Embed Size (px)

Citation preview

7.1

1 Taxation of Individuals,

Partnership Firms/LLPand Companies

This Chapter includes

! Basic Concepts and Taxation ofIndividuals

! Taxation of Companies.

! Taxation of Firm/Limited LiabilityPartnership (LLP)

Marks of Short Notes, Distinguish Between, Descriptive & Practical Questions

CS Professional Programme (Module III)

SHORT NOTES

2005 - Dec [3] Write notes on the following:(i) Minimum Alternate Tax (MAT) under Section 115JB of the Income-tax Act,

1961.

7.2 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

(5 marks)Answer:

Minimum Alternate Tax under Section 115JB of the Income-tax Act, 1961.

Where in the case of a company, the income tax payable on the total income as

computed under the Income tax Act, in respect of previous year relevant to the

assessment year 2014-15 or thereafter is less than 18.5% of its book profit, such

book profit shall be deemed to be the total income of the assessee and tax payable

by the assessee on such total income (book profit) shall be the amount of the

income-tax at the rate of 18.5%.

Every company for the purposes of this section shall prepare its Profit and Loss

Account for the relevant Previous Year in accordance with the provisions of Part II

and III of schedules VI to the Companies Act, 1956. However, while preparing the

annual accounts including profit and loss account, the accounting policies, the

accounting standards followed for preparing such accounts including profit and loss

account and the methods and rates adopted for calculating the depreciation shall be

the same as have been adopted for the purpose of preparing such accounts

including profit and loss account as laid before the company at its annual general

meeting in accordance with the provision of Section 210 of the Companies Act,

1956.

For the purpose of MAT, book profit means the net profit as shown in the profit and

loss account for the relevant previous year prepared as aforesaid and would be

subject to some adjustments as mentioned in section 115 JB of the Income Tax Act,

1961.

Every company to which section 115 JB applies shall furnish a report from Chartered

Accountant certifying that the book profit has been computed in accordance with the

provisions of Section 115JB alongwith the return of income filed.

DESCRIPTIVE QUESTIONS

2004 - June [2] (a) The incidence of income-tax of a company depends upon its

residential status. Explain. (10 marks)

Answer:

The incidence of income tax depends upon the residential status of a company in India

during the relevant previous year. A company may either resident or non-resident in

India. As per section 6 (3) of the Act, a company is said to be resident in India in any

previous year, if:

(a) it is an Indian company; or

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.3

(b) during the relevant previous year, the control and management of its affairs is

situated wholly in India.

If one of the above two tests is not satisfied, the company would be a non-resident.

As per section 5 (1) of the Act, the total income of a resident company would consist

of:

(a) any income which is received or is deemed to be received in India in the relevant

previous year by or on behalf of such company;

(b) any income which accrues or arises or is deemed to accrue or arise in India during

the relevant previous year;

(c) any income which accrues or arises outside India during the relevant previous

year.

2007 - June [3] (a) What is ‘minimum alternate tax’ (MAT) ? What is the treatment of

following debited to profit and loss account while calculating book profit:

(i) Fringe benefit tax

(ii) Wealth-tax

(iii) Provision for doubtful debt

(iv) Penalty for non-payment of income-tax

(v) Dividend tax

(vi) Banking cash transaction tax

(vii) Proposed dividend

(viii) Excise duty due, but not paid

(ix) Provision for gratuity

(x) Depreciation (12 marks)

Answer:

Minimum Alternate Tax (MAT)

Where in the case of a company, the income-tax payable on the total income as

computed under the Income-tax Act, in respect of previous year relevant to the

assessment year 2014-15 or thereafter is less than 18.5% of its book profit, such book

profit shall be deemed to be the total income of the assessee and the tax payable by the

assessee on such total income (book profit) shall be the amount of the income tax at the

rate of 18.5%.

Thus in case of a company income tax payable shall be higher of the following two

amounts:

1. Tax on total income computed as per the normal provisions of the Act by charging

applicable normal rates and special rates if any, income included in the total

7.4 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

income of the company is taxable at special rates.

2. 18.5% of book profit.

For the purpose of computing "book profit", the net profit as per profit and loss account

is adjusted for items given under Section 115 JB, by adding them back to net profit or

deducting from it. Treatment of the following debited to P & L Account while calculating

book profit:

(i) Fringe Benefit Tax–Not to be added back.

(ii) Wealth Tax–not to be added back.

(iii) Provision for doubtful debt–added back to net profit.

(iv) Penalty for non-payment of income tax-not to be added back.

(v) Dividend tax –added back to net profit.

(vi) Banking cash transaction tax–not to be added back.

(vii) Proposed dividend–added back to net profit.

(viii) Excise duty due, but not paid–not to be added back.

(ix) Provision for gratuity–not to be added back.

(x) Depreciation–The whole amount of depreciation is to be added back and the

amount of depreciation which is not on account of revaluation of assets is then

required to be deducted from the net profit.

2009 - June [3] (a) When will the 'book profits' of a company deemed to be the total

income of the company for the purposes of levy of minimum alternate tax (MAT) under

section 115JB ? (3 marks)

(b) Indicate briefly the points to be taken into account while preparing annual accounts

for the purpose of MAT. (3 marks)

(c) The MAT does not apply to foreign companies operating in India. Do you agree ?

Give reasons. (3 marks)

Answer:

(a) Minimum alternate tax on certain companies under Section 115 JB Wherein the

case of a company, the income tax payable on the total income as computed under

the Income Tax Act, in respect of previous year relevant to the assessment year

2014-15 or thereafter is less than 18.5% of its book profit, such book profit shall be

deemed to be the total income of the assessee and the tax payable by the

assessee on such total income (book profit) shall be the amount of the income tax

at the rate of 18.5%.

(b) According to sub-section (2) of section 115 JB requires the company to prepare

its profit and loss account for the relevant previous year in accordance with

provisions of Part II and III of Schedule VI of the companies Act, 1956. However,

while preparing the annual accounts including profit and loss account:

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.5

(a) The accounting policies of the company;

(b) The accounting standards followed for preparing such accounts including

profit and loss accounts;

(c) The method and rates adopted for calculating the depreciation by the

company, shall be the same as have been adopted for the purpose of

preparing such accounts including profit and loss account as laid before the

company at its annual general meeting in accordance with on the provisions

of section 210 of the Companies Act, 1956. But where the company has

adopted or adopts the financial year which is different from the previous year

under the Income Tax Act, (a), (b) and (c) aforesaid shall correspond to the

accounting policies, accounting standards and the method and rates for

calculating the depreciation which have been adopted for preparing such

accounts including profit and loss account for such financial year or part of

such financial year falling within the relevant previous year.

(c) No, MAT applies to any company whether it is domestic or foreign. However,

where a non-resident companies income is assessed on a presumptive basis

under Section 44 B or 44BB or at a flat rate under Section 115 A on royalty and

technical fees, the book profit becomes immaterial for regular assessment and the

presumptive income tax will prevail.

2010 - June [2] (a) Answer the following :

(i) What is the quantum of Minimum Alternate Tax (MAT) for a ‘domestic company’

and ‘foreign company’ for the assessment year 2014-15? (3 marks)

(c) Discuss the concept of ‘deemed dividend’ under section 2(22). (3 marks)

Answer:

(a) (i) The rates of Minimum Alternate Tax (MAT) for the A.Y. 2014-15 are as

follows:

(A) Domestic Company:

(i) If Book Profit does not exceed ` 1 crore:

IT 18.5

SC —

EC (@ 2%) + SHEC (@ 1%) 0.555

Total 19.055

(ii) If Book Profit is in the range of ` 1 crore - ` 10 crore:

IT 18.5

SC 0.925

EC (@2%) + SHEC (@1%) 0.58275

Total 20.00775

7.6 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

(iii) If Book Profit exceeds ` 10 crore:

IT 18.5

SC 1.85

EC (@ 2%) + SHEC (@ 1%) 0.6105

Total 20.9605

(B) Foreign Company:(i) If Book Profit does not exceed ` 1 crore:

IT 18.5SC —EC (@ 2%) + SHEC (@ 1%) 0.555Total 19.055

(ii) If Book Profit is in the range of ` 1 crore - ` 10 crore:IT 18.5SC 0.37EC (@2%) + SHEC (@1%) 0.5661Total 19.4361

(iii) If Book Profit exceeds ` 10 crore:IT 18.5SC 0.925EC (@ 2%) + SHEC (@ 1%) 0.58275Total 20.00775

(c) Dividend in its ordinary connotation means the sum paid to a shareholderproportionate to his shareholding in a company out of the total divisible profits.However, under section 2 (22) following disbursement are also treated as dividendif they are paid by a company to a shareholder to the extent of accumulated profits:(i) Any distribution by a company to the extent of accumulated profits involving

the release of the assets of the company;(ii) Distribution of debentures / deposit certificate to shareholders and bonus

shares to preference shareholders;(iii) Distribution to shareholders on liquidation of the company;(iv) Distribution on reduction of share capital;(v) Loans or advances by a closely held company to certain shareholders/

concerns.

