Embed Size (px)

Citation preview

1 January 2014 Renewals A Buyer’s Market : The Non-Life 2014 Renewal 23rd January 2014

Matthew Day – GC Business Intelligence Ben Grimwade – GC Benelux & Property Solutions Group

GUY CARPENTER

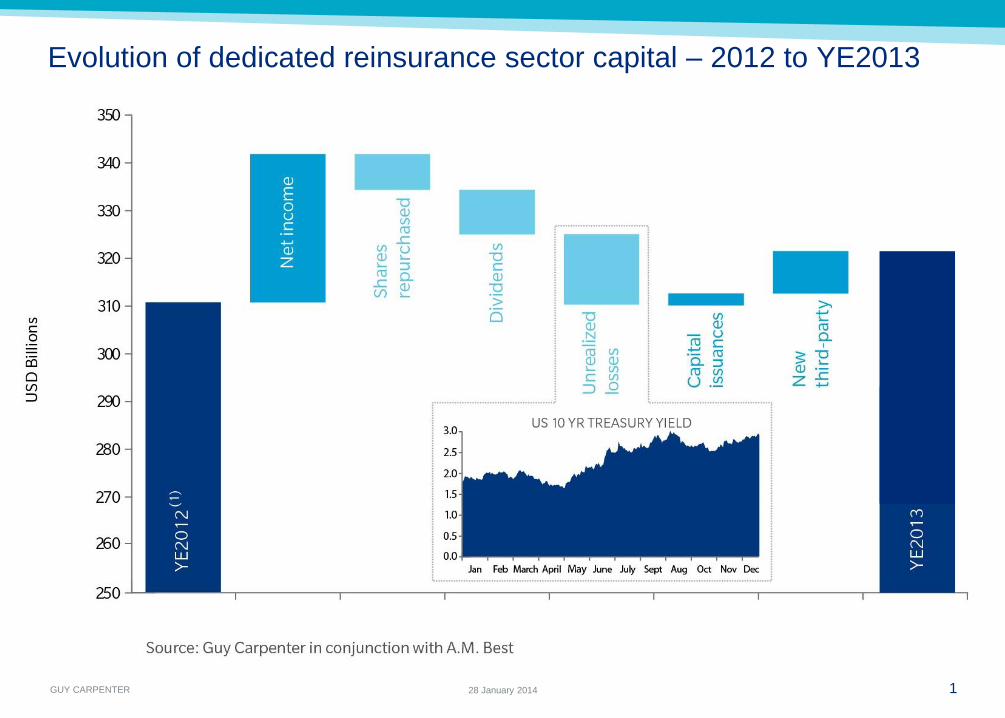

Evolution of dedicated reinsurance sector capital – 2012 to YE2013

1 28 January 2014

GUY CARPENTER

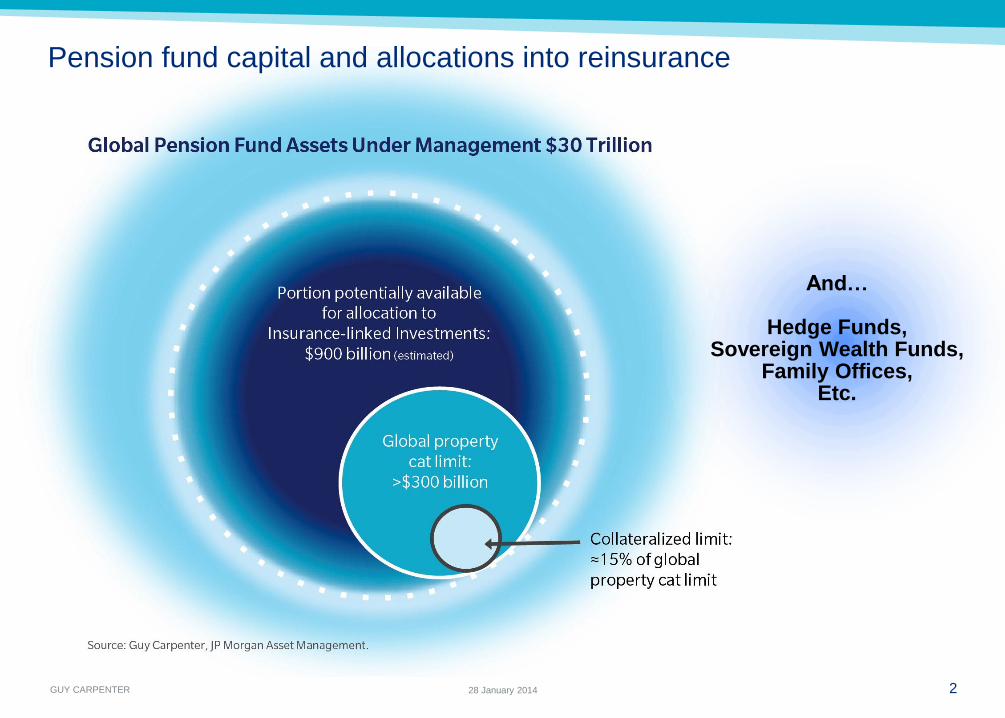

Pension fund capital and allocations into reinsurance

And…

Hedge Funds, Sovereign Wealth Funds,

Family Offices, Etc.

