Embed Size (px)

Citation preview

11

Bond MathematicsBond Mathematics

22

OverviewOverview This chapter covers the fundamental ideas This chapter covers the fundamental ideas

behind fixed income risk and risk measurement. behind fixed income risk and risk measurement. Although it uses the Treasury market as the Although it uses the Treasury market as the mechanism for examining these ideas, they form mechanism for examining these ideas, they form the basis for all fixed income analysis.the basis for all fixed income analysis.

The specific topics covered include:The specific topics covered include: Pricing conventionsPricing conventions Yield to maturity, yield to call, yield to worst, current Yield to maturity, yield to call, yield to worst, current

yieldyield Duration and convexityDuration and convexity Hedging of interest rate riskHedging of interest rate risk Trading: spreads and butterflysTrading: spreads and butterflys

33

Pricing ConventionsPricing Conventions If you pick up the Wall Street Journal or some other If you pick up the Wall Street Journal or some other

source of Treasury Bond prices, the prices that you source of Treasury Bond prices, the prices that you find in there are the “quoted” prices (sometimes find in there are the “quoted” prices (sometimes called the “clean” or “flat” price.)called the “clean” or “flat” price.)

If you were to buy one of those bonds, you would If you were to buy one of those bonds, you would have to pay the quoted price have to pay the quoted price plusplus the accrued the accrued interest.interest.

Calculating the accrued interest is not particularly Calculating the accrued interest is not particularly difficult, just quirky.difficult, just quirky.

First, realize that Treasury Bonds/Notes pay ½ of First, realize that Treasury Bonds/Notes pay ½ of their stated coupon every six months. Thus an 8% their stated coupon every six months. Thus an 8% bond pays 4% of the principal amount ($1000) every bond pays 4% of the principal amount ($1000) every 6 months.6 months.

44

Pricing ConventionsPricing Conventions The convention in the market is that if the bond is sold The convention in the market is that if the bond is sold

between coupon payment dates, the accrued interest is between coupon payment dates, the accrued interest is calculated as equal to the percentage of the time between calculated as equal to the percentage of the time between coupon dates that the seller held the bond.coupon dates that the seller held the bond.

Thus, if you are two-thirds of the way through the coupon Thus, if you are two-thirds of the way through the coupon period, the accrued interest that would have to be paid period, the accrued interest that would have to be paid would be equal to two-thirds of the coupon payment that would be equal to two-thirds of the coupon payment that would be made at the next coupon date.would be made at the next coupon date.

This percentage is calculated on an “actual/actual” basis, This percentage is calculated on an “actual/actual” basis, meaning that you take the exact number of days since the meaning that you take the exact number of days since the last payment and divide it by the exact number of days last payment and divide it by the exact number of days between coupon payments.between coupon payments.

One effect of this is that since the number of days between One effect of this is that since the number of days between payments will vary (from 178 to 184) the payments will vary (from 178 to 184) the dailydaily interest interest accrual rate changes from period to period!accrual rate changes from period to period!

55

Pricing ConventionsPricing Conventions

Let LC stand for the last coupon payment date, Let LC stand for the last coupon payment date, let NC stand for the next coupon payment date, let NC stand for the next coupon payment date, and let T stand for today. C is the annual coupon and let T stand for today. C is the annual coupon on the bond.on the bond.

To calculate the accrued interest, simply do the To calculate the accrued interest, simply do the following:following:

LD T ND

LDND

LDT

*2

C* Face Int Acc.

66

Pricing ConventionsPricing Conventions So let’s say that we had an 8% bond, with a face So let’s say that we had an 8% bond, with a face

value of $1000, that pays interest on February 15 value of $1000, that pays interest on February 15 and August 15 of every year. If we purchase this and August 15 of every year. If we purchase this bond on January 22, how much accrued interest bond on January 22, how much accrued interest would we owe?would we owe?

There are 184 days between August 15 and There are 184 days between August 15 and February 15, and 160 days between August 15 February 15, and 160 days between August 15 and January 22.and January 22.

The accrued interest, therefore is:The accrued interest, therefore is:78.34$86956.*04.*1000

184

160*

2

.08 * 1000 interest Acc

77

Pricing ConventionsPricing Conventions Note, however, that since normally prices are Note, however, that since normally prices are

quoted as a percentage of face (par) value, the quoted as a percentage of face (par) value, the accrued interest will also be quoted that way.accrued interest will also be quoted that way.

This means that the 34.78 would be quoted as This means that the 34.78 would be quoted as 3.478 if prices were quoted in terms of par. Thus 3.478 if prices were quoted in terms of par. Thus if the bond were quoted as a price of 103.5, the if the bond were quoted as a price of 103.5, the accrued interest would be quoted as 3.478.accrued interest would be quoted as 3.478.

88

Pricing ConventionsPricing Conventions It is very common in debt markets to quote bonds It is very common in debt markets to quote bonds

in terms of yield instead of price. Since the two in terms of yield instead of price. Since the two are (generally) monotonic transformations of are (generally) monotonic transformations of each other, traders use whichever is convenient. each other, traders use whichever is convenient. Using yield avoids confusion in quotes because of Using yield avoids confusion in quotes because of differences in par amounts, etc.differences in par amounts, etc.

Yield for Treasury Bonds and Notes are the same Yield for Treasury Bonds and Notes are the same – they are “bond equivalent yields”, and are – they are “bond equivalent yields”, and are quoted under the assumption that interest is paid quoted under the assumption that interest is paid on a semi-annual basis.on a semi-annual basis.

The market quotes Treasury Bills differently. They The market quotes Treasury Bills differently. They are quoted on a “discount” basis.are quoted on a “discount” basis.

99

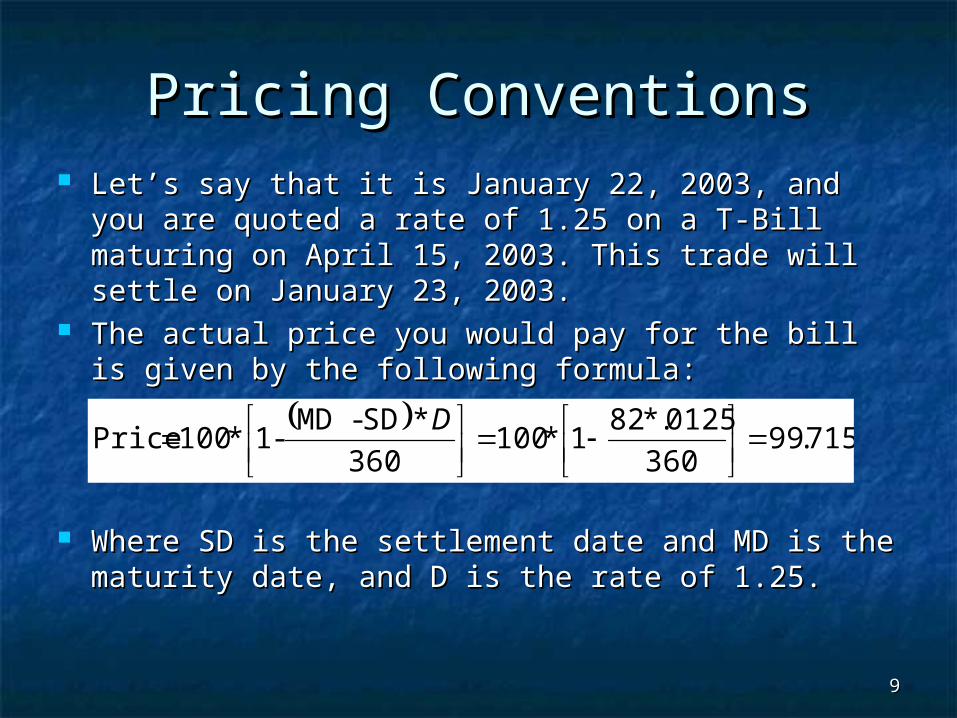

Pricing ConventionsPricing Conventions Let’s say that it is January 22, 2003, and you are Let’s say that it is January 22, 2003, and you are

quoted a rate of 1.25 on a T-Bill maturing on April quoted a rate of 1.25 on a T-Bill maturing on April 15, 2003. This trade will settle on January 23, 15, 2003. This trade will settle on January 23, 2003.2003.

The actual price you would pay for the bill is The actual price you would pay for the bill is given by the following formula:given by the following formula:

Where SD is the settlement date and MD is the Where SD is the settlement date and MD is the maturity date, and D is the rate of 1.25.maturity date, and D is the rate of 1.25.

715.99

360

0125.*821*100

360

*SD-MD-1 * 100 Price

D

1010

Pricing ConventionsPricing Conventions Notice that unlike the Treasury Bond, Treasury Bills Notice that unlike the Treasury Bond, Treasury Bills

pay interest on what is called the actual/360 basis. pay interest on what is called the actual/360 basis. Thus, if you held a Treasury for exactly 1 calendar Thus, if you held a Treasury for exactly 1 calendar year, you would earn slightly year, you would earn slightly moremore than the quoted than the quoted rate!rate!

Converting between the discount yield and the bond Converting between the discount yield and the bond equivalent yield is cumbersome, and depends on equivalent yield is cumbersome, and depends on how many days the bill has outstanding.how many days the bill has outstanding.

