Embed Size (px)

Citation preview

1

Reverse Mortgages

A consumer perspective

Kelli Jo Greiner, Elderly Health Care Programs Specialist Consumer Information Assistance and Advocacy Team

August 6, 2004

2

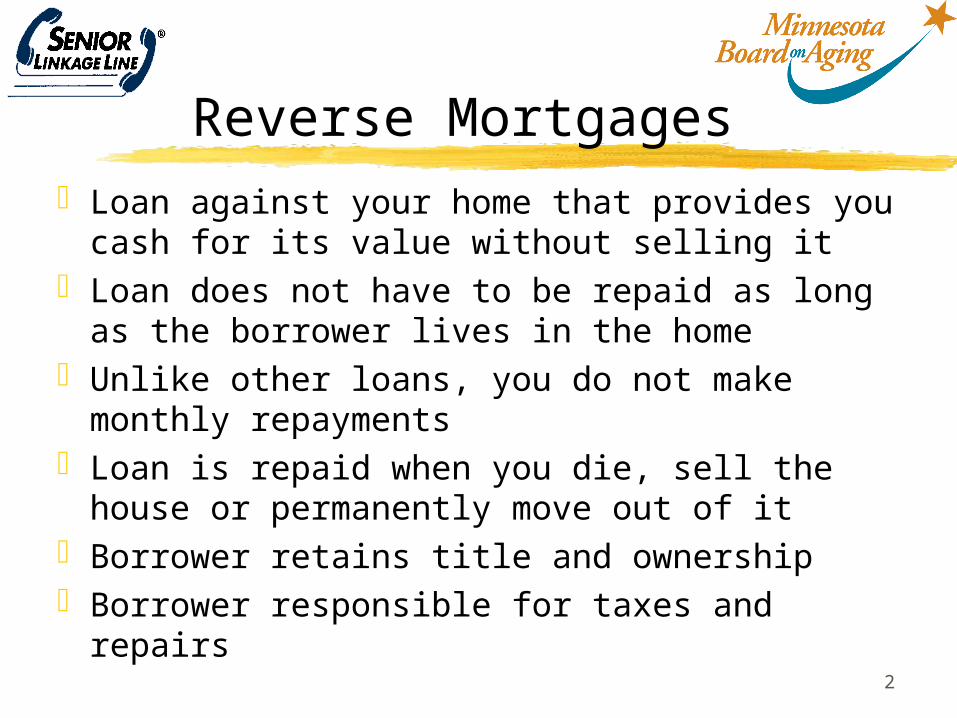

Reverse MortgagesLoan against your home that provides you

cash for its value without selling itLoan does not have to be repaid as long

as the borrower lives in the homeUnlike other loans, you do not make

monthly repaymentsLoan is repaid when you die, sell the

house or permanently move out of itBorrower retains title and ownershipBorrower responsible for taxes and repairs