28 January 2014 2

GUY CARPENTER

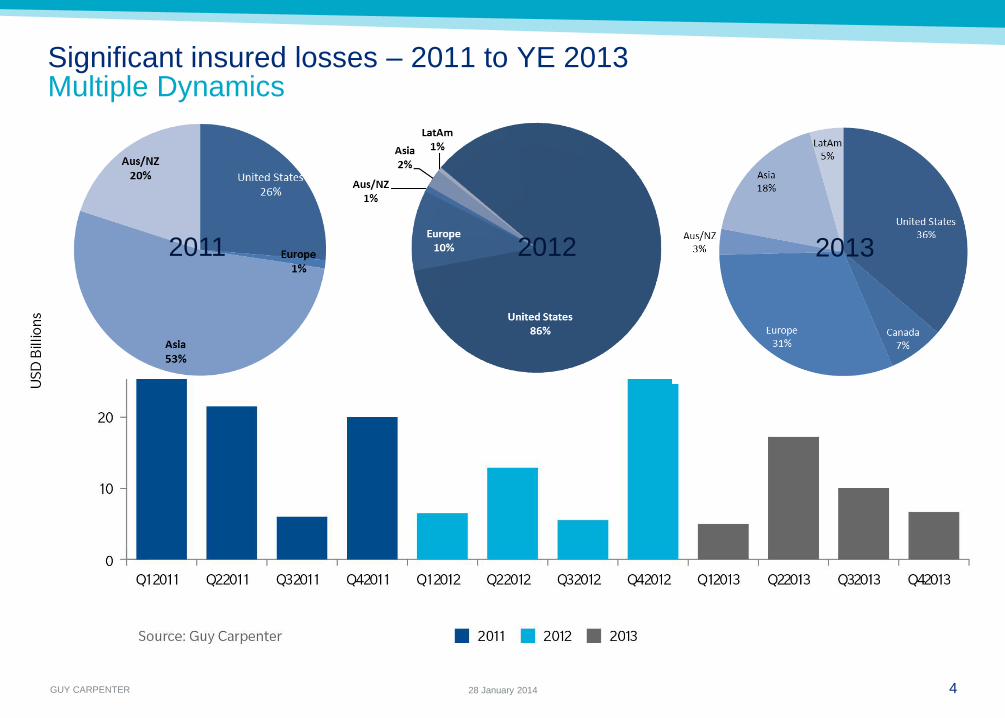

Significant insured losses – 2011 to YE 2013 Multiple Dynamics

3 28 January 2014

Tohoku Earthquake approx. $35bn

Hurricane Sandy approx. $25bn

Eastern European Flood approx. $4bn

GUY CARPENTER

Significant insured losses – 2011 to YE 2013 Multiple Dynamics

4 28 January 2014

2011 2012 2013

GUY CARPENTER

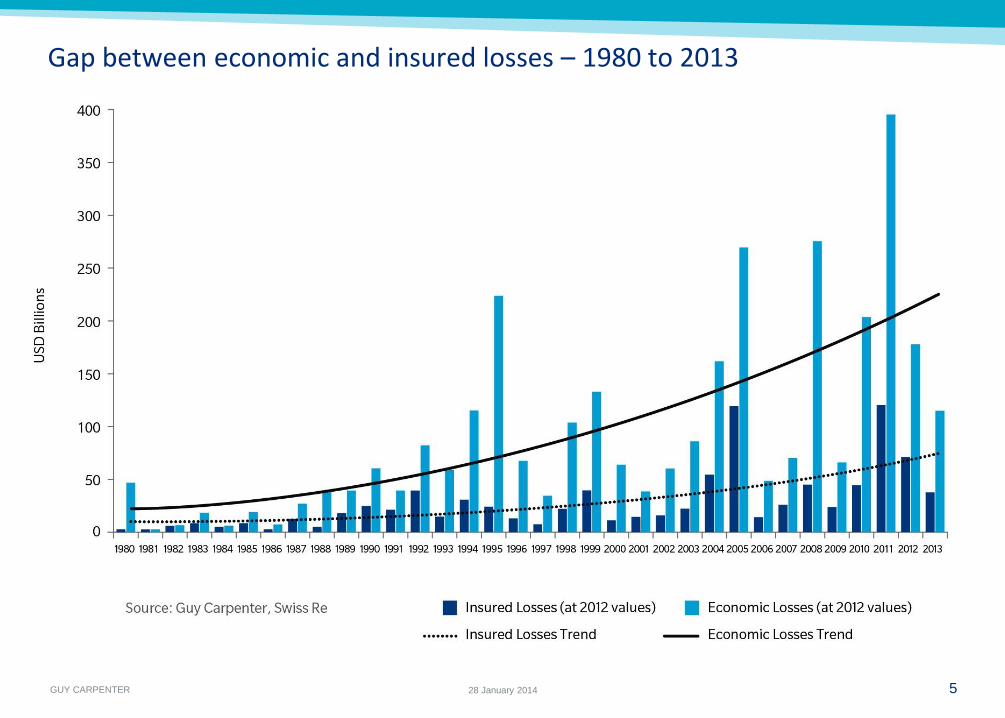

