Embed Size (px)

Citation preview

1

Page 1 of 79

Farm Estate Planning Strategies

2

Page 2 of 79

The Need for Estate Planning

One of the challenges of Planning is to make people

aware that they need to take action. Nowhere is

that more of an issue than with the family farm. * Iowa Farm Bureau

3

Page 3 of 79

Why is First Resources Involved?1. One of the most common methods of

paying Estate Taxes is Insurance – We sell insurance.

2. One of the risk factors for farms is Long Term Care – We sell LTC.

3. Investments are a key element in planning – We advise investors.

4

Page 4 of 79

Three Levels of Planning

1. Family Plan

2. Elimination of Tax

3. Management of Asset Cost and Continuity of Business

5

Page 5 of 79

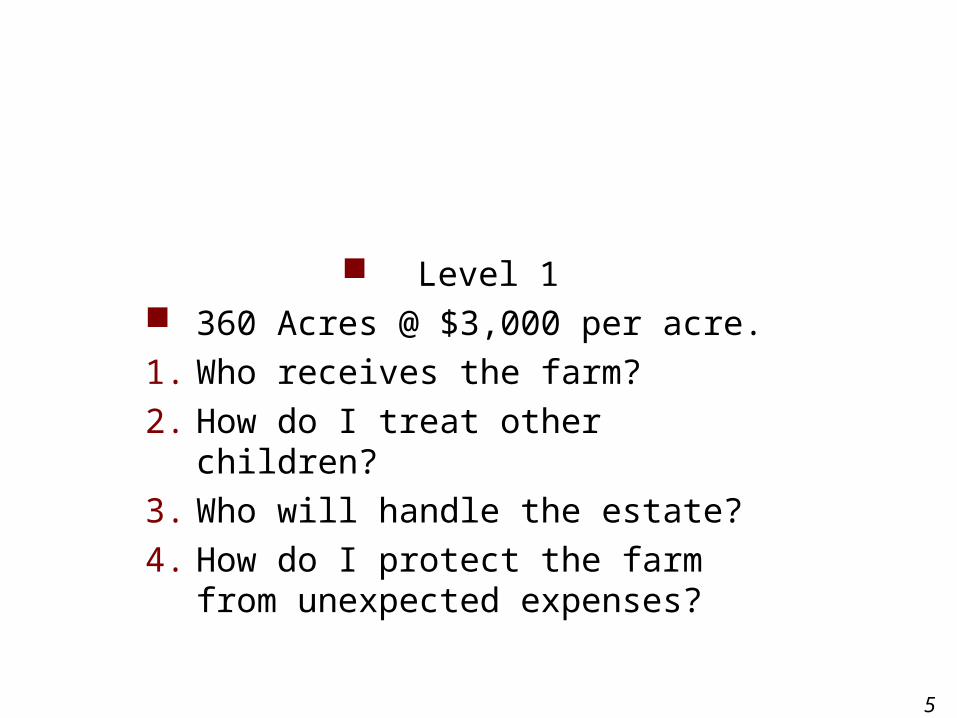

Level 1 360 Acres @ $3,000 per acre.

1. Who receives the farm?

2. How do I treat other children?

3. Who will handle the estate?

4. How do I protect the farm from unexpected expenses?

6

Page 6 of 79

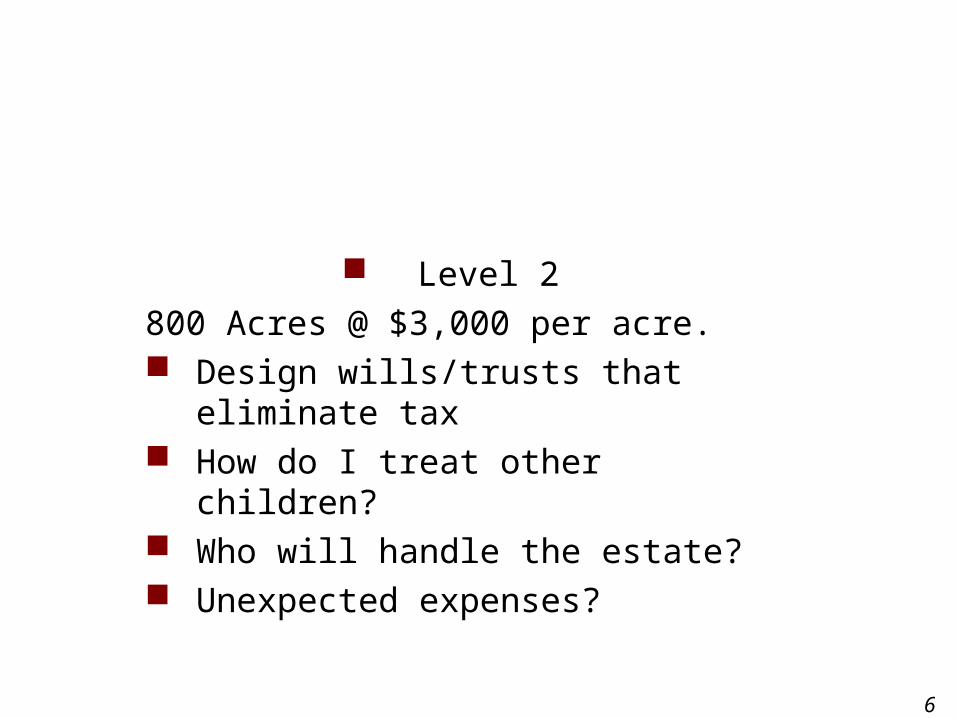

Level 2

800 Acres @ $3,000 per acre. Design wills/trusts that eliminate tax How do I treat other children? Who will handle the estate? Unexpected expenses?

7

Page 7 of 79

Level 3 1500 Acres @ $3,000 per acre

1. Minimize Estate Tax

2. How do I treat other children?

3. Who will handle the estate?

4. Unexpected expenses?

5. Management of Tax Payments?

8

Page 8 of 79

The Need for Estate Planning

The tendency to listen to politicians in Washington discourages effective action. For 40 years, they have talked about solutions and we still have a tax of 45% for all values over $2,000,000.

Minnesota tax is imposed for values over $1,000,000.

9

Page 9 of 79

What is Estate Planning?

Arranging your property to accomplish these goals.

Determining goals with respect to your property both during life and at death.

Protecting your assets from depletion risks.

10

Page 10 of 79

Who Needs Estate Planning?

11

Page 11 of 79

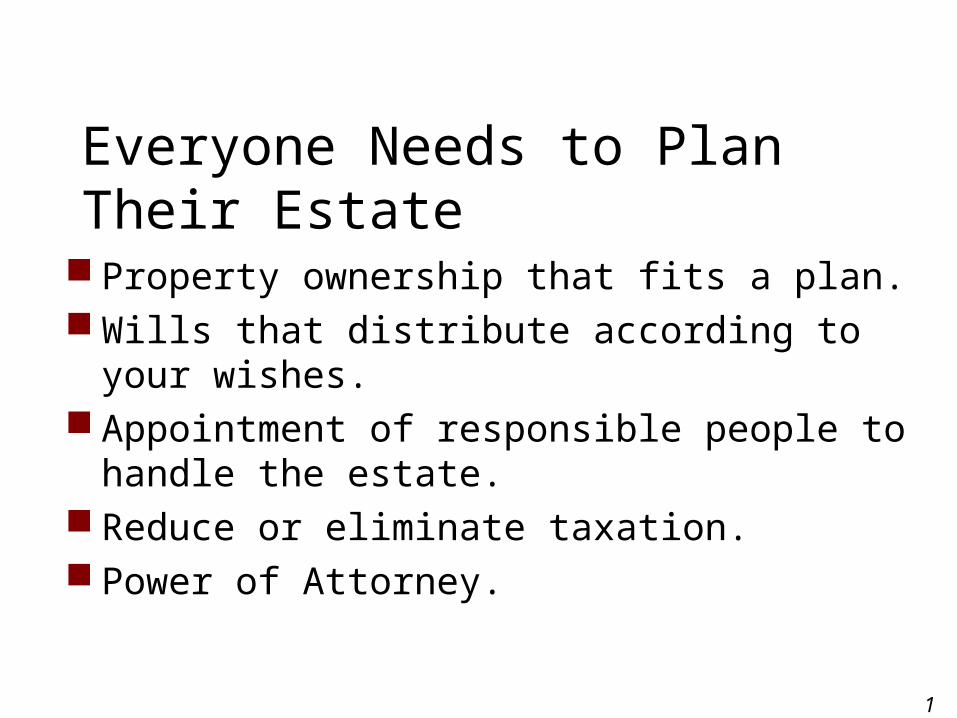

Everyone Needs to Plan Their Estate

Property ownership that fits a plan. Wills that distribute according to your wishes. Appointment of responsible people to handle the

estate. Reduce or eliminate taxation. Power of Attorney.

12

Page 12 of 79

Property Ownership

Joint Tenancy Bypass the will Non-probate Reduces stepped up basis Can be fully subject to

Medicaid claims

Tenancy in Common Proportionate Ownership Does not transfer to other owner at death Can raise questions of % ownership Subject to transfer by will or intestacy

rules Probate

13

Page 13 of 79

The Need for Estate Planning

Everyone has an estate plan! If you don’t develop one, the state has

one for you.

