Embed Size (px)

Citation preview

1

MAN 702

MANAGERIAL FINANCE

2

COURSE OUTLINE:

SCOPE AND NATURE OF FINANCE

AN OVERVIEW OF THE NIGERIAN FINANCIAL SYSTEM

FINANCIAL ANALYSIS, PLANNING AND CONTROL

WORKING CAPITAL MANAGEMENT

CAPITAL BUDGETING

COST OF CAPITAL

FINANCIAL STRUCTURE AND DIVIDEND DECISION

MERGERS AND ACQUISITIONS

INTERNATIONAL FINANCIAL MANAGEMENT

3

SCOPE AND NATURE OF FINANCE

Meaning of Financial Management

The Finance Function

Finance in the organisation structure of the firm

Goals of the firm

(a) Meaning of Financial Management

Financial management is simply explained as the management of the finance of a

business. That is, applying management functions such as planning and control in order

to achieve the financial objectives of the business.

It is that managerial activity which is concerned with the planning and controlling of the

firm’s financial resources.

As a separate discipline, it is a recent development because up till 1890, it was a branch

of economics. Until today, it has no unique body of knowledge of its own, and it draws

heavily on economics for its theoretical concepts.

(b) The Finance Function

Viewing an organisation from functional perspective presents an organisation comprising

of various functional areas among which are finance, production and marketing. The

company (firm) secures capital it needs and employs it (finance activity) in activities

which generate returns on invested capital (production and marketing activities). A

business organisation therefore engages in activities to perform functions such as those

discussed above; Finance, production and marketing. The most important of these is the

finance function. The finance function is so important that all organisations perform

them. There is ranging from business firms to government units or agencies and other

non-profit organisations. Finance function has to do with the financial management,

which is defined, by the functions and areas of responsibilities of financial managers.

4

The functions of financial managers are broadly appreciated under the following

activities

(i) Planning and Forecasting

The financial manager has to set financial objectives and work toward achieving such

predetermined target. Thus, setting a realistic target requires making educative guesses

about the future based on the past and present information. Areas of concern here include

planning for working capital components, capital budgeting etc.

(ii) Investment and Financing Decision

The financial manager has the primary responsibility for: (a) acquiring funds, which are

obtained from a wide range of financial institutions; (b) Determining a sound rate of

growth and ranking alternative investment opportunities to ensure that the firm achieves a

high rate of growth in sales (c) Deciding the specific investment to be made and

alternative sources of funds for financing these investments; (d) Deciding about the use

of internal vs. external funds, of debt vs. owner’s funds, and of long term vs. short-term

financing; and (e) Should be concerned with the management of cash inflows (in form

of retained earnings) and cash outflows (in form of dividends) since some cash is

recycled and some returned to financing sources.

(iii) Interaction with Other Managers in the firm. Since all business decisions have

financial implications.

(iv). Using money and capital markets.

According to Weston and Copeland (1989:33) financial managers have two important

areas of responsibility:

To obtain external funds through the financial markets.

What financing forms and sources are available?

How can the funds be acquired efficiently?

What is the most economical mix of financing?

What will be the timing and form of returns and repayments to financing

sources?

5

To see that the funds obtained are used effectively.

To what projects and products should funds be allocated?

What assets and resources must be acquired in order to produce the product or

service?

How should the use of funds be monitored so that they are most effectively

distributed among the various operating activities?

It is the financial manager’s responsibility to implement these choices in the various

financial markets to meet the firm’s capital requirements

(c) Finance in the Organisation Structure of the Firm

The place of the Chief Financial Officer (CFO) is high in the organisational hierarchy of

the firm because of the central role of finance in the various levels of decision-making.

The organisational structure below shows the position of the CFO.

CHAIRMAN OF THE BOARD

MANAGING DIRECTOR

BOARD

RESEARCH DIRECTOR

PRODUCTION DIRECTOR

MARKETING DIRECTOR

FINANCIAL DIRECTOR

(CFO)

CONTROLLER TREASURER

6

Chief Financial Officer (C F O)

Is responsible for formulation of major financial policies in the firm.

Interact with other senior officers to present the financial implications of

major decisions in other areas.

Defines the duties of other financial officers who report to him.

Is accountable for the analytical aspects of the treasurer and controller’s

activities.

The Treasurer: handles the acquisition and custody of funds. In addition he also

handles

Forecasting and financial needs.

Banking and custody

Credits and collections

Investments

Insurance

Controller: his areas of responsibility include:

Accounting

Reporting

Control/Government’s reporting and

Protection of Assets

(d) Goals of the Firm

The firm’s investment and financing decisions are unavoidable and continuous. In order

to make them rationally, the firm must have a goal. It is generally agreed however, that

the financial goal of the firm should be the maximisation of owner’s economic welfare.

The three major goals of the firm discussed in literature are: profit maximization;

shareholders’ wealth maximization; and social responsibility.

(i) Profit Maximisation:-This goal is to increase the firm’s Naira earnings to as large an

amount as possible, usually in as short a time as possible.

7

- This goal has the advantage of focusing the firm’s effort on profits, which are

absolute necessity for the company’s continued independent existence.

- However, the firm can suffer if the profit maximisation goal is taken to extremes.

This is because of the following reasons:

(a) Pursuit of profits alone can lead to poor risk judgment.

(b) An emphasis on short-term profits can cause the neglect of long-term

possibilities.

(c) The firm’s managers, especially in a corporation, may be willing to

undertake the risks essential to profit maximisation.

(d) Capital and other resources may be insufficient to take advantage of

immediate opportunities.

(ii) Shareholders’ wealth maximisation

- This goal stresses the maximisation of the market value of the firm (Maximising

the price of the firm’s ordinary shares) and hence the wealth of its shareholders.

- In finance, this goal is seen as the critically logical and operationally feasible

normative goal for guiding the financial decision-making.

- This corporate goal should reflect all favourable as well as unfavourable factors

affecting the firm.

- The wealth of the shareholders is increased when the share price goes up. The

share price reflects:

Management’s performance is achieving earnings.

Their ability to judge risks and

Factors outside the firm’s control to which investors respond e.g. interest rate.

The wealth maximisation goal is consistent with the objective of maximising

owner’s economic welfare. The latter is equivalent to maximising the utility of

their consumption over-time. With their wealth maximised, owners can adjust

their cash flows in such a way as to optimise their consumption.

- Value maximisation is therefore broader than profit maximisation for several

reasons:-

8

(i) Maximisation of value takes the time value of money into consideration.

Funds received this year have more value than funds that may be received ten

years later.

(ii) Value maximisation considers the risk-ness of the income streams, e.g. the

rate of return required on risk-free government securities would be lower than

the rate of return required on an investment in starting a new business.

(iii) Social Responsibility

This is a new concept which is now in vogue. -It stresses that business should not strictly

operate in shareholders’ best interest but should partly be responsible for the welfare of

society. There is no one, and especially large firm, that can afford to ignore obligations

for responsible citizenship.

9

AN OVERVIEW OF NIGERIAN FINANCIAL SYSTEM

Definition:

A financial system comprises the entire conglomerate of institutions and institutional

arrangements established to serve the needs of modern economies.

(a) It ensures the provision of financial resources to meet the borrowing needs of

individuals, business enterprises and government.

(b) It provides facilities to collect and to invest savings and a sound payment

mechanism.

History

- Before independence, indigenous financial system was almost non-existing. Only

the traditional financial institutions and some few modern but colonial financial

institutions existed whose main objective was to mobilise local savings and

channel them for the sustenance of the metropolitan country’s economy.

- Roots of modern and indigenous financial system – political independence in the

West African countries. First major step was the establishment of CBN in March

1958 under CBN Ordinance 1958. Later series of banks, (commercial and

merchants), non-banks financial institutions and financial markets were

established.

Classification:

One way of identifying or classifying the Nigerian Financial system is by generic names

of the institutions. Thus, we have four major classifications:

1. The Apex Institutions:

(a) CBN - This is at the apex of the banking system.

(b) NSEC - This is the apex of the financial particularly capital markets.

(c) NDIC – This is concerned with insuring all the commercial and merchant

banks i.e. all deposit financed financial institutions.

2. The Banking Institutions

(a) National Development Banks

(b) The Commercial Banks

(c) The Merchant Banks

10

3. The Non-Bank Financial Institutions

(a) Various State Development Financial Institutions

(b) Insurance Companies

(c) Pension Funds

(d) Provident Funds

4. Financial Markets

Money

Capital Markets

11

FINANCIAL ANALYSIS, PLANNING, AND CONTROL FINANCIAL ANALYSIS

- Financial analysis is defined as the process of identifying the financial strengths

and weaknesses of the organisation by properly establishing the relationships

between the various items in the organisations financial statements.

- Financial statements are the results of the process of recording, classifying and

summarising a firm’s transactions.

- Of special interest to financial managers and financial analyst are the Balance

Sheet and the Income Statement that provide a measure of the firm’s financial

condition.

Steps in Financial Statement Analysis:

(i) Select the information relevant to the decision under consideration from the

total information contained in the financial statements

(ii) Arrange the information in a way as to highlight significant relationship.

(iii) The acquired information is to be interpreted, inference and conclusions

drawn.

Users of Financial Statement:

(i) Creditors i.e. short-term and long -term.

(ii) Shareholders and potential investors

(iii) Labour Unions – i.e. justifying wage increase and other welfare services.

(iv) Competitors

(v) Management analysts

Financial Ratio Analysis

- It is a widely used tool of financial analysis

- It is used as an index or yardstick for evaluating the financial position and

performance in finance.

12

Basic Types of Financial Ratios

(a) Liquidity Ratios: Measure the short-term solvency of the firm.

(b) Gearing /Capital Structure/Leverage/Debt Ratios: They measure the extent to

which the firm’s assets are financed by debt and firm’s ability to meet long-term

commitments.

(c) Activity Ratios: They measure the overall effectiveness of financial utilisation i.e.

ability of a firm to manage and utilize its asset.

(d) Profitability Ratios: These provide a measure of profitability to firm.

(e) Growth Ratios: These ratios measure how well the firm is maintaining its

economic position in the economy as a whole as well as its own industry.

(f) Valuation Ratios: These are the most comprehensive measures of performance for

the firm in that they reflect the combined influence of risk ratios and return ratios.

General Uses/Advantages

(i) They explain the ability of the firm to meet the financial obligation when they

fall due.

(ii) They aid decision making by summarising, simplifying and classifying

accounting records.

(iii) Yardstick for measuring performance

(iv) Used for the purpose of comparison

Limitations:

Although they are important and useful, they must be used with caution because:

(a) There is a high chance of window- dressing technique in which published data are

presented to outside users.

(b) Differences in accounting systems e.g. depreciation methods.

(c) Impact of inflation

(d) Conceptual Differences e.g. what constitutes shareholders’ equity or using the

value of sales or cost of goods sold in the computation of the turnover ratios.

FINANCIAL RATIOS AS PREDICTIONS OF CORPORATE FAILURE

- The ratios are tools of analysing financial record i.e. its strengths and weaknesses,

depending on who the user is.

13

- One serious shortcoming of ratio analysis arises from the fact that the

methodology is univariate i.e. each ratio is examined in isolation.

- To overcome this univariate position, it is necessary to put together different

ratios into a meaningful predictive model.

- So many people attempted a predictive model and their contributions are

discussed below:

William Beaver:

- Made first attempt in 1966 to develop a univariate model

- Wrote on “Financial ratios and predictors of Failure”

- He was interested in finding out which ratios are most important in predicting a

firm’s inability to pay its debts.

- He compared the ratios of 79 firms and another 79 firms. The former failed and

the latter solvent.

- He found that there are five (5) key ratios that could discriminate between a firm

that failed and the firm that survived. These ratios are:

(1) The Cash flow to Total Debt

(2) Net Income to Total Asset

(3) Total Debt to Total Asset

(4) Working capital to Total Asset

(5) Current- Ratio.

- He found that all firms that failed had more debt, lower return on assets, less cash

balances, more receivable and low current ratios.

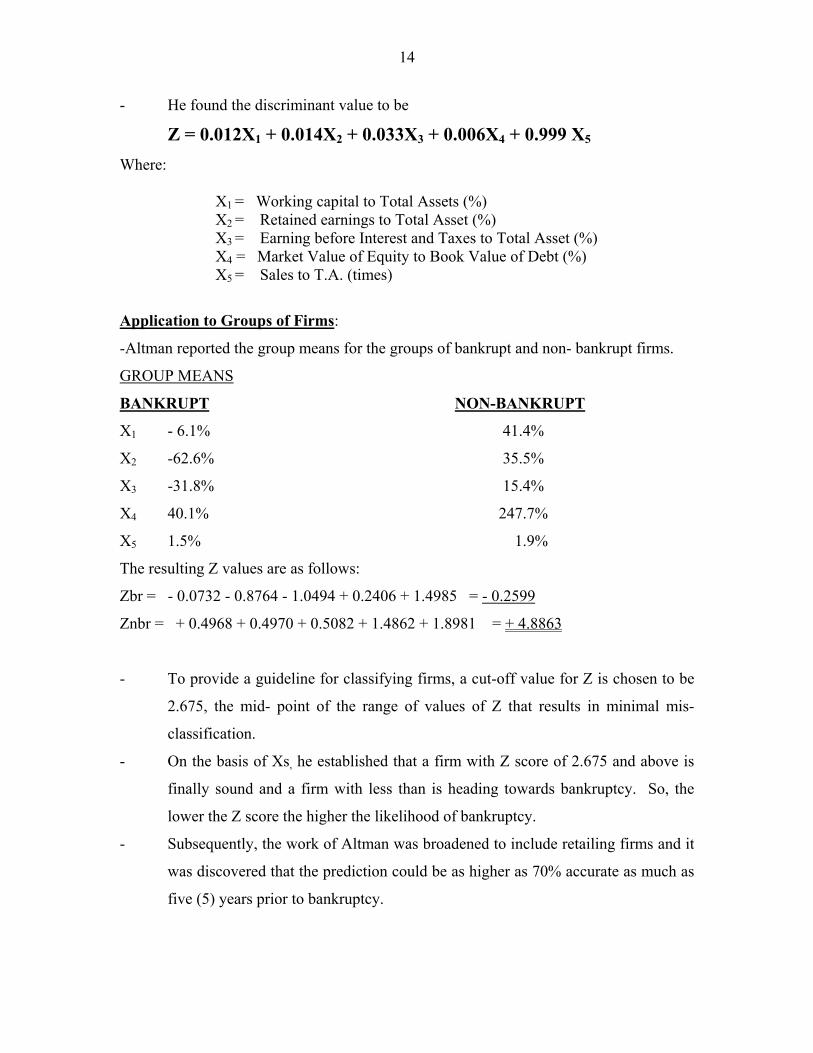

Altman Edward:

- He uses the Discriminant Analysis to develop a multivariate model.

- He developed a model of predicting bankruptcy of firms in U.S. (Financial Ratio

Discriminant analysis and prediction of corporate bankruptcy)

- He used a sample of 66 manufacturing firms. Half of which went bankruptcy.

- From their financial statements one period before the bankrupt, he discovered 22

financial ratios out of which five were found to contribute immensely to the

prediction model.

14

- He found the discriminant value to be

Z = 0.012X1 + 0.014X2 + 0.033X3 + 0.006X4 + 0.999 X5

Where:

X1 = Working capital to Total Assets (%) X2 = Retained earnings to Total Asset (%) X3 = Earning before Interest and Taxes to Total Asset (%) X4 = Market Value of Equity to Book Value of Debt (%) X5 = Sales to T.A. (times)

Application to Groups of Firms:

-Altman reported the group means for the groups of bankrupt and non- bankrupt firms.

GROUP MEANS

BANKRUPT NON-BANKRUPT

X1 - 6.1% 41.4%

X2 -62.6% 35.5%

X3 -31.8% 15.4%

X4 40.1% 247.7%

X5 1.5% 1.9%

The resulting Z values are as follows:

Zbr = - 0.0732 - 0.8764 - 1.0494 + 0.2406 + 1.4985 = - 0.2599

Znbr = + 0.4968 + 0.4970 + 0.5082 + 1.4862 + 1.8981 = + 4.8863

- To provide a guideline for classifying firms, a cut-off value for Z is chosen to be

2.675, the mid- point of the range of values of Z that results in minimal mis-

classification.

- On the basis of Xs, he established that a firm with Z score of 2.675 and above is

finally sound and a firm with less than is heading towards bankruptcy. So, the

lower the Z score the higher the likelihood of bankruptcy.

- Subsequently, the work of Altman was broadened to include retailing firms and it

was discovered that the prediction could be as higher as 70% accurate as much as

five (5) years prior to bankruptcy.

