Embed Size (px)

Citation preview

12-1

Activity-Activity-Based Based

CostingCosting

Prepared by Douglas Cloud

Pepperdine University

Prepared by Douglas Cloud

Pepperdine University

12-2

1. Discuss the limitations of using only unit-based drivers to assign costs.

2. Provide a detailed description of activity-based product costing.

3. Explain how homogenous cost pools can be used to reduce the number of activity rates.

4. Describe activity-based system concepts including an ABC relational database and ABC software.

ObjectivesObjectivesObjectivesObjectives

After studying this After studying this chapter, you should chapter, you should

be able to:be able to:

After studying this After studying this chapter, you should chapter, you should

be able to:be able to:

12-3

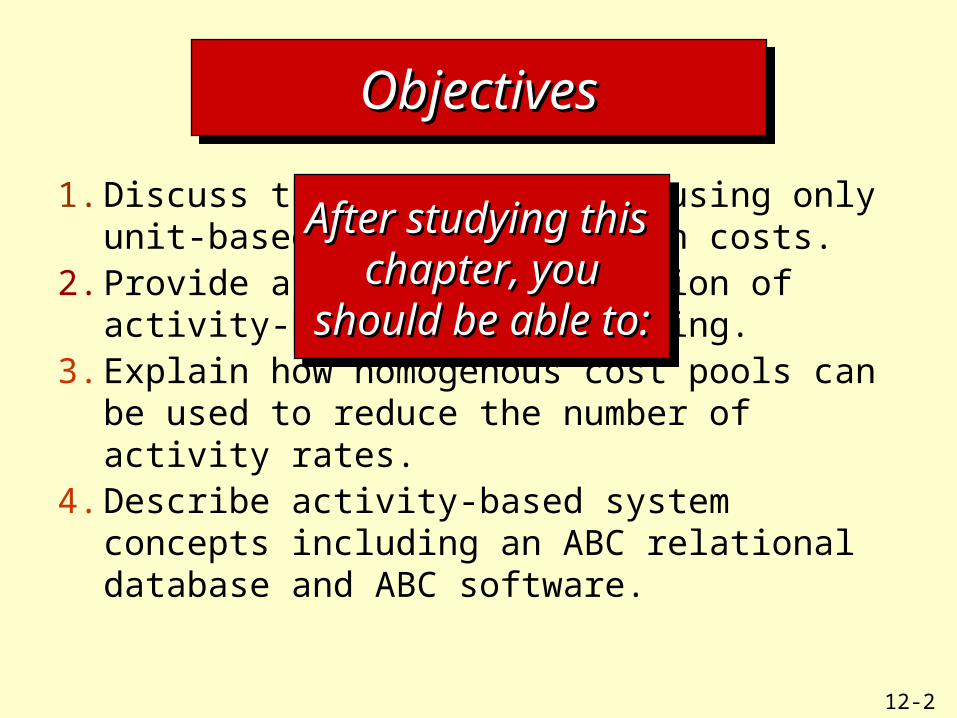

Functional-Based ProductCosting Model

Direct Direct MaterialsMaterials

Direct Direct LaborLabor

OverheadOverhead

PRODUCTSPRODUCTS

Direct Tracing

Direct Tracing

Plant/Departmental Plant/Departmental Cost PoolsCost Pools

Direct Tracing Driver Tracing Allocation

Unit-Based Driver

12-4

Goodmark Company—An ExampleGoodmark Company—An Example

Goodmark Company produces two products: scented and regular birthday cards.

12-5

Goodmark Company—An ExampleGoodmark Company—An Example

Scented Cards Regular Cards TotalScented Cards Regular Cards Total

Unit produced per year 20,000 200,000 --Prime costs $160,000 $1,500,000 $1,660,000Direct labor hours 20,000 160,000 180,000Number of setups 60 40 100Machine hours 10,000 80,000 90,000Inspection hours 2,000 16,000 18,000Number of moves 180 120 300

Product Costing DataProduct Costing Data

12-6

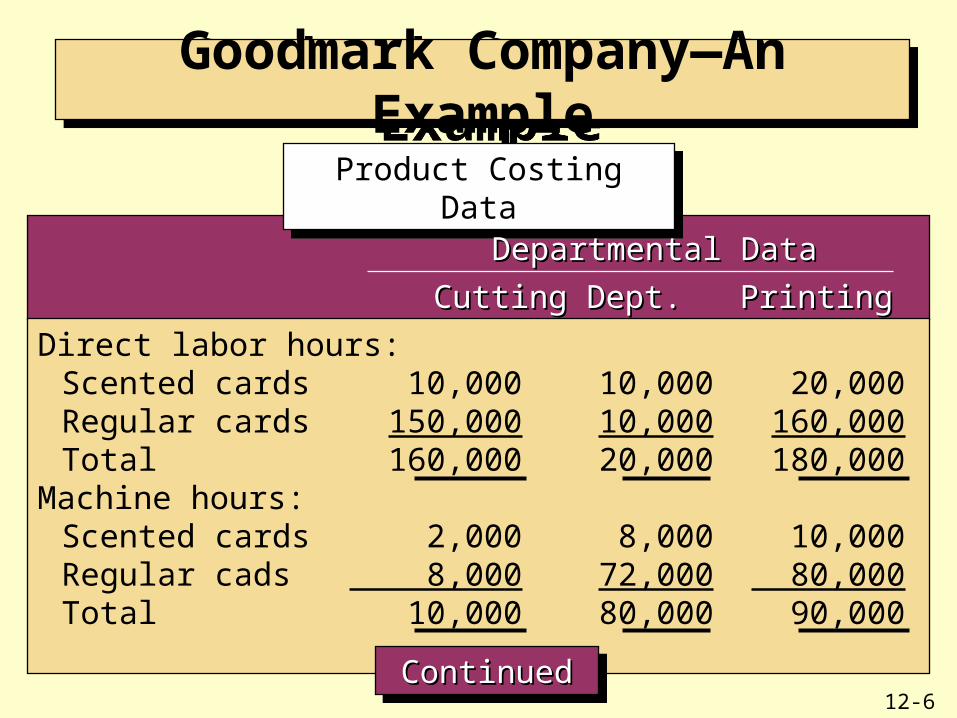

Goodmark Company—An ExampleGoodmark Company—An Example

Cutting Dept. Printing Dept. TotalCutting Dept. Printing Dept. Total

Direct labor hours:Scented cards 10,000 10,000 20,000Regular cards 150,000 10,000 160,000Total 160,000 20,000 180,000

Machine hours:Scented cards 2,000 8,000 10,000Regular cads 8,000 72,000 80,000Total 10,000 80,000 90,000

Product Costing DataProduct Costing Data

Departmental DataDepartmental Data

ContinuedContinuedContinuedContinued

12-7

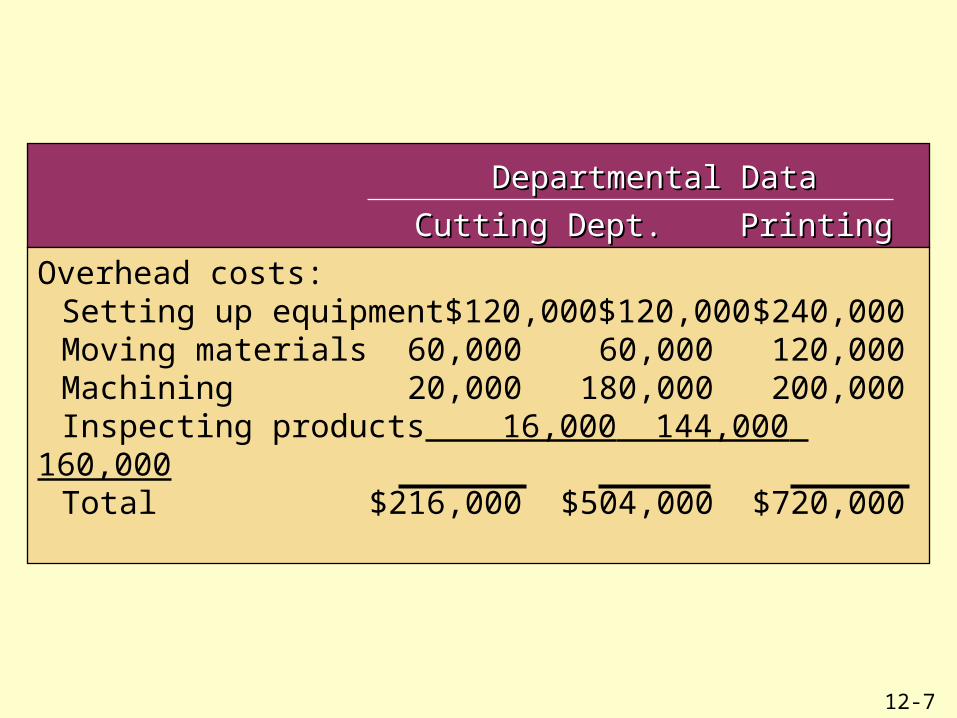

Cutting Dept. Printing Dept. TotalCutting Dept. Printing Dept. Total

Overhead costs:Setting up equipment $120,000 $120,000 $240,000Moving materials 60,000 60,000 120,000Machining 20,000 180,000 200,000Inspecting products 16,000 144,000 160,000Total $216,000 $504,000 $720,000