14

Page 14 of 79

State Provided Plan

15

Page 15 of 79

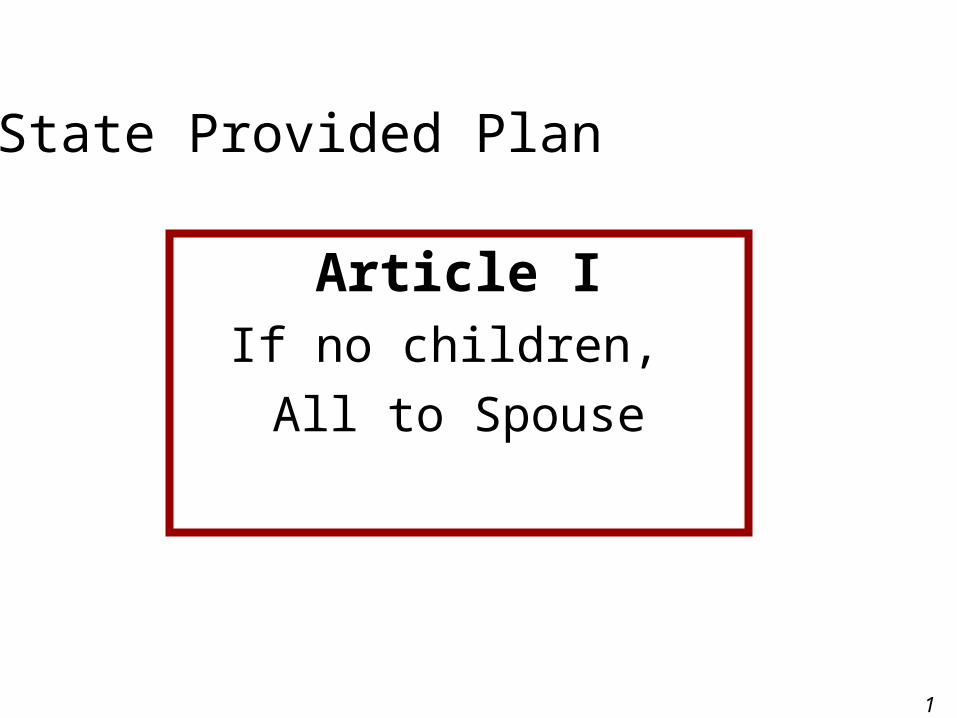

Article IIf no children,

All to Spouse

State Provided Plan

16

Page 16 of 79

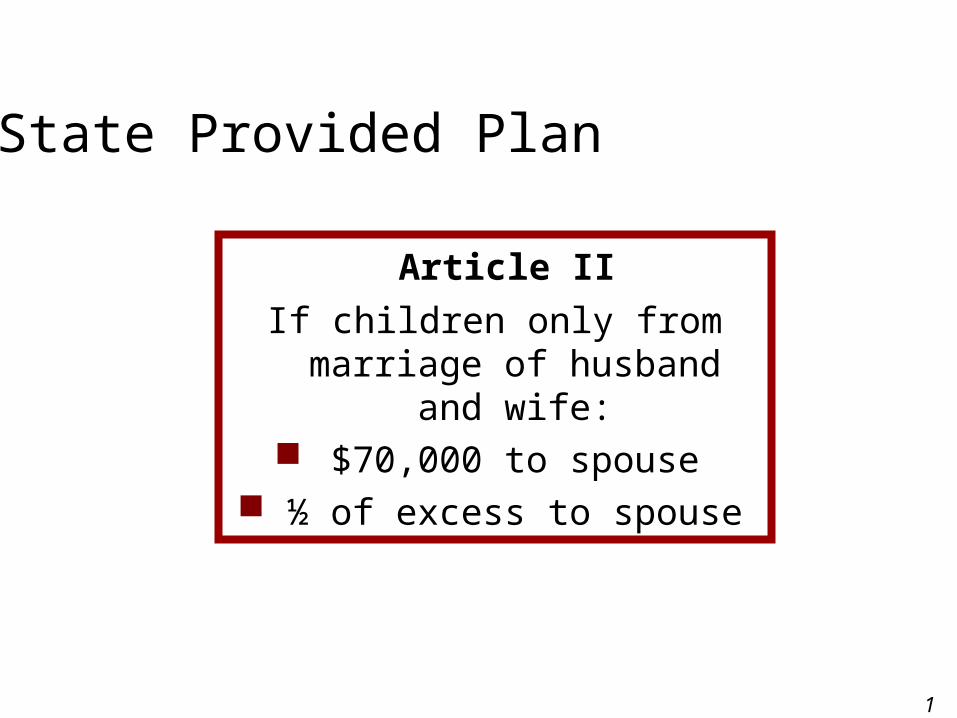

Article II

If children only from marriage of husband and wife:

$70,000 to spouse ½ of excess to spouse

State Provided Plan

17

Page 17 of 79

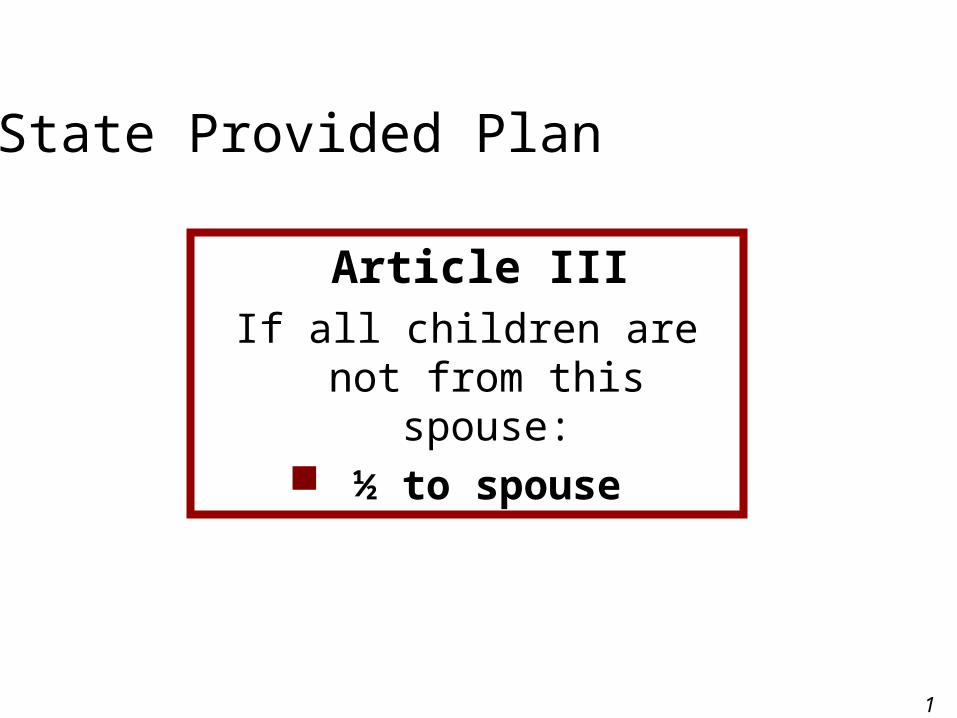

Article IIIIf all children are not from

this spouse: ½ to spouse

State Provided Plan

18

Page 18 of 79

Article IV

Children receive equal shares by right of

representation.

State Provided Plan

19

Page 19 of 79

Article VIf a child has pre-deceased the

parent without grandchildren, then to

parent(s) of child; if not alive, then escheat!

State Provided Plan

20

Page 20 of 79

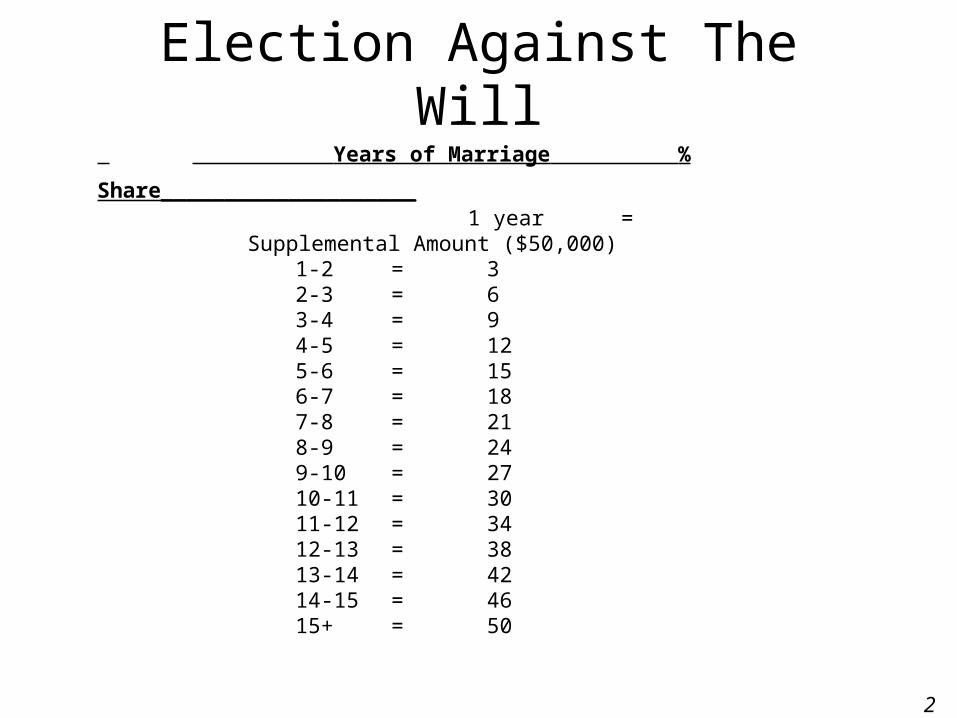

Election Against The Will Years of Marriage % Share____________________

1 year = Supplemental Amount ($50,000)1-2 = 32-3 = 63-4 = 94-5 = 125-6 = 156-7 = 187-8 = 218-9 = 249-10 = 2710-11 = 3011-12 = 3412-13 = 3813-14 = 4214-15 = 4615+ = 50

21

Page 21 of 79

Who Needs Estate Tax Planning?