15

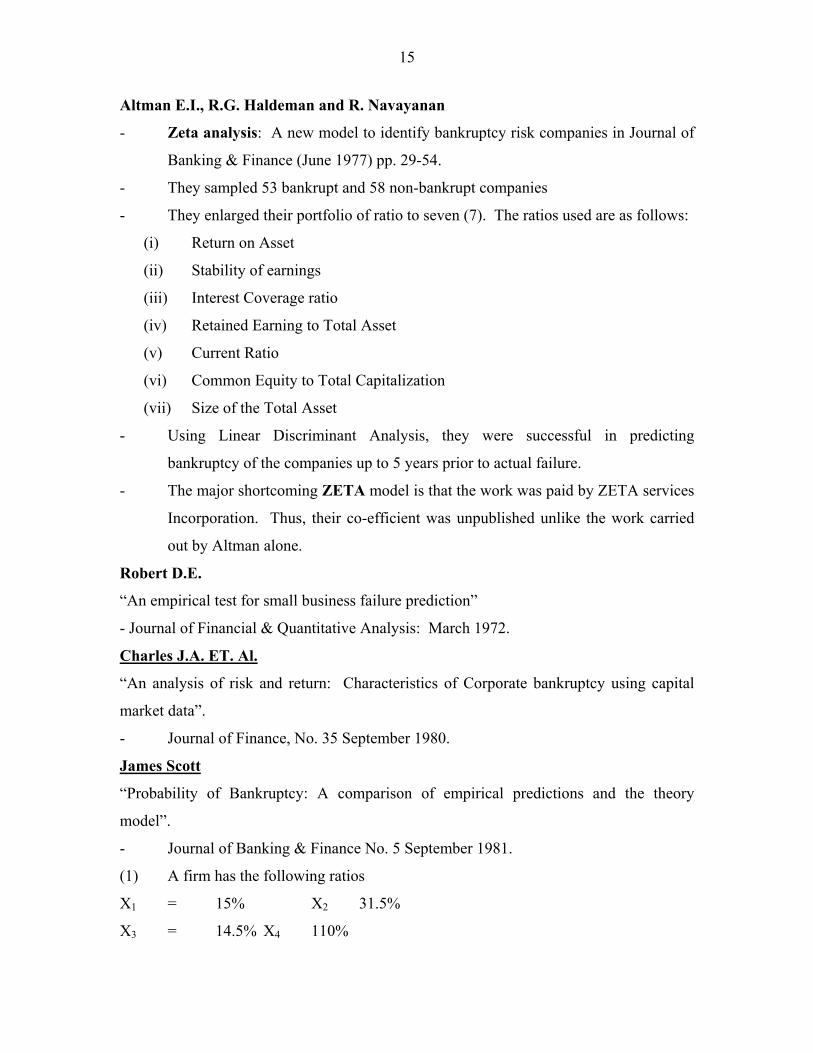

Altman E.I., R.G. Haldeman and R. Navayanan

- Zeta analysis: A new model to identify bankruptcy risk companies in Journal of

Banking & Finance (June 1977) pp. 29-54.

- They sampled 53 bankrupt and 58 non-bankrupt companies

- They enlarged their portfolio of ratio to seven (7). The ratios used are as follows:

(i) Return on Asset

(ii) Stability of earnings

(iii) Interest Coverage ratio

(iv) Retained Earning to Total Asset

(v) Current Ratio

(vi) Common Equity to Total Capitalization

(vii) Size of the Total Asset

- Using Linear Discriminant Analysis, they were successful in predicting

bankruptcy of the companies up to 5 years prior to actual failure.

- The major shortcoming ZETA model is that the work was paid by ZETA services

Incorporation. Thus, their co-efficient was unpublished unlike the work carried

out by Altman alone.

Robert D.E.

“An empirical test for small business failure prediction”

- Journal of Financial & Quantitative Analysis: March 1972.

Charles J.A. ET. Al.

“An analysis of risk and return: Characteristics of Corporate bankruptcy using capital

market data”.

- Journal of Finance, No. 35 September 1980.

James Scott

“Probability of Bankruptcy: A comparison of empirical predictions and the theory

model”.

- Journal of Banking & Finance No. 5 September 1981.

(1) A firm has the following ratios

X1 = 15% X2 31.5%

X3 = 14.5% X4 110%

16

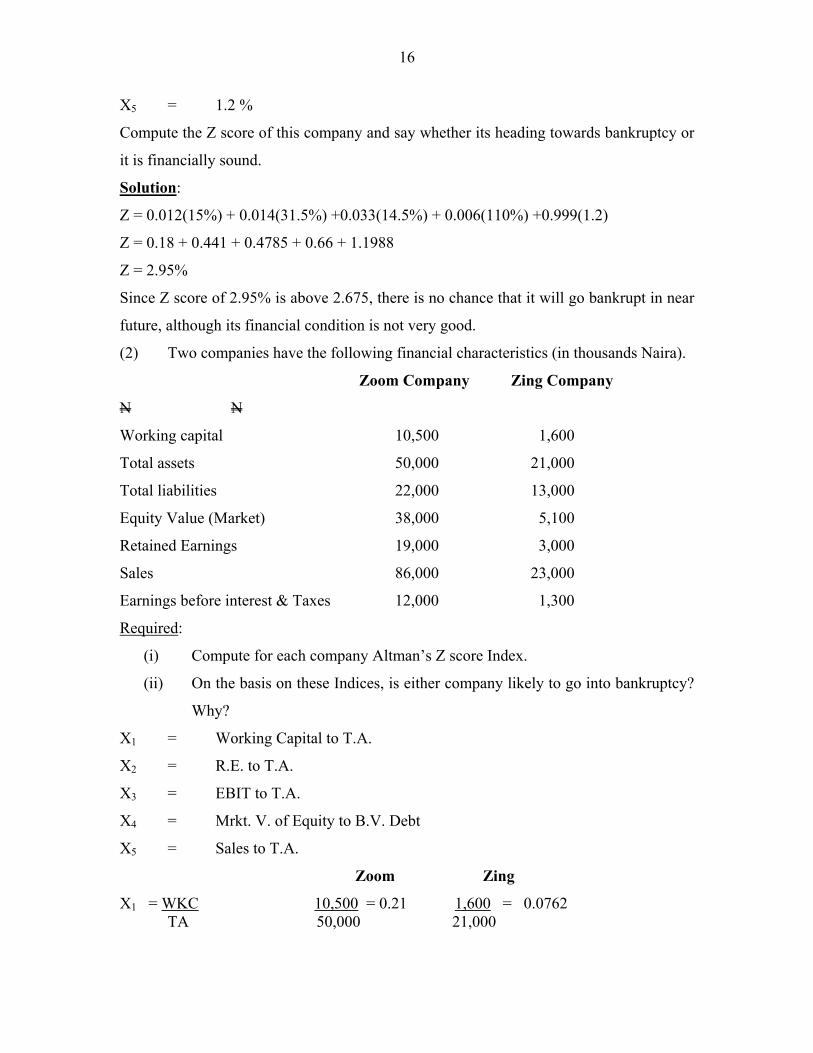

X5 = 1.2 %

Compute the Z score of this company and say whether its heading towards bankruptcy or

it is financially sound.

Solution:

Z = 0.012(15%) + 0.014(31.5%) +0.033(14.5%) + 0.006(110%) +0.999(1.2)

Z = 0.18 + 0.441 + 0.4785 + 0.66 + 1.1988

Z = 2.95%

Since Z score of 2.95% is above 2.675, there is no chance that it will go bankrupt in near

future, although its financial condition is not very good.

(2) Two companies have the following financial characteristics (in thousands Naira).

Zoom Company Zing Company

N N

Working capital 10,500 1,600

Total assets 50,000 21,000

Total liabilities 22,000 13,000

Equity Value (Market) 38,000 5,100

Retained Earnings 19,000 3,000

Sales 86,000 23,000

Earnings before interest & Taxes 12,000 1,300

Required:

(i) Compute for each company Altman’s Z score Index.

(ii) On the basis on these Indices, is either company likely to go into bankruptcy?

Why?

X1 = Working Capital to T.A.

X2 = R.E. to T.A.

X3 = EBIT to T.A.

X4 = Mrkt. V. of Equity to B.V. Debt

X5 = Sales to T.A.

Zoom Zing

X1 = WKC 10,500 = 0.21 1,600 = 0.0762 TA 50,000 21,000

17

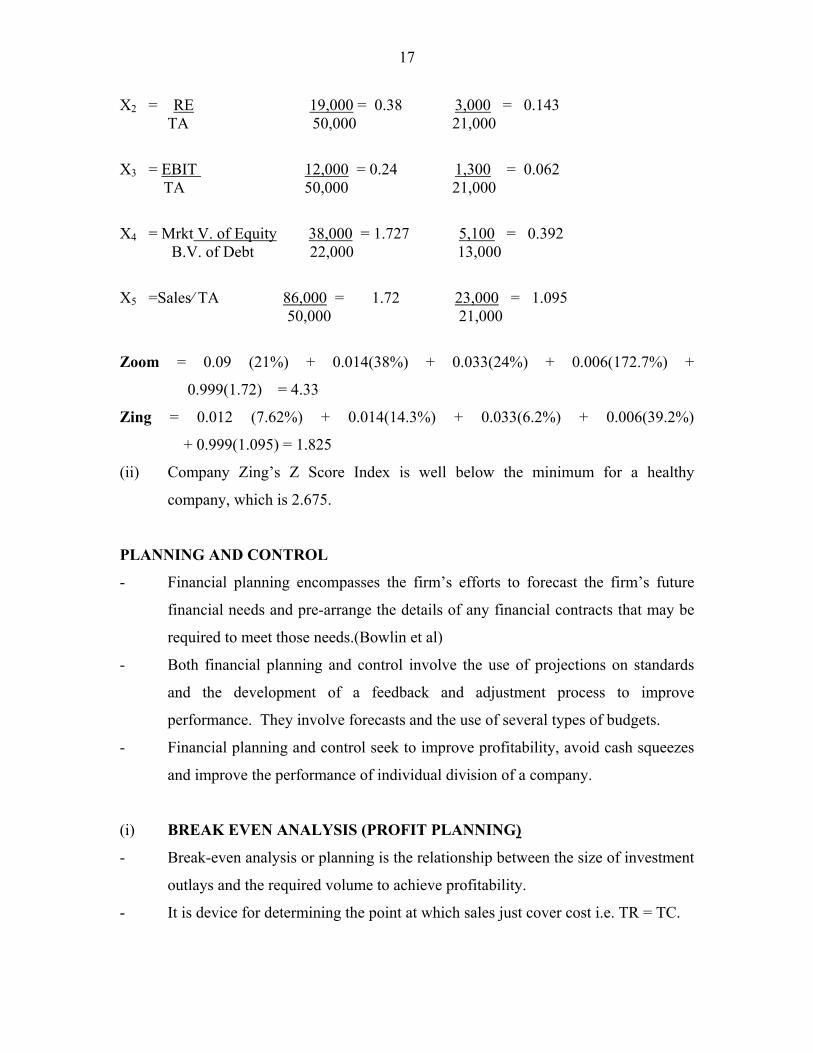

X2 = RE 19,000 = 0.38 3,000 = 0.143 TA 50,000 21,000

X3 = EBIT 12,000 = 0.24 1,300 = 0.062 TA 50,000 21,000

X4 = Mrkt V. of Equity 38,000 = 1.727 5,100 = 0.392 B.V. of Debt 22,000 13,000

X5 =Sales⁄ TA 86,000 = 1.72 23,000 = 1.095 50,000 21,000

Zoom = 0.09 (21%) + 0.014(38%) + 0.033(24%) + 0.006(172.7%) +

0.999(1.72) = 4.33

Zing = 0.012 (7.62%) + 0.014(14.3%) + 0.033(6.2%) + 0.006(39.2%)

+ 0.999(1.095) = 1.825

(ii) Company Zing’s Z Score Index is well below the minimum for a healthy

company, which is 2.675.

PLANNING AND CONTROL

- Financial planning encompasses the firm’s efforts to forecast the firm’s future

financial needs and pre-arrange the details of any financial contracts that may be

required to meet those needs.(Bowlin et al)

- Both financial planning and control involve the use of projections on standards

and the development of a feedback and adjustment process to improve

performance. They involve forecasts and the use of several types of budgets.

- Financial planning and control seek to improve profitability, avoid cash squeezes

and improve the performance of individual division of a company.

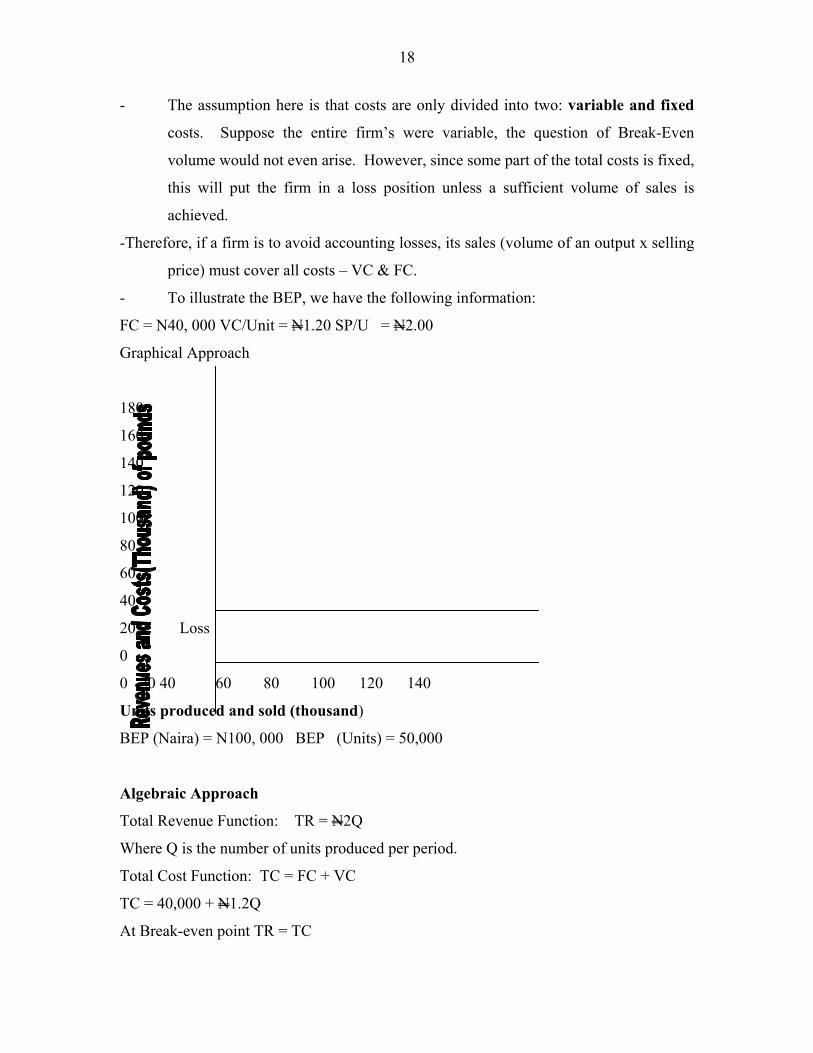

(i) BREAK EVEN ANALYSIS (PROFIT PLANNING)

- Break-even analysis or planning is the relationship between the size of investment

outlays and the required volume to achieve profitability.

- It is device for determining the point at which sales just cover cost i.e. TR = TC.

18

- The assumption here is that costs are only divided into two: variable and fixed

costs. Suppose the entire firm’s were variable, the question of Break-Even

volume would not even arise. However, since some part of the total costs is fixed,

this will put the firm in a loss position unless a sufficient volume of sales is

achieved.

-Therefore, if a firm is to avoid accounting losses, its sales (volume of an output x selling

price) must cover all costs – VC & FC.

- To illustrate the BEP, we have the following information:

FC = N40, 000 VC/Unit = N1.20 SP/U = N2.00

Graphical Approach

180

160

140

120

100

80

60

40

20 Loss

0

0 20 40 60 80 100 120 140

Units produced and sold (thousand)

BEP (Naira) = N100, 000 BEP (Units) = 50,000

Algebraic Approach

Total Revenue Function: TR = N2Q

Where Q is the number of units produced per period.

Total Cost Function: TC = FC + VC

TC = 40,000 + N1.2Q

At Break-even point TR = TC

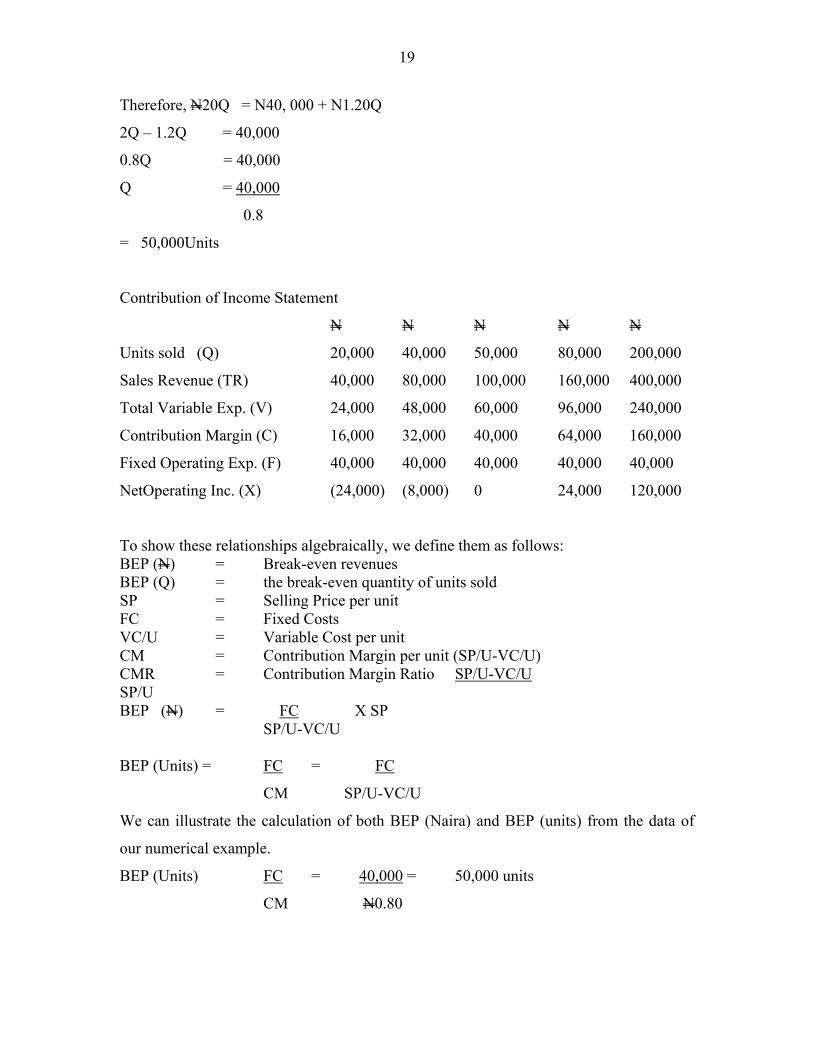

19

Therefore, N20Q = N40, 000 + N1.20Q

2Q – 1.2Q = 40,000

0.8Q = 40,000

Q = 40,000

0.8

= 50,000Units

Contribution of Income Statement

N N N N N

Units sold (Q) 20,000 40,000 50,000 80,000 200,000

Sales Revenue (TR) 40,000 80,000 100,000 160,000 400,000

Total Variable Exp. (V) 24,000 48,000 60,000 96,000 240,000

Contribution Margin (C) 16,000 32,000 40,000 64,000 160,000

Fixed Operating Exp. (F) 40,000 40,000 40,000 40,000 40,000

NetOperating Inc. (X) (24,000) (8,000) 0 24,000 120,000

To show these relationships algebraically, we define them as follows: BEP (N) = Break-even revenues BEP (Q) = the break-even quantity of units sold SP = Selling Price per unit FC = Fixed Costs VC/U = Variable Cost per unit CM = Contribution Margin per unit (SP/U-VC/U) CMR = Contribution Margin Ratio SP/U-VC/U SP/U BEP (N) = FC X SP

SP/U-VC/U BEP (Units) = FC = FC

CM SP/U-VC/U

We can illustrate the calculation of both BEP (Naira) and BEP (units) from the data of

our numerical example.

