Embed Size (px)

Citation preview

11

EUE43E: ‘Trade & EUE43E: ‘Trade & Commerce’Commerce’

Understanding Cost BehaviourUnderstanding Cost Behaviour

Break-Even & Pricing PolicyBreak-Even & Pricing Policy

Robert J. WilliamsRobert J. Williams

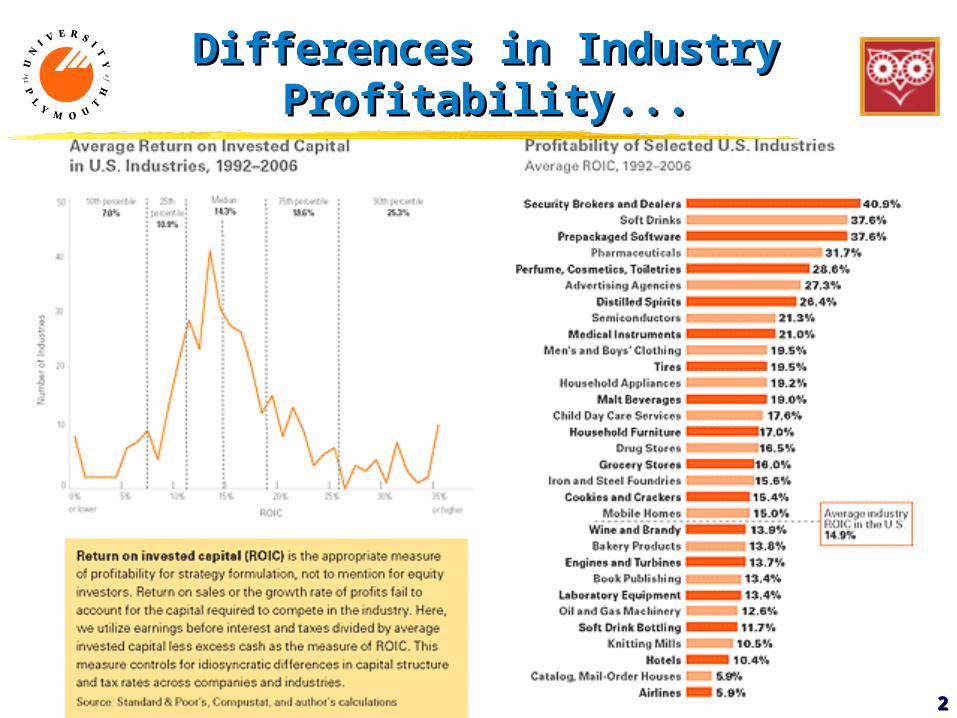

Differences in Industry Differences in Industry Profitability...Profitability...

22

33

IntroductionIntroduction

Understand the Understand the categorisationcategorisation & & behaviourbehaviour of costs of costs and the implications for decision making based on:and the implications for decision making based on:

1.1. Categorisation 1 Categorisation 1 based on based on ease of allocation ease of allocation

2.2. Categorisation 2 Categorisation 2 based on behaviour with based on behaviour with changing changing

levels of productionlevels of production

3.3. Categorisation 3 Categorisation 3 based on behaviour at the based on behaviour at the margins of productionmargins of production