The book covers this in great detail, and you will The book covers this in great detail, and you will implement this as part of the first project set.implement this as part of the first project set.

1111

Yield ConventionsYield Conventions Treasury Bonds and notes are quoted on a Treasury Bonds and notes are quoted on a Yield Yield

to Maturityto Maturity convention, and Treasury Bills are convention, and Treasury Bills are based on a based on a discount rate discount rate convention.convention.

Bonds that have a callable feature will be quoted Bonds that have a callable feature will be quoted on a on a yield to callyield to call basis – meaning assume the basis – meaning assume the bond is called on its call date and solve for yield.bond is called on its call date and solve for yield.

Callable bonds can also be quoted on a Callable bonds can also be quoted on a yield to yield to worstworst basis, meaning solve for yield to maturity basis, meaning solve for yield to maturity and yield to each call date (there may be more and yield to each call date (there may be more than one), and assume you will get the lowest of than one), and assume you will get the lowest of all of those yields.all of those yields.

1212

Yield ConventionsYield Conventions Recall that the yield curve is just a plot of each Recall that the yield curve is just a plot of each

bond’s yield against its maturity date for a given bond’s yield against its maturity date for a given set of bonds.set of bonds.

The following are the yield curves for January 13, The following are the yield curves for January 13, 2003, and July 21, 2003.2003, and July 21, 2003.

The Federal Reserve releases interest rate data The Federal Reserve releases interest rate data daily on their web site at daily on their web site at http://www.federalreserve.gov/releases/h15/updahttp://www.federalreserve.gov/releases/h15/update/te/

They also have historical data available there. They also have historical data available there. You will need this site to collect data for some of You will need this site to collect data for some of the projects.the projects.

1313

Yield CurvesYield CurvesYield Curves of January 13, 2002 and July 21, 2003.

0

1

2

3

4

5

6

0 100 200 300 400

Months

Yie

ld

13-Jan 21-Jul Difference

1414

Measuring Risk in Fixed Measuring Risk in Fixed IncomeIncome

The most basic risk in fixed income is The most basic risk in fixed income is price riskprice risk. . That is, that they price of the asset will change That is, that they price of the asset will change because of a change in interest rates.because of a change in interest rates.

Normally, yields and prices are inversely related.Normally, yields and prices are inversely related. The primary methods that finance people use to The primary methods that finance people use to

measure price risk is a concept known as measure price risk is a concept known as durationduration, and its related concept of , and its related concept of convexity.convexity.

In the next slides we will examine these concepts.In the next slides we will examine these concepts.

1515

DurationDuration Duration is a measure of how much the price of a Duration is a measure of how much the price of a

bond or other fixed-income asset will change when bond or other fixed-income asset will change when the discount rate changes.the discount rate changes.

What duration measures is the What duration measures is the instantaneous instantaneous rate of changerate of change in price with respect to yield (i.e. in price with respect to yield (i.e. the discount rate.)the discount rate.)

In other words, what we want to measure is the In other words, what we want to measure is the rate at which the bond price changes when yield rate at which the bond price changes when yield changes.changes.

This means we want to know the slope of the price This means we want to know the slope of the price curve.curve.

Note that technically, the price of a bond is a Note that technically, the price of a bond is a mathematical mathematical functionfunction of interest rates. of interest rates.

1616

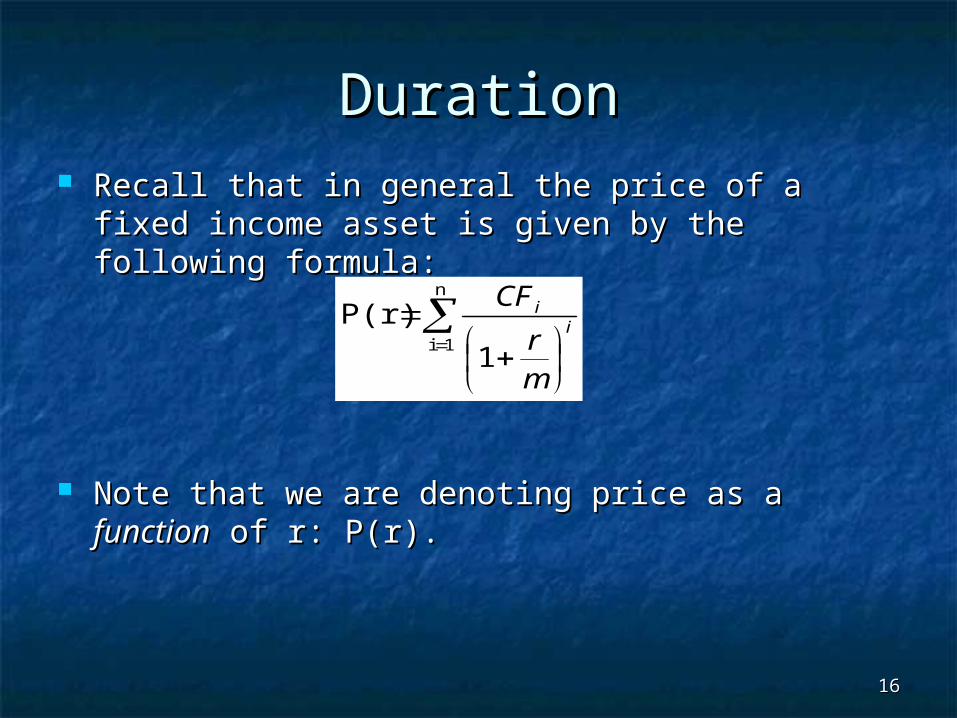

DurationDuration Recall that in general the price of a fixed income Recall that in general the price of a fixed income

asset is given by the following formula:asset is given by the following formula:

Note that we are denoting price as a Note that we are denoting price as a functionfunction of r: of r: P(r).P(r).

n

1i1

P(r) ii

mr

CF

1717

DurationDuration For our purposes, it perhaps more convenient to For our purposes, it perhaps more convenient to

write this as a product instead of as a quotient.write this as a product instead of as a quotient.

A couple of rules from differential calculus are A couple of rules from differential calculus are also useful to remember:also useful to remember:

N

i

i

i m

rcfPV

1

1*

1818

DurationDuration First, the derivative of a sum is equal to the sum First, the derivative of a sum is equal to the sum

of the derivatives. This means that we can treat of the derivatives. This means that we can treat each term of our summation independently.each term of our summation independently.

Second, when dealing with an equation of the Second, when dealing with an equation of the form:form:

)('*)(**)('

:bygiven is derivative itsthen

)( * )(

1 xgxgazxf

xgaxf

z

z

1919

DurationDuration In this context, g(x) is (1+r/m). So that means In this context, g(x) is (1+r/m). So that means

our derivative will be:our derivative will be:

Notice that the 1/m term come from the fact Notice that the 1/m term come from the fact that we have to take the derivative of (1+r/m), that we have to take the derivative of (1+r/m), which is simply 1/m.which is simply 1/m.

N

i

i

i

N

i

i

i

mm

rcfi

dr

dPV

m

rcfPV

1

1

1

1*1**

then

1*

Given

2020

DurationDuration Reassembling this into a perhaps more Reassembling this into a perhaps more

conventional form:conventional form:

N

iii

N

iii

mr

cfi

mdr

dPV

m

mr

cfi

dr

dPV

11

11

1

*1

so

1

*

1

*

2121

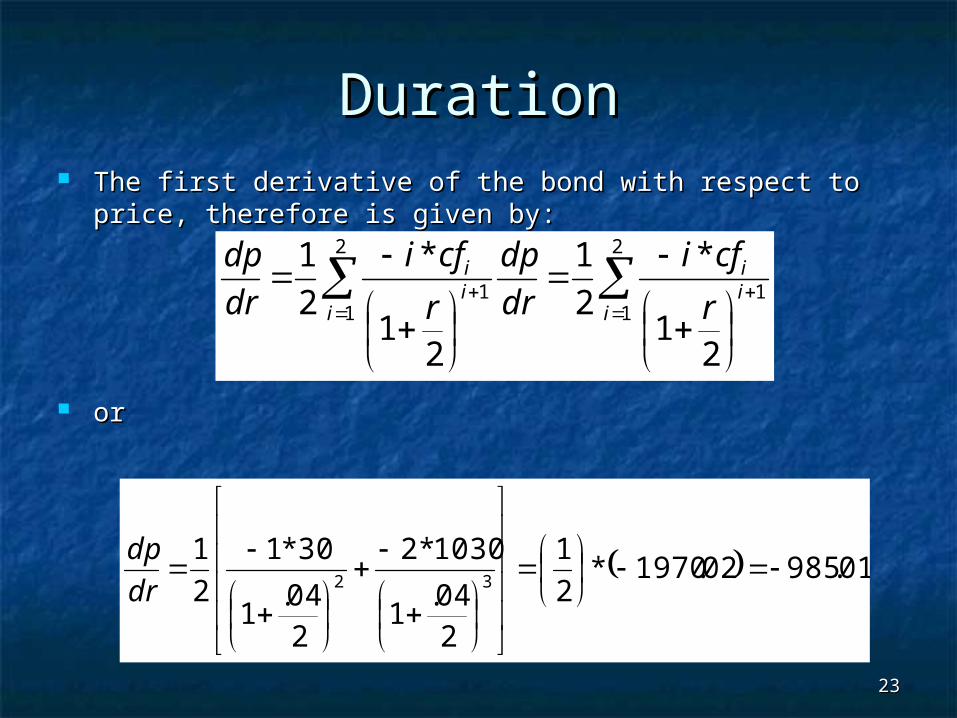

DurationDuration Thus, the first derivative of price with respect to r Thus, the first derivative of price with respect to r

is: is:

The first derivative tells us the instantaneous rate The first derivative tells us the instantaneous rate at which P is changing – that is, it is the rate at at which P is changing – that is, it is the rate at which P is changing given a specific value of r.which P is changing given a specific value of r.

