Embed Size (px)

Citation preview

Ind

ustr

ial M

iner

als

1

2002 saw the end of an era with mining in

its present form in the open pit coming to

an end at precisely 14:45 on Thursday,

25 April 2002. The detonator to ignite

64 000 kg of explosives to blast 166 000

tons of ore was activated at bench 60 in the

Palabora open pit. It signified the end of an

era and the transition from an open cast

mine to an underground operation.

2

Scenic view over Foskor-thickener with the Palabora shafts in the backgroundScenic view over Foskor-thickener with the Palabora shafts in the background

Group o perations in brief

PALABORA MIN ING COMPANY IS SOUTH AFR ICA’S LARGEST

PRODUCER OF REFINED COPPER.

PRODUCT

THE COMPANY PRODUCES COPPER AS A PR IMARY PRODUCT

TOGETHER WITH BY-PRODUCTS, WHICH INCLUDE MAGNETITE,

N ICKEL SULPHATE , ANODE SL IMES AND SULPHUR IC AC ID .

INDUSTRIAL MINERALS PRODUCTION COMPRISES VERMICULITE,

AND ZIRCONIUM BASIC SULPHATE (ZBS) .

OPERATIONS

THE COPPER D IV IS ION COMPRISES AN OPEN-P IT AND

UNDERGROUND MINING OPERATION, A CONCENTRATOR CAPABLE

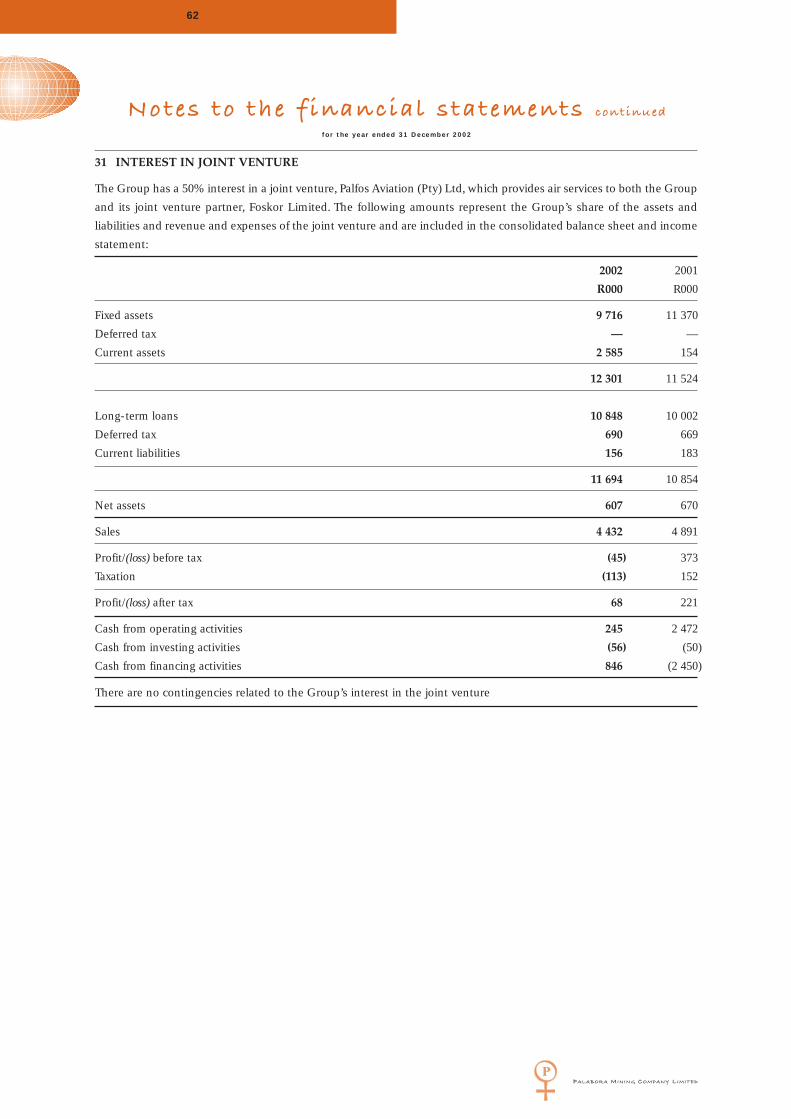

OF MILLING 80000 TONS OF ORE PER DAY, A COPPER SMELTER

WITH ANODE CASTING FACIL IT IES AND AN ASSOCIATED ACID

PLANT, AN ELECTROLYT IC REF INERY TANK HOUSE , A ROD

CASTING PLANT AND BY-PRODUCT RECOVERY PLANTS.

THE INDUSTRIAL MINERALS DIVIS ION COMPRISES AN ADJACENT

OPEN-P IT VERMICUL ITE MIN ING OPERAT ION AND RECOVERY

PLANT, AND A NEW ZIRCONIUM BASIC SULPHATE PRODUCTION

PLANT, WHICH USES IMPORTED ZIRCON SAND AS A FEEDSTOCK.

OVERSEAS SUBSIDIARIES IN THE UNITED STATES OF AMERICA,

THE UNITED KINGDOM AND SINGAPORE ARE INVOLVED WITH THE

SELLING OF INDUSTRIAL MINERAL PRODUCTS.

3

Financial

and o perational

highligh ts

2002 2001

Share performance

Rand per share

Headline earnings 8,39 7,75

Dividends declared — 0,60

Cash available from operations 20,80 27,24

Interests of shareholders

(net asset value) 70,96 63,31

Market price

High 76,00 65,50

Low 58,50 34,00

Financial

R million

Revenue 2 121 1 985

Distributable earnings 257 220

Headline earnings 237 219

Shareholders’ equity 2 009 1 793

Capital expenditure 695 702

Production

000 metric tons

Material mined 9 976 12 002

Ore milled 9 933 14 522

Concentrate produced

(new copper content) 52 78

Cathode produced 81 87

Sales

000 metric tons

Cathode sold 83 96

Concentrate sold (copper content) 10 4

Employees 2 011 2 428

(tons are metric tons)

160

140

120

100

80

60

40

20

081

Tons

Actual Indicative

99 01

Copper produced (thousand tons)

Material mined (million tons)

2002

Production perspective 1981 - 2002

Palabora Mining Company LimitedRegistered in the Republic of South Africa

Reg No. 1956/002134/0647th Annual Report 2002

4

DIRECTORS

Chairman

Z W Ntuli (57) (Resigned 31 December 2002)

J H K Sachikonye (48) (Zimbabwean)

Appointed with effect from 1 January 2003

(Acting non-executive Chairman)

EXECUTIVE

Managing Director

D S Sadler (54) (Australian)

Appointed 21 August 2000

General Manager and Chief Financial Officer –

Finance Compliance and Administration

M D Humphries (48) Appointed 4 May 2000

General Manager – External Affairs

S Langa (49) Appointed 24 April 2002

NON-EXECUTIVE

D A Farnaby (38) Appointed 1 July 2000

O L Groeneveld (Australian) (49)

Appointed 20 April 1999

R M Maruma (43) Appointed 29 April 1999

G M Negota (51) Appointed 20 May 1998

J E Rickus (55) (British) Appointed 17 February 2000

R M Whyte (59) (British) Appointed 5 September 2000

J C M van Gaalen (46) (Dutch)

Appointed 24 January 2002

C N Zungu (47) Appointed 24 April 2002

ALTERNATE DIRECTORS

F B Weldon (55) Appointed 8 August 2002

B K Wood (52) Appointed 24 January 2002

W R J Ranson (37) Appointed 11 March 2003

MANAGEMENT

General Manager – Underground Mining Project

K P P Calder (until 31 December 2002)

K J McLeish (with effect 1 January 2003)

General Manager – Copper Operations

H J R Kenyon-Slaney

General Manager – Industrial Minerals

A S Siregar (until 31 December 2002)

L du Plessis (with effect 1 January 2003)

General Manager – Asset Management

K J McLeish (until 31 December 2002)

B Iqani (Acting) (with effect 1 January 2003)

General Manager – Safety, Health, Environment and

Quality

A Grundling

Company Secretary

E B R Hone

Directorate and management

PALABORA MINING COMPANY LIMITED

PALABORA MINING COMPANY LIMITED

5

Directorate

EXECUTIVE DIRECTORsDavid S Sadler (54) was appointed managingdirector in August 2000. A metallurgist with aMSc in Metallurgical Quality Control/Statistics and a BSc in Metallurgy, he has heldvarious managerial positions within the RioTinto Group in Australia and London since1984. He came to Palabora from Londonwhere he was safety adviser to the ChiefExecutive of Rio Tinto plc

Michael (Mike) D Humphries (48) is thegeneral manager for Finance and HumanResources. He joined Palabora in May 2000when he was appointed to the board. He hasheld previous managerial positions within theRio Tinto Group in Namibia and Portugal andelsewhere in the mining industry over aperiod of years. Mr Humphries has a BCommand MBA degrees from the University ofCape Town. He is a chartered accountant andis a member of the South African Institute ofChartered Accountants and AAPA (des).

Simeon Langa (49) is the general managerfor External Affairs. He joined Palabora inSeptember 1987 as a personnel officer. He was promoted within the Company untilhe was appointed general manager – HumanResources in 1999. In 2002 he moved fromhuman resources to external affairs and wasappointed as an executive director in April2002. Mr Langa has a BComm degree fromthe University of the North and an honoursdegree in Business Administration andManagement from the University ofStellenbosch, Business School.

NON-EXECUTIVE DIRECTORS Deborah (Debbie) A Farnaby (38) is anindependent non-executive director havingbeen appointed to the board in July 2000.Mrs Farnaby is the director: GroupInformation Technologies and Services forSappi Limited as well as a non-executivedirector on the Sappi Fine Paper Europeanboard. She is also a Trustee for the SappiProvident Fund. She has held variouspositions within Sappi since 1989. She has aBSc (Hons) Computer Science degree fromthe University of the Witwatersrand and aMSc Computer Science (Cum Laude) degreefrom the University of Stellenbosch as well asa GDE (Mechanical Engineering) qualification.

