Embed Size (px)

Citation preview

1

1818 Energy Group

Electric Power Reform: Lessons and Implications for the World Bank’s

Energy Strategy

John Besant-JonesNovember 20, 2007

2

1. What Has Happened Under Power Market Reform

3. Implications and Issues for the World Bank

Structure of the Presentation

2. Evolution of The World Bank’s Approach to Power Market Reform

3

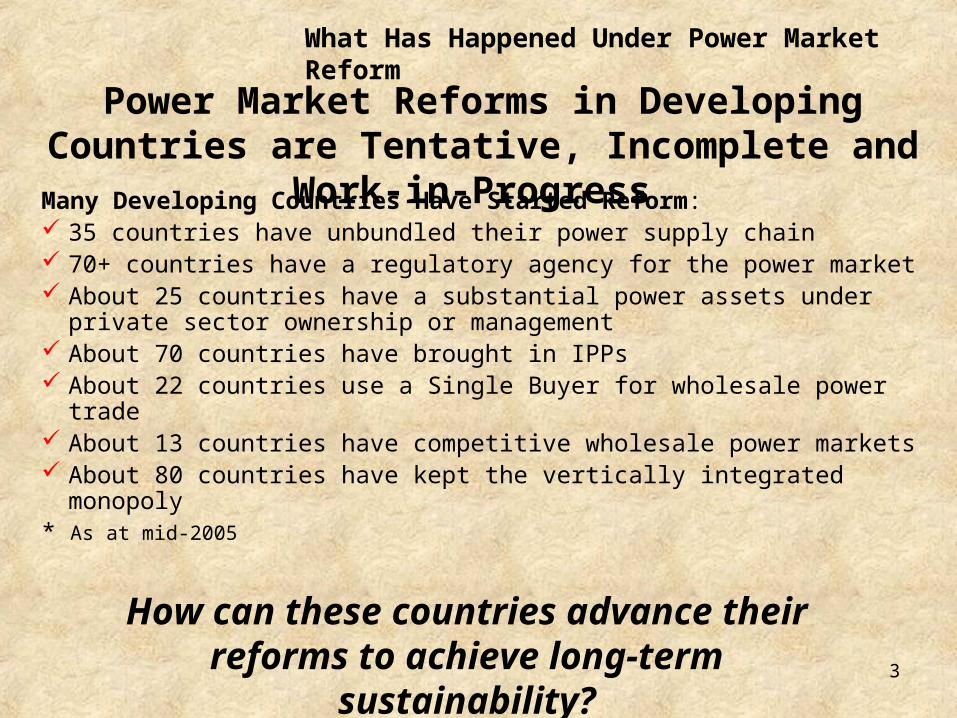

Many Developing Countries Have Started Reform: 35 countries have unbundled their power supply chain 70+ countries have a regulatory agency for the power market About 25 countries have a substantial power assets under private

sector ownership or management About 70 countries have brought in IPPs About 22 countries use a Single Buyer for wholesale power trade About 13 countries have competitive wholesale power markets About 80 countries have kept the vertically integrated monopoly* As at mid-2005

Power Market Reforms in Developing Countries are Tentative, Incomplete and Work-in-Progress

How can these countries advance their reforms to achieve long-term sustainability?

What Has Happened Under Power Market Reform

4

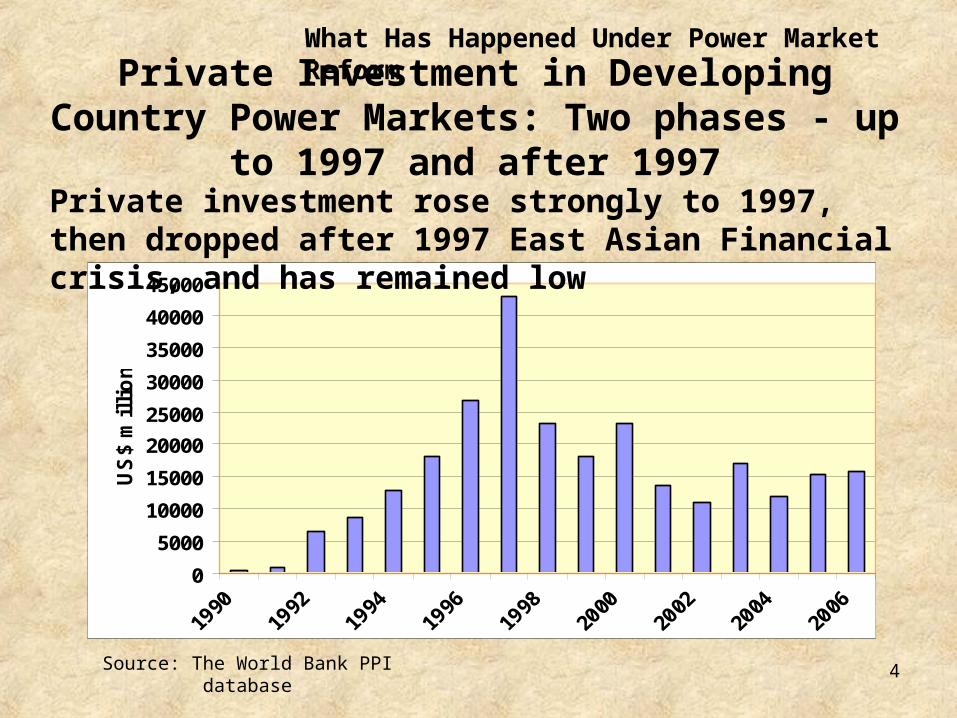

Private Investment in Developing Country Power Markets: Two phases - up to 1997 and after 1997

What Has Happened Under Power Market Reform

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

US

$ m

illi

on

Private investment rose strongly to 1997, then dropped after 1997 East Asian Financial crisis, and has remained low

