Embed Size (px)

Citation preview

1

Overheads

2

Overheads

Overhead includes a large number of types of indirect costs

Direct cost are identifiable to cost units, but overhead which are often considerable, cannot be related directly to cost units

3

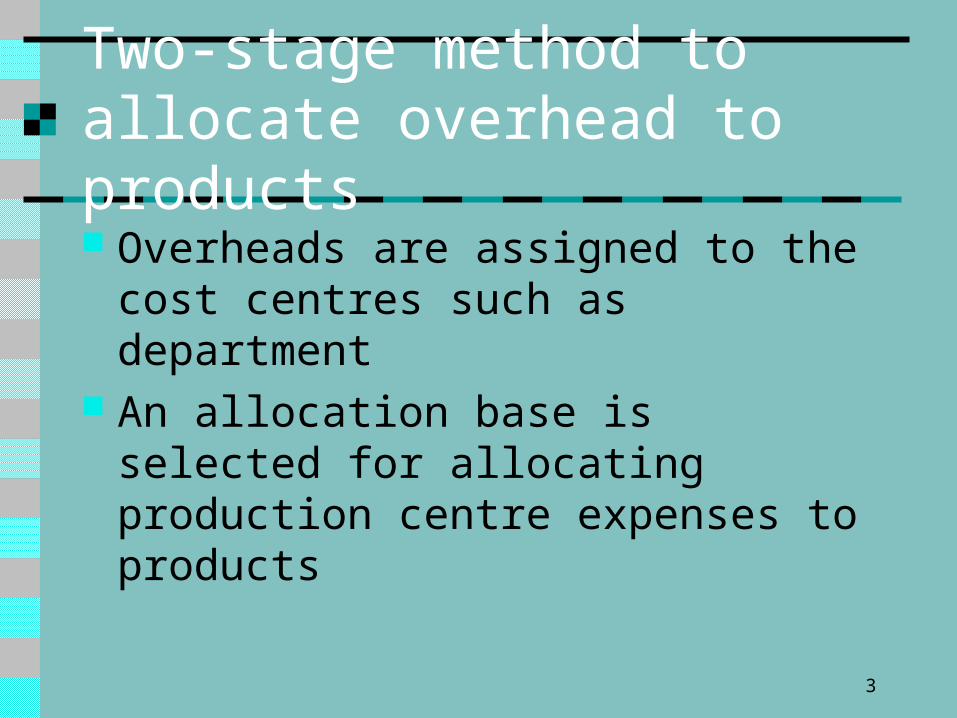

Two-stage method to allocate overhead to products Overheads are assigned to the cost centres

such as department An allocation base is selected for allocating

production centre expenses to products

4

Procedures of overhead allocation to product Assign all factory overheads to cost centres Reallocate service-centre overheads to

production cost centres Calculate separate overhead absorption rate

for each cost centre Assign cost-centre overhead to products

5

Assign all factory overheads to cost center

6

Assign all factory overhead to cost centres Cost allocation Cost apportionment

7

Cost allocation

Where a cost can be clearly identified with a cost center or cost unit, then it can be allocated to that cost center or cost unit

