Embed Size (px)

Citation preview

© Areopa Trust Oct 2014

10 Steps to realising real cash value from Innovation and IC

Assets

Ludo Pyis Areopa

AREOPA provoking innovat ive intel l igence

Topics

The Fundamentals of Intellectual Capital and Intellectual Property

Quick Scan of IC approach to identify key risks The creation of new Intellectual Capital including IP The development of IPR and IC protection strategies. The Collection of Evidence , the Rules, the conditions for International Accountancy Standards 36 and 38 The use of Intellectual Capital to create new products

and services, new business models and new markets. Putting IC on the Balance Sheet

2 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Why do I need to take care of my IC ?

Today, know how is the key source of competitive advantage in the global market. Companies that manage knowledge, innovation and complexity are showing us the key to

future long term growth. Companies that understand that their business models have to change quickly over time

are winning the race.

This shift reversed the historical pattern where tangibles made up 80% of corporate value.

Today, the exact opposite is true. Tangibles make up just 18% of corporate value and the remaining 82% is intangible. “ If you don’t manage your intangibles you are not managing 82% of your organisation”

3 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

4 © Areopa Trust October 2015

What Is Intellectual Capital?

Intellectual Capital

Human Capital

Intellectual Assets

Value Creation - Tacit Value Extraction -Explicit

Intellectual Property

Intellectual Capital, knowledge that can be converted

into profits, has two components:

AREOPA provoking innovat ive intel l igence

Why is Intellectual Capital Management Different?

IC is 1. Context specific 2. Used to create multiple simultaneous value streams 3. Used in combinations with other assets (both tangible and

Intangible) to create new services and product mixes 4. Key part of strategy, innovation, performance, market

development, customer satisfaction, and relate to ensuring multiple simultaneous revenue from the same assets.

This is the real management challenge

5 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Why is IC Different?

Let us take an example The Company has a customer database. If this was a fixed asset e.g. (a piece of

furniture) you could only use it one way. However as an intangible asset that can be separated, protected, managed, and controlled it can be used in many ways to derive future value depending on the companies objectives.

1. It can be used to drive sales of products or services

2. It can be used to market the brand

3. It could be used to beta test new products from R&D

4. It could be packaged with a tangible asset and licensed to other complimentary businesses

5. It could be separated from the company and sold

Depending on the strategy of the organisation, the way that this asset is treated and is valued would be different. Therefore it is important to understand the purpose and context of the asset and to analyse it with that set of purposes and context in mind. The determination of whether such assets can be placed on the balance sheet is determined by whether it conforms to the rules of IAS