Departmental DataDepartmental Data

12-8

Goodmark Company—An ExampleGoodmark Company—An Example

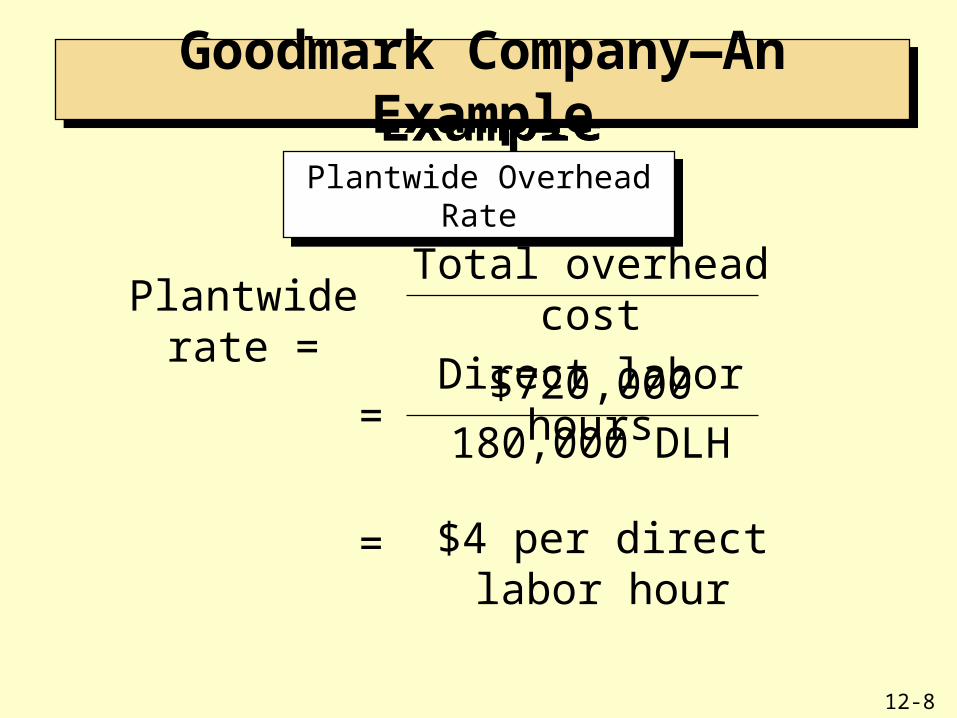

Plantwide Overhead RatePlantwide Overhead Rate

Plantwide rate =Total overhead cost

Direct labor hours

=$720,000

180,000 DLH

= $4 per direct labor hour

12-9

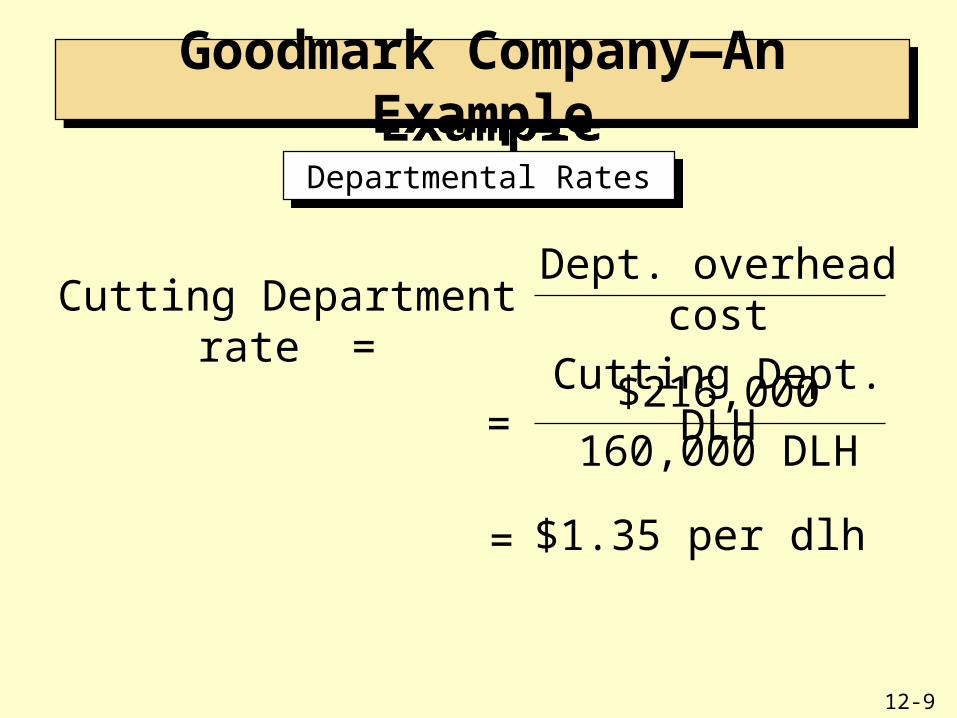

Goodmark Company—An ExampleGoodmark Company—An Example

Departmental RatesDepartmental Rates

Cutting Department rate =Dept. overhead cost

Cutting Dept. DLH

=$216,000

160,000 DLH

= $1.35 per dlh

12-10

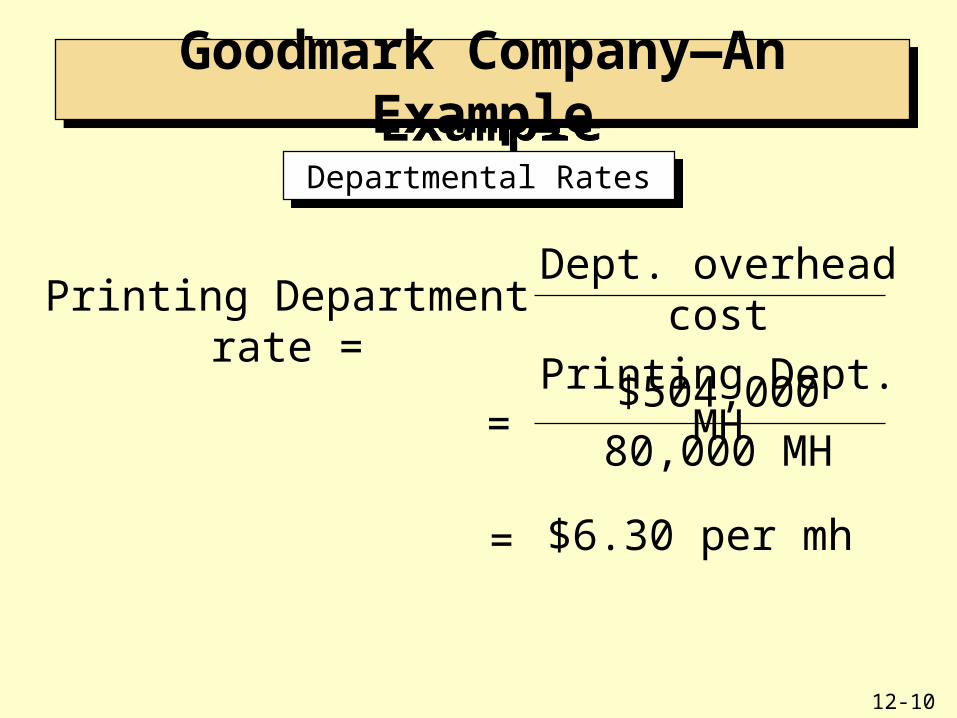

Goodmark Company—An ExampleGoodmark Company—An Example

Departmental RatesDepartmental Rates

Printing Department rate =Dept. overhead cost

Printing Dept. MH

=$504,000

80,000 MH

= $6.30 per mh

12-11

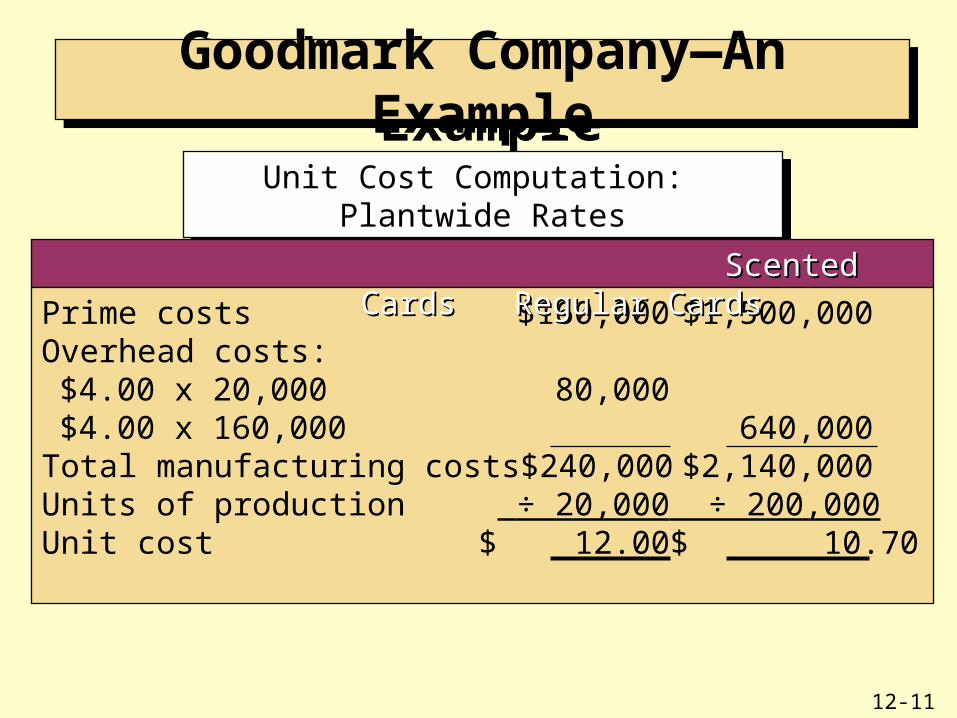

Goodmark Company—An ExampleGoodmark Company—An Example

Unit Cost Computation: Plantwide RatesUnit Cost Computation: Plantwide Rates

Prime costs $160,000 $1,500,000Overhead costs:

$4.00 x 20,000 80,000$4.00 x 160,000 640,000

Total manufacturing costs $240,000 $2,140,000Units of production ÷ 20,000 ÷ 200,000Unit cost $ 12.00 $ 10.70

Scented Cards Regular CardsScented Cards Regular Cards

12-12

Goodmark Company—An ExampleGoodmark Company—An Example

Unit Cost Computation: Departmental RatesUnit Cost Computation: Departmental Rates

Scented Cards Regular CardsScented Cards Regular Cards

Prime costs $160,000 $1,500,000Overhead costs:

[($1.35 x 10,000) + ($6.30 x 8,000)] 63,900[($2.35 x 150,000) + ($6.30 x 72,000)] 656,100

Total manufacturing costs $223,900 $2,156,100Units of production ÷ 20,000 ÷ 200,000Unit cost $ 11.20 $ 10.78*

*Rounded to nearest cent

*

12-13

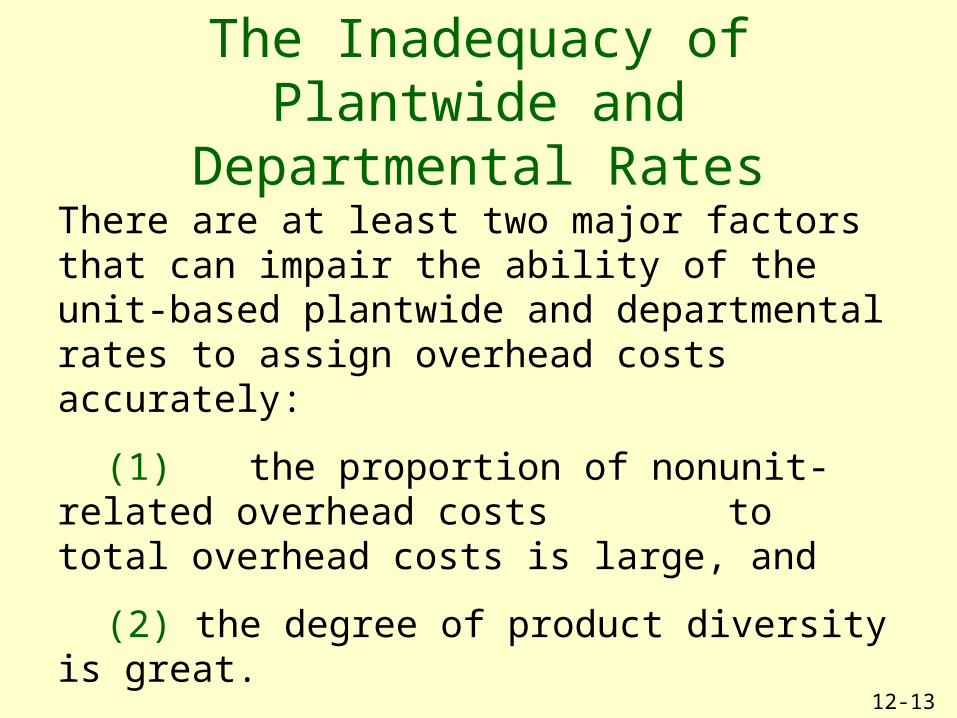

The Inadequacy of Plantwide and Departmental Rates

There are at least two major factors that can impair the ability of the unit-based plantwide and departmental rates to assign overhead costs accurately:

(1) the proportion of nonunit-related overhead costs to total overhead costs is large, and

(2) the degree of product diversity is great.

12-14

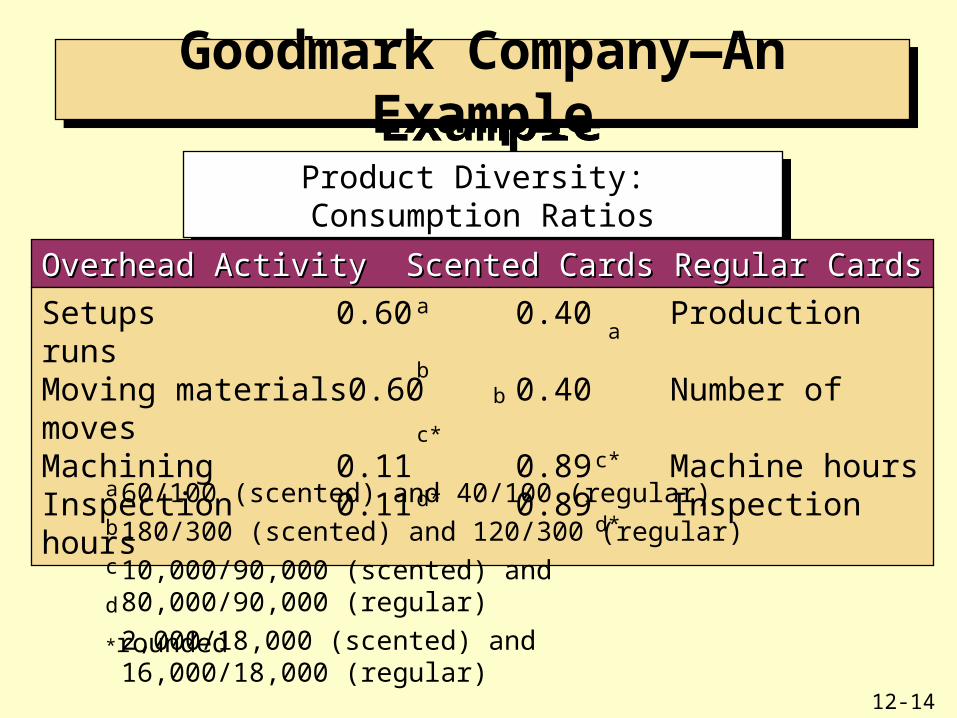

Goodmark Company—An ExampleGoodmark Company—An Example

Product Diversity: Consumption RatiosProduct Diversity: Consumption Ratios

Overhead Activity Scented Cards Regular Cards Activity DriversOverhead Activity Scented Cards Regular Cards Activity Drivers

Setups 0.60 0.40 Production runsMoving materials 0.60 0.40 Number of movesMachining 0.11 0.89 Machine hoursInspection 0.11 0.89 Inspection hours

a a

b b

c* c*

d* d*

a

b

c

d

60/100 (scented) and 40/100 (regular)

180/300 (scented) and 120/300 (regular)

10,000/90,000 (scented) and 80,000/90,000 (regular)

2,000/18,000 (scented) and 16,000/18,000 (regular)*rounded

12-15

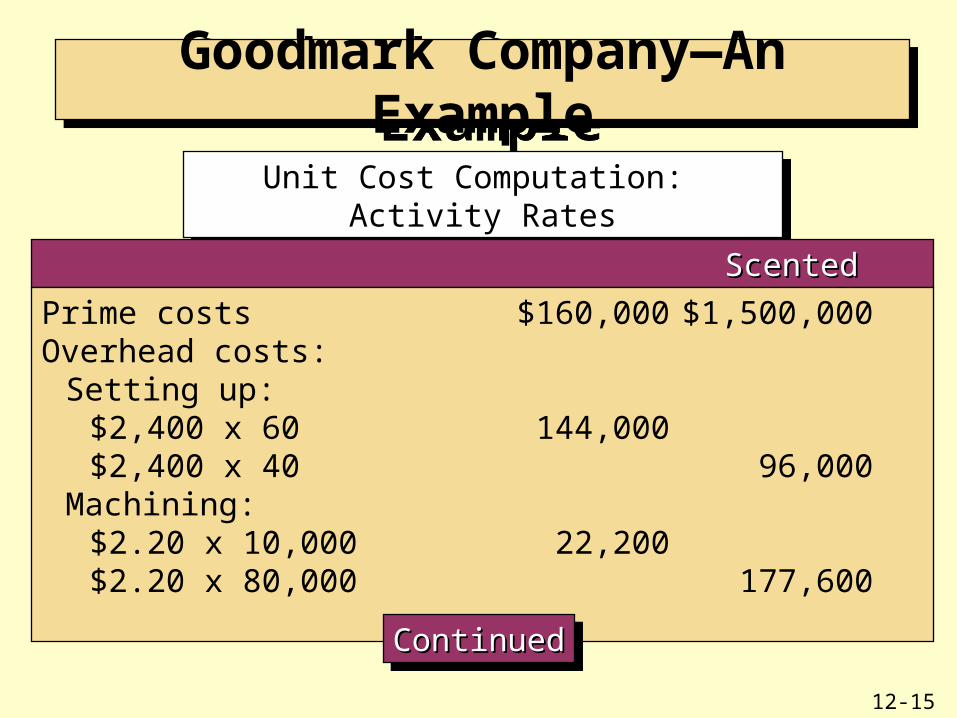

Goodmark Company—An ExampleGoodmark Company—An Example

Unit Cost Computation: Activity RatesUnit Cost Computation: Activity Rates

Scented Cards Regular CardsScented Cards Regular Cards

Prime costs $160,000 $1,500,000Overhead costs:

