Embed Size (px)

Citation preview

1

Dr. Amelia Baldwin Dr. Amelia Baldwin

ACC 211ACC 211

University of Alabama in HuntsvilleUniversity of Alabama in Huntsville

© Copyright 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star Logo, and

South-Western are trademarks used herein under license.

FINANCIAL ACCOUNTING

2ND EDITION

BY

DUCHAC, REEVE, & WARREN

1Role of Accounting in Business

2

LEARNING GOALS

When you finish this chapter, you should be able to

3

1. Describe types, forms of business; business stakeholders

2. Describe 3 business activities

3. Define accounting, its role

4. Describe, illustrate basic financial statements

LEARNING GOALSLEARNING GOALS

Continued

4

LEARNING GOALSLEARNING GOALS

5. Describe 8 accounting concepts

6. Describe, illustrate horizontal analysis

5

HERSHEY FOODS CORP.

Hershey Foods Corporation

Began in early 1900

A leading candy manufacturer

Produces more than 1 billion pounds of candy each year

6

LEARNING GOALSLEARNING GOALS

1Describe types, forms of business; business stakeholders.

7

What forms do businesses take and how do they differ?

LG 1

8

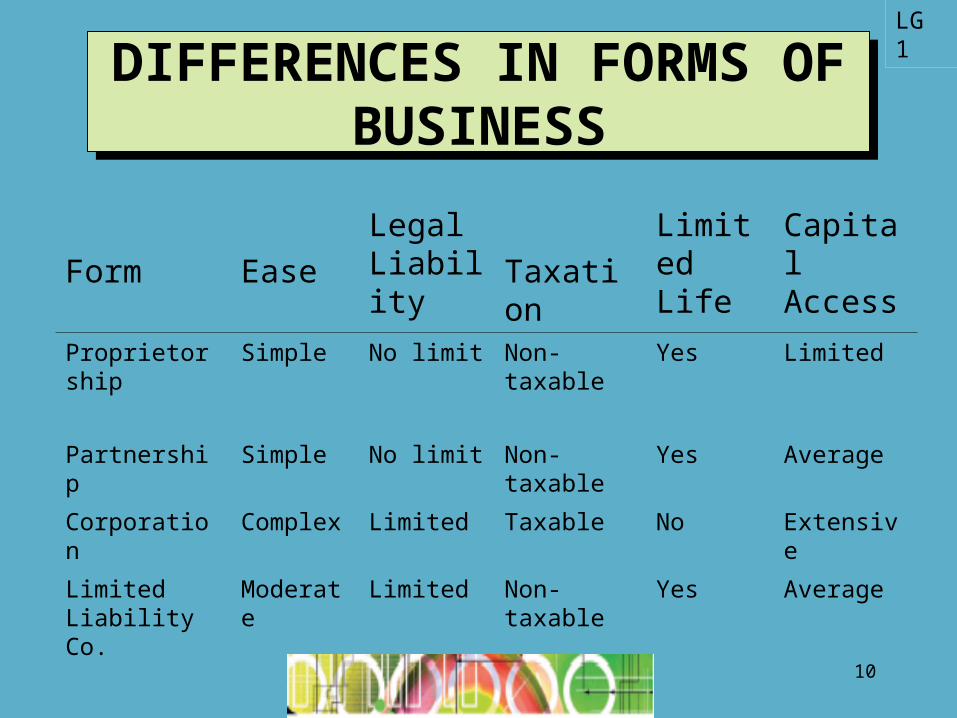

3 forms of business are

•Sole proprietor

•Partnership

•Corporation

•Limited liability corporation

LG 1

3 FORMS OF BUSINESS

9

5 differences are

•Ease of formation

•Legal liability

•Taxation

•Limited life

•Capital access

5 DIFFERENCES

LG 1

10

DIFFERENCES IN FORMS OF BUSINESS

DIFFERENCES IN FORMS OF BUSINESS

Form Ease

Legal Liability Taxation

Limited Life

Capital Access

Proprietorship Simple No limit Non-taxable Yes Limited

Partnership Simple No limit Non-taxable Yes Average

Corporation Complex Limited Taxable No Extensive

Limited Liability Co.

Moderate Limited Non-taxable Yes Average

LG 1

11

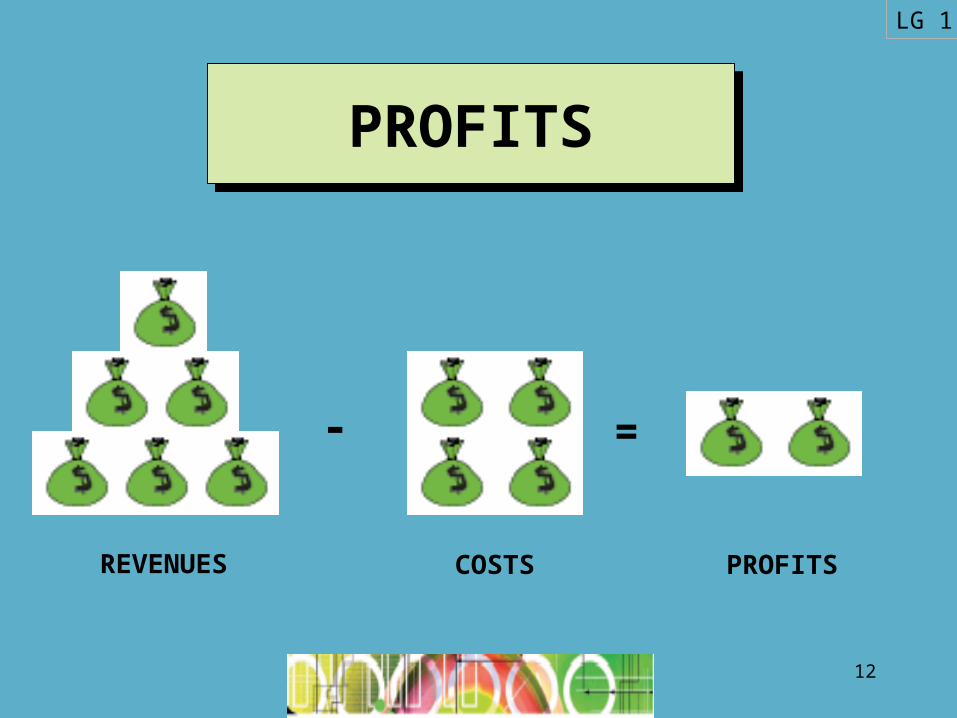

HOW DO BUSINESSES MAKE MONEY?

HOW DO BUSINESSES MAKE MONEY?

• Businesses– Provide goods and services

• Businesses maximize profits– Must gain advantage over competitors

to maximize profits

LG 1

12

PROFITSPROFITS

- =

LG 1

REVENUES COSTS PROFITS

13

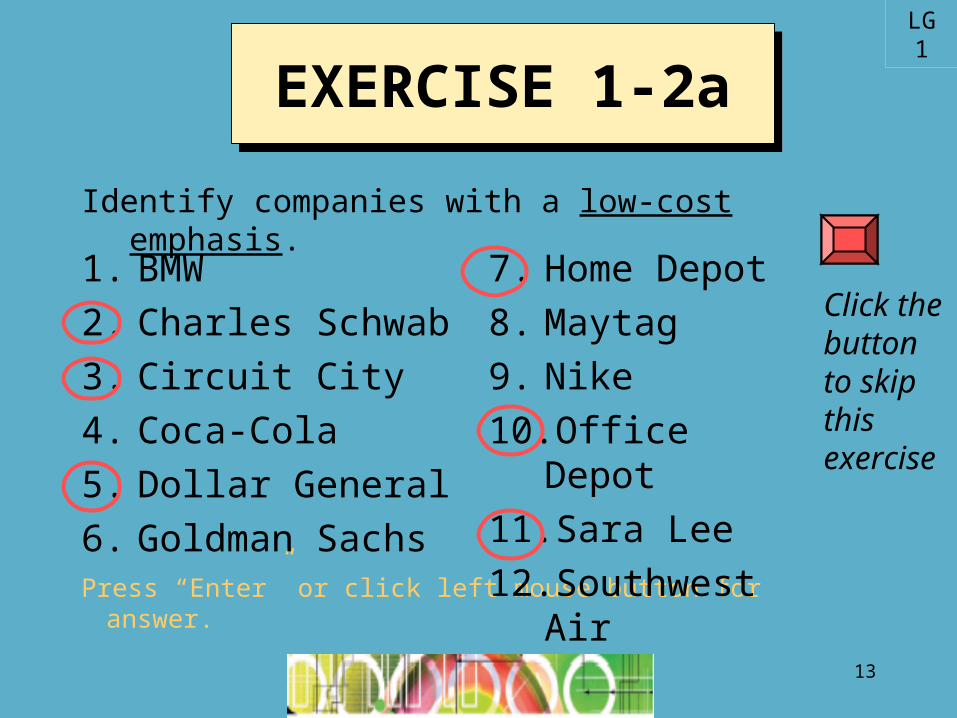

EXERCISE 1-2aEXERCISE 1-2a

Press “Enter” or click left mouse button for answer.

