Embed Size (px)

Citation preview

1

Information System AuditEssential of IS Audit for IT Engineer

UP-ITTCOctober. 2010

2

SummaryInformation system Audit (IS Audit), is needed long experience and lot of skill and knowledge about both Audit and Information Technology. Because of this, This training course and text book include summary of knowledge and skill that IS Auditor needs and especially detail skill and knowledge about IS Audit processes and methods for IT engineers who want to become IS Auditor or conduct audit tasks.

AcknowledgmentsContent of this training and text book is based on Certified Information Systems Auditor (CISA) and Japan Information Technology Engineers Examination- .System Auditor ExaminationContent of this training and text book is copyrighted to JICA (Japan International Cooperation Agency) and UP-ITTC(UP Information Technology Training Center), and developed by Go Ota, PADECO Co., Ltd. and UP-ITTC

Expected TraineesIS Audit is needed wide area of IT skill and knowledge, the training expects the trainees have ,at least, passed FE exam or have had same level of IT experience (at least 5 five years, desirable more than 10 years) and knowledge.

U

3

Chapter 0.Introduction

What is IS Audit

How to become IS Auditor &

Task and role of IS Auditor

U

4

What is Audit? What is IS Audit?

“An official examination of accounts to see that they are in order” – The Oxford DictionaryAn INDEPENDENT assessment of / opinion on how well

(badly) the financial statements were prepared

IS audit:- A review of the controls within an entity's technology

infrastructure- Official examination of IT related processes to see that

they are in order

U

5

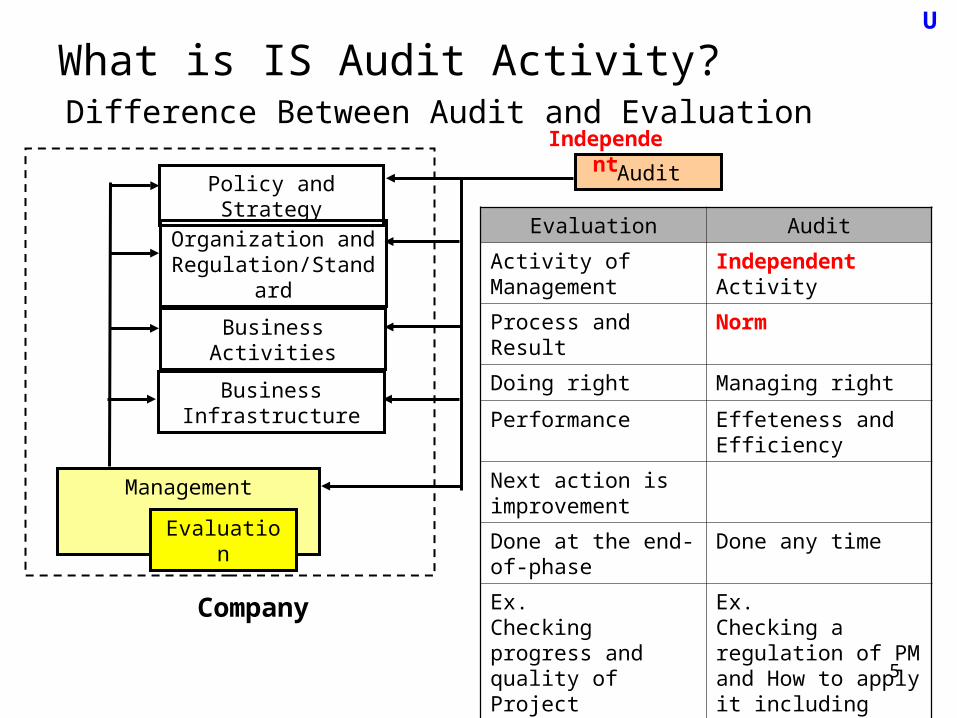

What is IS Audit Activity?Difference Between Audit and Evaluation

U

Policy and Strategy

Organization and Regulation/Standard

Business Activities

Business Infrastructure

Management

Evaluation

Audit

Independent

Evaluation Audit

Activity of Management

Independent Activity

Process and Result Norm

Doing right Managing right

Performance Effeteness and Efficiency

Next action is improvement

Done at the end-of-phase

Done any time

Ex.Checking progress and quality of Project

Ex.Checking a regulation of PM and How to apply it including current situation.

Company

6

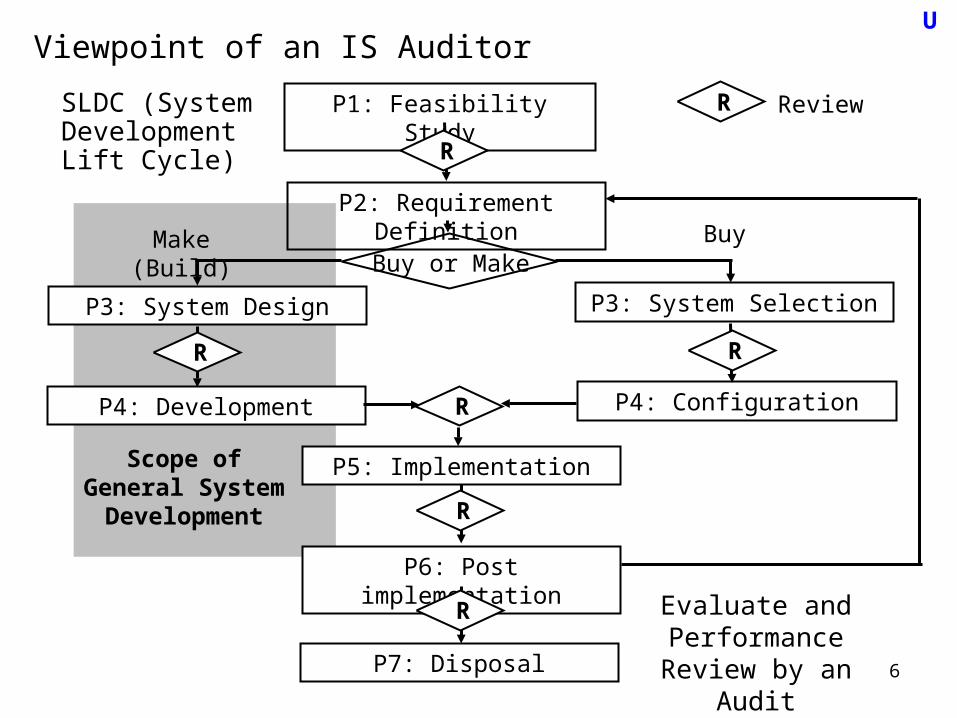

Viewpoint of an IS AuditorU

P1: Feasibility Study

P2: Requirement Definition

P3: System Design

P4: Development

P3: System Selection

P4: Configuration

P5: Implementation

Review

P6: Post implementation

P7: Disposal

R

Buy or Make

R

R

R R

R

R

BuyMake (Build)

Scope of General System

Development

SLDC (System Development Lift Cycle)

Evaluate and Performance

Review by an Audit

7

Why IS Audit is needed? Social BackgroundInformation System has been becoming a main function for business.•Supporting business activity•Keeping business information•Main interface to customer

U

Innovation of ICT gave information system major role in business

Problem of business management•Inappropriate IT system to business strategy• Bug investment for IT system and unclear ROI

Problem of security/ risk management• Computer virus/ illegal Access• System trouble and Backup of disaster

Effective and Efficient inter management and operation for Information system should be needed

Independent Information System Audit

8

Why IS Audit is needed? Legal Background (1)

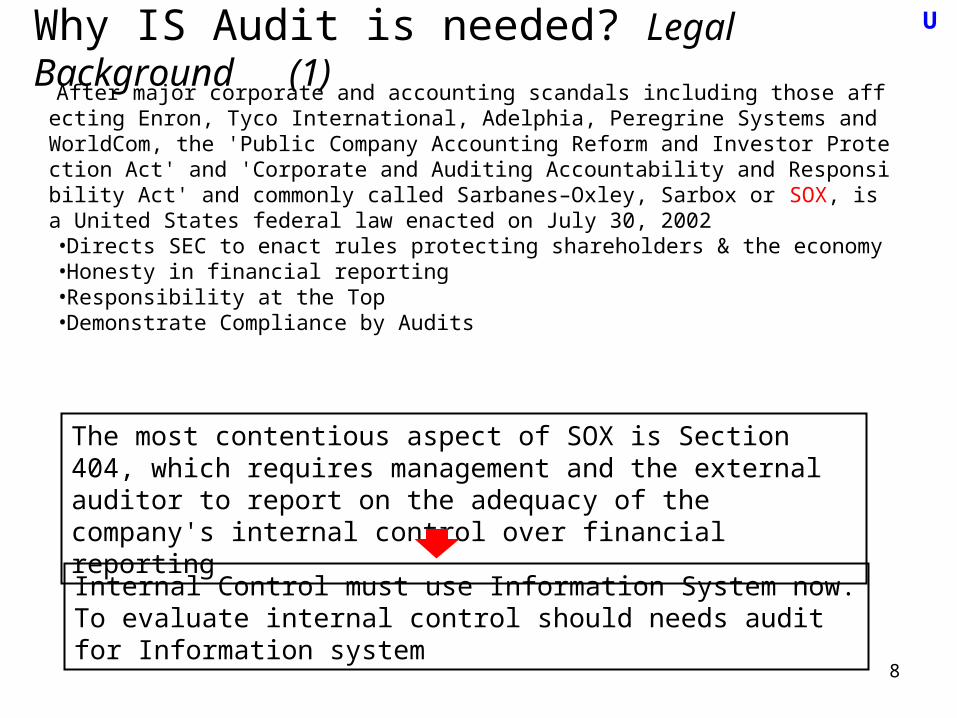

After major corporate and accounting scandals including those affecting Enron, Tyco International, Adelphia, Peregrine Systems and WorldCom, the 'Public Company Accounting Reform and Investor Protection Act' and 'Corporate and Auditing Accountability and Responsibility Act' and commonly called Sarbanes–Oxley, Sarbox or SOX, is a United States federal law enacted on July 30, 2002•Directs SEC to enact rules protecting shareholders & the economy•Honesty in financial reporting•Responsibility at the Top•Demonstrate Compliance by Audits

U

The most contentious aspect of SOX is Section 404, which requires management and the external auditor to report on the adequacy of the company's internal control over financial reporting

Internal Control must use Information System now. To evaluate internal control should needs audit for Information system

9

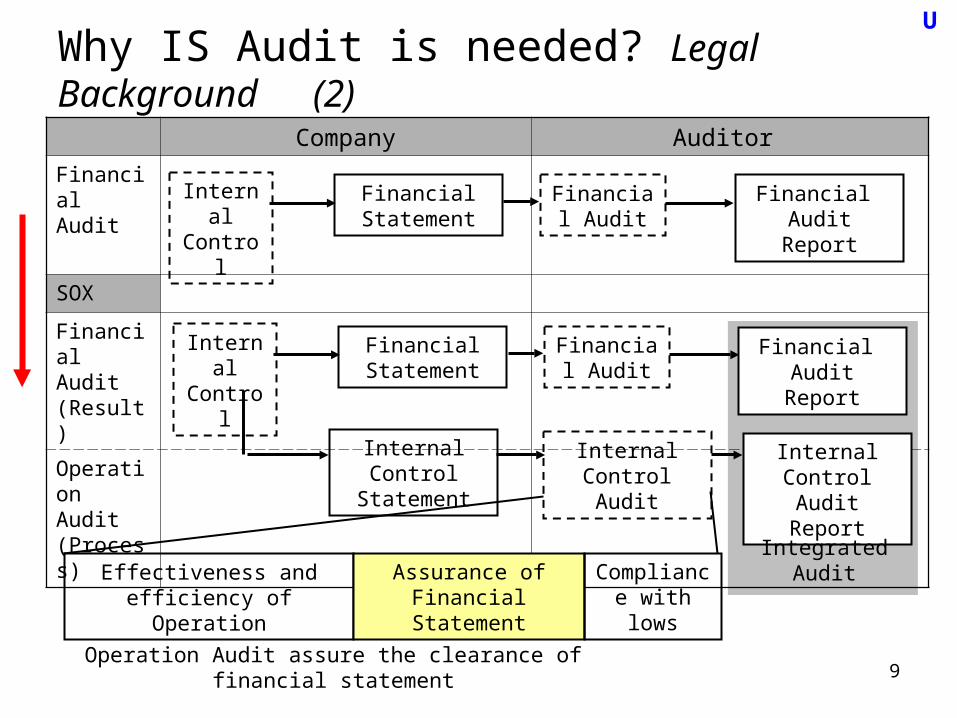

Why IS Audit is needed? Legal Background (2)

U

Company Auditor

Financial Audit

SOX

Financial Audit (Result)

Operation Audit (Process)

Internal Control

Financial Audit Report

Financial Audit

Financial Statement

Internal Control

Financial Audit Report

Financial Audit

Financial Statement

Internal Control Statement

Internal Control Audit

Internal Control Audit Report

IntegratedAudit

Operation Audit assure the clearance of financial statement

Effectiveness and efficiency of Operation

Assurance of Financial Statement

Compliance with lows

10

What is Internal Control?U

Internal Control Model by SOCOObjectives

Control Environment

Risk Management

Control Activity

Information and Communication

Monitoring

IT Control

Ope

ratio

n

Rep

ortin

g

Com

plia

nce

Activities

OrganizationEnterprise-level, Division or subsidiary and Business unit

Objective Risk Control

Financial Statement

11

Activities of Internal ControlU

Control Environment

The tone for the organization, influencing the control consciousness of its people. It is the foundation for all other components of internal control.

Risk Management The identification and analysis of relevant risks to the achievement of objectives, forming a basis for how the risks should be managed

Control Activity The policies and procedures that help ensure management directives are carried out.Consists of 2 aspects: Policy of what should be and Procedures to accomplish policy

Information and Communication

Support the identification, capture, and exchange of information in a form and time frame that enable people to carry out their responsibilities

Monitoring Assess the quality of internal control performance over time.

IT Control Procedure or policy that provides a reasonable assurance that the information technology (IT) used by an organization

12

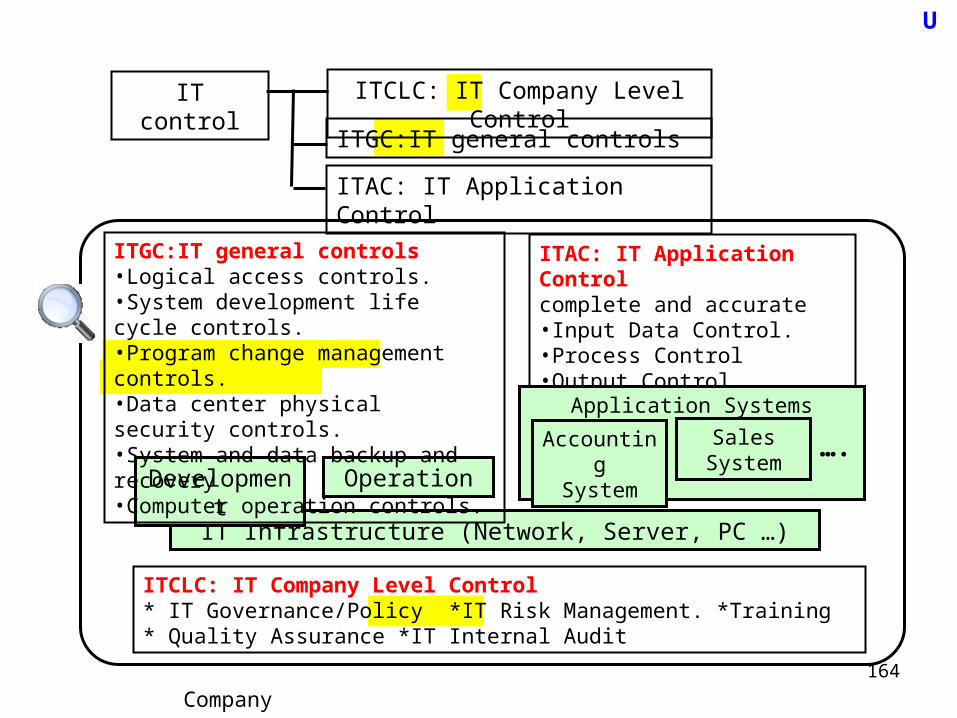

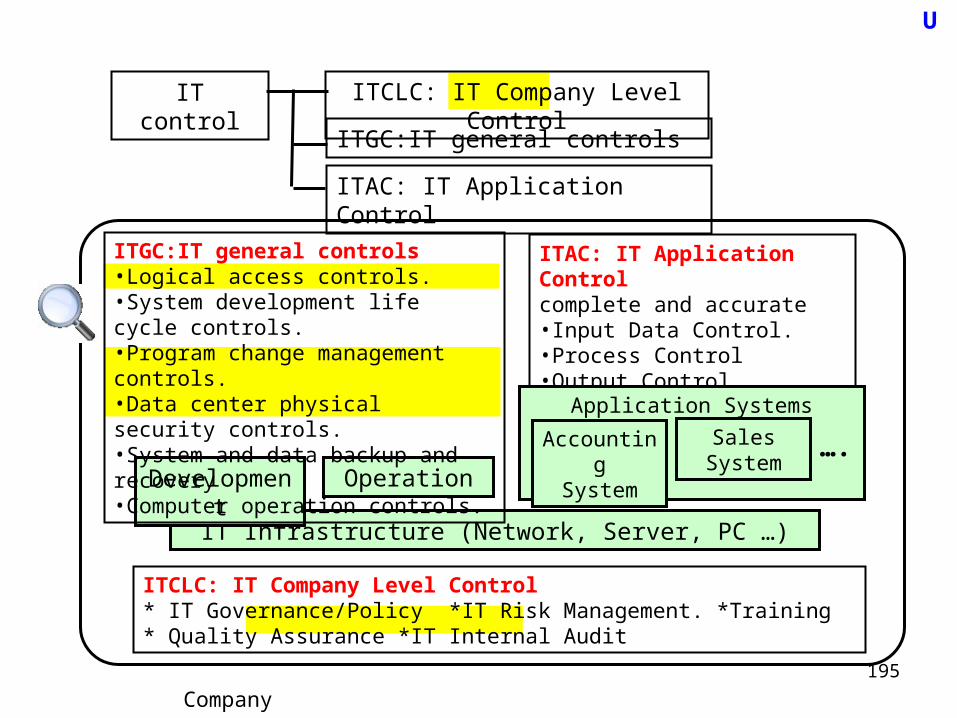

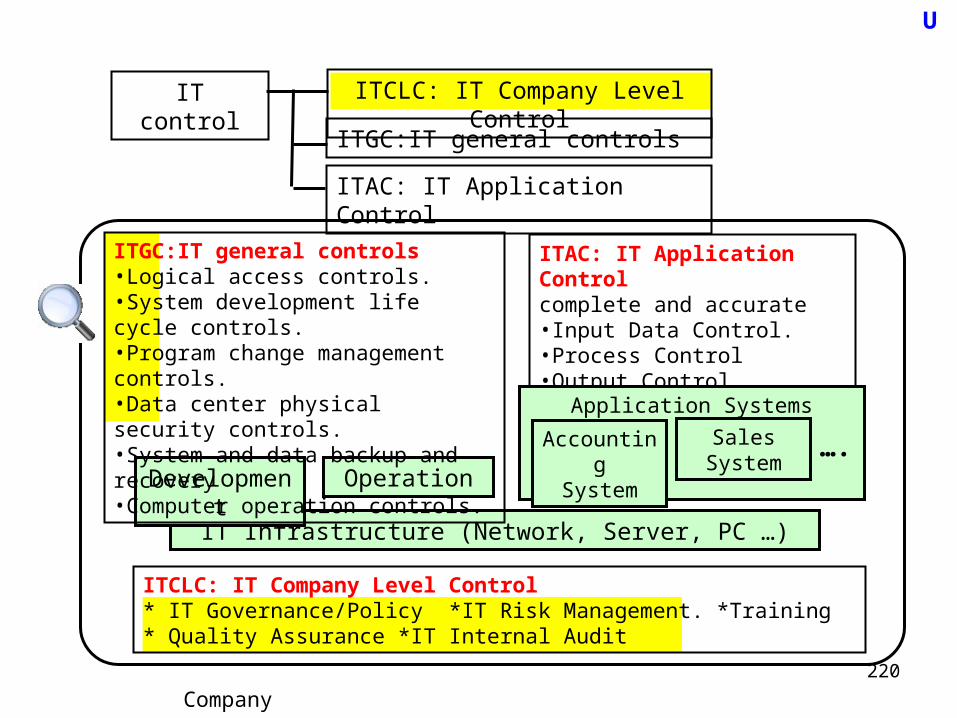

IT Internal Control <= Target of IS AuditU

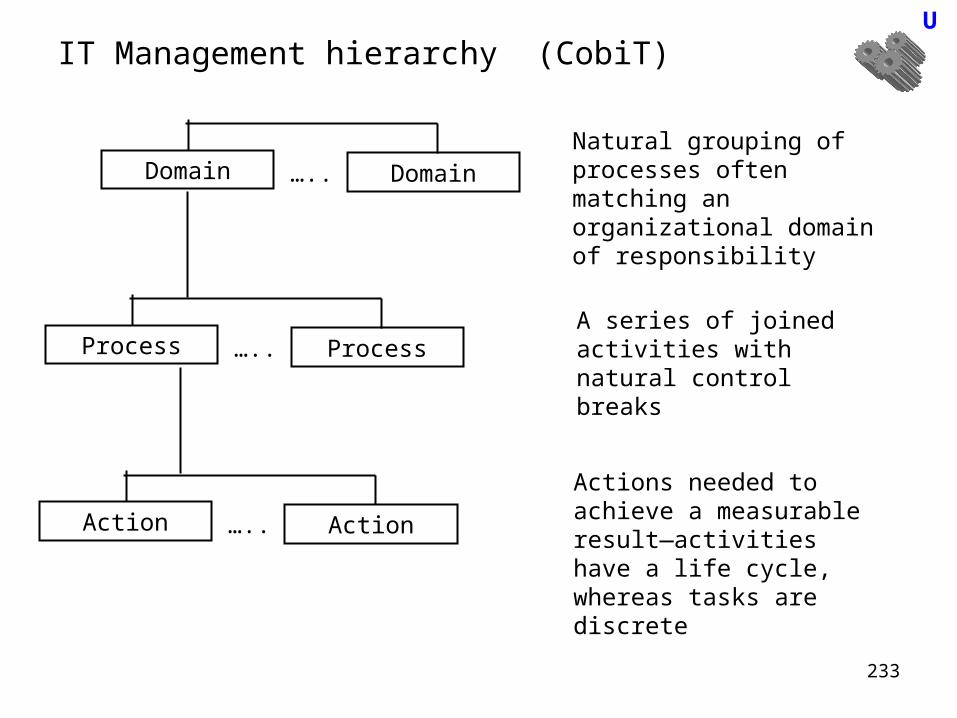

IT control

ITGC:IT general controls

ITCLC: IT Company Level Control

ITAC: IT Application Control

ITGC:IT general controls•Logical access controls.•System development life cycle controls.•Program change management controls.•Data center physical security controls.•System and data backup and recovery•Computer operation controls.

ITCLC: IT Company Level Control* IT Governance/Policy *IT Risk Management. *Training* Quality Assurance *IT Internal Audit

IT Infrastructure (Network, Server, PC …)

Development Operation

ITAC: IT Application Controlcomplete and accurate •Input Data Control.•Process Control•Output Control

Application Systems

AccountingSystem

Sales System

Company

….

13

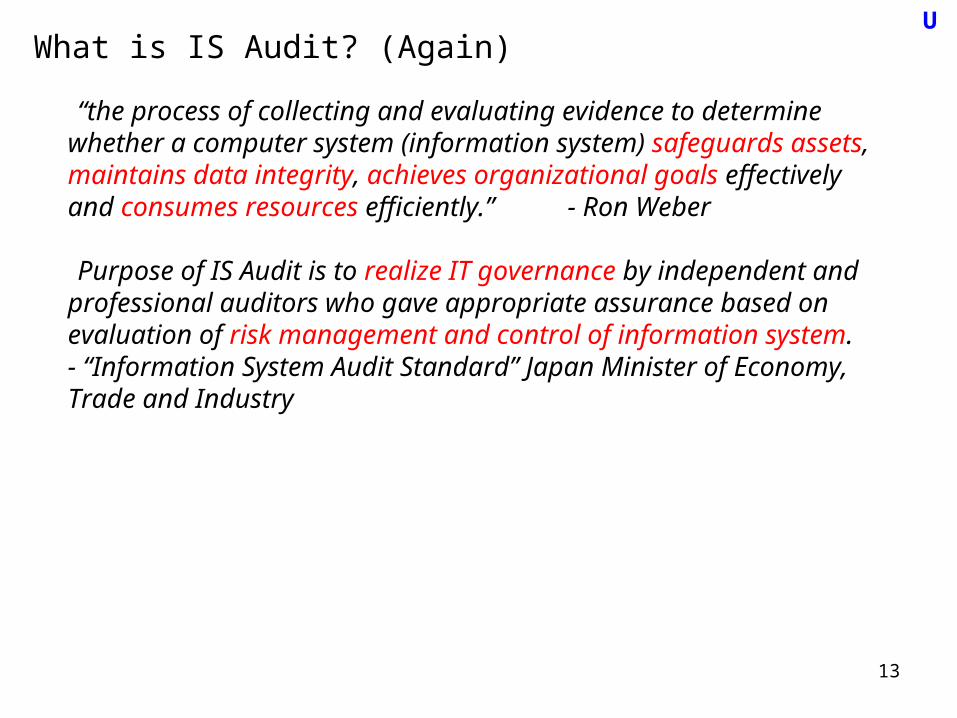

What is IS Audit? (Again)

“the process of collecting and evaluating evidence to determine whether a computer system (information system) safeguards assets, maintains data integrity, achieves organizational goals effectively and consumes resources efficiently.” - Ron Weber

Purpose of IS Audit is to realize IT governance by independent and professional auditors who gave appropriate assurance based on evaluation of risk management and control of information system.- “Information System Audit Standard” Japan Minister of Economy, Trade and Industry

U

14

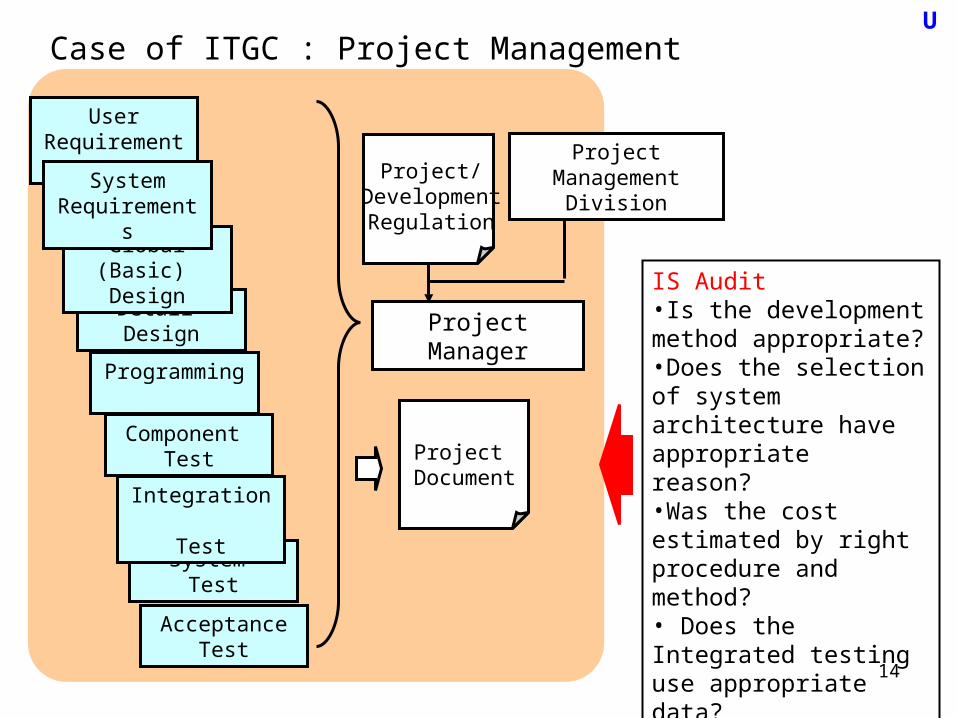

Case of ITGC : Project ManagementU

User Requirements

Detail Design

Acceptance Test

System Test

Integration Test

Global (Basic) Design

Component Test

System Requirements

Programming

Project Manager

Project Management

Division

Project/ Development

Regulation

Project Document

IS Audit•Is the development method appropriate?•Does the selection of system architecture have appropriate reason?•Was the cost estimated by right procedure and method?• Does the Integrated testing use appropriate data?•Does the project follow the regulation

15

Who becomes an Auditor?U

(Account)Auditor

IT Specialist

With experiences of • Accounting• Audit

With experiences of • IT Strategy• Development• Project Management• IT Security• Service Management…..

