Embed Size (px)

Citation preview

1

Credit and Debt ManagementCredit and Debt Management Including Using the Equity in Your HomeIncluding Using the Equity in Your Home

2

Agenda

Understanding Your Credit and Your Credit Score

Managing Your Debt

Debt Relief Solutions - Putting Your Home Equity to Work

3

Understanding Your Credit Understanding Your Credit

and Your Credit Scoreand Your Credit Score

4

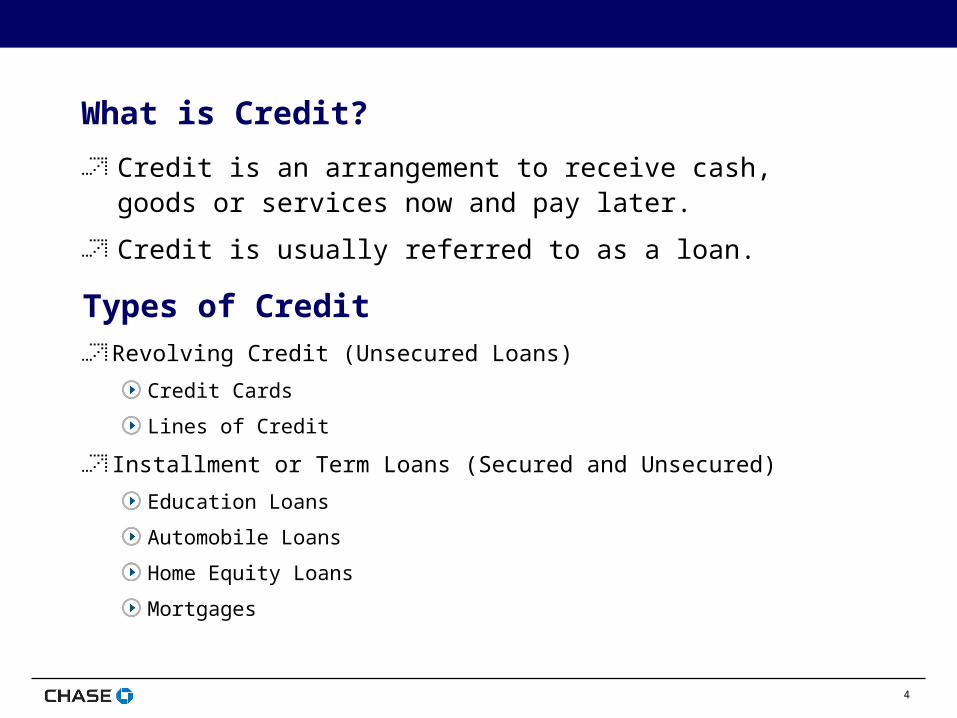

What is Credit?

Credit is an arrangement to receive cash, goods or services now and pay later.

Credit is usually referred to as a loan.

Types of Credit

Revolving Credit (Unsecured Loans)

Credit Cards

Lines of Credit

Installment or Term Loans (Secured and Unsecured)

Education Loans

Automobile Loans

Home Equity Loans

Mortgages

5

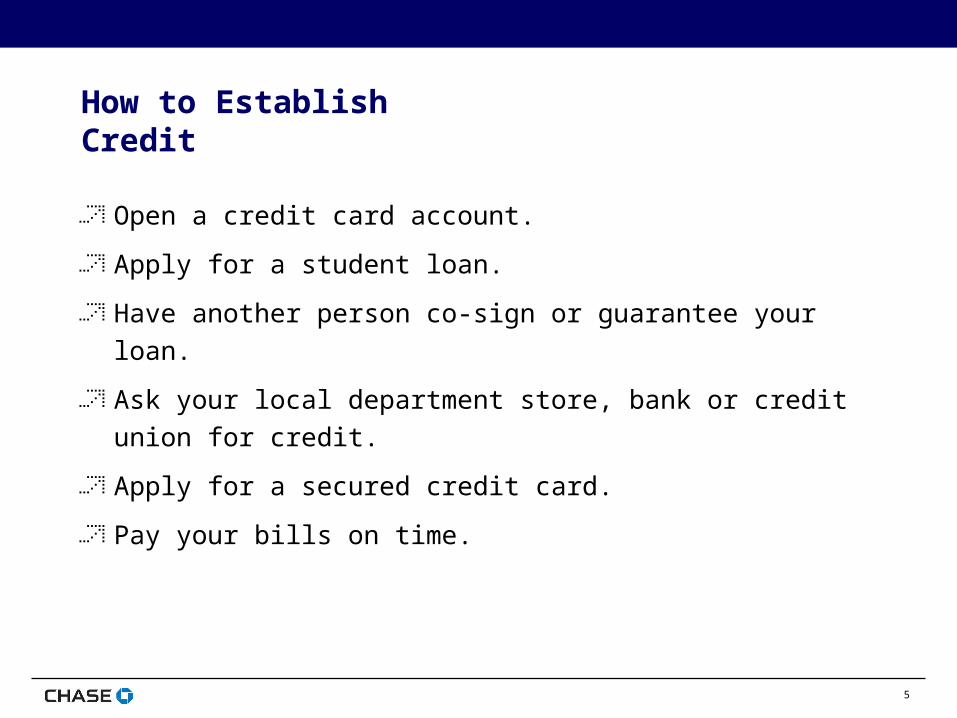

How to Establish Credit

Open a credit card account.

Apply for a student loan.

Have another person co-sign or guarantee your loan.

Ask your local department store, bank or credit union for credit.

Apply for a secured credit card.

Pay your bills on time.

