREET

PARKLANE

GREEN STREET

WELBECK WAY

UPPER GROSVENOR STREET

UPPER BROOK STREET

UPPER GROSVENOR STREET

WIM

POLE

STREET

MARGARET STREET

MORTIMER STREET

WIGMORE STREET

HINDE MEWS

WOODS MEWS

ALBEMARLESTREET

PARKSTREET

GANTON STREET

BENTINCK STREET

PARKLANE

GRAFTON STREET

LANGHAM

PLACE

MARGARET STREET

GEORGE YARD

LITTLE PORTLAND STREET

CAVENDISH SQUARE

CARLOS

PLACE

JASO

NCO

URT

DUNRAVENSTREET

ORCHARD

STREET

GREAT

PORTLAND

STREET

CARPENTERSTREET

GOLDEN SQUARE

BIRDSTREET

GREAT CASTLE STREET

MARYLEBONE

LANE

BRUTON STREET

MANCHESTER SQUARE

NEWQ

UEBECSTREET

MOUNT STREET

CORK STREET MEWS

GROSVENOR STREET

BEAK STREET

NEWBOND

STREET

GOLDEN SQUARE

LITTLE PORTLAND STREET

UPPER BROOK STREET

LANCER

COURT

HEDDON STREET

DUKESTREET

MILL STREET

MOUNT STREET

WELBECK

STREET

BROWN HART GARDENS

HILLS

PLACEBROWN HART GARDENS

LEES PLACE

PORTM

ANSQ

UARE

SOUTH

AUDLEYSTREET

SWALLOW

STREET

BOURDO

NPLACE

MARKET PLACE

GREAT

PORTLAND

STREET

NORTH

AUDLEYSTREET

CONDUIT

STREE

T

ORCHARD COURT

GREAT MARLBOROUGH STREET

PARKSTREET

PORTMAN SQUARE

UPPER BERKELEY STREET

PORTMAN MEWS SOUTH

MARYLEBONE PASSAGEGEORGE STREET

GREAT

TITCHFIELDSTREET

JACOBS

WELL

MEW

S

GRAYS YARD

REEVES MEWS

POLANDSTREET

MARKET PLACE

TENISON COURT

BERNERSSTREET

SWALLO

WPLACE

HINDE STREET

EDWARDS MEWS

MANDEVILLE

PLACE

BENTINCK MEWS

WIG

MO

REPLACE

GANTON STREET

GRE

ATM

ARLB

ORO

UG

HST

REET

HENRIETTA PLACE

CAVENDISHSQ

UARE

MOUNT ROW

BROADBENT

STREET

COACH

&HORSE

SYA

RD

GEORGE STREET

WELBECK

STREET

BALDERTON

STREET

CONDUITST

REET

GROSVENOR SQUARE

WELLS

STREET

PROVIDENCE COURT

MARGARET STREET

JONESSTREET

LOWER

JOHNSTREET

EASTCASTLE STREET

BARRETT STREET

UPPERJOHN

STREET

PORTM

ANSQ

UARE

PICTON PLACE

BRYANSTON STREET

SEYMOUR STREET

BRUTON STREET

MANCHESTER SQUARE

ROBERT ADAM STREET

MADDO

XST

REET

ARGYLLSTREET

NORTH ROW

MOUNT STREET MEWS

ARGYLLSTREET

CARNABYSTREET

NEW BURLINGTON STREET

FITZHARDINGE STREET

SEYMO

URM

EWS

BEAK STREET

DUKES MEWS

PARKLANE

SPANISH PLACE

GRANVILLE PLACE

OXFORD STREET

LOWNDES COURT

GREAT MARLBOROUGH STREET

DUKESTREET

BROADWICK STREET

MANCHESTER

STREET

BOURDO

NSTREET

GROSVENOR STREET

WIGMORE STREET

BERKELEYM

EWS

WELLS

STREET

NOEL STREET

PARKSTREET

KINGLYSTREET

CORKSTREET

JAMES

STREET

WELLS

MEW

S

PARKLANE

KINGLYSTREET

MADDOX STREET

OLD

QUEBEC

STREET

GLO

UCESTERPLACE

WIGMORE STREET

WINSLEY

STREET

POLAND

STREET

SACKVILLESTREET

RAMILLIES

STREETCHAPEL PLACE

OLDBURLINGTON

STREET

POLLEN

STREET

MASO

NSARM

SM

EWS

MARLBOROUGH COURT

RAMILLIES

STREET

CLIFFORD STREET

HERON PLACE

HAREWO

OD

PLACE

LITTLE ARGYLL STREET

LUMLEY

STREET

VIGO STREET

STG

EORG

ESTREET

HANOVER SQUARE

SAVILEROW

BAKERSM

EWS

BURLINGTON GARDENS

MARGARET STREET

BOYLE STREET

JOHNPRINCES

STREET

SAVILEROW

BLOOMFIELD PLACE

FOUBERTS PLACE

MARSHALLSTREET

BROADWICK STREET

KINGLYCOURT

UPPERJAMES

STREET

REGENTSTREET

BREWER STREET

HARLEYSTREET

WELLS STREET

REGENT

STREET

ADAMS ROW

CARLOS PLACE

OXFORD STREET

GROSVENOR HILL

BRUTON PLACEBOURDON STREET

BEAK STREET

CAVENDISH PLACE

CLEVELAND ROW

WARW

ICKSTREET

GREAT CASTLE STREET

PORTM

ANSTREET

OXFORD STREET

BERKELEY SQUARE

NEW BURLINGTON PLACE

PRINCES STREET

DUFOURSPLACE

REGENT STREET

CAVENDISHSQ

UARE

CARNABYSTREET

RAMILLIES PLACE

HEDDONSTREET

BAKERSTREET

FOUBERTS PLACE

NEWBURGH

STREET

HANOVER STREET

THAYERSTREET

MARYLEBO

NELANE

WIM

POLE

STREET

EASLEYSM

EWS

NORTH ROW

KINGLYCOURT

GLASSHOUSE STREET

BARLOWPLACE

BRU

TON

LAN

E

PORTMAN CLOSE

MOUNT STREET

ET

PARK LANE

CROSS KEYS CLOSE

GREAT PULTENEYSTREET

KEMPS COURT

PORTLAND MEWS

BRIDLELANE

BRIDLELANE

STAFFORD STREET

PICCADILLYPLACE

PORTLAND PLACE

D`ARBLAY STREET

BERNERSSTREET

NEWMAN

PASSAGE

BREWER STREET

THEPLAZA

GEORGE STREET

CHAPEL PLACE

NORTH

BERWICK

STREET

BERWICK

STREET

BLANDFORD STREET

NOEL STREET

MORTIMER STREET

LITTLE TITICHFIELD STREET

BOOTHS PLACE

BLANDFORD STREET

HAY HILL

GREAT

CUMBERLAND

PLACE

MORTIMER STREET

SILVER PLACE

MORTIMER STREET

BERNERSPLACE

WELBECK

STREET

BULSTRODE PLACE

BLANDFORD STREET

MAR

YLEBONE

HIG

HSTREET

SHERATON STREET

BERWICK

STREET

JERMYN STREET

RIDING HOUSE STREET

PETER STREET

NEWM

ANSTREET

KENDALLPLACE

GREAT WINDMILL STREET

BROADSTO

NEPLACE

GREATPULTENEY

STREET

D`ARBLAY STREET

QUADRANTARCADE

PICCADILLY

QUEBEC MEWS

SACKVILLESTREET

WARDOUR

STREET

RBLE ARCH

LOWER

JAMESSTREET

AIRSTREET

CHILTERNSTREET

INGESTREPLACE

BABMAESSTREET

BRICKSTREET

MO

NTAGU

STREET

OLDBOND

STREET

WARDOUR

STREET

LEXINGTONSTREET

BERWICK

STREET

SMITHS COURT

WARDOUR

MEWS

BROADWICK STREET

CHURCHPLACE

VINE STREET

WELLS STREET

PICCADILLY

HOLLEN STREET

LIVONIA STREET

HOPKINSSTREET

ALBANYCOURT

YARD

SOUTH

AUDLEYSTREET

LEXINGTONSTREET

AIRSTREET

MARYLEBONE LANE

BULSTRODE STREET