38. 6 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

4 Types of Intellectual Capital – Areopa Approach

Human Capital

Structural Capital

Customer Capital

Strategic Alliance Capital

7 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

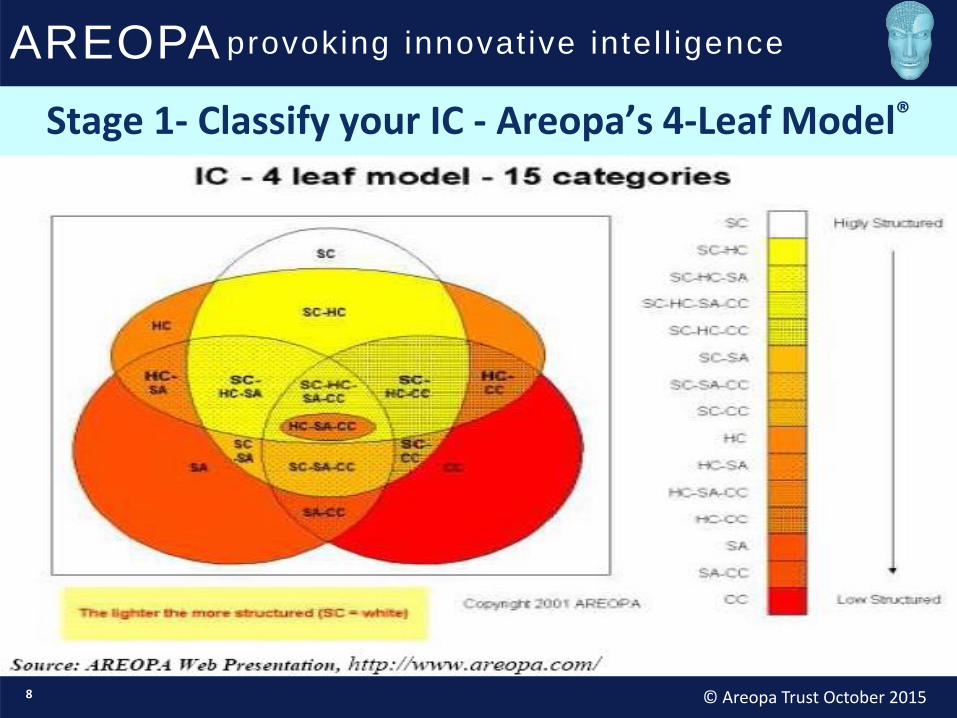

Stage 1- Classify your IC - Areopa’s 4-Leaf Model®

8 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Putting it together - Managing

For a business to manage its development and revenue creation it must

1. Attract the right people, partners and knowledge to the organisation

2. Safeguard and protect that knowledge

3. Put it to work inside a business model that connects with a market need

4. Develop the products and services that generate the revenues and profits in line with the market

5. Account for those revenues and assets in its accounts and on its balance sheet using the Areopa method

9 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

4 Steps to Realising the real Cash Value of your Intellectual Capital

10 © Areopa Trust October 2014

Account and Audit

•Prepare Areopa IC Accounting

System

•Audit using IAS 36 and 38

Deliver and Grow

•Control

•Manage

•Create and Combine to

Deliver additional Value

Protect

•Safeguard the

knowledge

•Ensure Ownership

•Protect

Prepare

•IC Quick Scan

•Build IC Inventory

•Create a

Management Plan

•Estimate Value

AREOPA provoking innovat ive intel l igence

Stage 1 :Identify your Intellectual Capital – Explicit Build the Inventory

Some examples 1. Training materials

2. Databases

3. Documented Systems

4. Models and tools

5. Trademarks

6. Research Papers

7. Patents

8. Standard Operating Procedures

9. Quality Standards

10. Documented Strategies

11. Market Information

11 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 1 – Identify your Intellectual Capital – Tacit- Build the Inventory

Some examples derived by semi structured questionnaire and interviews

1. Knowledge about your processes

2. Knowledge about your systems

3. Knowledge about your customers

4. Knowledge about your networks

5. Knowledge about partners

6. Knowledge about strategies and direction

7. Knowledge about your content and subject matter

8. Service and Product Information

9. Service and Product Delivery standards

12 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Evidence Collection Rules The data collection sheet and the inventory should contain a Full Description of asset what does the asset include key information from the document, artefact or discussion Describe objectives, roles how the relationship works targets markets type Age Info on separation Info on Safeguarding Info on Protection and ownership 13 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