Source: The World Bank PPI database

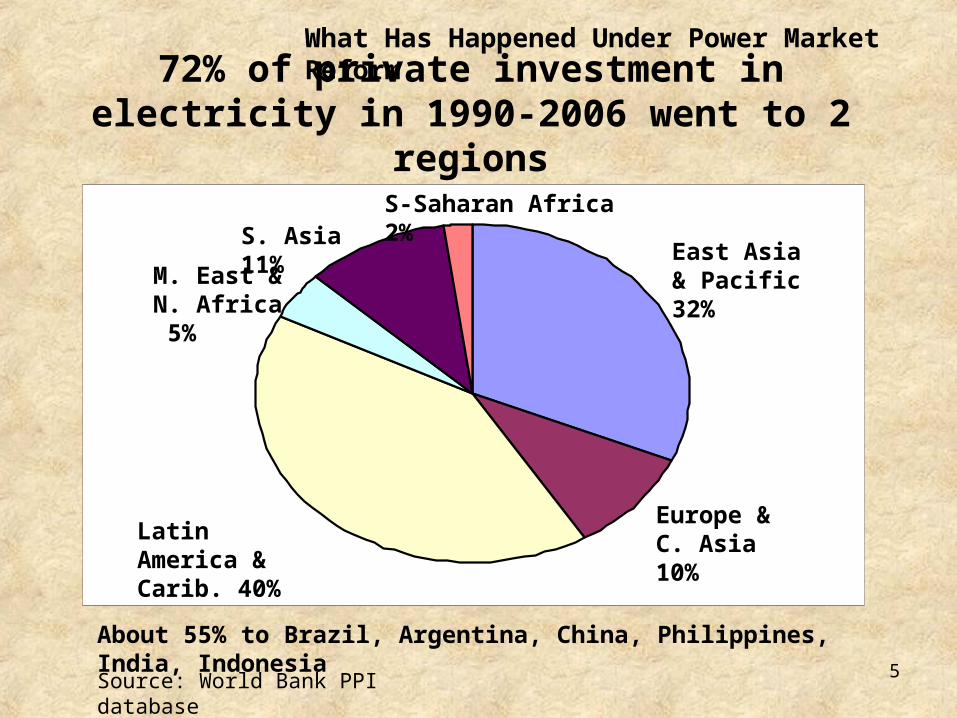

5

72% of private investment in electricity in 1990-2006 went to 2 regions

Latin America & Carib. 40%

Europe & C. Asia 10%

East Asia & Pacific 32%

S-Saharan Africa 2%S. Asia 11%

M. East & N. Africa 5%

About 55% to Brazil, Argentina, China, Philippines, India, Indonesia

Source: World Bank PPI database

What Has Happened Under Power Market Reform

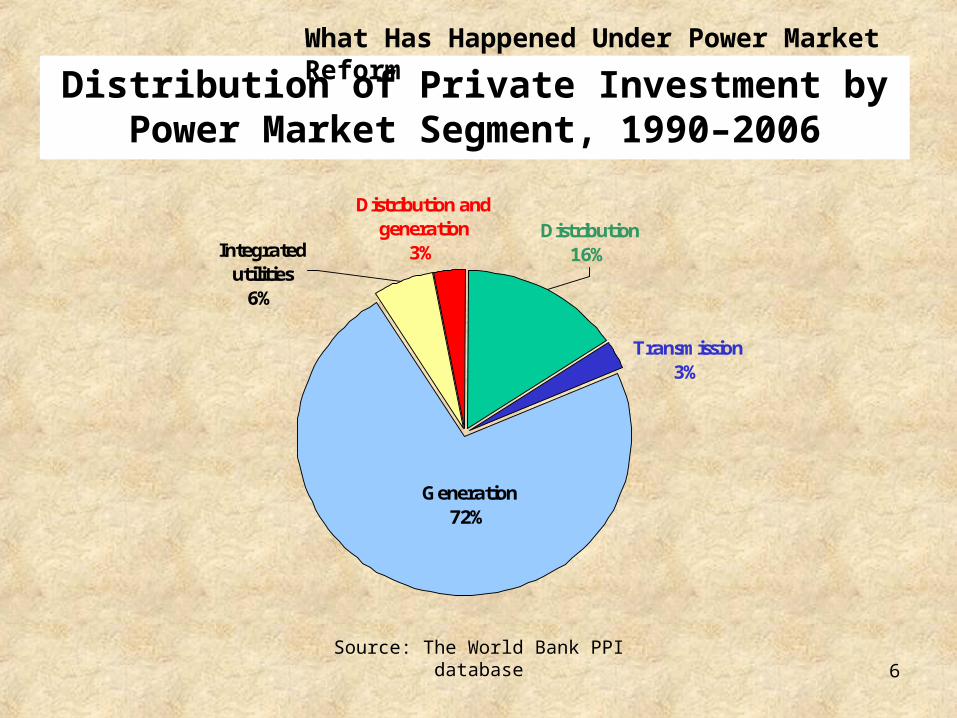

6

Distribution of Private Investment by Power Market Segment, 1990–2006

Distribution16%

Distribution and generation

3%Integrated utilities

6%

Transmission3%

Generation72%

Source: The World Bank PPI database

What Has Happened Under Power Market Reform

7

In 8 Latin American countries:*

Divestiture and concessions through unbundling and regulation for market competition

Have progressed most among these countries under a clear reform vision

Private participation was steered first to power distribution to reduce the huge system losses—technical and non-technical

Initial reform priority was predictably regulated retail tariffs with pass-through of purchased power costs beyond the distributor’s control, freedom to disconnect non-payers, and regulated access to the transmission network.

*Argentina, Bolivia, Brazil, Chile, Colombia, El Salvador, Panama, Peru

Two Regional Approaches to Power Reform - 1

What Has Happened Under Power Market Reform

8

Two Regional Approaches to Power Reform - 2

Greenfield investment by IPPs through long-term contracts with state-owned suppliers

Have progressed much less than the 8 Latin American countries

Private participation was steered first to investments in power generation to meet rapidly growing demand for electricity

Initial reform priority was to remove serious distortions in wholesale power prices, create viable purchasers of the output, and help IPPs to manage uncertainty in their revenues.

* China, India-Orissa, Indonesia, Malaysia, Pakistan, Philippines, Thailand

In 7 Asian countries:*

What Has Happened Under Power Market Reform

9

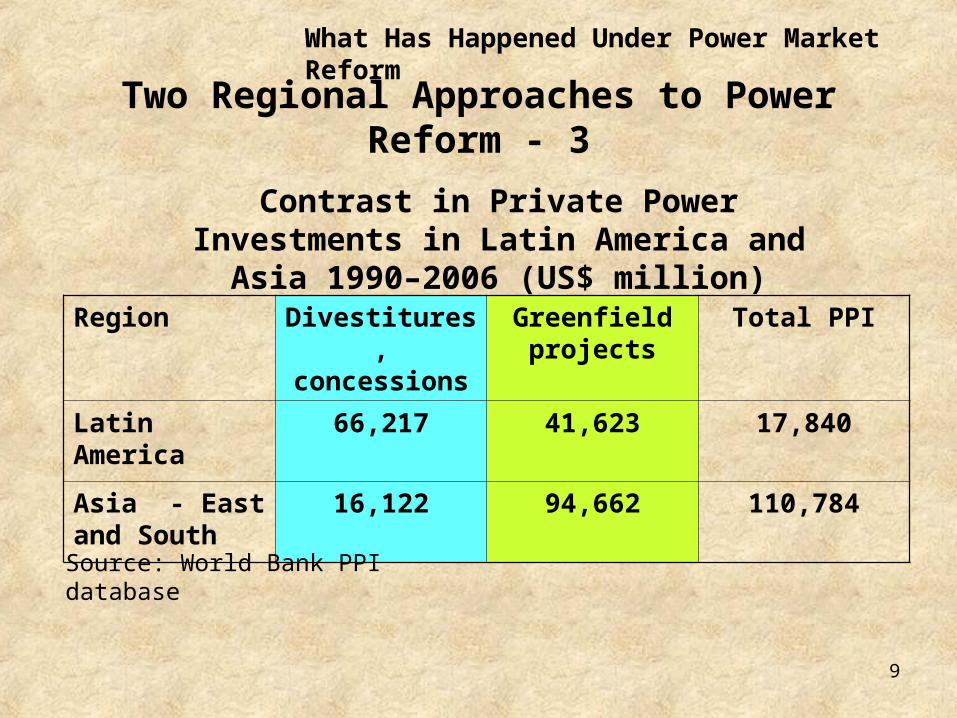

Two Regional Approaches to Power Reform - 3

Region Divestitures, concessions

Greenfield projects

Total PPI

Latin America 66,217 41,623 17,840

Asia - East and South

16,122 94,662 110,784

Contrast in Private Power Investments in Latin America and Asia 1990–2006 (US$ million)

Source: World Bank PPI database

What Has Happened Under Power Market Reform

10

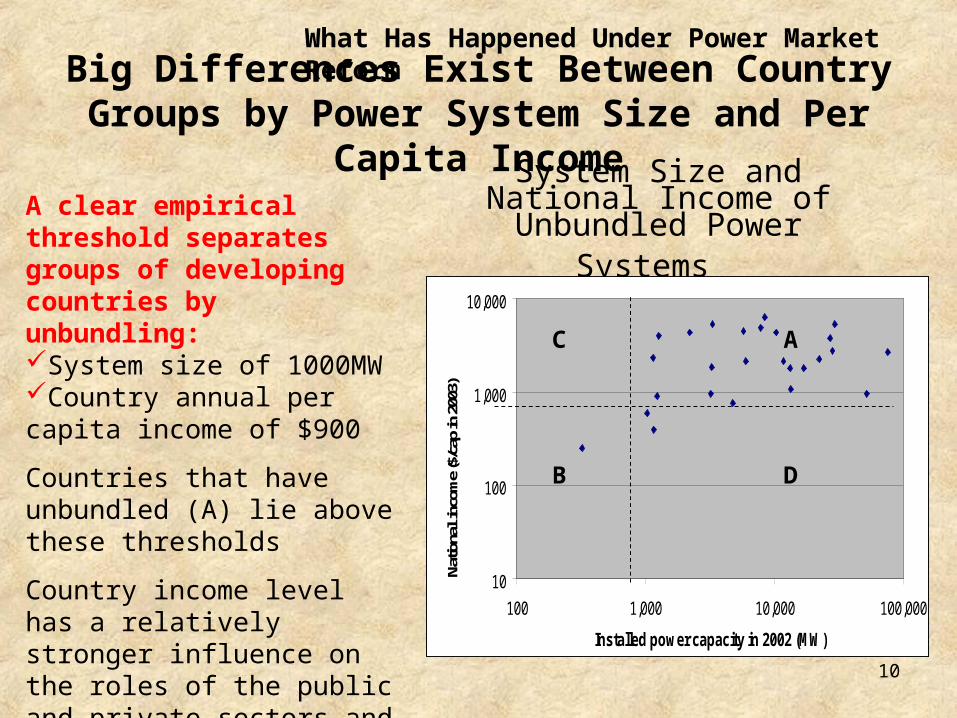

System Size and National Income of Unbundled Power Systems

10

100

1,000

10,000

100 1,000 10,000 100,000

Installed power capacity in 2002 (MW)

Natio

nal i

ncom

e ($

/cap

in 2

003)

A clear empirical threshold separates groups of developing countries by unbundling:System size of 1000MWCountry annual per capita income of $900

Countries that have unbundled (A) lie above these thresholds

Country income level has a relatively stronger influence on the roles of the public and private sectors and market regulation. Power system size has a relatively stronger influence on market structure.