Gap between economic and insured losses – 1980 to 2013

5 28 January 2014

GUY CARPENTER

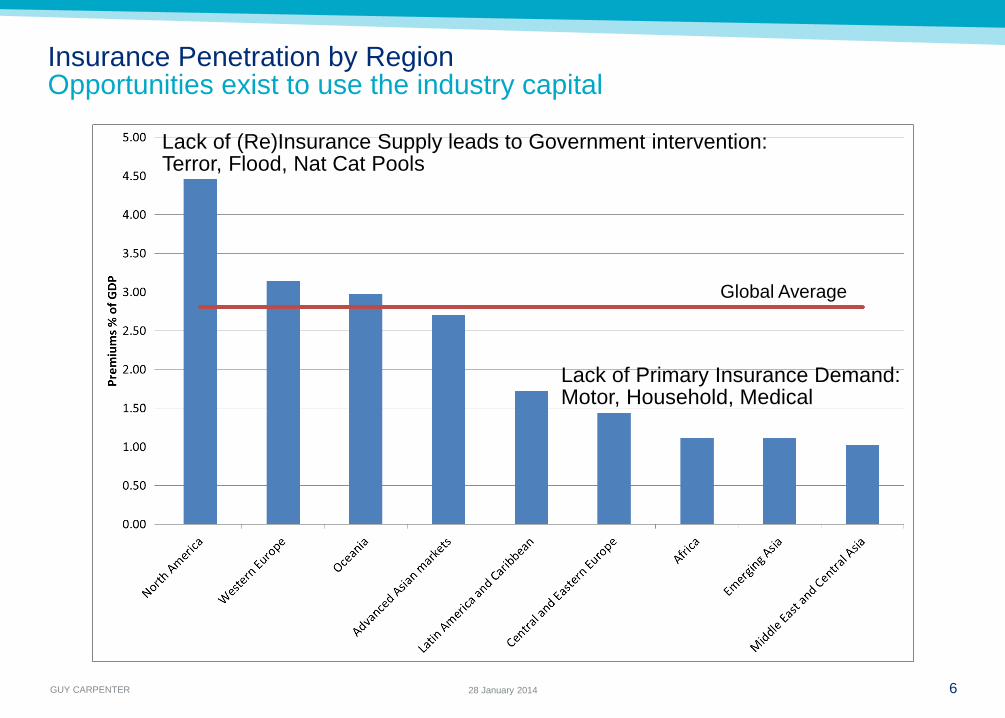

Insurance Penetration by Region Opportunities exist to use the industry capital

6 28 January 2014

Lack of (Re)Insurance Supply leads to Government intervention: Terror, Flood, Nat Cat Pools

Lack of Primary Insurance Demand: Motor, Household, Medical

Global Average

GUY CARPENTER