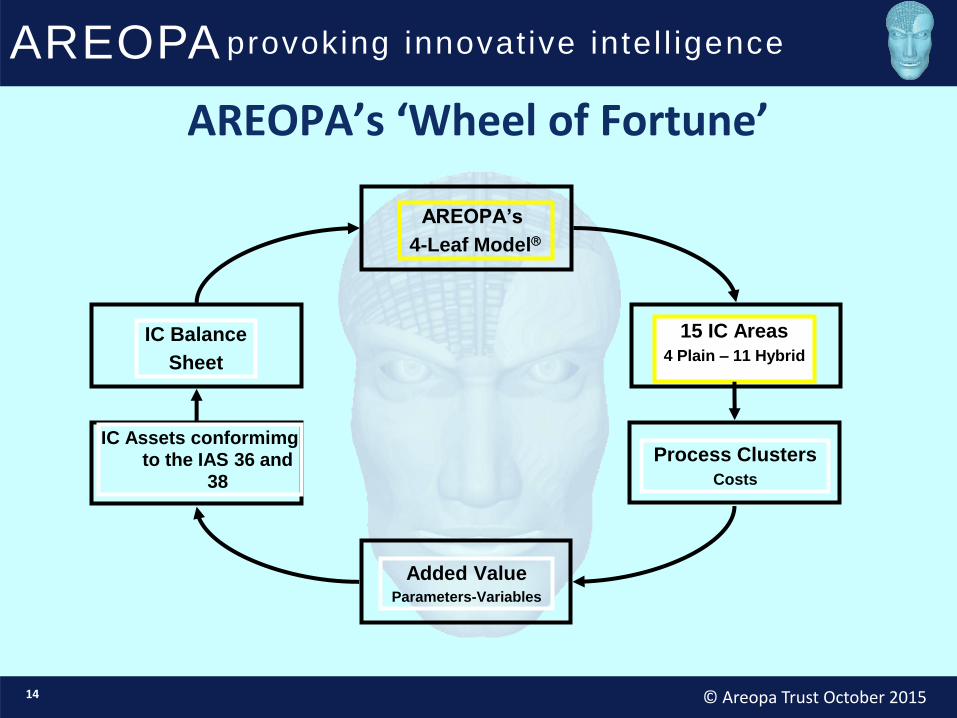

AREOPA’s ‘Wheel of Fortune’

14 © Areopa Trust October 2015

AREOPA’s

4-Leaf Model

Added Value Parameters-Variables

IC Balance

Sheet

IC Assets conformimg to the IAS 36 and

38

15 IC Areas

4 Plain – 11 Hybrid

Process Clusters

Costs

AREOPA provoking innovat ive intel l igence

Stage 2 - Estimate

Carry out an IC Estimation exercise where we will

Provide From Stage 1 an Inventory of Intellectual Capital Estimate the value of your present IC assets Estimate the value of your future IC assets Provide a route plan to cover all 10 stages of the Areopa

Method

15 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 3 – Safeguard

Begin to turn Tacit into Explicit Identify Key Knowledge Identify Key Knowledge Carriers Write down processes Collate and Manage Inventory of IC Assets Ensure that the company owns the IC either by

Acquistion

Contract

16 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 4 - Ownership

Who is the owner in the following ?

employer and employee relationship

independent contractor.

government employee.

joint-ownership.