SHERWOOD

STREET

DENMAN STREET

SHERWOOD

STREET

AIRSTREET

DOVERSTREET

GLASSHOUSE STREET

BERKELEYSTREET

GREAT

TITCHFIELDSTREET

ALDFORD STREET

DUCKLANE

ALL SOULS PLACE

GREAT

PORTLAND

STREET

MANCHESTER

STREET

GREAT

CHAPELSTREET

RIDING HOUSE STREET

CHAPLE PLACE

SOUTH

DEVONSHIRE STREET

WHEATLEY STREET

BEAUMONT STREET

BEAUM

ON

TM

EWS

GREAT

PORTLAND

STREET

NEW CAVENDISH STREET

AYBRO

OK

STREET

DORSET STREET

DE WALDEN STREET

MARYLEBONE ROAD

ST VINCENT STREET

MARYLEBONE ROAD

ASHLANDPLAC

E

BOLSO

VERSTREET

CHILTERNSTREET

NEW CAVENDISH STREET

NOTTINGHAM STREET

WESLEY

STREET

MAR

YLEBONE

STREET

WEYMOUTH STREET

CLARKES MEWS

DUCHESS STREET

WESTM

ORLAND

STREET

BROW

NINGM

EWS

WEYMOUTH STREET

GARBU

TTPLAC

E

GREAT

PORTLAND

STREET

PORTLAND

PLACE

LANGHAM STREET

MAR

YLEB

ONE

HIG

HST

REET

DEVONSHIRE STREET

MOXON STREET

MAYBU

RYCO

URT

OLDBURY PLACE

NO

TTING

HAMPLACE

BEAUMO

NTSTREET

CARBURTON STREET

PADDINGTON STREET

GREAT

PORTLAND

STREET

DORSET STREET

CRAM

ERSTR

EET

NOTTING

HAM

PLACE

PADDINGTON STREET

HALLAMSTREET

NEW CAVENDISH STREET

GREENWELL STREET

GLENTW

ORTH

STREET

CLEVELANDSTREET

WHITFIELD

STREET

HOWLAND

MEWS

EAST

GREAT

PORTLAND

STREET

MARYLEBONE ROAD

CAPPER STREET

GOODGE STREET

CLIPSTONE STREET

WHITFIELD

STREET

GLENTW

ORTH

STREET

HOWLAND STREET

MIDDLETO

NPLACE

CLEVELANDSTREET

HANSON

STREET

FITZROYSTREET

CLEVELANDSTREET

MAPLE STREET

BOLSO

VERSTREET

GRAFTON WAY

YORK STREET

DAVIDM

EWS

NASSAUSTREET

CHARLOTTESTREET

MAPLE STREET

TOTTENHAM STREET

NEW CAVENDISH STREET

LANGHAM STREET

CLIPSTONE

MEW

S

GILDEA STREET

ELCOMBE STREET

KENRICKPLACE

CHILTERNSTREET

CANDOVERSTREET

DURWESTO

NM

EWS

CLEVELANDSTREET

BERKELEY ARCADE

GO

SFIELDSTREET

CYPRESSPLACE

DORSET STREET

CLEVELANDSTREET

ALLSOP

PLACE

FOLEY STREET

BOURLETCLOSE

SHERLOCK

MEW

S

NEW CAVENDISH STREET

EET

OG

LESTREET

GREAT

TITCHFIELDSTREET

NSLANE

PORTER STREET

BICKENHALL STREET

GREAT

TITCHFIELDSTREET

CRAWFORD STREET

BAKERSTREET

TOTTENHAMCOURT

ROAD

TORRINGTON PLACE

CONWAY

STREET

CHARLOTTEPLACE

GREAT

TITCHFIELDSTREET

GOODGEPLACE

CLIPSTONE STREET

RIDINGHOUSE STREET

FITZROY SQUARE

SOUTH STREET

DEANSTREET

DEAN

ERY

STRE

ET

STJAMES`S

STREET

MEARD STREET

QUEEN

STREET

RUSSELL COURT

THE ECONOMIST PLAZA

ARCHER STREET

PICCADILLY

CLARGES MEWS

TILNEY STREET

PARKLANE

SOUTH STREET

BABMAESSTREET

JERMYN STREET

MAYFAIRPLACE

LITTLE ST JAMES`SSTREET

RYDER STREET

KING STREET

STAFFORD STREET

CHARLES STREET

BENNET STREET

CHESTERFIELDSTREET

WINNETT STREET

ST JAMES SQUARE

CARLISLE STREET

CARLISLE STREET

DUKEOF

YORKSTREET

FLAXMAN COURT

RICHMOND

MEW

SST

ALBANSSTREET

BOLTONSTREET

JERMYN STREET

CLARGES STREET

FITZMAURICEPLACE

GREENSCOURT

PICCADILLY

SOUTH

AUDLEYSTREET

CARLTON STREET

DEANSTREET

CHARLES II STREET

BRICK STREET

HANWAY STREET

STJAMES

SQUARE

TROCADERO

STALBANS

STREET

RATHBONEPLACE

STANHOPE

ROW

PERRYSPLACE

GREAT

CHAPELSTREET

SHAVERSPLACE

WATERLOO

PLACE

CURZ

ON

STRE

ET

RUPERTSTREET

REGENTSTREET

RICHMOND BUILDINGS

HANWAY PLACE

CHAPONEPLACE

SOHOSTREET

ORMOND YARD

APPLE TREE YARD

HAYMARKET

BATEMAN STREET

CHARLES II STREET

BURYSTREET

NORRIS STREET

OXFORD STREET

SHAF

TESB

URY

AVEN

UE

WARDOUR

STREET

PERCY MEWS

GREATW

INDMILL

STREET

STEPHEN

STREET

STEPHEN MEWS

RUPERTSTREET

CHENIES STREET

ALFRED MEWS

ALBEMARLESTREET

GRESSE STREET

HUNTLEYSTREET

WARDOUR

STREET

DUKESTREET

STJAM

ES`S

TISBURY COURT

ROYALTY

MEW

S

ST ANNES COURT

OLD COMPTON STREET

DUKESTREET

BOURCHIER STREET

STJAMES`S

STREET

REGENTSTREET

PALL MALL

ST JAMES`S MARKET

STJAMES

SQUARE

BERKELEYSTREET

MASONS YARD

CLARGES STREET

SHAF

TESB

URYAV

ENUE

SOHO SQUARE

JERMYN STREET

NORTH CRESCENT

BOURCHIER STREET

STRATTONSTREET

CURZON STREET

TROCADERO

SOHO SQUARE

ARLINGTONSTREET

LANS

DOW

NERO

W

HAM YARD

COVENTRY STREET

TREBECKSTREET

FALCONBERGM

EWS

DEANSTREET

CHESTERFIELDG

ARDENS

BATEMANS

BUILDINGS

OXENDONSTREET

DANSEY PLACE

RYDER STREET

WARDOUR

STREET

STANHOPE GATE

GERRARD STREET

FRITHSTREET

HALF MOON STREET

WATERLOO

PLACERIDGEMOUNT

STREET

SHAFTESBURY AVENUE

PALL MALL

HERTFORD STREET

CLEVELANDPLACE

ROYAL OPERAARCADE

CARLTONGARDENS

PANTON STREET

HAYMARKET

SHEPHERD MARKET

PICCADILLY

PARK PLACE

CRAIGS COURT

LEICESTERSTREET

SAVOYBUILDINGS

SAVOYCOURT

GATE STREET

CAXTON WALK

NEW OXFORD STREET

WILLIAM IV STREET

BULL INNCOURT

WILLIAM IV STREET

JAMESSTREET

BRICK STREET

SOUTHAM

PTON

ROW

PIED BULL

PLACE

SMARTS PLACE

ARNE STREET

NEWPORT COURT

MAR

LETT

COUR

T

GREAT RUSSELL STREET

BUCKINGHAMSTREET

BUCKNALL STREET

WARWICK HOUSE STREET

OLDPARK

LANE

STREATHAM STREET

INIGO PLACE

PALL MALL

VICTO

RIAEM

BANKMENTKE

MBLE

STRE

ET

CH

ARIN

GC

RO

SSR

OAD

BETTERTON STREET

THE

ARCHES

EARNSHAWSTREET

SHORTS GARDENS

FLITCROFT STREET

BLUE BALL YARD