Categorising Costs 1Categorising Costs 1

1.1. Direct CostsDirect Costs

2.2. Indirect CostsIndirect Costs

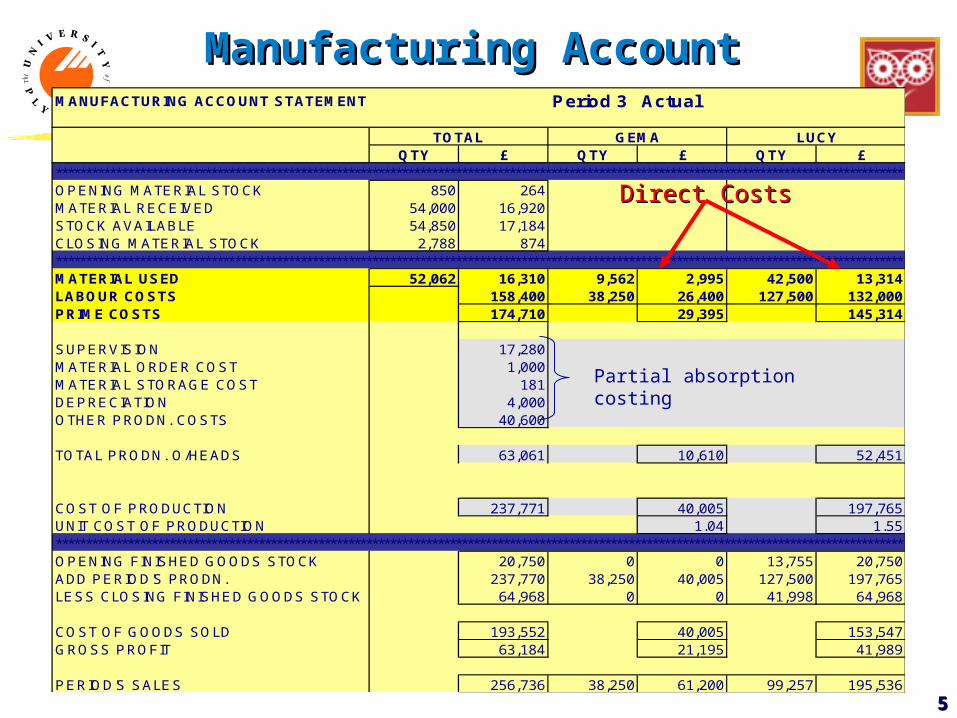

44

55

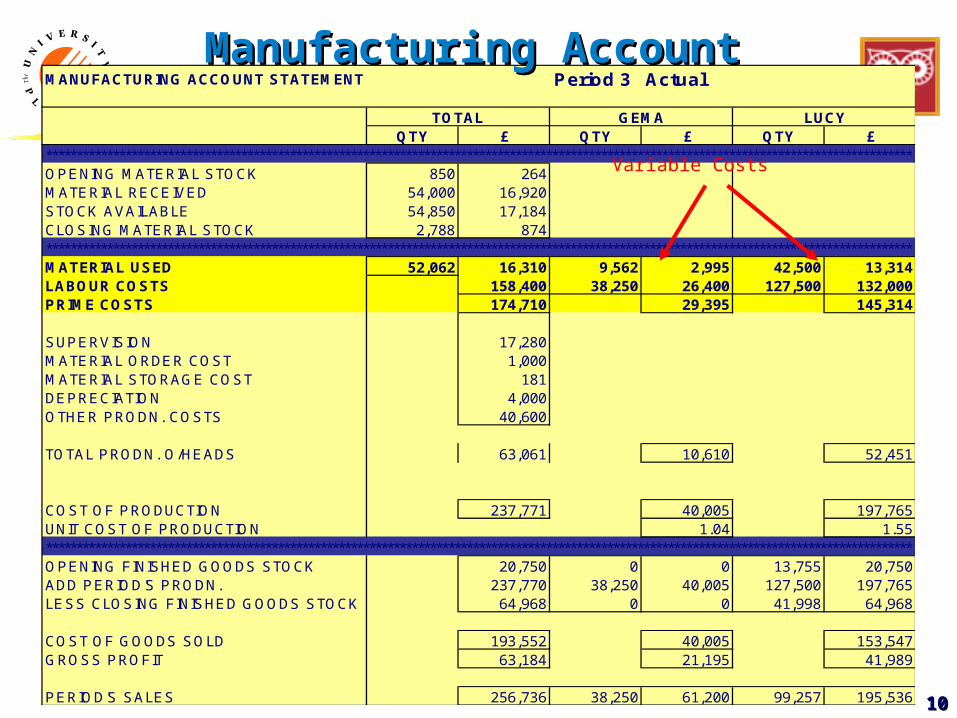

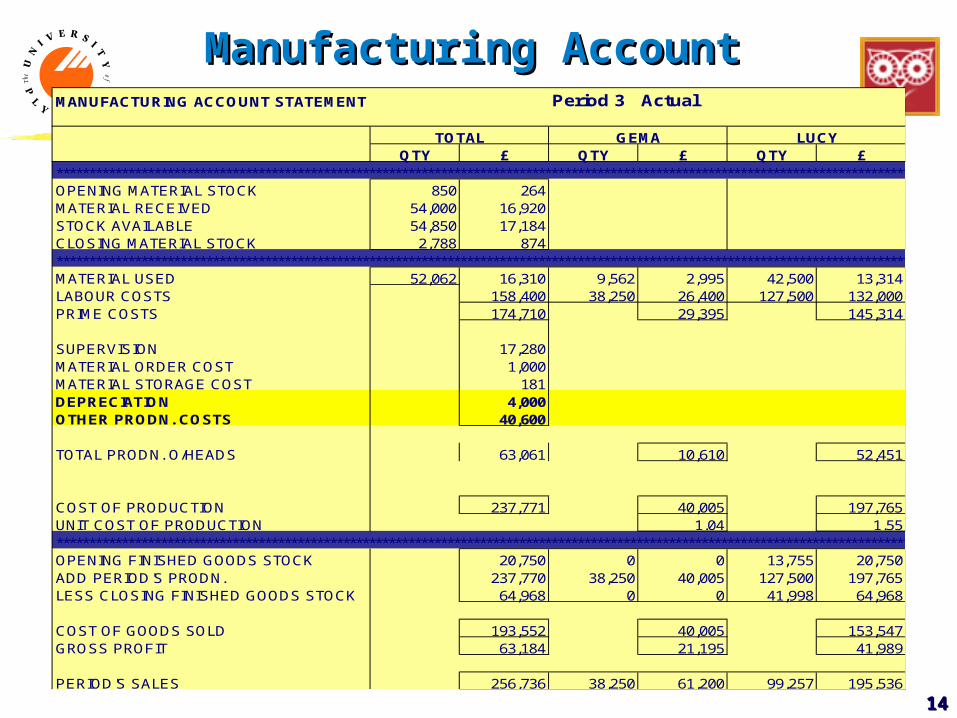

MANUFACTURING ACCOUNT STATEMENT Period 3 Actual

TOTAL GEMA LUCYQTY £ QTY £ QTY £

**********************************************************************************************************************************************OPENING MATERIAL STOCK 850 264MATERIAL RECEIVED 54,000 16,920STOCK AVAILABLE 54,850 17,184CLOSING MATERIAL STOCK 2,788 874**********************************************************************************************************************************************MATERIAL USED 52,062 16,310 9,562 2,995 42,500 13,314LABOUR COSTS 158,400 38,250 26,400 127,500 132,000PRIME COSTS 174,710 29,395 145,314

SUPERVISION 17,280MATERIAL ORDER COST 1,000MATERIAL STORAGE COST 181DEPRECIATION 4,000OTHER PRODN. COSTS 40,600

TOTAL PRODN. O/HEADS 63,061 10,610 52,451

COST OF PRODUCTION 237,771 40,005 197,765UNIT COST OF PRODUCTION 1.04 1.55**********************************************************************************************************************************************OPENING FINISHED GOODS STOCK 20,750 0 0 13,755 20,750ADD PERIOD'S PRODN. 237,770 38,250 40,005 127,500 197,765LESS CLOSING FINISHED GOODS STOCK 64,968 0 0 41,998 64,968

COST OF GOODS SOLD 193,552 40,005 153,547GROSS PROFIT 63,184 21,195 41,989

PERIOD'S SALES 256,736 38,250 61,200 99,257 195,536

Manufacturing AccountManufacturing Account

Partial absorption costing

Direct CostsDirect Costs

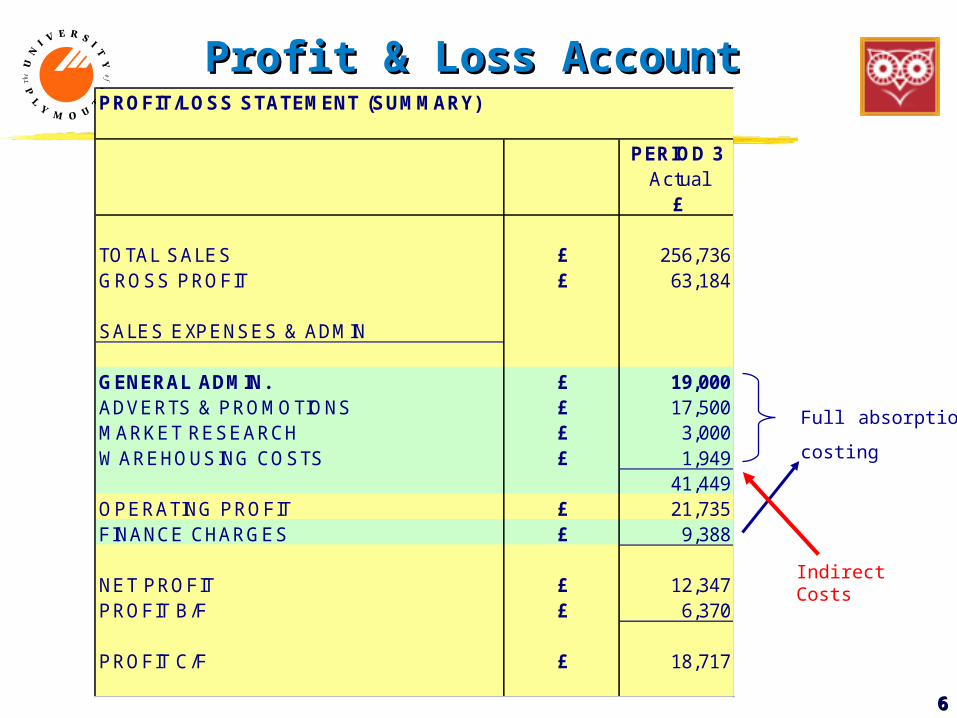

66

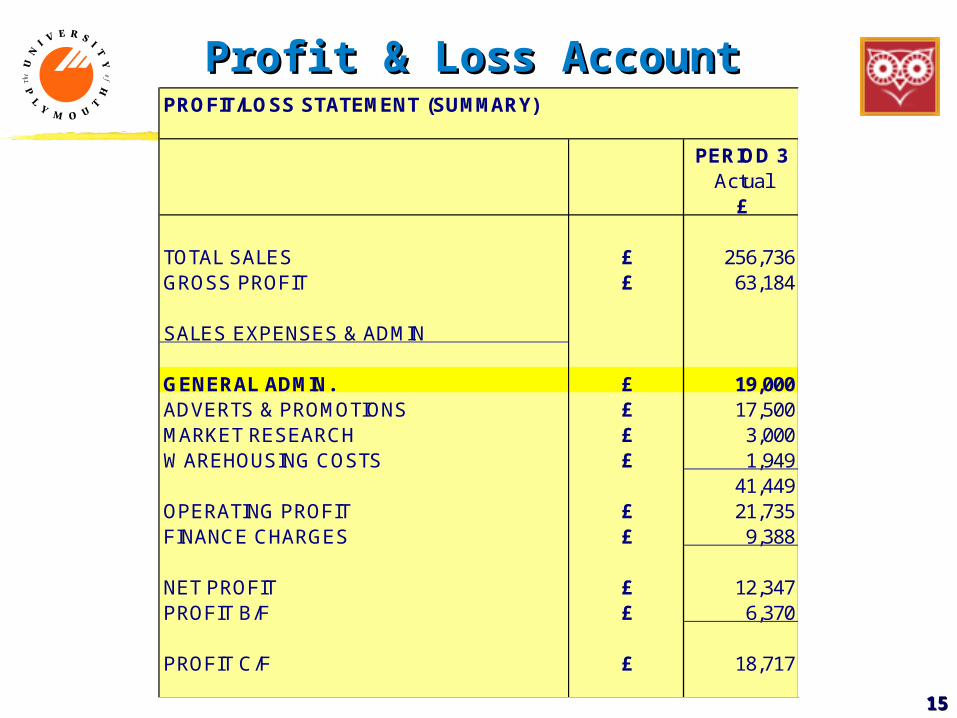

Profit & Loss AccountProfit & Loss AccountPROFIT/LOSS STATEMENT (SUMMARY)

