Embed Size (px)

Citation preview

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 1/34

Interest Rates and Self-Sufficiency

LESSON 1

THE ROLE OF INTEREST RATES

Interest is the amount paid by a borrower to a lender in exchangefor the use of the lender's money for a certain period of time.

Money is a scarce resource. There is a limited amount of it, and it has value for everyone.Interest represents the cost of money — what a borrower pays in order to rent money for acertain period of time. Interest rates help determine the allocation of money because, aswith other goods in the economy, the demand for money is influenced by its cost.

Interest does more than determine the allocation of money; it provides income to lenders.

Interest is a cost paid by borrowers that enables lenders to provide an efficient lendingservice and to generate a reasonable profit. For microenterprise credit institutions,interest income determines whether the institution is dependent on donor funds or able tomaintain itself with its own earned income.

For entrepreneurs who borrow, interest rates provide a "hurdle rate" over whichinvestments must pass to be a valid use of scarce resources. If it costs an entrepreneur 9percent to borrow $1,000 for a year, then the investment must earn more than $1,090 tobe potentially worthwhile. Investments that earn 9 percent or less are inefficient uses ofscarce financial resources.

In short, interest rates on loans are critical to borrowers, lenders, and the economy as awhole. The establishment of appropriate interest rates is crucial for the effectiveoperation and financial management of microenterprise finance institutions.

Interest Rates from Two Perspectives

A. The Borr ower' s Perspect ive

Financial Costs are the interest and fees that borrowers pay tolenders in order to use the money for a specific period of time.

Transaction costs are indirect costs incurred to obtain loans.

Because transaction costs do not benefit either the lender or theborrower, lenders should minimize them to the greatest extentpossible.

When a borrower approaches a lender for a loan, he is confronted with two different typesof costs. The most obvious cost is the actual cost of the money, including the interest tobe paid for the use of the loan, and the fees paid to the lender for processing and

disbursing the loan. These costs are the financial costs of the loan.

ACCION 1

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 2/34

Interest rates and self sufficiency

The borrower must also pay transaction costs. Transaction costs are indirect costs incurredto obtain loans. They include bus fares to the lender's place of business, the cost ofobtaining documents (like financial statements) required for the loan, the cost of the timespent by the borrower fulfilling the requirements for the loan, and any other costs relatedto acquiring the loan. Transaction costs also include costs due to inefficiencies in lender

delivery systems, such as missed investment opportunities because of delays in loandisbursement; the extra time spent processing a loan because the lending institutionmisplaces a document, and others. Transaction costs are often greater than the financialcosts if lenders are inefficient in their loan approval or disbursal process.

Financial and transaction costs represent the total borrowing costs of a loan. Becausetransaction costs do not benefit either the lender or the borrower, lenders should minimizethem to the greatest extent possible. Financial costs, on the other hand, provide incometo the lender in the form of interest and fees. Lenders that minimize transaction costsmake it easier for their borrowers to afford higher financial costs. Financial costs should beestablished carefully by the lending institution in order to generate the income that theinstitution needs for survival and growth.

Given a fixed level of transaction costs, what level of financial costs can microentrepreneurs afford to pay? How much in interest and fees can micro entrepreneurs payand still benefit from borrowing money? These are controversial questions, and the sourceof continual debate in the micro enterprise credit field. The response depends on theprofitability of the enterprises in question.

A financial analysis of microenterprises will usually show the activities to be quiteprofitable, enabling the entrepreneurs to pay financial costs equivalent to or higher than"commercial" rates1 and still benefit from the loans. In some cases, however, when thelevel of profitability is extremely low, financial costs near commercial levels may

represent an unbearable burden for certain activities. In such cases, loans may be aninappropriate intervention, and alternative mechanisms to promote economic developmentshould be investigated.

B. The Lender's Perspective

There are three basic costs that lending institutions must cover with their income: thefinancial cost of the funds in their portfolio, known as the cost of funds, the cost ofmaintaining a loan loss reserve so that the portfolio does not decapitalize when loans aredefaulted, and other operating costs that include the salaries of staff, rent, and otheroperating expenses.

To be self-sufficient, a financial institution must cover the above costs with incomegenerated by financial services. For microenterprise credit institutions, interest charged onloans and fees associated with lending are the primary sources of earned income. The loanportfolio (funds lent to borrowers and funds on deposit available to be lent) produces agross rate of return, or yield, which is the interest and fee income divided by the averageportfolio. Self-sufficient lending institutions have a rate of return high enough to cover allof their costs, and keep the value of their funds from deteriorating because of the effectsof inflation.

1 Commercial rates refer to the interest rates charged by commercial banks for small enterprise of similarloans.

ACCION 2

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 3/34

Interest rates and self sufficiency

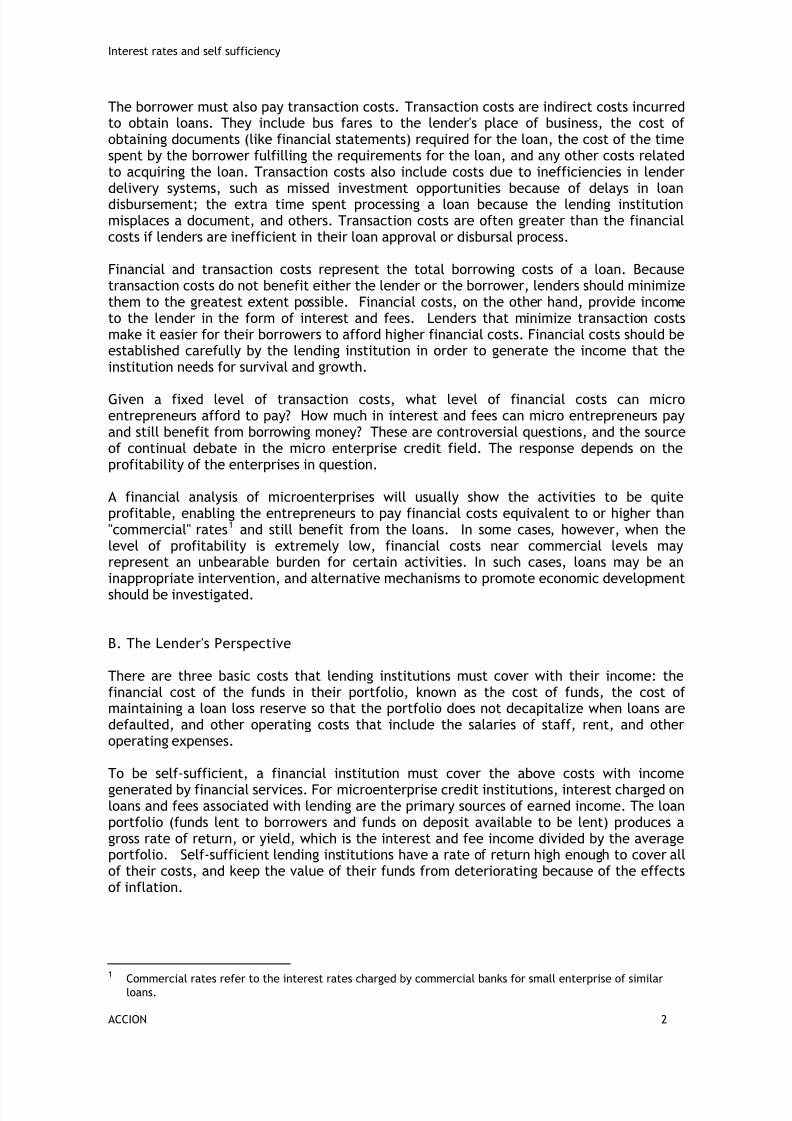

The diagram below shows the flow of cash for borrowers and lenders during a loantransaction. What the borrower pays in financial costs becomes the lender's income, whichis used to pay for expenses. What the borrower pays in transaction costs is lost to both theborrower and the lender. The loan principal goes back and forth between the borrower andthe lender.

Figure 1

CASH FLOW OF LENDING TRANSACTIONS

Loan

PrincipalBORROWERS LENDER

FINANCIAL COSTS:

• Interest

• Fees INCOME

Transactioncosts

Cost of fundsLoan loss reserveOperational costs

ACCION 3

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 4/34

Interest Rates and Self-Sufficiency

LESSON 2

NOMINAL, EFFECTIVE AND REAL INTEREST RATES

Understanding interest rates for microenterprise lending requires knowledge of a fewfinancial terms, concepts, and formulas. This lesson discusses basic types of interest ratesand their methods of calculation.

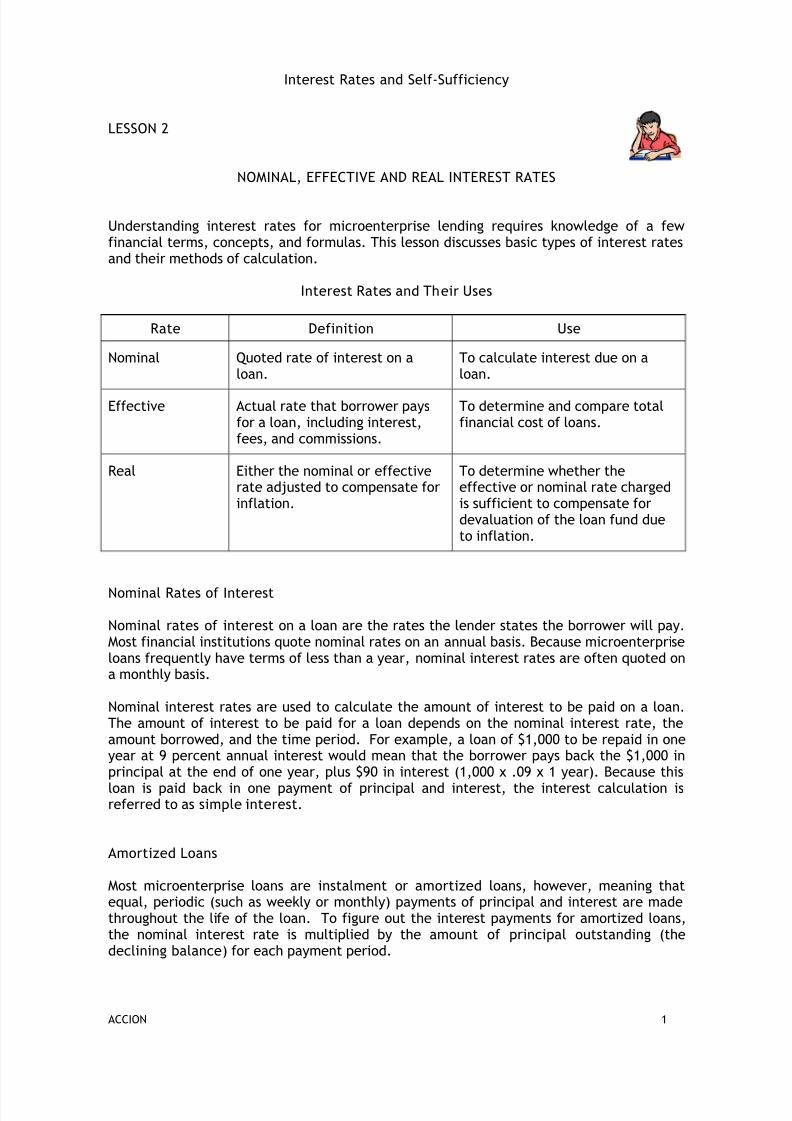

Interest Rates and Their Uses

Rate Definition Use

Nominal Quoted rate of interest on a

loan.

To calculate interest due on a

loan.

Effective Actual rate that borrower paysfor a loan, including interest,fees, and commissions.

To determine and compare totalfinancial cost of loans.

Real Either the nominal or effectiverate adjusted to compensate forinflation.

To determine whether theeffective or nominal rate chargedis sufficient to compensate fordevaluation of the loan fund dueto inflation.

Nominal Rates of Interest

Nominal rates of interest on a loan are the rates the lender states the borrower will pay.Most financial institutions quote nominal rates on an annual basis. Because microenterpriseloans frequently have terms of less than a year, nominal interest rates are often quoted ona monthly basis.

Nominal interest rates are used to calculate the amount of interest to be paid on a loan.The amount of interest to be paid for a loan depends on the nominal interest rate, theamount borrowed, and the time period. For example, a loan of $1,000 to be repaid in one

year at 9 percent annual interest would mean that the borrower pays back the $1,000 inprincipal at the end of one year, plus $90 in interest (1,000 x .09 x 1 year). Because thisloan is paid back in one payment of principal and interest, the interest calculation isreferred to as simple interest.

Amortized Loans

Most microenterprise loans are instalment or amortized loans, however, meaning thatequal, periodic (such as weekly or monthly) payments of principal and interest are madethroughout the life of the loan. To figure out the interest payments for amortized loans,the nominal interest rate is multiplied by the amount of principal outstanding (thedeclining balance) for each payment period.