8

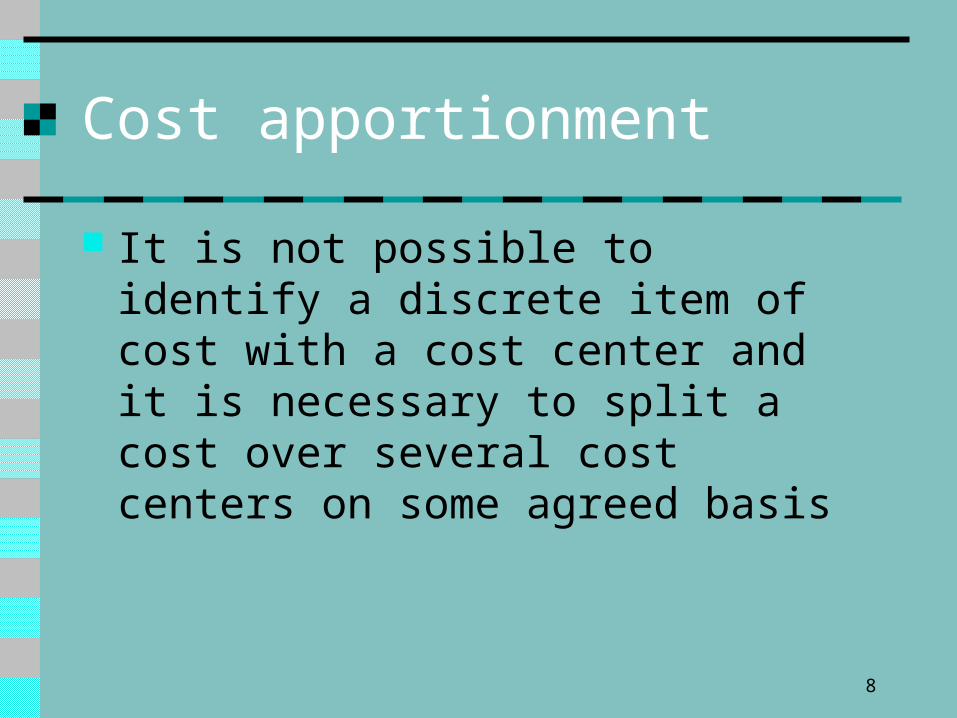

Cost apportionment

It is not possible to identify a discrete item of cost with a cost center and it is necessary to split a cost over several cost centers on some agreed basis

9

Bases of apportionment

Apportionment of indirect expenses to cost centers must be made on fair and reasonable bases

Different types of expense require different bases according to their individual characteristics

10

Base of apportionment Costs

Area Rent and rates, heat and lighting, insurance of lighting

Machine value Depreciation, machine insurance

No. of employees Wages of supervisors, canteen cost

Example textbook P.183

11

Reallocate service-center overheads to production center

12

Reallocate service-centre overheads to production cost centres Service departments are not directly involved in

production They only support service to other production

departments in order to facilitate the production process

Therefore, it is necessary to reallocate the service-centre overheads to production departments so that all production costs can be absorbed into production.

Typical bases are listed as follows:

13

Typical bases are listed as follows:

Service departments Possible bases of apportionment

Maintenance Maintenance labour hours, machine value

Stores Value or weight of materials issued, number of requisitions

inspection No. of employees, no. of jobs

Example textbook P.183

14

Calculate separate overhead absorption rate for each cost center

15

Calculate separate overhead absorption rate for each cost centre To determine the overheads to be absorbed

by a cost centre, it is necessary to establish an overhead absorption rate (OAR)

OAR =Total overhead of cost centre

Total number of units of absorption base applicable to cost centre

16

An appropriate OAR should reflect the effort or time taken to produce the products

Some commonly used absorption bases are listed as follows:

Direct labour hours It is frequently used in the labour intensive department because overheads assigned to this department are closely related to the direct labour hours worked

Machine hours It is most appropriate for the appropriate for the machining department since most of the overheads are closely related to machine hours