Oscar L Groeneveld (49) became a directorin April 1999. Mr Groeneveld has been adirector of Rio Tinto plc since 1998. A miningengineer with qualifications in engineering,science and management, he joined the Rio Tinto Group in 1975 and has since held aseries of management positions, includinghead of Technology, before being appointedchief executive of the Copper Group of Rio Tinto in 1999. He is also a director ofFreeport-McMoRan Copper & Gold INC.

Makgabo (Rufus) R Maruma (43) has beenan independent non-executive directorsince April 1999. Mr Maruma is a leadingenvironmental and waste managementexpert and has reviewed environmentalprogrammes for leading utilities andindustries in over forty six countries. He isthe chairman and a director of a number ofcompanies, including Enviroserv Holdings,Stewart Scott International, BohlwekiEnvironmental, Amafaun Faun, Pan AfricanShop Fitters, Group Five Limited, Geo Scottand Bakwena Concession Company. He waschairman of the task team that drew up anational environmental policy for SouthAfrica (CONNEP) and also serves on anumber of committees, including theConservation Advisory Committee of SouthAfrica. Mr Maruma holds a MSc degree inEnvironmental Science from the Universityof Aberdeen.

George M Negota ( 51) was appointed anindependent non- executive director in May1998. He is a practising attorney. Mr Negotastarted a legal firm, Negota IncorporatedAttorneys in June 1998. He has conducted anumber of commissions of enquiry on behalfof government. He has led a team thatrestructured Eskom and has also conducteda study on the rationalization of state assetsin Mpumalanga. He is currently involved inthe research study in preparation for theGauteng express train. He is chairman of theCross Border Transport Agency and of the Gauteng Operating Licence Board andKuthele Projects (Pty) Limited. He is adirector of the N3 Consortium, ORT StepSouth Africa, Read Education Trust, theNational Institute for Community Educationand BKS Group Holdings (Pty) Limited. Mr Negota is also a member of the IncomeTax Appeal Court. He has BA (Hons) and MCom degrees from Rand AfrikaansUniversity, a LLB and a BCom (Hons)degrees from Unisa. In addition Mr Negotahas a H Diploma in Tax Law and a H Diploma in Company Law fromWitwatersrand University and a certificate inTax Law from Unisa.

Directorate

6

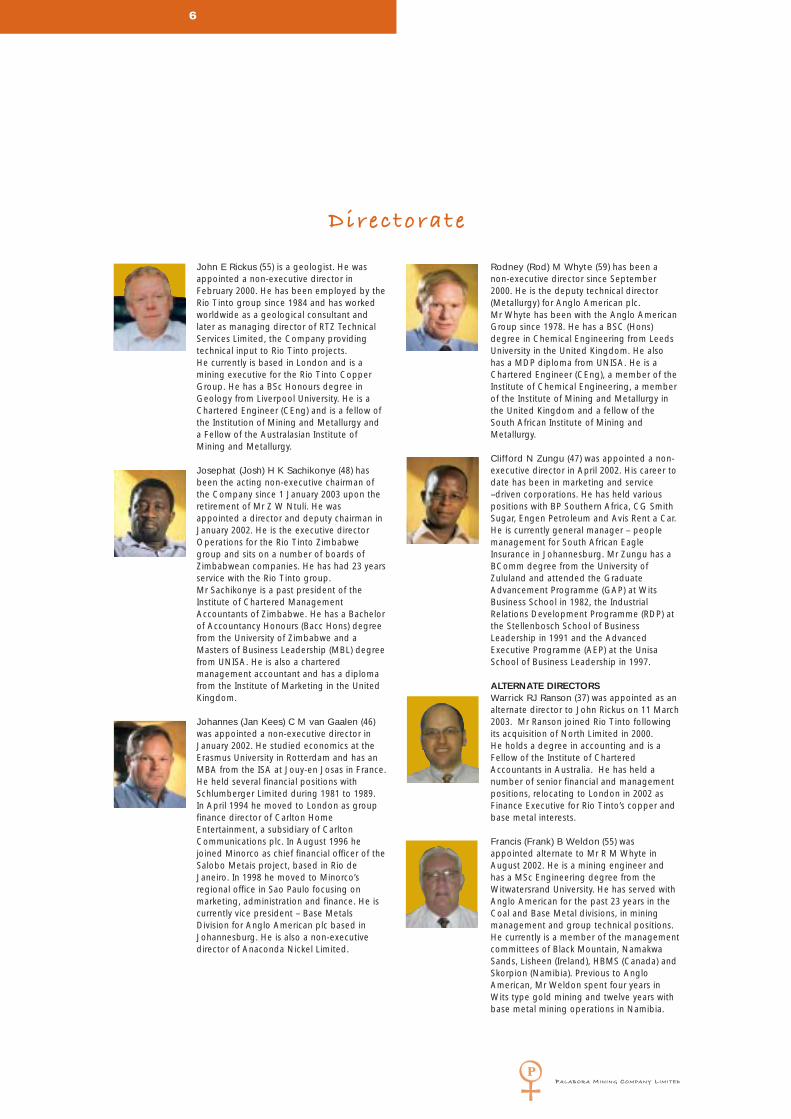

John E Rickus (55) is a geologist. He wasappointed a non-executive director inFebruary 2000. He has been employed by theRio Tinto group since 1984 and has workedworldwide as a geological consultant andlater as managing director of RTZ TechnicalServices Limited, the Company providingtechnical input to Rio Tinto projects. He currently is based in London and is amining executive for the Rio Tinto CopperGroup. He has a BSc Honours degree inGeology from Liverpool University. He is aChartered Engineer (CEng) and is a fellow ofthe Institution of Mining and Metallurgy anda Fellow of the Australasian Institute ofMining and Metallurgy.

Josephat (Josh) H K Sachikonye (48) hasbeen the acting non-executive chairman ofthe Company since 1 January 2003 upon theretirement of Mr Z W Ntuli. He wasappointed a director and deputy chairman inJanuary 2002. He is the executive directorOperations for the Rio Tinto Zimbabwegroup and sits on a number of boards ofZimbabwean companies. He has had 23 yearsservice with the Rio Tinto group. Mr Sachikonye is a past president of theInstitute of Chartered ManagementAccountants of Zimbabwe. He has a Bachelorof Accountancy Honours (Bacc Hons) degreefrom the University of Zimbabwe and aMasters of Business Leadership (MBL) degreefrom UNISA. He is also a charteredmanagement accountant and has a diplomafrom the Institute of Marketing in the UnitedKingdom.

Johannes (Jan Kees) C M van Gaalen (46)was appointed a non-executive director inJanuary 2002. He studied economics at theErasmus University in Rotterdam and has anMBA from the ISA at Jouy-en Josas in France.He held several financial positions withSchlumberger Limited during 1981 to 1989. In April 1994 he moved to London as groupfinance director of Carlton HomeEntertainment, a subsidiary of CarltonCommunications plc. In August 1996 hejoined Minorco as chief financial officer of theSalobo Metais project, based in Rio deJaneiro. In 1998 he moved to Minorco’sregional office in Sao Paulo focusing onmarketing, administration and finance. He iscurrently vice president – Base MetalsDivision for Anglo American plc based inJohannesburg. He is also a non-executivedirector of Anaconda Nickel Limited.

Rodney (Rod) M Whyte (59) has been a non-executive director since September2000. He is the deputy technical director(Metallurgy) for Anglo American plc. Mr Whyte has been with the Anglo AmericanGroup since 1978. He has a BSC (Hons)degree in Chemical Engineering from LeedsUniversity in the United Kingdom. He alsohas a MDP diploma from UNISA. He is aChartered Engineer (CEng), a member of theInstitute of Chemical Engineering, a memberof the Institute of Mining and Metallurgy inthe United Kingdom and a fellow of theSouth African Institute of Mining andMetallurgy.

Clifford N Zungu (47) was appointed a non-executive director in April 2002. His career todate has been in marketing and service–driven corporations. He has held variouspositions with BP Southern Africa, CG SmithSugar, Engen Petroleum and Avis Rent a Car.He is currently general manager – peoplemanagement for South African EagleInsurance in Johannesburg. Mr Zungu has aBComm degree from the University ofZululand and attended the GraduateAdvancement Programme (GAP) at WitsBusiness School in 1982, the IndustrialRelations Development Programme (RDP) atthe Stellenbosch School of BusinessLeadership in 1991 and the AdvancedExecutive Programme (AEP) at the UnisaSchool of Business Leadership in 1997.

ALTERNATE DIRECTORSWarrick RJ Ranson (37) was appointed as analternate director to John Rickus on 11 March2003. Mr Ranson joined Rio Tinto followingits acquisition of North Limited in 2000. He holds a degree in accounting and is aFellow of the Institute of CharteredAccountants in Australia. He has held anumber of senior financial and managementpositions, relocating to London in 2002 asFinance Executive for Rio Tinto’s copper andbase metal interests.

Francis (Frank) B Weldon (55) wasappointed alternate to Mr R M Whyte inAugust 2002. He is a mining engineer andhas a MSc Engineering degree from theWitwatersrand University. He has served withAnglo American for the past 23 years in theCoal and Base Metal divisions, in miningmanagement and group technical positions.He currently is a member of the managementcommittees of Black Mountain, NamakwaSands, Lisheen (Ireland), HBMS (Canada) andSkorpion (Namibia). Previous to AngloAmerican, Mr Weldon spent four years inWits type gold mining and twelve years withbase metal mining operations in Namibia.

PALABORA MINING COMPANY LIMITED

PALABORA MINING COMPANY LIMITED

7

Directorate and management

Brian K Wood (52) has been an alternatedirector since July 2001. He was firstlyalternate to Mr R M Whyte and then inJanuary 2002 he was appointed alternate toMr J C M van Gaalen. Mr Wood has had 27 years service with Anglo American plc inthe financial area, including financial andmanagement accounting in AngloCoal andAngloBase Divisions. He is currently vicepresident, finance and administration in theAngloBase Division in Johannesburg. He hasa CA (SA) qualification and is a member ofthe SA Institute of Chartered Accountants(SAICA).

