Embed Size (px)

Citation preview

1

Mortgage Risk Management

Blackwell, Griffiths and WintersChapter 14 and other material

2

Learning Objectives

1. Understand the primary risks of mortgages

2. Understand the process of securitization in the mortgage markets

3. Understand mortgage-backed securities (MBS)

4. Understand interest-rate risk management in the mortgage market

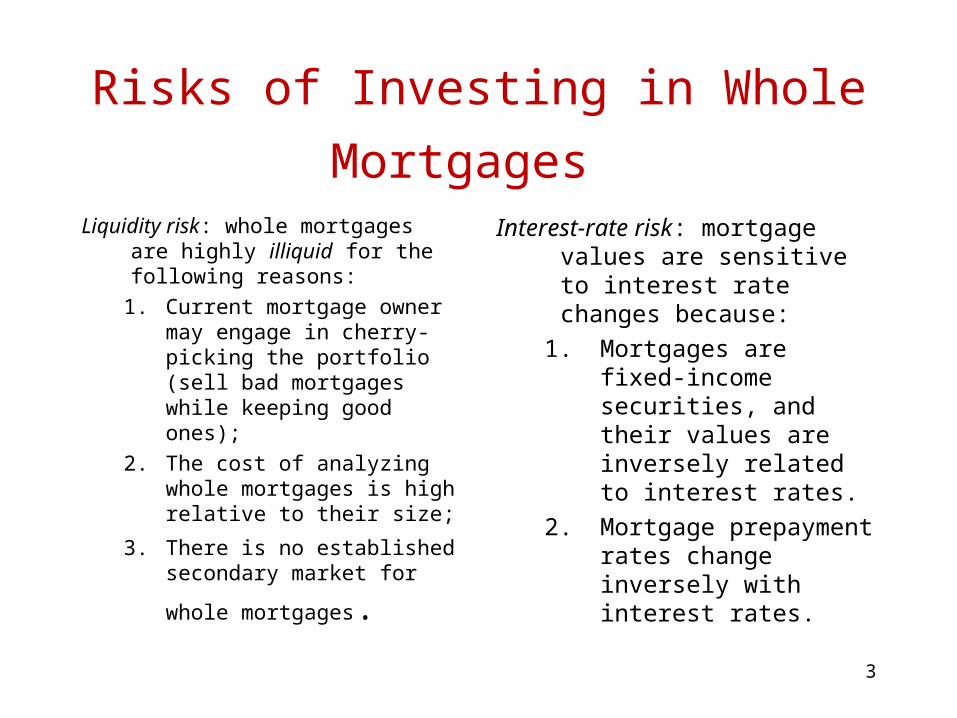

Risks of Investing in Whole Mortgages Liquidity risk: whole mortgages are

highly illiquid for the following reasons:

1. Current mortgage owner may engage in cherry-picking the portfolio (sell bad mortgages while keeping good ones);

2. The cost of analyzing whole mortgages is high relative to their size;

3. There is no established secondary market for whole

mortgages.

Interest-rate risk: mortgage values are sensitive to interest rate changes because:

1. Mortgages are fixed-income securities, and their values are inversely related to interest rates.

2. Mortgage prepayment rates change inversely with interest rates.

3

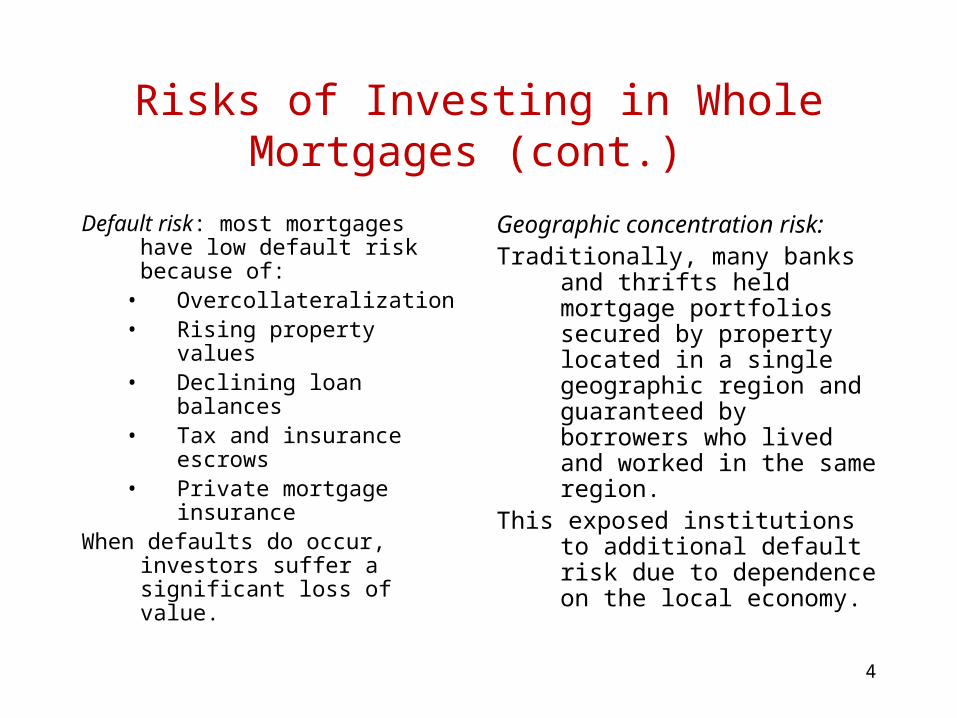

Risks of Investing in Whole Mortgages (cont.)

Default risk: most mortgages have low default risk because of:

• Overcollateralization• Rising property values• Declining loan balances• Tax and insurance escrows • Private mortgage insurance

When defaults do occur, investors suffer a significant loss of value.

Geographic concentration risk:Traditionally, many banks and thrifts

held mortgage portfolios secured by property located in a single geographic region and guaranteed by borrowers who lived and worked in the same region.

This exposed institutions to additional default risk due to dependence on the local economy.