2012 - June [3] What is the difference between ‘minimum alternate tax’ under section115JAA and ‘alternate minimum tax’ under section 115JC? Who is subject to thesetaxes? Also discuss the implication of these taxes in the case of an overseas entityhaving a permanent establishment (PE) in India. (15 marks)

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.7

Answer:Minimum Alternate Tax (MAT) under Section 115 JB of the Income Tax Act, 1961 :Where in the case of a company, the Income Tax payable on the total income ascomputed under the Income Tax Act, in respect of previous year relevant to theassessment year 2013-14 & 2014-15 or thereafter is less than 18.5% of its book profitsuch book profit shall be deemed to be the total income of the assessee and taxpayable by the assessee on such total income (book-profit)shall be the amount of theincome-tax at the rate of 18.5%.

Every company for the purpose of this section shall prepare its Profit and Loss

Account for the relevant previous year in accordance with the provisions of Part II and

III Schedules VI to the Companies Act, 1956. However, while preparing the annual

accounts including Profit and Loss Account, the accounting policies, the accounting

standards followed for preparing such accounts including profit and loss account and

the methods and rates adopted for calculating the depreciation shall be the same as

have been adopted for the purpose of preparing such accounts including Profit and

Loss account as laid before the company at its annual general meeting in accordance

with the provision of Section 210 of the Companies Act, 1956.

For the purpose of MAT, book profit means the net profit shown in the profit and loss

account for the relevant previous year prepared as aforesaid and would be subject to

some adjustments as mentioned in section 115 JB of the Income Tax Act, 1961.

Every company to which section 115 JB applies shall furnish a report from Chartered

Accountant certifying that the book profit has been computed in accordance with the

provisions of section 115 JB alongwith the return of income filed.

Alternative Minimum Tax for Limited Liability Partnership [Section 115 JC

to115JF]

As per newly inserted section 115JC where the regular income tax payable for a

previous year by a limited liability partnership is less than the alternative minimum tax

payable for such previous year, the adjusted total income shall be deemed to be the

total income of such limited liability partnership and it shall be liable to pay income-tax

on such total income at the rate of 18.5%.

Meaning of adjusted total income alternate minimum tax and regular income tax

[Section 115JC (2) and section 115 JF]

(i) "adjusted total income" shall be the total income before giving effect to this newly

inserted chapter XII-BA as increased by the deduction claimed under any section

included in chapter VI-A under the heading "C-Deduction in respect of certain

incomes" and deduction claimed under Section 10AA [Section 115 JC (2)];

(ii) "alternative minimum tax" shall be the amount of tax computed on adjusted total

income at a rate of 18.5%; and

7.8 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

(iii) "regular income tax" shall be the income tax payable for a previous year by a

limited liability partnership on its total income in accordance with the provisions

of the act other than the provisions of this newly inserted Chapter XII-BA.

Report of Chartered Accountant [Section 115 JC (3)]

Every limited liability partnership to which this section applies shall obtain a report, in

such form as may be prescribed, from an accountant certifying that the adjusted total

income and the alternate minimum tax have been computed in accordance with the

provisions of this chapter and furnish such report on or before the due date of filing of

return u/s 139 (1).

Tax credit for alternate minimum tax [Section 115 JD]

1. Credit for tax paid [Section 115JD (1)] : The credit for tax paid by a limited

liability partnership under Section 115 JC shall be allowed to it in accordance with

the provisions of this section.

2. How to compute tax credit [Section 115 JD (2)] : The tax credit of an

assessment year to be allowed under Section 115 JD (I) shall be the excess of

alternate minimum tax paid over the regular income tax payable of that year.

3. Interest not payable on tax credit allowed [Section 115 JD (3) ] : No interest

shall be payable on tax credit allowed under sub-section (1).

4. Tax credit to be carried forward and set-off upto next 10 assessment years

[Section 115 JD (4)] : The amount of tax credit determine u/s 115 JD (2) shall be

carried forward and set-off in accordance with the provisions of Section 115 JD (5)

and 115 JD (6) mentioned below but such carry forward shall not be allowed

beyond the 10th assessment year immediately succeeding the assessment year for

which tax credit become allowable u/s 115 JD (1).

5. Tax credit is allowed to the maximum extent of the excess of regular income

tax over alternate minimum Tax : In any assessment year in which the regular

income - tax exceeds the alternate minimum tax, the tax credit shall be allowed to

set-off to the extent of the excess of regular income-tax over the alternate minimum

tax and the balance of the tax credit, if any shall be carried forward.

6. Effect of assessment order to be adjusted [Section 115 JD (6)] : If the amount

of regular income tax or the alternate minimum tax is reduced or increased as a

result of any order passed under this act, the amount of tax credit allowed under

this section shall also be varied accordingly.

2012 - Dec [1] (a) Discuss briefly the treatment of un-availed tax credit of minimum

alternate tax (MAT) in case of conversion of a private company or unlisted public

company into a limited liability partnership (LLP). (3 marks)

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.9

Answer:

Section 115JAA provides that where tax is paid by a company for any assessment year

in relation to deemed income under Section 115JA(1) or 115JB(1), a tax credit will be

allowed in subsequent years.

However, newly inserted Section 115JAA(7) w.e.f. 1.04.2011, Assessment Year

2011-12 and onwards, provides that in case of conversion of a private company or

unlisted public company into a Limited Liability Partnership Act, 2008, the provisions of

Section 115JAA shall not apply to the successor LLP, that is to say tax credit will not be

allowed to such LLP.

2012 - Dec [3] (a) Discuss with the help of an example, the cascading effect of dividend

distribution tax and the remedial action taken by the government. (7 marks)

Answer:

According to Section 115-O, the domestic company shall, in addition to the income tax

chargeable in respect of its total income, be liable to pay additional income tax on any

amount declared, distributed, or paid by such company by way of dividend (whether

interim or otherwise), whether out of current on accumulated profits such additional

income tax shall be payable @ 15% plus surcharge plus education and secondary and

higher education cess. Such tax is known as Dividend Distribution Tax (DDT). Such

distributed dividend is exempt in the hands of recipients. As per Section 10 (34), any

income by way of dividends referred to in Section 115-O shall be exempt from income

tax. However, this provision resulted in a cascading effect in the case of holding

company declaring dividend out of dividend received from its subsidiary.

To mitigate cascading effect of DDT, Section 115-O (1A) of the Act provides that

dividend liable for DDT in case of a company is to be reduced by an amount of dividend

received from its subsidiary after payment of DDT if the following conditions are

satisfied:

(i) the amount of dividend is received from its subsidiary;

(ii) the subsidiary has paid tax under this section on such dividend; and

(iii) the domestic company (holding company) is not a subsidiary of any other

company.

For Example:

A Ltd. holds 65% shares in B Ltd. A Ltd. received 40,00,000 dividend from B Ltd.

A Ltd. declares Final Dividend of ` 80,00,000 to its shareholders.A Ltd. shall be liable

to pay DDT of ` 12,97,800 @ 16.2225% on full amount of ` 80,00,000 including the

amount received from B Ltd. Due to this the amount of ̀ 40,00,000 is taxed twice once

in the hands of B Ltd. and secondly in the hands of A Ltd.

Thus, to mitigate the cascading effect of above said DDT, A Ltd. shall be liable to

7.10 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

pay DDT on ` 40,00,000 (` 80,00,000 - ` 40,00,000) @ 16.2225% of ` 6,48,900.