B

AC

D

Big Differences Exist Between Country Groups by Power System Size and Per Capita Income

What Has Happened Under Power Market Reform

11

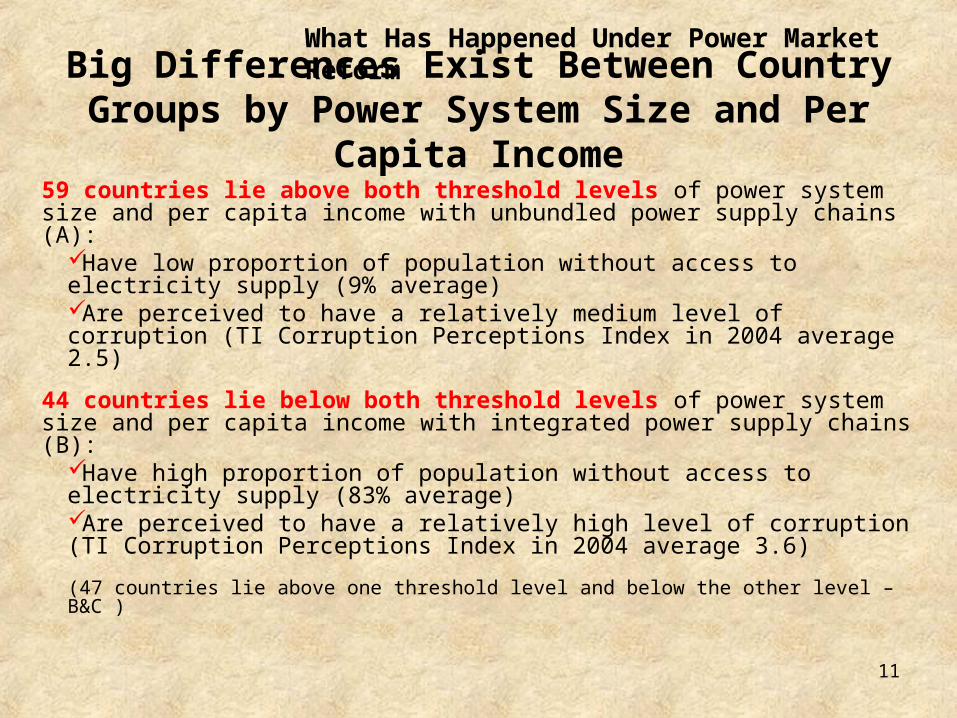

59 countries lie above both threshold levels of power system size and per capita income with unbundled power supply chains (A):

Have low proportion of population without access to electricity supply (9% average)Are perceived to have a relatively medium level of corruption (TI Corruption Perceptions Index in 2004 average 2.5)

44 countries lie below both threshold levels of power system size and per capita income with integrated power supply chains (B):

Have high proportion of population without access to electricity supply (83% average)Are perceived to have a relatively high level of corruption (TI Corruption Perceptions Index in 2004 average 3.6)

(47 countries lie above one threshold level and below the other level – B&C )

Big Differences Exist Between Country Groups by Power System Size and Per Capita Income

What Has Happened Under Power Market Reform

12

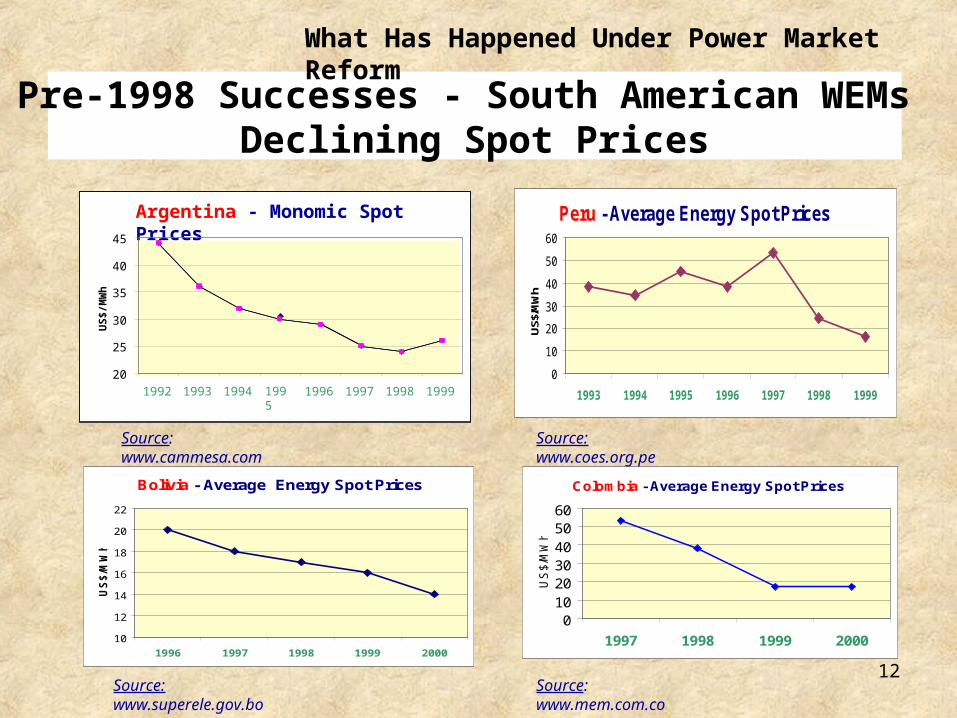

Argentina - Monomic Spot Prices

20

25

30

35

40

45

1992 1993 1994 1995

1996 1997 1998 1999

US

$/M

Wh

Bolivia - Average Energy Spot Prices

10

12

14

16

18

20

22

1996 1997 1998 1999 2000

US

$/M

Wh

Peru - Average Energy Spot Prices

0

10

20

30

40

50

60

1993 1994 1995 1996 1997 1998 1999

US$

/MW

h

Colombia - Average Energy Spot Prices

0102030405060

1997 1998 1999 2000

US

$/M

Wh

Source: www.cammesa.com Source: www.coes.org.pe

Source: www.superele.gov.bo Source: www.mem.com.co

Pre-1998 Successes - South American WEMs Declining Spot Prices

What Has Happened Under Power Market Reform

13

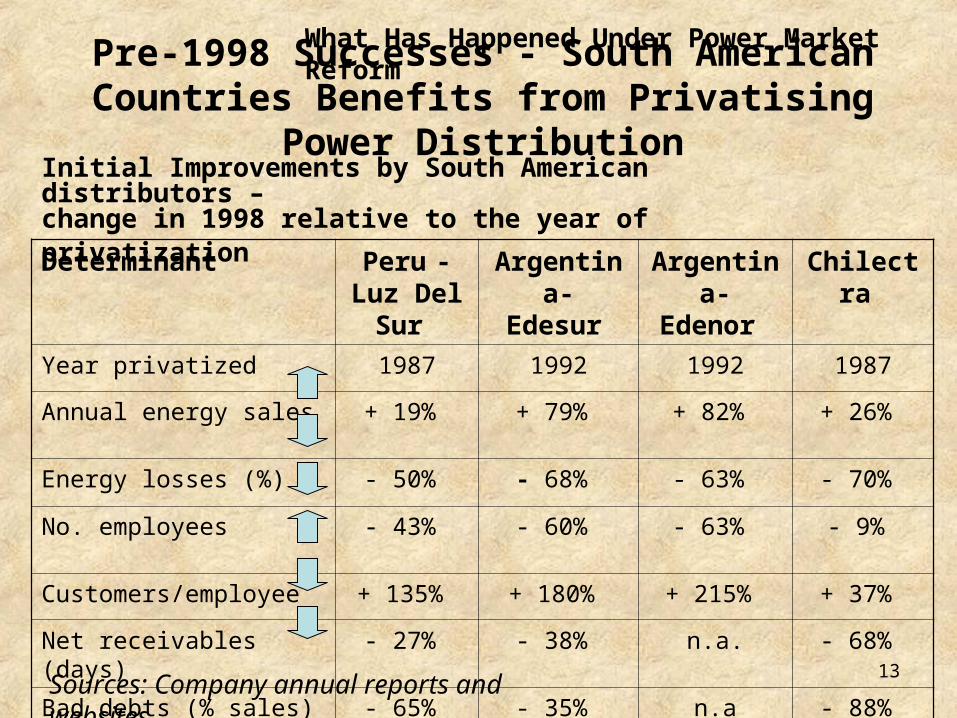

Pre-1998 Successes - South American Countries Benefits from Privatising Power Distribution

Determinant Peru - Luz Del Sur

Argentina- Edesur

Argentina- Edenor

Chilectra

Year privatized 1987 1992 1992 1987

Annual energy sales + 19% + 79% + 82% + 26%

Energy losses (%) - 50% - 68% - 63% - 70%

No. employees - 43% - 60% - 63% - 9%

Customers/employee + 135% + 180% + 215% + 37%

Net receivables (days) - 27% - 38% n.a. - 68%

Bad debts (% sales) - 65% - 35% n.a - 88%

Initial Improvements by South American distributors – change in 1998 relative to the year of privatization

Sources: Company annual reports and websites.

