Embed Size (px)

Citation preview

1

Macroeconomic Causesof Banking Crises

Pierre-Richard Agénor

Washington Area Finance Association Conference

Catholic University

November 10, 2000

The World Bank

2

Definition of a banking crisis. Recent evidence on banking sector problems. Macroeconomic causes of banking crises. A brief review of the evidence.

Definition of a Banking Crisis

4

Problematic. Example: (Detragiache and Demirguc-Kunt (1998)). A distress episode is a crisis when

Ratio of nonperforming loans to total bank loans exceeded 10%.

Cost of the rescue operation was at least 2% of GDP. Episode involved a large-scale nationalization of

banks. Extensive bank runs took place or emergency

measures (deposit freeze, prolonged bank holidays, or generalized deposit guarantees) were enacted by the government.

5

Information on nonperforming loans: often not reliable and timely. Evergreening problem.

Cost of rescue operations is often difficult to measure. Importance of quasi-fiscal costs and contingent liabilities, and restructuring costs. Liquidity provided at below-market interest rates. Promise to bail out ailing banks provides an implicit

subsidy.

Problems

6

Estimating the net costs of banking sector restructuring is difficult; requires assumptions about amount of liquidity support; present and future incidence of nonperforming loans

and their recovery rate. Estimates are often calculated on a gross basis; lead to

overestimation by excluding future proceeds from reprivatization; loan recovery; repayment of the liquidity assistance provided by the

government.

7

“Run” or “event” criterion: A crisis can indeed, in some cases, be dated that way. Examples: Massive bank runs in Ecuador, following the

currency crisis of February 1999. The crisis in Indonesia, dated in reference to the

closure of 16 banks in late 1997.

Problems Runs are often short lived. Dramatic “events” rarely represent either the beginning,

or the end, of the crisis. In most cases insolvency problems were already present

and worsened over a period of time; event itself is merely the point at which underlying problems are revealed (either to the regulator or the public).

Banking Sector Problems:Recent Evidence

9

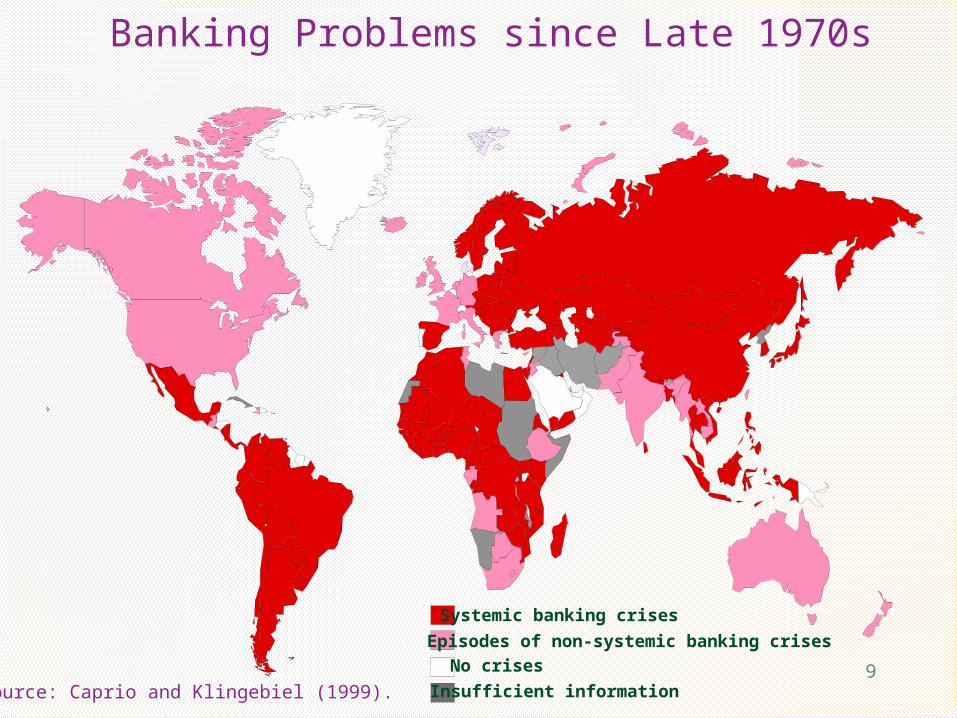

Banking Problems since Late 1970s

Systemic banking crises

No crises

Episodes of non-systemic banking crises

Insufficient informationSource: Caprio and Klingebiel (1999).