Information System Audit

CertificationCISA (Certified Information Systems Auditor) by ISACA (Information Systems Audit and Control Association) From 1978•More than 75,000 professionals in nearly 160 countries•for both (Account) Auditor and IT Specialist

System Auditor by Japan Information Technology Engineers Examination) From 1985• mainly for IT Specialist

If (Account ) Auditor want to become IS auditor, he/she should master as least skill and knowledge of FE exam. Level.

16

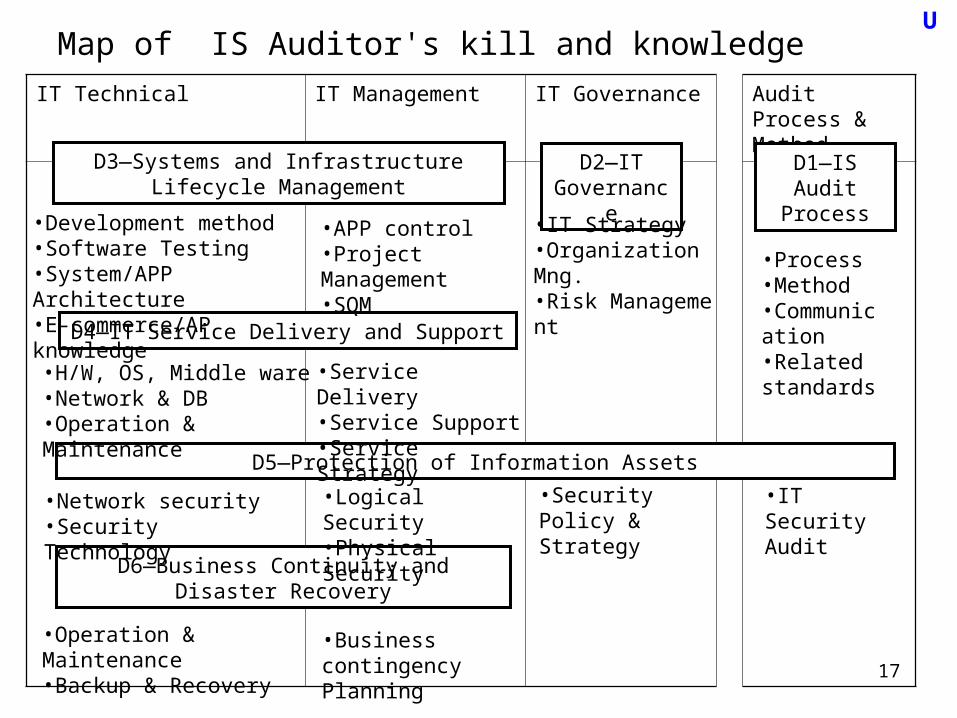

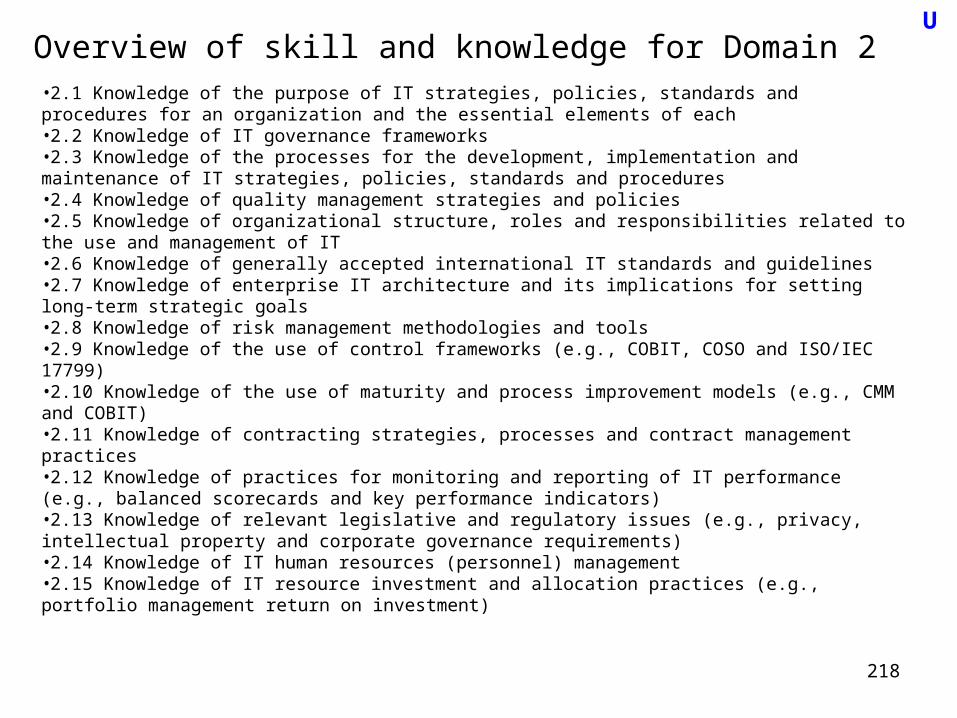

Target of IS Audit and IS Auditor's Skill and Knowledge

CISA examination domains (% of num. of question in CISA exam.)

•Domain 1—IS Audit Process (10%) <= Skill and Knowledge for conducting IT Audit

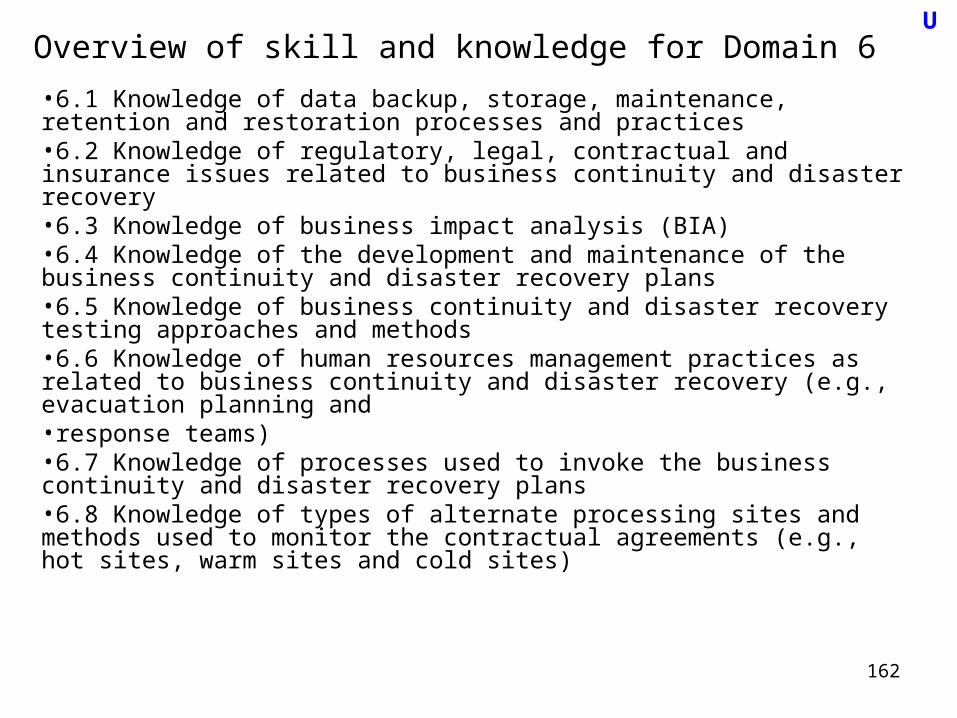

•Domain 2—IT Governance (15%)•Domain 3—Systems and Infrastructure Lifecycle Management (16%)•Domain 4—IT Service Delivery and Support (14%)•Domain 5—Protection of Information Assets (31%)•Domain 6—Business Continuity and Disaster Recovery (14%)

<= Target of IS Audit and Skill and knowledge for IT system and points of audits

U

17

Map of IS Auditor's kill and knowledgeU

IT Technical IT Management IT Governance Audit Process & Method

D3—Systems and Infrastructure Lifecycle Management

D1—IS Audit

Process

D2—IT Governance

D4—IT Service Delivery and Support

D5—Protection of Information Assets

D6—Business Continuity and Disaster Recovery

•IT Strategy•Organization Mng.•Risk Management

•Development method•Software Testing •System/APP Architecture•E-commerce/AP knowledge

•Service Delivery•Service Support•Service Strategy

•H/W, OS, Middle ware•Network & DB•Operation & Maintenance

•APP control•Project Management•SQM

•IT Security Audit

•Logical Security•Physical Security

•Security Policy & Strategy

•Network security•Security Technology

•Operation & Maintenance•Backup & Recovery

•Business contingency Planning

•Process•Method•Communication•Related standards

18

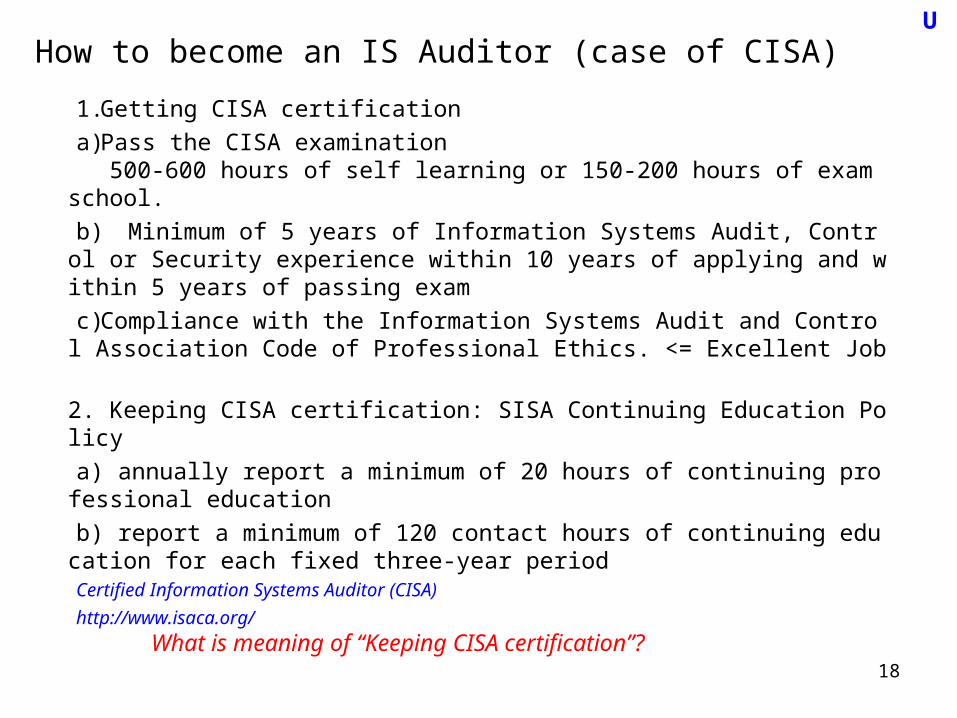

How to become an IS Auditor (case of CISA)

1.Getting CISA certification

a)Pass the CISA examination 500-600 hours of self learning or 150-200 hours of exam school.

b) Minimum of 5 years of Information Systems Audit, Control or Security experience within 10 years of applying and within 5 years of passing exam

c)Compliance with the Information Systems Audit and Control Association Code of Professional Ethics. <= Excellent Job

2. Keeping CISA certification: SISA Continuing Education Policy

a) annually report a minimum of 20 hours of continuing professional education

b) report a minimum of 120 contact hours of continuing education for each fixed three-year periodCertified Information Systems Auditor (CISA)

http://www.isaca.org/

What is meaning of “Keeping CISA certification”?

U

19

Professional Ethics (ISACA Code)

•Support the implementation of, and encourage compliance with, appropriate standards, procedures and controls for information systems.• Perform their duties with objectivity, due diligence and professional

care, in accordance with professional standards and best practices.• Serve in the interest of stakeholders in a lawful and honest

manner, while maintaining high standards of conduct and character, and not engage in acts discreditable to the profession.•Maintain the privacy and confidentiality of information obtained in

the course of their duties unless disclosure is required by legal authority. Such information shall not be used for personal benefit or released to inappropriate parties.• Maintain competency in their respective fields and agree to

undertake only those activities, which they can reasonably expect to complete with professional competence.• Inform appropriate parties of the results of work performed;

revealing all significant facts known to them.• Support the professional education of stakeholders in enhancing

their understanding of information systems security and control.

U

20

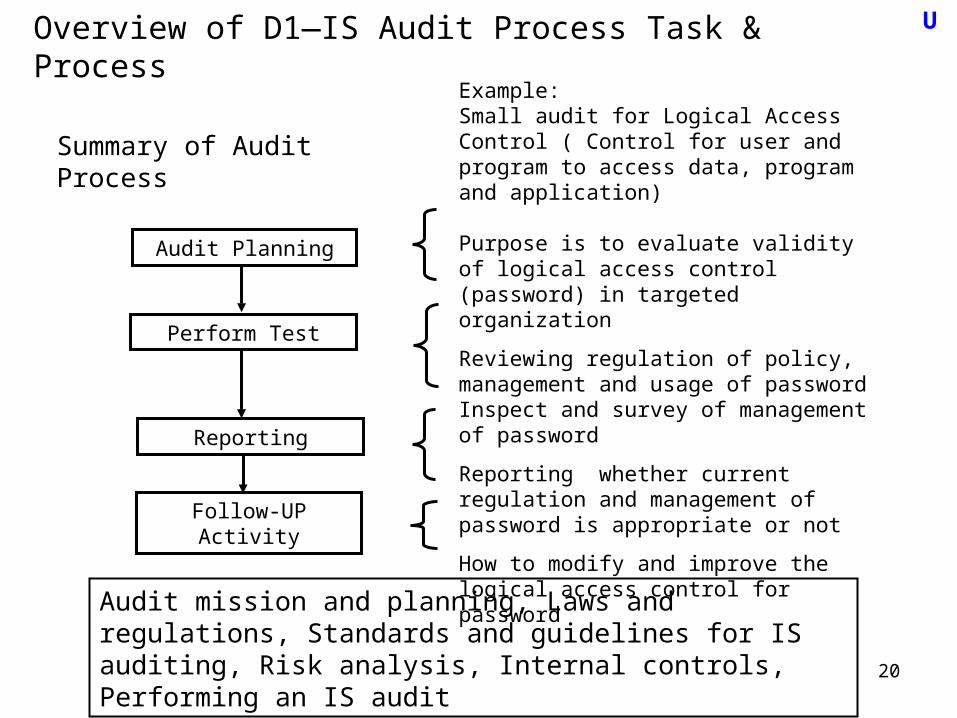

Overview of D1—IS Audit Process Task & ProcessU

Audit Planning

Perform Test

Reporting

Follow-UPActivity

Summary of Audit Process

Example: Small audit for Logical Access Control ( Control for user and program to access data, program and application)

Purpose is to evaluate validity of logical access control (password) in targeted organization

Reviewing regulation of policy, management and usage of passwordInspect and survey of management of password

Reporting whether current regulation and management of password is appropriate or not

How to modify and improve the logical access control for password

Audit mission and planning, Laws and regulations, Standards and guidelines for IS auditing, Risk analysis, Internal controls, Performing an IS audit

21

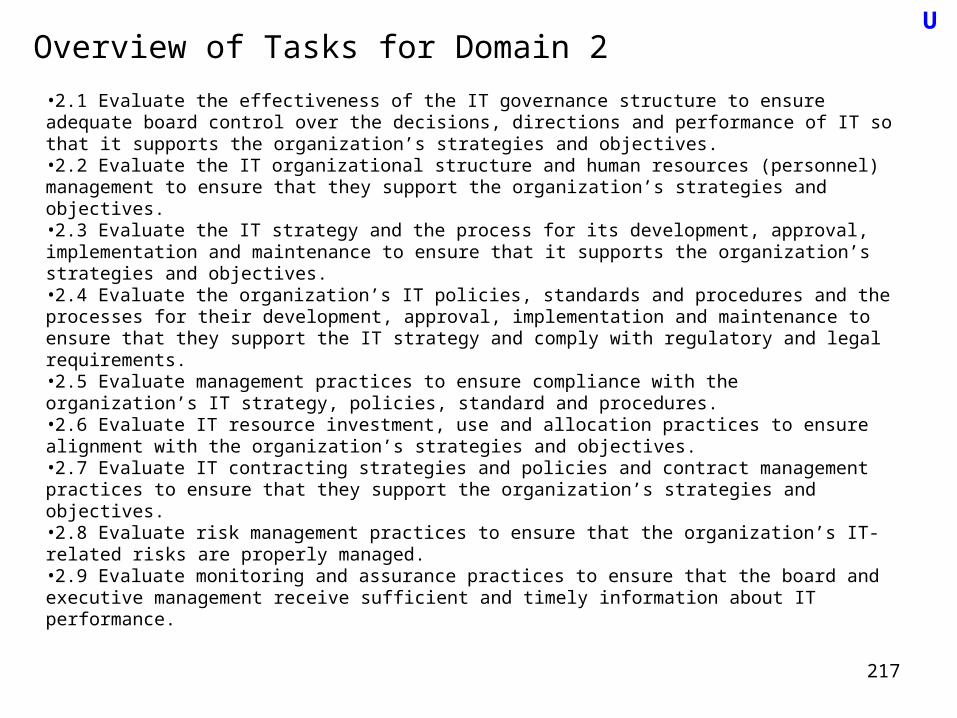

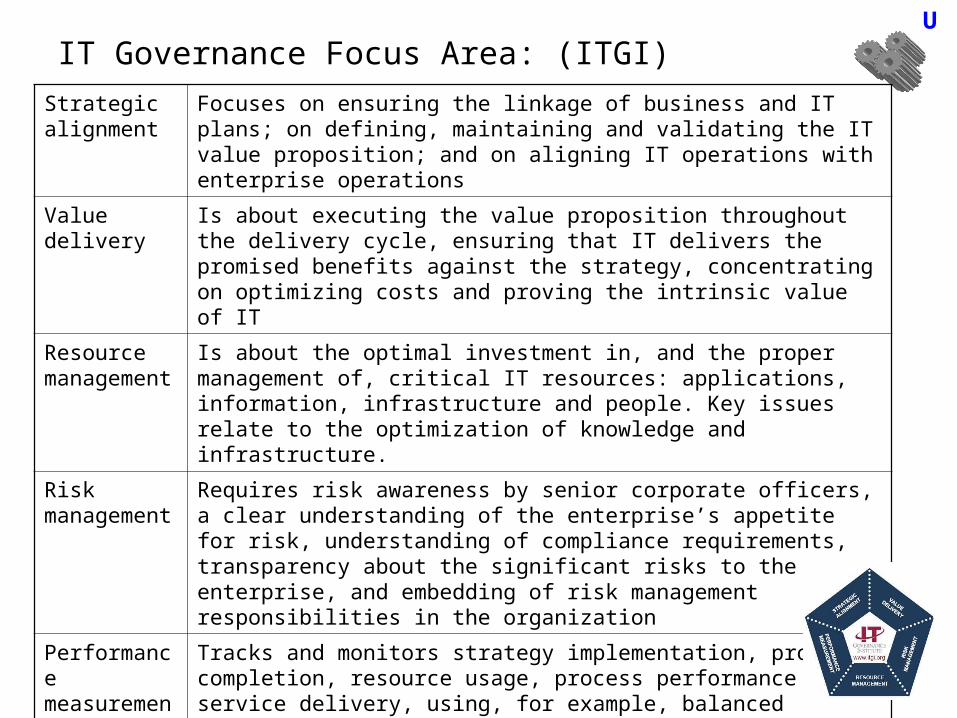

Overview of D2—IT Governance

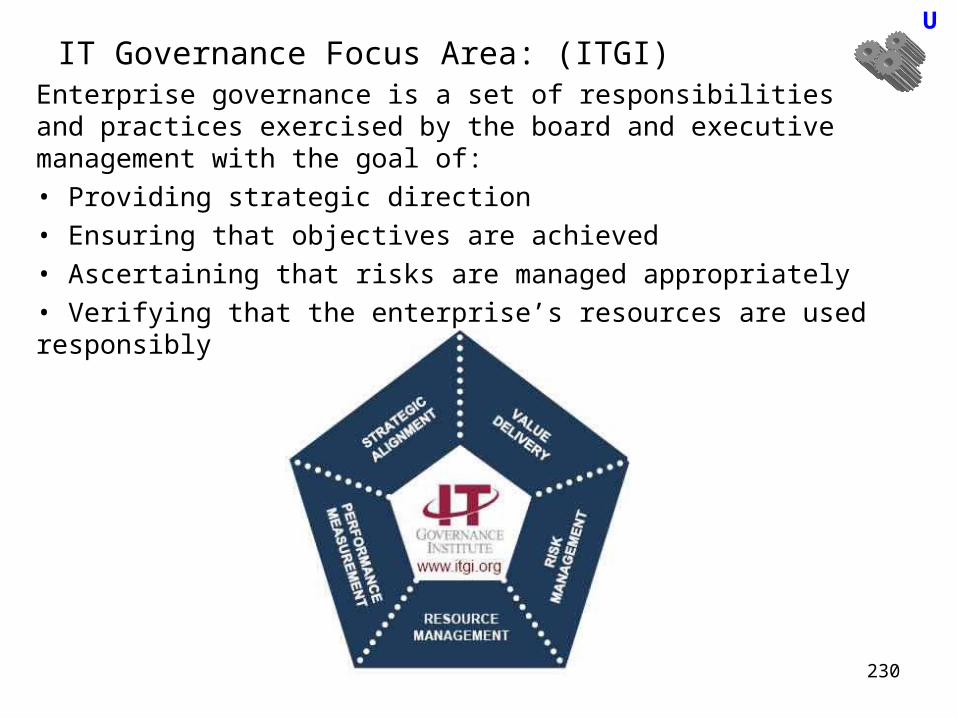

To provide assurance that the organization has the structure, policies, accountability, mechanisms, and monitoring practices in place to achieve the requirements of corporate governance of IT.

Examples of target • Planning IT Strategy with IT Steering Committee• Implementation of the IT strategy • Business Process Reengineering• Risk management for IT strategy• Organization and Personnel Management

U

22

Overview of D3—Systems and Infrastructure Lifecycle Management

To provide assurance that the management practices for the development/acquisition, testing, implementation, maintenance, and disposal of systems and infrastructure will meet the organization’s objectives.

Examples of target•Application development process and regulation including needs analysis, including cost estimation and •Quality Management•Validation of computer & system architecture for Application•Application control•Management of outsourcing and vender

U

23

Overview of D4—IT Service Delivery and Support

To provide assurance that the IT service management practices will ensure the delivery of the level of services required to meet the organization’s objectives.

Example of Target• Service level Agreement• Validation of Hardware and software• Validation of network infrastructure• Monitoring of Information System/Infrastructure• Capacity and Configuration Management• Configuration Management of software• Regulation of operation and maintenance • Help (Service) Desk and Incident/Problem management

U

24

Overview of D5—Protection of Information Assets

To provide assurance that the security architecture (policies, standards, procedures, and controls) ensures the confidentiality, integrity, and availability of information assets.