What Has Happened Under Power Market Reform

14

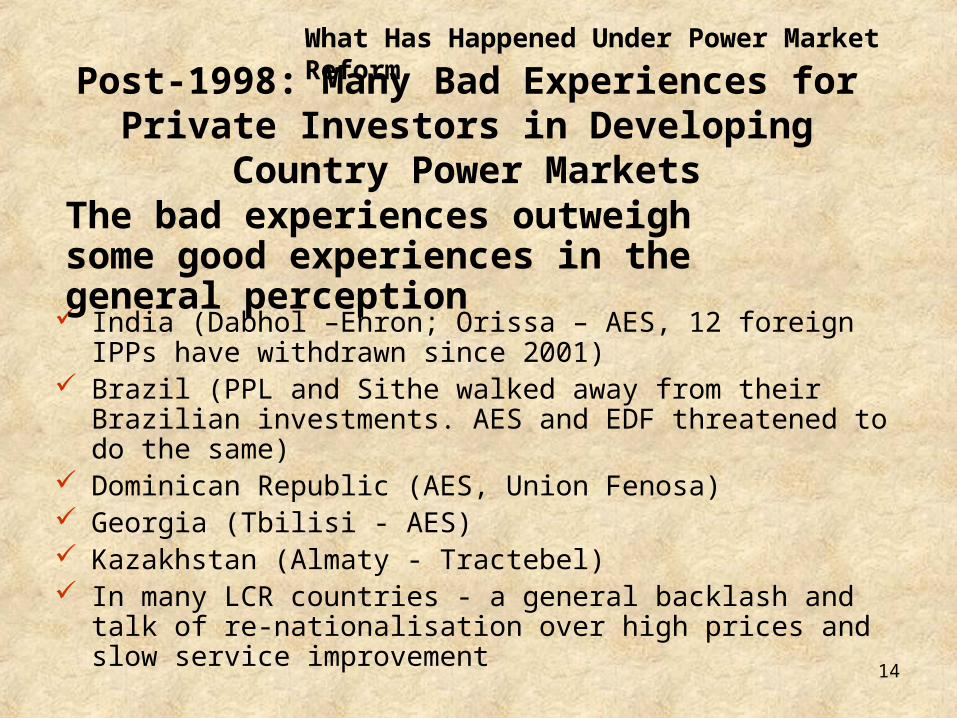

Post-1998: Many Bad Experiences for Private Investors in Developing Country Power Markets

India (Dabhol –Enron; Orissa – AES, 12 foreign IPPs have withdrawn since 2001)

Brazil (PPL and Sithe walked away from their Brazilian investments. AES and EDF threatened to do the same)

Dominican Republic (AES, Union Fenosa) Georgia (Tbilisi - AES) Kazakhstan (Almaty - Tractebel) In many LCR countries - a general backlash and talk of re-

nationalisation over high prices and slow service improvement

The bad experiences outweigh some good experiences in the general perception

What Has Happened Under Power Market Reform

15

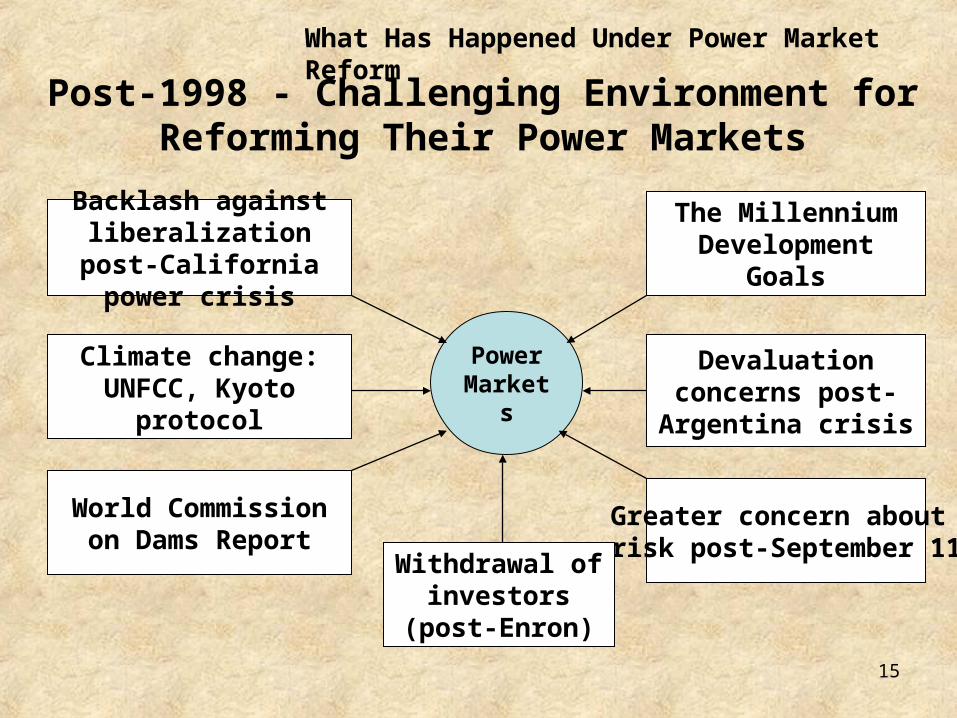

Greater concern about risk post-September 11

Climate change: UNFCC, Kyoto protocol

The Millennium Development Goals

Devaluation concerns post-Argentina crisis

World Commission on Dams Report

Backlash against liberalization post-

California power crisis

Power Market

s

Withdrawal of investors (post-

Enron)

Post-1998 - Challenging Environment for Reforming Their Power Markets

What Has Happened Under Power Market Reform

16

Better service quality for electricity consumers. Achieved in a few S. American countries under distribution concessions to

private operators. Efficiency gains not shared equitably with consumers. Some short-term gains elsewhere – such as Africa – under management

contracts. Improvement in Government’s fiscal position.

Privatization yielded substantial fiscal benefits in some Latin America countries.

But PPAs with IPPs created huge contingent liabilities in Asian countries. Affordable access to electricity for the poor.

The poor in general have hardly benefited from reform. Few have benefited directly, and few have even lost directly by it.

Overall, reforms have been constrained by lack of country commitment, macroeconomic and political crises, and lack of experience with political economy factors

Overall - Desired Outcomes of Power Sector Reform Were Partly Achieved

What Has Happened Under Power Market Reform

17

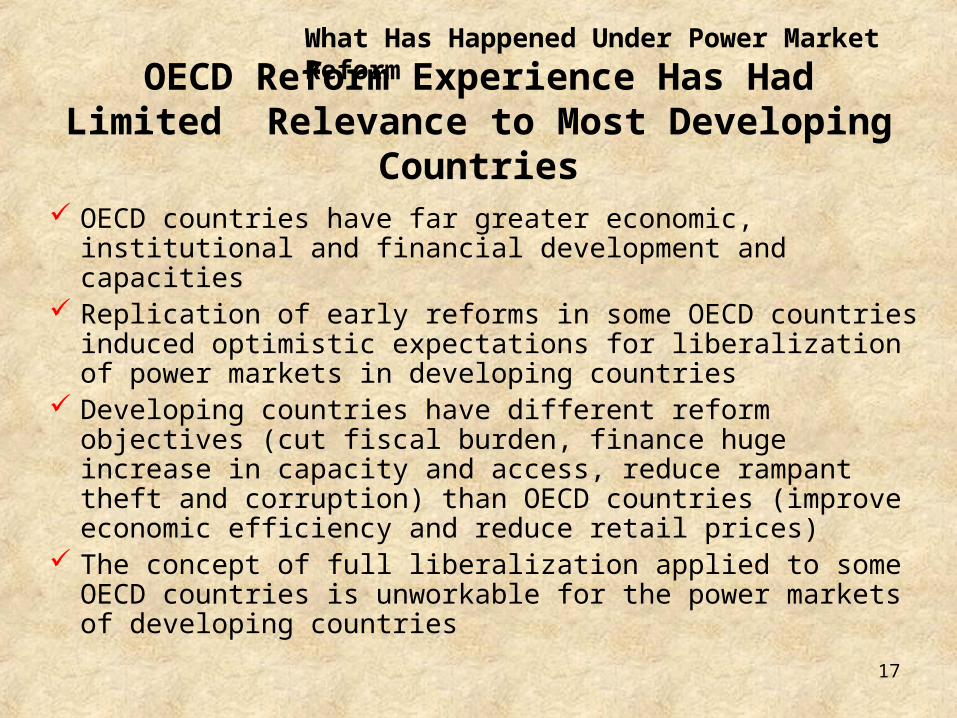

OECD countries have far greater economic, institutional and financial development and capacities

Replication of early reforms in some OECD countries induced optimistic expectations for liberalization of power markets in developing countries

Developing countries have different reform objectives (cut fiscal burden, finance huge increase in capacity and access, reduce rampant theft and corruption) than OECD countries (improve economic efficiency and reduce retail prices)

The concept of full liberalization applied to some OECD countries is unworkable for the power markets of developing countries

OECD Reform Experience Has Had Limited Relevance to Most Developing Countries

What Has Happened Under Power Market Reform

18

1. What Has Happened Under Power Market Reform

3. Implications and Issues for the World Bank

Structure of the Presentation

2. Evolution of the World Bank’s Approach to Power Market Reform

19

1993 Policy Paper “The World Bank’s Role in the Electric Power Sector: Policies for Effective Institutional, Regulatory and Financial Reform”

Advocated unbundling, arm’s length regulation, competition and privatisation to replace the failed state-owned monopoly