Banking Sector Problems:Why we Should Care

11

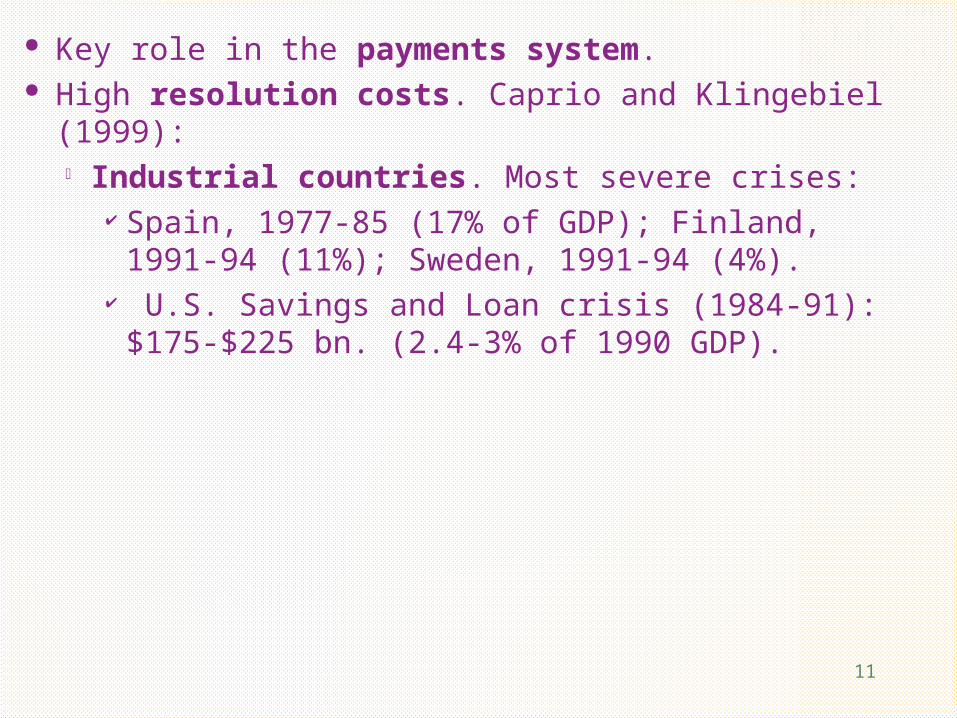

Key role in the payments system. High resolution costs. Caprio and Klingebiel (1999):

Industrial countries. Most severe crises: Spain, 1977-85 (17% of GDP); Finland, 1991-94

(11%); Sweden, 1991-94 (4%). U.S. Savings and Loan crisis (1984-91): $175-

$225 bn. (2.4-3% of 1990 GDP).