3

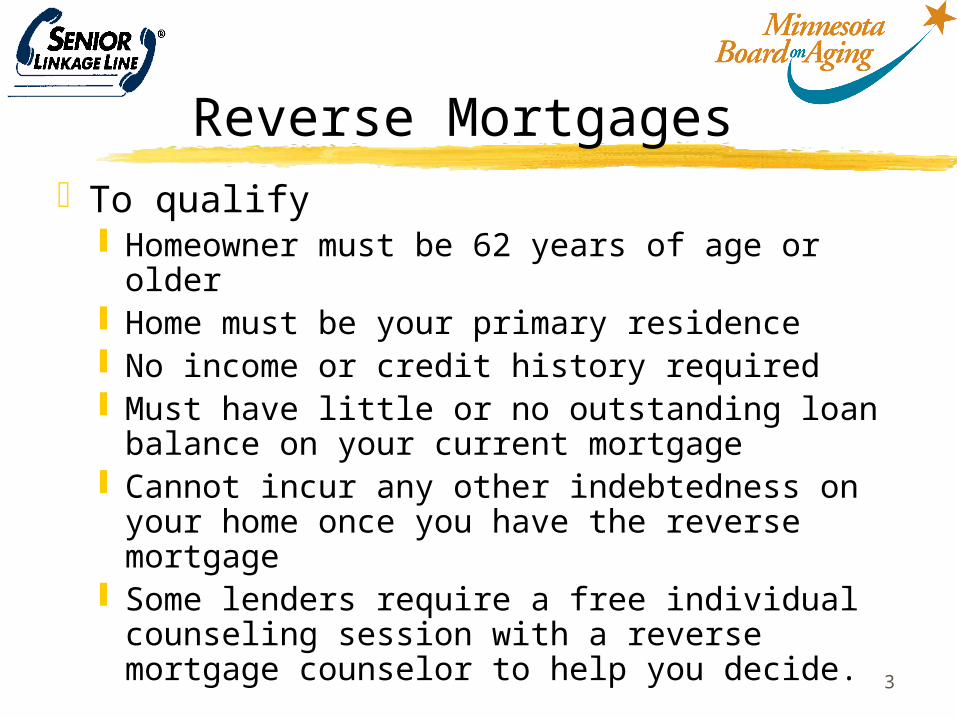

Reverse MortgagesTo qualify

Homeowner must be 62 years of age or older

Home must be your primary residence No income or credit history required Must have little or no outstanding loan

balance on your current mortgage Cannot incur any other indebtedness on your

home once you have the reverse mortgage Some lenders require a free individual

counseling session with a reverse mortgage counselor to help you decide.

4

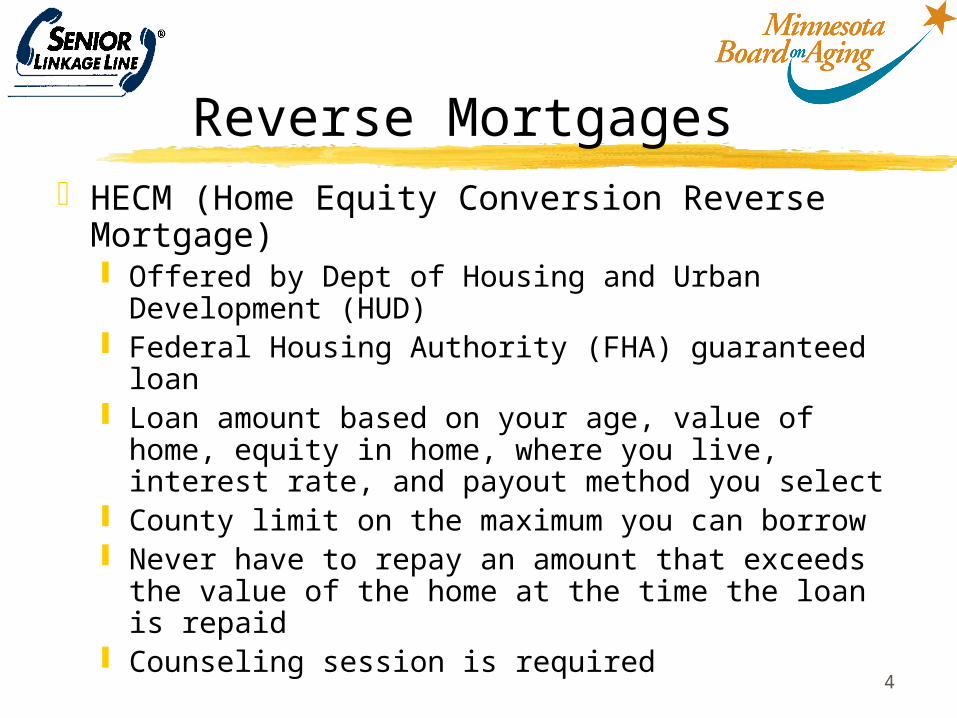

Reverse MortgagesHECM (Home Equity Conversion Reverse

Mortgage) Offered by Dept of Housing and Urban

Development (HUD) Federal Housing Authority (FHA) guaranteed loan Loan amount based on your age, value of home,