MANAGEMENT The Company is managed by an executivecommittee comprising the managing director,Mr D S Sadler, the two executive directors,Mr M D Humphries who is the generalmanager – Finance, Mr S Langa, the generalmanager – External Affairs and five generalmanagers. The post of general manager –Asset Management is being filled by Mr B Iqani in an acting capacity since thebeginning of 2003 until a permanentappointment is made. The remaining fourcurrent members are:

Louis du Plessis (48) was appointed generalmanager – Industrial Minerals in January2003. He is accountable for the productionand marketing of vermiculite and zirconiumbasic sulphate (ZBS). Mr Du Plessis is ageologist and holds a BSc Hons. degree inGeology from Witwatersrand University and aMBL degree from the University of SouthAfrica. He has been with the Company since1981 and has had management roles intechnical support services and marketing. In 1999 he was seconded to the UnitedKingdom to head up the European sales andmarketing office in Guildford. Mr Du Plessisreturned to South Africa in 2001 to managethe Company’s SAP implementation project.

Andre Grundling (53) has held the positionof general manager – Safety, Health,Environment and Quality since 1999. Prior tothis he managed his own Company by thename of Grundling Environmental Servicesfrom 1997 to 1999. From 1993 to 1996 Mr Grundling was employed by Palabora inthe position of Environmental SciencesSuperintendent. For the period 1983 to 1993he was head of the Atmospheric SciencesDivision of the Atomic Energy Corporation.Mr Grundling has a BSc (Hons) degree inapplied mathematics and meteorology.

Harry J R Kenyon-Slaney (41) who is thegeneral manager – Copper Operations.Mr Kenyon-Slaney was appointed to thisposition in March 2001. He previously heldthe positions of general manager – IndustrialMinerals and marketing director at Palabora,having joined the Company in 1997. Prior tothis Mr Kenyon-Slaney held the positions ofcommercial director – Far East, RTZ MineralServices in London from 1993 to 1997 andManager – New Projects, RTZ MineralServices in London from 1990 to 1993.Between 1984 and 1990 he worked for AngloAmerican initially as a geologist and latterlyin the New Mining Business Division. He hasa BSc degree in Geology as well as aDiploma in Business Management.

Kevin J McLeish (42) was appointed to theposition of general manager – UndergroundMining Project in January 2003. With theintegration of the underground project withthe surface operations, the title of projectdirector has now fallen away and Mr McLeish’s new title is general manager -Underground Operations. He previously heldthe position of general manager – AssetManagement and was seconded to theCompany from Hamersley Iron Ore in 2000.Mr McLeish has been with Rio Tinto for 14 years. He has held various managerialpositions within the Rio Tinto Group inAustralia including manager Remelt -Comalco and manager Port Operations atHamersley Iron Ore. Mr McLeish holds a BSc degree in Metallurgical studies as well asa MSc degree in Business Administration.

During 2002, the following held the positionsindicated:Keith P P Calder held the position ofgeneral manager – Underground MiningProject for the whole year. He has beentransferred within the Rio Tinto Group toNorthparkes/Peak in Australia as managingdirector. Mr Calder was project director sinceFebruary 1999.

Arif S Siregar has returned to Indonesia totake up the position of vice president Rio Tinto Indonesia, a Company within theRio Tinto Group. Dr Siregar held the positionof general manager – Industrial Mineralssince August 2001 to December 2002.

COMPANY SECRETARYE B R (Brett) Hone (52) was appointedcompany secretary in September 1999,having previously filled this role at RossingUranium Limited from 1984 through 1992 andat Rio Tinto Zimbabwe from 1980 to 1984.He gained a LL.B (London) degree in 1972;a post-graduate LL.B (Rhodesia) degree in1979 and was admitted as an advocate inZimbabwe in 1980.

The delayed ramp-up of the underground mine resulted

in production of new copper in concentrate of 52 197 tons,

down 33% on the 78 381 tons achieved in 2001.

Reduced new copper in concentrate production was

supplemented by the processing of smelter secondaries

and low-grade concentrate stockpiles. These sources

provided an additional 12 170 tons of copper in

concentrate. Total production of copper in concentrate

was 64 367 tons (2001:82 243 tons). Imported concentrate

and stock-piled concentrates and scrap copper were also

processed as feed to the smelter. As a result of this,

refined copper production was 81 392 tons, 6% lower than

2001 production of 86 848 tons.

As regards the development of the mine, the ore

handling system, with a capacity of 30 000 tons per day, is

in place. More specifically, the undercut progressed well

and according to plan. The third crusher was

commissioned on schedule and construction of the fourth

and last crusher commenced according to plan. This was

commissioned in May 2003. 113 draw bells were

completed and handed over to operations by the end of

2002 against a target of 120 draw bells.

As a direct result of the delay in the ramp-up of the

underground mine and the strengthening of the Rand

against the US dollar, the Company requires additional

finance. Rio Tinto, Palabora’s largest single shareholder,

has made available a US$50 million short-term loan

facility. This will meet working capital and other

requirements until the process of raising additional

financial resources is complete. The Board of Directors

agreed during May 2003 to raise additional capital in

the form of a shareholder supported re-financing

package. It is anticipated that the re-financing will include

an offer to shareholders to participate and will be

underwritten by Palabora’s major shareholders.

The funds raised will be utilised to service existing

debt commitments as well as to allow completion of the

underground project and other fixed capital

commitments, including enhancements to various plants.

In these circumstances the board is of the opinion

that it is unlikely that dividend payments will

recommence within the next two years.

A number of factors will influence operating costs in

2003. Most significant of these are additional mining

costs associated with the delay in the ramp up of the

underground mine, while another results from the change

from defined benefit pension funds to a defined

contribution pension fund in late 2002. Palabora is in the

process of liquidating the existing defined benefit funds.

The new defined contribution fund was established with

effect from 1 September 2002 and the Company is now

contributing 12,5% of pensionable emoluments to this

Fund for its employees. This adds approximately

R31 million annually to Palabora’s cost base, although the

cost impact would have been twice this if the change in

schemes had not taken place.

The Total Operational Performance programme

(TOP) which was introduced at Palabora in 2000 to create

a culture of performance enhancement and improvement

for the business was concluded for Copper Operations,

Industrial Minerals, SHEQ, Finance, Compliance and

Administration, Asset Management as well as Human

Resources. All departments have up to two years to

implement their TOP ideas and to deliver savings in

operating costs, working capital and capital expenditure

through elimination of uncontrolled process variability

and waste, improved quality and reducing downtime.

A number of other business improvement initiatives

are underway at Palabora, namely:

• Reliability Centred Maintenance (RCM) in order to

ensure that equipment works the way it should, when it

is needed.

• Integrated Process Management System (IPMS)/6

Sigma in order to understand processes, eliminate

unnecessary work and set control plans; and

• 5S – a rigorous way in which an area can prepare itself

for improvement.

During 2002, good progress was made with these

programmes, including implementation of IPMS in

copper operations and development of the ZBS process

control plan. This has resulted in improvements in

productivity, reduced scrap generation and reduction in

equipment in a number of areas.

Key areas that will need to be managed during 2003

Chairman’s statement

8

PALABORA MINING COMPANY LIMITED

include:

• the ramp-up of the underground to full

production and demobilization of the

project team;

• the raising of additional finance;

• the importation of concentrate required to

supplement smelter feed;

• continuation of the business and process

improvement initiatives; and

• further improving the management/union relationship.

Regrettably, the safety performance at Palabora

deteriorated in 2002. The Safety Management Auditing

Techniques (SMAT) system will again be a key driver of

improved safety performance at Palabora in 2003. All

leaders within the business are required to participate in

the SMAT process. The quality of SMATs will be improved

by team leader review and engagement.

A contractor supervisor accreditation system will be

introduced during 2003. This will be used to educate

contractor supervisors in Palabora’s safety standards,

assess their level of understanding and competency and

monitor their performance.

Aside from the re-financing of the business, HIV/AIDS

has been identified as the highest risk facing the

Company within the medium/long term. The Company’s

HIV/AIDS management programme is spearheaded by

the HIV/AIDS steering committee, which is chaired by the

general manager – External Affairs. The programme

focuses on employees and, through the Palabora

Foundation and with other stakeholders, on the local

community from which the Company recruits most of its

employees. Discussions aimed at increased participation

by the National Employees Trade Union (NETU) and the

National Union of Mineworkers (NUM) in the programme

progressed well during the year and should be

concluded during 2003.

Work will continue in 2003 on improving the

leadership skills within the organization. Potential leaders

continue to attend leadership courses based on the

MacDonald & Associates models.

Employment equity targets have been set at

superintendent level. High potential employees will be

supported though a system of mentoring

and coaching in order to meet these

targets. Promotion will be based on merit.

From 2004, the underground operation

should be producing at 30 000 tons per day,

initially at 0,8% copper. This should result in

production of 77 000 tons of copper in

concentrate in 2003, 85 000 in 2004 and

then a steady decline in future years in line

with ore grade.

The key issue in future years is therefore to maintain

the smelter at full capacity through the processing of

purchased concentrate. A project team has been

established to identify and analyse probable impacts on

the operation and possible sources.

The Palabora Foundation has effectively re-focused

on education, skills development, development of

entrepreneurs and the management of HIV/AIDS within

the communities as its core work.

Wells Ntuli retired as a director and as chairman on

31 December 2002. He has been a director since 1991

and chairman since July 1999. On behalf of the Board,

management and employees, I would like to thank Wells

for his invaluable contribution to the Company during

this period and would like to wish him a fulfilling

retirement in Pietermaritzburg. I would like to welcome

Clifford Zungu to the Board. I have been asked to act as

chairman by the Board until a successor to Wells is

appointed later this year.

My thanks and appreciation goes to all our

employees and contractors for their commitment during

a challenging year.

