Embed Size (px)

Citation preview

1

Some Observations on Current Trends in Public

Policy & Budgeting

Barry AndersonDeputy Director

National Governors [email protected]

March 13, 2012

1

2

My Goal TodayDiscuss a series of observations

on current trends in public policy and budgeting

These observations are not intended to be definitive or all inclusive, but I hope they will be thought-provoking, or at least entertaining

2

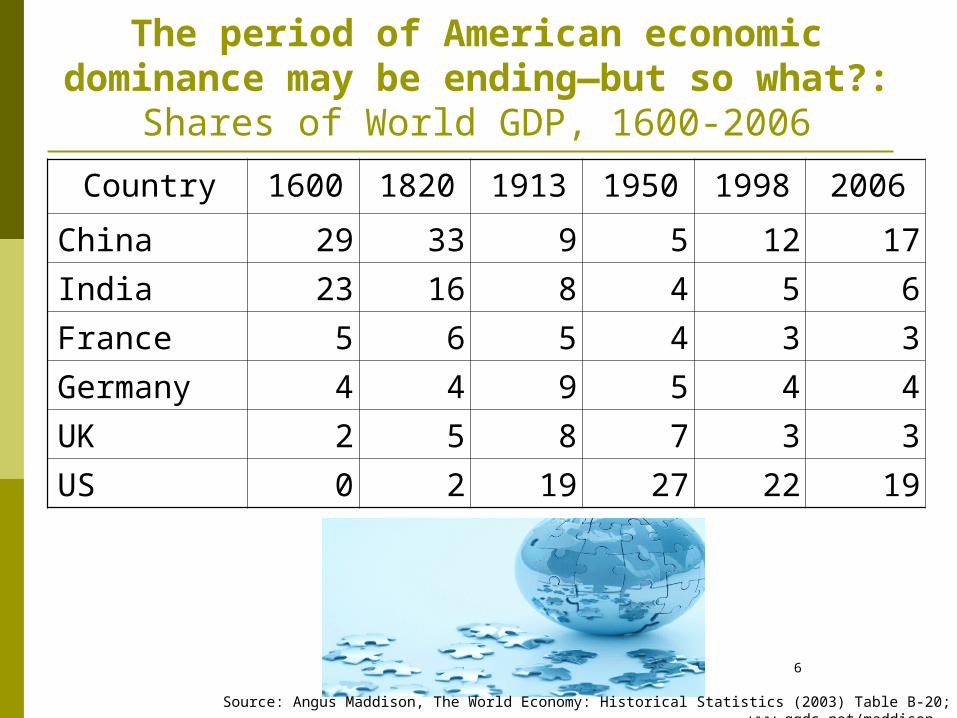

Some Observations The period of American economic dominance may be

ending—but so what? And it is not at all clear that State Capitalism will dominate

in the long run. Adaptability may be our most valuable asset. Our inherent ability to think strategically, which may be a

product of our political system(!), is also an asset. Speaking of our political system, some good news: more

competitive House races. A positive budget trend: long-term budget projections. As to the budget caps: what’s wrong with what works? In fact, the Europeans should learn from us: shuck their GRH

& adopt a BEA. With respect to tax reform, could there be agreement on

“broaden the base & lower the rates”? But isn’t the budget process broken beyond repair? A final word on What We Will See in the Year Ahead.3

4

About Me—Experience

30+ Years in Federal Budgeting GAO OMB: Senior Career Civil Servant CBO: Acting & Deputy Director

FASAB

IMF in WashingtonOECD in ParisIndependent ConsultantNational Governors Ass’n

4

5

About Me—Personal

Not an ‘R’ or a ‘D’, but an SOB! An “Card-Carrying Middle of the Roader”

5

6

The period of American economic dominance may be ending—but so

what?:Shares of World GDP, 1600-2006

Country 1600 1820 1913 1950 1998 2006

China 29 33 9 5 12 17

India 23 16 8 4 5 6

France 5 6 5 4 3 3

Germany 4 4 9 5 4 4

UK 2 5 8 7 3 3

US 0 2 19 27 22 19

Source: Angus Maddison, The World Economy: Historical Statistics (2003) Table B-20; www.ggdc.net/maddison

And it is not at all clear that State Capitalism will dominate in the

long run State Owned Enterprises (SOEs, including sovereign funds,

Chinese banks, State-controlled energy companies) have advantages Mimic the market Import Western ideas Impose some discipline