PERIOD 3Actual

£

TOTAL SALES £ 256,736GROSS PROFIT £ 63,184

SALES EXPENSES & ADMIN

GENERAL ADMIN. £ 19,000ADVERTS & PROMOTIONS £ 17,500MARKET RESEARCH £ 3,000WAREHOUSING COSTS £ 1,949

41,449OPERATING PROFIT £ 21,735FINANCE CHARGES £ 9,388

NET PROFIT £ 12,347PROFIT B/F £ 6,370

PROFIT C/F £ 18,717

Full absorption

costing

Indirect Costs

77

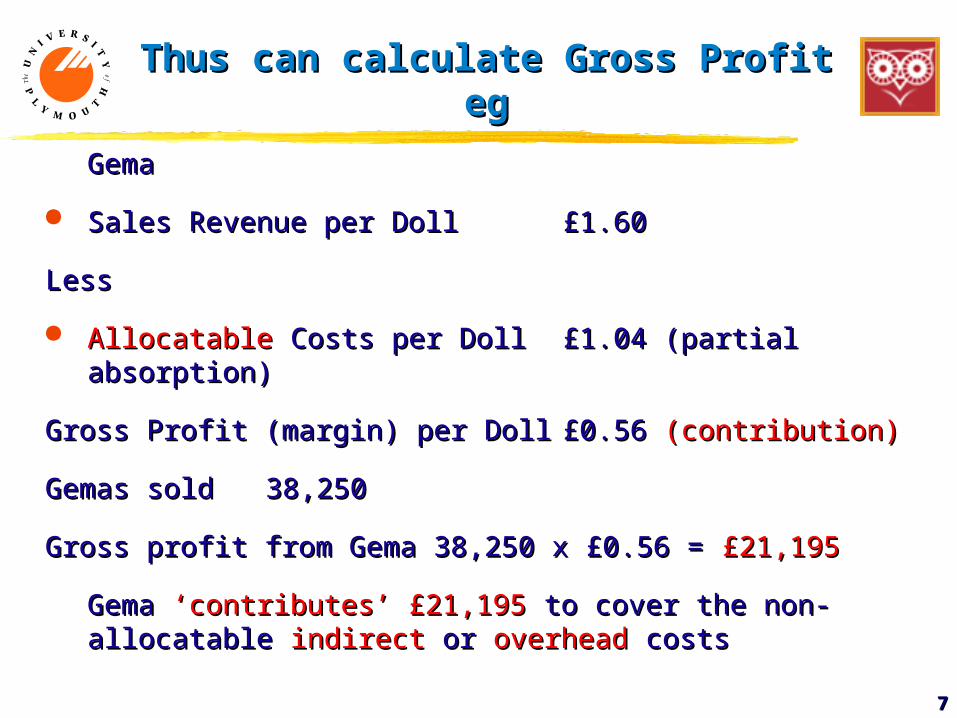

Thus can calculate Gross Profit Thus can calculate Gross Profit egeg

GemaGema

Sales Revenue per Doll Sales Revenue per Doll £1.60£1.60

LessLess

AllocatableAllocatable Costs per Doll Costs per Doll £1.04 (partial £1.04 (partial absorption)absorption)

Gross Profit (margin) per DollGross Profit (margin) per Doll £0.56 £0.56 (contribution)(contribution)

Gemas soldGemas sold 38,25038,250

Gross profit from Gema 38,250 x £0.56 = Gross profit from Gema 38,250 x £0.56 = £21,195£21,195

Gema Gema ‘contributes’ £21,195‘contributes’ £21,195 to cover the non- to cover the non-allocatable allocatable indirectindirect or or overheadoverhead costs costs

88

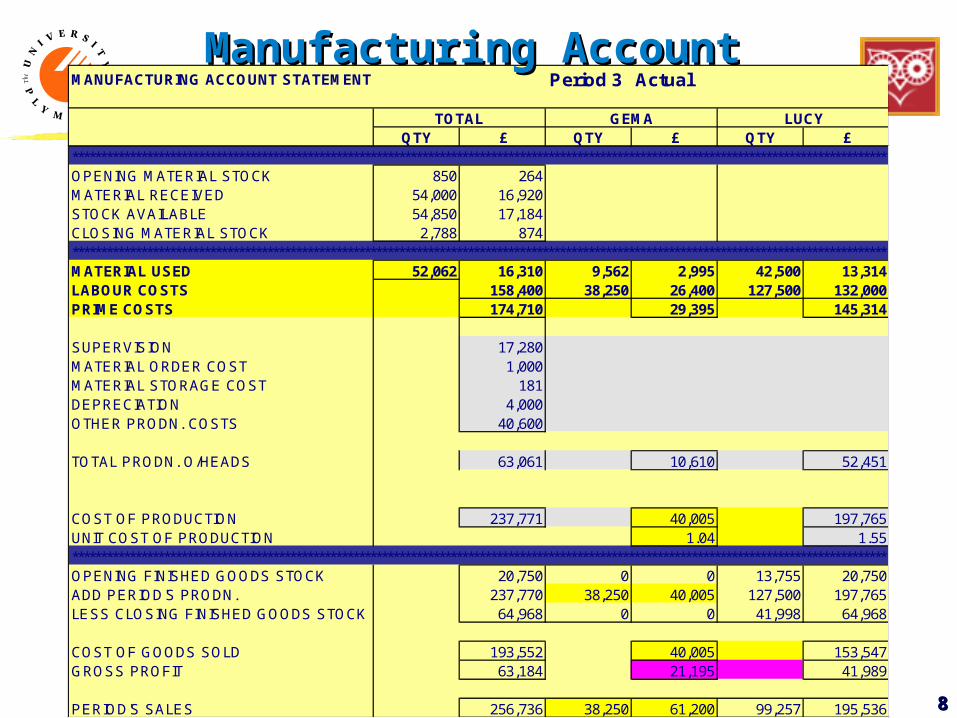

MANUFACTURING ACCOUNT STATEMENT Period 3 Actual

TOTAL GEMA LUCYQTY £ QTY £ QTY £

**********************************************************************************************************************************************OPENING MATERIAL STOCK 850 264MATERIAL RECEIVED 54,000 16,920STOCK AVAILABLE 54,850 17,184CLOSING MATERIAL STOCK 2,788 874**********************************************************************************************************************************************MATERIAL USED 52,062 16,310 9,562 2,995 42,500 13,314LABOUR COSTS 158,400 38,250 26,400 127,500 132,000PRIME COSTS 174,710 29,395 145,314

SUPERVISION 17,280MATERIAL ORDER COST 1,000MATERIAL STORAGE COST 181DEPRECIATION 4,000OTHER PRODN. COSTS 40,600

TOTAL PRODN. O/HEADS 63,061 10,610 52,451

COST OF PRODUCTION 237,771 40,005 197,765UNIT COST OF PRODUCTION 1.04 1.55**********************************************************************************************************************************************OPENING FINISHED GOODS STOCK 20,750 0 0 13,755 20,750ADD PERIOD'S PRODN. 237,770 38,250 40,005 127,500 197,765LESS CLOSING FINISHED GOODS STOCK 64,968 0 0 41,998 64,968

COST OF GOODS SOLD 193,552 40,005 153,547GROSS PROFIT 63,184 21,195 41,989

PERIOD'S SALES 256,736 38,250 61,200 99,257 195,536

Manufacturing AccountManufacturing Account

99

Costs categorised on the basis of their cost Costs categorised on the basis of their cost behaviourbehaviour with with changing production levelschanging production levels

variable costsvariable costs

vary in vary in directdirect proportion to the level or scale proportion to the level or scale of production/operationof production/operation

eg?eg?

Categorising Costs 2Categorising Costs 2

1010

MANUFACTURING ACCOUNT STATEMENT Period 3 Actual

TOTAL GEMA LUCYQTY £ QTY £ QTY £

**********************************************************************************************************************************************OPENING MATERIAL STOCK 850 264MATERIAL RECEIVED 54,000 16,920STOCK AVAILABLE 54,850 17,184CLOSING MATERIAL STOCK 2,788 874**********************************************************************************************************************************************MATERIAL USED 52,062 16,310 9,562 2,995 42,500 13,314LABOUR COSTS 158,400 38,250 26,400 127,500 132,000PRIME COSTS 174,710 29,395 145,314

SUPERVISION 17,280MATERIAL ORDER COST 1,000MATERIAL STORAGE COST 181DEPRECIATION 4,000OTHER PRODN. COSTS 40,600

TOTAL PRODN. O/HEADS 63,061 10,610 52,451

COST OF PRODUCTION 237,771 40,005 197,765UNIT COST OF PRODUCTION 1.04 1.55**********************************************************************************************************************************************OPENING FINISHED GOODS STOCK 20,750 0 0 13,755 20,750ADD PERIOD'S PRODN. 237,770 38,250 40,005 127,500 197,765LESS CLOSING FINISHED GOODS STOCK 64,968 0 0 41,998 64,968

