Embed Size (px)

Citation preview

11

An Overview of An Overview of Impact Fees in Impact Fees in ColoradoColorado

Eric Bergman, ModeratorEric Bergman, ModeratorTina Axelrad, PanelistTina Axelrad, PanelistCarolynne White, PanelistCarolynne White, Panelist

20052005

Impact Fee Impact Fee RoundtableRoundtableOctober 6, 2005October 6, 2005

22

Overview of Panel DiscussionOverview of Panel Discussion

Today’s Landscape in Colorado (Tina Axelrad)Today’s Landscape in Colorado (Tina Axelrad)The Legal Landscape in Colorado (Carolynne The Legal Landscape in Colorado (Carolynne

White) White) Colorado’s Use of Impact Fees (Eric Bergman) Colorado’s Use of Impact Fees (Eric Bergman) Lessons Learned: Considerations During Lessons Learned: Considerations During

ImplementationImplementationQuestions and AnswersQuestions and Answers

33

Today’s Landscape in Today’s Landscape in ColoradoColorado

Tina AxelradTina Axelrad

Principal, Clarion AssociatesPrincipal, Clarion Associates

[email protected]@clarionassociates.com

20052005

Impact Fee Impact Fee RoundtableRoundtableOctober 6, 2005October 6, 2005

44

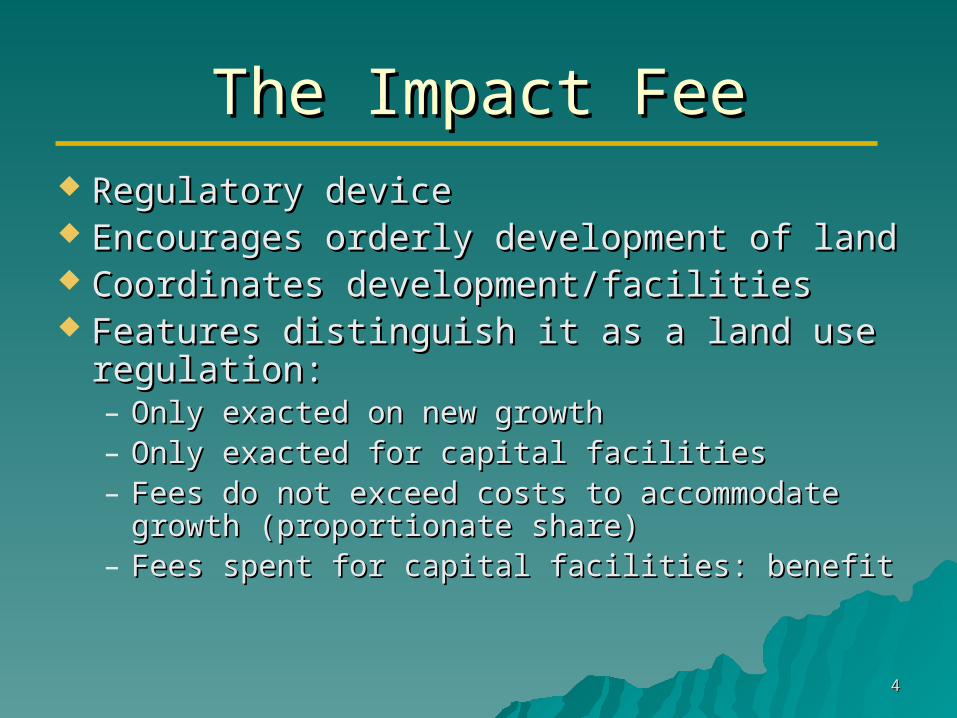

The Impact FeeThe Impact Fee Regulatory deviceRegulatory device Encourages orderly development of landEncourages orderly development of land Coordinates development/facilitiesCoordinates development/facilities Features distinguish it as a land use Features distinguish it as a land use

regulation:regulation:– Only exacted on new growthOnly exacted on new growth– Only exacted for capital facilitiesOnly exacted for capital facilities– Fees do not exceed costs to accommodate Fees do not exceed costs to accommodate

growth (proportionate share)growth (proportionate share)– Fees spent for capital facilities: benefitFees spent for capital facilities: benefit

55

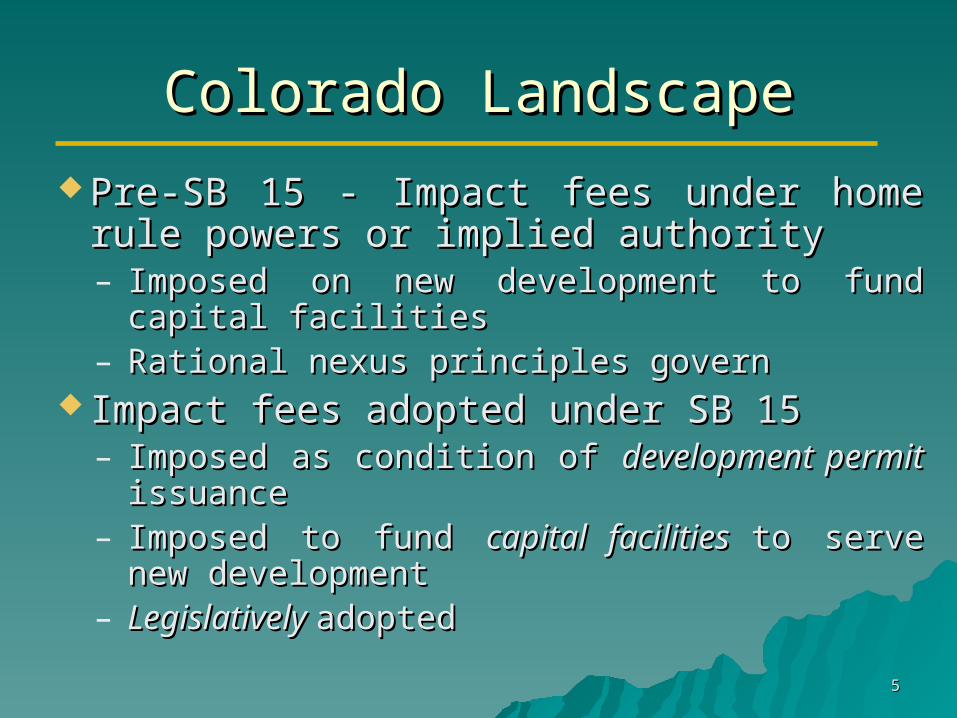

Colorado LandscapeColorado Landscape

Pre-SB 15 - Impact fees under home rule powers or Pre-SB 15 - Impact fees under home rule powers or implied authorityimplied authority– Imposed on new development to fund capital facilitiesImposed on new development to fund capital facilities– Rational nexus principles governRational nexus principles govern

