Embed Size (px)

Citation preview

1

ASFMRA Annual MeetingOctober 28, 2009

Appraisers, Lenders, and Flood Insurance

2

Appraisers, Lenders, Flood Insurance

• Federally regulated lenders are subject to requirements of the National Flood Insurance Program (‘NFIP’).

• FEMA clarified it’s flood insurance guidelines in 2007.

• Lenders are responsible to determine if a building is, or will be, located in a Special Flood Hazard Area (‘SFHA’).

• Flood determination is made prior to loan origination.

• If a flood determination is made on the property and any portion of the property lies in a FEMA-defined flood zone, then the loan is “designated”.

• Lender must provide notice to landowner if the collateral is in a SFHA; this applies even if the collateral is “land only”.

Appraisers, Lenders, Flood Insurance

FEMA Flood Hazard Zone Designations

• Mandatory flood insurance is required on buildings situated in Zones beginning with A or V. These areas are highly susceptible to flooding.

• Zones B, C, and X are areas lying outside of the 100-year floodplain or protected by a levee. Flood insurance is not mandatory within these areas.

• Property must be in a community that participates in the NFIP for mandatory purchase requirements to apply.

3

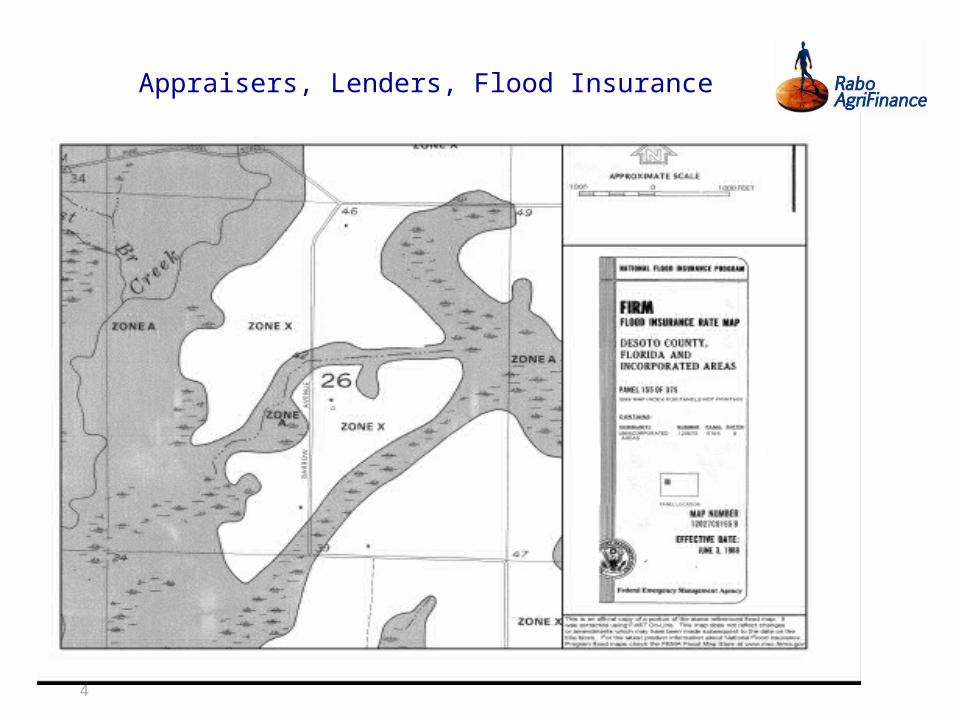

Appraisers, Lenders, Flood Insurance

4

5

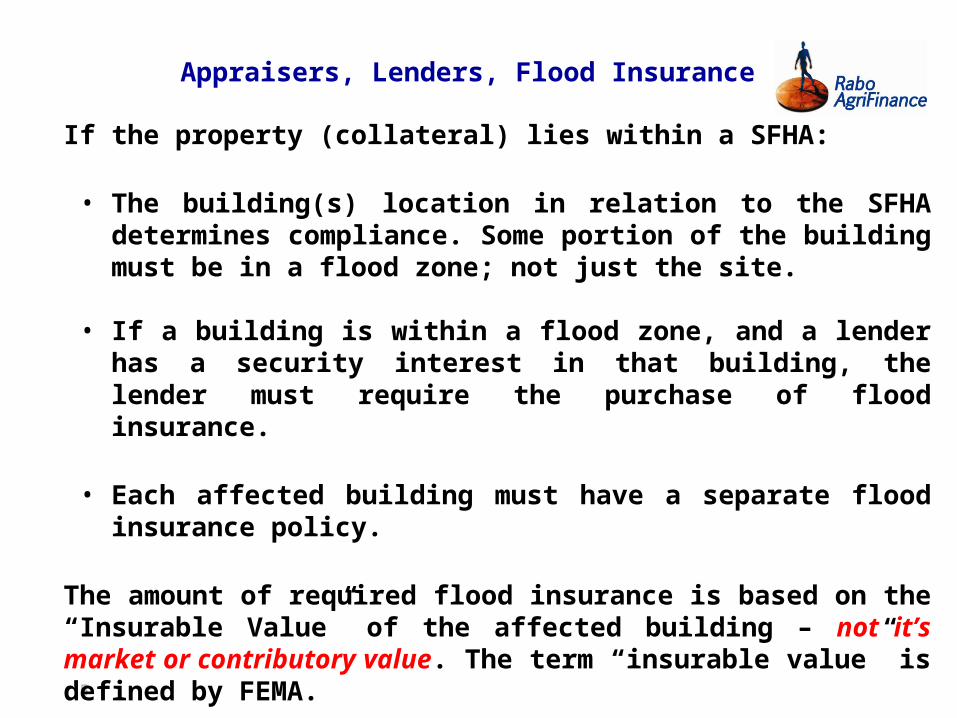

Appraisers, Lenders, Flood Insurance

If the property (collateral) lies within a SFHA:

• The building(s) location in relation to the SFHA determines compliance. Some portion of the building must be in a flood zone; not just the site.

• If a building is within a flood zone, and a lender has a

security interest in that building, the lender must require the purchase of flood insurance.

• Each affected building must have a separate flood insurance policy.

The amount of required flood insurance is based on the “Insurable Value” of the affected building – not it’s market or contributory value. The term “insurable value” is defined by FEMA.