6

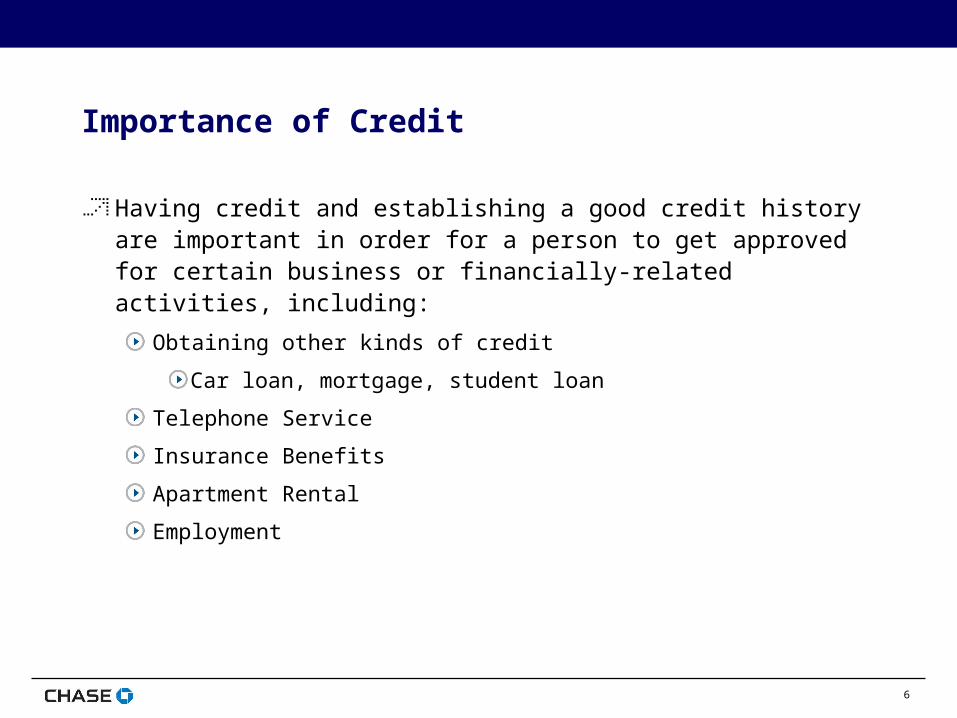

Importance of Credit

Having credit and establishing a good credit history are important in order for a person to get approved for certain business or financially-related activities, including:

Obtaining other kinds of credit

Car loan, mortgage, student loan

Telephone Service

Insurance Benefits

Apartment Rental

Employment

7

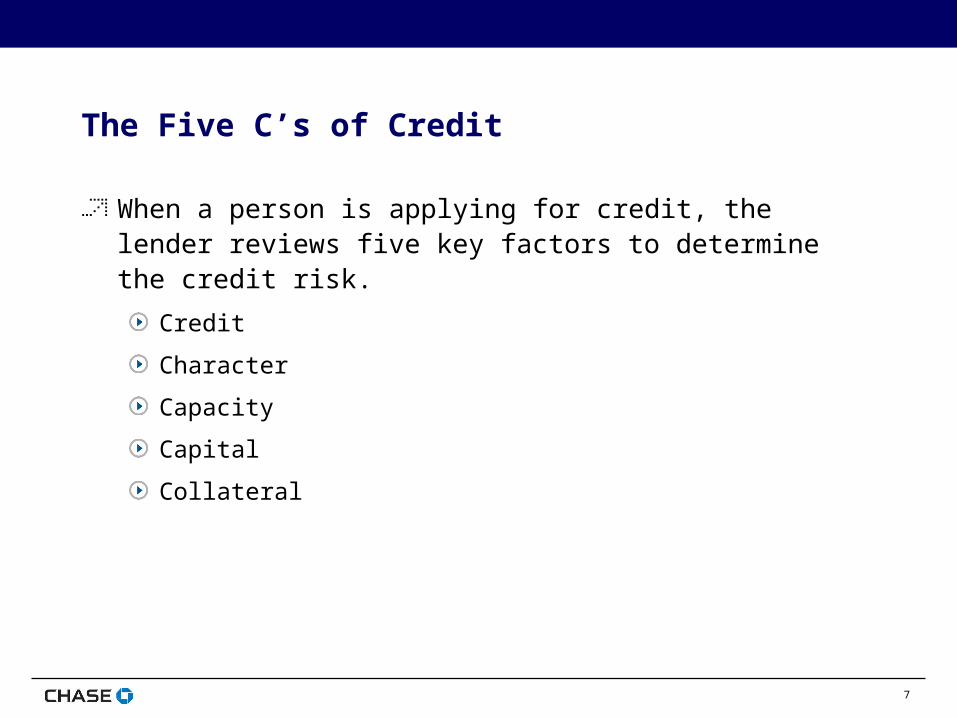

The Five C’s of Credit

When a person is applying for credit, the lender reviews five key factors to determine the credit risk.

