Embed Size (px)

Citation preview

1

Capital Raising: Public vs Private Issues

Advanced Corporate Finance

Semester 1 2009

2

Why Go Public?

Remember majority of firm (by number not size) are private and most firms (albiet small) choose to issue private

Then why list• Funding demand

• Growth potential

• Distinct life cycle stages

• Favourable market conditions

• Realization of return (venture capitalist)

• More dispersed ownership

3

Who Do We Issue Securities To?

Existing security holders - family or rights issue• For equity renounceable rights issues (can sell your

entitlement to the new shares to a third party) account for 68% of all issues

Market or public issue• For equity most common when firms initially listed

Private placements/financial intermediaries.

4

Underwriting Equity Issues

Underwritten• firm commitment contract

• underwriter purchases issue and on sells it

• standby contract• underwriter takes up unsubscribed portion of issue

• best effort contract Non-underwritten

5

Why Do Firms Underwrite Security Issues?

What is the evidence• The underwriter certifies firm quality

• The choice of underwriting firm is relevant

• Process expertise

• Firms choose most cost effective method for their shareholders• Those US firms choosing standby rights have higher

ownership concentration.

• Trade-off between fee and issue price discount

• Underwriting fee is a function of risk

6

Anomalies in IPO’s

Abnormally high listing day returns Non stationary “hot markets”

• go to the market when prices “high”

• first day returns lowest in periods of high volume

• go public near peak of industry specific fads Back door listings In the long run IPO’s appear overpriced