Josh Sachikonye

Acting Chairman

PALABORA MINING COMPANY LIMITED

9

Chairman’s statement

Josh Sachikonye

Acting Chairman

Palabora achieved a consolidated net profit of

R257 million compared with R220 million in 2001.

The increase can largely be attributed to the

strengthening of the Rand in 2002 compared to 2001.

The Board of Directors declared no dividends in

2002 (2001: R0,60 per share). This is in line with the

undertaking given by the Company that it would not, in

respect of the calendar years 2001 and 2002, distribute

any of its distributable profits for each calendar year

except for the dividend that was declared on 24 April

2001. This is one of the conditions pertaining to the

granting of a four-and-a-half year unsecured syndicated

loan of US$125 million by a consortium of nine local and

overseas banks in 2001.

The Group’s net debt decreased by R158 million

during the year. Consolidated net debt was

R1 435 million at 31 December 2002. This was largely due

to exchange gains on the dollar porton of the medium

term loan facility due to the strengthening of the Rand

between the start and end of 2002. The Company will be

paying the first half yearly instalment of its medium-term

loan facility of US$15 million and R47 million on 11 June

2003. As a consequence of the strengthening of the

South African Rand in late 2002, coupled with the delay

in ramp up of underground mine production, the cash

flow in the latter part of 2002 was worse than expected.

Management is taking the necessary action to ensure

that adequate funding is made available and it is unlikely

that dividend payments will recommence within the next

two years.

Copper sales, including concentrates, amounted to

R1 459 million (2001: R1 378 million) representing 69% of

turnover. Vermiculite sales were R373 million compared

to R291 million in 2001.

Some 4 340 dry metric tons of concentrate (952 tons

of contained copper) were sold during 2002 compared to

13 284 tons in 2001.

Capital expenditure

The capital expenditure for the year was R695 million,

R7 million lower than the R702 million in 2002. The major

projects included:

R million

Underground project 504

Information systems strategy – SAP 45

ZBS plant upgrade 22

Electric blowers and 11Kv upgrade 20

Projected expenditure for 2003 includes the following:

R million

Underground project 323

Acid plant modifications 21

Primary converter hood upgrade 7

Operating Costs

Operating costs were R1 720 million compared with

R1 625 million in the previous year.

The increase was mainly due to the increased imports

of copper concentrates (R91 million), open pit contract

mining costs (R88 million) and the cost of pension fund

contributions arising from a change in pension fund

legislation (R30 million). These additional costs were

partly offset by the realization of cost savings from the

Total Operating Performance (TOP) programme.

The average unit cash cost of cathode delivered to

customers in Rand per ton increased by 62%

(31% increase in US cents per lb.) compared with 2001.

Rand/ton US cents/lb

2002 2001 2002 2001

Cathode cash cost

delivered 14 476 8 928 62,3 47,4

The following major processes and activities contributed

to cash costs in US cents per lb.:

% %

2002 2001

Mining and underground mining 45 37

Milling 30 22

Smelting/refining 16 26

Indirect/selling 24 36

By-products (15) (21)

100 100

10

Review by the managing director

PALABORA MINING COMPANY LIMITED

As expected, 2002 was a year of transition for

Palabora Mining Company.

The planned closure of the open pit for

large-scale mining took place as scheduled in

April 2002. Smaller scale contract mining of

the open pit ramps began in May. This has

been a great success with mining rates being

in excess of those forecast.

The underground mine did not achieve its

targeted full production rate of 30 000 tons of ore per

day by the end of 2002. Production increased during the

year from a monthly average of 4 700 tons per day in

January to 13 500 tons per day in December.

Production rates have been constrained primarily by

the poor availability of secondary breaking equipment.

This equipment is required to handle oversize material

reporting to the draw bells from the cave. Operating

plans to improve production rates are currently being

implemented, including the increase in size of the

secondary breaking fleet and changes to operating

methods. It is anticipated that the target of 30 000 tons

per day will be achieved in the third quarter of 2003.

The delay in the ramp up of production from the

underground mine has necessitated the mining of

the haulage ramps in the open pit (ramp scavenging); the

recovery of low grade or weathered ore from surface

dumps and the purchase of imported concentrate, in

order to maintain consistent feed to the smelter.

The impact of this variation in ore sources from 2001 to

2002 is demonstrated in the following table.

Source Tons ore (000) Tons ore (000)

2002 % 2001 %

Mining (conventional) 2 473 26 11 348 82

Mining (scavenging) 2 705 29 - -

Surface dumps 892 10 1 549 11

Underground 3 277 35 1 007 7

9 347 100 13 905 100

Tons concentrate

purchased 37 000 12 000

Zirconium Basic Sulphate ( ZBS )

The upgraded ZBS plant was commissioned in the second

half of 2002. Commissioning of the plant was delayed

following a fire in January 2002. As a result, production of

ZBS was limited to 501 tons in 2002

(2001: 1 229 tons). Production of ZBS within

tightened customer specifications was being

achieved from the refurbished plant by the

end of 2002. Average sales prices achieved for

ZBS in 2002 were low due to the sale of

stockpiled low-grade material.

Safety and Environment

Palabora’s safety performance deteriorated in 2002,

but I am pleased to report that there were no fatalities

compared to the two fatalities that occurred in 2001.

The lost time injury frequency rate for the year was

0,46 compared to 0,27 achieved in 2001. The 0,27 in 2001

was the lowest on record. Of the 26 lost time injuries

17 occurred in the underground mine. Contractors

accounted for 65% of the lost time injuries.

On the environmental front there was an increase in

the annual average raw water consumption with an

average of 43,5 Ml/day for 2002, compared with

36,6 Ml/day achieved in 2001. This increase is largely due

to the low rainfall for the calendar year of 154mm against

the annual average of 527mm.

Sulphur recovery for the year was 69%, 2% lower

than in 2001. The lower sulphur capture was mainly

due to low SO2 gas flows caused by low smelter

throughput, resulting in poor acid plant performance.

The performance of the primary hooding on converter

1 also contributed to increased fugitive and secondary

gas emissions. This issue will be addressed during 2003.

Conclusion

Detailed reports on Copper Operations, Industrial

Minerals, Asset Management, Human Resources and the

Underground Mine are contained in the following pages.

A detailed Sustainable Development Report accompanies

this Annual Report as a separate document. In conclusion

I would like to express my appreciation to management,

all our employees and contracting staff for their

endeavours during one of the most telling years of

change in the Company’s history.

David Sadler

Managing Director

14 May 2003

PALABORA MINING COMPANY LIMITED

11

Review by the managing director

David Sadler

Managing Director

The smelter experienced a markedly wider variation

in matte grade during the year as the ability to blend concentrate

from different sources diminished

12

Copper

Mining from the open pit ceased in its conventional

form in April 2002 after 38 years. The depth of the pit

was extended to 822 metres, or 416m below sea level,

and production slowed progressively as access

diminished and haul distances to the in-pit crusher

lengthened.

In May a programme to reclaim ore from the main

access ramps was initiated. The exercise, which

involves lowering the ramp level by 20m along most

of its 4.8km available length, supplied a further

2,7 million tons of ore during 2002. Total production

from the open pit was 5,2 million tons at an average

grade of 0.63% Cu.

The recovery of reverbatory furnace slag

continued during the year and a total of almost

680 000 tons, grading 0.60% Cu, was delivered to the

concentrator for further processing.

Ore production from the underground mine rose

steadily during the year and totalled 3,3 million tons,

a rise of 70% over 2001.

Concentrator

Production of copper concentrate declined in 2002 as

the full impact of formal closure of the open pit was

felt. Output of copper-in-concentrate reduced by

16% to 64 367 tons of which just under 20% was

derived from the processing of smelter secondaries,

including slag and low grade reverts.

The copper concentrate grade reduced sharply to

31,1% in line with the change in ore mix. Copper

recoveries declined marginally to 80,9% from 82,3% in

2001 as the weathered nature of ore removed from

the open pit ramps influenced flotation performance.

Smelter

Production of new anode copper totalled 82 262 tons,

a slight decline of 3,8% on the prior year. Output was

constrained by the lower production of concentrate

with the shortfall being filled by the reclaiming of

various low grade concentrate stockpiles. Towards the

end of the year a trial parcel of 10 000 tons imported

copper concentrate was successfully transported to

Palabora and processed through the smelter.

A markedly wider variation in matte grade was

experienced during the year as the ability to blend

ore from different sources diminished. This was

successfully managed in the converters where a

process control initiative enabled a significant

reduction in blowing cycle times to be achieved.

Sulphuric acid production reduced by 15,7% to

117 238 tons on the back of lower throughput in the

converters. Stable plant operations resulted in SO2

emission levels reducing again to 14ppb, a new

record low.

Refinery

Cathode production was dependant upon the supply

of anode copper from the smelter and, with this

dipping slightly, new refined cathode output slipped

by 6% to 81 619 tons.

Production of copper rod rose by 12% from

65 801 tons in 2001 to 73 513 tons in 2002. Production

of the old imperial sizes of 12,25mm and 9,50mm rod

were stopped and replaced by new metric products

of 10mm and 14mm rod. Small quantities of cathode

were again imported in order to supplement feed to

the rod plant during periods when domestic market

demand exceeded the cathode available from the

tank house.

Copper By-Products

Magnetite

Magnetite production reduced to 171 651 tons during

2002 as lower demand from the South African coal

washing industry and a stock draw down during the

commissioning of a new recovery circuit both

influenced output.

Nickel Sulphate

Production rose sharply to 316 tons as higher nickel

levels in certain of the ore sources translated into

higher production in the tank house.

PALABORA MINING COMPANY LIMITED

13

Operations review

Co

pp

er

Sales

Sales of copper rod rose to 71 095 tons, a 7% increase

on 2001. Demand remained firm from all sectors of

the local market and small quantities of rod were also

exported to selected Southern African customers.

Sales of copper cathode declined sharply as reduced

product availability necessitated the rescheduling of

certain export commitments.