World Bank’s First Milestones in Power Market Reform

Evolution of World Bank’s Approach

20

The World Bank Then Withdrew From Its Main Business Lines for Energy

New thermal power generation capacity would be left for private investment

Power distribution would be left for private investment In addition, World Bank avoided new hydropower projects

(after Narmada, Arun III, etc) under external criticisms by NGOs, etc – led to World Commission on Dams report

World Bank announced this new operating policy at landmark regional conferences in 1993 – Mexico and India:

So, World Bank lending for Energy dropped sharply –

as anticipated

Evolution of World Bank’s Approach

21

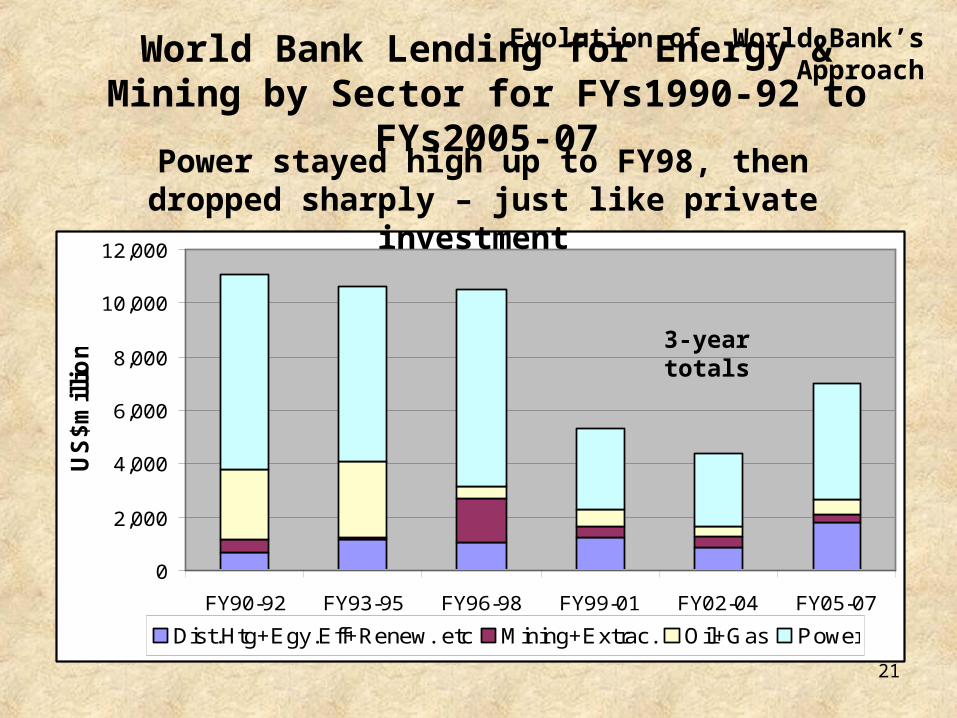

World Bank Lending for Energy & Mining by Sector for FYs1990-92 to FYs2005-07

0

2,000

4,000

6,000

8,000

10,000

12,000

FY90-92 FY93-95 FY96-98 FY99-01 FY02-04 FY05-07

US

$m

illi

on

Dist.Htg+Egy.Eff+Renew. etc Mining+Extrac. Oil+Gas Power

Power stayed high up to FY98, then dropped sharply – just like private investment

3-year totals

Evolution of World Bank’s Approach

22

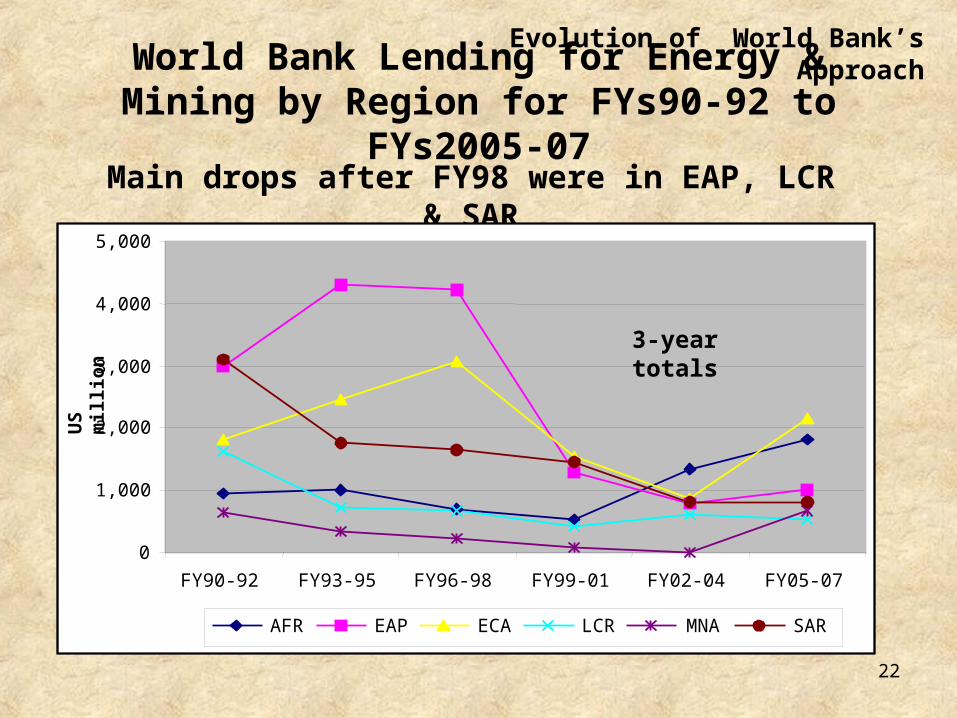

World Bank Lending for Energy & Mining by Region for FYs90-92 to FYs2005-07

Main drops after FY98 were in EAP, LCR & SAR

0

1,000

2,000

3,000

4,000

5,000

FY90-92 FY93-95 FY96-98 FY99-01 FY02-04 FY05-07

US

mil

lio

n

AFR EAP ECA LCR MNA SAR

3-year totals

Evolution of World Bank’s Approach

23

Unforeseen Consequences of World Bank’s 1993 Policy for Power Market Reform

Public sector investment dropped sharply as The World Bank and governments cut back financing in areas considered for private sector investment - esp. generation.

This cutback coincided with post-1997 downturn in private investment– so investment in new power capacity dropped sharply.

But, economies of many developing countries have grown well since 1998 despite low growth in public power supply. One reason is huge increase in captive power generation (e.g. 20-40GW in India). China’s huge expansion is an obvious exception .

Sub-Saharan Africa generally reflects this paradox (partly due to the boom in commodity exports), but has low access to electricity for the population (below 20% on average), since access rate has not kept up with population growth).

