Embed Size (px)

DESCRIPTION

FOREX ASSOCIATION OF INDIA

Citation preview

FOREX ASSOCIATION OF INDIA

Seminar on the Credit Support Annex

6th April 2013

U N D E R S T A N D I N G C O L L A T E R A L F O R O T C D E R I V A T I V E S

Christopher Moores

NT

IAL

ST

RIC

TL

YP

RI

VA

TE

AN

DC

ON

FI

DE

English_General

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

J.P. Morgan is a marketing name for investment banking businesses of JPMorgan Chase & Co. and its subsidiaries worldwide. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by a combination of J.P. Morgan Securities LLC, J.P. Morgan Limited, J.P. Morgan Securities Ltd. and the appropriately licensed subsidiaries of JPMorgan Chase & Co. in EMEA and Asia-Pacific, and lending, derivatives and other commercial banking activities are performed by JPMorgan Chase Bank, N.A. J.P. Morgan deal team members may be employees of any of the foregoing entities.

Agenda

OTC Derivatives Collateral - Introduction and Basic s 1

OTC Derivatives Collateral - Legal Concepts and Agreement Parameters 8

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

OTC Derivatives Collateral - Collateral Assets 18

OTC Derivatives Collateral - The Operational Process 21

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

F O R E X A S S O C I A T I O N O F I N D I A 1

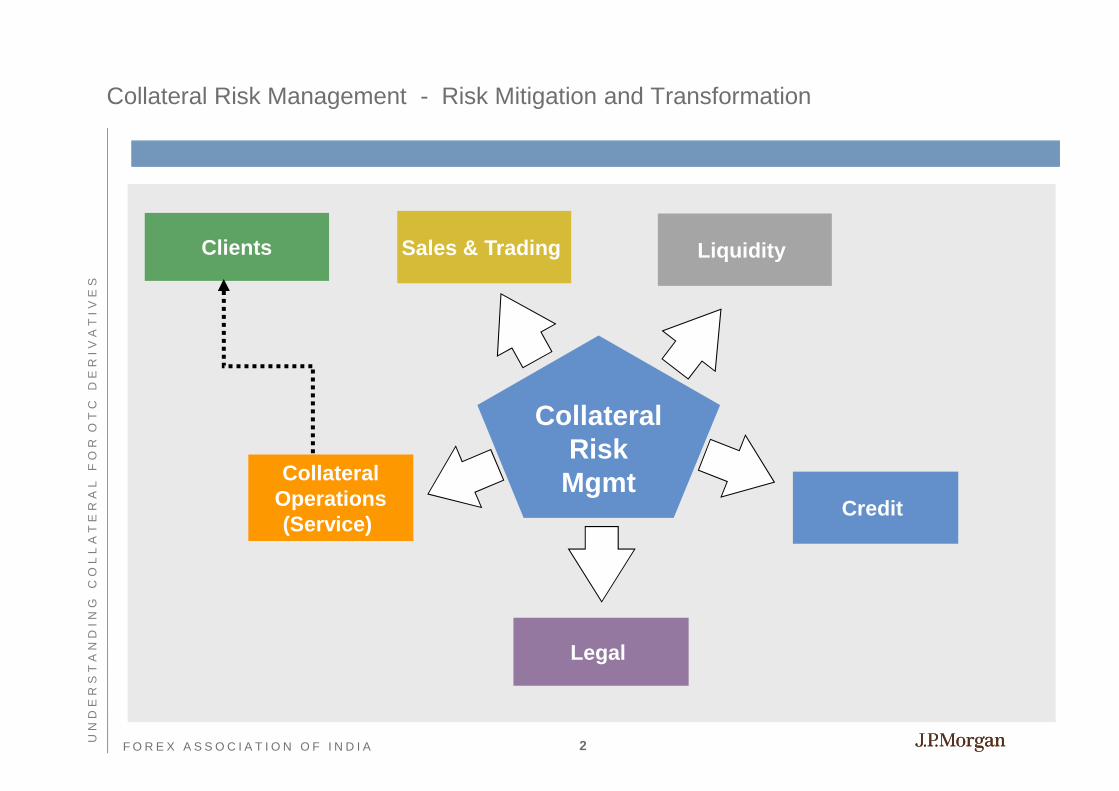

Collateral Risk Management - Risk Mitigation and Transformation

Sales & TradingClients Liquidity

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

CollateralOperations(Service)