Impact fees adopted under SB 15Impact fees adopted under SB 15– Imposed as condition of Imposed as condition of development permit development permit issuanceissuance– Imposed to fund Imposed to fund capital facilities capital facilities to serve new to serve new

developmentdevelopment– Legislatively Legislatively adopted adopted

66

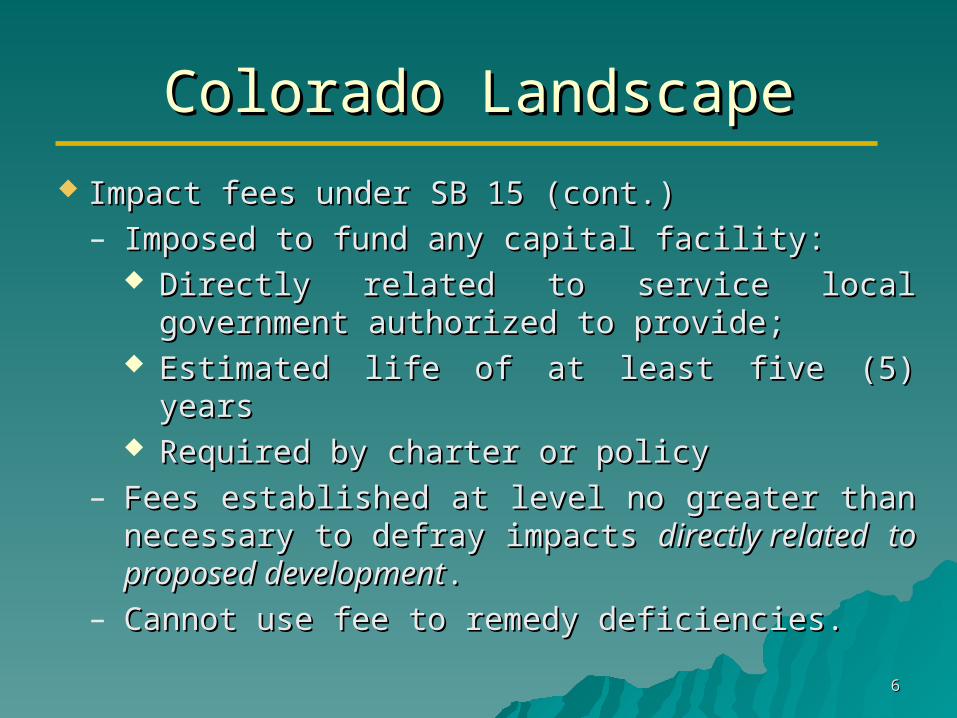

Colorado LandscapeColorado Landscape

Impact fees under SB 15 (cont.)Impact fees under SB 15 (cont.)– Imposed to fund any capital facility:Imposed to fund any capital facility:

Directly related to service local government authorized Directly related to service local government authorized to provide;to provide;

Estimated life of at least five (5) yearsEstimated life of at least five (5) yearsRequired by charter or policy Required by charter or policy

– Fees established at level no greater than necessary to Fees established at level no greater than necessary to defray impacts defray impacts directly relateddirectly related to proposed developmentto proposed development. .

– Cannot use fee to remedy deficiencies.Cannot use fee to remedy deficiencies.

77

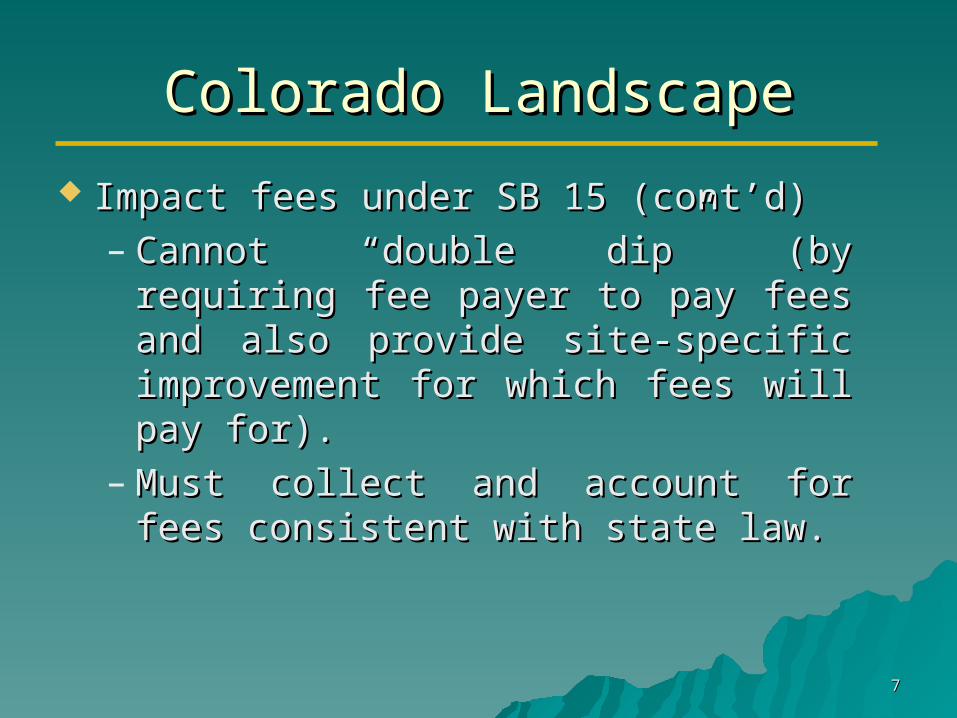

Colorado LandscapeColorado Landscape

Impact fees under SB 15 (cont’d)Impact fees under SB 15 (cont’d)– Cannot “double dip” (by requiring fee payer to pay Cannot “double dip” (by requiring fee payer to pay

fees and also provide site-specific improvement for fees and also provide site-specific improvement for which fees will pay for). which fees will pay for).

– Must collect and account for fees consistent with Must collect and account for fees consistent with state law.state law.