Identify companies with a low-cost emphasis.

1. BMW

2. Charles Schwab

3. Circuit City

4. Coca-Cola

5. Dollar General

6. Goldman Sachs

7. Home Depot

8. Maytag

9. Nike

10. Office Depot

11. Sara Lee

12. Southwest Air

LG 1

Click the button to skip this exercise

14

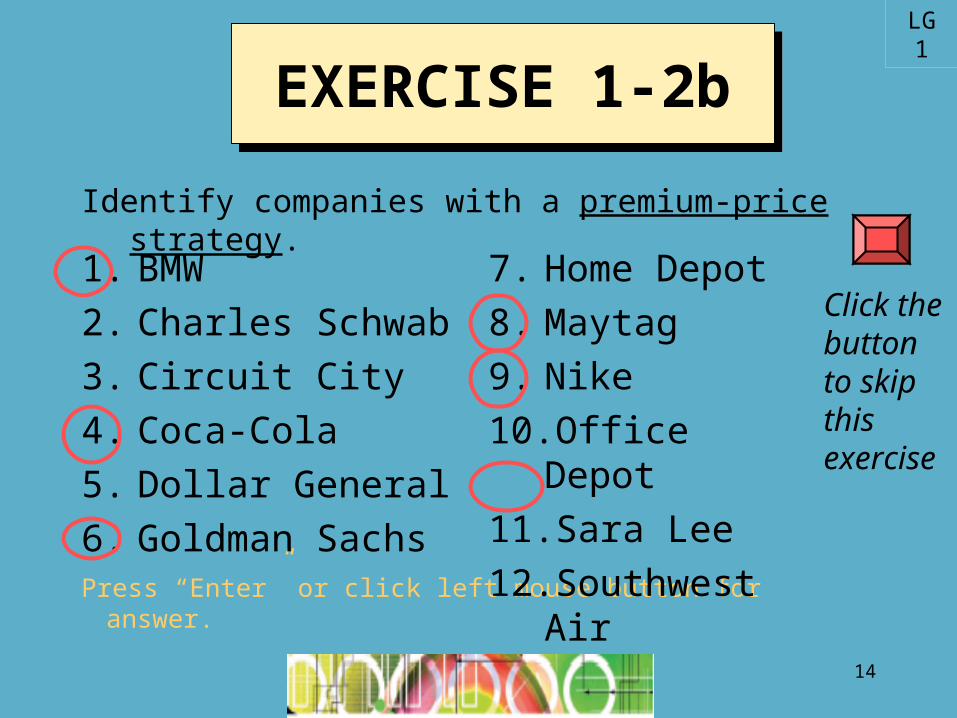

EXERCISE 1-2bEXERCISE 1-2b

Press “Enter” or click left mouse button for answer.

Identify companies with a premium-price strategy.

1. BMW

2. Charles Schwab

3. Circuit City

4. Coca-Cola

5. Dollar General

6. Goldman Sachs

7. Home Depot

8. Maytag

9. Nike

10. Office Depot

11. Sara Lee

12. Southwest Air

LG 1

Click the button to skip this exercise

15

Who are stakeholders and how are they related to the

corporation?

LG 1

16

A business stakeholder is a person or entity that has

an interest in the economic performance and well-

being of a business.