THEOBALDS ROAD

DRYDENSTR

EET

NEW OXFORD STREET

JAMESSTREET

STM

ARTINS

LANE

MONTAGUESTREET

STJAMES`S

STREET

BAINBRIDGE STREET

NEWTO

NSTREET

DRAGONSYARD

HANOVERPLACE

TOW

ERCO

URT

GOSLETT YARD

CATHERINE STREET

GREAT QUEEN STREET

GREAT NEWPORT STREET

LEICESTERCO

URT

CURZON STREET

DUNCANNON STREET

RUSS

ELL

STRE

ET

OLDGLOUCESTER

STREET

NEW OXFORD STREET

HIGH HOLBORN

BLOOMSBURYSQUARE

EXCHANGECOURT

EXETER STREET

ANGEL COURT

WEST STREET

TRAFALGAR

SQUARE

CHANDOS PLACE

FLORAL STREET

ADELAID

ESTR

E ET

WHITCOM

BSTREET

BEDFORDSTREET

DERBYSTREET

FILTCROFT STREET

COVENT GARDEN

LEICESTER SQUARE

MATTHEWS

YARD

CARRINGTO

NSTREET

WILD COURT

WHITE

HORSESTREET

STREATHAMSTREET

OLD COMPTON STREET

LITTLE NEWPORT STREET

ADAMSTREET

RUSSELL SQUARE

MANETTE STREET

EXETER STREET

HERTFORD STREET

NEWPORT

PLACE

MERCER STREET

COVENT GARDEN

STJAMES`S

PLACE

TAVISTOCK STREET

GARRICK STREET

BEDFORDPLACE

HOP GARDENS

BAINBRIDGE STREET

STEDMAN

PLACE

WHITCOM

BSTREET

HIGH HOLBORN

WILLOUGHBY

STREET

YARMOUTH PLACE

GREAT RUSSELL STREET

LANGLEYCOURT

GREAT RUSSELL STREET

BLOOMSBURY PLACE

MUSEUM

STREET

VERNON PLACE

BROAD

COUR

T

SPRINGG

ARDENS

DYOTTSTREET

CORNER

HOUSE

STREET

BLOOMSBURYCOURT

DURHAM HOUSE STREET

CAMBRIDGECIRCUS

SHORTS GARDENS

BURLEIGH STREET

HORSE &

DOLPHIN YARD

GREAT QUEE

NST

REET

DRURYLANE

CROWN COURT

BLOOMSBURY

STREET

SICILIAN AVENUE

GALEN PLACE

CRAVENPASSAGE

COVENT GARDEN

CRANBOURN STREET

LONGS COURT

HOBHOUSECOURT

SHAFTESBURYAVENUE

WHITCOMB COURT

DYOTTSTREET

PANTON STREET

STACEYSTREET SHORTS GARDENS

NEW OXFORD STREET

HERTFORD

STREET

MO

NM

OU

THST

REE

T

SHAF

TESB

URY

AVEN

UE

HUNTS COURT

UPPER

STM

ARTIN

SLAN

E

SHAFTE

SBURY

AVEN

UE

GRAPESTREET

PANTON STREET

YORK PLACE

ST GILES HIGH STREET

VILLIERS STREET

ST JAMES`SPLACE

SANDRINGHAM BUILDINGS

WAT

ERGA

TEW

ALK

CRAVENPASSAGE

GEORGE COURT

ORANG

EYARD

DRURY LANE

FRITHSTREET

BLOOMSBURYSTREET

HENRIETTA STREET

BLOOMSBURYSQUARE

COVENT GARDEN

LONG

ACRE

EARLHAM STREET

SHORTS GARDENS

SAVOYWAY

WILD STREET

DRURY LANE

NEW

COM

PTON

STRE

ET

MUSEUM

STREET

DUDLEYCOURT

BANBURYCOURT

ROSE STREET

LONG ACRE

PARKER STREET

CECIL COURT

COSMO PLACE

BURLEIGHSTREET

BEDFORDSTREET

ROSE

STREET

ROMILLY STREET

ROMILLY STREET

BATEMAN STREET

TOTTENHAMCOURT

ROAD

QUEENSQUARE

VICT

ORIA

EMBA

NKM

ENT

LITCHFIELD STREET

BEDFORD COURT

WEST

CENTRAL STREET

BURYPLACE

EXETERSTREET

WEDGWOOD MEWS

CROWN COURT

OLD BREWERS YARD

MERCER STREET

ADELINEPLACE

CRANBOURN STREET

THOMAS NEALS

MAR

LETT

COUR

T

MO

NMO

UTH

STRE

ET

TOW

ERCO

URT

ST GILES PASSAGE

FLORAL STREET

CHING

COURT

MAYS COURT

GILBERT PLACE

GOWER

STREET

BEDFORD AVENUE

WHITCO

MB

STREET

ADMIRALTYARCH

TRAFALGAR SQUARE

ENDELL STREET

BETTERTON STREET

SHAF

TESB

URY

AVEN

UE

CHARINGCROSSSPRING GARDENS

PHOENIX STREET

NEWTON

STREET

DENMARK STREET

BEAR STREET

KING STREET

MOOR STREET

MACCLESFIELD

STREET

ROMILLY STREET

LISLE STREET

ST MARTINS COURT

ROSE&

CROWN

YARD

CHARINGCRO

SSROAD

GERRARDPLACE

MAIDEN LANE

NOTTINGHAMCOURT

EMBA

NKM

ENT

PLAC

E

LEICESTERPLACE

SWISS COURT

LANGLEY STREET

BUCKNALL STREET

GREEKSTREET

BLOOMSBURY WAY

KINGSWAY

ST MARTINS PLACE

STM

ARTINSSTREET

OXENDONSTREET

STM

ARTINSSTREET

COCKSPUR COURT

IRVING STREET

SUFFOLKSTREET

ORANGE STREET

ORANGE STREET

DOWN

STREET

SUFFOLK PLACE

GREAT SCOTLAND YARD

WHITEHALL

JOHN ADAM STREET

CRAVEN STREET

SOUTHAMPTONSTREET

TAVISTOCK STREET

SOUTHAMPTONROW

LITTLE RUSSELL STREET

STUKELEY STREET

MACKLINSTREET

PARK

ERST

REET

BARTER STREET

LONG

ACRE

NORTHUMBERLAND AVENUE

BOWSTREET

SOUTHAMPTONPLACE

AGARSTREET

WELLINGTON STREET

COPTIC

STREET

SPRI

NGG

ARDE

NS

CARTINGLANE

KEELEY STR

EET

LUMLEYCOURT

MARKET MEWS

STM

ARTIN

SPLAC

E

SHEPHERD STREET

ENDELL STREET

COCKSPUR STREET

PALL MALL EAST

STRAND

NORTHUMBERLAND STREET

STRAND

HIGH HOLBORN

SHELTON STREET

NEAL STREET

WEST STREET

RUSSELL STREET

LEICESTER SQUARE

BEDFORDBURY

NEAL STREET

TOWER STREET

NEAL

SYA

RD

SUTTON ROW

ST GILES HIGH STREET

CHARINGCRO

SSRO

AD

NEW ROW

MERCERSTREET

EARLHAM STREET

PITTS HEAD MEWS

MONTREAL PLACE

LINCOLNSINN

FIELD

HO

UGH

TON

STREET

DRURY LANE

KEANSTREET

KEMBLE STREET

TWYFORD PLACE

NEW INN PASS

PORTUGAL STREET

SARDINIA STREET

SAVOYSTEPS

KINGSW

AY

GATESTREET

SAVOYSTREET

KINGSWAY

SAVOY ROW

TAVI

STOC

KST

REET

LANCASTERPLACE

REMNANT STREET

WELLINGTON

STREET

INDIA PLACEALDW

YCH

PICCADILLY

BRYDGES PLACE

GOODWINS COURT

WALKERS

COURT

LANCASHIRE COURT

PICCADILLY

ARCADE

BUSH

HOUSE

ARCADE

BUCKINGHAMARCADE

TYLERS COURT

HEATHCOCKCOURT

PRINCESARCADE

LITTLE MARLBOROUGH STREET

FOUBERTS PLACE

ROYAL ARCADE

GLOBE YARD

CROWN

PASSAGE

RUPERT COURT

EXCEL COURT

BURLINGTONARCADE

(90) (ESTIMATED)

(80) (ESTIMATED)

(455) (ESTIMATED)

(100) (ESTIMATED)

