Embed Size (px)

Citation preview

1

V. Simplifying the Portfolio Process

2

Simplifying the Portfolio Process Estimating correlations

Single Index ModelsMultiple Index ModelsAverage Models

Finding Efficient Portfolios

3

1956 Markowitz – not implemented

i j2 2

j=12

j ii=1 i=1

NN NX X X

NR X Rp i ii 1

i i i j ijp

4

5

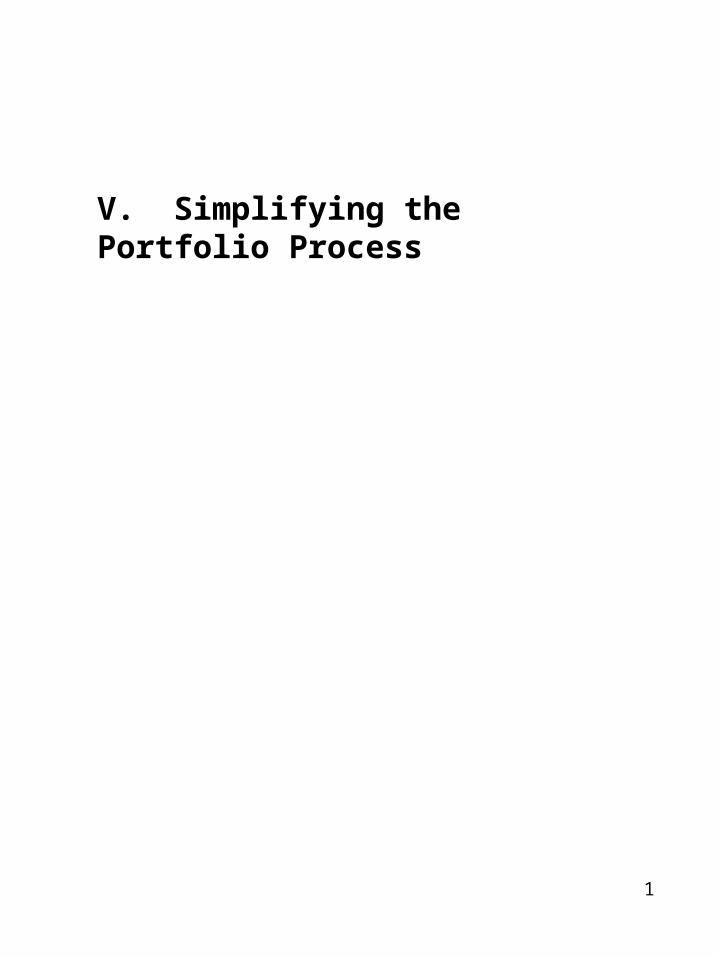

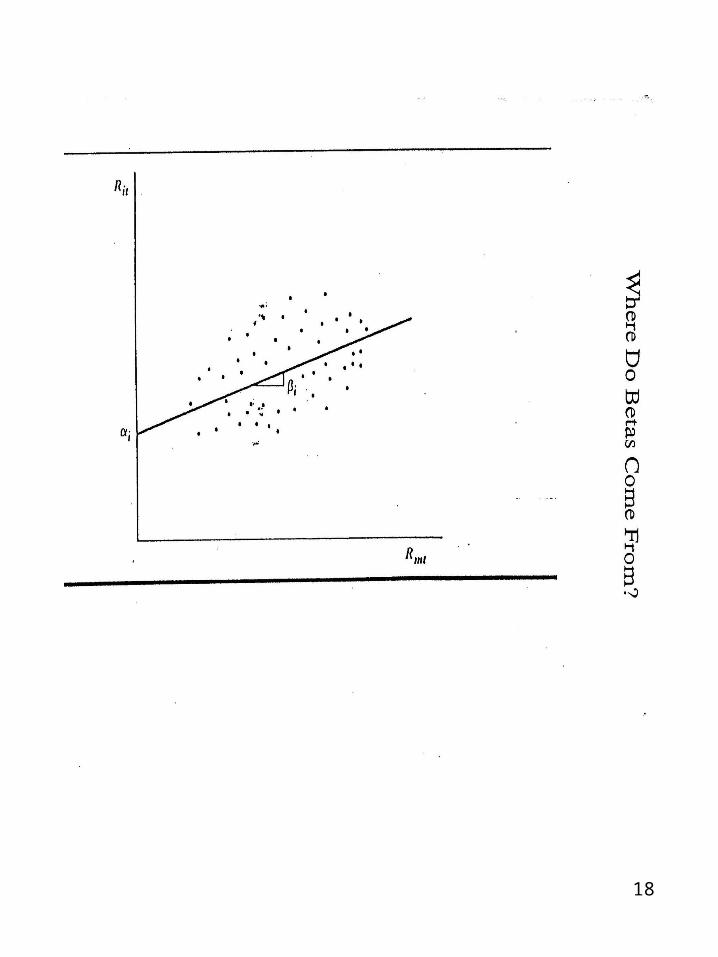

MRiiaiR

iEa

i or e

i i ia

R R eMi i i i

= return on the market = what expect stock i to return if Rm = 0 = sensitivity of stock i to return on the

