Embed Size (px)

Citation preview

1

Economic and Political Challenges of Acceding to the Euro area in a

post-Lehman Brothers World: The case of Poland

Przemysław Woźniak

Center for Social and Economic Research

2

Contents

Brief overview of economic developments Economic aspects – Maastricht criteria Political process

3

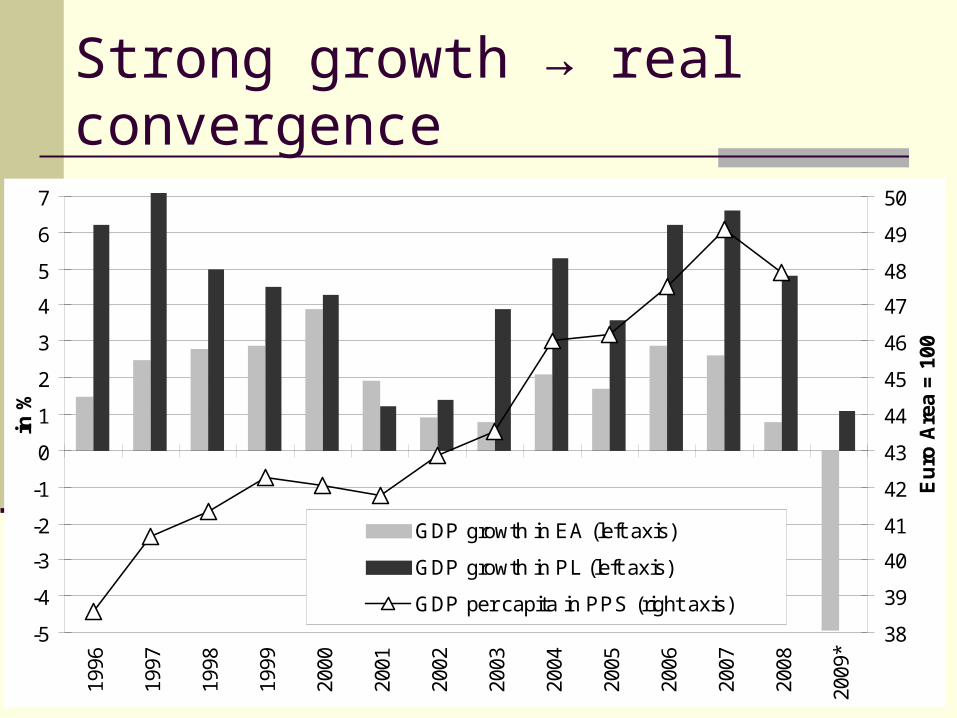

Strong growth → real convergence

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

*

in %

38

39

40

41

42

43

44

45

46

47

48

49

50

Eu

ro A

rea

= 1

00

GDP growth in EA (left axis)

GDP growth in PL (left axis)

GDP per capita in PPS (right axis)