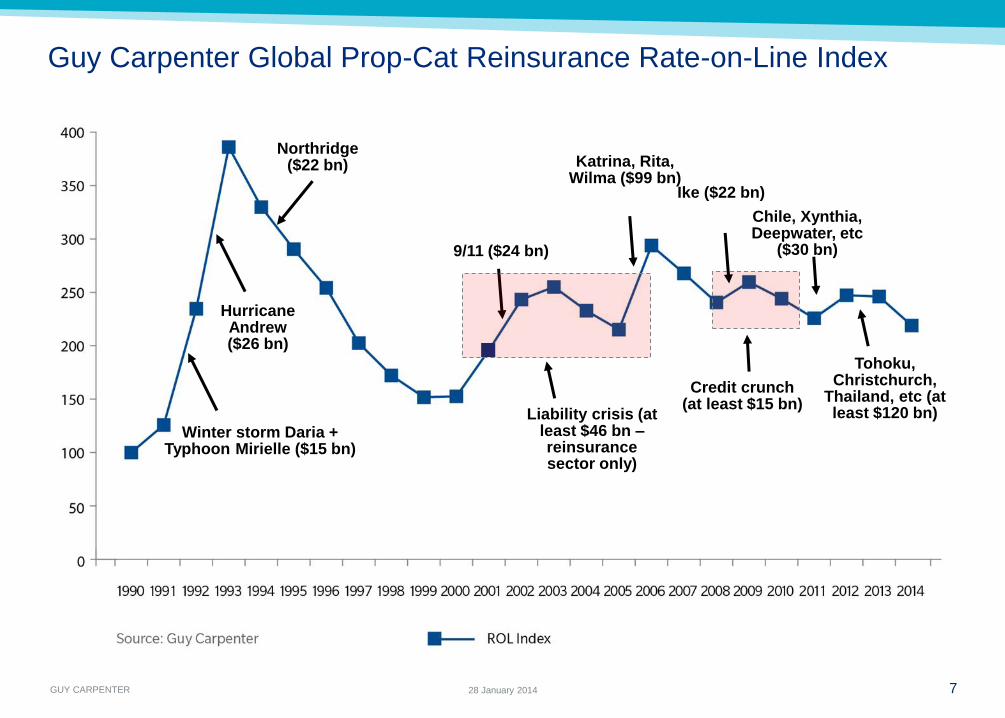

Guy Carpenter Global Prop-Cat Reinsurance Rate-on-Line Index

7 28 January 2014

Winter storm Daria + Typhoon Mirielle ($15 bn)

Hurricane Andrew ($26 bn)

Northridge ($22 bn)

9/11 ($24 bn)

Liability crisis (at least $46 bn – reinsurance sector only)

Katrina, Rita, Wilma ($99 bn)

Credit crunch (at least $15 bn)

Ike ($22 bn)

Chile, Xynthia, Deepwater, etc

($30 bn)