LANGHAM HOTEL

THE RITZ HOTEL

BROWNS HOTEL

GROSVENOR HOUSE MARRIOTT HOTEL

THE DORCHESTER HOTEL

HILTON HOTEL

FOUR SEASONS HOTEL

HILTON HOTEL

PATISSERIE

VALERIE

ESSIE

CARPETS

CAFE

CONCERTO

DE BEERS

JEWELLER

MAPPIN

& WEBB

ROYAL ACADEMY OF ARTS

ROYAL ACADEMY OF ARTS

PRET A

MANGER

ITSUVODAFONE

TUMI TRAVEL GO

ODS

STARBUCKS COFFEE

RICHOUX CAFE

PAUL BAKER & CAFE

LA MAISON

FREY WILLE

WASABI

PRET A

MANAGER

LLOYDS TSB

BANK

SANTANDER

BANK

EAT

CAFE

NERO

MO

NEYCORP

THE STING

BARB

OU

R

GIL

LY H

ICKS

HO

LLIS

TER

CO

CLARK

’SSH

OES

SUPERDRY

AUST

IN R

EED

VIYE

LLA

LADIE

S WEA

RCH

ARLE

S TYR

WHI

TT

MO

SS

UN

IQLO

OFF

ICE

LUSH

COAC

H

CAFE

ROYA

L

WO

LFO

RD NESP

RESS

O LOTU

S O

RIGI

NALS

GIFT

S

ITALIAN FACTORY

OUTLET M

ENS WEAR

CATH

KIDSTON

FORTNUM

AND MASO

N

HATCHARDS BOO

KS

RAIL EUROPE

LLADRO

VACANT

VACANT

KAHVE DUNYASI CAFE

RUSH HAIRDRESSING

WATERSTO

NES

NATWEST BANK

TIGER OF SW

EDEN

CICHETTI ITALIAN

RESTERAUNT

BARBOUR

GROSVENO

R SHIRTS

CRITERION BRITISH

RESTAURANT

COOL BRITANNIA GIFTS

PIZZA HUT

OSPREY

TESCO METRO

LILLYWHITE’S

VACANT RESTAURANT

EAT

ITSU

MITSUKOSHI DEPARTMENT STORE

JAPAN CENTRE DELICATESSEN

TOKU JAPANESE

RESTAURANTAPOLLO

MOUNTAIN WAREHOUSE

OFFICE

COSTA COFFEE

WHITARD

VACANT

HAUSER &

WIRTH

ART

GALLERY

OFFICE

COSTA CO

FFEE

BIAGIO PICADILLY

ITALIAN RESTERAUNT

ENT

PRET A

MAN

GER

KFC

CREST OF

LON

DO

N

EVANS

TOPSH

OP

WALLIS

GEO

X

MO

THERCARE

HO

LLAND

& BARRETT

ANN

SUM

MERS

DO

ROTH

Y PERKINS

SUPERD

RUG

NEXT

NEW

LOO

K

MO

NSO

ON

RUSSELL & BRO

MLEY

BOO

TS

CLAIRE’S

LA SEN

ZA

CLARKS SH

OES

VOD

AFO

NE

SCHU

H

MA

RKS & SPENCER

ASICS

PIZZA HU

T

PRIMARK

OFFICE

URBAN

OU

TFITTERS

RIVER ISLAND

BERSHKA

ZARAPAND

ORA

SELFRIDG

ES

FRENCH

CON

NECTIO

N

JANE N

ORM

AN

GAP

THE BO

DY SH

OP

ALDO

INTIM

ISSIMI

H&M

FOREVER 21

THE D

ISNEY STO

RE

DEBEN

HAM

S

SUN

GLASS H

UT

FOSSIL

FLIGH

T CASE

STARBUCKS

HO

USE O

F FRASER

JOH

N LEW

IS

G STAR

COAST

THE BO

DY SH

OP

GEO

X

VACANT

CARPHO

NE W

AREHO

USE

CLARKS SHO

ES

BHS

H SAM

UEL JEW

ELLERS

ZARA

H&M

NIKETO

WN

TOPSH

OP & TO

PMAN

MISS SELFRID

GE

URBAN

OU

TFITTERS

SCHU

H

HSBC BAN

K

OFFICE SH

OES

ALDO

H&M

UN

IQLO

LA SENZA

3 STORE

GLOBAL GIFTS

SOCCER SCEN

E SPORTS GO

OD

S

HM

V

CALL IT

SPRING

SHO

ES

AMERICAN

APPAREL

ESPRIT

MO

SS

O2

COLO

R COLO

R

HIG

H & M

IGH

TYW

ATERSTON

ES

PHO

NES 4U

CLAIRE’S

AN

N SU

MM

ERS

BOO

TS

UN

ITED CO

LOU

RS OF BEN

ETTON

RUSH

HAIRD

RESSING

GLS LAD

IES

ACCESSORIES

CURRYS &

PC WO

RLD

IMPERIALE M

ENS

WEAR

WESTSID

E

SOU

VENIRS

& GIFTS

KING

DO

M O

F

SOU

VENIRS

EAT

THE

BOD

Y

SHO

P

HA

LIFAX

WA

SABI

PRET A

MAN

GER

HO

LLAND

&

BARRETT

VACAN

T

VACAN

T

VACAN

T

VACAN

T

VACAN

T

LLOYD

S TSB

PRIMA

RK

MCD

ON

ALD’S

THE CARPH

ON

E

WAREH

OU

SE

BURTO

N &

DO

ROTH

Y

PERKINS

STARBUCKS

DO

NELLI

SHO

ES

ALL BARO

NE

VACANT

OFFICE

VACANT

LON

DO

N TRAVEL

GO

OD

S

PEACH G

IFTS

ECCO SH

OES

WASABI

HSBC

STARBUCKS

3 STORE

WATERSTO

NES

ADID

AS

LLOYD

S TSB BANK

RUSSELL &

BROM

LEY

EE TELEPHO

NES

BOO

TS

DO

ROTH

Y PERKINS &

BURTO

N

OM

EGA

HM

V

BOO

TS

O2 VODAFONE

ZARA

NEXT

SWAROVSKI

MASSIM

O DUTTIPULL & BEAR

UN

IQLO

ALDO

RIVER ISLAND

LON

DO

N G

IFTS

TIE RACK

MCD

ON

ALD’S

EE TELEPHO

NES

WEST EN

D LU

GG

AGE & G

IFTSCARPISA

FOO

T LOCKER

ERNEST

JON

ES

JD SPO

RTS

VISION

EXPRESS

PAND

ORA

3 STORE

UN

ITED CO

LOU

RS

OF BEN

ETTON

TEZENIS

GAP

MAN

GO

BERSHKA

ZARA

RIVER ISLAND

NEW

LOO

K

NEXT

BOOTS

MCDO

NALD’SVISIO

N EXPRESS

JACK & JONES

MUJI

MO

SS

SWATCH

PHO

NES

4 U

WATCH

ES OF

SWITZERLAN

D

VERO M

ODA

MARKS & SPEN

CER

H SAM

UEL JEW

ELLERS

FLIGH

T

CENTRE

COO

LAWAY

UN

DER ALTERATIO

N

SWARO

VSKI

RETRO

LONDO

N

JESSOPS

VOD

AFON

E

LON

DO

N SO

UVEN

IRS

& LUG

GAG

E

SANTAN

DER

BANK

THE CARPHONE

WAREHO

USE

CLARKS SHO

ES

UN

DER ALTERATIO

N

WA

LK SHO

ES

FOO

T LOCKER

FRENCH

EYE

HARM

ON

Y

ADU

LT SHO

P

PIZZA HU

T

BENZER

BELLO UO

MO

UND

ER ALTERATION

UND

ER ALTERATION

SOU

VENIRS

SOU

VENIRS

OFFICE SH

OES

OFFICE SH

OES

SUBW

AY

LON

DIS

CUBE G

IFTS

ROCK LO

ND

ON

MR TO

PPER’S

CHIN

A EXPRESS

SOU

VENIRS

DIW

AN

MID

EAST REST

OFFICE

OFFICE

SOU

VENIRS

LIVE 4

LOVE

OFFICE

APARTMEN

T 58

PUBLIC H

OU

SE

OFFICE

SUBW

AY

VACANT

ROY ROBSON

T M LEWIN

SAKARE

PRONOVIAS

VICTORINOX

RBS BANK

BOUDI CLOTHING

VACANT

MEPHISTO SHOES

BONHAMS AUCTIONEERS & VALUERS

RM WILLIAMS

CHRISTIE’S

IVORY SHOES

VACANT

KRONOMETRY 1999 JEWELLER

MARITHE FRANCOIS GIRBAUD

FROST JEWELLER

RUSSELL &

BROMLEY

VICTORIA’S SECRET

BALLY

ANYA HINDMARSH

TARA JARMON

FOLLI FOLLIE

HUGO BOSS

CAR SHOES

PAL ZILERI

CANALI

HSBC BANK

BREITLING

CORNELIANI

CHURCH’S SHOES

BELSTAFF

MISSONI

ZILLI

TORY BURCH

MIU MIU

HERMES

BURBERRY

LOUIS VUITTON

WATCHES OF

SWITZERLAND

GEORG

JENSEN

MICHAEL KORS

LORO PIANA

CHANEL

DIOR

VACANT

BOUCHERON

ASPREY

JEWELLER

BVLGARI

PIAGET

MOUSSAIEFF

CHANEL

CHAUMET

CARTIER

BOODLES

MIKIMOTO

TIFFANY & CO

CHANEL

CAMPER SHOES

ROLEX

AKRIS CLOTHING

LEVIEV

SAINT LAURENT

GUCCI

VERTU

CARTIER

ETRO

MARINA

RANALDI

DKNY

(& VACANT RESTAURANT UNDER)