12

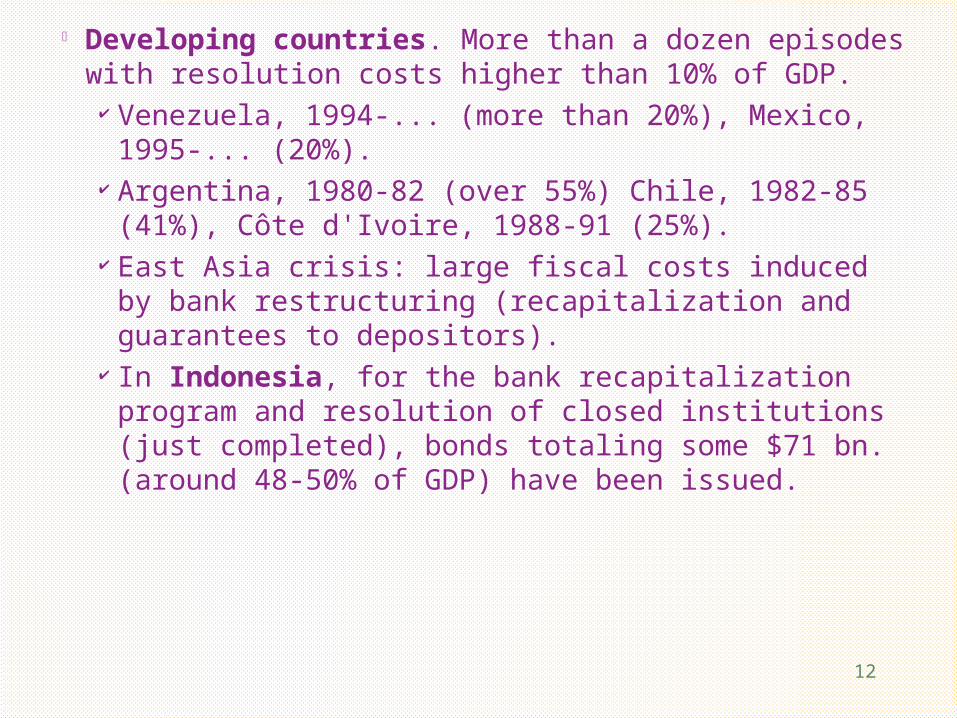

Developing countries. More than a dozen episodes with resolution costs higher than 10% of GDP.

Venezuela, 1994-... (more than 20%), Mexico, 1995-... (20%).

Argentina, 1980-82 (over 55%) Chile, 1982-85 (41%), Côte d'Ivoire, 1988-91 (25%).

East Asia crisis: large fiscal costs induced by bank restructuring (recapitalization and guarantees to depositors).

In Indonesia, for the bank recapitalization program and resolution of closed institutions (just completed), bonds totaling some $71 bn. (around 48-50% of GDP) have been issued.

13

In Thailand, total cost of bank restructuring (in terms of public debt issued) is estimated at 32% of GDP; for Korea, 15-16%.

Pressure on fiscal deficits, public debt, and domestic interest rates (default risk premium).

Adverse incentive effects. Intervention may reduce private incentives to monitor

the behavior of banks in the future. Expectation of future rescues creates incentives for

excessive risk taking.

14

Reduction in bank credit and higher interest rates: adverse supply-side effects (small firms).

During a financial crisis: Worsening of information and adverse selection

problems. Reason: only the least creditworthy borrowers are

prepared to pay higher interest rates. Adverse effect on the quality of loan portfolios.

15

Constrains the conduct of monetary policy. Limits on the possibility to raise interest rates. Problematic when such response is needed to fend

off speculative pressures. Contraction in output that accompanies (or is

exacerbated by) financial crises: has an asymmetric effect on poverty rates.

Causes of Banking Crises

17

Causes of Banking Crises

Mismatches between assets and liabilities. Government intervention. Weaknesses in the regulatory and legal framework. Government guarantees and incentive failures. Premature financial liberalization.

Microeconomic Distortions and Institutional Failures

Macroeconomic Factors Domestic and exogenous shocks. Lending booms. The exchange rate regime.

Self-Fulfilling Panics and Information-Based Runs

Macroeconomic Factors

19

Domestic and External Shocks

Domestic Shocks

Example: increase in domestic interest rates (to reduce inflation or defend the currency). Slows output growth and may weaken the ability of

borrowers to service their loans; may lead to an increase in nonperforming assets or a

full-blown crisis. Country example: Jamaica (1994-99).