Collateral Risk

MgmtCredit

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

(Service)

Legal

2

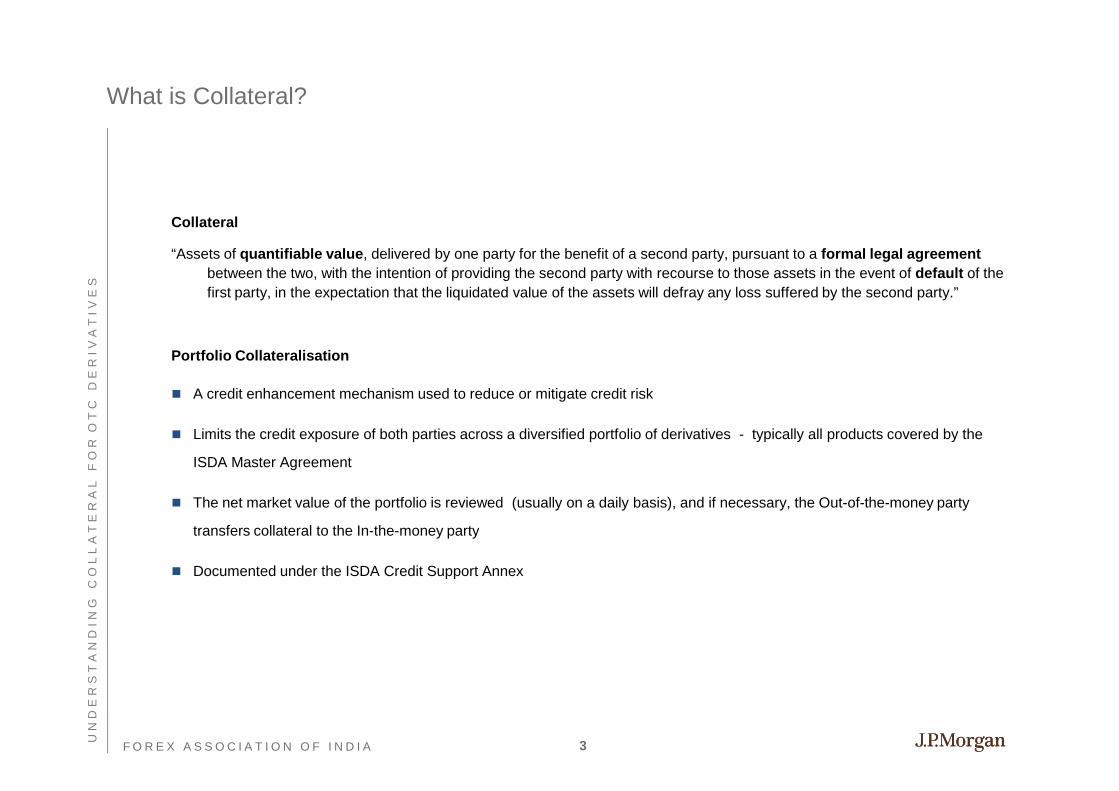

What is Collateral?

Collateral

“Assets of quantifiable value , delivered by one party for the benefit of a second party, pursuant to a formal legal agreement

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S between the two, with the intention of providing the second party with recourse to those assets in the event of default of the

first party, in the expectation that the liquidated value of the assets will defray any loss suffered by the second party.”