2013 - Dec [3] (b) What is the time-limit in the following different cases:

(i) To file return of income under section 139(1) by an assessee who is required to

furnish audit report under section 92E.

(ii) To file a revised return, if the assessee discovers any omission or wrong

statement in the originally filed return. (2 marks each)

PRACTICAL QUESTIONS

2004 - Dec [2] Sunil Ltd., an Indian company, is engaged in the business ofdevelopment of computer software. The following is the profit and loss account for theyear ended 31st March, 2013:

` `

To Freight and insurance By Sale of software attributable to delivery in India 12,00,000 of software outside India 1,00,000 By Sale of softwareTo Expenses incurred in foreign and providing

exchange for providing technical servicestechnical services outside India 17,00,000outside India 1,50,000 By Export incentives 70,000

To Other business expenses 7,50,000 By Interest 2,10,000To Depreciation 3,00,000 By Profit of foreignTo Income-tax penalty 20,000 branch 3,60,000To Income-tax 2,20,000To Net profit 20,00,000

35,40,000 35,40,000For tax purposes, other information are submitted as under:

(i) Depreciation allowed under section 32 is ` 2,10,000.(ii) Customs duty pertaining to financial year 2011-12 paid during the previous year

2012-13 amounted to ` 60,000 were not charged to profit and loss account.(iii) Amount received in convertible foreign exchange upto 30th September, 2013

was ̀ 13,90,000 (out of which ̀ 60,000 was freight and insurance for delivery ofsoftware).

Compute the net income of Sunil Ltd. for the assessment year 2013-14. (20 marks)Answer:Computation of Total Income of Sunil Ltd. for the Assessment Year 2013-14

` `

Net Profit as per P/L A/c 20,00,000

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.11

Add: Expenes not allowed:Income tax penalty 20,000

Depreciation over charged 90,000

Income Tax 2,20,0000 3,30,000

23,30,000

Less: Expenses allowable but not charged:

Customs duty paid for Financial Year 2011-12 60,000

Total Taxable Income 22,70,000

2007 - June [3] (b) Sun Bright Ltd., an Indian company, furnishes following particularsof its income for the previous year 2013-14. Calculate its total income and income-taxliability for the assessment year 2014-15:

`Income from business 5,20,000Dividend received during the year:

— from Indian company 20,000— from foreign company 5,000

Gains from transfer of capital assets:— short term capital gains 25,000— long term capital gains 50,000

Agricultural income in India 35,000Additional information:

(i) Income from business includes '1,50,000 profit earned from a new small scaleindustry set up on 1st October, 2013 which is eligible for deduction under section80-IB.

(ii) Business expenses already charged from business income include ` 10,000revenue expenditure and ` 30,000 capital expenditure on family planningprogramme for employees.

(iii) Company has debited following donations in the profit and loss account of thebusiness of company:— Rajiv Gandhi Foundation: ` 50,000; and— Prime Minister’s National Relief Fund: ` 25,000. (8 marks)

Answer:Computation of Total Income for the

Assessment Year 2014-15Amount `

Income from Business as per P/L A/c 5,20,000

Add: Disallowed Expenditure

(a) Donation 75,000

7.12 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

(b) Capital Expenditure on Family (+)

Planning (` 30,000-6,000) 24,000 90,000

6,19,000

Capital Gains on long term 50,000

Capital Gain on short-term 25,000 75,000

Dividend from Indian Co. Exempt

Dividend from Foreign Co. 5,000 5,000

Agriculture Income Exempt –

6,99,000

Less: Deduction

(a) Under Section 80IB 30% of 1,50,000 45,000

(b) Under Section 80-G

(i) PMNRF 25,000

(ii) 50% of Rajiv Gandhi

Foundation 25,000 50,000 -95,000

Total Income 6,04,000

Tax Liability

(i) 20% on LTCG [50,000] 10,000

(ii) 30% on other Income [5,54,000] 1,66,200

1,76,200

(iii) Surcharge NIL

1,76,200

(iv) 2% Education Cess & 1% SHEC 5,286

Tax Liability 1,81,486

2008 - June [1] A company claims deduction of certain expenditures in computation of

its total income under the Income-tax Act, 1961. Consider the allowability or otherwise

of the following expenditures giving brief reasons for your answers:

(i) Payments made by the company for sponsoring a sports tournament.

(ii) Water pollution treatment plant installed permanently in the factory in

compliance with statutory requirements.

(iii) As a holding company, it has borrowed money and advanced the same to its

subsidiary in whose business it has deep interest. The subsidiary uses the same

for its business. The company claims interest paid on such borrowings as a

deduction.

(iv) Expenditure incurred for earning share income from a firm.

(v) Provision made in the accounts of the company on a scientific basis in respect

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.13

of liabilities estimated to arise under warranty provided to customers in respect

of products sold. (4 marks each)

Answer:

(i) This is an activity of business promotion through advertisement and the

sponsoring of the tournaments carries with it. Hence it is allowable as a revenue

expenditure.

(ii) It is a revenue expenditure because expenses incurred under a statutory

stipulation rather than on personal wish.

(iii) Where it is obvious that a holding company has deep interest in its subsidiary

and hence if the holding company advances borrowed money to its subsidiary

and the same has been used by the subsidiary for some business purpose, then

the assessee will be entitled to a deduction of interest under Section 36(1) (iii).

(iv) According to section 14-A, if the income is exempt any expenditure incurred on

earning that income shall not be allowed as deduction.

(v) Warranty provided on a scientific basis or past experience is allowable as

deduction.

2009 - Dec [2] (b) Modern Ltd. entered into an agreement with Synergy Ltd. for granting

on lease to Synergy Ltd. its 8000 sq. mtr. land lying vacant adjacent to the factory

premises of Synergy Ltd. for a period of 12 years commencing from May, 2001. Under

the terms of the agreement, Synergy Ltd. had to build a factory building, pay an annual

rent @`100 per sq. mtr. of the leased land of 8,000 sq. mtr. and surrender the building

to Modern Ltd. at the end of the lease without any consideration. Synergy Ltd. complied

with the terms and conditions of the lease agreement.

The depreciated value of the building surrendered and taken possession by

Modern Ltd. in May, 2013 was `4,22 crore. Accounts department of Modern Ltd. is of

the opinion that an equivalent amount is to be taken in the accounts of the year 2013-14

as income received.

Critically examine the matter and offer your comments. (3 marks)

Answer:

Accounts Department's opinion of Modern Ltd. is incorrect. The depreciated value of the

building is of course to be brought into the books of accounts.

However, the equivalent amount viz. ` 4.22 crores cannot be treated as income

from the business. By its very nature it is a capital receipt and is not a revenue income.

The amount cannot be treated as a revenue receipt unless it is conclusively established

that this represented deferred rent as the lease rent was unreasonably low. Further

Modern Ltd. is not in the business of real estate to treat the benefit as incidental

revenue receipt earned during the course of such business.

7.14 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

2010 - Dec [3] (a) The book profits of a company in the previous year 2013-14

computed in accordance with section 115JB is ` 15 lakh. If the total income computed

for the same period as per the provisions of the Income-tax Act, 1961 is ` 3 lakh,

calculate the tax payable by the company in the assessment year 2014-15 and also

indicate whether the company is eligible for any tax credit. (5 marks)

Answer :

1. Calculation of tax liability u/s 115JB:

Particulars Details Amount

Book profit Given 15,00,000

Tax Liability 18.5% of ` 15 lakhs 2,77,500

Add: Surcharge NIL

Tax Liability after surcharge 2,77,500

Add: Education cess and SHEC @ 3% 3% of ` 2,77,500 8,325

Tax Liability after cess 2,85,825

2. Calculation of tax liability as per Income Tax Act, 1961:

Particulars Details Amount

Total Income Given 3,00,000

Tax Liability 30% of ` 3 lakhs 90,000

Add: Education cess and SHEC @ 3% 2,700

Tax Liability after cess 92,700

3. Computation of Final Tax payable:

Particulars Details Amount

Tax Liability Tax Liability u/s 115B> Normal Tax liability 2,85,825

Actual tax liability 2,85,825

The company is eligible for MAT tax credit of ` 1,93,125 (` 2,85,825 - ` 92,700), which

can be carried forward for 10 years or is to be awaited within 10 years u/s 115JAA.