DAVID MORRIS

JEWELLER

FENDI

RALPH LAUREN

CHILDRENS WEAR

S J PHILIPS

ANTIQUES

OPERA ART

GALLERY (RETAIL)

BYFORD

BATEEL DELI

SARAH

PACINI

VACANT

VACANT

VACANT

VACANT

VACANT

ORO

GOLD

LUNGTA DE FANCY

FENWICK

EMPORIO ARMANI

MULBERRY

PINET

BALLY

WEMPE

JEWELLER

COACH

HALCYON ART

GALLERY (RETAIL)

HALCYON ART

GALLERY (RETAIL)

RICHARD GREEN

ART GALLERY (RETAIL)

THE FINE ART SOCIETY

ART GALLERY (RETAIL)

HUBLOT JEWELLER

ANNE FONTAINE

UNDER ALTERATION

JIMM

Y CHOO

SMYTHSON OF

BOND STREET

ERMENEGILDO

ZEGNA

DOLCE &

GABBANA

ERMENEGILDO

ZEGNA

GRAFF

RALPH

LAUREN

SALVATORE FERRAGAMO

JOSEPH

CHATILA

MAX MARA

PRADA

BOTTEGA VENETA

BOTTEGA VENETA

MONT BLANC

OMEGA

DAKS

DOLCE & GABBANA

ALEXANDER

MCQUEEN

TOD’S

GREEN PARK TUBE

GINA

SHOES

KIKO MAKE

UP MILANO

OMEGA

FRENCH

CONNECTION

KAREN MILLEN

TED BAKER

APPLE

LACOSTE

LONGCHAMP

& OTHER STORIES

NATWEST

ARMANI EXCHANGE

ALL SAINTS

H&M

BANANA REPUBLIC

COS

DESIGUAL

GAP

JAEGER

HAMLEY’S

HUGO

BOSS

JUICY

COUTURE

MOLTON

BROWN

7 FOR ALL

MANKIND

MICHAEL KORS

FURLA

HOBBS

CAMPER SHOES

KIPLING

CLARKS

SHOES

CHURCH’S

SHOES

THE PEN

SHOP

BARKER

SHOES

HOSS

INTROPIA

ESPRIT

LEVI’S STORE

REISS

CALVIN KLEIN JEANS

GUESS

ANTHROPOLOGIE

MASSIMO DUTTI

BROOKS BROTHERS

TIMBERLAND

TOMMY HILFIGER

MAPPIN & WEBB

RUSSELL &

BROMLEY

T M LEWIN

FOLLI FOLLIE

HACKETT

GANT

BOSE

UNDER

CONSTRUCTION

UNDER

CONSTRUCTION

UNDER

CONSTRUCTION

UNDER

CONSTRUCTION

ZARA

MANGO

J CREW

WATCHES OF SWITZERLAND

HACKETT

GODIVA

SWAROVSKI

HSBC

ZARA

HOME

CRABTREE &

EVELYN

BURBERRY

PICCADILLY TUBE

£400 ZA

£800 ZA

£950 ZA

£1,000 ZA

£315 ZA

£850 ZA

£330 ZA

£200 ZA

£300 ZA

£305 ZA

£400 ZA

£575 ZA

£750 ZA

£800 ZA

£525 ZA

£350 ZA

£225 ZA

£275 ZA

£260 ZA

£600 ZA

£725 ZA

£450 ZA£550 ZA

£550 ZA

£760 ZA

£500 ZA

£375 ZA

£425 ZA

Q4 – 2013 - Headline Rent GuideLocation Headline Rent

Zone AOxford Street (Marble Arch) £575Oxford Street (Selfridges) £750Oxford Street (John Lewis) £800Oxford Street (Great Portland) £525Oxford Street (Tottenham Court Rd) £350New Oxford Street £225Regent Street (Top) £600Regent Street (Middle) £725Regent Street (Bottom) £375New Bond Street (Top) £400New Bond Street (Middle) £800New Bond Street (Bottom) £950Old Bond Street £1,000Piccadilly (Regent Street) £260Piccadilly (Burlington) £275Jermyn Street £300Burlington Arcade £850Albermarle Street £200Dover Street £330Bruton Street £315Mount Street £400South Molton Street £425Marylebone High Street £305Carnaby Street £450Long Acre £550James Street £760King Street £550Covent Garden Market £500Kings Rd (East) £420Sloane Street £800Sloane Street (South)/Sloane Square £450 Note:The following streets operate with 30 feet zones:-Oxford, Regent, Bond, Piccadilly, Victoria, Kensington High St

TOTTENHAM COURT ROADEASTERN TICKET HALL

DUE FOR COMPLETION 2017

TOTTENHAM COURT ROADWESTERN TICKET HALL

DUE FOR COMPLETION 2017

BOND STREETWESTERN TICKET HALL

DUE FOR COMPLETION 2016

BOND STREETEASTERN TICKET HALL

DUE FOR COMPLETION 2016

BOND STREETNORTH TICKET HALL

DUE FOR COMPLETION 2016

CLARIDGES HOTELMARRIOTT HOTEL

MARRIOTT HOTEL

MILLENNIUM MAYFAIR HOTEL

THE CONNAUGHTHOTEL

CHARING CROSS

TUBE

COVENT GARDEN

TUBE

TOTTENHAM COURT ROAD TUBE

OXFORD CIRCUS TUBE

BOND STREET TUBE

MARBLE ARCH TUBE

LEICESTER SQUARE

TUBE

8M

18M

40M

12M

20M

20M

11M

17M

10M

50

96

10

100

65

38

75

40

42

49

79

33

26

Source: FSP

0 500 1000 1500 2000 2500 3000

Tourist SpendWorker SpendResident Spend

Spend (£m)

Piccadilly

Sloane Street

Kings Road

Regent Street

Bond Street

East Oxford Street

West Oxford Street

Knightsbridge

Shopper Spend

794 19

1,556 334

1,055 220

521180612

608

881

149

137 90

133

20 183

380 292

332

555

542

Mercer Yard, 6/14 Mercer StreetLandlord: The Mercers Company Size: 42,000 sq ft retail plus 30,000 sq ft of residential Planning approved. Mid 2014 start

27/32 King StreetLandlord: Capital & CountiesSize: 34,000 sq ft retail plus 37 flatsPlanning approved. On site Mid 2014

St James’ Market, 14/22 Regent Street and 52/56 Haymarket Landlord: The Crown EstateSize: 210,000 sq ft of offices and 50,000 sq ft retail Planning approved. On site 2014

107/111 Charing Cross Road Landlord: Soho Estates Size: 230,000 sq ft mixed use.Timing TBA

Centre Point Tower, 103 New Oxford Street Landlord: AlmacanterSize: 46,000 sq ft retail plus 95 apartments Completion: 2016

111/125 Oxford Street Landlord: Peterson Group Size: 65,000 sq ft of offices, plus 25,000 sq ft retail and 15,000 sq ft residential Planning approved. Completion: 2015

69/89 Oxford Street Landlord: Great Portland Estates Size: 39,000 sq ft retail plus 83,000 sq ft of offices Planning approved. Completion 2016

149/151 Oxford Street Landlord: AXA REIM Ltd Size: 26,000 sq ft of retail and 14,000 sq ft of offices plus 6 apartmentsCompletion: Early 2015

163/167 Oxford Street Landlord: Aviva Size: 68,000 sq ft offices and 17,000 sq ft retail Planning approved

14/40 Oxford Street (Phase 2) Landlord: OrianaSize: 75,000 sq ft retail plus 18 apartments part pre-let to Schuh and Primark.Completion: 2016

70/88 Oxford Street Landlord: Great Portland Estates Size: 20,000 sq ft retail plus 89 flats Planning approved

61/69 Oxford Street Landlord: Dukelease Properties Ltd.Size: 35,00 sq ft of retail (pre-let to Zara) 35,000 sq ft offices and residential.On Site. Completion February 2015

Plaza Shopping Centre, 122 Oxford Street Landlord: Sirosa Libert Ltd Size: 193,000 sq ft of offices and 73,000 sq ft of retail Planning approved. On site 2014

35/50 Rathbone Place Landlord: Great Portland Estates Size: 217,000 sq ft of offices plus 162 apartments, 42,000 sq ft retail Planning approved. Completion: 2016

40 Leicester Square Landlord: Edwardian Group Size: 220,000 sq ft mixed use scheme (hotel, retail, cinema and residential)Timing TBA

48/50 Leicester Square Landlord: Private InvestorSize: 135,000 sq ft offices and 32,000 sq ft of retail On site 2014

82/84 Piccadilly Landlord: British Land Size: 59,000 sq ft of offices and 14,000 sq ft of retail and 15,000 sq ft spa plus 38,000 sq ft pre let to The Kennel ClubPlanning approved