equity in home, where you live, interest rate, and payout method you select

County limit on the maximum you can borrow Never have to repay an amount that exceeds

the value of the home at the time the loan is repaid

Counseling session is required

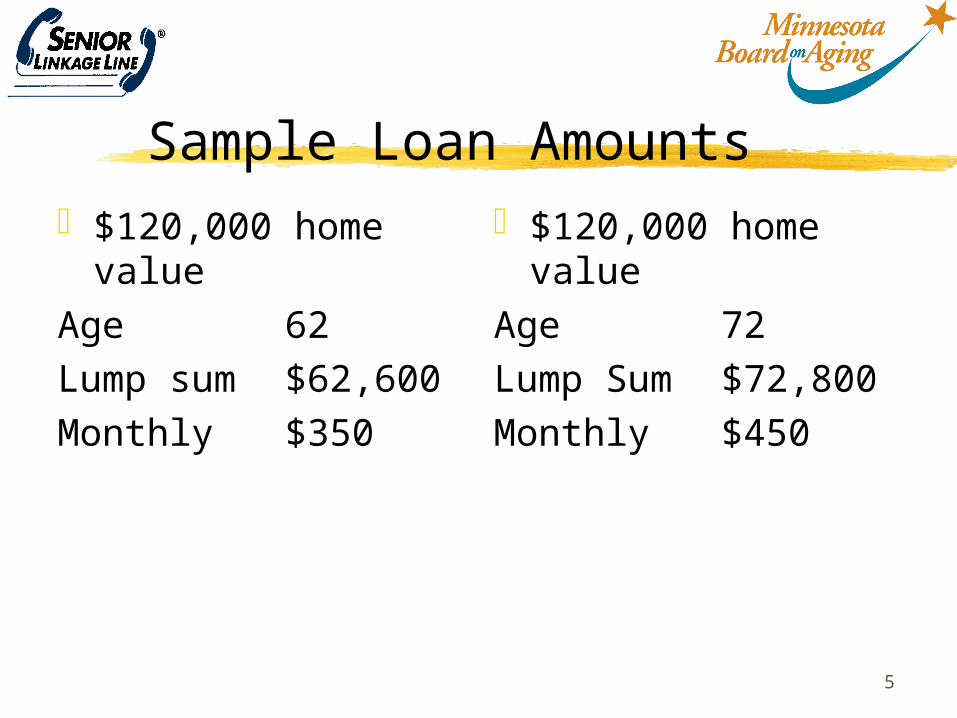

5

Sample Loan Amounts$120,000 home

valueAge 62Lump sum $62,600Monthly $350

$120,000 home value

Age 72Lump Sum $72,800Monthly $450

6

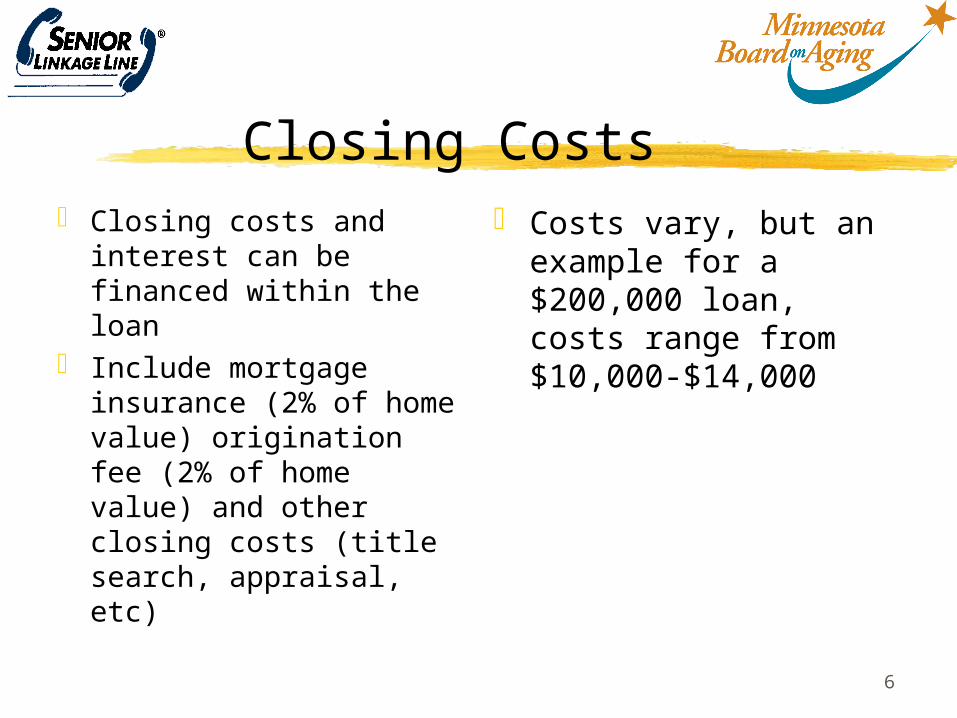