BEP (Units) FC = 40,000 = 50,000 units

CM N0.80

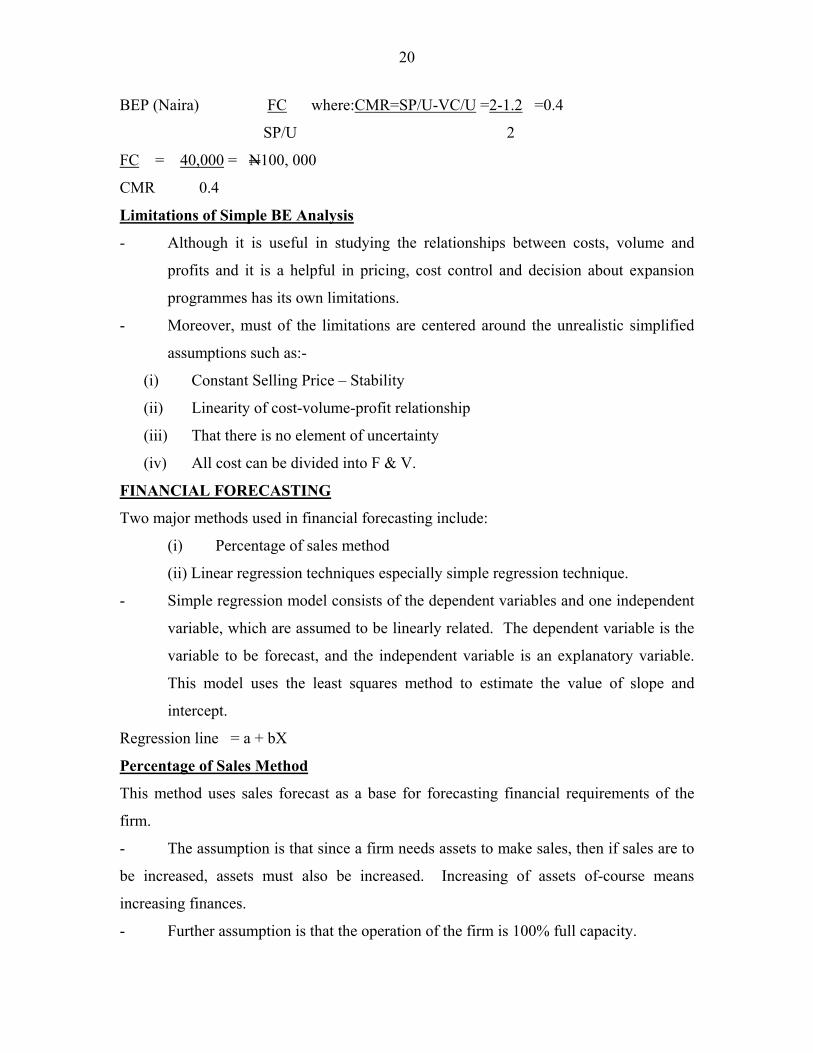

20

BEP (Naira) FC where:CMR=SP/U-VC/U =2-1.2 =0.4

SP/U 2

FC = 40,000 = N100, 000

CMR 0.4

Limitations of Simple BE Analysis

- Although it is useful in studying the relationships between costs, volume and

profits and it is a helpful in pricing, cost control and decision about expansion

programmes has its own limitations.

- Moreover, must of the limitations are centered around the unrealistic simplified

assumptions such as:-

(i) Constant Selling Price – Stability

(ii) Linearity of cost-volume-profit relationship

(iii) That there is no element of uncertainty

(iv) All cost can be divided into F & V.

FINANCIAL FORECASTING

Two major methods used in financial forecasting include:

(i) Percentage of sales method

(ii) Linear regression techniques especially simple regression technique.

- Simple regression model consists of the dependent variables and one independent

variable, which are assumed to be linearly related. The dependent variable is the

variable to be forecast, and the independent variable is an explanatory variable.

This model uses the least squares method to estimate the value of slope and

intercept.

Regression line = a + bX

Percentage of Sales Method

This method uses sales forecast as a base for forecasting financial requirements of the

firm.

- The assumption is that since a firm needs assets to make sales, then if sales are to

be increased, assets must also be increased. Increasing of assets of-course means

increasing finances.

- Further assumption is that the operation of the firm is 100% full capacity.

21

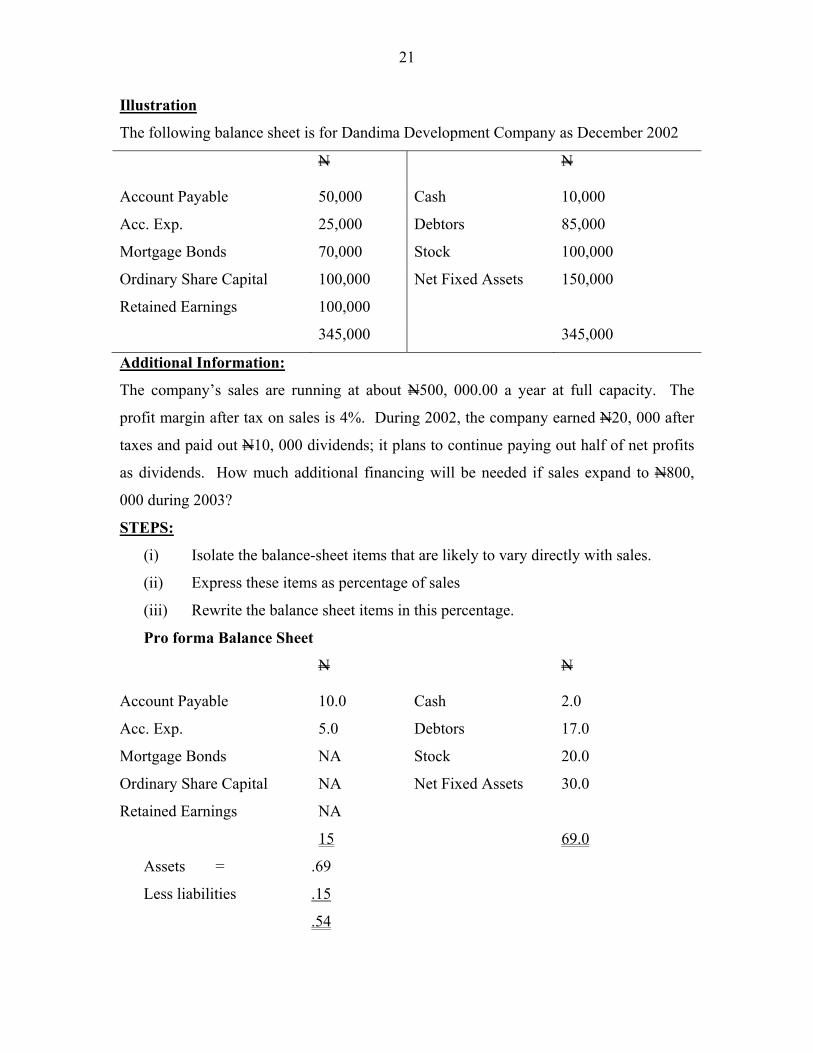

Illustration

The following balance sheet is for Dandima Development Company as December 2002

N N

Account Payable 50,000 Cash 10,000

Acc. Exp. 25,000 Debtors 85,000

Mortgage Bonds 70,000 Stock 100,000

Ordinary Share Capital 100,000 Net Fixed Assets 150,000

Retained Earnings 100,000

345,000 345,000

Additional Information:

The company’s sales are running at about N500, 000.00 a year at full capacity. The

profit margin after tax on sales is 4%. During 2002, the company earned N20, 000 after

taxes and paid out N10, 000 dividends; it plans to continue paying out half of net profits

as dividends. How much additional financing will be needed if sales expand to N800,

000 during 2003?

STEPS:

(i) Isolate the balance-sheet items that are likely to vary directly with sales.

(ii) Express these items as percentage of sales

(iii) Rewrite the balance sheet items in this percentage.

Pro forma Balance Sheet

N N

Account Payable 10.0 Cash 2.0

Acc. Exp. 5.0 Debtors 17.0

Mortgage Bonds NA Stock 20.0

Ordinary Share Capital NA Net Fixed Assets 30.0

Retained Earnings NA

15 69.0

Assets = .69

Less liabilities .15

.54

22

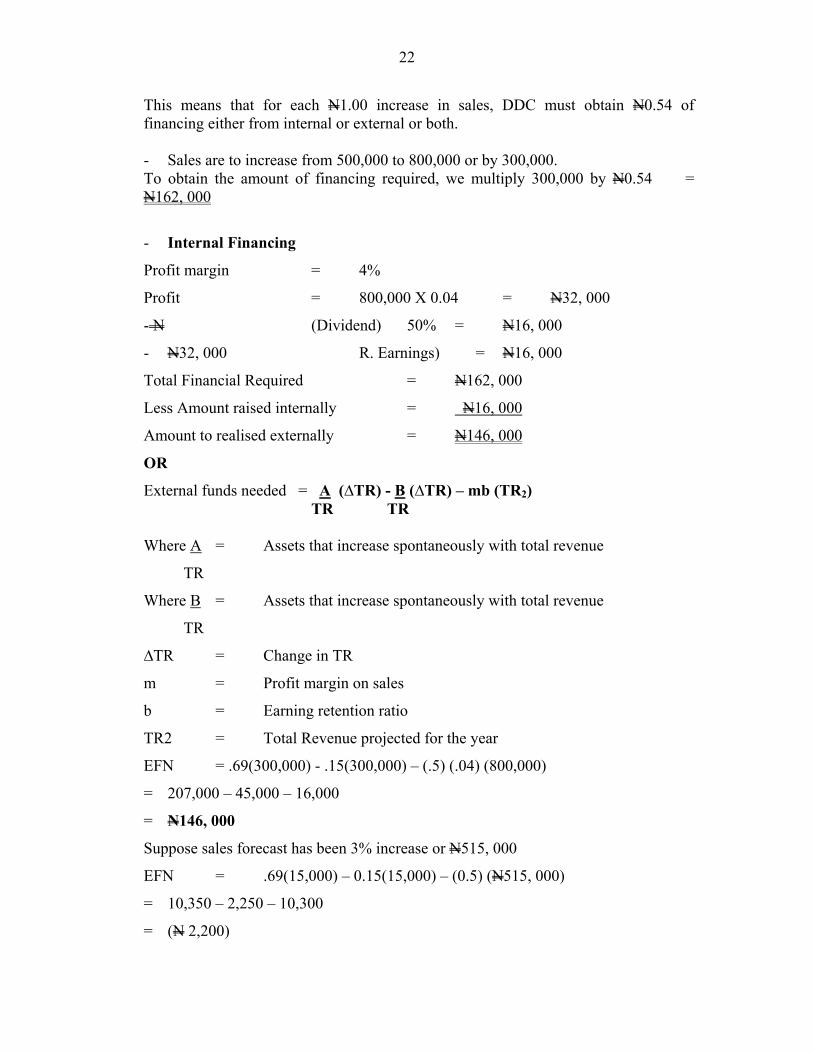

This means that for each N1.00 increase in sales, DDC must obtain N0.54 of financing either from internal or external or both. - Sales are to increase from 500,000 to 800,000 or by 300,000. To obtain the amount of financing required, we multiply 300,000 by N0.54 = N162, 000

- Internal Financing

Profit margin = 4%

Profit = 800,000 X 0.04 = N32, 000

- N (Dividend) 50% = N16, 000

- N32, 000 R. Earnings) = N16, 000

Total Financial Required = N162, 000

Less Amount raised internally = N16, 000

Amount to realised externally = N146, 000

OR

External funds needed = A (∆TR) - B (∆TR) – mb (TR2) TR TR

Where A = Assets that increase spontaneously with total revenue

TR

Where B = Assets that increase spontaneously with total revenue

TR

∆TR = Change in TR

m = Profit margin on sales

b = Earning retention ratio

TR2 = Total Revenue projected for the year

EFN = .69(300,000) - .15(300,000) – (.5) (.04) (800,000)

= 207,000 – 45,000 – 16,000

= N146, 000

Suppose sales forecast has been 3% increase or N515, 000

EFN = .69(15,000) – 0.15(15,000) – (0.5) (N515, 000)

= 10,350 – 2,250 – 10,300

= (N 2,200)

23

Under this circumstance, no external funds are required.

- The company has N 2,200 in excess of the requirements

- The company should therefore do any of the following or combination.

(i) Repay its debts

(ii) Increase dividends

(iii) Seek additional investment opportunities

We can also compute the percentage of the increase in sales that will have to be financed

externally (PEFR)

PEFR = i- m (1 + g) b g Where i = A - B

TR TR g = growth rate in sales

Using our earlier illustration:

i = 0.69 – 0.15 = 0.54

g = 300,000 + 500,000 = 60

PEFR = 0.54 - 0.04 (1.60)0.50

0.60

0.54 – 0.05333

= 48.6%

So 300,000 x 48.6%

PEFR = N146, 000

Suppose the inflation rate is considered and it is estimated at say 10 percent, we add this

to the previous 60 percent to obtain a growth rate of 70 percent.

At 70% PEFR = 0.54 - 0.04 (1.70)0.50

0.70

0.54 – 0.04857

= __ 0.49 or 49%

24

WORKING CAPITAL MANAGEMENT

This is the analysis that involves focusing on only part of the balance sheet by studying

current assets, current liabilities, and the relationship between these two sets of accounts.

The term working capital refers to the capital available for running the day to day

operations of an organization. It is defined as current assets less current liabilities.

Current assets include mainly cash, debtors and stock while current liabilities include

mainly creditors. Thus, working capital represents the firm’s investment in cash,

marketable security, account receivable, and inventories less the current liabilities used to

finance the current assets.

Concepts of Working Capital Management

In the discussion of working capital, it is good to distinguish between different concepts

of working capital.

Gross Working Capital - This refers to a firm’s investment in short-term assets – cash,

marketable securities, debtors, stock etc.

Net Working Capital- This is defined as current assets minus current liabilities used to

finance them such as short-term creditors and accrued expenses.

Working Capital Management – This refers to all aspects of the administration of both

current assets and current liabilities.

Importance of Working Capital Management

(i) Time devoted to Working Capital Management - Financial managers devote a lot

of time to the day-to-day internal operations of the firm’s working capital

management.

(ii) High Investment in Current Assets – Current Assets represent more than half the

total assets of a business firm and therefore worthy of the financial manager’s

careful attention.

(iii) Working Capital in Small Companies - It is particularly important to small firms

because they cannot avoid investment in cash, debtors and stock while they can

minimize investment in fixed (long term) assets by way of renting, hiring and

25

leasing (of plants and equipment for example). Therefore, serious attention must

be paid to working capital management.

(iv) Relationship between Sales Growth and Current Assets - There is close and direct

relationship between sales growth and the need to finance current assets. Consider

the cycle below:

Cash: Raw Materials W.I.P. Finished Goods

Debtors Sales

Determinants of Working Capital

There are no set rules or formulae for determining the working capital level a firm

should hold. It is however, determined by a wide range of factors. These include:

(i) General Nature of the Business – Example trading and financial firms have less

investment in fixed assets – only in working capital.

(ii) Promotion/Manufacturing Cycle - The longer the cycle, the longer the working

capital requirement.

(iii) Growth and Expansion – Growth industries require more working capital than

those that are static.

(iv) Dividend- Policy - The payment of dividend consumes cash resources, and

thereby affects working capital to that extent.

(v) Government Industrial Policy – For example, commercial banks are sometimes

required to maintain a certain minimum amount of cash in a special account with the

Central Bank, the lower the rate, the higher the working capital and vice-versa.

Other factors include business cycle, production policy, credit policy, profit level,

depreciation policy and so on.

Optimum Level for Current Asset Investments

If a firm could be able to forecast perfectly enough cash to make disbursements as

required, enough stocks to meet production and sales requirements, the exact trade

debtors called for by an optimal credit policy and investment in marketable securities,

where the interest returns on such assets exceeded the cost of capital, it is referred to as

the theoretical optimum for working capital.