2012 - Dec [2] (b) Whether minimum alternate tax (MAT) under section 115JB is

payable in advance and interest under sections 234B and 234C is payable on failure

to pay such advance tax? Also explain whether MAT credit admissible under section

115JAA has to be set-off against the assessed tax payable before calculating the

interest under sections 234A, 234B and 234C.

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.15

You may take help of decided case law, if any. (6 marks)

Answer :

Companies liable to pay tax on the basis of MAT under section 115JB are required to

pay advance tax and interest under sections 234B and 234C is payable on failure to pay

such advance tax. [JCIT v Rolta India Ltd. (2011)]

For the purpose of computing interest chargeable under section 234A, 234B and

234C, credit of MAT under section 115JAA has to be set off against the assessed tax

payable. [CIT v Tulsian NEC Ltd. (2011)]

2013 - June [2] (a) The net profit of Renuka Ltd., an Indian company, as per its profit

and loss account prepared as per the Income-tax Act, 1961 is ̀ 90,00,000 after debiting

and crediting following items:

`

Provision for income-tax 5,00,000

Provisions for deferred tax 3,00,000

Proposed dividend 7,50,000

Depreciation including depreciation on revaluation of assets

` 20,00,000 debited to profit and loss account 60,00,000

Profit from industrial unit in SEZ area 80,000

Provision for permanent diminution in the value of investments 70,000

Compute tax liability under section 115JB for the assessment year 2014-15.

(9 marks)

Answer:

Computation of Tax Liability of Renuka Limited for Assessment Year 2014-15.

(a) Computation of book profits : `

Net Profit as per Profit & Loss A/c 90,00,000

Add : Non-admissible Expenditure :

— Provision for Income-tax 5,00,000

— Provision for deferred tax 3,00,000

— Proposed dividend 7,50,000

— Depreciation 60,00,000

— Provision for diminution 70,000 76,20,000

Less : Inadmissible Incomes &

Admissible Expenditure :

— Depreciation allowed 40,00,000 (40,00,000)

BOOK PROFITS 1,26,20,000

(b) Computation of Taxable Income ` `

7.16 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

Profit as per Profit & Loss A/c 90,00,000

Add : Inadmissible Expenditure,

if debited to Profit & Loss Account :

— Provision for Income tax 5,00,000

— Provision for deferred tax 3,00,000

— Proposed dividend 7,50,000— Provision for diminution in the value of the asset 70,000— Depreciation as per A/c’s 60,00,000 76,20,000

Less : Depreciation as per income tax (assumed same amount excluding depreciation on revaluation) 40,00,000 (40,00,000)

GROSS TOTAL INCOME 1,26,20,000Less : Deduction on Profit from SEZ unit (80,000)

TAXABLE INCOME 1,25,40,000

— Tax Liability as per the provisions of MAT `

@ 18.5% on ` 1,26,20,000 23,34,700Add : Surcharge @ 5% 1,16,735Add : Education cess @ 2% & SHEC @ 1% 73,543Total Tax Liability 25,24,978

— Tax Liability as per normal tax rates@ 30% on ` 1,25,40,000 37,62,000Add : Surcharge @ 5% 1,88,100Add : Education cess @ 2% & SHEC @ 1% 1,18,503Total Tax Liability 40,68,603

Here, the tax liability as per MAT provisions is less than the tax liability as per normaltax provisions, therefore, the Tax payable shall be ` 40,68,603.

2013 - June [3] (a) A limited liability partnership (LLP) has following income for theassessment year 2014-15:

`

Profit from business eligible for deduction @ 100% of profitsunder section 80-IA 32,00,000

Profit from other business 48,00,000Compute the tax payable by the LLP, assuming that it has no other income during theassessment year 2014-15. (5 marks)Answer:(i) Computation of Total Income and Income Tax Payable

For Assessment Year 2014-15.As per the normal provisions of the Act `

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.17

Profits & gains of business or profession (Total) 80,00,000Less : Deduction under section 80-IA 32,00,000

Total Income 48,00,000Tax payable @ 30% 14,40,000Add : EC @ 2% & SHEC @ 1% 43,200

Tax Payable 14,83,200

(ii) Computation of Alternate Minimum Tax (AMT)

`

Profits & Gains of business or profession 48,00,000

Add : Deduction under section 80IA 32,00,000

Adjusted Total Income 80,00,000

AMT @ 18.5% 14,80,000

Add: EC @ 2% & SHEC @ 1% 44,400

AMT Payable 15,24,400

Here, as per Section 115JC, since the income tax payable as per normal provisions of

the Income Tax Act is less than the AMT, the LLP would be liable to pay ` 15,24,400

as tax.

2013 - Dec [1] (a) Y Ltd. is a company in which 80% shares are held by G Ltd. Y Ltd.

declared a dividend amounting to ` 30 lakh to its shareholders for the financial year

2012-13 in its annual general meeting held on 18th May, 2013. Dividend distribution tax

was paid by Y Ltd. on 20th May, 2013. G Ltd. declared an interim dividend amounting

to ` 40 lakh on 1st December, 2013 for the year ended 31st March, 2014.

Compute the amount of tax on dividend payable by G Ltd. What would be your answer,

if 52% shares of G Ltd. are held by S Ltd., an Indian company? (6 marks)

2013 - Dec [2] (b) X Ltd. charged depreciation on its fixed assets at the rate prescribed

in the income tax rules. However, the Assessing Officer disallowed the same and

allowed the rate as prescribed in the Companies Act, 1956 for the purpose of

computation of book profit under section 115JB for the previous year 2013-14. Examine

the legality of action taken by the Assessing Authority. (5 marks)

2013 - Dec [3] (a) Comment in brief on allowability of following expenditure while

computing the income under the head ‘profits and gains of business or profession’ for

the assessment year 2014-15:

(i) Kanha commenced operations of the business of setting-up a warehousing

facility for storage of sugar on 1st June, 2013. He incurred capital expenditure on

purchase of building during the period from January, 2013 to March, 2013

exclusively for the above business and capitalised the same in its books of

7.18 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

account on 1st June, 2013.

(ii) Ms. Radha incurred expenditure on purchase of computer software and

capitalised such expenditure in her books of account.

(iii) Murli is operating a pharmaceutical factory. he incurred expenditure in providing

freebees to medical practitoners. (3 marks each)

CS Executive Programme (Module I)

SHORT NOTES

2008 - Dec [4] (b) Write short notes on the following:

(i) The activities of a co-operative society which are eligible for deduction under

section 80P. (3 marks)

Answer:

The activities of a co-operative society which are eligible for deduction @ 100% under

Section 80P are as follows:

(i) Income from banking business & providing credit facilities to its members

(ii) Cottage Industry

(iii) Marketing agricultural produce

(iv) Purchase of agricultural implements

(v) Processing of agricultural produce without aid of power of its member

(vi) Collective disposal of Labour for its members

(vii) Primary Society engaged in supply of milk, oilseeds, fruits etc

(viii) Investment in securities

(ix) Letting of Godowns & warehouses.

2009 - Dec [2] (b) Write short notes on the following:

(i) Taxation of zero coupon bonds

(ii) Share of profit from partnership firm (3 marks each)

Answer:

(i) Zero coupon bonds means –

1. Bond issued by an infrastructure capital company or infrastructure capital

fund or public sector company on or after 1st June, 2005.

2. Bond in respect of which no payment and benefit is received or receivable

before maturity or redemption from infrastructure capital company or

infrastructure capital fund or public sector company.

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.19

3. Bonds which Central Government may, by notification in the Official Gazette

specify in this behalf.

Maturity and redemption of Zero coupon bonds to be treated as transfer. The

profits arising on the transfer of zero coupon bonds shall be subject to capital

gains tax. In case of short term capital asset, the same will be taxable as per

assessee specific income tax slab rates.

In case of long term capital asset, the assessee will have either of the two

options to pay minimum tax u/s 112(1):

Option I: 20% of long term capital gain after indexation of the cost of such

bonds; or Option II: 10% of long term capital gains before indexation of the cost

of such bonds;

(ii) Share of Profits from partnership firm

Share of profits which a partner receives from the firm (after deduction of

remuneration and interest allowable) shall be fully exempt in the hands of the

partners. However, only that part of the interest and remuneration which was

allowed as a deduction to the firm shall be taxable in the hands of the partners

in their individual assessment under the head ‘profits and gains of business or

profession’.