Setting up:$2,400 x 60 144,000$2,400 x 40 96,000

Machining:$2.20 x 10,000 22,200$2.20 x 80,000 177,600

ContinuedContinuedContinuedContinued

12-16

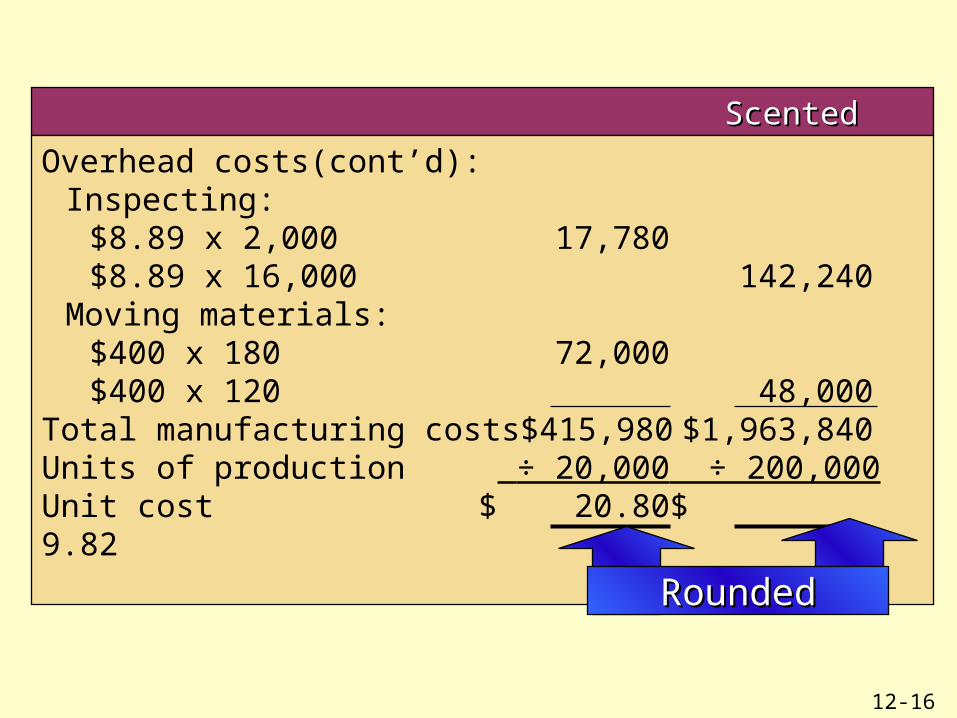

Scented Cards Regular CardsScented Cards Regular Cards

Overhead costs(cont’d):Inspecting:

$8.89 x 2,000 17,780$8.89 x 16,000 142,240

Moving materials:$400 x 180 72,000$400 x 120 48,000

Total manufacturing costs $415,980 $1,963,840Units of production ÷ 20,000 ÷ 200,000Unit cost $ 20.80 $ 9.82

RoundedRounded

12-17

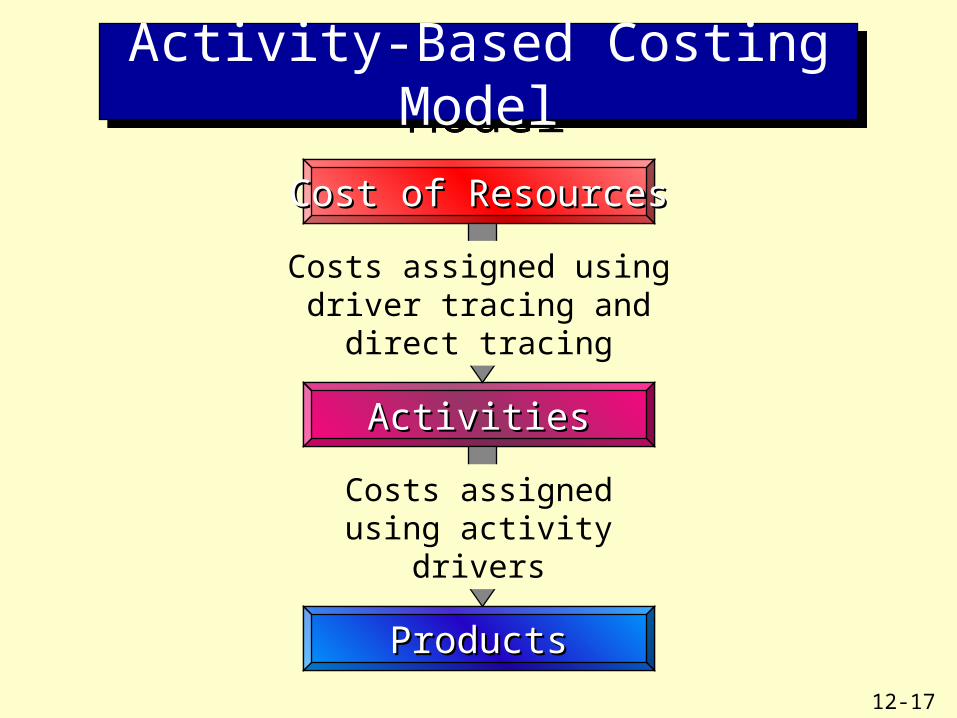

Activity-Based Costing ModelActivity-Based Costing Model

Cost of ResourcesCost of Resources

ActivitiesActivities

Costs assigned using driver tracing and direct tracing

ProductsProducts

Costs assigned using activity drivers

12-18

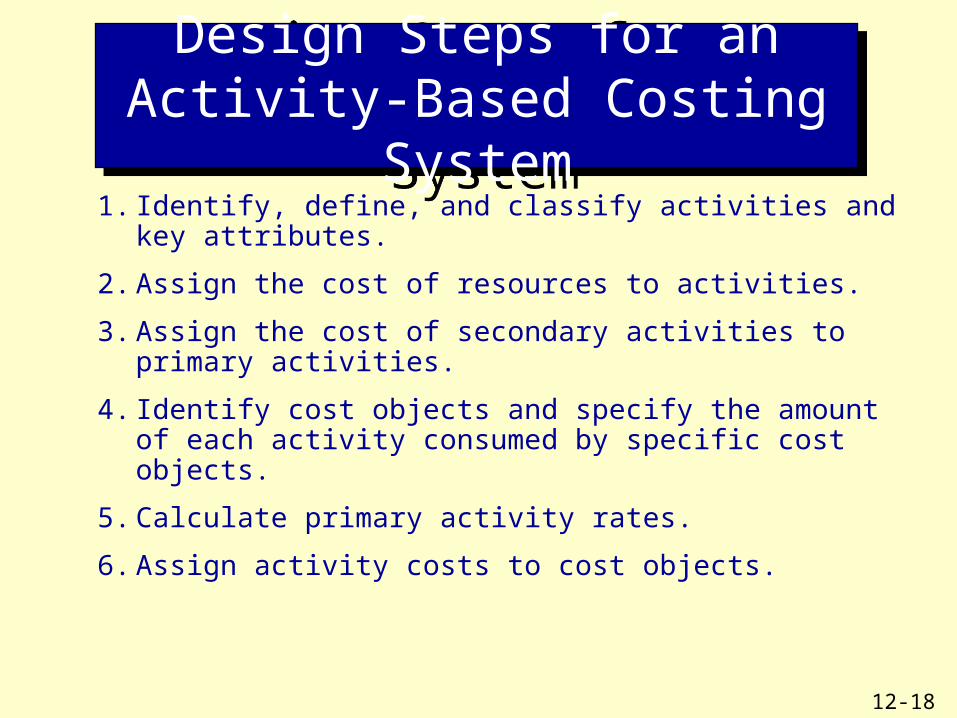

1. Identify, define, and classify activities and key attributes.

2. Assign the cost of resources to activities.

3. Assign the cost of secondary activities to primary activities.

4. Identify cost objects and specify the amount of each activity consumed by specific cost objects.

5. Calculate primary activity rates.

6. Assign activity costs to cost objects.

Design Steps for an Activity-Based Costing System

Design Steps for an Activity-Based Costing System

12-19

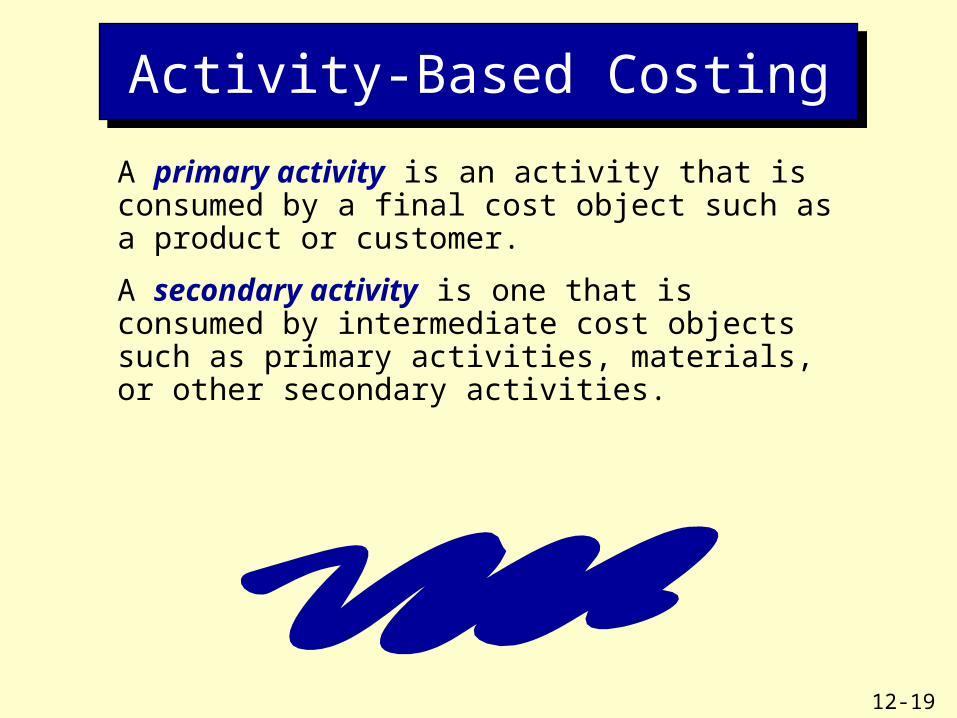

A primary activity is an activity that is consumed by a final cost object such as a product or customer.