LG 1

17

STAKEHOLDERSSTAKEHOLDERS

Stakeholders areEmployees/Managers

Customers

Suppliers

Bank, owners

Government

Stakeholders areEmployees/Managers

Customers

Suppliers

Bank, owners

Government

LG 1

Continued

18

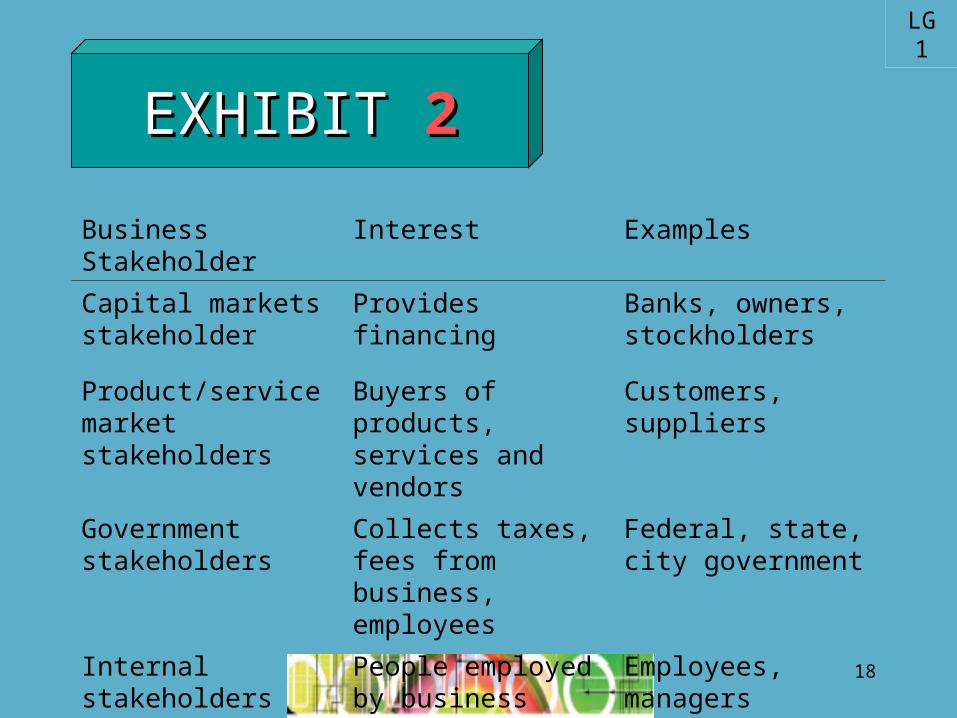

Business Stakeholder Interest Examples

Capital markets stakeholder

Provides financing Banks, owners, stockholders

Product/service market stakeholders

Buyers of products, services and vendors

Customers, suppliers

Government stakeholders

Collects taxes, fees from business, employees

Federal, state, city government

Internal stakeholders People employed by business

Employees, managers

LG 1

EXHIBITEXHIBIT 22

19

LEARNING GOALSLEARNING GOALS

2 Describe 3 business activities.

20

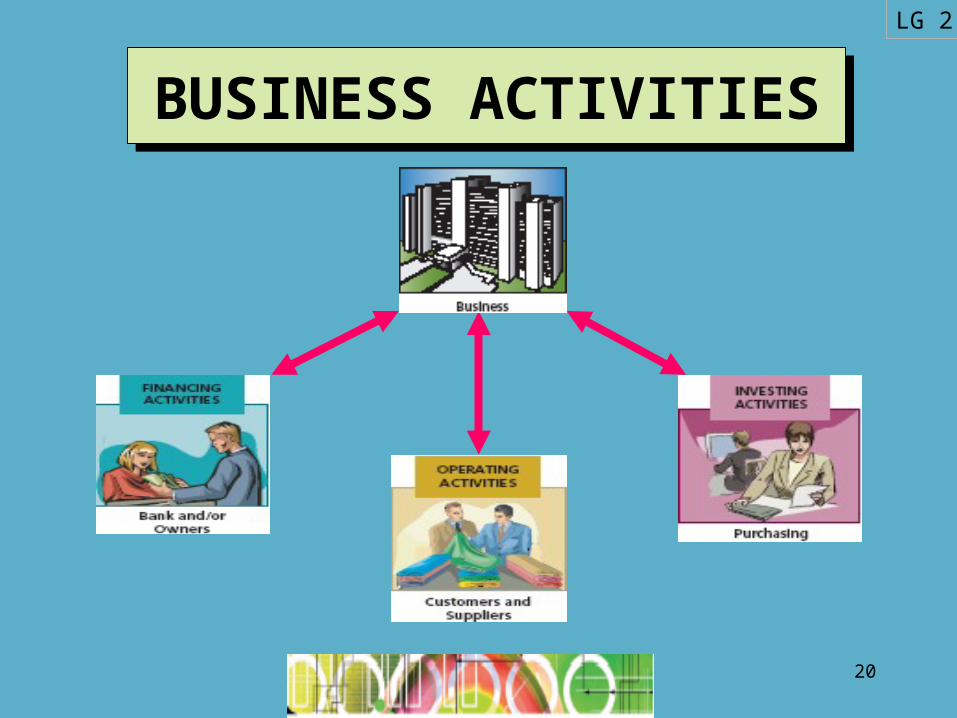

BUSINESS ACTIVITIESBUSINESS ACTIVITIES

LG 2

21

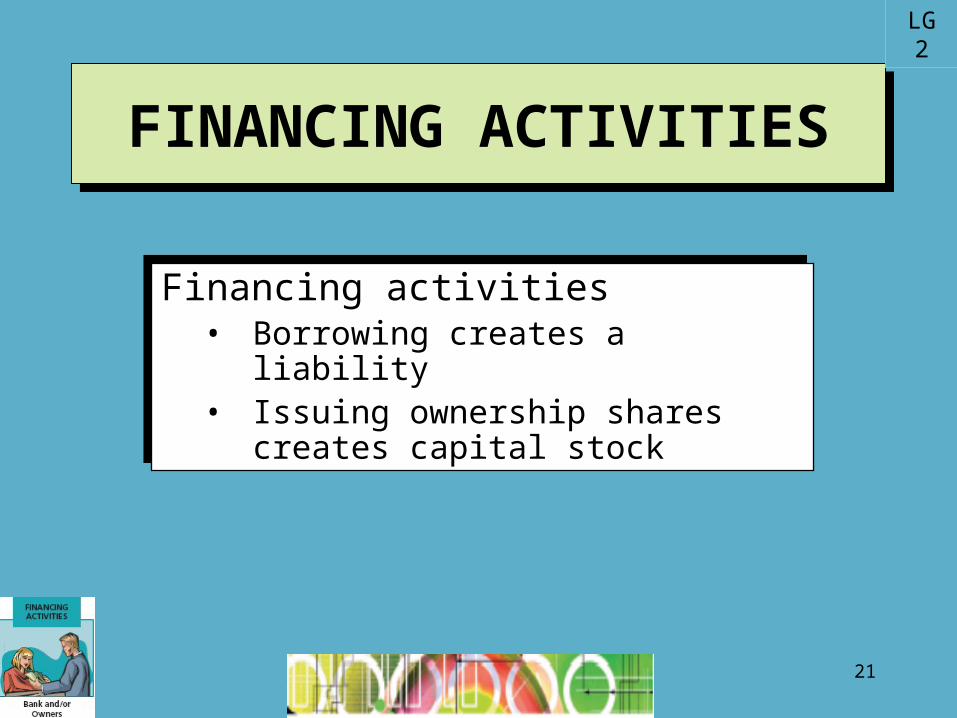

FINANCING ACTIVITIESFINANCING ACTIVITIES

LG 2

Financing activities• Borrowing creates a liability• Issuing ownership shares creates

capital stock

Financing activities• Borrowing creates a liability• Issuing ownership shares creates

capital stock

22

INVESTING ACTIVITIESINVESTING ACTIVITIES

Investing activities• Obtaining assets to operate business

Investing activities• Obtaining assets to operate business

LG 2

23

OPERATING ACTIVITIESOPERATING ACTIVITIES

Operating activities• Offer product, service

Operating activities• Offer product, service

LG 2

24

LEARNING GOALSLEARNING GOALS

3 Define accounting, its role

LG 3

25

ROLE OF ACCOUNTING

LG 3

Accounting is “an Accounting is “an information system that information system that provides reports to provides reports to stakeholders about the stakeholders about the economic activities and economic activities and condition of a business.”condition of a business.”

26

LG 3

EXHIBITEXHIBIT 33

27

LEARNING GOALSLEARNING GOALS

4 Describe, illustrate basic financial statements

LG 4

28

Can you name the four financial statements and their objectives?

