Embed Size (px)

Citation preview

1

Principles of AccountingPrinciples of Accounting•• Kimmel Kimmel •• Weygandt Weygandt •• Kieso Kieso

Chapter 10Chapter 10

Reporting and Analyzing Liabilities

Prepared by Barbara MullerPrepared by Barbara MullerArizona State University WestArizona State University West

John Wiley & Sons, Inc. © 2005

2

Chapter 10

Reporting and Analyzing LiabilitiesAfter studying this chapter, you should be able to:

Explain a current liability and identify the major types of current liabilities.

Describe the accounting for notes payable.Explain the accounting for other current

liabilities.Identify the types of bonds.

3

After studying this chapter, you should be able to:

Prepare the entries for the issuance of bonds and interest expense.

Describe the entries when bonds are redeemed.

Identify the requirements for the financial statement presentation and analysis of liabilities.

Chapter 10

Reporting and Analyzing Liabilities

4

Current Liabilities STUDY OBJECTIVE 1

Current liabilities are debts which can reasonably be expected to be paid

• From existing current assets or through the creation of other current liabilities

• Within 1 year or the operating cycle, whichever is longer

Debts that do not meet both criteria are Long-Term Liabilities

5

Types of Current Liabilities

Notes Payable Accounts Payable Unearned Revenues Accrued Liabilities

• Taxes• Salaries and Wages• Interest

6

Let’s ReviewLet’s Review

The time period for classifying a liability as The time period for classifying a liability as current is one year or the operating cycle, current is one year or the operating cycle, whichever is:whichever is:a.a. longer.longer.

d.d. possible. possible.

c.c. probable. probable.

b.b. shorter. shorter.

7

Let’s ReviewLet’s Review

The time period for classifying a liability as The time period for classifying a liability as current is one year or the operating cycle, current is one year or the operating cycle, whichever is:whichever is:a.a. longer.longer.

d.d. possible. possible.

c.c. probable. probable.

b.b. shorter. shorter.

8

Notes PayableSTUDY OBJECTIVE 2

Notes payable are• Obligations in the form of written notes• Often used instead of accounts payable; they give

written documentation if needed for legal remedies• Used for short-term and long-term financing needs• Usually require the borrower to pay interest

9

Note Payable

10

Remember - Interest accrues over life of the note and must be recorded periodically.

JournalSept 1 Cash 100,000

Notes Payable 100,000 (To record issuance of 12%, 4-month note to bank)

Dec 31 Interest Expense 4,000Interest Payable 4,000

(To accrue interest for 4 months on note)

$100,000 x .12 x 4\12 months

11

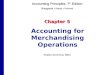

JournalJan 1 Notes Payable 100,000

Interest Payable 4,000

Cash 104,000

(To record payment of 1st National Bank interest-bearing note

and accrued interest at maturity)

12

Sales Taxes Payable STUDY OBJECTIVE 3

Are collected from customers Are expressed as a % of sales

price Are required by state law. Remitted to the state monthly Usually rung separately from

sales on the cash register.

13

Journal

Mar 25 Cash 10,600 Sales

10,000Sales Taxes Payable

600(To record daily sales and sales taxes)

14

Payroll Deductions

15

Payroll Taxes

Various payroll taxes are required by law to be withheld from employees’ gross pay• Social Security (FICA) taxes withheld, employer

and employee make equal contributions• Federal income taxes

• State income taxes (if applicable)

16

Journal

Mar 7 Salaries and Wages Expense 100,000FICA Taxes Payable (employee’s share)

7,250Federal Income Taxes Payable 21,864States Income Taxes Payable 2,922Salaries and Wages Payable 67,964

Mar 7 Salaries and Wages Payable 67,964 Cash

67,964

17

Journal

Mar 7 Payroll Tax Expense 13,450 FICA Taxes Payable (employer’s share) 7,250Federal Unemployment Taxes Payable 800State Unemployment Taxes Payable 5,400

Employers incur a second type of payroll-related activity.1) Employer’s share of FICA2) Federal unemployment3) State unemployment

18

Unearned Revenue

Unearned revenue is cash received before service or product is delivered (that is, before revenue is earned)

Recorded as a liability until it is earned

19

Unearned Revenues Examples of unearned revenues• Magazine subscriptions

• Rent received in advance

• Customer deposits for future service

• Sale of airline tickets for future travel

• Sale to season sporting events

20

As each game is completed

JournalAug 6 Cash 500,000

Unearned Ticket Revenue 500,000

(To record sale of 10,000 tickets at $50 each)

Sept 7 Unearned Ticket Revenue 100,000

Ticket Revenue 100,000

(To record ticket revenue earned)