Examples of Target•Policy and regulation of IT Security including risk management•Validation of logical access control such as password and authentication•Validation of physical access control with security technology and devices• Validation of security of network infrastructure• Validation of encryption system• Validation of environmental control against fire, power break down and …

U

25

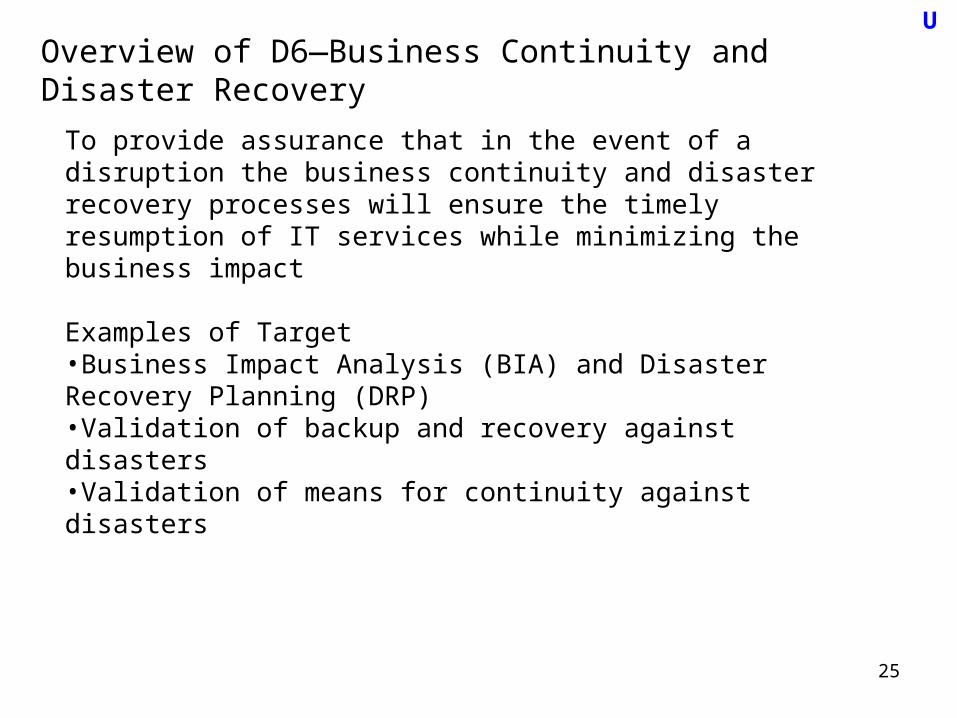

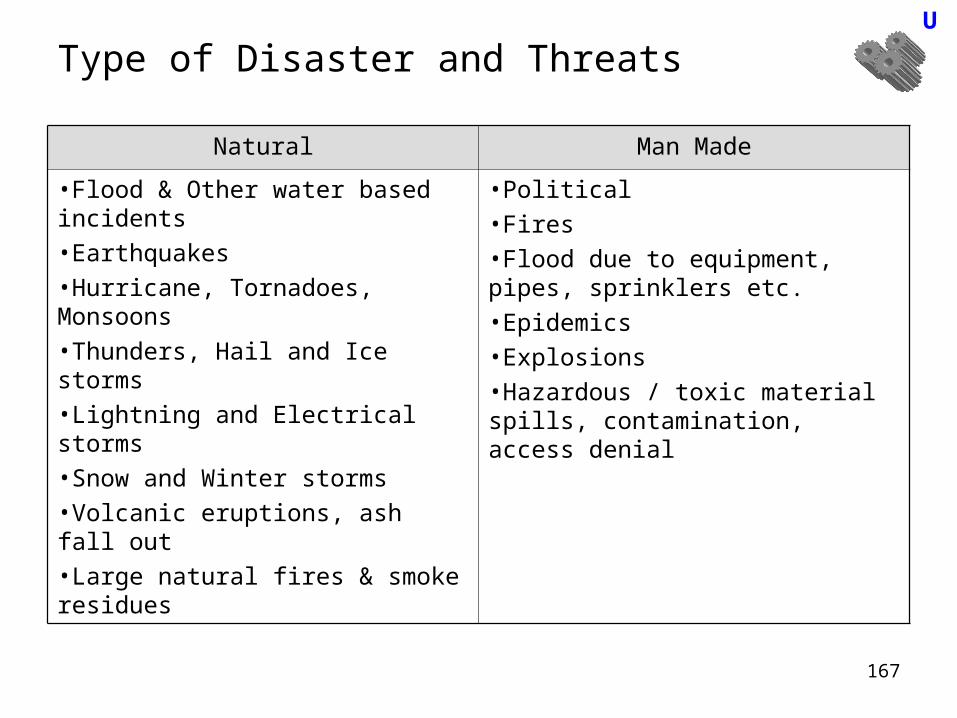

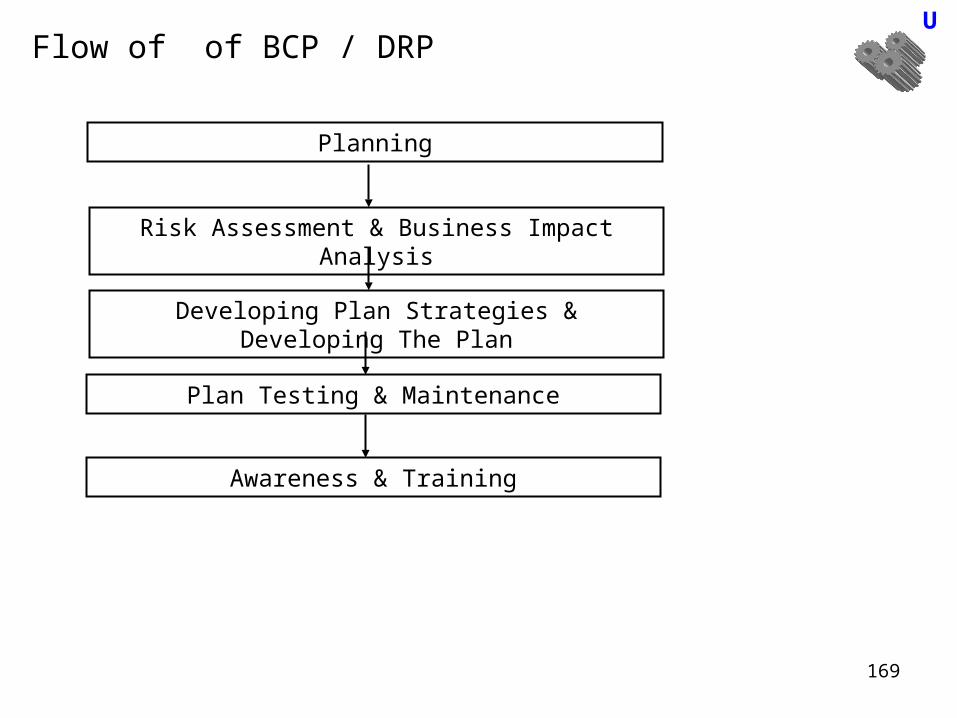

Overview of D6—Business Continuity and Disaster Recovery

To provide assurance that in the event of a disruption the business continuity and disaster recovery processes will ensure the timely resumption of IT services while minimizing the business impact

Examples of Target•Business Impact Analysis (BIA) and Disaster Recovery Planning (DRP)•Validation of backup and recovery against disasters•Validation of means for continuity against disasters

U

26

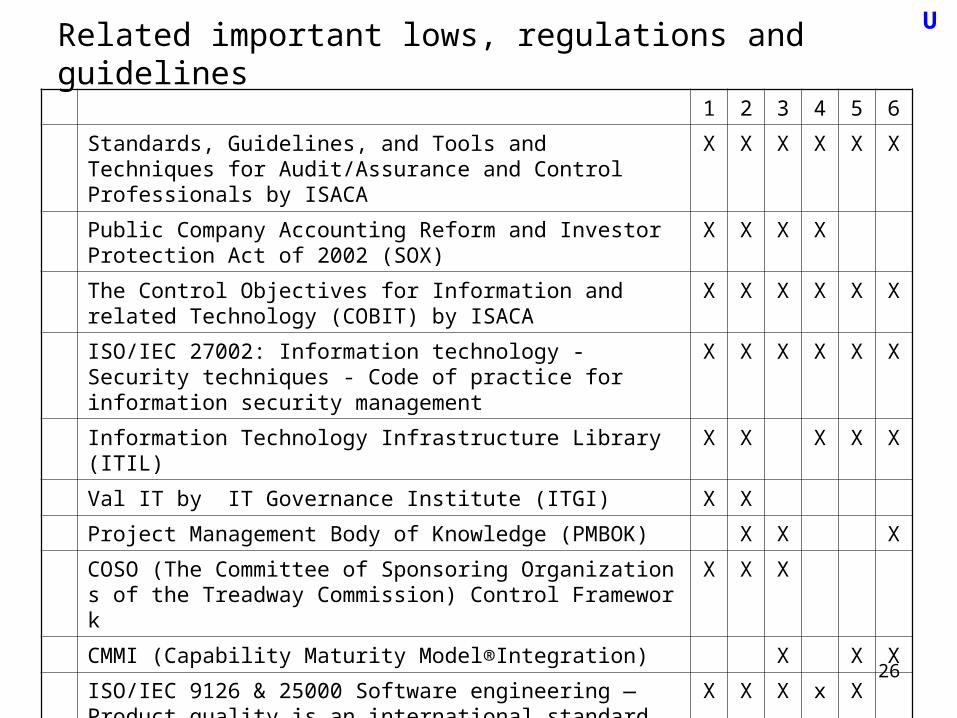

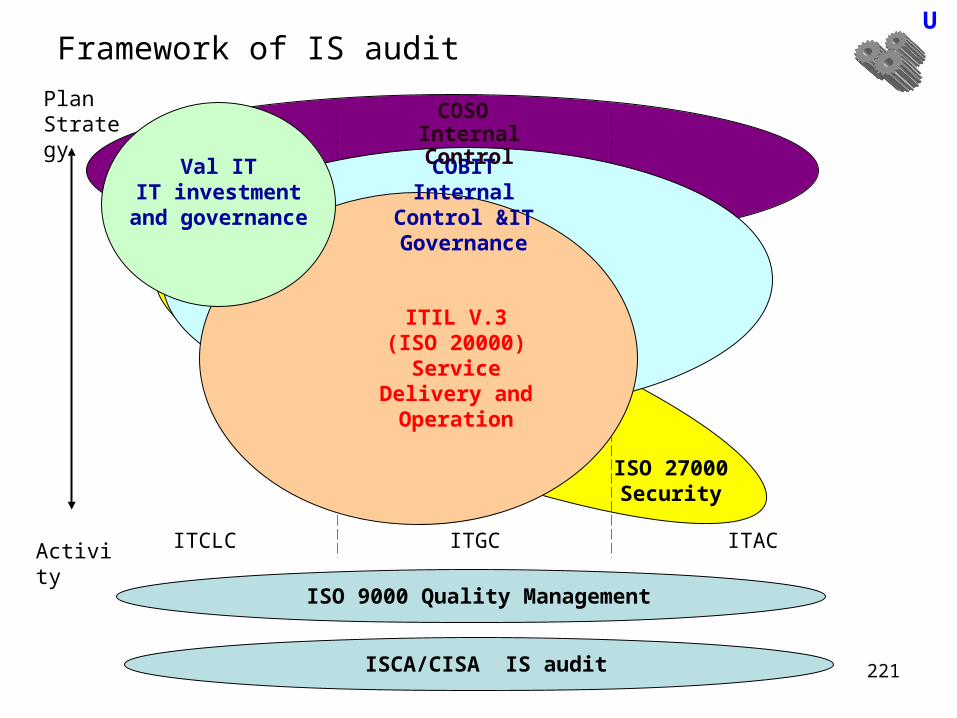

Related important lows, regulations and guidelines U

1 2 3 4 5 6

Standards, Guidelines, and Tools and Techniques for Audit/Assurance and Control Professionals by ISACA

X X X X X X

Public Company Accounting Reform and Investor Protection Act of 2002 (SOX)

X X X X

The Control Objectives for Information and related Technology (COBIT) by ISACA

X X X X X X

ISO/IEC 27002: Information technology - Security techniques - Code of practice for information security management

X X X X X X

Information Technology Infrastructure Library (ITIL) X X X X X

Val IT by IT Governance Institute (ITGI) X X

Project Management Body of Knowledge (PMBOK) X X X

COSO (The Committee of Sponsoring Organizations of the Treadway Commission) Control Framework

X X X

CMMI (Capability Maturity Model®Integration) X X X

ISO/IEC 9126 & 25000 Software engineering — Product quality is an international standard for the evaluation of software quality.

X X X x X

27

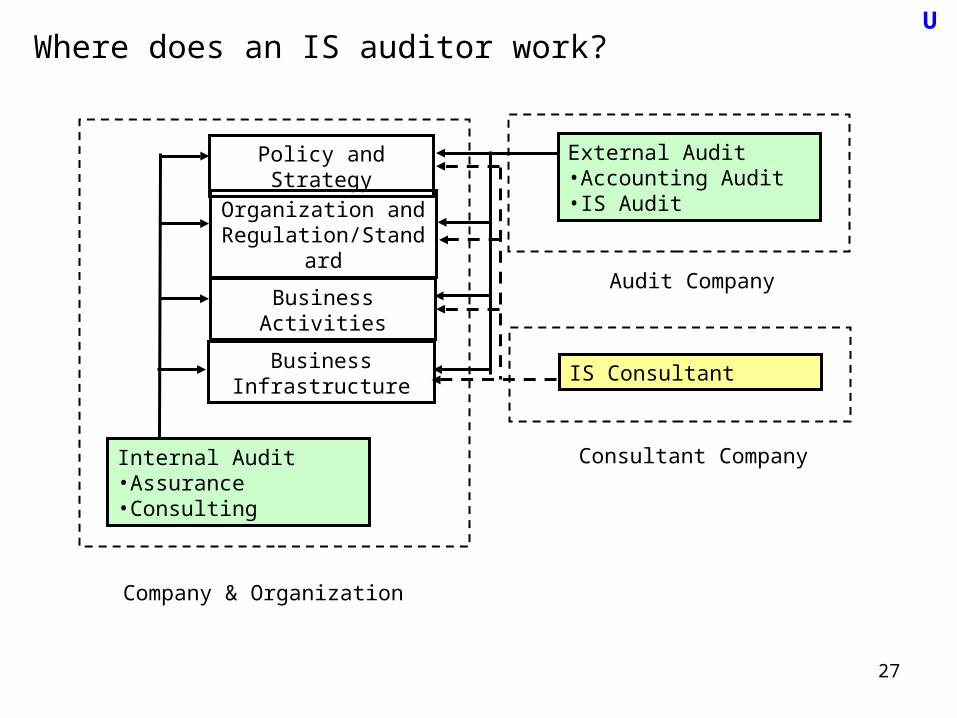

Where does an IS auditor work?U

Policy and Strategy

Organization and Regulation/Standard

Business Activities

Business Infrastructure

Internal Audit•Assurance•Consulting

Audit Company

External Audit•Accounting Audit•IS Audit

Company & Organization

Consultant Company

IS Consultant

28

New movement of IS Audit : SecurityU

IT Technical IT Management IT Governance Audit Process & Method

D3—Systems and Infrastructure Lifecycle Management

D1—IS Audit

ProcessD2—IT Governance

D4—IT Service Delivery and Support

D5—Protection of Information Assets

D6—Business Continuity and Disaster Recovery

CISM (Certified Information Security Manager)

by ISACA

Information Security Specialistby Japan Information Technology Engineers Examination

29

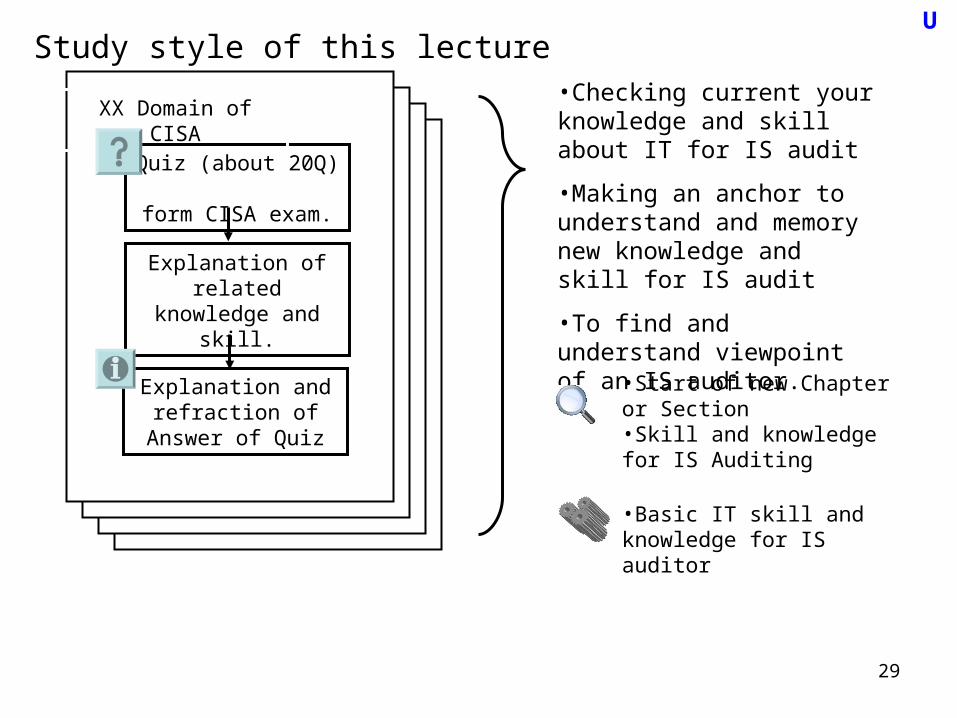

Study style of this lectureU

Quiz (about 20Q) form CISA exam.

XX Domain of CISA

Explanation of related knowledge

and skill.

Explanation and refraction of Answer

of Quiz

•Checking current your knowledge and skill about IT for IS audit

•Making an anchor to understand and memory new knowledge and skill for IS audit

•To find and understand viewpoint of an IS auditor.

•Start of new Chapter or Section•Skill and knowledge for IS Auditing

•Basic IT skill and knowledge for IS auditor

30

Chapter 1.Domain 3

Systems and Infrastructure Lifecycle Management

U

31

Overview of Tasks for Domain 3

3.1 Evaluate proposed system development/acquisition to ensure that it meets the business goals.3.2 Evaluate the project management framework and project governance practices to ensure that business objectives are achieved in a cost-effective manner 3.3 Perform reviews to ensure that a project is progressing in accordance with project plans and project management regulation.3.4 Evaluate proposed control mechanisms for systems and/or infrastructure during specification, development/acquisition, and testing.3.5 Evaluate the processes by which systems and/or infrastructure are developed/ acquired and tested to ensure that the deliverables meet the organization’s objectives.3.6 Evaluate the readiness of the system and/or infrastructure for implementation and migration into production.3.7 Perform post-implementation review and periodic reviews of systems and/or infrastructure to ensure that they meet the organization’s objectives and are subject to effective internal control.3.8 Evaluate the process by which systems and/or infrastructure are maintained to ensure the continued support of the organization’s objectives and are subject to effective internal control.3.9 Evaluate the process by which systems and/or infrastructure are disposed of to ensure that they comply with the organization’s policies and procedures.

U

32

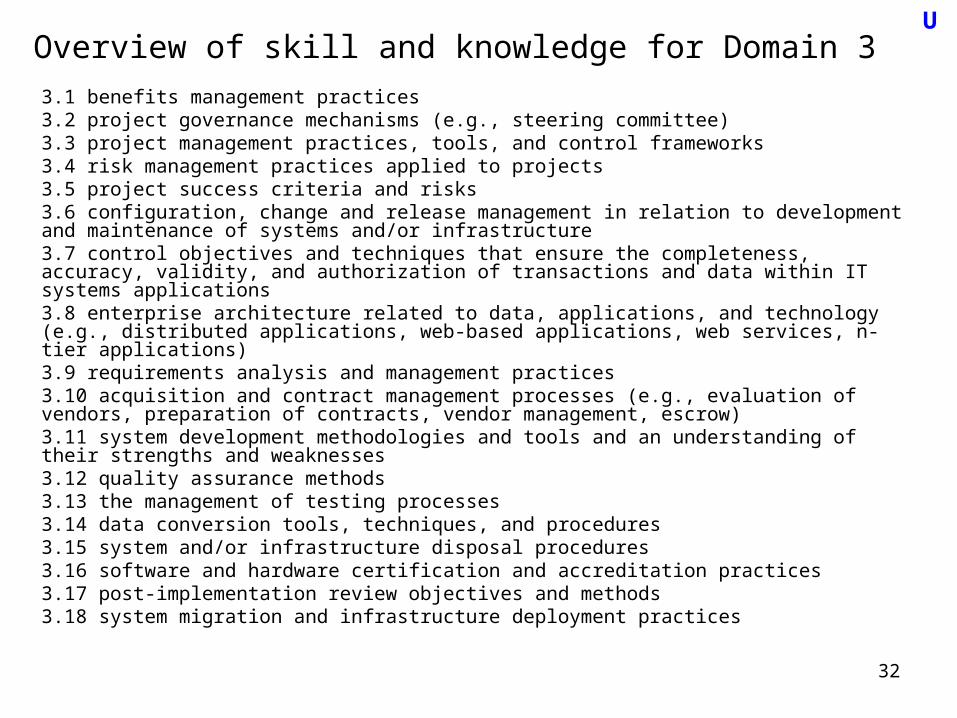

Overview of skill and knowledge for Domain 3U

3.1 benefits management practices3.2 project governance mechanisms (e.g., steering committee)3.3 project management practices, tools, and control frameworks3.4 risk management practices applied to projects3.5 project success criteria and risks3.6 configuration, change and release management in relation to development and maintenance of systems and/or infrastructure3.7 control objectives and techniques that ensure the completeness, accuracy, validity, and authorization of transactions and data within IT systems applications3.8 enterprise architecture related to data, applications, and technology (e.g., distributed applications, web-based applications, web services, n-tier applications)3.9 requirements analysis and management practices 3.10 acquisition and contract management processes (e.g., evaluation of vendors, preparation of contracts, vendor management, escrow)3.11 system development methodologies and tools and an understanding of their strengths and weaknesses 3.12 quality assurance methods3.13 the management of testing processes 3.14 data conversion tools, techniques, and procedures3.15 system and/or infrastructure disposal procedures3.16 software and hardware certification and accreditation practices3.17 post-implementation review objectives and methods 3.18 system migration and infrastructure deployment practices

33

IS Audit Small Quiz No.1

Domain 3 (1) Systems and Infrastructure Lifecycle Management

Subject: Project Plan, Project Management, Architecture, method and APP

U

Quiz book

34

U

IT control

ITGC:IT general controls

ITCLC: IT Company Level Control

ITAC: IT Application Control

ITGC:IT general controls•Logical access controls.•System development life cycle controls.•Program change management controls.•Data center physical security controls.•System and data backup and recovery•Computer operation controls.

ITCLC: IT Company Level Control* IT Governance/Policy *IT Risk Management. *Training* Quality Assurance *IT Internal Audit

IT Infrastructure (Network, Server, PC …)

Development Operation

ITAC: IT Application Controlcomplete and accurate •Input Data Control.•Process Control•Output Control

Application Systems

AccountingSystem

Sales System

Company

….

35

Overview : SLDC (System Development Lift Cycle) by ISACAU

P1: Feasibility Study

P2: Requirement Definition

P3: System Design

P4: Development

P3: System Selection

P4: Configuration

P5: Implementation

Review

P6: Post implementation

P7: Disposal

R

P3: Buy or Make

R

R

R R

R

R

BuyMake (Build)

Scope of General System

Development

36

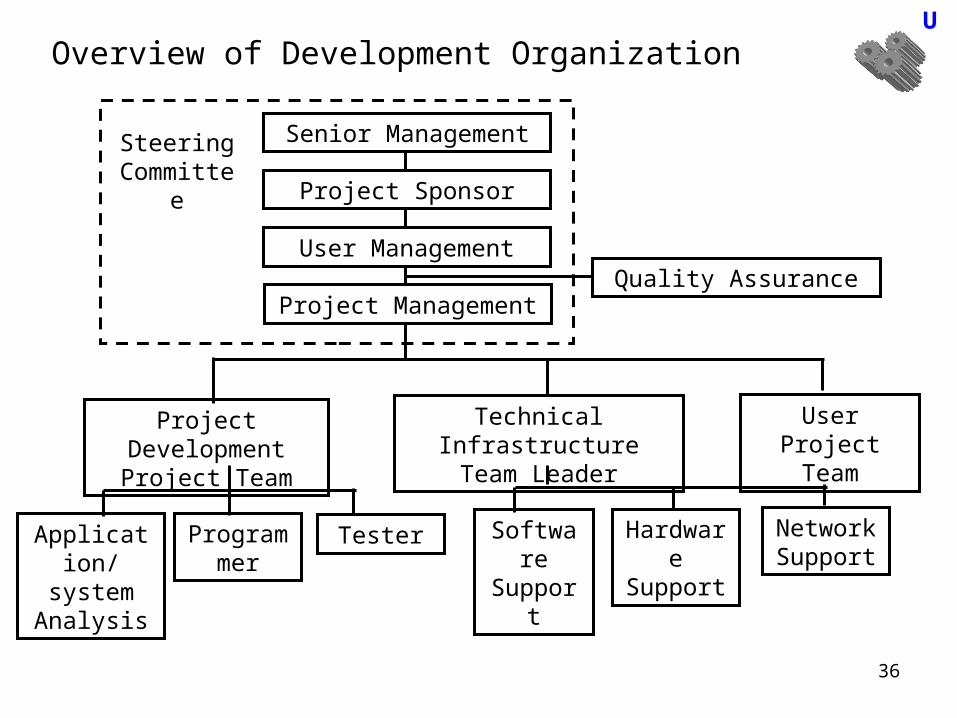

Overview of Development OrganizationU

Senior Management

Project Sponsor

User Management

Project ManagementQuality Assurance

Project Development Project Team

UserProject Team

Technical Infrastructure Team Leader

SoftwareSupport

HardwareSupport

NetworkSupport

Application/ system Analysis

Programmer

Tester

Steering Committee

37

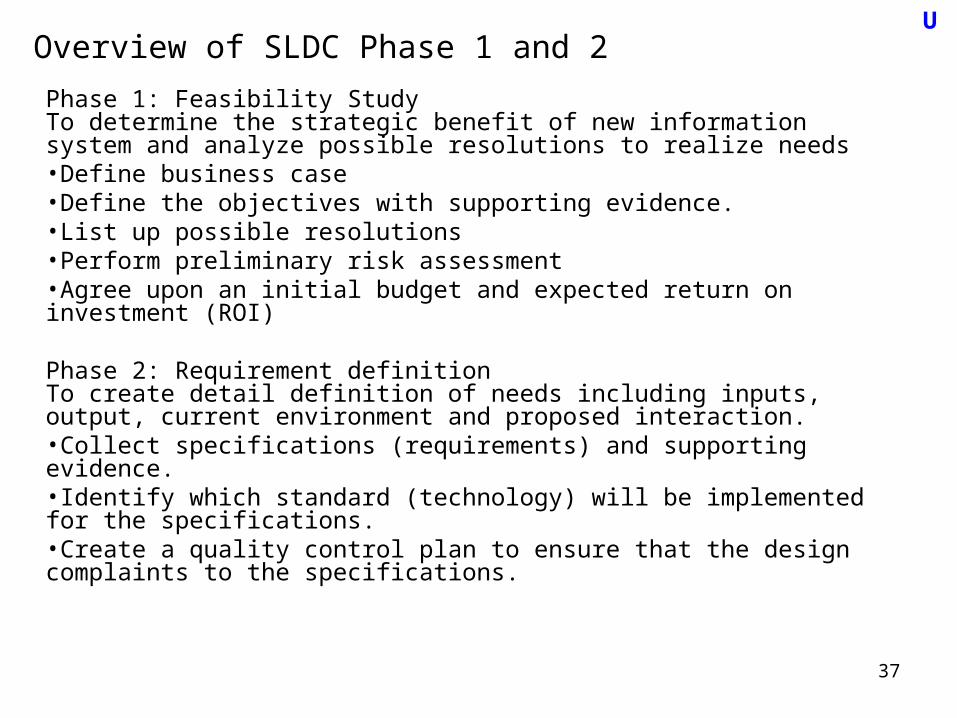

Overview of SLDC Phase 1 and 2

Phase 1: Feasibility StudyTo determine the strategic benefit of new information system and analyze possible resolutions to realize needs •Define business case•Define the objectives with supporting evidence.•List up possible resolutions•Perform preliminary risk assessment•Agree upon an initial budget and expected return on investment (ROI)

Phase 2: Requirement definitionTo create detail definition of needs including inputs, output, current environment and proposed interaction.•Collect specifications (requirements) and supporting evidence.•Identify which standard (technology) will be implemented for the specifications.•Create a quality control plan to ensure that the design complaints to the specifications.

U

38

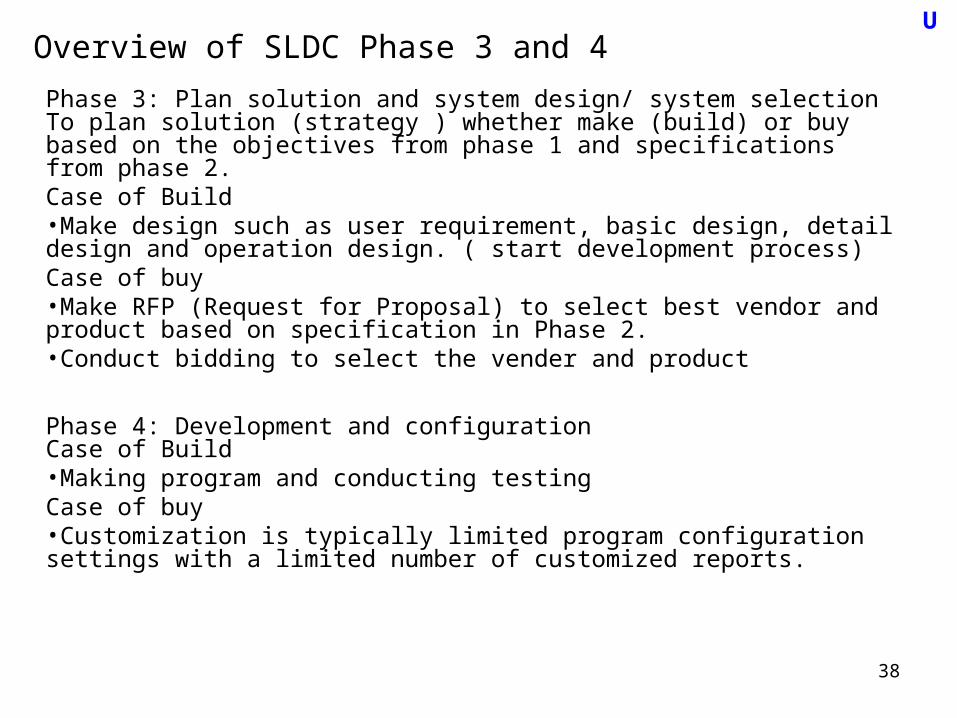

Overview of SLDC Phase 3 and 4

Phase 3: Plan solution and system design/ system selectionTo plan solution (strategy ) whether make (build) or buy based on the objectives from phase 1 and specifications from phase 2.Case of Build •Make design such as user requirement, basic design, detail design and operation design. ( start development process)Case of buy•Make RFP (Request for Proposal) to select best vendor and product based on specification in Phase 2.•Conduct bidding to select the vender and product

Phase 4: Development and configurationCase of Build •Making program and conducting testingCase of buy•Customization is typically limited program configuration settings with a limited number of customized reports.