ACCION 1

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 5/34

Interest rates and self sufficiency

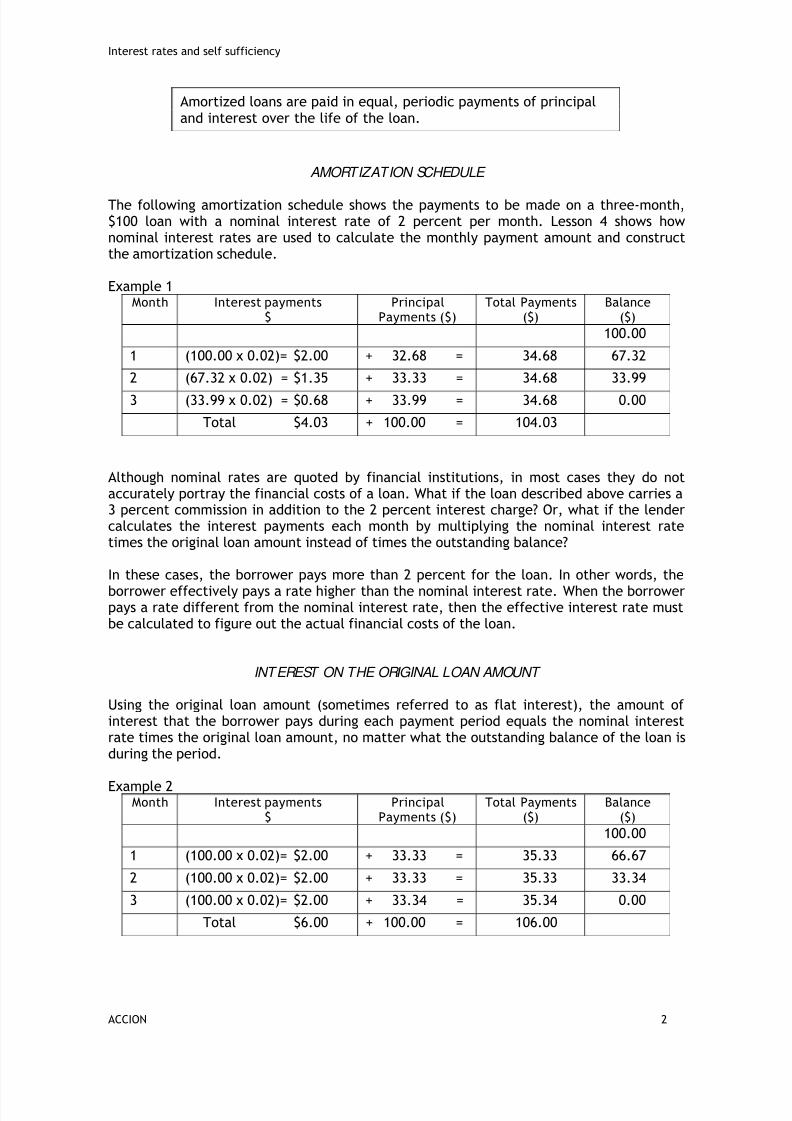

Amortized loans are paid in equal, periodic payments of principaland interest over the life of the loan.

AMORTIZATION SCHEDULE

The following amortization schedule shows the payments to be made on a three-month,$100 loan with a nominal interest rate of 2 percent per month. Lesson 4 shows hownominal interest rates are used to calculate the monthly payment amount and constructthe amortization schedule.

Example 1Month Interest payments

$Principal

Payments ($)Total Payments

($)Balance

($)

100.00

1 (100.00 x 0.02)= $2.00 + 32.68 = 34.68 67.32

2 (67.32 x 0.02) = $1.35 + 33.33 = 34.68 33.993 (33.99 x 0.02) = $0.68 + 33.99 = 34.68 0.00

Total $4.03 + 100.00 = 104.03

Although nominal rates are quoted by financial institutions, in most cases they do notaccurately portray the financial costs of a loan. What if the loan described above carries a3 percent commission in addition to the 2 percent interest charge? Or, what if the lendercalculates the interest payments each month by multiplying the nominal interest ratetimes the original loan amount instead of times the outstanding balance?

In these cases, the borrower pays more than 2 percent for the loan. In other words, theborrower effectively pays a rate higher than the nominal interest rate. When the borrowerpays a rate different from the nominal interest rate, then the effective interest rate mustbe calculated to figure out the actual financial costs of the loan.

INTEREST ON THE ORIGINAL LOAN AMOUNT

Using the original loan amount (sometimes referred to as flat interest), the amount ofinterest that the borrower pays during each payment period equals the nominal interestrate times the original loan amount, no matter what the outstanding balance of the loan is

during the period.

Example 2Month Interest payments

$Principal

Payments ($)Total Payments

($)Balance

($)

100.00

1 (100.00 x 0.02)= $2.00 + 33.33 = 35.33 66.67

2 (100.00 x 0.02)= $2.00 + 33.33 = 35.33 33.34

3 (100.00 x 0.02)= $2.00 + 33.34 = 35.34 0.00

Total $6.00 + 100.00 = 106.00

ACCION 2

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 6/34

Interest rates and self sufficiency

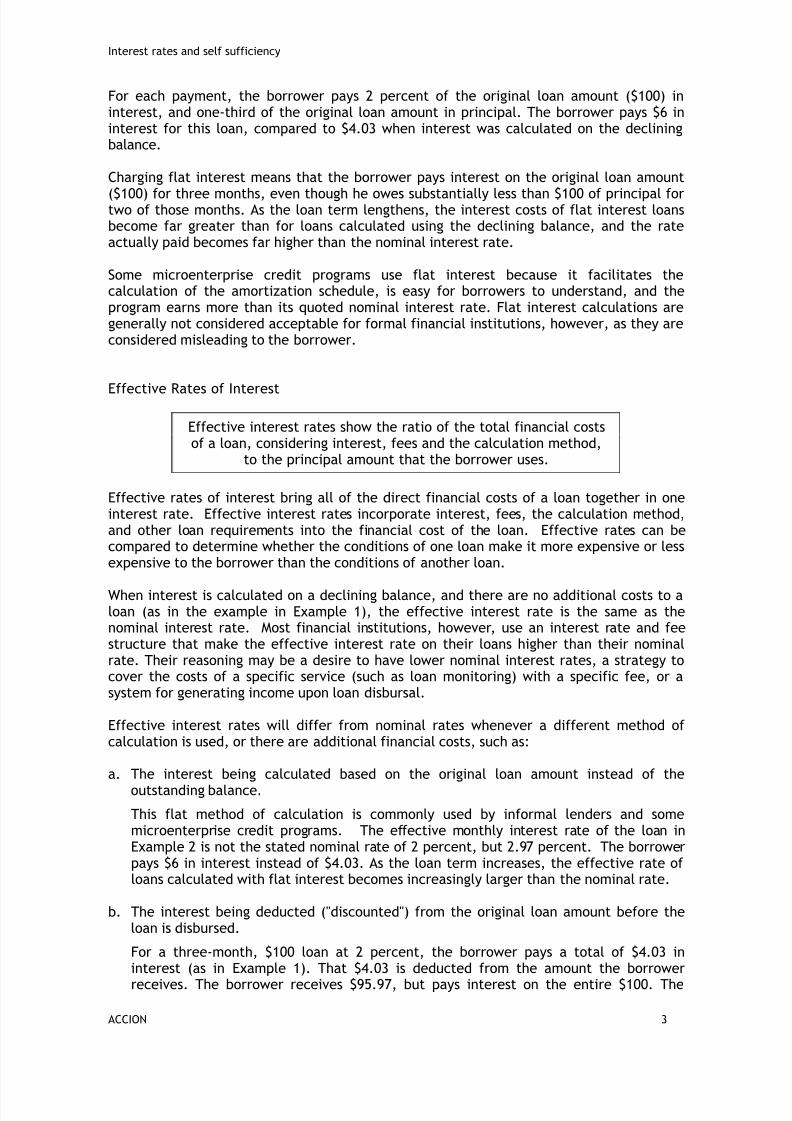

For each payment, the borrower pays 2 percent of the original loan amount ($100) ininterest, and one-third of the original loan amount in principal. The borrower pays $6 ininterest for this loan, compared to $4.03 when interest was calculated on the decliningbalance.

Charging flat interest means that the borrower pays interest on the original loan amount

($100) for three months, even though he owes substantially less than $100 of principal fortwo of those months. As the loan term lengthens, the interest costs of flat interest loansbecome far greater than for loans calculated using the declining balance, and the rateactually paid becomes far higher than the nominal interest rate.

Some microenterprise credit programs use flat interest because it facilitates thecalculation of the amortization schedule, is easy for borrowers to understand, and theprogram earns more than its quoted nominal interest rate. Flat interest calculations aregenerally not considered acceptable for formal financial institutions, however, as they areconsidered misleading to the borrower.

Effective Rates of Interest

Effective interest rates show the ratio of the total financial costsof a loan, considering interest, fees and the calculation method,

to the principal amount that the borrower uses.

Effective rates of interest bring all of the direct financial costs of a loan together in oneinterest rate. Effective interest rates incorporate interest, fees, the calculation method,and other loan requirements into the financial cost of the loan. Effective rates can becompared to determine whether the conditions of one loan make it more expensive or less

expensive to the borrower than the conditions of another loan.

When interest is calculated on a declining balance, and there are no additional costs to aloan (as in the example in Example 1), the effective interest rate is the same as thenominal interest rate. Most financial institutions, however, use an interest rate and feestructure that make the effective interest rate on their loans higher than their nominalrate. Their reasoning may be a desire to have lower nominal interest rates, a strategy tocover the costs of a specific service (such as loan monitoring) with a specific fee, or asystem for generating income upon loan disbursal.

Effective interest rates will differ from nominal rates whenever a different method ofcalculation is used, or there are additional financial costs, such as:

a. The interest being calculated based on the original loan amount instead of theoutstanding balance.

This flat method of calculation is commonly used by informal lenders and somemicroenterprise credit programs. The effective monthly interest rate of the loan inExample 2 is not the stated nominal rate of 2 percent, but 2.97 percent. The borrowerpays $6 in interest instead of $4.03. As the loan term increases, the effective rate ofloans calculated with flat interest becomes increasingly larger than the nominal rate.

b. The interest being deducted ("discounted") from the original loan amount before theloan is disbursed.

For a three-month, $100 loan at 2 percent, the borrower pays a total of $4.03 ininterest (as in Example 1). That $4.03 is deducted from the amount the borrowerreceives. The borrower receives $95.97, but pays interest on the entire $100. The

ACCION 3

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 7/34

Interest rates and self sufficiency

monthly effective interest rate is 2.08 percent, even though the nominal rate is 2percent. The effective interest rate on discounted loans becomes increasingly largerthan the nominal rate as the loan term increases.

c. A commission or other fee.

Fees will alter the effective interest rate to varying degrees depending on how they arecalculated and paid. For example, if the bank charges a 5 percent fee on the loan inExample 1, payable upon loan disbursal, then the borrower receives a $100 loan, buthas to pay $5 right away. The borrower pays interest on $100, but only gets to use $95.The effective monthly interest rate on the loan is 4.68 percent, more than double thenominal rate of 2 percent. Unlike the previous cases, the effective interest rate onloans with fees decreases as the loan term increases, because the cost of those fees isspread out over more payment periods.

d. A requirement that the borrower maintain a minimum amount, a compensatingbalance, in a savings account in order to receive a loan.

Compensating balances arc a common practice of credit unions and somemicroenterprise programs. The borrower in Example 1 might be required to place $25on deposit in a savings account to receive a loan for $100. Effectively, the borrowerreceives a $100 loan, pays interest on $100, but has $25 of his own money tied upwithout being able to use it to generate income. The monthly effective interest rate is4.3 percent.

The higher the effective interest rate, the more this loan isactually costing the borrower, and the more it is earning the

lender.

As the examples above show, a three-month loan advertised at 2 percent monthly interestcan have an effective interest rate considerably higher than 2 percent. The higher theeffective interest rate, the more this loan is actually costing the borrower, and the more itis earning the lender. All of these types of interest calculations are used, underscoringhow little nominal interest rates reveal about the costs of a loan. The only way toascertain the true financial costs of loans and compare the costs of loans from differentlenders is by using the effective interest rate.

Calculating Effective Interest Rates

The effective interest rate represents the total financial cost of a loan to the borrower,

considering the conditions of the loan (as in the four examples above). For loans with onlyone payment at the end, simple interest loans, calculating the effective interest rate iseasy. The effective interest rate is the amount the borrower pays in interest, fees, andcommissions, divided by the amount the borrower receives.

Effective Interest Rate = amount paid in interest, fees and commissionsprincipal amount received by borrower

For example, the effective interest rate (EIR) of a $100 simple interest loan at 2 percentper month, with a 5 percent fee paid upon loan disbursal, is:

EIR = ($100x0.06 interest) + ($100 x 0.05 fee)($100 - $5 fee)

= 11.6% for three months or 3.9% per month

ACCION 4

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 8/34

Interest rates and self sufficiency

Calculating the effective interest rate for amortized loans is more complicated becausethe amount on which the interest payments are calculated (the amount of principaloutstanding) is different for each payment period. A rough approximation of the effectiveinterest rate can be calculated by dividing the interest, fees, and commissions on the loanby the sum of the amounts outstanding during the loan period. The result is the effective

interest rate per payment period.

EIR = amount paid in interest, fees and commissionssum of principal amounts outstanding

For example an approximation of the effective interest rate of a $100 amortized loan withmonthly payments, a monthly nominal interest rate of 2 percent and a 5 percentcommission paid upon loan disbursal is:

EIR = 4.03 interest1 + (0.05 x 100 fee)(100 + 66.67 + 33.34)

EIR = 4.5% per month.