17

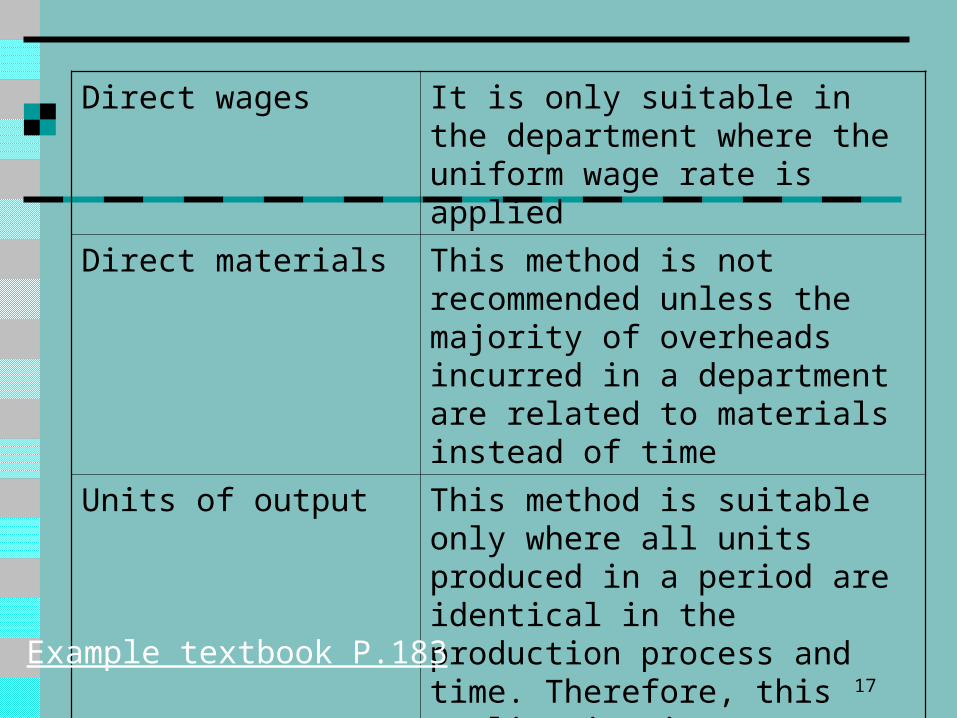

Direct wages It is only suitable in the department where the uniform wage rate is applied

Direct materials This method is not recommended unless the majority of overheads incurred in a department are related to materials instead of time

Units of output This method is suitable only where all units produced in a period are identical in the production process and time. Therefore, this application is very rare

Example textbook P.183

18

Example 1

Refer to textbook P.183 and P.184

19

O/H Apportionment Total Production dept. Service dept.item Basis Maching Assembly Finishing Stores Maintenance

Indirect Actual 727 200 199 185 20 123material

$000 $000 $000 $000 $000 $000

Indirect Actual 510 200 200 80 10 20wages

Rent& Area 200 40 20 60 60 20RatesMachine Machine 30 16 10 2 1 1Insurance ValueDep. Machine 300 160 100 20 10 10