U

39

Overview of SLDC Phase 5,6 and 7

Phase 5: ImplementationTo install new system and final user acceptance (mainly function testing) test begins. The system undergoes a process of final certification and approval.

Phase 6: post implementationAfter the system has been in production use, it is reviewed for effectiveness to full fill the original objectives. •Compare performance metrics to the original objectives.•Re-review the specifications and requirement annually.•Implement request for new requirement, update or disposal

Phase 7: DisposalFinal phase is the proper disposal of equipment and purging data.

U

40

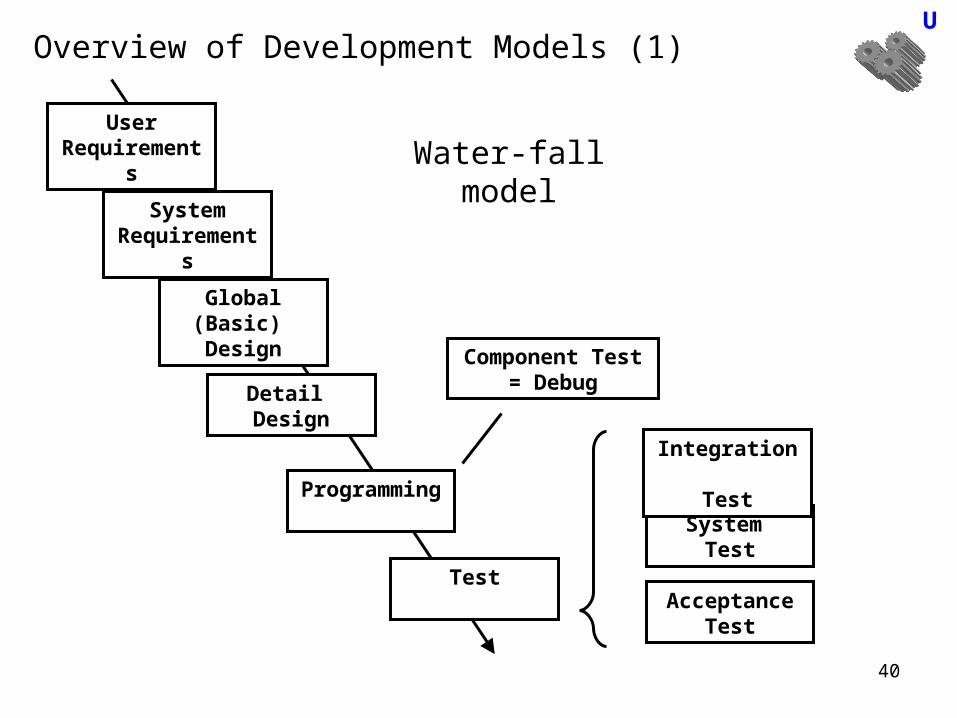

Overview of Development Models (1)

User Requirements

Detail Design

Acceptance Test

System Test

Integration Test

Global (Basic) Design

Component Test= Debug

System Requirements

Programming

Test

Water-fall model

U

41

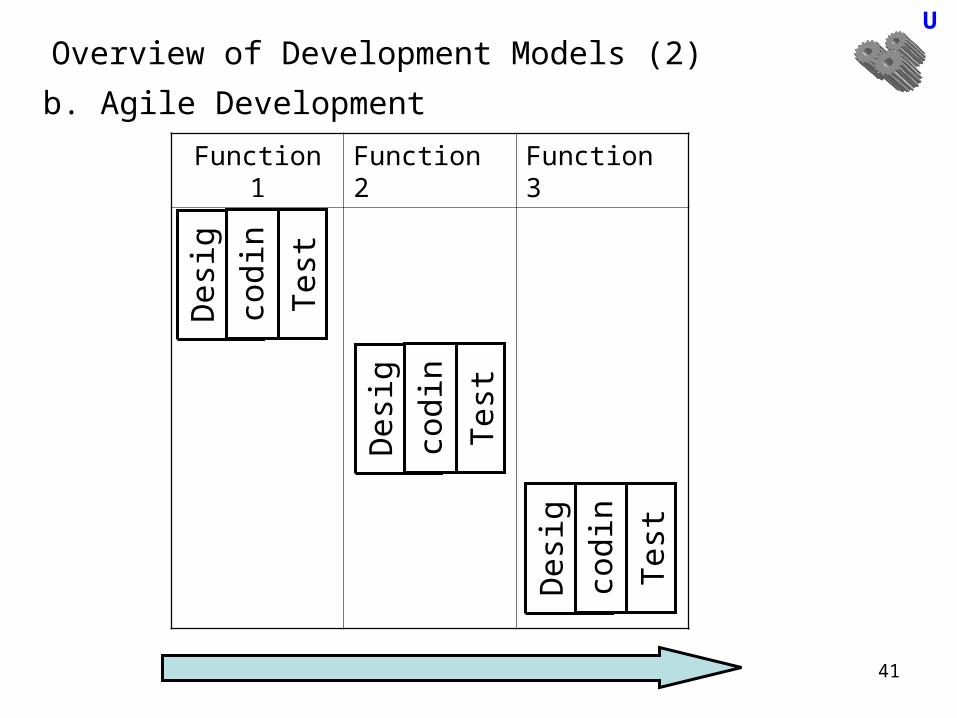

Overview of Development Models (2)U

b. Agile Development

Function 1 Function 2 Function 3

Des

ign

codi

ng

Tes

t

Des

ign

codi

ng

Tes

t

Des

ign

codi

ng

Tes

t

42

Overview of Development models (3)U

Water fall Agile Spiral (Prototyping)

Document Document base Minimum Minimum

Confirmation of requirement

By document By software By software

Changing requirement

Difficult Easy Easy

Programmer A few - hundreds A few – 20

1 cycle Months - years Weeks - months Month – a year

Management Initial plan In each cycle

Collaboration Defined by regulation

personal

43

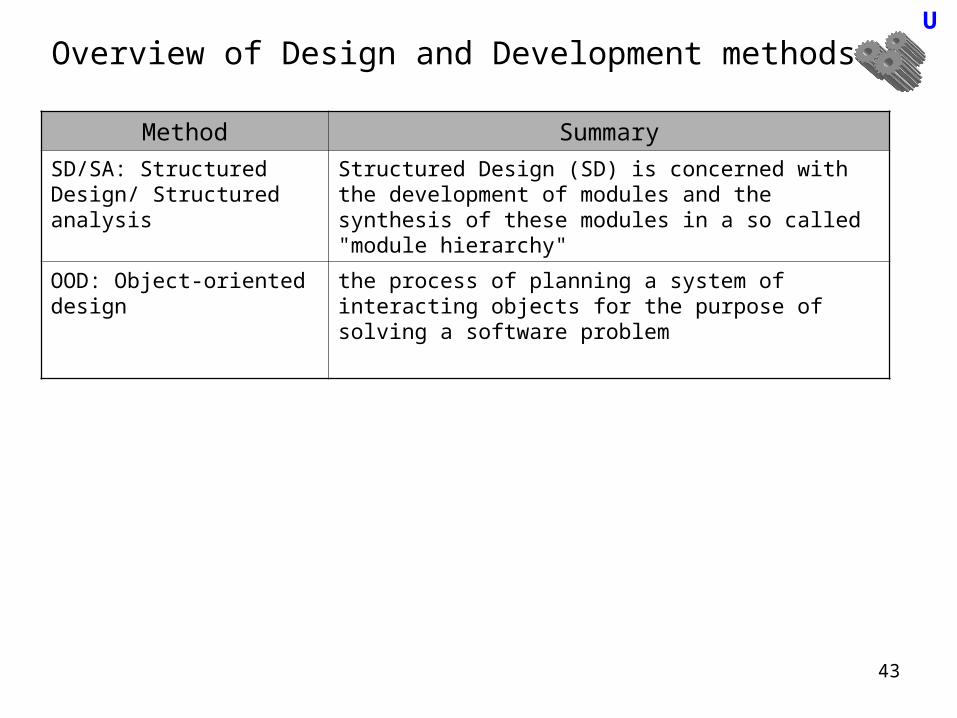

Overview of Design and Development methodsU

Method Summary

SD/SA: Structured Design/ Structured analysis

Structured Design (SD) is concerned with the development of modules and the synthesis of these modules in a so called "module hierarchy"

OOD: Object-oriented design

the process of planning a system of interacting objects for the purpose of solving a software problem

44

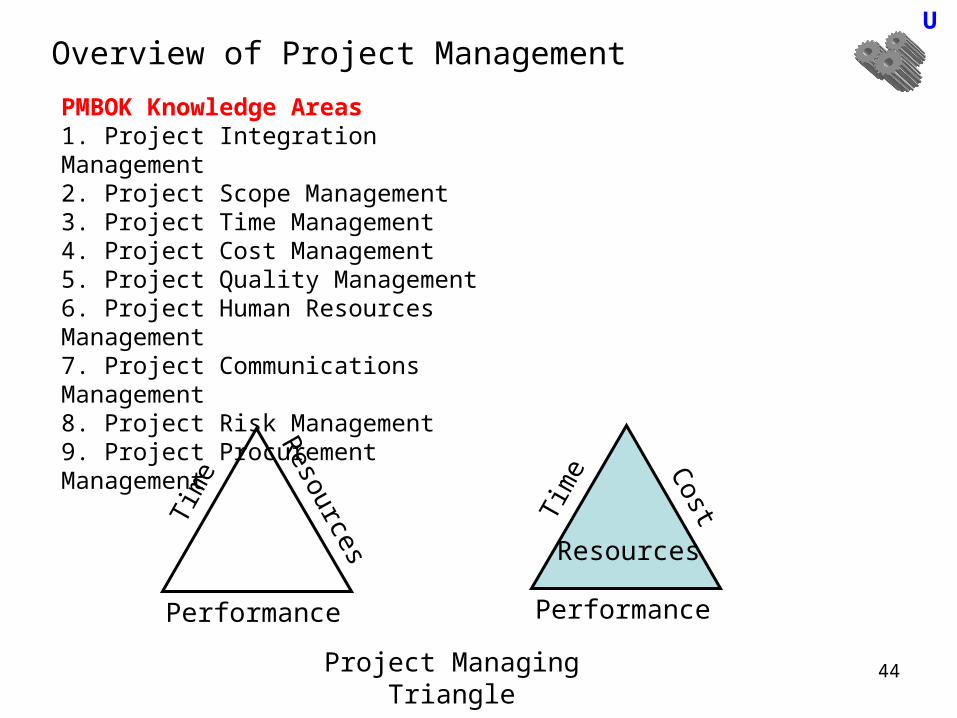

Overview of Project ManagementU

PMBOK Knowledge Areas1. Project Integration Management2. Project Scope Management3. Project Time Management4. Project Cost Management5. Project Quality Management6. Project Human Resources Management7. Project Communications Management8. Project Risk Management9. Project Procurement Management

Resources

Performance

Tim

e Cost

Performance

Tim

eResources

Project Managing Triangle

45

Overview of Cost estimation and SchedulingU

Planning

Cost estimation

Scheduling

Function point

Lines of code

WBS (Work Breakdown Structure)

Bottom-up estimate

Parametric modeling

Analogous estimate

PERT

Gantt chart

46

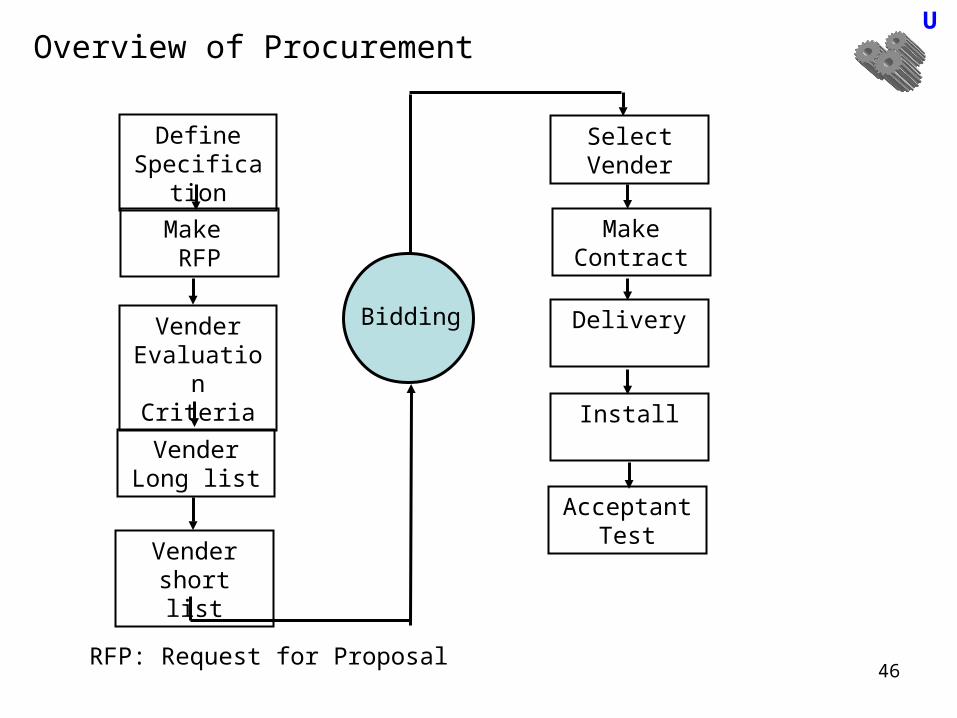

Overview of ProcurementU

Define Specification

Make RFP

Vender Evaluation

Criteria

Vender Long list

Vender short list

Select Vender

Make Contract

Delivery

Install

AcceptantTest

RFP: Request for Proposal

Bidding

47

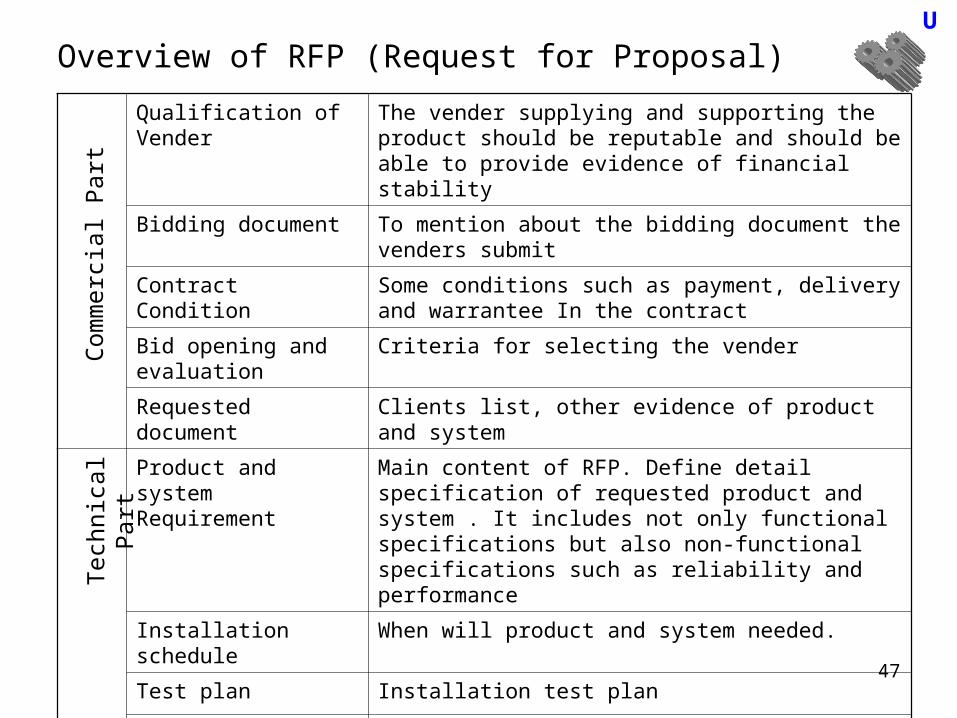

Overview of RFP (Request for Proposal)U

Qualification of Vender The vender supplying and supporting the product should be reputable and should be able to provide evidence of financial stability

Bidding document To mention about the bidding document the venders submit

Contract Condition Some conditions such as payment, delivery and warrantee In the contract

Bid opening and evaluation

Criteria for selecting the vender

Requested document Clients list, other evidence of product and system

Product and system Requirement

Main content of RFP. Define detail specification of requested product and system . It includes not only functional specifications but also non-functional specifications such as reliability and performance

Installation schedule When will product and system needed.

Test plan Installation test plan

Client support Training, operation support, maintenance, warrantee

Com

mer

cial

Par

tT

echn

ical

Par

t

48

Overview of Business APPU

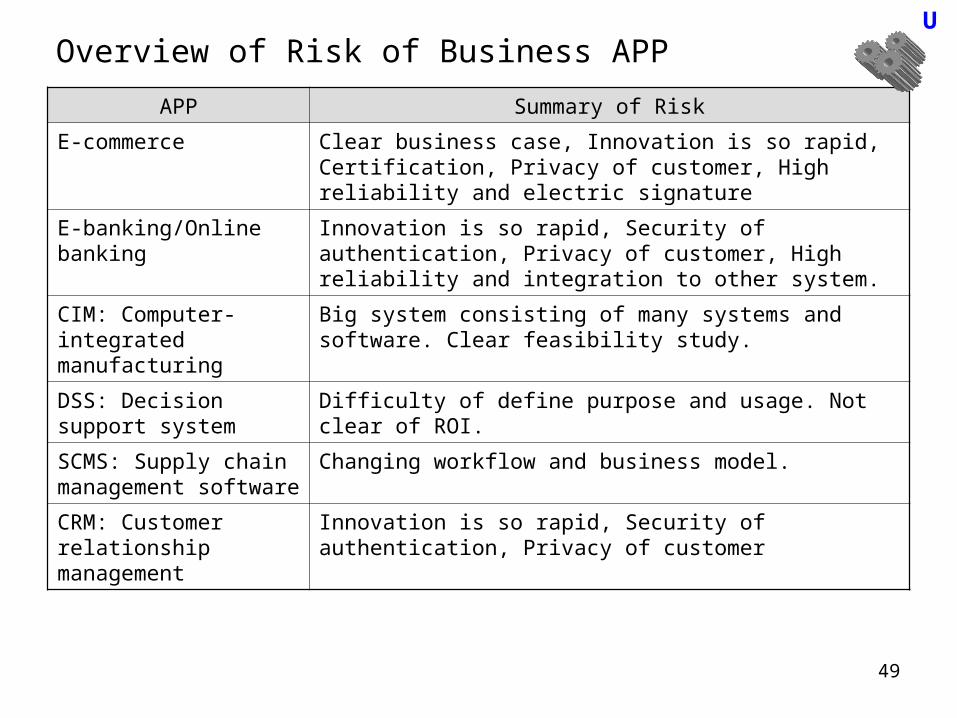

APP Summary

E-commerce the buying and selling of products or services over electronic systems such as the Internet and other computer networks.

E-banking/Online banking

To conduct financial transactions on a secure website operated by their retail or virtual bank, credit union or building society.

CIM: Computer-integrated manufacturing

Both a method of manufacturing and the name of a computer-automated system in which individual engineering, production, marketing, and support functions of a manufacturing enterprise are organized.

DSS: Decision support system

DSSs serve the management, operations, and planning levels of an organization and help to make decisions, which may be rapidly changing and not easily specified in advance.

SCMS: Supply chain management software

Supply chain transactions, managing supplier relationships and controlling associated business processes. it commonly includes: Customer requirement processing Purchase order processing, Inventory management, Goods receipt and Warehouse management, Supplier Management/Sourcing

CRM: Customer relationship management

Sales force automation, Marketing and Customer Service and Support

49

Overview of Risk of Business APPU

APP Summary of Risk

E-commerce Clear business case, Innovation is so rapid, Certification, Privacy of customer, High reliability and electric signature

E-banking/Online banking

Innovation is so rapid, Security of authentication, Privacy of customer, High reliability and integration to other system.

CIM: Computer-integrated manufacturing

Big system consisting of many systems and software. Clear feasibility study.

DSS: Decision support system

Difficulty of define purpose and usage. Not clear of ROI.

SCMS: Supply chain management software

Changing workflow and business model.

CRM: Customer relationship management

Innovation is so rapid, Security of authentication, Privacy of customer

50

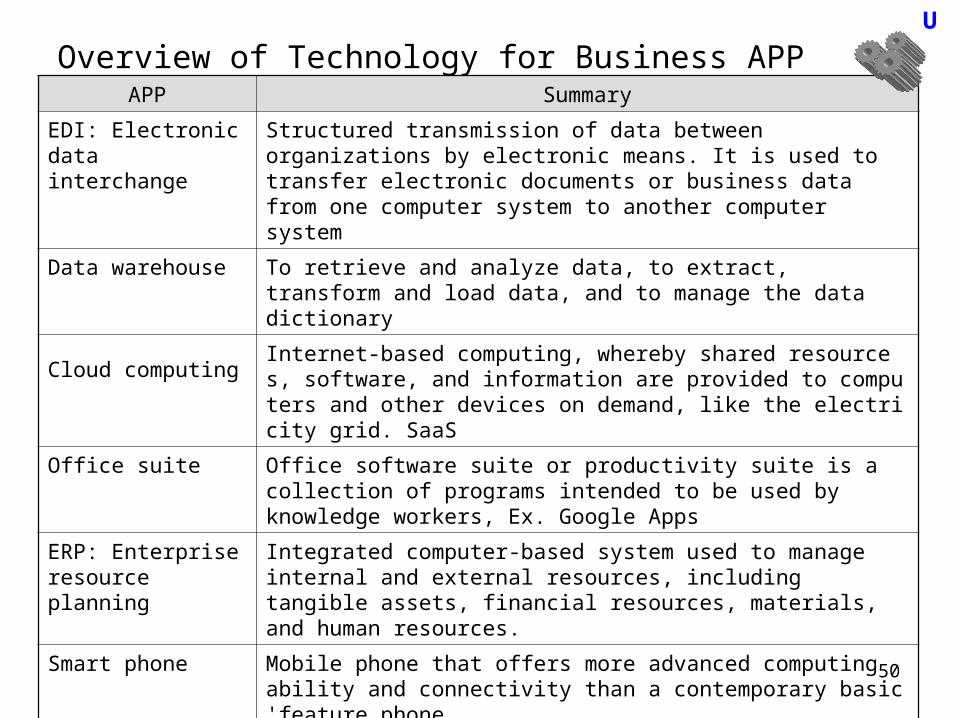

Overview of Technology for Business APPU

APP Summary

EDI: Electronic data interchange

Structured transmission of data between organizations by electronic means. It is used to transfer electronic documents or business data from one computer system to another computer system

Data warehouse To retrieve and analyze data, to extract, transform and load data, and to manage the data dictionary

Cloud computing Internet-based computing, whereby shared resources, software, and information are provided to computers and other devices on demand, like the electricity grid. SaaS

Office suite Office software suite or productivity suite is a collection of programs intended to be used by knowledge workers, Ex. Google Apps

ERP: Enterprise resource planning

Integrated computer-based system used to manage internal and external resources, including tangible assets, financial resources, materials, and human resources.

Smart phone Mobile phone that offers more advanced computing ability and connectivity than a contemporary basic 'feature phone

CTI: Computer telephony integration

technology that allows interactions on a telephone and a computer to be integrated or co-ordinated. As contact channels have expanded from voice to include email, web, and fax, the definition of CTI has expanded to include the integration of all customer contact channels (voice, email, web, fax, etc.) with computer systems.

51

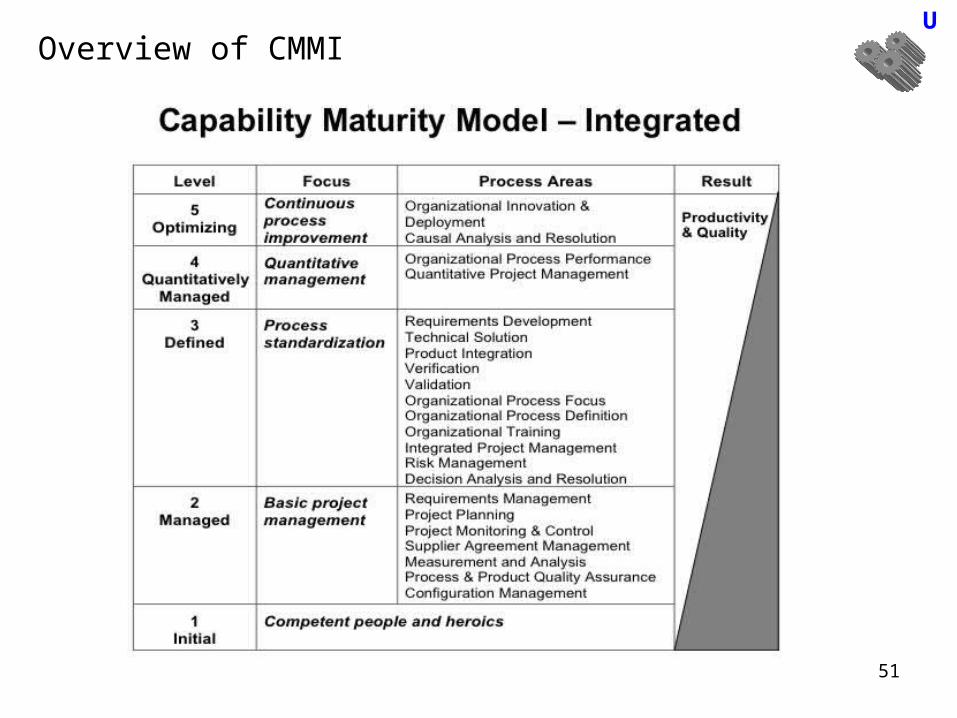

Overview of CMMIU

52

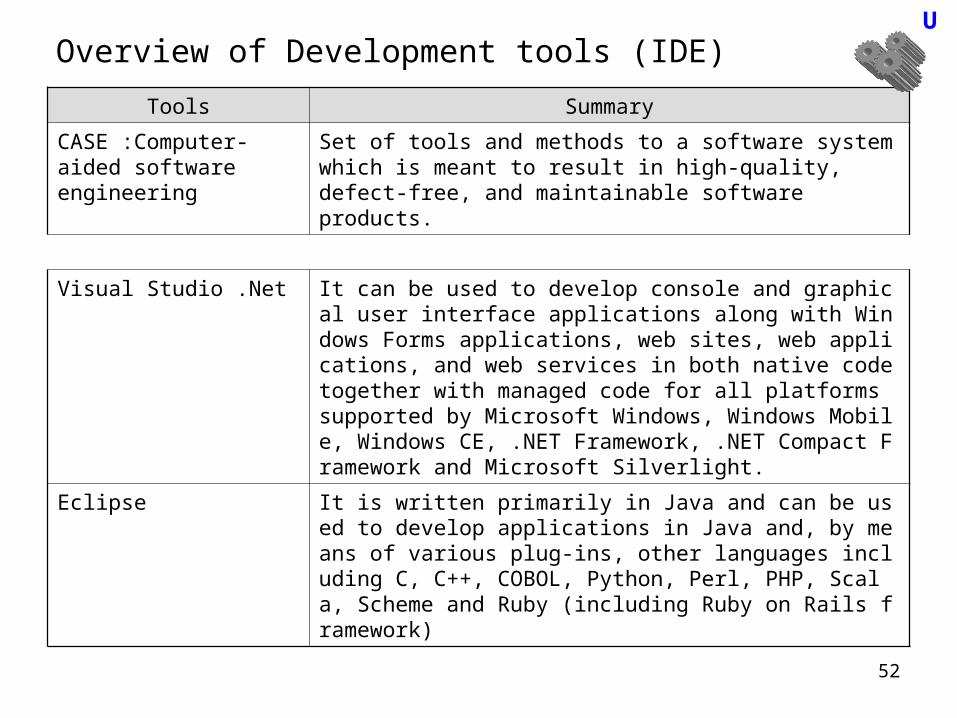

Overview of Development tools (IDE)U

Tools Summary

CASE :Computer-aided software engineering

Set of tools and methods to a software system which is meant to result in high-quality, defect-free, and maintainable software products.