88

Colorado Statutory and Colorado Statutory and Case Law on Impact Case Law on Impact

FeesFees

Carolynne C. WhiteCarolynne C. White

Brownstein, Hyatt & Farber, PCBrownstein, Hyatt & Farber, PC

[email protected]@bhf-law.com

20052005

Impact Fee Impact Fee RoundtableRoundtableOctober 6, 2005October 6, 2005

99

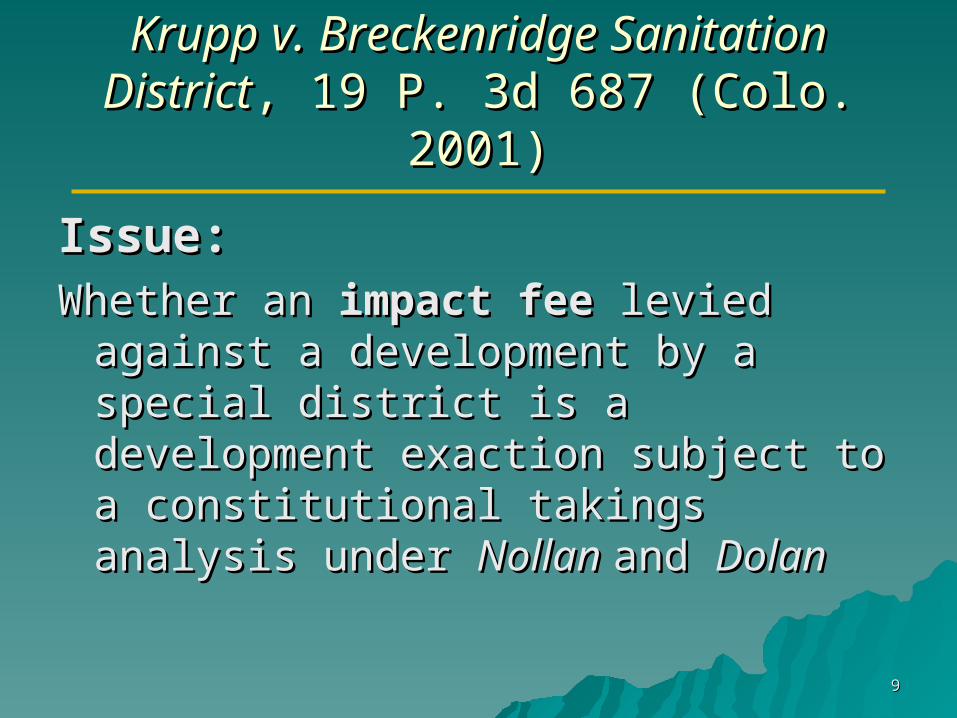

Krupp v. Breckenridge Sanitation Krupp v. Breckenridge Sanitation DistrictDistrict, 19 P. 3d 687 (Colo. 2001), 19 P. 3d 687 (Colo. 2001)

Issue:Issue:Whether an Whether an impact fee impact fee levied against a development levied against a development

by a special district is a development exaction by a special district is a development exaction subject to a constitutional takings analysis under subject to a constitutional takings analysis under Nollan Nollan and and DolanDolan

1010

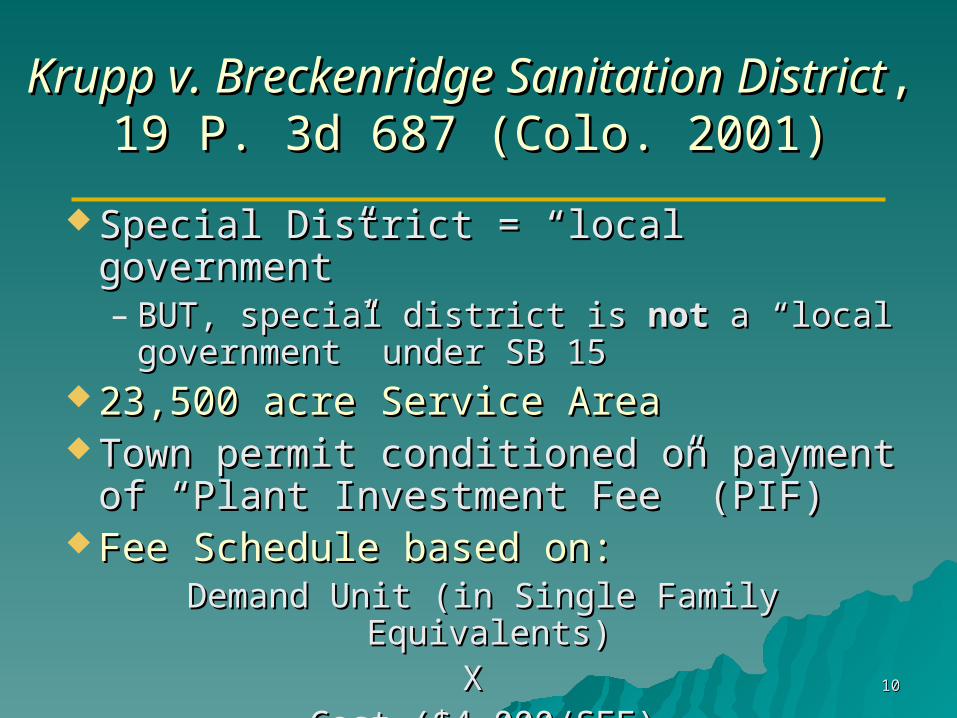

Krupp v. Breckenridge Sanitation Krupp v. Breckenridge Sanitation DistrictDistrict, 19 P. 3d 687 (Colo. 2001), 19 P. 3d 687 (Colo. 2001)

Special District = “local government”Special District = “local government”– BUT, special district is BUT, special district is notnot a “local government” under a “local government” under

SB 15SB 15 23,500 acre Service Area23,500 acre Service Area Town permit conditioned on payment of “Plant Town permit conditioned on payment of “Plant

Investment Fee” (PIF)Investment Fee” (PIF) Fee Schedule based on: Fee Schedule based on:

Demand Unit (in Single Family Equivalents) Demand Unit (in Single Family Equivalents) X X

Cost ($4,000/SFE)Cost ($4,000/SFE)