market = random element of return

MR

i

i

ie

6

Sharpe Single Index Models Basic Equation

ieRiiiRM

By Construction

0ieE i = 1,2,…N

By Definition

2ei

2ieE i = 1,2,…N

E2

2R RMM M

By Assumption

0M

RMR ,ieE

i = 1,2,…N

E e , e 0i j

j i; i = 1,2,...N; j=1,2...N

7

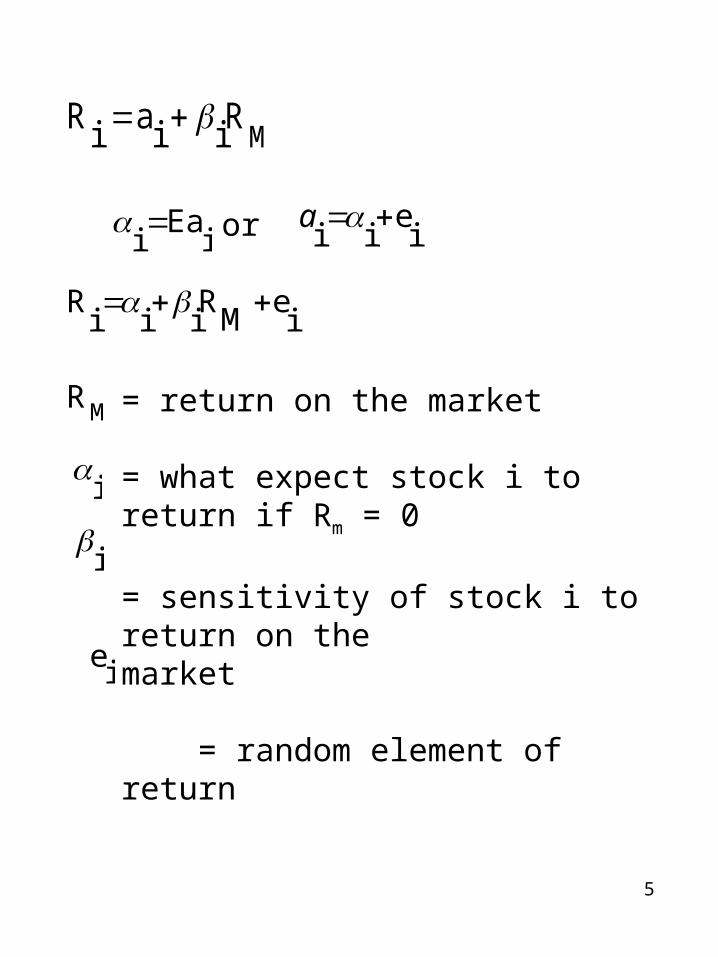

Expected Value

MRiiR i

1. EN N N

R X E R X R XP i i i i i iMi 1 i 1 i 1

E( ) MP P PR a R

8

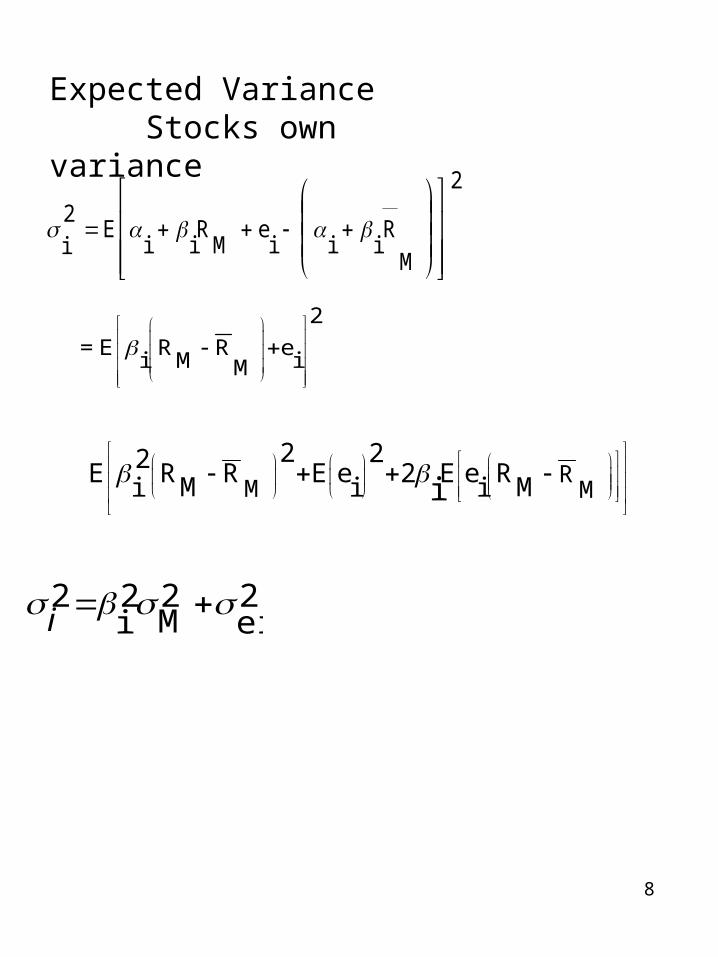