20

Example: a change in terms of trade. May affect even well-run banks. An unanticipated drop in export prices, for instance, can

impair the capacity of domestic firms (those in the tradable sector) to service their debts.

This can result in a deterioration in the quality of banks' loan portfolios.

Adverse shock to domestic income associated with a decline in the terms of trade: may slow output and raise default rates.

Country examples: Côte d'Ivoire (1986-90), Ecuador (1998-99).

External Shocks

21

Example: capital outflows induced by an increase in world interest rates or loss of confidence. If these flows are intermediated, to begin with, via the

banking system: drop in deposits; may force banks to liquidate long-term assets to

raise liquidity or cut lending abruptly. May entail a recession and a rise in default rates.

Country examples: too many to count!

22

Clearly, the impact of these shocks on the banking system depends on their duration.

But volatility matters also. With highly volatile shocks, it is more difficult for banks to assess project quality and credit risk (distorted price signals).

23

Lending Booms Rapid increases in bank credit growth to the economy. Source of increase in banks' capacity to lend: often

large capital inflows. Often at the expense of credit quality. Distinguishing between good and bad credit risks is

harder when the economy is expanding rapidly because many borrowers are temporarily profitable and liquid.

Boom is often accompanied by asset price bubbles (stock market, real estate).

24

Banking crisis may occur when the bubble bursts. Collapse in equity prices:

affects overall confidence. reduces profitability of bank debtors.

Collapse in real estate prices: may also affect confidence. reduces the value of collateral.

Crisis often exacerbated by a high degree of loan concentration (to groups and sectors).

Examples: East Asia, Latin America.

25

Pegged exchange rate regime: two issues. A credibly-fixed exchange rate provides an implicit

guarantee (no foreign exchange risk) which may lead to excessive (and unhedged) short-term foreign borrowing. Example: East Asia.

This increases the fragility of the banking system to adverse external shocks, particularly if the degree of capital mobility is high.

Example: adverse shift in market sentiment that leads to capital outflows.

The Exchange Rate Regime

26

Lowers (without full sterilization) the money supply and leads to higher interest rates.

Higher cost of credit: increases the incidence of default and leads to a deterioration in the quality of bank portfolios.

Thus: under any pegged rate regime, capital outflows affect the financial system through an expansion or contraction of bank balance sheets; they can lead to instability in the banking sector.

Additional problem with a rigid regime (e.g. currency board): it also constrains the lender-of-last-resort function of the central bank; prevents it from reacting quickly to stop a bank run by injecting liquidity.

27

Example: Argentina, 1995 (Tequila crisis). Bank deposits fell by 16% (more than $7.5 billion)

between mid-Dec 1994 and end-March 1995. Foreign currency withdrawals translated into

contractions of the monetary base and, via the money multiplier, into declines in domestic credit and a sharp rise in domestic interest rates.

Foreign exchange reserves fell by 40% between end-Dec 1994 and end-March 1995 and prime interest rates tripled over the same period, reaching 50% in March 1995.

Central bank did intervene subsequently.

28

Flexible exchange rate regime: may also create problems. An abrupt outflow of capital can lead to a sharp

depreciation of the nominal exchange rate. The depreciation may raise the domestic-currency value

of foreign-currency liabilities, for banks and their customers.

Large, unhedged foreign-currency positions increase risk of default on existing loans and vulnerability to adverse (domestic or external) shocks.

The fall in borrowers’ net worth may also lead to a rise in the finance premium and to increased default rates;

higher incidence of nonperforming loans may lead to a banking crisis.

The Evidence

30

Take it with a grain of salt! Serious measurement problems; but also endogeneity and

misspecification problems. Nevertheless: suggests that external shocks (movements

in world interest rates and induced capital flows) and lending booms are important determinants of financial crises in developing countries.

But further research is needed to understand interactions between (domestic) micro and macro factors.

Macroeconomic shocks are often the triggering factors that reveal underlying microeconomic weaknesses.