Visual Studio .Net It can be used to develop console and graphical user interface applications along with Windows Forms applications, web sites, web applications, and web services in both native code together with managed code for all platforms supported by Microsoft Windows, Windows Mobile, Windows CE, .NET Framework, .NET Compact Framework and Microsoft Silverlight.

Eclipse It is written primarily in Java and can be used to develop applications in Java and, by means of various plug-ins, other languages including C, C++, COBOL, Python, Perl, PHP, Scala, Scheme and Ruby (including Ruby on Rails framework)

53

Test Frame JUnit

Overview of Actual (Practical) Tools U

Acceptance Test

System Test

Programming

Component Test

Integration Test

Exsample1: OSS for eclipse (Java)

Ecllipse Metrics PlusinCalculate Code metrics such as complexity and dependency

djUnitMake Moc-class for testing/ Coverage

Junit FactoryAutomatically generating Test case

TPTPSupproit Making test code and executing test case including remote host

Automated ContinuousExecuting test case automatically

Checkstyle/ PMDCheck style of Code

FindbugsFind bad cording that seems to make bugs

CAP/Jdepend4eclipseShow dependency

Static Analysis Code Metrics

Test design/ Test case/ Executing

SolexRecod, Replay and edit HTML Session

WSUnitSimulate XML web servise

Test Executing for Web

Extensible Java Profiler/iMechanic/Eclipse profiler plug-inMeasure Nun.Call, Time and Usage of memory

Performance Testing

SeleniumRecord, Re-play and edit Browser action.

JMeterExecuting Web access session automatically

Test Executing for Web / Performance Testing

54

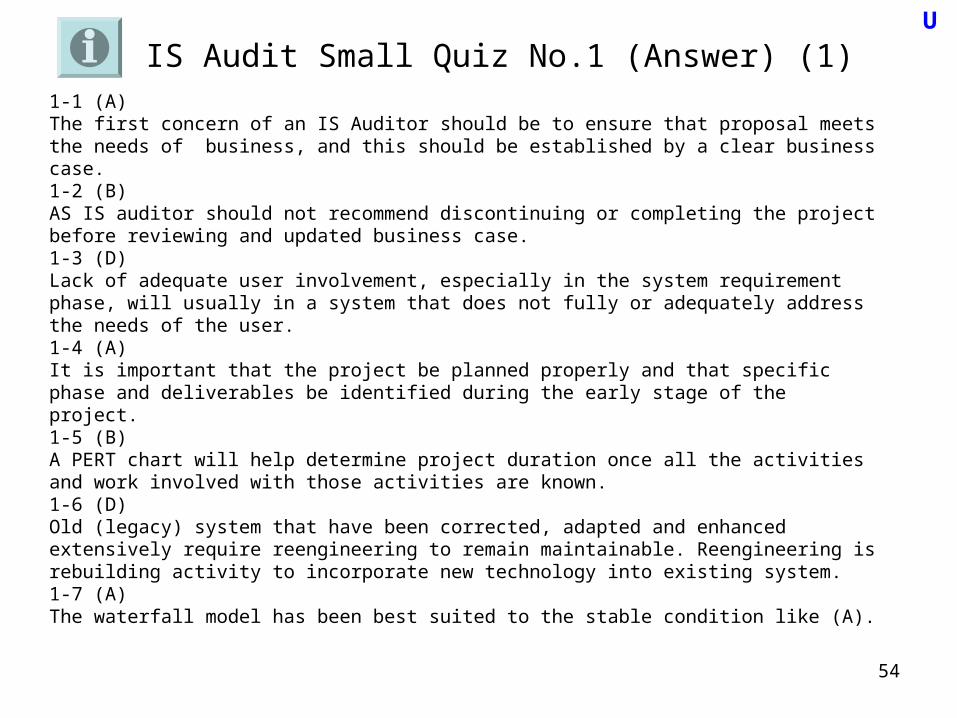

IS Audit Small Quiz No.1 (Answer) (1)1-1 (A)The first concern of an IS Auditor should be to ensure that proposal meets the needs of business, and this should be established by a clear business case.1-2 (B)AS IS auditor should not recommend discontinuing or completing the project before reviewing and updated business case.1-3 (D)Lack of adequate user involvement, especially in the system requirement phase, will usually in a system that does not fully or adequately address the needs of the user.1-4 (A)It is important that the project be planned properly and that specific phase and deliverables be identified during the early stage of the project.1-5 (B)A PERT chart will help determine project duration once all the activities and work involved with those activities are known.1-6 (D)Old (legacy) system that have been corrected, adapted and enhanced extensively require reengineering to remain maintainable. Reengineering is rebuilding activity to incorporate new technology into existing system.1-7 (A)The waterfall model has been best suited to the stable condition like (A).

U

55

IS Audit Small Quiz No.1 (Answer) (2)1-8 (A)If resource allocation is decreased, and increase in quality can be achieved if a delay in delivery time will be accepted.1-9 (A)Cost performance of a project cannot be properly assessed in isolation for schedule performance.1-10 (C)Projects often have a tendency to expand, this expansion often grows to point where the originally anticipated cost-benefit are diminished. When this occur, the project be stopped or frozen to allow review of all the cost –benefits and the payback period.1-11 (C)A project steering committee is responsible for reviewing the project progress to ensure that it will deliver the expected result.1-12(D)In the case of deviation from the predefined procedure, an IS auditor should first ensure the procedure followed for acquiring the software is consistent with business objectives and has been approved by appropriate authorities.1-13 (B)Quality plan is essential element of all projects. It is critical that the contracted supplier be required to produce such test plan.

U

56

IS Audit Small Quiz No.1 (Answer) (3)1-14 (C)Choice A,B and D are not risk, but characteristics of a DDS.1-15 (B)Once the data are in a warehouse, no modification should be made to them and access controls should be in place to prevent data modification.1-16 (C) Best resolution.1-17 (C)When implementing an application software package, incorrect parameter would be the great risk.1-18 (C)The Project portfolio database contains project data such as organization, schedule, objectives status and cost.1-19 (D)Criteria of CMMI show the development organization follows stable and predictable software process, CMMI doesn’t guarantee quality of each project.1-20 (B)A strength of IDE is that it expands the programming resources and aids available.

U

57

IS Audit Small Quiz No.2

Domain 3 (2) Testing, Implementation/Migration and APP control

U

Quiz book

58

Definition of basic terms related bug, error, ….

Bug

Defect

Fault

Flaw in component or system to fail to perform its required function

Error Human action that produces incorrect result

Other Factors・ Malice・ Natural Environment

FailureDeviation of the component or system from its expected delivery, service or result.

Without defect, Human error occurs failure

Sometimes, defect appears as failure

U

Risk A factor that could result in future negative result consequences; usually expressed as impact and likelihood

One of negative result: Attribute: impact and likelihood Factor

59

Overview of Test PhaseU

User Requirements

Detail Design

Acceptance Test

System Test

Integration Test

Global (Basic) Design

Component Test

System Requirements

Programming

a. Water fall model (V-model )

Preparation

Preparation

Preparation

Preparation

60

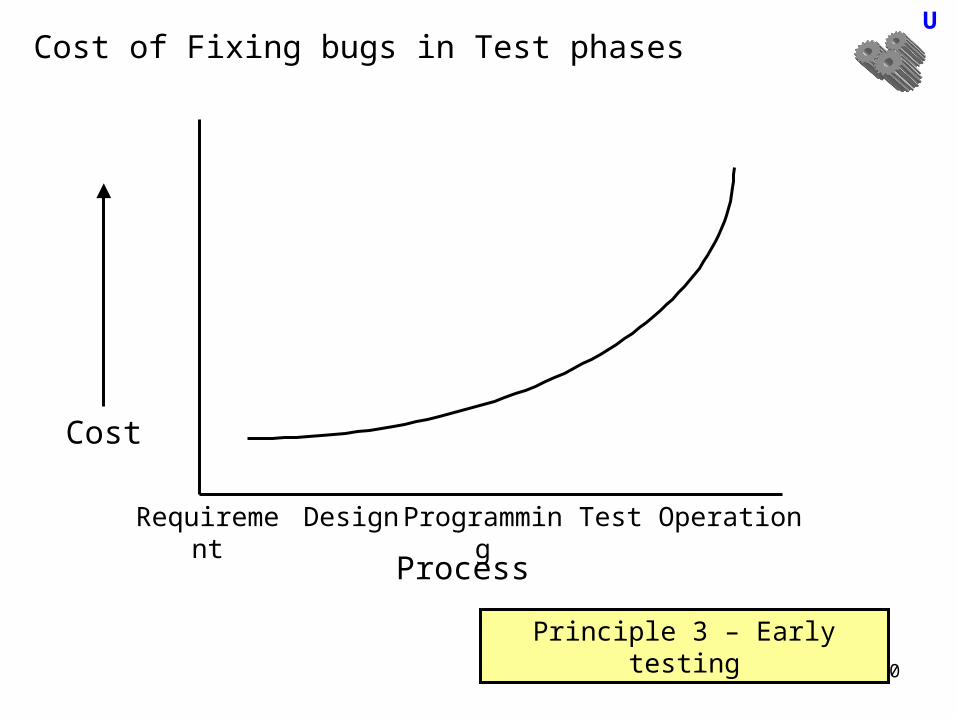

Cost of Fixing bugs in Test phases

Process

Cost

DesignRequirement Programming Test Operation

U

Principle 3 – Early testing

61

Target of Testing

Functional Testing Non-Functional Testing

suitability accuracy

compliance

interoperability security

reliabilityusability

efficiencymaintainability

Ordinal TestingFunctions of system and/Or software , that are typically described ( implicitly) in a requirements specification, a functional specification , or in use cases.

Performance TestingLoad TestingStress TestingSecurity TestingUsability TestingMaintenance TestingReliability Testing

U

Integration Test(In Test Environment)

System Test(In Real Environment)

62

Overview of Testing Techniques

Static

Document Check

(Review)

Code Check

Formal Review

Walk-through

Technical Review

Inspection

StyleCheck

FlowCheck

BugDetect

Metrics of Code

Dynamic

Structure (Code) -Based

Specification - Based

Experience -Based

Statement

Decision

Condition

MultipleCondition

EquivalencePartitioning

Boundary Value

Analysis

Informal Review

DecisionTable

State Transition

User Case Testing

ErrGuessing

ExploratoryTesting

White BoxTesting

Black BoxTesting

Running ProgramWithout Running Program

U

63

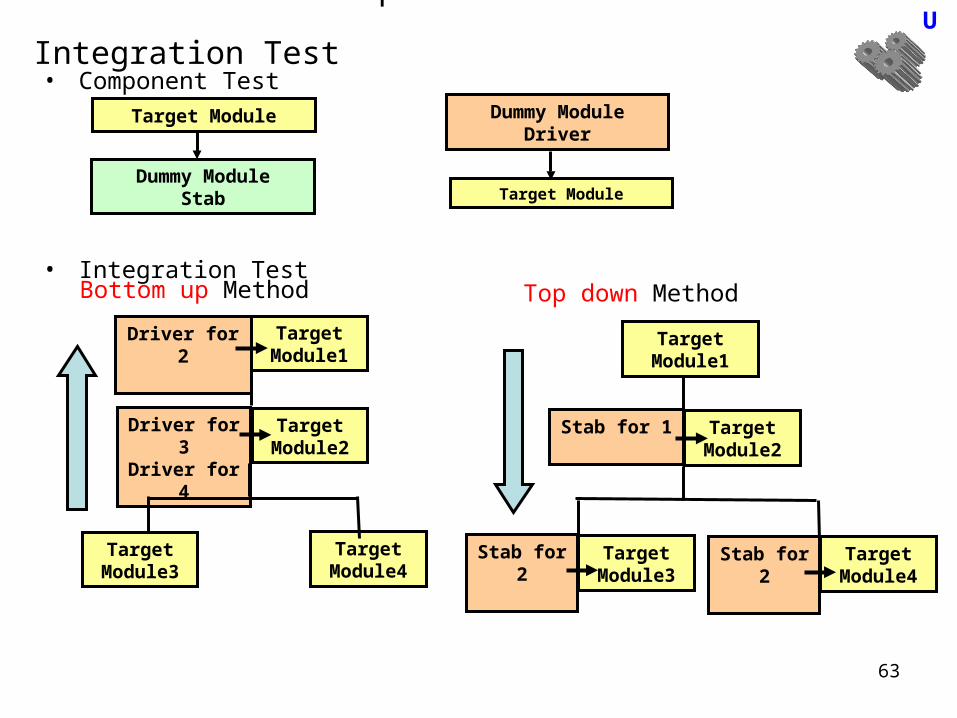

How to Conduct Component Test and Integration Test U

• Component Test

• Integration Test

Target Module

Dummy ModuleStab

Dummy ModuleDriver

Target Module

Target Module3

Target Module4

Driver for 3Driver for 4

Driver for 2

Target Module2

Target Module1

Bottom up Method

Target Module3

Target Module4

Stab for 1

Target Module1

Target Module2

Top down Method

Stab for 2Stab for 2

64

Overview of Quality Management/Monitoring/Reporting•Quality of Testing

CoverageTest Case densityBug density

•Quality of target softwareNum. of bugs in each moduleBug density in each moduleBug history (Num of detect:Open and Num of fixed:Close ) Software reliability growth curve

U

Num of

Bugs

Days

Open

Close

65

Ensample: Useful Metrics U

Project Implementation Program/systemTesting

CostTime

Progress of implementation

Features

LOC: Line of Code Complexity of codeLOC for modificationTime for build

CoverageNum. of test itemMum of test item curried by automated tools

Quality

Expected MTTF (Mean Time to Failure)Expected MTTF (Mean Time to Failure) on stress

Num. of bugs for buildType of problem in build

Num. of bugs in each moduleBug density in each moduleBug historySoftware reliability growth curve

What kind of Metrics Microsoft is using

66

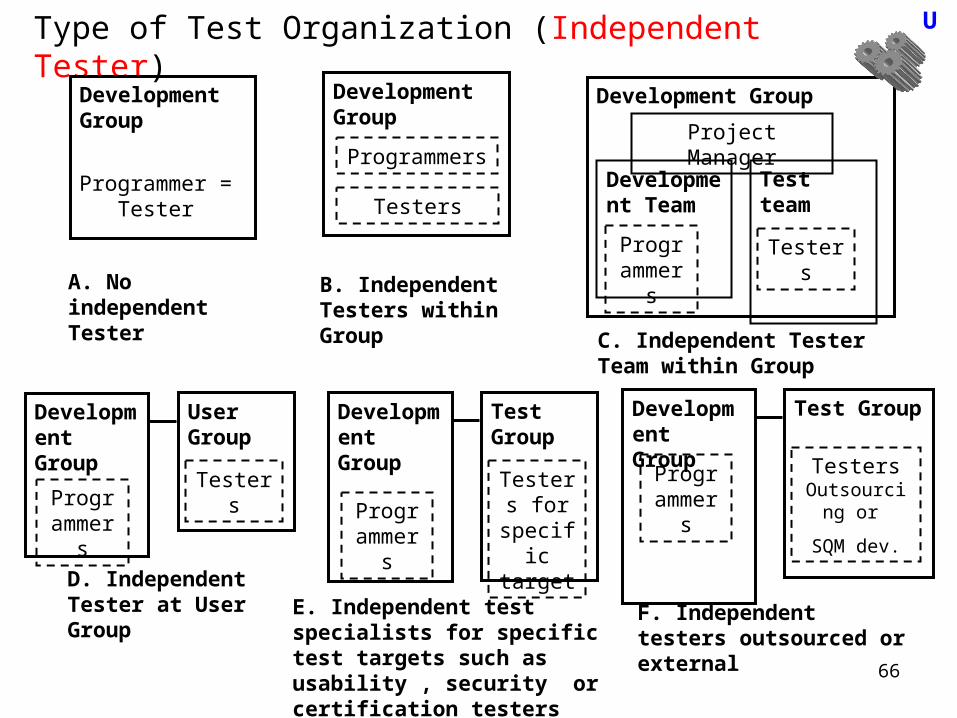

Development Group

Type of Test Organization (Independent Tester)U

Development Group

Programmer = Tester

Development Group

Programmers

TestersDevelopment Team

Programmers

Test team

Testers

Project Manager

Development Group

Programmers

User Group

Testers

Development Group

Programmers

Test Group

Testers for

specific target

Development Group

Programmers

Test Group

Testers Outsourcing

or

SQM dev.

A. No independent Tester

B. Independent Testers within Group C. Independent Tester Team

within Group

D. Independent Tester at User Group

E. Independent test specialists for specific test targets such as usability , security or certification testers

F. Independent testers outsourced or external

67

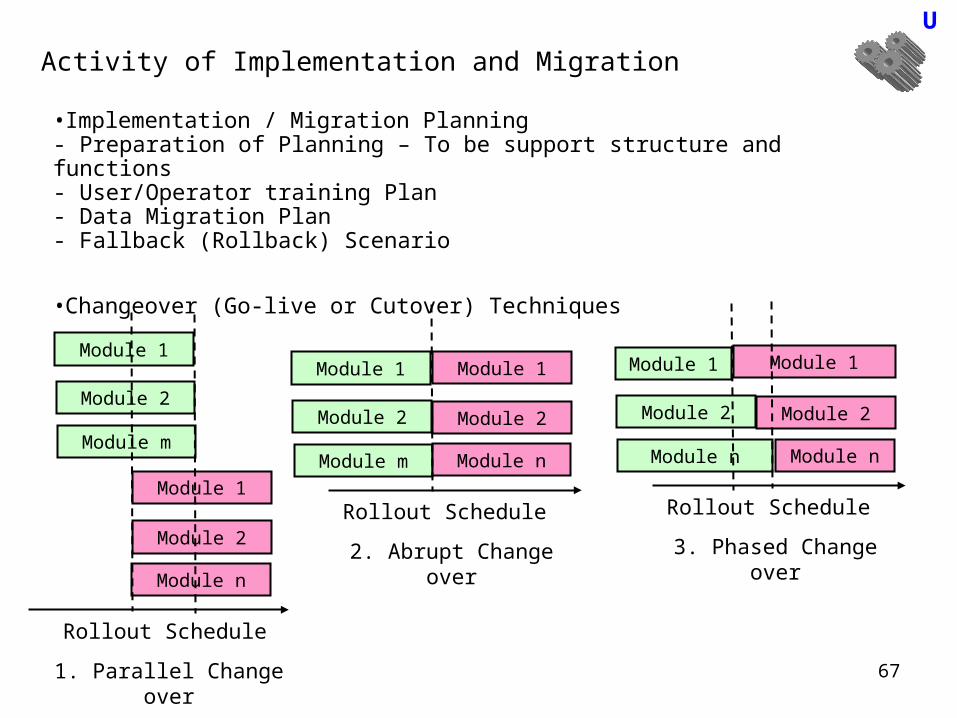

Activity of Implementation and Migration

U

•Implementation / Migration Planning- Preparation of Planning – To be support structure and functions- User/Operator training Plan- Data Migration Plan- Fallback (Rollback) Scenario

•Changeover (Go-live or Cutover) Techniques

Module 1

Module 2

Module m

Module 1

Module 2

Module n

Rollout Schedule

1. Parallel Change over

Module 1

Module 2

Module m

Module 1

Module 2

Module n

Rollout Schedule

2. Abrupt Change over

Module 1

Module 2

Module n

Module 1

Module 2

Module n

Rollout Schedule

3. Phased Change over

68

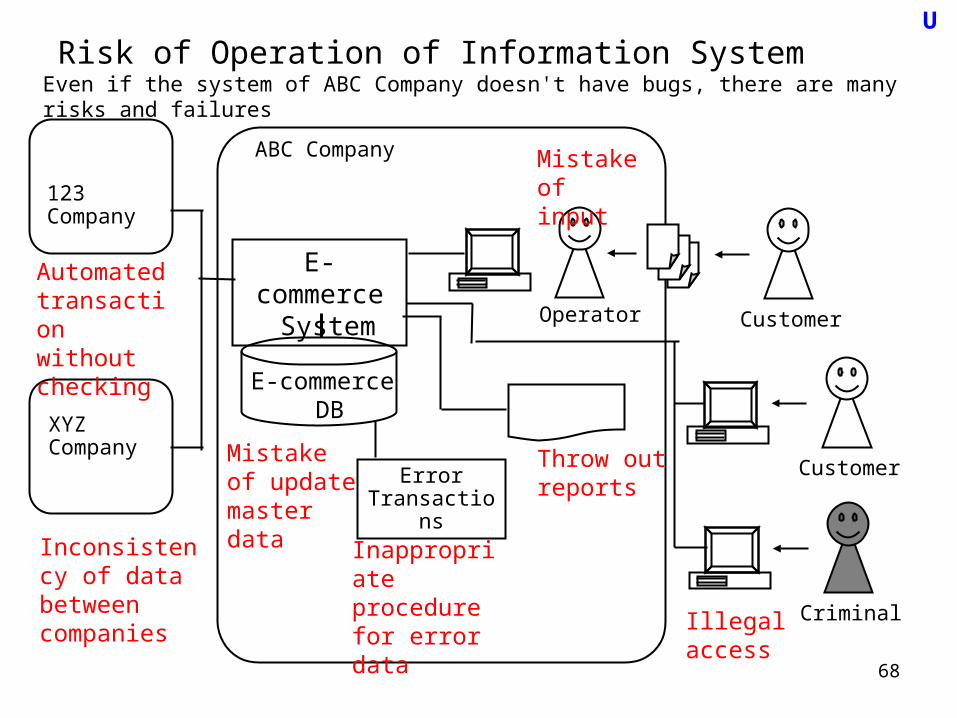

Mistake of update master data

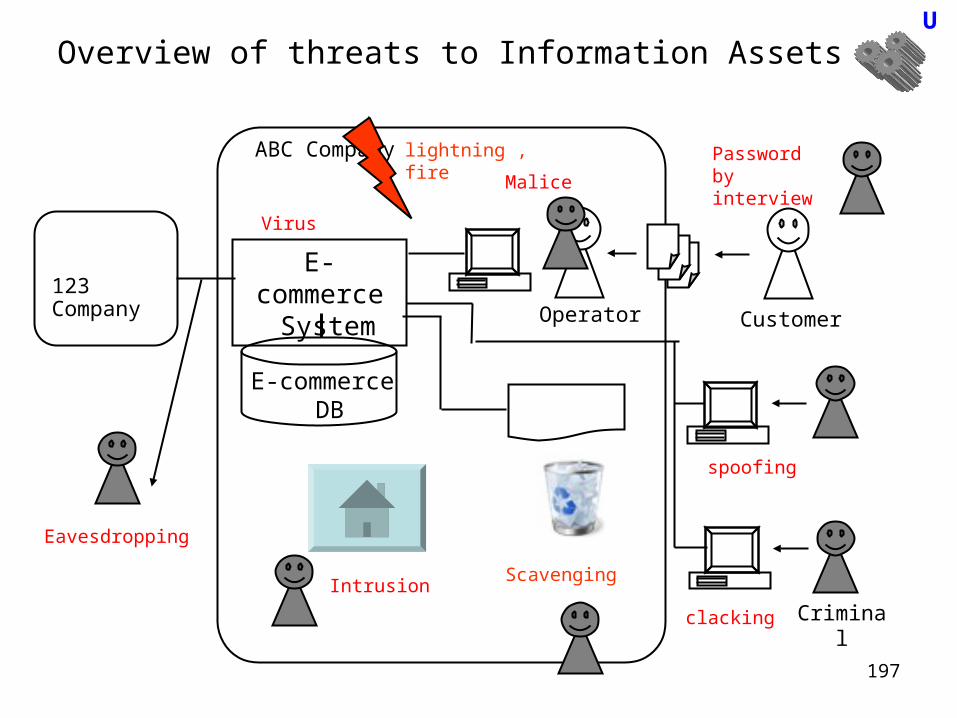

Risk of Operation of Information SystemU

E-commerce System

E-commerce DB

CustomerOperator

Even if the system of ABC Company doesn't have bugs, there are many risks and failures

CustomerError Transactions

Criminal

ABC Company

123Company

XYZCompany

Mistake of input

Illegal access

Inappropriate procedure for error data

Throw out reports

Automated transaction without checking

Inconsistency of data between companies

69

Definition of error, failure and risk in Test and Control

BugDefect

FaultFlaw in component or system to fail to perform its required function

Human Error Human action that produces incorrect result

Failure Deviation of the component or system from its expected delivery, service or result.

U

Risk A factor that could result in future negative result consequences; usually expressed as impact and likelihood

Factor Malice Chang of EnvironmentDisaster, New standard

Test

Remaining Bugs Operation error Crime System Break

Appear and/or occur

Risk

Failure

Risk management and Control

Control preventing from failure

70

Test and ITAC (Control ) and Audit in context of risk management

U

•Test

Activity to get rid of factors to make risks and failures before cut-over•ITAC (IT Application Control)

Activity, process and means to prevent from risks and failures and/ or to reduce affect of risks and failures (after cut-over)

Role of Auditors related to ITAC• Propose and suggest activity, process and means for control• Audit (monitor and check ) controls

71

System Development and IT ControlU

Requirement Analysis

OperationDesign & Program

Testing Migration

Maintenance

Changing

Monitoring

Cut - over

Project Management

Software Quality Assurance

Operation Management

IT Control(ITAC)

Control function

Manual & Procedure

Activity

Regulation

Management

All items are targets of IS audit

72

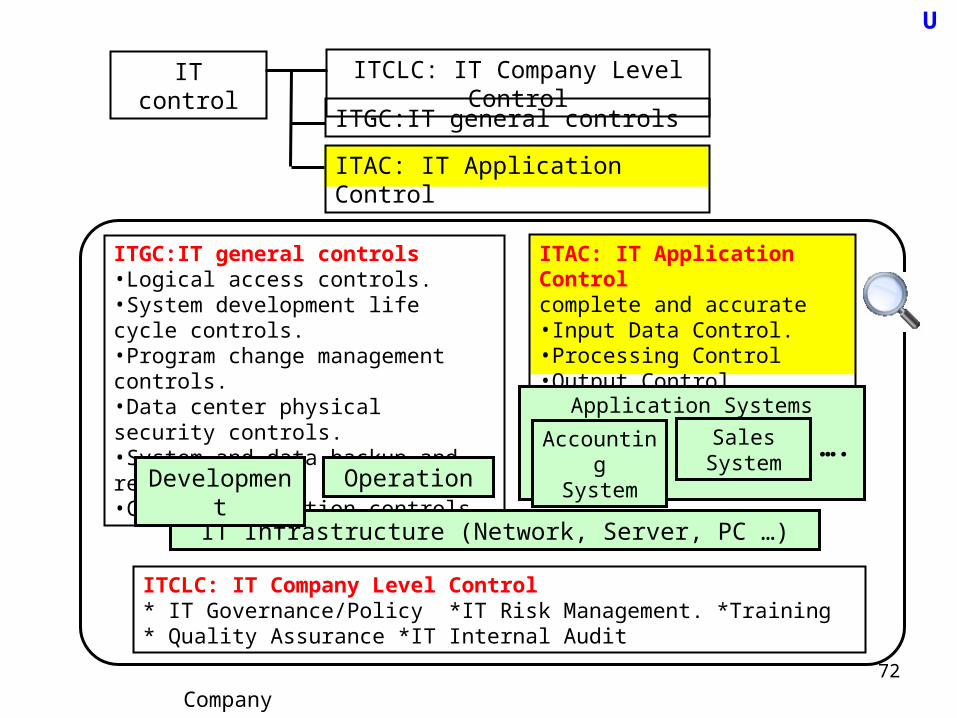

ITGC:IT general controls•Logical access controls.•System development life cycle controls.•Program change management controls.•Data center physical security controls.•System and data backup and recovery•Computer operation controls.