Tohoku, Christchurch,

Thailand, etc (at least $120 bn)

GUY CARPENTER

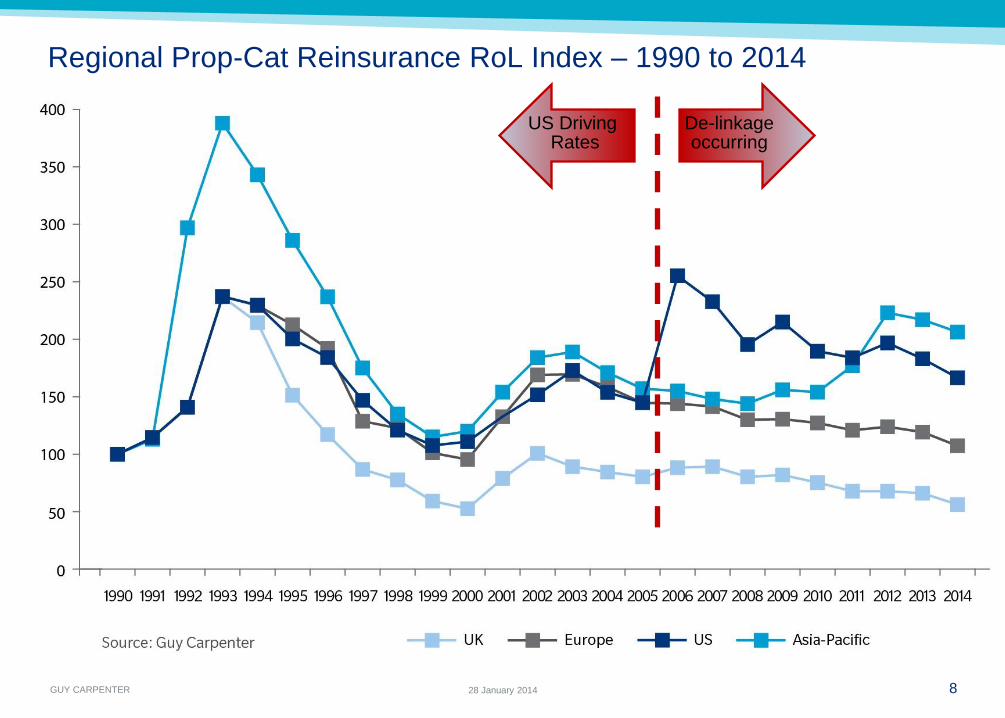

Regional Prop-Cat Reinsurance RoL Index – 1990 to 2014

8 28 January 2014

De-linkage occurring

US Driving Rates

GUY CARPENTER

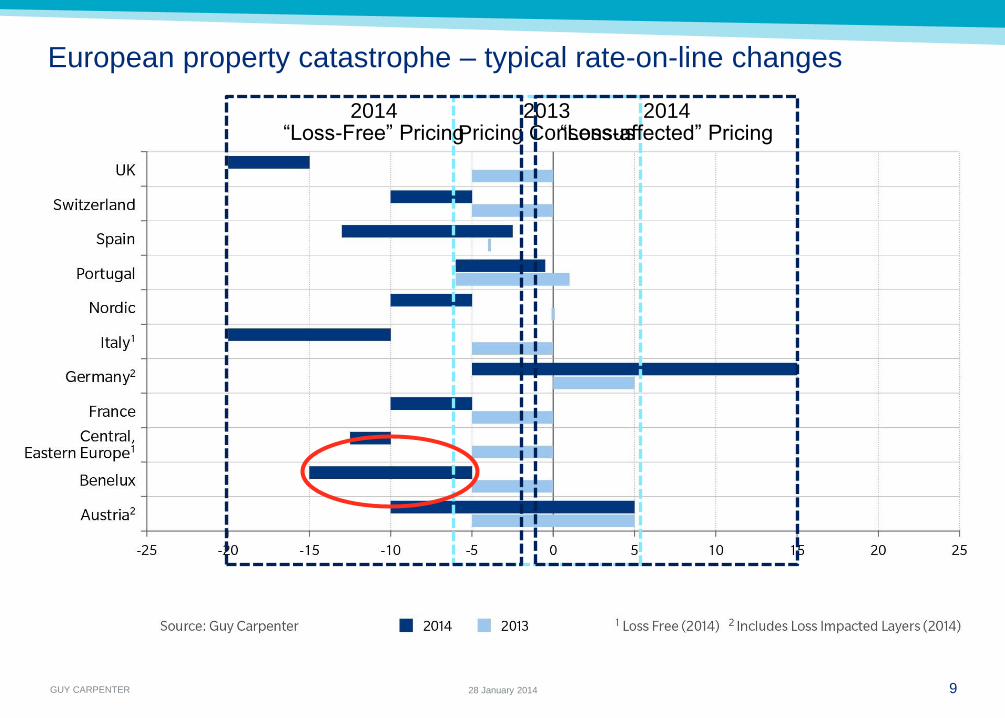

European property catastrophe – typical rate-on-line changes

9 28 January 2014

2013 Pricing Consensus

2014 “Loss-Free” Pricing

2014 “Loss-affected” Pricing

GUY CARPENTER 10 28 January 2014

Property Cat Dutch Market - Main Themes

• Benign loss activity

• Capacity more than adequate

• Limited impact of Capital and ‘alternative markets’