W4. 135/167 Regent Street Landlord: The Crown EstateSize: 140,000 sq ft of offices and 47,000 sq ft of retail (pre let to J. Crew and Watches of Switzerland)Opening Spring 2014

W5, 169/183 Regent Street Landlord: The Crown Estate Size: 150,000 sq ft of offices and 45,000 sq ft of retail Completion 2015

7/10 Hanover Square Landlord: Legal & General Size: 47,000 sq ft of offices and 9,000 sq ft of retail Completion March 2017

64-72 New Bond Street Landlord: Great Portland Estates Size: 250,000 sq ft of offices and 47,000 sq ft of retail Planning approved. Completion 2018

34/36 Bruton Street Landlord: Lancer Size: 12,500 sq ft of offices and 7,500 sq ft of retail Planning approved. On site 2014

354-356 Oxford Street Landlord: ReAssure Limited / LUL.Size: 6,000 sq ft of retail and 11,000 sq ft of residential On Site. Planning approved. Completion 2017

75/85 Shaftesbury Avenue Landlord; Dolford Property Holdings.Size: 87,000 sq ft office space, 17,000 sq ft of retail and 5 apartments.Planning approved Jan.2013

96

18M

Footfall Index – 100 represents the location with the highest footfall(Source: FSP)

The following Landlords predominantly own and manage the tenant mix in the areas shaded

Tube Annual Exit Figure in Millions

Crown Estate

Shaftesbury Plc

Capital and Counties

Key

3

One thing that is clear from any post mortem carried out on recession-hit high streets and less prime shopping centres (certainly not the major regional centres) is the appreciation of a good tenant mix, between good local operators and national multiples. Whilst landlords, especially in shopping centres, are keen to have good tenant covenants, the balance of viable, attractive localised traders who can offer something unique to a shopping centre or high street is arguably more important to the short, medium and long term retail

vitality; this surely should have an effect on the intrinsic value of the shop or centre?

Investors need to value this vitality especially in under-performing shopping centres, which would be similar to a goodwill valuation bearing in mind these local traders may create additional footfall benefits beyond the financial drivers of rent/yield assessed by valuers.

Currently, ‘old school’ valuers value the building’s worth rather than the tenant’s worth and as a result the property market has this love affair with covenant strength at any cost. We need to regard local traders as enhancing a centre’s vibrancy. However, although more enlightened valuers reflect a ’tenant mix’, few take a more holistic view with perceived weaker tenants. This is assuredly a dichotomy when those local trades are enhancing the retail offer in the location? Recently, the Local Data Company published a report which stated that 44 independent shops opened every day in 2013 as small businesses replaced contracting big

chains, which closed an average of 16 shops a day.

The growth in independent shopping was most prevalent in Wales, the Midlands and the South West, where the number of new shop openings significantly outpaced the number of closures. London was one of just three regions to see a net decline in the number of independent shops, with the South East and North East also recording small reductions. The number of independent shops has grown consistently since 2009, according to the LDC and BIRA, but the rate of growth has slowed more recently.

For example, Gloucester Road in Bristol bears witness to the additional footfall generation and brings vitality to the retail high street. A good mix of greengrocers, butchers and fishmongers entwined with the café montage is better than a high street full of bookmakers, charity shops and discounters. Perhaps this is where real-world retail and retail values are headed: our shopping parades and secondary shopping centres reverting to older models of economic activity, where they serve the needs of physical customers in physical stores as an intrinsic adjunct to the internet.

How much is that retail vitality worth, to the landlord, to the tenant, the local shop keeper and the wider community? Comparables are used to derive the value of an investment worth to a landlord according to the approach undertaken by the valuation profession. However, this falls short of the upside benefits of a good tenant mix and do not truly reflect the commercial benefits of a kind of indirect goodwill. Landlords are prevented from benefitting directly from tenant’s goodwill in leases either at rent review or lease renewal. The indirect benefits need to be

considered by the valuation profession and a good tenant mix could and should lead to considering a goodwill value for the retail vitality of any given location.

If retail landlords are not sensitive to the tenant mix and merely concentrate on rents then potentially they are putting their investments at risk. To see an array of florists, boutiques and independent clothes shops and occupied shops is a greater footfall generator and the upside benefit needs to be recognised. These retailers could be put on a concessionary or turnover basis with an additional value being applied to the upside benefit of the retail vibrancy delivered to the retail environment.

There is no simple panacea for the issues currently facing the retail market, but a realisation of market factors and a dynamic approach from all involved must surely assist in restoring the confidence and desire to shop in physical stores by the public and in retail property investment by owners.

Where is the intrinsic value from a good tenant mix?

Jerry BurtonHead of Lease Consultancy+44 (0) 117 988 [email protected]

4

The use of pop-up retailers has become a popular trend in the UK, providing landlords with a temporary fix to negate void costs whilst providing retailers with a chance to take space in a location they may not have had an opportunity to before. Done well, pop-ups can be a fantastic way of bringing a new dimension to a centre, helping to attract additional footfall and complement, rather than compete with, existing long-term retailers. It also provides an opportunity to secure a longer term letting should the pop-up be seen as mutually successful.

Pop-up units should provide flexibility and by using a three to six month licence agreement this provides sufficient time to ensure that it is a good fit which adds value. In addition to rates mitigation, pop-up occupiers can help with service charge contributions for the unit which

would otherwise fall as an additional cost to the landlord during the void period, which provides another incentive. They can also provide a great opportunity to connect with different types of retailers without exposing the centre to the risk of agreeing to a long term lease when there is uncertainty around whether the retailer will flourish in that environment.

The success of a mixed-use destination is not only based on the variety of occupiers and retailers but also creating the right atmosphere to drive footfall and increase customer dwell time during the day, evening and weekends. A pop-up, if done correctly, will provide an opportunity to generate press and PR for the development and to reach an audience that has not yet been targeted. Increasingly, social media plays an important part of this mix to create a buzz about the development, especially if they have a strong social media presence themselves.

As part of the landlord’s asset strategy at St Katharine Docks, GVA has introduced pop-up retailers in two retail units which were mothballed pending lease expiries of adjoining units and presented an opportunity for the landlord and estate. The pop-ups successfully reduced

rates and service charge liability, and importantly, brought different occupiers to the estate, bringing both marketing opportunities and visitor interest.

Every location is different but we have found that the type of retailer can make a big difference in terms of appeal and increase in footfall. At St Katharine Docks we have found that art galleries have performed really well, fitting well with our target demographic for the development.

As well as pop-up shops at St Katharine Docks, the introduction of a weekly food market every Friday and a street food market on the first Tuesday of every month has created a great atmosphere and has also helped drive footfall through the promotion of the markets via Twitter and the website. These initiatives have enabled us to entice customers to the estate who ordinarily may not have visited whilst gaining long term custom for the long term retailers. Using pop-ups on a short term basis has brought benefits and interest in the estate, occupiers and landlord, whilst also offering an opportunity to support local and emerging businesses. Should the landlord wish, the short term nature allows for agents to continue marketing the unit to attract the desired tenant mix.

The use of pop-ups can bring opportunities and benefits to existing and new occupiers, visitors and landlords alike. We anticipate that there will continue to be a future for pop-ups in a retail environment for the medium to long term whilst there is still a higher than normal number of void units, whilst existing and new retailers explore different products and avenues to trade in, and as the retail environment continues to change and develop. As is so often the case however, there still remains a need for balance and, whilst pop-ups are a great way of tackling rates and service charge mitigation in the short term, they should not be confused with the stability of long term occupiers who secure long term income for the development.

Pop-up retail trend

Janet FranklinHead of Shopping Centre Management+44 (0) 20 7911 [email protected]

5

Retail is concerned with providing products that people need and desire. Sustainability is about using resources more efficiently whilst improving or maintaining living standards. The Earth has survived for around 4.5 billion years and no matter how much we change it through burning fossil fuels and depleting its resources it will survive. However, societies and individuals are not so resilient. Sustainability isn’t about saving the planet; like retail, it’s about meeting the requirements of people.

Retailers and those involved in the manufacture of consumer goods are finding themselves on the front line of sustainability, facing severe risks to both supply chains and

brand image. An increasing number of consumer brands are recognising these threats and reacting by placing sustainability at the heart of their business plans. Think M&S’s Plan A, Patagonia’s Common Threads Partnership, Unilever’s Sustainable Living Plan and Kingfisher’s Net Positive programme. Puma took to heart the adage of ‘You can’t manage what you can’t measure’ and published an environmental profit and loss account in 2011, and their parent company Kering are now implementing this methodology across all their brands with a group E P&L planned for 2016.