1 See Example 1 for calculation of amount of interest

The easiest way to accurately calculate effective interest rates, however, is to use aspreadsheet. The spreadsheet can be set up to calculate the effective rate when providedwith the amount the borrower receives (sometimes called present value [PV]), thenumber of payment periods (N), and the amount to be paid in each period (PMT, oftenentered as a negative number). These three variables change depending upon theconditions of the loan. The following example shows how these variables are used todetermine the effective interest rate of an amortized loan with a commission.

Example 3: USING A SPREADSHEET TO CALCULATE EFFECTIVE INTEREST RATES

To calculate the effective interest rate of a $100, 3-month loan with a nominal interestrate of 2 percent per month and a commission of 5 percent paid upon loan disbursement:

1. Determine the monthly payment:

a) Enter into the spreadsheet the loan amount, the number of payment periods andthe nominal monthly interest rate:

PV = 100

N = 3i = 2

b) Solve for payment: PMT = -34.68.

2. Determine the effective interest rate:

a) Enter into the spreadsheet the monthly payment, the amount the borrowereffectively received and the number of payment periods:

PMT = -34.68PV = 95 ($100 minus 5% of $100)

N = 3

b) Solve for effective interest rate: i = 4.7% (per month).

ACCION 5

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 9/34

Interest rates and self sufficiency

Lesson 4 shows how to use a spreadsheet for loans with flat interest, interest deducted upfront, and compensating balances. A spreadsheet is attached to this study guide, whichyou can use to make these calculations.

It is important to realize that the effective interest rates of loans with the same nominalinterest rate and fee can vary with the loan size and loan term. A three-month, $100 loanat 2 percent per month, with a 5 percent fee paid up front, has an effective rate ofinterest of 4.7 percent per month (see above for calculation). The same loan over a sixmonth period has an effective rate of 3.5 percent per month. If the fee is a set amount,instead of a percentage of the loan amount, then the effective rate will changeconsiderably as the size of the loan increases or decreases as well.

Real Rates of Interest

The real rate of interest is the rate of interest adjusted to allowfor inflation and is the interest rate minus the rate of inflation.

Real rates of interest are rates that have been adjusted to compensate for the effects ofinflation. Real interest rates are either nominal or effective rates of interest minus theinflation rate. They can be either positive or negative. For instance, if an institutioncharges an effective rate of 45 percent annually in an economy where inflation is 24percent a year, then the real effective rate of interest is 21 percent (45 - 24). If only 20percent interest is charged, then the real effective rate is negative 4 percent. Real ratesof interest are important analytical tools for managers who must ensure that they do notlet inflation eat away the value of their lending portfolios. With negative-real rates of

interest, the value of a loan portfolio cannot be maintained.

THE EFFECTS OF INFLATION

The effects of inflation on the value of a portfolio can be calculated with the followingformula, where VPf is the value of the portfolio at the end of the period, VP i the value ofthe portfolio at the beginning of the period, and i the rate of inflation of the period:

VPf = VPi

(1+i)

In Colombia, during the period from 1980 to 1988, the average annual rate of inflation was24 percent. If a credit program had a portfolio in Colombian pesos worth US$ 100,000 in1985, and neither lost nor added any new money to the portfolio through 1987, then thechange in value of the portfolio during the three-year period would have been:

Year Value of BeginningPortfolio ($)

Value of EndingPortfolio ($)

Value Lost to Inflation($)

1985 100,000 80,645 19,3531986 80,645 65,036 15,6091987 65,036 52,488 12,588

By 1988, the pesos in the portfolio would have been worth only $52,448! To preserve thevalue of its portfolio, the program would have to generate enough income to add theamount shown in the "Value Lost to Inflation" column to its portfolio each year. In 1985,

ACCION 6

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 10/34

Interest rates and self sufficiency

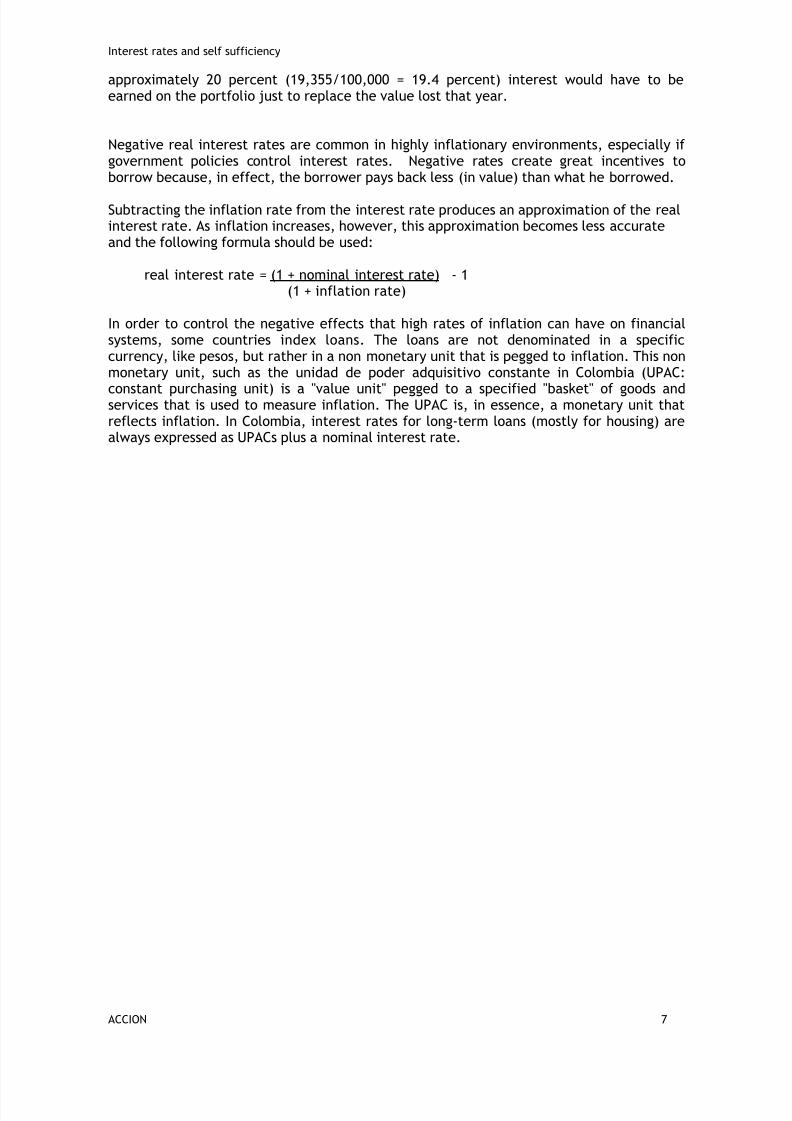

approximately 20 percent (19,355/100,000 = 19.4 percent) interest would have to beearned on the portfolio just to replace the value lost that year.

Negative real interest rates are common in highly inflationary environments, especially ifgovernment policies control interest rates. Negative rates create great incentives toborrow because, in effect, the borrower pays back less (in value) than what he borrowed.

Subtracting the inflation rate from the interest rate produces an approximation of the realinterest rate. As inflation increases, however, this approximation becomes less accurateand the following formula should be used:

real interest rate = (1 + nominal interest rate) - 1(1 + inflation rate)

In order to control the negative effects that high rates of inflation can have on financialsystems, some countries index loans. The loans are not denominated in a specificcurrency, like pesos, but rather in a non monetary unit that is pegged to inflation. This non

monetary unit, such as the unidad de poder adquisitivo constante in Colombia (UPAC:constant purchasing unit) is a "value unit" pegged to a specified "basket" of goods andservices that is used to measure inflation. The UPAC is, in essence, a monetary unit thatreflects inflation. In Colombia, interest rates for long-term loans (mostly for housing) arealways expressed as UPACs plus a nominal interest rate.

ACCION 7

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 11/34

Interest Rates and Self-Sufficiency

LESSON 3

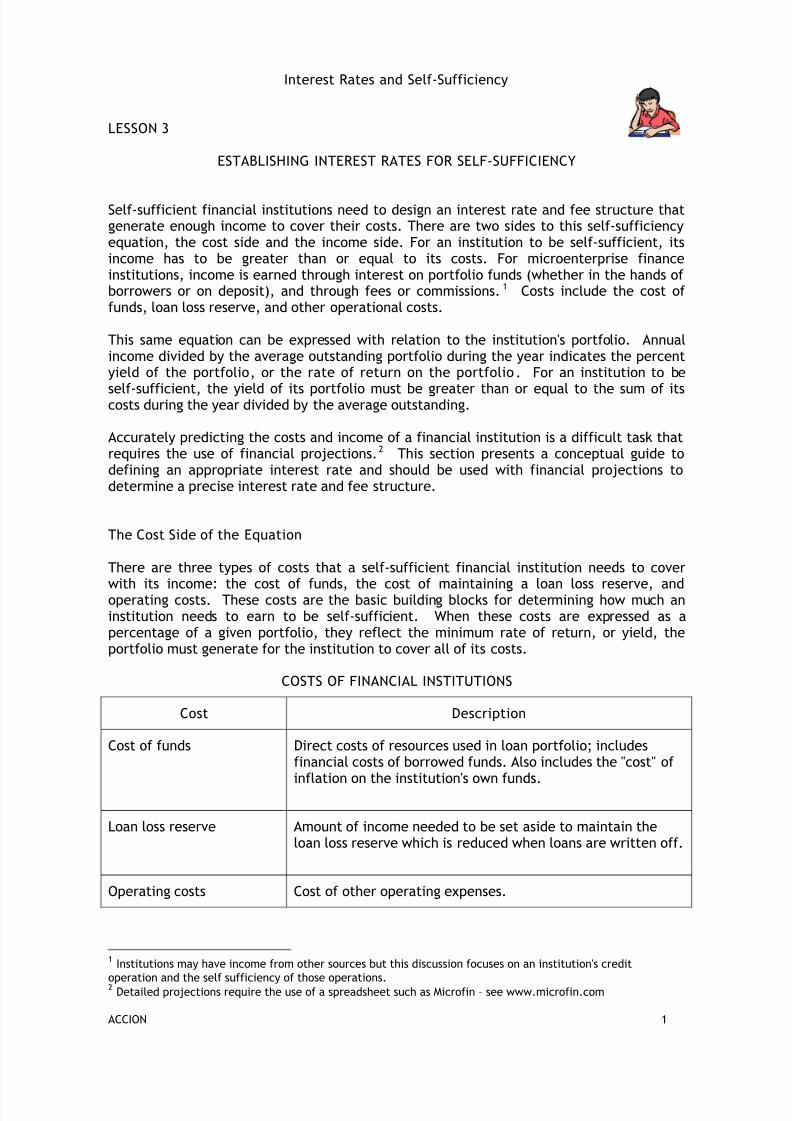

ESTABLISHING INTEREST RATES FOR SELF-SUFFICIENCY

Self-sufficient financial institutions need to design an interest rate and fee structure thatgenerate enough income to cover their costs. There are two sides to this self-sufficiencyequation, the cost side and the income side. For an institution to be self-sufficient, itsincome has to be greater than or equal to its costs. For microenterprise financeinstitutions, income is earned through interest on portfolio funds (whether in the hands ofborrowers or on deposit), and through fees or commissions. 1 Costs include the cost offunds, loan loss reserve, and other operational costs.

This same equation can be expressed with relation to the institution's portfolio. Annualincome divided by the average outstanding portfolio during the year indicates the percent

yield of the portfolio, or the rate of return on the portfolio. For an institution to beself-sufficient, the yield of its portfolio must be greater than or equal to the sum of itscosts during the year divided by the average outstanding.

Accurately predicting the costs and income of a financial institution is a difficult task thatrequires the use of financial projections.2 This section presents a conceptual guide todefining an appropriate interest rate and should be used with financial projections todetermine a precise interest rate and fee structure.

The Cost Side of the Equation

There are three types of costs that a self-sufficient financial institution needs to coverwith its income: the cost of funds, the cost of maintaining a loan loss reserve, andoperating costs. These costs are the basic building blocks for determining how much aninstitution needs to earn to be self-sufficient. When these costs are expressed as apercentage of a given portfolio, they reflect the minimum rate of return, or yield, theportfolio must generate for the institution to cover all of its costs.

COSTS OF FINANCIAL INSTITUTIONS

Cost Description

Cost of funds Direct costs of resources used in loan portfolio; includesfinancial costs of borrowed funds. Also includes the "cost" ofinflation on the institution's own funds.

Loan loss reserve Amount of income needed to be set aside to maintain theloan loss reserve which is reduced when loans are written off.

Operating costs Cost of other operating expenses.

1 Institutions may have income from other sources but this discussion focuses on an institution's creditoperation and the self sufficiency of those operations.2 Detailed projections require the use of a spreadsheet such as Microfin – see www.microfin.com

ACCION 1

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 12/34

Interest rates and self sufficiency

Cost of Funds

The cost of funds is what lending institutions pay for the resourcesthey use to lend to their borrowers.

The cost of funds refers to the amount institutions pay for the resources they use to lend

to their borrowers. These resources may be loans from local banks, savings deposited byborrowers, retained earnings of the institution, donated funds, or other funds in theportfolio.

Traditionally, most microenterprise credit programs have begun operations with donations,which have close to zero costs (the time and expense of applying for the funds is a cost).In order to expand, however, an increasing number of microenterprise institutions areborrowing funds at both subsidized and commercial rates of interest. Like any borrower,the microenterprise institution must pay financial costs for the funds it borrows for itsportfolio. These costs include interest paid to depositors (if the institution accepts savingsdeposits), interest paid to lenders, fees paid to lenders (or donors), compensating balancesrequired by lenders or donors, and any other financial costs.