4

5

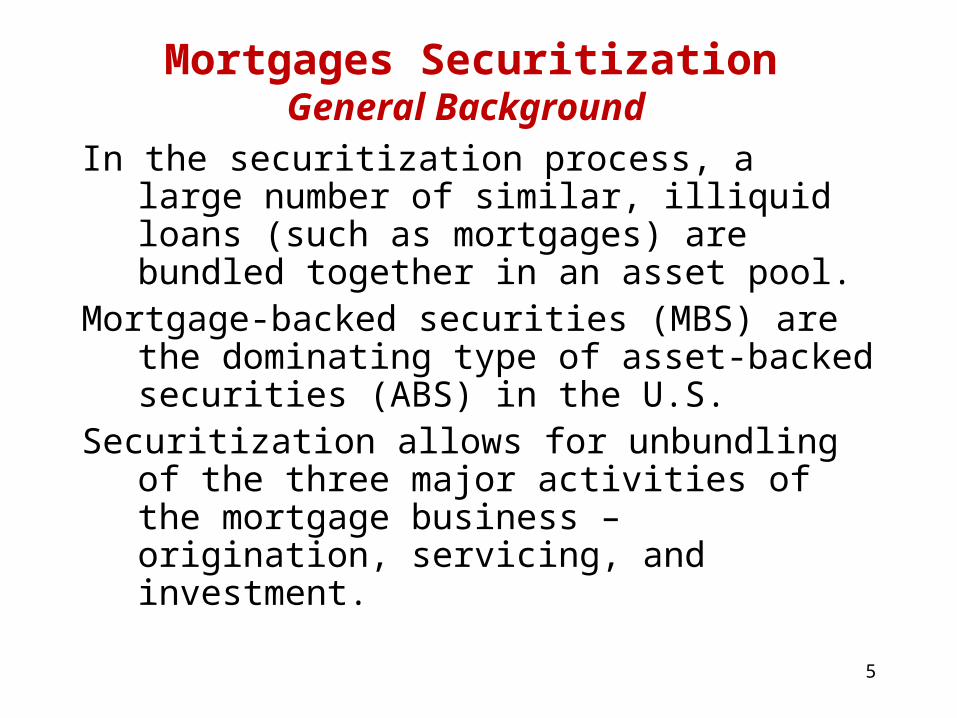

Mortgages SecuritizationGeneral Background

In the securitization process, a large number of similar, illiquid loans (such as mortgages) are bundled together in an asset pool.

Mortgage-backed securities (MBS) are the dominating type of asset-backed securities (ABS) in the U.S.

Securitization allows for unbundling of the three major activities of the mortgage business – origination, servicing, and investment.

6

Mortgages SecuritizationSteps in Creating a Mortgage Pool

- The institution that intends to issue MBS assembles a pool of relatively similar mortgages (e.g., in terms of maturity and coupon rate);

- A trustee is hired to verify the existence of the mortgages and to ensure that they are not sold after the MBS are issued;

- The pool is insured by a third party;- The responsibility for servicing the mortgage is

transferred to an independent servicer; - MBS are issued and sold to investors.

7

Mortgages Securitization Mortgage Servicing

Responsibilities of the servicer:1) Collecting payments from borrowers and

transferring those funds to the mortgage pool;2) Collecting taxes and insurance escrow payments; 3) Interacting with borrowers, answering questions and

resolving problems;4) Pursuing delinquent payments and forcing

foreclosure in the case of default;Servicing business has become highly automated; it is

characterized by economies-of-scale. Servicer may have little incentive to provide high quality

services to the borrower.

8

Mortgages Securitization The Mortgage-Backed Security

The issuer starts with the expected cash flows of the pool and sets the rules that govern how these cash flows will be distributed among investors.

The goal of the MBS issuer is to create a set of securities that have the highest possible value to investors.

The issuer’s profit comes from selling the MBS for more money than was spent to assemble the pool, design the MBS, and market them to investors.

MBS are owned by various investors.

9

MBS Issuers Ginnie Mae (GNMA) provides guarantees against

default losses for mortgages that are used to back privately issued MBS.

Fannie Mae (FNMA) and Freddie Mac (FHLMC) are largest issuers of MBS.

Ginnie, Fannie, and Freddie are agencies that were established to create and develop the secondary market in mortgages. They hold or insure about $4.1 trillion in mortgages, almost 44% of the market.

MBS backed by mortgages that do not conform to agency standards offer higher returns than those issued or insured by the agencies.

10

MBS Secondary Market

- OTC market;- Many MBS are held as long-term

investments and rarely trade;- When comparing ask prices, it is important to

recognize that different dealers may be quoting prices for different securities.

11

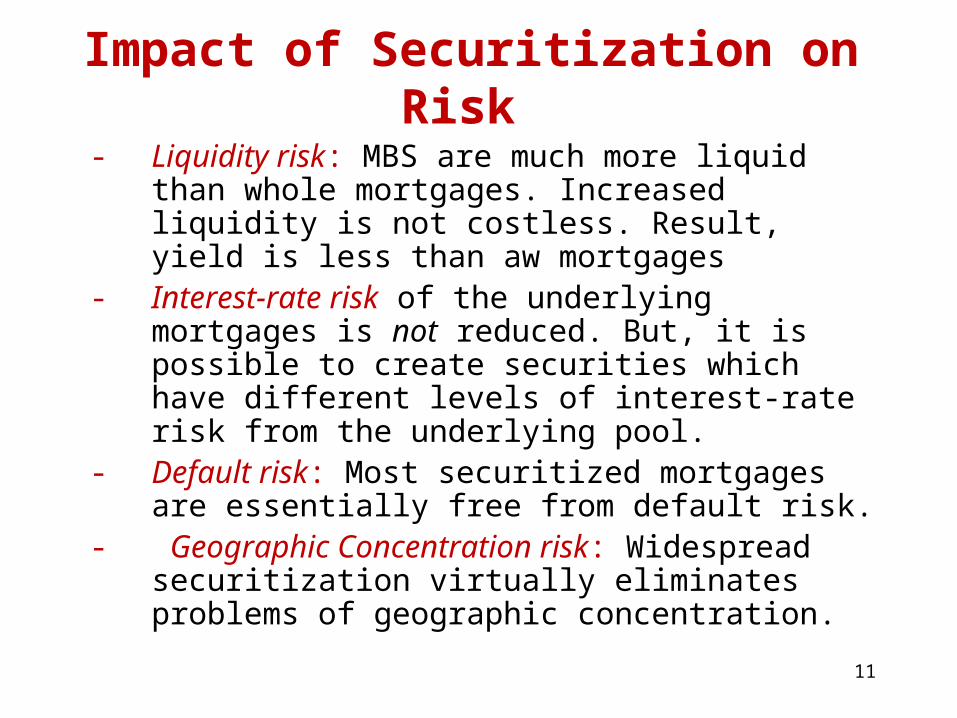

Impact of Securitization on Risk

- Liquidity risk: MBS are much more liquid than whole mortgages. Increased liquidity is not costless. Result, yield is less than aw mortgages

- Interest-rate risk of the underlying mortgages is not reduced. But, it is possible to create securities which have different levels of interest-rate risk from the underlying pool.

- Default risk: Most securitized mortgages are essentially free from default risk.

- Geographic Concentration risk: Widespread securitization virtually eliminates problems of geographic concentration.