4

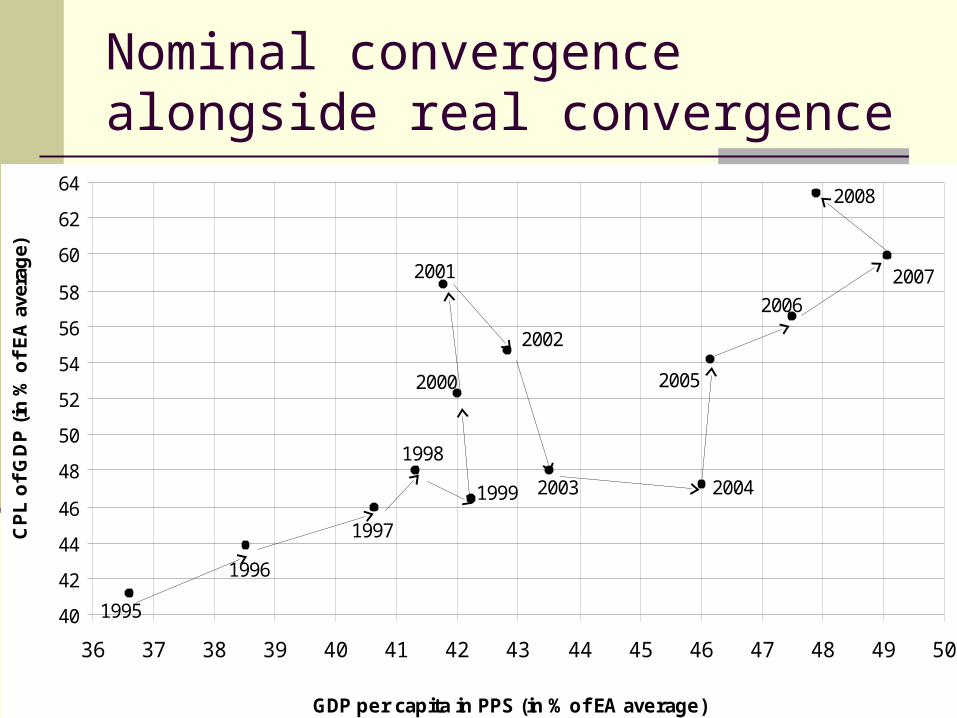

Nominal convergence alongside real convergence

2008

1995

1996

1997

1998

1999

2000

2001

2002

2003 2004

2005

2006

2007

40

42

44

46

48

50

52

54

56

58

60

62

64

36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

GDP per capita in PPS (in % of EA average)

CP

L o

f G

DP

(in

% o

f E

A a

vera

ge)

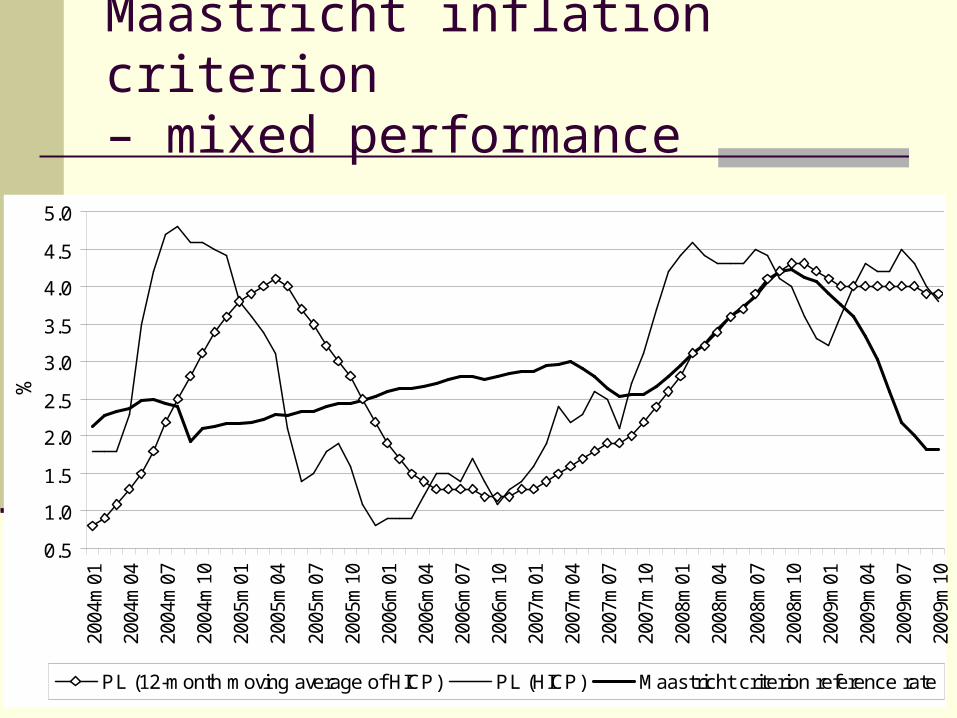

Maastricht inflation criterion – mixed performance

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2004

m01

2004

m04

2004

m07

2004

m10

2005

m01

2005

m04

2005

m07

2005

m10

2006

m01

2006

m04

2006

m07

2006

m10

2007

m01

2007

m04

2007

m07

2007

m10

2008

m01

2008

m04

2008

m07

2008

m10

2009

m01

2009

m04

2009

m07

2009

m10

%

PL (12-month moving average of HICP) PL (HICP) Maastricht criterion reference rate

