Embed Size (px)

Citation preview

1

U.S. Expansion and Upgrade

Growth investment at 9 of 12 domestic refineries

Bayway

LakeCharles

Sweeny

WoodRiver

Ponca City

Borger

Billings

LAR

Rodeo

Ferndale

Trainer

Alliance

Investment Drivers:• Advantaged crude growth• Growing clean products• Enhancing E&P integration• Increasing capacity

$4 – $5 B Investment Program(2006 – 2011)

$4 – $5 B Investment Program(2006 – 2011)

2

Heavy Sour

SweetSweet

Current Future

Heavy Sour

SourSour

Grow U.S. Refining Capabilities

• Integration with E&P

• Enhanced refining profitability

• Attractive economics

• Increased capabilities

Capacity DistributionCapacity Distribution$4 – $5 B Investment Program(2006 – 2011)

$4 – $5 B Investment Program(2006 – 2011)

3

Commercial

• Scope

- 2.5 B BBL/yr crude oil and refined products

- 4.2 TCF/yr gas marketing business

- Global trading operation

• Objectives- Optimize value chain to maximize earnings

- Trade around asset base & market knowledge for additional value

• Financial contribution- Improves total company ROCE

- Included in E&P / R&M realizations

4

• LUKOIL’s sole equity partner

• 14.8% equity ownership1, moving to 20%

• JV partner in Timan-Pechora

• Jointly pursuing upstream and downstream opportunities globally

• 2005 earnings2 estimated at $700 MM

LUKOIL Update

1 Equity ownership as of the end of third-quarter 2005.2 2005 equity earnings to COP are based on annualized YTD Q3 actuals.

5

Technology

• Enable E&P / R&M initiatives– Heavy oil, Arctic, LNG – Clean fuels / hydroprocessing,

coking, alkylation– Capacity expansion and flexibility– Project management / execution

• Emerging energy opportunities – Disciplined, phased approach– Extending core competencies– Renewable fuels– E-GasTM Gasification Technology

6

Rising to the Challenge• Deliver strong operating and financial performance

– Continued focus on Operating Excellence

– Manage cost inflation and project execution

• Well-defined, sustainable growth plan– Portfolio of strong E&P / R&M growth projects

– Increased production and refining capacity / capability

• Financial strategy to complement value creation

SettingObjectives

2003

DeliveringPerformance

2004

Raising Expectations

2005

Continuous improvement Shareholder value creation

Investing for Growth

2006+

7

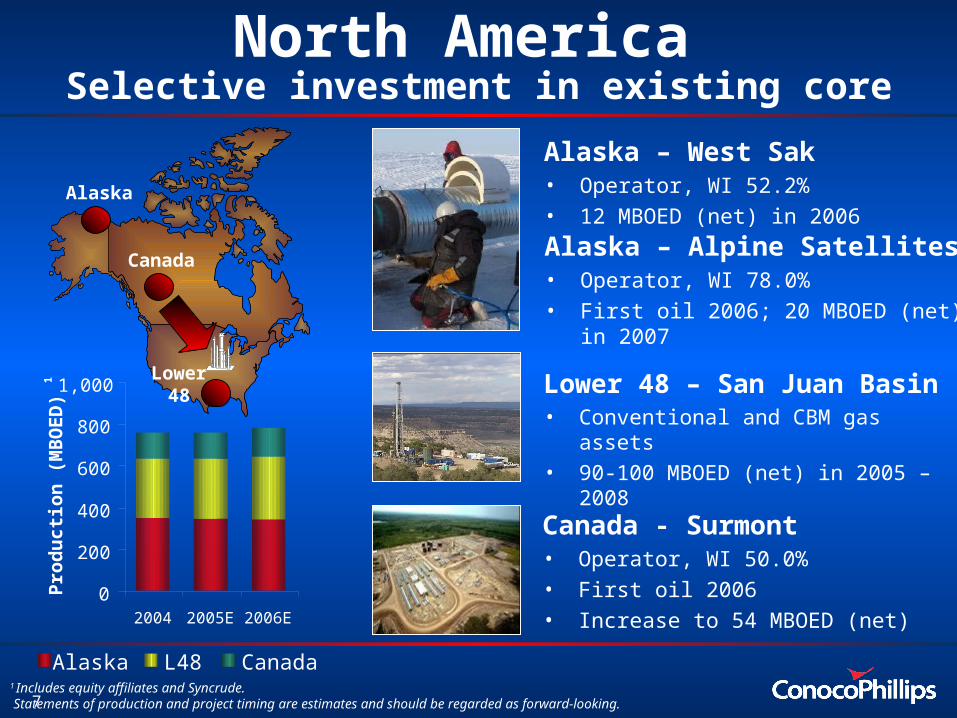

North America Selective investment in existing core

Alaska – West Sak• Operator, WI 52.2%• 12 MBOED (net) in 2006

Canada - Surmont• Operator, WI 50.0%• First oil 2006• Increase to 54 MBOED (net)

1 Includes equity affiliates and Syncrude. Statements of production and project timing are estimates and should be regarded as forward-looking.

Alaska

Canada

Lower 48 Lower 48 – San Juan Basin

• Conventional and CBM gas assets• 90-100 MBOED (net) in 2005 – 2008

Alaska – Alpine Satellites• Operator, WI 78.0%• First oil 2006; 20 MBOED (net) in 2007

0

200

400

600

2004 2005E 2006E

800

1,000

Pro

du

ctio

n (

MB

OE

D)

1

Alaska L48 Canada

8

ANS

Mackenzie Delta

Alaska - ANS Gas• WI 4.9-36.1%• COP agreement in principle with State• Largest leaseholder• Estimated net resources of 8 TCF• Estimated net production of

~1-1.3 BCFD • Federal enabling legislation in 2004

Canada - Northern Gas• Mackenzie Delta – Estimated net

resources of 1.8 TCF • Initial net production of 230 MMCFD• Ongoing negotiations• Startup 2011• Additional upside potential

North AmericaArctic gas

Statements of production and project timing are estimates and should be regarded as forward-looking.

9

North Sea Selective investment in existing core

Norway - Ekofisk Growth• Operator, WI 35.1%• First oil October 2005 • 25 MBOED (net) in 2009

1 Combined Satellite WI - Callanish WI 83.5%, Brodgar WI 75%. Statements of production and project timing are estimates and should be regarded as forward-looking.

Greater Ekofisk

Greater Britannia

AlvheimU.K. - Britannia Satellites• First oil 2007; Operator, WI 79.0%• Development drilling is complete• 50 MBOED (net) in 2007

1

Norway - Alvheim• First oil 2007, WI 20.0%• FPSO and subsea completions• 15 MBOED (net) in 20070

200

400

600

2004 2005E 2006E

Pro

du

ctio

n (

MB

OE

D)

U.K. Norway

10

0

200

400

600

800

2004 2005E 2006E

China

Australia / Timor-LesteVietnam

Indonesia

Venezuela

1

Rest of World

LUKOIL

Pro

du

ctio

n (

MB

OE

D)

New Legacy Growth AreasIncreasing access and growing production

1 Includes equity affiliates and Syncrude. Statements of production and project timing are estimates and should be regarded as forward-looking.