LG 4

29

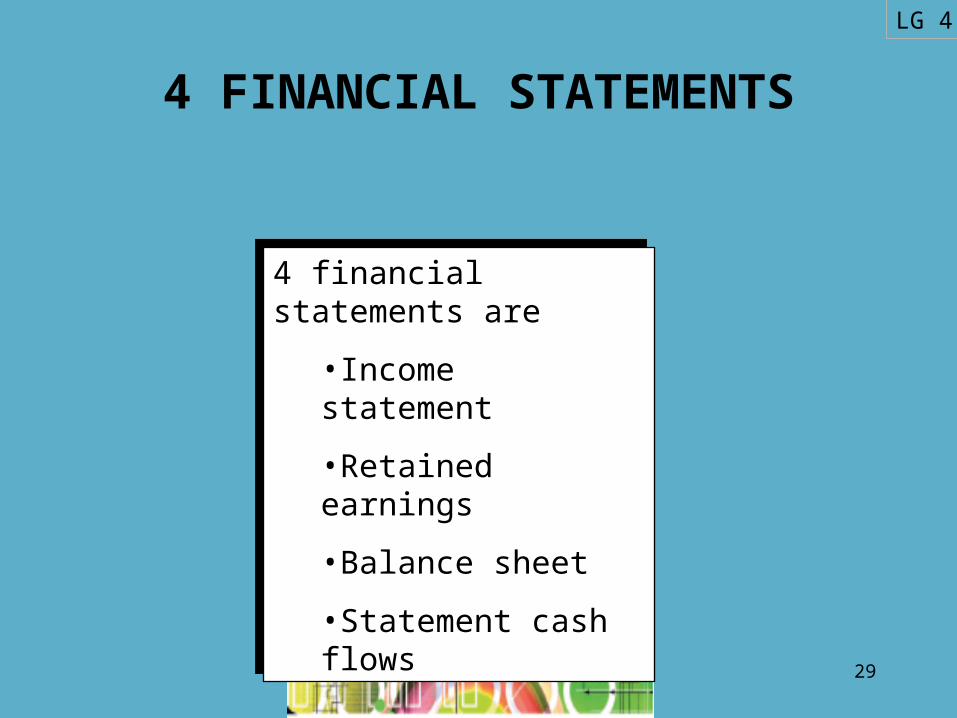

4 financial statements are

•Income statement

•Retained earnings

•Balance sheet

•Statement cash flows

4 financial statements are

•Income statement

•Retained earnings

•Balance sheet

•Statement cash flows

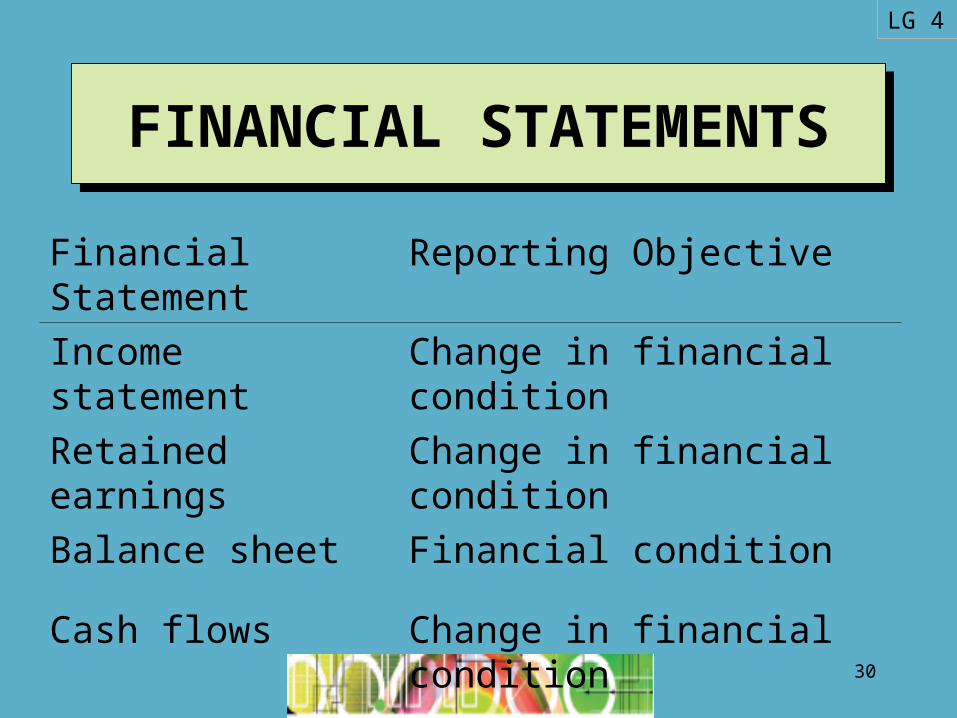

4 FINANCIAL STATEMENTS

LG 4

30

FINANCIAL STATEMENTSFINANCIAL STATEMENTS

Financial Statement Reporting Objective

Income statement Change in financial condition

Retained earnings Change in financial condition

Balance sheet Financial condition

Cash flows Change in financial condition

LG 4

31

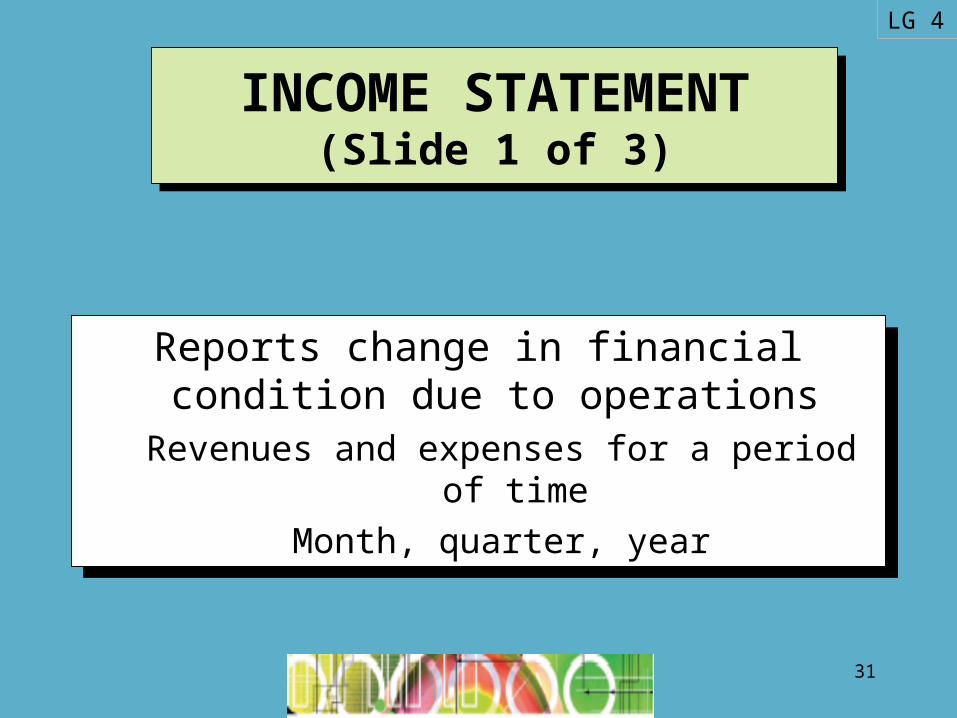

INCOME STATEMENT(Slide 1 of 3)

INCOME STATEMENT(Slide 1 of 3)

Reports change in financial condition due to operations

Revenues and expenses for a period of time

Month, quarter, year

Reports change in financial condition due to operations

Revenues and expenses for a period of time

Month, quarter, year

LG 4

32

INCOME STATEMENT(Slide 2 of 3)

INCOME STATEMENT(Slide 2 of 3)

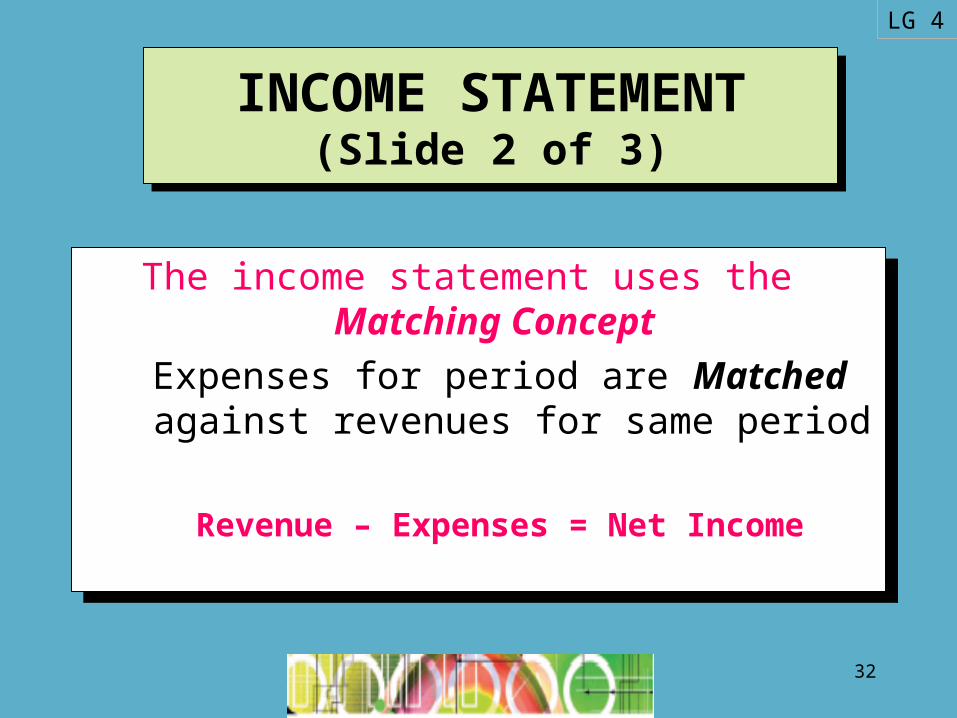

The income statement uses the Matching Concept

Expenses for period are Matched against revenues for same period

Revenue – Expenses = Net Income

The income statement uses the Matching Concept

Expenses for period are Matched against revenues for same period

Revenue – Expenses = Net Income

LG 4

33

LG 4

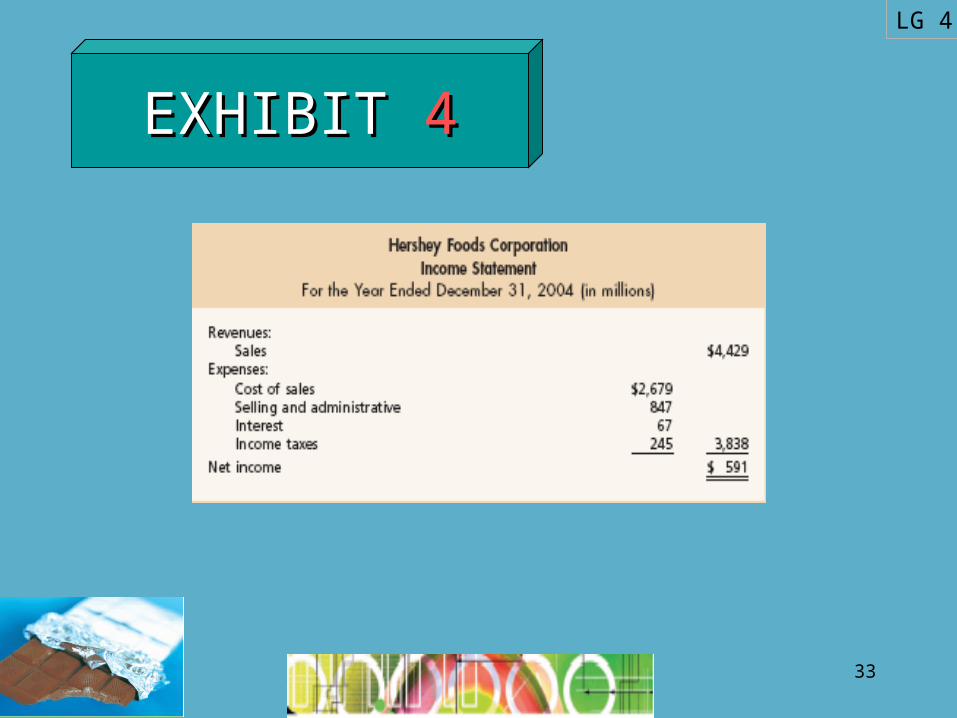

EXHIBIT EXHIBIT 44

34

RETAINED EARNINGS(Slide 1 of 2)

RETAINED EARNINGS(Slide 1 of 2)

Reports changes in financial condition due to changes in retained earnings during a

period.

Retained earnings is the portion of net income retained by the business.

Reports changes in financial condition due to changes in retained earnings during a

period.

Retained earnings is the portion of net income retained by the business.

LG 4

35

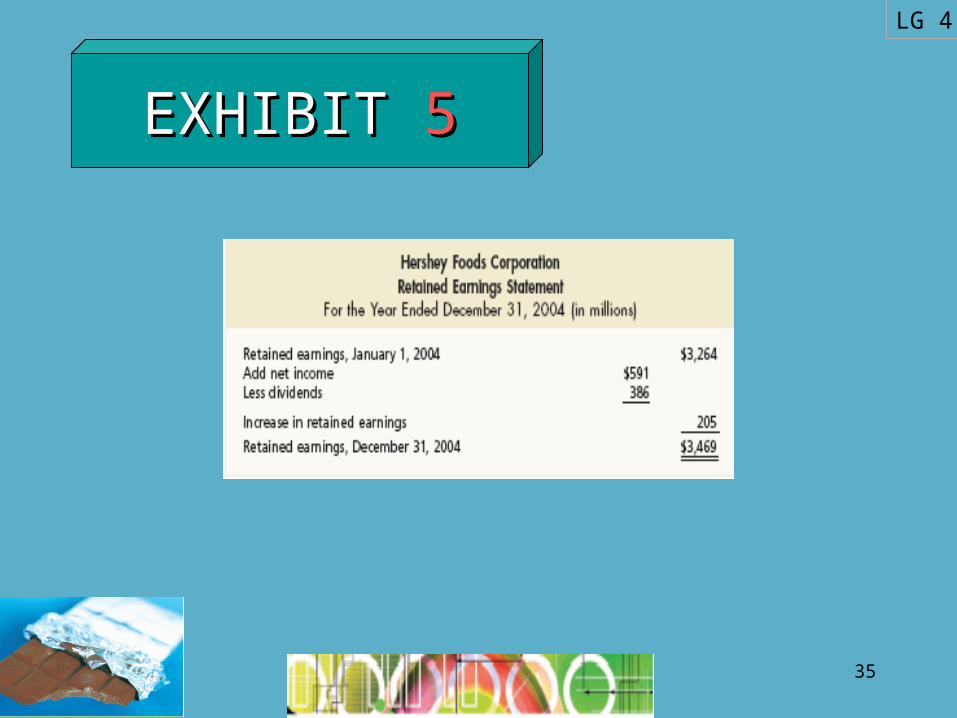

LG 4

EXHIBIT EXHIBIT 55

36

BALANCE SHEET(Slide 1 of 2)