ITGC:IT general controls

U

IT control ITCLC: IT Company Level Control

ITAC: IT Application Control

ITCLC: IT Company Level Control* IT Governance/Policy *IT Risk Management. *Training* Quality Assurance *IT Internal Audit

IT Infrastructure (Network, Server, PC …)

Development Operation

ITAC: IT Application Controlcomplete and accurate •Input Data Control.•Processing Control•Output Control

Application Systems

AccountingSystem

Sales System

Company

….

73

Control Items of ITACU

Input Management

(Control)

Processing Management

(Control)

Output Management

(Control)

ITAC

ITGC Access Management (Control)

User-IDs/Passwords Data SecurityNetwork Security Security AdministrationAccess Authorization

•Data Entry Controls•Input (Transaction) Authorization•Batch control•Segregation of Duties•System Edits•Error Reporting and handling

• Interface Control• Data file control• System Edits• Error Reporting and handling

• Reconciliation• Distribution• Access

Major means of control

74

Overview of Means and TechniqueU

Internal Control

Information System Audit

Human ComputerComputer

&Human

Regulation of Human operation

Working Record

Function of Detecting

Error

Operation Logs

System Logs & Transaction Log

Regulation of Monitoring System

Checking regulations

Checking working Records

Checking System logs

Testing functions

Testing & Monitoring

System

75

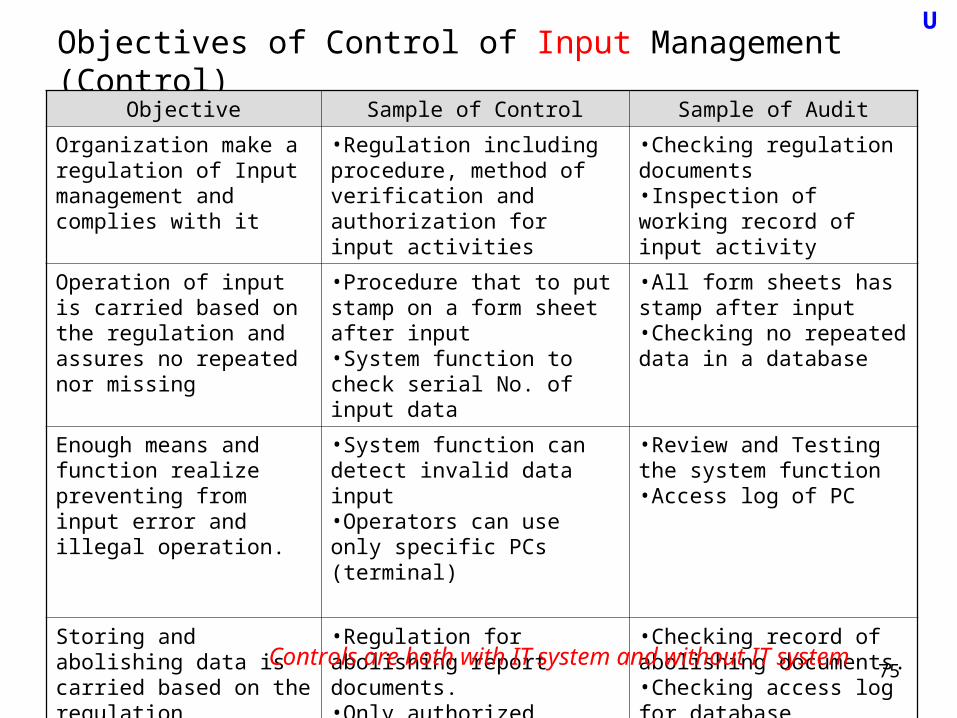

Objectives of Control of Input Management (Control)U

Objective Sample of Control Sample of Audit

Organization make a regulation of Input management and complies with it

•Regulation including procedure, method of verification and authorization for input activities

•Checking regulation documents•Inspection of working record of input activity

Operation of input is carried based on the regulation and assures no repeated nor missing

•Procedure that to put stamp on a form sheet after input •System function to check serial No. of input data

•All form sheets has stamp after input•Checking no repeated data in a database

Enough means and function realize preventing from input error and illegal operation.

•System function can detect invalid data input•Operators can use only specific PCs (terminal)

•Review and Testing the system function•Access log of PC

Storing and abolishing data is carried based on the regulation

•Regulation for abolishing report documents.•Only authorized person access (see) past data.

•Checking record of abolishing documents.•Checking access log for database

Controls are both with IT system and without IT system

76

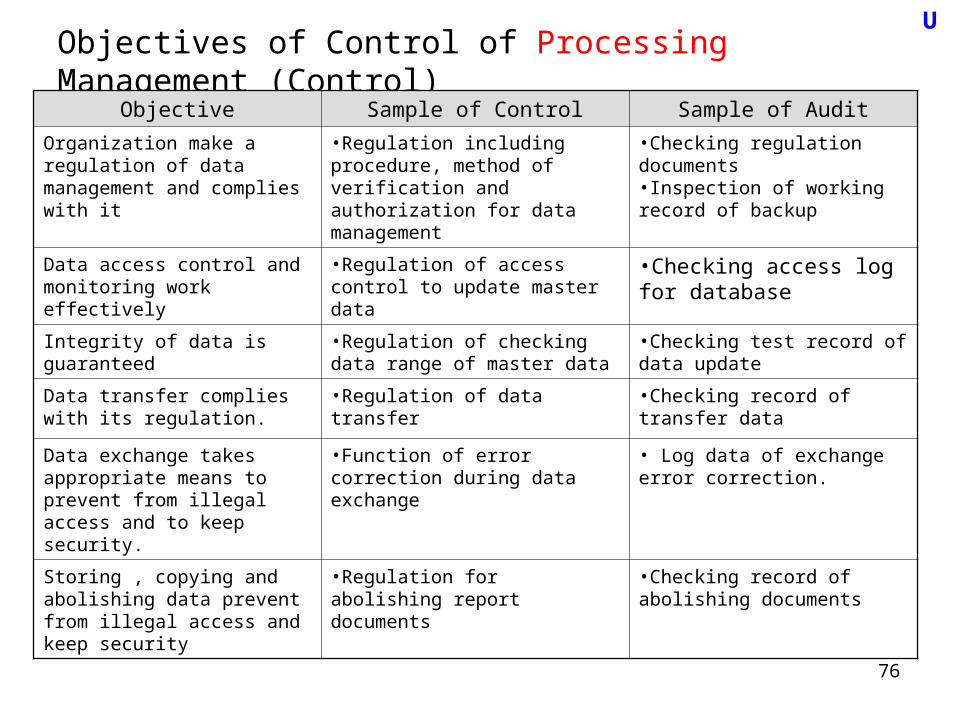

Objectives of Control of Processing Management (Control)U

Objective Sample of Control Sample of Audit

Organization make a regulation of data management and complies with it

•Regulation including procedure, method of verification and authorization for data management

•Checking regulation documents•Inspection of working record of backup

Data access control and monitoring work effectively

•Regulation of access control to update master data

•Checking access log for database

Integrity of data is guaranteed •Regulation of checking data range of master data

•Checking test record of data update

Data transfer complies with its regulation.

•Regulation of data transfer •Checking record of transfer data

Data exchange takes appropriate means to prevent from illegal access and to keep security.

•Function of error correction during data exchange

• Log data of exchange error correction.

Storing , copying and abolishing data prevent from illegal access and keep security

•Regulation for abolishing report documents

•Checking record of abolishing documents

77

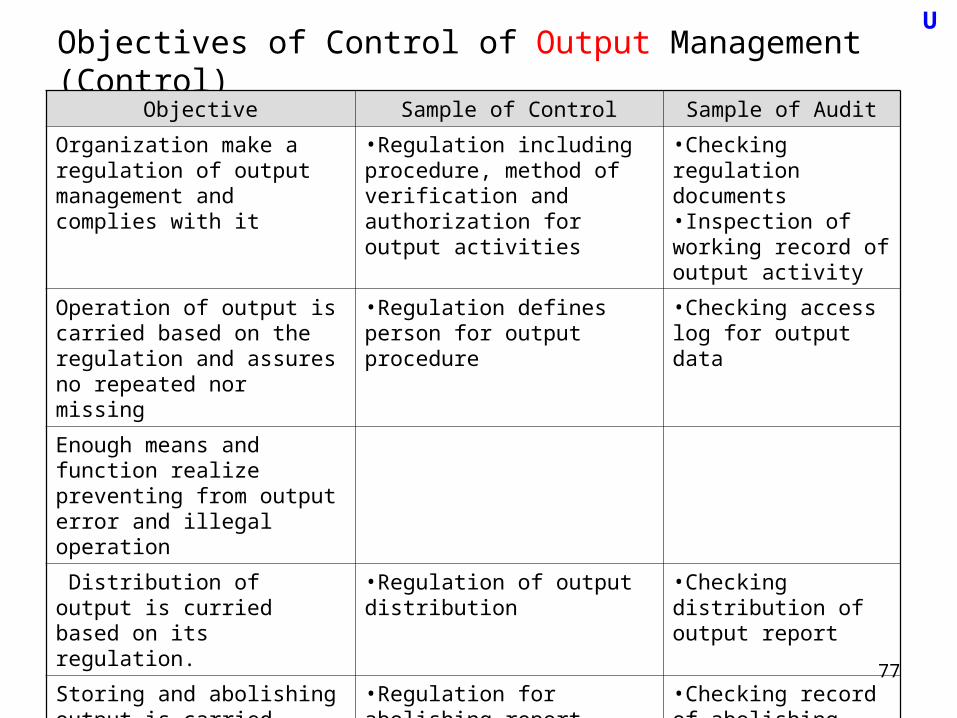

Objectives of Control of Output Management (Control)U

Objective Sample of Control Sample of Audit

Organization make a regulation of output management and complies with it

•Regulation including procedure, method of verification and authorization for output activities

•Checking regulation documents•Inspection of working record of output activity

Operation of output is carried based on the regulation and assures no repeated nor missing

•Regulation defines person for output procedure

•Checking access log for output data

Enough means and function realize preventing from output error and illegal operation

Distribution of output is curried based on its regulation.

•Regulation of output distribution

•Checking distribution of output report

Storing and abolishing output is carried based on the regulation

•Regulation for abolishing report documents

•Checking record of abolishing documents.

78

Technique and Means of Control of Input Management (Control)

U

Area Description

Date control preparation

•Good design source document or form- Grouping similar input fields- Providing appropriate code to reduce error- Containing appropriate serial No. and cross-reference No.- Appropriate input filed style to reduce error- Including Appropriate filed for document authorization

Input Authorization

•Signature on form or souse document•Online Access Control (Only authorized individual can access specific information)•Unique password (Don’t share password nor grant password to others)•Usage of specific terminals or specific area.•Segregation of duties

Batch control

•Appropriate batch header form including application name, transaction code, preprinted No., identification data,•Total minatory amount (Verification the total monetary values of items processed equals the total monetary values of batch documents.•Total items ( No. of units ordered in the batch and No. of units processed)•Total num of documents•Hash totals (Verification of total of Hash value: no meaning in the form, but preprinted the fixed numbers)•Reviewing online batching input by manager.

79

Technique and Means of Control of Input ( Processing) Management

U

Area Description

Regulation and Monitoring

•Transaction log ( input process and batch process)•Documented Regulation•Transmittal log•Cancellation of source document ( By pouncing with holes or marking to avoid duplicate entry)

Error Reporting and Handling

•Appropriate error handing- Rejecting only transition with error- Rejecting the whole batch of transition- Holding the batch as suspense- Accepting the batch and flagging error transactions•Appropriate error collection procedure- logging of errors- Timely corrections- Upstream resubmission- Approval of correction- Suspense file- Error file- Validity of corrections

80

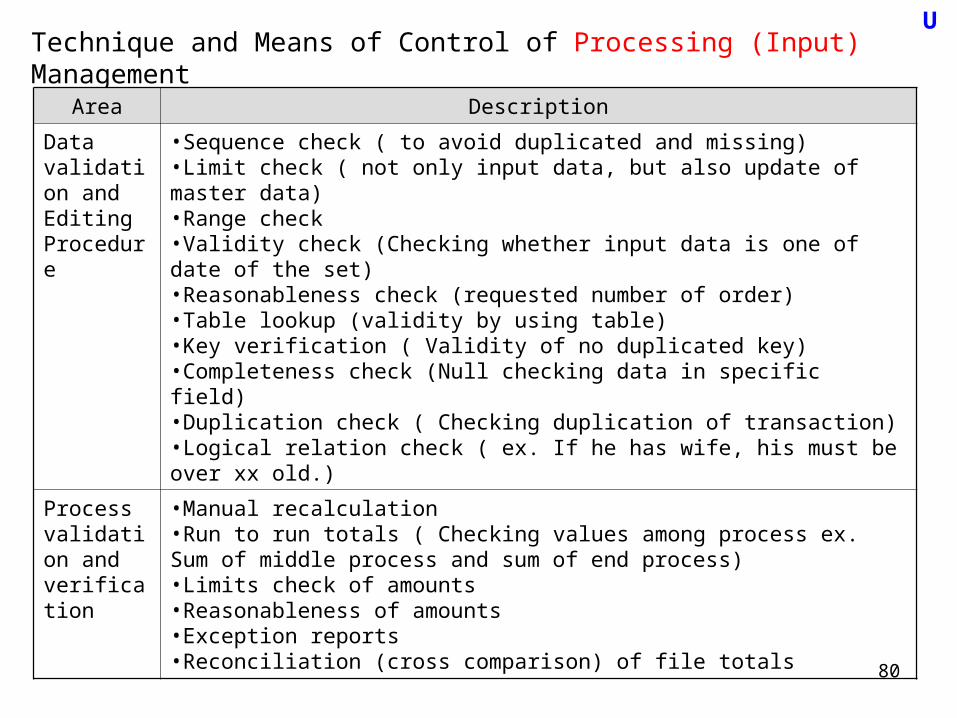

Technique and Means of Control of Processing (Input) Management

U

Area Description

Data validation and Editing Procedure

•Sequence check ( to avoid duplicated and missing)•Limit check ( not only input data, but also update of master data)•Range check•Validity check (Checking whether input data is one of date of the set)•Reasonableness check (requested number of order)•Table lookup (validity by using table)•Key verification ( Validity of no duplicated key)•Completeness check (Null checking data in specific field)•Duplication check ( Checking duplication of transaction)•Logical relation check ( ex. If he has wife, his must be over xx old.)

Process validation and verification

•Manual recalculation•Run to run totals ( Checking values among process ex. Sum of middle process and sum of end process)•Limits check of amounts•Reasonableness of amounts•Exception reports•Reconciliation (cross comparison) of file totals

81

Technique and Means of Control of Processing Management

U

Area Description

Data File Control

•Before and after image report ( Difference proves transactions done correctly)•Maintenance error reporting and handling (Checking and reviewing error handing by personnel who did not handle)•Source document retention ( Verification of file and source data)•Internal and external labeling (labeling on physical removable storage such as tapes and disk cartridge.•Version management•Data file security•One for one checking ( Verification by comparison between data and source document)•Transaction log•File updating and maintenance authorization•Parity checking

Type of data files•System control parameter (Configuration parameter)•Master data (Standing data) : Not be changed by transaction•Master data (Balancing data): Be changed by transaction•Transaction file

82

Technique and Means of Control of Output Management

U

Area Description

Outputvalidation Procedure

•Sequence check ( to avoid duplicated and missing)•Balancing and reconciling•Log of online distribution

Output delivery and storage

•Logging and storage of negotiable, sensitive and critical forms in secure place•Computer generation of negotiable instrument, forms and signature including intelligent property.•Appropriate report printing and distribution including electric reporting- Control of printing spool- Authentication of printing- printing in secure and safe room- Delivery and recipient evidence such as a signature•Output report retention•Output error handling

83

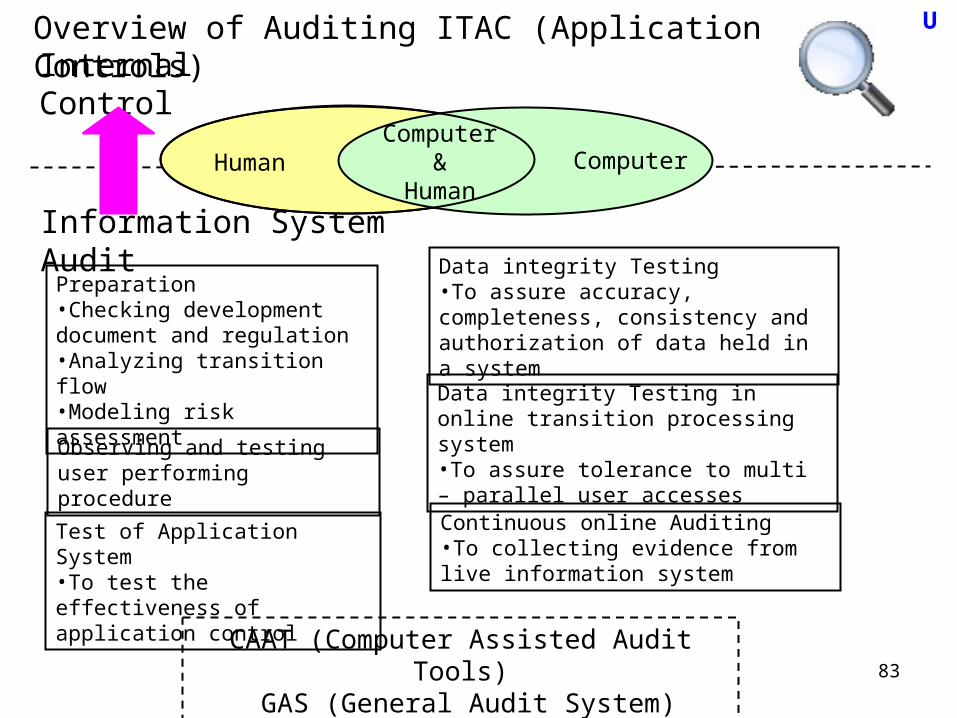

Overview of Auditing ITAC (Application Controls)U

Internal Control

Information System Audit

Human ComputerComputer &Human

Observing and testing user performing procedure

Preparation•Checking development document and regulation•Analyzing transition flow•Modeling risk assessment Data integrity Testing in online transition

processing system•To assure tolerance to multi – parallel user accesses

Data integrity Testing•To assure accuracy, completeness, consistency and authorization of data held in a system

Test of Application System•To test the effectiveness of application control

Continuous online Auditing•To collecting evidence from live information system

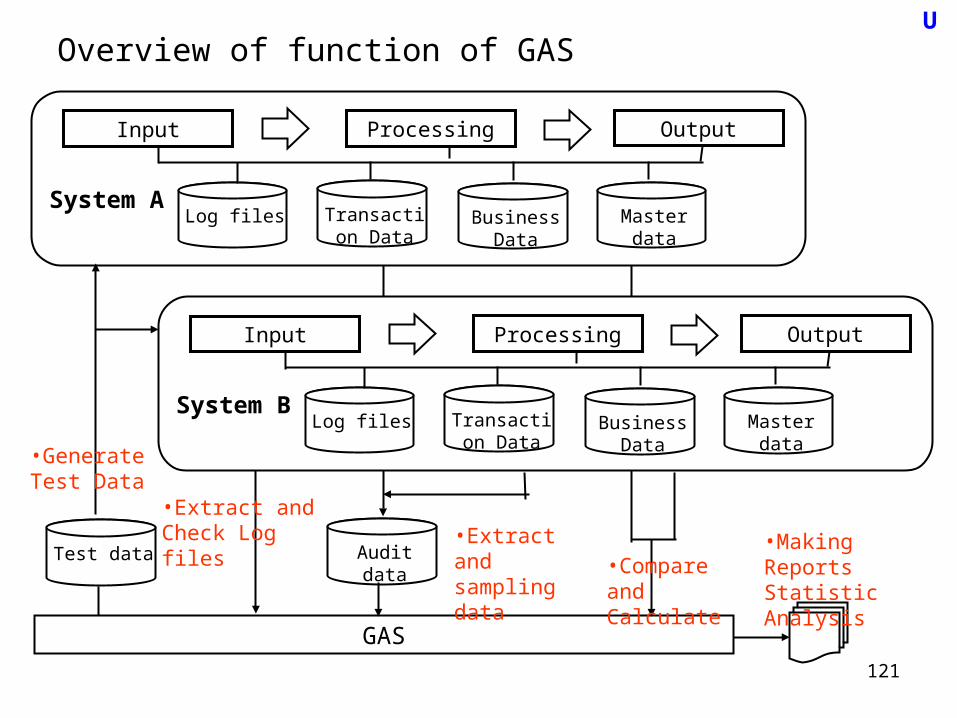

CAAT (Computer Assisted Audit Tools) GAS (General Audit System)

84

Preparation of Auditing for ITAC

U

Area Description

Checking document and interview

•System methodology documents•Function design documents•User manual/ Operation manual and regulation•Technical reference document•Records of program changes

Analyzing transition flow

•To find important controls•To find week point of transitions and controls

Modeling risk assessment

Factors of risk model•Quality of Internal condition•Economic condition / Regulatory agency impact•Time in existence•Staff turn over•Time elapsed since last audit / Prior audit result•Complexity of operation•Recent account system changes / Recent changes in key position•Transaction volume / Monetary volume•Sensitivity of transition•Impact of application failure

85

Methods and Targets of Observing and testing user performing procedure: Auditing ITAC

U

Area Description

Separation of duties •Ensure that no individual ha the capability of more than one following process: input, authorization, verification and distribution by reviewing job descriptions and authorization levels.

Balancing •Verify run-to-run control totals and other application totals

Error control and correction

•Error and correction reports provide evidence of appropriate review, timely correction and resubmission.

Distribution of reports

•Critical output reports should be produced and maintained in secure area and distributed in an authorized manner.

Review and testing of access authorization and capability

•Access control tables provide information for individual access level, To test appropriate access rule as management intended.•Activity report or access (log-in) log provide detail information of actual access, especially violation log of access should be reviewed.

86

Methods and Targets of Data integrity TestingU

•Data integrity testing is set of substantive tests that examines Accuracy, Completeness, Consistency and Authorization.

•Failure of data integrity is result of failure of input and/ processing. Because of this, data integrity testing uses similar method and technique of testing input control.

•Two type of data integrity- Relational integrity Targets are each record level and/or items in record. Relational integrity is enforced by checking data function of input process and - Reference integrity Targets are existence relationships between entities in deferent tables of a database. It is necessary that references (by primary key and foreign key )be kept consistent in the event of Insert, Delete and Update.

87

Methods and Targets of Data integrity Testing in online transition processing system

U

Importance of data integrity is known as ACID principal.

•AtomicityFrom the user perspective, a transition is either completed or net at all. If an error or interruption occurred, all changed made up to the point are backed out.

•ConsistencyAll integrity conditions in the database are maintained.

•IsolationUnder multi user condition, each transaction is isolated from other transitions.

•DurabilityIf a transaction has been reported to user as complete, the result of changes to database survive subsequent hardware or software failures.

88

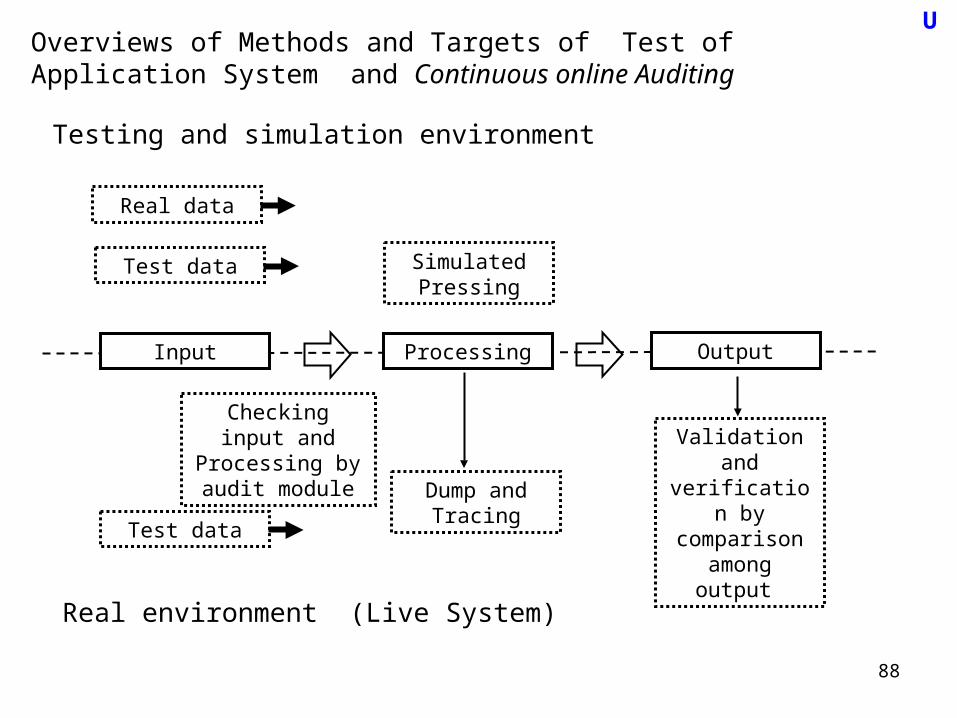

Overviews of Methods and Targets of Test of Application System and Continuous online Auditing

U

Input Processing Output

Testing and simulation environment

Real environment (Live System)

Test data

Dump and Tracing

Validation and verification by comparison

among output

Simulated Pressing

Test data

Real data

Checking input and Processing by audit module

89

Methods and Targets of Test of Application System and Continuous online Auditing (1)

U

Method Description Comment

Mapping •To detect code that is not tested. Similar to measuring testing coverage.

•To Need function to measure coverage

Tracing and Tagging

•To trace specific transaction in real or simulated system

•To Need skill for tracing or development of tracing function

Test data /deck •Inputting teat data to real system. The result is expected.

•It doesn’t prove that all the code done.

