Embed Size (px)

Citation preview

VANGUARD SECURITIES CORP.

Presented By:Henry Chen

Jill ChiJason Coffee

Katherine LiangHeenal Patel

FOREIGN EXCHAGE HEDGING DILEMMA

Fin 570Dr. Greco

1

AGENDA

• Company background• Brief VSC financial analysis• Introduction of Bench Mark Company- Trend Micro• Explain the bid• Explore Matrix & Fish Bone• State Hedging Options• Identify Our Decision Criteria• Explain Options• Recommendation (chosen based on the criteria)

2

BACKGROUND

Source: Thunderbird School of Global Management

Vanguard Security Corporations • Financial security provider for

companies founded in early 1990’s

• Headquarters in Portugal• Main clients include major

European banks

3

BACKGROUND

Source: Thunderbird School of Global Management

Vanguard Security Corporations

• Experienced rapid expansion in revenues and profit during early growth stages

• Increased competition from Asian has reduced market share

• Competition eroding profit margin

4

BRIEF FINANCIAL ANALYSIS

• VSC projects Net Income loss of €8.7 million for 2008

• Balance sheet shows cash assets only €2.1 million

- Cash/Total current assets= 1.4%

• Cash on hand very limitedSales and Income Statement (in millions of Euro)

2007 2008

Net Sales 379.9 307.5

Net Income 46.3 -8.75

BENCHMARK COMPANY

• Provides security solutions• Headquarted in Japan• Operations in More than 50 countries &

9 Global R&D centers • Customers being Enterprises & Small to Medium size

Businesses• 2007 Revenue US $848 Million

Source: Trend Micro’s Annual Report for Fiscal Year 2008 6

BENCHMARK COMPANY

• Translation exposure

• Translation of major foreign currency assets and liabilities into “Japanese Yen”

• Exchange loss $1,411 million (Yen) in 2008 in their financial statement

Source: Trend Micro’s Annual Report for Fiscal Year 2008 7

SITUATION AT HAND

• Forced to cut prices to retain customers

• Acquired long-term debt to fund research

• Fear of takeover as many private equity companies show interest in VSC

• U.S. viewed as potentional new market to develop a new customer base as well as generate revenue

8

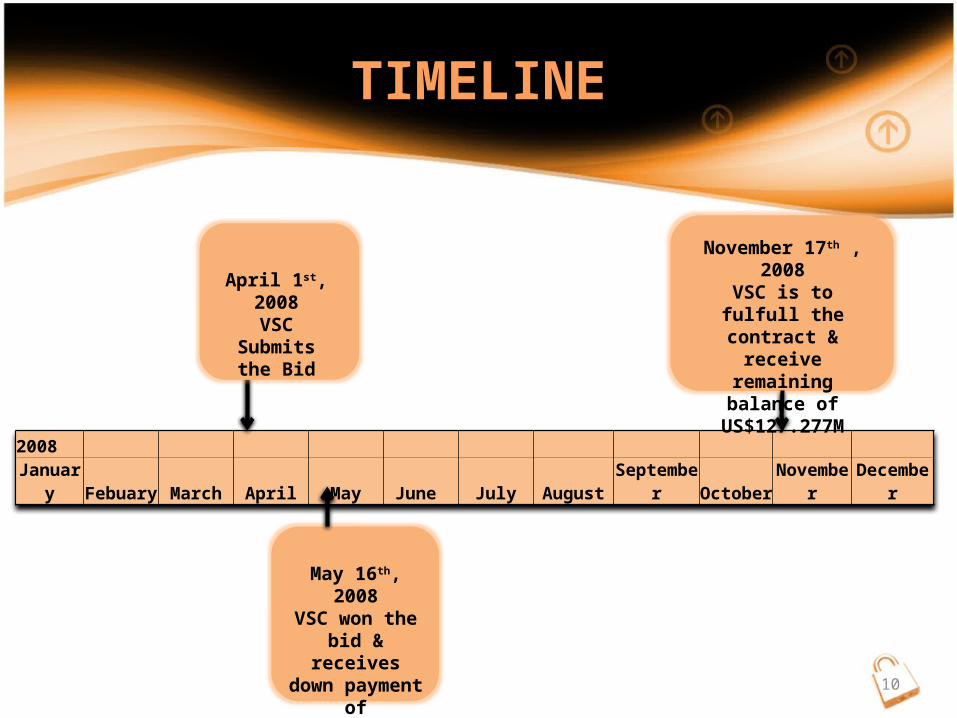

THE BID

• Contract Tendered on April 1st

• Awarded on May 15th

• May 16th, Received 10% down payment; US$16.103M

• Remainder 90% (US$127,277M) to be paid at the time of system installment– 6 months from the receipt of down payment;