Commissioned works

17 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 5: Protection

Why is IP important in IC

1. Protects the economic rights of creators

2. Enables the commercial exploitation of the IC by the owner

3.May attract capital expenditure

4.Enables the transfer of technology

5. Drives Future Value Streams 18 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence Intellectual Property

Universal Right

Copyright Industrial Rights

Trademarks

Patent

Industrial designs

Confidential information

Trade Secrets

Geographical Typical Indications

Plant Rights

AREOPA provoking innovat ive intel l igence

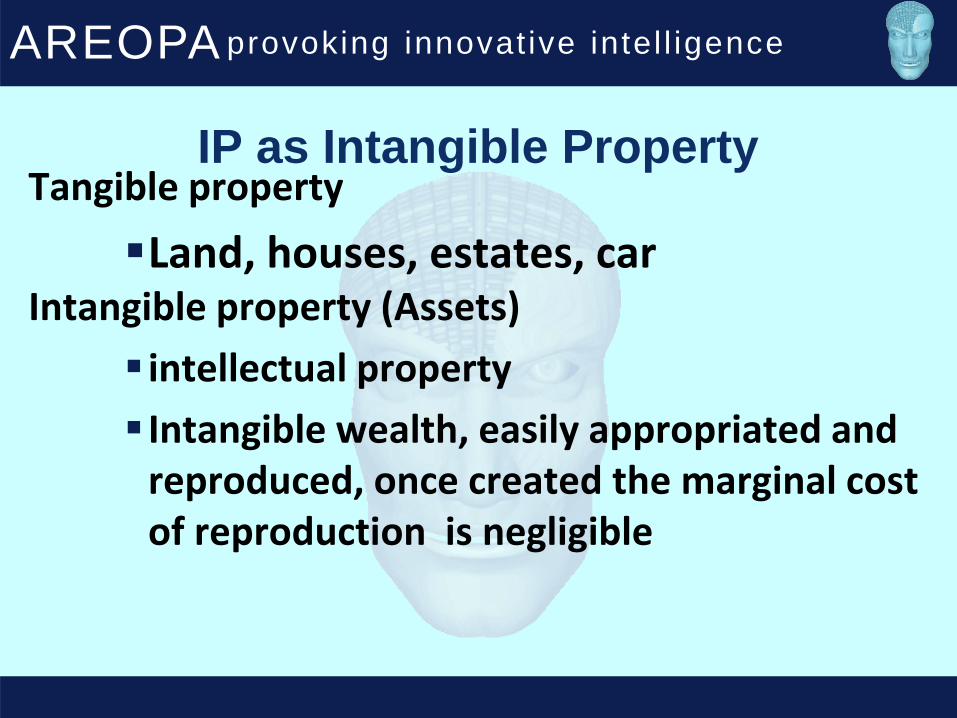

IP as Intangible Property

Tangible property

Land, houses, estates, car Intangible property (Assets)

intellectual property

Intangible wealth, easily appropriated and reproduced, once created the marginal cost of reproduction is negligible

AREOPA provoking innovat ive intel l igence

The role of IP within intangible property

1. Protects the economic rights of creators 2. Enables the commercial exploitation of owner of IC 3.May attract capital expenditure 4.Enables the transfer of technology

AREOPA provoking innovat ive intel l igence Why IP protection is sought by companies

Capital expenditure for new products R and D Marketing and advertisement No free loaders Maintaining loyal followers profit

AREOPA provoking innovat ive intel l igence

The Five Approaches for Measuring Intangibles (1/3)

1. Direct Intellectual Capital methods (DIC): Estimate the $-value of intangible assets by identifying its various components. Once these components are identified, they can be directly evaluated, either individually or as an aggregated coefficient.

2. Market Capitalization Methods (MCM): Calculate the difference between a company’s market capitalization and its stockholders’ equity as the value of its intellectual capital or intangible assets.

3. Return on Assets methods (ROA): Average pre-tax earnings of a company for a period of time are divided by the average tangible assets of the company. The result is a company ROA that is then compared with its industry average. The difference is multiplied by the company’s average tangible assets to calculate an average annual earnings from the intangibles. Dividing the above-average earnings by the company’s average cost of capital or an interest rate, one can derive an estimate of the value of its intangible assets or intellectual capital

23 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

The Five Approaches for Measuring Intangibles (2/3)

4. Scorecard Methods (SC): The various components of intangible assets or intellectual capital are indentified and indicators and indices are generated and reported in scorecards or as graphs.

24 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

The Five Approaches for Measuring Intangibles (3/3)

5. Areopa 10 stage integrated process Only Method Directly related to IFRS and IAS 38

Identify

Estimate

Ensure Ownership

Safeguard

Protect

Manage

Control

Derive Future Value

Calculate and PUT ON THE BALANCE SHEET

25 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

International Accounting Standards (IAS) IAS 38 Intangible Assets (1/3)

Key definitions

Intangible asset: an identifiable non-monetary asset without physical substance. An asset is a resource that is controlled by the entity as a result of past events (for example, purchase or self-creation) and from which future economic benefits (inflows of cash or other assets) are expected. [IAS 38.8]

Intangibles can be acquired:

by separate purchase

as part of a business combination

by a government grant

by exchange of assets

by self-creation (internal generation)

