Embed Size (px)

Citation preview

11

Bank of Zambia

THE EMERGENCE OF THE GLOBAL ECONOMIC CRISIS AND ITS IMPACT TO SOCIAL ECONOMIC DEVELOPMENT OF ZAMBIA

BY

CALEB M. FUNDANGA

Governor

BANK OF ZAMBIA

Paper Presented at the ZCTU Top Leadership Workshop

3rd March, 2009

1.0 INTRODUCTION

This paper discusses the origins of the global financial and economic crisis

USA crisis and the rest of the global economy. The social and economic impact on Zambia Prospects for the Zambia in 2009 and beyond Role of the trade union movement and its

leadership Conclusion

Bank of Zambia

2

2.0 Origins of the Global Financial Crisis

• Causes of the Sub-Prime Crisis:Poor underwriting standards for mortgage loans;

Weak regulation and supervision of banks; and

Exposure to the sub-prime security backed financial assets.

• Signs of Problem:Inability to service debt when interest rates rose.

High loan defaults, foreclosures, and decline in demand for homes.

Bank of Zambia

3

3.0 USA Crisis and the Rest of the Global Economy.

• Implications on World Economies:

Banking system short of liquidity (Credit Crunch);

Business scale down or closure of operations ; and

Slow down in economic growth.

Bank of Zambia

4

3.0 USA Crisis and the Rest of the Global Economy (cont’d)

• US Response to the crisis:

Stimulus measures including:

Fiscal, interest rate and exchange rate adjustments;

Initially US $700 billion to unblock credit for the financial system

Further US $787 billion to boost economy under the new US President, Obama.

Bank of Zambia

5

3.0 USA Crisis and the Rest of the

Global Economy (cont’d)

• UK response to the crisis:

Temporary tax cuts (reduction in VAT, 17.5% to 15.0%).

• Euro response to the crisis:

• China response to the crisis:

Stimulus package of US $586 billion to boost demand; and

“Moderately easy” monetary policy.

Bank of Zambia

6

4.0 Social and Economic Impact

Growth

• Effect on the Zambian Economy:

Withdrawals by foreign portfolio investors; Weakening Kwacha exchange rate;Lower commodity prices; Reduced economic activity;Increased unemployment; andLow GDP.

Bank of Zambia

7

4.0 Social and Economic Impact (cont’d)

• Prolonged recession may:

Deepen risk aversion and discourage both portfolio and FDI flows;

Reduce Zambia’s export earnings;

Increase inflation;

Rise in interest rates; and

Reduced GDP growth.

Bank of Zambia

8

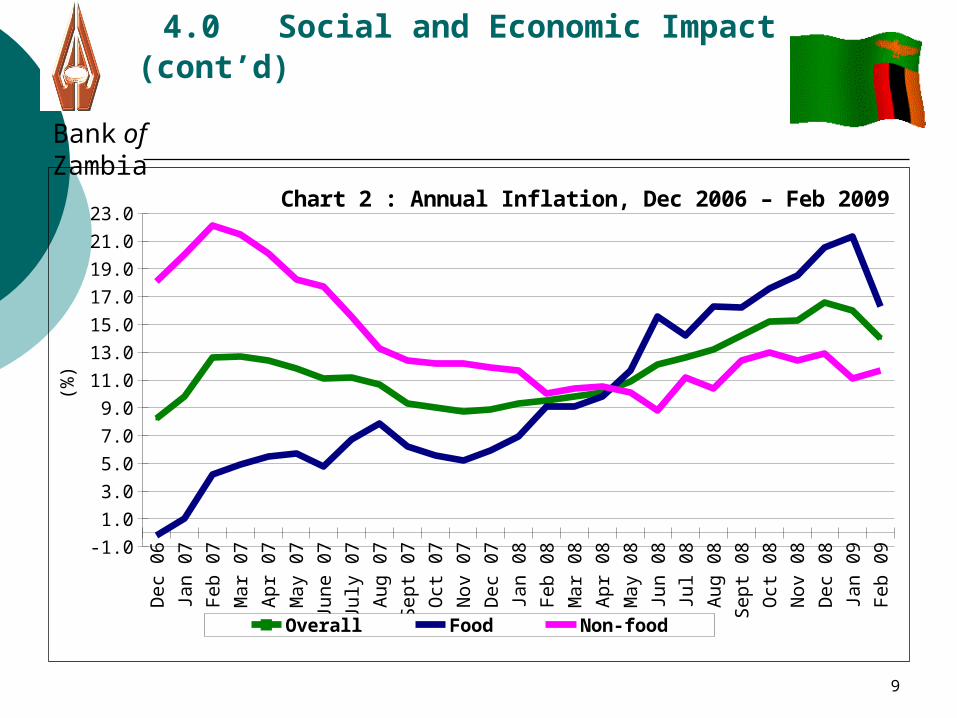

4.0 Social and Economic Impact (cont’d)

Bank of Zambia

De

c 0

6

Jan

07

Fe

b 0

7

Ma

r 0

7

Ap

r 0

7

Ma

y 0

7

Jun

e 0

7

July

07

Au

g 0

7

Se

pt 0

7

Oct

07

No

v 0

7

De

c 0

7

Jan

08

Fe

b 0

8

Ma

r 0

8

Ap

r 0

8

Ma

y 0

8

Jun

08

Jul 0

8

Au

g 0

8

Se

pt 0

8

Oct

08

No

v 0

8

De

c 0

8

Jan

09

Fe

b 0

9-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0Chart 2 : Annual Inflation, Dec 2006 – Feb 2009