3,000,000

2,000,000

1,000,000

4,000,000

1,500,000

2,000,000 2,000,000 2,000,000

3,500,000

1,000,000

2006

2007 2008 2009 2010 20112005

No

Est

ate

Ta

x

22

Page 22 of 79

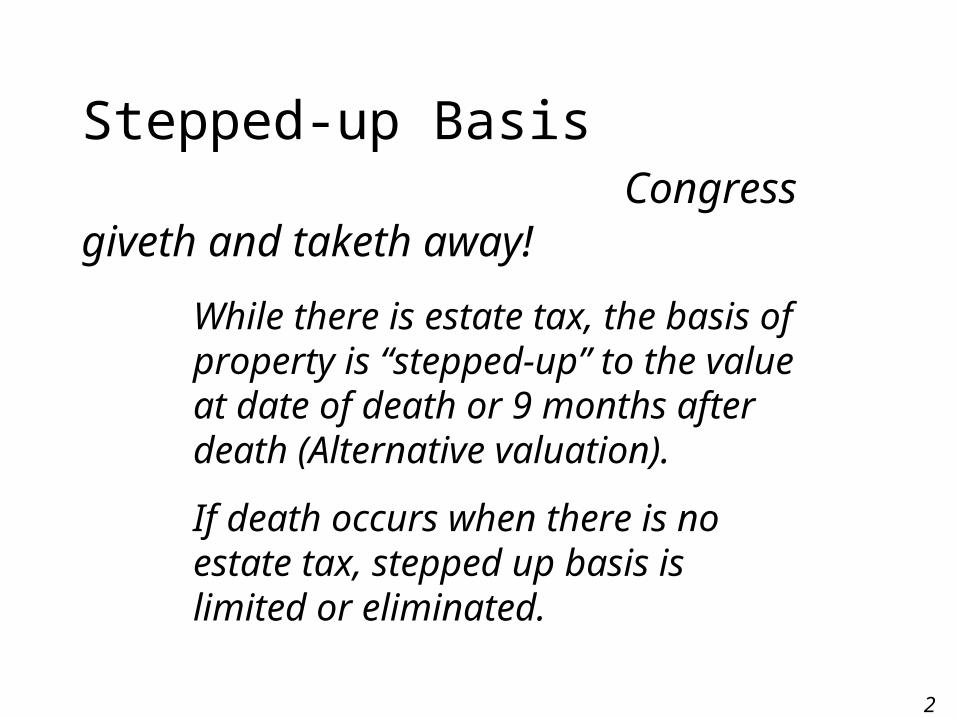

Stepped-up Basis Congress giveth and taketh away!

While there is estate tax, the basis of property is “stepped-up” to the value at date of death or 9 months after death (Alternative valuation).

If death occurs when there is no estate tax, stepped up basis is limited or eliminated.

23

Page 23 of 79

Simple WillHusband’s

Estate($3,000,000)

24

Page 24 of 79

Simple Will

Wife’s Estate($3,000,000)

No Federal Estate Tax

Husband’s Estate

($3,000,000)

25

Page 25 of 79

Simple Will

Wife’s Estate($3,000,000)

Husband’s Death* No Federal Estate Tax

Husband’s Estate

($3,000,000)

Federal Estate Tax$460,000

Wife’s Death*

Wife’s Heirs($2,551,700)

* Assumes death in 2006.

26

Page 26 of 79

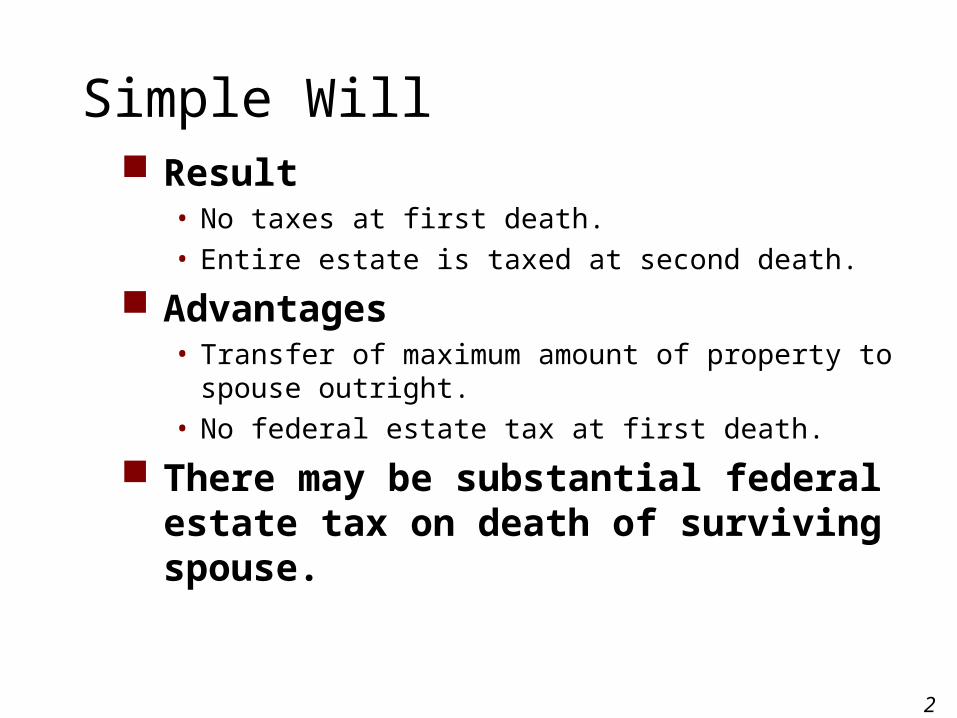

Simple Will Result

• No taxes at first death.

• Entire estate is taxed at second death.

Advantages• Transfer of maximum amount of property to

spouse outright.

• No federal estate tax at first death.

There may be substantial federal estate tax on death of surviving spouse.

27

Page 27 of 79

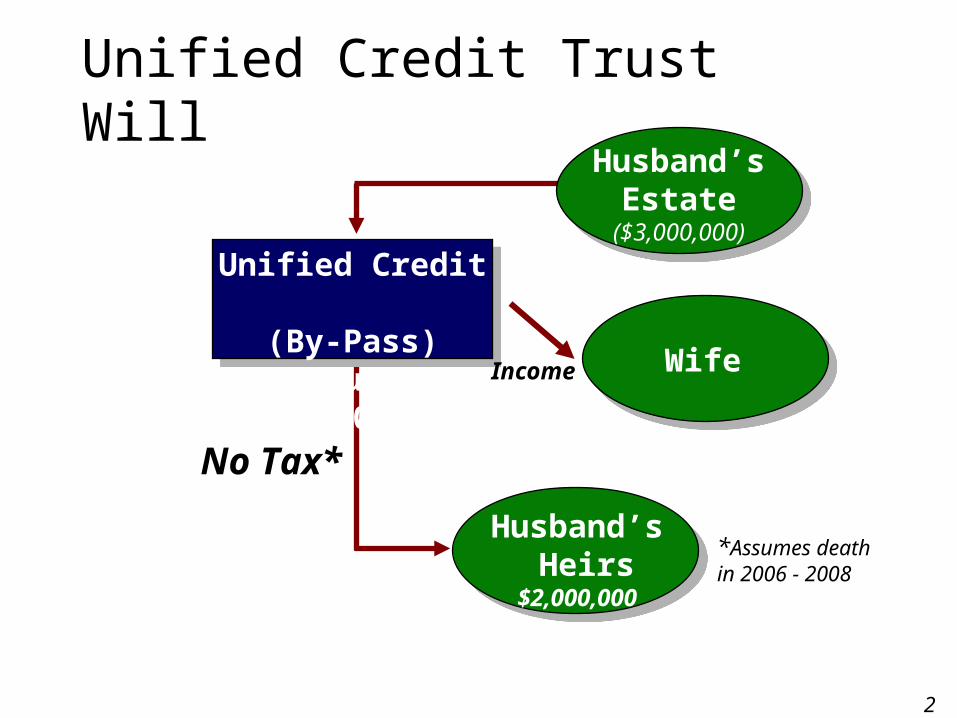

Unified Credit Trust WillHusband’s

Estate($3,000,000)

Husband’s Heirs

$2,000,000

No Tax*

Unified Credit (By-Pass) Trust

$2,000,000

*Assumes death in 2006 - 2008

Wife

WifeIncome

28

Page 28 of 79

Unified Credit Trust WillHusband’s

Estate($3,000,000)

Unified Credit (By-Pass) Trust

$2,000,000

Husband’sHeirs

$2,000,000

No Tax*

No Federal Estate Tax

Wife’s Estate($1,000,000)

Wife’s Heirs$1,000,000

No Tax*

*Assumes death in year 2006.

29

Page 29 of 79

Increased Unified CreditIf death occurs

in year. . .