Portfolio Collateralisation

� A credit enhancement mechanism used to reduce or mitigate credit risk

� Limits the credit exposure of both parties across a diversified portfolio of derivatives - typically all products covered by the

ISDA Master Agreement

� The net market value of the portfolio is reviewed (usually on a daily basis), and if necessary, the Out-of-the-money party

transfers collateral to the In-the-money party

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

transfers collateral to the In-the-money party

� Documented under the ISDA Credit Support Annex

3

Risk mitigation tool which offers mutual protection

What is collateral and

Executive Summary

� Collateral is the most effective risk mitigation tool for derivative transactions

� It allows each party to receive cash/securities as guarantee of payment of the Mark-to-Market (MTM) of a derivative

1

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

mutual protection

Added benefits

ISDA + Credit Support Annex

(CSA)

collateral andwhy is it

beneficial?

How is a collateral relationship

established and what are the

key parameters?

� Collateral protects each party against a default of the other, reducing the risk of entering into derivatives

� All the terms of the collateral relationship are agreed in the Credit Support Annex (CSA), which is an attachment to the ISDA Master Agreement

� There are a number of key collateral terms that are flexible and subject to negotiation between the parties

2

� Reduced counterparty risk means enhanced capacity to trade greater volume, complexity and tenor. Lower capital requirements and lower trading costs for both parties

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

Who calls for collateral and

when?

key parameters? and subject to negotiation between the parties

How does collateral work mechanically?

� The party who is In-The-Money on each Collateral Valuation Date has the right (not the obligation) to make a Collateral Call on the other party.

� There are ways to reduce the operational burden on parties

3

4

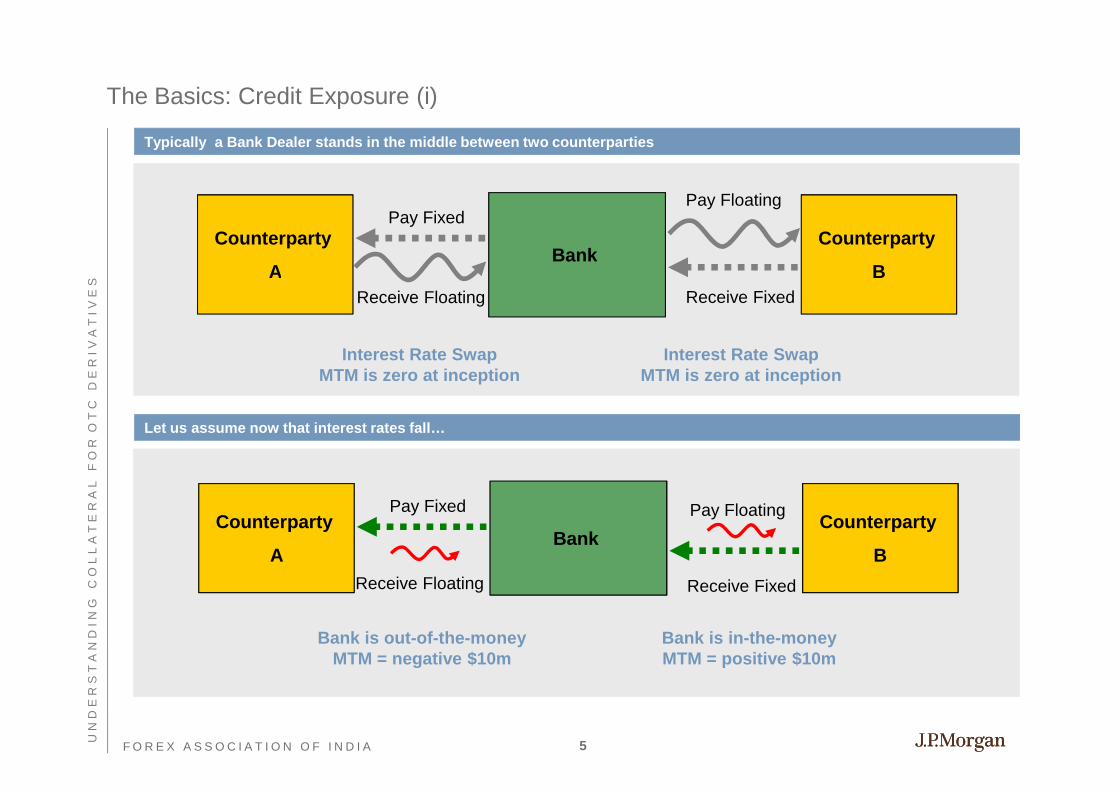

The Basics: Credit Exposure (i)