November 17th

• Between April 1st-May 16th Euro increases in value 0.74% 9

TIMELINE

2008

January Febuary March April May June July August September October November December

November 17th , 2008VSC is to fulfull the contract & receive

remaining balance of US$127.277M

May 16th, 2008VSC won the bid & receives down

payment of US$16.103M

April 1st, 2008VSC Submits

the Bid

10

ISSUE MATRIX

Global

Business

Expansion

Product Quality

Hedging Strategy Profitabilit

y

Basic

LOW HIGH

LOW

HIGH

Importance

Urgency

11

ISSUE MATRIX

Sucessfully Gain U.S.

Market

Share

Controlling Project Costs

Meeting Deadlines

Minimize Hedgi

ng CostsImmediate

LOW HIGH

LOW

HIGH

Importance

Urgency

12

CAUSE AND EFFECT

Hedging Costs

Economic Conditions

Currency Exchange Rates

Hedging Method & Risks

Bank Relationship

Management Oversight

13

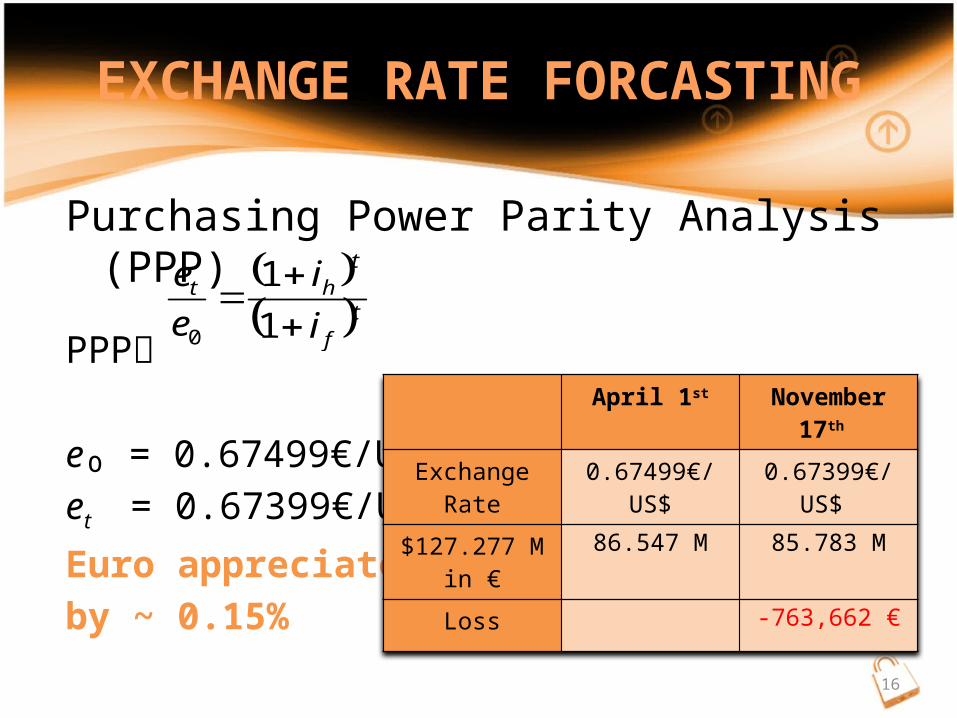

EXCHANGE RATE FORCASTING

Source: Board of Governors of the Federal Reserve System14

Purchasing Power Parity Analysis (PPP)• Given:May 16th e₀ = 0.67499€/US$

t = 6 months

PPP tf

tht

i

i

e

e

1

1

0

EXCHANGE RATE FORCASTING

2008 Annual Rate 2008 Monthly RateHome inflation rate– Europe 2.00% 0.17%

Foreign inflation rate– US 2.30% 0.19%

Rate on November 17th

15

Purchasing Power Parity Analysis (PPP)