200320042005200620072008200920102011

Amount passing estate tax free

$1,000,000 1,500,000 1,500,000 2,000,000 2,000,000 2,000,000 3,500,000Repealed

1,000,000

30

Page 30 of 79

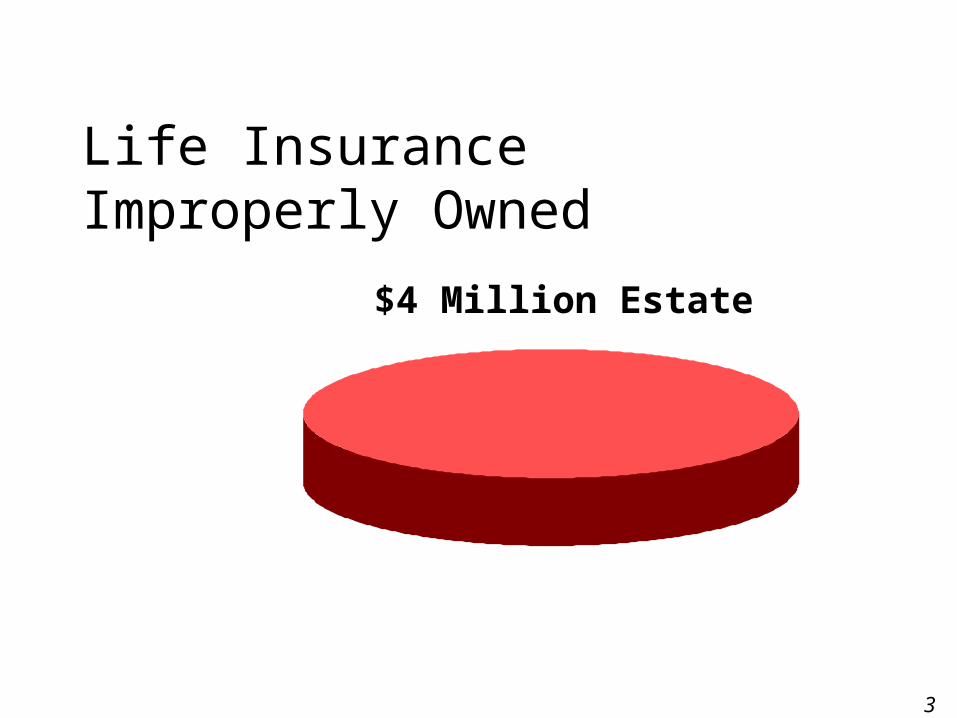

Life Insurance Improperly Owned

$4 Million Estate

31

Page 31 of 79

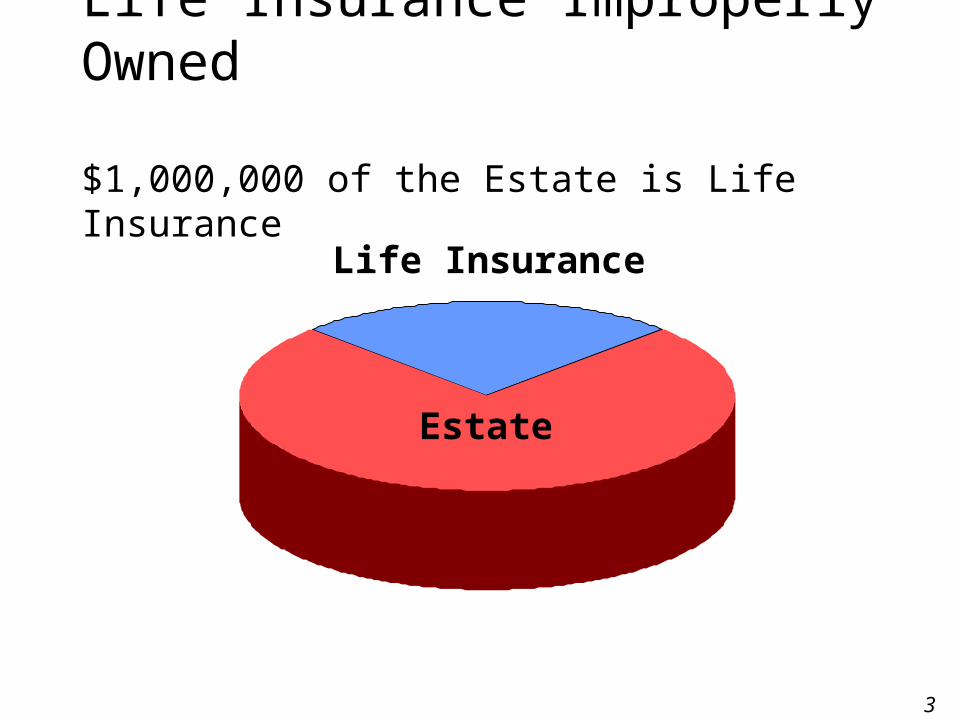

Life Insurance Improperly Owned $1,000,000 of the Estate is Life Insurance

Estate

Life Insurance

32

Page 32 of 79

Life Insurance Improperly Owned

Estate

Life Insurance

Estate Taxes

0Estate without Life Insurance but with a unified credit trust:

$0 Taxes

With Life Insurance in the Estate:

$460,000 Taxes

33

Page 33 of 79

Life Insurance Properly Owned

Individuals

Trust

Life Insurance$4,000,000 Estate

$0 Taxes

34

Page 34 of 79

The Need for Estate Planning?

35

Page 35 of 79

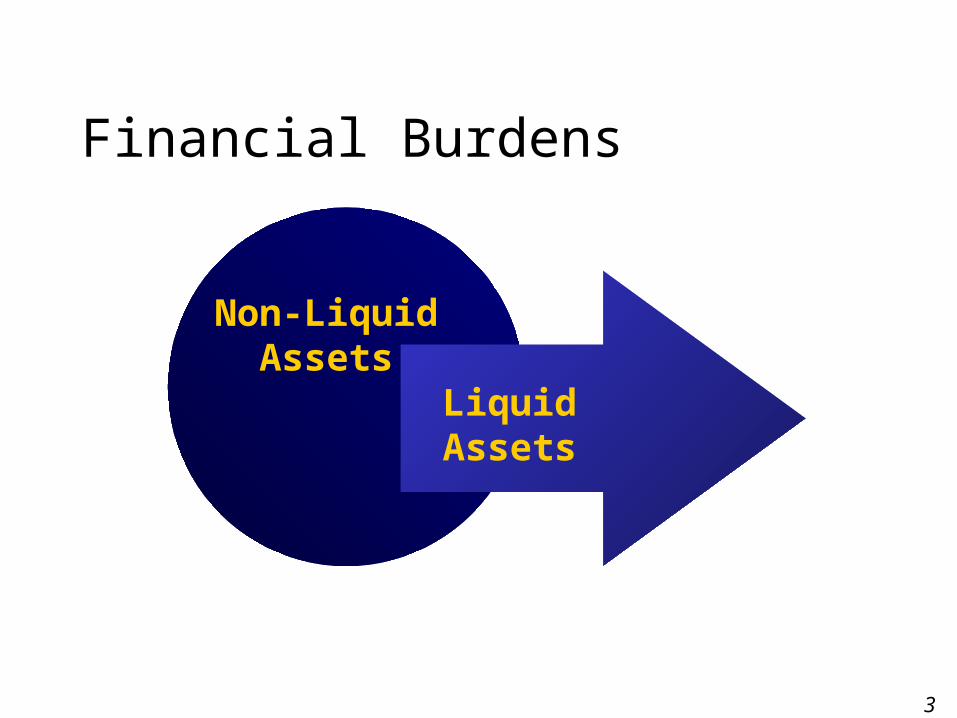

Financial Burdens Estate settlement costs are too high

• Probate fees• Death taxes • Debts

36

Page 36 of 79

Financial Burdens Estate Settlement costs are too high

• Probate fees

• Death taxes

• Debts

Estate assets are improperly arranged• Liquidity

• Cash flow

37

Page 37 of 79

Financial Burdens

Non-LiquidAssets

Liquid Assets

38

Page 38 of 79

Common Mistakes

No written plan. Improper ownership of assets. Life insurance is improperly owned.