Closing Costs Closing costs and

interest can be financed within the loan

Include mortgage insurance (2% of home value) origination fee (2% of home value) and other closing costs (title search, appraisal, etc)

Costs vary, but an example for a $200,000 loan, costs range from $10,000-$14,000

7

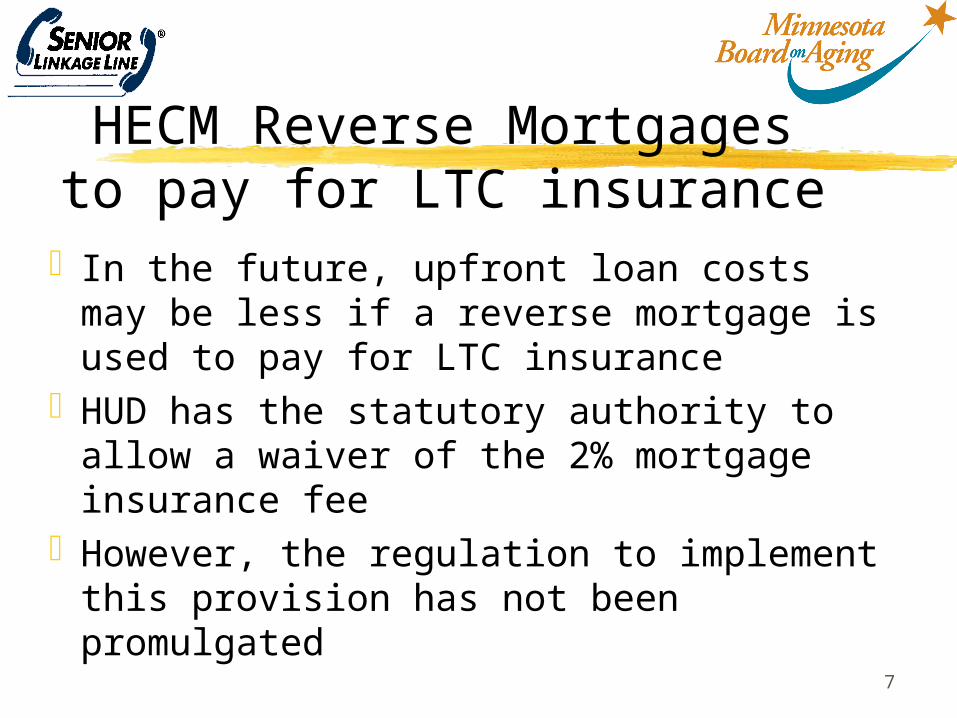

HECM Reverse Mortgages to pay for LTC insurance

In the future, upfront loan costs may be less if a reverse mortgage is used to pay for LTC insurance