But their disadvantages—especially in the areas of liberty & scrutiny—outweigh their pros Can states regulate the companies that they run? Can SOEs stop throwing good money after bad—no market discipline? Can SOEs innovate when innovation requires freedom to experiment? Can effective oversight be provided by politicians? Can SOEs operate efficiently with both commercial & social missions? Can SOEs institute effective cost controls to inform stakeholders and

discourage corruption?7

Adaptability may be our most valuable asset—the view from

Sacre Couer

8

Our inherent ability to think strategically, which may be a

product of our political system(!), is also an asset

9

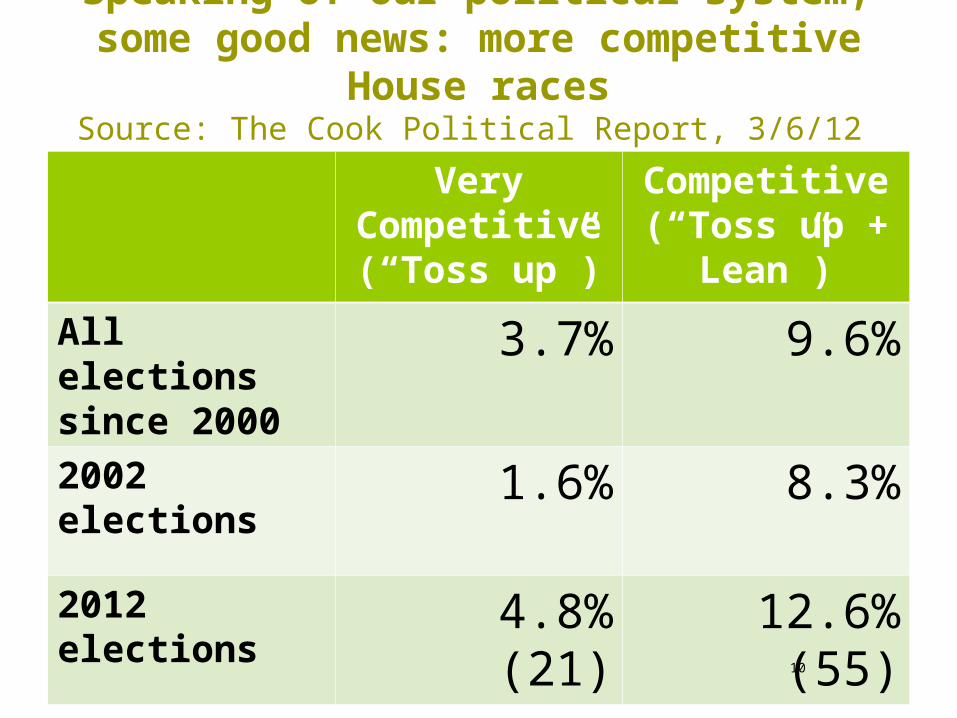

Speaking of our political system, some good news: more competitive

House racesSource: The Cook Political Report, 3/6/12

Very Competitive(“Toss up”)

Competitive(“Toss up +

Lean”)

All elections since 2000

3.7% 9.6%

2002 elections

1.6% 8.3%

2012 elections

4.8%(21)

12.6%(55)10

11

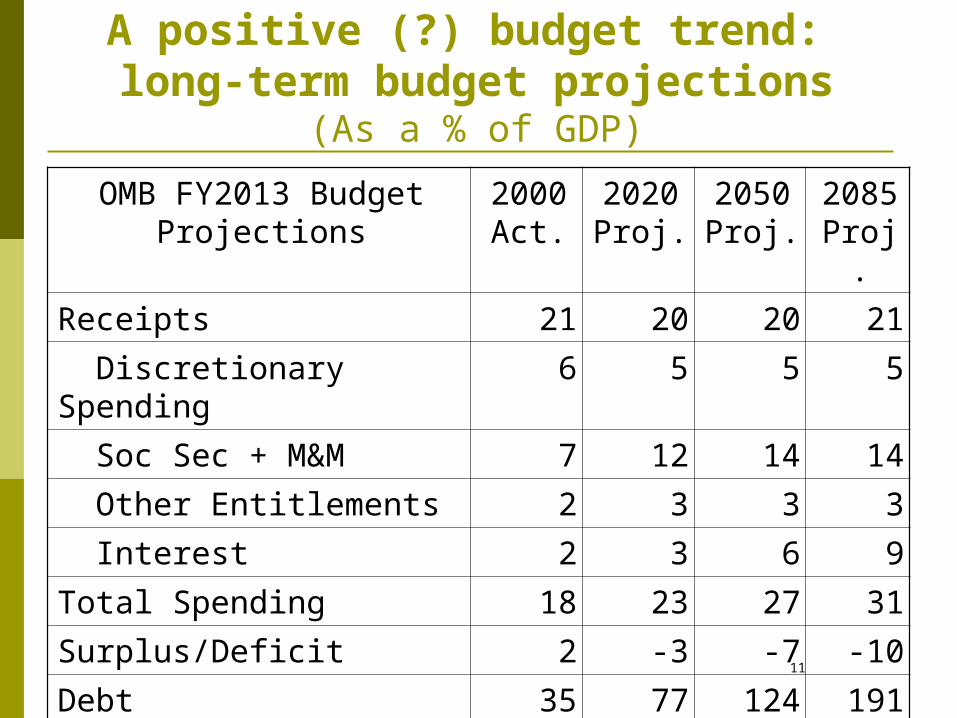

A positive (?) budget trend: long-term budget projections

(As a % of GDP)

