Embed Size (px)

Citation preview

1

Creating Value fromCorporate Governance:

focus on private equity

Teresa C. BargerInternational Finance Corporation / The World Bank

April 23, 2007

2

Venture Capital extremely high growth prospects

Private Equity •Earnings Growth•Margin Expansion•Multiple Expansion

Buy Out same as above + leverage + de- and re-listing

Key Investment Theses of Private Equity

3

Achieving PE Investment Theses:Two Basic Approaches

Private Equity

•Earnings Growth•Margin Expansion•Multiple Expansion

Fix Something Broken

Add Something New

4

Three Kinds of Restructuring in Investee Companies

Operational Financial Organizational

Fix Something Broken

E.g. Rebalance production

E.g. Debt restructuring E.g. Fix corp governance

Add Something New

E.g. New product introduction or changing product to sell internationally

E.g. Introduce new leverage

E.g. Introduce modern corp governance

5

What is Corporate Governance?

Systems, procedures, processes and structures which ensure the maximization of shareholder wealth by reinforcing inter alia the strategic positioning of the company and the performance of all parts of the organization in relation to that strategy through:

- Management accountability

- Systems to incentivize and ensure the employees and the capital are working to execute the strategy

- Fulfillment of fiduciary duties to financial stakeholders

- Assurance that corporate direction and culture are functioning for the good of the company

6

Five Areas of Corporate Governance

1. Commitment to Corporate Governance

2. Structure and Functioning of the Board

3. Treatment of Minority Shareholders

4. Internal Controls

5. Transparency and Disclosure

7

The equity contract is . . .

8

The equity contract is CG

Lending Private Equity Listed Equity

Loan Agreement

Equity Agreement:- Self Dealing- Capital spend- Dividend policy- Voting rights- etc.

CorporateGovernance

9

CG adds value in three financially quantifiable ways.

1. Decreases the cost of capital > raises price / earnings ratio

2. Decreases cost of debt

3. Adds productivity

10

Higher Market Valuations

• Experience of Activist Institutional Investors: CalPERS Governance Portfolio Performance 17.7% over seven years. Three times the benchmark.

• Deutsche Bank research: S&P500 firms with good governance outperformed those with poor governance by 19% in P/E over two year period

• McKinsey Survey: institutional investors would pay: - 22% premium for well-governed companies in Asia - 30% premium in Eastern Europe and Latin America

• Lazard Korea Corp Governance Fund: first company invested in doubled in 5 days and tripled in three weeks

11

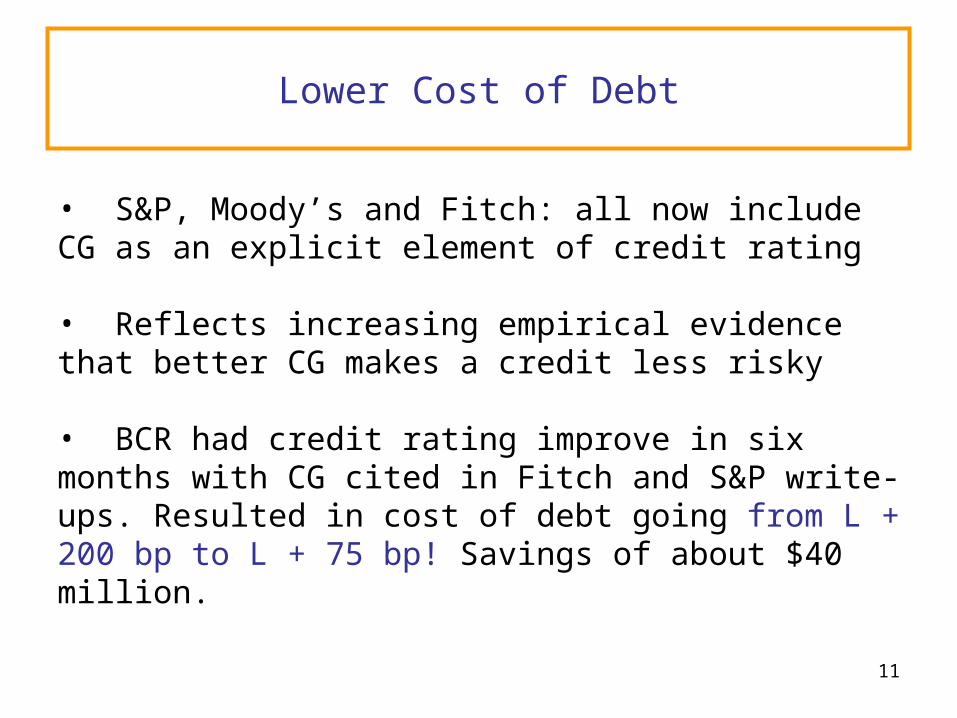

Lower Cost of Debt

• S&P, Moody’s and Fitch: all now include CG as an explicit element of credit rating