GUY CARPENTER 11 28 January 2014

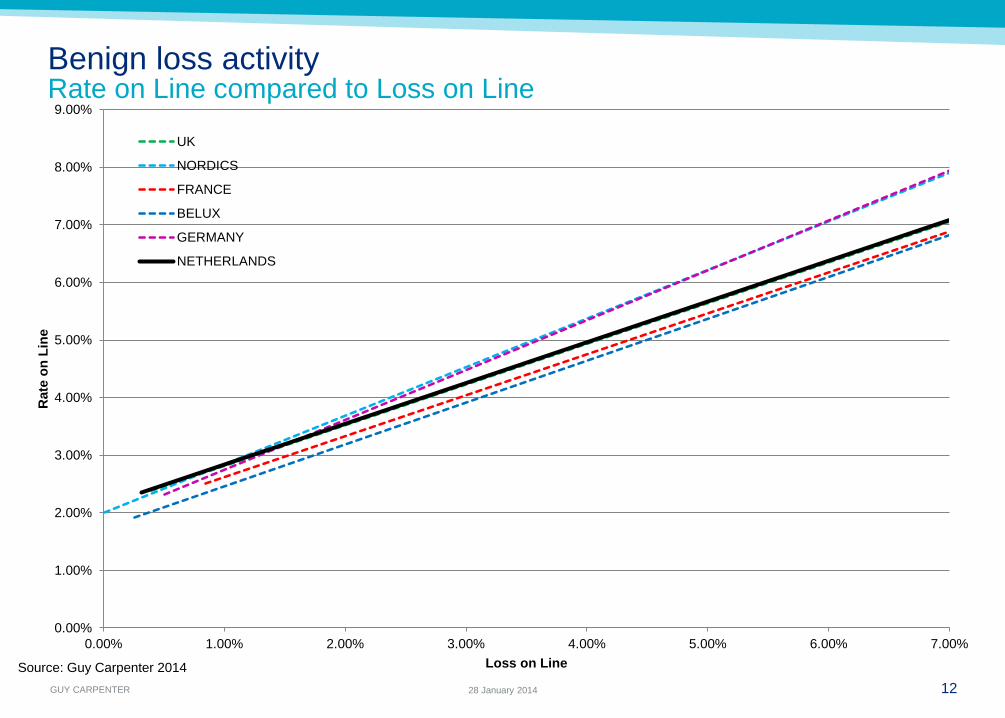

Benign loss activity Netherlands Rate on Line / Loss on Line Evolution

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00%

Rate

on

Lin

e

Loss on Line

2012

2013

2014

GUY CARPENTER 12 28 January 2014

Benign loss activity Rate on Line compared to Loss on Line

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00%

Rate

on

Lin

e

Loss on Line

UK

NORDICS

FRANCE

BELUX

GERMANY

NETHERLANDS

Source: Guy Carpenter 2014

GUY CARPENTER 13 28 January 2014

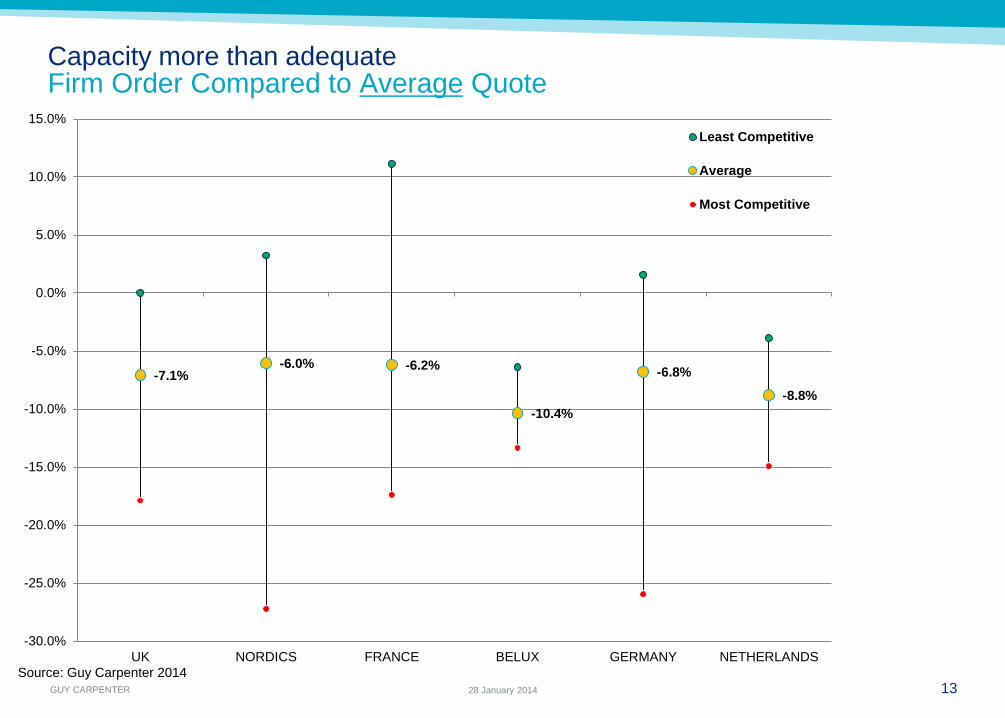

Capacity more than adequate Firm Order Compared to Average Quote

-7.1% -6.0% -6.2%

-10.4%

-6.8%

-8.8%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

UK NORDICS FRANCE BELUX GERMANY NETHERLANDS

Least Competitive

Average

Most Competitive

Source: Guy Carpenter 2014

GUY CARPENTER 14 28 January 2014

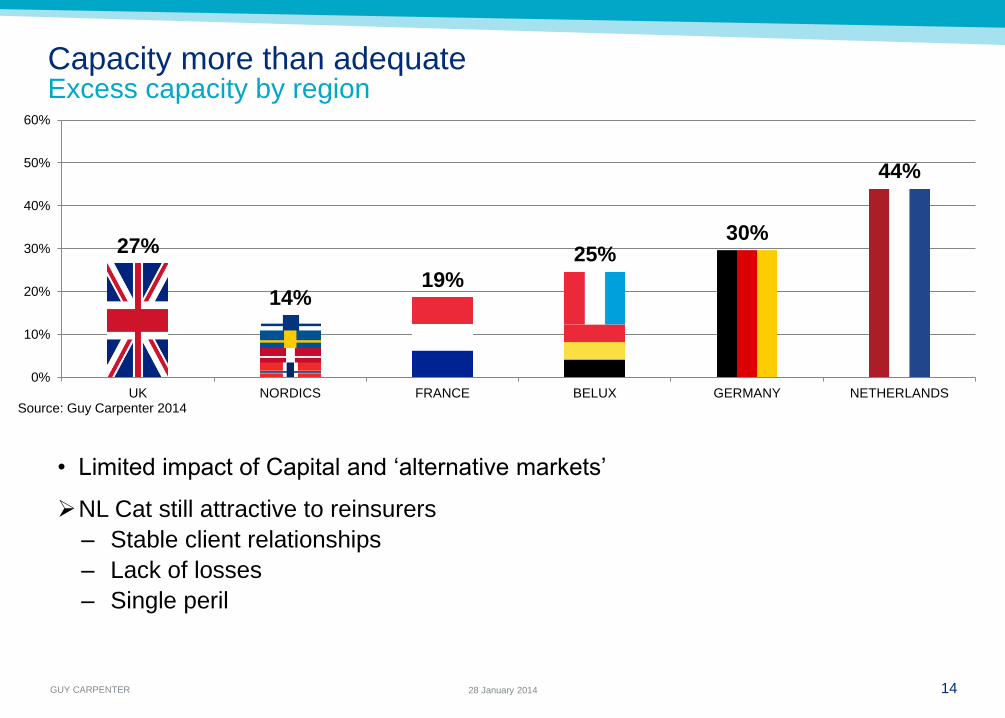

Capacity more than adequate Excess capacity by region

• Limited impact of Capital and ‘alternative markets’

NL Cat still attractive to reinsurers

– Stable client relationships

– Lack of losses

– Single peril

27%

14% 19%

25% 30%

44%

0%

10%

20%

30%

40%

50%

60%

UK NORDICS FRANCE BELUX GERMANY NETHERLANDSSource: Guy Carpenter 2014

GUY CARPENTER 15 28 January 2014

Property Risk & TPL

• Property Risk

– 2013 a relatively poor year for NL fire losses impacting reinsurers.