BALANCE SHEET(Slide 1 of 2)

Reports financial condition as of a point in time

Accounting equation

Assets = Liabilities + Stockholders’ Equity

Reports financial condition as of a point in time

Accounting equation

Assets = Liabilities + Stockholders’ Equity

LG 4

37

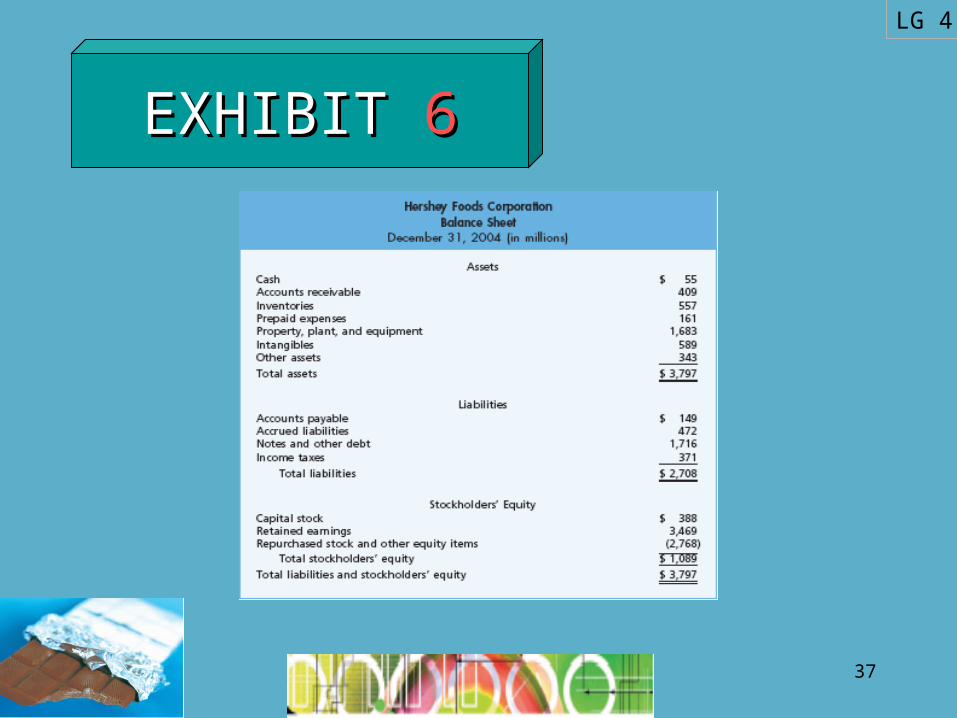

LG 4

EXHIBIT EXHIBIT 66

38

STATEMENT OF CASH FLOWS(Slide 1 of 2)

STATEMENT OF CASH FLOWS(Slide 1 of 2)

Reports change in financial condition from changes in cash during a period that occur due to

a) Cash flows from operating activities

b) Cash flows from investing activities

c) Cash flows from financing activities

Reports change in financial condition from changes in cash during a period that occur due to

a) Cash flows from operating activities

b) Cash flows from investing activities

c) Cash flows from financing activities

LG 4

39

LG 4

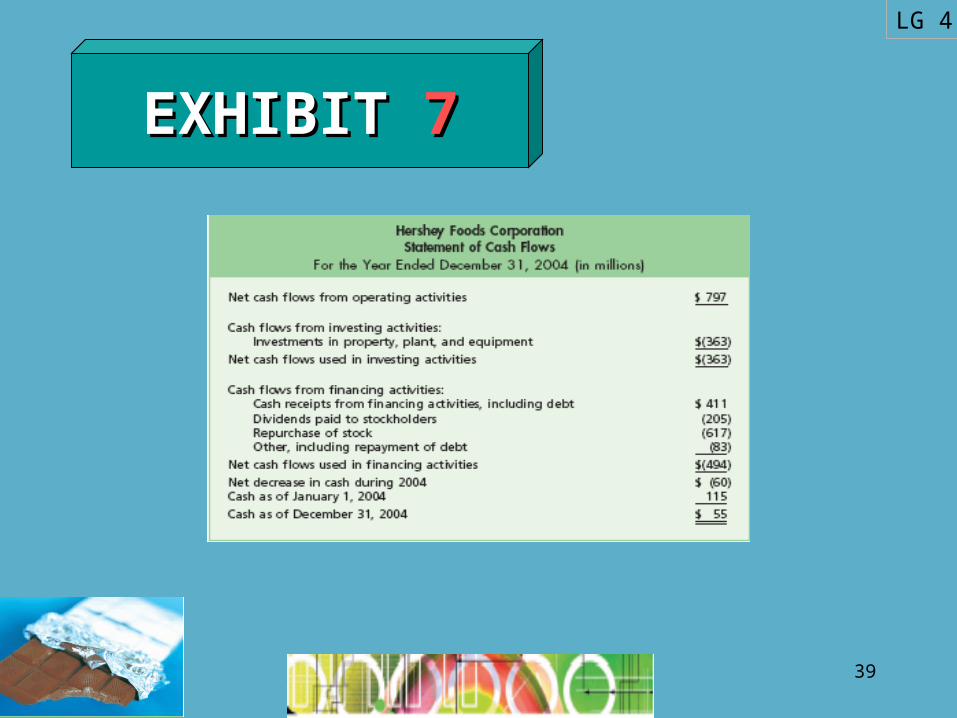

EXHIBIT EXHIBIT 77

40

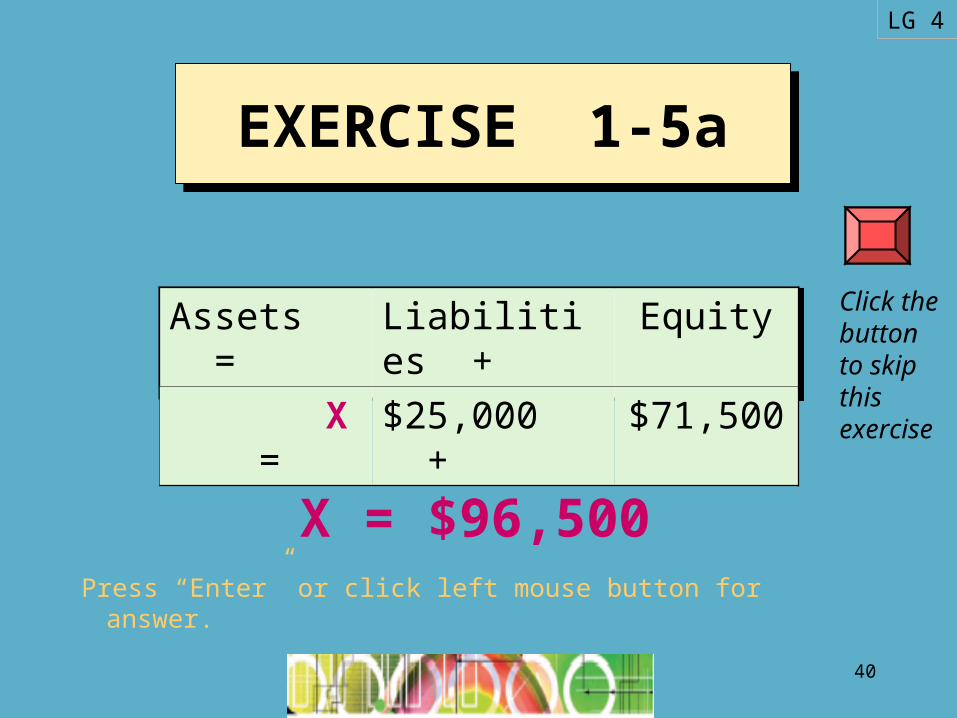

EXERCISE 1-5aEXERCISE 1-5a

Press “Enter” or click left mouse button for answer.