The derivative of a specific bond calculated at two The derivative of a specific bond calculated at two different values of r will be different.different values of r will be different.

Let’s work a couple of examples to see exactly how Let’s work a couple of examples to see exactly how this is calculated.this is calculated.

n

1i1

m

1*

1

*

dr

dPii

mr

CFi

2222

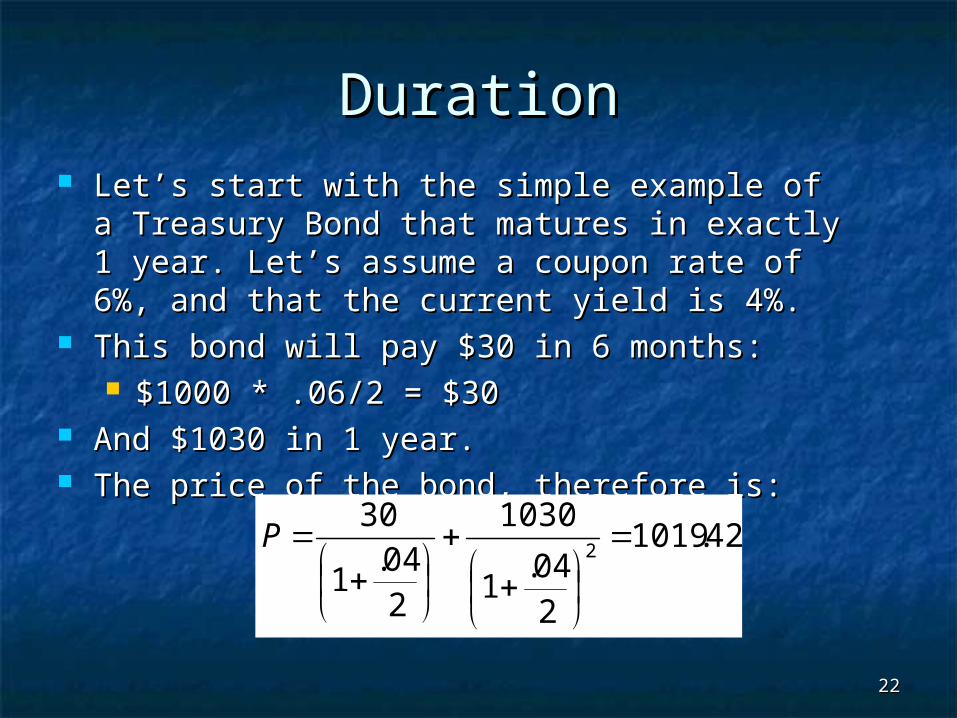

DurationDuration Let’s start with the simple example of a Let’s start with the simple example of a

Treasury Bond that matures in exactly 1 year. Treasury Bond that matures in exactly 1 year. Let’s assume a coupon rate of 6%, and that Let’s assume a coupon rate of 6%, and that the current yield is 4%.the current yield is 4%.

This bond will pay $30 in 6 months:This bond will pay $30 in 6 months: $1000 * .06/2 = $30$1000 * .06/2 = $30

And $1030 in 1 year.And $1030 in 1 year. The price of the bond, therefore is:The price of the bond, therefore is:

42.1019

204.

1

1030

204.

1

302

P

2323

DurationDuration The first derivative of the bond with respect to price, The first derivative of the bond with respect to price,

therefore is given by:therefore is given by:

oror

2

11

2

11

21

*

2

1

21

*

2

1

iii

iii

r

cfi

dr

dp

r

cfi

dr

dp

01.98502.1970*2

1

204.

1

1030*2

204.

1

30*1

2

132

dr

dp

2424

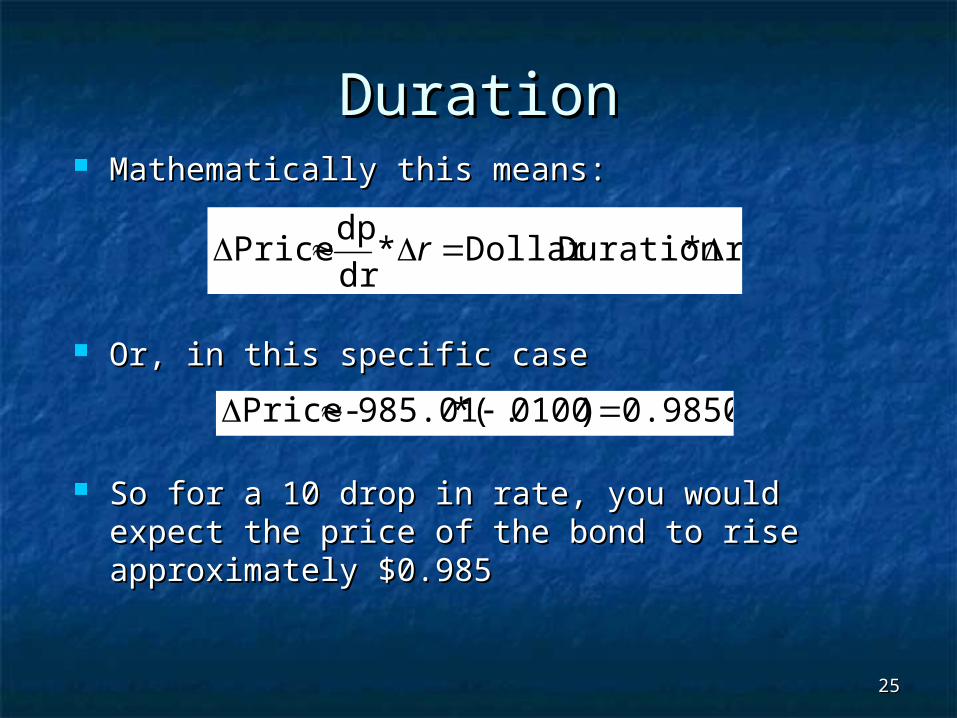

DurationDuration The first derivative of price with respect to r is The first derivative of price with respect to r is

frequently referred to in Finance as “frequently referred to in Finance as “dollar dollar durationduration”. ”.

By convention the negative sign is usually omitted, By convention the negative sign is usually omitted, so that dollar duration is quoted as a positive so that dollar duration is quoted as a positive number.number.

The reason that it is referred to as “dollar duration” The reason that it is referred to as “dollar duration” is that you can use it to predict the dollar change in is that you can use it to predict the dollar change in price for a given change in interest rate.price for a given change in interest rate.

To do this, you simply multiply the dollar duration by To do this, you simply multiply the dollar duration by the change in rate (but you must keep in mind the the change in rate (but you must keep in mind the sign of the change and dollar duration!).sign of the change and dollar duration!).

2525

DurationDuration Mathematically this means:Mathematically this means:

Or, in this specific caseOr, in this specific case

So for a 10 drop in rate, you would expect the So for a 10 drop in rate, you would expect the price of the bond to rise approximately $0.985price of the bond to rise approximately $0.985

r *Duration Dollar *dr

dp Price r

0.98501 )0100.(*985.01- Price

2626

DurationDuration In reality if rates fell from 4% to 3.9%, the In reality if rates fell from 4% to 3.9%, the

bond’s price will rise from 1019.41 to bond’s price will rise from 1019.41 to 1020.40, a change of .98573.1020.40, a change of .98573.

The reason that this is not exact, of course, is The reason that this is not exact, of course, is because duration uses a because duration uses a linearlinear approximation approximation to the curved price function – we make a to the curved price function – we make a tradeoff between ease of calculation and tradeoff between ease of calculation and accuracy.accuracy.

40.1020

2039.

1

1030

2039.

1

302

P

2727

DurationDuration To demonstrate this, let us use another example, To demonstrate this, let us use another example,

one using a longer-maturing treasury bond.one using a longer-maturing treasury bond.

In particular let us use a 30 year Treasury bond In particular let us use a 30 year Treasury bond with a coupon of 8%. with a coupon of 8%.