COST OF GOODS SOLD 193,552 40,005 153,547GROSS PROFIT 63,184 21,195 41,989

PERIOD'S SALES 256,736 38,250 61,200 99,257 195,536

Manufacturing AccountManufacturing Account

Variable Costs

1111

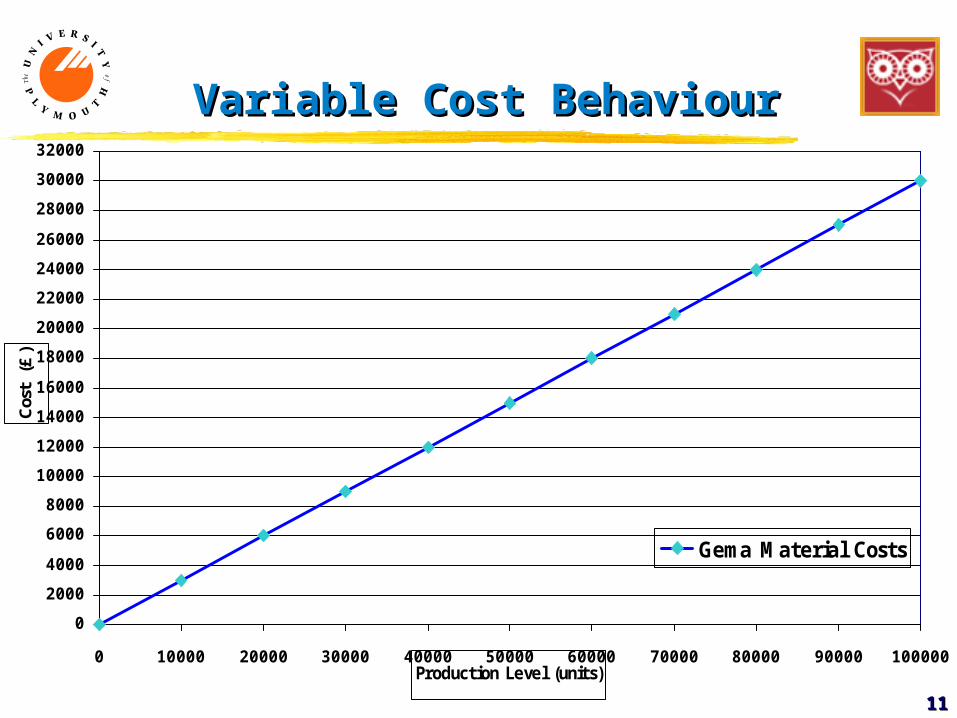

Variable Cost BehaviourVariable Cost Behaviour

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

22000

24000

26000

28000

30000

32000

0 10000 20000 30000 40000 50000 60000 70000 80000 90000 100000Production Level (units)

Cos

t (

£)

Gema Material Costs

1212

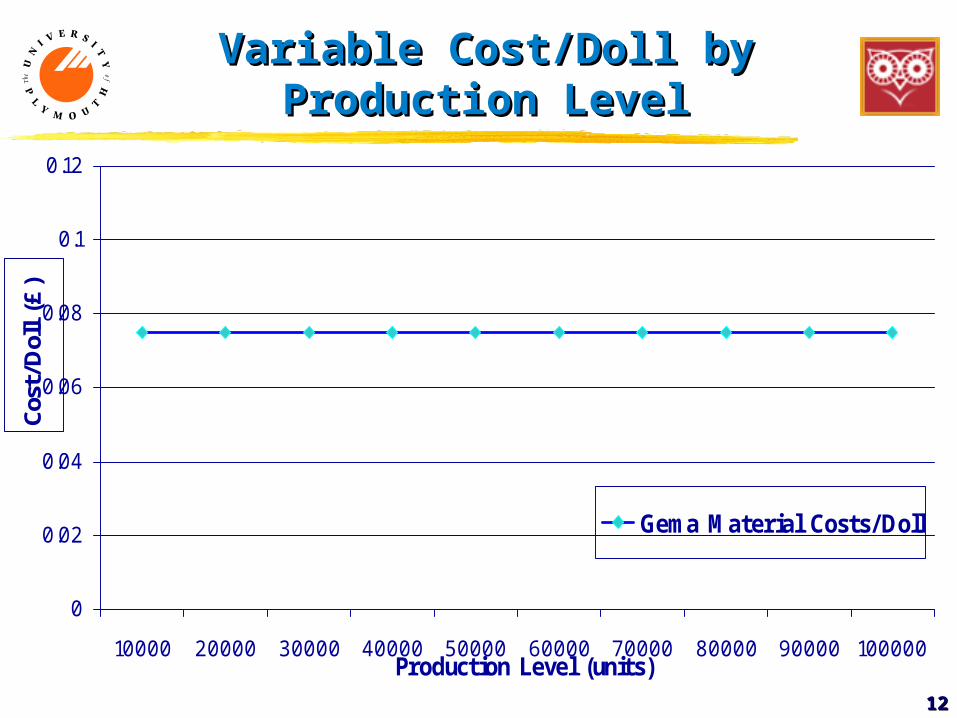

Variable Cost/Doll by Variable Cost/Doll by Production LevelProduction Level

0

0.02

0.04

0.06

0.08

0.1

0.12

10000 20000 30000 40000 50000 60000 70000 80000 90000 100000Production Level (units)

Cost

/Dol

l (£

)

Gema Material Costs/Doll

1313

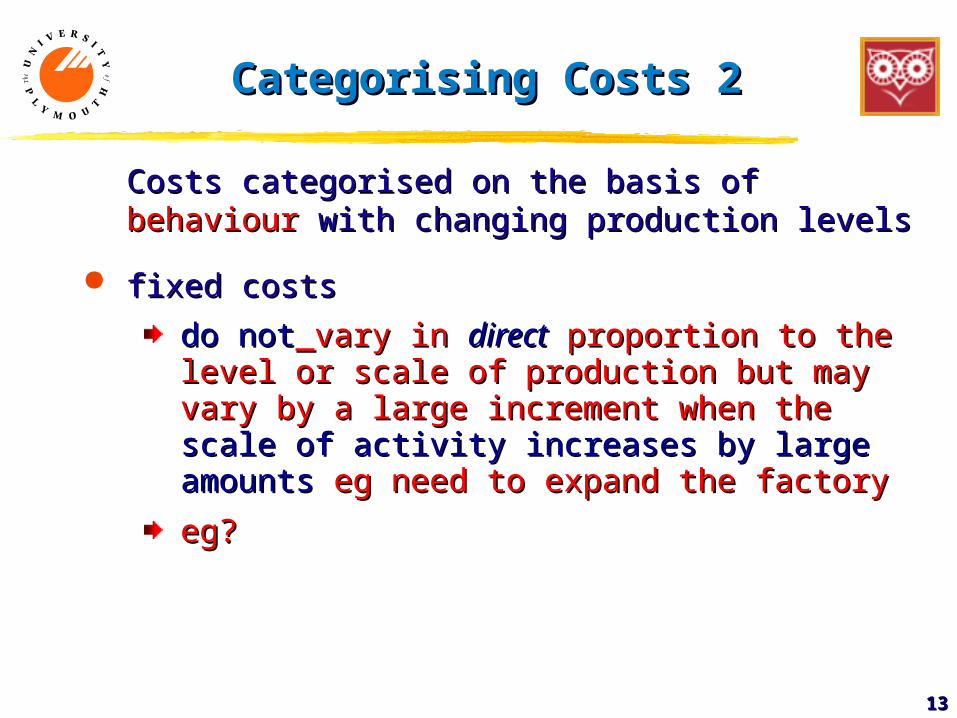

Costs categorised on the basis of Costs categorised on the basis of behaviourbehaviour with with changing production levelschanging production levels

fixed costsfixed costs

do notdo not vary in vary in directdirect proportion to the level or proportion to the level or scale of production but may vary by a large scale of production but may vary by a large increment when the increment when the scale of activity scale of activity increases by large amountsincreases by large amounts eg need to eg need to expand the factoryexpand the factory

eg?eg?

Categorising Costs 2Categorising Costs 2

1414

MANUFACTURING ACCOUNT STATEMENT Period 3 Actual

TOTAL GEMA LUCYQTY £ QTY £ QTY £

**********************************************************************************************************************************************OPENING MATERIAL STOCK 850 264MATERIAL RECEIVED 54,000 16,920STOCK AVAILABLE 54,850 17,184CLOSING MATERIAL STOCK 2,788 874**********************************************************************************************************************************************MATERIAL USED 52,062 16,310 9,562 2,995 42,500 13,314LABOUR COSTS 158,400 38,250 26,400 127,500 132,000PRIME COSTS 174,710 29,395 145,314

SUPERVISION 17,280MATERIAL ORDER COST 1,000MATERIAL STORAGE COST 181DEPRECIATION 4,000OTHER PRODN. COSTS 40,600

TOTAL PRODN. O/HEADS 63,061 10,610 52,451

COST OF PRODUCTION 237,771 40,005 197,765UNIT COST OF PRODUCTION 1.04 1.55**********************************************************************************************************************************************OPENING FINISHED GOODS STOCK 20,750 0 0 13,755 20,750ADD PERIOD'S PRODN. 237,770 38,250 40,005 127,500 197,765LESS CLOSING FINISHED GOODS STOCK 64,968 0 0 41,998 64,968

COST OF GOODS SOLD 193,552 40,005 153,547GROSS PROFIT 63,184 21,195 41,989

PERIOD'S SALES 256,736 38,250 61,200 99,257 195,536

Manufacturing AccountManufacturing Account

1515

Profit & Loss AccountProfit & Loss AccountPROFIT/LOSS STATEMENT (SUMMARY)