2010 - June [2] (b)Write short notes on the following:

(ii) Taxation of zero coupon bonds

(iii) Profit in lieu of salary. (3 marks each)

Answer:

(ii) Please refer 2009 Dec [2] (b) (i) on page no. 28

(iii) Profit in lieu of salary

Following Items are Included in this Category

Compensation: By virtue of Sec. 17(3) (i), any compensation due to or received

by an employee from his employer or former employer at or in connection with

the termination of his employment or modification in terms of his employment is

taxable as profit in lieu of salary.

Other Payments

Any payment in the form of:

• Gratuity

• Commuted value of pension

• Retrenchment compensation

• House rent allowance

Received or due to be received to the extent which is not exempt, and which

it does not consist of contribution made by the employee, or interest thereon, is

7.20 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

taxable as profits in lieu of salary.

Keyman Insurance Policy: Surrender value of the policy endorsed in favour of

the employee, or the sum received by him at the time of retirement, will be

taxable as profit in lieu of salary.

Lump-sum Incentives:

Any amount due or received- before joining employment or after leaving

employment, it is Taxable as profit in lieu of salary.

2010 - Dec [6] (a) Write short notes on the following:

(ii) Capital gains in case of damage or destruction of capital asset

(iii) Clubbing of income of a minor child

(v) Tax on income of foreign institutional investors from capital gains arising from

transfer of their securities. (3 marks each)

Answer:

(ii) Where any person receives at any time during any previous year any money or

other assets under insurance from an insurer on account of damages to, or

destruction of any capital asset, as a result of:

(a) Flood, typhoon, hurricane, cyclone, earthquake or other convulsion of

nature; or

(b) Riot or civil disturbance; or

(c) Accidental fire or explosion; or

(d) Action by an enemy or action taken in combating an enemy (whether with

or without a declaration of war)

Then, any profits or gains arising from receipts of such money or other assets

shall be chargeable to income-tax under the head “capital gains” and shall be

deemed to be the income of such person of the previous year in which such

money or other asset was received and for the purposes of section 48, value of

any money or the fair market value of other assets on the date of such receipts

shall be deemed to be the full value of the consideration received or accruing as

a result of the transfer of such capital asset.

(iii) Clubbing of Income of a minor child

As per this section, income of a minor child will be clubbed in the income of the

parent, whose total income before such clubbing is higher.

Following points are relevant to be noted in this regard –

C If the child earns any income by doing manual work or due to a special skill,

such income will not be clubbed.

C A special deduction of ` 1,500 per child will be allowed to the parent, in

whose income it is clubbed.

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.21

C Child’s income will be added to the income of parent, whose income before

such clubbing is higher, in case of separated couple, income of the child will

be added in the income of the parent who maintains the child in the

previous year.

C Any income of a minor child, suffering from any disability of the nature

specified in section 80U will not be clubbed.

(v) Tax on foreign institutional investors from capital gains arising from transfer oftheir securities [Section 115AD]Where the total income of the above assessee includes:(a) Income received in respect of securities other than units of mutual funds

covered under section 10(23D) or of Unit Trust of India; or(b) Income by way of short term or long term capital gains arising from the

transfer of such securitiesThe income-tax on the total income shall be chargeable as under:(a) On the income in respect of securities referred to in clause (a) above @

20%(b) On the income by way of short term capital gains covered under section

111A @ 15%(c) On the income by way of long term capital gains referred to in clause (b)

above @10%(d) On the balance income included in total income special/normal rate as the

case may be.

2011 - Dec [5] (a) Write short notes on the following:(i) Deduction in respect of interest on loan taken for higher education. (3 marks)

Answer:The deduction under section 80E is available to an individual if following conditions aresatisfied:1. Deduction available only to Individual not to HUF or other type of Assessee.2. Deduction amount:– The amount of interest paid is eligible for deduction and

moreover there is no cap on the amount to be deducted. You can deduct the entireinterest amount from your taxable income. However there is no benefit availableon the repayment of principal amount of the loan.

3. Deduction available if Interest is been paid during the previous year and was paidout of income chargeable to tax which means if repayment is made from incomenot chargeable to tax than deduction will not available.

4. Interest should have been paid on loan taken by him from any financial institutionor any approved charitable institution for the purpose of pursuing his highereducation. Interest on Loan taken from relatives or friends will not be eligible fordeduction under section 80E.

7.22 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

5. Loan should have been taken for the purpose of pursuing higherstudies ofIndividual, Spouse, Children of Individual or of the student of whom individual islegal Guardian.

6. The whole of the amount paid during previous year towards interest is allowed asdeduction and deduction shall be allowed for 8 assessment years starting from theassessment year in which the assessee starts paying the interest on loan, or untilthe interest thereon is paid by the assessee in full, whichever is earlier.

2012 - June [5] (b) Write short notes on the following:

(i) Scientific research expenditure

(ii) Capital assets (3 marks each)

Answer:

(i) Scientific Research Expenditure

Section 35 of the Act provides tax incentives for scientific research expenditure.

Where the assessee himself carries on scientific research and incurs revenue

& capital expenditure, deduction is allowed for such expenditure only if the

research relates to his business. Further, Expenditure incurred during 3 years

prior to commencement of business shall be deemed to be the expenditure of

the year in which business commenced.

Where the assessee does not himself carry on scientific research but makes

contribution to an approved scientific research association, university, college or

approved institutions to be used for scientific research, related or unrelated to the

business of assessee, deduction shall be allowed to the extent of 175% of the

sum paid.

(Where any sum is paid to a National Laboratory, approved for this purpose

by the ICAR or ICMR or CSIR etc. or to any university, or to I.I.T. (Indian Institute

of Technology), a weighted deduction of 175% or 200% of the sum paid shall be

allowed as deduction.)

(ii) Capital Assets

Section 2 (14) of the Income-tax Act defines the term "Capital Assets: to

means:

Property of any kind held by an assessee whether or not connected with his

business or profession, but does not include:

(i) Any stock-in-trade, consumable stores, or raw materials, held for the

purposes of business or profession

(ii) Personal effects (excluding jewellery, archaeological collections, drawings,

painting. Sculptures or any work art.)

(iii) Rural Agricultural land in India. In other words, it must not be an Urban

agricultural land. Rural agricultural land means an agricultural land in India

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.23

provided it is not situated in !

(a) Any area which is comprised within th jurisdiction of a municipality

having a population of 10,000 or more.

(b) Any area within the distance, measured aerially :

C More than 2 kms from the local limits of any Municipality or

Cantonment Board having a population of more than 10,000 but not

exceeding 1,00,000; or

C More than 6 kms from the local limits of any Municipality or

Cantonment Board having a population of more than 1,00,000 but

not exceeding 10,00,000 ; or

C More than 8 kms from the local limits of any Municipality or

Cantonment Board having a population of more than 10,00,000.

(iv) 6½% Gold Bond, 1977 or 7% Gold Bonds, 1980 or National Defence Gold

Bonds, 1980 issued by the Central Government.

(v) Special Bearer Bonds, 1991 issued by Central Government.

(iv) Gold Deposit Bonds issued under Gold Deposit Scheme, 1999.

DISTINGUISH BETWEEN

2008 - Dec [3] (b) Distinguish between of the following:

(i) ‘House rent allowance’ and ‘rent free house’.

(ii) ‘Cost of acquisition’ and ‘cost of improvement’.

(iii) ‘Fair rent’ and ‘annual rent’. (3 marks each)

Answer:

(i) ‘House rent allowance’ and ‘rent free house’

S. No. House Rent Allowance Rent free house

1 It is dealt under section 10(13A) and

Rule 2A

It is a kind of perquisite. It is dealt

under section 17(2)(i) of the Act.

2 While calculating salary and basic pay,

dearness allowance and commission (if

terms of employment provide) is

included.

Under calculation of salary, apart

f rom basic pay, DA and

Commission, Bonus, fees and other

taxable allowance are also included

3 Only taxable portion (after deduction) is

added to the Gross Salary of the

assessee

In this case, it is included in the

Gross Salary of the assessee as

perquisite.