A secondary activity is one that is consumed by intermediate cost objects such as primary activities, materials, or other secondary activities.

Activity-Based CostingActivity-Based Costing

12-20

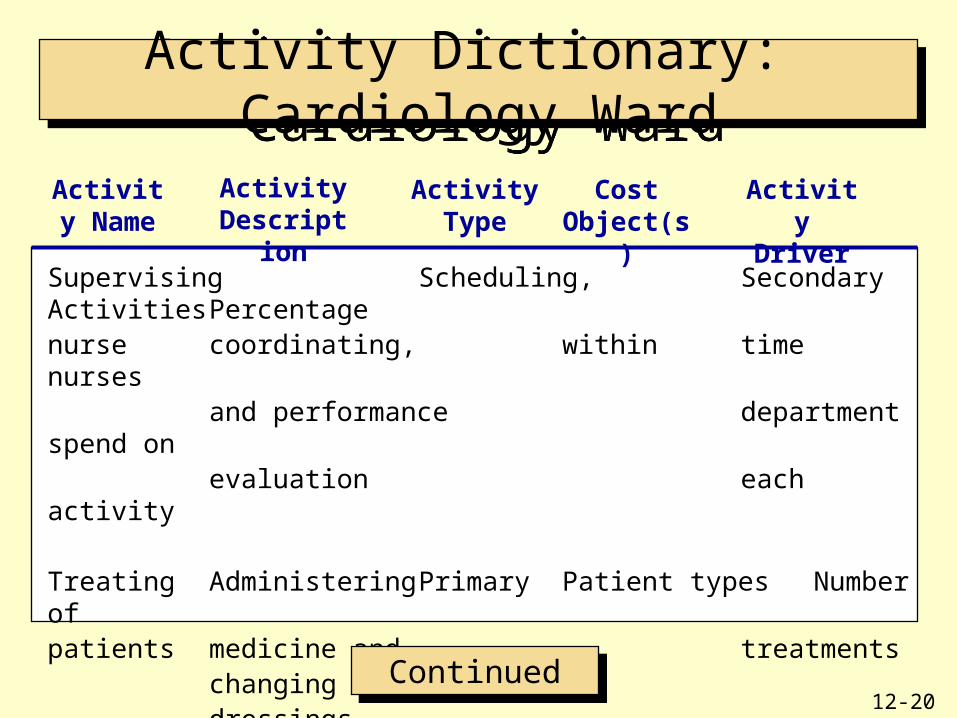

Activity Dictionary: Cardiology WardActivity Dictionary: Cardiology Ward

Supervising Scheduling, Secondary Activities Percentagenurse coordinating, within time nurses

and performance department spend onevaluation each activity

Treating Administering Primary Patient types Number ofpatients medicine and treatments

changingdressings

Activity Name

Activity Description

Activity Type

Cost Object(s)

Activity Driver

ContinuedContinued

12-21

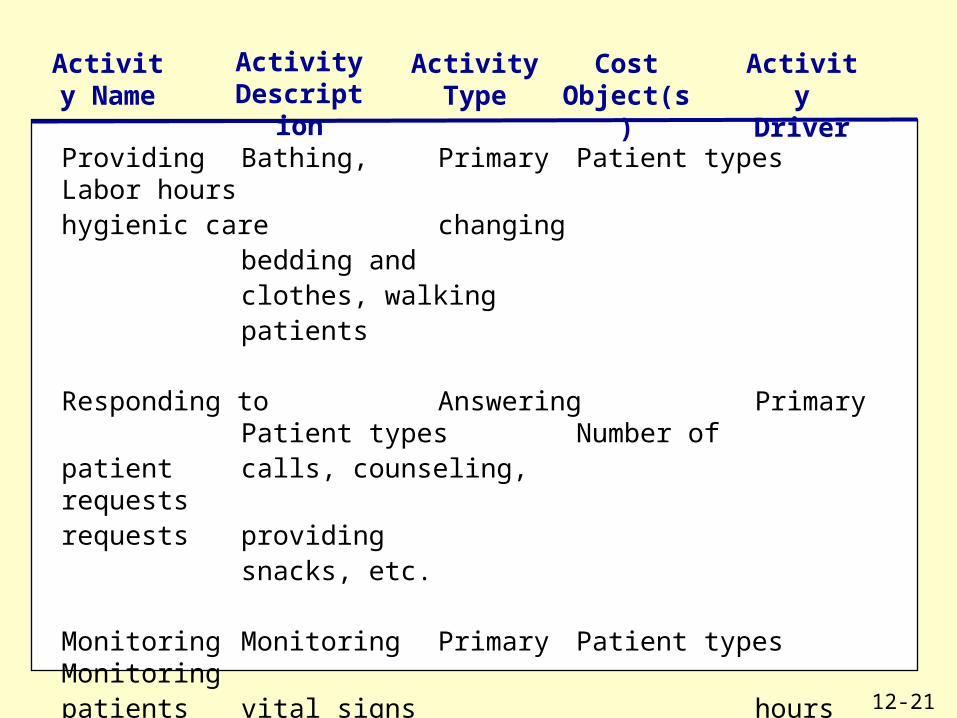

Activity Name

Activity Description

Activity Type

Cost Object(s)

Activity Driver

Providing Bathing, Primary Patient types Labor hourshygienic care changing

bedding andclothes, walkingpatients

Responding to Answering Primary Patient types Number ofpatient calls, counseling, requestsrequests providing

snacks, etc.

Monitoring Monitoring Primary Patient types Monitoringpatients vital signs hours

and postingpatient information

12-22

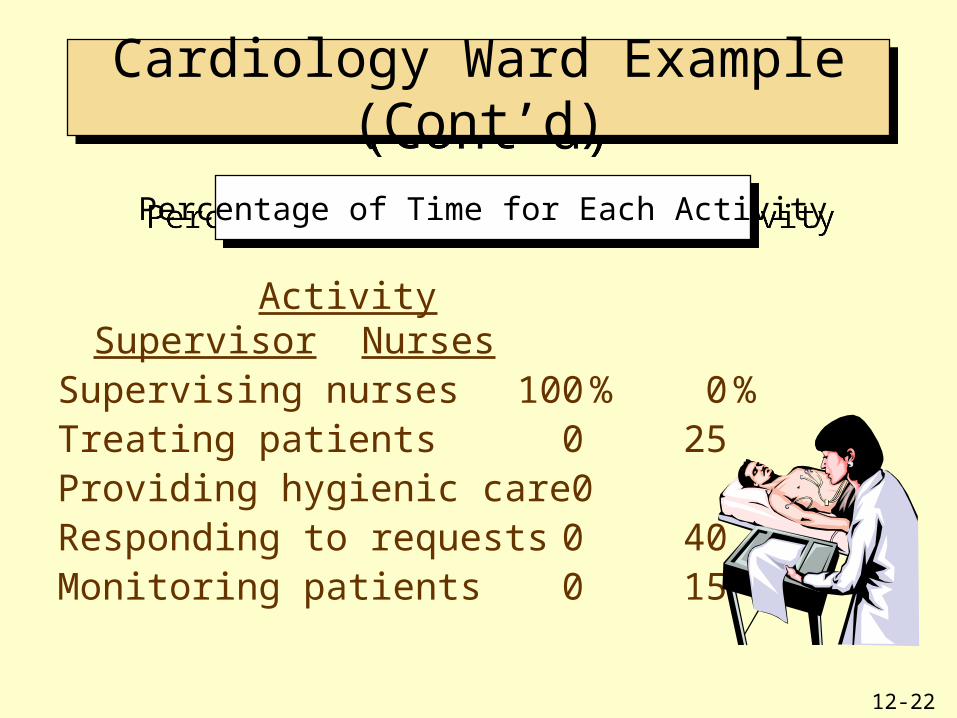

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

Activity Supervisor NursesSupervising nurses 100 % 0 %Treating patients 0 25Providing hygienic care 0 20Responding to requests 0 40Monitoring patients 0 15