PERIOD 3Actual

£

TOTAL SALES £ 256,736GROSS PROFIT £ 63,184

SALES EXPENSES & ADMIN

GENERAL ADMIN. £ 19,000ADVERTS & PROMOTIONS £ 17,500MARKET RESEARCH £ 3,000WAREHOUSING COSTS £ 1,949

41,449OPERATING PROFIT £ 21,735FINANCE CHARGES £ 9,388

NET PROFIT £ 12,347PROFIT B/F £ 6,370

PROFIT C/F £ 18,717

1616

Fixed Cost BehaviourFixed Cost Behaviour

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

22000

24000

0 10000 20000 30000 40000 50000 60000 70000 80000 90000 1E+05

Production Level (units)

Cost

(£

)

General Admin Cost

1717

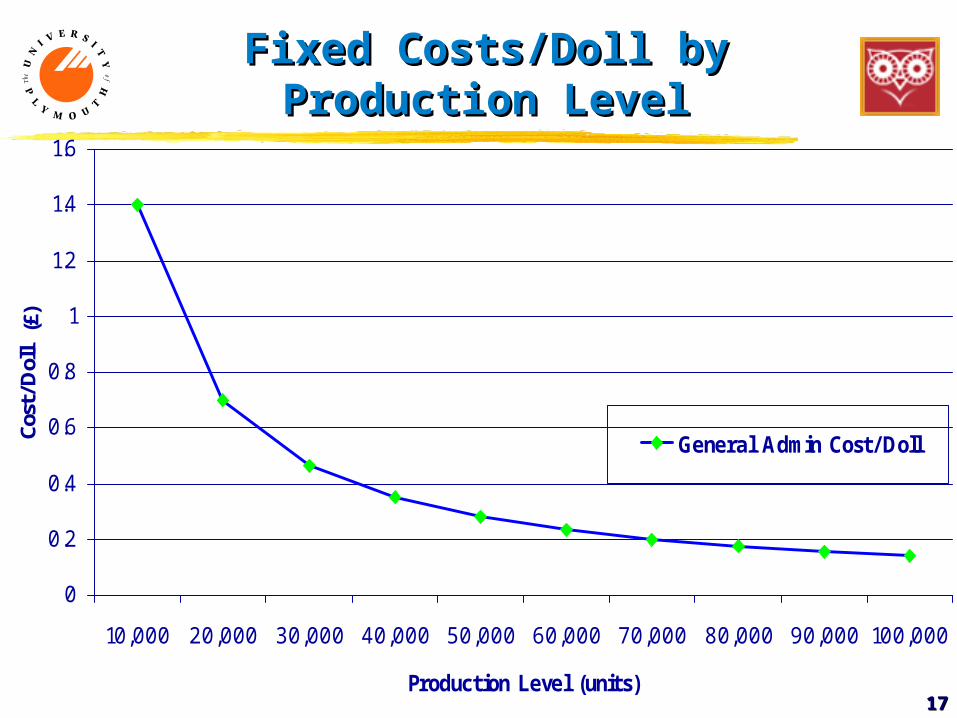

Fixed Costs/Doll by Fixed Costs/Doll by Production LevelProduction Level

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Production Level (units)

Cost

/Dol

l (£

)

General Admin Cost/Doll

1818

Categorising Costs 2Categorising Costs 2

Costs categorised on the basis of Costs categorised on the basis of behaviourbehaviour with with

changing production levelschanging production levels

semi-variablesemi-variable

contain both contain both fixedfixed & & variablevariable elements elements

eg?eg? business vehicles: ownership costs; tax, business vehicles: ownership costs; tax,

insurance - fixed insurance - fixed use costs; fuel, oil - variableuse costs; fuel, oil - variable what about depreciation? what about depreciation?

see graphsee graph

1919

Semi - Variable BehaviourSemi - Variable Behaviour

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

22000

24000

10000 20000 30000 40000 50000 60000 70000 80000 90000 1E+05

Production Level (units)

Cost

(£

)

Other Prod'n Costs - Variable

Other Prod'n Costs - Fixed

Fixed Cost

+ Variable Cost

Total Cost

2020

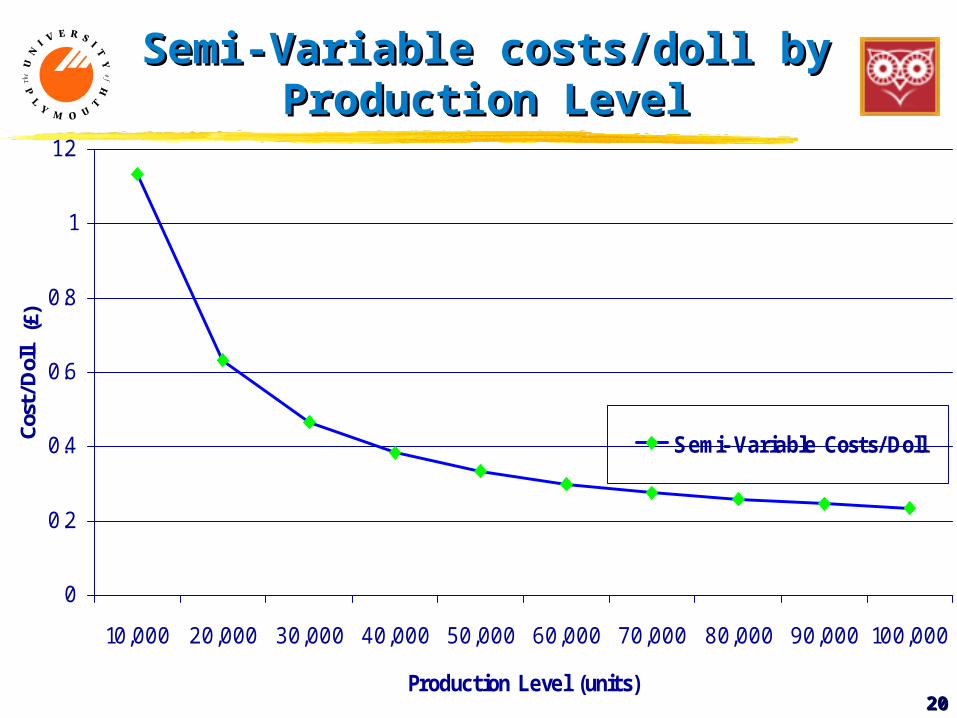

Semi-Variable costs/doll by Semi-Variable costs/doll by Production LevelProduction Level

0

0.2

0.4

0.6

0.8

1

1.2

10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Production Level (units)

Cost

/Dol

l (£

)

Semi- Variable Costs/Doll

2121

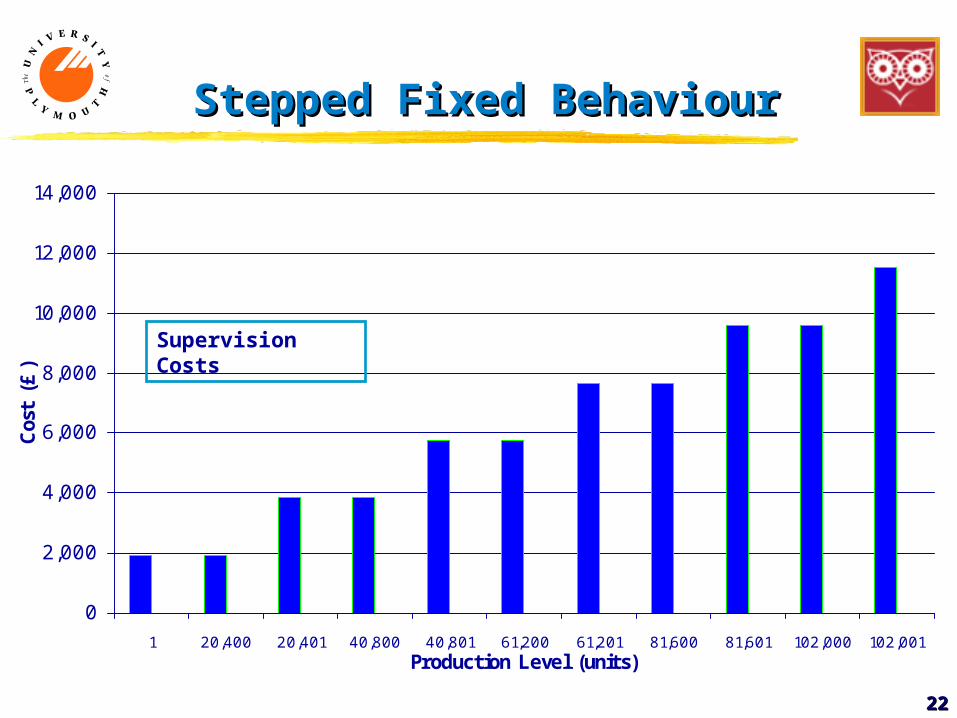

Costs categorised on the basis of Costs categorised on the basis of behaviourbehaviour with changing production levelswith changing production levels

stepped-fixedstepped-fixed

behave as fixed costs over a specific but behave as fixed costs over a specific but limited range of activity then change limited range of activity then change dramaticallydramatically

eg?eg? supervision costssupervision costs some mechanisation costssome mechanisation costs

see graphsee graph

Categorising Costs 2 Categorising Costs 2

2222

Stepped Fixed BehaviourStepped Fixed Behaviour

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1 20,400 20,401 40,800 40,801 61,200 61,201 81,600 81,601 102,000 102,001Production Level (units)

