Embed Size (px)

Citation preview

1

Assessment Under Threat

Enid SlackInstitute on Municipal Finance and Governance

Presentation to the Association of Municipalities of Ontario

Niagara Falls, OntarioOctober 18, 2005

2

Outline of Presentation

Introduction: the characteristics of a good local tax: how does the property tax stack up?

Market value assessment under threat

An alternative to market value assessment – area based taxation

Addressing volatility under a market value system – examples from the U.S. and the U.K.

Concluding remarks: Addressing volatility in the Ontario system

3

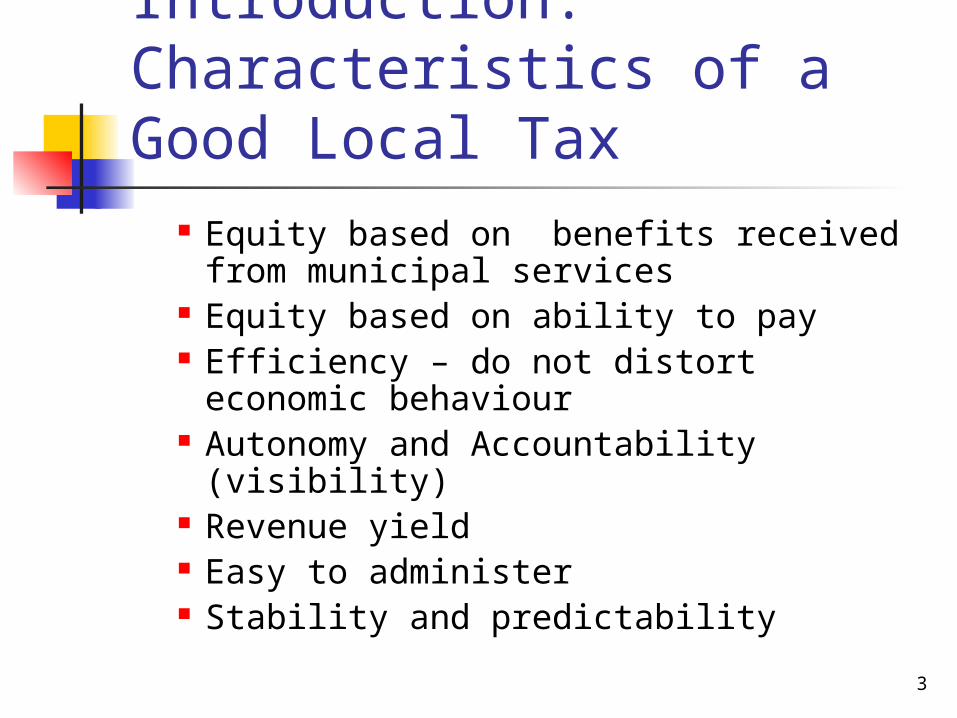

Introduction: Characteristics of a Good Local Tax

Equity based on benefits received from municipal services

Equity based on ability to pay Efficiency – do not distort economic

behaviour Autonomy and Accountability (visibility) Revenue yield Easy to administer Stability and predictability