Credit

Character

Capacity

Capital

Collateral

8

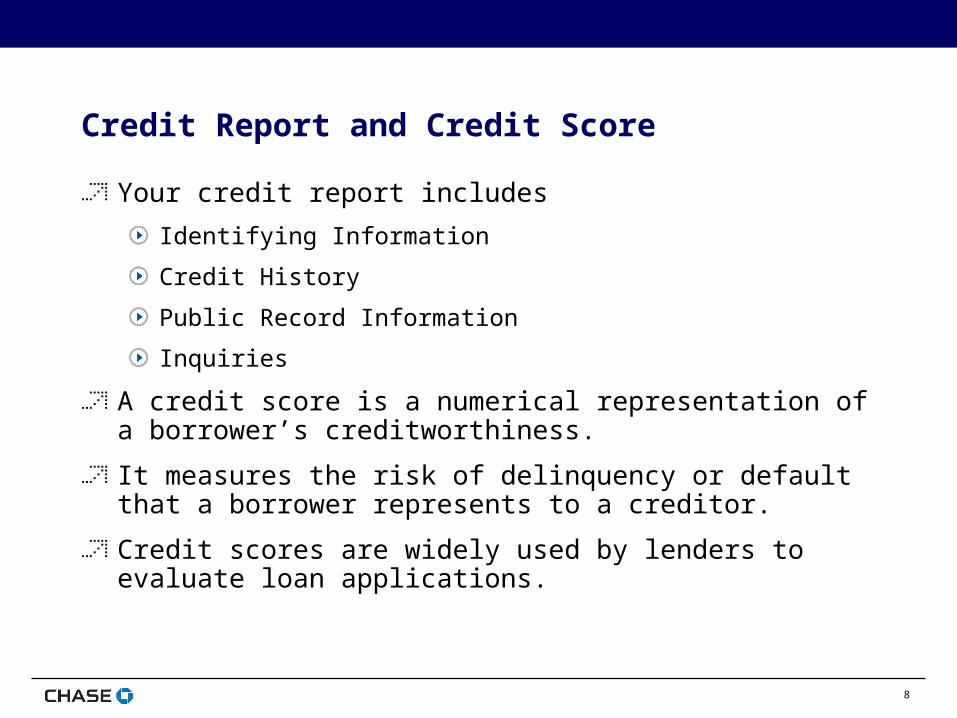

Credit Report and Credit Score

Your credit report includes

Identifying Information

Credit History

Public Record Information

Inquiries

A credit score is a numerical representation of a borrower’s creditworthiness.

It measures the risk of delinquency or default that a borrower represents to a creditor.

Credit scores are widely used by lenders to evaluate loan applications.

9

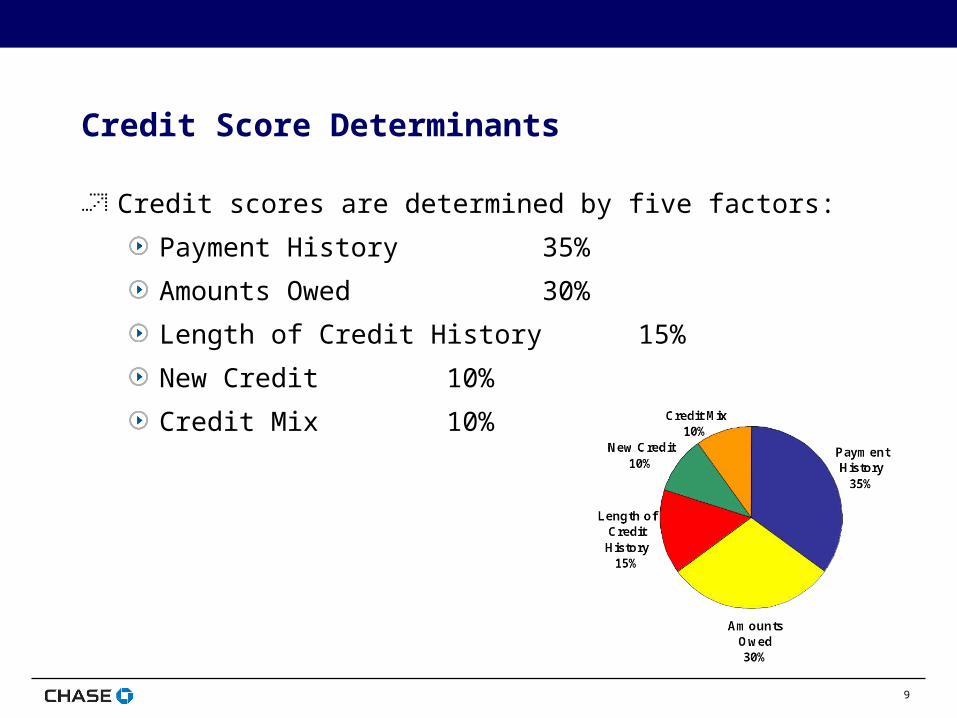

Credit Score Determinants

Credit scores are determined by five factors:

Payment History 35%

Amounts Owed 30%

Length of Credit History 15%

New Credit 10%

Credit Mix 10%

10

Credit Score Rating

Fair Isaac Corporation (FICO) developed the scoring model used by the three credit bureaus.

Equifax

Experian

TransUnion

Credit scores generally range between 300 – 850.

Higher credit scores are considered “better” scores. The higher the credit score, the lower the credit risk.

Scores increase/decrease depending on your credit activities.Each time you make a payment on time, you acquire more points, thus increasing your score.

Each time you make a 30, 60, or 90-day late payment, you lose points, thus decreasing your score.

11

Maintaining Good Credit Scores

Do not needlessly open new revolving accounts.

Do not needlessly fill out credit card applications.

Do not keep your credit cards at or near their maximum limits.

Do use your credit occasionally.

Pay your bills on time.

12

Credit Report Accuracy

It is your responsibility to make sure your credit report is accurate.

Contact the agency if you think there is an error.

If the matter remains unsolved, provide a letter of explanation to the credit agency that becomes part of your credit report.

Review your credit report regularly.

Repairing Your Credit History

To repair credit on your own:

Start by contacting the credit reporting agencies to get a copy of your credit report.