12

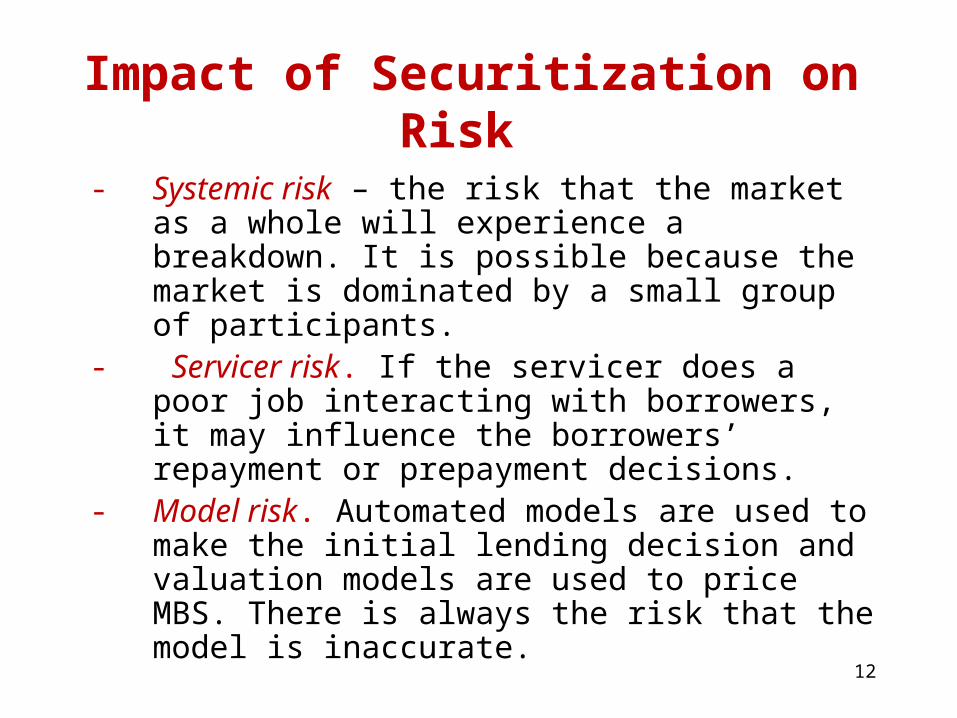

Impact of Securitization on Risk

- Systemic risk – the risk that the market as a whole will experience a breakdown. It is possible because the market is dominated by a small group of participants.

- Servicer risk. If the servicer does a poor job interacting with borrowers, it may influence the borrowers’ repayment or prepayment decisions.

- Model risk. Automated models are used to make the initial lending decision and valuation models are used to price MBS. There is always the risk that the model is inaccurate.

13

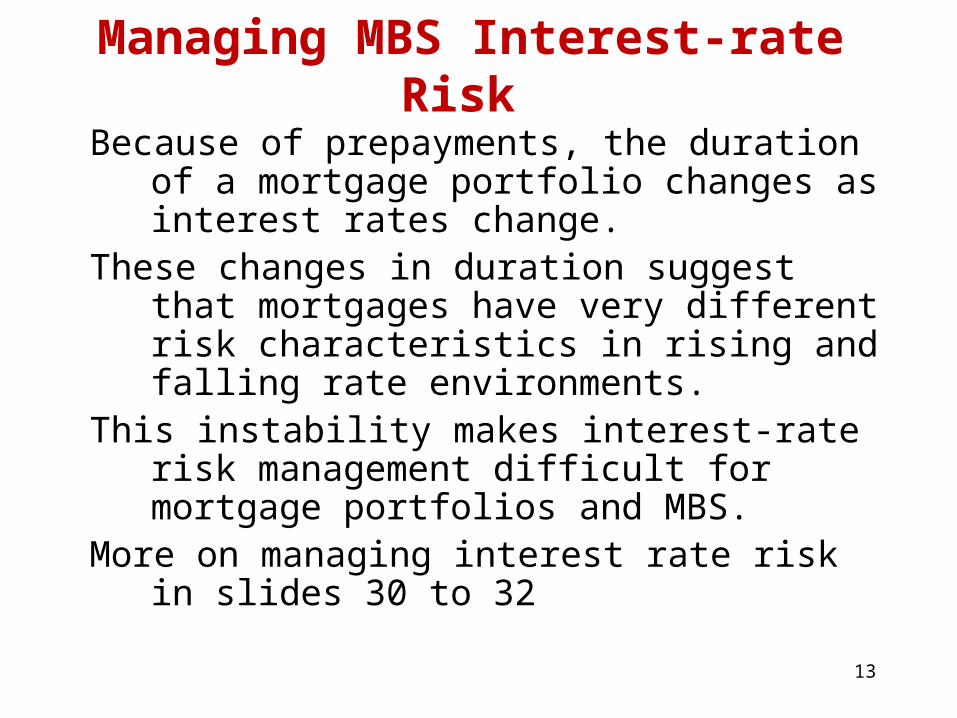

Managing MBS Interest-rate Risk

Because of prepayments, the duration of a mortgage portfolio changes as interest rates change.

These changes in duration suggest that mortgages have very different risk characteristics in rising and falling rate environments.

This instability makes interest-rate risk management difficult for mortgage portfolios and MBS.

More on managing interest rate risk in slides 30 to 32

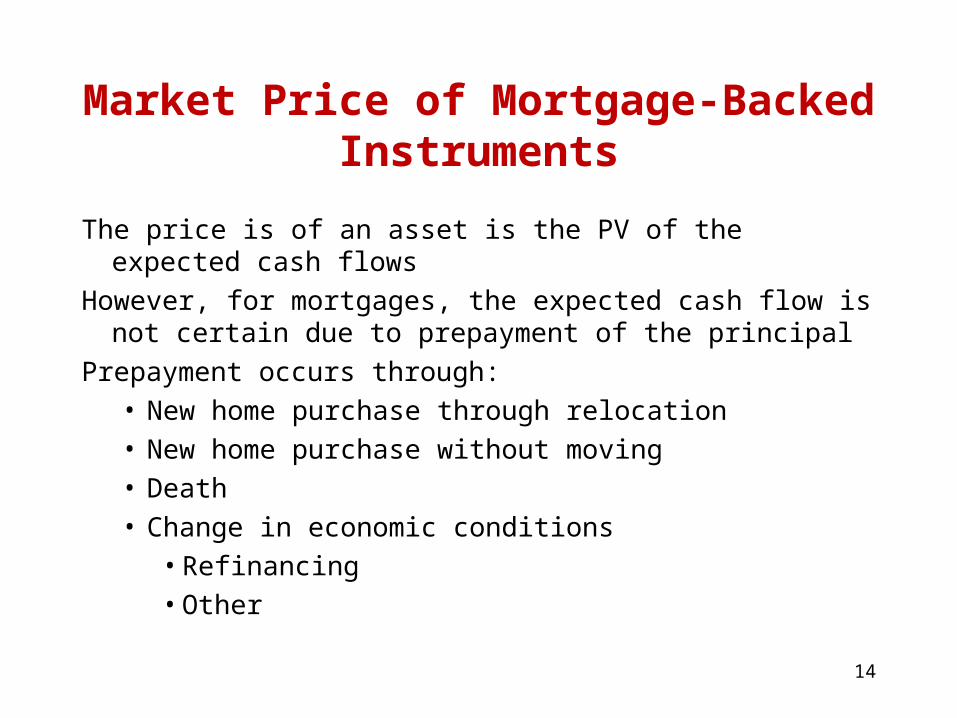

Market Price of Mortgage-Backed Instruments

The price is of an asset is the PV of the expected cash flows

However, for mortgages, the expected cash flow is not certain due to prepayment of the principal