Cos

t (£

)

Supervision Costs

2323

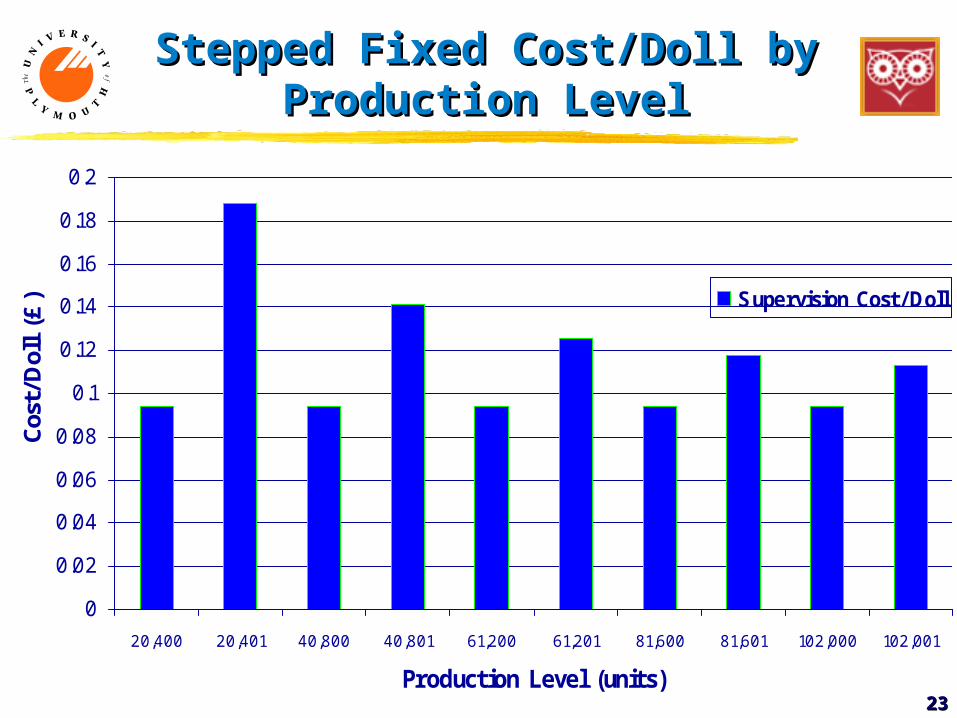

Stepped Fixed Cost/Doll by Stepped Fixed Cost/Doll by Production LevelProduction Level

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

20,400 20,401 40,800 40,801 61,200 61,201 81,600 81,601 102,000 102,001

Production Level (units)

Cos

t/D

oll

(£) Supervision Cost/Doll

2424

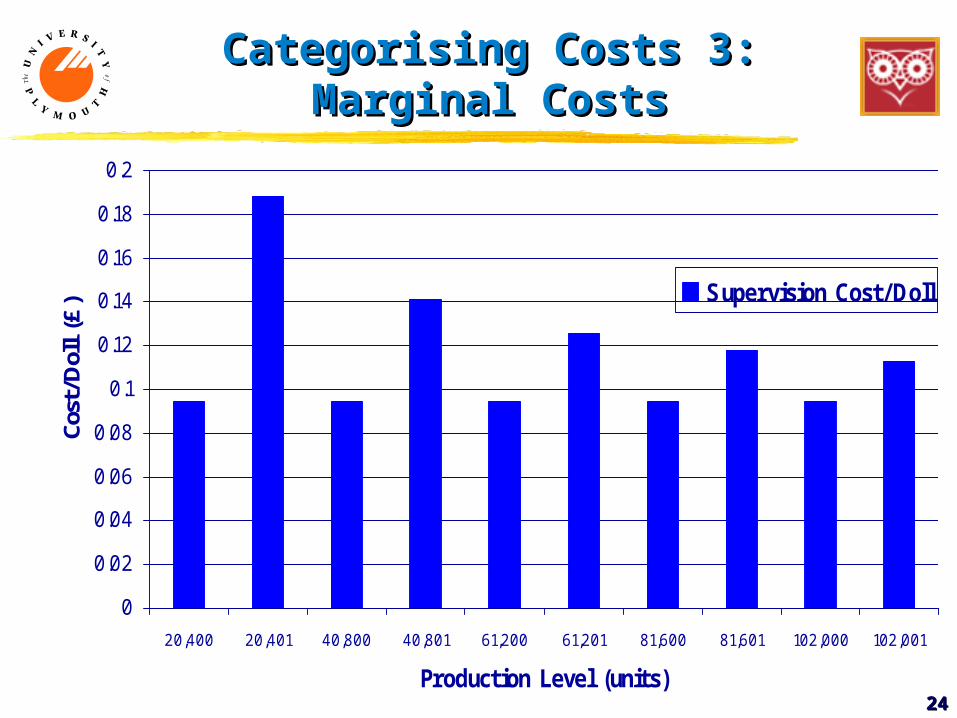

Categorising Costs 3: Categorising Costs 3: Marginal CostsMarginal Costs

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

20,400 20,401 40,800 40,801 61,200 61,201 81,600 81,601 102,000 102,001

Production Level (units)