39

Page 39 of 79

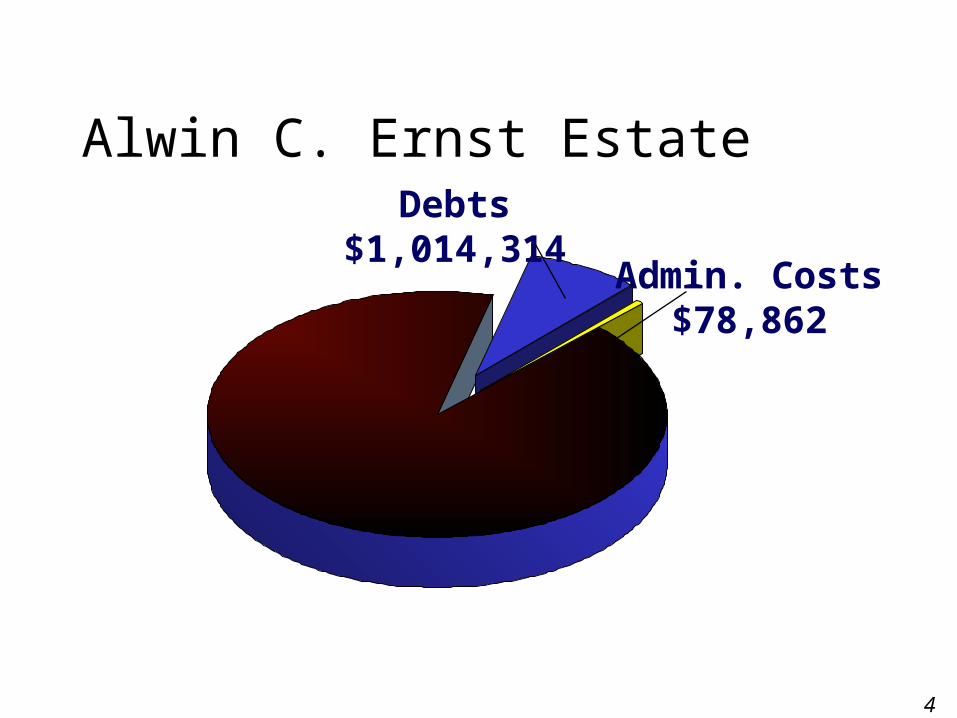

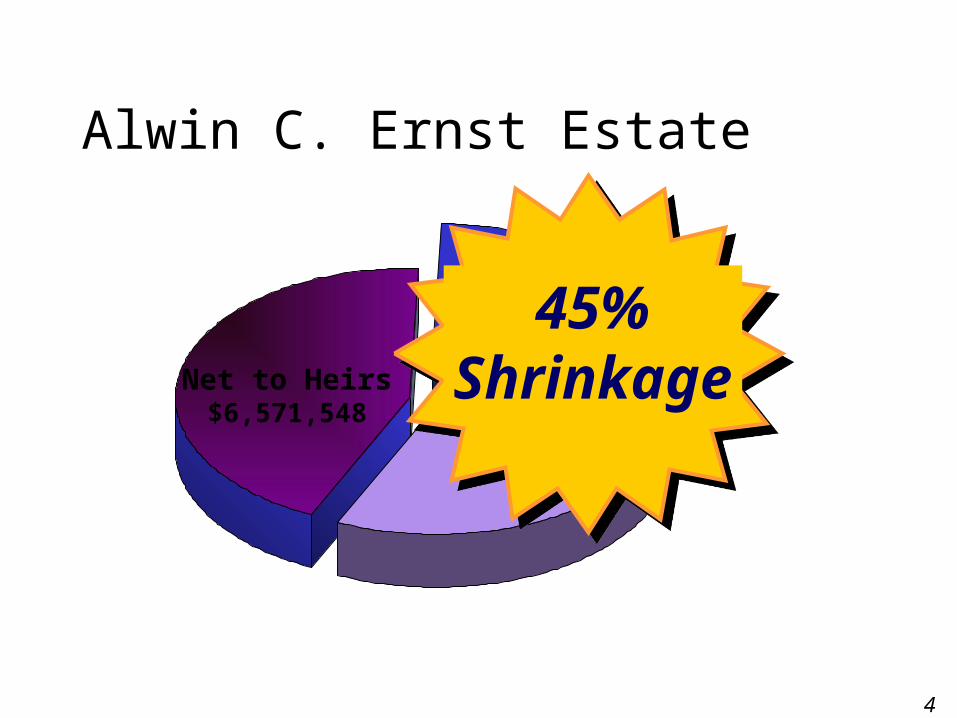

Alwin C. Ernst Estate

Gross Estate$12,642,431

40

Page 40 of 79

Alwin C. Ernst EstateDebts $1,014,314

41

Page 41 of 79

Alwin C. Ernst EstateDebts

$1,014,314Admin. Costs

$78,862

42

Page 42 of 79

Alwin C. Ernst EstateDebts

$1,014,314 Admin. Costs$78,862

Estate Taxes$ 4,335,000

43

Page 43 of 79

Alwin C. Ernst Estate

Net to Heirs$6,571,548

45%Shrinkage

44

Page 44 of 79

Discuss Here the

“Estates of 4 Famous People”

Handouts

45

Page 45 of 79

Advanced DirectivesThe Advanced Directive or “Living Will” is the best method tocontrol medical care when you’ve lost communication

Assign an AgentDescribe your desire for pain reliefLimit medical treatment, if desired

46

Page 46 of 79

Power of Attorney

Assign Responsibility and ability to act on your behalf.

47

Page 47 of 79

Protecting Assets from Medicaid

48

Page 48 of 79

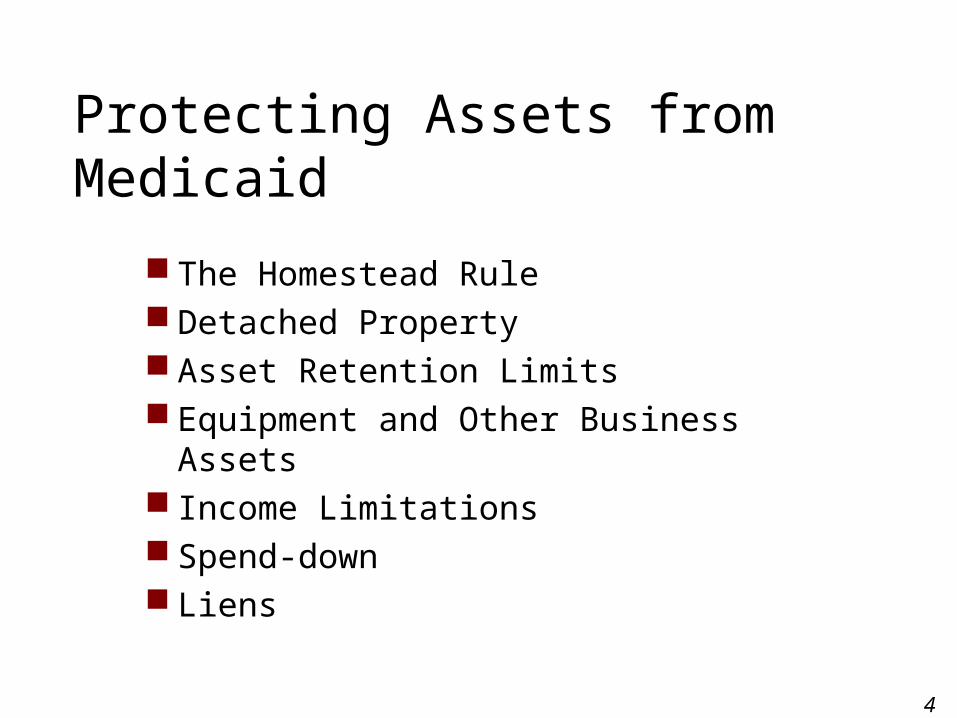

Protecting Assets from Medicaid

The Homestead Rule Detached Property Asset Retention Limits Equipment and Other Business Assets Income Limitations Spend-down Liens

49

Page 49 of 79

Protections for the Community Spouse Community Spouse Resource Allowance (CSRA):

– Minimum $28,001

– Maximum $99,540 Increased CSRA:

– Permitted, but rarely used. Minnesota follows the income-first rule.

Annuities

– Actuarially sound annuities are permitted (but restrictions apply; check with attorney).

Monthly Maintenance Needs Allowance:

– Minimum $1,604.00

– Maximum $2,488.50

50

Page 50 of 79

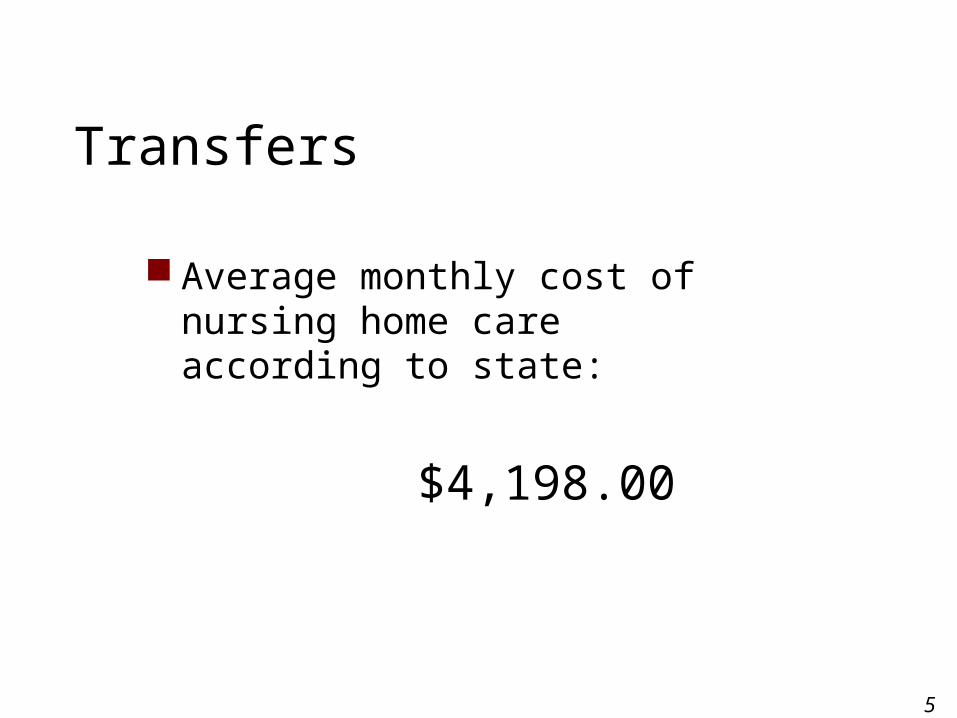

Transfers

Average monthly cost of nursing home care according to state:

$4,198.00

51

Page 51 of 79

Income

Is the state an “income cap” state?

NO

52

Page 52 of 79

Estate Recovery

Has the state expanded the definition of “estate” beyond the probate estate?

– No (but exceptions apply; check with attorney)

Has the state included a hardship?