As well as acting on the pressing resource concerns there is an acknowledgment that consumers are expecting more from companies with their non-financial commitments. Sainsbury’s CFO, John Rogers, recently made the point that although we saw a credit crunch between 2007 and 2012 we didn’t see a “values crunch”. Consumers in the UK now expect sustainability along with quality and affordability. This trend is demonstrated by the increasing number of corporate responsibility reports that are published as

companies seek to meet the expectations of consumers and shareholders.

The role of propertyProperty is both the embodiment of a company’s brand and a source of significant resource use. This is acknowledged in the British Retail Consortium’s (BRC) updated commitment to reducing the environmental impact of the retail industry. A Better Retailing Climate: Driving Resource Efficiency is an update on progress since 2008 and sets targets up to 2020 with signatories representing over half of the UK sector and a combined turnover of £160 billion.

Between 2008 and 2013 signatories reduced energy-related emissions from buildings by 30% and now aim for a further 50% reduction by 2020 and an 80% reduction in refrigerant gases. The proportion of waste sent to landfill has fallen from 47% to just 6% with the aspiration to have this down to just one per cent by the end of this decade. It is still difficult for retailers to obtain accurate water usage data at about 20% of sites but the target is to have measurement at all sites by 2020. As with many individual retailers and other companies, the aspirations of the BRC go much further than required or asked for by government.

The BRC targets echo the importance recognised by Puma, that you can’t manage what you can’t measure. This is also clear in the updated Sustainability Charter of the

British Council of Shopping Centres (BCSC), which is soon to be released and provides methods for measuring environmental impacts as well as benchmarks against which to assess performance.

Improving performanceAt GVA we recognise the importance of gathering robust environmental performance data from properties and then using that data to identify opportunities for improvement. We are standardising this process across the properties we manage and already have some excellent examples of action, such as at Merseyway Shopping Centre which was recently shortlisted for the BCSC Sustainability Gold award. Between 2010 and 2013, Merseyway management staff identified and implemented actions that halved energy use and resulted in no waste going to landfill. The actions also had a positive impact financially with both energy and waste collection costs more than halving. Occupiers and visitors are kept up to date with environmental initiatives through a newsletter and QR code accessible app, with the strap line of “Sustainability makes sense”.

The threats from resource scarcity and the need to meet the expectations of customers and investors is bringing sustainability to the heart of retail property. It is therefore important for all involved to understand the concerns and be able to implement solutions.

It’s the people, stupid!What sustainability and retail have in common

Alastair MantDirectorSustainability+44 (0) 20 7911 [email protected]

7000

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

6000

5000

4000

3000

2000

1000

0

Source: corporateregister.com

Corporate sustainability reports

6

The final piece in the government’s planning policy reform is now in place: the publication of the National Planning Practice Guidance (NPPG). In the same way that the National Planning Policy Framework (NPPF) slashed the number of pages of planning policy, the NPPG significantly slashes the number of pages of national practice guidance. So, what does this mean for retail and town centre planning?

Apart from one area of note, there are no significant changes from the Practice Guidance (prepared by GVA) published by the Department for Community and Local Government in 2009. In particular, the importance of preparing town centre visions and strategies has been successfully summarised, as has guidance on town centre health checks and planning for new retail development at the local level. The guidance on assessing planning applications for retail development also successfully treads a fine line between the needs of the general public and property/planning professionals.

However, the one area which will no doubt be the main talking point for the retail industry is the sequential test and the need to consider disaggregation of retail developments proposed on sites outside of town centres. A simple example of the principle of ‘disaggregation’ is where a promoter of a multi-unit retail/leisure park has to consider breaking

up (i.e. disaggregating) the development on to separate sites in a town centre.

Until recently, there has been tension between the wording of the NPPF and the 2009 Practice Guidance. The NPPF does not refer to disaggregation, with some commentators seeing this as a deliberate omission and change in policy by DCLG, whilst others have continued to rely on the Practice Guidance which did refer to disaggregation. Even the draft NPPG in August 2013 referred to the need to consider “what contribution town centre sites are able to make, either individually or collectively, to meeting the same requirements as the application is intended to meet”, which many took as a sign of disaggregation.

Although the reference to ‘collectively’ has been removed in the final version of the NPPG, which again some may argue as a sign of a deliberate omission by DCLG, this could pave the way for promoters of out-of-centre schemes to argue that, so long as flexibility in format and scale has been shown, there is no need to consider breaking up multi-unit out-of-centre retail/leisure developments.

This subtle change in wording could have unintended

consequences for major retail developments across the country. Like most things in retail planning, this will be argued at planning appeal and judicial review, and the recent publication of the NPPG is unlikely to be the end of the story. At least DCLG have decided to publish the NPPG as an on-line resource, thus making changes to the Practice Guidance must easier in the future.

The National Planning Practice Guidance Making guidance shorter doesn’t always make it more straightforward

Matthew MorrisDirectorPlanning Consultancy+44 (0) 117 988 [email protected]

7

It is quite difficult to remain loyal to a single asset class these days, as the answer to all our property woes is MUD! At least that is the acronym; the rest of you might know it as ‘mixed-use development’. There has been a good deal of commentary about how retail is fast changing, how the internet and now mobile is killing the high street and yet at the same time we have seen the rise of the supermarkets and the food and beverage sector.

Those of us who are old enough will remember the boom in development in the 1990s following the last recession. We saw the wide-scale development of shopping centres, supermarkets, out of town retail parks and stand-alone leisure parks. Times have changed since then as we are now in more educated, instant and demanding times as consumers. We believe

we have less time so we are demanding more from our leisure time experience.

GVA has previously suggested that we are seeing the polarisation of centres and major retailers are taking larger stores, but fewer of them, using lease expiries, breaks and any other levers to reduce their store counts or costs. This means that some assets and towns need to reposition themselves to survive for the next 15 – 25 years and a good way of doing so is with mixed-use developments. Every experienced shopping centre leasing agent has been promoting ‘experiential retail’ for some time now. Providing a wider and improved retail experience is one way to broaden the catchment to increase both dwell time and spend per capita.

It is no surprise that the things people want and use the most are the classes that are performing the best. The latest generation of “super” shopping centres deliver tenant mixes that have a much higher proportion of catering and leisure than previous generations. For example, Westfield Stratford was almost the only major scheme to be delivered in the recession, due to commitments to the 2012 Olympics. The catering and leisure element of that

scheme was all pre-let prior to opening. However, the retail was having a tougher time and some units remained vacant until post opening and post Olympics. People love to shop, but they have to eat!

Older shopping centres are responding by remodelling themselves and introducing MUD - more entertainment and more catering in order to compete and retain customer visits and spend. GVA cannot deliver a mini-Bluewater in every town, but we are involved in a considerable amount of mixed-use development that will see those centres with a boost to their offer, economy and rankings. Masterplanners and councils have been promoting the “18 – 7” economy - activity in centres for 18 hours a day 7 days a week. This means restaurant and entertainment activity in addition to retail and it also means bringing people back in to towns to live.

GVA is currently helping to deliver new mixed-use schemes and rejuvenation to towns for a number of clients:

Canning Town Bouygues Development UK

Having entered the race for this local authority primed urban regeneration scheme in 2007 we introduced our developer client to recent UK market entrants Bouygues. We knew that in order for the joint venture to be successful we needed a consortium with both strong development experience and

strong financial resources to win this £600 million creation of a new town centre. The partnership delivered that.

Now working solely with Bouygues, GVA has already delivered and funded Phase I of this impressive scheme, the topping out ceremony was just last week. Morrisons will soon begin to fit out their new 80,000 sq ft supermarket and we have an adjoining unit to fill. We are just commencing the marketing of Phase II, with interest from multiple retailers, restaurateurs and a hotel deal agreed. This has required intelligent marketing; Canning Town was a run down and deprived area of East London. However, the proximity to Canary Wharf, unrivalled transport links, City Airport and the river has meant that it has been easy to put a compelling case forward. With the amount of development happening in the area, including a new town square and library and vast residential development, you need to go and see it.

Bedford Riverside CoPlan and Bouygues Construction UK

Both CoPlan and GVA knew Bedford well from differing angles. CoPlan from the development angle and GVA from a local authority advice and retail lettings (Next, amongst others). We started work on a development site elsewhere in Bedford that proved to be non-viable in 2010. We then focused our attention on the local authority led development

MUD Glorious MUD

David HooperDirectorRetail Agency+44 (0) 20 7911 [email protected]

8

The proposed MUD in Redhill, Surrey

of Bedford Riverside, “the best site in the town”. Having assisted the client’s pitch we were delighted to be selected preferred developer, beating development companies with a more established track record.