OMB FY2013 Budget Projections

2000 Act.

2020 Proj.

2050 Proj.

2085 Proj.

Receipts 21 20 20 21

Discretionary Spending 6 5 5 5

Soc Sec + M&M 7 12 14 14

Other Entitlements 2 3 3 3

Interest 2 3 6 9

Total Spending 18 23 27 31

Surplus/Deficit 2 -3 -7 -10

Debt 35 77 124 191

12

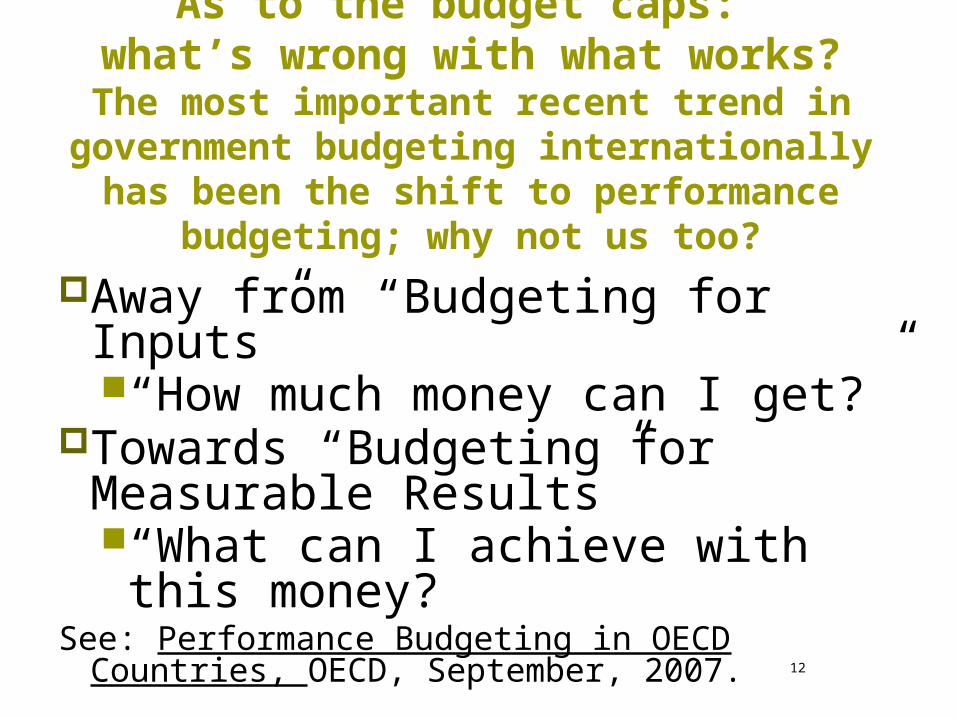

As to the budget caps: what’s wrong with what works?The most important recent trend in

government budgeting internationally has been the shift to performance

budgeting; why not us too?

Away from “Budgeting for Inputs” “How much money can I get?”

Towards “Budgeting for Measurable Results”“What can I achieve with this

money?See: Performance Budgeting in OECD Countries, OECD,

September, 2007.

13

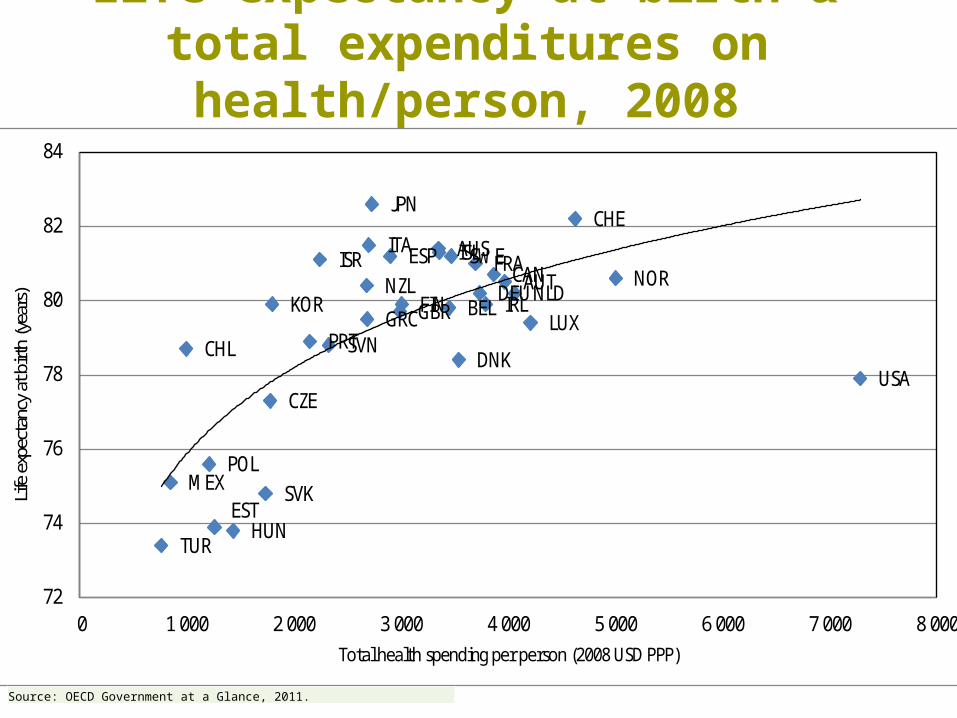

Life expectancy at birth & total expenditures on health/person,

2008

14

AUS

AUTBEL

CAN

CHL

CZE

DNK

EST

FIN

FRADEU

GRC

HUN

ISL

IRL

ISRITA

JPN

KORLUX

MEX

NLDNZL NOR

POL

PRT

SVK

SVN

ESP SWE

CHE

TUR

GBR

USA

72

74

76

78

80

82

84

0 1 000 2 000 3 000 4 000 5 000 6 000 7 000 8 000

Life

expe

ctan

cy a

t birt

h (y

ears

)

Total health spending per person (2008 USD PPP)

Source: OECD Government at a Glance, 2011.