X = $96,500

Assets = Liabilities + Equity

X = $25,000 + $71,500

LG 4

Click the button to skip this exercise

41

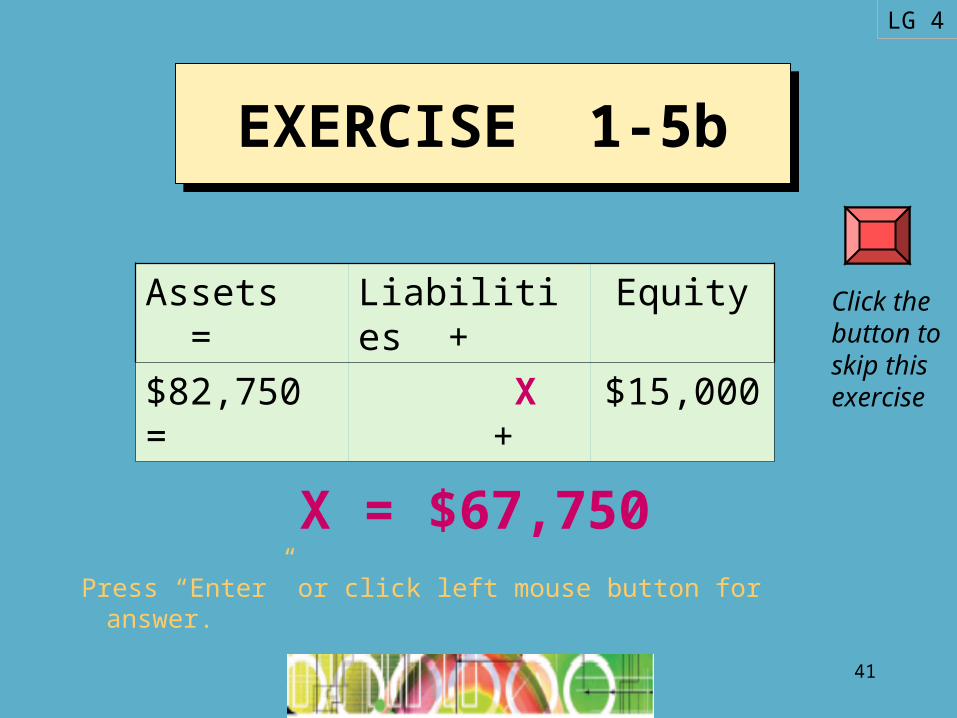

EXERCISE 1-5bEXERCISE 1-5b

Press “Enter” or click left mouse button for answer.

X = $67,750

Assets = Liabilities + Equity

$82,750 = X + $15,000

LG 4

Click the button to skip this exercise

42

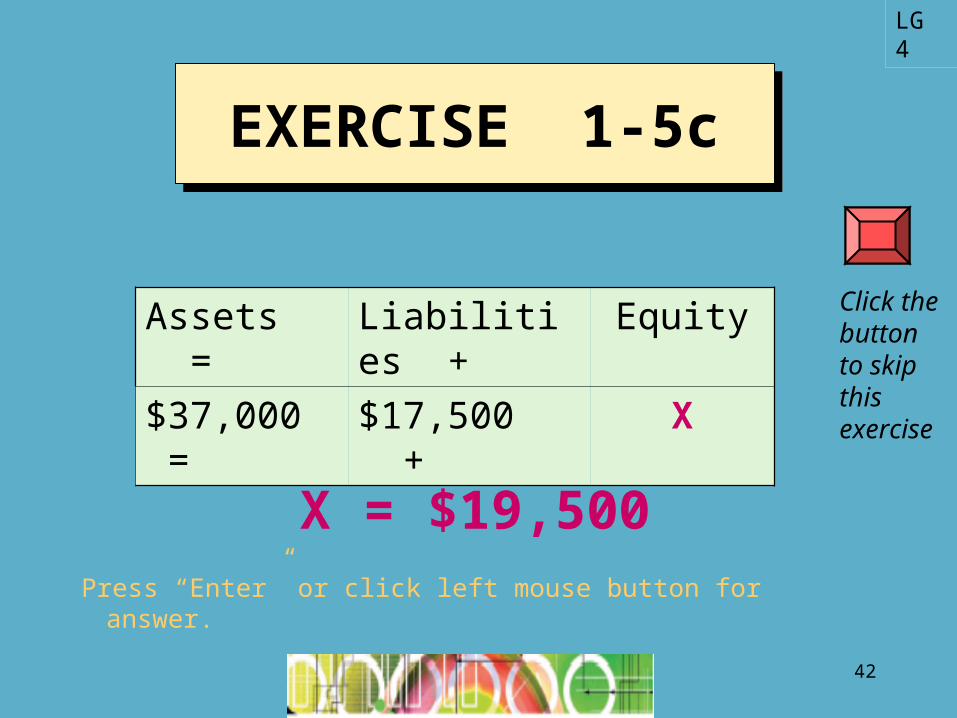

EXERCISE 1-5cEXERCISE 1-5c

Press “Enter” or click left mouse button for answer.

X = $19,500

Assets = Liabilities + Equity

$37,000 = $17,500 + X

LG 4

Click the button to skip this exercise

43

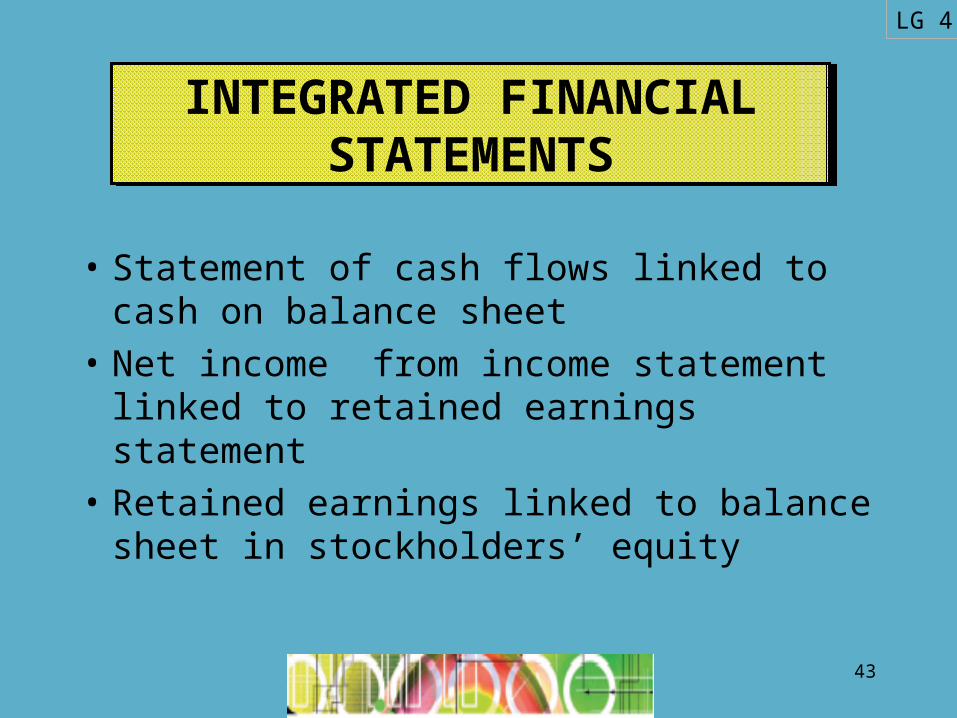

• Statement of cash flows linked to cash on balance sheet

• Net income from income statement linked to retained earnings statement

• Retained earnings linked to balance sheet in stockholders’ equity

INTEGRATED FINANCIAL STATEMENTS

INTEGRATED FINANCIAL STATEMENTS

LG 4

44

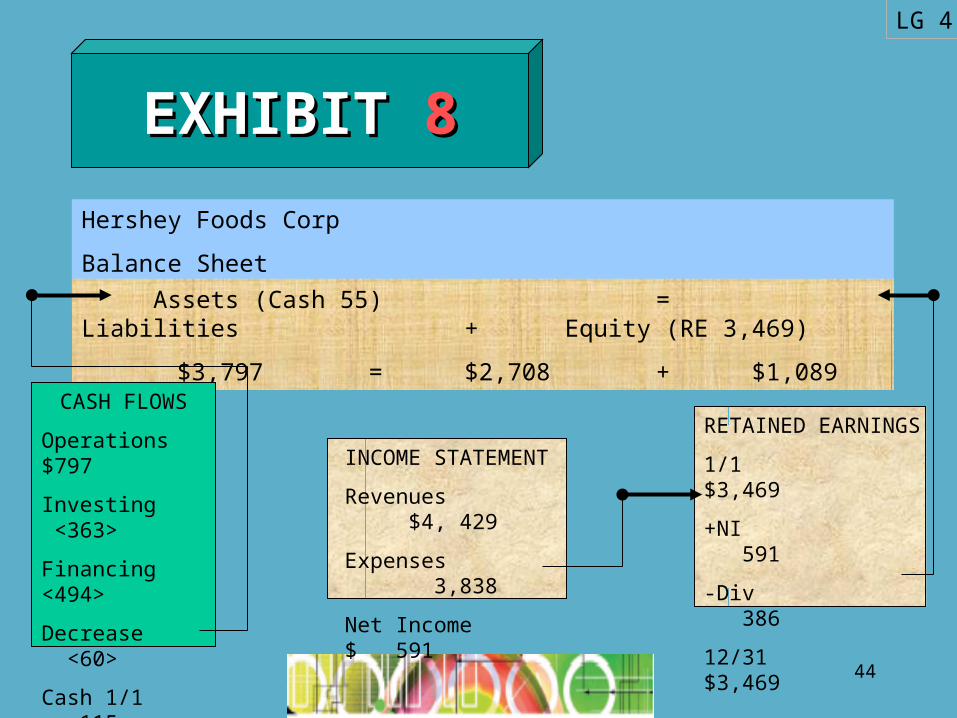

Hershey Foods Corp

Balance Sheet 12/31/2004

Assets (Cash 55) = Liabilities + Equity (RE 3,469)