1111

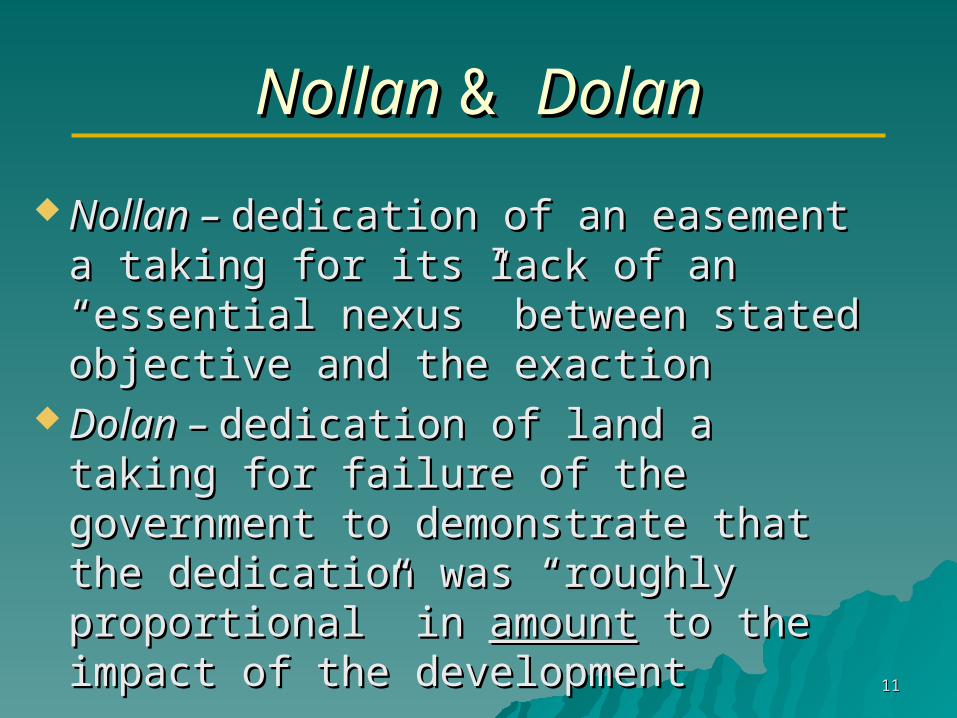

Nollan Nollan & & DolanDolan

Nollan – Nollan – dedication of an easement a taking for its dedication of an easement a taking for its lack of an “essential nexus” between stated lack of an “essential nexus” between stated objective and the exactionobjective and the exaction

Dolan – Dolan – dedication of land a taking for failure of the dedication of land a taking for failure of the government to demonstrate that the dedication was government to demonstrate that the dedication was “roughly proportional” in “roughly proportional” in amountamount to the impact of to the impact of the developmentthe development

1212

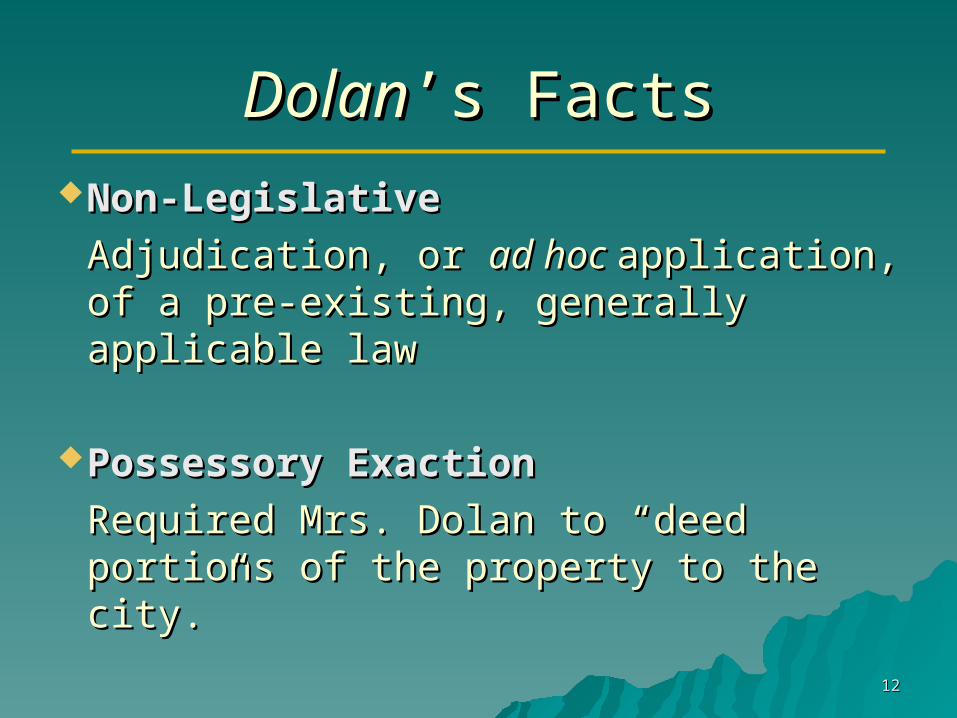

DolanDolan’s Facts’s FactsNon-LegislativeNon-Legislative

Adjudication, or Adjudication, or ad hoc ad hoc application, of a pre-application, of a pre-existing, generally applicable lawexisting, generally applicable law

Possessory ExactionPossessory Exaction

Required Mrs. Dolan to “deed portions of the Required Mrs. Dolan to “deed portions of the property to the city.”property to the city.”

1313

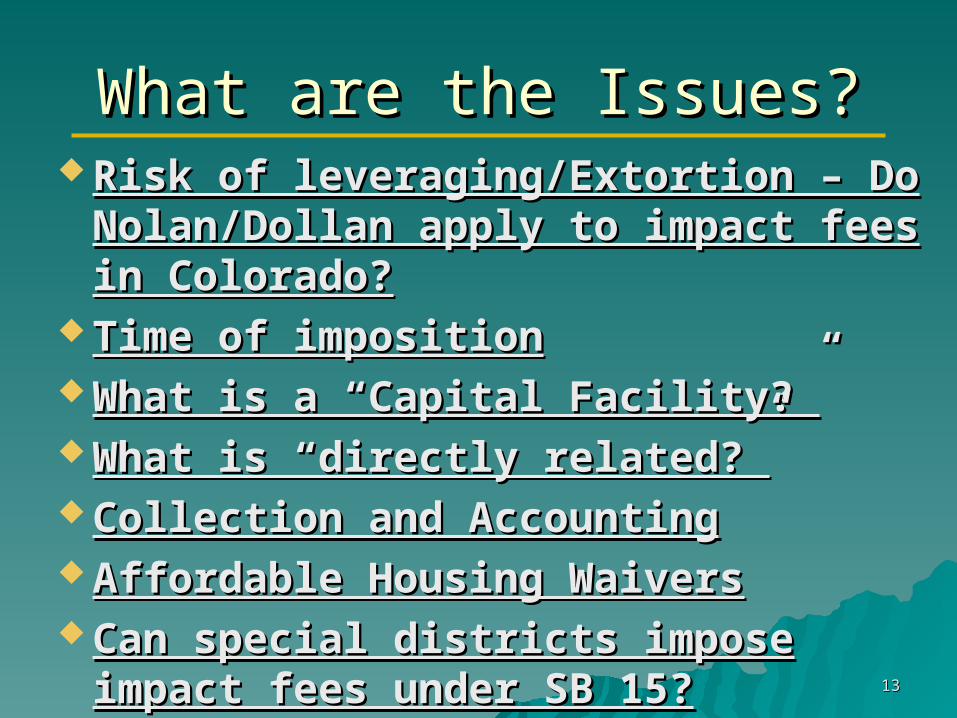

What are the Issues?What are the Issues? Risk of leveraging/Extortion – Do Nolan/Dollan Risk of leveraging/Extortion – Do Nolan/Dollan

apply to impact fees in Colorado?apply to impact fees in Colorado? Time of impositionTime of imposition What is a “Capital Facility?”What is a “Capital Facility?” What is “directly related?”What is “directly related?” Collection and AccountingCollection and Accounting Affordable Housing WaiversAffordable Housing Waivers Can special districts impose impact fees under SB Can special districts impose impact fees under SB

15?15?