Prepayment occurs through:

• New home purchase through relocation

• New home purchase without moving

• Death

• Change in economic conditions

• Refinancing

• Other14

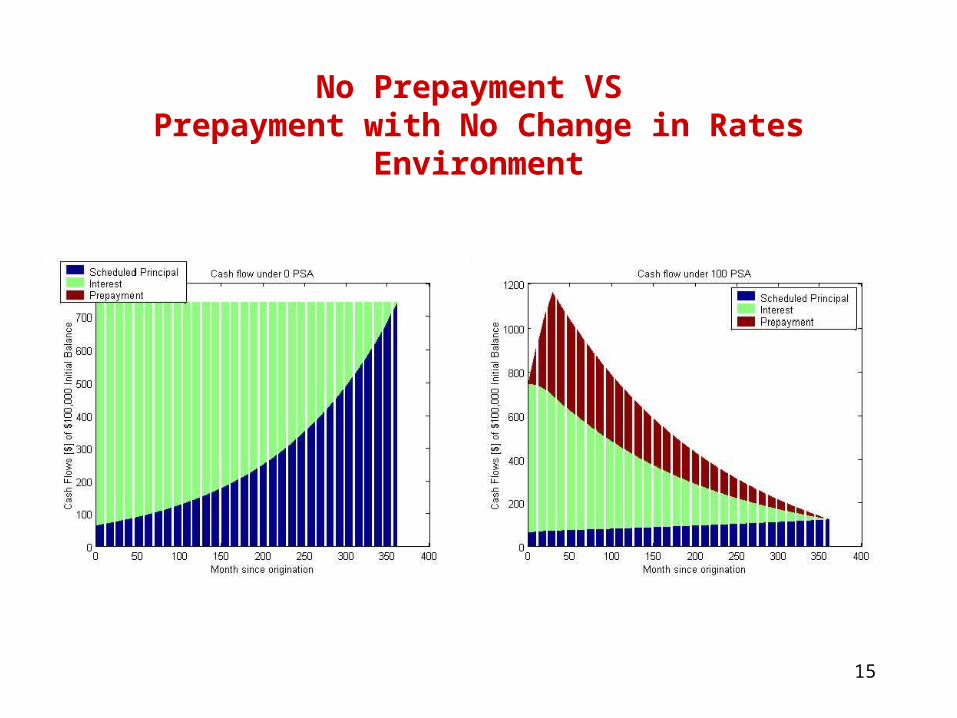

No Prepayment VS Prepayment with No Change in Rates Environment

15

Estimating Prepayments and The Conditional Cash Flow in a MBS

Suppose that

• A $250 million pool of mortgage is assembled and a MBS is issued against those mortgages

• Suppose that the average rate on the mortgage in that pool is around 8%

16

Effect of interest rate changes on the conditional cash flow

• If interest rates should rise above 8%, individuals will prepay the pool of mortgages slower; and it will take longer for the mortgages to be fully paid

• If interest rates should fall below 8%, the prepayment will speed up; and the mortgages will be fuller paid sooner

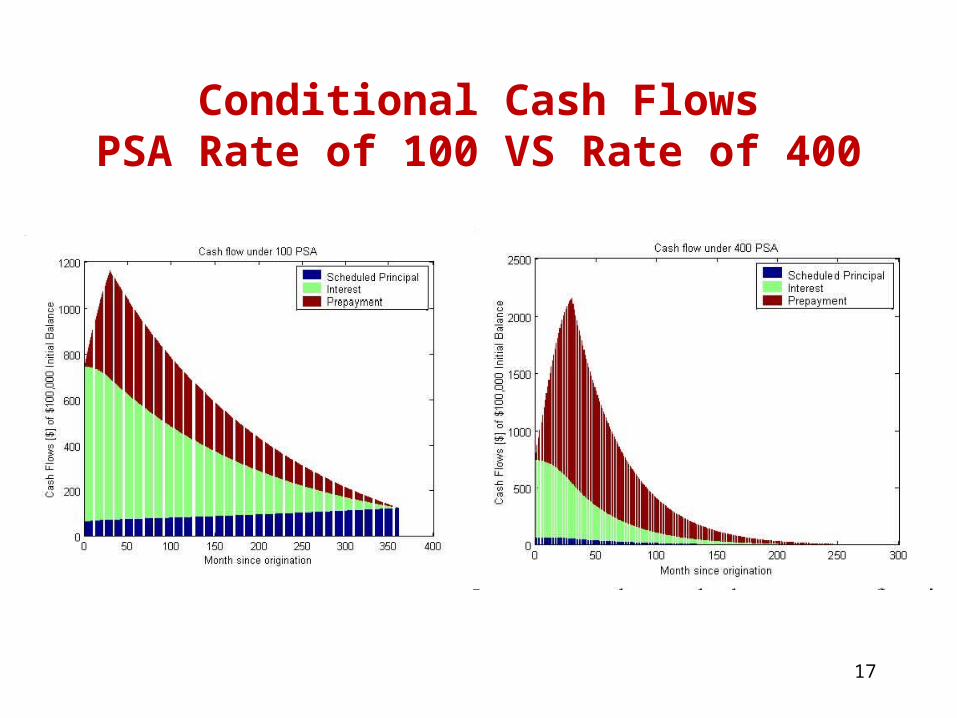

Conditional Cash FlowsPSA Rate of 100 VS Rate of 400

17

Effects of Changes in Interest Rates

The principal takes longer to pay if current mortgage rates are higher than the average rate on the mortgages in the pool

• The higher the rate the slower the payoff

• Effect is for periodic cash flow to last longer, the higher are mortgage rates

The principal pays off faster, if the current mortgage rate is lower than the average rate on the pool

• The lower the rate, the faster the payoff

• Effect is for periodic cash flow to end sooner, the lower are mortgage rates

• If rates far far enough fast enough, the cash flow could disappear so fast that the value of the bond falls as interest rates fall