The portion of an institution's portfolio funds that is not borrowed, but was donated orearned by the institution (or invested in it), form part of its equity. Though it pays nointerest on these funds, the institution should protect them from devaluation due toinflation. One way to preserve the value of equity funds in the portfolio is to consider thatthey have a cost equal to the expected rate of inflation.3 Interest is then charged to coverthat cost, and the income generated is reinvested in the portfolio to preserve its realvalue.

The institution does not have to preserve the value of the money it has borrowed from abank or other source for its portfolio. The bank should charge the institution sufficient

interest to preserve the value of those funds. If the bank does not charge sufficientinterest, then the institution pays the bank back less (in value) than it borrowed; asituation that benefits the institution to the detriment of the bank.

In sum, the cost of funds includes the effective rate of interest on all borrowed money. Italso includes the "cost" of inflation on the institution's own funds.

Loan Loss Reserve

Credit institutions must earn enough income to replace funds lost from the portfoliobecause of loan defaults. The loan loss reserve is established from income earned by theinstitution and is used to replenish funds lost to the portfolio when loans are written off.

Through this process, non-recoverable amounts lost from the portfolio are replaced byincome earned by the institution, thereby preventing the decapitalization of the portfolio.

Normally, financial institutions estimate the amount of expected bad debt (on the basis ofprior experience and estimated potential losses from the current portfolio), and express itas a percentage of the portfolio. Mature financial institutions can usually predict with ahigh degree of accuracy the amount that will not be recovered and that should be in theloan loss reserve. As a general role, well-managed microenterprise credit institutionsshould not have loan losses exceeding 3 percent of the average portfolio in any given year.With estimated annual losses of 3 percent of the average portfolio, an institution's loanloss reserve should be maintained at 3 percent of the portfolio, and the interest ratecharged to borrowers should include 3 percent to maintain that reserve.

3 Estimating future inflation rates is extremely difficult. Estimates calculated by a country's Central Bank oranother reliable source can be used.

ACCION 2

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 13/34

Interest rates and self sufficiency

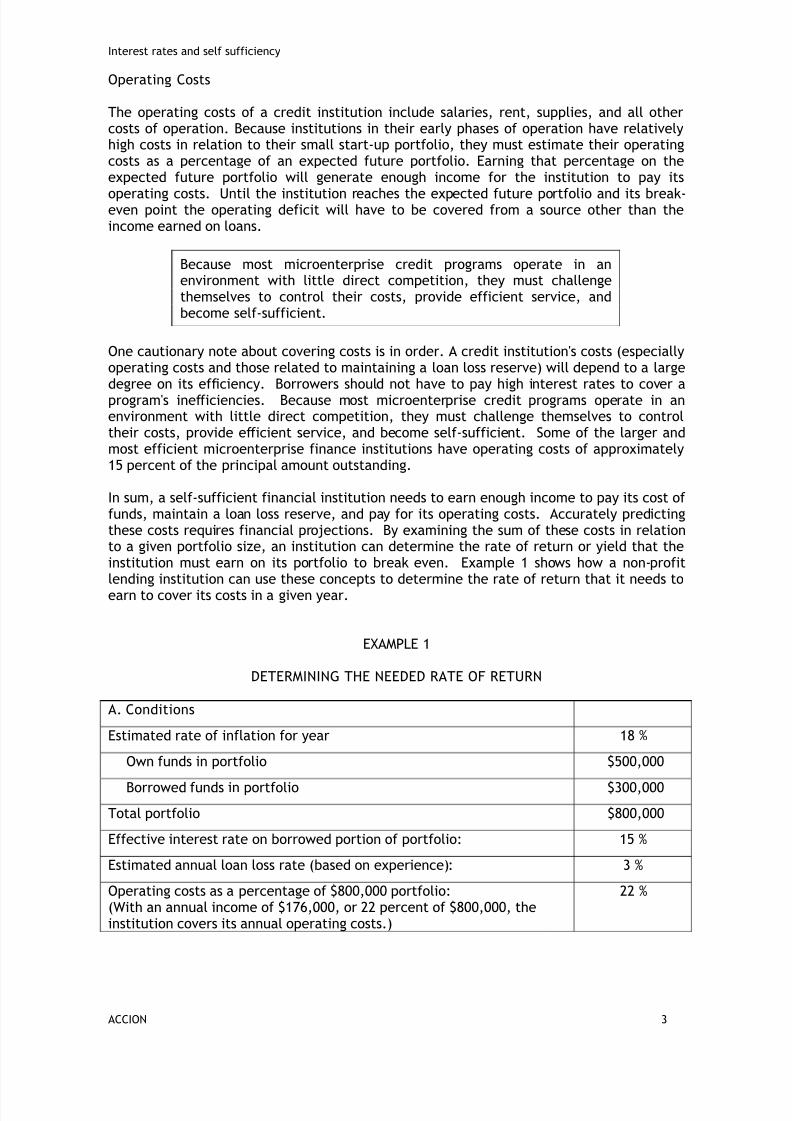

Operating Costs

The operating costs of a credit institution include salaries, rent, supplies, and all othercosts of operation. Because institutions in their early phases of operation have relativelyhigh costs in relation to their small start-up portfolio, they must estimate their operatingcosts as a percentage of an expected future portfolio. Earning that percentage on theexpected future portfolio will generate enough income for the institution to pay its

operating costs. Until the institution reaches the expected future portfolio and its break-even point the operating deficit will have to be covered from a source other than theincome earned on loans.

Because most microenterprise credit programs operate in anenvironment with little direct competition, they must challengethemselves to control their costs, provide efficient service, andbecome self-sufficient.

One cautionary note about covering costs is in order. A credit institution's costs (especiallyoperating costs and those related to maintaining a loan loss reserve) will depend to a largedegree on its efficiency. Borrowers should not have to pay high interest rates to cover aprogram's inefficiencies. Because most microenterprise credit programs operate in anenvironment with little direct competition, they must challenge themselves to controltheir costs, provide efficient service, and become self-sufficient. Some of the larger andmost efficient microenterprise finance institutions have operating costs of approximately15 percent of the principal amount outstanding.

In sum, a self-sufficient financial institution needs to earn enough income to pay its cost offunds, maintain a loan loss reserve, and pay for its operating costs. Accurately predictingthese costs requires financial projections. By examining the sum of these costs in relationto a given portfolio size, an institution can determine the rate of return or yield that the

institution must earn on its portfolio to break even. Example 1 shows how a non-profitlending institution can use these concepts to determine the rate of return that it needs toearn to cover its costs in a given year.

EXAMPLE 1

DETERMINING THE NEEDED RATE OF RETURN

A. Conditions

Estimated rate of inflation for year 18 %

Own funds in portfolio $500,000

Borrowed funds in portfolio $300,000

Total portfolio $800,000

Effective interest rate on borrowed portion of portfolio: 15 %

Estimated annual loan loss rate (based on experience): 3 %

Operating costs as a percentage of $800,000 portfolio:(With an annual income of $176,000, or 22 percent of $800,000, theinstitution covers its annual operating costs.)

22 %

ACCION 3

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 14/34

Interest rates and self sufficiency

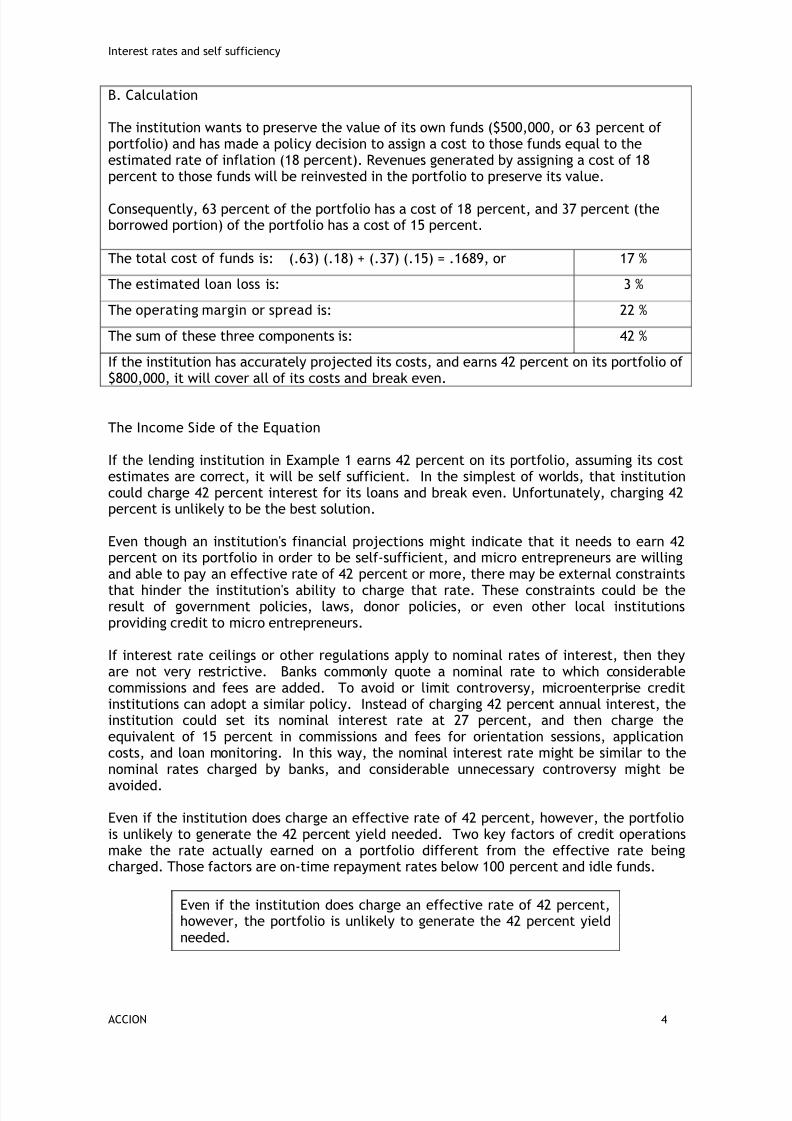

B. Calculation

The institution wants to preserve the value of its own funds ($500,000, or 63 percent ofportfolio) and has made a policy decision to assign a cost to those funds equal to theestimated rate of inflation (18 percent). Revenues generated by assigning a cost of 18percent to those funds will be reinvested in the portfolio to preserve its value.

Consequently, 63 percent of the portfolio has a cost of 18 percent, and 37 percent (theborrowed portion) of the portfolio has a cost of 15 percent.

The total cost of funds is: (.63) (.18) + (.37) (.15) = .1689, or 17 %

The estimated loan loss is: 3 %

The operating margin or spread is: 22 %

The sum of these three components is: 42 %

If the institution has accurately projected its costs, and earns 42 percent on its portfolio of

$800,000, it will cover all of its costs and break even.

The Income Side of the Equation

If the lending institution in Example 1 earns 42 percent on its portfolio, assuming its costestimates are correct, it will be self sufficient. In the simplest of worlds, that institutioncould charge 42 percent interest for its loans and break even. Unfortunately, charging 42percent is unlikely to be the best solution.

Even though an institution's financial projections might indicate that it needs to earn 42percent on its portfolio in order to be self-sufficient, and micro entrepreneurs are willingand able to pay an effective rate of 42 percent or more, there may be external constraintsthat hinder the institution's ability to charge that rate. These constraints could be theresult of government policies, laws, donor policies, or even other local institutionsproviding credit to micro entrepreneurs.

If interest rate ceilings or other regulations apply to nominal rates of interest, then theyare not very restrictive. Banks commonly quote a nominal rate to which considerablecommissions and fees are added. To avoid or limit controversy, microenterprise creditinstitutions can adopt a similar policy. Instead of charging 42 percent annual interest, theinstitution could set its nominal interest rate at 27 percent, and then charge theequivalent of 15 percent in commissions and fees for orientation sessions, application

costs, and loan monitoring. In this way, the nominal interest rate might be similar to thenominal rates charged by banks, and considerable unnecessary controversy might beavoided.

Even if the institution does charge an effective rate of 42 percent, however, the portfoliois unlikely to generate the 42 percent yield needed. Two key factors of credit operationsmake the rate actually earned on a portfolio different from the effective rate beingcharged. Those factors are on-time repayment rates below 100 percent and idle funds.

Even if the institution does charge an effective rate of 42 percent,however, the portfolio is unlikely to generate the 42 percent yieldneeded.

ACCION 4

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 15/34

Interest rates and self sufficiency

The Ef fect of Loan Terms on Income

As discussed in the section on effective interest rates, loans with commissions or fees willhave higher effective interest rates as the loan term decreases. Likewise, a lendinginstitution that charges fees will earn more income the shorter the terms of its loans, asthe same portfolio amount generates fees more frequently.

Assume that the institution with an $800,000 portfolio charges 27 percent interest and 20percent of the loan amount as an up-front fee. There is no delinquency and the money isre-lent the same day it is paid.