1414

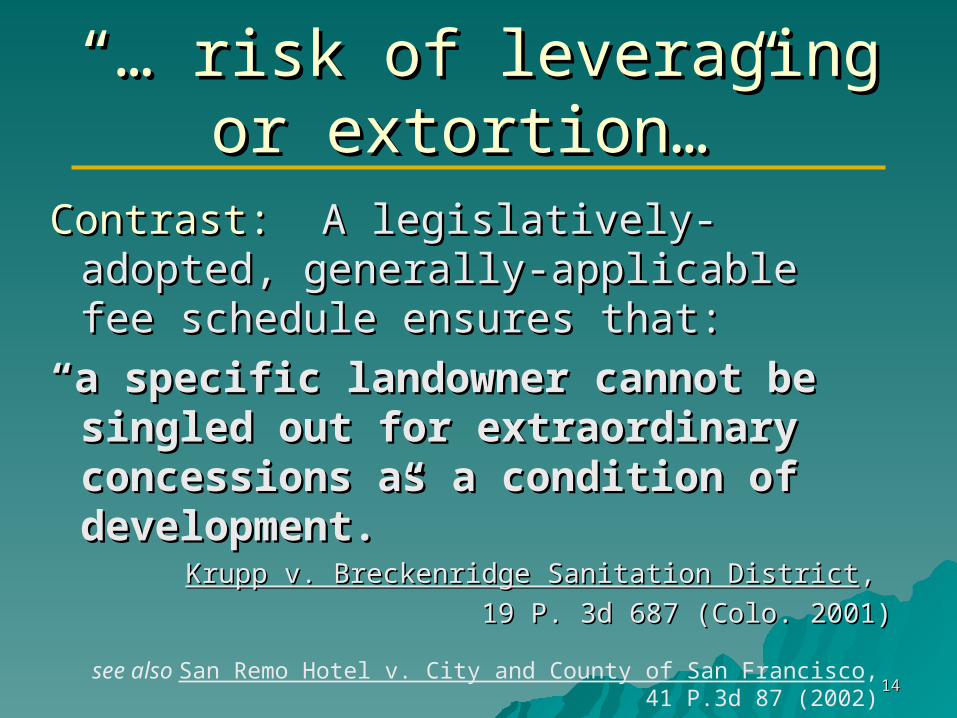

“… “… risk of leveraging or risk of leveraging or extortion…”extortion…”

Contrast: Contrast: A legislatively-adopted, generally-A legislatively-adopted, generally-applicable fee schedule ensures that: applicable fee schedule ensures that:

““a specific landowner cannot be singled out a specific landowner cannot be singled out for extraordinary concessions as a for extraordinary concessions as a condition of development.”condition of development.”

Krupp v. Breckenridge Sanitation DistrictKrupp v. Breckenridge Sanitation District, ,

19 P. 3d 687 (Colo. 2001)19 P. 3d 687 (Colo. 2001)

see also San Remo Hotel v. City and County of San Francisco, 41 P.3d 87 (2002)

1515

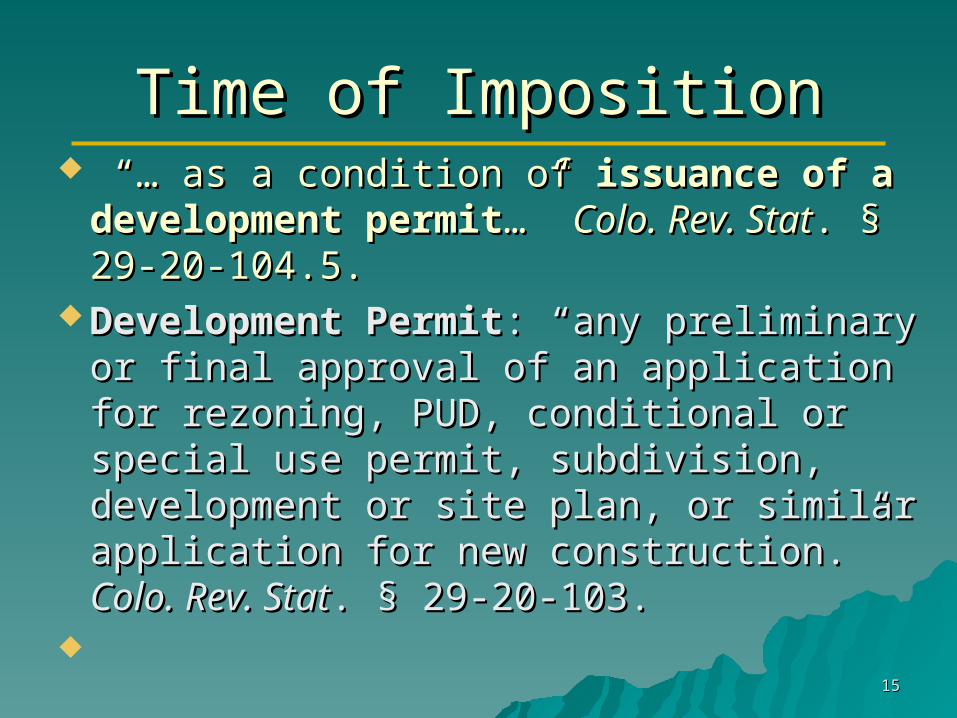

Time of ImpositionTime of Imposition “… “… as a condition of as a condition of issuance of a development issuance of a development

permitpermit…” …” Colo. Rev. StatColo. Rev. Stat. § 29-20-104.5.. § 29-20-104.5. Development PermitDevelopment Permit: “any preliminary or final : “any preliminary or final

approval of an application for rezoning, PUD, approval of an application for rezoning, PUD, conditional or special use permit, subdivision, conditional or special use permit, subdivision, development or site plan, or similar application for development or site plan, or similar application for new construction.” new construction.” Colo. Rev. StatColo. Rev. Stat. § 29-20-103.. § 29-20-103.