Copper prices remained stable during the year

averaging US 70,6c/lb, as compared with US 71,6 c/lb

in 2001. The lacklustre copper price was given some

shine through the depreciation of the local currency

against the US dollar with the result that the average

SA Rand price achieved during 2002 rose by 22% over

the prior year. Negative sentiment in many major

economies weighed down copper prices, which failed

to respond to several significant cutbacks in output,

mainly in North and South America.

14

Operations review

Feeding of Wehnberg machine with starting sheets in the refinery tankhouse

Continual casting of copper anodes on the casting wheel

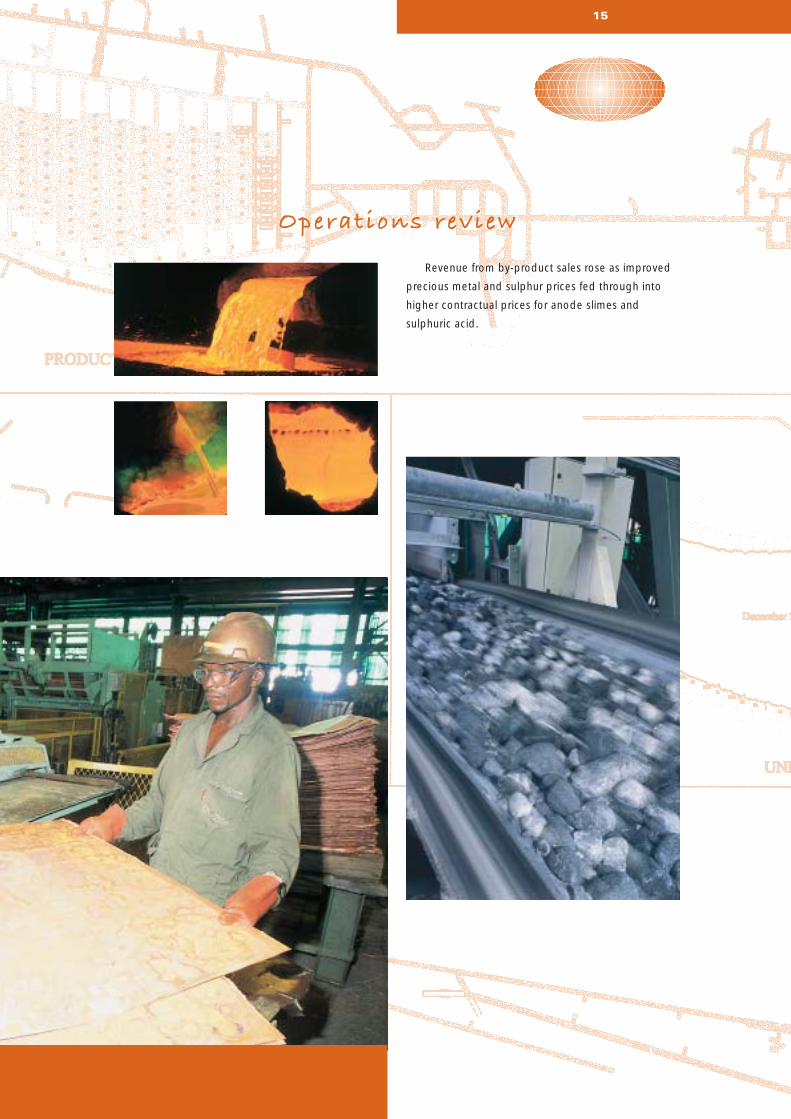

Revenue from by-product sales rose as improved

precious metal and sulphur prices fed through into

higher contractual prices for anode slimes and

sulphuric acid.

15

Operations review

Tarpaulins cover rail trucks filled with vermiculite

16

Ind

ustr

ial M

iner

als

PALABORA MINING COMPANY LIMITED

17

Operations review

Vermiculite

Production of vermiculite improved 40% over the

previous year to 225 033 tons. This set a new record

for the plant. Fortunately 2002 proved to be a dry

year and the projects embarked upon to manage the

effects of high rainfall proceeded according to plan.

The new roof for the covered stockpile was

completed early in the year and construction work on

the Loole creek diversion channel neared completion

at year end.

Plant recoveries improved significantly to 56%,

which was above the planned level of 48% and

allowed for a reduction in plant feed. Product quality

was in line with plan.

Sales volumes to end customers for the full year

improved from 174 392 tons in 2001 to 189 990 tons.

European sales were maintained at the previous years

levels despite a downturn in the international

refractory industry. In America, a key customer

switching grades impacted sales whilst in Asia stiff

competition in the fireproofing industry affected sales.

Palabora still maintains its lead as the main supplier of

vermiculite in the world commanding 40% of the

market

Logistics continues to be an important

component in the industrial minerals market and the

geographic location of Palabora relative to the end

customers contributes almost 70% of the delivered

costs of vermiculite. Ocean freight rates were

successfully contained and remained flat for the year.

Rail transport during the year presented significant

challenges for the logistics team as the local rail

service provider struggled to meet national demands.

Sales revenue was aided by favourable exchange

rates. The development of a particle board in 2002 for

use in dry wall construction in the Far East by one of

Palabora’s vermiculite customers has reached the

stage where the board is now being offered for sale.

Palabora’s vermiculite has been found to be the ideal

raw material in the boards manufacture to meet the

required performance specifications. The impact of

this development will have a significant effect on sales

volumes in the future should the markets find favour

with the end product.

Zirconia

Cessation of mining activities in the copper open pit

also culminated in the closure of the baddeleyite

plants and 193 tons of baddeleyite, the bulk of the

remaining stock, were sold in Europe and America.

Zirconium Basic Sulphate

The zirconium basic sulphate (ZBS) plant upgrade

project was successfully completed, below budget,

on 4 January 2002. However a fire related incident on

29 January 2002 caused extensive damage to the

leaching section of the plant. Repairs to re-instate the

integrity in all sections damaged by the fire

commenced in February and were completed by the

end of April 2002.

Plant operations improved to the extent that the

stringent final product specifications for the major

customer were met by mid December 2002. The plant

is now in a production ramp up mode to meet sales

as they are secured. Total production of ZBS for 2002

was 501 tons of which 399 tons were sold.

Development of markets for the product will be

the key focus for 2003.

Safety

The Industrial Minerals division had an excellent year

on the safety front completing the year without a lost

time injury.

18

The major focus during 2002 was on cost reduction,

improvement of process and equipment effectiveness

and implementation of new business systems.

Asset Management continued to provide high levels

of support and service to the Copper and Industrial

Minerals businesses. The major focus during 2002 was

on cost reduction, improvement of process and

equipment effectiveness and implementation of new

business systems.

The division achieved over eight months LTI Free

during 2002 due to effective safety leadership using

systems such as safety management audit technique

(SMAT) and hazard identification and risk assessment

(HIRA). Asset Management projects team designed

and implemented a new contractor safety

management system for Palabora which included a

revised permit to work system.

Implementation of the SAP R3/4.6c business

system under budget and on time was a major

highlight in 2002. The finance, maintenance, materials

management and human resource modules of SAP

were implemented as part of an overall information

systems strategy that resulted in the mainframe

system being decommissioned. Extensive change

management and communication ensured excellent

business support during “go live” and the business

benefits from SAP are already being realised ahead of

the plan.

Asset Management successfully completed the

total operational performance (TOP) process in

electrical and instrumentation, provisioning and

maintenance services areas during the year. A total of

R36 million was targeted for saving over the next two

years.

PALABORA MINING COMPANY LIMITED

19

O p e r a t i o n s r e v i e w

Service/support departments

Asset planning

The implementation of reliability centred maintenance

(RCM) based equipment strategies was completed on

plan for all critical equipment in both the copper and

industrial minerals businesses. These maintenance

strategies now form the basis for the SAP maintenance

system. A new integrated maintenance planning and

scheduling process was also introduced and is now

fully supported by the SAP system.

Information services and technology

The implementation of the information systems

strategy was the key focus of the IS&T team.

In addition to the implementation of SAP, the team

had to replace the mainframe based legacy systems

and develop a data warehouse and reporting tools to

provide the business with more timely and effective

management information. These projects were

completed on time and under budget.

Provisioning

The provisioning team managed a particularly

challenging year, implementing both SAP materials

management and undertaking TOP successfully.

The SAP implementation required a complete

overhaul of the stock catalogue. SAP has allowed the

integration of the maintenance planning process with

the procurement and warehousing functions.

Cost savings of R10 million were identified in the

Provisioning TOP programme.

A successful programme of asset sales was

undertaken in 2002 to maximise the resale values of

redundant mining equipment from the open pit

operation.

Maintenance services

The maintenance workshops identified R18 million of

cost savings during the TOP programme.

The heavy support equipment team have

achieved excellent availability for the vermiculite

operations through the application of RCM based

maintenance strategies. The maintenance workshops

increased efficiency through the successful

implementation of the “5S” improvement programme

and steadily increased the support for the new

underground mine during 2002.

The power plant provided consistent blowing

rates to the smelter convertors despite the steam

driven blowers reaching the end of their economic

life. These units will be replaced by electric blowers

early in 2003.

Projects

The projects team completed a very challenging year

of project management maintaining an excellent

“on time / on budget” completion rate of over 90%.

The diverse range of projects included the diversion

of Loole Creek to extend the Vermiculite mining

operations, the construction of materials handling

infrastructure for the imported copper concentrate

and demolition and rehabilitation of the Heavy

Minerals and Zirconia plants.

Process improvement

The implementation of the integrated process

management system (IPMS) continued to gather pace

during 2002 with the completion of the copper stream

and commencing in Vermiculite and ZBS plants.

This process improvement approach has provided

significant operational improvements in reducing

smelter cycle times, reducing scrap rates in rod

casting, improved process management in the

concentrator given the variety of feed materials in

2002 and significantly increasing plant recoveries from

the Vermiculite processing plant.

Electrical and instrumentation

This team identified significant savings of R8 million

during the TOP process including better power

management for the business. The instrumentation

team provided excellent support for the IPMS work

throughout Copper and the upgraded ZBS plant.