26

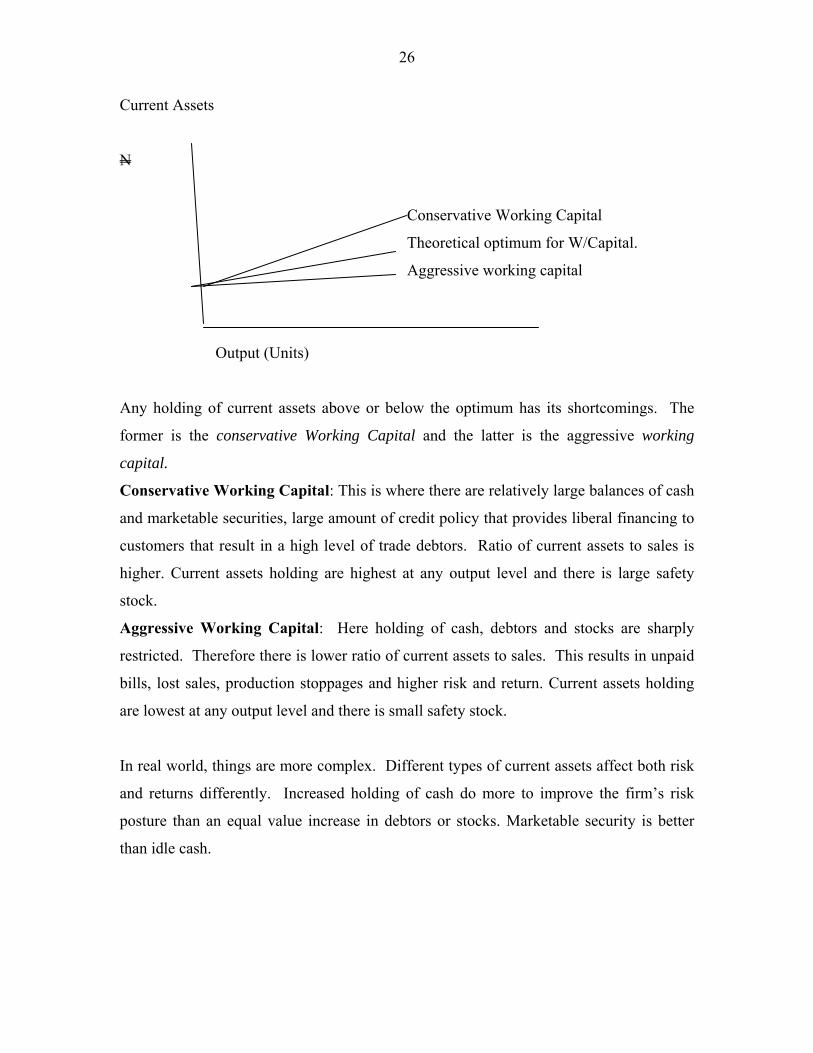

Current Assets

N

Conservative Working Capital

Theoretical optimum for W/Capital.

Aggressive working capital

Output (Units)

Any holding of current assets above or below the optimum has its shortcomings. The

former is the conservative Working Capital and the latter is the aggressive working

capital.

Conservative Working Capital: This is where there are relatively large balances of cash

and marketable securities, large amount of credit policy that provides liberal financing to

customers that result in a high level of trade debtors. Ratio of current assets to sales is

higher. Current assets holding are highest at any output level and there is large safety

stock.

Aggressive Working Capital: Here holding of cash, debtors and stocks are sharply

restricted. Therefore there is lower ratio of current assets to sales. This results in unpaid

bills, lost sales, production stoppages and higher risk and return. Current assets holding

are lowest at any output level and there is small safety stock.

In real world, things are more complex. Different types of current assets affect both risk

and returns differently. Increased holding of cash do more to improve the firm’s risk

posture than an equal value increase in debtors or stocks. Marketable security is better

than idle cash.

27

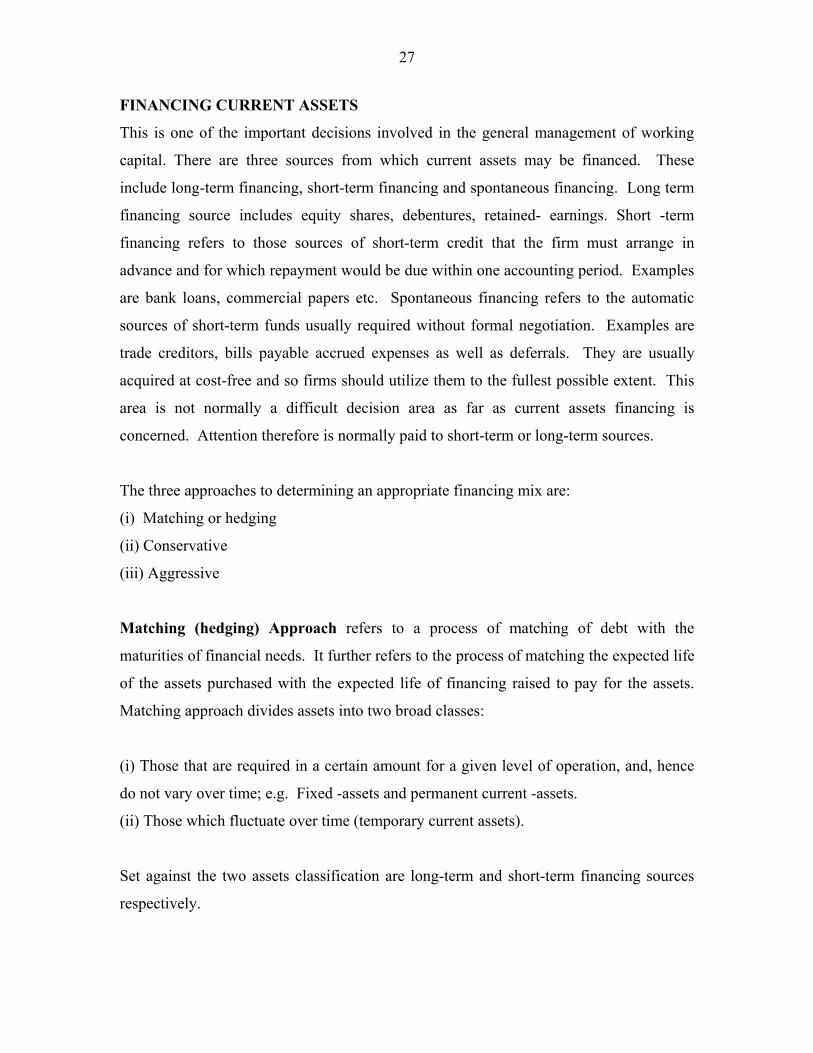

FINANCING CURRENT ASSETS

This is one of the important decisions involved in the general management of working

capital. There are three sources from which current assets may be financed. These

include long-term financing, short-term financing and spontaneous financing. Long term

financing source includes equity shares, debentures, retained- earnings. Short -term

financing refers to those sources of short-term credit that the firm must arrange in

advance and for which repayment would be due within one accounting period. Examples

are bank loans, commercial papers etc. Spontaneous financing refers to the automatic

sources of short-term funds usually required without formal negotiation. Examples are

trade creditors, bills payable accrued expenses as well as deferrals. They are usually

acquired at cost-free and so firms should utilize them to the fullest possible extent. This

area is not normally a difficult decision area as far as current assets financing is

concerned. Attention therefore is normally paid to short-term or long-term sources.

The three approaches to determining an appropriate financing mix are:

(i) Matching or hedging

(ii) Conservative

(iii) Aggressive

Matching (hedging) Approach refers to a process of matching of debt with the

maturities of financial needs. It further refers to the process of matching the expected life

of the assets purchased with the expected life of financing raised to pay for the assets.

Matching approach divides assets into two broad classes:

(i) Those that are required in a certain amount for a given level of operation, and, hence

do not vary over time; e.g. Fixed -assets and permanent current -assets.

(ii) Those which fluctuate over time (temporary current assets).

Set against the two assets classification are long-term and short-term financing sources

respectively.

28

Financing Under Matching/Hedging Approach

Temporary Current Assets

Short-term

Assets financing

Permanent Current Assets Long-term

Financing

Total Permanent Fixed Assets Assets

Time

Fixed Assets and permanent current assets are financed by long-term financing and

temporary current assets with short-term financing principles of suitability.

Here short-term financing requirement (Current Assets) would just be equal to the short-

term financing available (Current Liabilities.) Therefore, (i) Net Working Capital would

be zero or C.A. ratio of 1:1 (ii) It presupposes a moderate return and moderate risk

position.

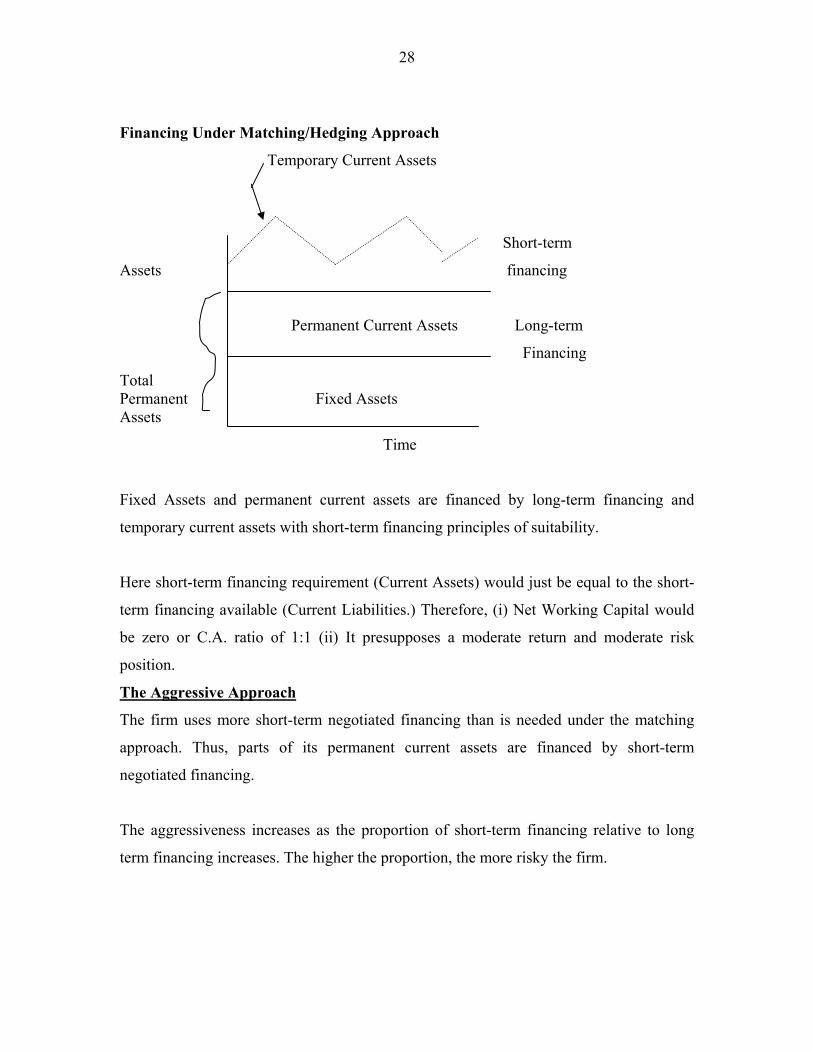

The Aggressive Approach

The firm uses more short-term negotiated financing than is needed under the matching

approach. Thus, parts of its permanent current assets are financed by short-term

negotiated financing.

The aggressiveness increases as the proportion of short-term financing relative to long

term financing increases. The higher the proportion, the more risky the firm.

29

An Aggressive Financing Approach

Short-term

Assets financing

Permanent Current Assets Long-term

Financing

Fixed Assets

Time

This approaches increases the firm’s profitability since a relatively larger position of its

assets is financed through lower cost short-term borrowing.

However, the firm is also increasing its exposure to risk by borrowing more on a short

term basis. Its inability to renew its short-term debt could force it into bankruptcy.

The Conservative Financing Approach

This is where more long-term financing is used than needed in matching approach. The higher the proportion of long-term financing source to short-term source, the more conservative.

Assets

Short-term financing

Permanent Current Asset Long-term financing

Fixed Assets

Time

30

Here the level of permanent financing is relatively higher than matching approach as

permanent funds are used to finance temporary fluctuating current assets. Thus, during

periods of low fluctuating current assets required by the firm may invest its excess funds

in marketable securities. The approach reduces the amount of funds requirements to be

borrowed temporary, resulting in high liquidity and so less risk of insolvency. However,

it suffers from low returns because;

(i) The cost of permanent financing is generally higher than the cost of short-term

credit.

(ii) Marketable securities have a relatively low rate of return compared to the returns

from on going long-term projects.

Which Approach to Adopt?

It is not an easy task for a financial manager to decide on one of the three approaches to

adopt. Where all the variables the approaches assumed to be known one in practice,

really knows the task then becomes easy one. Since the world of practice is however full

of uncertainties, most financial managers use estimates by way of attaching certain

probabilities to the occurrence levels of each variable to easy their decisions. They then

determine the risk to take and the appropriate return acceptable to the risk taken. This is

so because, as already shown, whatever approach is taken, there are risks as well as

returns considerations. Financial managers are then in a risk-return tangle.

TC Function

Cost of Liquidity

Cost of Illiquidity

Optimum Level

COMPONENTS OF WORKING CAPITAL

The components of working capital are cash, marketable securities, debtors and stock

(inventory).

31

A. Cash & Marketable Securities Management

This involves managing the monies of the firm in order to attain maximum cash available

and maximum interest income on any idle fund. It is also concerned with the most

effective ways of accelerating collections and handling cash disbursements so that

maximum cash is available.

Motives for Holding Cash

(i) Transaction motive

(ii) Precautionary motive

(iii) Speculative motive

(iv) Compensation- balance – motive

Transaction motive: A firm needs to hold cash in ordinary course of business for the day–

to–day operations. For instance, cash is needed to pay creditors, t buy stocks, to pay

wages, operating expenses, taxes, dividends etc.

Precautionary motive: A firm needs too hold cash to meet any contingencies in the

future. Contingent losses may be material; .e.g. pending law suits against the company or

a bill of exchange that that the company has accepted. Holding cash provides a cushion to

withstand unexpected emergency cash flows.

Speculative motive: A firm needs to hold cash to finance profitable investment

opportunities as and when they arise. The investment opportunities might be risky

ventures, e.g. purchasing a machine for a speculative project.

Compensating Balance Motive: Banks typically require that a regular borrower maintains

an average account balance equal to 15% to 20% of the outstanding loan. This balance,

commonly called Compensating balance, is a method of raising the effective interest rate.

32

Cash Management Models

Several types of mathematical models have been developed to help determine optimal

cash balances. An early model developed by William J. Baumol applies a basic

inventory model to cash management. The model believes that there are costs for too low

or too high cash balance. It is assumed that a firm on the average is growing and is a net

user of cash. Marketable securities in the model represent a buffer stock between

episodes of external financing, which is drawn down as required periodically. Ordering

costs are represented by the clerical and transactions costs of making transfer between the

investment portfolio and the cash account. The holding cost is the interest foregone on

cash balances held. It is also assumed that cash expenditure occurs evenly over-time and

that cash replenishment comes in lump sum at periodic interval.

Baumol formulated the optimal size of cash transfer as follows:

c= 2bt Where: i

c = Optimal cash transaction

t = Total cash usage for the period of time involved b = Cost of the transaction in the purchase or sale of marketable securities i = the applicable interest rate on marketable securities Illustration

A company’s total demand for cash for one year is N1, 800,000. The cost of transaction

is N25. Applicable interest on marketable securities is 10%. Compute the firm’s optimum

size of cash transaction.

Solution:

t = 1.8m b = N25, i = 10%

c = √2bt = √ 2(25) (1,800,000) = N30, 000 i 0.1 Average cash balance - C/2 = 30,000/2= N15, 000 No. of transfer/operations per year t⁄c = 1,800,000 = 60 times 5 times /month Total cost of maintaining cash balance per year TC b (T/C) + i (C/2) 25 (1.8m) + .1 (30,000) 30,000 2

TC = N3, 000

33

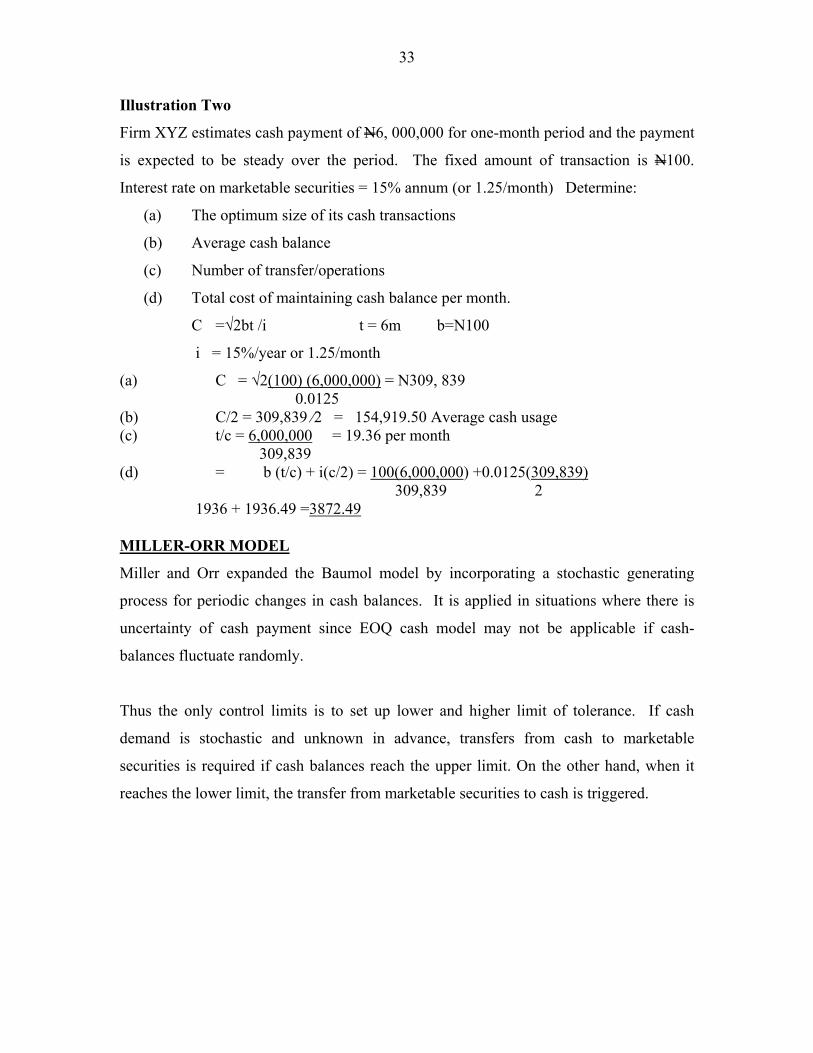

Illustration Two

Firm XYZ estimates cash payment of N6, 000,000 for one-month period and the payment

is expected to be steady over the period. The fixed amount of transaction is N100.