Overall Food Non-food

(%)

9

4.0 Social and Economic Impact (cont’d)

Revenue Earnings from Mineral Resources

• Copper prices fell, hence reduced earnings;

• Reduced tax revenue;

• Reduced Government capacity to develop infrastructure; and

• Constrain economic growth.

Bank of Zambia

10

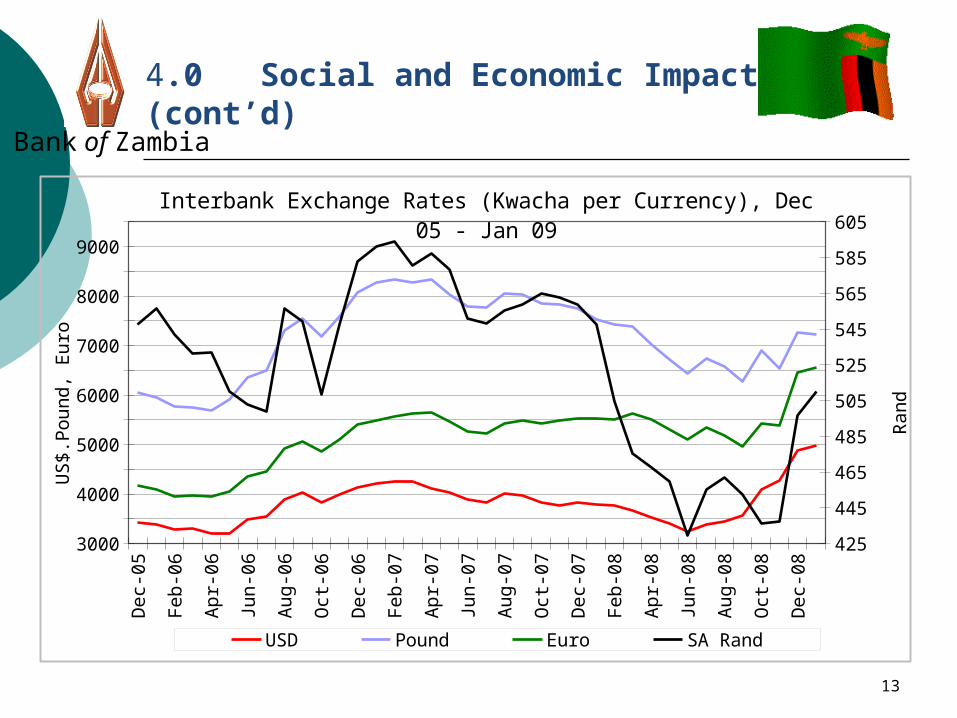

4.0 Social and Economic Impact (cont’d)

Bank of Zambia

Copper Prices in US dollars per Tonne, Jan 2007 - Dec 2008

Jan

2007 M

arMay Ju

lSe

pNov

Jan

08 Mar

May Ju

lSe

pNov

1000.02000.03000.04000.05000.06000.07000.08000.09000.0

10000.0

11

4.0 Social and Economic Impact (cont’d)

• Exchange Rate Volatility

• High volatility and weakening of Kwacha due to:

Political uncertainty; Global financial crisis; and Fall in copper prices.

• Kwacha depreciated against most major foreign currencies.

• BoZ continues to participate in foreign exchange market.