• Average performance

7

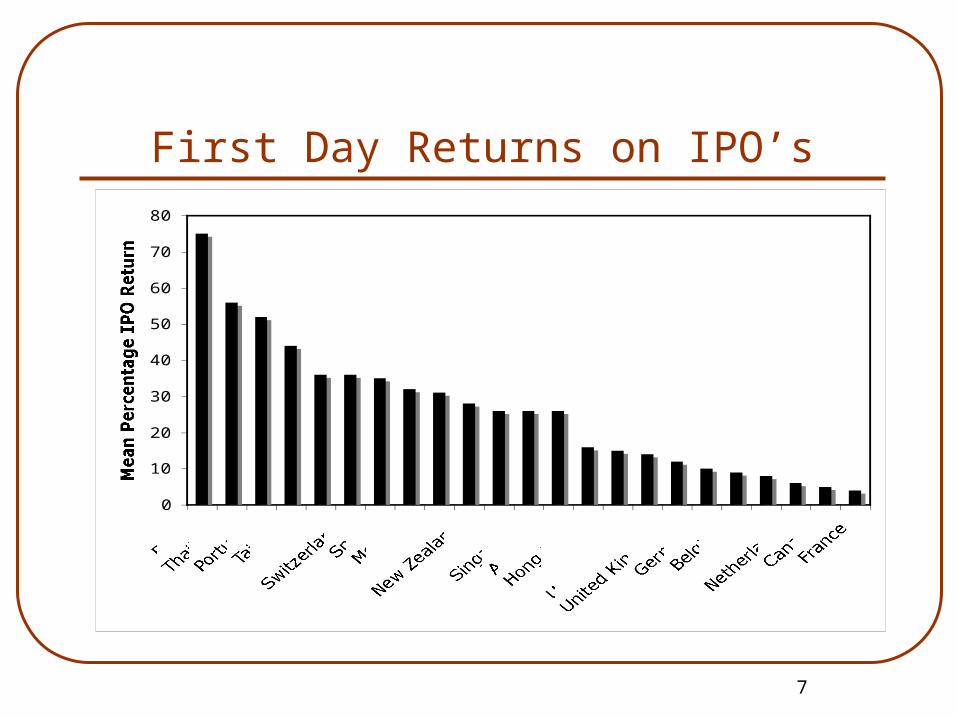

First Day Returns on IPO’s

0

10

20

30

40

50

60

70

80

BrazilThailandPortugalTaiwanSweden

Switzerland

SpainMexicoJapan

New Zealand

Italy

SingaporeAustraliaHong Kong

Chile

United StatesUnited Kingdom

GermanyBelgiumFinland

Netherlands

CanadaFrance

Mean Percentage IPO Return

8

Explanations for Underpricing

Asymmetry between Firm and Investors as to Firm’s Value• Lemons problem

• Underpricing as a signal of quality

• Leave investor’s with a “good taste”• In the game for the long run

• Underprice to create “goodwill” and make subsequent issues easier

9

Empirical Support

Low balling questionable• No evidence of a propensity to return to the

market to raise additional funds - seasoned offering or higher dividend payout

• But less underpricing the higher the fractional ownership retained (but could be a governance issue)

10

Explanations for Underpricing

Asymmetry between Investors as to Firm’s Value• Underpricing being the compensation for this

uncertainty

• The more fully informed investors are regarding the firm’s value, the lower will be the underpricing.• winner’s curse

• information acquisition by issuer

• information cascade

11

Winner’s Curse

If you are an uniformerd investor and ask for allocation, you will likely be stuck disproportionately with the hard-to-sell offerings.

Assume

• Large informed and many small uninformed investors

• Capital rationing

• Large investors get preferential treatment

• Bid only for successful offerings

• Small investors full allocation of overpriced IPOs (100%) but only partial allocation of underpriced offerings (50%)