– Yes

53

Page 53 of 79

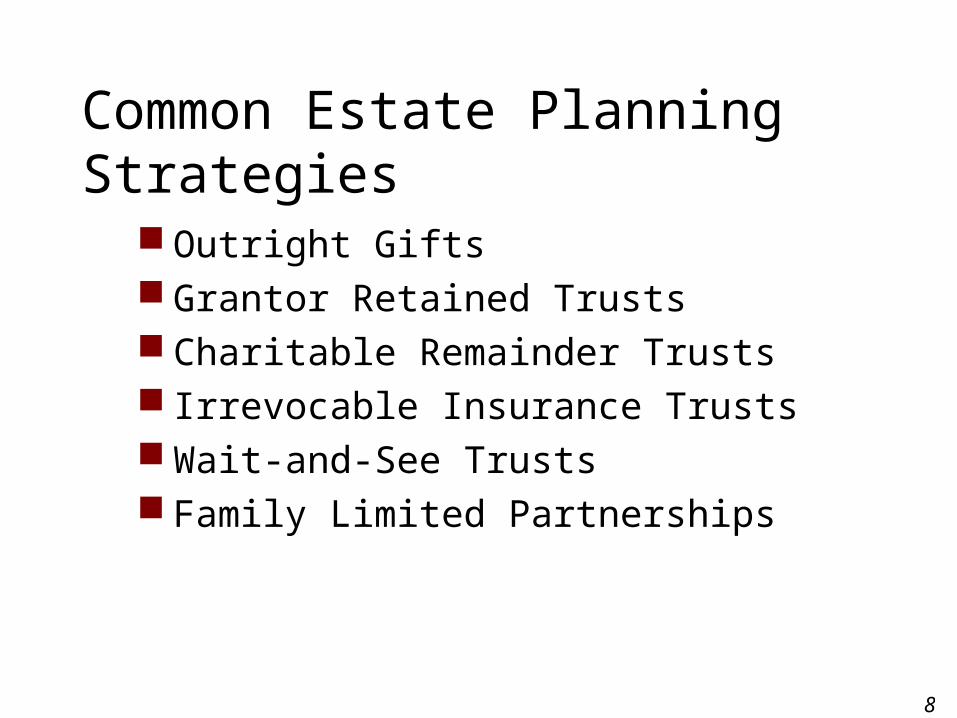

CommonEstate Planning Strategies

54

Page 54 of 79

Common Estate Planning Strategies Outright Gifts Family Farm Owned Business Deduction Grantor Retained Trusts Charitable Remainders Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

55

Page 55 of 79

Outright Gifts

$12,000 donor/donee

56

Page 56 of 79

Gift tax annual exclusion amount is $12,000 for gifts

made in 2006, and is subject to indexing in the future.

$12,000/donor/donee

Parent

Child 1 Child 2

Outright Gifts

57

Page 57 of 79

Gifting Through the Unified CreditHusband - $2,000,000 ► Gift to ChildrenWife - $2,000,000

Requires a gift Tax Return No Stepped-up basis Cannot retain control or enjoy the

benefit of Gifted property

58

Page 58 of 79

Gift Challenges

Estate Growth exceeds tax free gifts Gift assets may be essential to owners Gifting the Farm requires restructuring

and valuations

59

Page 59 of 79

Family Farm Business DeductionIf elected, Applies To Estates Prior To 2004 or After 2010

The deduction is the lesser of the unified credit equivalent or the adjusted value of the business

The business must pass to a qualified heir The business must be operated by a qualified

heir for five of any eight year period in the first 10 years after decedent's death

Many other rules apply

60

Page 60 of 79

Common Strategies

Grantor Retained Trusts Charitable Remainder Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

Outright Gifts

61

Page 61 of 79

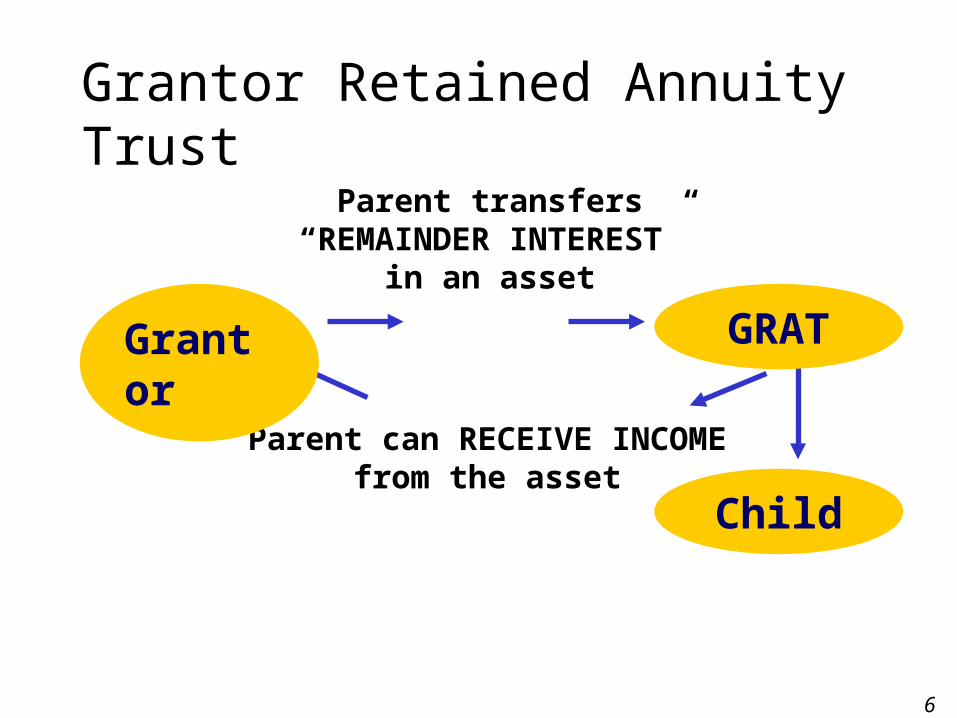

Grantor Retained Annuity Trust

Parent can RECEIVE INCOMEfrom the asset

Grantor

GRAT

Parent transfers“REMAINDER INTEREST”

in an asset

Child

62

Page 62 of 79

Clearance Sale! 20 - 30 - 40% Off!

Common Strategies

63

Page 63 of 79

Common Strategies Outright Gifts Grantor Retained Trusts Charitable Remainder Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

64

Page 64 of 79

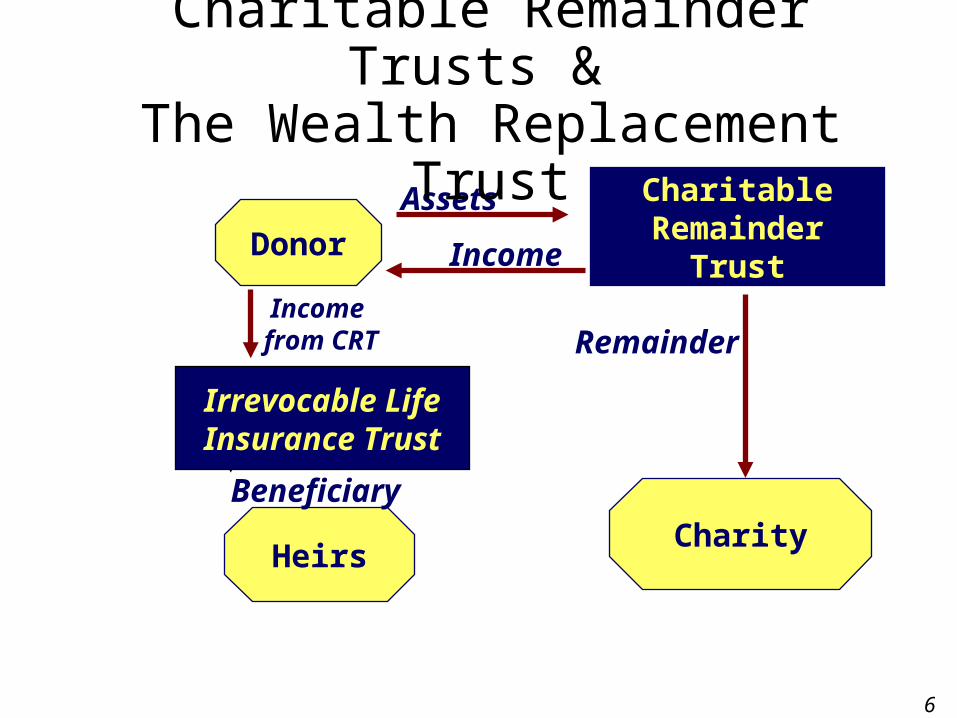

Charitable Remainder Trusts

Donor

Spouse or Children

Charitable Remainder Trust

CHARITY

Assets

Income

Remainder

65

Page 65 of 79

Donor

Heirs

Charitable Remainder Trust

Charity

Assets

Income

Remainder

Irrevocable Life Insurance Trust

Income from CRT

Beneficiary

Charitable Remainder Trusts & The Wealth Replacement Trust

66

Page 66 of 79

A sizable gift has been made to donor’s favorite charity.

Charitable Remainder/Wealth Replacement Results

67

Page 67 of 79

A sizable gift has been made to donor’s favorite charity.

A current income tax charitable deduction is available for the gift of remainder interest.

Charitable Remainder/Wealth Replacement Results

68

Page 68 of 79

A sizable gift has been made to donor’s favorite charity.

A current income tax charitable deduction is available for the gift of remainder interest.

The assets transferred to charity escape estate taxation.

Charitable Remainder/Wealth Replacement Results

69

Page 69 of 79

A sizable gift has been made to donor’s favorite charity.

A current income tax charitable deduction is available for the gift of remainder interest.

The assets transferred to charity escape estate taxation.

Donor receives cash flow from CRT (to pay premiums in the wealth replacement trust).

Charitable Remainder/Wealth Replacement Results

70

Page 70 of 79

A sizable gift has been made to donor’s favorite charity.