Evolution of World Bank’s Approach

24

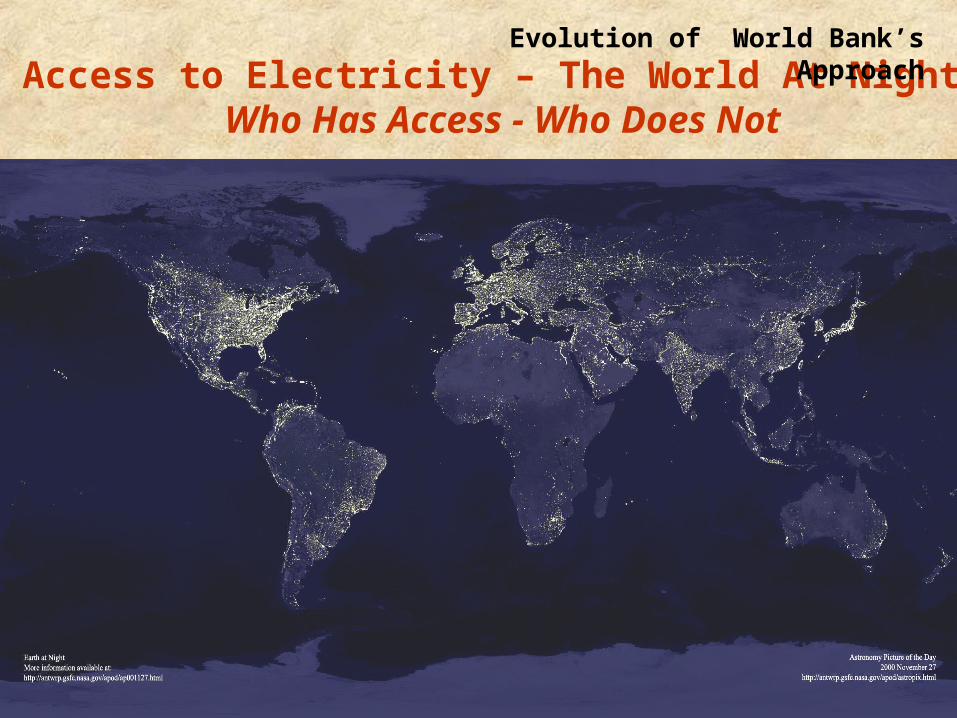

Access to Electricity – The World At Night Who Has Access - Who Does Not

Evolution of World Bank’s Approach

25

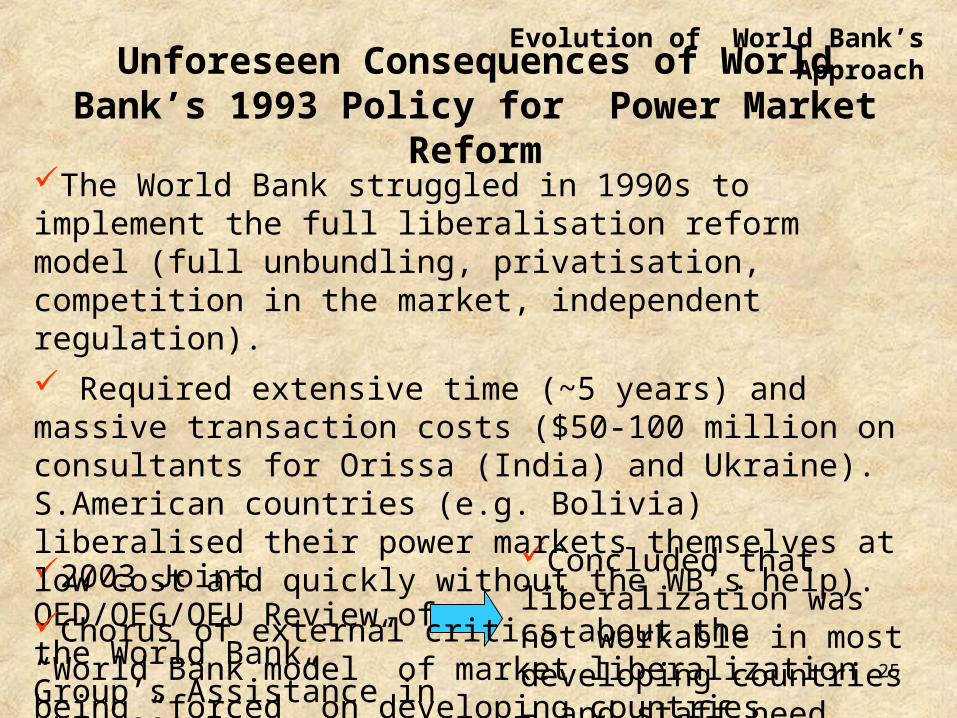

Unforeseen Consequences of World Bank’s 1993 Policy for Power Market Reform

2003 Joint OED/OEG/OEU Review of the World Bank Group’s Assistance in the 1990s

Concluded that liberalization was not workable in most developing countries – and staff need guidance

Evolution of World Bank’s Approach

The World Bank struggled in 1990s to implement the full liberalisation reform model (full unbundling, privatisation, competition in the market, independent regulation).

Required extensive time (~5 years) and massive transaction costs ($50-100 million on consultants for Orissa (India) and Ukraine). S.American countries (e.g. Bolivia) liberalised their power markets themselves at low cost and quickly without the WB’s help).

Chorus of external critics about the “World Bank model” of market liberalization being “forced” on developing countries

26

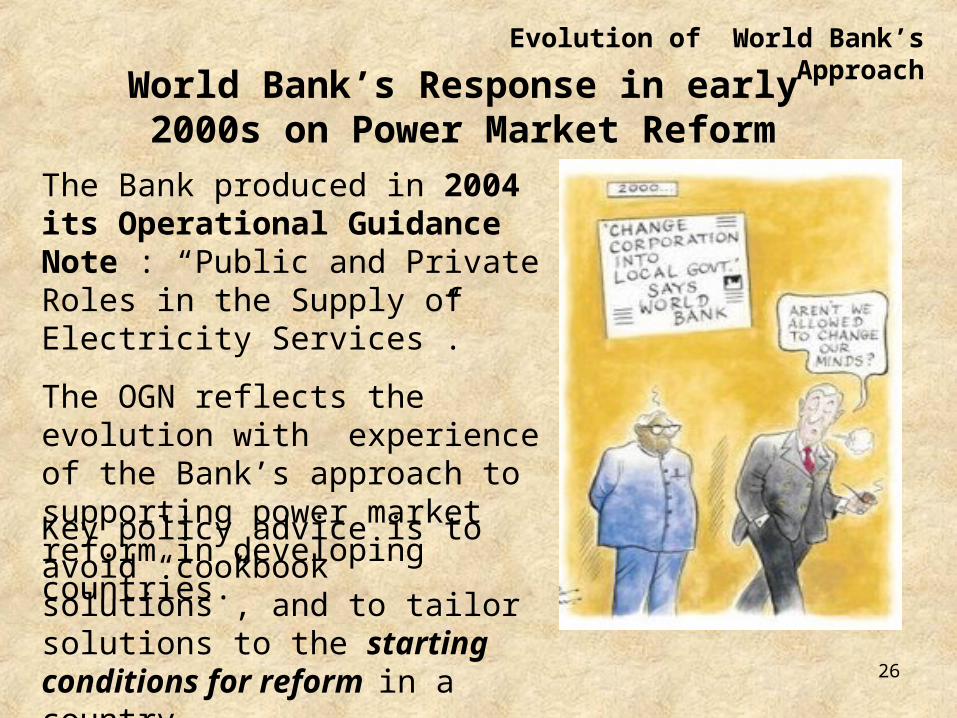

The Bank produced in 2004 its Operational Guidance Note : “Public and Private Roles in the Supply of Electricity Services”.

The OGN reflects the evolution with experience of the Bank’s approach to supporting power market reform in developing countries.

Key policy advice is to avoid “cookbook solutions”, and to tailor solutions to the starting conditions for reform in a country

World Bank’s Response in early 2000s on Power Market Reform

Evolution of World Bank’s Approach

27

How The Bank’s Current Approach to Power Market Reform Reflects Country Conditions

“Cookbook” solutions don’t work for reforming power sectors.

Power reform strategies should reflect the priorities for the sector and the country conditions.

Restructuring programs should be assessed on a case by case basis and are likely to include a continuing role for the state.

Practical solutions may be public-private partnerships.

The level of private participation depends on political economy factors, the investment climate and the legal framework.

For small markets, regulation of a vertically integrated monopoly may be the most cost-effective choice.

Governments should consider gradual market opening and limited competition for the market, and should approach full competition cautiously.

Evolution of World Bank’s Approach

28

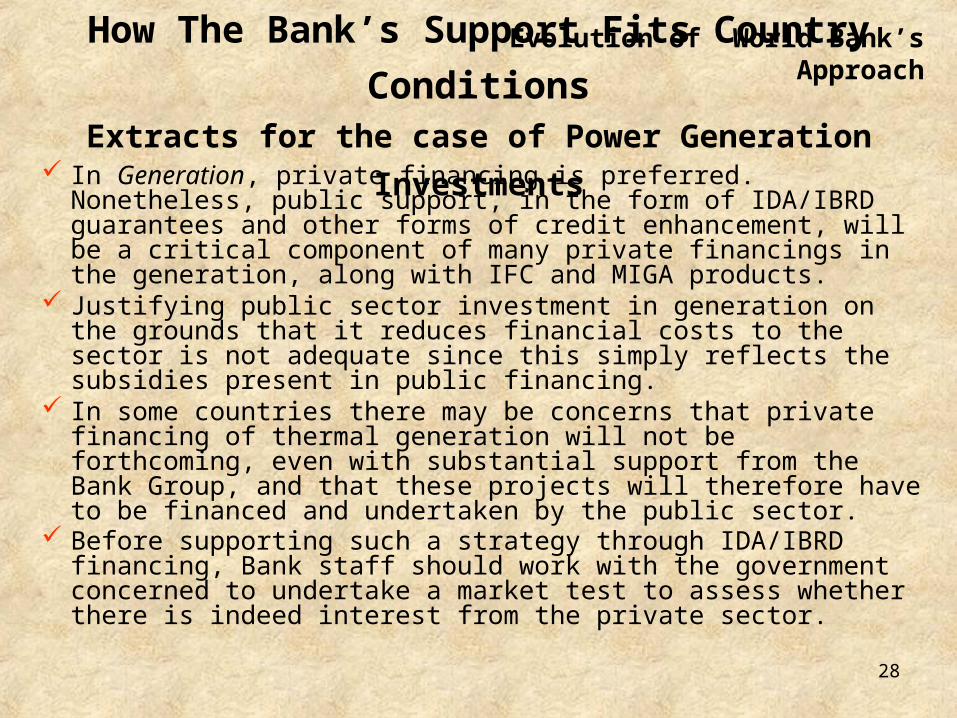

In Generation, private financing is preferred. Nonetheless, public support, in the form of IDA/IBRD guarantees and other forms of credit enhancement, will be a critical component of many private financings in the generation, along with IFC and MIGA products.

Justifying public sector investment in generation on the grounds that it reduces financial costs to the sector is not adequate since this simply reflects the subsidies present in public financing.