18

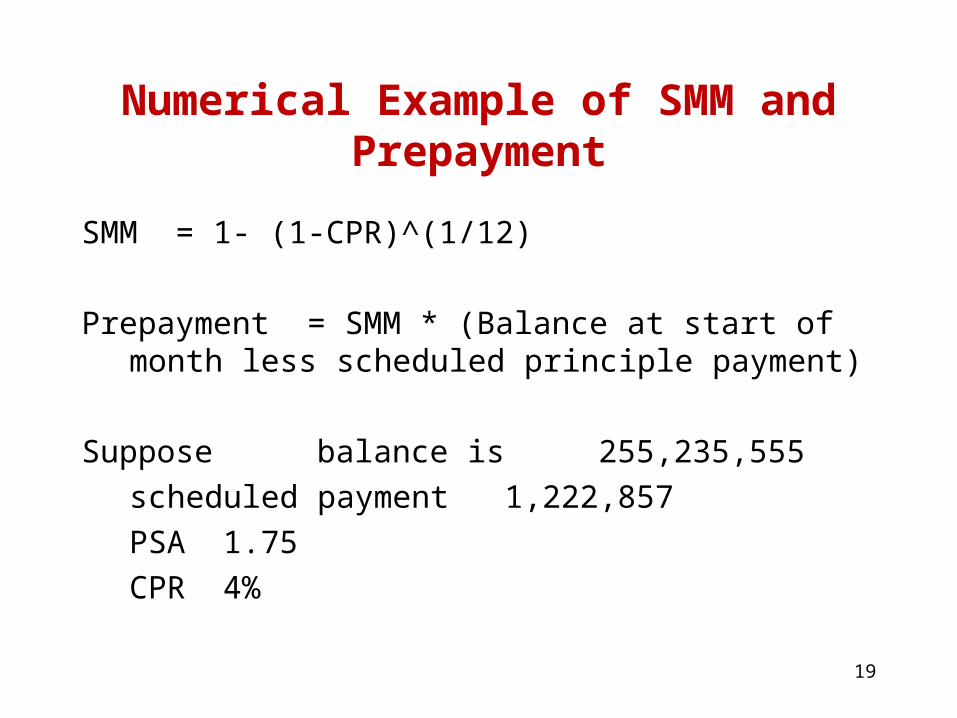

Numerical Example of SMM and Prepayment

SMM = 1- (1-CPR)^(1/12)

Prepayment = SMM * (Balance at start of month less scheduled principle payment)

Suppose balance is 255,235,555

scheduled payment 1,222,857

PSA 1.75

CPR 4%

19

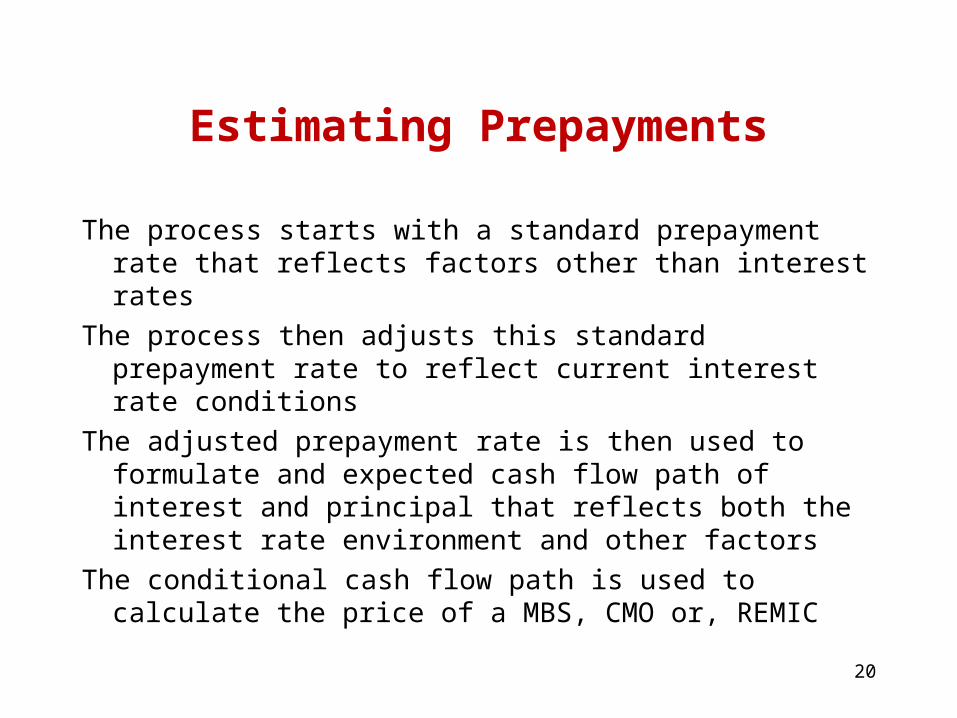

Estimating Prepayments

The process starts with a standard prepayment rate that reflects factors other than interest rates

The process then adjusts this standard prepayment rate to reflect current interest rate conditions

The adjusted prepayment rate is then used to formulate and expected cash flow path of interest and principal that reflects both the interest rate environment and other factors

The conditional cash flow path is used to calculate the price of a MBS, CMO or, REMIC

20

21

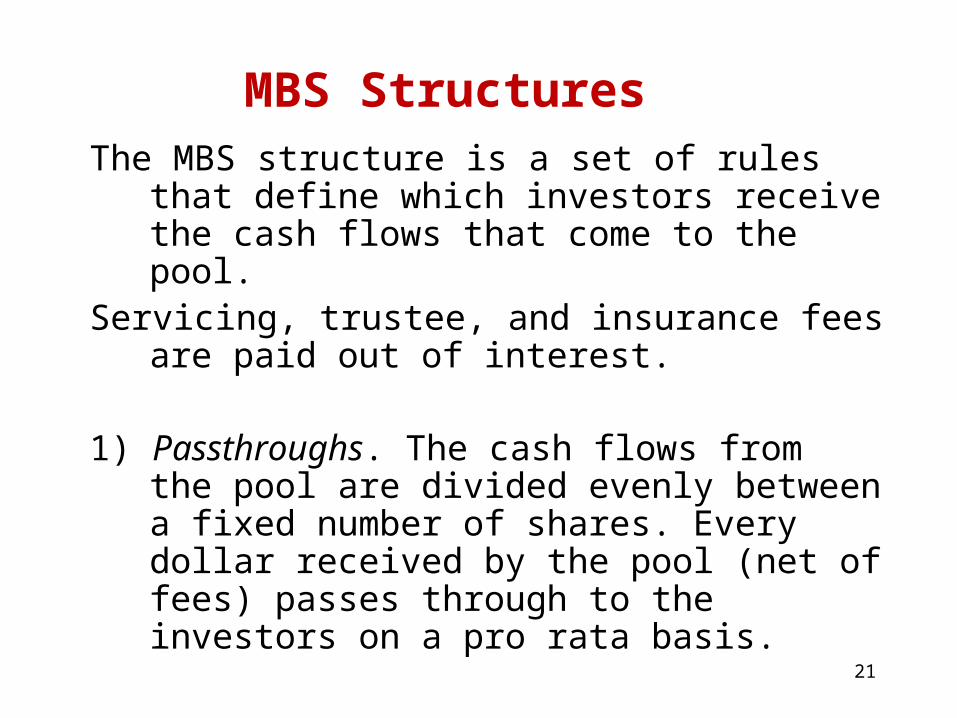

MBS Structures

The MBS structure is a set of rules that define which investors receive the cash flows that come to the pool.

Servicing, trustee, and insurance fees are paid out of interest.