15

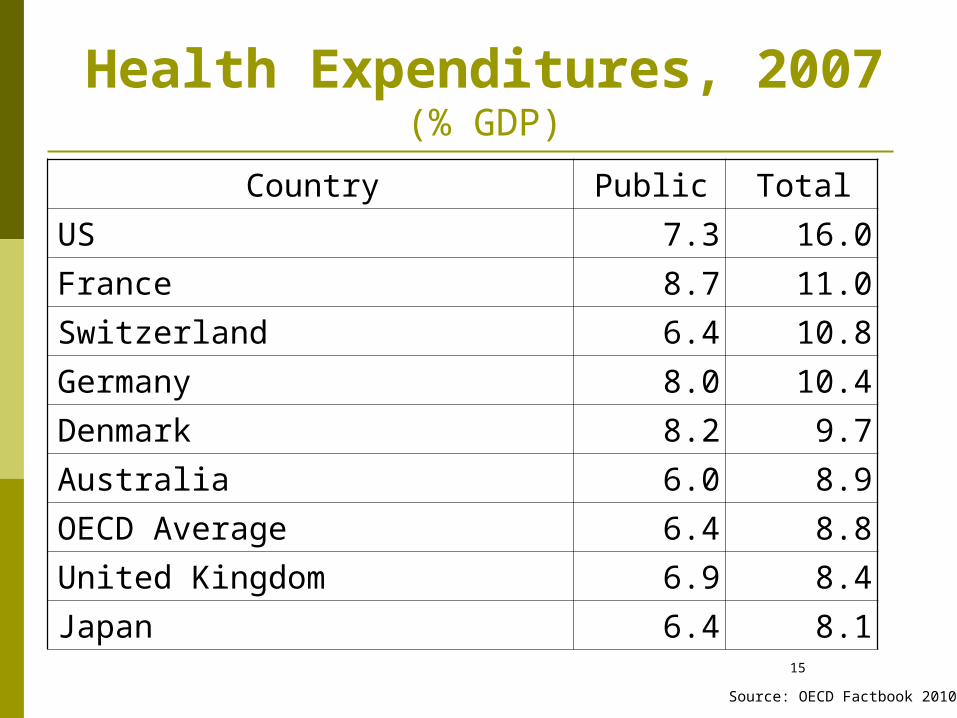

Health Expenditures, 2007(% GDP)