PPP

e₀ = 0.67499€/US$et = 0.67399€/US$

Euro appreciates by ~ 0.15%

tf

tht

i

i

e

e

1

1

0

EXCHANGE RATE FORCASTING

April 1st November 17th

Exchange Rate 0.67499€/US$ 0.67399€/US$

$127.277 M in € 86.547 M 85.783 M

Loss -763,662 €

16

The International Fisher Effect (IFE)

• Given: May 16th e₀ = 0.67499€/US$ t = 6 months

IFE

EXCHANGE RATE FORCASTING

2008 Annual Rate 2008 Monthly RateHome interest rate– Europe 4.30% 0.36%Foreign interest rate– US 4.30% 0.36%

tf

tht

r

r

e

e

)1(

)1(

0

17

The International Fisher Effect (IFE)

IFE

et = e0 = 0.67499€/US $

No change in interest rate IFE is not in effect• Costs are same everywhere in terms of Short-term

Financing

EXCHANGE RATE FORCASTING

tf

tht

r

r

e

e

)1(

)1(

0

18

Additional Factors Affecting Exchange Rates

• Economic Condition

• Unemployment Rates in Europe

• U.S. Money Supply

All factors Favor in the Euro Appreciating

– Hence, increasing its Economic Exposure

EXCHANGE RATE FORCASTING

19

SIX HEDGING ALTERNATIVES

Forward Currency Contract

Forward Currency Futures Contract

Foreign Currency Option

Tunnel Forward

Foreign Currency Loan

Pre-sale of Foreign Contract20

DECISION CRITERIA

•Minimizing Hedging Costs

Cost

•Preventing Exchange rate loss on future payment

Retaining Contract Value

•Minimizing Risk associated with being locked in to a particular strategy

Risk

Cash Flow • Attaining up-front cash flow to fund project

21

KEY HEDGING INFORMATION

• VSC is receiving a payment of $127,277,000 in 6 months

• The valuation of this payment at April 1st exchange rates is €86,547,668

• The same payment valuation with May 16th exchange rates is €85,910,901 – a loss of €636,767 from the Euro appreciating

• PPP analysis projects a further appreciation of the Euro

22

No Hedging Strategy Graph

23

OPTION 1: FORWARD CURRENCY CONTRACT

Details:• Purchased through VSC’s bank at the May 16th quoted 6-

month forward exchange rate of 1€ = US$1.4650, or €0.6826 = US$1.

• VSC is only obligated to the contract if they complete the work for the American company.

• This hedge risk is medium risk since they are still obligated to the contract if they complete the work.

24

OPTION 1

Results:

• At an exchange rate of €0.6826 = US$1, VSC would receive €86,878,498 for its $127,277,000 Nov. 17th payment.

– Retained Value: €330,830 gain over the Apr. 1st valuation of the payment results from this hedging strategy.

– Timeline: 6 month wait to get the Euros.

– Risk: Medium25

OPTION 1

•Graph

Option 1 Graph

26

OPTION 2: FOREIGN CURRENCY FUTURES CONTRACTS

Details:• VSC would purchase Euro futures contracts through the

Chicago Mercantile Exchange in blocks of $125,000.

• The contracts would require delivery of US Dollars at the end of December.

• VSC would purchase 1,018 contracts at a cost of $50,900 in broker’s fees, with a remainder of $27,000 that is not hedged.

• ($127,277,000) / ($125,000) = 1,018.216

• ($125,000) * 0.216 = $27,00027

OPTION 2: FOREIGN CURRENCY FUTURES CONTRACTS

Details:

• The December Euro futures exchange rate is 1€=US$1.4655, or €0.6824=$1.

• The unprotected remainder of $27,000 would be hedged by purchasing a 6-month forward contract at the exchange rate of €0.6826 = US$1

28

OPTION 2

Results:

• VSC would net €86,814,131 from its $127,277,000 Nov. 17th payment.

– Retained Value: €266,464 gain over the Apr. 1st valuation of the payment results from this hedging strategy. Overall, a less favorable exchange rate than Option 1 at higher cost.

– Timeline: 7.5 month wait to get the Euros.

– Risk: High due to the fact that once the contract is purchased, VSC is obligated to the contract’s terms.

