Embed Size (px)

Citation preview

For Financial Professionals Only – Not For Use With the Public

1035 Exchange

Connie Dello BuonoCA Life Lic 0G60621 [email protected] 408-854-1883

[Agent Name] is a Registered Representative of, and securities are offered solely by Equity Services, Inc., Member FINRA/SIPC, [branch office address and telephone number]. [DBA name] is independent of Equity Services, Inc. Registered Broker/Dealer affiliate of National Life Insurance Company, Montpelier,

Vermont [DBA name] is independent of Equity Services, Inc. National Life Group® is a trade name of National Life Insurance Company, Montpelier, VT, and its affiliates.

TC68124(0512)

For Financial Professionals Only – Not For Use With the Public

This information is not intended as tax or legal advice. Please consult with your Attorney or Accountant prior to acting upon any of the information contained herein.

We have no obligation (express or implied) to update any of the contents herein or advise you of any changes ; nor do we make any express or implied warranties or representations as to the completeness or accuracy or accept responsibility for errors. The information contained herein has been prepared solely for educational purposes and is not a solicitation for any product or financial instrument.

For Financial Professionals Only – Not For Use With the Public

What is a “1035 Exchange”

• Governed by IRC Sec. 1035

• Nontaxable exchange of life insurance, annuity, (and now) long-term care contracts

• Defer recognition of gain

For Financial Professionals Only – Not For Use With the Public

What is a “1035 Exchange”

• Governed Sec. 1035• Nontaxable exchange of one life insurance or annuity

contract for another

• Defer Recognition of Gains

For Financial Professionals Only – Not For Use With the Public

1035 Exchange

Reasons to Replace Existing Coverage

(Must be in Client’s best interest)

For Financial Professionals Only – Not For Use With the Public

1035 Exchange

Reasons to Keep Existing Coverage

For Financial Professionals Only – Not For Use With the Public

1035 Exchange Rules & Requirements

Life insurance contract for:

• Another life insurance contract

• An Annuity contract

• A long-term care contract

For Financial Professionals Only – Not For Use With the Public

1035 Exchange Rules & Requirements

Endowment contract for:

– An annuity

– A long-term care contract

Endowment contracts are no longer issued

For Financial Professionals Only – Not For Use With the Public

1035 Exchange Rules & Requirements

Annuity contract for

• Another annuity contract

• A long-term care contract

For Financial Professionals Only – Not For Use With the Public

1035 Exchange Rules & Requirements

• VUL vs. UL vs. WL

• Term Conversions

For Financial Professionals Only – Not For Use With the Public

Life for Life

• Same person must be insured for both

– Annuity for Annuity

• Contracts must have the same obligee/owner

1035 Exchange Rules & Requirements

For Financial Professionals Only – Not For Use With the Public

Life for Life

• Ownership may change (before or after exchange)