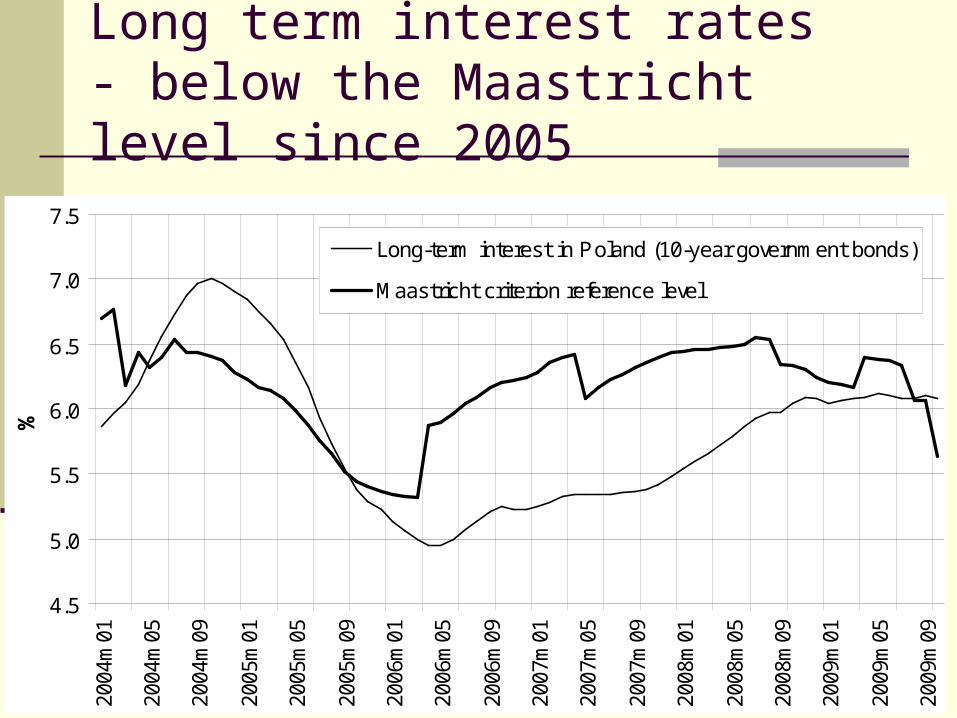

Long term interest rates- below the Maastricht level since 2005

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2004

m01

2004

m05

2004

m09

2005

m01

2005

m05

2005

m09

2006

m01

2006

m05

2006

m09

2007

m01

2007

m05

2007

m09

2008

m01

2008

m05

2008

m09

2009

m01

2009

m05

2009

m09

%

Long-term interest in Poland (10-year government bonds)