Country Public Total

US 7.3 16.0

France 8.7 11.0

Switzerland 6.4 10.8

Germany 8.0 10.4

Denmark 8.2 9.7

Australia 6.0 8.9

OECD Average 6.4 8.8

United Kingdom 6.9 8.4

Japan 6.4 8.1

Source: OECD Factbook 2010

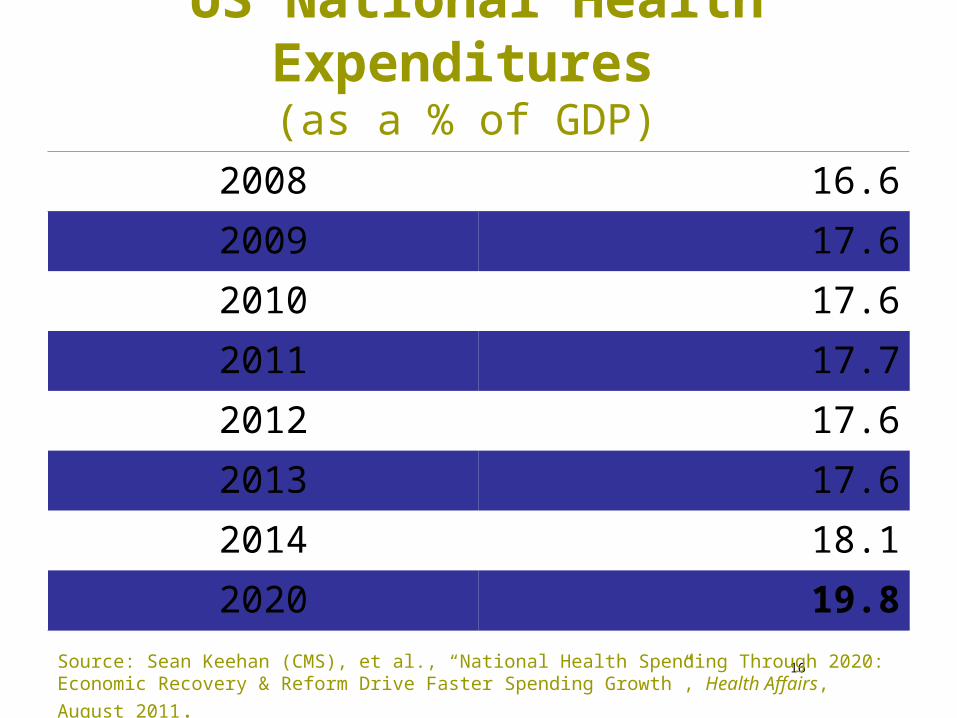

US National Health Expenditures

(as a % of GDP) 2008 16.6

2009 17.6

2010 17.6

2011 17.7

2012 17.6

2013 17.6

2014 18.1

2020 19.8

16Source: Sean Keehan (CMS), et al., “National Health Spending Through 2020: Economic

Recovery & Reform Drive Faster Spending Growth”, Health Affairs, August 2011.

17

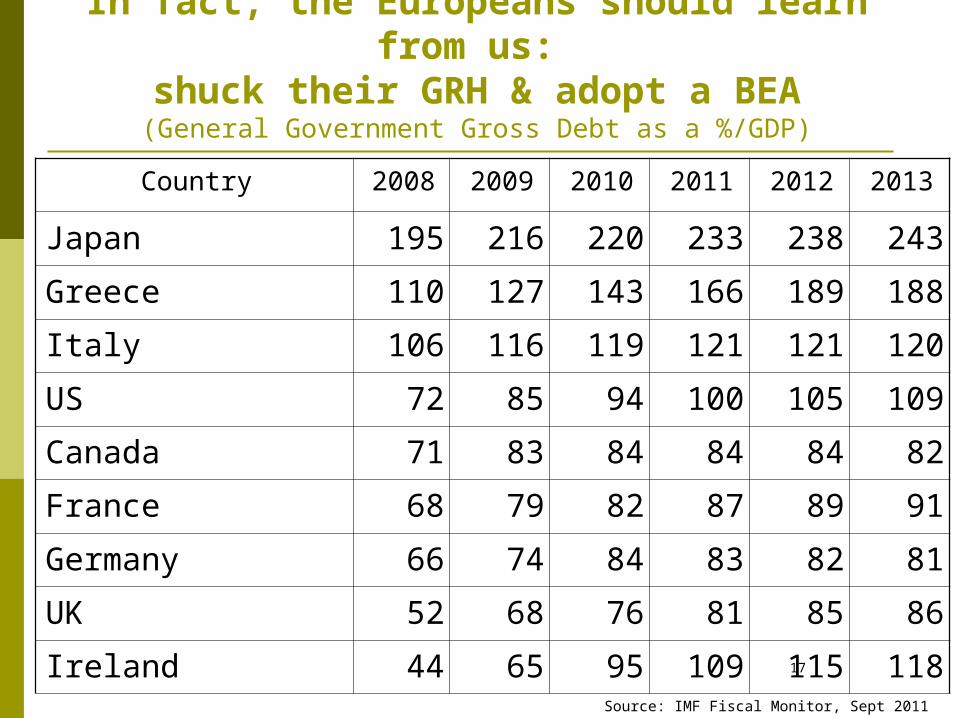

In fact, the Europeans should learn from us:

shuck their GRH & adopt a BEA(General Government Gross Debt as a %/GDP)