Pre-leasing has gone extremely well with pre-lets to Premier Inn, Vue Cinemas, Zizzi, Chimichanga, Harvester, Bella Italia and other major restaurateurs under negotiation. GVA Investment team has recently undertaken a campaign to secure funding which attracted many well-known investors, demonstrating the continuing improvement in the funding and investment industry and heralding the return of the development market. Our clients are already on site undertaking demolition works and Bedford will be open for trade in 2016. GVA is also looking at development monitoring via our Building Consultancy team.

Addlestone, Surrey Bouygues Development UK

GVA undertook the soft market testing and input considerable advice on demand, configuration and values into the client’s detailed submission to Runnymede Council. We were successfully appointed with Bouygues in 2011. GVA has subsequently advised throughout the architectural design process and was instrumental in bringing Premier Inn to the table. This was not easy as we had to persuade them to walk away from commitments elsewhere.

We have now exchanged an agreement for lease, agreed terms with a supermarket and have discussions on-going with other multiple retailers, restaurateurs and family pub companies. Our Investment team is advising on funding and our Property Management team has advised on property management strategy.

Redhill, Surrey CoPlan and British Airways Pension Fund

This is a recent win for GVA and our clients via the interesting and possibly bizarre ‘competitive dialogue’ route. Beating five other developers who submitted for this scheme, we were pleased to win this very central town centre refurbishment. GVA was able to exploit our intimate knowledge of the town and also engaged early with other neighbouring land owners. The extra homework, coupled with a great scheme and bundles of enthusiasm gave us the edge; that and a creative JV partnership with BA Pension Fund. Whilst at an early stage, this development is already proving popular with cinemas, restaurants and retailers alike who see the opportunity that an affluent catchment and distant competition bring. We have been giving CPO advice and investment acquisition advice too, showing our full-service offer.

Herne Bay, Kent CoPlan and Bouygues Construction

This scheme demonstrates GVA’s tenacity and commitment to delivery. We have been working on this scheme since 2008. Having explored a number of options and discussions with developers, the initial ambitions for the town proved too difficult to deliver in a recession. When all else fails, simplify the plan. We have now exchanged with Aldi, the rising star in the supermarket sector, delivering a new store, some competition and some much needed public realm. We are now seeking pre-lets for phase II and funding for phase I.

Market activity is continuing to improve this year and GVA is being asked to look at more opportunities throughout the South East and the rest of the country. Particular hot spots seem to be the Home Counties, Birmingham and the Midlands, Cambridge, Liverpool and Southampton. The residential market is playing a role in these developments as demand and prices continue to rise. As a firm, GVA has also developed a specialism in the private rented sector (PRS) and also student housing market. We also advise in the health sector, offices, industrial and with our specialists in rights of light, CPO, sustainability and minerals all covered we are

very well placed to advise on all aspects. We might struggle on nuclear power…no, “we do that as well”, I have just been told. GVA do that and we definitely do MUD!

As property professionals we need to remember a factor called obsolescence. Things are changing faster these days and, as fashions continue to change, so do our life styles.

Whether we are talking about new-build, re-development or refurbishment, investors want modern, fit-for-purpose stock, let on long leases, at viable rents to good covenants with interesting and desirable uses. Some landlords would lead you to believe that tenant mix is the panacea, but they must all be answerable to the lender, shareholder or valuer at some point.

The proposed MUD in Redhill, Surrey

9

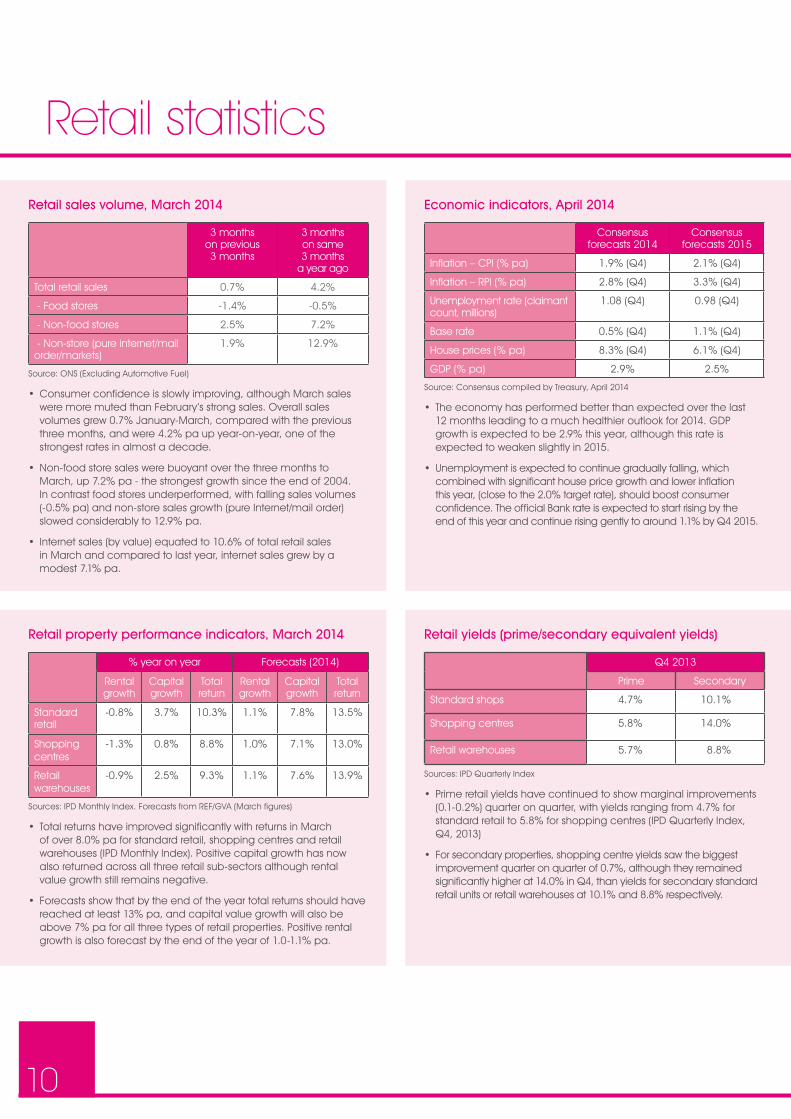

Retail sales volume, March 2014

3 months on previous 3 months

3 months on same 3 months

a year ago

Total retail sales 0.7% 4.2%

- Food stores -1.4% -0.5%

- Non-food stores 2.5% 7.2%

- Non-store (pure internet/mail order/markets)

1.9% 12.9%

Source: ONS (Excluding Automotive Fuel)

• Consumer confidence is slowly improving, although March sales were more muted than February’s strong sales. Overall sales volumes grew 0.7% January-March, compared with the previous three months, and were 4.2% pa up year-on-year, one of the strongest rates in almost a decade.

• Non-food store sales were buoyant over the three months to March, up 7.2% pa - the strongest growth since the end of 2004. In contrast food stores underperformed, with falling sales volumes (-0.5% pa) and non-store sales growth (pure Internet/mail order) slowed considerably to 12.9% pa.

• Internet sales (by value) equated to 10.6% of total retail sales in March and compared to last year, internet sales grew by a modest 7.1% pa.

Economic indicators, April 2014

Consensus forecasts 2014

Consensus forecasts 2015

Inflation – CPI (% pa) 1.9% (Q4) 2.1% (Q4)

Inflation – RPI (% pa) 2.8% (Q4) 3.3% (Q4)

Unemployment rate (claimant count, millions)

1.08 (Q4) 0.98 (Q4)

Base rate 0.5% (Q4) 1.1% (Q4)

House prices (% pa) 8.3% (Q4) 6.1% (Q4)

GDP (% pa) 2.9% 2.5%

Source: Consensus compiled by Treasury, April 2014

• The economy has performed better than expected over the last 12 months leading to a much healthier outlook for 2014. GDP growth is expected to be 2.9% this year, although this rate is expected to weaken slightly in 2015.

• Unemployment is expected to continue gradually falling, which combined with significant house price growth and lower inflation this year, (close to the 2.0% target rate), should boost consumer confidence. The official Bank rate is expected to start rising by the end of this year and continue rising gently to around 1.1% by Q4 2015.

Retail property performance indicators, March 2014

% year on year Forecasts (2014)

Rental growth

Capital growth

Total return

Rental growth

Capital growth

Total return

Standard retail

-0.8% 3.7% 10.3% 1.1% 7.8% 13.5%

Shopping centres

-1.3% 0.8% 8.8% 1.0% 7.1% 13.0%

Retail warehouses

-0.9% 2.5% 9.3% 1.1% 7.6% 13.9%

Sources: IPD Monthly Index. Forecasts from REF/GVA (March figures)