$3,797 = $2,708 + $1,089

CASH FLOWS

Operations $797

Investing <363>

Financing <494>

Decrease <60>

Cash 1/1 115

Cash 12/31 55

INCOME STATEMENT

Revenues $4, 429

Expenses 3,838

Net Income $ 591

RETAINED EARNINGS

1/1 $3,469

+NI 591

-Div 386

12/31 $3,469

LG 4

EXHIBIT EXHIBIT 88

45

LEARNING GOALSLEARNING GOALS

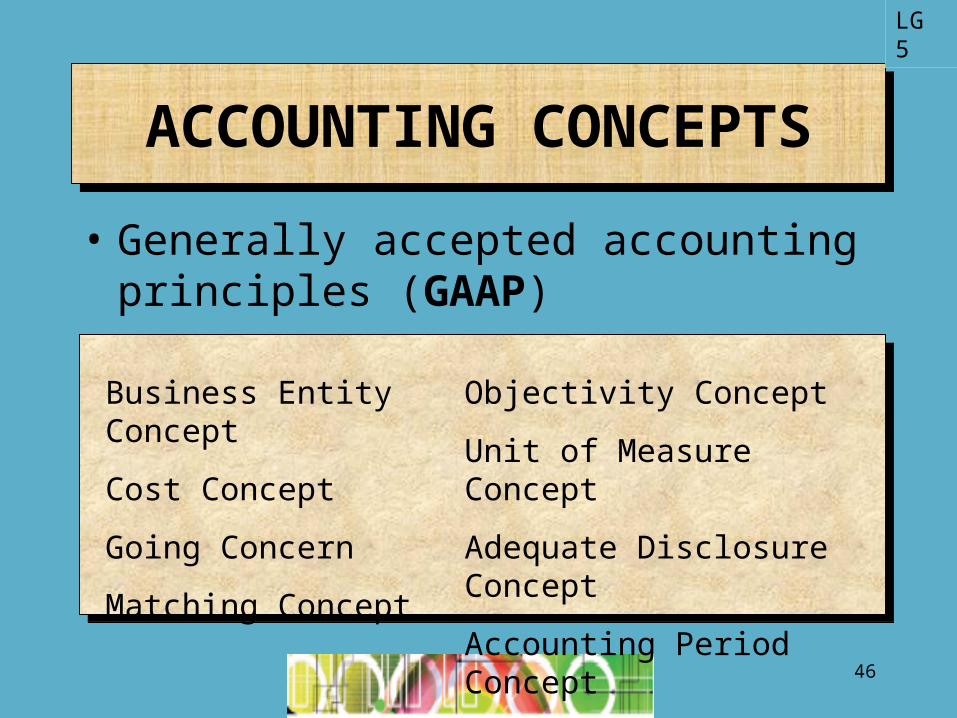

5 Describe 8 accounting concepts

46

ACCOUNTING CONCEPTSACCOUNTING CONCEPTS

• Generally accepted accounting principles (GAAP)

LG 5

Business Entity Concept

Cost Concept

Going Concern

Matching Concept

Objectivity Concept

Unit of Measure Concept

Adequate Disclosure Concept

Accounting Period Concept

47

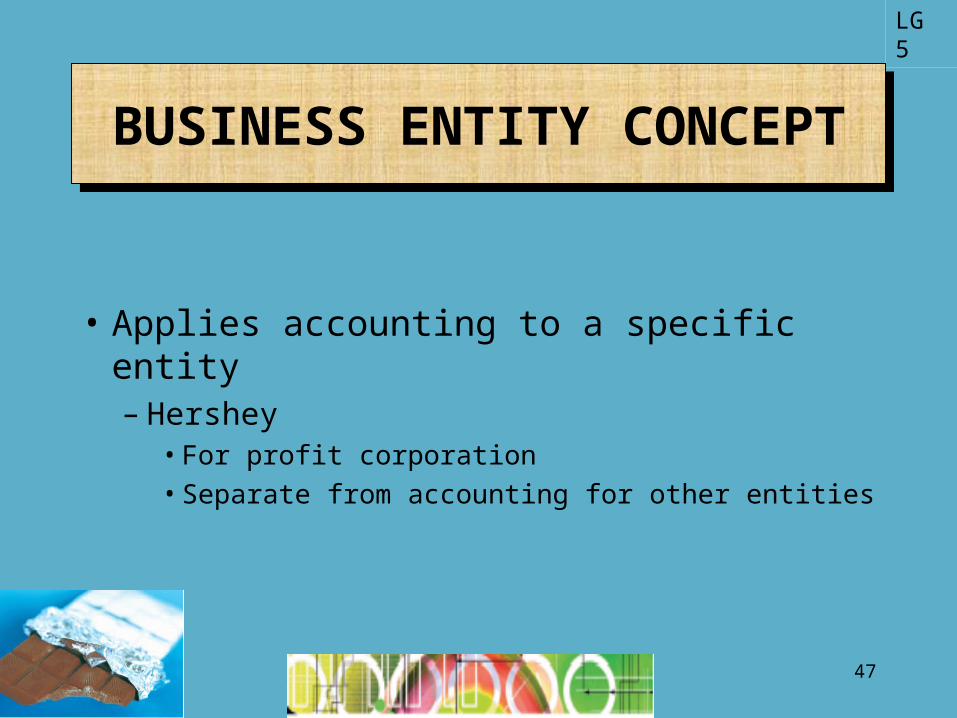

• Applies accounting to a specific entity– Hershey

• For profit corporation

• Separate from accounting for other entities

LG 5

BUSINESS ENTITY CONCEPTBUSINESS ENTITY CONCEPT

48

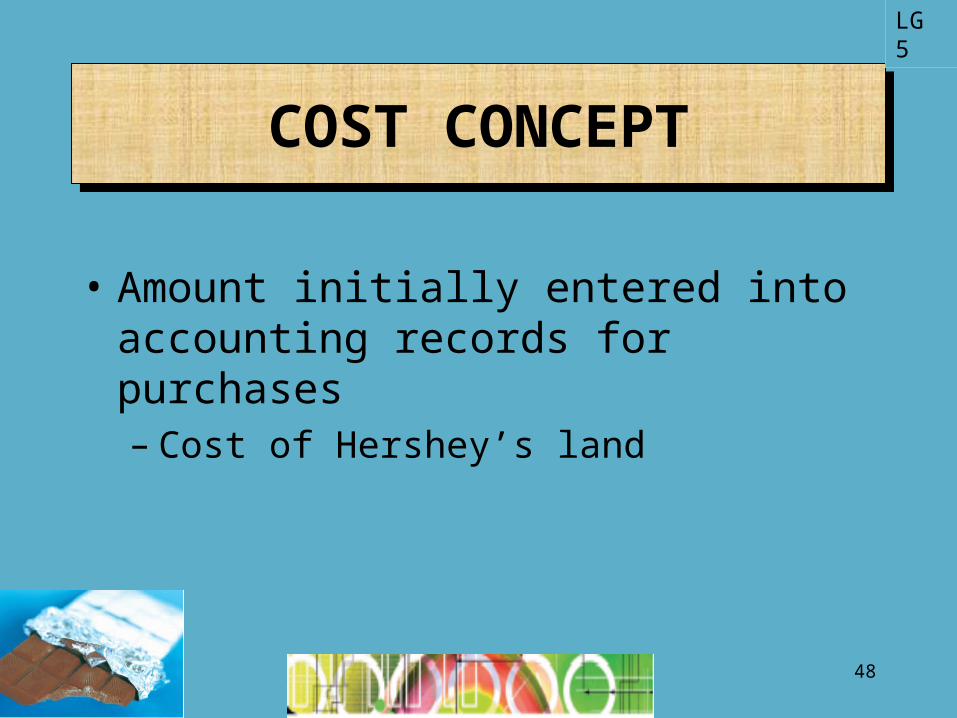

COST CONCEPTCOST CONCEPT

• Amount initially entered into accounting records for purchases– Cost of Hershey’s land