• Reflects increasing empirical evidence that better CG makes a credit less risky

• BCR had credit rating improve in six months with CG cited in Fitch and S&P write-ups. Resulted in cost of debt going from L + 200 bp to L + 75 bp! Savings of about $40 million.

12

Productivity and Performance

• US firms with better governance found to have higher sales growth and higher profitability than peers (Harvard/Wharton)

• Brazilian firms with above-average CG had ROEs 45% higher and net margins 76% higher that below average

• Best governed companies in India and East Asia had Economic Value Added (EVA) 8% points higher than national averages (CLSA 2001)

13

Example: Banca Comerciala Romana

• Largest Commercial Bank in Romania• State-owned (70%), with minority (30%) held by Investment Funds (SIFs)• Fraud nearly once-a-month • Two failed privatization attempts in 2002• Management and board indistinguishable

- Board composed of senior managers and SIF representatives

- Met more than 25 times annually• Risk management and internal controls systems weak, accounts not credible

14

BCR: IFC’s Investment

• 12.5% + one share for US$111 million- .88x book value- Negotiated pari passu and in tandem

with EBRD- Tag-along / drag-along

• Institution-building program part of Investment Agreement

15

CG Program Put in Place

•Introduced Two-Tiered Board Structure- Management off the Supervisory Board- Redrafted Charter- Amendments to Banking Law- Audit & Compliance and Compensation Committees

•IFC and EBRD-nominated directors

•Active engagement at Shareholders Meeting

•Two-Stage Training Program- IMD/IIF Seminar for Board members- In-house Program

•Implementation of control systems- Improvement of Risk Management and Internal Controls- IFC-sponsored Resident Advisor to Internal Controls

Unit

16

Initial Results Were Good

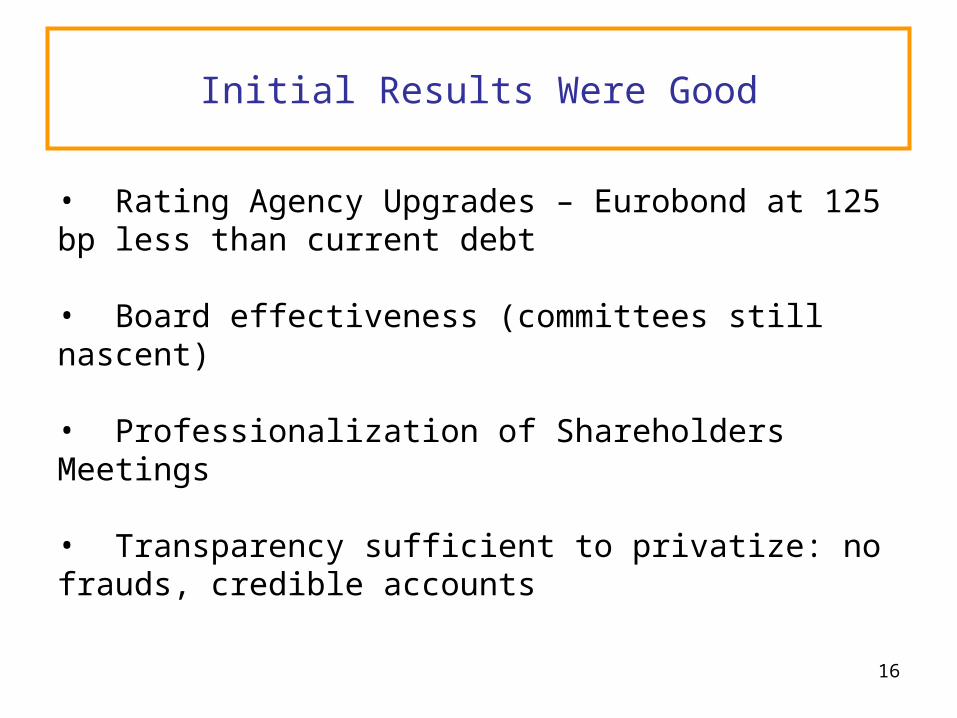

• Rating Agency Upgrades – Eurobond at 125 bp less than current debt

• Board effectiveness (committees still nascent)