Maastricht criterion reference level

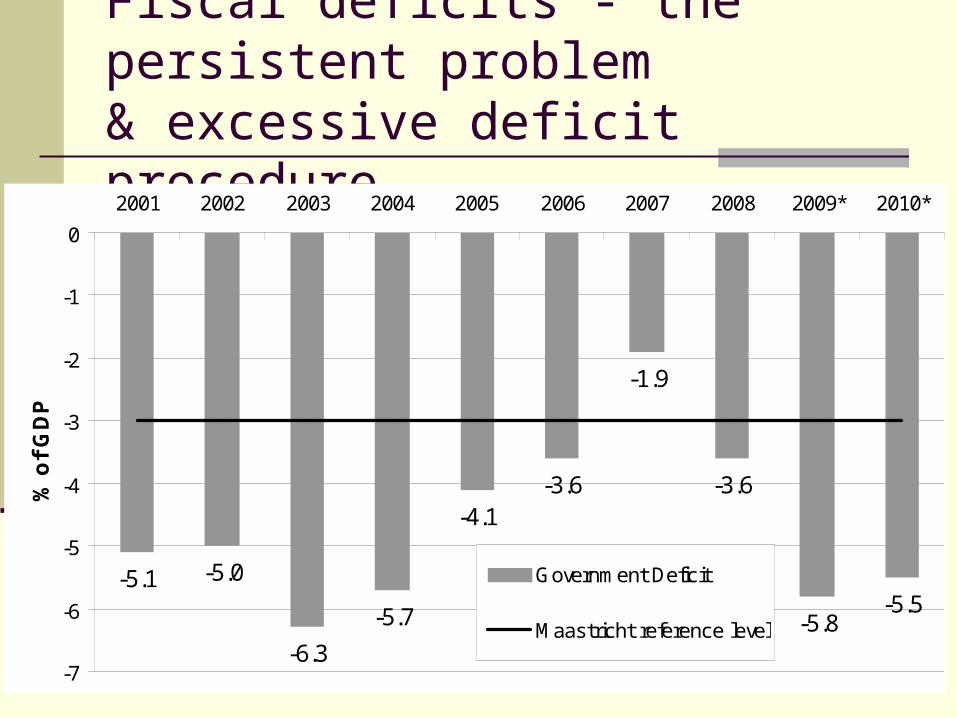

Fiscal deficits - the persistent problem & excessive deficit procedure

-5.1 -5.0

-6.3

-5.7

-4.1-3.6

-1.9

-3.6

-5.8-5.5

-7

-6

-5

-4

-3

-2

-1

0

2001 2002 2003 2004 2005 2006 2007 2008 2009* 2010*

% o

f G

DP

Government Deficit

Maastricht reference level

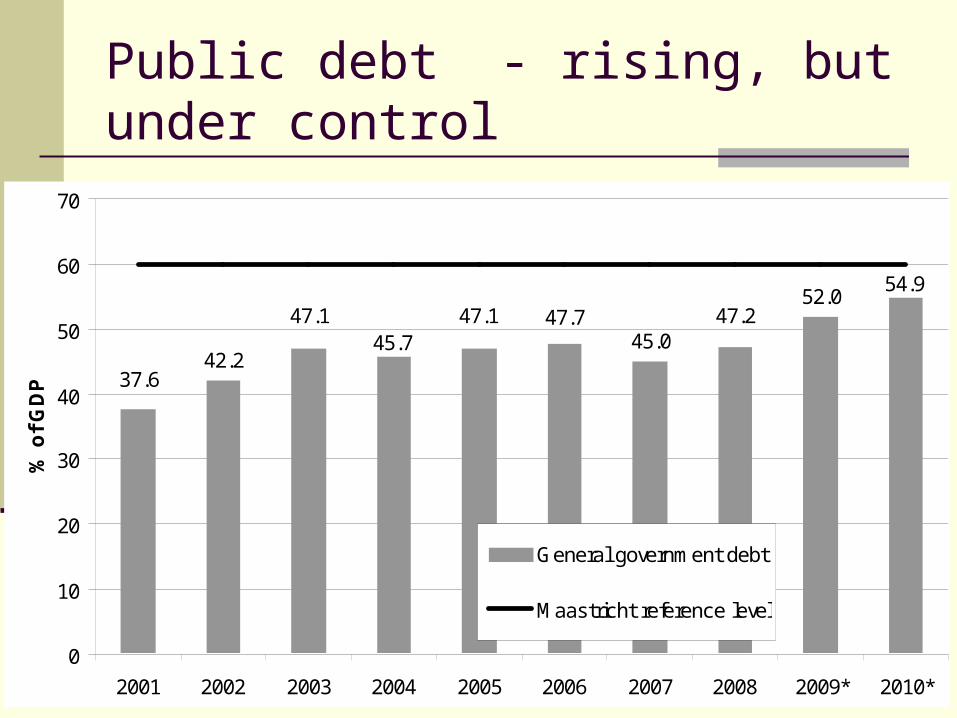