LG 5

49

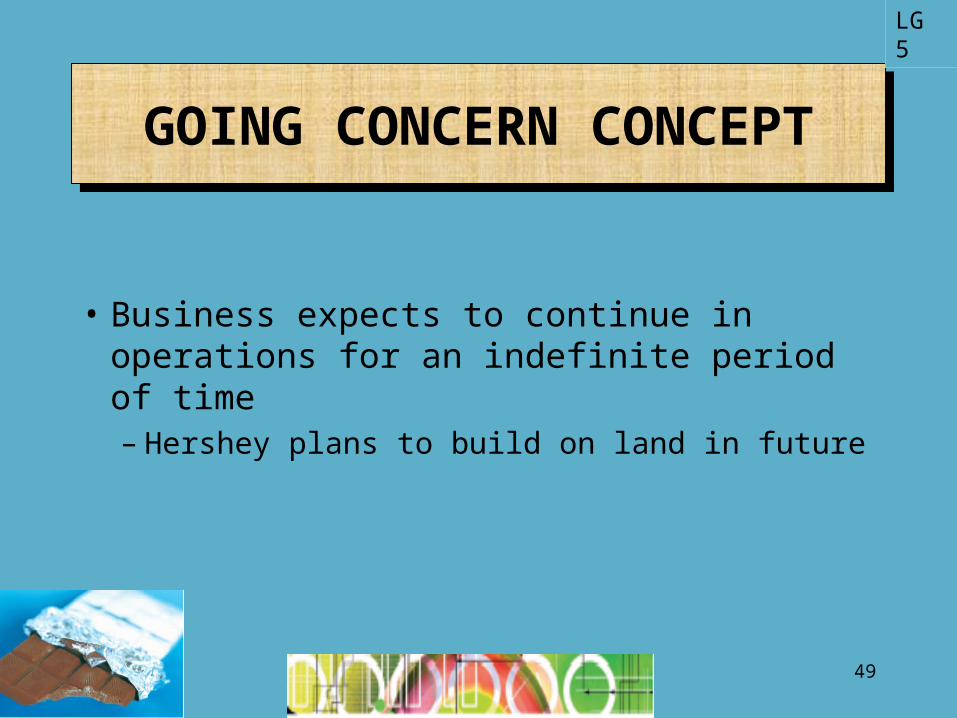

GOING CONCERN CONCEPTGOING CONCERN CONCEPT

• Business expects to continue in operations for an indefinite period of time– Hershey plans to build on land in future

LG 5

50

MATCHING CONCEPTMATCHING CONCEPT

• Expenses for a period are matched with revenue they generate– Hershey subtracts expenses from revenues on

income statement

LG 5

51

OBJECTIVITY CONCEPTOBJECTIVITY CONCEPT

• Entries into accounting records based on objective evidence– Hershey’s bank statements support entries in

cash account

LG 5

52

UNIT OF MEASURE CONCEPTUNIT OF MEASURE CONCEPT

• All economic data recorded in dollars– Hershey presents financial statements in dollars

LG 5

53

ADEQUATE DISCLOSURE CONCEPT

ADEQUATE DISCLOSURE CONCEPT

• Financial statements include all relevant data needed to understand financial condition and performance– Hershey provides other disclosures in footnotes

LG 5

54

ACCOUNTING PERIOD CONCEPT

ACCOUNTING PERIOD CONCEPT

• Economic data collected for a period of time in preparation of– Hershey’s income statement– Hershey’s retained earnings– Hershey’s cash flow statement

LG 5

55

RESPONSIBLE REPORTINGRESPONSIBLE REPORTING

• Reliability of financial reporting important – To economy– For ability of business to raise money from

investors• Stockholders

• creditors

56

LEARNING GOALSLEARNING GOALS

6 Describe, illustrate horizontal analysis.

57

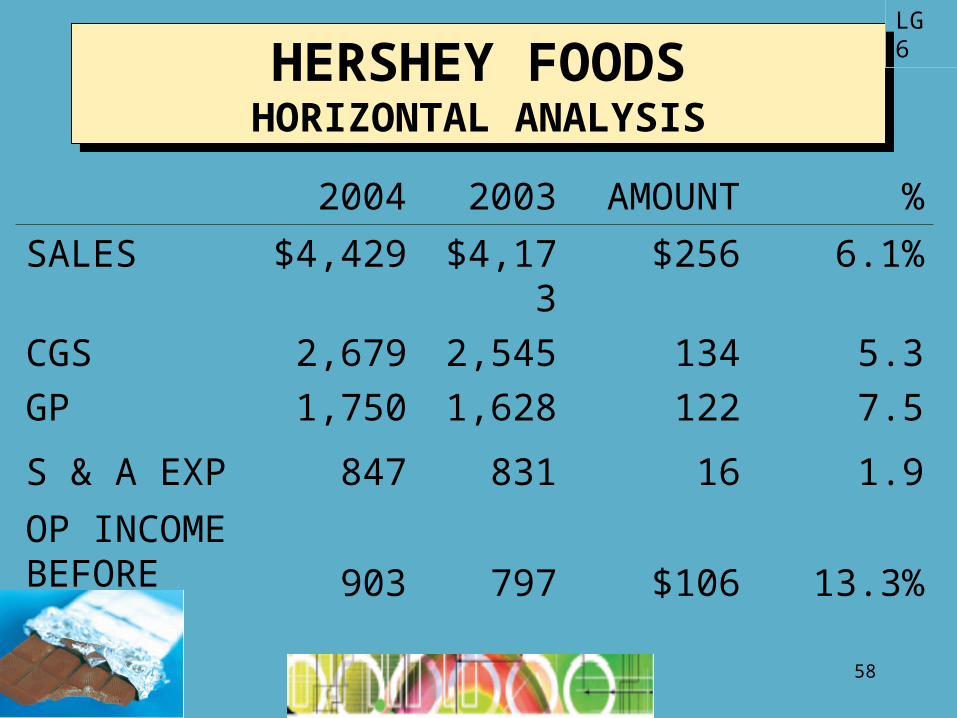

HORIZONTAL ANALYSISHORIZONTAL ANALYSIS

Uses comparative financial statements toCompute percentage increases &

decreases

Examine trends year to year

LG 6

58

HERSHEY FOODSHORIZONTAL ANALYSIS

HERSHEY FOODSHORIZONTAL ANALYSIS

2004 2003 AMOUNT %

SALES $4,429 $4,173 $256 6.1%

CGS 2,679 2,545 134 5.3

GP 1,750 1,628 122 7.5

S & A EXP 847 831 16 1.9

OP INCOME BEFORE TAX

903 797 $106 13.3%

LG 6

59

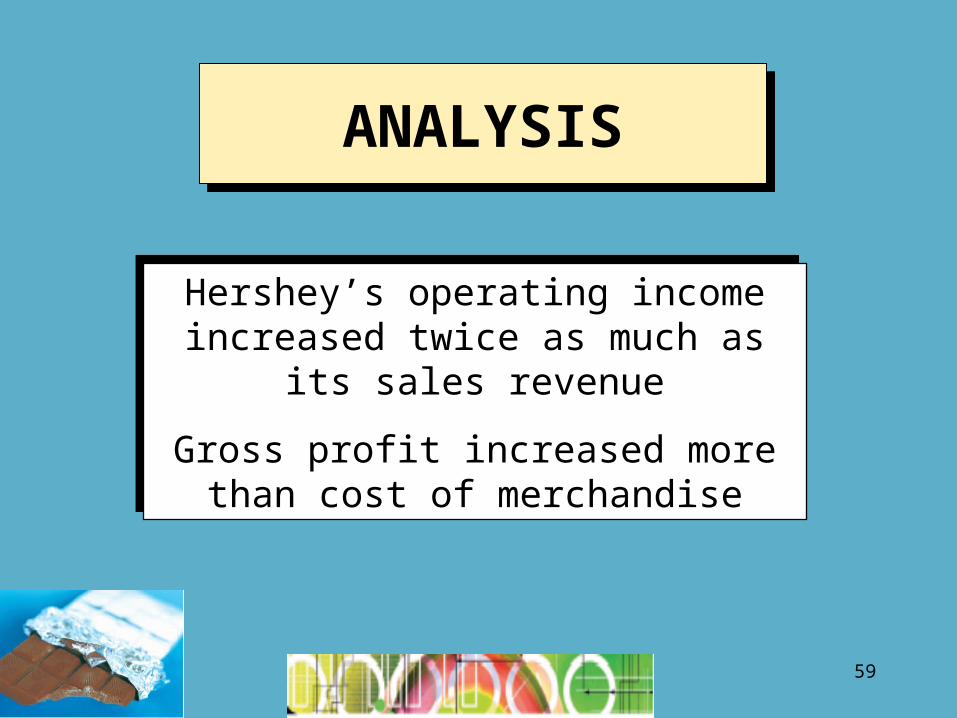

ANALYSISANALYSIS

Hershey’s operating income increased twice as much as its sales revenue

Gross profit increased more than cost of merchandise

Hershey’s operating income increased twice as much as its sales revenue

Gross profit increased more than cost of merchandise

60

THE END

CHAPTER 1