1035 Exchange Rules & Requirements

For Financial Professionals Only – Not For Use With the Public

1035 Exchange Rules & Requirements

• Single Life to Survivorship

• Survivorship to Single Life

• Survivorship to Annuity

• Single Life to Joint and Survivor Annuity

For Financial Professionals Only – Not For Use With the Public

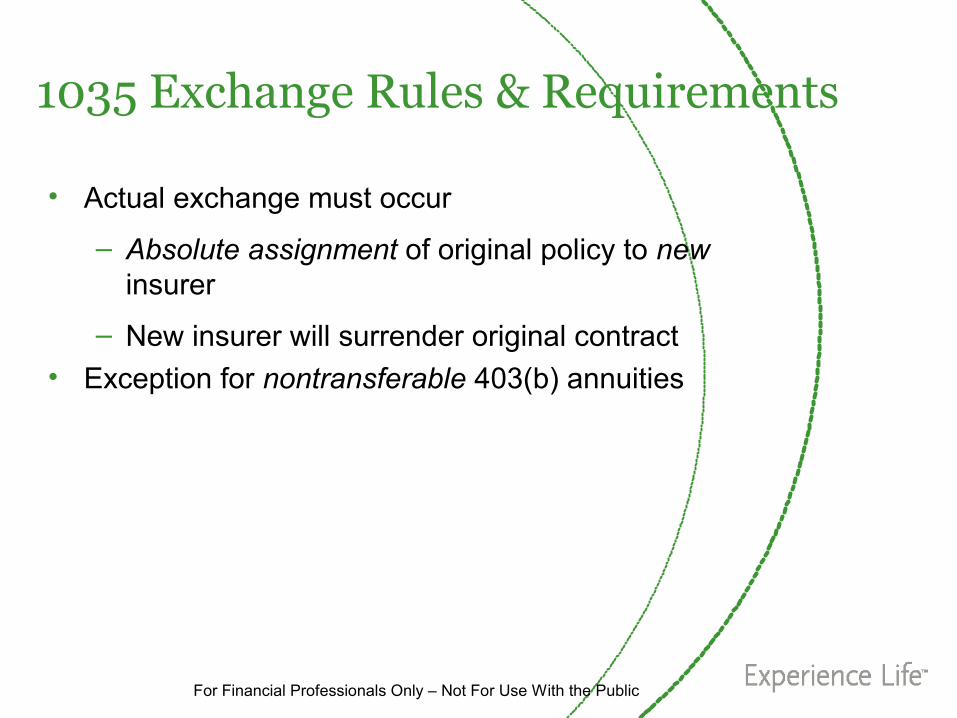

1035 Exchange Rules & Requirements

• Actual exchange must occur

– Absolute assignment of original policy to new insurer

– New insurer will surrender original contract

• Exception for nontransferable 403(b) annuities

For Financial Professionals Only – Not For Use With the Public

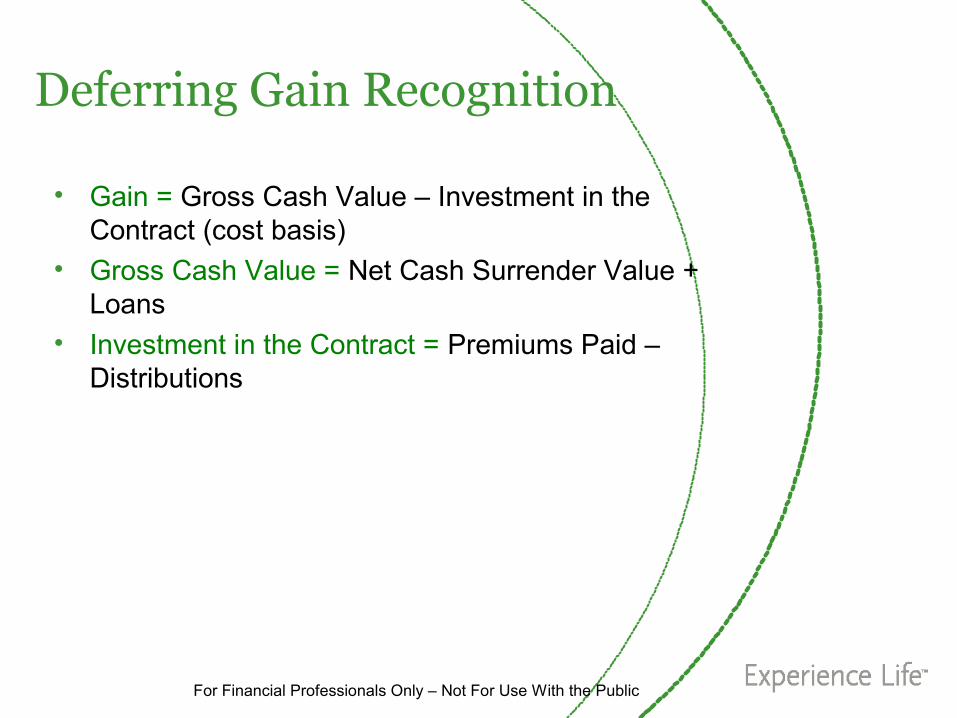

Deferring Gain Recognition

• Gain = Gross Cash Value – Investment in the Contract (cost basis)