Typically a Bank Dealer stands in the middle betwe en two counterparties

BankCounterparty

A

Counterparty

B

Pay FixedPay Floating

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

BankA B

Let us assume now that interest rates fall…

Pay FixedCounterparty Counterparty

Pay Floating

Receive Floating

Interest Rate SwapMTM is zero at inception

Receive Fixed

Interest Rate SwapMTM is zero at inception

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

BankCounterparty

A

Receive Fixed

Counterparty

BReceive Floating

Bank is out-of-the-moneyMTM = negative $10m

Bank is in-the-moneyMTM = positive $10m

5

The Basics: Credit Exposure (ii)

Let us assume that Counterparty B defaults at that particular moment in time…

Bank

Pay FixedCounterparty

A

Counterparty

B

Pay Floating

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S A

Receive Fixed

BReceive Floating

Bank is out-of-the-moneyMTM = negative $10m

Bank is in-the-moneyMTM = positive $10m

… the Bank is then left with just one side, where it is out-of-the-money

Bank

Pay FixedCounterparty

� Bank will no longer receive the payment of $10m from Counterparty B, but will still have to honour the $10m payment to Counterparty A

� That means that Bank loses $10m upon default of

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

BankA

Receive Floating

Bank is out-of-the-moneyMTM = negative $10m

� That means that Bank loses $10m upon default of Counterparty B. That is our Credit Exposure to Counterparty B as of today

6

Collateral in more depth

Collateral Reduces Credit Exposure Collateralisation protects

Exposure

� Derivatives generate Credit Exposure

Credit Limit / appetite

� If our counterparty defaults half way down the life of the trade…

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

Time

� Collateralisation reduces Credit Exposure, allowing for:

� Significant Credit Risk reduction

� More trades under the same credit appetite

� More complex structures / longer tenors, etc.

Credit Limit / appetite

� With Collateral in place, your new exposure curve Reduced Credit Exposure also means….

TimeLoss

Time

Without Collateral

With Collateral

With Collateral

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

Exposure

Time

Credit Limit / appetite

� With Collateral in place, your new exposure curve appears as follows:

Without Collateral

With Collateral

� Better Credit Pricing (Lower CVA): because the level of expected exposure is lower, so are the costs of hedging that exposure in the CDS market