Ass

et

Man

agem

ent

To enhance operational performance, all employees are encouraged

to participate in reducing costs associated with all mine activities

20

PALABORA MINING COMPANY LIMITED

21

Hum

an R

eso

urce

s

The Company integrated all systems related to

Employment Equity, such as bursaries,

apprenticeships and engineers in training, as well as

recruitment and selection. The Palabora Foundation,

has been actively running Master Maths and ProTec

programmes with tangible results emerging over the

past several years. This has assisted with the

recruitment of historically disadvantaged South

Africans.

Palabora constituted a task team in August 2002,

arising from the Mineral and Petroleum Resources

Development Act and Charter, to monitor the

development of the legislation and to prepare

Palabora’s compliance with anticipated requirements.

The State President has signed the Act, but a

commencement date has not yet been set. The draft

Charter was issued in October 2002, but has not yet

been finalised. Palabora is in a strong position to

comply with the documentary requirements regarding

the proof of surface and mining rights. The task team

is currently compiling statistics relating to human

resources development, progress with employment

equity plans, socio-economic empowerment in the

mine community and rural development and

procurement from Black Economic Empowerment

businesses. Development of Black Economic

Empowerment businesses is carried out through the

support of the Business Linkage Centre, which assists

with skills training and with preparing tender

documents and business plans.

New mines are being developed in South Africa,

which are anticipated to employ some 13 000 people

over the next two years. 1 800 positions are

anticipated to be in the technically skilled categories,

which are the categories in which Palabora

experiences the highest turnover. There is strong

competition for technical skills in the labour market,

with demand exceeding the presently available

supply. Palabora has developed a new system to

attract and retain key South African professionals.

The year 2002 also delivered a reduction in labour

strength:

• Manpower reductions during 2002

January 2002: 2428

December 2002: 2011

The following avenues were used to redeploy those in

redundant positions:

• Voluntary retrenchment: 46

• Voluntary early retirement: 154

• Redeployment: 121

These labour reductions had an impact on

employment equity through demographic change

and a changed profile in terms of skills requirements.

The Company aspired during 2002 to establish a

culture change to entrench leadership principles and

models, meritocracy, and accountability at the

respective levels. As part of this culture change the

Company continues to identify and develop new

leaders through the leadership courses, implementing

new systems and symbols and integrating the

underground mine with the surface organisation.

New systems were developed to entrench leadership

accountability, such as the new recruitment and

selection redesign, the new disciplinary redesign and

the potential assessment system to identify high

potential employees.

The Company continued to use TOP target

setting exercises, to broaden business objectives at

all levels of the organisation and to improve business

skills. Systems, such as IPMS and RCM, have been

successfully implemented and applied across the

business to achieve process and equipment

performance, continuous improvement and to

develop key people in facilitator roles.

Industrial relations

During the year the National Union of Mineworkers

(NUM) suspended the Palabora Branch Committee

due to internal conflict. The suspension has since

been lifted and the NUM Branch Committee

Operations review

re-instated. With the expiry of the term of office of

this committee, a new Branch Committee and

Executive Committee was elected and appointed.

The election and appointment of the new committee

has since ushered a steady improvement in the

relationship between the Company and the NUM.

With this improved relationship, the parties

succeeded in bringing about amendments to the

Recognition Agreement, Retrenchment Agreement

and the Recognition of Full Time Shop Steward

Agreement to be focused with business objectives.

A successful management/unions annual

“bosberaad” was held in the latter part of the year.

The parties shared their future vision of the Company

and the challenges ahead.

The Congress of South African Trade Unions’

(COSATU) two day strike on 1 and 2 October 2002,

protesting against the government’s privatisation

plans had no effect on Palabora.

The National Employees’ Trade Union (NETU) has

agreed to change from the Performance Management

System to the Work Performance System, which is in

line with the Company’s future objectives. The NUM

are also being engaged with the view to change to

this system.

Audits were conducted on the Company’s

Industrial Relations systems and Employment Equity

initiatives, the results of which were largely

satisfactory.

22

Blacksmiths shaping reaming bars

Operations reviewcontinued

PALABORA MINING COMPANY LIMITED

23

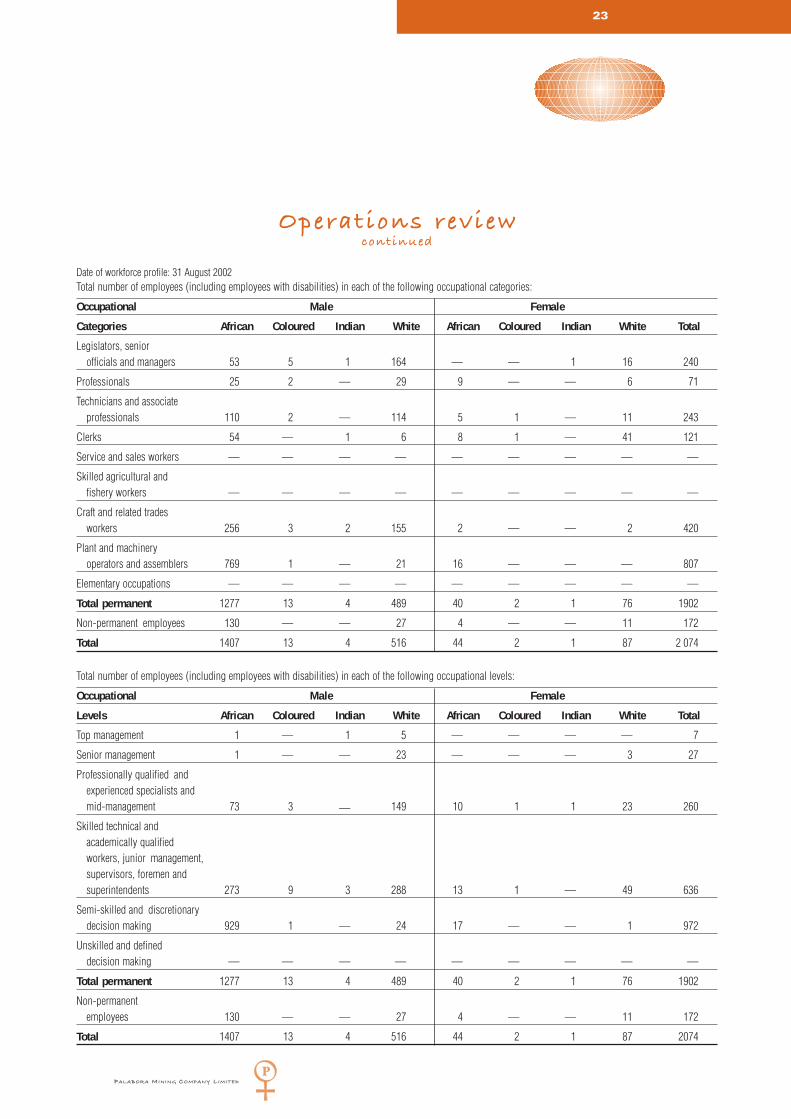

Date of workforce profile: 31 August 2002Total number of employees (including employees with disabilities) in each of the following occupational categories:

Occupational Male Female

Categories African Coloured Indian White African Coloured Indian White Total

Legislators, senior officials and managers 53 5 1 164 — — 1 16 240

Professionals 25 2 — 29 9 — — 6 71

Technicians and associateprofessionals 110 2 — 114 5 1 — 11 243

Clerks 54 — 1 6 8 1 — 41 121

Service and sales workers — — — — — — — — —

Skilled agricultural andfishery workers — — — — — — — — —

Craft and related tradesworkers 256 3 2 155 2 — — 2 420

Plant and machineryoperators and assemblers 769 1 — 21 16 — — — 807

Elementary occupations — — — — — — — — —

Total permanent 1277 13 4 489 40 2 1 76 1902

Non-permanent employees 130 — — 27 4 — — 11 172

Total 1407 13 4 516 44 2 1 87 2 074

Total number of employees (including employees with disabilities) in each of the following occupational levels:

Occupational Male Female

Levels African Coloured Indian White African Coloured Indian White Total

Top management 1 — 1 5 — — — — 7

Senior management 1 — — 23 — — — 3 27

Professionally qualified and experienced specialists andmid-management 73 3 — 149 10 1 1 23 260

Skilled technical andacademically qualifiedworkers, junior management, supervisors, foremen andsuperintendents 273 9 3 288 13 1 — 49 636

Semi-skilled and discretionary decision making 929 1 — 24 17 — — 1 972

Unskilled and defineddecision making — — — — — — — — —

Total permanent 1277 13 4 489 40 2 1 76 1902

Non-permanentemployees 130 — — 27 4 — — 11 172

Total 1407 13 4 516 44 2 1 87 2074

Operations reviewcontinued

24

The development of the underground continues

towards its target of 30 000 tons per day

PALABORA MINING COMPANY LIMITED

25

Operations review

Und

erg

roun

d

The underground project achieved a number of

significant milestones in 2002 as the mine moved

toward completion. The installation and successful

commissioning of crushers two and three were

achieved on time with minimum delay to the

production schedule. The final crusher is due for

commissioning in the second quarter 2003.

Lateral development for the year totalled 3 690m.

This development continued ahead of plan.

The eastern development of the mine is now

complete leaving a reduced quantity of development

required in 2003 to complete the western

development.

Undercutting progressed well during the year with

42 950 sqm exposed, which was 116% of target.

The cumulative area of undercutting equates to

100 086 sqm which represents 85% of the total

project. On reflection, the method of using an

“inclined undercut” has proved to be very successful

and has allowed a relatively high rate of advance to be

achieved in a safe and efficient manner.

Draw bell development continued steadily,

achieving a cumulative total of 113 draw bells by the

end of 2002. This was against a target of 120 and

the project total of 166. The provision of concrete

roadways to ensure minimum load and haul cycle

times continues on plan.

The key issue for 2002 has been the lower than

expected production ramp up. The coarse

fragmentation of the rock at this early stage of the

cave development has caused significant challenges

with secondary breaking of the rock. The prototype

equipment developed specifically for Palabora to deal

with secondary breaking has experienced design and

maintenance related issues. Improvement actions are

currently underway to address these equipment

reliability issues.