Expected VarianceStocks own variance

2

MR

iiie

MR

iiE

2i

2

= E R R ei M iM

RM M

2 22E R R E e 2 E e RM Mi i ii

2ei

2M

2i

2 i

9

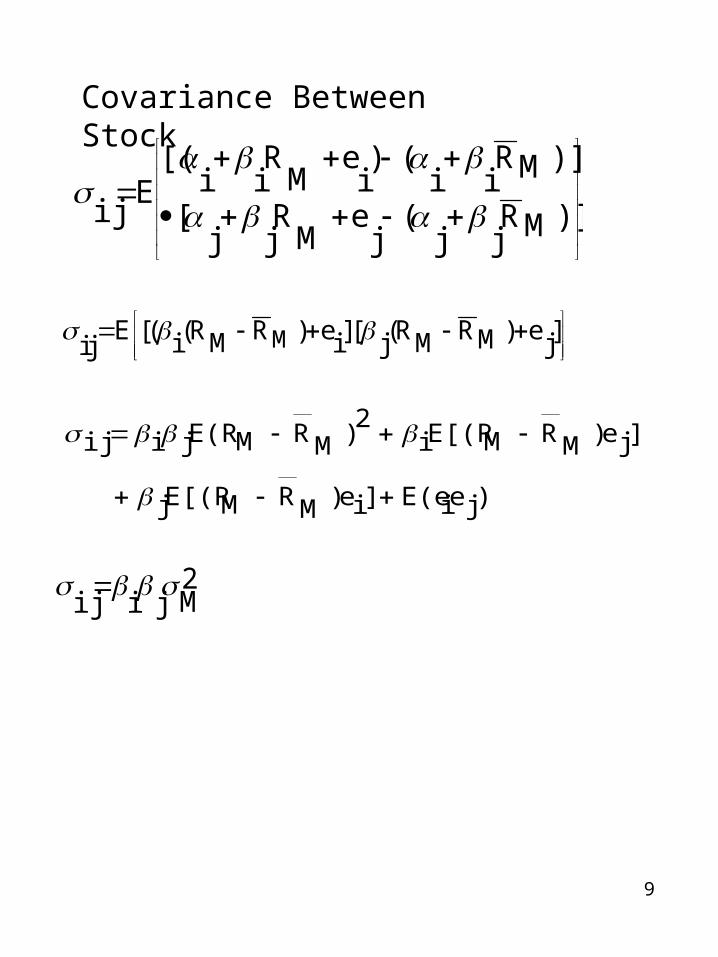

Covariance Between Stock

)]MRjj

(j

eM

Rjj

[

)]MRii

()i

eM

Rii

[(E

ij

ME [( (R R ) e ][ (R R ) e ]M Mi i j jij M

)jeiE(e]ie)MRME[(Rj

]je)MRME[(Ri2

)MRME(Rjiij

2Mjiij

10

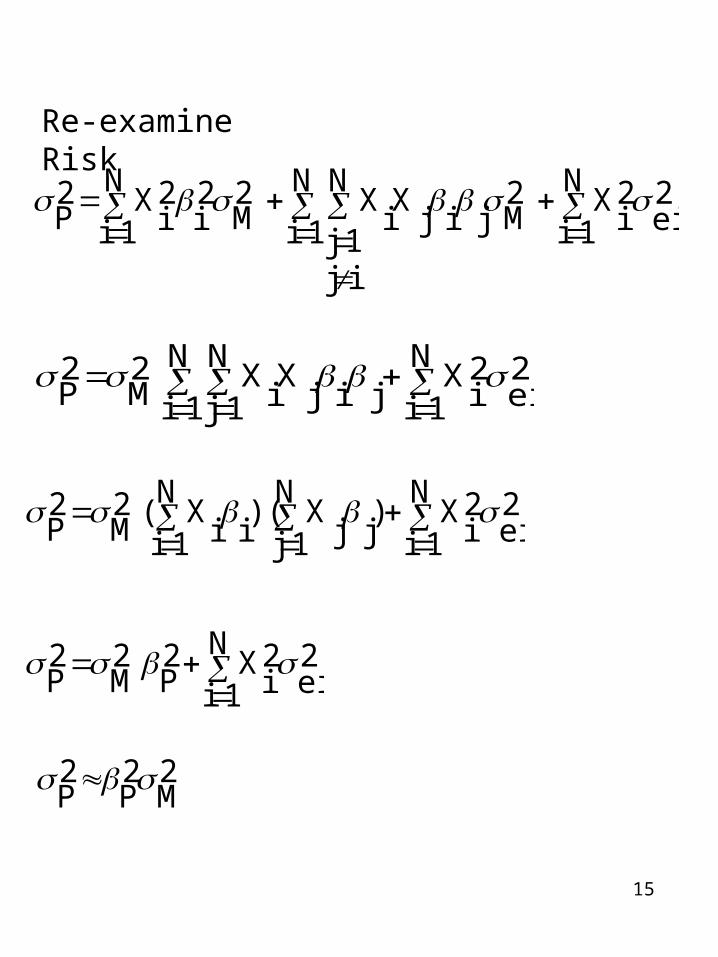

N N N2 2 2 X X XP i i i j ij1 i 1j 1