• With an average loan term of 12 months, the yearly income is:$376,000 [(800,000 x 0.27) + (800,000 x 0.20)]

• If the average term is 6 months, annual income increases to:$536,000 [(800,000 x 0.27) + (1,600,000 x 0.20)]

• If the institution charged 47 percent interest and no fees, its annual income regardlessof the loan term, would be:$376,000 (800,000 X 0.47)

Repayment Rates

Late payments can have a devastating effect on an institution's income. The cost side ofthe self-sufficiency equation includes the cost of default through the maintenance of aloss reserve. In addition, the side of the equation must incorporate the interest incomepostponed from loans that fall into arrears (some of which might eventually be lost if theloans are defaulted). If interest payments on loans are not made when they are due,

interest income during a specific period will be far lower than the amount outstandingtimes the nominal interest rate for that period.

One common method used by financial institutions to compensate for income postponeddue to delinquency is to charge a penalty for late payments. Such penalties also serve tomotivate on-time repayment.

Ef fect of Lat e Payments on Int erest Income

The institution in Example 1 calculates that it needs to earn 42 percent on its portfolio of

$800,000 to break even in a given year. The nominal interest rate is 27 percent, and therest is through fees collected upon loan disbursal.

• Assume that only 90 percent of the amount due during the year (principal andinterest) is actually paid during the year.

• Instead of earning 27 percent in interest on the portfolio during the year, i.e.$216,000, the program earns only 24 percent (0.90 x 0.27), i.e. $194,400 (0.90 x 0.27x 800,000).

ACCION 5

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 16/34

Interest rates and self sufficiency

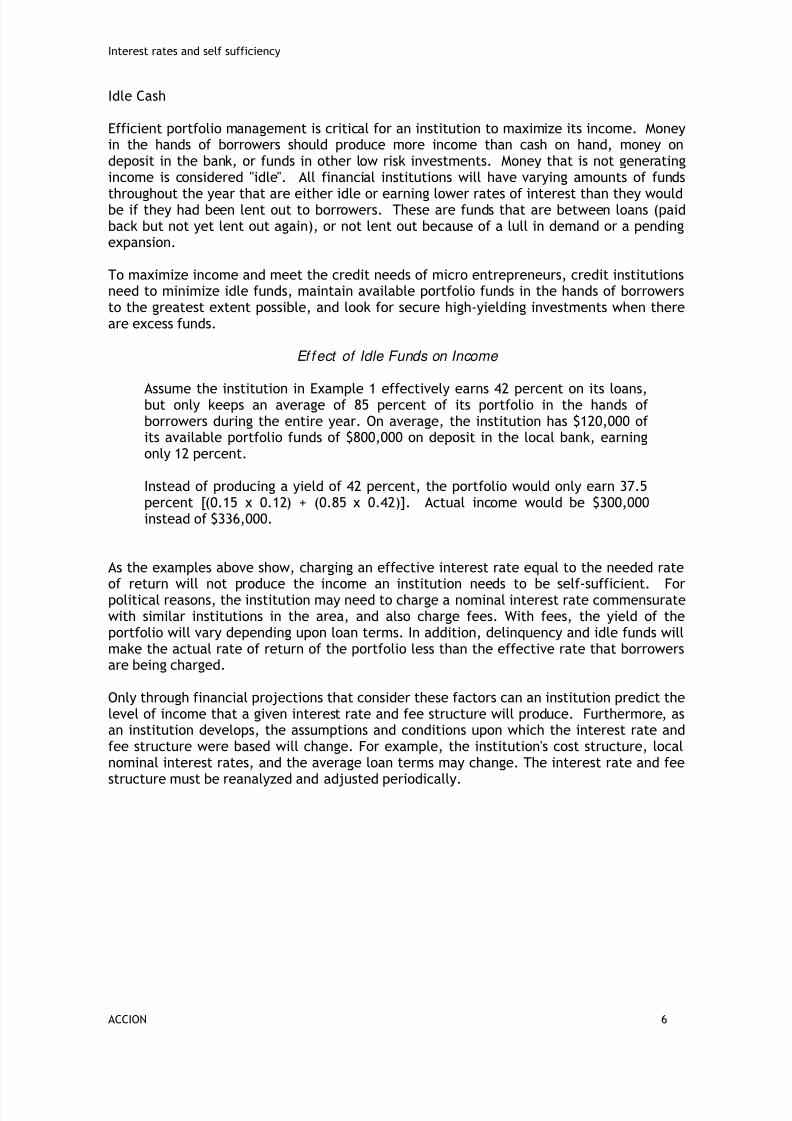

Idle Cash

Efficient portfolio management is critical for an institution to maximize its income. Moneyin the hands of borrowers should produce more income than cash on hand, money ondeposit in the bank, or funds in other low risk investments. Money that is not generatingincome is considered "idle". All financial institutions will have varying amounts of funds

throughout the year that are either idle or earning lower rates of interest than they wouldbe if they had been lent out to borrowers. These are funds that are between loans (paidback but not yet lent out again), or not lent out because of a lull in demand or a pendingexpansion.

To maximize income and meet the credit needs of micro entrepreneurs, credit institutionsneed to minimize idle funds, maintain available portfolio funds in the hands of borrowersto the greatest extent possible, and look for secure high-yielding investments when thereare excess funds.

Ef fect of Idle Funds on Income

Assume the institution in Example 1 effectively earns 42 percent on its loans,but only keeps an average of 85 percent of its portfolio in the hands ofborrowers during the entire year. On average, the institution has $120,000 ofits available portfolio funds of $800,000 on deposit in the local bank, earningonly 12 percent.

Instead of producing a yield of 42 percent, the portfolio would only earn 37.5percent [(0.15 x 0.12) + (0.85 x 0.42)]. Actual income would be $300,000instead of $336,000.

As the examples above show, charging an effective interest rate equal to the needed rateof return will not produce the income an institution needs to be self-sufficient. Forpolitical reasons, the institution may need to charge a nominal interest rate commensuratewith similar institutions in the area, and also charge fees. With fees, the yield of theportfolio will vary depending upon loan terms. In addition, delinquency and idle funds willmake the actual rate of return of the portfolio less than the effective rate that borrowersare being charged.

Only through financial projections that consider these factors can an institution predict thelevel of income that a given interest rate and fee structure will produce. Furthermore, asan institution develops, the assumptions and conditions upon which the interest rate andfee structure were based will change. For example, the institution's cost structure, localnominal interest rates, and the average loan terms may change. The interest rate and feestructure must be reanalyzed and adjusted periodically.

ACCION 6

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 17/34

Interest rates and self sufficiency

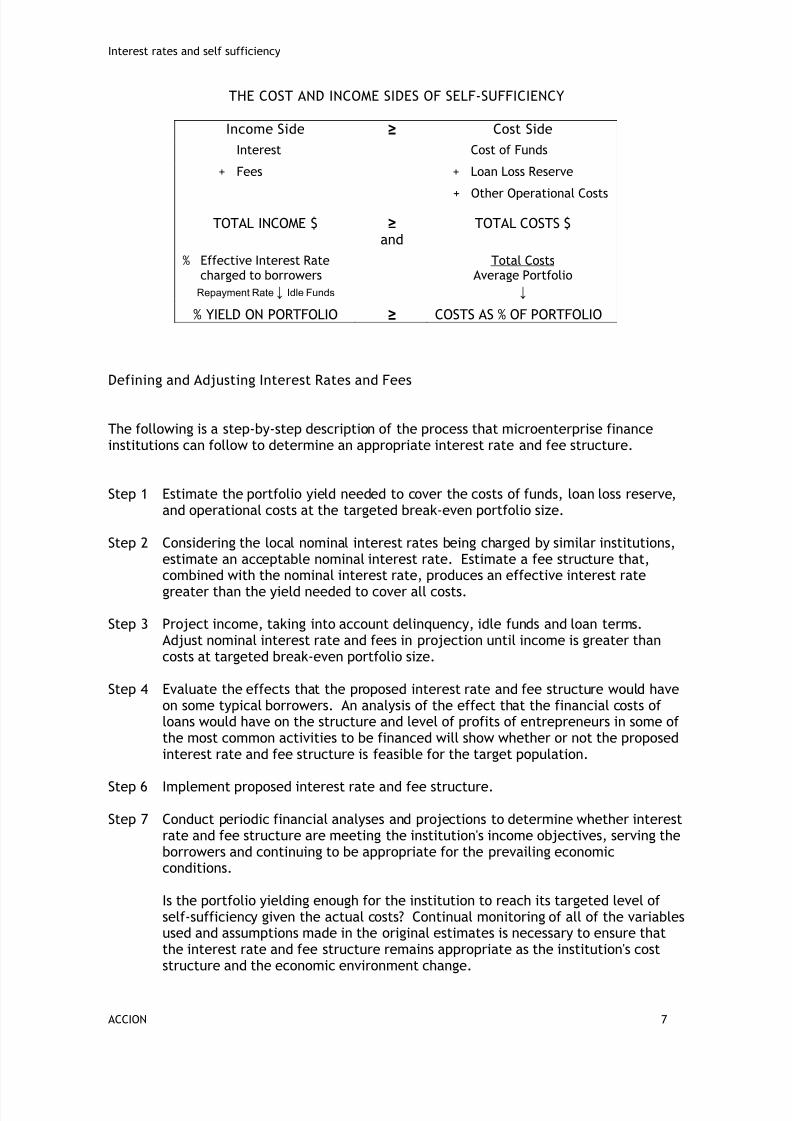

THE COST AND INCOME SIDES OF SELF-SUFFICIENCY

Income Side ≥ Cost Side

Interest Cost of Funds

+ Fees + Loan Loss Reserve

+ Other Operational Costs

TOTAL INCOME $ ≥ TOTAL COSTS $and

% Effective Interest Ratecharged to borrowers

Repayment Rate ↓ Idle Funds

Total CostsAverage Portfolio

↓

% YIELD ON PORTFOLIO ≥ COSTS AS % OF PORTFOLIO

Defining and Adjusting Interest Rates and Fees

The following is a step-by-step description of the process that microenterprise financeinstitutions can follow to determine an appropriate interest rate and fee structure.

Step 1 Estimate the portfolio yield needed to cover the costs of funds, loan loss reserve,and operational costs at the targeted break-even portfolio size.

Step 2 Considering the local nominal interest rates being charged by similar institutions,estimate an acceptable nominal interest rate. Estimate a fee structure that,combined with the nominal interest rate, produces an effective interest rategreater than the yield needed to cover all costs.

Step 3 Project income, taking into account delinquency, idle funds and loan terms.Adjust nominal interest rate and fees in projection until income is greater thancosts at targeted break-even portfolio size.

Step 4 Evaluate the effects that the proposed interest rate and fee structure would haveon some typical borrowers. An analysis of the effect that the financial costs ofloans would have on the structure and level of profits of entrepreneurs in some ofthe most common activities to be financed will show whether or not the proposed

interest rate and fee structure is feasible for the target population.

Step 6 Implement proposed interest rate and fee structure.

Step 7 Conduct periodic financial analyses and projections to determine whether interestrate and fee structure are meeting the institution's income objectives, serving theborrowers and continuing to be appropriate for the prevailing economicconditions.

Is the portfolio yielding enough for the institution to reach its targeted level ofself-sufficiency given the actual costs? Continual monitoring of all of the variablesused and assumptions made in the original estimates is necessary to ensure that

the interest rate and fee structure remains appropriate as the institution's coststructure and the economic environment change.

ACCION 7

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 18/34

Interest rates and self sufficiency

Step 8 Adjust interest rate and fee structure as conditions change. Institutions inrelatively stable economies may need to make only minor adjustments every 6 or12 months. Institutions in unstable economies with variable inflation may need tomake adjustments every month or even index their interest rate so that itcontinually fluctuates with inflation.