ValueHeat & Area 100 20 10 30 30 10Light

Production No. of 160 48 32 48 16 16Supervisor Employees

2027 684 571 425 147 200

20

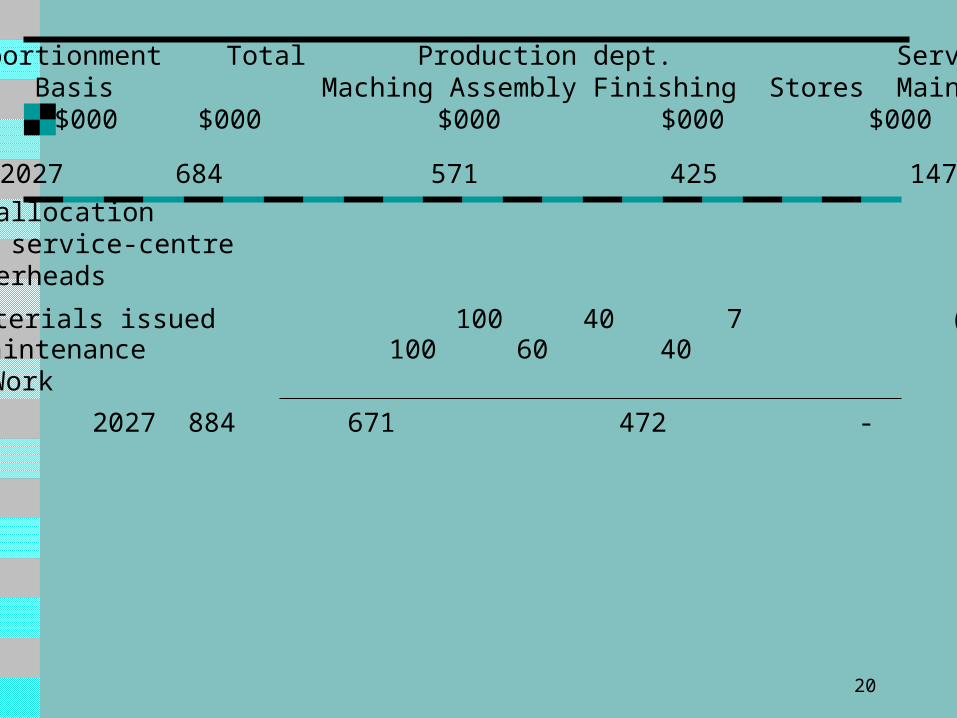

O/H Apportionment Total Production dept. Service dept.item Basis Maching Assembly Finishing Stores Maintenance

$000 $000 $000 $000 $000 $000

2027 684 571 425 147 200

Reallocationof service-centreoverheads

Stores Materials issued 100 40 7 (147)Maintenance Maintenance 100 60 40 (200)

Work

2027 884 671 472 - -

21

Calculation of overhead absorption rates:

Maching Assembly Finishing

Overhead absorption basis

Machine hours

Machine hours Labour hours

Overhead absorption rates

$884000/200000 hrs

= $4.42/hr

$671000/100000 hrs

= $6.71 /hr

$472000/40000 hrs

= $11.8/hr

22

Assign cost-center overhead to products

23

Assign cost-centre overheads to products The final step is to charge the overheads to

the products passing through the production departments

24

Example

25

The facts are the same as those in Example on slide no. 18. The number of hours needed to finish the products are listed as follows:

Departments Product A Product B

Machining 4 hours 5 hours

Assembly 2 hours 1 hour

Finishing 1/10 hour 1/10 hour

26

Departments Product A $

Machining 4 hours at $4.42 per mach. hr. 17.68Assembly 2 hours at $6.71 per mach. hr. 13.42Finishing 1/10 hour at $11.88 per labour hr. 1.19Total overhead charged per unit 32.29

Departments Product A $

Machining 5 hours at $4.42 per mach. hr. 22.10Assembly 1 hours at $6.71 per mach. hr. 6.71Finishing 1/10 hour at $11.88 per labour hr. 1.19Total overhead charged per unit 30.00

27

Predetermined overhead absorption rates (POAR)

28

Predetermined overhead absorption rates (POAR) The overhead absorption rates are usually

computed in advance of operations In practice, most absorption rates are only

predetermined because the actual overheads are not known until the end of the period

If the actual overheads are used to compute the OAR, the product cost can only be obtained at the end of the accounting period

A delay in product cost calculation will also affect the pricing setting, the profit calculation and stock valuation

29

POAR = Budgeted total overheads

Budgeted total number of units of absorption base

The formula are as follows:

The formula of POAR

30

Under-absorption and over-absorption base Since the POAR are based on the estimated

production and estimated overheads, the overheads absorbed seldom agree with the actual overheads incurred for the period

Under-absorption occur when overhead absorbed are small than the actual overheads

Over-absorption occurs when the overhead absorbed are greater than actual overheads

31

For financial accounting, under- or over-absorption of overheads should be treated as period cost and written off against the profit and loss account in the current accounting period

The under- or over-absorption of overheads should be debited or credited to the profit and loss account