– Continued overcapacity in the market, Zurich market still challenging

‘traditional’ reinsurers for new business

– Softening pricing and more so on loss free programmes

• Liability

– Trend in 2014 renewal stable to slight reductions, general consistent

panel but plenty of new entrants looking to grow

– MTPL - Continuing trend of no major increases in large losses following

5th directive

– GTPL - Cancellation of Fire non-recourse agreement

GUY CARPENTER 16 28 January 2014

Marine & Energy European renewal

• Despite the MOL Comfort claim being well publicised, the loss was well

spread in Europe and had little impact on reinsurance programme pricing

for 2014

• Against the backdrop of a low level of 2013 marine claims affecting the

European marine market, renewals saw general reductions ranging

between 2.5% - 10%

• Capacity remains very buoyant for small to medium sized programmes.

Important Disclosure

Guy Carpenter & Company, LLC provides this document for general information only. The information and data contained herein is based on sources we believe reliable, but we do not guarantee its accuracy, and it should be understood to be general insurance/reinsurance information only. Guy Carpenter &

Company, LLC makes no representations or warranties, express or implied. The information is not intended to be taken as advice with respect to any individual situation and cannot be relied upon as such. Please consult your insurance/reinsurance advisors with respect to individual coverage issues.

Readers are cautioned not to place undue reliance on any calculation or forward-looking statements. Guy Carpenter & Company, LLC undertakes no obligation to update or revise publicly any data, or current or forward-looking statements, whether as a result of new information, research, future events or

otherwise. The rating agencies referenced herein reserve the right to modify company ratings at any time.

Statements concerning tax, accounting or legal matters should be understood to be general observations based solely on our experience as reinsurance brokers and risk consultants and may not be relied upon as tax, accounting, regulatory or legal advice, which we are not authorized to provide. All such

matters should be reviewed with your own qualified advisors in these areas.

This document or any portion of the information it contains may not be copied or reproduced in any form without the permission of Guy Carpenter & Company, LLC, except that clients of Guy Carpenter & Company, LLC need not obtain such permission when using this report for their internal purposes.

The trademarks and service marks contained herein are the property of their respective owners.

© 2014 Guy Carpenter & Company, LLC

All Rights Reserved

28 January 2014 17