26 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

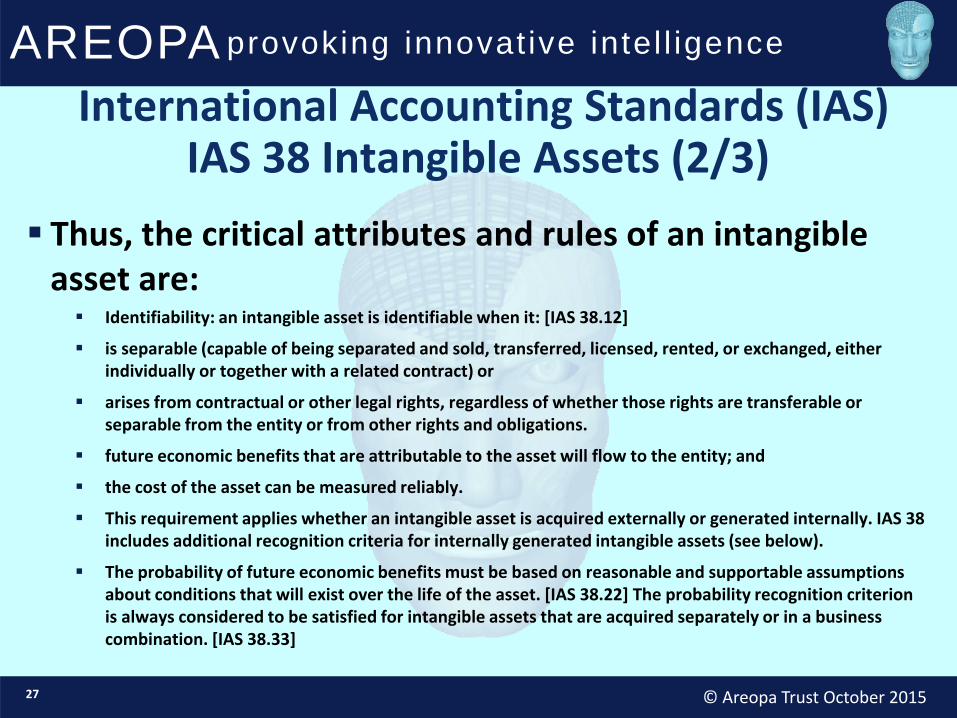

International Accounting Standards (IAS) IAS 38 Intangible Assets (2/3)

Thus, the critical attributes and rules of an intangible asset are:

Identifiability: an intangible asset is identifiable when it: [IAS 38.12]

is separable (capable of being separated and sold, transferred, licensed, rented, or exchanged, either individually or together with a related contract) or

arises from contractual or other legal rights, regardless of whether those rights are transferable or separable from the entity or from other rights and obligations.

future economic benefits that are attributable to the asset will flow to the entity; and

the cost of the asset can be measured reliably.

This requirement applies whether an intangible asset is acquired externally or generated internally. IAS 38 includes additional recognition criteria for internally generated intangible assets (see below).

The probability of future economic benefits must be based on reasonable and supportable assumptions about conditions that will exist over the life of the asset. [IAS 38.22] The probability recognition criterion is always considered to be satisfied for intangible assets that are acquired separately or in a business combination. [IAS 38.33]

27 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

International Accounting Standards (IAS) IAS 38 Intangible Assets (3/3)

Examples of intangible assets

patented technology, computer software, databases and trade secrets

trademarks, trade dress, newspaper mastheads, internet domains

video and audiovisual material (e.g. motion pictures, television programmes)

customer lists

mortgage servicing rights

licensing, royalty and standstill agreements

import quotas

franchise agreements

customer and supplier relationships (including customer lists)

marketing rights

28 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

IAS 38 Exceptions

IAS 38 applies to all intangible assets other than:

Financial assets (see Financial Instruments: Presentation)

Exploration and evaluation assets (see Exploration for and Evaluation of Mineral Resources)

Expenditure on the development and extraction of minerals, oil, natural gas, and similar resources

Intangible assets arising from insurance contracts issued by insurance companies

Intangible assets covered by another IFRS, such as intangibles held for sale (Non-current Assets Held for Sale and Discontinued Operations), deferred tax assets (Income Taxes), lease assets (Leases), assets arising from employee benefits (Employee Benefits (2011)), and goodwill (Business Combinations).

29 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

IAS 38 Valuation approaches

IAS 38 is not just a financial approach but an econometric approach.

Areopa has developed and trade secreted 77 econometric formulas that enable through the collection of evidence the identification of present and future value.

Econometrics are defined as Econometrics is an inter-disciplinary effort to understand

economic and financial behaviour through the use of data, economic theory, mathematics, statistical methods, and other quantitative and qualitative techniques in order to reach a valuation.