If there are errors on your report, you can contact the credit reporting agency to request an investigation.

13

Free Credit Reports

Once per calendar year, U.S. consumers can obtain one FREE copy of their Credit Report from each of the three Credit Bureaus.

Consumers can order credit reports online or via phone:

Annualcreditreport.com, (877) 322-8228

This is the only site that is really FREE!!!

Equifax, 1-800-525-6285, www.equifax.com

Experian, 1-888-397-3742, www.experian.com

TransUnion, 1-800-680-7289, www.transunion.com

14

Managing Your DebtManaging Your Debt

15

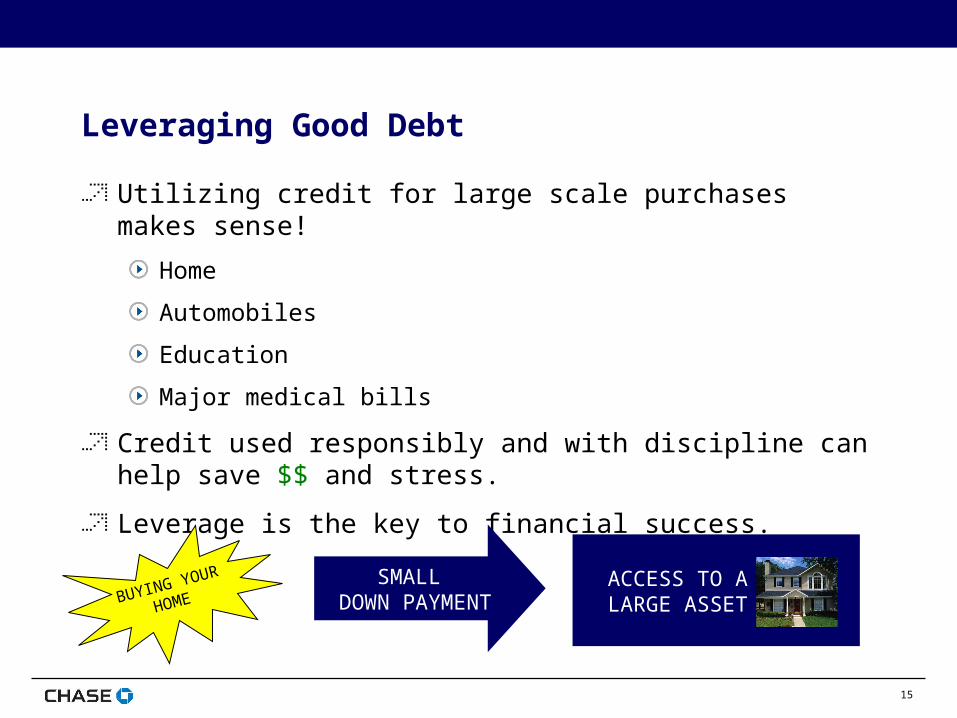

Leveraging Good Debt

Utilizing credit for large scale purchases makes sense!

Home

Automobiles

Education

Major medical bills

Credit used responsibly and with discipline can help save $$ and stress.

Leverage is the key to financial success.

SMALL DOWN PAYMENT

ACCESS TO A LARGE ASSETBUYING YOUR

HOME

16

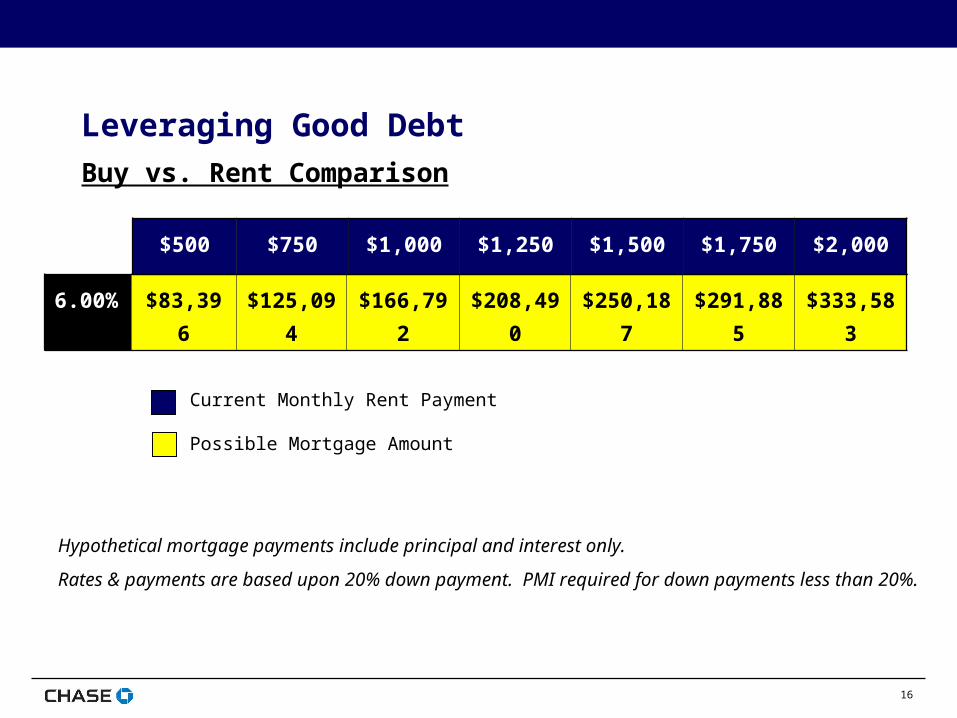

Buy vs. Rent Comparison

6.00% $83,396 $125,094 $166,792 $208,490 $250,187 $291,885 $333,583

$500 $750 $1,000 $1,250 $1,500 $1,750 $2,000

Current Monthly Rent Payment

Hypothetical mortgage payments include principal and interest only.