In some countries there may be concerns that private financing of thermal generation will not be forthcoming, even with substantial support from the Bank Group, and that these projects will therefore have to be financed and undertaken by the public sector.

Before supporting such a strategy through IDA/IBRD financing, Bank staff should work with the government concerned to undertake a market test to assess whether there is indeed interest from the private sector.

How The Bank’s Support Fits Country ConditionsExtracts for the case of Power Generation Investments

Evolution of World Bank’s Approach

29Horizontal unbundling and competition

Vertically integrated monopoly as a national utility or monopolies as regional utilities

Wholesale power competition in a national power market of gencos, discos, and large users with an ISO and transco

Complete

Complete

Purchasing agency as the national genco, transco, disco, genco/transco, or transco/disco

Purchasing agency as the national transco, with many gencos and regional discos

Retail power competition with supply unbundled from distribution in addition to wholesale competition

Ver

tica

l unb

undl

ing

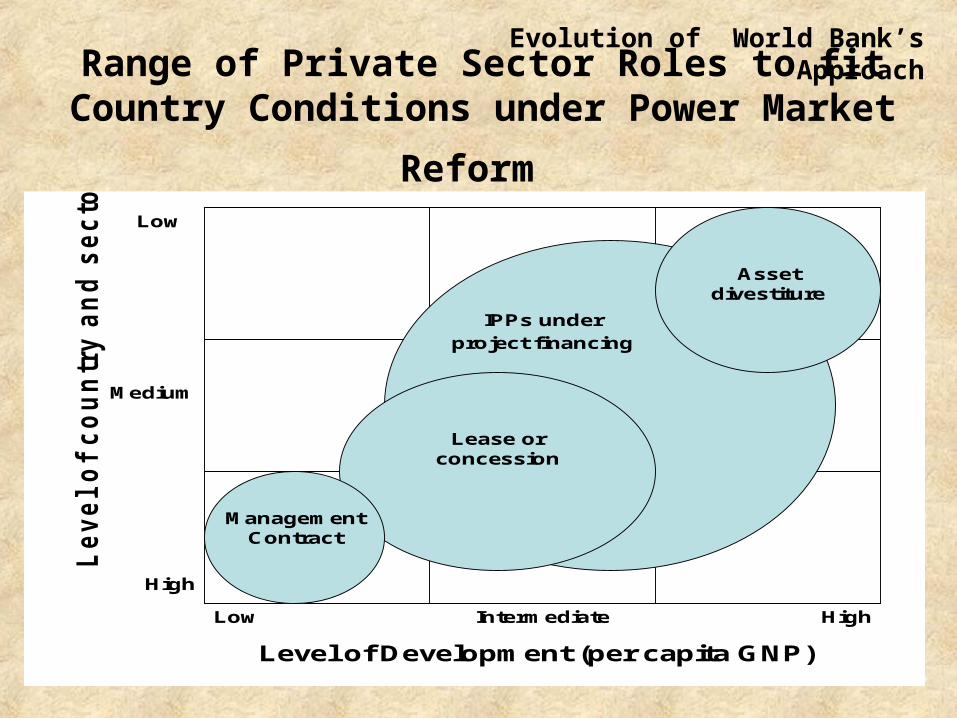

Range of Structures to fit Country Conditions under Power Market Reform

Evolution of World Bank’s Approach

30

Range of Private Sector Roles to fit Country

Conditions under Power Market Reform

Low Intermediate High

Low

Medium

High

Level of Development (per capita GNP)

Le

ve

l o

f c

ou

ntr

y a

nd

se

cto

r ri

sk

Management Contract

Lease or concession

Asset divestiture

IPPs under project financing

Evolution of World Bank’s Approach

31

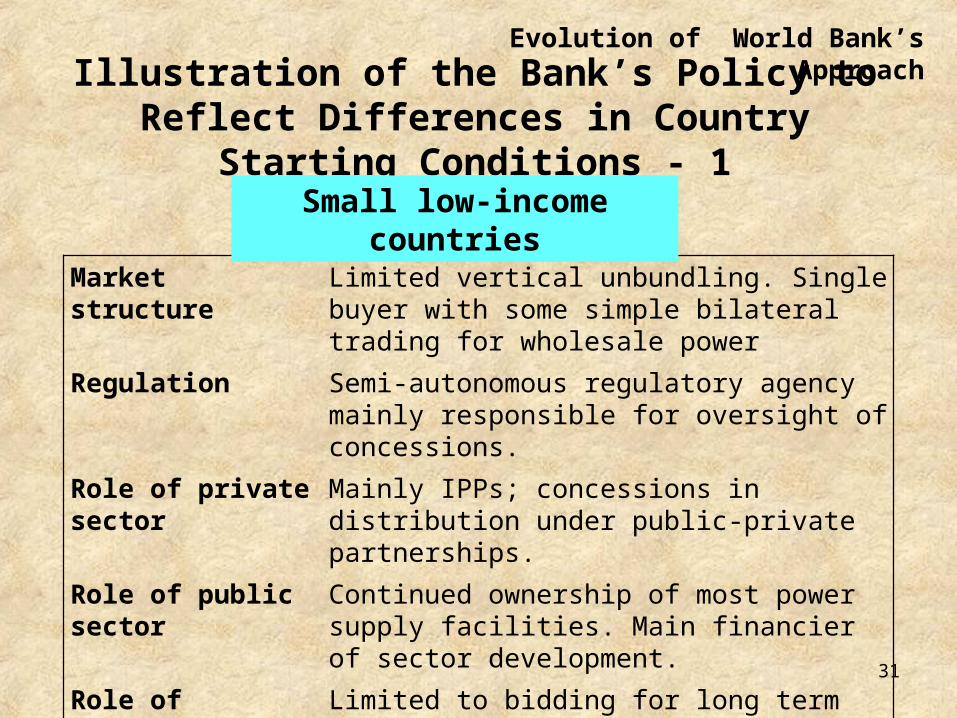

Illustration of the Bank’s Policy to Reflect Differences in Country Starting Conditions - 1

Market structure Limited vertical unbundling. Single buyer with some simple bilateral trading for wholesale power

Regulation Semi-autonomous regulatory agency mainly responsible for oversight of concessions.

Role of private sector Mainly IPPs; concessions in distribution under public-private partnerships.

Role of public sector Continued ownership of most power supply facilities. Main financier of sector development.

Role of competition Limited to bidding for long term agreements by IPPs and distribution concessions by private operators.

Small low-income countries

Evolution of World Bank’s Approach

32

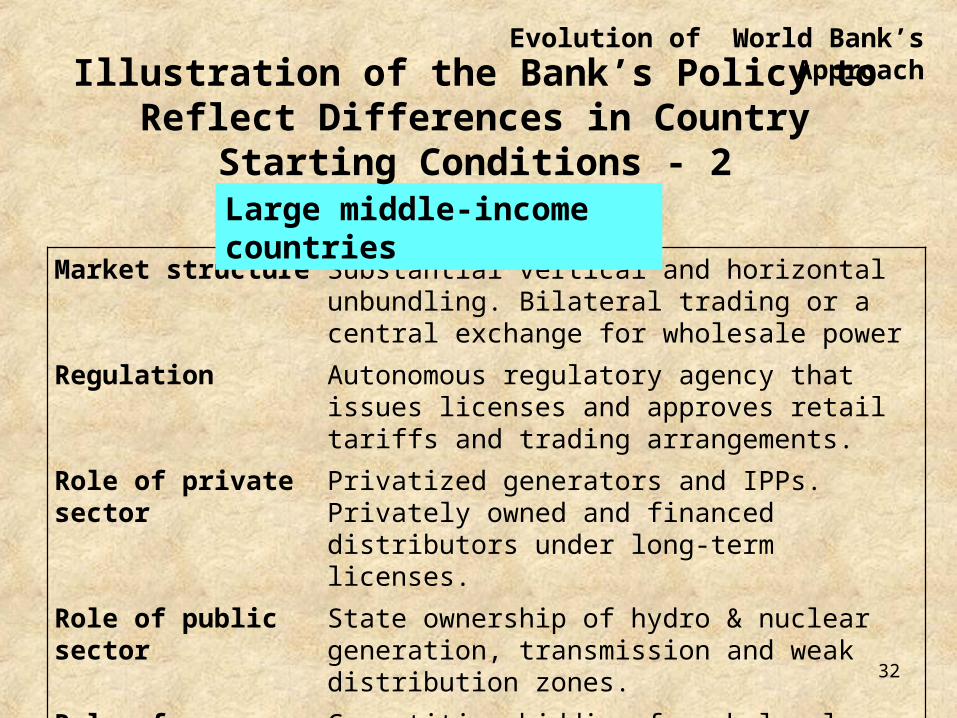

Market structure Substantial vertical and horizontal unbundling. Bilateral trading or a central exchange for wholesale power

Regulation Autonomous regulatory agency that issues licenses and approves retail tariffs and trading arrangements.

Role of private sector Privatized generators and IPPs. Privately owned and financed distributors under long-term licenses.

Role of public sector State ownership of hydro & nuclear generation, transmission and weak distribution zones.