Percentage of Time for Each ActivityPercentage of Time for Each Activity

12-23

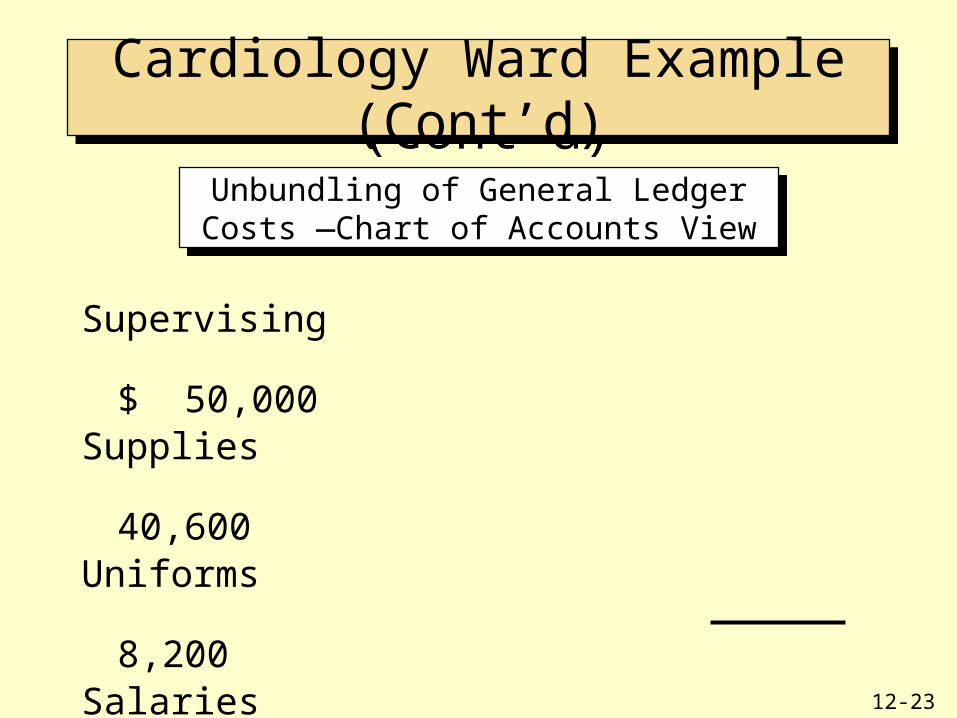

Unbundling of General Ledger Costs —Chart of Accounts View

Unbundling of General Ledger Costs —Chart of Accounts View

Supervising

$ 50,000Supplies

40,600Uniforms

8,200Salaries

300,000Computer

1,200Monitor

80,000 Total

$480,000

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

12-24

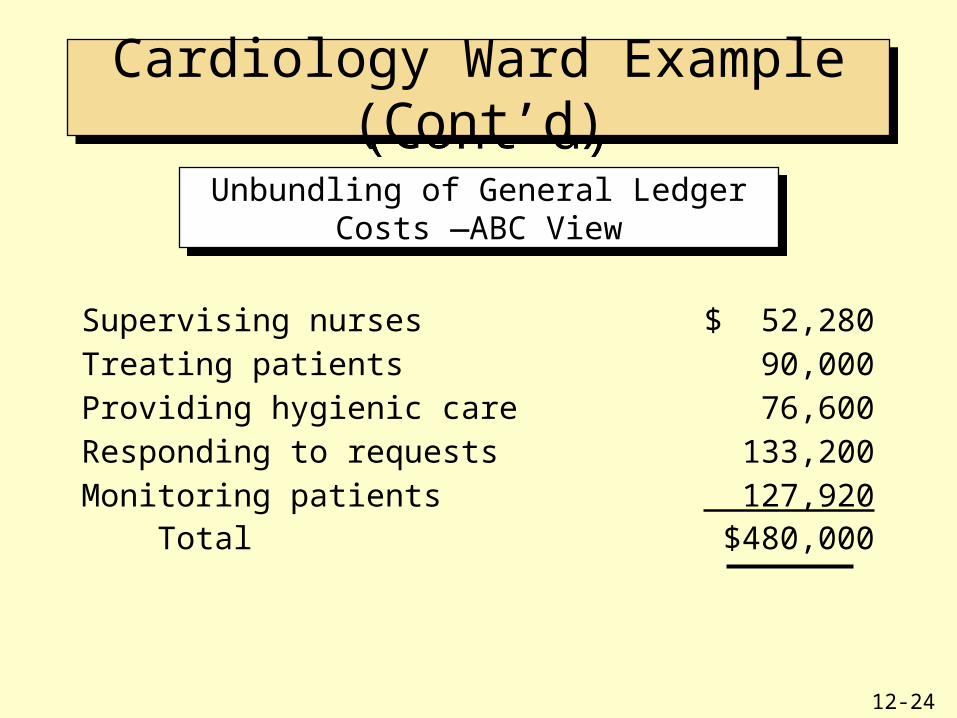

Unbundling of General Ledger Costs —ABC View

Unbundling of General Ledger Costs —ABC View

Supervising nurses $ 52,280

Treating patients 90,000

Providing hygienic care 76,600

Responding to requests 133,200

Monitoring patients 127,920 Total $480,000

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

12-25

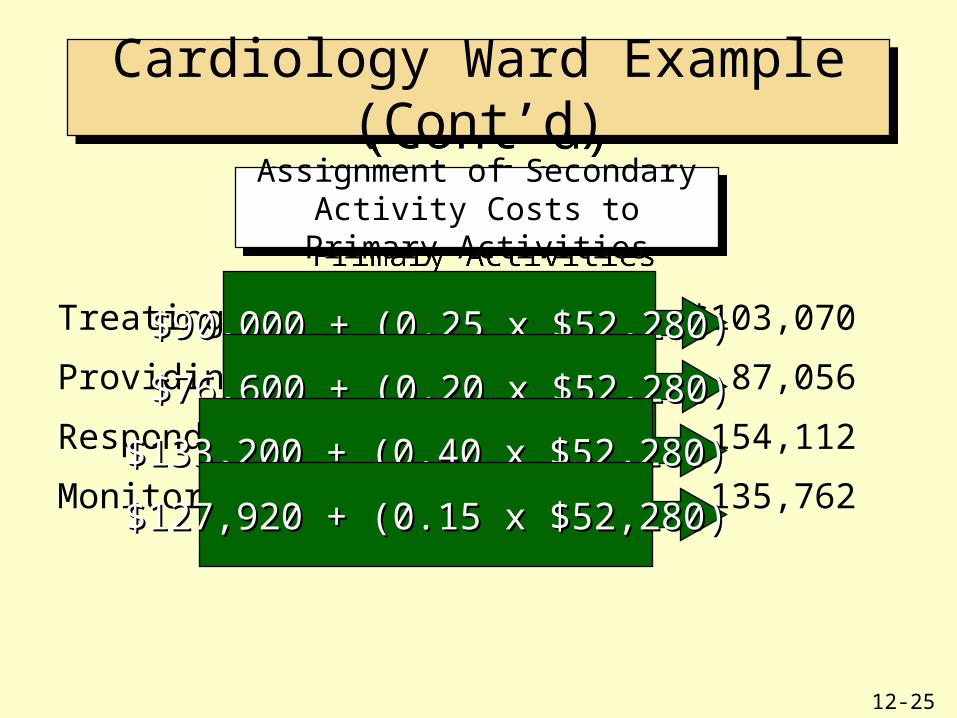

Treating patients $103,070

Providing hygienic care 87,056

Responding to requests 154,112

Monitoring patients 135,762

Assignment of Secondary Activity Costs to Primary Activities

Assignment of Secondary Activity Costs to Primary Activities

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

$90,000 + (0.25 x $52,280)$90,000 + (0.25 x $52,280)

$76,600 + (0.20 x $52,280)$76,600 + (0.20 x $52,280)

$133,200 + (0.40 x $52,280)$133,200 + (0.40 x $52,280)

$127,920 + (0.15 x $52,280)$127,920 + (0.15 x $52,280)