Cost

/Dol

l (£

) Supervision Cost/Doll

2525

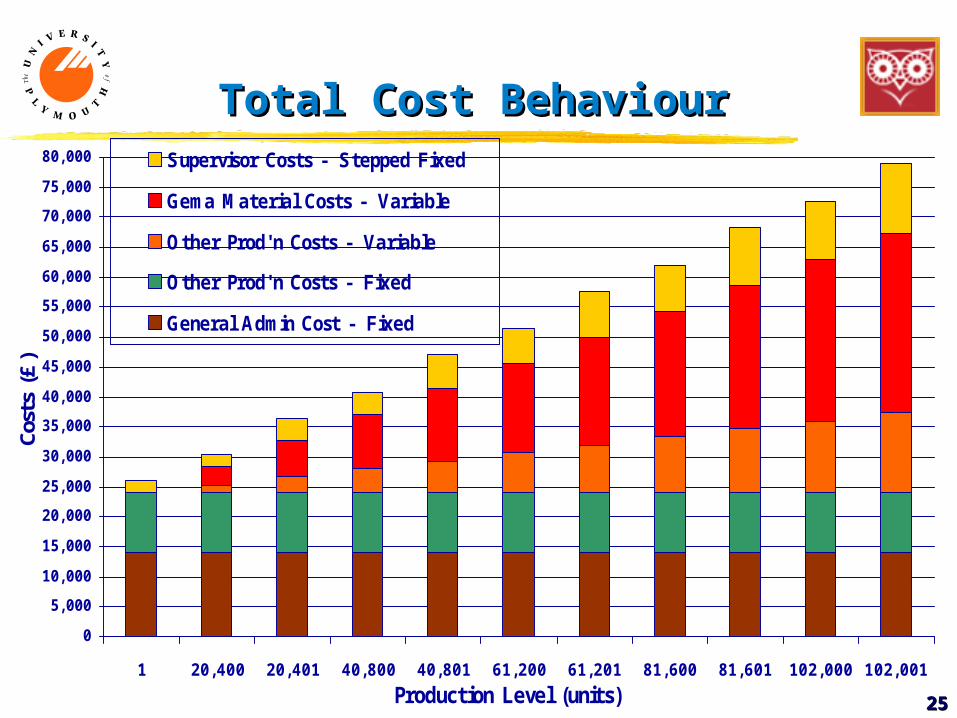

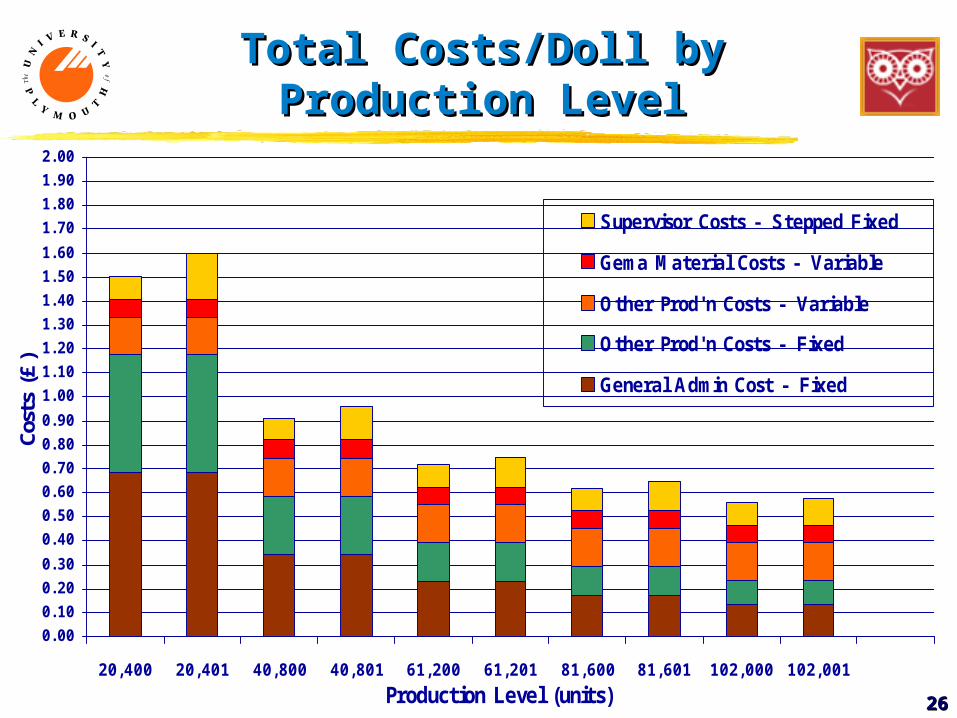

Total Cost Behaviour Total Cost Behaviour

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

80,000

1 20,400 20,401 40,800 40,801 61,200 61,201 81,600 81,601 102,000 102,001

Production Level (units)

Cost

s (£

)

Supervisor Costs - Stepped Fixed

Gema Material Costs - Variable

Other Prod'n Costs - Variable

Other Prod'n Costs - Fixed

General Admin Cost - Fixed

2626

Total Costs/Doll by Total Costs/Doll by Production LevelProduction Level

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

20,400 20,401 40,800 40,801 61,200 61,201 81,600 81,601 102,000 102,001

Production Level (units)

Cost

s (£

)

Supervisor Costs - Stepped Fixed

Gema Material Costs - Variable

Other Prod'n Costs - Variable

Other Prod'n Costs - Fixed

General Admin Cost - Fixed

2727

Total Costs Behaviour?Total Costs Behaviour?

How will the cost per doll change with increased How will the cost per doll change with increased production?production?

What do we call this phenomenon?What do we call this phenomenon?

Does this principal invariably work?Does this principal invariably work?

Can you think of a wider impact of this Can you think of a wider impact of this phenomenon?phenomenon?

2828

Why do women live longer than Why do women live longer than men?men?

2929

3030

EUE43E: ‘Trade & EUE43E: ‘Trade & Commerce’Commerce’

Understanding Break-Even Understanding Break-Even

Robert J. WilliamsRobert J. Williams

3131

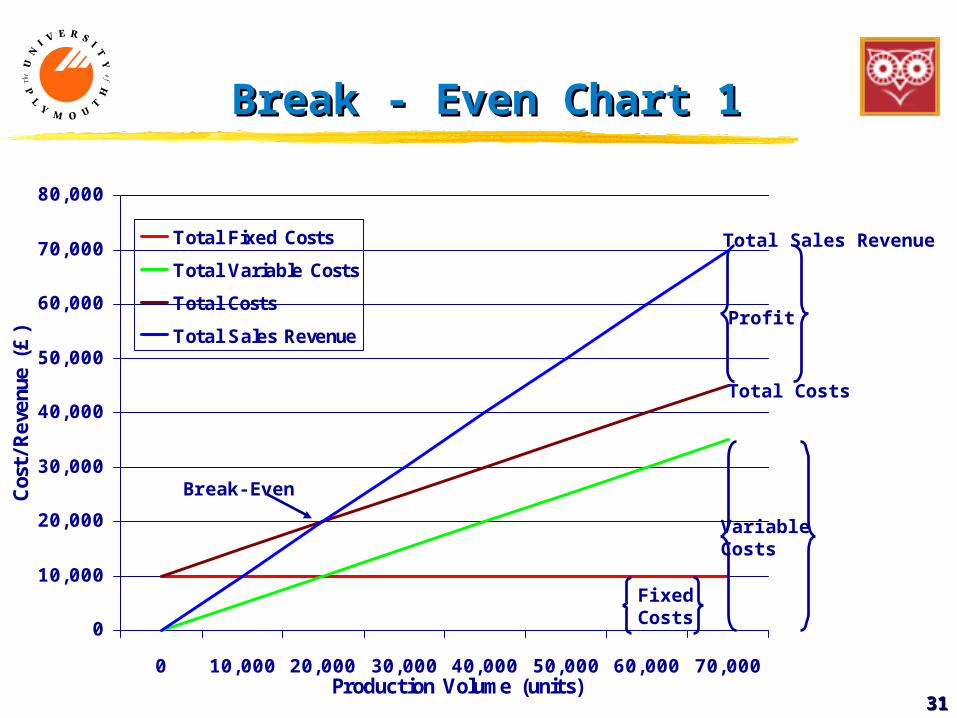

Break - Even Chart 1Break - Even Chart 1

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000Production Volume (units)

Cos

t/Rev

enue

(£

)

Total Fixed Costs

Total Variable Costs

Total Costs

Total Sales Revenue

FixedCosts

Variable Costs

Total Costs

Total Sales Revenue

Profit

Break-Even

3232

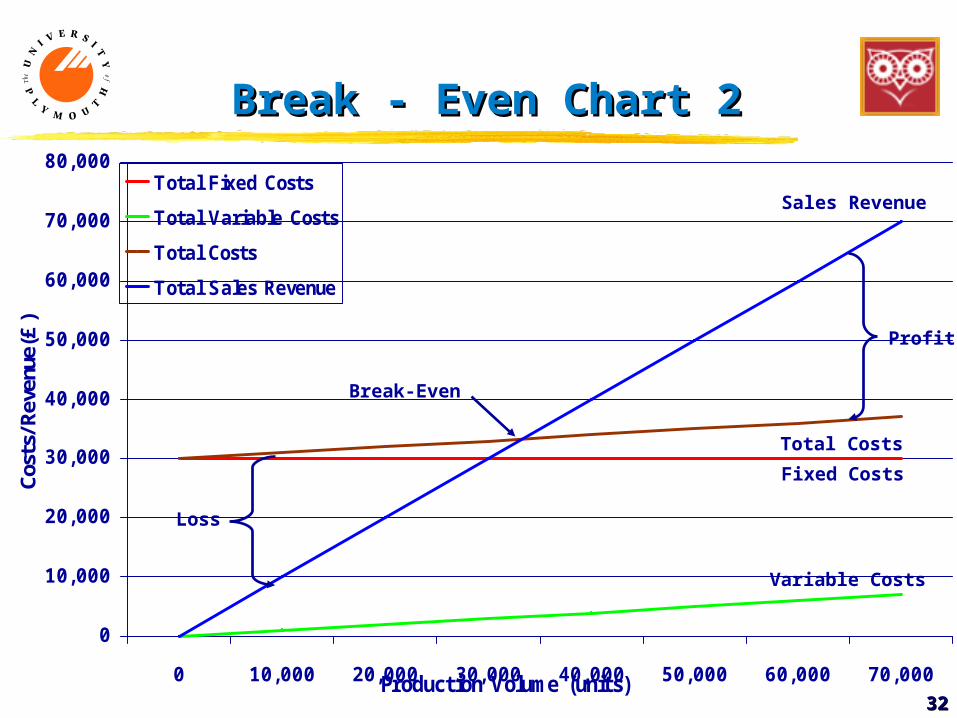

Break - Even Chart 2Break - Even Chart 2

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000Production Volume (units)

Cos

ts/R

even

ue(£

)

Total Fixed Costs

Total Variable Costs

Total Costs

Total Sales Revenue

Fixed Costs

Variable Costs

Total Costs

Sales Revenue

Profit

Loss

Break-Even

3333

3434

EUE43E: ‘Trade & EUE43E: ‘Trade & Commerce’Commerce’

ProductProduct Pricing Pricing

Robert J. WilliamsRobert J. Williams

3535

PricingPricing

The Accountants approach....The Accountants approach....