1) Passthroughs. The cash flows from the pool are divided evenly between a fixed number of shares. Every dollar received by the pool (net of fees) passes through to the investors on a pro rata basis.

22

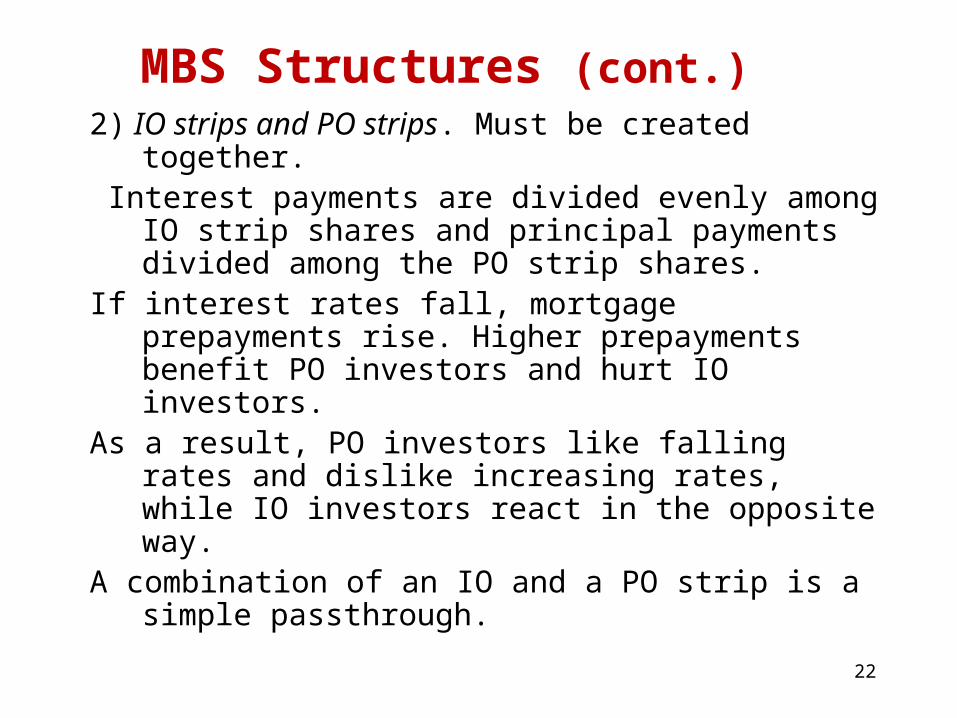

MBS Structures (cont.) 2) IO strips and PO strips. Must be created together. Interest payments are divided evenly among IO strip

shares and principal payments divided among the PO strip shares.

If interest rates fall, mortgage prepayments rise. Higher prepayments benefit PO investors and hurt IO investors.

As a result, PO investors like falling rates and dislike increasing rates, while IO investors react in the opposite way.

A combination of an IO and a PO strip is a simple passthrough.

23

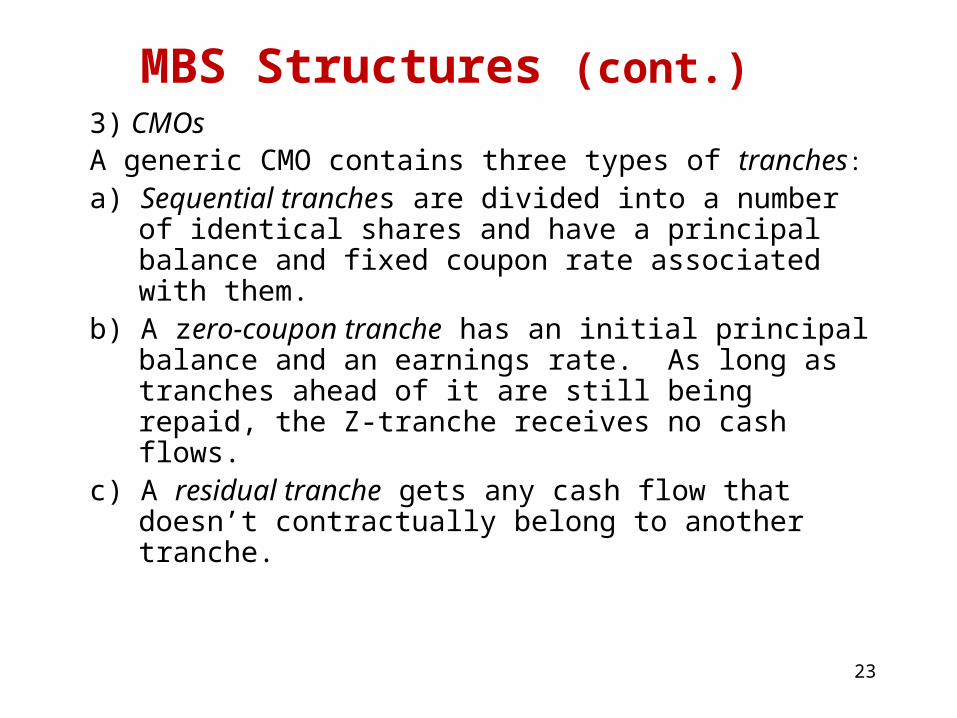

MBS Structures (cont.) 3) CMOs A generic CMO contains three types of tranches:

a) Sequential tranches are divided into a number of identical shares and have a principal balance and fixed coupon rate associated with them.

b) A zero-coupon tranche has an initial principal balance and an earnings rate. As long as tranches ahead of it are still being repaid, the Z-tranche receives no cash flows.

c) A residual tranche gets any cash flow that doesn’t contractually belong to another tranche.