The establishment of the final manning levels and

the transfer of project functions to Palabora is well

underway, in addition to the planned demobilisation

of contract resources in line with a project completion

in 2003.

PALABORA MINING COMPANY LIMITED

26

Statement of responsibility by the board of directors

The Directors are responsible for the preparation, integrity and fair presentation of the financial statements of Palabora

Mining Company Limited and its subsidiaries. The financial statements, presented on pages 36 to 63, have been

prepared in accordance with South African Statements of Generally Accepted Accounting Practice, and include amounts

based on judgements and estimates made by management. The directors also prepared the other information included

in the annual report and are responsible for both its accuracy and its consistency with the financial statements.

The going concern basis has been adopted in preparing the financial statements.The directors have no reason to believe

that the Company or the Group will not be a going concern in the foreseeable future based on forecasts and available

cash resources. The viability of the Company and the Group are supported by the financial statements.

The financial statements have been audited by the independent accounting firm, PricewaterhouseCoopers Inc, which

was given unrestricted access to all financial records and related data, including minutes of all meetings of shareholders,

the Board of Directors and committees of the Board. The Directors believe that all representations made to the

independent auditors during their audit were valid and appropriate. PricewaterhouseCoopers Inc's audit report is

presented on page 35.

The financial statements were approved by the board of directors on 14 May 2003 and are signed on its behalf.

J H K Sachikonye D S Sadler

(Acting) Chairman Managing Director

Statement by the company secre tary

I, the undersigned, in my capacity as Company Secretary, do hereby confirm that for the financial year ended

31 December 2002, Palabora Mining Company Limited has lodged with the Registrar of Companies all such returns as

are required of a public Company in terms of the Companies Act 61 of 1973, as amended, and that all such returns are

true, correct and up to date.

E B R Hone

Company Secretary

14 May 2003

Palabora Mining Company, its subsidiaries and its joint venture (“the Group”) are committed to the principles of

openness, integrity and accountability advocated in the King Report on Corporate Governance. Accordingly, the

directors have taken careful note of the new recommendations contained in the second King Report on Corporate

Governance issued in March 2002. A great deal of the Group’s practices are already in line with these requirements.

The directors have identified three areas where strict compliance with King II would add little or no value and where

alternative, workable systems existed.These three areas required some adjustment to bring them into line with Rio Tinto

plc’s policies and procedures. These areas are:

• Executive directors’ remuneration, which is determined according to the holding Company’s (Rio Tinto plc) scales of

remuneration.

• Directors’appointments, which are influenced by the two major shareholders; Rio Tinto plc and Anglo American plc;

and

• Evaluations and risk management, which are managed by the Company’s Executive Committee.

However, attention will be given during the remainder of 2003 to the other recommended practices in the code of

Corporate Practices and Conduct (“the Code”) which still need to be adopted by the Group. By supporting the code the

directors have demonstrated their commitment to conduct the enterprise with integrity and in accordance with generally

accepted corporate practices.

Application

Although the code is generally applied to all entities in the Group, it is specifically adopted by Palabora Mining Company

Limited, the Company, as the subsidiaries are not material in size. Specifically, the directors report on the matters that

follow:

Board of Directors

The Company has a unitary Board structure. The Board meets on a quarterly basis, retains effective control over the

Company and monitors executive management.

Since the beginning of 2003 the board of directors comprises nine non-executive directors and three executive

directors. The three executive directors and three of the non-executive directors are nominees of Rio Tinto plc and a

further two non-executive directors are nominees of Anglo American plc. The remaining four non-executive directors

are independent appointees. During part of 2002 there were four executive directors. Mr Z W Ntuli, an executive director

and a Rio Tinto nominee, was chairman until 31 December 2002 when he retired. Mr J H K Sachikonye, a Rio Tinto

nominee, as deputy chairman, is acting chairman until a successor to Mr Ntuli is appointed later in the year. The new

chairman will be an independent non-executive director as recommended by King II.

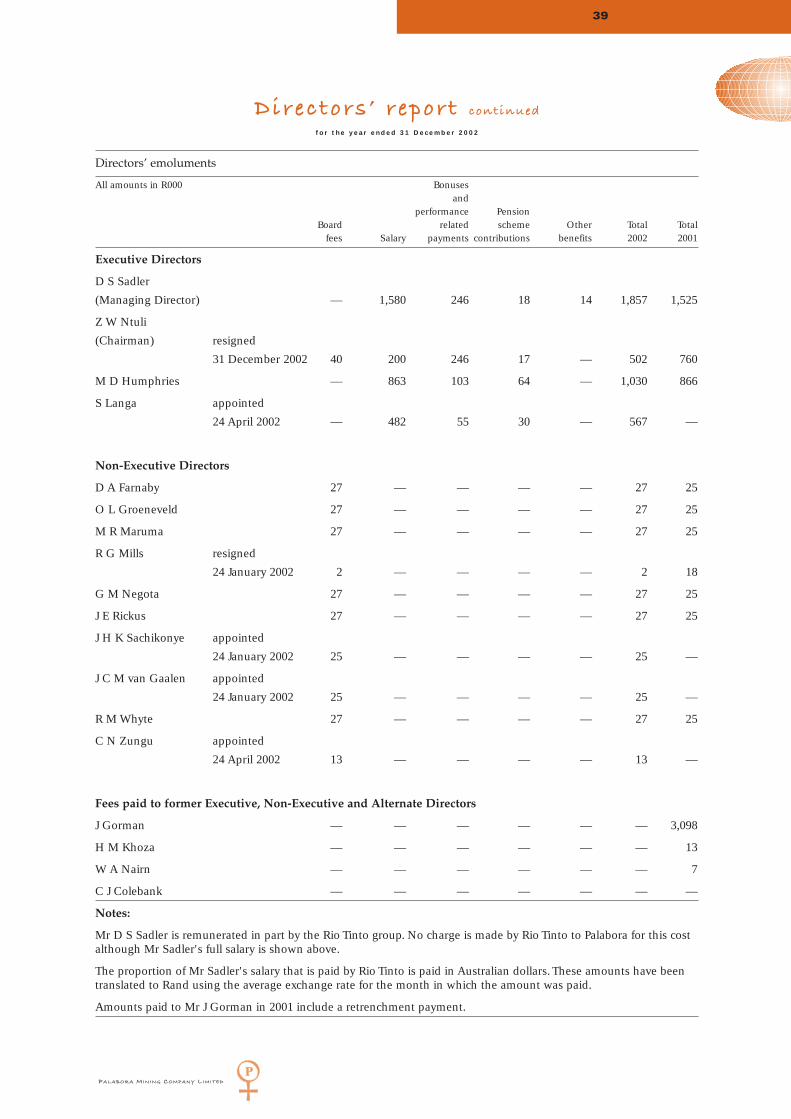

Full details regarding changes in the Company’s directorate and emoluments paid to directors are disclosed in the

directors’ report on pages 36 to 39.

Details of directors and alternate directors presently constituting the Board appear on pages 5 to 7.

There are no contracts of service between any directors and the Company or any of its subsidiaries that are

terminable at periods of notice exceeding one year and requiring payment of compensation.

No director holds any shares beneficially in the Company and there are no share option schemes.

A third of the directors are subject to retirement by rotation and re-election by shareholders each year in accordance

with the Company’s articles of association. In addition, all directors are subject to re-election by shareholders at the first

annual general meeting following their appointment. The appointment of new directors is approved by the Board as a

whole. The names of the directors submitted for re-election are accompanied by sufficient biographical details in the

notice of the annual general meetings to enable shareholders to make an informed decision in respect of their re-

election.

27

Corporate governance statement

PALABORA MINING COMPANY LIMITED

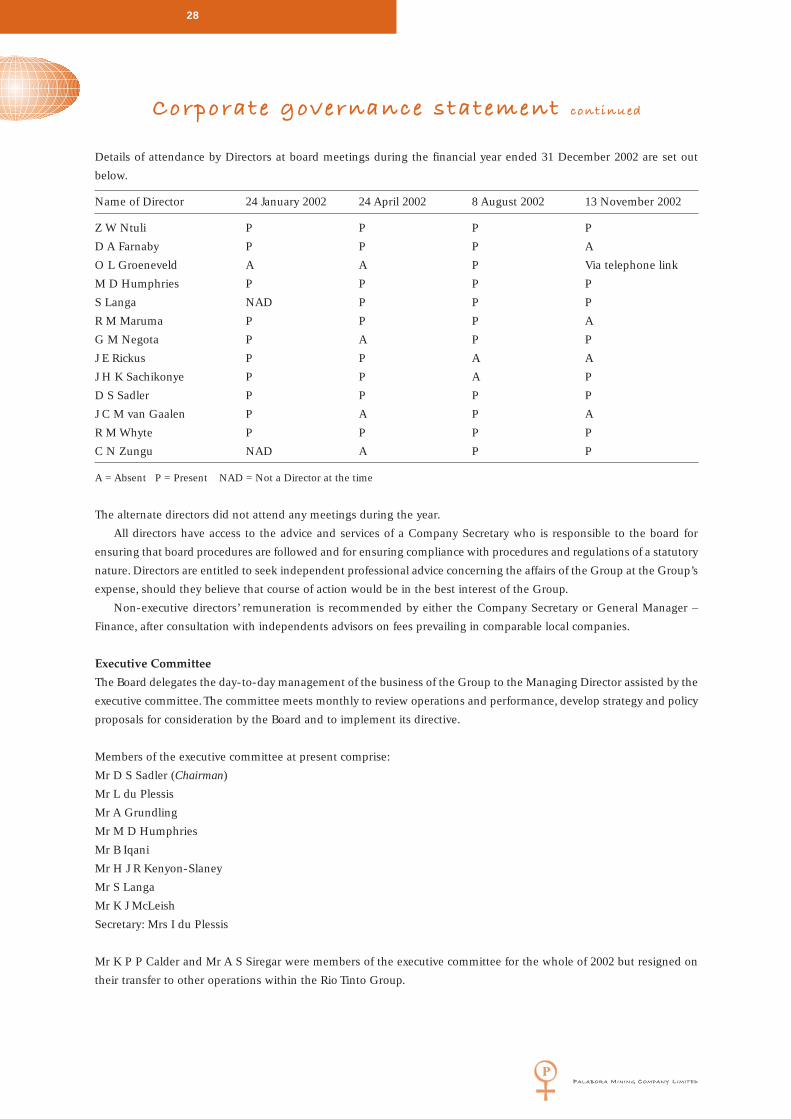

Details of attendance by Directors at board meetings during the financial year ended 31 December 2002 are set out

below.