12-26

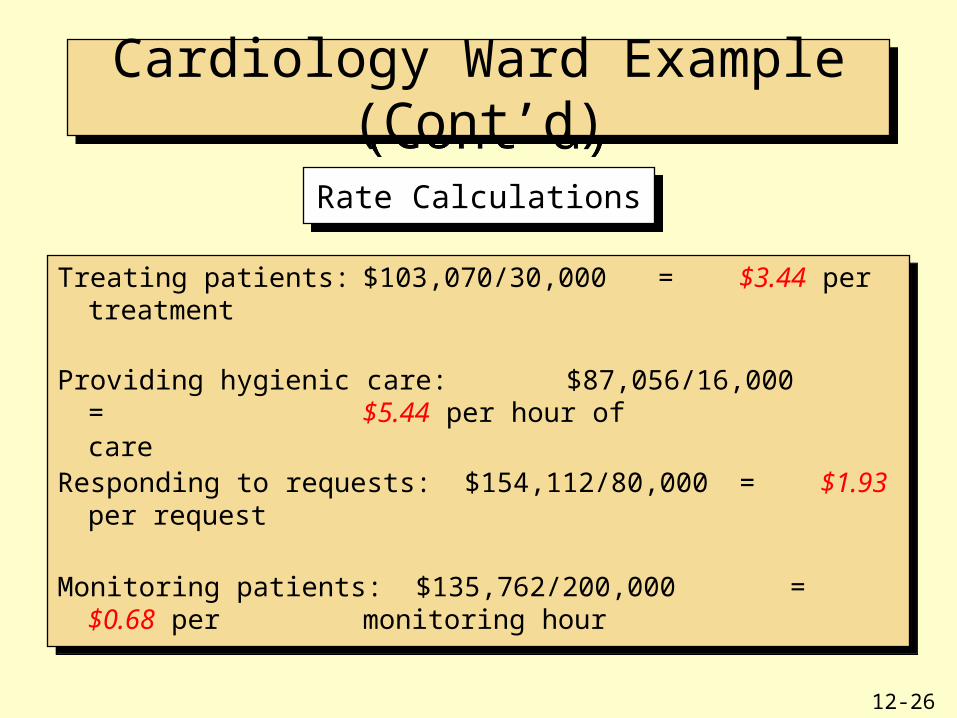

Treating patients: $103,070/30,000 = $3.44 per treatment

Providing hygienic care: $87,056/16,000 = $5.44 per hour ofcare

Responding to requests: $154,112/80,000 = $1.93 per request

Monitoring patients: $135,762/200,000 = $0.68 per monitoring hour

Treating patients: $103,070/30,000 = $3.44 per treatment

Providing hygienic care: $87,056/16,000 = $5.44 per hour ofcare

Responding to requests: $154,112/80,000 = $1.93 per request

Monitoring patients: $135,762/200,000 = $0.68 per monitoring hour

Rate CalculationsRate Calculations

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

12-27

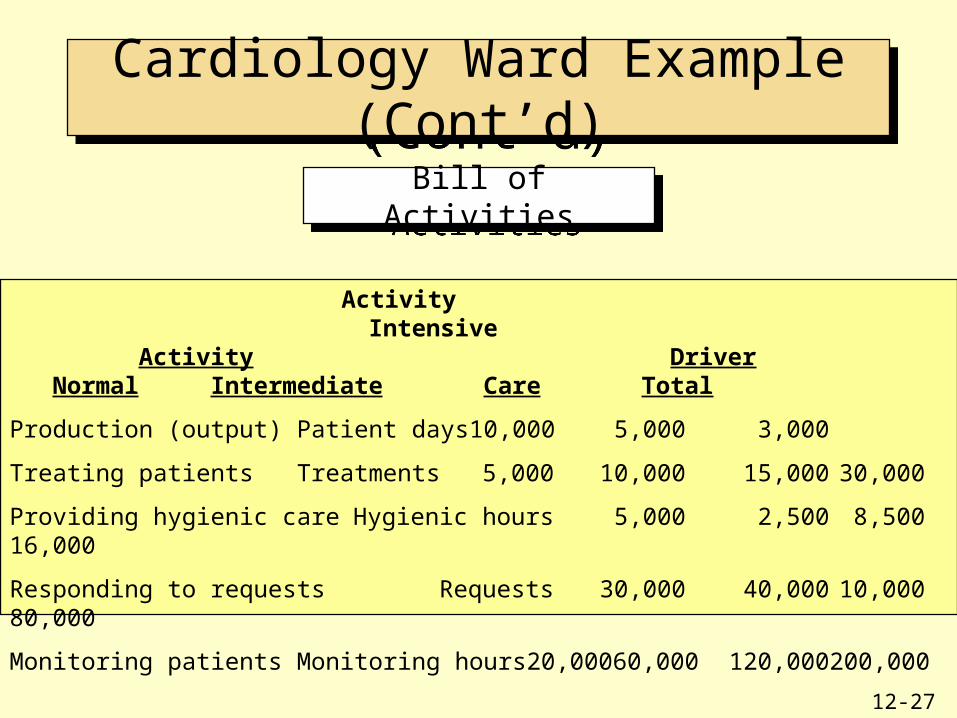

Bill of ActivitiesBill of Activities

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

Activity Intensive Activity Driver Normal Intermediate Care Total

Production (output) Patient days 10,000 5,000 3,000

Treating patients Treatments 5,000 10,000 15,000 30,000

Providing hygienic care Hygienic hours 5,000 2,500 8,500 16,000

Responding to requests Requests 30,000 40,000 10,000 80,000

Monitoring patients Monitoring hours 20,000 60,000 120,000 200,000

12-28

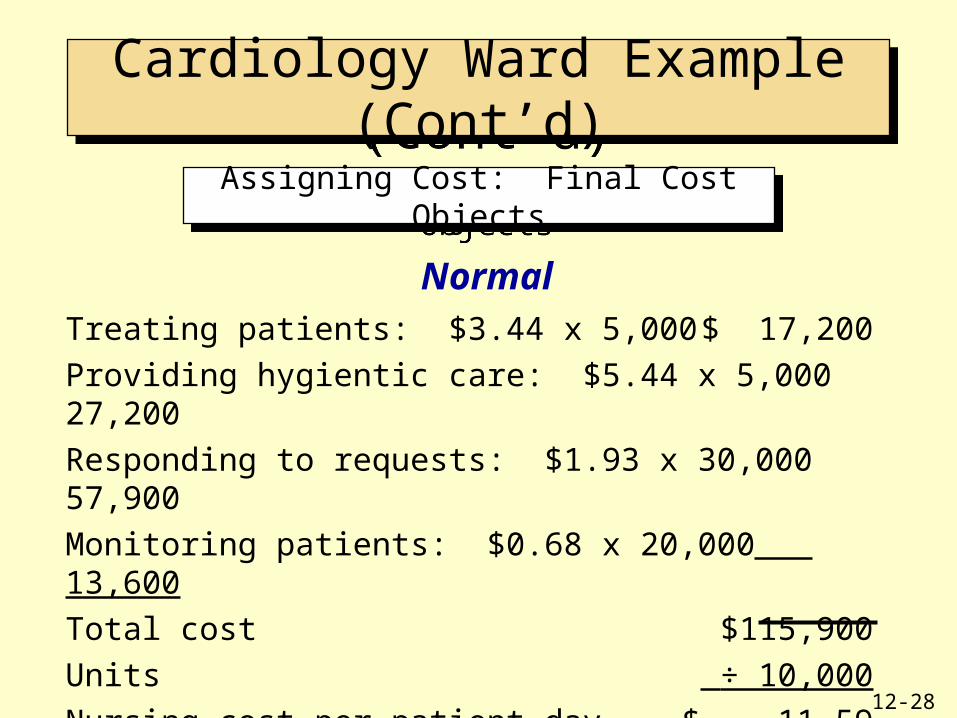

Assigning Cost: Final Cost ObjectsAssigning Cost: Final Cost Objects

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

NormalTreating patients: $3.44 x 5,000 $ 17,200

Providing hygientic care: $5.44 x 5,000 27,200

Responding to requests: $1.93 x 30,000 57,900

Monitoring patients: $0.68 x 20,000 13,600

Total cost $115,900

Units ÷ 10,000

Nursing cost per patient day $ 11.59

12-29

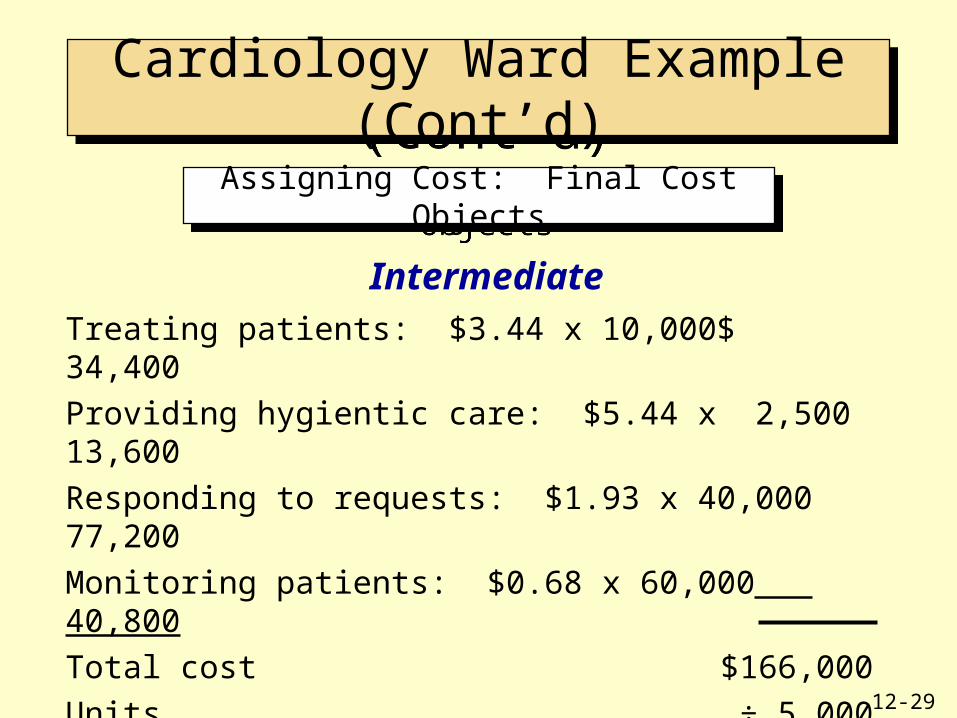

Assigning Cost: Final Cost ObjectsAssigning Cost: Final Cost Objects

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

IntermediateTreating patients: $3.44 x 10,000 $ 34,400

Providing hygientic care: $5.44 x 2,500 13,600

Responding to requests: $1.93 x 40,000 77,200

Monitoring patients: $0.68 x 60,000 40,800

Total cost $166,000

Units ÷ 5,000

Nursing cost per patient day $ 33.20

12-30

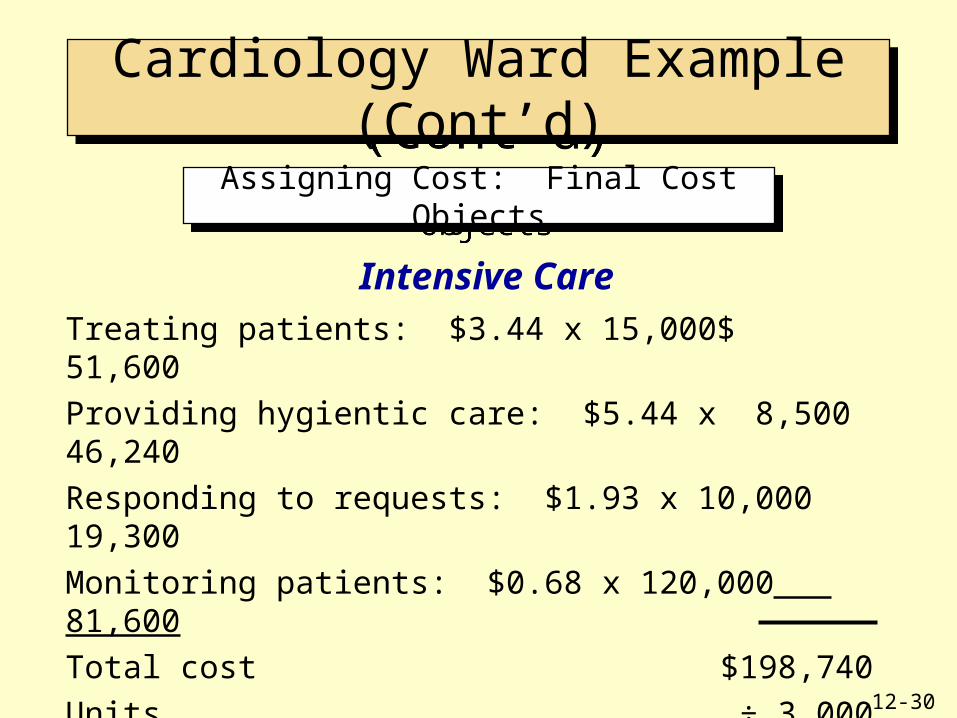

Assigning Cost: Final Cost ObjectsAssigning Cost: Final Cost Objects

Cardiology Ward Example (Cont’d)Cardiology Ward Example (Cont’d)

Intensive CareTreating patients: $3.44 x 15,000 $ 51,600

Providing hygientic care: $5.44 x 8,500 46,240

Responding to requests: $1.93 x 10,000 19,300

Monitoring patients: $0.68 x 120,000 81,600

Total cost $198,740

Units ÷ 3,000

Nursing cost per patient day $ 66.25