A current income tax charitable deduction is available for the gift of remainder interest.

The assets transferred to charity escape estate taxation. Donor receives cash flow from CRT (to pay premiums

in the wealth replacement trust). Amount passing to heirs has been preserved. Death

proceeds in irrevocable trust provide attractive replacement for assets given to charity.

Charitable Remainder/Wealth Replacement Results

71

Page 71 of 79

A sizable gift has been made to donor’s favorite charity. A current income tax charitable deduction is available for

the gift of remainder interest. The assets transferred to charity escape estate taxation. Donor receives cash flow from CRT (to pay premiums in

the wealth replacement trust). Amount passing to heirs has been preserved. Death

proceeds in irrevocable trust provide attractive replacement for assets given to charity.

Death proceeds are not includible in donor’s estate.

Charitable Remainder/Wealth Replacement Results

72

Page 72 of 79

Common Estate Planning Strategies Outright Gifts Grantor Retained Trusts Charitable Remainder Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

73

Page 73 of 79

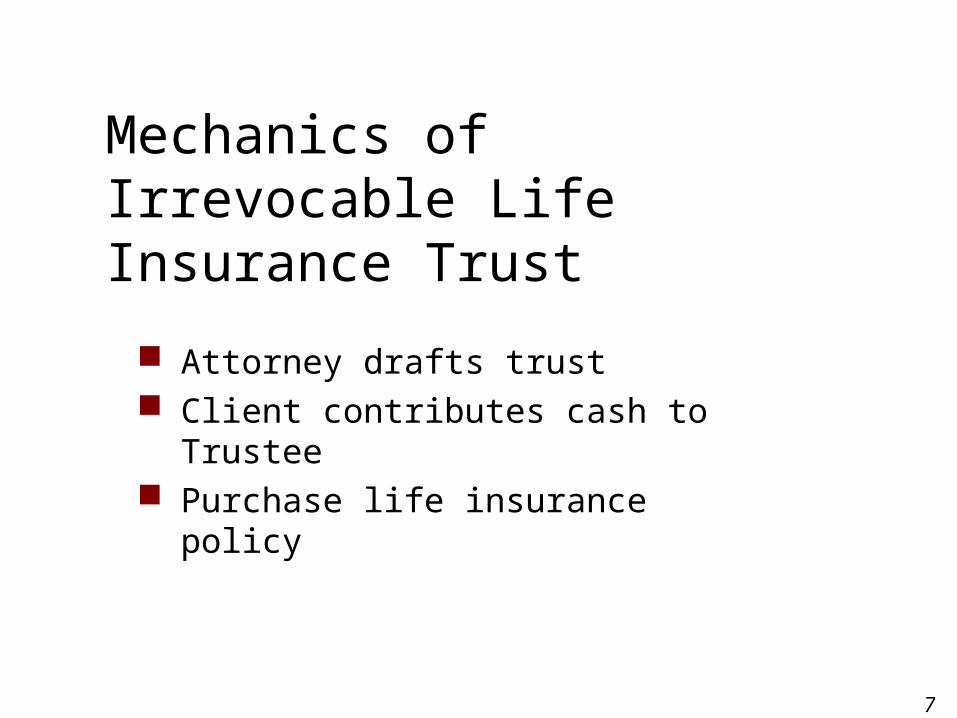

Attorney drafts trust Client contributes cash to Trustee Purchase life insurance policy

Mechanics of Irrevocable Life Insurance Trust

74

Page 74 of 79

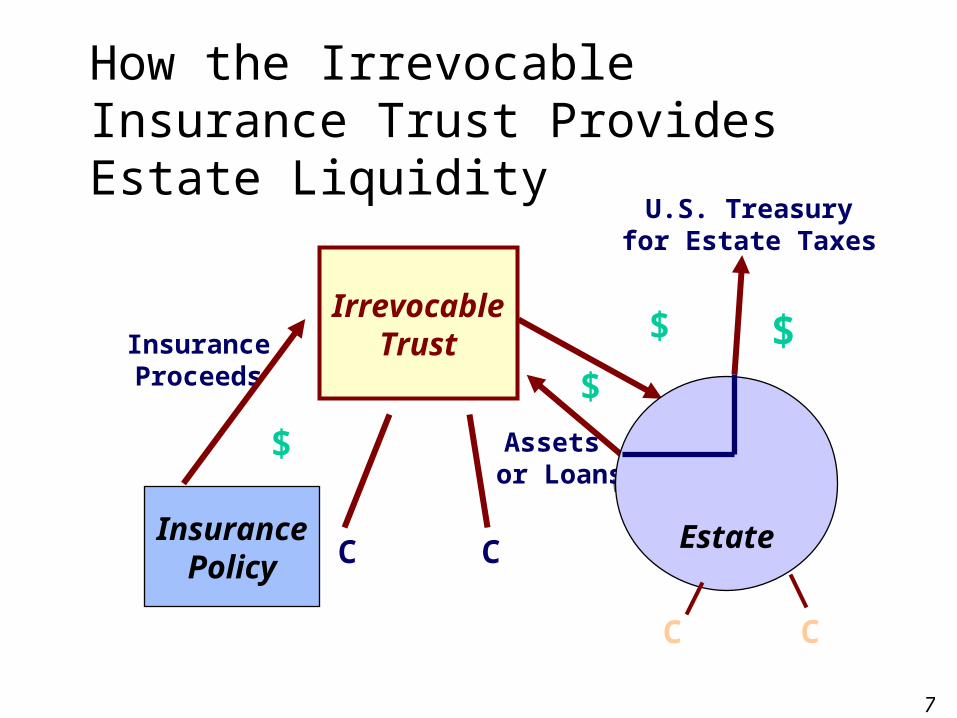

Insurance Policy

Irrevocable TrustInsurance

Proceeds

$

$$

$

U.S. Treasuryfor Estate Taxes

Assets or Loans

C C Estate

CC

How the Irrevocable Insurance Trust Provides Estate Liquidity

75

Page 75 of 79

Common Estate Planning Strategies

Outright Gifts Grantor Retained Trusts Charitable Remainder Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

76

Page 76 of 79

Wait-and-See TrustToday. . .own policy

After one spouse dies

Policy

After Second Death Death Benefit Cash

TRUST

TRUST

77

Page 77 of 79

Common Estate Planning Strategies

Outright Gifts Grantor Retained Trusts Charitable Remainder Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

78

Page 78 of 79

Family Limited Partnerships

Corporate General Partners

79

Page 79 of 79

Family Limited Partnerships

Corporate General Partners

1% Family Limited

Partnership

80

Page 80 of 79

Family Limited Partnerships

Corporate General Partners

1% Family Limited

Partnership

99%Limited Partners

81

Page 81 of 79

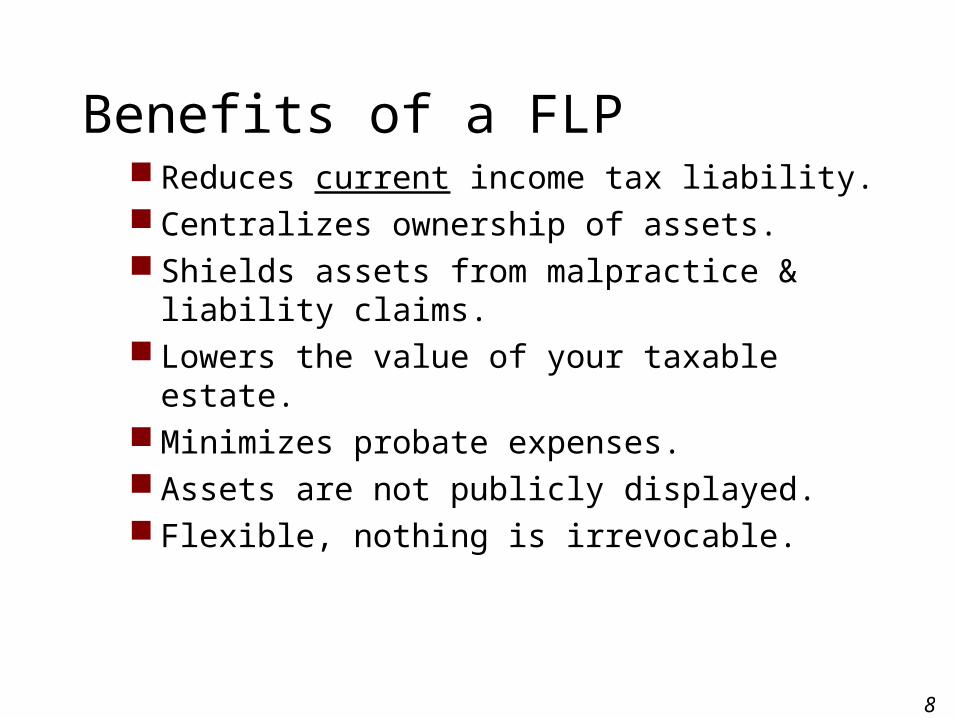

Benefits of a FLP Reduces current income tax liability. Centralizes ownership of assets. Shields assets from malpractice & liability

claims. Lowers the value of your taxable estate. Minimizes probate expenses. Assets are not publicly displayed. Flexible, nothing is irrevocable.