Rates & payments are based upon 20% down payment. PMI required for down payments less than 20%.

Possible Mortgage Amount

Leveraging Good Debt

17

Debt Becomes A Problem When…..

Too many credit “opportunities”

Acquiring multiple credit lines

Using debt for staple purchases

Lack of budget discipline

Minimum payment syndrome

You are frequently reaching maximum credit limits

You are borrowing to pay current bills

Debt becomes a never-ending cycle Cash Flow Crunch!!

Cash Flow Crunch + Minimum Payment Syndrome = Disaster

18

More Debt Means Less Money for….

Retirement

College expenses

Emergency reserves

Vacations

And so on….

19

Debt Relief SolutionsDebt Relief Solutions

Putting Your Home Equity to Work

20

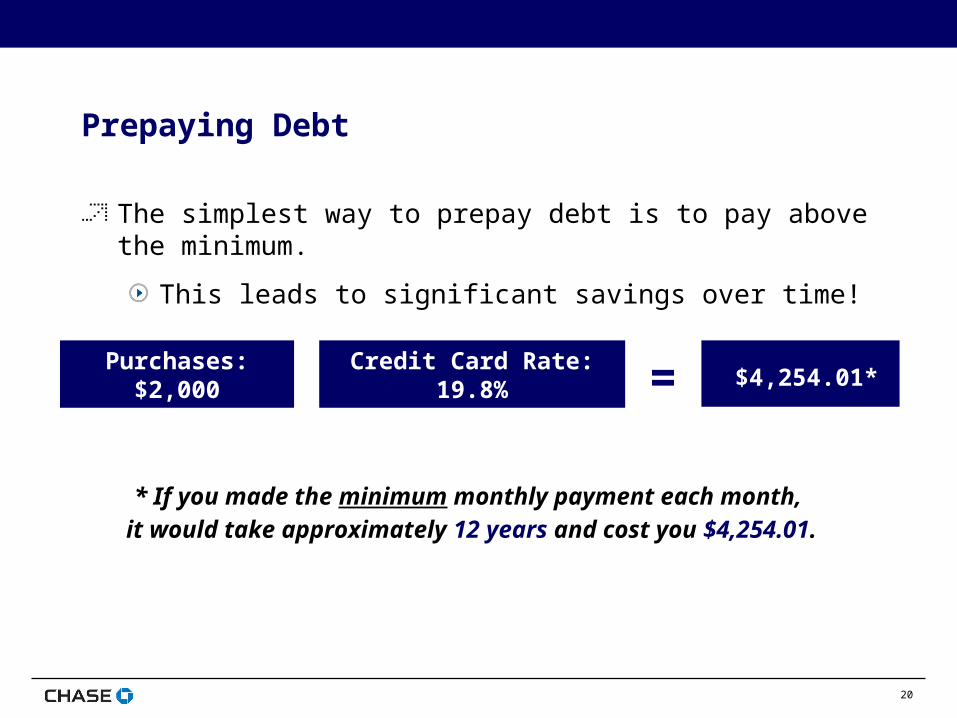

Prepaying Debt

The simplest way to prepay debt is to pay above the minimum.

This leads to significant savings over time!

Purchases:$2,000

Credit Card Rate:19.8% = $4,254.01*

* If you made the minimum monthly payment each month, it would take approximately 12 years and cost you $4,254.01.

21

Developing a Budget

Create a simple general ledger account to track household spending over one or two months.

Re-assess your financial situation.

Debt-to-Income Ratio (DTI) = Monthly Expenses/Monthly Income

Determine where to reduce your expenses.

Discipline is the key to staying on track!

22

If You Do Not Own Your Home, Then….

Get an unsecured consolidation loan.

Consolidate multiple credit cards to one with 0%.

Double your minimum payments to pay off high credit card balances more quickly.

Use a vehicle, boat, etc. to get a secured loan to consolidate your debt.

If you have education financing needs, use education loans, such as Education One Loans.