30 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 6: Managing Intellectual Capital

Some objectives of managing IC for companies

40% Increase in Revenue Generation

40% Increase in your assets on your balance sheet

25% Increase performance linked to strategic objectives

Greater Management of Risk

35% Greater Customer Satisfaction

10% Increase in customers and investors

To be clear about the Key assets of your company

To know the real value of your company when you decide to retire

31 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 6: ICM Toolbox

Business strategy and plan Technology audit IC and R&D processes Information mining Tactical decision making Valuation in context Brand strategy evaluation Data systems integration Coaching in communications

and managing the change

IC Tactics to meet plan Portfolio Management Identifying and packaging deal

elements Negotiating business deals Audit technology licenses Effective scenario planning Dynamic cash flow analysis Measurement of success of

ICM activity Value reporting to

stakeholders

32 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 7 : Control – some key questions

Who will Control the IC process in house How will IC help to deliver the companies products and

services How will it be exploited Who will decide which IC asset to protect, which to

trade, which to sell, which to invest in, which to combine and which approach should be taken for Exploitation

Who will manage IC risk Who will decide on IC costs How will IC revenue be monitored

33 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 8- Deriving Future Value

Intangibles differ from tangibles in many ways that “change the rules of the game”, (if not the game itself):

Value in context

Multiple simultaneous value streams

Understand how technologies will evolve

(Both your own and those on which you rely)

Understand how customer needs will evolve

Develop world class products and services that meet customer needs

34 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Stage 8: Deriving Future Value

Converting Ideas Into Cash

35 © Areopa Trust October 2015

Integrate

Out-license or Contract

Joint Venture

Strategic Alliance

Store

Store

€

Adequate IC Protection Available?

Specific Complementary Assets Required?

Complementary Assets Available?

No

No

No

No

No

Yes

Yes

Yes

Yes

Yes

Competitors Better Positioned in Marketplace?

Invention

Adapted from David Teece, 1986.

Meets Market Need

Use IC as source

of funding through

Securitisation

AREOPA provoking innovat ive intel l igence

Stage 8: Deriving Future Value

Strategic Investment is the Foundation of a Successful Commercialization Model

36 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

The look at the Fundamental Dilemma The main problem with measurement systems is that it is not possible to measure social

phenomena with anything close to scientific accuracy All measurement systems, including traditional accounting, have to rely on proxies, such

as dollars, euros, and indicators that are far removed from the actual event or action that caused the phenomenon

This creates a basic inconsistency between manager’s expectations, the promises made by the method developers and what the system can actually achieve and makes the systems very fragile and open to manipulation

SOLVE THIS BY HELPING YOU MEET THE INTERNATIONAL

ACCOUNTANCY STANDARDS 38 AND ENABLE YOU TO INCREASE BOTH YOUR REVENUES AND YOUR BALANCE SHEET BY USING AN

ECONOMETRICS APPROACH

37 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

(Financial) Balance Sheet

38 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

Intellectual Capital Balance Sheet

39 © Areopa Trust October 2015

•Assets are either Internal or External and vary from highly structured to not

structured at all

•Assets are owned by the company (explicit) by contract or as described in IAS 38

•Assets not owned by the company or borrowed from 3rd parties: staff, customers,

alliances, partners, public authorities may be considered liabilities or risks.

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

IC balance sheet: follows the structure logic of the financial BS

40 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

Consolidated Balance Sheet

41 © Areopa Trust October 2015

• Consolidated Balance Sheet shows the total value of the enterprise, combining financial with

IC elements

• The assets side gives a clear insight into the relative values of ALL assets, offering THE

ultimate management tool to managers

• The liabilities side shows how assets are ‘financed’, i.e. ‘who owns’ the assets

• Balance Sheet analytics can be developed in line with BS analysis concepts which already

exist for the ‘classical’ BS

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

The fundamentals of accounting

42 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

43 Thursday, November 24, 2016

IC Accounting: the same principles apply

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Future Value In addition to the Book Value of IC Assets we need to add

A second portion which expresses the Future Potential (FP) of the IC Asset on hand.

This FP will be calculated based on the 77 added value calculation formula’s of the AREOPA 4 leaf model .