4

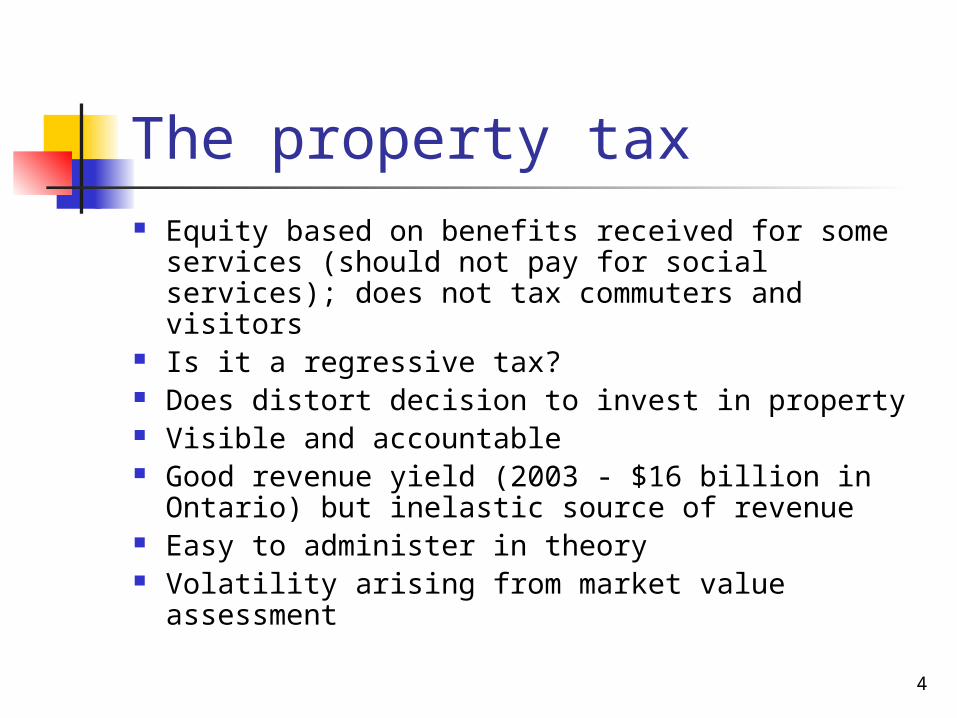

The property tax Equity based on benefits received for some

services (should not pay for social services); does not tax commuters and visitors

Is it a regressive tax? Does distort decision to invest in property Visible and accountable Good revenue yield (2003 - $16 billion in

Ontario) but inelastic source of revenue Easy to administer in theory Volatility arising from market value

assessment

5

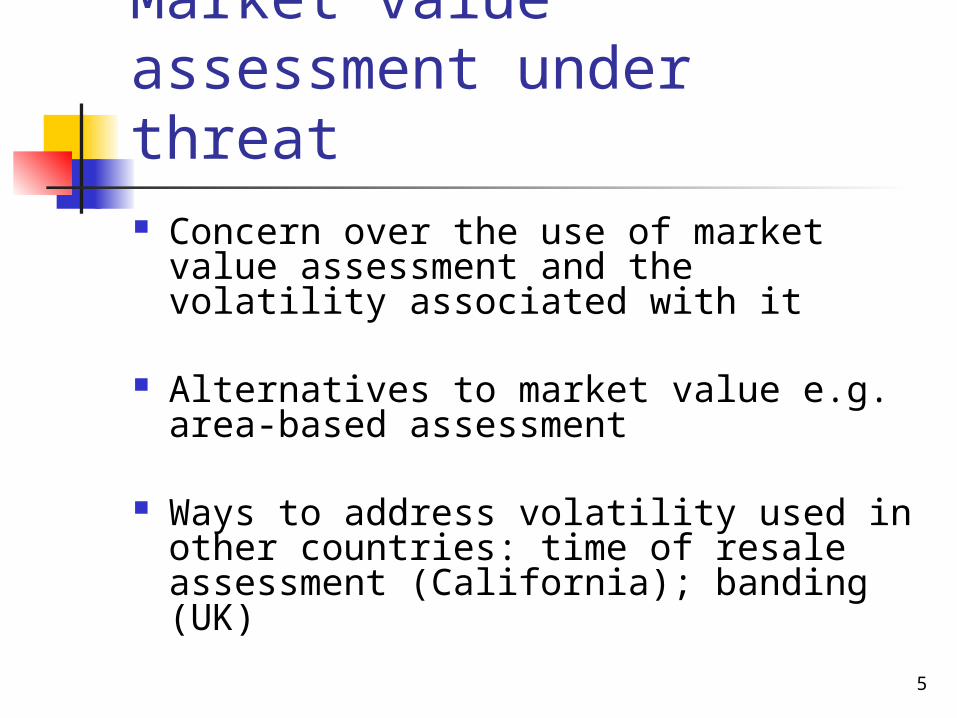

Market value assessment under threat Concern over the use of market value

assessment and the volatility associated with it

Alternatives to market value e.g. area-based assessment

Ways to address volatility used in other countries: time of resale assessment (California); banding (UK)

6

Alternative to market value assessment: area-based taxation

Under unit assessment, assessment is calculated as the sum of an assessment rate per square meter multiplied by the size of the land parcel and an assessment rate per square meter multiplied by the size of the building.

7

Alternative to market value assessment: area-based taxation

Under unit value assessment, the assessment rate per square meter is adjusted to reflect location (zone), quality of the structure (e.g. age, construction materials), or other factors.

Market value has an indirect influence on the assessment base through the application of adjustment factors.

8

Alternative to market value assessment: area-based taxation

Area-based assessments are commonly used in Central and Eastern Europe where the absence of developed property markets makes it difficult to determine market value.

They are also used in parts of Germany (in the former GDR), China, Chile, Israel, Kenya, and Tunisia.