Country 2008 2009 2010 2011 2012 2013

Japan 195 216 220 233 238 243

Greece 110 127 143 166 189 188

Italy 106 116 119 121 121 120

US 72 85 94 100 105 109

Canada 71 83 84 84 84 82

France 68 79 82 87 89 91

Germany 66 74 84 83 82 81

UK 52 68 76 81 85 86

Ireland 44 65 95 109 115 118Source: IMF Fiscal Monitor, Sept 2011

17

18

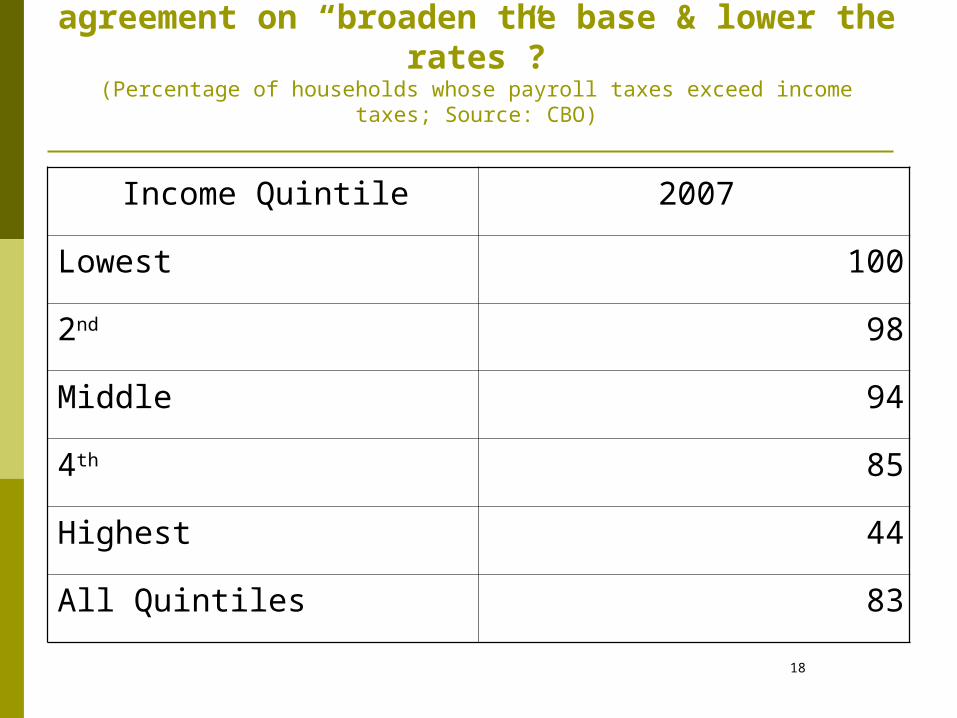

With respect to tax reform, could there be agreement on “broaden the base & lower

the rates”?(Percentage of households whose payroll taxes exceed income taxes; Source:

CBO)