23

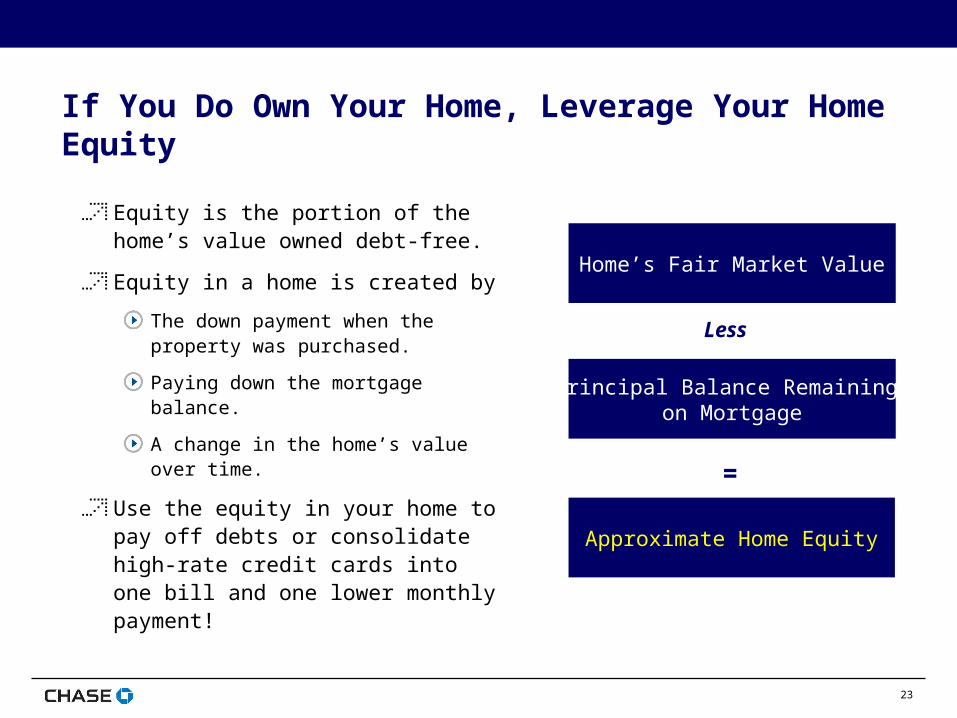

If You Do Own Your Home, Leverage Your Home Equity

Equity is the portion of the home’s value owned debt-free.

Equity in a home is created by

The down payment when the property was purchased.

Paying down the mortgage balance.

A change in the home’s value over time.

Use the equity in your home to pay off debts or consolidate high-rate credit cards into one bill and one lower monthly payment!

Home’s Fair Market Value

Principal Balance Remaining on Mortgage

Approximate Home Equity

=

Less

24

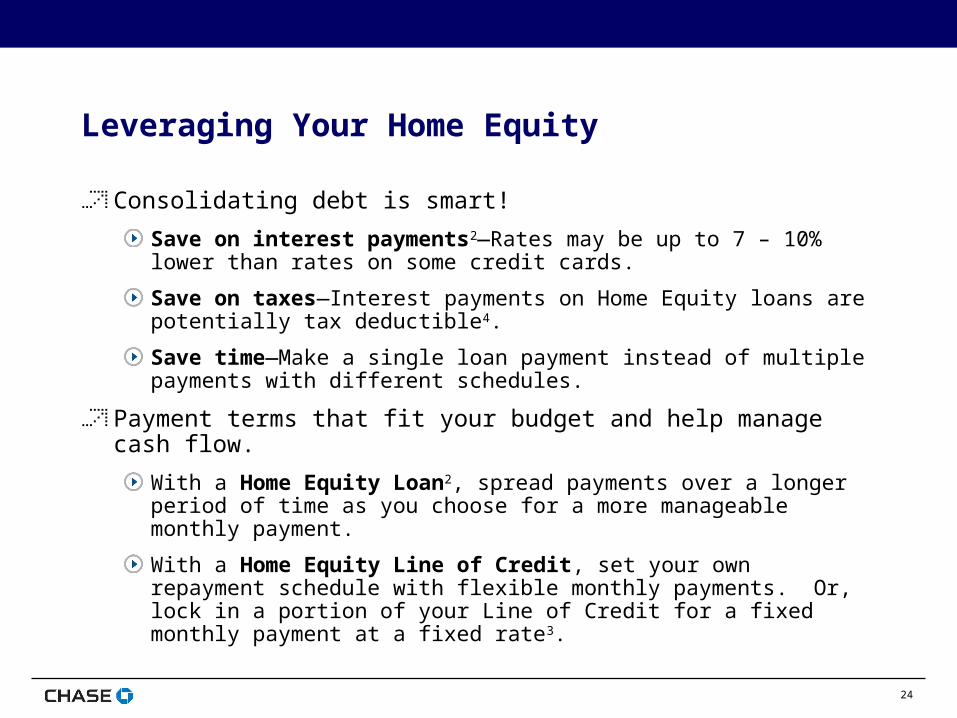

Leveraging Your Home Equity

Consolidating debt is smart!

Save on interest payments2—Rates may be up to 7 – 10% lower than rates on some credit cards.

Save on taxes—Interest payments on Home Equity loans are potentially tax deductible4.

Save time—Make a single loan payment instead of multiple payments with different schedules.

Payment terms that fit your budget and help manage cash flow.

With a Home Equity Loan2, spread payments over a longer period of time as you choose for a more manageable monthly payment.

With a Home Equity Line of Credit, set your own repayment schedule with flexible monthly payments. Or, lock in a portion of your Line of Credit for a fixed monthly payment at a fixed rate3.