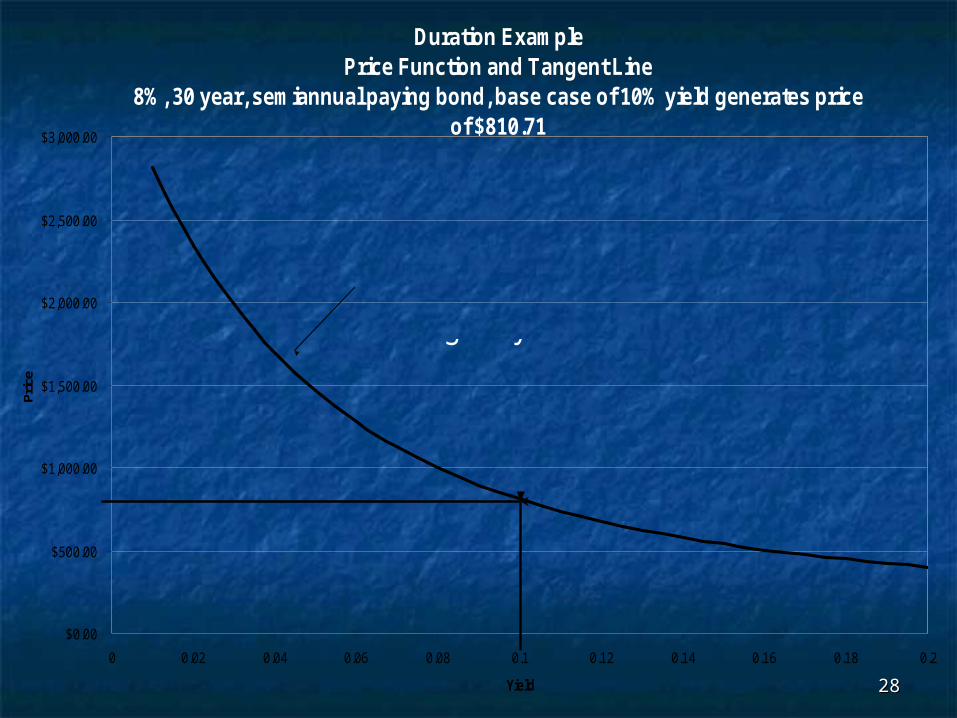

If the yield on this bond is 8%, then the bond is If the yield on this bond is 8%, then the bond is worth $1000, but at 10% it is worth $810.71.worth $1000, but at 10% it is worth $810.71.

The following graph shows the price for all The following graph shows the price for all interest rates between 1% and 20%.interest rates between 1% and 20%.

2828

Duration ExamplePrice Function and Tangent Line

8%, 30 year, semiannual paying bond, base case of 10% yield generates price of $810.71

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2

Yield

Pric

e

Price Function [P(r)]Actual change in price given a change in yield

$ 810.71

2929

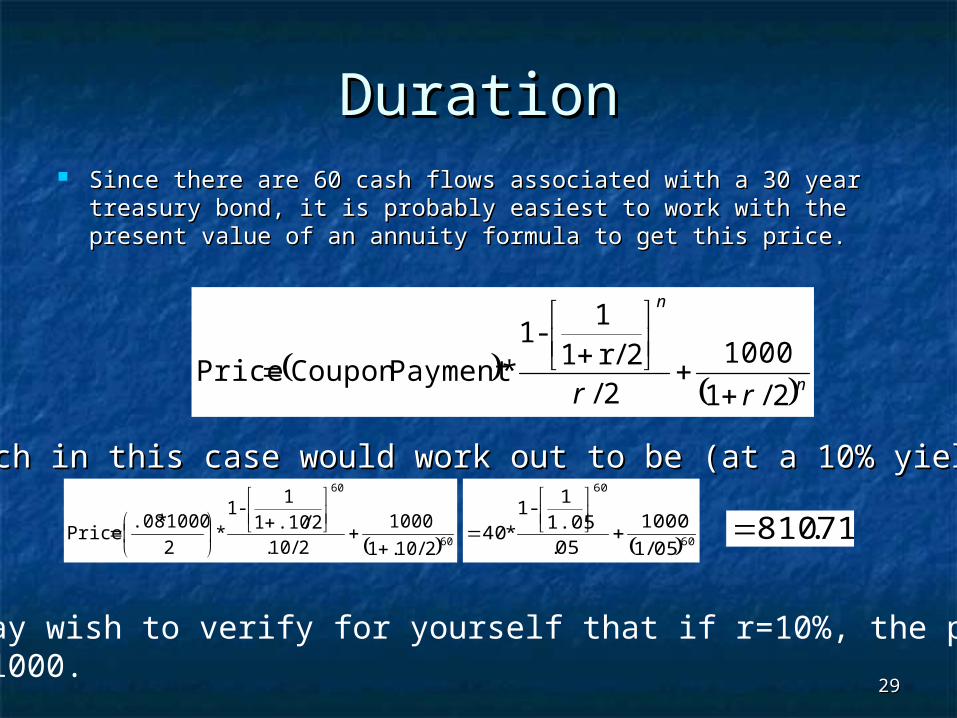

DurationDuration Since there are 60 cash flows associated with a 30 year Since there are 60 cash flows associated with a 30 year

treasury bond, it is probably easiest to work with the treasury bond, it is probably easiest to work with the present value of an annuity formula to get this price.present value of an annuity formula to get this price.

n

n

rr 2/1

1000

2/2/r1

1-1

*PaymentCoupon Price

60

60

2/10.1

1000

2/10.2/.101

1-1

*2

1000*.08 Price

60

60

05/1

1000

05.1.05

1-1

*40

71.810

Which in this case would work out to be (at a 10% yield):Which in this case would work out to be (at a 10% yield):

You may wish to verify for yourself that if r=10%, the price is $1000.

3030

DurationDuration We could use the same formula for the derivative We could use the same formula for the derivative

that we did in the original equation, but, with 60 that we did in the original equation, but, with 60 cash flows, it is cumbersome to do so. cash flows, it is cumbersome to do so.

Instead we can use a variation of that formula Instead we can use a variation of that formula that is based on the present value of annuity that is based on the present value of annuity formula we just used. That formula is:formula we just used. That formula is:

mmr

n

mr

mr

mm

mrm

nr

pmtdr

dpn

nn

1*

/1

1000*1

11

1

1*

* 2

12

3131

DurationDuration So, at 10%, the first derivative of the bond with So, at 10%, the first derivative of the bond with

respect to yield would be given by:respect to yield would be given by:

Or:Or:

2

1*

2/1.1

1000*60

21.

210.

12

121

21.

1

12

60*1.

*40 612

601602

dr

dp

627.787758.15297011.158*40

58.15290025.0

0267677.021

)05098.0(5.1*40

dr

dp

dr

dp

3232

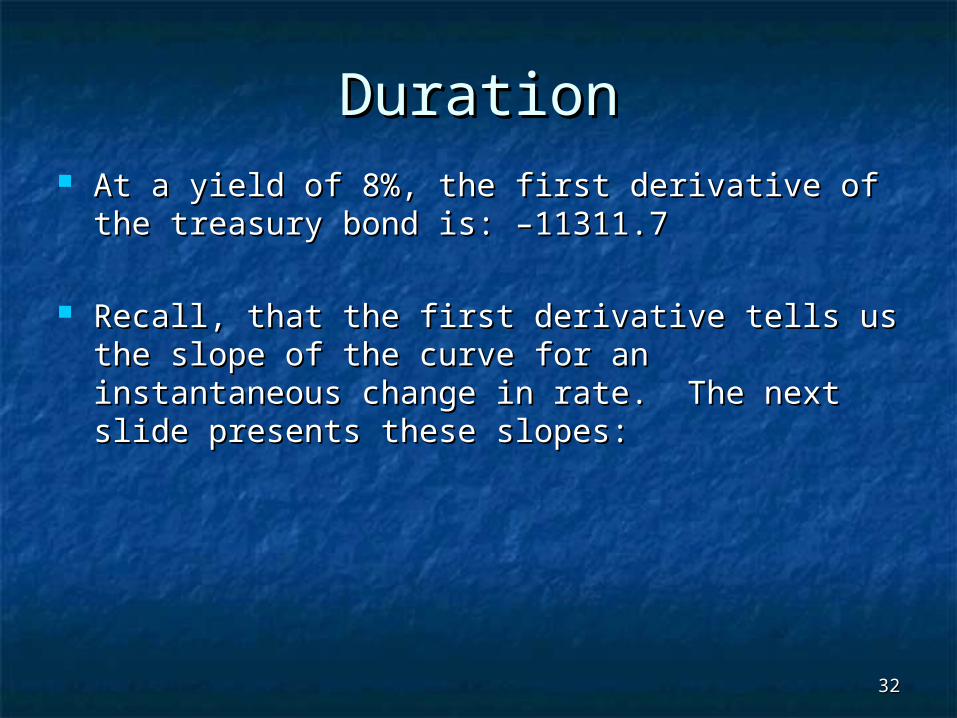

DurationDuration At a yield of 8%, the first derivative of the At a yield of 8%, the first derivative of the

treasury bond is: –11311.7 treasury bond is: –11311.7

Recall, that the first derivative tells us the slope Recall, that the first derivative tells us the slope of the curve for an instantaneous change in rate. of the curve for an instantaneous change in rate. The next slide presents these slopes:The next slide presents these slopes:

3333

First deriviative when r=10% and r=8%.