1616

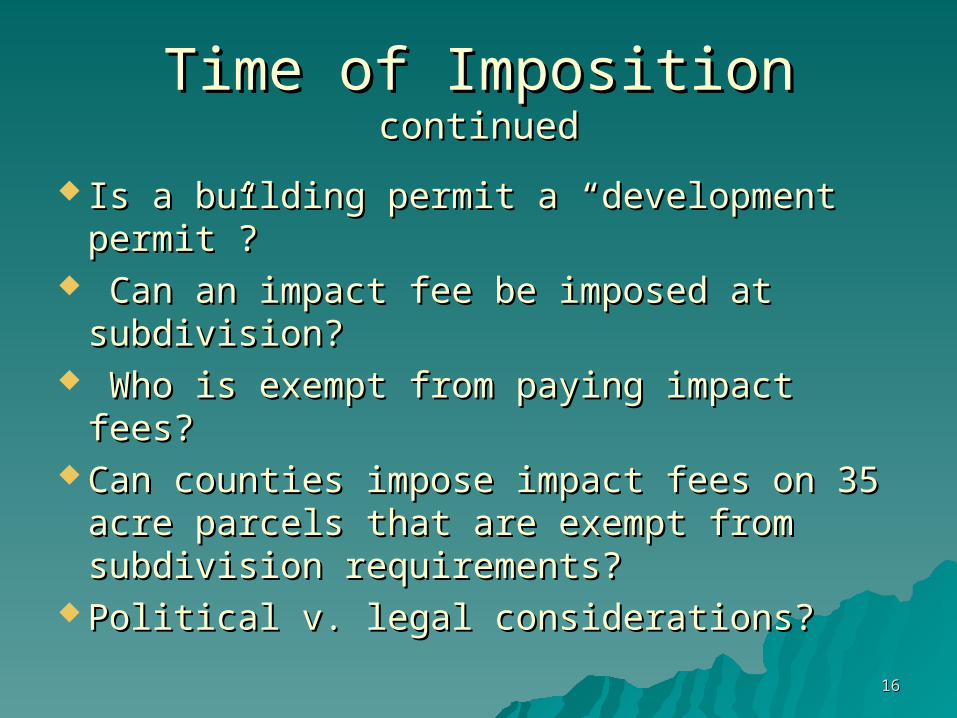

Time of Imposition Time of Imposition continuedcontinued

Is a building permit a “development permit”?Is a building permit a “development permit”? Can an impact fee be imposed at subdivision?Can an impact fee be imposed at subdivision? Who is exempt from paying impact fees?Who is exempt from paying impact fees? Can counties impose impact fees on 35 acre Can counties impose impact fees on 35 acre

parcels that are exempt from subdivision parcels that are exempt from subdivision requirements?requirements?

Political v. legal considerations?Political v. legal considerations?

1717

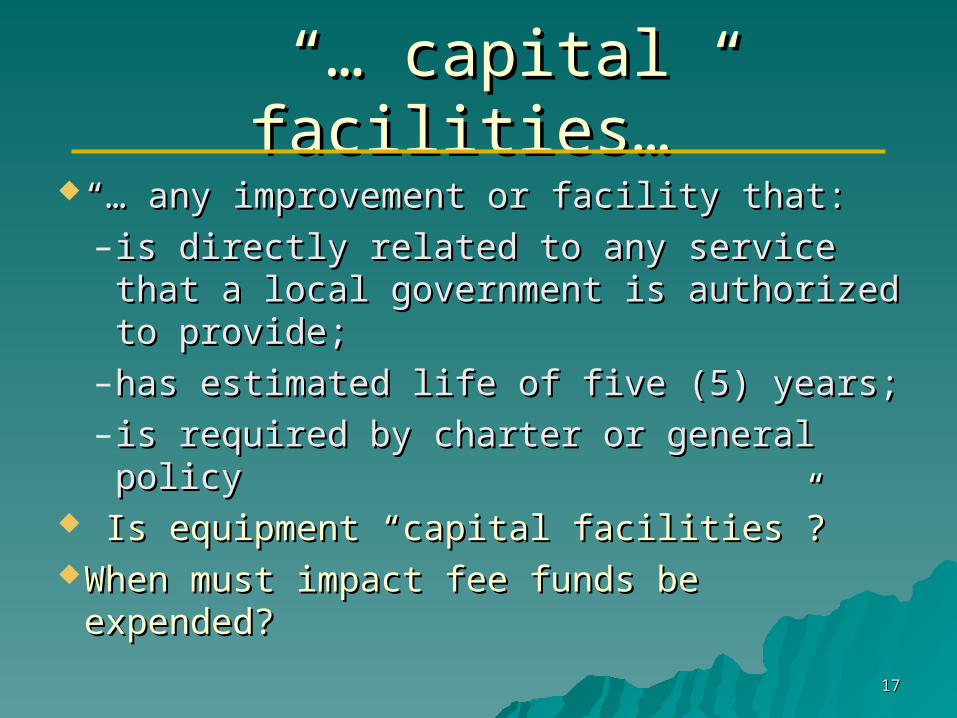

“… “… capital facilities…”capital facilities…”

“… “… any improvement or facility that:any improvement or facility that:– is directly related to any service that a local is directly related to any service that a local

government is authorized to provide;government is authorized to provide;– has estimated life of five (5) years;has estimated life of five (5) years;– is required by charter or general policyis required by charter or general policy

Is equipment “capital facilities”? Is equipment “capital facilities”? When must impact fee funds be expended?When must impact fee funds be expended?