j i

i

2 2 2 2 Mi i ei

2Mjiij

N

1i MRi

N

1i iiXPR .1

11

N

1i2ei

2i

X2Mjij

XN

1i

N

1i

N

ij1j

iX2

M2i

2i

X2P

a b c a Stocks own variances due to market b Covariance risk c Independent component of stocks own

variance

12

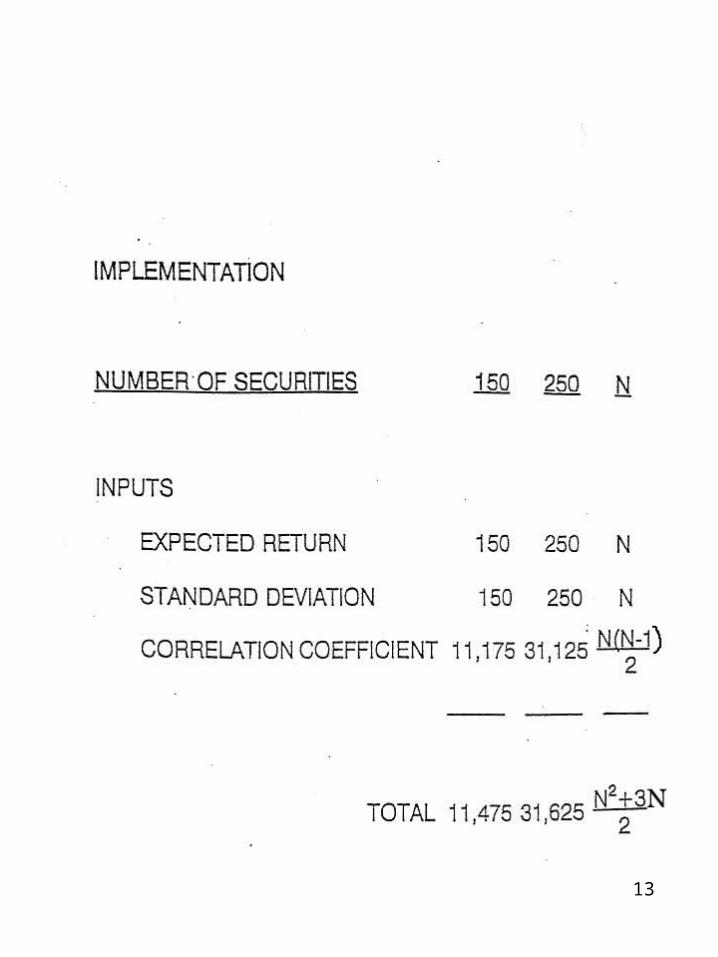

# of rec. N 150 250

i N 150 250

i N 150 250

2ei

N 150 250

MR 1 1 1

2M 1 1 1

Sharpe Single Index3N + 2 452 752

General Model 2N+N(N-1) 2

(11,475) (31,625)