Role of competition Competitive bidding for wholesale power contracts under bilateral trading or bidding into a power exchange.

Large middle-income countries

Illustration of the Bank’s Policy to Reflect Differences in Country Starting Conditions - 2

Evolution of World Bank’s Approach

33

We do know what: matters most for reform design are starting conditions, such as

power system size and country income conditions are sought by private investors in these power

markets political and social factors are important for reform design and

implementation challenges governments face in developing credible regulation limited forms of competition are workable in these power

markets – central energy trader, bilateral trading, cost-based bidding

technical options that are suited to providing electricity services to the poor

What Do We Know and Don’t Know about Reforming Power Markets after 15 years? - 1

Implications and Issues for The World Bank

34

What Do We Know and Don’t Know about Reforming Power Markets after 15 years? - 2

But we still don’t know how to: trade off reform of power market with easing the fiscal burden

of power sector debt and subsidies attract and keep private investors in the current conditions devise politically and socially sustainable reform programs –

few good cases exist create lasting incentives for governments to develop a good

track record for attracting investors control the high economic risks of fully competitive power

markets (price-based bidding into a power pool is too risky) mobilise support of winners to counter opposition of losers

from reform

Implications and Issues for The World Bank

35

Developing Countries have Innovated – and Need to Continue Innovating

Ring-fencing of investor’s risk exposure

Regulation by contract in a nascent regulatory framework

Capitalisation of newly corporatized state-owned entities for privatization

Third party guarantees of government and regulatory performance for long-term concessions

Output-based approaches to off-grid and rural electricity supply

Innovations that help reform power markets under developing country conditions:

Implications and Issues for The World Bank

36

On Balance, We Still have a Lot to Learn about Implementing Reform

We know what is needed for reform design

But we’re still experimenting about how to implement reform under the conditions of developing countries

Implications and Issues for The World Bank

37

1. What Has Happened Under Power Market Reform

3. Implications and Issues for the World Bank

Structure of the Presentation

2. Evolution of the World Bank’s Approach to Power Market Reform

38

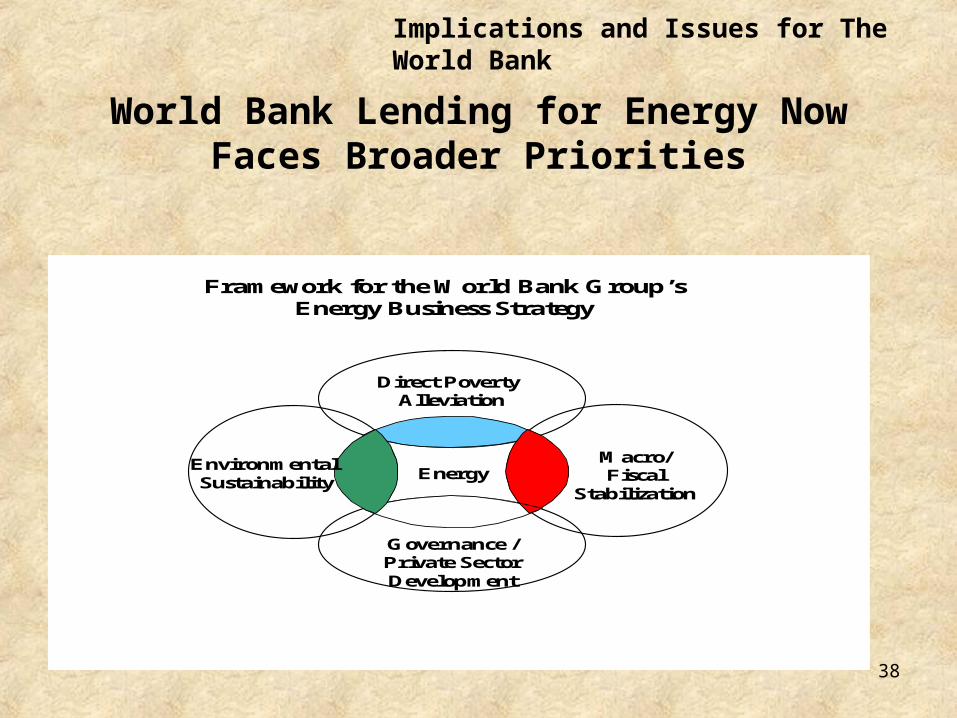

World Bank Lending for Energy Now Faces Broader Priorities

Framework for the World Bank Group’s Energy Business Strategy

Energy

Direct Poverty Alleviation

Governance /Private Sector Development

Macro/Fiscal

Stabilization

Environmental Sustainability

Implications and Issues for The World Bank

39

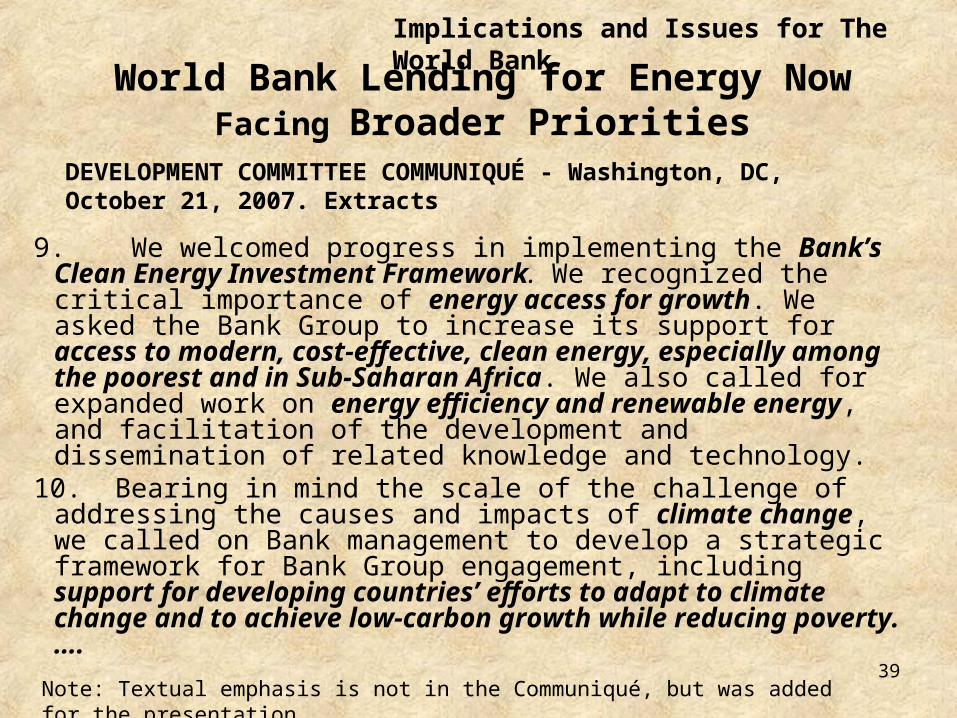

World Bank Lending for Energy Now Facing

Broader Priorities

9. We welcomed progress in implementing the Bank’s Clean Energy Investment Framework. We recognized the critical importance of energy access for growth. We asked the Bank Group to increase its support for access to modern, cost-effective, clean energy, especially among the poorest and in Sub-Saharan Africa. We also called for expanded work on energy efficiency and renewable energy, and facilitation of the development and dissemination of related knowledge and technology.

10. Bearing in mind the scale of the challenge of addressing the causes and impacts of climate change, we called on Bank management to develop a strategic framework for Bank Group engagement, including support for developing countries’ efforts to adapt to climate change and to achieve low-carbon growth while reducing poverty.….

DEVELOPMENT COMMITTEE COMMUNIQUÉ - Washington, DC, October 21, 2007. Extracts

Note: Textual emphasis is not in the Communiqué, but was added for the presentation

Implications and Issues for The World Bank

40

Why Should the World Bank Still Be Interested in Power Market Reform?

It’s big and it can’t be ignored.

Power Market Reform is vital for the World Bank’s Corporate Priorities:

• Clean energy

• Access

• Anti-corruption

Implications and Issues for The World Bank

41

Where Next for the World Bank’s Support for Power Market Reform?

Power market reforms in developing countries are tentative, incomplete and work-in-progress

Reforms have been constrained by lack of country commitment, macroeconomic and political crises, and lack of experience with political economy factors

Countries are facing massive investment requirements in their power sectors

They also face external constraints on developing their power supply, especially on carbon emissions

These countries cannot turn back to the failed old model of power supply (a few are considering whether to backtrack)

Implications and Issues for The World Bank

The basic dilemma is how can these countries advance their reforms to achieve long-term sustainability in their power markets?

42

Where Next for the World Bank’s Support for Power Market Reform?

integrate reform into its corporate priorities refine its reform designs to country conditions better understand the political economy of reform help attract private investors to the sector help countries design low-carbon development strategies for

power supply be the adviser and financier of choice for middle income

countries help poor countries substantially increase access to electricity

for the population (necessary for achieving the millennium development goals)

Implications and Issues for The World Bank

How should the World Bank Group respond to:

43

THANK YOU