• Professionalization of Shareholders Meetings

• Transparency sufficient to privatize: no frauds, credible accounts

17

Full Sale with Spectacular Results

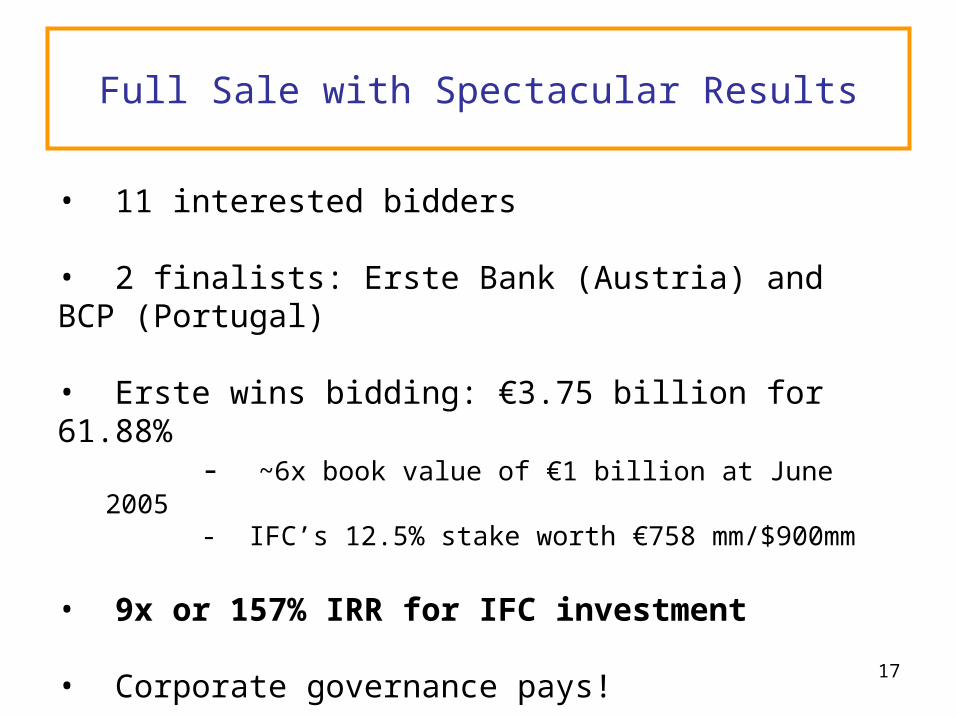

• 11 interested bidders • 2 finalists: Erste Bank (Austria) and BCP (Portugal) • Erste wins bidding: €3.75 billion for 61.88%

- ~6x book value of €1 billion at June 2005- IFC’s 12.5% stake worth €758 mm/$900mm

• 9x or 157% IRR for IFC investment

• Corporate governance pays!

18

Find companies with mediocre or worse governance. Fix it or introduce it.

Deal Sourcing > Agreeing on Solution > Fixing Issues > Publicizing Results

Sale on Public Market or to Investor Who Cares

So What Can PE Firms Do Tomorrow?

19

Progression MatricesLEVELS

AT

TR

IBU

TE

S

PROGRESSION

1. Acceptable 2. Better 3. Desirable 4. Best Practice

Commitment to Good Corporate Governance

Structure and Functioning of the Board of Directors

Treatment of Minority Shareholders

Internal Controls

Transparency and Disclosure

See: www.ifc.org/corporategovernance

How to Judge an Investee’s Current Position

20

Common Issues to Resolve

1. Loose distinctions among roles of Shareholders > Directors > Management

To Do:• Terms of reference for the Board and Board

Committees (which Committees?)• Revamp Articles re oversight of shareholders

vs. Board, e.g., capital expenditures, new strategies

• Performance contract with management and clear evaluation criteria (could cover: strategy execution, financial and non-financial targets, internal controls, compliance, HR policies and hiring/firing)

21

Common Issues to Resolve (cont.)