HUD has the statutory authority to allow a waiver of the 2% mortgage insurance fee

However, the regulation to implement this provision has not been promulgated

8

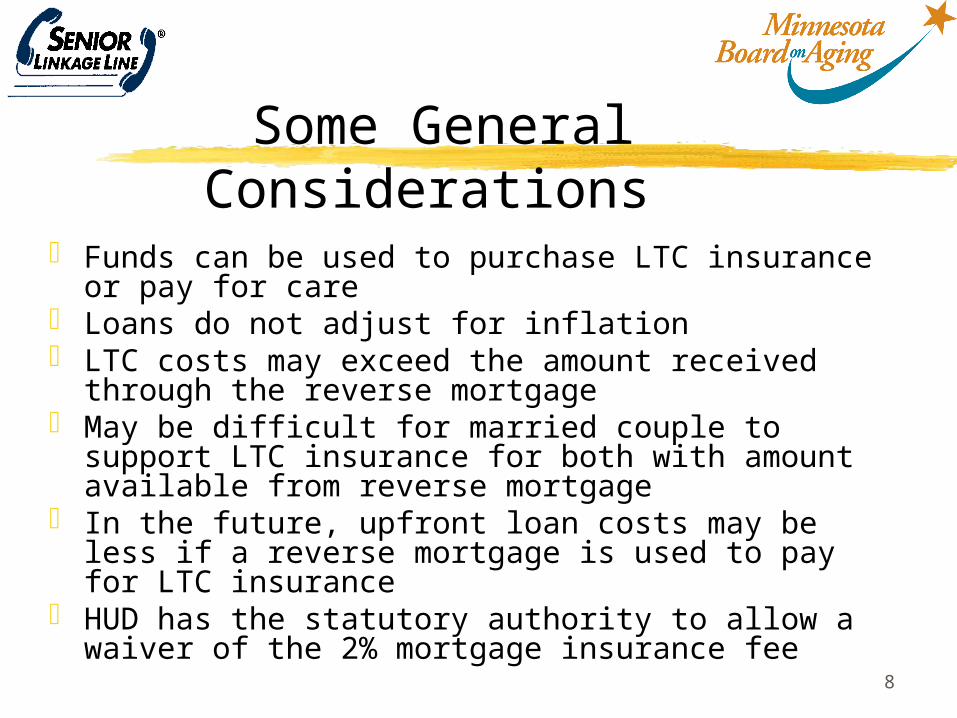

Some General Considerations

Funds can be used to purchase LTC insurance or pay for care

Loans do not adjust for inflation LTC costs may exceed the amount received

through the reverse mortgage May be difficult for married couple to support LTC

insurance for both with amount available from reverse mortgage

In the future, upfront loan costs may be less if a reverse mortgage is used to pay for LTC insurance

HUD has the statutory authority to allow a waiver of the 2% mortgage insurance fee

9

Some General Considerations

Heirs can retain home by repaying reverse mortgage

Heirs can “keep the difference” if the home’s sale price exceeds the loan balance at the time the loan is repaid

10

Some General Considerations

Consumers for the most part are unaware of reverse mortgages

Must address the issue of “leaving my house to my kids”

Few people know about or have considered using a reverse mortgage for LTC

Must have objective, neutral sources

11

Spreading the word:The CMS Long-term care

initiativePurpose

Increase consumer awareness of the options available to plan for and finance long-term care, including long-term care insurance and the use of reverse mortgages

12

Spreading the word:The CMS Long-term care

initiativeAwareness Campaign

Under development Will promote financing options including

the reverse mortgage/LTC insurance option

13

For Assistance….

Call Minnesota Senior LinkAge Line® at 1-800-333-2433 (for all 87 counties) All staff are certified health

insurance counselors Phone, in person and community

based assistance available