Public debt - rising, but under control

42.245.0

52.0

37.6

47.145.7

47.1 47.7 47.2

54.9

0

10

20

30

40

50

60

70

2001 2002 2003 2004 2005 2006 2007 2008 2009* 2010*

% o

f G

DP

General government debt

Maastricht reference level

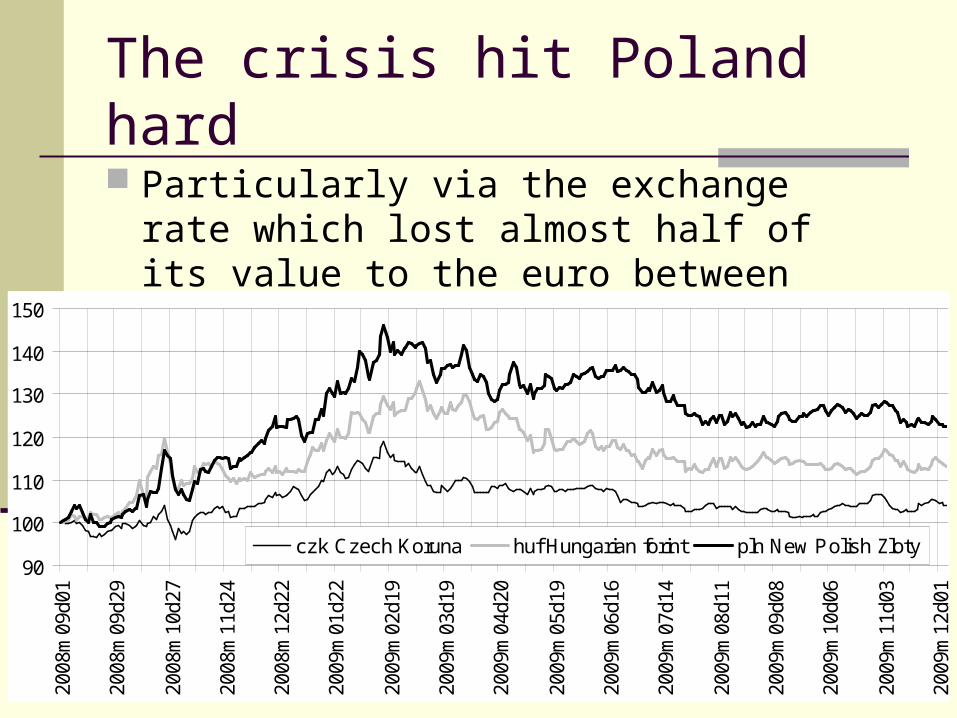

The crisis hit Poland hard

Particularly via the exchange rate which lost almost half of its value to the euro between Sep08 and mid Feb09