9

Alternative to market value assessment: area-based taxation

Area-based taxes are less volatile than value-based taxes but also less equitable

Benefits from services are more closely reflected in property values than in the size of the property (e.g. properties close to transit systems or parks)

10

Alternative to market value assessment: area-based taxation

Area-based assessments (particularly unit assessment) are unlikely to capture neighbourhood amenities (amenities that have often been created by government expenditures and policies) because they do not take into account differences in the quality of buildings nor their location.

Two identical properties – one next to an abbatoir and one next to a park – pay same tax under area-based system

11

Alternative to market value assessment: area-based taxation

Area-based assessment results in a relatively greater burden on low-income taxpayers than high-income taxpayers when compared to value-based assessment. The reason is that average household incomes in high-value neighbourhoods are higher than in low-value neighbourhoods.

12

Alternative to market value assessment: area-based taxation

It has been argued that unit value assessment is easier to understand and cheaper to administer than value-based assessments

Difficult to use for the multi-residential rental, residential condominium, commercial, and industrial properties (e.g. how to allocate common areas)

13

Alternative to market value assessment: area-based taxation

In market economies, there is a tendency to a proliferation of multipliers applied to area base to reflect relative differences in values

The resulting complexity led to the abandonment of area-based taxation in the Netherlands, for example

14

Alternative to market value assessment: area-based taxation

Conclusion on area-based taxation:

Where it is possible to use market value, it is generally regarded as a better tax base

15

Addressing volatility: Proposition 13 in California Time of sale reassessment:

assessment increased by inflation or 2% per year (whichever is less) until property is sold

No reassessment if property transferred to children of owner

Stability and predictability of taxes

16

Addressing volatility: Proposition 13 in California Inequitable: unequal treatment of

properties of comparable value

Some owners pay 17 times as much in taxes as neighbours in comparable properties

Inequities can go on for generations: one young family buys a new home and pays market value taxes; another inherits a home and pays taxes on parents’ acquisition value

17

Addressing volatility: Proposition 13 in California Young first-time homeowners face higher taxes

because starter homes are reassessed more frequently

Proposition 13 favours older, more affluent generation over younger first-time homebuyers

Decreases household mobility

Favours existing businesses over new businesses

18

Addressing volatility: Proposition 13 in California Does not always reduce volatility –

when property values fell (1990s) and then rose, entire increase was allowed as long as it was below acquisition value

Later introduced provision to allow for reductions to be reflected in full

Still some properties whose values fell below acquisition value faced assessment increases greater than 2%

19

Addressing volatility: Proposition 13 in California Nordlinger v Hahn case went to U.S.

Supreme Court (1992) In an 8-1 decision, court upheld

acquisition value system New owner purchasing a property is

different than someone who is already saddled with purchase and does not have the option not to buy

Also upheld on grounds of neighbourhood preservation, continuity, and stability

20

Addressing volatility: Banding in the U.K. Applies to the council tax (residential property

tax) introduced in 1993 after community charge (poll tax) abolished

Individual valuations (market value) in 1991 used to assign each property into one of eight bands

Change in value does not affect banding (increase in value from expansion or improvement does not take effect until time of sale)

No revaluation since introduction in 1993

21

Addressing volatility: Banding in the U.K. Stability and predictability of taxes

Inequitable: same impact as out of date market value assessment

Revaluation would result in large tax shifts

Revaluation for 2007 (based on 2005 values) has been postponed, pending further review

22

Addressing volatility: assessment and property tax freezes

Breaks the link between taxes and market values:

Taxes less uniform and more arbitrary Properties with similar values pay different

taxes No incentive to review assessment “Once a freeze is imposed, the process of

thawing may be too painful to bear” (Joan Youngman, Lincoln Institute of Land Policy)

23

Addressing volatility: property tax freezes

Stability and predictability at the expense of equity

But, ignoring sound economics principles can result in an even less equitable tax in the long run and even greater taxpayer resistance

24

Addressing volatility in Ontario Accuracy in assessment is critical to a

market value assessment base Assessment increases cannot be used

as excuse for property tax increases Taxpayer (and media) education is

needed to understand the relationship between assessment and taxes

Taxpayers should be offered more payment options

25

Addressing volatility in Ontario Existing tools can be used to mitigate

impact of tax increases:

Property tax credits for low-income taxpayers

Tax deferrals for the elderly (to address cash-flow problem)

Phase-ins of tax increases Unduly burdensome provision under

Section 365 of the Municipal Act (for those facing undue hardship)

26

Concluding Comments

Market value may have its problems but the alternatives are worse