24

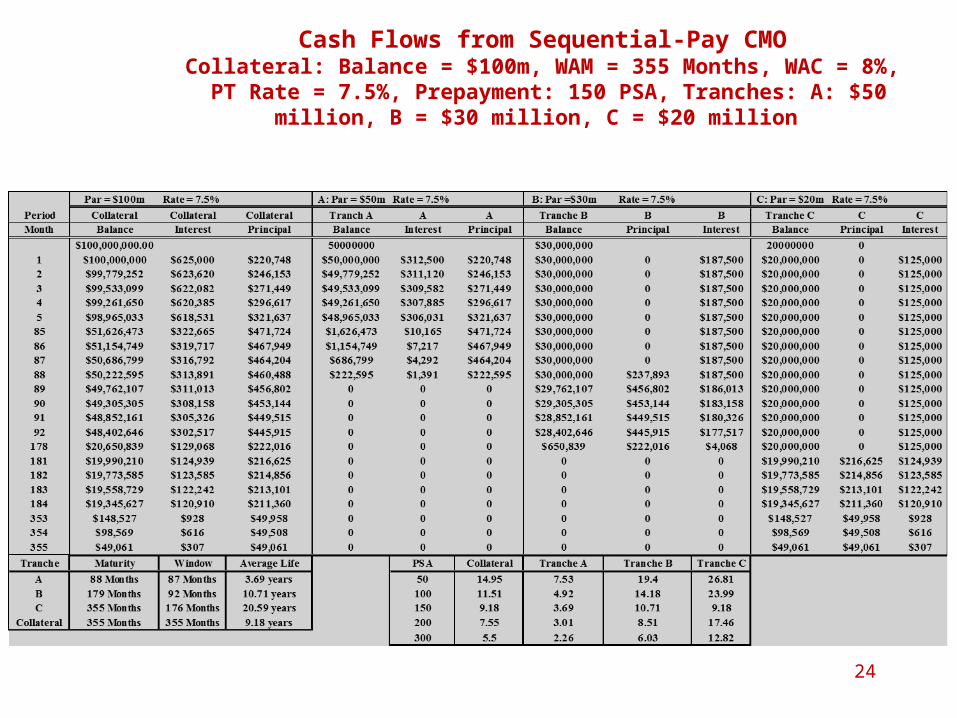

Cash Flows from Sequential-Pay CMOCollateral: Balance = $100m, WAM = 355 Months, WAC = 8%, PT Rate = 7.5%, Prepayment: 150 PSA, Tranches: A: $50 million, B = $30 million, C =

$20 million

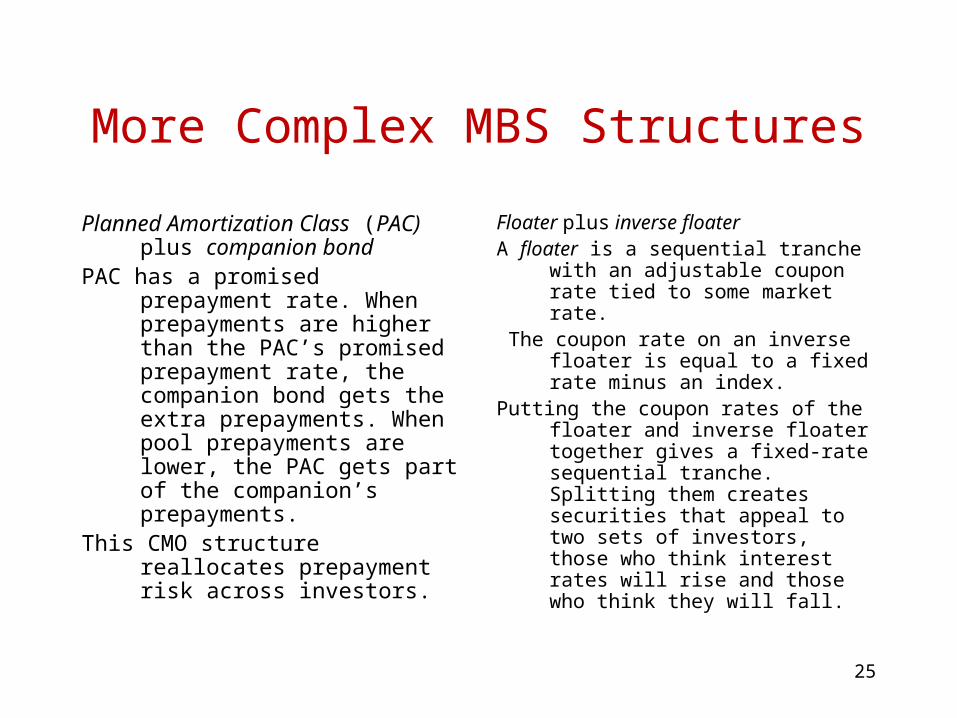

More Complex MBS Structures

Planned Amortization Class (PAC) plus companion bond

PAC has a promised prepayment rate. When prepayments are higher than the PAC’s promised prepayment rate, the companion bond gets the extra prepayments. When pool prepayments are lower, the PAC gets part of the companion’s prepayments.

This CMO structure reallocates prepayment risk across investors.

Floater plus inverse floaterA floater is a sequential tranche with

an adjustable coupon rate tied to some market rate.

The coupon rate on an inverse floater is equal to a fixed rate minus an index.

Putting the coupon rates of the floater and inverse floater together gives a fixed-rate sequential tranche. Splitting them creates securities that appeal to two sets of investors, those who think interest rates will rise and those who think they will fall.

25

Prepayments and MBSs, CMOs, and REMICs

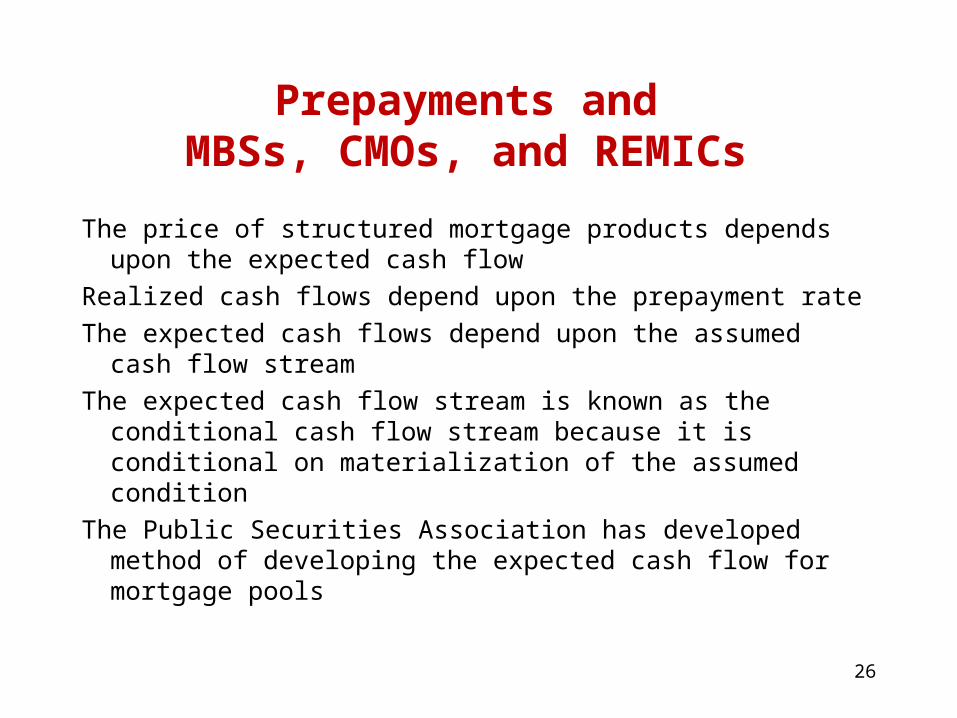

The price of structured mortgage products depends upon the expected cash flow

Realized cash flows depend upon the prepayment rate

The expected cash flows depend upon the assumed cash flow stream

The expected cash flow stream is known as the conditional cash flow stream because it is conditional on materialization of the assumed condition

The Public Securities Association has developed method of developing the expected cash flow for mortgage pools

26

More Complex Structured SecuritiesCollateralized Debt and Loan Obligation

A type of asset backed security in which a special purpose vehicle owns a portfolio of wide variety of fixed-income assets