Interest rate on marketable securities = 15% annum (or 1.25/month) Determine:

(a) The optimum size of its cash transactions

(b) Average cash balance

(c) Number of transfer/operations

(d) Total cost of maintaining cash balance per month.

C =√2bt /i t = 6m b=N100

i = 15%/year or 1.25/month

(a) C = √2(100) (6,000,000) = N309, 839 0.0125 (b) C/2 = 309,839 ⁄2 = 154,919.50 Average cash usage (c) t/c = 6,000,000 = 19.36 per month 309,839 (d) = b (t/c) + i(c/2) = 100(6,000,000) +0.0125(309,839) 309,839 2 1936 + 1936.49 =3872.49 MILLER-ORR MODEL

Miller and Orr expanded the Baumol model by incorporating a stochastic generating

process for periodic changes in cash balances. It is applied in situations where there is

uncertainty of cash payment since EOQ cash model may not be applicable if cash-

balances fluctuate randomly.

Thus the only control limits is to set up lower and higher limit of tolerance. If cash

demand is stochastic and unknown in advance, transfers from cash to marketable

securities is required if cash balances reach the upper limit. On the other hand, when it

reaches the lower limit, the transfer from marketable securities to cash is triggered.

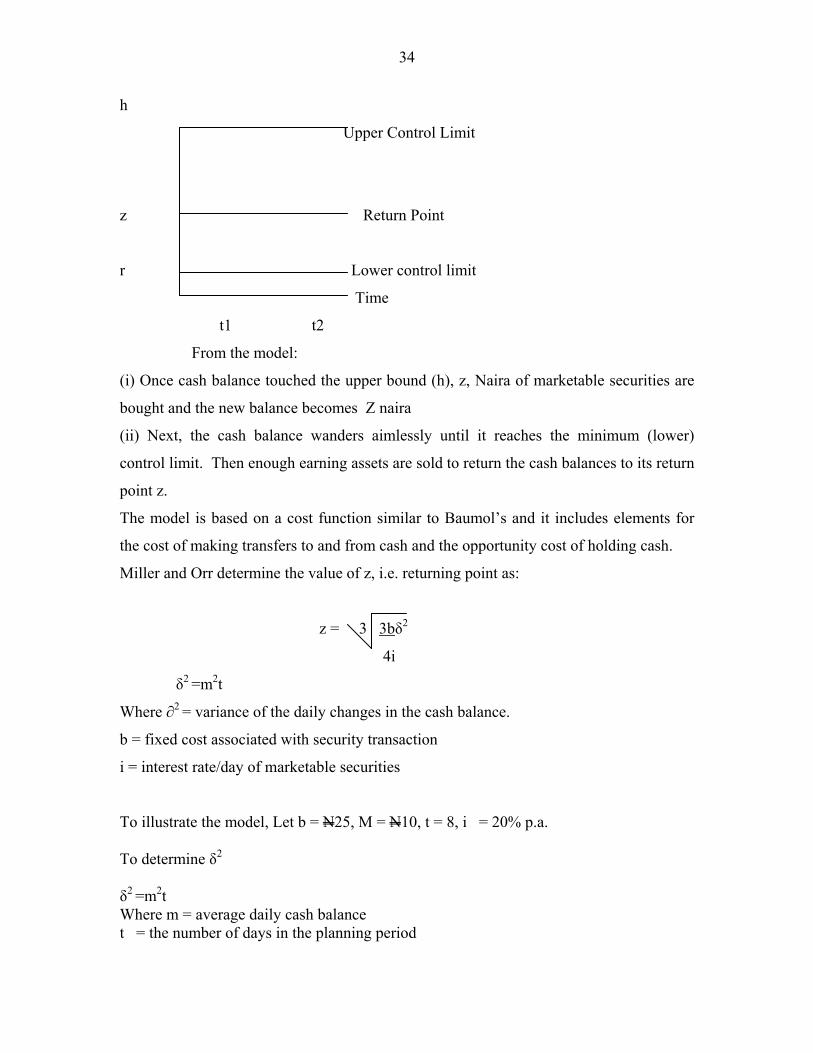

34

h

Upper Control Limit

z Return Point

r Lower control limit

Time

t1 t2

From the model:

(i) Once cash balance touched the upper bound (h), z, Naira of marketable securities are

bought and the new balance becomes Z naira

(ii) Next, the cash balance wanders aimlessly until it reaches the minimum (lower)

control limit. Then enough earning assets are sold to return the cash balances to its return

point z.

The model is based on a cost function similar to Baumol’s and it includes elements for

the cost of making transfers to and from cash and the opportunity cost of holding cash.

Miller and Orr determine the value of z, i.e. returning point as: z = 3 3b2

4i

2 =m2t

Where ∂2 = variance of the daily changes in the cash balance.

b = fixed cost associated with security transaction

i = interest rate/day of marketable securities

To illustrate the model, Let b = N25, M = N10, t = 8, i = 20% p.a. To determine 2 2 =m2t Where m = average daily cash balance t = the number of days in the planning period

35

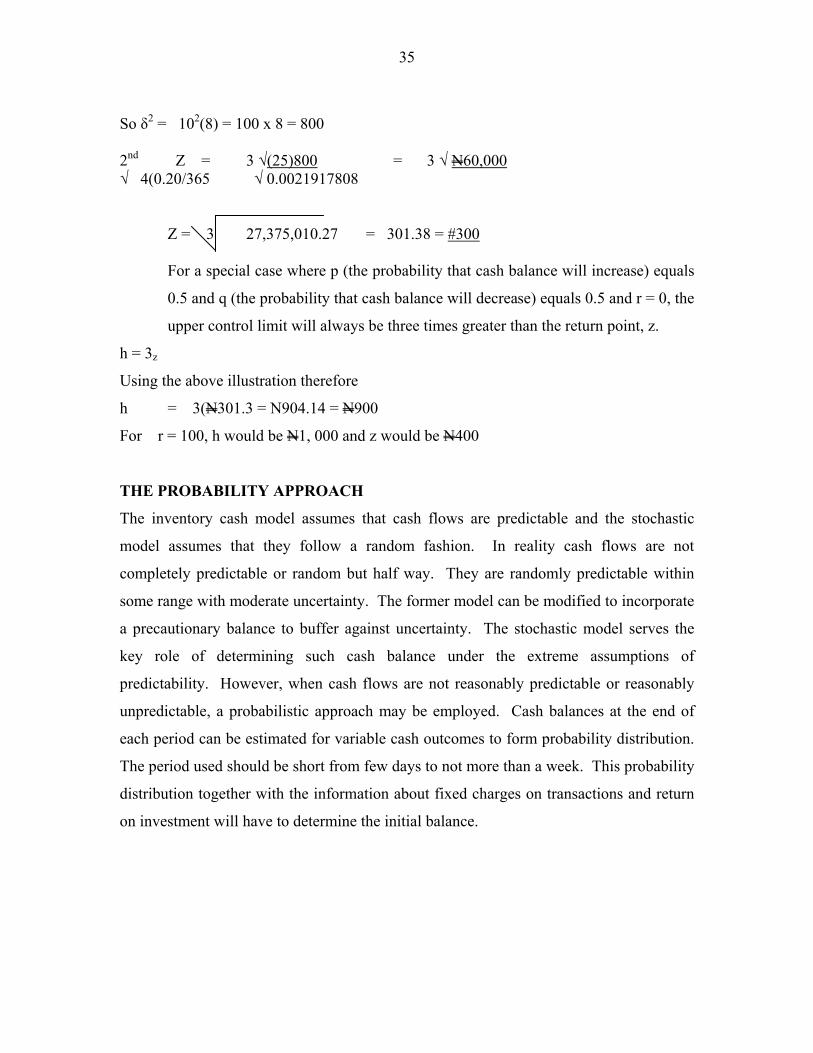

So 2 = 102(8) = 100 x 8 = 800 2nd Z = 3 √(25)800 = 3 √ N60,000 √ 4(0.20/365 √ 0.0021917808 Z = 3 27,375,010.27 = 301.38 = #300

For a special case where p (the probability that cash balance will increase) equals

0.5 and q (the probability that cash balance will decrease) equals 0.5 and r = 0, the

upper control limit will always be three times greater than the return point, z.

h = 3z

Using the above illustration therefore

h = 3(N301.3 = N904.14 = N900

For r = 100, h would be N1, 000 and z would be N400

THE PROBABILITY APPROACH

The inventory cash model assumes that cash flows are predictable and the stochastic

model assumes that they follow a random fashion. In reality cash flows are not

completely predictable or random but half way. They are randomly predictable within

some range with moderate uncertainty. The former model can be modified to incorporate

a precautionary balance to buffer against uncertainty. The stochastic model serves the

key role of determining such cash balance under the extreme assumptions of

predictability. However, when cash flows are not reasonably predictable or reasonably

unpredictable, a probabilistic approach may be employed. Cash balances at the end of

each period can be estimated for variable cash outcomes to form probability distribution.

The period used should be short from few days to not more than a week. This probability

distribution together with the information about fixed charges on transactions and return

on investment will have to determine the initial balance.

36

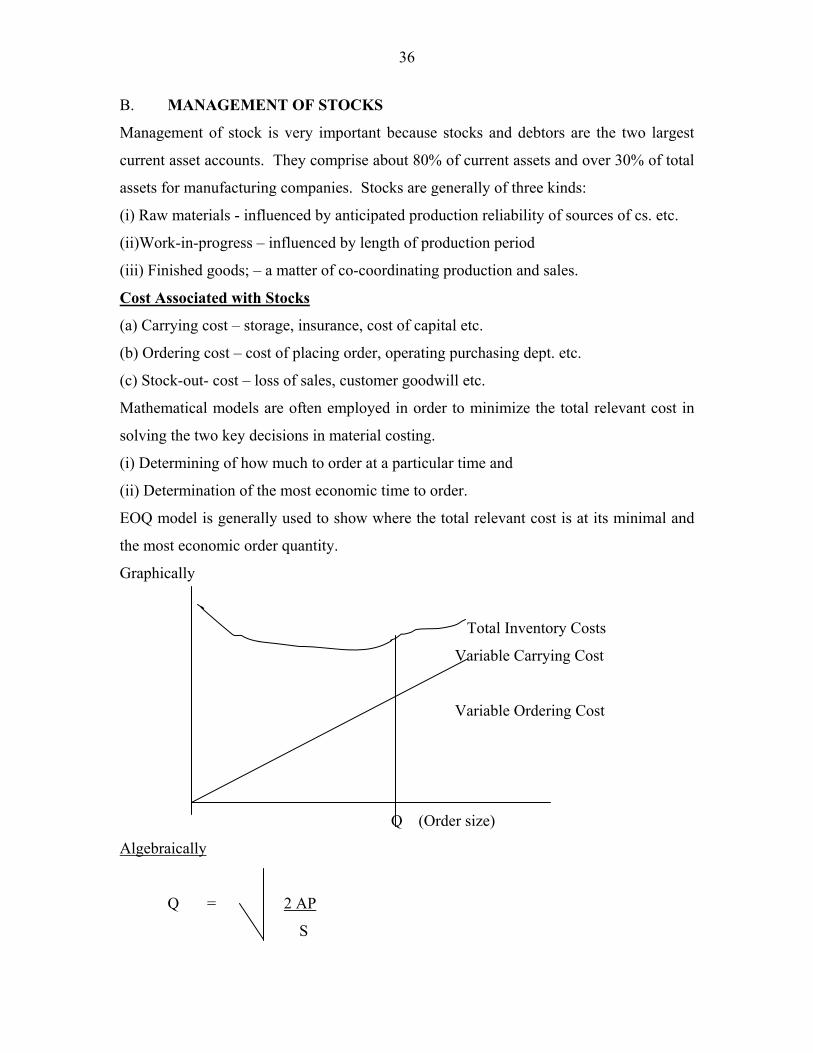

B. MANAGEMENT OF STOCKS

Management of stock is very important because stocks and debtors are the two largest

current asset accounts. They comprise about 80% of current assets and over 30% of total

assets for manufacturing companies. Stocks are generally of three kinds:

(i) Raw materials - influenced by anticipated production reliability of sources of cs. etc.

(ii)Work-in-progress – influenced by length of production period

(iii) Finished goods; – a matter of co-coordinating production and sales.

Cost Associated with Stocks

(a) Carrying cost – storage, insurance, cost of capital etc.

(b) Ordering cost – cost of placing order, operating purchasing dept. etc.

(c) Stock-out- cost – loss of sales, customer goodwill etc.

Mathematical models are often employed in order to minimize the total relevant cost in

solving the two key decisions in material costing.

(i) Determining of how much to order at a particular time and

(ii) Determination of the most economic time to order.

EOQ model is generally used to show where the total relevant cost is at its minimal and

the most economic order quantity.

Graphically

Total Inventory Costs

Variable Carrying Cost

Variable Ordering Cost

Q (Order size)

Algebraically

Q = 2 AP

S

37

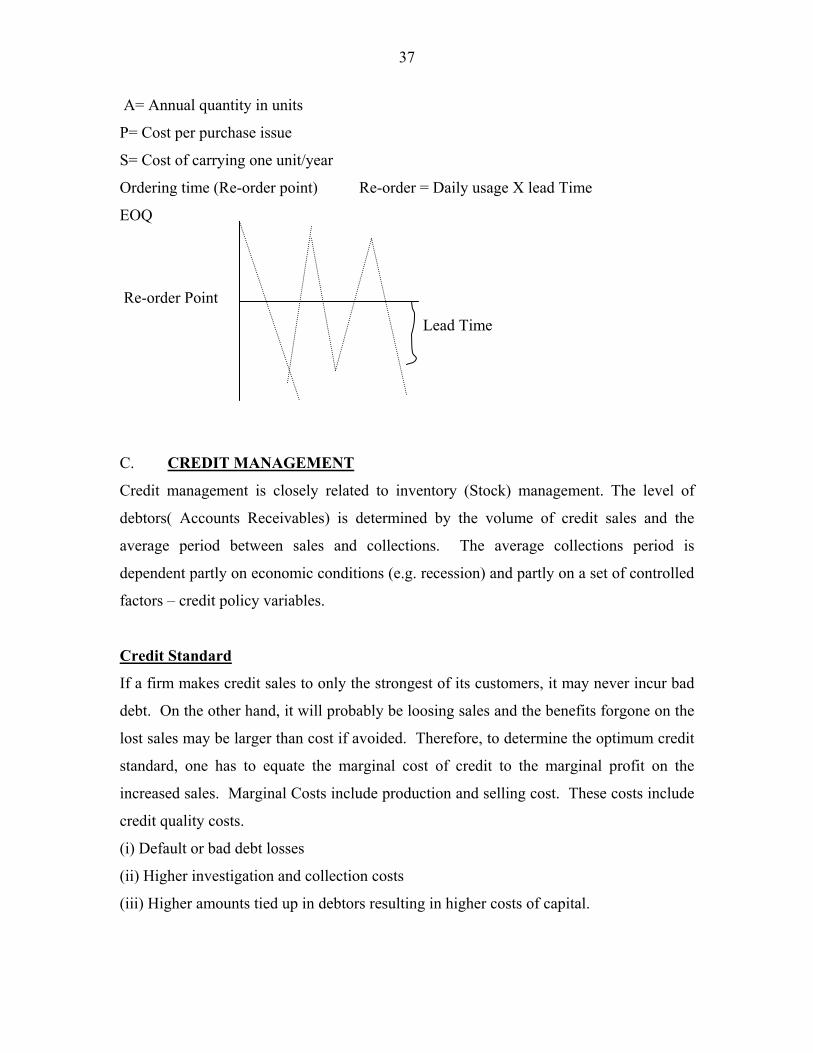

A= Annual quantity in units

P= Cost per purchase issue

S= Cost of carrying one unit/year

Ordering time (Re-order point) Re-order = Daily usage X lead Time

EOQ

Re-order Point

Lead Time

C. CREDIT MANAGEMENT

Credit management is closely related to inventory (Stock) management. The level of

debtors( Accounts Receivables) is determined by the volume of credit sales and the

average period between sales and collections. The average collections period is

dependent partly on economic conditions (e.g. recession) and partly on a set of controlled

factors – credit policy variables.

Credit Standard

If a firm makes credit sales to only the strongest of its customers, it may never incur bad

debt. On the other hand, it will probably be loosing sales and the benefits forgone on the

lost sales may be larger than cost if avoided. Therefore, to determine the optimum credit

standard, one has to equate the marginal cost of credit to the marginal profit on the

increased sales. Marginal Costs include production and selling cost. These costs include

credit quality costs.

(i) Default or bad debt losses

(ii) Higher investigation and collection costs

(iii) Higher amounts tied up in debtors resulting in higher costs of capital.

38

Since credit cost and credit quality are negatively correlated, it is important to be able to

judge the quality of a customer, and perhaps the best way to do this is in terms of the

probability of default. A good credit manager should therefore be able to make a near

accurate judgment of his customers. In evaluating any credit policy, the benefits of the

policy should be compared with the costs of the policy. For instance, the benefits of a

proposed policy to ease credit terms include increases in sales and profit from sales,

while the costs of the policy include:

(i) Interest charges on an additional increase in debtors.

(ii) Increase in bad debt.

FIVE Cs of CREDIT

To evaluate the credit-risk, credit managers should consider the five Cs of credit:

Character of the Customer: This is subjective – willingness to pay. Some

customers are capable but not willing to pay N 100,000 in debit collection, and

average collection period of 2 months. Bad debt also currently amounts to

Capacity: The customer’s ability to pay. Look at past Behaviour of the

customers and making physical investigation of the customers’ assets like store,

balance sheet records etc.

Capital: A measure of the general financial situation of the firm’s position with

special attention to risk ratios and time interest analysis ratio.

Collateral: Security – what a customer places against the loan.

Conditions: The general economic conditions. Is it boom or doom condition?

These represent the factors by which the credit risks are judged.

Terms of Credit

These specify the period for which credit is extended and the discount if any, for early

payment. E.g. if a firm’s credit terms to all approved customers are stated as 2/10, net 30,

then 2% discount from the stated sales price is granted if payment is made within 10

days, and the entire amount is due 10 days from the invoice date if the discount is not

taken. If the terms are stated ‘net 60’, this indicates that no discount is offered and that

the bill is due and payable 60 days after the invoice date.