cost cost plusplus what you think a competitive what you think a competitive market will bear?market will bear?

consider:consider: price sensitivity (elasticity) of demandprice sensitivity (elasticity) of demand marketing effortsmarketing efforts customer loyalty effectscustomer loyalty effects product differentiation (marketing)product differentiation (marketing)

cost cost minus minus penetration pricing with loss leaderspenetration pricing with loss leaders

3636

Demand Price InelasticDemand Price Inelastic£

0.0

0£

2.0

0£

4.0

0£

6.0

0

0

6,0

00

12,0

00

18,0

00

24,0

00

30,0

00

36,0

00

42,0

00

48,0

00

54,0

00

60,0

00

DemandPri

ce p

er

Doll (

£)

Quantity Demanded (Dolls)

P2

Q2

P1

Q1

3737

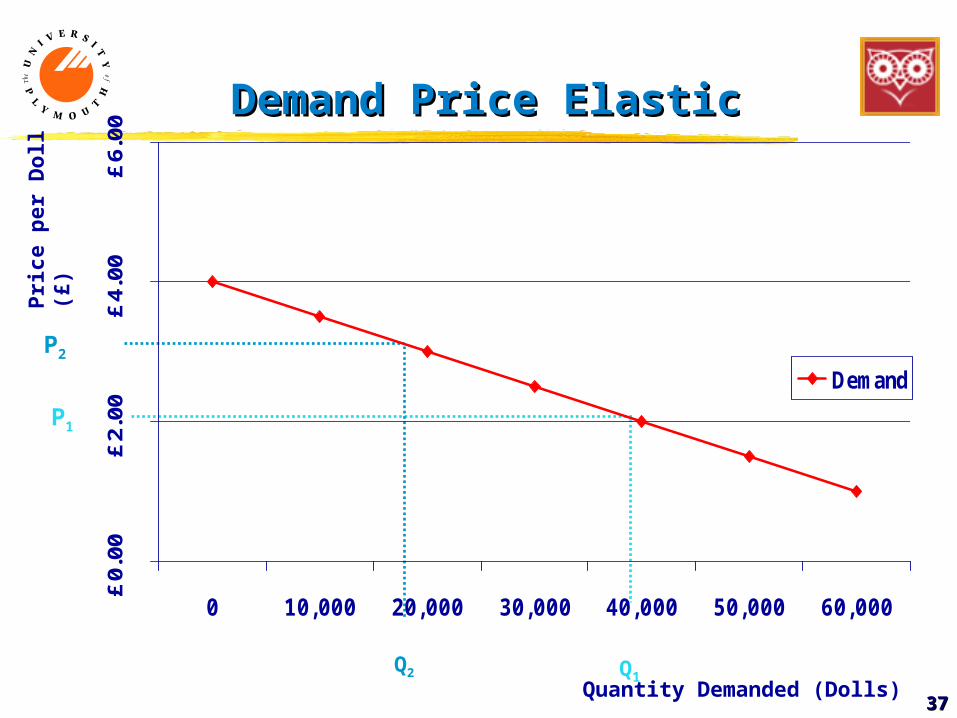

Demand Price ElasticDemand Price Elastic

P1

Q1

P2

Q2

£0.

00£

2.00

£4.

00£

6.00

0 10,000 20,000 30,000 40,000 50,000 60,000

Demand

Pri

ce p

er

Doll

(£)

Quantity Demanded (Dolls)

What you need to do…What you need to do…

Period 5 Period 5 decisions bydecisions by 12.00 12.00 & & Period 6 Period 6 decisions bydecisions by 16.0016.00

In e-mail ‘In e-mail ‘subject’subject’ put put Team Number, Team NameTeam Number, Team Name and and Decision Number (D2)Decision Number (D2)

Put all Results onto Put all Results onto Bosscat Business Management Bosscat Business Management Simulation Trend Analysis Data Sheet Blank Simulation Trend Analysis Data Sheet Blank and try and try to understand what they tell you about your to understand what they tell you about your business?business?

3838

3939

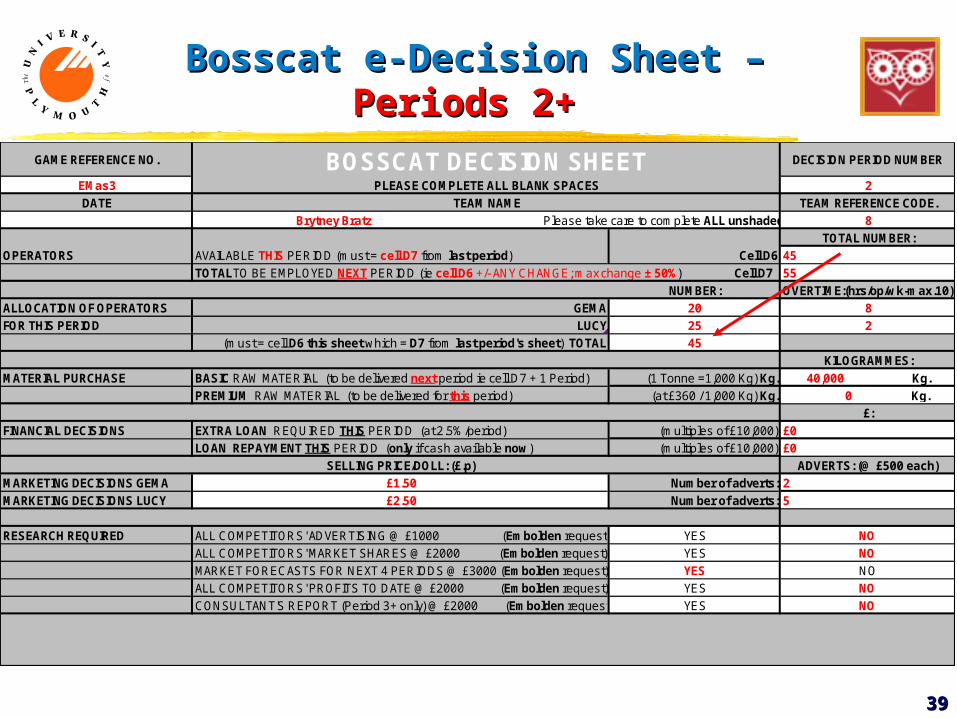

Bosscat e-Decision Sheet – Bosscat e-Decision Sheet – Periods 2+Periods 2+

GAME REFERENCE NO. DECISION PERIOD NUMBER

EMas3 2DATE TEAM REFERENCE CODE.

8TOTAL NUMBER:

OPERATORS AVAILABLE THIS PERIOD (must = cell D7 from last period) Cell D6 4555

NUMBER: OVERTIME:(hrs/op/wk-max.10)ALLOCATION OF OPERATORS GEMA 20 8FOR THIS PERIOD LUCY 25 2

(must = cell D6 this sheet which = D7 from last period's sheet) TOTAL 45KILOGRAMMES:

MATERIAL PURCHASE BASIC RAW MATERIAL (to be delivered next period ie cell D7 + 1 Period) (1 Tonne =1,000 Kg) Kg. 40,000 Kg.PREMIUM RAW MATERIAL (to be delivered for this period) (at £360 / 1,000 Kg) Kg. 0 Kg.

£:FINANCIAL DECISIONS EXTRA LOAN REQUIRED THIS PERIOD (at 2.5%/period) (multiples of £10,000) £0

LOAN REPAYMENT THIS PERIOD (only if cash available now) (multiples of £10,000) £0SELLING PRICE/DOLL: (£.p) ADVERTS: (@ £500 each)

MARKETING DECISIONS GEMA £1.50 Number of adverts: 2MARKETING DECISIONS LUCY £2.50 Number of adverts: 5

RESEARCH REQUIRED ALL COMPETITORS' ADVERTISING @ £1000 (Embolden request) YES NO ALL COMPETITORS' MARKET SHARES @ £2000 (Embolden request) YES NO MARKET FORECASTS FOR NEXT 4 PERIODS @ £3000 (Embolden request) YES NO ALL COMPETITORS' PROFITS TO DATE @ £2000 (Embolden request) YES NO CONSULTANT'S REPORT (Period 3+ only) @ £2000 (Embolden request) YES NO

TOTALTO BE EMPLOYED NEXT PERIOD (ie cell D6 +/- ANY CHANGE; max change ± 50%) Cell D7

PLEASE COMPLETE ALL BLANK SPACESTEAM NAME

BOSSCAT DECISION SHEET

Brytney Bratz Please take care to complete ALL unshaded cells correctly.

4040

EUE43E: ‘Trade & EUE43E: ‘Trade & Commerce’Commerce’

The EndThe End

Robert WilliamsRobert Williams