13

14

Alternative way of getting inputs

N Securities

Input Alternative Input

i

i N

i

iRN

2ei

2i

MRM

R

2M

2M

N

1

1

3N + 2

Miii RR

2ei

2M

2i

2i

15

Re-examine Risk

N

1i2ei

2i

X2Mjij

XN

1i

N

1i

N

ij1j

iX2

M2i

2i

X2P

2ei

N

1i2i

Xjij

XN

1i

N

1j iX2

M2P

N

1i2ei

2i

X)N

1i

N

1j jjX)(

iiX(2

M2P

N

1i2ei

2i

X2P

2M

2P

2 2 2 P P M

16

2M

2P

2P

2ei

2M

2i

2i

Non Diversifiable DiversifiableMarket Risk Residual Risk

17

18

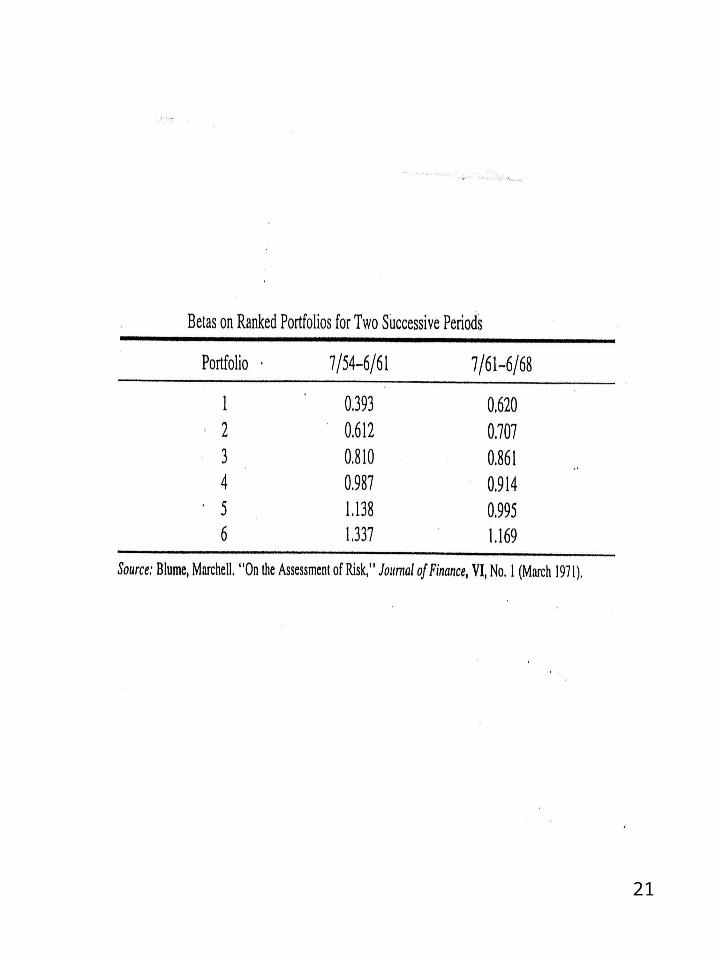

19

ieMRiiiR

60

1t 60

1t2]RMt[R

)]RMtR)(Rit[(R

2M

iMi

Mt

Mtit

R Ri i Mi

20

21

22

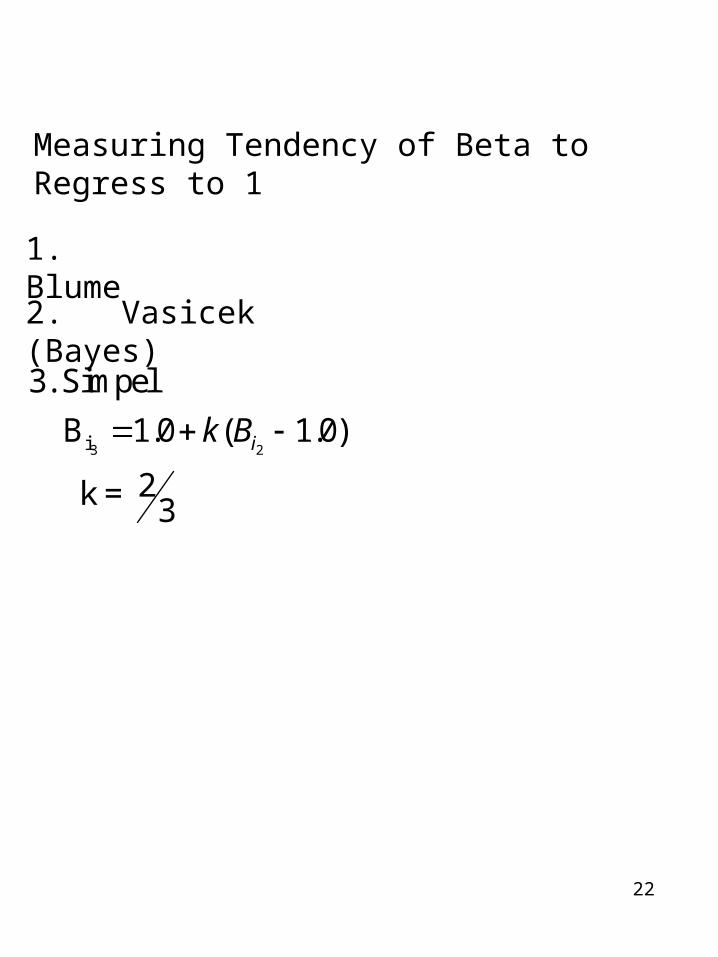

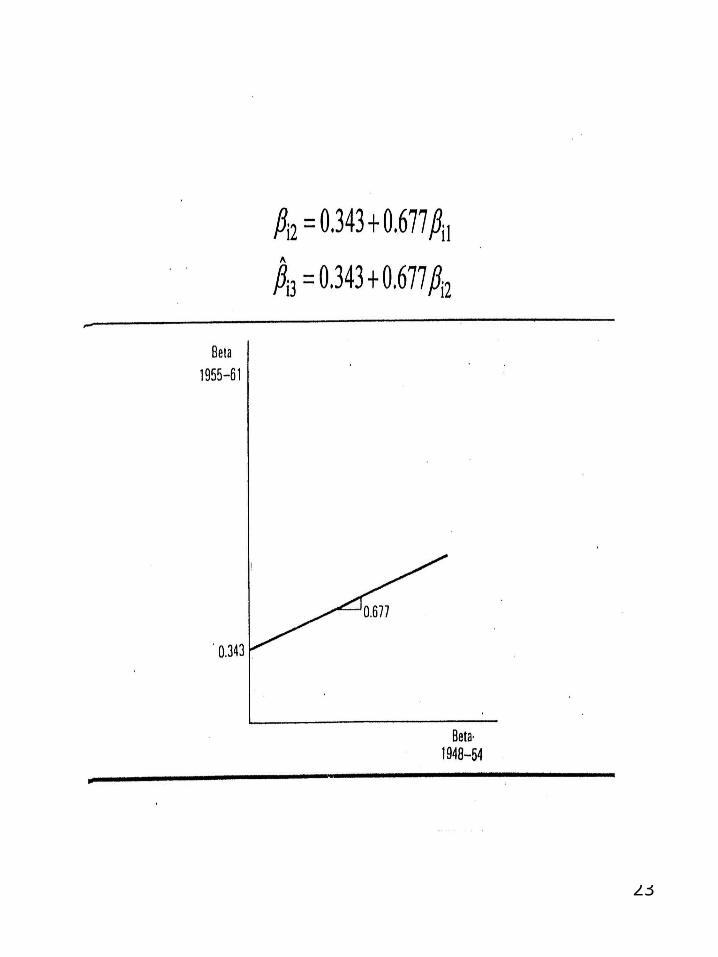

Measuring Tendency of Beta to Regress to 1

1. Blume

2. Vasicek (Bayes)

3 2i

3. Simpel

B 1.0 ( 1.0)