The SPV issues bonds to pay for these assets

These bonds have a ratings depending upon their claim against the cash flow from the vehicle’s assets

• senior tranches (AAA)

• mezzanine tranches (AA to BB)

• equity tranches (unrated)

Losses are applied in reverse order of seniority

• junior tranches offer higher coupons to compensate for the higher default risk

27

More Complex Structured SecuritiesOther Collateralized Obligation

Collateralized Bond Obligations (CBO)

Collateralized Loan Obligation (CLO)

Collateralized Debt Obligations (CDO)

Collateralized Fund Obligations (CFO)

These are similar in structure, except that the holdings of each SPV each is limited to the type of assets in its name

CDOs, in contrast, can hold almost any type of debt as an asset in the SPV

28

Credit Enhancements to Private MBS

Subordination or credit tranching

Over collateralization

Excess spread

External Enhancements

Surety Bond

Wrapped security – a security insured by a third party

LOC

Cash collateral

29

30

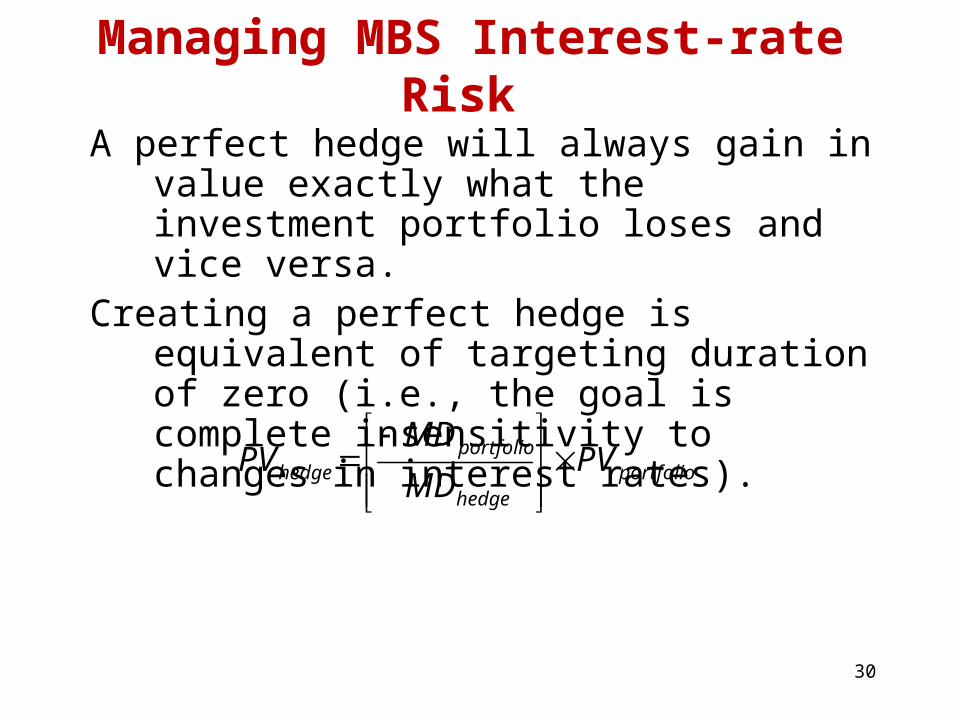

Managing MBS Interest-rate Risk

A perfect hedge will always gain in value exactly what the investment portfolio loses and vice versa.

Creating a perfect hedge is equivalent of targeting duration of zero (i.e., the goal is complete insensitivity to changes in interest rates).

portfoliohedge

portfoliohedge PV

MD

MDPV

31

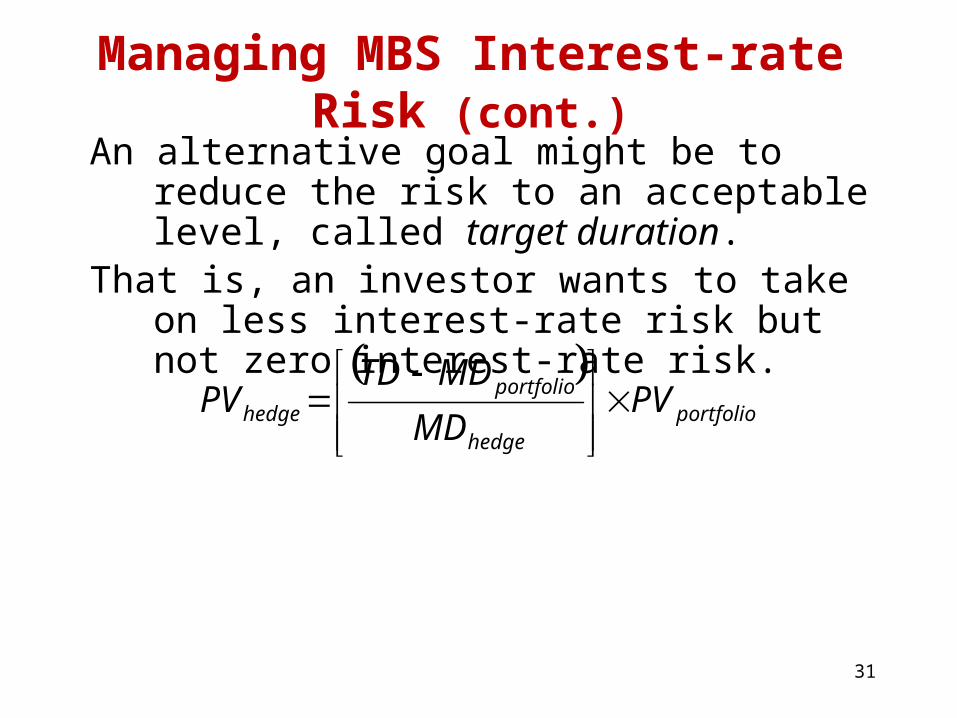

Managing MBS Interest-rate Risk (cont.)

An alternative goal might be to reduce the risk to an acceptable level, called target duration.

That is, an investor wants to take on less interest-rate risk but not zero interest-rate risk.

portfolio

hedge

portfoliohedge PV

MD

MDTDPV

32

Managing MBS Interest-rate Risk (cont.)

Hedging MBS with Treasury forwardswith Optionswith Treasury Futures

Preference is for Treasury futures

Duration of Treasury bond is calculated the same as the duration of a bond in the cash market

Most MBS have a positive duration and the investor will need a short position to neutralize interest rate (price ) risk.

Because the correct hedge amount will change with interest rates, this is a dynamic hedge.

In contrast, a static hedge does not need to be adjusted as interest rates change.

33

Basis Risk Basis risk is a possibility of the price of the risky

security (an MBS) and the value of the hedge changing in an unexpected way.

When hedges are designed, the assumption generally made is that changes in the value of the hedge will exactly offset changes in the value of the risky security.

There may be a time when a risky security loses value and the hedge position doesn’t gain enough to make up for the loss.

No hedge is perfect!