7.24 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

(ii) ‘Cost of acquisition’ and ‘cost of improvement’:

The distinction between ‘Cost of acquisition’ and ‘cost of improvement’ can be

explained in the following lines. The above two terms are associated with the

capital assets.

Cost of Acquisition:

Cost of acquisition of an asset is the value for which it was acquired by the

assessee. Expenses of capital nature for completing or acquiring the title to the

property are includible in the cost of acquisition. Cost of acquisition always

precedes cost of improvement.

Cost of Improvement:

It is the capital expenditure incurred by the assessee in making any

additions/improvement to the capital asset. It also includes any expenditure

incurred to protect or complete the title to the capital assets or cure such title.

Any expenditure incurred to increase the value of the capital asset is treated as

cost of improvement. Any cost of improvement incurred before 1.4.1981 is not

taken into consideration for calculating capital gains chargeable to tax.

(iii) ‘Fair rent’ and ‘annual rent’:

Fair rent means the sum of for which the property might reasonably be expected

to let from year to year. This rent is also known as notional rent. It will be equal

to the rent which a similar property fetches in the neighborhood.

Where as annual rent means the actual rent. This happens only where the house

property has been actually let. Again annual rent means (i) if property is let out

throughout the previous year the annual rent received or receivable for that year

and (ii) if the property is let out for a part of the year the amount which bears the

same proportion to actual rent received or receivable for the period of letting as

the period of twelve month bears to the period of letting.

2009 - June [3] (a) Distinguish between the following:

(ii) 'Long-term capital gain' and 'short-term capital gain'. (2 marks)

Answer:

Distinguish between Short - term capital gain and long - term capital gain:

Short term capital gain:

S.T.C. gains means any gains arising from transfer of a Capital Asset for which the

holding period is less than 36 months from date of purchase except for shares &

securities of such companies listed on recognised stock exchanges & traded through

such exchanges & on which securities transaction tax is paid where the holding period

less than 12 months shall be termed as short term. If Capital Asset as defined u/s

2(42A). Short Term Capital gains also includes S.T.C. Loss termed as negative gains

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.25

Long term capital gain:

L.T.C. Gains means any gains arising from transfer of any Capital Asset, for which the

holding period is 36 months or more, except for shares & securities of such companies

listed on recognised Stock Exchanges & traded through such exchanges on which

securities transaction tax is paid, the holding period shall be 12 months or more from

the date of purchase. Such Assets Shall be termed as Long Term Capital Assets.

2009 - Dec [3] (a) Distinguish between the following:

(ii) ‘Recognised provident fund’ and ‘statutory provident fund’. (4 marks)

(iv) ‘Exemptions’ and ‘deductions’. (4 marks)

Answer:

(ii) Recognized Provident Fund is set-up under the provisions of Employee's

Provident Fund Act, 1952. This fund is maintained by the private sector

organizations and factories.

Apart from this where provident fund maintained by other organization is

recognized by the income-tax authorities, such fund is also deemed as

recognized provident fund. On the other hand statutory provident fund is set-up

under the provisions of Provident Fund Act, 1925. This fund is applicable to the

employees of Central Government, State Government and Semi-Government.

Under this fund only the employee's contribution is deposited. The Government

does not contribute any amount while in case of RPF both employer and

employee can deposit the contribution. Employer's contribution to RPF up to

12% of salary is exempted and any amount in excess of 12% is included in gross

sal ary of the employee. Interest up to 9.5% p.a. is exempted and any amount

of interest in excess of 9.5% p.a. included in the gross salary of the employee.

(iv) Exemptions from tax are covered under section 10 and 11 of the income tax act

and deductions are covered under chapter VIA of the Income Tax act.

Certain incomes are exempt and they are not considered during the

calculation of total income such as interest from PPF, dividends from Indian

companies, agricultural income, income from NRE account, etc. These are

known as exempt incomes.

But deductions are done from taxable income suppose you invest in ELSS,

PPF, LIC ,etc. pay medical insurance or donate to approved charitable

institutions then you get deductions from your gross total income. There are

however limitations to the quantum of deductions. as per provision laid down in

Sec. 80

7.26 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

2010 - June [3] (b) Distinguish between the following:

(iii) ‘Exemption to capital gains under section 54G’ and ‘exemption to capital gains

under section 54GA’. (2 marks)

Answer:

Exemption under section 54G is available for capital gains on transfer of assets in cases

of shifting of industrial undertakings from urban areas whereas exemption under section

54GA is available for capital gains on transfer of shifting of industrial undertaking from

urban area to any special economic zone.

Under section 54G the transfer is affected in the course of or in consequence of shifting

the undertaking from an urban area to any area whereas under section 54GA the

transfer is effected in the course of or in consequence of shifting the undertaking from

an urban area to any special economic zone.

2010 - Dec [5] (a) Distinguish between the following:

(i) ‘Long-term capital gains’ and ‘short-term capital gains’.

(iii) ‘Normal depreciation’ and ‘additional depreciation’. (4 marks each)

Answer:

(i) Please refer 2009 - June [3] (a) (ii) on page no. 34

(iii) Normal depreciation & additional depreciation

(a) Normal depreciation is available in respect of all tangible assets and

intangible asset such as building, machinery, plant, furniture, patent, etc.

while additional depreciation is available only in the case of Plant &

Machinery.

(b) Normal depreciation is available in respect of both types of new and old

while additional depreciation is available only in respect of new plant &

machinery which is acquired and installed after 31st March, 2005

(c) Normal depreciation is computed by applying different rates of depreciation

prescribed for a particular asset while additional depreciation is computed

by applying a uniform rate of depreciation viz. 20% of the actual cost of new

plant & machinery

(d) The system of “block of assets” is quite relevant for computing normal

depreciation while it is not relevant for computing additional depreciation

(e) Any plant & machinery which is used in business of the assessee is eligible

for normal depreciation while certain plant & machinery, even if new, are not

eligible for additional depreciation like ships and aircrafts, plant & machinery

which was already used by a person either in India or abroad, plant &

machinery which is used in any office premises or any residential

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.27

accommodation or in a guest house, any office appliances or road transport

vehicle or plant & machinery the entire cost of which has already been

allowed as deduction either by way of depreciation or otherwise.

2011 - June [4] (b) Distinguish between the following:

(i) 'Cost of acquisition' and 'cost of improvement'.

(iii) 'Short-term capital gains' and 'long-term capital gains'. (3 marks each)

Answer:

(i) Please refer 2008 - Dec [3] (b) (ii) on page no. 33

(iii) Please refer 2009 - June [3] (a) (ii) on page no. 34

2011 - Dec [4] (a) Distinguish between the following:

(ii) ‘Allowances’ and ‘perquisites’.

(iv) ‘Exemption under section 54G’ and ‘exemption under section 54GA’.

(v) ‘Statutory provident fund’ and ‘public provident fund’. (3 marks each)

Answer:

(ii) ‘Allowances’ and ‘perquisites’

S.No. Allowance Perquisites

1. An allowance is a cash payment to

employees on regular basis in

addition to salary to meet certain

expenses incurred by him in

connection with duties of his office

or to compensate him for any

expenditure relating to performance

of his duty in particular circums-

tances or at particular place or

under a contract

Perquisites means any casual emolument,

fee or profit attached to an office or

position in addition to salary or wages.