2 k = 3

ik B

23

24

Vasicek

2

2

22 i2

2

ˆ i2i3 1 1

2 2

i2

25

How Well Do They Forecast Future Betas

1. Vasicek2. Blume3. Unadjusted4. All Betas = 1.0

26

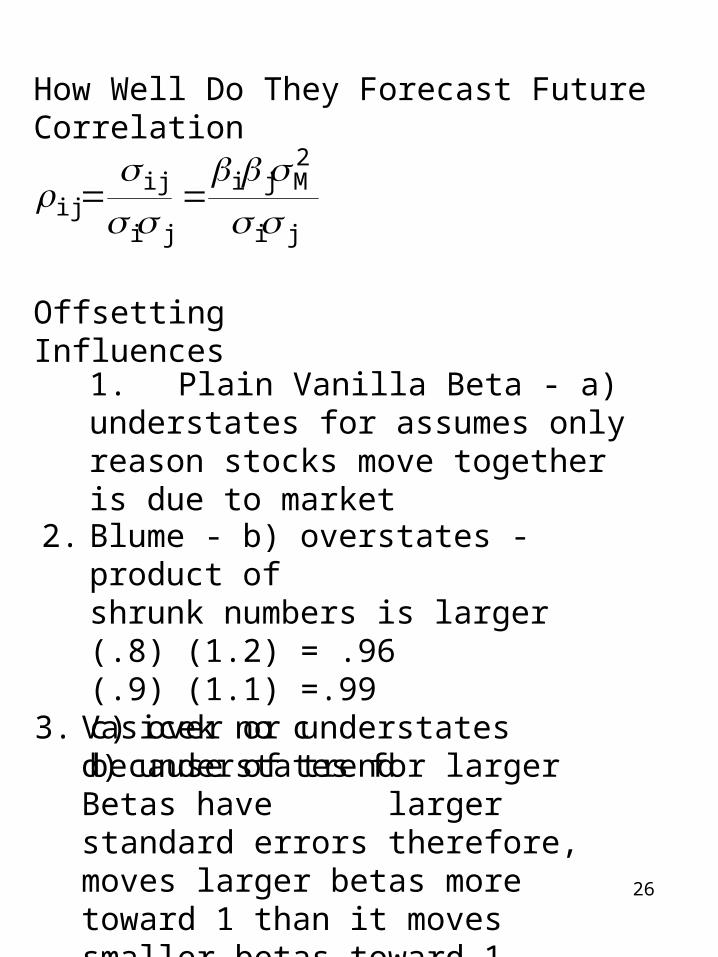

How Well Do They Forecast Future Correlation

ji

2Mji

ji

ijij

Offsetting Influences

1. Plain Vanilla Beta - a) understates for assumes only reason stocks move together is due to market

Blume - b) overstates - product of shrunk numbers is larger (.8) (1.2) = .96(.9) (1.1) =.99 c) over or understates because of trend

2.

Vasicek no c

d) understates for larger Betas have larger standard errors therefore, moves larger betas more toward 1 than it moves smaller betas toward 1.

3.

27

Which of these biases are more important - empirical matter - ranking when adjust for mean