12

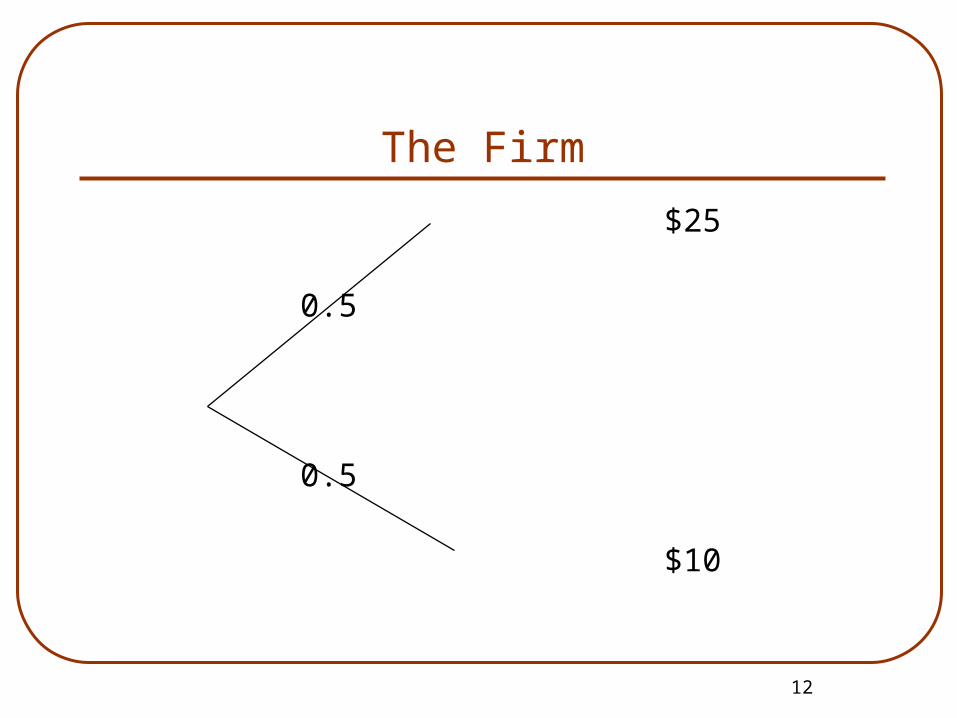

The Firm

$25 0.5

0.5

$10

13

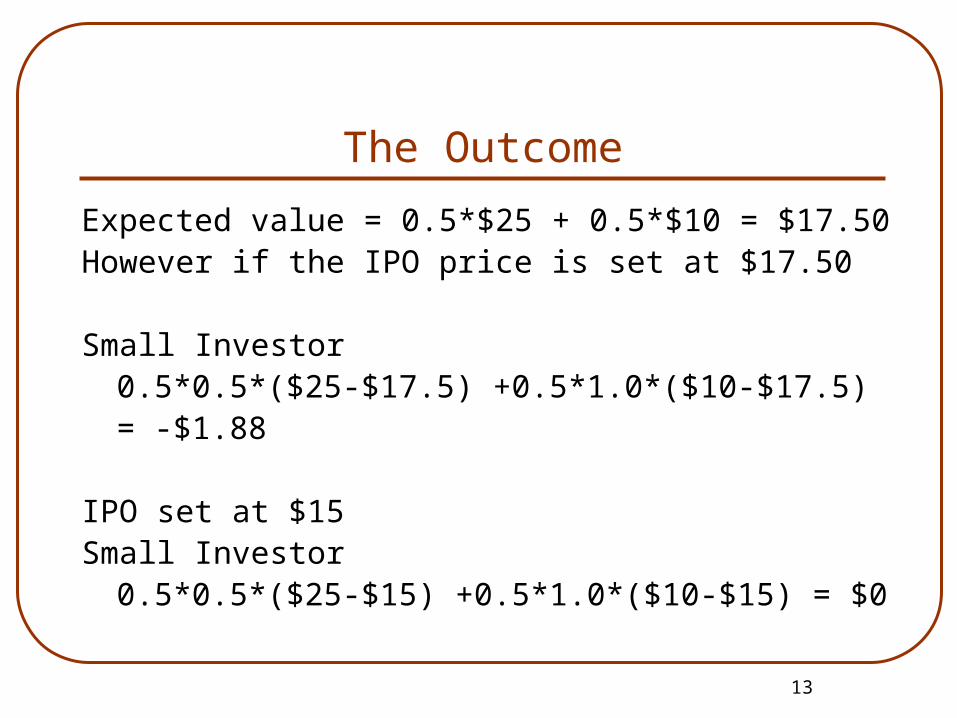

The Outcome

Expected value = 0.5*$25 + 0.5*$10 = $17.50However if the IPO price is set at $17.50

Small Investor0.5*0.5*($25-$17.5) +0.5*1.0*($10-$17.5)= -$1.88

IPO set at $15Small Investor

0.5*0.5*($25-$15) +0.5*1.0*($10-$15) = $0

14

Information Acquisition

Information acquisition by issuer• Book building

• If bidding (disclosure of demand) will result in higher offer price then issuing firm must offer investor something in return.

• Empirical support• Informed investors receive higher allocation

• When offer price exceeds the original price range (higher demand let to upward offer price revision), the underpricing is still significantly above average

• The compensation necessary to induce investors to reveal high demand

Role of Underwriter

When underwriter is informed• Costly to monitor underwriter

• Underpricing acts to incentive underwriter• But – underpricing is same for underwriter IPOs

Underpricing substitutes for marketing expenditure• But underpricing extreme during internet bubble –

when marketing costs low

15

16

Cascading Demand

Learn a lot from how “excited” other investors are about the IPO• Investors follow one another

• IPO success depends on whether the investor herd is stampeding

Ensure success by creating “enthusiasm”

Share Allocation

Future wealth• Underpricing allowed because information gained

about increase in post issue value Ownership structure

• Institutional investors are more informed and preferred – receive preferential allocation – monitoring role

• Seek blockholders for defensive and monitoring reasons

• Disperse shareholding entrenches mangement

17

18

Empirical Support

Information asymmetry• Underpricing is lower for IPOs:

• Where the firm provides more publicly available information

• With high reputation underwriters

• Winner’s curse• Informed investors preferentially received higher allocation

• Receive higher allocation of hot issues

• Information acquisition• When offer price exceeds the original price range the underpricing is

still significantly above average

• Information cascades• IPOs either undersubscribed or hugely oversubscribe no in-between