29

Option 2 Graph

30

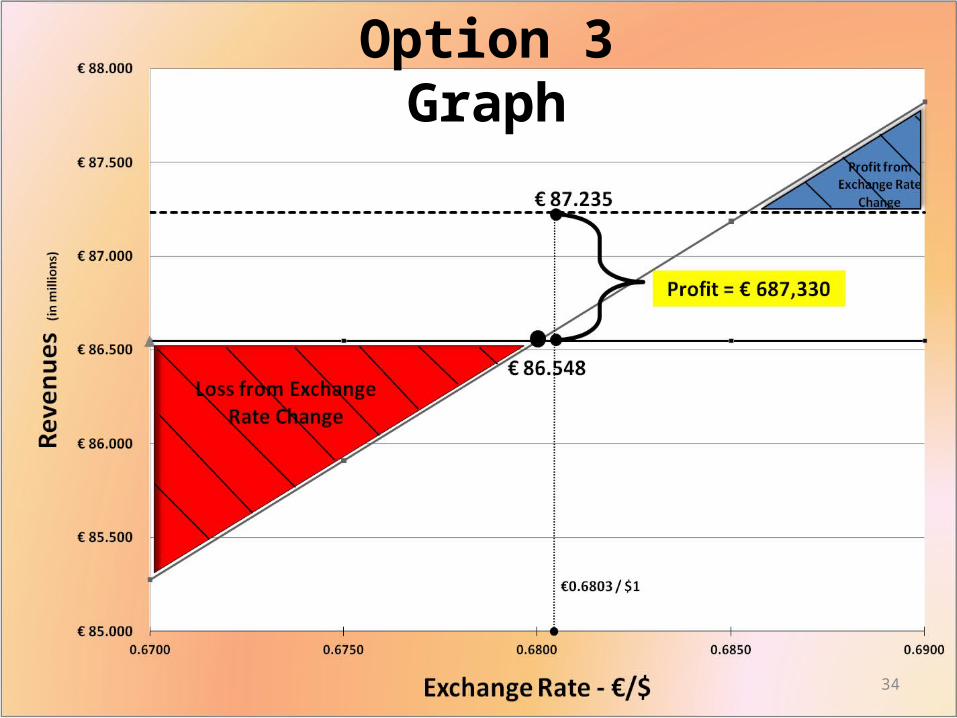

OPTION 3: FUTURES CURRENCY OPTIONS

Details:

• VSC can simultaneously buy a put option and write a call option at the same strike price.

• Both options would be European, exercisable in 6 months, and the option premiums would be paid at the time of issue.

• The 180-day currency option premium on a strike price of 1€ = US$1.4699, or €0.6803 = US$1, is:

• US$0.03256/euro for a call premium, and • US$0.0215/euro for a put premium.

31

OPTION 3: FUTURES CURRENCY OPTIONS

Details:• The put option allows VSC to sell US dollars for Euros at the

strike exchange rate. VSC is protected from a appreciation of the Euro.

• The call option allows the buyer of the option to buy US dollars with Euros at the strike exchange rate. VSC would benefit by collecting the option’s premium. A “Covered Call”

• The call premium exceeds the put premium, so VSC would have an immediate net inflow from entering into these options.

32

OPTION 3

Results:• Regardless of whether the €/$ increases, decreases, or

remains constant, under this hedging strategy VSC will receive a net of €87,234,997

– Retained Value: €687,330 gain over the Apr. 1st valuation of the payment results from this hedging strategy.

– Timeline: 6 month wait to get the Euros.– Risk: Low

The risk was initially assessed at medium since there is a risk that the deal could break-down shortly after writing the call, and if the dollar appreciates, VSC would suffer a loss from the call being exercised. The PPP calculation, however, indicates that a dollar appreciation is highly unlikely. 33

Option 3 Graph

34

OPTION 4: TUNNEL FORWARDS

Details:

• Also known as Currency Collar

• A contract that provides protection against currency moves outside an agree-upon range (€0.6429 - €0.7105)

• Agree to convert at the future spot rate if:

– The rate falls within the range

– At the boundary rates when future spot rate falls beyond the range

35

OPTION 4

Tunnel Call (€0.6429) Nov. Spot Rate (€0.6740)