39

Credit Period

Lengthening the credit period is likely to stimulate sales, but there is a cost to tying up

funds in debtors. For example, if a firm changes its terms from net 30 to net 60, the

average debtors for the year may rise from N100,000 to N300,000 – the increase is

caused partly by the longer credit terms and partly by the larger volume of sales. The

optimal credit policy is therefore determined by the point where marginal profits on

increased sales are exactly offset by the cost carrying the higher amount of debtors.

Practice Question

Dotcom Ltd. With a turnover of N3 million is currently contemplating changing its debt

collection policy. It currently incurs administrative cost of N 100,000 in debt collection

and average collection is 2 months. Bad debt also currently amounts to 2.5% of sales.

The company is considering two options as follows:

Option A Option B

Administrative cost of bad debt #150,000 #10,000

Bad debt losses (% of sales) 1.5% -

Average collection period 1 month 1/5

Factoring fee (% of sales) - 3%

The company currently requires a 16% return on its investment. Please advice the

company on the best option.

40

CAPITAL BUDGETING

(a) Introduction

This involves the entire process of planning expenditure whose returns are expected to

extend beyond one year. Capital expenditure which is expected to yield benefit in two

or more years include expenditure for land, building, machinery, advertising and sales

promotions etc. The decision to invest in these areas based on cost-benefit analysis is

called capital budgeting decision.

(b) Features of Capital Budgeting:

Investment decisions are generally grouped into three:

The problems of searching out project and obtaining information about them.

Deciding which project(s) to invest and the extent of investment in each and;

Deciding upon the sources of finance upon which to draw and how much to

obtain from each source.

The third of these decisions is the principal concern of Capital Budgeting. There are

three capital budgeting decisions:

(a) The accept-reject decisions

(b) Mutually exclusive choice decisions

(c) Capital rationing decisions

(c) Cash Flow Analysis

After the firm has decided to embark on any capital expenditure, estimates of cash

inflows and outflows in respect of each respective proposal must be determined.

However, it is difficult to predict the outcome of an investment with certainty in

determining;

(a) The net cash inflows for each proposal, one must consider the cost of the new project,

the installation costs (if any i.e. income taxes etc.)

(b)The net cash inflows on the other hand, all expected benefits from a proposed project

must be measured on a cash flow basis, profit after taxes and depreciation

41

(d) Importance of Capital Budgeting Decision

They have long-term implications for the firm and can influence its risk

complexion.

They involve commitment of large funds.

They are irreversible decisions that cannot be reversed without certain costs.

They are among the most difficult decisions to make.

(e) Capital Budgeting Techniques

There are different techniques that are used in ranking investment proposals. Prominent

among them are:

Payback method or payback period (PBP)

Discounted Payback Period (DPBP)

Average Rate of Return (ARR)

Net Present Value (NPV)

Internal Rate Of Return (IRR)

Profitability Index (PI)

The first two (3) techniques are sometimes referred to as unsophisticated and the last

three as sophisticated.

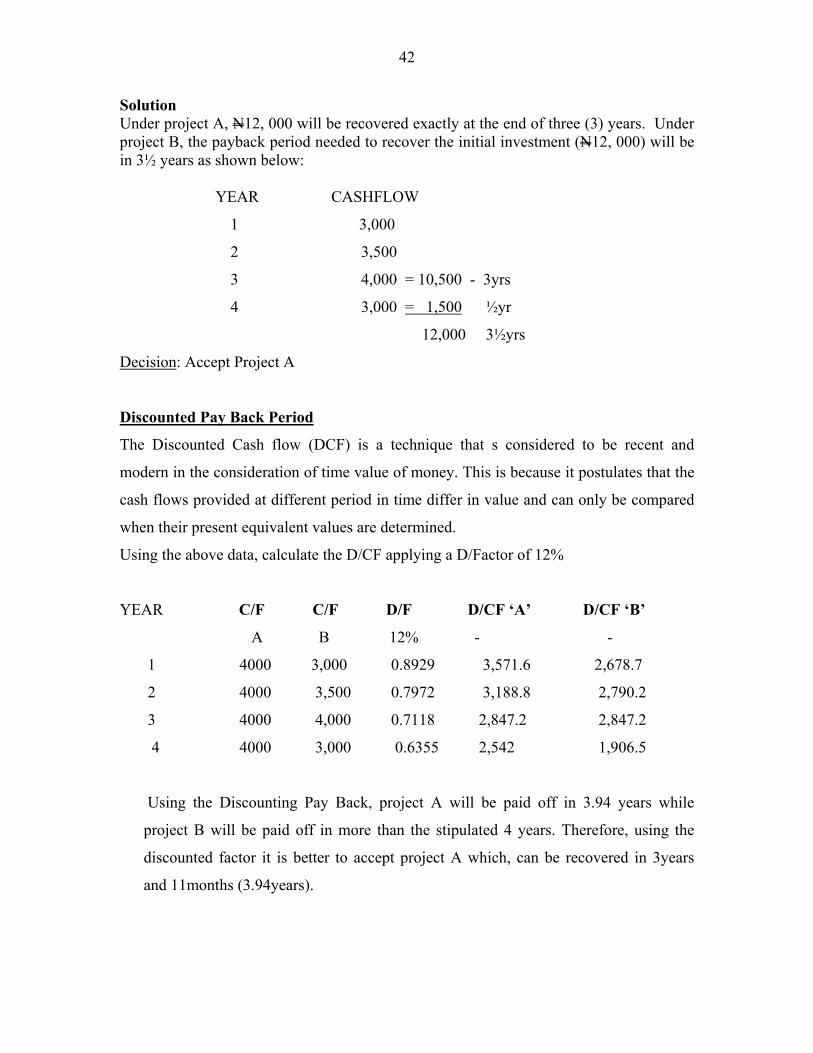

Payback Period - This is defined as the number of years it takes the project to recover

the initial investment.

Illustration:

Assume that a firm is considering two mutually exclusive projects, each project requires

investment of N12, 000. It is estimated that net cash inflow for the next 5 years in respect

of each project is as follows:

Year 1 2 3 4 5

Project A (N) 4,000 4,000 4,000 4,000 4,000

Project B (N) 3,000 3,500 4,000 3,000 8,500

Required: Which project should the firm select using payback period?

42

Solution Under project A, N12, 000 will be recovered exactly at the end of three (3) years. Under project B, the payback period needed to recover the initial investment (N12, 000) will be in 3½ years as shown below:

YEAR CASHFLOW

1 3,000

2 3,500

3 4,000 = 10,500 - 3yrs

4 3,000 = 1,500 ½yr

12,000 3½yrs

Decision: Accept Project A

Discounted Pay Back Period

The Discounted Cash flow (DCF) is a technique that s considered to be recent and

modern in the consideration of time value of money. This is because it postulates that the

cash flows provided at different period in time differ in value and can only be compared

when their present equivalent values are determined.

Using the above data, calculate the D/CF applying a D/Factor of 12%

YEAR C/F C/F D/F D/CF ‘A’ D/CF ‘B’

A B 12% - -

1 4000 3,000 0.8929 3,571.6 2,678.7

2 4000 3,500 0.7972 3,188.8 2,790.2

3 4000 4,000 0.7118 2,847.2 2,847.2

4 4000 3,000 0.6355 2,542 1,906.5

Using the Discounting Pay Back, project A will be paid off in 3.94 years while

project B will be paid off in more than the stipulated 4 years. Therefore, using the

discounted factor it is better to accept project A which, can be recovered in 3years

and 11months (3.94years).

43

Average Rate of Return (ARR) - It is seen as the average cash flow (after taxes) divided

by initial (or average) investment.

ARR= ∑_Cft/n Initial Investment ÷ 2

ARR (Project A) (4,000 + 4,000+ 4,000 + 4,000 + 4,000)/5 12,000 ÷ 2

4,000 = 0.67 or 67% 6,000

ARR (Project B) (3,000 + 3,500+ 4,000 + 3,000 + 8,500)/5 12,000 ÷ 2 4,400 = 0.73 or 73% 6,000 Decision: In mutually exclusive events (or projects) as in the example above, the

decision is to accept projects with the highest ARR. Thus, we accept Project B with 73%

as against Project A’s 67%

Net Present Value (NPV): - This is arrived at by first finding the present value (PV) of

the expected net cash flows of investment, discounted at the cost of capital and then

subtracts from it the initial cost outlay of the project. If the net present value is positive,

the project should be accepted, if negative it should be rejected. If the projects are

mutually exclusive, the one with the highest net present value should be chosen.

NPV = Present Value of cash flow less Initial Investment

NPV =∑ CFt - Initial Investment = CF1 + CF2….CFn (1+k) t (1+k) 1 + (1+k) 2+…… (1+k) n

Where:

CF = Net Cash flow

K = The Project’s required rate of return

N = The Project’s expected life

NPV (Project A)

PV = 4,000 X 3.60478 (3.60478 is from the annuity table)

= N14, 419.20

44

NPV = PV – Initial Investment

= 14,419.20 – 12,000 = N2, 419.20

NPV (Project B)

PV = 3000 + 3,500 + 4,000 + 3,000 + 8,500 = 15,045.75

(1.12) (1.12)2 (1.12)3 (1.12)4 (1.12)5

NPV = 15,045.75 – 12,000 = N3, 045.75

Decision: The decision using this technique is to accept Project B for it has the highest

NPV.

Internal Rate of Return

IRR is that rate which equates the present value of cash inflows with the present value of

cash outflows of an investment. The objective is to find a discount rate, which equates the

present value of all future cash out flows from the investment with the initial cash outlay.

All other parameters remain the same as in the NPV equation except that the value ‘r’

replaces ‘K’ (i.e. Cost of capital already assumed to be known in NPV) r -value in IRR

has to be determined where NPV is equal to zero. The calculation of IRR using even -

stream of cash flows is not different. In a situation where there is unequal cash flow, the

equation can only be solved through trial and error.

IRR = ∑ CFt - 1 = 0 (1+r) t

IRR = (CF1 + CF2 + CF3 …..CFn) - I = 0 (1+r) (1+r) 2 (1+r) 3….. (1+r) n Where CF = Cash Inflows (known) I = Initial Investment (Known) r = (Unknown) Returning to our earlier example, the IRR for Project A may be calculated as follows:

4000 + 4000 + 4000 + 4000 + 4000 (1+r) (1+r) 2 (1+r) 3 (1+r) 4 1+r) 5 r = 19.86%

3,337.23 + 2,784.27 + 2,322.94 + 1,938.04 + 1,616.92 = 11,999.4

45

#12,000 - #12,000 = 0

The process of getting the rate of return is by Trial and Error

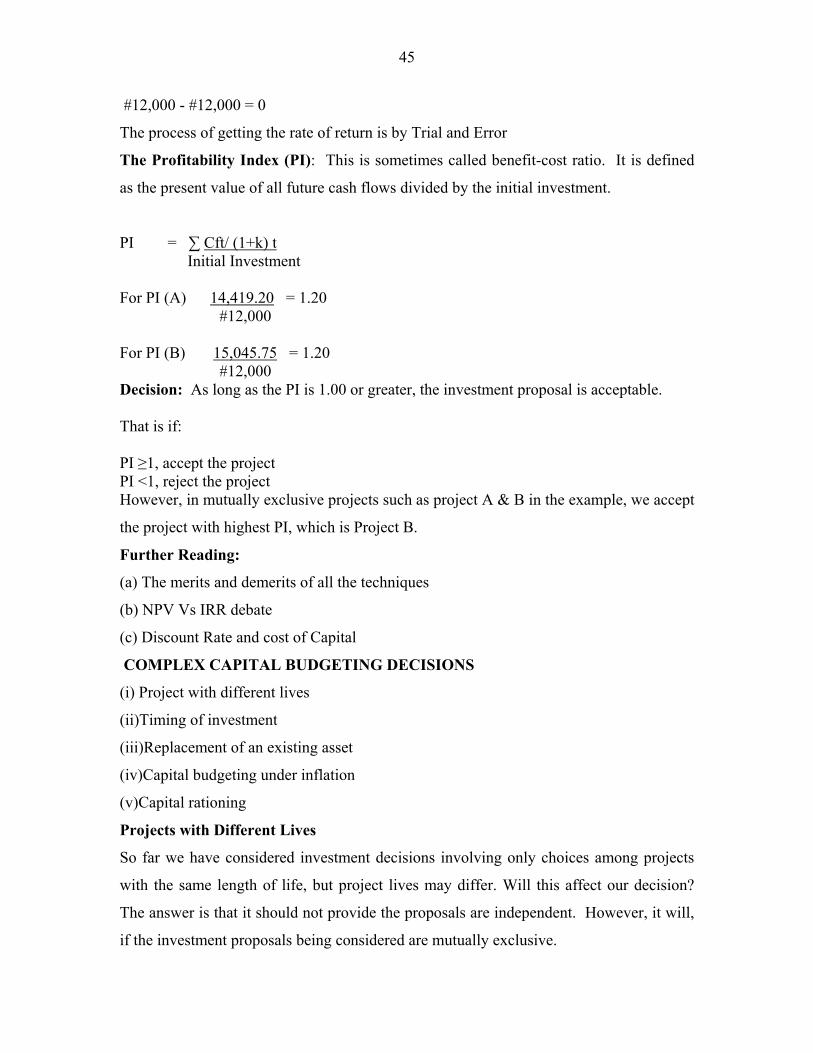

The Profitability Index (PI): This is sometimes called benefit-cost ratio. It is defined

as the present value of all future cash flows divided by the initial investment.

PI = ∑ Cft/ (1+k) t Initial Investment For PI (A) 14,419.20 = 1.20 #12,000 For PI (B) 15,045.75 = 1.20 #12,000 Decision: As long as the PI is 1.00 or greater, the investment proposal is acceptable. That is if: PI ≥1, accept the project PI <1, reject the project However, in mutually exclusive projects such as project A & B in the example, we accept

the project with highest PI, which is Project B.

Further Reading:

(a) The merits and demerits of all the techniques

(b) NPV Vs IRR debate

(c) Discount Rate and cost of Capital

COMPLEX CAPITAL BUDGETING DECISIONS

(i) Project with different lives

(ii)Timing of investment

(iii)Replacement of an existing asset

(iv)Capital budgeting under inflation

(v)Capital rationing

Projects with Different Lives

So far we have considered investment decisions involving only choices among projects

with the same length of life, but project lives may differ. Will this affect our decision?

The answer is that it should not provide the proposals are independent. However, it will,

if the investment proposals being considered are mutually exclusive.

46

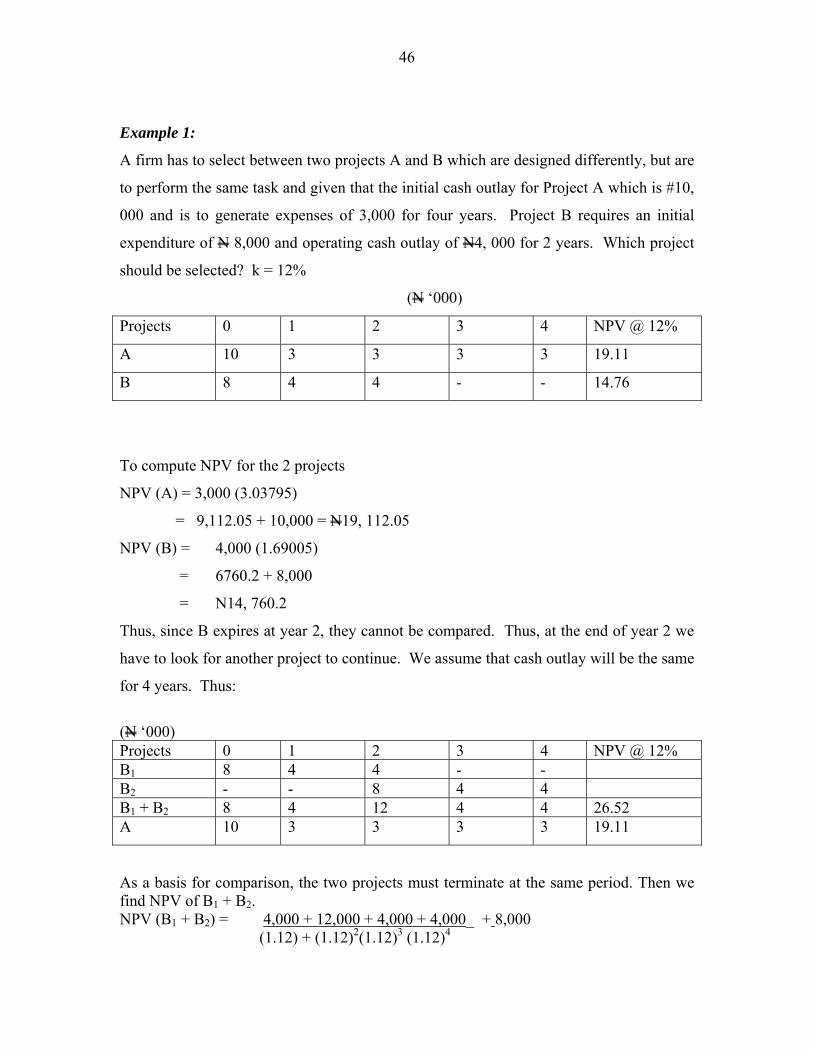

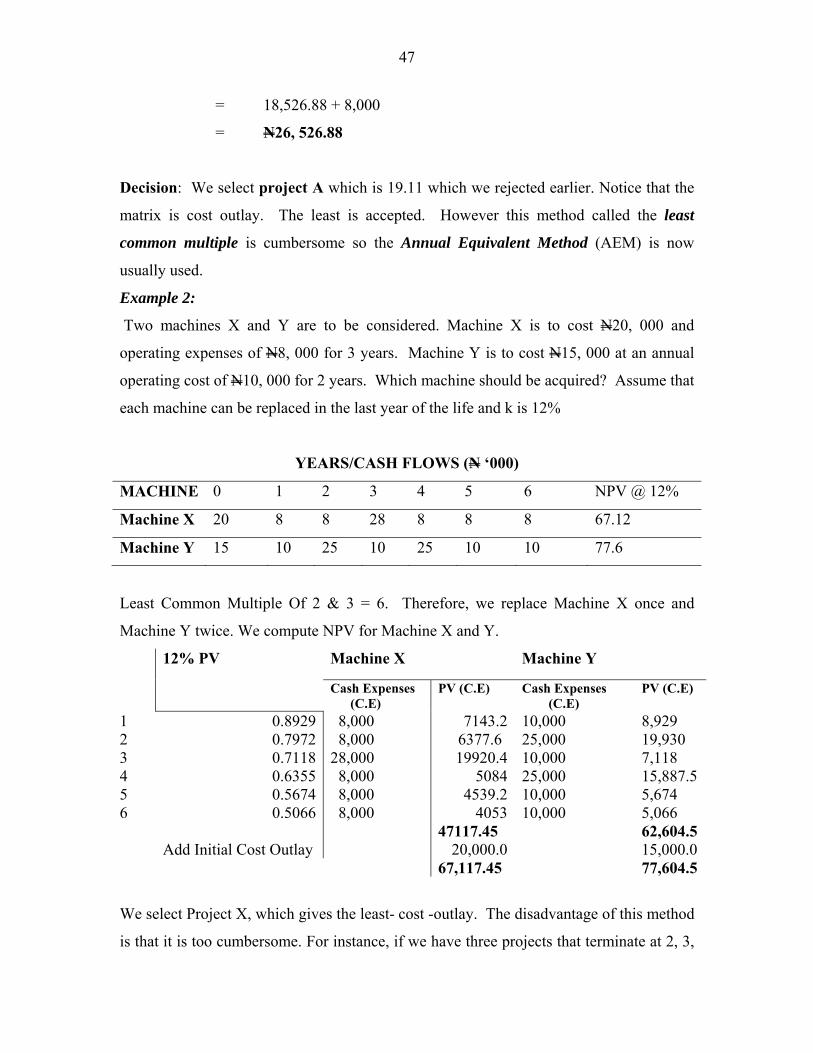

Example 1:

A firm has to select between two projects A and B which are designed differently, but are

to perform the same task and given that the initial cash outlay for Project A which is #10,

000 and is to generate expenses of 3,000 for four years. Project B requires an initial

expenditure of N 8,000 and operating cash outlay of N4, 000 for 2 years. Which project

should be selected? k = 12%

(N ‘000)

Projects 0 1 2 3 4 NPV @ 12%

A 10 3 3 3 3 19.11

B 8 4 4 - - 14.76

To compute NPV for the 2 projects

NPV (A) = 3,000 (3.03795)

= 9,112.05 + 10,000 = N19, 112.05

NPV (B) = 4,000 (1.69005)

= 6760.2 + 8,000

= N14, 760.2

Thus, since B expires at year 2, they cannot be compared. Thus, at the end of year 2 we

have to look for another project to continue. We assume that cash outlay will be the same

for 4 years. Thus:

(N ‘000) Projects 0 1 2 3 4 NPV @ 12% B1 8 4 4 - - B2 - - 8 4 4 B1 + B2 8 4 12 4 4 26.52 A 10 3 3 3 3 19.11

As a basis for comparison, the two projects must terminate at the same period. Then we find NPV of B1 + B2. NPV (B1 + B2) = 4,000 + 12,000 + 4,000 + 4,000_ + 8,000 (1.12) + (1.12)2(1.12)3 (1.12)4

47

= 18,526.88 + 8,000

= N26, 526.88

Decision: We select project A which is 19.11 which we rejected earlier. Notice that the

matrix is cost outlay. The least is accepted. However this method called the least

common multiple is cumbersome so the Annual Equivalent Method (AEM) is now

usually used.

Example 2:

Two machines X and Y are to be considered. Machine X is to cost N20, 000 and

operating expenses of N8, 000 for 3 years. Machine Y is to cost N15, 000 at an annual

operating cost of N10, 000 for 2 years. Which machine should be acquired? Assume that

each machine can be replaced in the last year of the life and k is 12%

YEARS/CASH FLOWS (N ‘000)

MACHINE 0 1 2 3 4 5 6 NPV @ 12%

Machine X 20 8 8 28 8 8 8 67.12

Machine Y 15 10 25 10 25 10 10 77.6

Least Common Multiple Of 2 & 3 = 6. Therefore, we replace Machine X once and

Machine Y twice. We compute NPV for Machine X and Y.

12% PV Machine X Machine Y

Cash Expenses (C.E)

PV (C.E) Cash Expenses (C.E)

PV (C.E)

1 0.8929 8,000 7143.2 10,000 8,929 2 0.7972 8,000 6377.6 25,000 19,930 3 0.7118 28,000 19920.4 10,000 7,118 4 0.6355 8,000 5084 25,000 15,887.5 5 0.5674 8,000 4539.2 10,000 5,674 6 0.5066 8,000 4053 10,000 5,066 47117.45 62,604.5 Add Initial Cost Outlay 20,000.0 15,000.0 67,117.45 77,604.5

We select Project X, which gives the least- cost -outlay. The disadvantage of this method

is that it is too cumbersome. For instance, if we have three projects that terminate at 2, 3,

48

and 5 years, the least common multiple will be 30 years. Therefore, the Annual

Equivalent Method is more preferred.

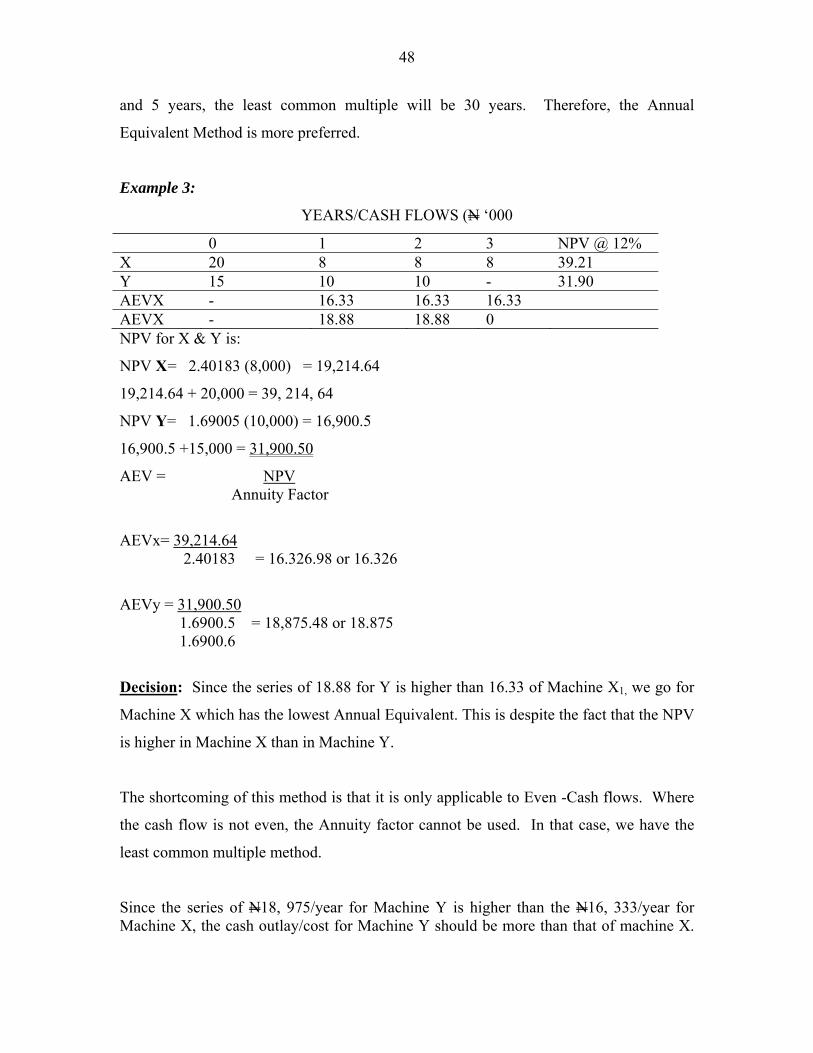

Example 3:

YEARS/CASH FLOWS (N ‘000

0 1 2 3 NPV @ 12% X 20 8 8 8 39.21 Y 15 10 10 - 31.90 AEVX - 16.33 16.33 16.33 AEVX - 18.88 18.88 0 NPV for X & Y is:

NPV X = 2.40183 (8,000) = 19,214.64

19,214.64 + 20,000 = 39, 214, 64

NPV Y= 1.69005 (10,000) = 16,900.5

16,900.5 +15,000 = 31,900.50

AEV = NPV Annuity Factor

AEVx= 39,214.64 2.40183 = 16.326.98 or 16.326

AEVy = 31,900.50 1.6900.5 = 18,875.48 or 18.875 1.6900.6

Decision: Since the series of 18.88 for Y is higher than 16.33 of Machine X1, we go for

Machine X which has the lowest Annual Equivalent. This is despite the fact that the NPV

is higher in Machine X than in Machine Y.

The shortcoming of this method is that it is only applicable to Even -Cash flows. Where

the cash flow is not even, the Annuity factor cannot be used. In that case, we have the

least common multiple method.

Since the series of N18, 975/year for Machine Y is higher than the N16, 333/year for Machine X, the cash outlay/cost for Machine Y should be more than that of machine X.

49

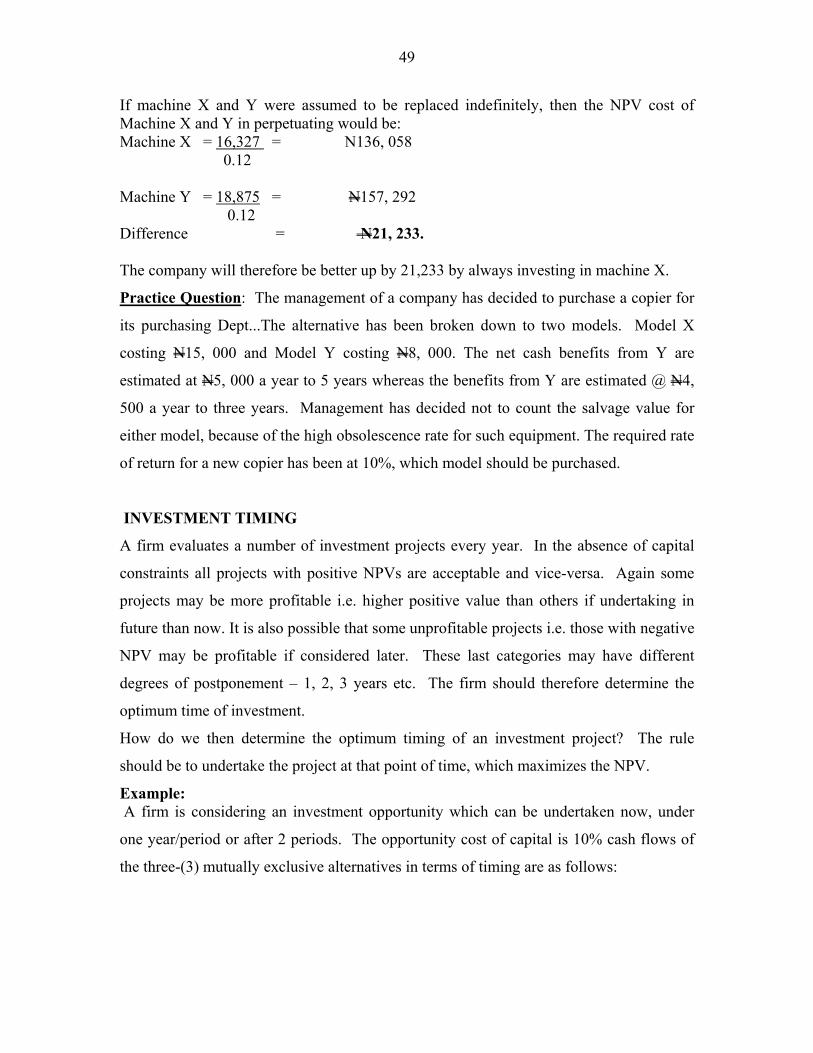

If machine X and Y were assumed to be replaced indefinitely, then the NPV cost of Machine X and Y in perpetuating would be: Machine X = 16,327 = N136, 058 0.12 Machine Y = 18,875 = N157, 292

0.12 Difference = N21, 233. The company will therefore be better up by 21,233 by always investing in machine X.

Practice Question: The management of a company has decided to purchase a copier for

its purchasing Dept...The alternative has been broken down to two models. Model X

costing N15, 000 and Model Y costing N8, 000. The net cash benefits from Y are

estimated at N5, 000 a year to 5 years whereas the benefits from Y are estimated @ N4,

500 a year to three years. Management has decided not to count the salvage value for

either model, because of the high obsolescence rate for such equipment. The required rate

of return for a new copier has been at 10%, which model should be purchased.

INVESTMENT TIMING

A firm evaluates a number of investment projects every year. In the absence of capital

constraints all projects with positive NPVs are acceptable and vice-versa. Again some

projects may be more profitable i.e. higher positive value than others if undertaking in

future than now. It is also possible that some unprofitable projects i.e. those with negative

NPV may be profitable if considered later. These last categories may have different

degrees of postponement – 1, 2, 3 years etc. The firm should therefore determine the

optimum time of investment.

How do we then determine the optimum timing of an investment project? The rule

should be to undertake the project at that point of time, which maximizes the NPV.

Example: A firm is considering an investment opportunity which can be undertaken now, under

one year/period or after 2 periods. The opportunity cost of capital is 10% cash flows of

the three-(3) mutually exclusive alternatives in terms of timing are as follows:

50

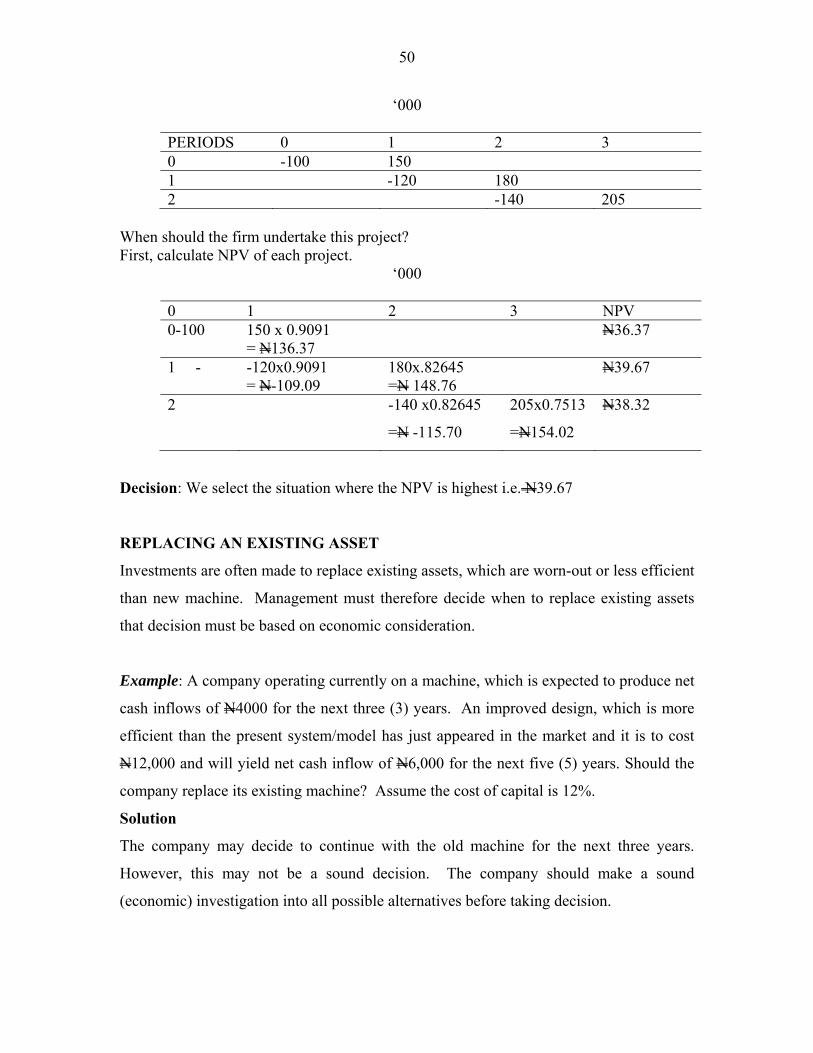

‘000

PERIODS 0 1 2 3 0 -100 150 1 -120 180 2 -140 205

When should the firm undertake this project? First, calculate NPV of each project.