21

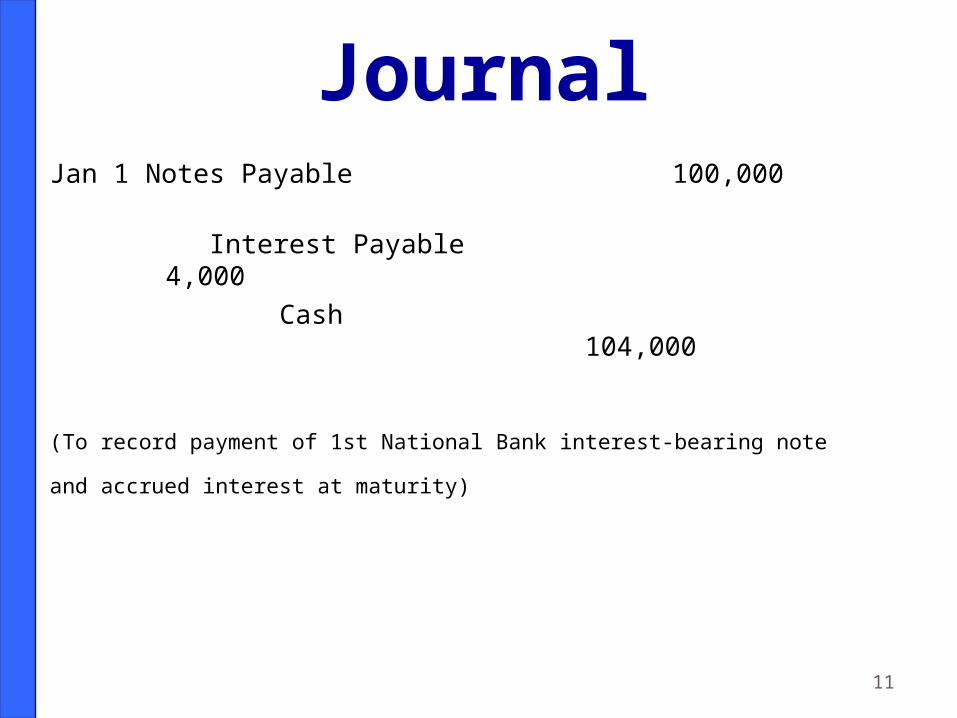

Current Maturities of Long-Term Debt

Current maturities of long-term debt are• The portion of long-term debt due within the

current year or operating cycle

• Classified as a current liability

• No adjusting entry is necessary

22

FICTICTIOUS COMPANYBalance Sheet

December 31, 2004AssetsCurrent Assets

Cash $ 272Marketable securities (current) 609Receivables 74Other current assets 83

Total current assets 1,038Property and equipment (net) 317

Marketable securities (long-term) 322 Other long-term assets 280 Total Assets $1,957 Liabilities and Stockholders’ Equity Liabilities

Current LiabilitiesAccounts payable $ 527

Notes payable 133Current maturities of long term debt 100Accrued liabilities and expenses 56 Total current liabilities 816

Long-term debt 83 Total liabilities 899

Stockholders’ equityCommon stock 830Retained earnings 228

Total Liabilities and stockholders’ equity $1,957

23

Bonds STUDY OBJECTIVE 4

Bonds• A form of long-term, interest-bearing note payable issued by

corporations, universities and governmental agencies

• Sold in small denominations, (usually multiples of $1,000) which makes them attractive to investors

• Are in the form of a legal document that indicates the name of the issuer, the face value of the bonds, the contractual interest rate, and the maturity date

24

Bond Certificate

25

Bond Features

Bonds have many different features

• Secured bonds have specific assets pledged as collateral, unsecured do not

• Convertible bonds may be converted into common stock at the bondholder’s option

• Callable bonds are subject to retirement at a stated dollar amount prior to maturity

26

Accounting for Bond Issues STUDY OBJECTIVE 5

Bonds may be issued at• Face value wheno stated rate = market rate

• Below face value (discount) wheno stated rate < market rate must discount price to get

investors to buy

• Above face value (premium) wheno stated rate > market rate all investors want to own so the

price is bid up

27

Interest Rates and Bond Prices

28

Bond Terms

Face Value the amount of principal due at the maturity date of the bond

Discount when a bond is sold for less than its face value (the difference between the face value of a bond and its selling price)

Premium - when a bond is sold for more than its face value (the difference between the selling price and the face value of a bond)