Name of Director 24 January 2002 24 April 2002 8 August 2002 13 November 2002

Z W Ntuli P P P P

D A Farnaby P P P A

O L Groeneveld A A P Via telephone link

M D Humphries P P P P

S Langa NAD P P P

R M Maruma P P P A

G M Negota P A P P

J E Rickus P P A A

J H K Sachikonye P P A P

D S Sadler P P P P

J C M van Gaalen P A P A

R M Whyte P P P P

C N Zungu NAD A P P

A = Absent P = Present NAD = Not a Director at the time

The alternate directors did not attend any meetings during the year.

All directors have access to the advice and services of a Company Secretary who is responsible to the board for

ensuring that board procedures are followed and for ensuring compliance with procedures and regulations of a statutory

nature. Directors are entitled to seek independent professional advice concerning the affairs of the Group at the Group’s

expense, should they believe that course of action would be in the best interest of the Group.

Non-executive directors’ remuneration is recommended by either the Company Secretary or General Manager –

Finance, after consultation with independents advisors on fees prevailing in comparable local companies.

Executive Committee

The Board delegates the day-to-day management of the business of the Group to the Managing Director assisted by the

executive committee. The committee meets monthly to review operations and performance, develop strategy and policy

proposals for consideration by the Board and to implement its directive.

Members of the executive committee at present comprise:

Mr D S Sadler (Chairman)

Mr L du Plessis

Mr A Grundling

Mr M D Humphries

Mr B Iqani

Mr H J R Kenyon-Slaney

Mr S Langa

Mr K J McLeish

Secretary: Mrs I du Plessis

Mr K P P Calder and Mr A S Siregar were members of the executive committee for the whole of 2002 but resigned on

their transfer to other operations within the Rio Tinto Group.

PALABORA MINING COMPANY LIMITED

28

Corporate governance statement continued

Board Audit Committee

A board appointed Audit Committee was established in 1995 and is an important element of the Board’s system of

monitoring and control. The Board Audit Committee has adopted a formal written Audit Committee Charter, which

contains terms of reference dealing with membership, structure, and levels of authority and duties. To assist the Board

Audit Committee in discharging its responsibilities, internal audits are performed throughout the Group, according to a

three year internal audit plan, and function under the control of, and report to, the Internal Audit Superintendent. The

internal audits are performed by teams of appropriate, qualified and experienced employees and by the Business Risk

Services Division of Ernst & Young. The primary mandate of the Group’s internal auditors is to examine, review and

evaluate the effectiveness of the applicable operating activities, the attendant business risks and the systems of internal

operation and financial control, so as to bring material deficiencies, instances of non-compliance, high-risk exposure

and development work needs to the attention of management for resolution. The Internal Auditing Superintendent

reports on an administrative basis to the General Manager – Finance, who is an executive director, and functionally to

the Board Audit Committee.

Members of the Board Audit Committee at present comprise:

Mr J H K Sachikonye (Chairman)

Mr J Ashmore

Mrs D A Farnaby

Mr M Leech

Mr J C M van Gaalen

Secretary: Ernst & Young

While the Chairman of the Board Audit Committee, Mr Sachikonye is a Non-Executive Director, he is a Rio Tinto

nominee. The appointment of a non-executive independent director to the position of chairman of this committee will

be reviewed during 2003. Mr van Gaalen is a non-executive director of the Company and a Anglo American nominee.

Mrs Farnaby is a non-executive independent director. Mr Ashmore is a Senior Surveillance Officer at the Surveillance

Division of the JSE Securities Exchange South Africa. Mr Leech is General Manager – Commercial, of Rossing Uranium

in Namibia.

Both the external and internal auditors have free access to this committee and to the Chairman of the Board Audit

Committee and where necessary, to the Chairman of the Board and the Managing Director. All important findings

arising from the audit are brought to the attention of the committee and, if necessary, to the board. Meetings are held

at least four times a year and are attended by the Group’s internal and external auditors and the General Manager –

Finance, to review the financial statements and accounting policies, the effectiveness of management information and

other systems of internal control, the interim financial position, the effectiveness of the internal audit function and the

internal and external auditors’ findings.

Details of attendance by members of the Board Audit Committee during the financial year ended 31 December 2002 are

set out below.

Name of Member 23 January 2002 10 April 2002 24 July 2002 30 October 2002

J Ashmore P P P P

D A Farnaby* NAM NAM NAM NAM

M Leech P P P P

G M Negota P NAM NAM NAM

J H K Sachikonye P P A P

J C M van Gaalen P P P P

*appointed a member 13 November 2002 A = Absent P = Present NAM = Not a member at the time

PALABORA MINING COMPANY LIMITED

29

Corporate governance statement continued

Internal Control

The Group maintains systems of internal control over financial reporting and over safeguarding of assets against

unauthorized acquisition, use or disposition, which are designed to provide reasonable assurance to the Board of

Directors regarding the preparation of reliable published financial statements and the safeguarding of the Company’s

assets. The systems include a documented organizational structure and division of responsibility, established policies

and procedures, and the careful selection, training and development of staff. Internal auditors monitor the operation of

the internal control system and report findings and recommendations to management and the Board of Directors.

Corrective actions are taken to address control deficiencies and other opportunities for improving the system as they are

identified. The board, operating through its Audit Committee, provides oversight of the financial reporting process.

There are inherent limitations in the effectiveness of any system of internal control, including the possibility of

human error and the circumvention or overriding of controls. Accordingly, even an effective internal control system can

provide only reasonable assurance with respect to financial statement preparation and the safeguarding of assets.

Furthermore, the effectiveness of an internal control system can change with circumstances.

The Group assessed its internal control system as at 31 December 2002 in relation to the criteria for effective internal

control over financial reporting as set out in the holding Company’s Group Internal Control Questionnaire. Based on its

assessment, the Group believes that, as at 31 December 2002 and at the date of this report, its system of internal control

over financial reporting and over safeguarding of assets against unauthorized acquisitions, use or disposition, met those

criteria.

Safety, Health, Environment and Quality Executive Committee

The Company attaches great importance to the safety and health of its employees and to the environment at large. One

of the prime objectives of this committee is the elimination of all accidents of a mining nature.

Through a comprehensive environmental policy, the committee assesses the impact that the Company’s operations

might have on the environment.

The committee, which meets on a monthly basis, comprises

Mr D S Sadler (Chairman)

Mr L du Plessis

Mr A Grundling

Mr M D Humphries

Mr I Iqani

Mr H J R Kenyon-Slaney

Mr S Langa

Mr K J McLeish

Secretary: Mrs I du Plessis

Mr K P P Calder and Mr A S Siregar were members of this committee for the whole of 2002 but resigned on their

transfer to other operations in the Rio Tinto Group.

Risk Management

The board is responsible for the total risk management process within the Group. The Executive Committee is

accountable to the board and has established a group-wide system of internal control to manage significant group risks.

This system supports the board in discharging its responsibility for ensuring that the range or risks associated with the

Group’s operations, are effectively managed in support of the creation and preservation of shareholder wealth.

The management of risk encompasses all significant risks, including operational risk, which could undermine the

achievement of business objectives. The board has approved the level of acceptable risk and required that operations

manage and report in terms thereof. Issues and circumstances which could give rise to material adverse reputational

considerations are also considered to be unacceptable risks.

PALABORA MINING COMPANY LIMITED

30

Corporate governance statement continued

Some of the major risks to which the Group is exposed are listed below:

• Financing the business

There is a need to finance the business because of the delay in the ramp-up of the underground mine and the

strenghening of the Rand against the US dollar. Management is taking the necessary action to ensure that adequate

funding is available. In the circumstances the board is of the opinion that it is unlikely that dividend payments will

recommence within the next two years. As mentioned in the Chairman’s statement, Rio Tinto, Palabora’s largest single

shareholder, has made available a US$50 million short-term loan facility. This will meet working capital and other

requirements until the process of raising additional financial resources is complete.The Board of Directors agreed in May

2003 to raise additional capital by means of a shareholder supported re-financing package.

The funds issue will be utilised to service existing debt commitments as well as to allow completion of the

underground project and other fixed capital commitments, including enhancements to various plants.

• HIV/AIDS

Discussions have started with the National Employees Trade Union (NETU) and the National Union

of Mineworkers (NUM) aimed at forming a partnership to jointly develop programmes to minimize the impact of

HIV/AIDS on all stakeholders. It is expected that an agreement will be signed in the near future. In the meantime the

Company’s HIV/AIDS management system is in place and is focusing on education and awareness, condom

distribution, voluntary counselling and testing, awareness about and treatment of STIs and opportunistic diseases, et

cetera.

• The Underground Mine

Full production from the new block cave underground mine was scheduled for the end of 2002, but this has not occurred

as a result of difficulties experienced with the ability of the secondary breaking equipment to deal with large rocks.

The ramp up to full production is delayed and is not now expected until the third quarter of 2003. This delay has

stretched financial resources. Other significant risks are water management and ground conditions in the faulted

western end of the mine.

• Industrial Minerals

Managing the threat from Chinese Vermiculite sources will be a key issue. As regards Zirconium Basic Sulphate,

it is essential that low Titanium levels in Zircon sand be maintained to meet customer specifications, as well as to

produce quality product on demand. Work will continue on optimising the process so that the constraint becomes sales