‘000

0 1 2 3 NPV 0-100 150 x 0.9091

= N136.37 N36.37

1 - -120x0.9091 = N-109.09

180x.82645 =N 148.76

N39.67

2 -140 x0.82645

=N -115.70

205x0.7513

=N154.02

N38.32

Decision: We select the situation where the NPV is highest i.e. N39.67

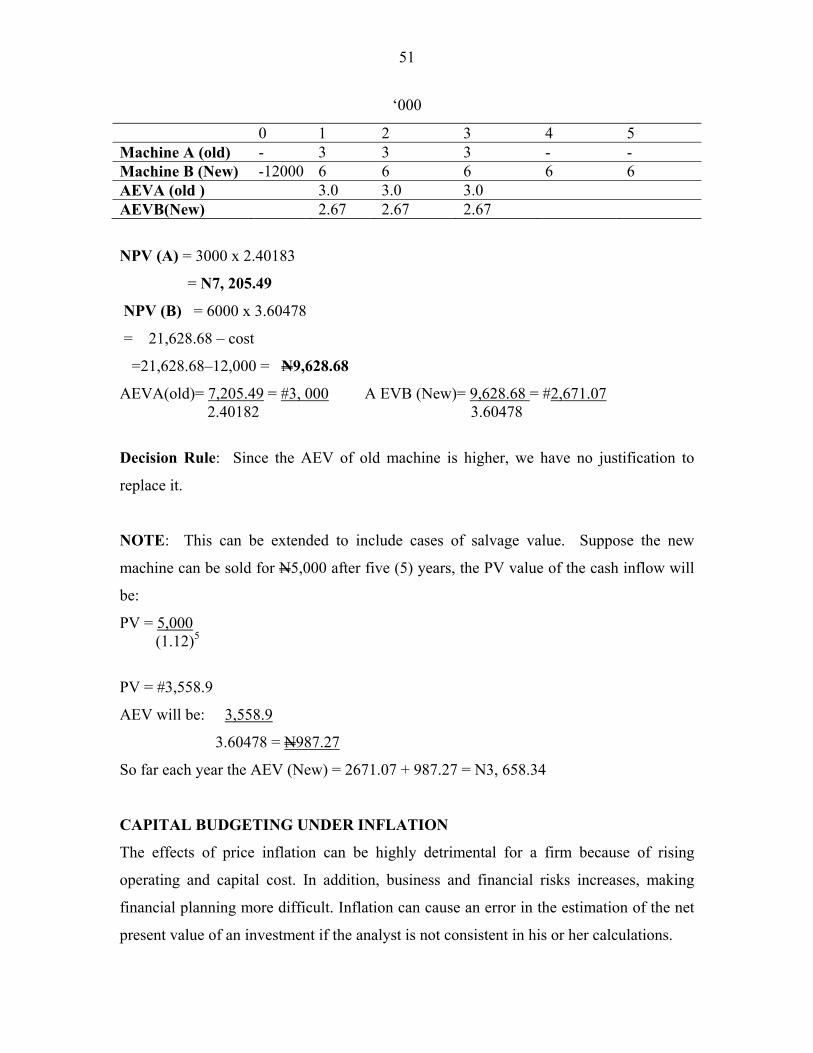

REPLACING AN EXISTING ASSET

Investments are often made to replace existing assets, which are worn-out or less efficient

than new machine. Management must therefore decide when to replace existing assets

that decision must be based on economic consideration.

Example: A company operating currently on a machine, which is expected to produce net

cash inflows of N4000 for the next three (3) years. An improved design, which is more

efficient than the present system/model has just appeared in the market and it is to cost

N12,000 and will yield net cash inflow of N6,000 for the next five (5) years. Should the

company replace its existing machine? Assume the cost of capital is 12%.

Solution

The company may decide to continue with the old machine for the next three years.

However, this may not be a sound decision. The company should make a sound

(economic) investigation into all possible alternatives before taking decision.

51

‘000

0 1 2 3 4 5 Machine A (old) - 3 3 3 - - Machine B (New) -12000 6 6 6 6 6 AEVA (old ) 3.0 3.0 3.0 AEVB(New) 2.67 2.67 2.67

NPV (A) = 3000 x 2.40183

= N7, 205.49

NPV (B) = 6000 x 3.60478

= 21,628.68 – cost

=21,628.68–12,000 = N9,628.68

AEVA(old)= 7,205.49 = #3, 000 A EVB (New)= 9,628.68 = #2,671.07 2.40182 3.60478

Decision Rule: Since the AEV of old machine is higher, we have no justification to

replace it.

NOTE: This can be extended to include cases of salvage value. Suppose the new

machine can be sold for N5,000 after five (5) years, the PV value of the cash inflow will

be:

PV = 5,000 (1.12)5

PV = #3,558.9

AEV will be: 3,558.9

3.60478 = N987.27

So far each year the AEV (New) = 2671.07 + 987.27 = N3, 658.34

CAPITAL BUDGETING UNDER INFLATION

The effects of price inflation can be highly detrimental for a firm because of rising

operating and capital cost. In addition, business and financial risks increases, making

financial planning more difficult. Inflation can cause an error in the estimation of the net

present value of an investment if the analyst is not consistent in his or her calculations.

52

Consistency requires that both the required rate of return and estimated cash flows of the

investment be stated in either “normal” terms or “real” terms. If the former are used, the

required rate of return will be based on current financing rates, which will include an

inflation component determined in the market. The required rate of return in this case is

not adjusted by the analyst to eliminate the effect of inflation cash flow also.

On the other hand, if real terms are used, both the required rate of return and the future

cash flows will have to be inflation- adjusted i.e. they will have to be reduced to eliminate

the effect of inflation.

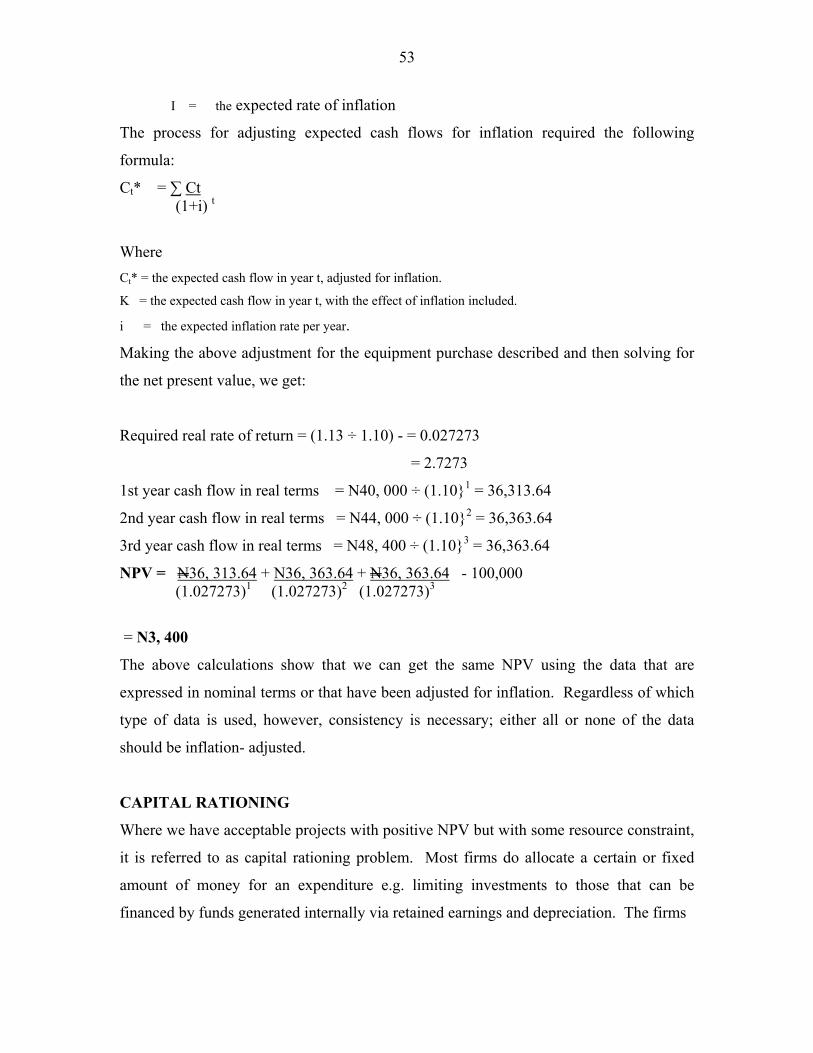

Example: Assume that a firm is considering the purchase new equipment, which is

expected to have following net cash flows:

YEAR 0 1 2 3

Cash flow N100,000 N40,000 N44,000 N48,400

The N100,000 outflow at time zero is the initial outlay. The future cash inflows are net

cash benefits from the investment that are estimated to increase annually at a 10%

because of inflation. Management sets a required rate of return on the equipment

purchased, based on the company’s current cost of capital. The net present value of the

project is:

NPV = N4,000 + N 44,000 + N48,000 - N100,000 = N3,400 (1.13)1 + (1.13)2 + (1.13)3

If real terms are used, both the required rate of return and the future cash flows will have

to be adjusted for inflation. The formula for adjusting the required return is:

K* = 1 + K - 1 1+i

Where

K* = the required rate of return adjusted for inflation

K = the required rate of return based on current capital costs

53

I = the expected rate of inflation

The process for adjusting expected cash flows for inflation required the following

formula:

Ct* = ∑ Ct

(1+i) t

Where

Ct* = the expected cash flow in year t, adjusted for inflation.

K = the expected cash flow in year t, with the effect of inflation included.

i = the expected inflation rate per year.

Making the above adjustment for the equipment purchase described and then solving for

the net present value, we get:

Required real rate of return = (1.13 ÷ 1.10) - = 0.027273

= 2.7273

1st year cash flow in real terms = N40, 000 ÷ (1.10}1 = 36,313.64

2nd year cash flow in real terms = N44, 000 ÷ (1.10}2 = 36,363.64

3rd year cash flow in real terms = N48, 400 ÷ (1.10}3 = 36,363.64

NPV = N36, 313.64 + N36, 363.64 + N36, 363.64 - 100,000 (1.027273)1 (1.027273)2 (1.027273)3

= N3, 400

The above calculations show that we can get the same NPV using the data that are

expressed in nominal terms or that have been adjusted for inflation. Regardless of which

type of data is used, however, consistency is necessary; either all or none of the data

should be inflation- adjusted.

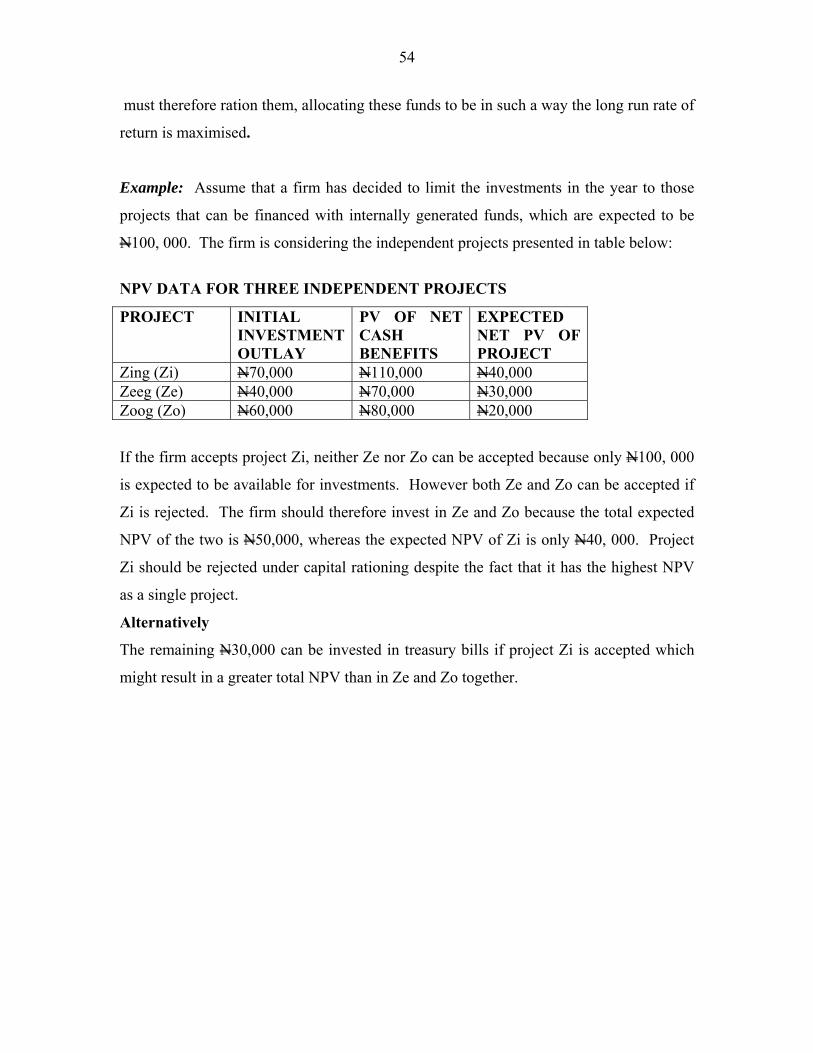

CAPITAL RATIONING

Where we have acceptable projects with positive NPV but with some resource constraint,

it is referred to as capital rationing problem. Most firms do allocate a certain or fixed

amount of money for an expenditure e.g. limiting investments to those that can be

financed by funds generated internally via retained earnings and depreciation. The firms

54

must therefore ration them, allocating these funds to be in such a way the long run rate of

return is maximised.

Example: Assume that a firm has decided to limit the investments in the year to those

projects that can be financed with internally generated funds, which are expected to be

N100, 000. The firm is considering the independent projects presented in table below:

NPV DATA FOR THREE INDEPENDENT PROJECTS

PROJECT INITIAL INVESTMENT OUTLAY

PV OF NET CASH BENEFITS

EXPECTED NET PV OF PROJECT

Zing (Zi) N70,000 N110,000 N40,000 Zeeg (Ze) N40,000 N70,000 N30,000 Zoog (Zo) N60,000 N80,000 N20,000

If the firm accepts project Zi, neither Ze nor Zo can be accepted because only N100, 000

is expected to be available for investments. However both Ze and Zo can be accepted if

Zi is rejected. The firm should therefore invest in Ze and Zo because the total expected

NPV of the two is N50,000, whereas the expected NPV of Zi is only N40, 000. Project

Zi should be rejected under capital rationing despite the fact that it has the highest NPV

as a single project.

Alternatively

The remaining N30,000 can be invested in treasury bills if project Zi is accepted which

might result in a greater total NPV than in Ze and Zo together.

55

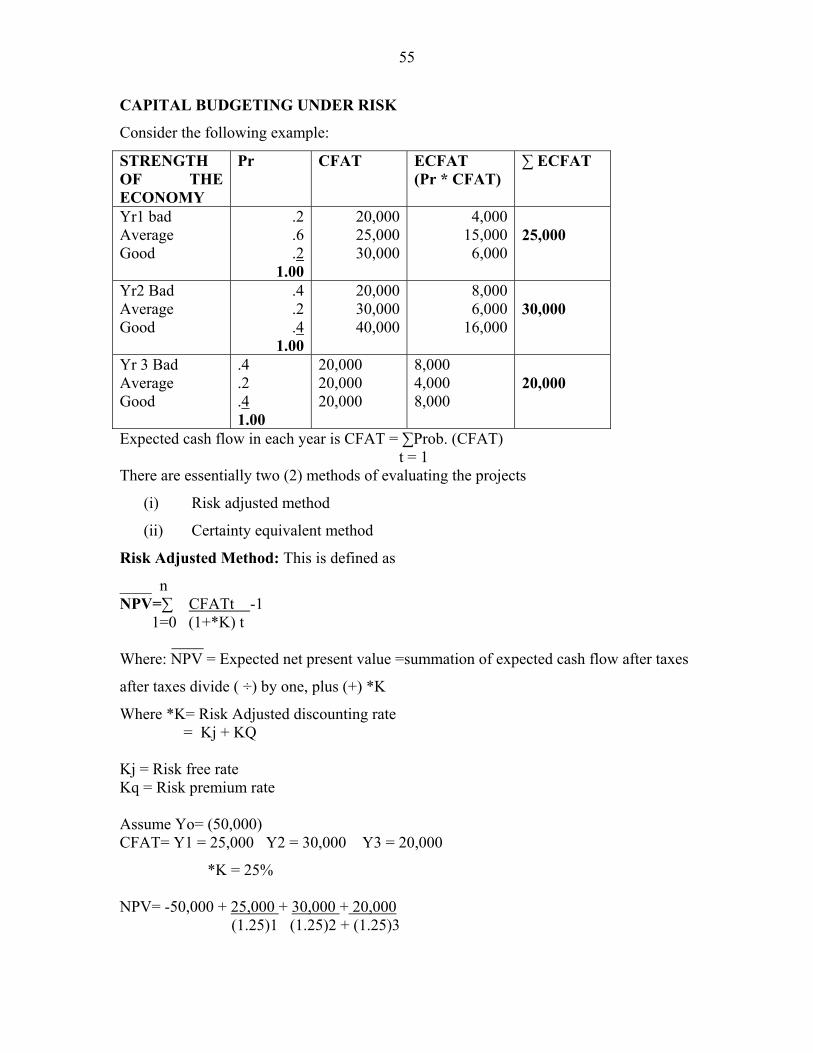

CAPITAL BUDGETING UNDER RISK

Consider the following example:

STRENGTH OF THE ECONOMY

Pr CFAT ECFAT (Pr * CFAT)

∑ ECFAT

Yr1 bad Average Good

.2

.6

.2 1.00

20,00025,00030,000

4,00015,0006,000

25,000

Yr2 Bad Average Good

.4

.2

.4 1.00

20,00030,00040,000

8,0006,000

16,000

30,000

Yr 3 Bad Average Good

.4

.2

.4 1.00

20,000 20,000 20,000

8,000 4,000 8,000

20,000

Expected cash flow in each year is CFAT = ∑Prob. (CFAT) t = 1 There are essentially two (2) methods of evaluating the projects

(i) Risk adjusted method

(ii) Certainty equivalent method

Risk Adjusted Method: This is defined as

____ n NPV=∑ CFATt -1 1=0 (1+*K) t ____ Where: NPV = Expected net present value =summation of expected cash flow after taxes

after taxes divide ( ÷) by one, plus (+) *K

Where *K= Risk Adjusted discounting rate = Kj + KQ Kj = Risk free rate Kq = Risk premium rate Assume Yo= (50,000) CFAT= Y1 = 25,000 Y2 = 30,000 Y3 = 20,000

*K = 25% NPV= -50,000 + 25,000 + 30,000 + 20,000 (1.25)1 (1.25)2 + (1.25)3

56

= (50,000) + 25,000 (0.8) + 30,000 (0.64) + 20,000 (0.512) = (50,000) + 20,000 + 19,200 + 10,240 = -560 or (560) This technique is found to be useful and has the following merit.

(i) Simple to calculate

(ii) It has a great deal of intuitive appeal for risk- adverse investors.

Demerits:

(i) No easy way to arrive at a risk adjusted discounting rate. The risk free is already

known. It is the risk rate that is difficult t determine.

(ii) It does not make any risk adjustment in the numerator.

(iii) It is based on the assumption that all investors are risk- averse – some are risk-

seekers.