� Lower Capital Requirements for the same Derivatives portfolio

7

Agenda

OTC Derivatives Collateral - Legal Concepts and Agr eement Parameters 8

OTC Derivatives Collateral - Introduction and Basics 1

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

OTC Derivatives Collateral - Collateral Assets 18

OTC Derivatives Collateral - The Operational Process 21

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

F O R E X A S S O C I A T I O N O F I N D I A 8

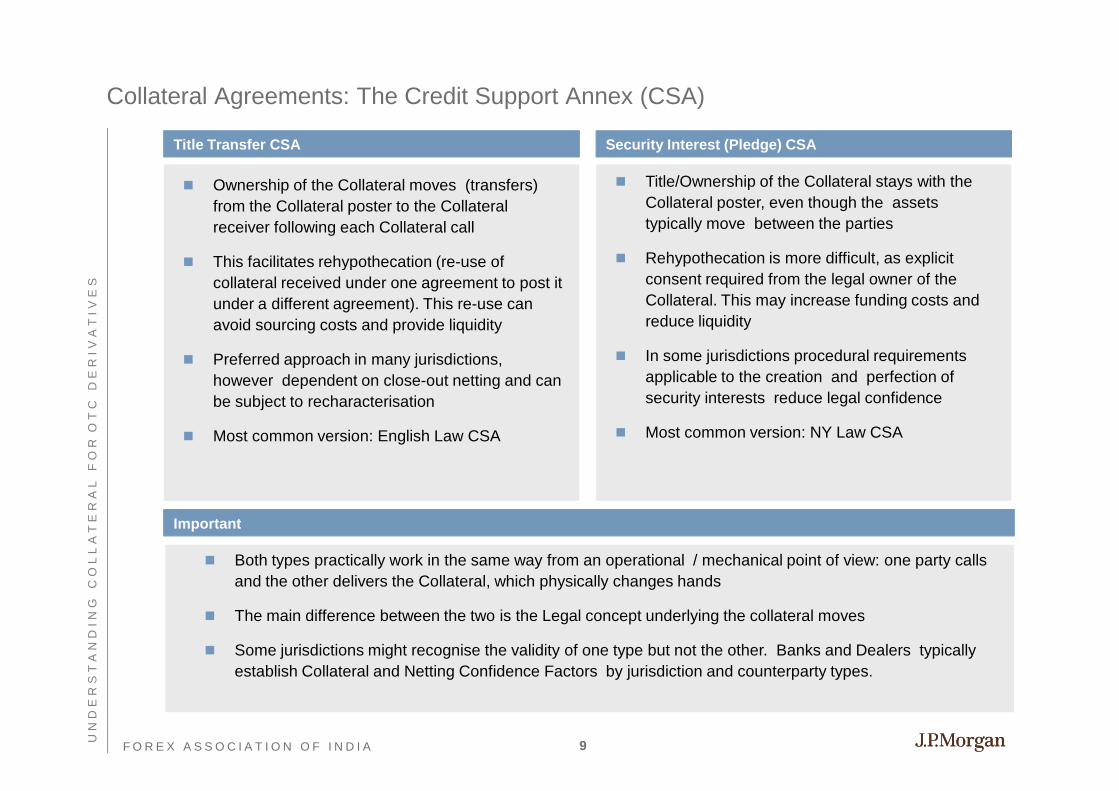

Collateral Agreements: The Credit Support Annex (CSA)

Title Transfer CSA Security Interest (Pledge) CSA

� Ownership of the Collateral moves (transfers) from the Collateral poster to the Collateral receiver following each Collateral call

� This facilitates rehypothecation (re-use of

� Title/Ownership of the Collateral stays with the Collateral poster, even though the assets typically move between the parties

� Rehypothecation is more difficult, as explicit

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

� This facilitates rehypothecation (re-use of collateral received under one agreement to post it under a different agreement). This re-use can avoid sourcing costs and provide liquidity

� Preferred approach in many jurisdictions, however dependent on close-out netting and can be subject to recharacterisation

� Most common version: English Law CSA

� Rehypothecation is more difficult, as explicit consent required from the legal owner of the Collateral. This may increase funding costs and reduce liquidity

� In some jurisdictions procedural requirements applicable to the creation and perfection of security interests reduce legal confidence

� Most common version: NY Law CSA

Important

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

Important

� Both types practically work in the same way from an operational / mechanical point of view: one party calls and the other delivers the Collateral, which physically changes hands

� The main difference between the two is the Legal concept underlying the collateral moves

� Some jurisdictions might recognise the validity of one type but not the other. Banks and Dealers typically establish Collateral and Netting Confidence Factors by jurisdiction and counterparty types.