1. Vasicek2. Blume3. Plain Vanilla Beta4. Beta = 15. Historical

28

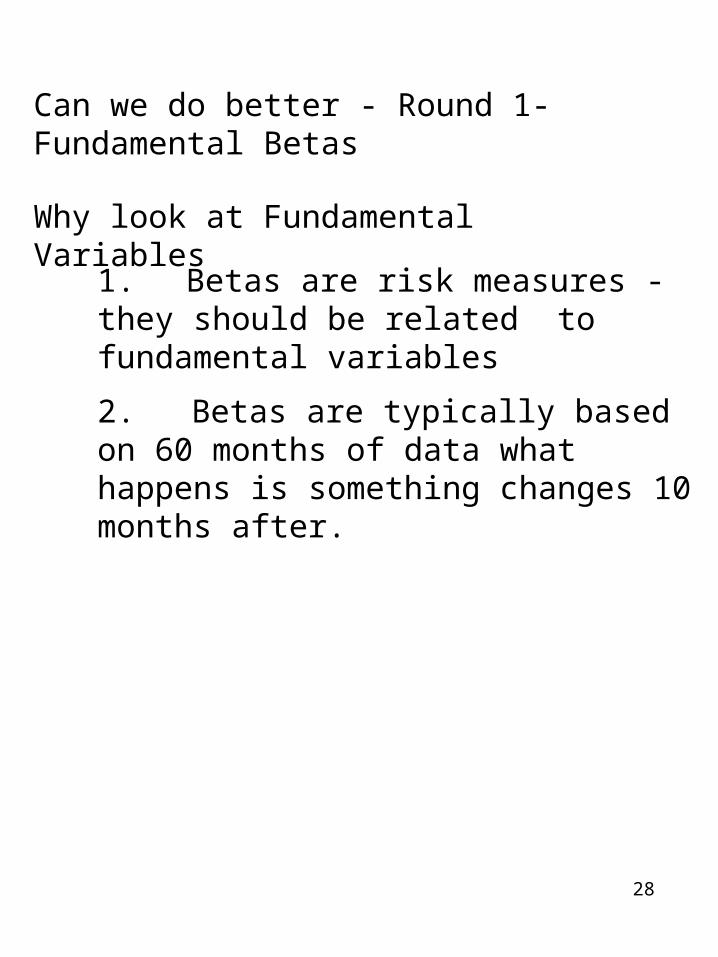

Can we do better - Round 1- Fundamental Betas

Why look at Fundamental Variables

1. Betas are risk measures - they should be related to fundamental variables

2. Betas are typically based on 60 months of data what happens is something changes 10 months after.

29

30

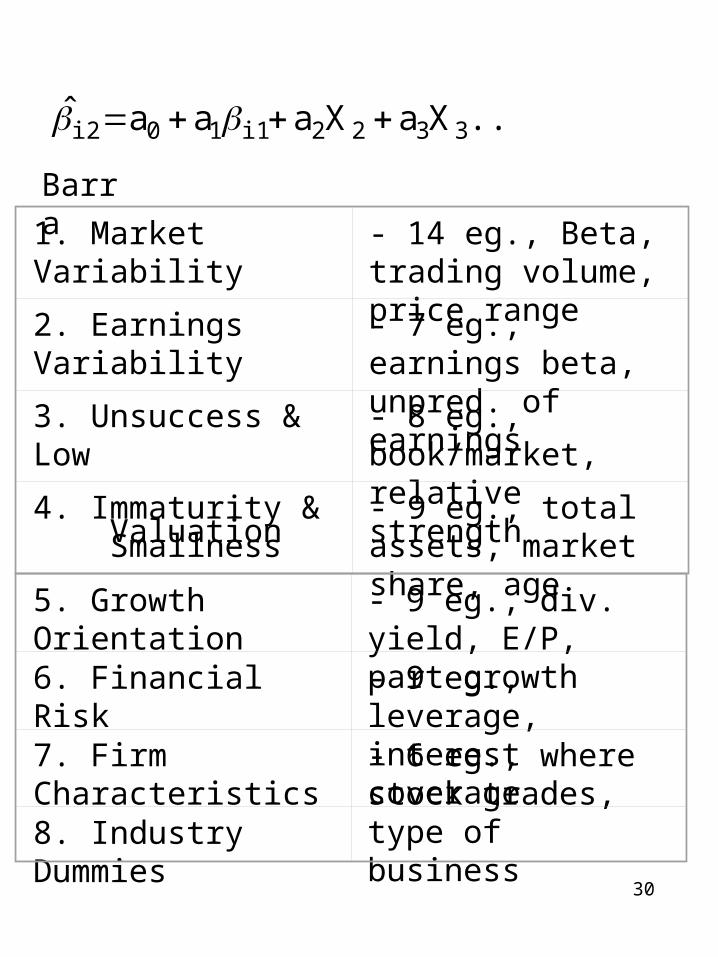

....XaXaaaˆ3322i110i2

Barra

1. Market Variability - 14 eg., Beta, trading volume, price range

2. Earnings Variability - 7 eg., earnings beta, unpred. of earnings

3. Unsuccess & Low Valuation

- 8 eg., book/market, relative strength

4. Immaturity & Smallness

- 9 eg., total assets, market share, age

5. Growth Orientation - 9 eg., div. yield, E/P, part growth

6. Financial Risk - 9 eg., leverage, interest coverage

7. Firm Characteristics - 6 eg., where stock trades, type of business

8. Industry Dummies

31

Forecast Fundamental

Can we do better - Round 2 - Multi Index Models

iKiK2i21i1ii cI...bIbIbaR

iMiii eRR

Assume E 0IIII jjii

Indexes uncorrelated Mathematically we can always take a set of correlated indexes and convert them to a set of uncorrelated indexes (Appendix A)

Then if E 0)cc( ji

...2I2ib1Ii1

bi

aiR

2ci

...2I2

2i2

b2I1

2i1

b2i

....2I2j2

bi2

b2I1j1

bi1

bij

32

Average Correlation Models

If the single index model works better than the historic correlation matrix will other types of smoothing work better.

Overall mean outperformed Single Index Models. Differences were statistically significant and economically significant 2 to 5 percent per year.

Industry and pseudo industry mean models performed almost as well.

International evidence.