Base case system evaluation

•Testing by using test cases of integrated testing

•To Need a lot of time and effort to conduct the test

Parallel operation •To compare old system and new system with same data

Parallel Simulation •To check real (live) data by using simulation program that has same process logic as real system

•To Need development of simulation program

Extended Record •To extract specific data and transaction to audit files. (Manual or automatically with audit module)

•When using audit module, to Need development of program

90

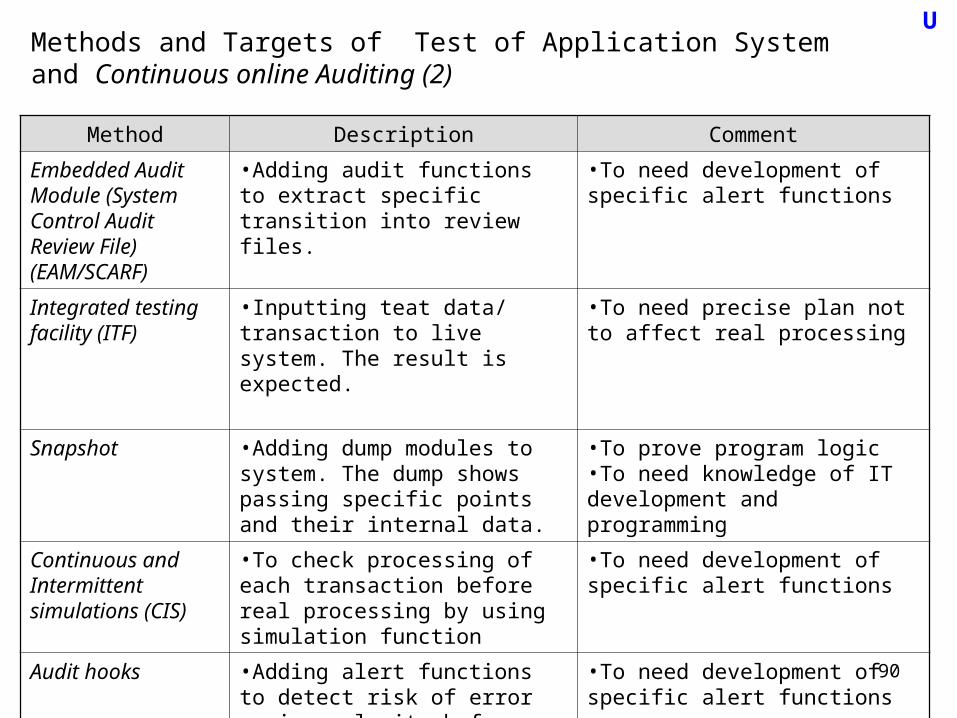

Methods and Targets of Test of Application System and Continuous online Auditing (2)

U

Method Description Comment

Embedded Audit Module (System Control Audit Review File) (EAM/SCARF)

•Adding audit functions to extract specific transition into review files.

•To need development of specific alert functions

Integrated testing facility (ITF)

•Inputting teat data/ transaction to live system. The result is expected.

•To need precise plan not to affect real processing

Snapshot •Adding dump modules to system. The dump shows passing specific points and their internal data.

•To prove program logic•To need knowledge of IT development and programming

Continuous and Intermittent simulations (CIS)

•To check processing of each transaction before real processing by using simulation function

•To need development of specific alert functions

Audit hooks •Adding alert functions to detect risk of error or irregularity before serious failure

•To need development of specific alert functions

91

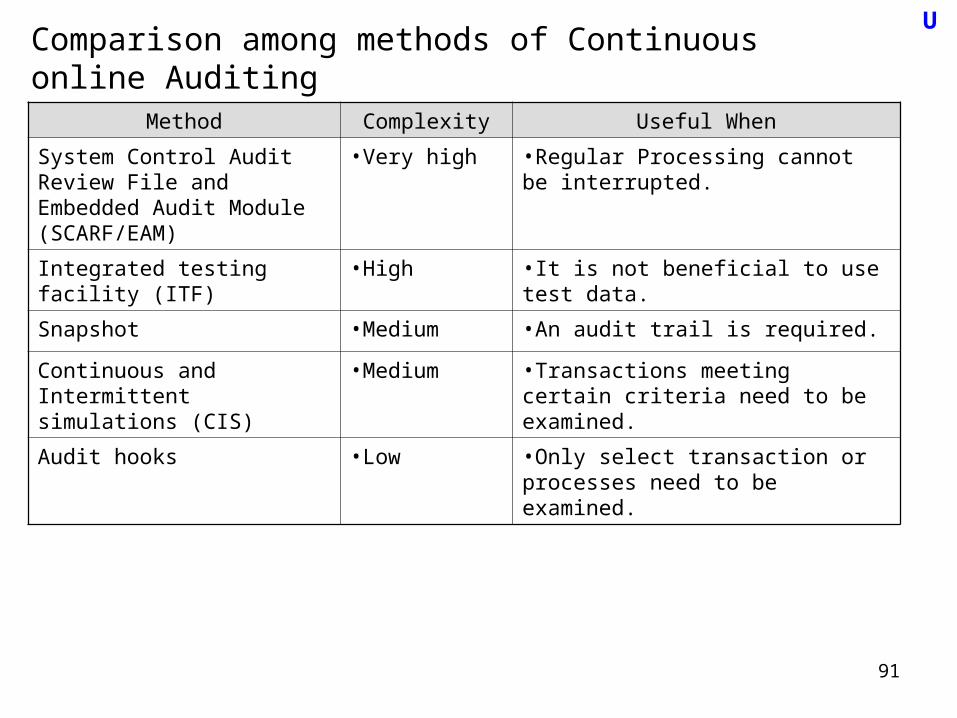

Comparison among methods of Continuous online AuditingU

Method Complexity Useful When

System Control Audit Review File and Embedded Audit Module (SCARF/EAM)

•Very high •Regular Processing cannot be interrupted.

Integrated testing facility (ITF) •High •It is not beneficial to use test data.

Snapshot •Medium •An audit trail is required.

Continuous and Intermittent simulations (CIS)

•Medium •Transactions meeting certain criteria need to be examined.

Audit hooks •Low •Only select transaction or processes need to be examined.

92

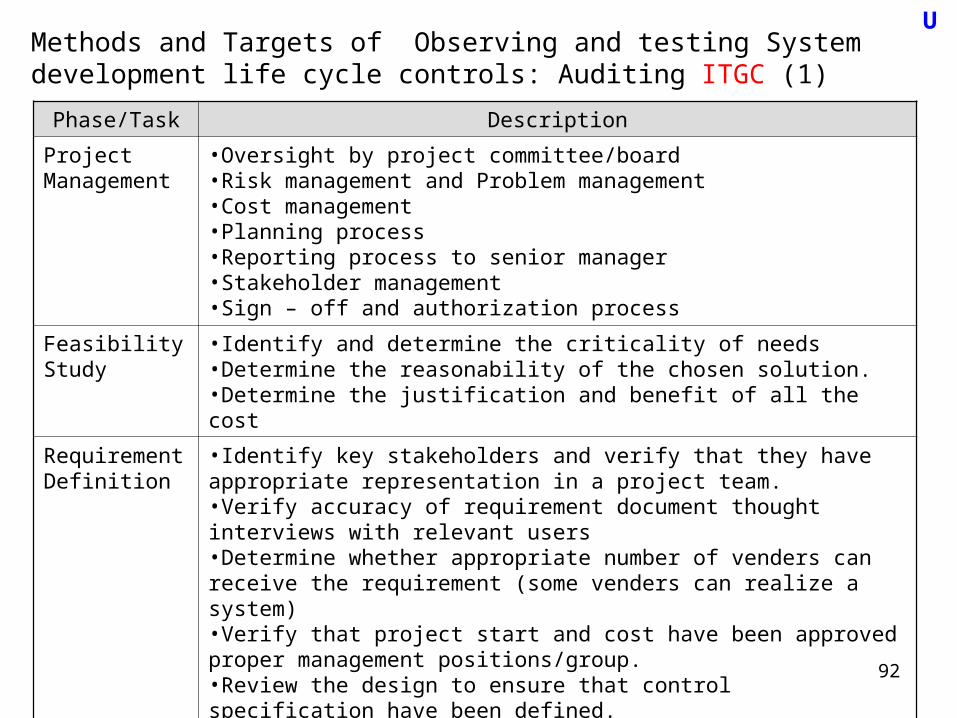

Methods and Targets of Observing and testing System development life cycle controls: Auditing ITGC (1)

U

Phase/Task Description

Project Management

•Oversight by project committee/board•Risk management and Problem management•Cost management•Planning process•Reporting process to senior manager•Stakeholder management•Sign – off and authorization process

Feasibility Study

•Identify and determine the criticality of needs•Determine the reasonability of the chosen solution.•Determine the justification and benefit of all the cost

Requirement Definition

•Identify key stakeholders and verify that they have appropriate representation in a project team.•Verify accuracy of requirement document thought interviews with relevant users•Determine whether appropriate number of venders can receive the requirement (some venders can realize a system)•Verify that project start and cost have been approved proper management positions/group.•Review the design to ensure that control specification have been defined.•Survey and design whether a system needs some embedded audit functions

93

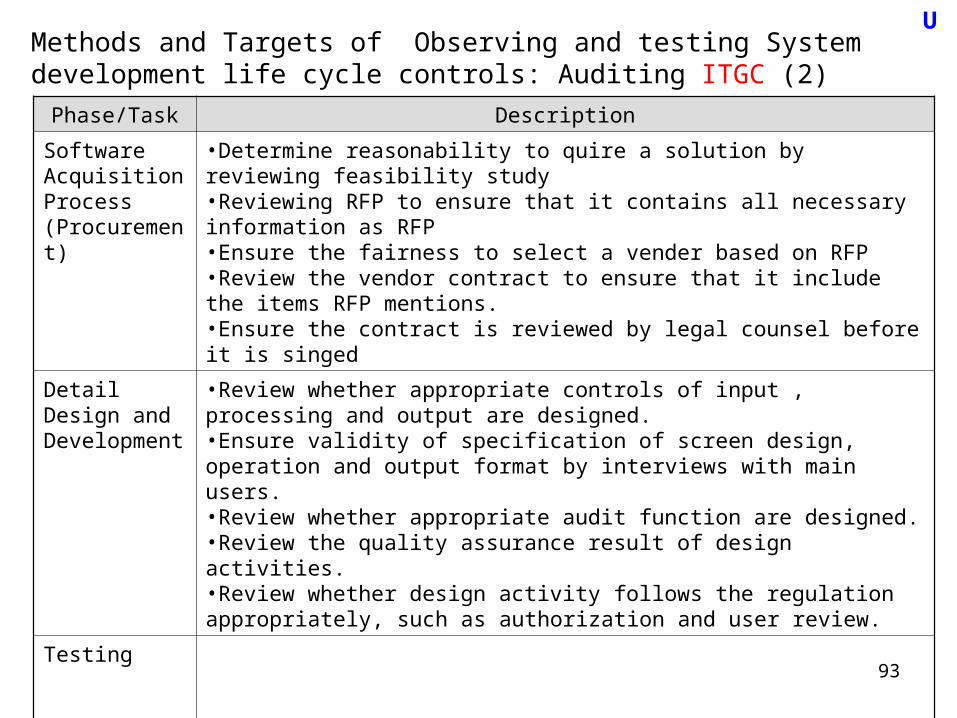

Methods and Targets of Observing and testing System development life cycle controls: Auditing ITGC (2)

U

Phase/Task Description

Software Acquisition Process (Procurement)

•Determine reasonability to quire a solution by reviewing feasibility study•Reviewing RFP to ensure that it contains all necessary information as RFP•Ensure the fairness to select a vender based on RFP•Review the vendor contract to ensure that it include the items RFP mentions.•Ensure the contract is reviewed by legal counsel before it is singed

Detail Design and Development

•Review whether appropriate controls of input , processing and output are designed.•Ensure validity of specification of screen design, operation and output format by interviews with main users.•Review whether appropriate audit function are designed.•Review the quality assurance result of design activities.•Review whether design activity follows the regulation appropriately, such as authorization and user review.

Testing

94

Chapter 2.Domain1:

IS Audit Process

U

95

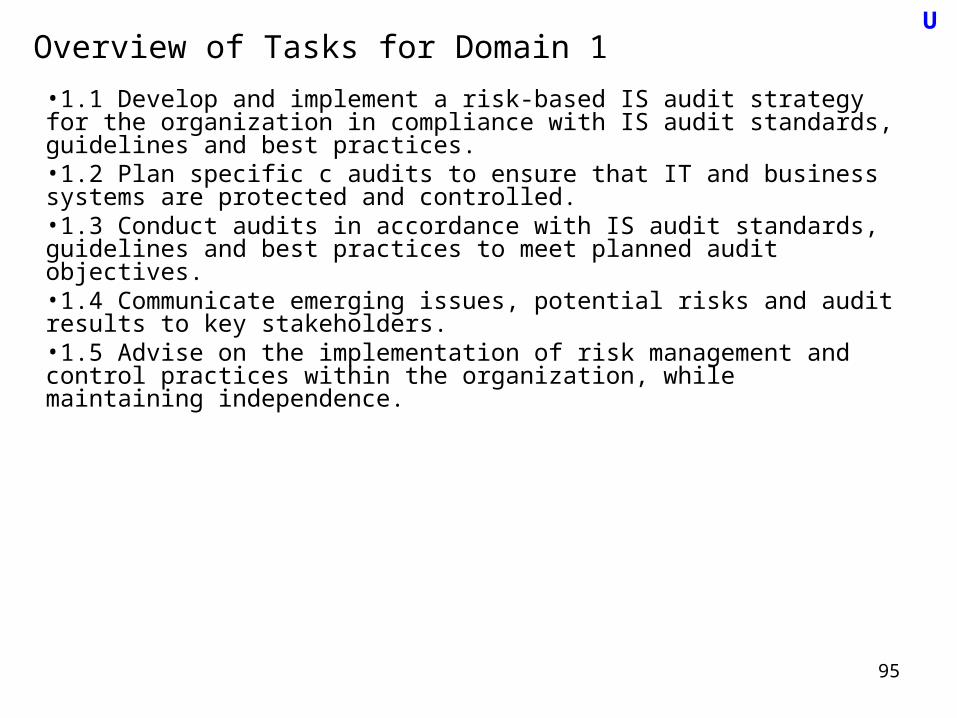

Overview of Tasks for Domain 1

•1.1 Develop and implement a risk-based IS audit strategy for the organization in compliance with IS audit standards, guidelines and best practices.•1.2 Plan specific c audits to ensure that IT and business systems are protected and controlled.•1.3 Conduct audits in accordance with IS audit standards, guidelines and best practices to meet planned audit objectives.•1.4 Communicate emerging issues, potential risks and audit results to key stakeholders.•1.5 Advise on the implementation of risk management and control practices within the organization, while maintaining independence.

U

96

Overview of skill and knowledge for Domain 1U

•1.1 ISACA IS Auditing Standards, Guidelines and Procedures and the Code of Professional Ethics

•1.2 IS auditing practices and techniques

•1.3 techniques to gather information and preserve evidence (e.g., observation, inquiry, interview, CAATTs and electronic media)

•1.4 the evidence life cycle (e.g., the collection, protection, chain of custody)

•1.5 control objectives and controls related to IS (e.g., COBIT)

•1.6 risk assessment in an audit context

•1.7 audit planning and management techniques

•1.8 reporting and communication techniques (e.g., facilitation, negotiation and confl ict resolution)

•1.9 control self-assessment (CSA)

•1.10 continuous audit techniques

97

IS Audit Small Quiz No.3

Domain 3 IS Audit Process

Subject: Audit Planning, Risk Management, Methods of Audit and Audit Reporting

U

Quiz book

98

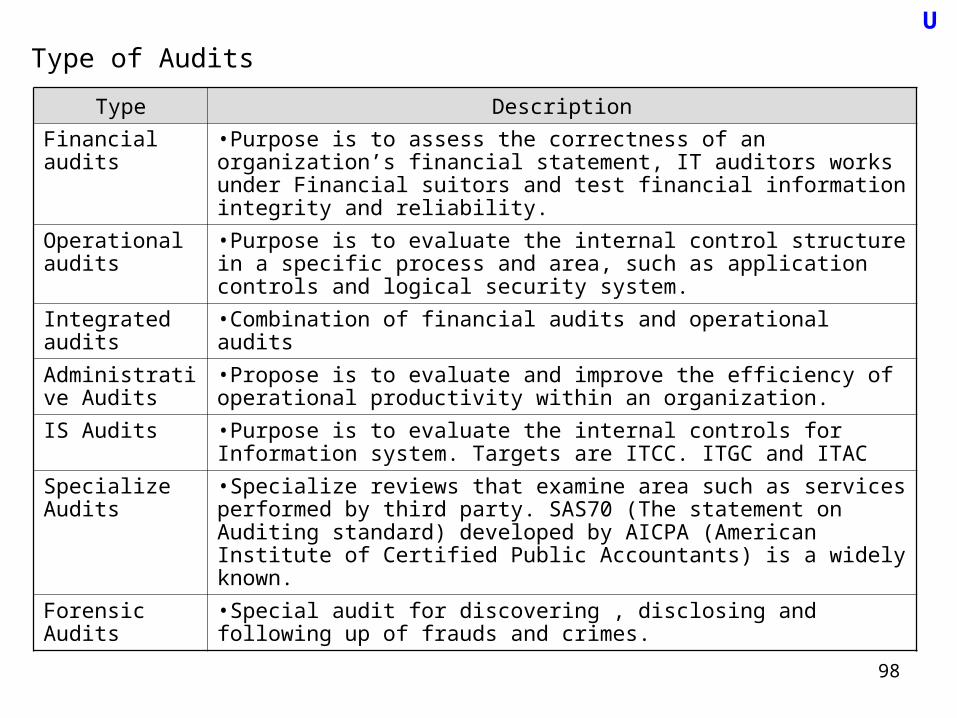

Type of Audits

U

Type Description

Financial audits •Purpose is to assess the correctness of an organization’s financial statement, IT auditors works under Financial suitors and test financial information integrity and reliability.

Operational audits

•Purpose is to evaluate the internal control structure in a specific process and area, such as application controls and logical security system.

Integrated audits

•Combination of financial audits and operational audits

Administrative Audits

•Propose is to evaluate and improve the efficiency of operational productivity within an organization.

IS Audits •Purpose is to evaluate the internal controls for Information system. Targets are ITCC. ITGC and ITAC

Specialize Audits

•Specialize reviews that examine area such as services performed by third party. SAS70 (The statement on Auditing standard) developed by AICPA (American Institute of Certified Public Accountants) is a widely known.

Forensic Audits •Special audit for discovering , disclosing and following up of frauds and crimes.

99

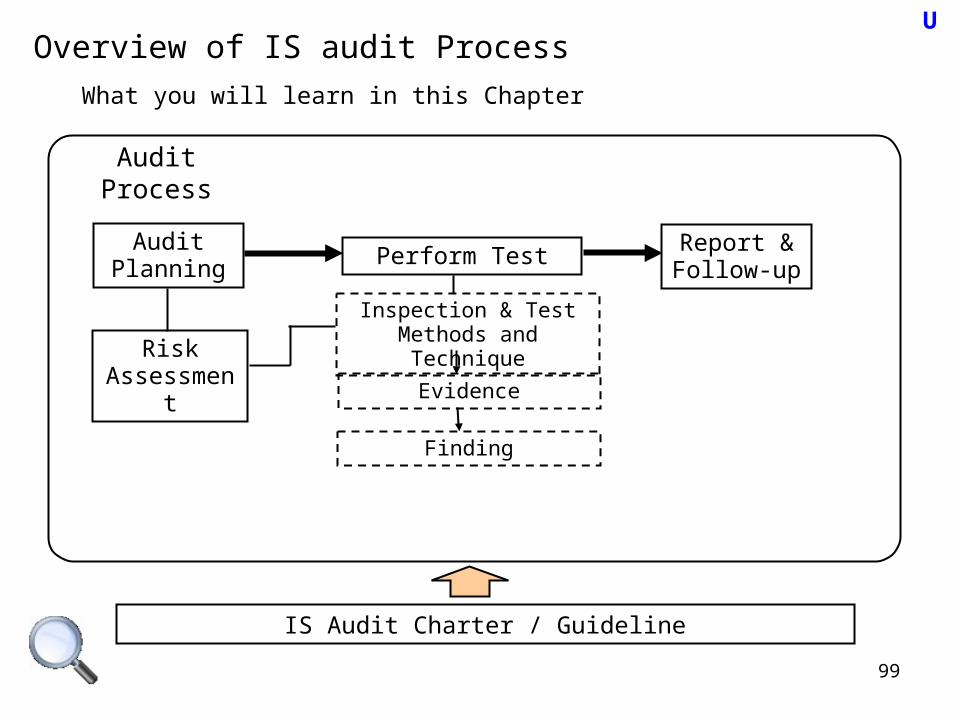

Overview of IS audit ProcessU

IS Audit Charter / Guideline

Audit Process

Audit Planning

Risk Assessment

Perform Test

Inspection & Test Methods and Technique

Evidence

Finding

Report & Follow-up

What you will learn in this Chapter

100

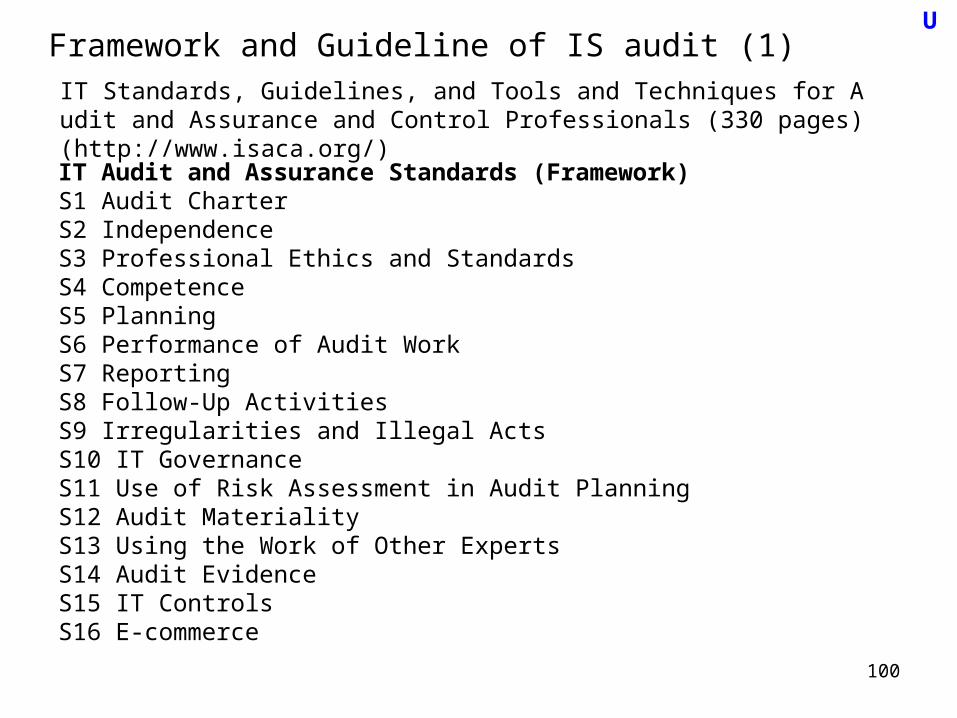

Framework and Guideline of IS audit (1)U

IT Standards, Guidelines, and Tools and Techniques for Audit and Assurance and Control Professionals (330 pages) (http://www.isaca.org/)

IT Audit and Assurance Standards (Framework)S1 Audit CharterS2 IndependenceS3 Professional Ethics and StandardsS4 CompetenceS5 PlanningS6 Performance of Audit WorkS7 ReportingS8 Follow-Up ActivitiesS9 Irregularities and Illegal ActsS10 IT GovernanceS11 Use of Risk Assessment in Audit PlanningS12 Audit Materiality S13 Using the Work of Other ExpertsS14 Audit EvidenceS15 IT ControlsS16 E-commerce

101

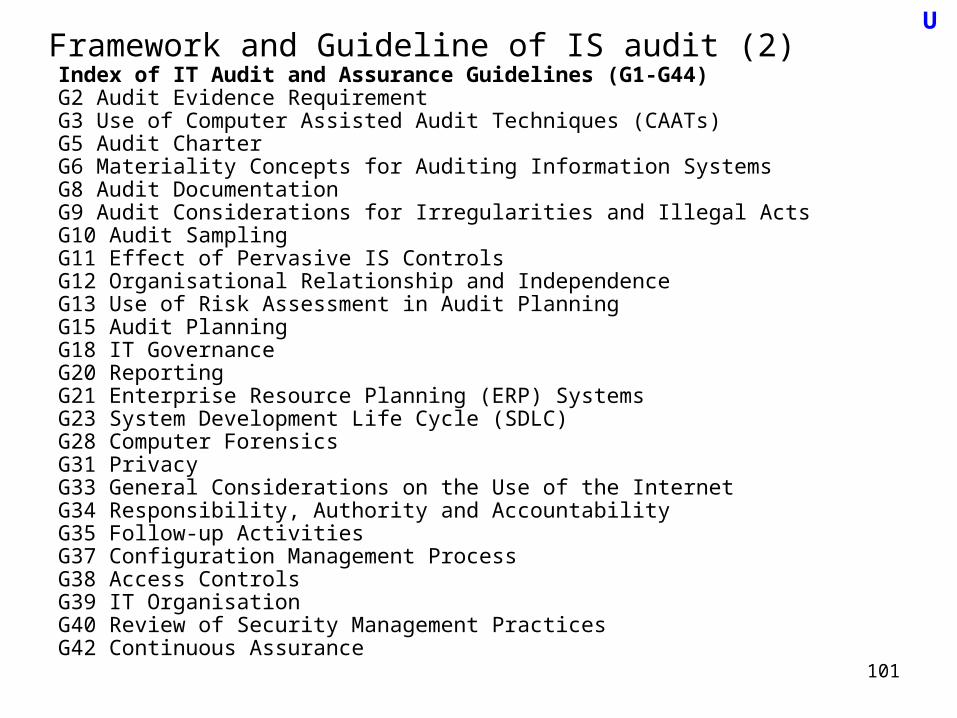

Framework and Guideline of IS audit (2)U

Index of IT Audit and Assurance Guidelines (G1-G44)G2 Audit Evidence Requirement G3 Use of Computer Assisted Audit Techniques (CAATs) G5 Audit Charter G6 Materiality Concepts for Auditing Information Systems G8 Audit Documentation G9 Audit Considerations for Irregularities and Illegal Acts G10 Audit Sampling G11 Effect of Pervasive IS Controls G12 Organisational Relationship and Independence G13 Use of Risk Assessment in Audit Planning G15 Audit Planning G18 IT GovernanceG20 Reporting G21 Enterprise Resource Planning (ERP) Systems G23 System Development Life Cycle (SDLC) G28 Computer Forensics G31 Privacy G33 General Considerations on the Use of the Internet G34 Responsibility, Authority and Accountability G35 Follow-up Activities G37 Configuration Management Process G38 Access ControlsG39 IT Organisation G40 Review of Security Management PracticesG42 Continuous Assurance

102

Framework and Guideline of IS audit (3)U

Index of IT Audit and Assurance Tools and TechniquesP1 IS Risk AssessmentP2 Digital Signatures P3 Intrusion DetectionP4 Viruses and other Malicious Code P5 Control Risk Self-assessmentP6 Firewalls P7 Irregularities and Illegal ActsP8 Security Assessment—Penetration Testing and Vulnerability AnalysisP9 Evaluation of Management Controls Over Encryption MethodologiesP10 Business Application Change ControlP11 Electronic Funds Transfer (EFT)