Tunnel Put (€0.7105)€0

€10,000,000

€20,000,000

€30,000,000

€40,000,000

€50,000,000

€60,000,000

€70,000,000

€80,000,000

€90,000,000

€100,000,000

€0.6429 €0.6740 €0.7105

Guaranteed Minimum Cash Flow

€81,826,383

€85,782,361

Guaranteed Maximum Cash Flow

€90,430,309

36

OPTION 4

Results:

• Vanguard takes some but not all the exchange rate risk associated with its receivable

– Retained Value: Gain or loss depends on November 17th Spot Rate

– Timeline: 6 month wait to get the Euros

– Risk: Medium

37

OPTION 5: FOREIGN CURRENCY LOAN

Details:Bid Preparation (Euro)

Design €3,700,000Materials €68,900,000Labor & Installation €6,900,000Shipping €1,200,000Direct Overhead €3,400,000Allocation of Indirect Overhead €1,700,000Total Required Funding €85,800,000 Less Initial Down Payment €10,869,389Amount Necessary To Borrow €74,930,611

38

OPTION 5

Results:U.S Loan Euro Loan

• 4% APR • Fee of 0.125% • Receive €74,836,948 on May 16th • Repay €77,927,835 on November 17th

• 3.68% APR • No Fees • Receive €74,930,611 on May 16th • Repay € 77,684,311 on November 17th

39

OPTION 5

Results:

• Borrow a 180-day loan on May 16th and then repay the principal plus interest on November 17th

– Cost: Interest plus agreement fee

– Timeline: Receive funds on May 16th

– Risk: Low

40

OPTION 6: PRESALE OF FOREIGN CONTRACT

Details:

• Allows Vanguard to presale its receivable of $127 million at a LIBOR rate

• Provide protection against a possible change in the value of the euro relative to the U.S. dollar

41

OPTION 6

• LIBOR stands for “London Inter-Bank Offered Rate”

• An interest rate at which banks can borrow money from other banks in the London wholesale money market

• An index that is used to set the cost of various variable-rate loans

• Credit spread is usually chargedSources: Bankrate.com

42

OPTION 6: PRESALE OF FOREIGN CONTRACT

Sources: Bankrate.com

6 Month LIBOR RateUpdated 7/1/2009

Last Week Month Ago Year Ago

Rate 1.11% 1.23% 3.12%

43

OPTION 6

Results:

• U.S. LIBOR offers (6 month term):

– An interest rate 4.15% plus a credit risk spread of 1.8%

– Flat upfront fee of 0.5% apply

– Amount receive on May 16th is €80,369,648

– Retained Value is -€6,178,020

(Difference between April 1st €86,547,668 & May 16th €80,369,648)

44

OPTION 6

Result:

• Euro LIBOR offers (6 month term):

– An interest rate 4.35%

– Amount to receive on May 16th is €82,173,777

– Retained Value: -€4,373,891

(Difference between April 1st €86,547,668 & May 16th €82,173,777)

– Euro LIBOR option retains more value45

ALTERNATIVE ANALYSIS MATRIX

OptionsDECISION CRITERIA

Project Funding Retained Contract Value Cost Risk

1. Forward Contract No € 330,830 Included Medium

2. Futures Contract No €266,464 $50,900 High

3. Currency Options No €687,330 Offset Low

4. Tunnel Forward No Depends Included Medium

5. Foreign Currency Loan

Yes €0 €2,753,700 Low

6. Presale of Foreign Contract Yes €0 €4,373,891 Low

46

RECOMMENDATION

OptionsDECISION CRITERIA

Project Funding

Retained Contract Value Cost Risk

3. Currency Options No €687,330 Offset Low

5. Foreign Currency Loan Yes €0 €2,753,700 Low

47

FIRST PHASE (MAY 16TH)

• Foreign Currency Loan– Borrow fund required to complete the project

• Cheaper than Presale of Foreign Contract– 4.37 million (Euro) vs 2.75 million (Euro)

48

SECOND PHASE (NOV 17TH)

• Receive 127.277 million USD on Nov 17th

• Foreign Currency Option– Amount retained from hedging: €687,330

• 1. Forward Contract: € 330,830• 2. Futures Contract: € 266,464

49

CONCLUSION

• Combination of Foreign Currency Loan and Foreign Currency Option

– Save more on interest expense

– Retain more on hedging amount

– Low risk

50

QUESTIONS ???

51