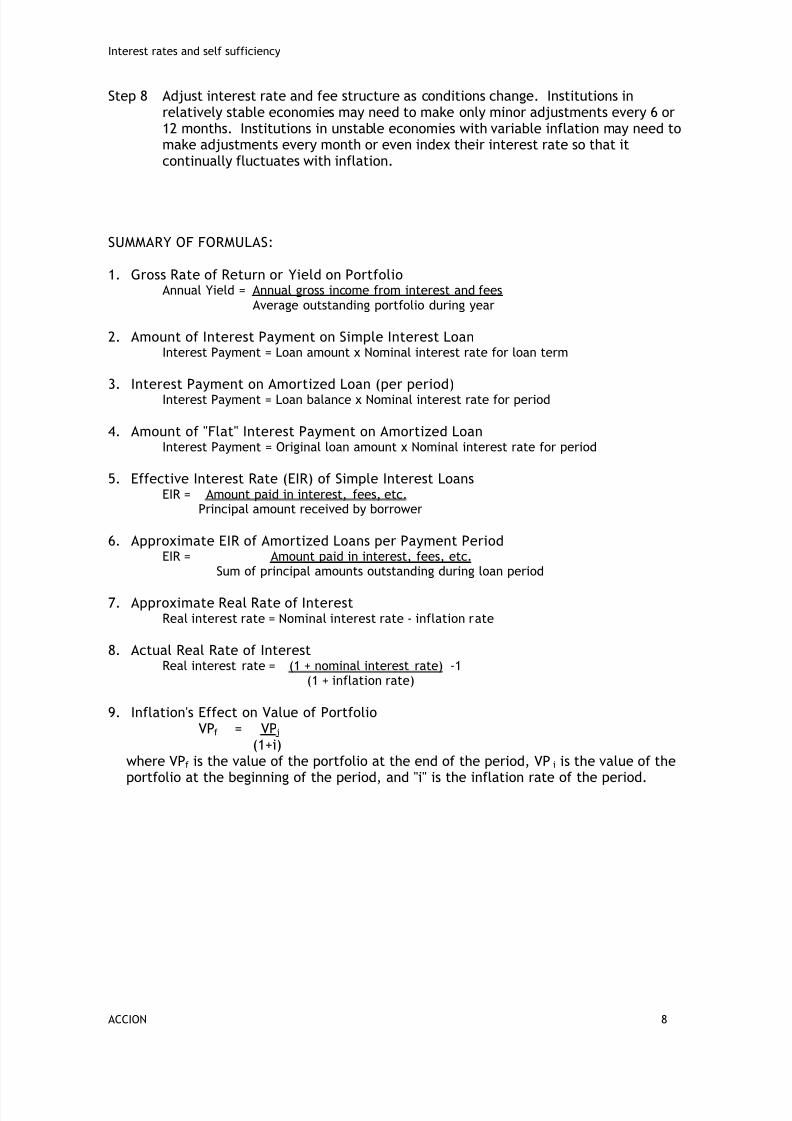

SUMMARY OF FORMULAS:

1. Gross Rate of Return or Yield on PortfolioAnnual Yield = Annual gross income from interest and fees

Average outstanding portfolio during year

2. Amount of Interest Payment on Simple Interest LoanInterest Payment = Loan amount x Nominal interest rate for loan term

3. Interest Payment on Amortized Loan (per period)Interest Payment = Loan balance x Nominal interest rate for period

4. Amount of "Flat" Interest Payment on Amortized LoanInterest Payment = Original loan amount x Nominal interest rate for period

5. Effective Interest Rate (EIR) of Simple Interest LoansEIR = Amount paid in interest, fees, etc.

Principal amount received by borrower

6. Approximate EIR of Amortized Loans per Payment PeriodEIR = Amount paid in interest, fees, etc.

Sum of principal amounts outstanding during loan period

7. Approximate Real Rate of InterestReal interest rate = Nominal interest rate - inflation rate

8. Actual Real Rate of InterestReal interest rate = (1 + nominal interest rate) -1

(1 + inflation rate)

9. Inflation's Effect on Value of PortfolioVPf = VPi

(1+i)

where VPf is the value of the portfolio at the end of the period, VP i is the value of theportfolio at the beginning of the period, and "i" is the inflation rate of the period.

ACCION 8

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 19/34

Interest Rates and Self-Sufficiency

LESSON 4

MAKING THE CALCULATIONS

Constructing an Amortization Schedule

There are several possible ways to construct the payment schedule when interest iscalculated on a declining balance. There are tables that can be consulted and calculatorsthat contain the formulae required to make the calculation when provided with the basicdetails of loan amount, interest rate and number of instalments. The followingmathematical formula can also be used to calculate the loan payments and to construct anamortization schedule.

instalment payment = PV x i x (1 + i)n

(1 + i)n - 1

where i = interest rate per payment periodn = number of paymentsPV = principal amount of the loan

Once the instalment payment is calculated with the above formula, then the amount thatgoes toward interest and principal can be determined for each payment period. Theamount that goes toward interest is the nominal interest rate times the balance at thebeginning of the period. The rest of the payment (the payment minus the amount goingtoward interest) is payment of principal.

For example, the amortization schedule for a three-month $100 loan, with 2 percentmonthly interest, would be calculated as follows:

1. Use the formula above to determine the monthly payment:

Payment = 100 x 0.2 x (1 + .02)3 = 100 x (.02 x 1.0612) = 34.68(1 + .02)3 -1 0.0612

2. Calculate the interest to be paid in the first payment:

$100.00 x 0.02 = $2.00 interest.

3. Subtract the interest from the first payment to see how much principal is paid with thefirst payment:

$34.68 - $2 = 32.68

4. Subtract the first principal payment from the outstanding balance to determine thenew outstanding balance:

100 – 32.68 = 67.32

Steps 2-4 can be repeated for each payment to construct the amortization schedule shownin Lesson 2.

ACCION 1

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 20/34

Interest rates and self sufficiency

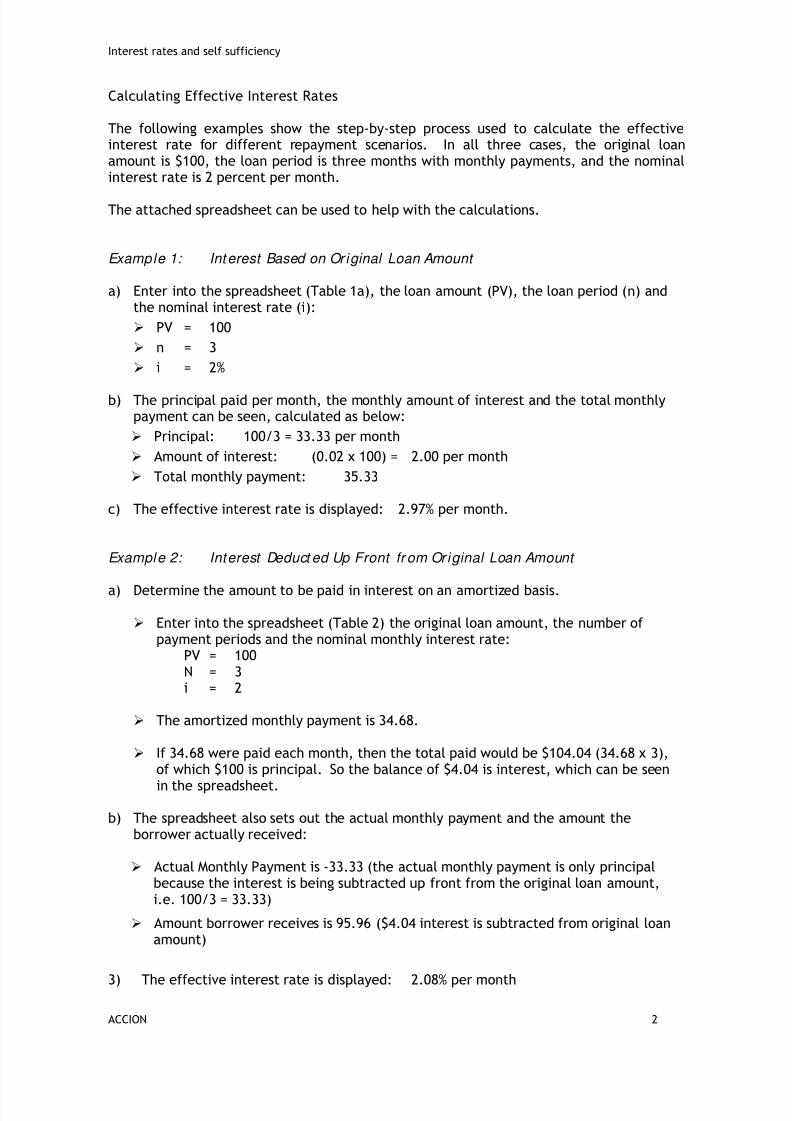

Calculating Effective Interest Rates

The following examples show the step-by-step process used to calculate the effectiveinterest rate for different repayment scenarios. In all three cases, the original loanamount is $100, the loan period is three months with monthly payments, and the nominalinterest rate is 2 percent per month.

The attached spreadsheet can be used to help with the calculations.

Example 1: Interest Based on Or iginal Loan Amount

a) Enter into the spreadsheet (Table 1a), the loan amount (PV), the loan period (n) andthe nominal interest rate (i):

PV = 100

n = 3

i = 2%

b) The principal paid per month, the monthly amount of interest and the total monthlypayment can be seen, calculated as below:

Principal: 100/3 = 33.33 per month

Amount of interest: (0.02 x 100) = 2.00 per month

Total monthly payment: 35.33

c) The effective interest rate is displayed: 2.97% per month.

Example 2: Interest Deduct ed Up Front fr om Or iginal Loan Amount

a) Determine the amount to be paid in interest on an amortized basis.

Enter into the spreadsheet (Table 2) the original loan amount, the number ofpayment periods and the nominal monthly interest rate:

PV = 100N = 3i = 2

The amortized monthly payment is 34.68.

If 34.68 were paid each month, then the total paid would be $104.04 (34.68 x 3),of which $100 is principal. So the balance of $4.04 is interest, which can be seenin the spreadsheet.

b) The spreadsheet also sets out the actual monthly payment and the amount theborrower actually received:

Actual Monthly Payment is -33.33 (the actual monthly payment is only principalbecause the interest is being subtracted up front from the original loan amount,i.e. 100/3 = 33.33)

Amount borrower receives is 95.96 ($4.04 interest is subtracted from original loan

amount)

3) The effective interest rate is displayed: 2.08% per month

ACCION 2

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 21/34

Interest rates and self sufficiency

Example 3: Loans wi t h Compensat ing Balances

The borrower receives a loan of $100, but $25 of his own money has to be kept on depositfor the life of the loan. The borrower loses the income that he could have earned on his$25 (which the lending institution can now earn). Furthermore, effectively, the borroweronly gets $75 in new money to use because his own $25 is on deposit. His $25 is not lost

but returned to him when he makes his final payment, effectively reducing the amount ofthat payment by $25.

a) Input the following assumptions into the spreadsheet (Table 3):PV = 100N = 3i = 2

and the amortized monthly payment shown will be 34.68 as before.

So the borrower pays 34.68 in each period but he is also incurring an additional cost inthe form of lost income on his deposit. Because he is paying 2 percent per month for

the loan, we can assume that his $25 deposit would be earning at least 2 percent if hedidn't have to keep it on deposit. (It is earning 2 percent for the bank if they lend it toanother borrower.) Thus, he is actually forfeiting 2 percent of $25 (0.50) each monthin lost income. In effect his monthly payments are $35.18 (34.68 +0 .50).

When his last payment is due, he gets his $25 returned to him, meaning that heeffectively pays only $10.18 (35.18 - 25) that month. So his monthly payments are35.18, 35.18, and 10.18.

b) The spreadsheet will display the effective interest rate of this loan.

Because the payment amounts vary, the effective interest rate is calculated with the

internal rate of return function in the spreadsheet. The flow of funds is:

Amount received by borrower = 75

First payment = (35.18)

Second payment = (35.18)

Third payment = (10.18)

The internal rate of return (IRR) will display as 4.3%.

Thus the effective interest rate on the loan is 4.3 percent.

ACCION 3

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 22/34

Interest rates and self sufficiency

Postscript

How Calculators Calculate the Effective Interest Rate

The effective rate is determined through an iterative process carried out by a calculator.

Given the three variables (present value, number of payment periods, and amount ofpayment), the effective interest rate is adjusted through trial and error until the result ofthe equation below is as close as possible to the present value (amount borrower receives)of the loan.

Using a three-month, $100 loan with monthly payments of $34.68 and no additional costs,the calculator continually adjusts the value of / (interest) until the sum of the Formulacolumn equals the present value of the loan ($100 in this case).

Payment Period Payment Formula

1 34.68

34.68

(1 + i)1

2 34.6834.68(1 + i)2

3 34.6734.68(1 + i)3

Total present value (amount borrower receives): 100.00

In this case, the value of i which correctly completes the equation is 0.02, meaning theloan has an effective monthly interest rate of 2 percent.

ACCION 4

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 23/34

Interest Rates and Self-Sufficiency

QUESTIONS AND EXERCISES

INTEREST RATE PROBLEMS

Note: Some of these problems require the use of the attached spreadsheet.

A. Nominal, Real and Effective Rates of Interest

1. What is a negative real interest rate? How is it affected by an increase in inflation?

2. What are nominal interest rates and how are they affected by:a. A dramatic increase in inflation?b. An increase in the commission on a loan?

3. What are effective interest rates and how are they affected by:a. A dramatic increase in inflation?b. An increase in the commission on a loan?

4. Besides financial costs, what other kinds of costs do borrowers pay for a loan? Give examples.

ACCION – with editing by RFLC 1

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 24/34

Interest rates and self sufficiency

5. What differentiates transaction costs from financial costs?

6. José Martínez is a carpenter who needs $500 to purchase wood. He would be able to repay theloan in equal instalments over a six-month period. He has two alternatives for the loan: theLoans for Entrepreneurial Development (LED) program or Margarita, the money lender. Bothsources offer him $500 for six months with monthly payments but differ in terms of theirspecific charges which are specified below:

Loans for Entrepreneurial Development

3 % monthly interest calculated on a declining balance.

3% loan processing fee (added to the loan amount and paid in full upon loan disbursal).$10 flat fee for fiscal stamps (added to the loan amount and paid in full upon loan disbursal).

Note: The loan amount would be for [500 + 10 + (0.03 x 500)], but Jose would only receive 500as the rest would cover the fee and commission.

Margarita the Moneylender

5% monthly interest calculated on original loan amount (flat), payable monthly.

a. Given the specific conditions of each of these sources of credit (detailed above), use thespreadsheet to work out which has the lowest financial cost, i.e. effective interest rate.

b. What other factors might José feel are important for deciding between the differentalternatives?

ACCION – with editing by RFLC 2

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 25/34

Interest rates and self sufficiency

7. The Microenterprise Credit Association (MCA) provides loans to micro entrepreneurs in a countrywhere annual inflation is 22%, with the following conditions:

• 2 % monthly interest on declining balance

• 6 – 12 month loan terms

•

monthly payments• 3 % commission payable upon loan disbursal

• $2 flat fee for fiscal stamps payable upon loan disbursal

(Note: as in question 6, the fee and commission are added on to the amount to be received bythe borrower, but then kept by the lending institution.)

a. What is the annual nominal interest rate?

b. What is the real annual nominal interest rate?

c. What is the monthly effective interest rate?