1818

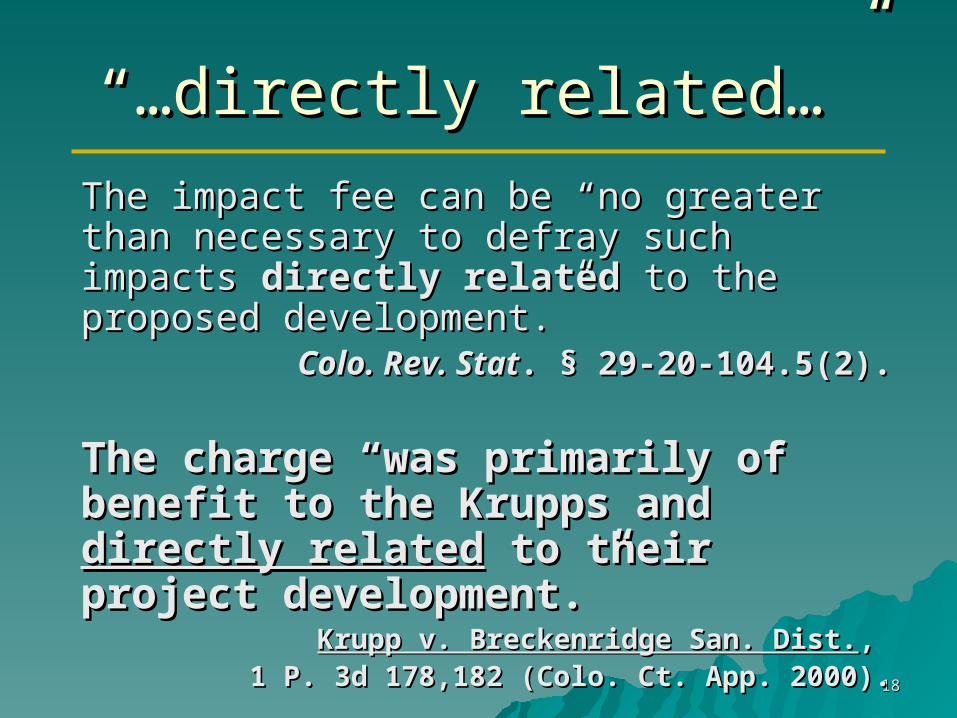

“…“…directly related…”directly related…”

The impact fee can be “no greater than necessary The impact fee can be “no greater than necessary to defray such impacts to defray such impacts directly relateddirectly related to the to the proposed development.” proposed development.”

Colo. Rev. StatColo. Rev. Stat. § 29-20-104.5(2).. § 29-20-104.5(2).

The charge “was primarily of benefit to the The charge “was primarily of benefit to the Krupps and Krupps and directly relateddirectly related to their project to their project development.” development.”

Krupp v. Breckenridge San. Dist.Krupp v. Breckenridge San. Dist., , 1 P. 3d 178,182 (Colo. Ct. App. 2000).1 P. 3d 178,182 (Colo. Ct. App. 2000).

1919

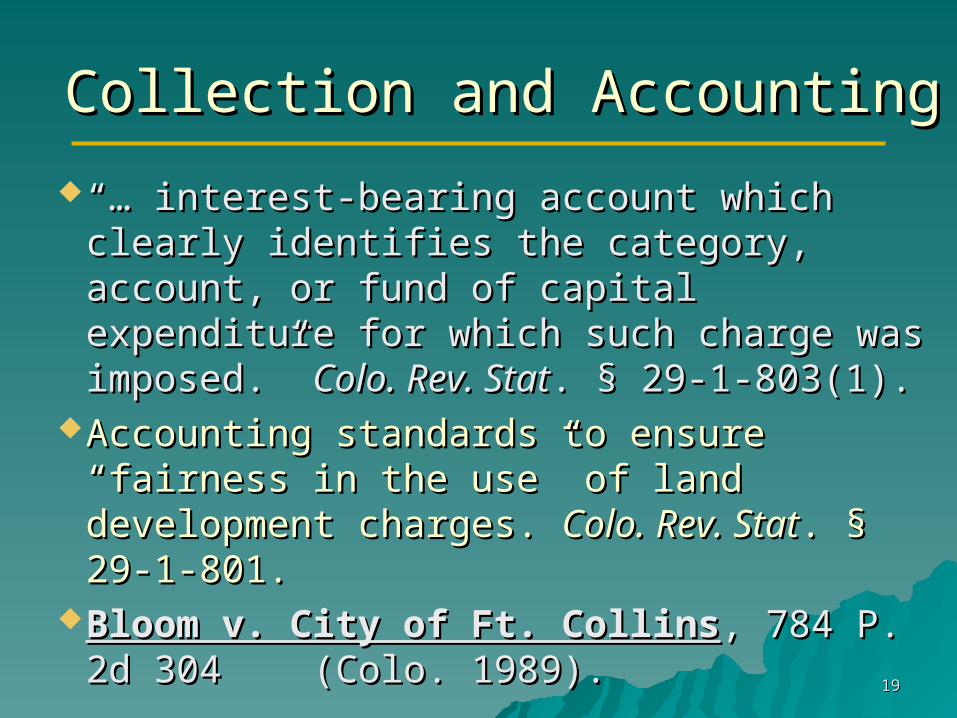

Collection and AccountingCollection and Accounting

“… “… interest-bearing account which clearly interest-bearing account which clearly identifies the category, account, or fund of identifies the category, account, or fund of capital expenditure for which such charge was capital expenditure for which such charge was imposed.” imposed.” Colo. Rev. StatColo. Rev. Stat. § 29-1-803(1).. § 29-1-803(1).

Accounting standards to ensure “fairness in the Accounting standards to ensure “fairness in the use” of land development charges. use” of land development charges. Colo. Rev. Colo. Rev. StatStat. § 29-1-801.. § 29-1-801.

Bloom v. City of Ft. CollinsBloom v. City of Ft. Collins, 784 P. 2d 304 , 784 P. 2d 304 (Colo. 1989).(Colo. 1989).