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2 0.22

Yield

Pric

e

Slope when r=10%

Slope when r=8%

Price Function

3434

DurationDuration From the graph we can see that as the interest From the graph we can see that as the interest

rate increases, the curve becomes less steep – rate increases, the curve becomes less steep – indicating that as price of the bond is indicating that as price of the bond is less less sensitivesensitive to interest rate changes. to interest rate changes.

By looking at the graph you can see that the rate By looking at the graph you can see that the rate at which price changes in not constant. at which price changes in not constant.

What we want to do is develop a measure of the What we want to do is develop a measure of the rate of change given a specific yield.rate of change given a specific yield.

Dollar duration provides this measure, but it does Dollar duration provides this measure, but it does have some drawbacks.have some drawbacks.

3535

DurationDuration One drawback in particular is that it is difficult to One drawback in particular is that it is difficult to

compare the relative risk of two bonds that have compare the relative risk of two bonds that have different face amounts. different face amounts.

A bond with a $5000 face amount will have a A bond with a $5000 face amount will have a derivative that is 5 times larger than one with a derivative that is 5 times larger than one with a $1000 face amount.$1000 face amount.

It would be nice if we could have a somewhat It would be nice if we could have a somewhat more standardized way of measuring the risk.more standardized way of measuring the risk.

3636

DurationDuration There are several other variants of duration There are several other variants of duration

other than dollar duration. They include:other than dollar duration. They include: DV01DV01 Modified DurationModified Duration Macaulay’s durationMacaulay’s duration

Usually finance textbooks will provide you with Usually finance textbooks will provide you with either Modified or Macaulay’s duration (which either Modified or Macaulay’s duration (which is why the number so far may have seemed a is why the number so far may have seemed a little odd-looking to those of you that have little odd-looking to those of you that have seen duration in other courses.)seen duration in other courses.)

Let us examine each of these in detail.Let us examine each of these in detail.

3737

DurationDurationDV01DV01 Since dollar duration numbers tend to Since dollar duration numbers tend to

be large in absolute terms, it is more be large in absolute terms, it is more convenient to scale them. One way of convenient to scale them. One way of scaling them is to multiply them by a scaling them is to multiply them by a small yield amount. One choice is to small yield amount. One choice is to use 1 basis point. This will tell you the use 1 basis point. This will tell you the approximate change in an instrument’s approximate change in an instrument’s price for a 1 basis point change in yield.price for a 1 basis point change in yield.

3838

DurationDurationDV01DV01 This measure is known as the Dollar Value of an This measure is known as the Dollar Value of an

01 – or simply as DV01.01 – or simply as DV01. It is used primarily to compare the magnitude of It is used primarily to compare the magnitude of

dollar changes across assets.dollar changes across assets. Unfortunately, it does not take into account the Unfortunately, it does not take into account the

scale of the underlying asset. That is, an asset scale of the underlying asset. That is, an asset with a face amount of $100,000 would have a with a face amount of $100,000 would have a DV01 100 times greater than an identical asset DV01 100 times greater than an identical asset with face amount of $100,000.with face amount of $100,000.

3939

DurationDurationDV01DV01 In the example presented earlier the DV01 for In the example presented earlier the DV01 for

the bond would be:the bond would be: DV01 = (dp/dr) * .0001 =DV01 = (dp/dr) * .0001 =

-7877.63* -.0001 = $.07877-7877.63* -.0001 = $.07877 Note that this is expressed in Dollars.Note that this is expressed in Dollars.

4040

DurationDurationModified DurationModified Duration Modified duration is a way of taking into Modified duration is a way of taking into

account the scale of the asset being measured.account the scale of the asset being measured.

Essentially it is dollar duration divided by price.Essentially it is dollar duration divided by price. When a trader – or most data sources – refer to When a trader – or most data sources – refer to

“duration” they normally mean modified “duration” they normally mean modified duration.duration.

This is also the variant of duration that can be This is also the variant of duration that can be viewed as a true “time measure”viewed as a true “time measure”

p

1*

dr

dp Duration Modified

4141

DurationDurationModified DurationModified Duration If you multiply modified duration by a change If you multiply modified duration by a change

in interest rates, it gives you the approximate in interest rates, it gives you the approximate percentagepercentage change in price for the asset. change in price for the asset.

Using modified duration to measure the Using modified duration to measure the interest rate risk in an asset lets one avoid the interest rate risk in an asset lets one avoid the scaling difficulty of the DV01 measure. scaling difficulty of the DV01 measure.

In our previous example, modified duration In our previous example, modified duration would be:would be:

Mod. Duration = dp/dr * 1/pMod. Duration = dp/dr * 1/p = = 7877.63* 1/810.71 = 9.7169.7877.63* 1/810.71 = 9.7169.

Remember that, in general, the larger the Remember that, in general, the larger the duration number, the greater the interest rate duration number, the greater the interest rate risk.risk.

4242

DurationDurationMacualay’s DurationMacualay’s Duration The first derivation of duration was made in the The first derivation of duration was made in the

1930’s by an economist named Macaulay. He 1930’s by an economist named Macaulay. He was not thinking of it as a risk measure was not thinking of it as a risk measure per seper se, , but rather as the price elasticity of a bond with but rather as the price elasticity of a bond with respect to interest rates. As such his measure respect to interest rates. As such his measure is given by:is given by:

One interesting fact is that for any bond with One interesting fact is that for any bond with only one cash flow the Macaulay’s duration of only one cash flow the Macaulay’s duration of that bond will exactly equal its maturity!that bond will exactly equal its maturity!

P

mr )/1(*

dr

dp Duration sMacaulay'

4343

DurationDuration So there are actually at least four measures of So there are actually at least four measures of

duration:duration: Dollar Duration: (dp/dr)Dollar Duration: (dp/dr) DV01: (dp/dr * .0001)DV01: (dp/dr * .0001) Modified Duration: (dp/dr * 1/p)Modified Duration: (dp/dr * 1/p) Macaulay’s Duration (dp/dr * (1+r/m)/p).Macaulay’s Duration (dp/dr * (1+r/m)/p).

Note that many books refer to duration as a Note that many books refer to duration as a time measure. It is possible to construe it that time measure. It is possible to construe it that way, but I think it is much more useful to think way, but I think it is much more useful to think of it as a rate of change.of it as a rate of change.

Also, recall that it is really a Also, recall that it is really a negativenegative number number (in most cases), it is just the convention in (in most cases), it is just the convention in finance that we omit the negative sign.finance that we omit the negative sign.

4444

DurationDurationComplications with Duration:Complications with Duration: The example we have worked with so far considers The example we have worked with so far considers

a case where the cash flows from the bond are a case where the cash flows from the bond are certain. What if they are not? certain. What if they are not?

If the cash flows do not vary with interest rates, then If the cash flows do not vary with interest rates, then you would calculate duration as normal – just realize you would calculate duration as normal – just realize there may be risks which duration is not capturing. there may be risks which duration is not capturing.

For example, some companies issue bonds that For example, some companies issue bonds that have contract rates which depend upon the price of have contract rates which depend upon the price of some factor of production – some ski resorts have some factor of production – some ski resorts have issued bonds where the interest rate is a function of issued bonds where the interest rate is a function of the amount of snow they get.the amount of snow they get.

You can still calculate duration as normal – just You can still calculate duration as normal – just realize that interest rate risk is not the only risk in realize that interest rate risk is not the only risk in the bond.the bond.

4545

DurationDurationComplications with Duration:Complications with Duration: Of course some assets, like mortgages, have cash Of course some assets, like mortgages, have cash

flows that do vary with interest rates.flows that do vary with interest rates. This means that the simple derivative formula This means that the simple derivative formula

does not work – cash flow itself must be treated as does not work – cash flow itself must be treated as a function of r, and so one must, at a minimum, a function of r, and so one must, at a minimum, use the chain rule to extend the derivative.use the chain rule to extend the derivative.

Frankly, this is not commonly done. The reason is Frankly, this is not commonly done. The reason is that most good prepayment models are so that most good prepayment models are so complex that they do not have easily computed complex that they do not have easily computed derivatives. derivatives.

Analysts can do one of two things, therefore. They Analysts can do one of two things, therefore. They can either:can either:

Ignore that cash flows are a function of r:Ignore that cash flows are a function of r: Approximate durationApproximate duration

4646

DurationDurationComplications with Duration:Complications with Duration: Both ways are fairly common, although if you ignore Both ways are fairly common, although if you ignore

the fact that cash flow is a function of interest rates, the fact that cash flow is a function of interest rates, you will misstate duration. If you feel the you will misstate duration. If you feel the misstatement is small enough, you may choose to do misstatement is small enough, you may choose to do this.this.

You approximate duration by approximating the You approximate duration by approximating the derivative. To do this you calculate the price of the derivative. To do this you calculate the price of the asset at two points on either side of the current rate:asset at two points on either side of the current rate:

For example, if the discount rate were at 10%, you For example, if the discount rate were at 10%, you would determine the price at 9.9% and 10.10%, and would determine the price at 9.9% and 10.10%, and then divided the difference in prices by the 20 basis then divided the difference in prices by the 20 basis point difference in yield. This approximates the point difference in yield. This approximates the slope and hence the derivative.slope and hence the derivative.