8. Marie makes clay pots and receives a $350 loan for six months from MCA (see Q.7 for terms ofloans from MCA).

a. How much does she pay in commissions and fees?

b. How much does she pay in interest? (Use the spreadsheet for this and questions c and d.)

c. What is the monthly effective interest rate on her loan?

d. If MCA calculated interest based on the original loan amount rather than the decliningbalance, how do the above values change?

e. Why is the effective interest rate higher when interest is calculated based on the originalloan amount (flat method), than using the declining balance method?

ACCION – with editing by RFLC 3

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 26/34

Interest rates and self sufficiency

9. Assume that Marie receives the same $350 loan (as in question 8), but for 18 months instead of6 months.

a. Use the spreadsheet to work out how much would she pay in interest over the 18 monthperiod, remembering that the interest is based on the declining balance. What is theeffective monthly interest rate?

b. If interest were based on the original loan amount, how much would she pay in interest overthe 18 month period? What is the effective monthly interest rate?

10. What happens to the costs of the loans (both on a declining balance and on the original loanamount) and to the effective interest rates when the loan term is increased? Can you explainthese changes?

B. Setting Interest Rates

1. What three types of costs should a lending institution try to cover with its income from interestand fees? Explain each type and give examples of the costs within each category.

ACCION – with editing by RFLC 4

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 27/34

Interest rates and self sufficiency

2. How can a lending institution maintain the value of its portfolio in a country where inflation is22 % per year?

3. How does inflation affect an institution's portfolio? What is the effect on the portion of theportfolio that is borrowed from a bank? What is the effect on the portion of the portfolio that isthe institution's own resources?

4. Which package of loans below (A or B) generates more income for a lending institution in one 12month period, and why? For both A and B assume that funds are lent out again as soon as theyhave been repaid, thereby never remaining idle, and that on-time repayment is 100%.

A B

Outstanding Portfolio $10,000 $10,000

Loan Terms 3 months 12 months

Average Loan Size $100 $1000

Fees or commissions None NoneMonthly interest rate 2 % (declining balance) 2 % (declining balance)

ACCION – with editing by RFLC 5

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 28/34

Interest rates and self sufficiency

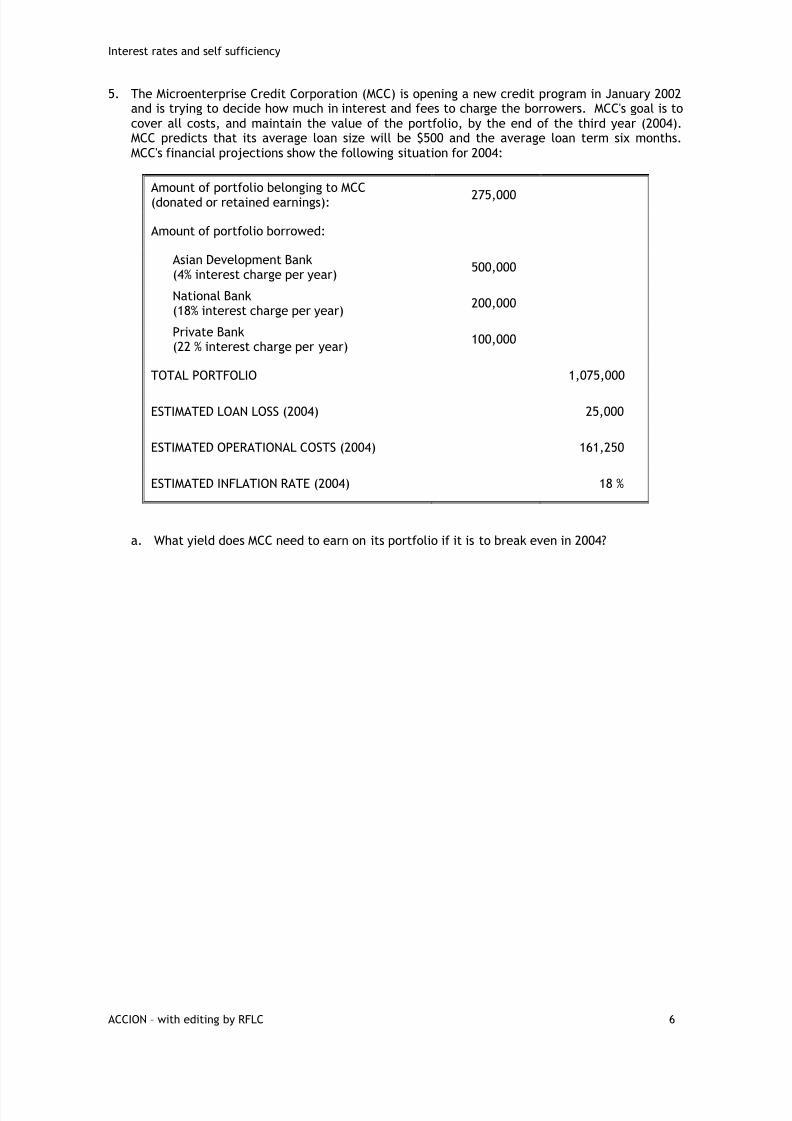

5. The Microenterprise Credit Corporation (MCC) is opening a new credit program in January 2002and is trying to decide how much in interest and fees to charge the borrowers. MCC's goal is tocover all costs, and maintain the value of the portfolio, by the end of the third year (2004).MCC predicts that its average loan size will be $500 and the average loan term six months.MCC's financial projections show the following situation for 2004:

Amount of portfolio belonging to MCC(donated or retained earnings):

275,000

Amount of portfolio borrowed:

Asian Development Bank(4% interest charge per year)

500,000

National Bank(18% interest charge per year)

200,000

Private Bank(22 % interest charge per year)

100,000

TOTAL PORTFOLIO 1,075,000

ESTIMATED LOAN LOSS (2004) 25,000

ESTIMATED OPERATIONAL COSTS (2004) 161,250

ESTIMATED INFLATION RATE (2004) 18 %

a. What yield does MCC need to earn on its portfolio if it is to break even in 2004?

ACCION – with editing by RFLC 6

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 29/34

Interest rates and self sufficiency

b. Assume that all borrowers pay on time, and that the entire portfolio is always lent out.How could the program charge a nominal rate equal to the nominal rate of commercialbanks (22%) and still break even?

c. Instead of charging any fees, MCC in 2004 charges 30% interest on a declining balance on allloans. MCC shows the following results for the year:

• No interest is earned on the 2.3 % of the portfolio which is to be written off at theend of the year;

• 12% of the portfolio does not generate any interest income during 2004 because of

delinquency.• Costs are the same as projected.• All $1,075,000 is lent out to borrowers for the whole year.• How much is MCC's deficit in 2004?

d. Assume that all of the conditions set out in c above are true, except the last one. Instead,MCC has an average of 10% of its portfolio on short-term deposit earning 20% during 2004,while the rest is always m the hands of borrowers. How much is their deficit under theseconditions?

e. If MCC could have predicted the results described above, what could they have done todiminish or eliminate their deficit in 2004?

ACCION – with editing by RFLC 7

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 30/34

Interest Rates and Self-Sufficiency

SOLUTIONS

INTEREST RATE PROBLEMS

A. Nominal, Effective and Real Interest Rates

1. Approximate real interest rates are calculated by subtracting the inflation rate from theinterest rate. The precise formula is:

real interest rate = (1 + nominal interest rate) - 1(1 + inflation rate)

If a real interest rate is negative, it means that the interest charge is less than the inflationrate. Even if all of the interest paid is used to capitalize the portfolio, the portfolio will beworth less each year. As inflation increases, the real rate of interest becomes more negative.

2. Nominal interest rates are the rate of interest that the lender states the borrower will pay.They are used to calculate the amount of interest to be paid in each payment period: thenominal interest rate times the outstanding (declining) balance of the loan.

a. A dramatic increase in inflation does not change the nominal interest rate of a loan.Increasing inflation will decrease the real nominal interest rate.

b. An increase in the commission on a loan will not change the nominal interest rate of theloan.

3. Effective interest rates most accurately reflect the actual costs of a loan. They combine theeffects of the calculation method and the costs of interest, commissions and fees over theperiod of the loan, and interpret them into one rate.

a. Effective rates do not change with inflation. The real effective rate of interest will vary withinflation.

b. An increased commission will result in a higher effective rate of interest on a loan.

4. Borrowers have to pay transaction costs for loans. They include transportation to the lendinginstitution, fees for the preparation of documents in order to qualify for the loan, and even theborrower's own time that would otherwise be used generating income. Transaction costs alsoinclude costs incurred because of inefficiencies in the lender's delivery system, such as extratrips to the lender because the lender misplaced a document, or a missed opportunity to buyraw materials at a special low price because the loan is delayed.

5. Transaction costs are paid by the borrower, but not to the lender. Financial costs are paiddirectly to the lender. To the greatest extent possible, lenders should try to minimize thetransaction portion of the total borrowing costs that their borrowers must pay.

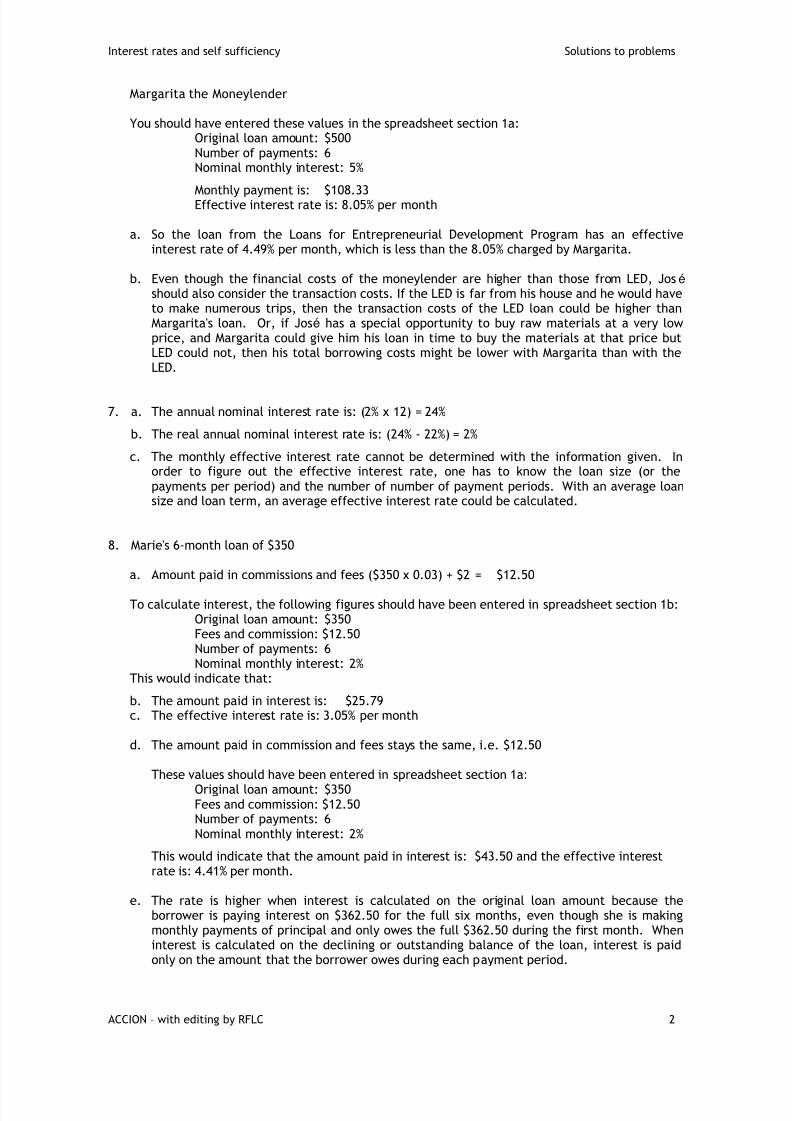

6. José’s loan - financial costs of each alternative:

Loans for Entrepreneurial Development Program

You should have entered these values in the spreadsheet section 1b:Original loan amount: $500Fees and commission: $10 + ($500 x .03) = $25Number of payments: 6Nominal monthly interest: 3%

Monthly payment is: $96.91Effective interest rate is: 4.49% per month

ACCION – with editing by RFLC 1

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 31/34

Interest rates and self sufficiency Solutions to problems

Margarita the Moneylender

You should have entered these values in the spreadsheet section 1a:Original loan amount: $500Number of payments: 6Nominal monthly interest: 5%

Monthly payment is: $108.33Effective interest rate is: 8.05% per month

a. So the loan from the Loans for Entrepreneurial Development Program has an effectiveinterest rate of 4.49% per month, which is less than the 8.05% charged by Margarita.

b. Even though the financial costs of the moneylender are higher than those from LED, José should also consider the transaction costs. If the LED is far from his house and he would haveto make numerous trips, then the transaction costs of the LED loan could be higher thanMargarita's loan. Or, if José has a special opportunity to buy raw materials at a very lowprice, and Margarita could give him his loan in time to buy the materials at that price butLED could not, then his total borrowing costs might be lower with Margarita than with theLED.