90

100

110

120

130

140

150

2008

m09

d01

2008

m09

d29

2008

m10

d27

2008

m11

d24

2008

m12

d22

2009

m01

d22

2009

m02

d19

2009

m03

d19

2009

m04

d20

2009

m05

d19

2009

m06

d16

2009

m07

d14

2009

m08

d11

2009

m09

d08

2009

m10

d06

2009

m11

d03

2009

m12

d01

czk Czech Koruna huf Hungarian forint pln New Polish Zloty

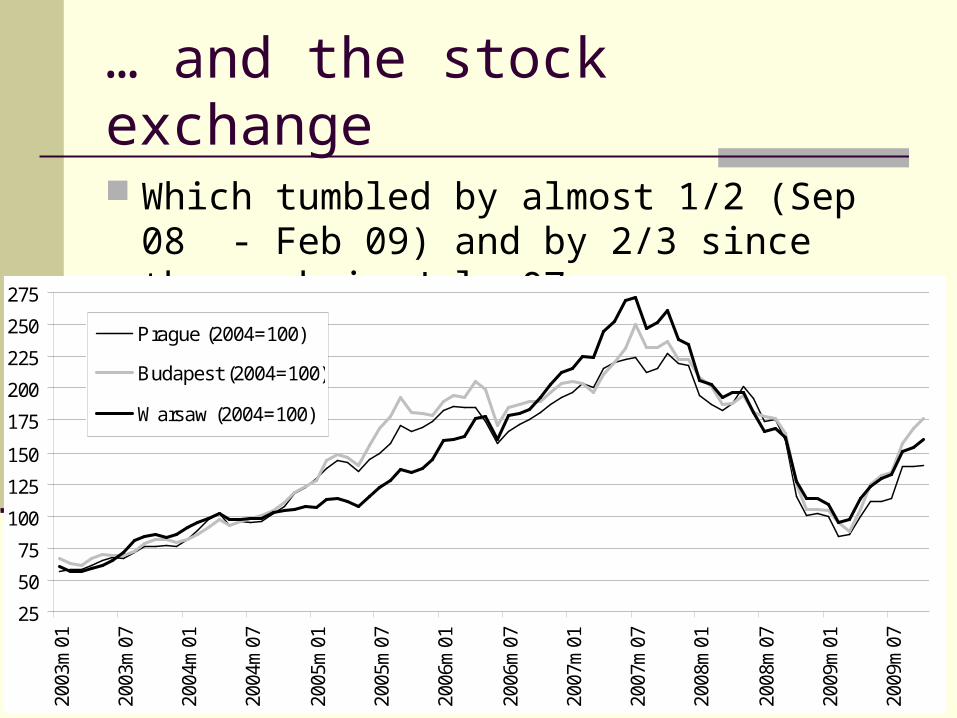

… and the stock exchange

Which tumbled by almost 1/2 (Sep 08 - Feb 09) and by 2/3 since the peak in July 07.

25

50

75

100

125

150

175

200

225

250

275

2003

m01

2003

m07

2004

m01

2004

m07

2005

m01

2005

m07

2006

m01

2006

m07

2007

m01

2007

m07

2008

m01

2008

m07

2009

m01

2009

m07

Prague (2004=100)

Budapest (2004=100)

Warsaw (2004=100)

The politics of euro adoption prior to 2008

Before 2007 – not a priority, no formal steps Two left wing-governments (2001-2005) and

two right wing governments (2005-2007) did little to initiate the path to the euro

The left wing coalitions – ideological consent but fear of political risk

The right-wing coalitions (Kaczynski) – ideological objections + political opportunism

Unpopularity of the euro

In the Eurobarometer surveys Poles emerge as one of the most euro-sceptic countries

Eurobarometer (May2008) The lowest awareness of no opt-out (15%). The biggest fear of price rise (83%) and abuses

during changeover (84%) Poles are generally uninterested in the euro

and consider it negative for their country Up to late 2007 politicians decided to give in to

or profit from those fears rather than change them.

Breakthrough in late 2007

The change came in late 2007 with the new centrist liberal government of Donald Tusk

Rostowski, the advocate of unilateral euroization prior to 2004, became the finance minister

The euro adoption emerges as a fully-fledged political plan:

- Roadmap to the euro (Oct 08) –

ERM2 in 2009H1 and EMU entry in 2012

- Nominating the plenipotentiary for the euro

- Convergence programmes

Euro-accession debate in late 2008 and early 2009 Macroeconomic criteria do not considered a

problem (except exchange rate stability) The biggest challenge – constitution

amendments to allow transferring powers to the ECB

Two-thirds majority required – that the coalition does not have (referendum).

Monetary Policy Council – entering ERM2 before the constitutional change unwise

The gridlock puts the roadmap under pressure

The debate shifts back to economics

As the year 2009 progressed, economic situation deteriorates

Euro more popular – according to the polls Fiscal deficit in 2008 revised downwards (to -

3.6%) → EDP Unprecedented fluctuations in the forex

market make it less realistic to enter ERM2 by mid-2009 as planned

Rostowski changes the tone – calls the euro adoption a pragmatic goal, not a dogma

|The deficit becomes the biggest problem

The ultimate blow came with EC Spring forecasts: deficit at 6.6% in 2009 and 7.3% in 2010

Better GDP performance and outlook likely to produce smaller deficits of below 6% in both years.

Bringing the deficit below 3% not likely before 2012. Inflation above the reference level since late 2008

(but expected to return below by mid 2010) Interest rates started to exceed the reference level in

October 2009. EC sees public debt rise to 51.7% and 57.0%

(2009&2010) and 61.3% in 2011 (autumn forecast)

2012 invalid but formal steps continued

In late summer the government officially gave up the plan to enter EMU in 2009 and EMU in 2012

However, administrative processes continue Early December – the first meeting of the

National Coordination Committee, the key body in the euro adoption process

Progress on the National Changeover Plan The median expectation of the euro-day is

2014 (November Reuters poll)

18

Thank you !