Example: in our previous example, the price of the bond at Example: in our previous example, the price of the bond at 9.9% is $818.65 and at 10.10% is 802.90.9.9% is $818.65 and at 10.10% is 802.90.

4747

DurationDurationComplications with Duration:Complications with Duration: We can approximate duration as follows:We can approximate duration as follows:

Clearly this yields an approximate duration Clearly this yields an approximate duration which is very close to the true duration.which is very close to the true duration.

This numerical approximation for duration is This numerical approximation for duration is commonly used in financial modeling and commonly used in financial modeling and financial modeling software packages.financial modeling software packages.

880,70020.

65.81889.802

0990.1010.

PricePrice Duration 9.910.10

4848

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

Fundamentally duration is an application of Fundamentally duration is an application of Taylor’s Theorem from mathematics. Taylor’s Taylor’s Theorem from mathematics. Taylor’s theorem says simply that if you know the theorem says simply that if you know the value of a function and all of its derivatives at value of a function and all of its derivatives at a given point (x), then you can calculate its a given point (x), then you can calculate its value at any other point (x+h). The exact value at any other point (x+h). The exact formula is formula is

!

)(...

!3

)('''

!2

)('')(')()( 32

n

xfh

xfh

xfhxhfxfhxf

nn

4949

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

What we do when we use duration is we What we do when we use duration is we simply use the first two terms of this formula simply use the first two terms of this formula and drop the rest (although we frequently will and drop the rest (although we frequently will add the second term – it is called add the second term – it is called convexityconvexity).).

That is, for a bond price (r), we use:That is, for a bond price (r), we use:

dr

dpdrrpdrrp )()(

5050

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

What this says is that if we have an asset with a What this says is that if we have an asset with a known price at a given interest rate, (p(r)), then if known price at a given interest rate, (p(r)), then if we change r by dr, the price at that new rate we change r by dr, the price at that new rate p(r+dr), will be approximately equal to the old p(r+dr), will be approximately equal to the old price plus the change in rate times the first price plus the change in rate times the first derivative of the pricing function (which we call derivative of the pricing function (which we call dollar duration!).dollar duration!).

The reason our value is not an exact match is The reason our value is not an exact match is because we drop those higher order terms.because we drop those higher order terms.

This can be extremely useful if are told the price of This can be extremely useful if are told the price of the bond and want to determine its yield. the bond and want to determine its yield.

5151

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

To see this, consider the first bond that we used in To see this, consider the first bond that we used in this section.this section.

Recall that that bond had a coupon rate of 6%. It Recall that that bond had a coupon rate of 6%. It had a yield of 4%, and thus had a price of 1019.41.had a yield of 4%, and thus had a price of 1019.41.

Now, instead let’s say that you were simply told that Now, instead let’s say that you were simply told that the price of the bond were 1005.00, and were asked the price of the bond were 1005.00, and were asked to find its yield, which we will denote as Y. How to find its yield, which we will denote as Y. How could you do this?could you do this?

One approach would be to use Taylor’s Theorem.One approach would be to use Taylor’s Theorem. We begin by simply guessing a yield, say 5%, and We begin by simply guessing a yield, say 5%, and

then determining the price of the bond at a yield of then determining the price of the bond at a yield of 5%:5%:

5252

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

The price if the is 5% is:The price if the is 5% is:

and the first derivative of price at a yield of 5% and the first derivative of price at a yield of 5% is:is:

63.1009025.1

1030

1.025

30 Price

2

73.9702

1*

025.1

1030*2

1.025

30*1-

dy

dp32

5353

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

Recall that Taylor’s theorem says that the value Recall that Taylor’s theorem says that the value of a function at a point x (i.e. f(x+h)) is given by:of a function at a point x (i.e. f(x+h)) is given by:

or, ignoring the higher order terms by:or, ignoring the higher order terms by:

Realize that we know the price of the bond at Realize that we know the price of the bond at 5% and we know its derivative at 5%, we also 5% and we know its derivative at 5%, we also know that when we find the current yield of the know that when we find the current yield of the bond, its price will be 1005 (we were given bond, its price will be 1005 (we were given that!).that!).

!

)(...

!3

)('''

!2

)('')(')()( 32

n

xfh

xfh

xfhxhfxfhxf

nn

)(')()( xhfxfhxf

5454

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

We can think of the price when the yield is 5% as We can think of the price when the yield is 5% as being f(x), the derivative of the price when the being f(x), the derivative of the price when the yield is 5% as being f’(x), and the price of the yield is 5% as being f’(x), and the price of the bond at the (still unknown) correct yield as being bond at the (still unknown) correct yield as being f(x+h) (h is the difference between the correct f(x+h) (h is the difference between the correct yield Y and our guessed yield of 5%.) Thus,yield Y and our guessed yield of 5%.) Thus, f(x) = 1009.63f(x) = 1009.63 f’(x) = -970.73f’(x) = -970.73 f(x+h) = 1005.00f(x+h) = 1005.00

If we insert these into Taylor’s equation, we get If we insert these into Taylor’s equation, we get the following:the following:

5555

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

Recall the formula:Recall the formula:

So we get:So we get:

We can then solve for h, the difference between We can then solve for h, the difference between 5% and the yield which will set the price of the 5% and the yield which will set the price of the bond to 1005:bond to 1005:

)(')()( xhfxfhxf

73.970*63.10091005 h

004771081.

43.970

63.10091005

h

5656

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

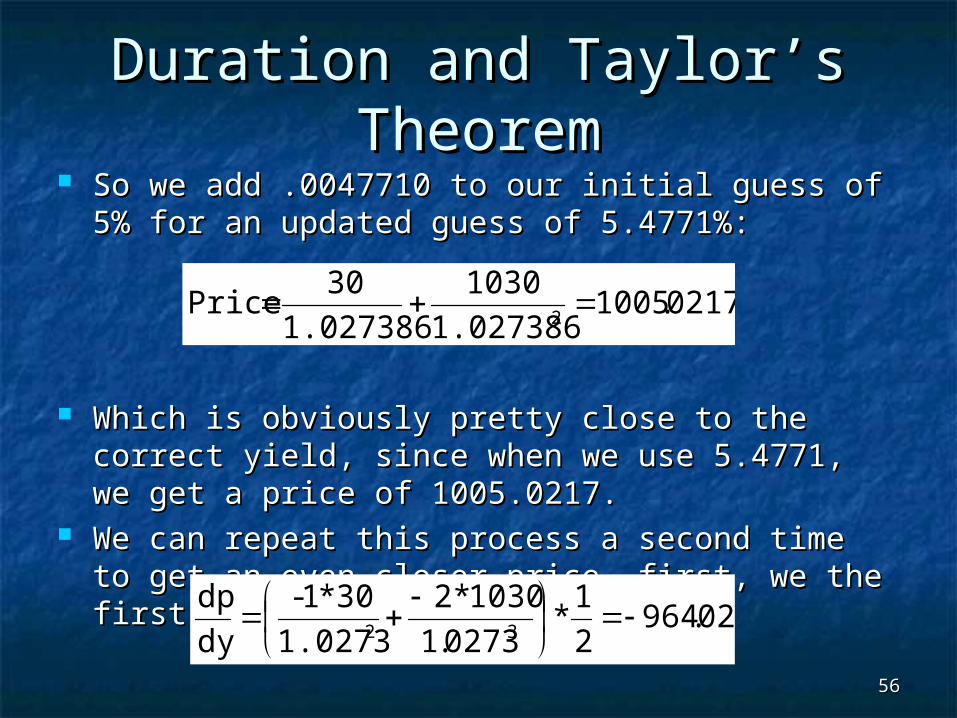

So we add .0047710 to our initial guess of 5% for So we add .0047710 to our initial guess of 5% for an updated guess of 5.4771%:an updated guess of 5.4771%:

Which is obviously pretty close to the correct Which is obviously pretty close to the correct yield, since when we use 5.4771, we get a price yield, since when we use 5.4771, we get a price of 1005.0217.of 1005.0217.

We can repeat this process a second time to get We can repeat this process a second time to get an even closer price, first, we the first derivative an even closer price, first, we the first derivative at 5.4771%.at 5.4771%.

0217.10051.027386

1030

1.027386

30 Price

2

02.9642

1*

0273.1

1030*2

1.0273

30*1-

dy

dp32

5757

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

Plugging back into Taylor’s theorem:Plugging back into Taylor’s theorem:

So we get:So we get:

We can then solve for h, the difference between We can then solve for h, the difference between 5% and the yield which will set the price of the 5% and the yield which will set the price of the bond to 1005:bond to 1005:

)(')()( xhfxfhxf

03.964*02.10051005 h

000022510.

02.964

02.10051005

h

5858

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

So we add .00002251 to our latest guess of So we add .00002251 to our latest guess of 5.4771% for an updated guess of 5.4779351%:5.4771% for an updated guess of 5.4779351%:

Which is close enough for our purposes. If you Which is close enough for our purposes. If you needed a more accurate answer, you can repeat needed a more accurate answer, you can repeat the process to any level of accuracy required.the process to any level of accuracy required.

This is the exact process that your calculator and This is the exact process that your calculator and Excel use to solve for yields (or IRR’s, which are Excel use to solve for yields (or IRR’s, which are the same thing.)the same thing.)