7. a. The annual nominal interest rate is: (2% x 12) = 24%

b. The real annual nominal interest rate is: (24% - 22%) = 2%

c. The monthly effective interest rate cannot be determined with the information given. Inorder to figure out the effective interest rate, one has to know the loan size (or thepayments per period) and the number of number of payment periods. With an average loansize and loan term, an average effective interest rate could be calculated.

8. Marie's 6-month loan of $350

a. Amount paid in commissions and fees ($350 x 0.03) + $2 = $12.50

To calculate interest, the following figures should have been entered in spreadsheet section 1b:Original loan amount: $350Fees and commission: $12.50Number of payments: 6Nominal monthly interest: 2%

This would indicate that:

b. The amount paid in interest is: $25.79c. The effective interest rate is: 3.05% per month

d. The amount paid in commission and fees stays the same, i.e. $12.50

These values should have been entered in spreadsheet section 1a:Original loan amount: $350Fees and commission: $12.50Number of payments: 6Nominal monthly interest: 2%

This would indicate that the amount paid in interest is: $43.50 and the effective interestrate is: 4.41% per month.

e. The rate is higher when interest is calculated on the original loan amount because theborrower is paying interest on $362.50 for the full six months, even though she is makingmonthly payments of principal and only owes the full $362.50 during the first month. When

interest is calculated on the declining or outstanding balance of the loan, interest is paidonly on the amount that the borrower owes during each payment period.

ACCION – with editing by RFLC 2

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 32/34

Interest rates and self sufficiency Solutions to problems

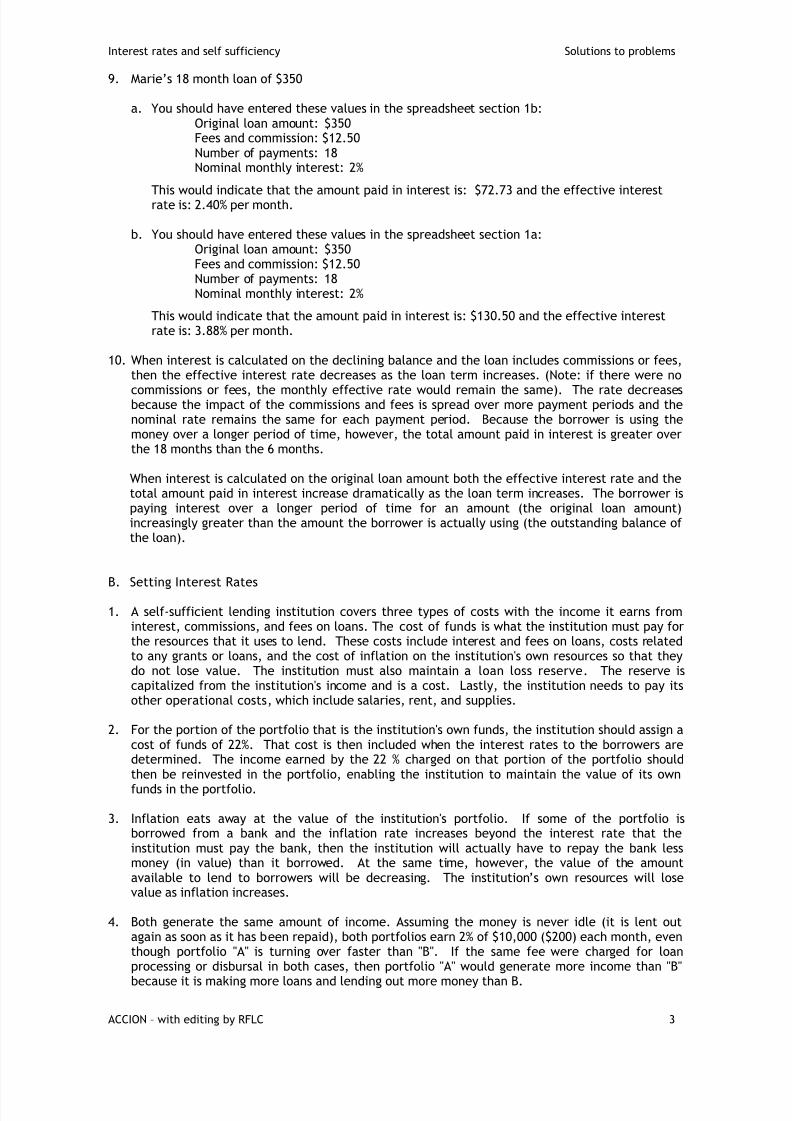

9. Marie’s 18 month loan of $350

a. You should have entered these values in the spreadsheet section 1b:Original loan amount: $350Fees and commission: $12.50Number of payments: 18Nominal monthly interest: 2%

This would indicate that the amount paid in interest is: $72.73 and the effective interestrate is: 2.40% per month.

b. You should have entered these values in the spreadsheet section 1a:Original loan amount: $350Fees and commission: $12.50Number of payments: 18Nominal monthly interest: 2%

This would indicate that the amount paid in interest is: $130.50 and the effective interestrate is: 3.88% per month.

10. When interest is calculated on the declining balance and the loan includes commissions or fees,

then the effective interest rate decreases as the loan term increases. (Note: if there were nocommissions or fees, the monthly effective rate would remain the same). The rate decreasesbecause the impact of the commissions and fees is spread over more payment periods and thenominal rate remains the same for each payment period. Because the borrower is using themoney over a longer period of time, however, the total amount paid in interest is greater overthe 18 months than the 6 months.

When interest is calculated on the original loan amount both the effective interest rate and thetotal amount paid in interest increase dramatically as the loan term increases. The borrower ispaying interest over a longer period of time for an amount (the original loan amount)increasingly greater than the amount the borrower is actually using (the outstanding balance ofthe loan).

B. Setting Interest Rates

1. A self-sufficient lending institution covers three types of costs with the income it earns frominterest, commissions, and fees on loans. The cost of funds is what the institution must pay forthe resources that it uses to lend. These costs include interest and fees on loans, costs relatedto any grants or loans, and the cost of inflation on the institution's own resources so that theydo not lose value. The institution must also maintain a loan loss reserve. The reserve iscapitalized from the institution's income and is a cost. Lastly, the institution needs to pay itsother operational costs, which include salaries, rent, and supplies.

2. For the portion of the portfolio that is the institution's own funds, the institution should assign acost of funds of 22%. That cost is then included when the interest rates to the borrowers are

determined. The income earned by the 22 % charged on that portion of the portfolio shouldthen be reinvested in the portfolio, enabling the institution to maintain the value of its ownfunds in the portfolio.

3. Inflation eats away at the value of the institution's portfolio. If some of the portfolio isborrowed from a bank and the inflation rate increases beyond the interest rate that theinstitution must pay the bank, then the institution will actually have to repay the bank lessmoney (in value) than it borrowed. At the same time, however, the value of the amountavailable to lend to borrowers will be decreasing. The institution’s own resources will losevalue as inflation increases.

4. Both generate the same amount of income. Assuming the money is never idle (it is lent outagain as soon as it has been repaid), both portfolios earn 2% of $10,000 ($200) each month, eventhough portfolio "A" is turning over faster than "B". If the same fee were charged for loanprocessing or disbursal in both cases, then portfolio "A" would generate more income than "B"because it is making more loans and lending out more money than B.

ACCION – with editing by RFLC 3

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 33/34

Interest rates and self sufficiency Solutions to problems

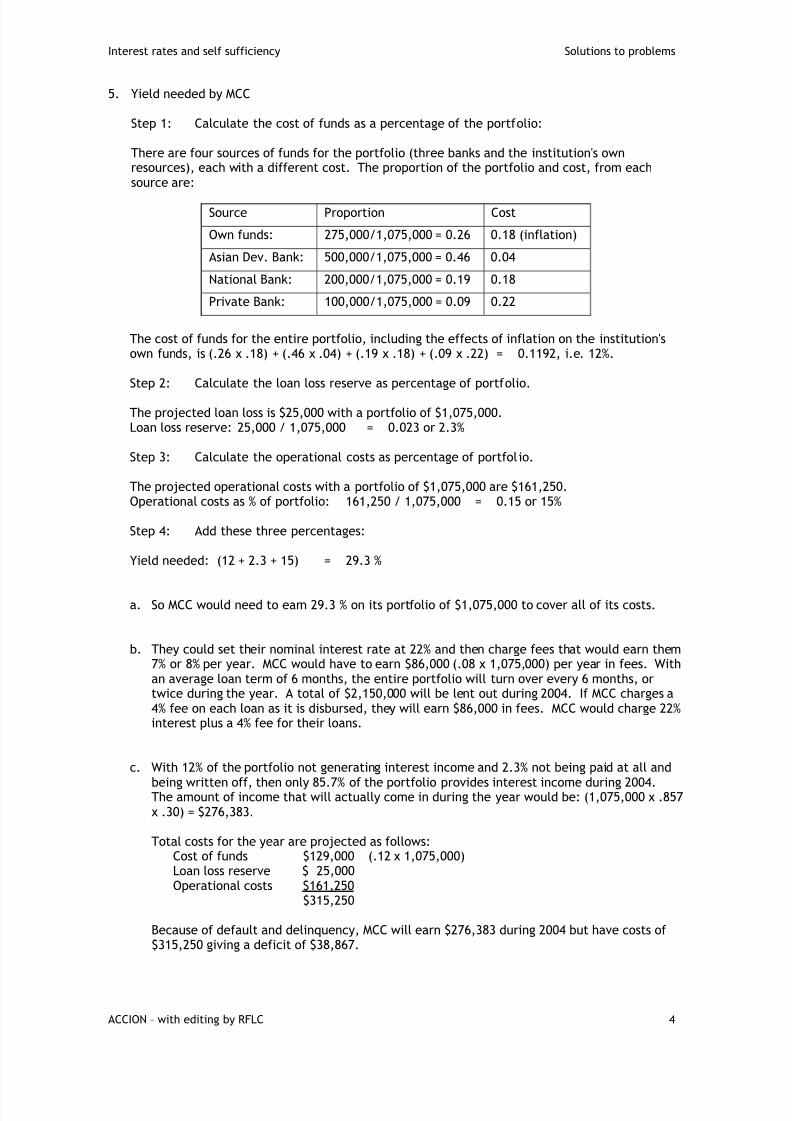

5. Yield needed by MCC

Step 1: Calculate the cost of funds as a percentage of the portfolio:

There are four sources of funds for the portfolio (three banks and the institution's ownresources), each with a different cost. The proportion of the portfolio and cost, from each

source are:

Source Proportion Cost

Own funds: 275,000/1,075,000 = 0.26 0.18 (inflation)

Asian Dev. Bank: 500,000/1,075,000 = 0.46 0.04

National Bank: 200,000/1,075,000 = 0.19 0.18

Private Bank: 100,000/1,075,000 = 0.09 0.22

The cost of funds for the entire portfolio, including the effects of inflation on the institution'sown funds, is (.26 x .18) + (.46 x .04) + (.19 x .18) + (.09 x .22) = 0.1192, i.e. 12%.

Step 2: Calculate the loan loss reserve as percentage of portfolio.

The projected loan loss is $25,000 with a portfolio of $1,075,000.Loan loss reserve: 25,000 / 1,075,000 = 0.023 or 2.3%

Step 3: Calculate the operational costs as percentage of portfolio.

The projected operational costs with a portfolio of $1,075,000 are $161,250.Operational costs as % of portfolio: 161,250 / 1,075,000 = 0.15 or 15%

Step 4: Add these three percentages:

Yield needed: (12 + 2.3 + 15) = 29.3 %

a. So MCC would need to earn 29.3 % on its portfolio of $1,075,000 to cover all of its costs.

b. They could set their nominal interest rate at 22% and then charge fees that would earn them7% or 8% per year. MCC would have to earn $86,000 (.08 x 1,075,000) per year in fees. Withan average loan term of 6 months, the entire portfolio will turn over every 6 months, ortwice during the year. A total of $2,150,000 will be lent out during 2004. If MCC charges a4% fee on each loan as it is disbursed, they will earn $86,000 in fees. MCC would charge 22%interest plus a 4% fee for their loans.

c. With 12% of the portfolio not generating interest income and 2.3% not being paid at all andbeing written off, then only 85.7% of the portfolio provides interest income during 2004.The amount of income that will actually come in during the year would be: (1,075,000 x .857x .30) = $276,383.

Total costs for the year are projected as follows:Cost of funds $129,000 (.12 x 1,075,000)Loan loss reserve $ 25,000Operational costs $161,250

$315,250

Because of default and delinquency, MCC will earn $276,383 during 2004 but have costs of

$315,250 giving a deficit of $38,867.

ACCION – with editing by RFLC 4

8/6/2019 1133308092351 Lesson 1 Interest Rates Merged

http://slidepdf.com/reader/full/1133308092351-lesson-1-interest-rates-merged 34/34

Interest rates and self sufficiency Solutions to problems

d. In this case, 10% of the portfolio ($107,500) earns 20%, 14.3% of the portfolio ($153,725)earns zero because of delinquency and 75.7% ($813,775) earns the full 30%.

Total income is:(107,500 x .20) + (153,725 x 0) + (813,775 x .30) = $265,633

Total costs are the same as in question c. $315,250, so MCC's deficit would be $49,617.

e. To reduce the deficit, MCC could have implemented any combination of the followingstrategies:

lowered its costs prevented such high levels of delinquency and default increased its interest rate added a fee on all loans charged a penalty fee for late payments

In other words, they needed to find a way to increase their income or decrease their costs.