2. An allowance may be wholly

taxable, partially taxable or wholly

exempt

It is a personal advantage & benefit of the

recipient. It may also be given voluntary or

under a contract, in cash or in kind by way

of goods, service benefit or amenities

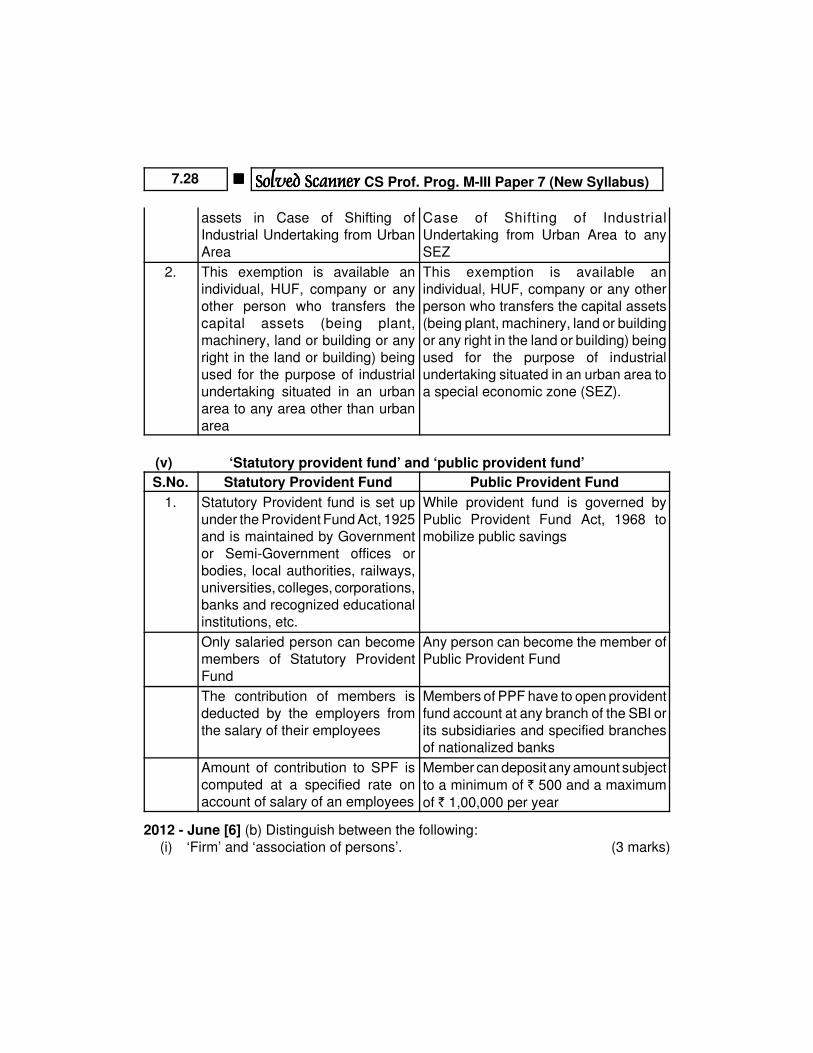

(iv) ‘Exemption under section 54G’ and ‘exemption under section 54GA’

S.No. Exemption under section 54G Exemption under section 54GA

1. This exemption is available on

Capital Gain on Transfer of Capital

This exemption is available on Capital

Gain on Transfer of Capital assets in

7.28 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

assets in Case of Shifting of

Industrial Undertaking from Urban

Area

Case of Shifting of Industrial

Undertaking from Urban Area to any

SEZ

2. This exemption is available an

individual, HUF, company or any

other person who transfers the

capital assets (being plant,

machinery, land or building or any

right in the land or building) being

used for the purpose of industrial

undertaking situated in an urban

area to any area other than urban

area

This exemption is available an

individual, HUF, company or any other

person who transfers the capital assets

(being plant, machinery, land or building

or any right in the land or building) being

used for the purpose of industrial

undertaking situated in an urban area to

a special economic zone (SEZ).

(v) ‘Statutory provident fund’ and ‘public provident fund’

S.No. Statutory Provident Fund Public Provident Fund

1. Statutory Provident fund is set up

under the Provident Fund Act, 1925

and is maintained by Government

or Semi-Government offices or

bodies, local authorities, railways,

universities, colleges, corporations,

banks and recognized educational

institutions, etc.

While provident fund is governed by

Public Provident Fund Act, 1968 to

mobilize public savings

Only salaried person can become

members of Statutory Provident

Fund

Any person can become the member of

Public Provident Fund

The contribution of members is

deducted by the employers from

the salary of their employees

Members of PPF have to open provident

fund account at any branch of the SBI or

its subsidiaries and specified branches

of nationalized banks

Amount of contribution to SPF is

computed at a specified rate on

account of salary of an employees

Member can deposit any amount subject

to a minimum of ` 500 and a maximum

of ` 1,00,000 per year

2012 - June [6] (b) Distinguish between the following:

(i) ‘Firm’ and ‘association of persons’. (3 marks)

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.29

Answer:

A firm refers to a partnership firm. Partnership has been defined under the Partnership

Act, 1932 as "relationship between persons who have agreed to share the profits of a

business carried on by all or any of them acting for all.” Persons who have entered into

partnership with one another are individually called partners and collectively a firm and

the name under which their business is carried on, is call the firm’s name.

An association of persons (AOP) implies a voluntary getting together for a common

design or particular venture to engage in an income producing activities.

2012 - Dec [6] (c) Distinguish between the following:

(i) ‘Recognised provident fund’ and ‘unrecognised provident fund’.

(iii) ‘Taxation of unrealised rent received’ and ‘taxation of arrears of rent received’.

(3 marks each)

Answer:

(i) Recognized Provident Fund is set-up under the provisions of Employee's

Provident Fund Act, 1952. This fund is maintained by the private sector

organizations and factories.

Apart from this where provident fund maintained by other organization is

recognized by the income-tax authorities, such fund is also deemed as

recognized provident fund. On the other hand statutory provident fund is set-up

under the provisions of Provident Fund Act, 1925. This fund is applicable to the

employees of Central Government, State Government and Semi-Government.

Under this fund only the employee's contribution is deposited. The Government

does not contribute any amount while in case of RPF both employer and

employee can deposit the contribution. Employer's contribution to RPF up to

12% of salary is exempted and any amount in excess of 12% is included in gross

salary of the employee. Interest up to 9.5% p.a. is exempted and any amount of

interest in excess of 9.5% p.a. included in the gross salary of the employee

(iii) Taxation of unrealized rent received and taxation of arrears of rent received

Provisions regarding taxation of unrealized rent are given under section 25AA,

where the assesses cannot realize rent from a property let to a tenant and

subsequently the assesses has realized any amount in respect of such rent the

amount so realized shall be deemed to be the income chargeable under the

head income from house property and accordingly charged to income tax as the

income of that previous year in which such rent is realized whether or not the

assessees is the owner of that property in the previous year.

While in case of taxation of arrears of rent, section 25B provides that if any

arrears of rent are received in subsequent year the same will be taxed in the

7.30 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

year of receipt whether the property is owned by the assesses in the year of

receipt or not, deduction of sum equal to 30% of such amount of rent shall be

allowed towards receipts and collection of rent.

DESCRIPTIVE QUESTIONS

2008 - Dec [3] (a) Attempt the following:

(ii) “Expenditure on scientific research is allowed as deduction even if contribution

is made to other institutions for scientific research.” Explain the statement.

(iii) A Person receives money from an insurer on account of damage to a capital

asset resulting from accidental fire. Whether such money shall be taxable as

capital gains? Explain. (3 marks each)

Answer:

(ii) • Contribution made to an approved Scientific Research Association/

University/ College/ Institution, a weighted deduction of 175% of the

contribution paid is available [Section 35(1) (ii)]. Such association has, as its

object, undertaking of scientific research related or unrelated to the business

of the assessee

• The payment is made to an approved university, college or institution for the

purpose of scientific research that is related or unrelated to the business of

the assessee, a weighted deduction of 125% is allowed.

• The payment is made to an approved university, college or institution for the

purpose of research for social sciences that is related or unrelated to the

business of the assessee

Contribution made to an approved Scientific Research Company, a weighted

deduction of the contribution paid is available subject to following conditions

[Section 35(1)(iia)]

• The Taxpayer may be any Person as defined under the Income Tax Act,

1961

• The Payee Company is registered in India;

• The scientific research may/ may not be related to the business of the

company;

• The Payee Company has as its main object Scientific research and

development;

• The Payee Company is, for the purposes of this clause, for the time being

approved by the prescribed authority in the prescribed manner;

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.31

• The Payee Company fulfils such other conditions as may be prescribed.

However deduction under Section 35(1)/ (2) would continue to be allowed being

Revenue/ Capital expenditure incurred.

Contribution made to Notified Institutions, wherein weighted deduction is

available to the extent of 200% of such payment made [Section 35(2AA)]

The Notified institutions are:

(i) National Laboratory.

(ii) University.

(iii) Indian Institute of Technology.

(iv) Specified persons as approved by the prescribed authority.

• The above payment is made under a specific direction that it should be

used by aforesaid persons for undertaking scientific research

programs approved by the prescribed authority.