000086.10051.027396

1030

1.027396

30 Price

2

5959

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

This type of search algorithm is known as a This type of search algorithm is known as a Newton-Raphson method, although frequently it Newton-Raphson method, although frequently it is called simply Newton’s method. It is one of a is called simply Newton’s method. It is one of a general category of search algorithm’s known as general category of search algorithm’s known as “Gradient Descent” algorithms.“Gradient Descent” algorithms.

These search algorithms work well for most These search algorithms work well for most financial problems.financial problems.

The general rule of the algorithm, therefore is as The general rule of the algorithm, therefore is as follows:follows:

6060

Duration and Taylor’s Duration and Taylor’s TheoremTheorem

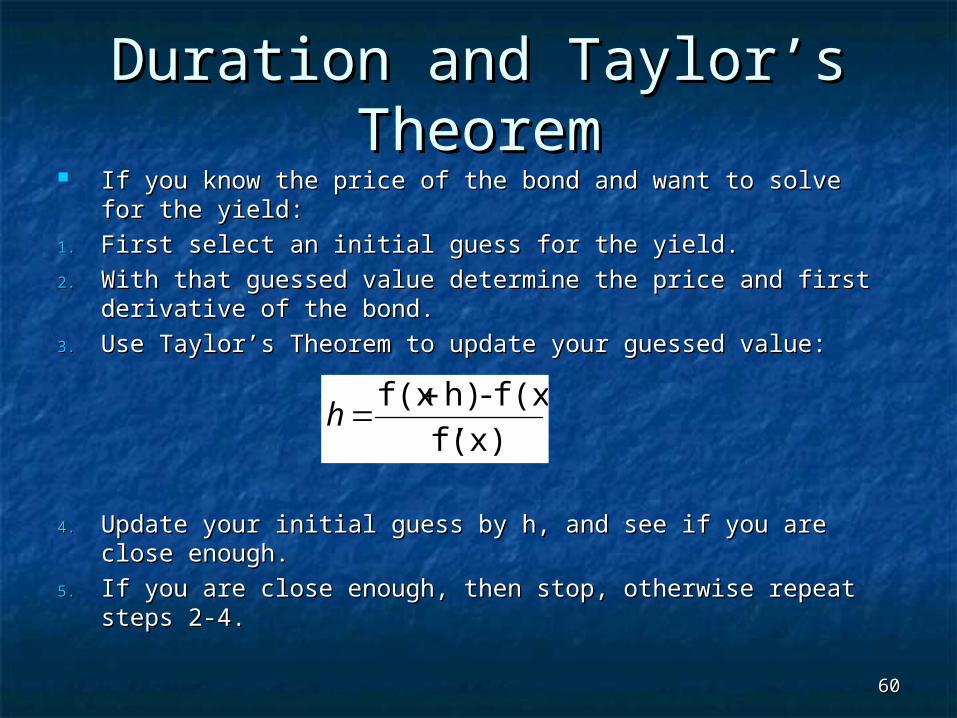

If you know the price of the bond and want to solve for the If you know the price of the bond and want to solve for the yield:yield:

1.1. First select an initial guess for the yield.First select an initial guess for the yield.

2.2. With that guessed value determine the price and first With that guessed value determine the price and first derivative of the bond.derivative of the bond.

3.3. Use Taylor’s Theorem to update your guessed value:Use Taylor’s Theorem to update your guessed value:

4.4. Update your initial guess by h, and see if you are close Update your initial guess by h, and see if you are close enough.enough.

5.5. If you are close enough, then stop, otherwise repeat steps 2-If you are close enough, then stop, otherwise repeat steps 2-4.4.

(x)f'

f(x) - h)f(x h

6161

ConvexityConvexity As mentioned earlier, Taylor’s Theorem uses As mentioned earlier, Taylor’s Theorem uses

higher order derivatives. It is common in finance higher order derivatives. It is common in finance to use only the first, although occasionally we will to use only the first, although occasionally we will use the second derivatives as well.use the second derivatives as well.

The second derivative is generally known as The second derivative is generally known as Convexity, and it measures the rate at which the Convexity, and it measures the rate at which the first derivative (duration) changes when the first derivative (duration) changes when the underlying interest rate changes.underlying interest rate changes.

6262

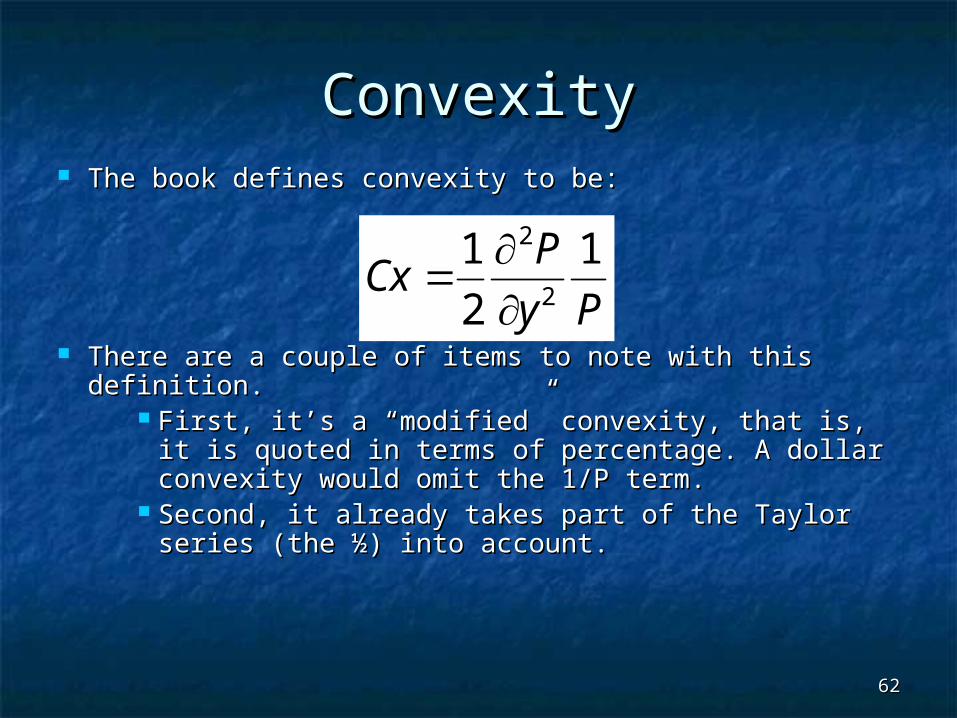

ConvexityConvexity The book defines convexity to be:The book defines convexity to be:

There are a couple of items to note with this definition.There are a couple of items to note with this definition. First, it’s a “modified” convexity, that is, it is First, it’s a “modified” convexity, that is, it is

quoted in terms of percentage. A dollar convexity quoted in terms of percentage. A dollar convexity would omit the 1/P term.would omit the 1/P term.

Second, it already takes part of the Taylor series Second, it already takes part of the Taylor series (the ½) into account. (the ½) into account.

Py

PCx

1

2

12

2

6363

ConvexityConvexity Recall that earlier we noted that the first derivative with respect to Recall that earlier we noted that the first derivative with respect to

price wasprice was

The second derivative, therefore must be given by:The second derivative, therefore must be given by:

n

1i1 (1)

m

1*

1

*

dr

dPii

mr

CFi

n

1i22

2

(2) m

1*

1

**)1(

dr

Pdi

i

mr

CFii

6464

ConvexityConvexity

Recall that Taylor’s theorem states:Recall that Taylor’s theorem states:

Or, putting it into book’s terms :Or, putting it into book’s terms :

Or in percentage terms :Or in percentage terms :

)3(!2

)('')(')()( 2 o

xfhxhfxfhxf

)3(*2

1* Price 2

2

2

oyy

Py

y

P

)3(*2

1*

P

Price 22

2

oyy

Py

y

P

6565

ConvexityConvexity

Now, you have to be a little bit careful of one Now, you have to be a little bit careful of one other issue, and that has to do with compounding other issue, and that has to do with compounding frequency.frequency.

Writing out Taylor’s theorem as we did in the last Writing out Taylor’s theorem as we did in the last slide, one has to recognize that we are working in slide, one has to recognize that we are working in periodicperiodic interest rates. Recall from equation (2) of interest rates. Recall from equation (2) of two slides ago that buried within it is a 1/m term. two slides ago that buried within it is a 1/m term. For semi-annual paying bonds, this will be ½, so For semi-annual paying bonds, this will be ½, so there are there are twotwo ½ terms in the convexity portion of ½ terms in the convexity portion of the Taylor expansion for the semi-annual paying the Taylor expansion for the semi-annual paying bond.bond.