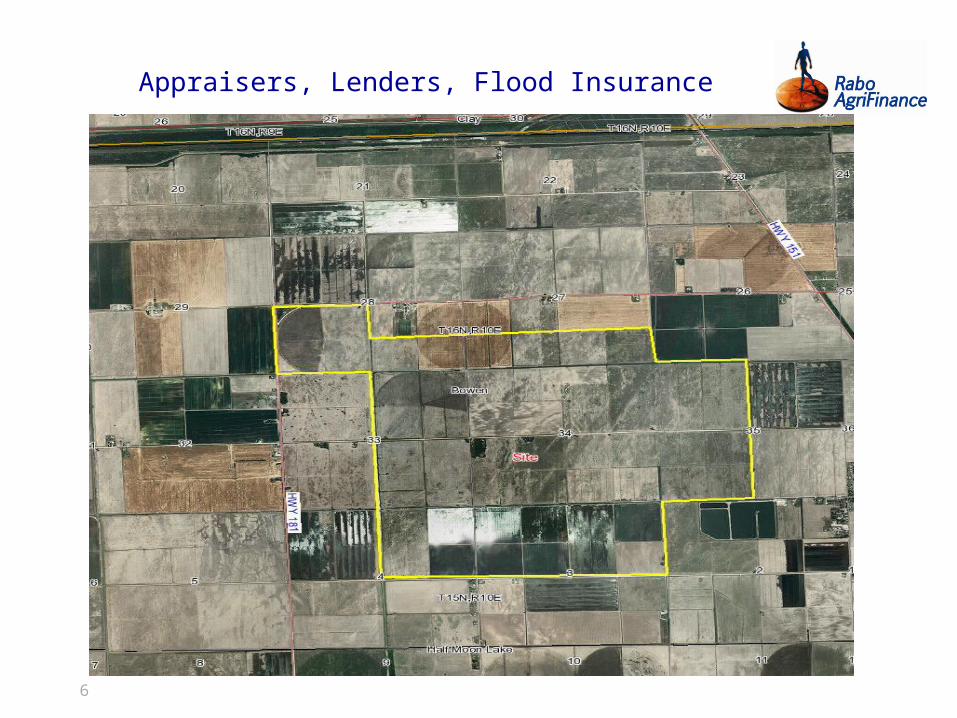

Appraisers, Lenders, Flood Insurance

6

Appraisers, Lenders, Flood Insurance

7

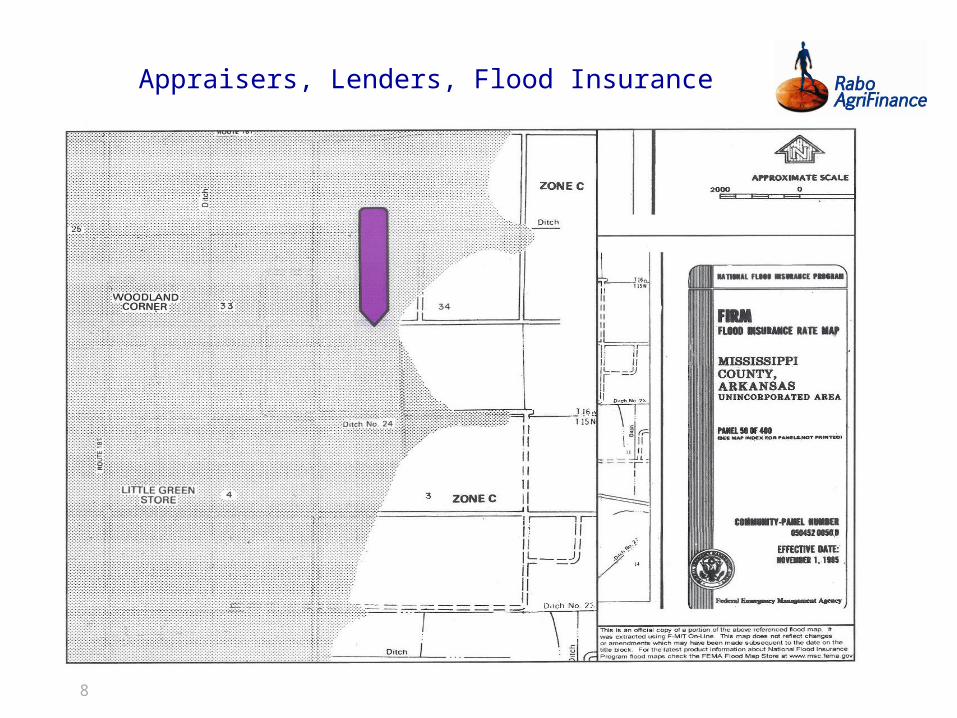

Appraisers, Lenders, Flood Insurance

8

Appraisers, Lenders, Flood Insurance

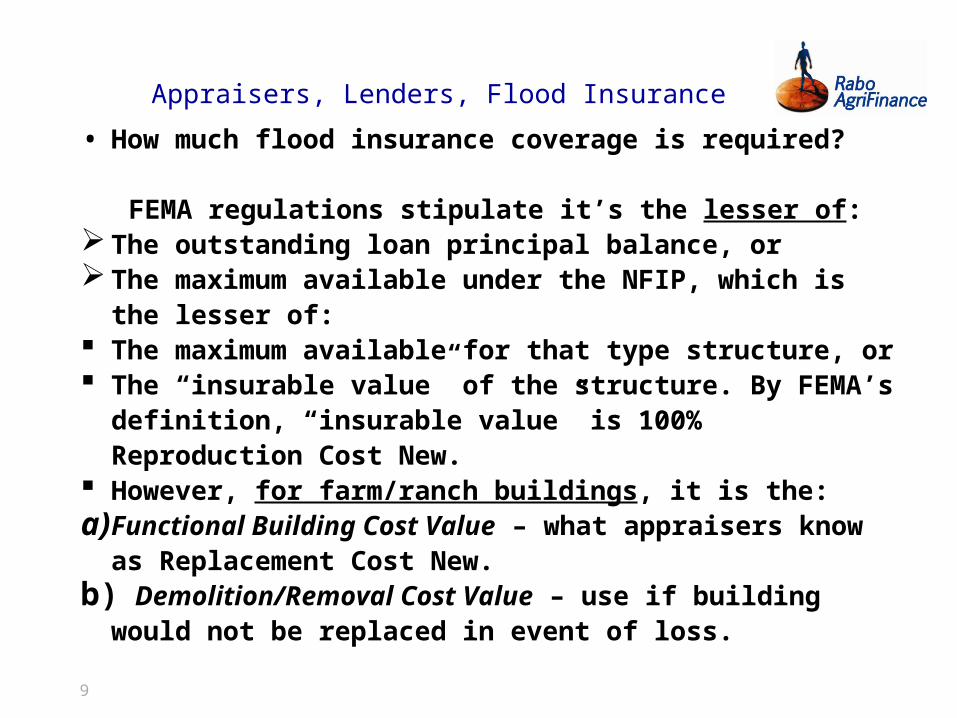

• How much flood insurance coverage is required? FEMA regulations stipulate it’s the lesser of:The outstanding loan principal balance, orThe maximum available under the NFIP, which is

the lesser of: The maximum available for that type structure, or The “insurable value” of the structure. By FEMA’s

definition, “insurable value” is 100% Reproduction Cost New.

However, for farm/ranch buildings, it is the:a)Functional Building Cost Value – what appraisers

know as Replacement Cost New.b) Demolition/Removal Cost Value – use if building

would not be replaced in event of loss.