25

Leveraging Your Home Equity

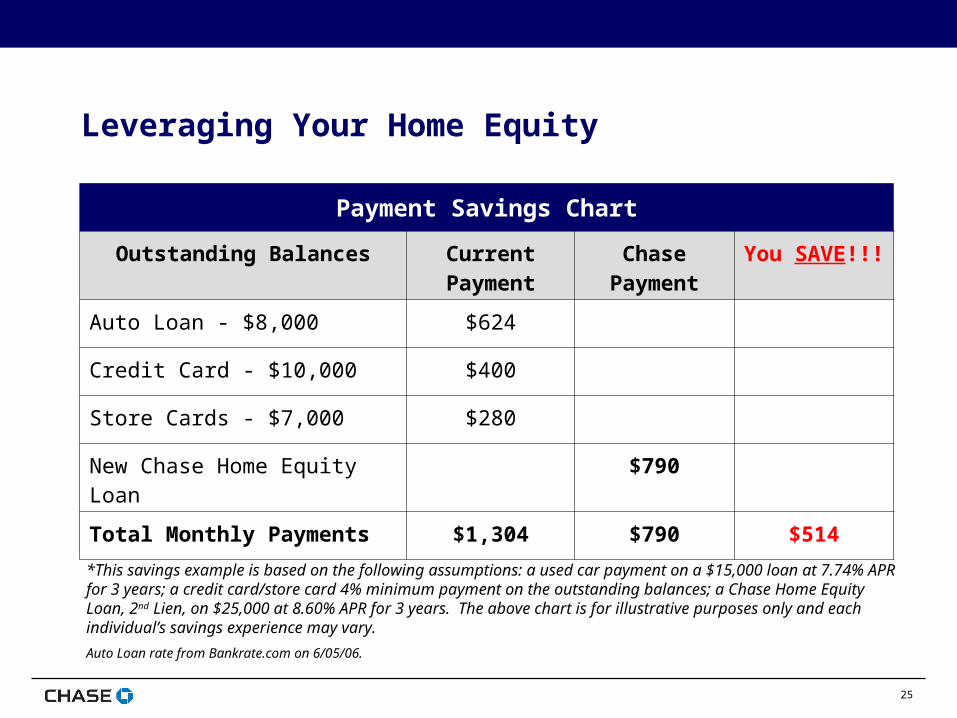

*This savings example is based on the following assumptions: a used car payment on a $15,000 loan at 7.74% APR for 3 years; a credit card/store card 4% minimum payment on the outstanding balances; a Chase Home Equity Loan, 2nd Lien, on $25,000 at 8.60% APR for 3 years. The above chart is for illustrative purposes only and each individual’s savings experience may vary.

Auto Loan rate from Bankrate.com on 6/05/06.

Payment Savings Chart

Outstanding Balances Current Payment

Chase Payment

You SAVE!!!

Auto Loan - $8,000 $624

Credit Card - $10,000 $400

Store Cards - $7,000 $280

New Chase Home Equity Loan $790

Total Monthly Payments $1,304 $790 $514

26

Home Equity Solutions

Home Equity Loan

A fixed rate and payment loan secured by the available equity in your home.

Home Equity Line of Credit

A revolving, variable rate line of credit secured by the available equity in your home.

Payments are based on the outstanding balance owed. As payments are applied to principal, your available credit increases accordingly.

27

Home Equity Solutions

Home Equity products can be used for:

Refinancing

Debt consolidation

Home improvements

College education

Major purchases

Cash access

Vacation

“Safety net” for unexpected events/emergencies

28

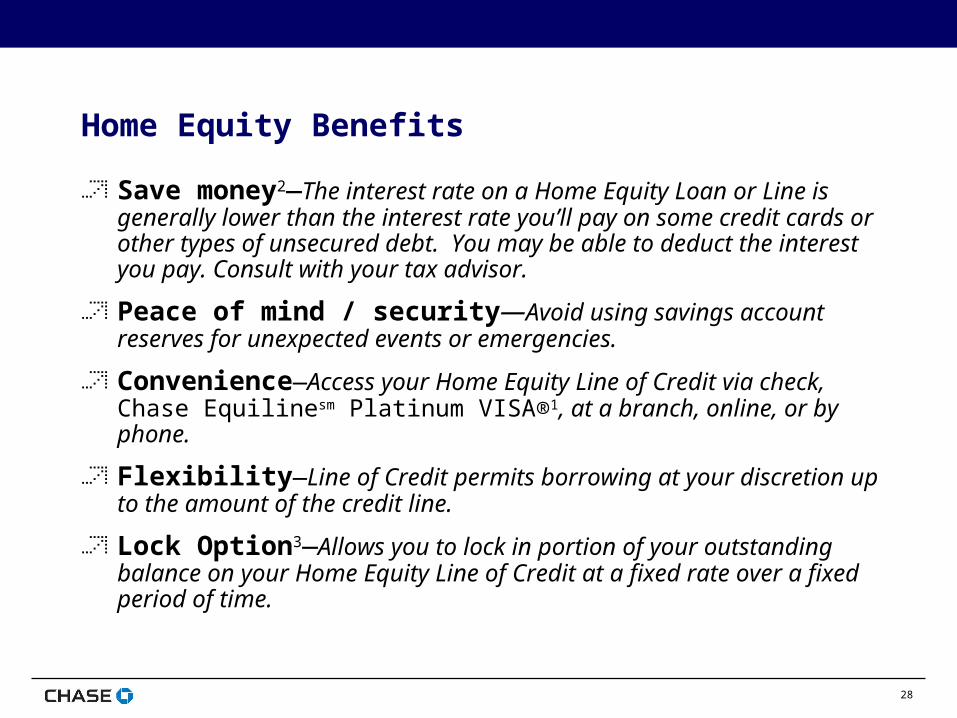

Home Equity Benefits

Save money2—The interest rate on a Home Equity Loan or Line is generally lower than the interest rate you’ll pay on some credit cards or other types of unsecured debt. You may be able to deduct the interest you pay. Consult with your tax advisor.

Peace of mind / security—Avoid using savings account reserves for unexpected events or emergencies.

Convenience—Access your Home Equity Line of Credit via check, Chase Equilinesm Platinum VISA®1, at a branch, online, or by phone.

Flexibility—Line of Credit permits borrowing at your discretion up to the amount of the credit line.

Lock Option3—Allows you to lock in portion of your outstanding balance on your Home Equity Line of Credit at a fixed rate over a fixed period of time.