If we use the basic resources ( see BV ) in the business processes they will have to create “ added value“. This added value is calculated by useing the 77 formula’s

44 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

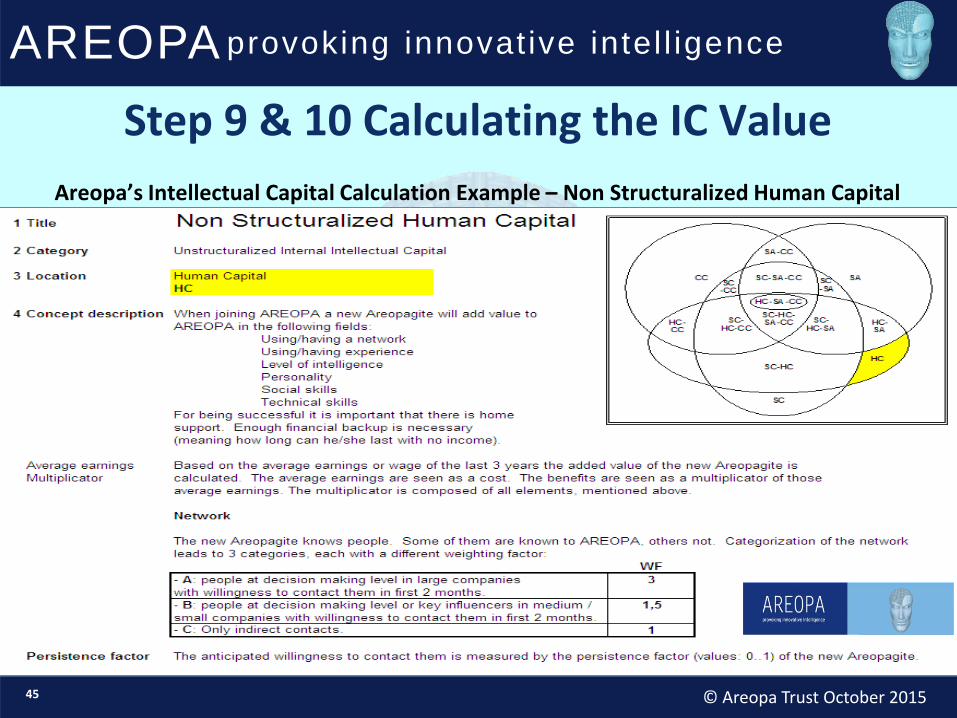

Step 9 & 10 Calculating the IC Value

Areopa’s Intellectual Capital Calculation Example – Non Structuralized Human Capital

45 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Value

46 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

Step 9 & 10 Calculating the IC Total Value Bringing the 2 elements (Book Value (BV)

and Future Potential (FP)) together allows us to complete the Total Value Equation of an IC Asset:

whereby: and:

Each of these composing elements will have to be

assessed,

defined and

computed

while putting together the initial inventory of the IC assets of an organisation. In preparation of the calculation of the IC value of all or a set of assets at preset intervals (monthly, quarterly, yearly) or the start of a continuous IC accounting exercise. The most difficult part lies in the calculation of the future potential of each of the IC Assets. These potential margin contributions will depend on the nature of each asset and The parameters and variables “driving” the value creating potential of each individual asset.

47 © Areopa Trust October 2015

TVIC = BVIC + FPIC

BVIC = (ACIC + ECIC) )- DIC + (VIIC - VDIC)

The formula’s which calculate the

added value of the 77 phenomena’s

AREOPA provoking innovat ive intel l igence

Additional thoughts

Areopa’s Positioning on Karl-Erik Sveiby’s Overview

48 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

The box we have … the fillings need to be gathered

49 © Areopa Trust October 2015

AREOPA provoking innovat ive intel l igence

50 © Areopa Trust October 2015

Thank You

If you have any questions or you would like to discuss with us further

Please Contact

![5 Steps to Measure Lead-to-Cash Performance [Webinar]](https://img.pdfslide.net/doc/110x75/555857f3d8b42a993b8b4e07/5-steps-to-measure-lead-to-cash-performance-webinar.jpg)