(iii) Yes, such money shall be taxable as capital gains.

Where any capital asset is destroyed as a result of fire, earthquake or for any

other reasons, e.g. sinking of a ship, etc, such destruction of asset will be

included in the extended meaning of the word ̀ transfer'. Section 2(47) of the Act

which defines `transfer' does not include destruction of an asset.

2008 - Dec [6] (b) Indicate the amount of deduction available to an assessee from his

gross total income under section 80GG in respect of rent paid. Point out the

circumstances when the deduction will be denied. (7 marks)

Answer:

Deduction in respect of Rent Paid (Section 80GG)

Deduction admissible under this section is:

C Actual rent paid less 10% of Adjusted Total Income

C 25% of such Adjusted Total Income

C Amount calculated at ` 2,000 p.m.

Whichever is least

Adjusted Total Income is the adjusted total income under section 80G except exempted

income less long term capital gain. However, certain conditions as given below are

required to be fulfilled/satisfied for claiming u/s 80GG

(i) The assessee should not be receiving any house rent allowance exempt under

section 10(13A) or rent free accommodation

(ii) The accommodation should be occupied by the assessee for the purpose of his

own residence

(iii) The assessee fulfills such other conditions or limitations as may be prescribed

having regard to the area or place in which such accommodation is situated and

7.32 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

other relevant consideration.

(iv) The assessee or his spouse or his minor child or an HUF of which he is a

member does not own any accommodation at the place where he ordinarily

resides or performs duties of his office or employment or carries on his business

or profession.

(v) If the assessee owns any accommodation at any place other than that referred

to above, such accommodation should not be in occupation of the assessee and

its annual value is not required to be determined.

(vi) Allowed only to an individual assessee after furnishing Form 10BA along with

return of income.

2009 - June [4] (c) Discuss the items which are disallowed as deduction under section

40 (b) while computing firm's income from business and profession. (3 ‘marks)

Answer:Section 40 (b) deals with the amount which are not deductible in case of a firm.Therefore deductions on accounts of interest and remunerations to the partners can beclaimed u/s 36 or 37, as the case may be, but it will be subject to conditions prescribedby section 40(b) which are as follows:1. Payment of salary, bonus, commission or remuneration, by whatever name called

to non – working partner shall not be allowed as deduction.2. Remuneration to working partners and interest to any partner will be allowed as

deduction only when it is authorized by partnership deed.3. Payment of remuneration/interest although authorized by partnership deed but

which relates to a period prior to the date of such partnership deed shall not beallowed.

4. Interest payable to a partner shall be allowed as deduction subject to a maximumof 12% simple interest p.a.

If the partnership deed provides for an interest @ less than 12% p.a. thendeduction of interest shall be allowed to that extent.

5. Payment of remuneration to a working partner although relates to period after thedate of partnership deed and authorized by the partnership deed shall be allowedas deduction to the extent provided in the partnership deed but subject to themaximum limits provided in the act.

2009 - Dec [4] (a) What are the special provisions for computing profits and gains ofretail business? (5 marks)(b) What are the provisions relating to clubbing of income arising to spouse from the

assets transferred ? (5 marks)Answer:(a) Provisions under section 44 AD shall become Applicable in case of an assessee

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.33

engaged in any business except the business of plying, hiring or leasing goodscarriage, 8% of the total turnover or such higher income as may be returned by theassessee shall be deemed to be the profits of such business. This provisionapplies only if the total turnover of sales of such retail business does not exceed` 1 crore. In calculating such presumptive profits @ 8% of sales the said provisionsshall have to be considered(i) All deductions u/s 30 to 38 including deprecation shall be deemed to have

been allowed [i.e no expenditure shall be allowed as deduction from suchincome @ 8% of T/o]

(ii) Provisions of Sec. 44AA & 44AB pertaining to maintaining of books ofAccounts & disallowance with reference to monetary limits of transactions shallnot apply. However all such data which [i.e. maintenance of books of accountsis not required] shall show the calculation of sales, stock, debtors, creditorsshall be maintained by the assessee.

(iii) In case of an assessee which is a firm to which prov. of 44AD are applied, the

salary/remuneration & interest paid to its partners shall be deducted from the

income computed under this provisions & the allowance of

salary/Remuneration & interest shall be subject to the conditions & limits

specified in sec 40(b)

(iv) WDV of assets used for the purpose of such business shall be calculated as

if depreciation has been actually provided.

(b) As per the provision of Sec 64(1) (iv) in computing the total income of the

individual, all such income arising directly or indirectly to the spouse of such

individual from assets transferred to the spouse by such individual otherwise then

for adequate consideration or in connection with an agreement to live apart shall

be clubbed in the income of transferor. However any further income earned on

such clubbed income shall be taxable in the hands of spouse.

Income from assets transferred to any person for the benefit of the spouse of the

transferor as per the provision of sec 64(1) (vii) shall be taxable in the hands of

transferor of the asset.

Condition for clubbing:

1. The relationship of husband and wife must exist both at the time of transfer of asset

and at the time of accrual of income.

2. Consideration must be NIL or inadequate.

3. Where such assets or cash transfer by way of gift to the spouse is invested by the

transferee in any business (except by way of capital contribution in a partnership

firm), the income shall be clubbed in the following manner.

7.34 OOOO Solved ScannerSolved ScannerSolved ScannerSolved Scanner CS Prof. Prog. M-III Paper 7 (New Syllabus)

No clubbing provision shall persist where both the spouse are prof. qualified and are

partners earning income by virtue of the qualifications.

2009 - Dec [5] (c) “Loss under any head of income for any assessment year can be set-

off against the income from other heads of income but when it has to be carried forward

for being set-off, it can only be set-off from income under the same head.” Explain.

(5 marks)

Answer:

Income of a person is computed under five heads. ‘Sources’ of income derived by an

individual may be many but yet they could be classified under the same head. For

instance, an individual may have a dual employment, yet the income would be classified

under the head ‘Salaries’. However, given the mechanism of computing taxable salary

income, it would be safe to say that an individual cannot incur losses under this head

of income. Consider a situation where Harsh has two properties – one, occupied by him

and the other, let out. Harsh pays interest on loan of ` 1.50 lakh on the property

occupied and derives net rental income of ̀ 1.50 lakh from the let-out property. In case

of a self-occupied property, income is computed as nil and interest expenditure results

in loss. The loss of ` 1.50 lakh can be set off against rent income of ` 1.50 lakh; the

income chargeable under the head ‘House property’ will be ‘Nil’.

An exception to intra head set off is loss under the head ‘Capital gains’, which may

arise from transfer of any capital asset. Long-term capital loss arises from transfer of

shares or units where holding period is more than 12 months and in respect of other

assets holding period is more than 36 months prior to sale. Transfer of assets held for

less than prescribed period results in short-term capital loss. Long-term capital loss

cannot be set off against short-term capital gains. but S. Term loss can be adjusted

against S.T.C.G or LTCG.

Further, loss incurred from speculation loss (e.g. from shares or commodities)

cannot be set off against any other income.

Also, it is unlikely that the benefit of set off of loss under an activity or source will

be available, where the income from an activity or source is exempt from taxation.

2009 - Dec [6] (b) What are ‘capital assets’ ? What items are not included in capital

assets? (5 marks)

Answer:

As per the definition of capital asset under section 2(14), Capital asset means property

of any kind, whether fixed, circulating, movable, immovable, tangible or intangible. The

following are however excluded:

[Chapter #### 1] Taxation of Individuals, Partnership Firms/LLP... OOOO 7.35

(i) Any stock in trade, consumable stores or raw materials held for the purposes of

business or profession.

(ii) Personal Assets of the assessee, i.e., movable property (including wearing

apparels of the assessee and furniture) held for personal use, but excludes:

• Jewellery;

• Archaeological collections;

• Drawings;

• Paintings;

• Sculptures;

• Any work of art.

(iii) Rural agricultural land in India.

(iv) Gold Deposit Bonds issued under Gold Deposit scheme 1999.

(v) Special Bearer bonds 1991 issued by the Central Government.

(vi) 6.5% Gold Bonds 1977; 7% Gold Bonds 1980 or National Defense Gold bonds

1980 issued by the Central Government.

2010 - June [3] (a) An asset is transferred by a person to another person under a partly