Income Quintile 2007

Lowest 100

2nd 98

Middle 94

4th 85

Highest 44

All Quintiles 83

19

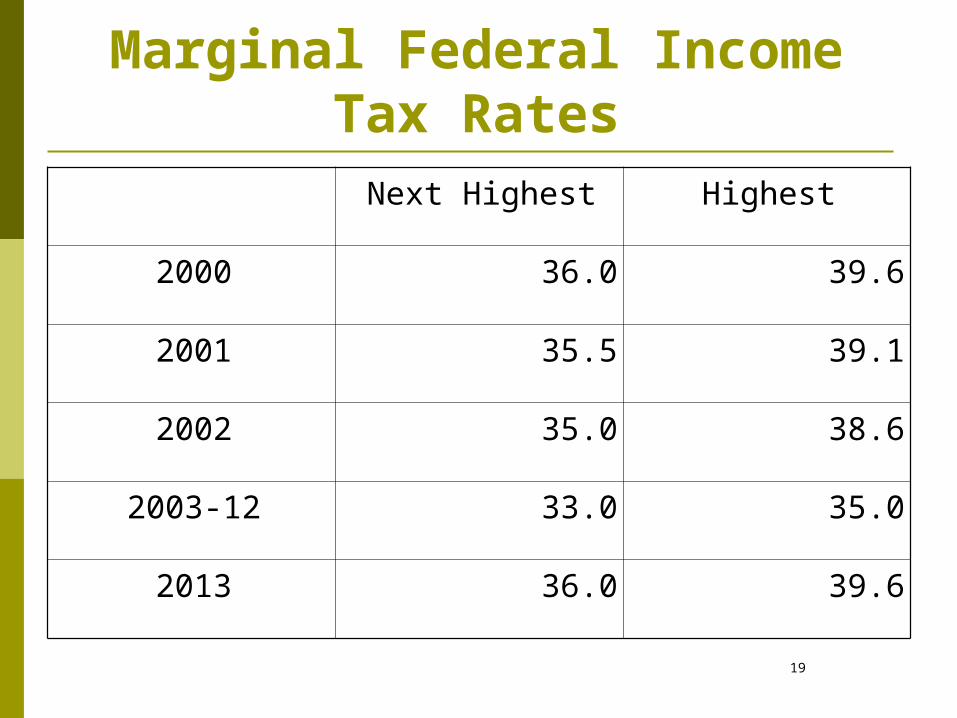

Marginal Federal Income Tax Rates

Next Highest Highest

2000 36.0 39.6

2001 35.5 39.1

2002 35.0 38.6

2003-12 33.0 35.0

2013 36.0 39.6

20

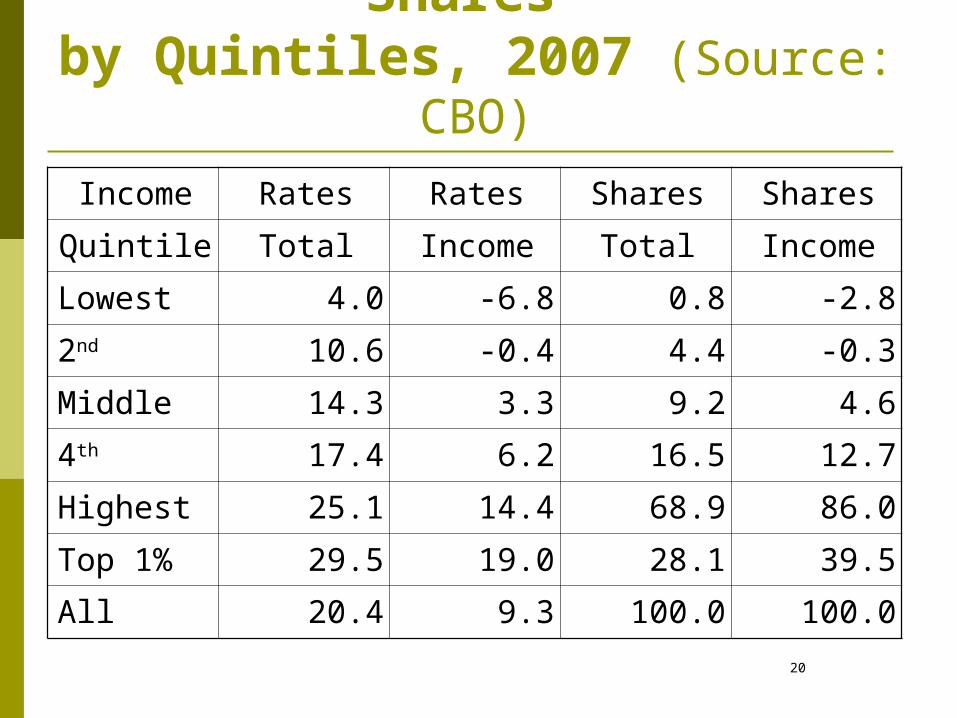

Effective Tax Rates & Shares

by Quintiles, 2007 (Source: CBO)

Income Rates Rates Shares Shares

Quintile Total Income Total Income

Lowest 4.0 -6.8 0.8 -2.8

2nd 10.6 -0.4 4.4 -0.3

Middle 14.3 3.3 9.2 4.6

4th 17.4 6.2 16.5 12.7

Highest 25.1 14.4 68.9 86.0

Top 1% 29.5 19.0 28.1 39.5

All 20.4 9.3 100.0 100.0

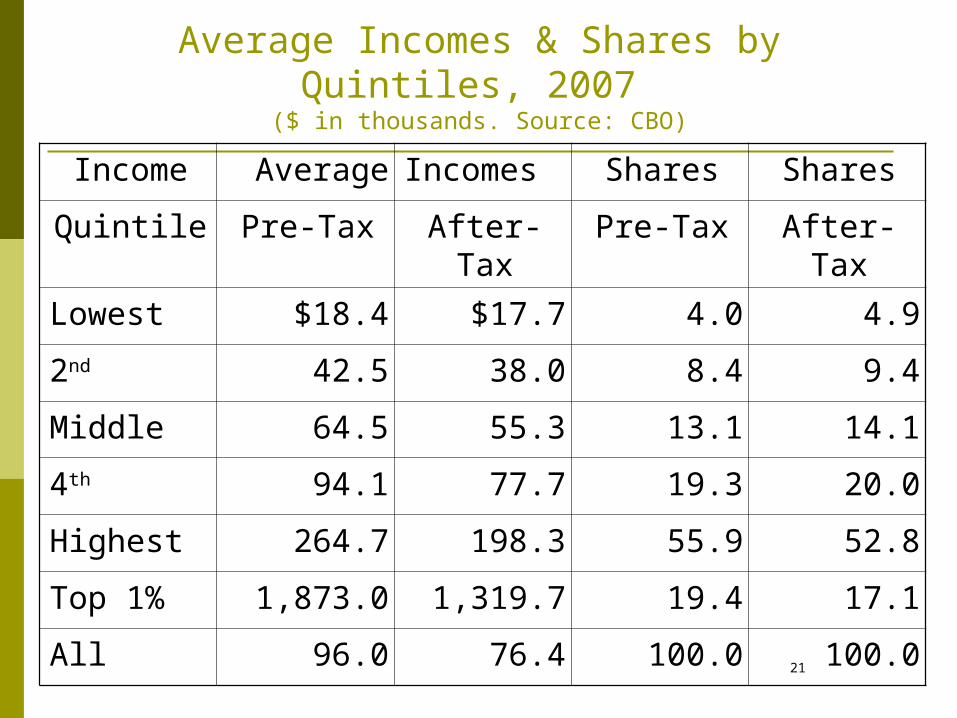

21

Income Average Incomes Shares Shares

Quintile Pre-Tax After-Tax Pre-Tax After-Tax

Lowest $18.4 $17.7 4.0 4.9

2nd 42.5 38.0 8.4 9.4

Middle 64.5 55.3 13.1 14.1

4th 94.1 77.7 19.3 20.0

Highest 264.7 198.3 55.9 52.8

Top 1% 1,873.0 1,319.7 19.4 17.1

All 96.0 76.4 100.0 100.0

Average Incomes & Shares by Quintiles, 2007

($ in thousands. Source: CBO)