82

Page 82 of 79

Common Estate Planning Strategies

Outright Gifts Grantor Retained Trusts Charitable Remainder Trusts Irrevocable Insurance Trusts Wait-and-See Trusts Family Limited Partnerships

83

Page 83 of 79

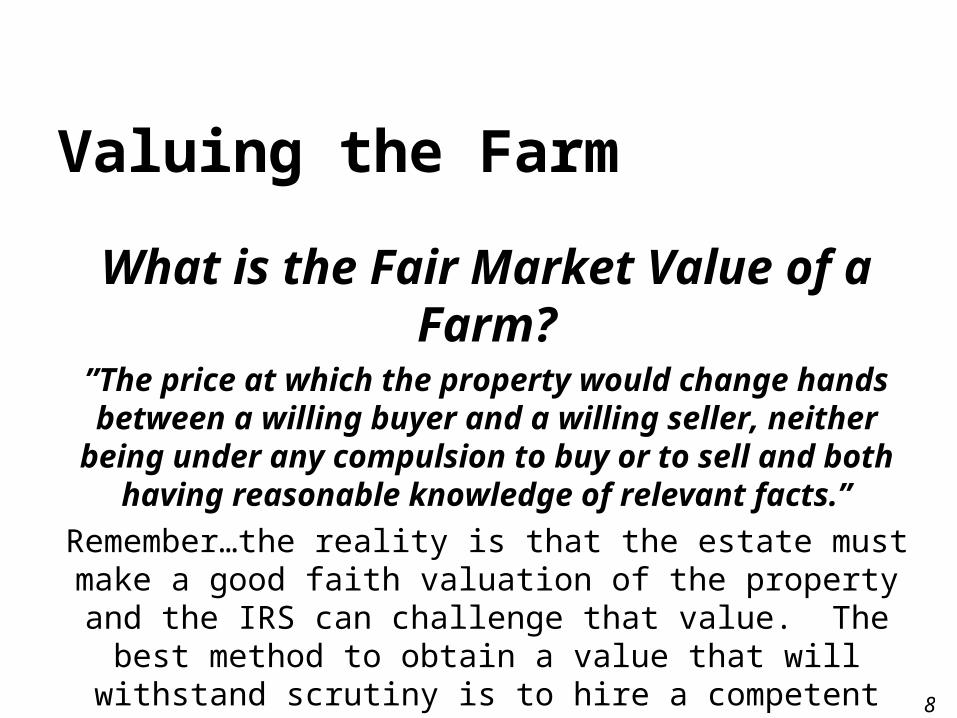

Valuing the Farm

What is the Fair Market Value of a Farm?”The price at which the property would change hands between a

willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable

knowledge of relevant facts.”

Remember…the reality is that the estate must make a good faith valuation of the property and the IRS can challenge that value.

The best method to obtain a value that will withstand scrutiny is to hire a competent appraiser

84

Page 84 of 79

Three Common Methods of Valuation

1. Market Data – An arms length sale of the property being valued, or if available, comparable values.

85

Page 85 of 79

2. Capitalization of Income – The projected net income of the property from the highest and best use of the property capitalized at a rate that reflects a fair return on this investment.

86

Page 86 of 79

3. Redemption Cost – An estimate of the cost of replacing a structure combined with an appraisal of the land.

87

Page 87 of 79

Alternative Valuation

The highest and best use provision is eliminated and the property is valued as a farm under section 2032(a) of the Internal Revenue Code.

88

Page 88 of 79

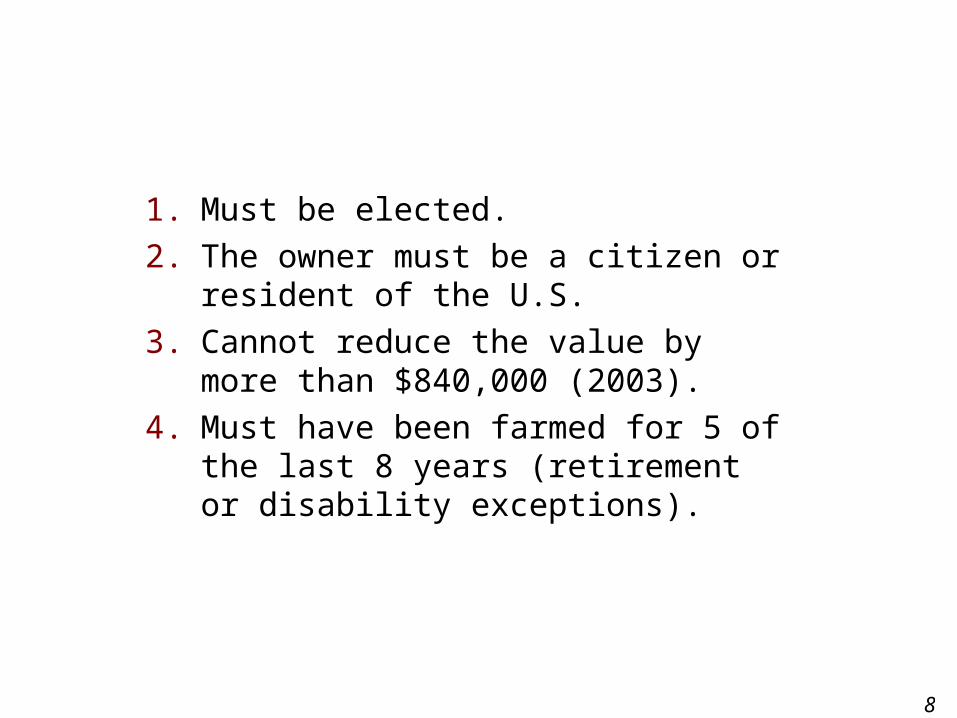

1. Must be elected.

2. The owner must be a citizen or resident of the U.S.

3. Cannot reduce the value by more than $840,000 (2003).

4. Must have been farmed for 5 of the last 8 years (retirement or disability exceptions).

89

Page 89 of 79

5. 50% of the adjusted gross estate consists of farm that was passed to a qualified heir.

6. 25% of the adjusted gross estate is farm real property.

7. Must continue to be operated as a farm for 10 years.

90

Page 90 of 79

The most commonly used method of valuation under this provision is the

cash rental approach:

Annual Gross Cash Rental,

minus Property Tax,

all divided by the

Federal Land Bank Loan Rate

91

Page 91 of 79

How You Can Help!

Estate inventory

92

Page 92 of 79

Creating a Transition Plan

1. Establish a process – Meet with the owners to lay the foundation of the process. Which advisors will be used? Who is in the first meeting? (Usually just the owners and a primary advisor)

93

Page 93 of 79

2. Establish Goals. What must be done to effectively transfer the business. What are their security needs now and in retirement? Do they have an intended buyer or someone who will receive the farm?

94

Page 94 of 79

3. What are the impediments to reaching these goals? Is there an equality issue? What would disability do to the plan? How do they execute the plan with the least tax and legal cost?

95

Page 95 of 79

Establishing the Process – The first meeting.

Who do you want the farm to go to? When do you plan to transfer the farm? What is the value of the farm? What terms do you want for the sale or

other transfer of the farm?

96

Page 96 of 79

What are your retirement goals? Is the farm the only source of income? Have you diversified the risk of having

adequate funds for retirement?

97

Page 97 of 79

If the children will not be receiving or keeping the farm, do you have a potential buyer? Do you want a full buy-out or will you carry a note on the property?

Are you willing to rent the farm for some period of time?

Will you consider a reverse mortgage?

98

Page 98 of 79

Who do you want in the next meeting? What do you want to accomplish (e.g. determine if

children want the farm, when, and under what terms). Have you discussed this topic with the children to

determine their interest and issues? What is your plan to ensure harmony, if possible?

99

Page 99 of 79

The process should end with wills, advanced directives, Power of Attorney, insurance, and agreements for purchase if appropriate.

100

Page 100 of 79

The Second Meeting… A family meeting Communication, Communication,

Communication Review discussions of first meetings Focus on results Design the family goals

101

Page 101 of 79

Goals

List the most important goals for the family.

The following are examples…

102

Page 102 of 79

1. Establish the who and how of transition of the farm.

2. Determine which children, if any, have an interest in working the farm.

3. Discuss and plan for equality of treatment between family members.

4. Establish a retirement plan, and a method of funding it.

103

Page 103 of 79

5. Account for events that can deter the plan and implement methods of dealing with those risks.

6. Establish wills and advanced directives and Power of Attorney.

7. Execute any documents that are needed to implement the plan.

104

Page 104 of 79

Risk Reduction

There are risks to any transition plan:

Disability Nursing Home Costs Change

105

Page 105 of 79

DisabilityA severe disability can significantly reduce income causing

acceleration of transfer or general dissolution of the plan.

– Rental Income– Social Security Disability– Private Disability Plans– Outside Income Group Plans– Retirement Plans

106

Page 106 of 79

Nursing Home Costs

Rental Income Retirement Income Long Term Care Insurance

107

Page 107 of 79

Dealing with Transition

The best laid plans often go astray.

Never has this been truer than with farm transition planning.

108

Page 108 of 79

1. It must be updated periodically.

2. It requires an impetus at time of implementation. (Who’s in charge of starting the transition)

3. The owners must deal with the emotional issues of change. (The Hero’s Farewell by Jeffrey A. Sonnenfeld).

109

Page 109 of 79

Final Tips

Volunteer to be the quarterback. Start Now Communicate openly with family

members about the transition goals and plan.

110

Page 110 of 79

Establish a vision and execute the documents to enable it to happen.

Deal with family equity. Select advisors and empower them to

do their job.

111

Page 111 of 79

Build a plan that makes you feel comfortable, and makes your family members feel they are being heard.

Implement the tools that you feel are necessary to reduce the risks in the plan.

Review the plan regularly.

112

Page 112 of 79

Thank You!

Thank you for attending today. Please fill out the evaluation form.