• Gross Cash Value = Net Cash Surrender Value + Loans

• Investment in the Contract = Premiums Paid – Distributions

For Financial Professionals Only – Not For Use With the Public

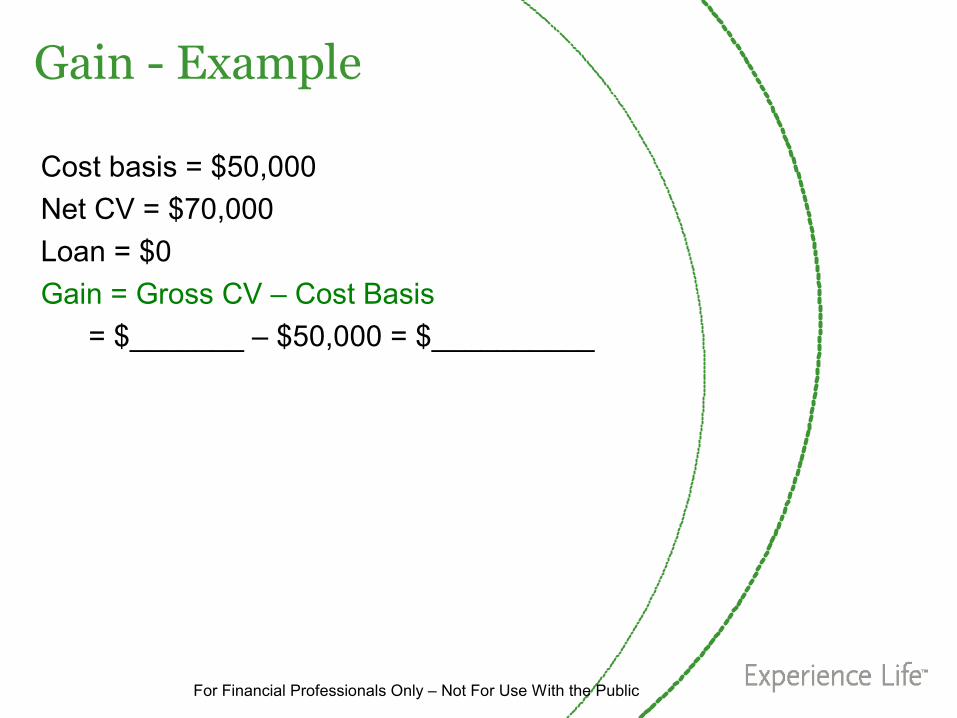

Gain - Example

Cost basis = $50,000

Net CV = $70,000

Loan = $0

Gain = Gross CV – Cost Basis

= $_______ – $50,000 = $__________

For Financial Professionals Only – Not For Use With the Public

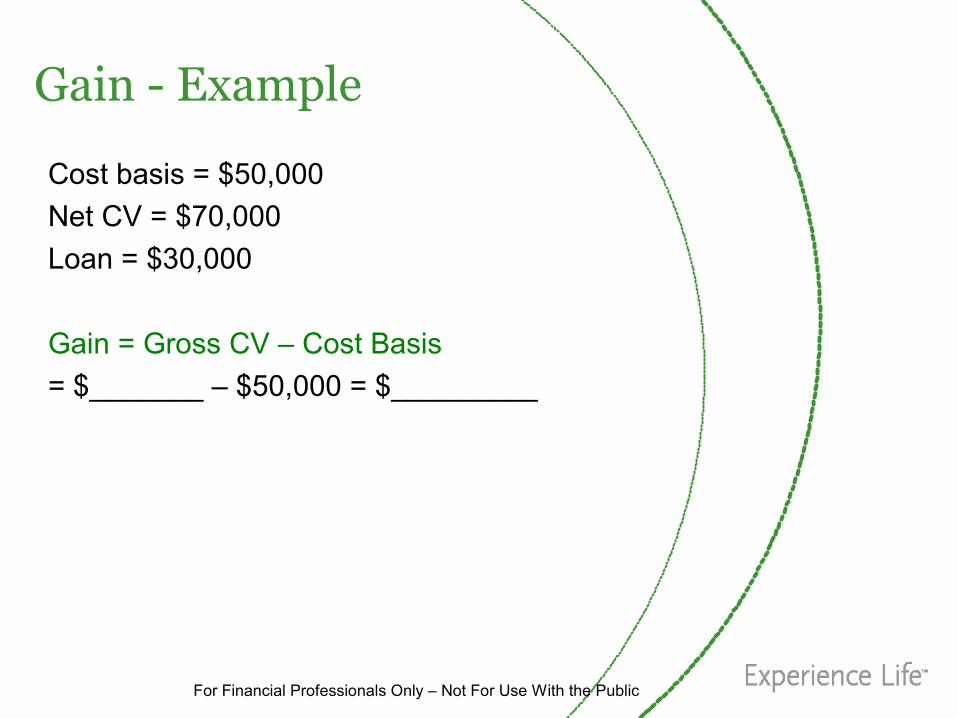

Gain - Example

Cost basis = $50,000

Net CV = $70,000

Loan = $30,000

Gain = Gross CV – Cost Basis

= $_______ – $50,000 = $_________

For Financial Professionals Only – Not For Use With the Public

Gain

• Gain equals gross cash value minus basis• May be taxable income when distributed

For Financial Professionals Only – Not For Use With the Public

“BOOT”

• If the contract owner receives, in addition to a qualifying contract, cash or other property “to boot” gain will be recognized on the exchange to the extent of the value of the other property

For Financial Professionals Only – Not For Use With the Public

Gain Recognized in 1035 Exchange

• Policy loans plus accrued interest recognized as taxable income to the extent of a gain in the contract

• …Unless loan is carried over to the new contract

For Financial Professionals Only – Not For Use With the Public

First Questions to Ask

1. Is there gain in the contract?

2. Is there a loan on the contract?

For Financial Professionals Only – Not For Use With the Public

Losses

•Loss on surrender of life contract is not deductible•Loss on surrender of annuity may be deductible•Loss can be “preserved” through 1035 – carry basis over