22

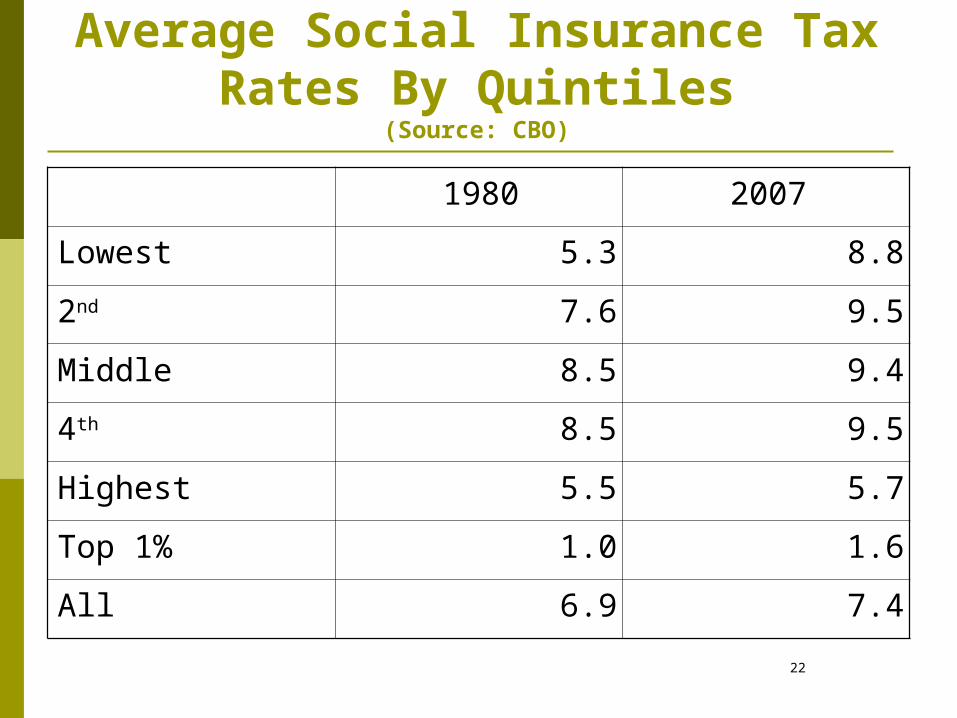

Average Social Insurance Tax Rates By Quintiles

(Source: CBO)

1980 2007

Lowest 5.3 8.8

2nd 7.6 9.5

Middle 8.5 9.4

4th 8.5 9.5

Highest 5.5 5.7

Top 1% 1.0 1.6

All 6.9 7.4

23

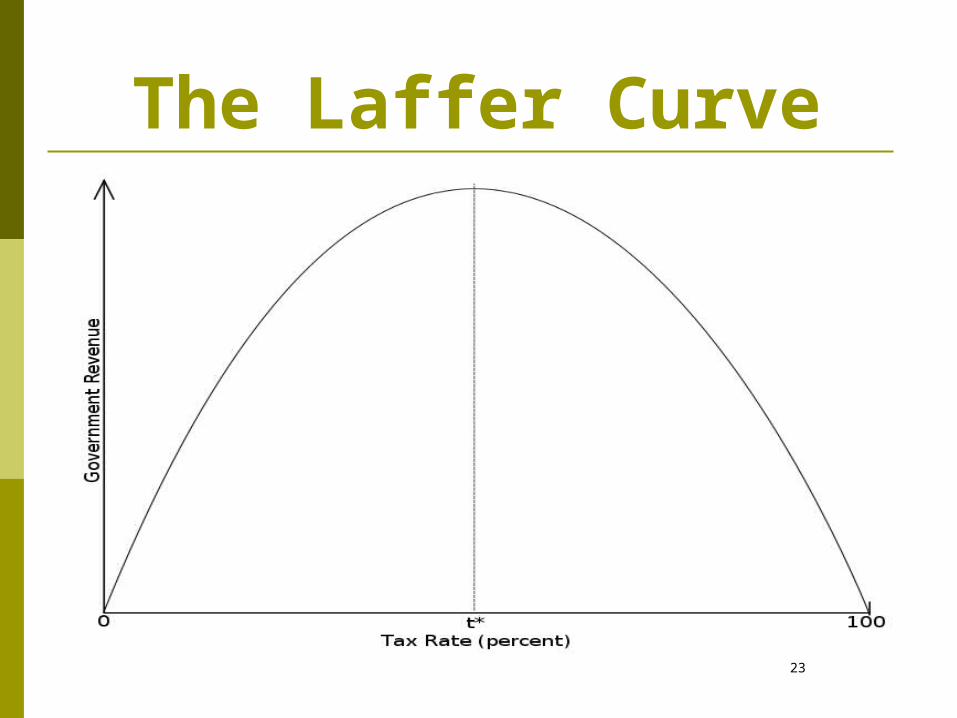

The Laffer Curve

24

The Neo-Laffer Curve

24

But Isn’t the Budget Process Broken Beyond

Repair? Long-term sustainability is the major issue, not short-

term borrowing ability—see payroll holiday pay-fors Improvements can be made

BRAC More and better credit reform

Insurance programs Administrative costs Market rates

But not: Line Item veto [Enhanced recession better] Biennial budgeting

But in sum, the process is not the problem; the problem is the problem 25

A Final Word on What We Will See in the Year Ahead

A Budgetary Perfect Storm at the end of the year: Expiration of tax cuts & payroll tax holiday Expiration of additional unemployment benefits;

TANF; R&E & other tax expenditures Then there is the sequester, debt limit, & CR

The states will be in a Big Squeeze

And finally there’s China

26

27

In conclusion, in the future—even more than in the past—it is good to

remember:

“Sunshine is the bestdisinfectant.”

Supreme Court Justice Louis Brandeis (1856-1941) 27