103

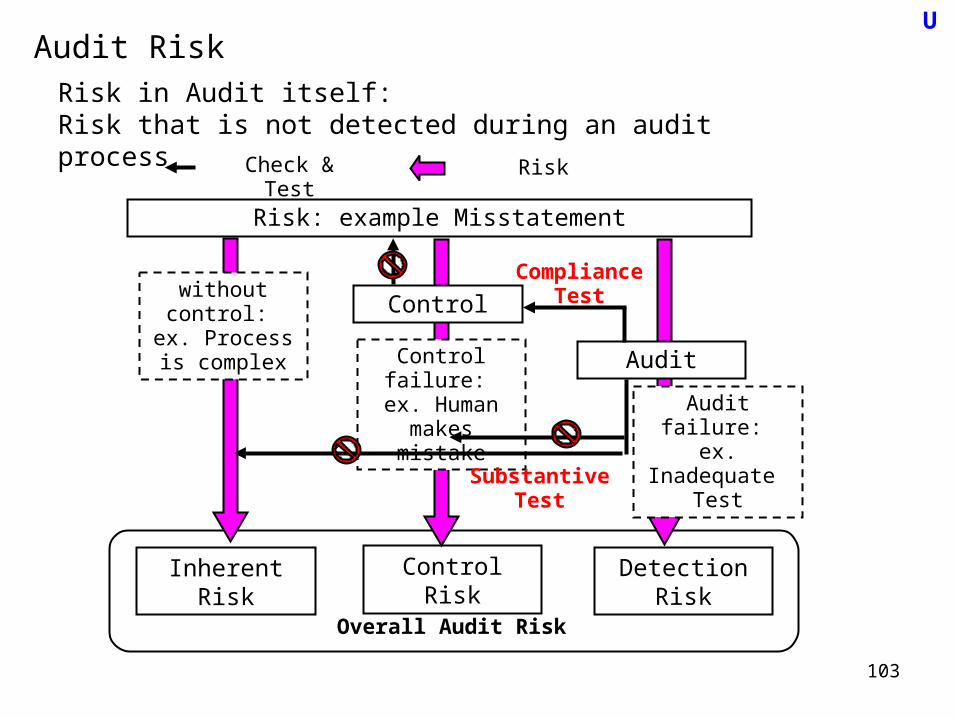

Audit RiskU

Inherent Risk

Risk in Audit itself:Risk that is not detected during an audit process

Risk: example Misstatement

without control: ex. Process is

complex

Check & Test

Control

Control failure: ex. Human

makes mistake

Risk

Audit

Control Risk

Audit failure: ex. Inadequate

Test

Detection Risk

Overall Audit Risk

Compliance Test

Substantive Test

104

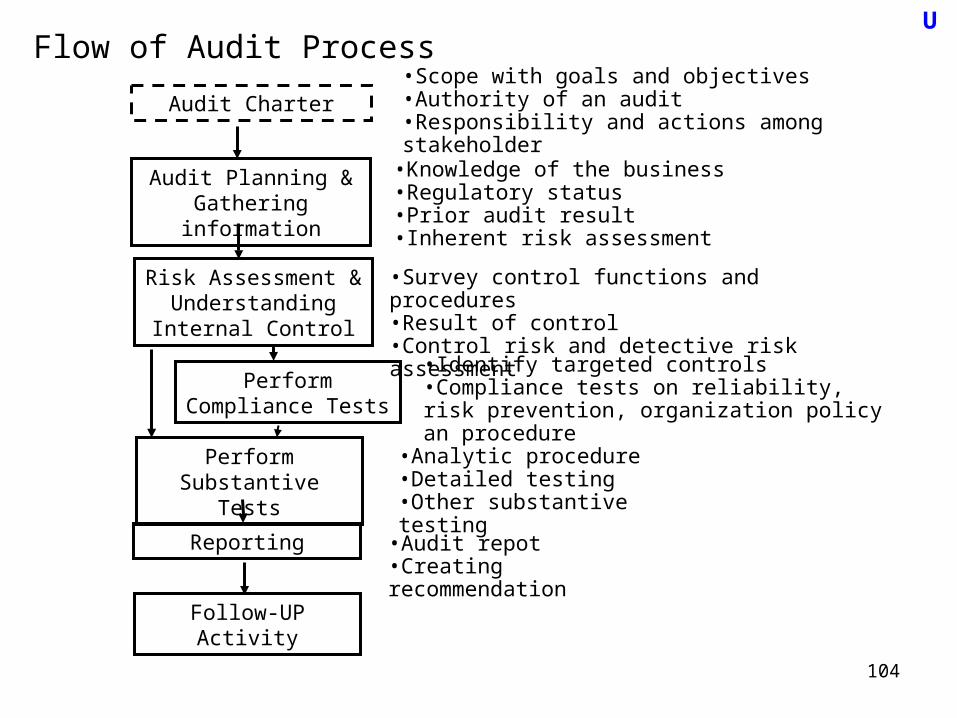

Flow of Audit ProcessU

Audit Planning & Gathering information

Perform Compliance Tests

Reporting

Follow-UPActivity

Audit Charter

Risk Assessment & Understanding Internal

Control

Perform Substantive Tests

•Audit repot•Creating recommendation

•Analytic procedure•Detailed testing•Other substantive testing

•Identify targeted controls•Compliance tests on reliability, risk prevention, organization policy an procedure

•Survey control functions and procedures•Result of control•Control risk and detective risk assessment

•Knowledge of the business•Regulatory status•Prior audit result•Inherent risk assessment

•Scope with goals and objectives•Authority of an audit•Responsibility and actions among stakeholder

105

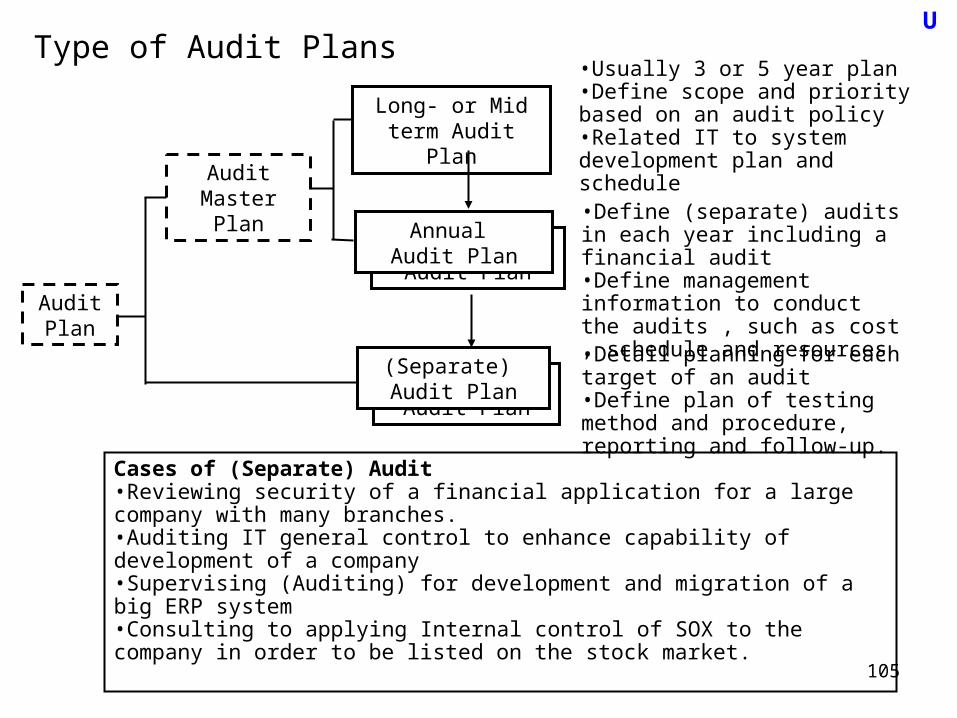

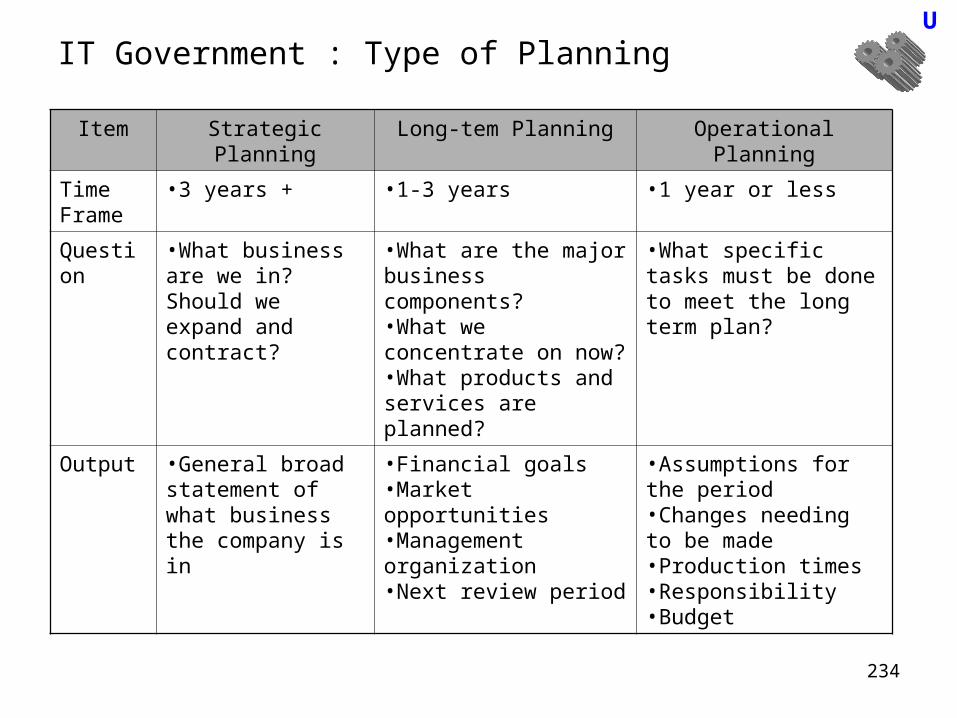

(Separate) Audit Plan

Type of Audit PlansU

Long- or Mid term Audit Plan

Audit Plan

•Detail planning for each target of an audit•Define plan of testing method and procedure, reporting and follow-up.

•Define (separate) audits in each year including a financial audit•Define management information to conduct the audits , such as cost , schedule and resources

Audit Master Plan

Annual Audit Plan

Annual Audit Plan

(Separate) Audit Plan

•Usually 3 or 5 year plan•Define scope and priority based on an audit policy•Related IT to system development plan and schedule

Cases of (Separate) Audit•Reviewing security of a financial application for a large company with many branches.•Auditing IT general control to enhance capability of development of a company•Supervising (Auditing) for development and migration of a big ERP system•Consulting to applying Internal control of SOX to the company in order to be listed on the stock market.

106

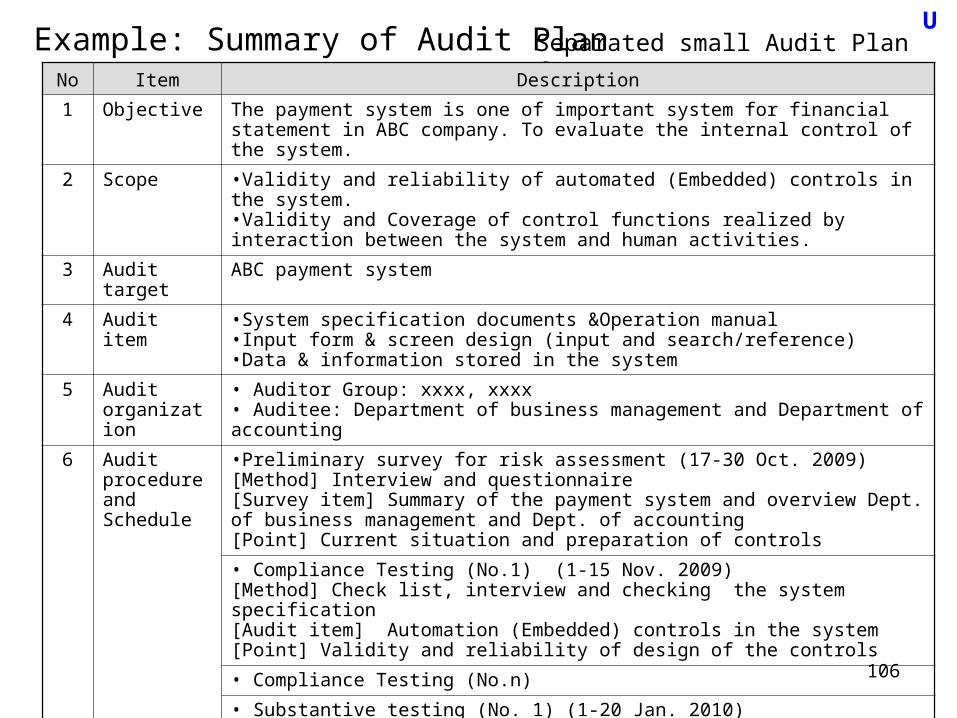

Example: Summary of Audit PlanU

Separated small Audit Plan for ITAC

No Item Description

1 Objective The payment system is one of important system for financial statement in ABC company. To evaluate the internal control of the system.

2 Scope •Validity and reliability of automated (Embedded) controls in the system.•Validity and Coverage of control functions realized by interaction between the system and human activities.

3 Audit target ABC payment system

4 Audit item •System specification documents &Operation manual •Input form & screen design (input and search/reference)•Data & information stored in the system

5 Audit organization

• Auditor Group: xxxx, xxxx• Auditee: Department of business management and Department of accounting

6 Audit procedure and Schedule

•Preliminary survey for risk assessment (17-30 Oct. 2009)[Method] Interview and questionnaire[Survey item] Summary of the payment system and overview Dept. of business management and Dept. of accounting[Point] Current situation and preparation of controls

• Compliance Testing (No.1) (1-15 Nov. 2009)[Method] Check list, interview and checking the system specification[Audit item] Automation (Embedded) controls in the system[Point] Validity and reliability of design of the controls

• Compliance Testing (No.n)

• Substantive testing (No. 1) (1-20 Jan. 2010)[Method] Comparison between database and printed quotation. Checking transaction log.[Point] Testing of result of control functions.

107

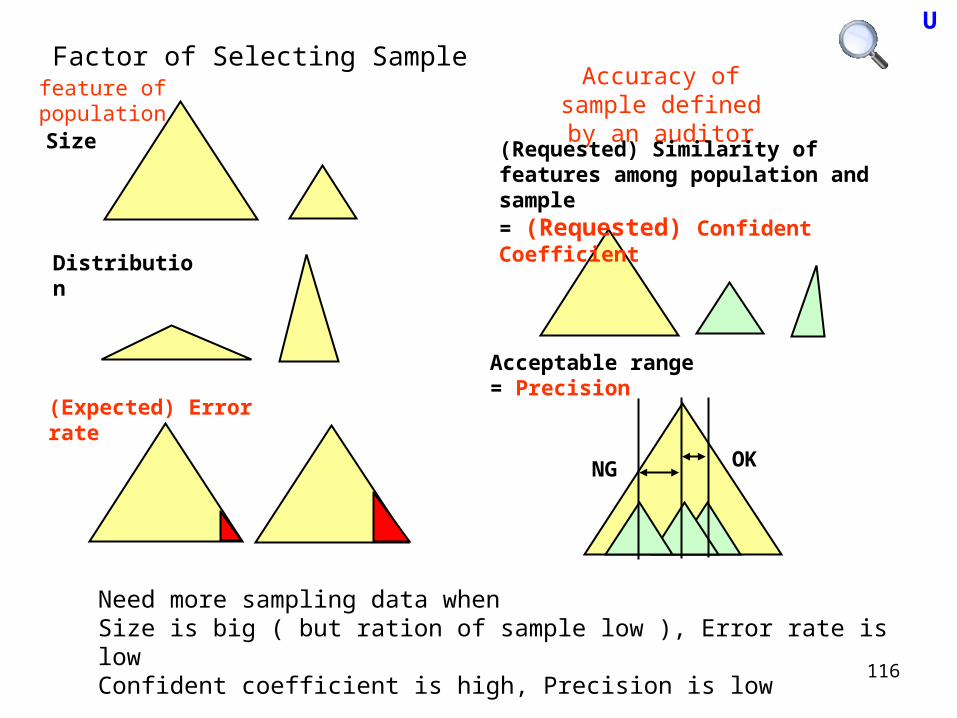

General idea of Risk Assessment (Evaluation)U

Basic element of Evaluating risks•Impact, Effect•Probabilities, likelihood

Big Medium Small

Often Fatal Serious Serious

Sometimes Serious Serious Minor

Rare Serious Minor Minor

Very Simple Risk Evaluation Table (weighting by Impact & Probability)

ImpactProbability

Other (further) Assessment methods•Weighting by dividing detail factorsImpact => Sensitivity of the function to executive management, MaterialityProbability => Extent of system or process change, Complexity•Ranking <- one reason of why auditors use risk assessmentTo multiple weight of business impact to making ranking score.Weight of business impact: example: Financial risk, Strategic risk, Operational risk and Legal compliance

108

Example: Summary of Risk Assessment DocumentU

No Category Risk Description Eva. Control

Covering all payment transaction

Missing invoice by EDI

Invoice by EDI has trouble and missing

1 Checking EDI’s invoice by human

Error transition

Error Transactions are not reported/ detected

3 Module for listing out error transition

Correctness of payment date

Input error Mistake of input for invoice by FAX

4 Cross checking to order transition

Not include inappropriate data

Cancel of invoice

Payment to cancel invoice

2 Procedure of cancellation of invoice

Security of operation xxx xxxx xxxxx

Integrity of payment data

xxx xxxx xxxxx

No authorized DB modification

xxx xxxx xxxxx

Contents of risk assessment document•A description of the risk assessment methodology used•The identification of significant exposures and the corresponding risks•The risks and exposures the audit is intended to address•The audit evidence used to support the IS auditor’s assessment of risk

109

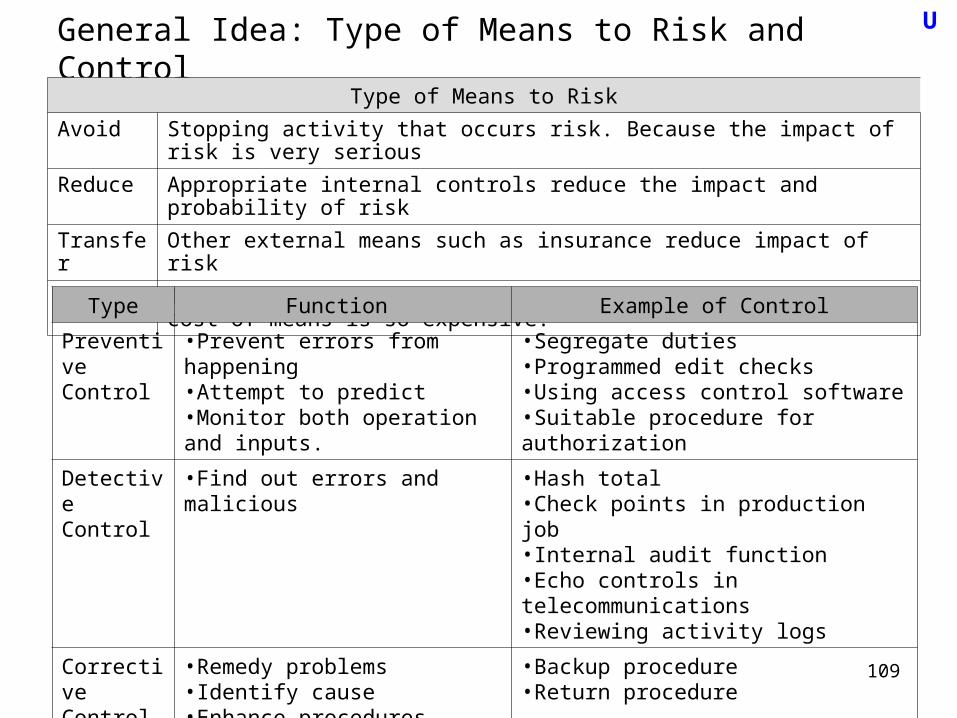

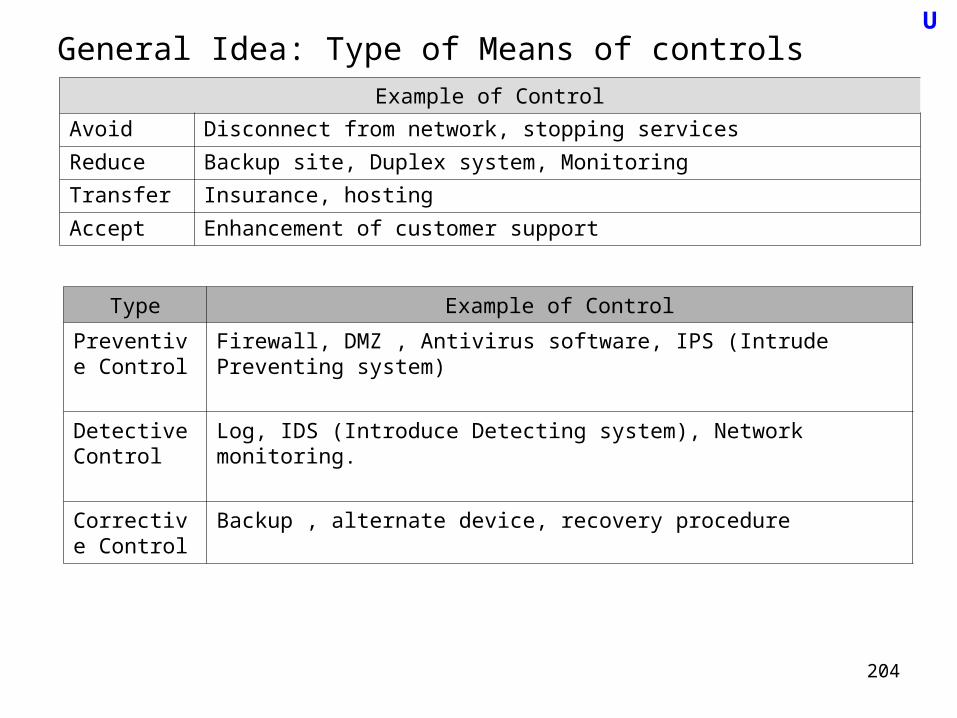

General Idea: Type of Means to Risk and ControlType of Means to Risk

Avoid Stopping activity that occurs risk. Because the impact of risk is very serious

Reduce Appropriate internal controls reduce the impact and probability of risk

Transfer Other external means such as insurance reduce impact of risk

Accept Impact of risk would be accepted, because impact is low or cost of means is so expensive.

U

Type Function Example of Control

Preventive Control

•Prevent errors from happening•Attempt to predict•Monitor both operation and inputs.

•Segregate duties•Programmed edit checks•Using access control software•Suitable procedure for authorization

Detective Control

•Find out errors and malicious •Hash total•Check points in production job•Internal audit function•Echo controls in telecommunications•Reviewing activity logs

Corrective Control

•Remedy problems•Identify cause•Enhance procedures•Minimize the impact of a threat

•Backup procedure•Return procedure

110

Overview of Method and Technique for Survey and Testing U

Audit Planning & Gathering information

Perform Compliance Tests

Risk Assessment & Understanding Internal

Control

Perform Substantive Tests

Survey and Testing

Evidence : Fact

Review

Interview & Observation

Questionnaire

Testing

Method of Statistics

CAAT (Computer Assisted Audit

Techniques

111

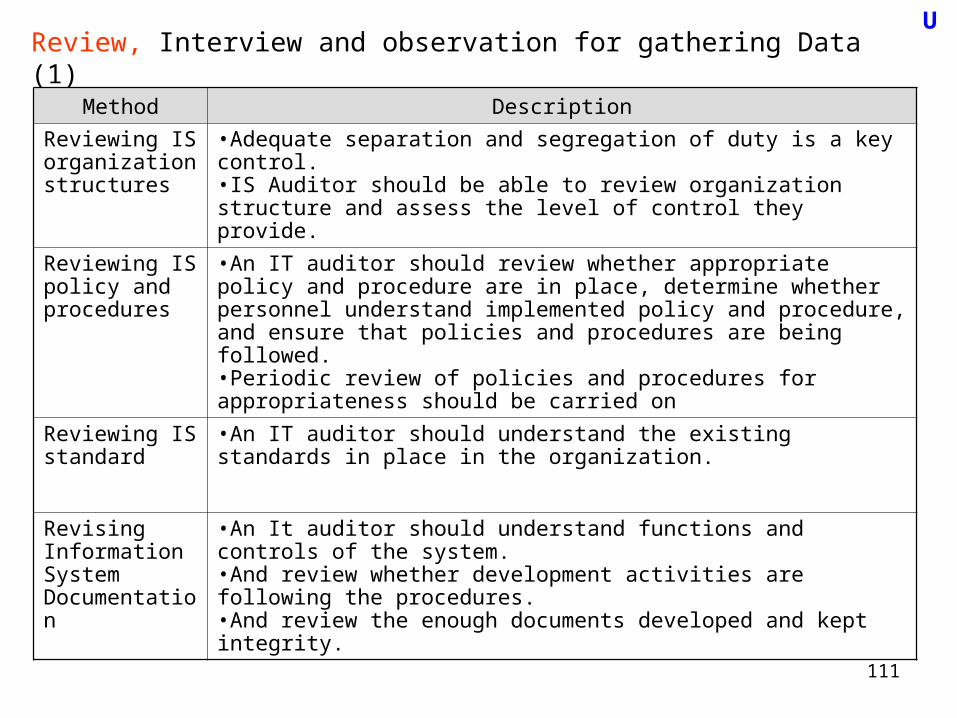

Review, Interview and observation for gathering Data (1)

U

Method Description

Reviewing IS organization structures

•Adequate separation and segregation of duty is a key control.•IS Auditor should be able to review organization structure and assess the level of control they provide.

Reviewing IS policy and procedures

•An IT auditor should review whether appropriate policy and procedure are in place, determine whether personnel understand implemented policy and procedure, and ensure that policies and procedures are being followed.•Periodic review of policies and procedures for appropriateness should be carried on

Reviewing IS standard

•An IT auditor should understand the existing standards in place in the organization.

Revising Information System Documentation

•An It auditor should understand functions and controls of the system.•And review whether development activities are following the procedures.•And review the enough documents developed and kept integrity.

112

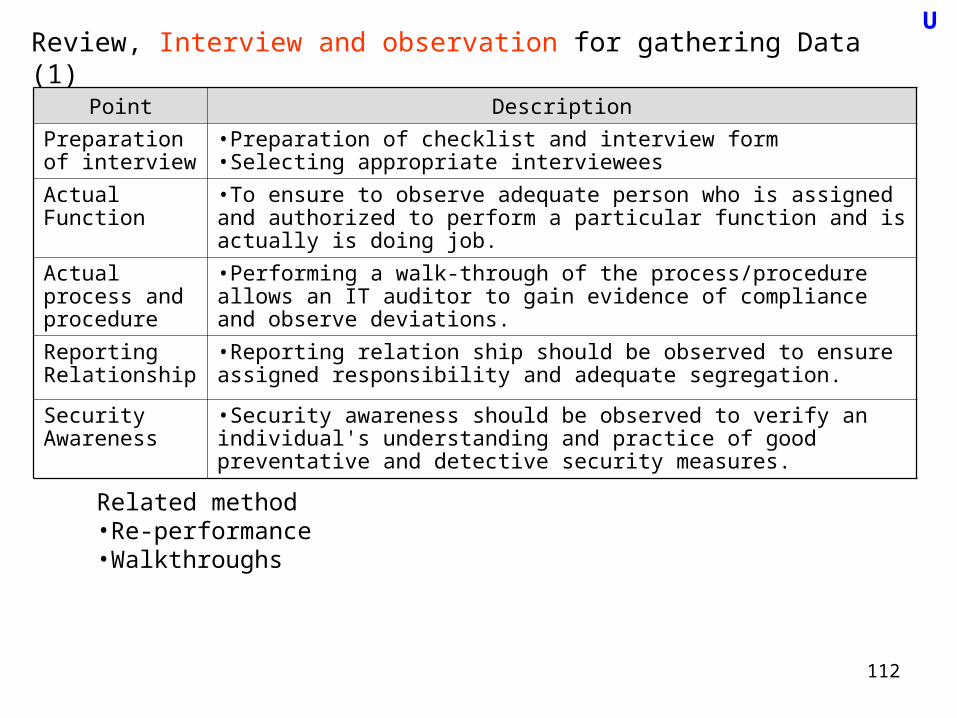

Review, Interview and observation for gathering Data (1)

U

Point Description

Preparation of interview

•Preparation of checklist and interview form•Selecting appropriate interviewees

Actual Function •To ensure to observe adequate person who is assigned and authorized to perform a particular function and is actually is doing job.

Actual process and procedure