6666

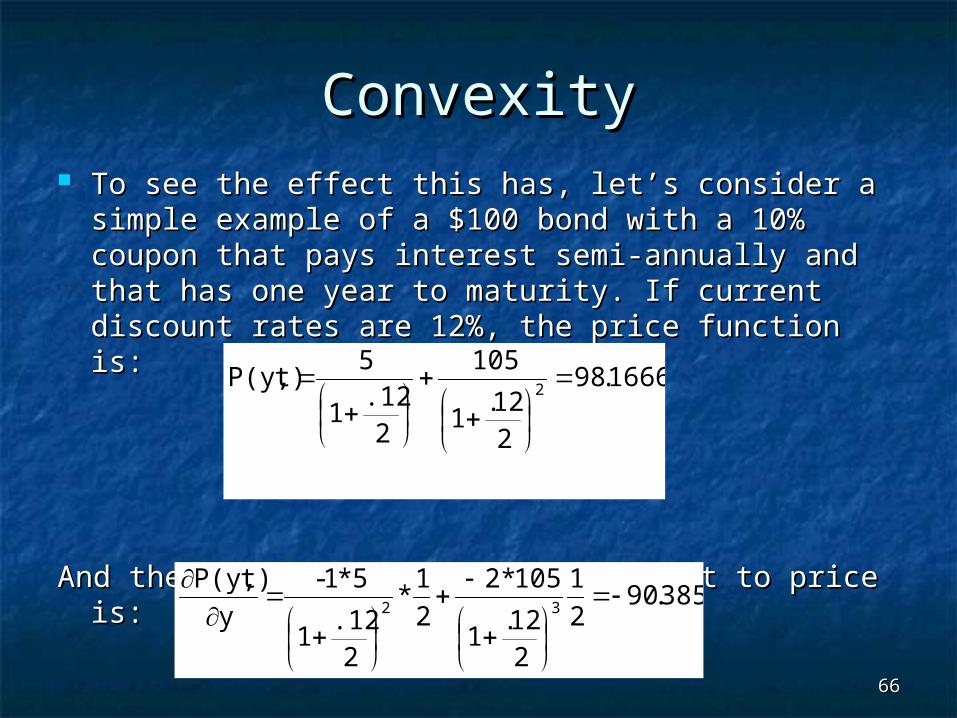

ConvexityConvexity To see the effect this has, let’s consider a simple To see the effect this has, let’s consider a simple

example of a $100 bond with a 10% coupon that example of a $100 bond with a 10% coupon that pays interest semi-annually and that has one year pays interest semi-annually and that has one year to maturity. If current discount rates are 12%, the to maturity. If current discount rates are 12%, the price function is:price function is:

And the first derivative with respect to price is:And the first derivative with respect to price is:

1666.98

212.

1

105

2.12

1

5 t)P(y, 2

385.902

1

212.

1

105*2

2

1*

2.12

1

5*1-

y

t)P(y,32

6767

ConvexityConvexity And the second derivative with respect to price is:And the second derivative with respect to price is:

Let’s say the annual discount rate changes from Let’s say the annual discount rate changes from 12% to 10%. Based on Taylor’s theorem we can 12% to 10%. Based on Taylor’s theorem we can approximate the change using just duration as:approximate the change using just duration as:

71.2532

1

212.

1

105*3*2

2

1*

2.12

1

5*2*1

y

t)P(y,43

99.96571.805798.16 Price Price Old Price New

be willprice new eapproximat theSo

8057.102.*90.285- )2(* Price

oyy

P

6868

ConvexityConvexity If we incorporate the convexity term, we will wind up with the If we incorporate the convexity term, we will wind up with the

following estimated price:following estimated price:

100.011.858498.16 Price Price Old Price New

:be willestimate price new theThus

8584.105074.8077.102.*71.2532

102.*90.385- Price

thatso

)3(*2

1* Price

2

22

2

oyy

Py

y

P

6969

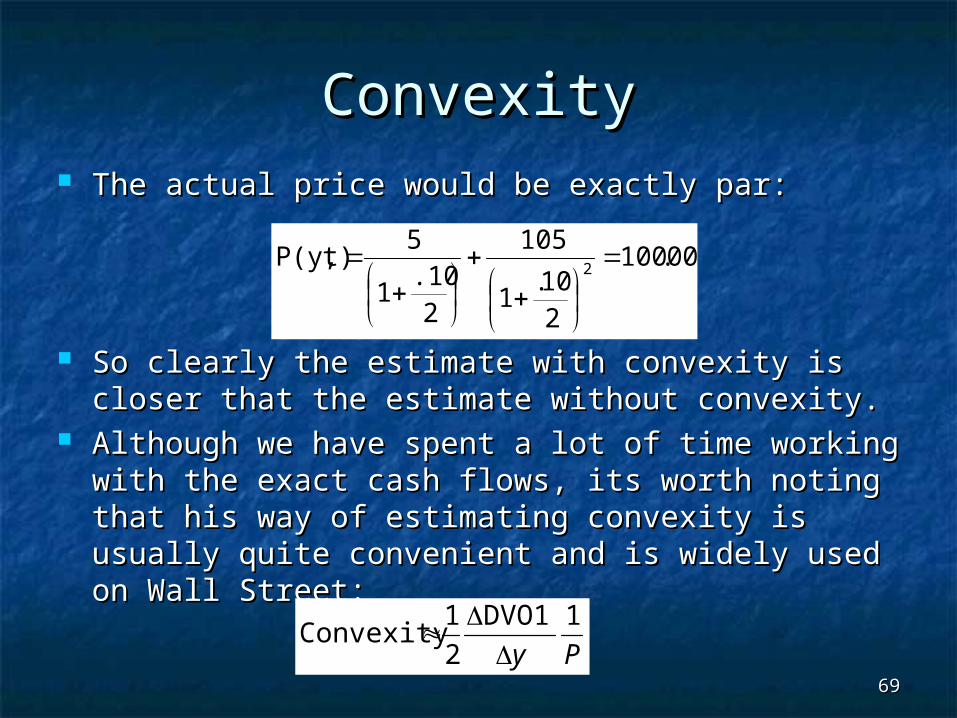

ConvexityConvexity The actual price would be exactly par:The actual price would be exactly par:

So clearly the estimate with convexity is closer So clearly the estimate with convexity is closer that the estimate without convexity.that the estimate without convexity.

Although we have spent a lot of time working with Although we have spent a lot of time working with the exact cash flows, its worth noting that his way the exact cash flows, its worth noting that his way of estimating convexity is usually quite of estimating convexity is usually quite convenient and is widely used on Wall Street:convenient and is widely used on Wall Street:

00.100

210.

1

105

2.10

1

5 t)P(y, 2

Py

1DVO1

2

1Convexity

7070

Duration: AppendixDuration: Appendix

Recall the present value of an annuity formula:Recall the present value of an annuity formula:

It is convenient to rewrite this a little and then It is convenient to rewrite this a little and then re-express it as a product:re-express it as a product:

mrmr

pmtpv

n

1

11

*

7171

Duration: AppendixDuration: Appendix

1*

1

11**

*

1

11*

1

11

*

r

mr

mpmtpv

or

r

m

mr

pmt

mrmr

pmtpv

n

nn

7272

Duration: AppendixDuration: Appendix Recall the product rule from differential calculus:Recall the product rule from differential calculus:

In our case we note that:In our case we note that:

)(*)()(*)()(dx

d

thenv(x),*u(x) f(x) If

xuxvdx

dxvxu

dx

dxf

rrv

and

mrmpmtru n

1)(

/1

11**)(

7373

Duration: AppendixDuration: Appendix

We can easily calculate the derivative for v(x),We can easily calculate the derivative for v(x),

22

1

11)(

1)(

rrrv

dr

d

so

rr

rv

7474

Duration: AppendixDuration: Appendix The derivative for u(x) is slightly more difficult, The derivative for u(x) is slightly more difficult,

11

1

/1

*/1*

)/1(

**)(

:us gives gsimplifyin

/1*)/1(***)(0)(

/1**)*(/1

11**)(

nn

n

n

n

mr

pmtnm

mr

mpmtnru

dr

d

mmrmpmtnrudr

d

so

mrmpmtmpmtmr

mpmtru

7575

Duration: AppendixDuration: Appendix We now have each component we need to We now have each component we need to

calculate the derivative for the entire pva calculate the derivative for the entire pva formula:formula:

2

1

1)( and

1)(

;/1

*)(

/1

11**)(

rrv

dr

d

rrv

mr

pmtnru

dr

d

and

mrmpmtru

n

n

7676

Duration: AppendixDuration: Appendix So plugging in the various values yields:So plugging in the various values yields:

21

21

/1

11**

*/1

*)(

/1

11***

11*

/1

*)(

or

)(*)()(*)()(pva

so

v(r)*u(r) pva(r)

r

mrmpmt

rmr

pmtnrpva

dr

d

or

mrmpmt

rrmr

pmtnrpva

dr

d

rurvdr

drvru

dr

dr

dr

d

n

n

nn

7777

Duration: AppendixDuration: Appendix So the formula to calculate the derivative of an So the formula to calculate the derivative of an

annuity with respect to interest rates is:annuity with respect to interest rates is:

If there is a final principal cash flow you must If there is a final principal cash flow you must modify this to include that cash flowmodify this to include that cash flow

21

/1

11**

*/1

*)(

r

mrmpmt

rmr

pmtnrpva

dr

dn

n

121 /1

*/1

11**

*/1

*)(

n

n

n mr

facen

r

mrmpmt

rmr

pmtnrpva

dr

d