29

Cash Flow of Bonds

30

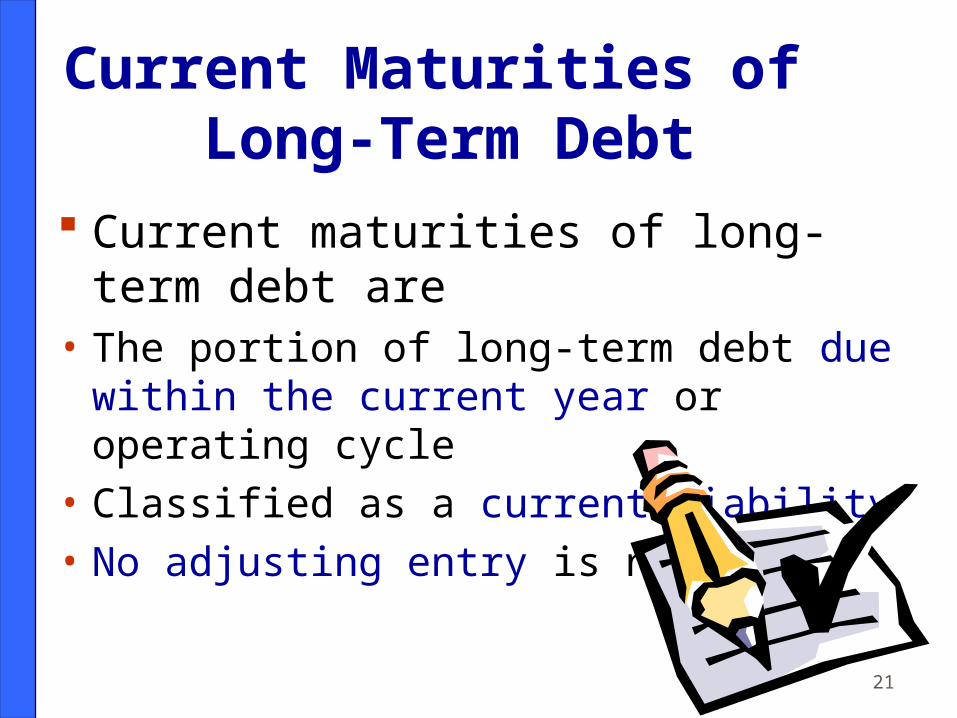

Selling Bonds at Discount

On January 1, 2005, Candlestick, Inc., sells $100,000, 5-year, 10% bonds at 98 with interest payable on January 1.

Jan 1 Cash 98,000 Discount on Bonds Payable 2,000* Bonds Payable 100,000

(To record sale of bonds at a discount)

*The discount account is a contra account to the bond payable, not an asset account.

31

Statement Presentation of Discounted Bonds

Long-term liabilities

Bonds payable $ 100,000

Less: Discount on bonds payable 2,000 $98,000

Carrying Value

32

Selling Bonds at Premium On January 1, 2005, Candlestick, Inc., sells $100,000, 5-year,

10% bonds at 102 with interest payable on January 1.

Jan 1 Cash 102,000 Bonds

Payable 100,000

Premium Bonds Payable 2,000*

(To record sale of bonds at a premium)

*Premium is added to bonds payable on the balance sheet

33

Statement Presentation of Premium Bonds

Long-term liabilities

Bonds payable $ 100,000

Add : Premium on bonds payable 2,000 $102,000

Carrying Value

34

Amortizing Bond Discount/Premium

Candlelight would amortize the $2,000 discount/premium as follows

$2,000 ÷ 5 Interest Periods

= $400 Annually

35

Amortization of Bond Discount

36

Amortization of Bond Premium

37

Bond Retirements STUDY OBJECTIVE 6

Bonds may be redeemed at maturity or before maturity

38

Redeeming Bonds Before Maturity

A company may decide to retire bonds before maturity to• reduce interest cost • remove debt from its balance sheet

A company should retire debt early only if it has sufficient cash resources

39

Redeeming Bonds Before Maturity

When bonds are retired before maturity, it is necessary to • Eliminate the carrying value of the bonds at the

redemption date• Record the cash paid• Recognize the gain or loss on redemption• The carrying value of the bonds is the bond payable

plus the premium or minus the discount

40

Financial Statement Presentation and AnalysisSTUDY OBJECTIVE 7

Current liabilities are listed first under “Liabilities” on the balance sheet

A common method is to list the current liabilities in order of magnitude, beginning with the largest

Long-term liabilities are listed in a separate section of the balance sheet

41

General Motors Corporation- Automotive Division Statement of Cash Flows (partial)

2001(in millions)

Cash flows from financing activitiesNet increase (decrease) in loans payable $ 194 Long-term debt - borrowings 5,850Long-term debt-repayments (2,602)Repurchases of common and preferred stocks (264)Proceeds from issuing common and preferred stocks 517Cash dividends paid to stockholders (1,201)Net cash (used in) provided by financing activities $2,494

42

ANALYSIS Debt to Total Assets Ratio indicates the extent to which a

company’s debt could be repaid by liquidating assets Times Interest Earned Ratio indicates a company’s ability

to meet interest payments as they become due

43

ANALYSIS

Unrecorded debt occurs because sometimes a company’s balance sheet does not properly record or disclose all its debts

• Contingencies are events with uncertain outcomes (lawsuits, warranties, etc)

• “Off-balance sheet financing” occurs when the company borrows funds in such a way that the obligations are not recorded (leases)

44

Let’s ReviewLet’s Review

What term is used for bonds that have What term is used for bonds that have specific assets pledged as collateral:specific assets pledged as collateral:

a.a. callable bonds.callable bonds.

d.d. discount bonds. discount bonds.

c.c. secured bonds. secured bonds.

b.b. convertible bonds. convertible bonds.

45

Let’s ReviewLet’s Review

What term is used for bonds that have What term is used for bonds that have specific assets pledged as collateral:specific assets pledged as collateral:

a.a. callable bonds.callable bonds.

d.d. discount bonds. discount bonds.

c.c. secured bonds.secured bonds.

b.b. convertible bonds. convertible bonds.

46

Copyright © 2002 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

COPYRIGHT