29

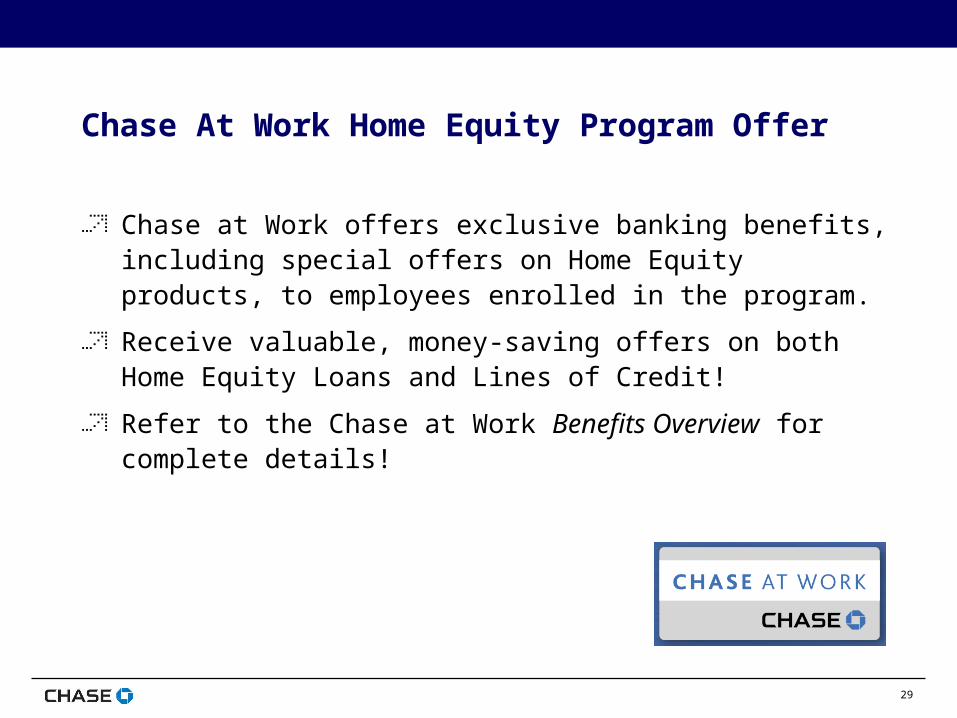

Chase At Work Home Equity Program Offer

Chase at Work offers exclusive banking benefits, including special offers on Home Equity products, to employees enrolled in the program.

Receive valuable, money-saving offers on both Home Equity Loans and Lines of Credit!

Refer to the Chase at Work Benefits Overview for complete details!

30

Disclosures

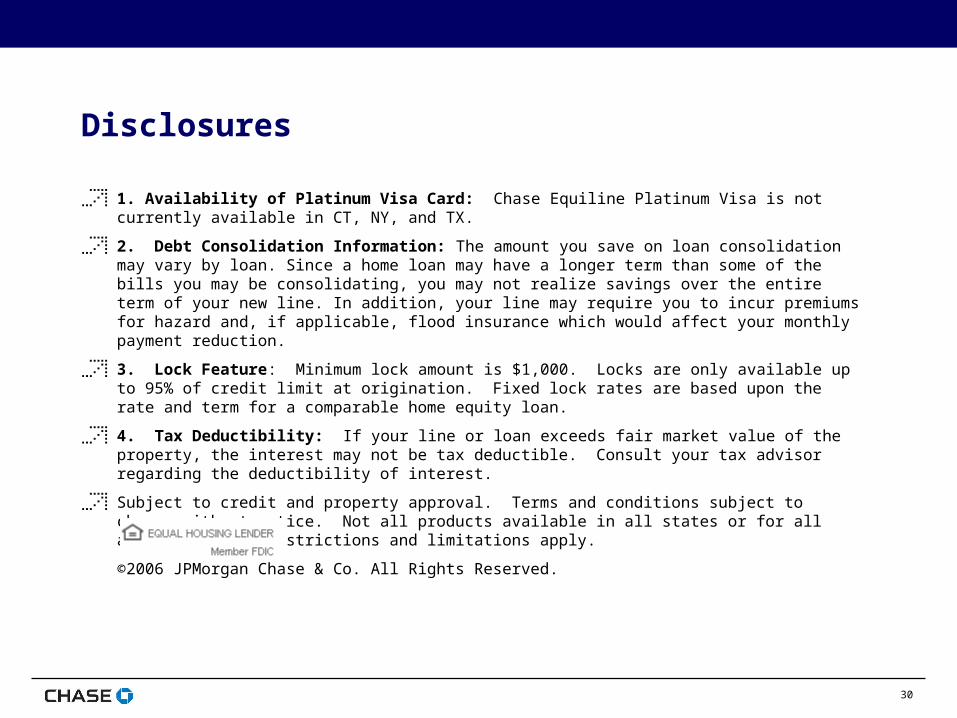

1. Availability of Platinum Visa Card: Chase Equiline Platinum Visa is not currently available in CT, NY, and TX.

2. Debt Consolidation Information: The amount you save on loan consolidation may vary by loan. Since a home loan may have a longer term than some of the bills you may be consolidating, you may not realize savings over the entire term of your new line. In addition, your line may require you to incur premiums for hazard and, if applicable, flood insurance which would affect your monthly payment reduction.

3. Lock Feature: Minimum lock amount is $1,000. Locks are only available up to 95% of credit limit at origination. Fixed lock rates are based upon the rate and term for a comparable home equity loan.

4. Tax Deductibility: If your line or loan exceeds fair market value of the property, the interest may not be tax deductible. Consult your tax advisor regarding the deductibility of interest.

Subject to credit and property approval. Terms and conditions subject to change without notice. Not all products available in all states or for all amounts. Other restrictions and limitations apply.

©2006 JPMorgan Chase & Co. All Rights Reserved.

31

Questions?Questions?