The under-absorbed overheads should be deducted from profit and vice versa

32

Example

33

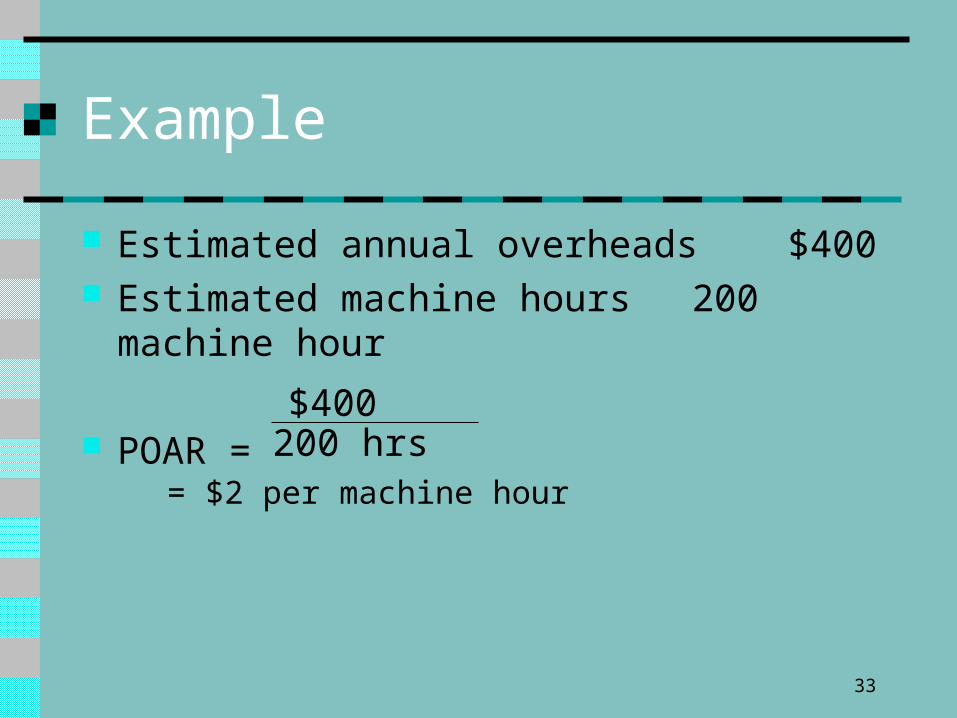

Example

Estimated annual overheads $400 Estimated machine hours 200 machine hour

POAR = $400200 hrs

= $2 per machine hour

34

Product 1 Product 2 Product 3 Product 4

Actual overheads incurred

$400 $400 $300 $500

Actual machine hours

250 hrs 160 hrs 200 hrs 200 hrs

Overhead absorbed

Under- or over-absorption

$2 * 250 hrs= $500

$2 * 160 hrs= $320

$2 * 200 hrs= $400

$2 * 200 hrs= $400

Over-absorbed$100

Under-absorbed$80

Over-absorbed$100

Under-absorbed$100s

35

Blanket Overhead Rate

36

Blanket overhead rate

According to the overhead allocation procedure, the overheads are allocated to departments and each department calculate its own OAR and allocate the overheads to products passing through that department

Alternatively, some firms do not assign overheads to departments. Rather, they adopted a single overhead rate, i.e. a blanket overhead rate, that is assigned to all products produced within the whole factory

37

The use of the blanket overhead rate is not recommended as many products are produced in different production centres, and products consume cost-centre overheads in different proportions

38

Example

39

The annual overhead costs of a factory with three production departments are shown as follows:

Dept. A Dept.B Dept. C Total

Overheads $20000 $400000 $180000 $600000

Direct machine hours

100000 100000 100000 300000

Departmental overhead rate per direct machine hour

$0.2 $4 $1.8

Blanket overhead rate pre machine hour

$2

40

If the production of product X only requires 10 direct machine hours in department A, the overheads absorbed will be computed as follows:

Using departmental overhead rate

Using blanket overhead rate

Overhead absorbed $0.2 *10

= $2

$2 *10

= $20

In this example, the production of product X does not consume Large amounts of overheads in department B and C. Therefore, there will be over-absorption of overheads if the blanket overheadrate is used