2. Entrenched or Suboptimal Board (wrong mix, not global enough, asleep, dictatorial)

To Do:• Institute one-year terms (tricky if all expect to be re-elected), non-preferred is term limits• Institute Board self-assessment (a) of the whole Board and (b) of each other as members• Board retreat with facilitator: purpose, mix of skills, need for new skills, ask for resignations• Infosys bomb: rank 1 to 10

22

Common Issues to Resolve (cont.)

Questions/Issues on Board Revamping• Does alienating current Directors by asking for

resignation jeopardize the company’s local position?

• Can the new investment be used as excuse to let the redundant go?

• How to attract experts, e.g., risk expert for a bank?

• Lots of talent available on marketing, less on control, risk and global expansion

• Decide on Board for interim versus long-term or public company board

23

Common Issues to Resolve (cont.)

• Get Board for the Interim:– Includes the PE partners– May want to search for key expert for new strategy both

for expertise and to signal to market embrace of professionalism (e.g., logistics, branding, branch expansion, auditing)

• Create Board for the sale or IPO– Prepare for PE partners to step down– No shareholders’ representatives as all members

represent shareholders– Get mix of skills, experience, gender, and credibility in

the market of the sale

24

Common Issues to Resolve (cont.)

3. In public companies, non-transparency• Korea, shareholders’ suit for accurate list of

beneficial owners• Mechanisms against self-dealing, tunneling, theft

of business opportunity• Financial and non-financial disclosure to analysts

and shareholders (also execution push for this tack)

25

Common Issues to Resolve (cont.)

4. Weak Internal Controls• Already classic for PE to appoint CFO• Get management commitment to have internal

audit reporting to Board Committee• Set up a compliance function with independence

and mechanisms for whistleblowers, redress, reporting to Board, etc.

26

Common Issues to Resolve (cont.)

5. Dominance of controlling shareholders invites theft or fiduciary lapses

• Consider one-share, one-vote• Change Articles to require shareholder approval

of related party transactions, entry of controllers into related businesses, consolidated reporting of controller’s holdings

• Institute formal procurement policies and reporting on it

• Revise the “change of control” provisions to share the premium

• Introduce cumulative voting (many PE managers hate this while they are in the deal)

27

Common Issues to Resolve (cont.)

6. Cleaning up an ethical mess– Create a Code of Conduct or Code of Ethics– Use as distinguishing factor as well as risk mitigation

and simply right thing to do– Code should be simple, compliance mechanisms can

be complex. Compliance procedures should be clearly stated on the website document.

– All sign, including Directors– Code covers values such as customer (or shareholder)

first + lying, cheating, stealing, bribery, money laundering + compliance with systems and procedures and laws

– Board needs to ask about compliance and receive data

28

Common Issues to Resolve (cont.)

7. Professionalization of family-owned companies• Agreed goal: listing, trade sale. Keep control or

not.• Succession planning and inheritance of shares• Professional HR policies re family members• Cleaning up family holdings: Family Constitution

or Family Protocol

29

Where you stand (may) depend on where you sit.

CG Element

Minority S/H Majority S/H IPO/Listed

Shareholder Rights

•Cumulative voting•One share, one vote

•Liquidation pref•Change of control premium to all

•No cumulative voting•Controlling shares (A+B)•No preferences•Change of control premium to controller

•Cumulative voting•One share, one vote

•Liquidation pref•Change of control premium to all

Board •Representation proportional to shares•Separate CEO/Chair

•Disproportional seats to controller•Same CEO/Chair

•No representation, all professionals•Separate CEO/Chair

Internal Controls

Strong anti-self dealing

Weak on self-dealing Strong anti-self dealing

Disclosure Full As little as possible Full

30

Good luck on the exit multiples!

Portfoliocompanyat investment

Portfolio company with good CG

Corporate

Governance

Value

Addition

31

One Last Request . . .

We are studying the local policy impediments and expedients to private equity and to venture capital.

If you know of examples of policies (tax, company registration, subsidies, pension restrictions, distribution requirements, etc) in a country, please contact me or

Clemente del Valle at [email protected].

![Private Equity in the Development World · 3This section is based in part on Carter, Barger, and Kuczynski [1996] and Sagari and Guidotti [1992]. 4According to the World Bank, developing](https://img.pdfslide.net/doc/110x75/5f42ff548419c61bda460cde/private-equity-in-the-development-3this-section-is-based-in-part-on-carter-barger.jpg)