Bank of Zambia

12

4.0 Social and Economic Impact (cont’d)Bank of Zambia

De

c-0

5

Fe

b-0

6

Ap

r-0

6

Jun

-06

Au

g-0

6

Oct

-06

De

c-0

6

Fe

b-0

7

Ap

r-0

7

Jun

-07

Au

g-0

7

Oct

-07

De

c-0

7

Fe

b-0

8

Ap

r-0

8

Jun

-08

Au

g-0

8

Oct

-08

De

c-0

8

30003500400045005000550060006500700075008000850090009500

425

445

465

485

505

525

545

565

585

605Interbank Exchange Rates (Kwacha per Currency), Dec 05 - Jan 09

USD Pound Euro SA Rand

US

$.P

ou

nd

, Eu

ro

Ra

nd

13

4.0 Social and Economic Impact (cont’d)

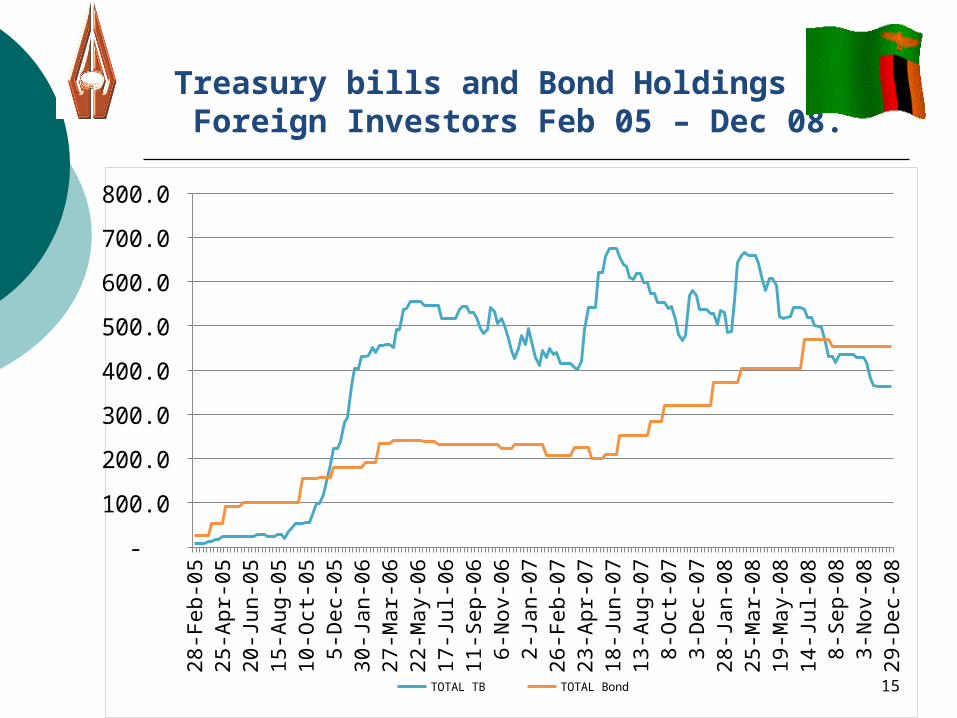

• Foreign Capital Flows

• FDI fell to US $938.6 million in 2008 from US $1,323.9 million in 2007.

• Foreign Portfolio Investment showed outflow of US $6.1 million in 2008 from inflow of US $41.8 million in 2007.

Bank of Zambia

14

Treasury bills and Bond Holdings by Foreign Investors Feb 05 – Dec 08.

28-F

eb-0

5

28-A

pr-0

5

28-J

un-0

5

28-A

ug-0

5

28-O

ct-0

5

28-D

ec-0

5

28-F

eb-0

6

28-A

pr-0

6

28-J

un-0

6

28-A

ug-0

6

28-O

ct-0

6

28-D

ec-0

6

28-F

eb-0

7

28-A

pr-0

7

28-J

un-0

7

28-A

ug-0

7

28-O

ct-0

7

28-D

ec-0

7

28-F

eb-0

8

28-A

pr-0

8

28-J

un-0

8

28-A

ug-0

8

28-O

ct-0

8

28-D

ec-0

8

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

TOTAL TB TOTAL Bond 15

5.0 Prospects for 2009 and Beyond.

Positive growth in real GDP expected but to slowdown.

Mainly :

mining output to decline;

tourism (especially foreign tourists);

Mining-related manufacturing & services (e.g. contracts) to be lower; and

Agriculture expected to recover.

16

5.0 Prospects for 2009 and Beyond (cont’d)

Given current challenges:

o 2009 National Budget aims at: o encouraging diversification (export

base);

o enhancing competitiveness;

o increasing local value-addition; and

o increasing expenditure on infrastructure and social services.

17

5.0 Prospects for 2009 and Beyond (cont’d)

Bank of Zambia will continue to monitor global developments;

And take appropriate measures to maintain confidence in the banking system and avoid systemic risk.

Maintenance of the macroeconomic stability gains achieved.

18

5.0 Prospects for 2009 and Beyond (cont’d)

Investment confidence in the Zambian economy continues. For instance:

New commercial banks (Access, Ecobank, FNB and International Commercial Bank);

Construction of the Chambishi MFEZ;

Konkola Deep Mine at advanced stage (sinking the shaft).

Zesco power rehabilitation programme.

Preparatory work on extension and construction of Kariba North Bank and Itezhi Tezhi Hydro power stations.

19

6.0 Role of the Trade Union

• Maintenance of industrial harmony;

• Support Government and Investor initiatives;

• Enhance education of union members; and

• Encourage labour efficiency and improving productivity and communication amongst members.

• Changing workers’ attitude for the better.

20

• Challenges from global financial crisis are huge but surmountable;

• Major economies are taking stimulus and mitigating measures;

• To benefit, we need to remain committed to strong socio-economic policies.

• We are all part of the solution.

7.0 Conclusion Bank of Zambia

21

Thank You

Bank of Zambia

22