12-31

Unit-level activities are those that are performed each time a unit is produced.

Examples: Power and machine hours are used each time a unit is produced. Direct materials and direct labor activities are also unit-level activities, even though they are not overhead costs.

Activity-Level ClassificationActivity-Level Classification

12-32

Activity-Level ClassificationActivity-Level Classification

Batch-level activities are those that are performed each time a batch of products is produced.

Examples: Setups, inspections, purchasing, and material handling.

12-33

Activity-Level ClassificationActivity-Level Classification

Product-level (sustaining) activities are those activities performed that enable the various products of a company to be produced. These activities and their costs tend to increase as the number of different products increases.

Examples: Engineering changes, developing product-testing procedures, introducing new products, and expediting goods.

12-34

Activity-Level ClassificationActivity-Level Classification

Facility-level activities are those that sustain a factory's general manufacturing processes.

Examples: Plant management, landscaping, maintenance, security, property taxes, and plant depreciation.

12-35

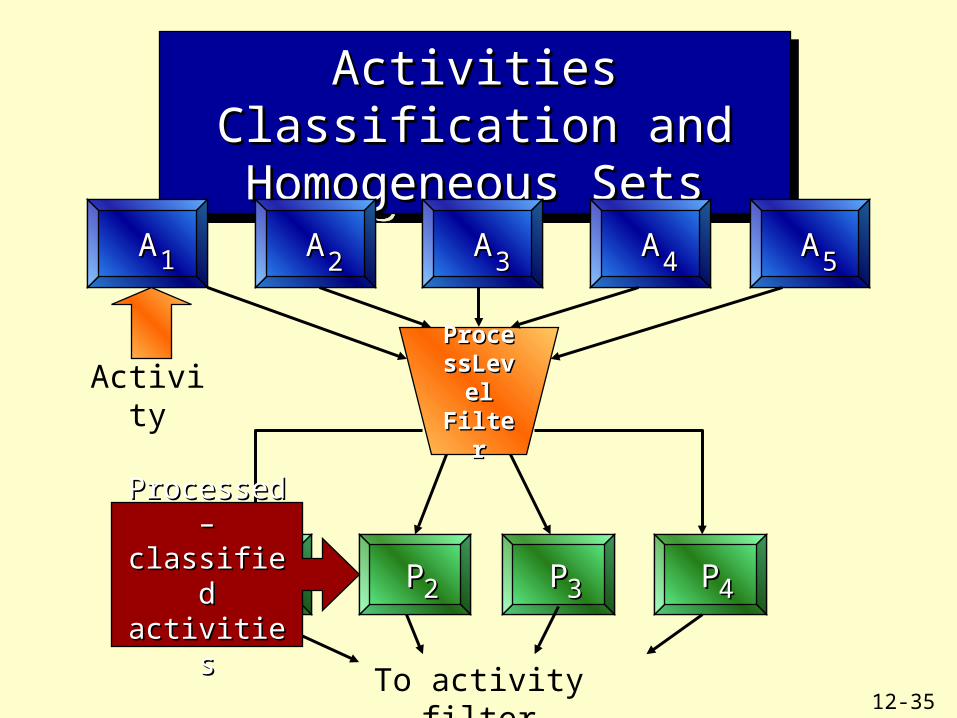

Activities Classification and Activities Classification and Homogeneous SetsHomogeneous Sets

Activities Classification and Activities Classification and Homogeneous SetsHomogeneous Sets

AA AA AA AA AA11 22 33 44 55

ProcesProcessLevel sLevel FilterFilter

Activity

PP PP PP PP11 22 33 44

To activity filter

Processed –Processed –classified classified activitiesactivities

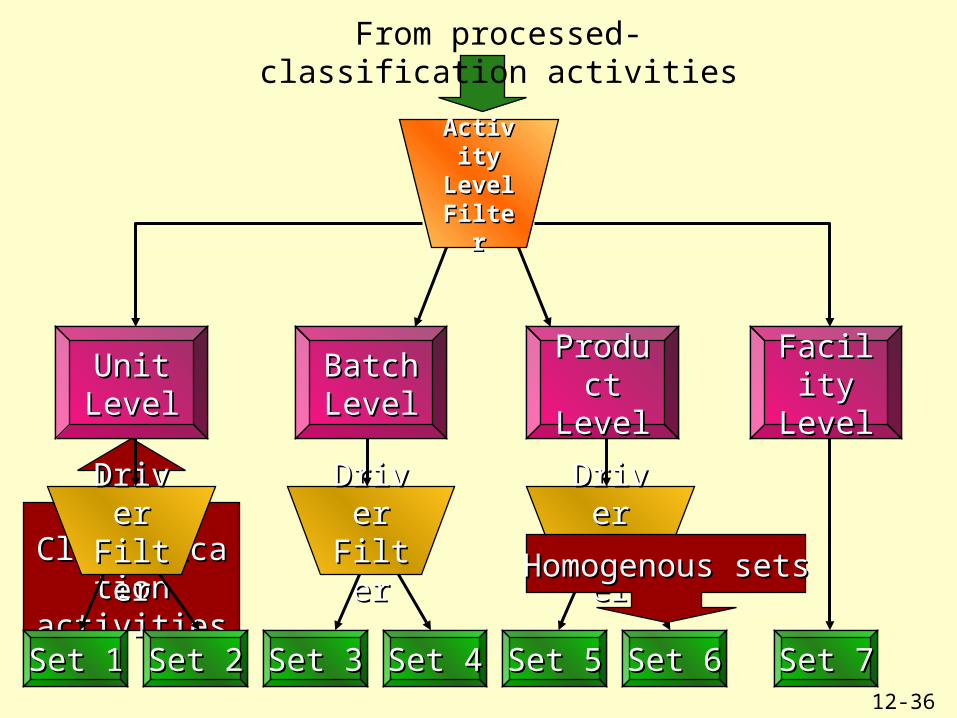

12-36

ActivitActivity Level y Level FilterFilter

From processed-classification activities

Unit Unit LevelLevel

Batch Batch LevelLevel

Product Product LevelLevel

Facility Facility LevelLevel

Level-Level-Classification Classification

activitiesactivities

DriveDriver r

FilterFilter

DriveDriver r

FilterFilter

DriveDriver r

FilterFilter

Set 1Set 1 Set 2Set 2 Set 3Set 3 Set 4Set 4 Set 5Set 5 Set 6Set 6 Set 7Set 7

Homogenous setsHomogenous sets

12-37

ABC DatabaseABC DatabaseABC DatabaseABC Database

An ABC database is the collected data sets that are organized and interrelated for use by an organization’s activity-based costing information system.

A data set is a grouping of logically related data.

12-38

ChapteChapterr

End ofEnd of

12-39