9

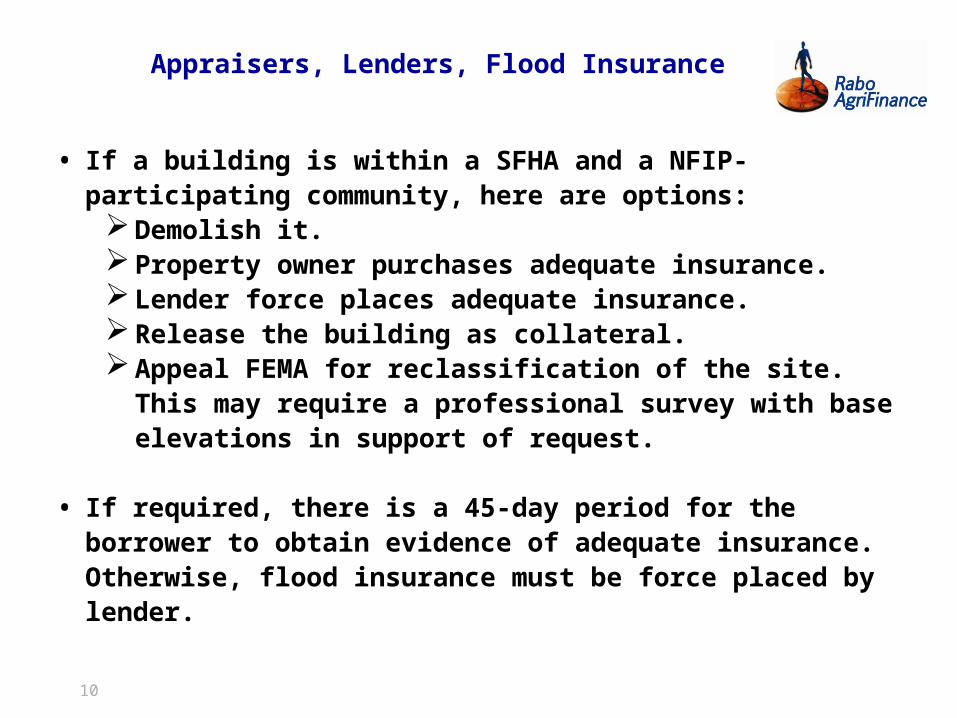

• If a building is within a SFHA and a NFIP- participating community, here are options:Demolish it.Property owner purchases adequate insurance.Lender force places adequate insurance.Release the building as collateral.Appeal FEMA for reclassification of the site. This

may require a professional survey with base elevations in support of request.

• If required, there is a 45-day period for the borrower to obtain evidence of adequate insurance. Otherwise, flood insurance must be force placed by lender.

10

Appraisers, Lenders, Flood Insurance

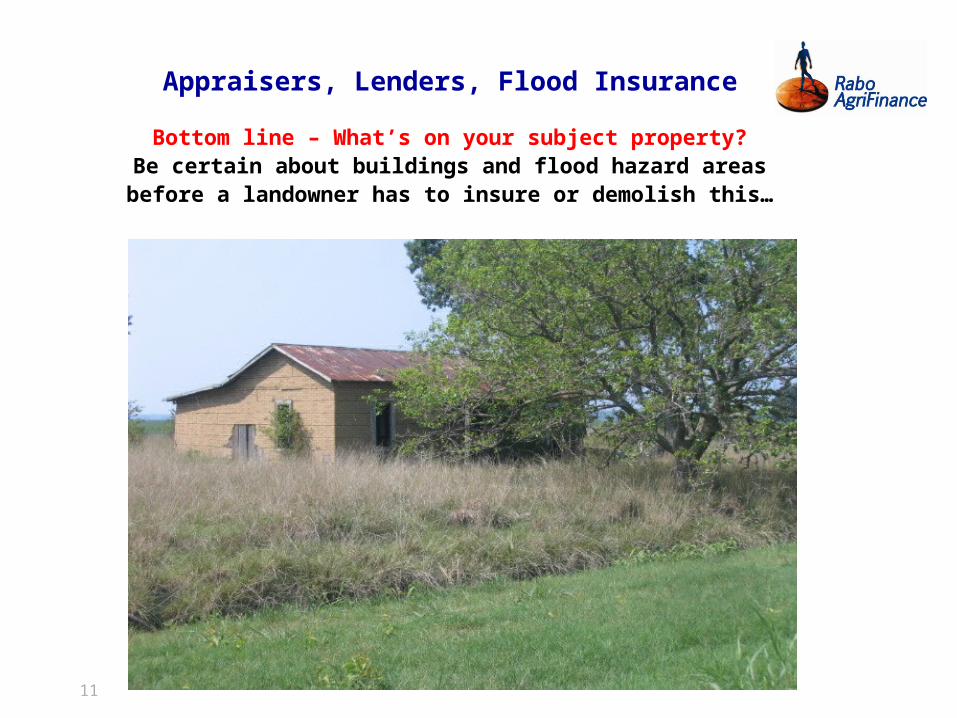

Bottom line – What’s on your subject property?Be certain about buildings and flood hazard areas

before a landowner has to insure or demolish this…

11

Appraisers, Lenders, Flood Insurance

QUESTIONS?

12