For Financial Professionals Only – Not For Use With the Public

Tax Reporting

•Insurance carrier whose contract is replaced must report– Taxable gain– Carryover basis

•Form 1099-R is used•Policy owner must report gains even if carrier does not

For Financial Professionals Only – Not For Use With the Public

Miscellaneous1035 Exchange Issues

• Deferred annuities retain tax character• Carryover loans• Multiple policies• Qualified retirement plans

For Financial Professionals Only – Not For Use With the Public

Miscellaneous1035 Exchange Issues

• Deferred annuities retain tax character

• Carryover loans

• Multiple policies

• Qualified retirement plans

For Financial Professionals Only – Not For Use With the Public

Miscellaneous1035 Exchange Issues

• Deferred annuities retain tax character

• Carryover loans

• Multiple policies

• Qualified retirement plans

For Financial Professionals Only – Not For Use With the Public

• Troubled insurers & serial payments• Modified Endowment Contracts

(MECs)

• Collateral Assignments

Miscellaneous1035 Exchange Issues

For Financial Professionals Only – Not For Use With the Public

Miscellaneous1035 Exchange Issues

• Troubled insurers & serial payments• Modified Endowment Contracts

(MECs)

• Collateral Assignments

For Financial Professionals Only – Not For Use With the Public

Miscellaneous1035 Exchange Issues

• Troubled insurers & serial payments

• Modified Endowment Contracts(MECs)

• Collateral Assignments

For Financial Professionals Only – Not For Use With the Public

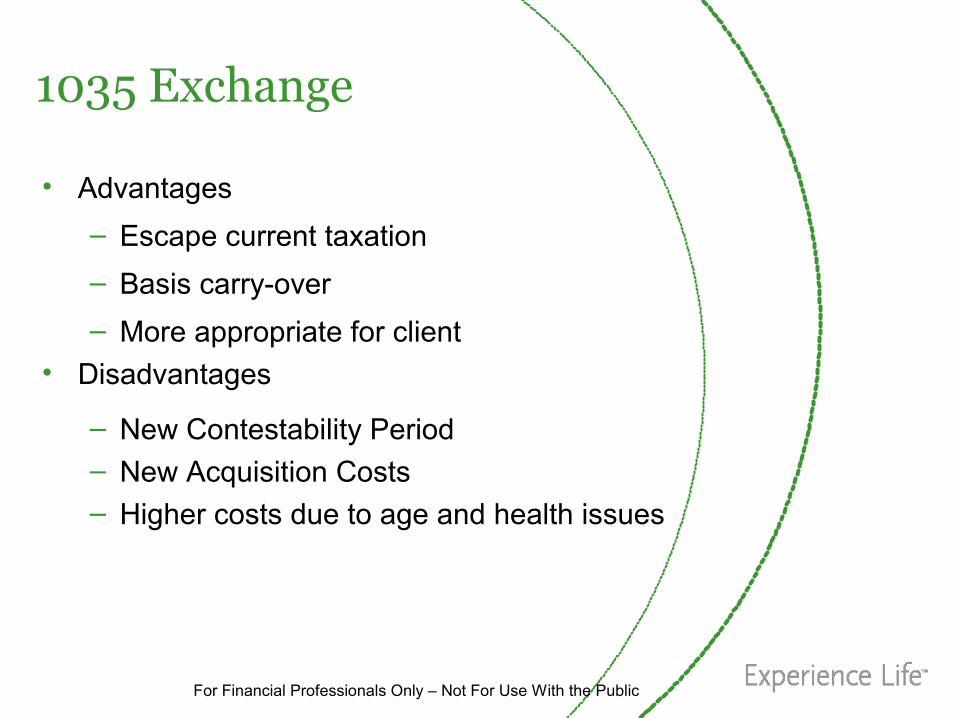

1035 Exchange

• Advantages

– Escape current taxation

– Basis carry-over

– More appropriate for client• Disadvantages

– New Contestability Period – New Acquisition Costs – Higher costs due to age and health issues

For Financial Professionals Only – Not For Use With the Public

Alternatives to 1035 Exchange

• Maintain existing policy

• Elect nonforfeiture option

For Financial Professionals Only – Not For Use With the Public

Alternatives to 1035 Exchanges

• Maintain existing policy• Elect nonforfeiture option

1) Extended Term Insurance2) Reduced paid up insurance3) cash distributions

For Financial Professionals Only – Not For Use With the Public

Questions and Answers

For Financial Professionals Only – Not For Use With the Public

Thank You