2020

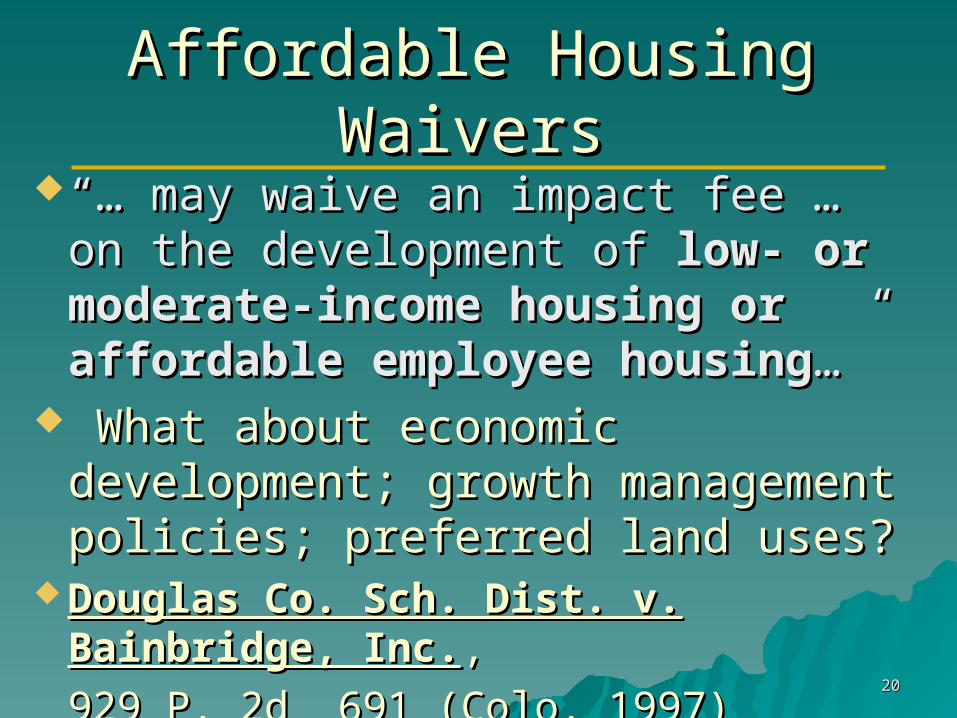

Affordable Housing Affordable Housing WaiversWaivers

“… “… may waive an impact fee … on the may waive an impact fee … on the development of development of low- or moderate-income low- or moderate-income housing or affordable employee housinghousing or affordable employee housing…”…”

What about economic development; growth What about economic development; growth management policies; preferred land uses?management policies; preferred land uses?

Douglas Co. Sch. Dist. v. Bainbridge, Inc.Douglas Co. Sch. Dist. v. Bainbridge, Inc. , , 929 P. 2d 691 (Colo. 1997)929 P. 2d 691 (Colo. 1997)

2121

Can special districts impose Can special districts impose impact fees under SB 15?impact fees under SB 15?

Statute does not expressly authorizeStatute does not expressly authorize Legislative history does not supportLegislative history does not support BUT . . . BUT . . . Krupp court approved of impact fee Krupp court approved of impact fee

imposed by special districtimposed by special district Special districts may have authority under Special districts may have authority under

enabling legislationenabling legislation Answer: municipality or county and Answer: municipality or county and

special district to design most appropriate special district to design most appropriate arrangementarrangement

2222

Colorado Communities Colorado Communities Use of Impact FeesUse of Impact Fees

Eric BergmanEric Bergman

Office of Smart Growth,Office of Smart Growth,

Colorado Heritage Colorado Heritage

Planning GrantsPlanning Grants

[email protected]@state.co.us

20052005

Impact Fee Impact Fee RoundtableRoundtableOctober 6, 2005October 6, 2005

2323

Land Use Planning SurveyLand Use Planning Survey

County Survey:County Survey:

Undertaken April, 2004 by interns Undertaken April, 2004 by interns with the Office of Smart Growthwith the Office of Smart Growth

2424

Land Use Planning SurveyLand Use Planning Survey

Municipal Survey: Municipal Survey:

Undertaken July – September, 2004, by Undertaken July – September, 2004, by Carolynne White in cooperation with the Carolynne White in cooperation with the Office of Smart GrowthOffice of Smart Growth

2525

Land Use Planning SurveyLand Use Planning Survey

County Survey: County Survey: 64 Counties surveyed64 Counties surveyed 59 Counties responded59 Counties responded

2626

Land Use Planning SurveyLand Use Planning Survey

County Survey: County Survey: Of those 59 counties, 20 indicated they Of those 59 counties, 20 indicated they

were using impact fees (34%)were using impact fees (34%)

2727

2828

2929

Land Use Planning SurveyLand Use Planning Survey

Municipal Survey: Municipal Survey: 270 municipalities surveyed270 municipalities surveyed To date, 153 have respondedTo date, 153 have responded

3030

Land Use Planning SurveyLand Use Planning Survey

Municipal Survey: Municipal Survey: Of those 153, 94 indicated they were using Of those 153, 94 indicated they were using

impact fees (61%) impact fees (61%)

3131

3232

Lessons Learned:Lessons Learned:Considerations for Considerations for ImplementationImplementation

Eric BergmanEric Bergman

Tina AxelradTina Axelrad

Carolynne WhiteCarolynne White

20052005

Impact Fee Impact Fee RoundtableRoundtableOctober 6, 2005October 6, 2005

3333

Considerations During Considerations During ImplementationImplementation

Fully consider legal limitations and implications Fully consider legal limitations and implications – How are benefits and burdens of impact fees How are benefits and burdens of impact fees

allocated?allocated? Work with counsel in design of fee programWork with counsel in design of fee program Prepare and adopt support studyPrepare and adopt support study

– Base fees on up-to-date CIP or LOSBase fees on up-to-date CIP or LOS– Comply with “directly related” nexus standardComply with “directly related” nexus standard– Identify past deficiencies, and correctIdentify past deficiencies, and correct– Ensure benefit; consider benefit districts as optionEnsure benefit; consider benefit districts as option

If waivers are provided, must replenish impact fee If waivers are provided, must replenish impact fee account with non-impact fee revenuesaccount with non-impact fee revenues

3434

Considerations During Considerations During ImplementationImplementation

Draft detailed legislative findings:Draft detailed legislative findings: – that the fees are “directly related to” new that the fees are “directly related to” new

developmentdevelopment– that all impact fee eligible expenditures are for that all impact fee eligible expenditures are for

“capital facilities”“capital facilities”– that facilities for which impact fees are collected that facilities for which impact fees are collected

are required by the charter or general policyare required by the charter or general policy– that fees will not be used to cure past that fees will not be used to cure past

deficienciesdeficiencies

3535

Considerations During Considerations During ImplementationImplementation

Draft fee ordinance carefully and thoughtfully…Draft fee ordinance carefully and thoughtfully…– Incorporate fee schedule by reference into fee ordinanceIncorporate fee schedule by reference into fee ordinance– Consider provision for automatic inflation adjustmentsConsider provision for automatic inflation adjustments– Allow independent analysisAllow independent analysis

Be prepared for careful administrationBe prepared for careful administration– Keep good records; track fees paid and revenues spent in Keep good records; track fees paid and revenues spent in

the event of challengethe event of challenge Provide for refunds if monies not spent

3636

Questions and DiscussionQuestions and Discussion

![4-Country Smoking & Vaping W1 Survey Code: 4CV1 Languages ... · 1 CA Leger panelist 2 US GfK panelist 3 EN Ipsos panelist 4 [leave blank] 5 US Ipsos panelist 6 AU RMR panelist 7](https://img.pdfslide.net/doc/110x75/5eccc5e909f46d75d3057abb/4-country-smoking-vaping-w1-survey-code-4cv1-languages-1-ca-leger-panelist.jpg)