9

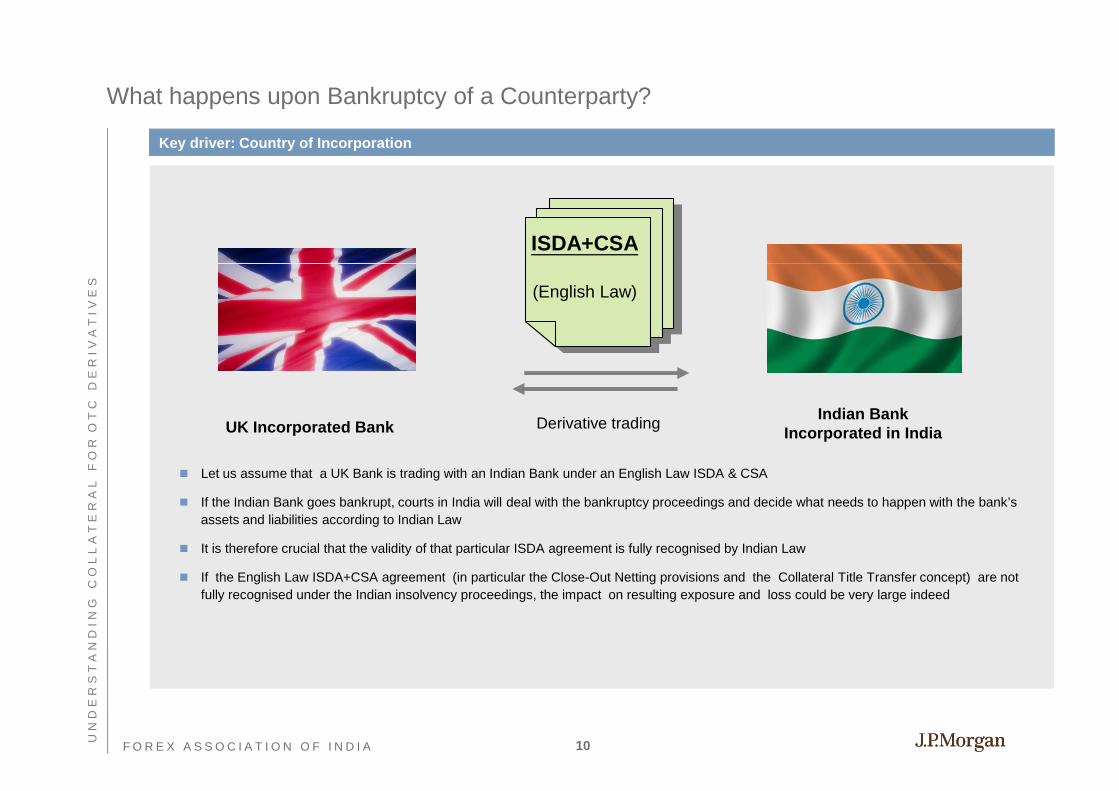

What happens upon Bankruptcy of a Counterparty?

Key driver: Country of Incorporation

ISDA+CSA

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

� Let us assume that a UK Bank is trading with an Indian Bank under an English Law ISDA & CSA

� If the Indian Bank goes bankrupt, courts in India will deal with the bankruptcy proceedings and decide what needs to happen with the bank’s assets and liabilities according to Indian Law

UK Incorporated BankIndian Bank

Incorporated in India

(English Law)

Derivative trading

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

� It is therefore crucial that the validity of that particular ISDA agreement is fully recognised by Indian Law

� If the English Law ISDA+CSA agreement (in particular the Close-Out Netting provisions and the Collateral Title Transfer concept) are not fully recognised under the Indian insolvency proceedings, the impact on resulting exposure and loss could be very large indeed

10

Parameters in a Collateral Agreement

General (usually a given)

� Title Transfer / Security Interest

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S Specific Terms (usually the object of negotiation b etween the parties)

� Acceptable Collateral Assets and Haircuts

� Thresholds

� Minimum Transfer Amount (MTA ) and Rounding

� Valuation Frequency

� Independent Amounts

� Valuation Agent

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

� Interest Rates

11

Threshold

Threshold = Unsecured Exposure

MTM

Threshold

� The Threshold is the level that the MTM needs to reach before a party can make a Collateral Call

$5m

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

t

Threshold� For example, if the Threshold is $5m,

until the MTM reaches $5m, no collateral calls will be made. Once that level is reached, the party who makes the collateral call, will only be able to call for the excess

No Collateral Calls would be madeuntil this point in time

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

Threshold

� Once the threshold level is surpassed, calls are made only on the amount above that level (i.e. if the MTM is $7m and the threshold is $5m, a collateral call is made for $2m only)

� Therefore the threshold is the level of unsecured exposure that one party takes towards the other (and in case of default it is – potentially – the loss level as well)

Collateral

12

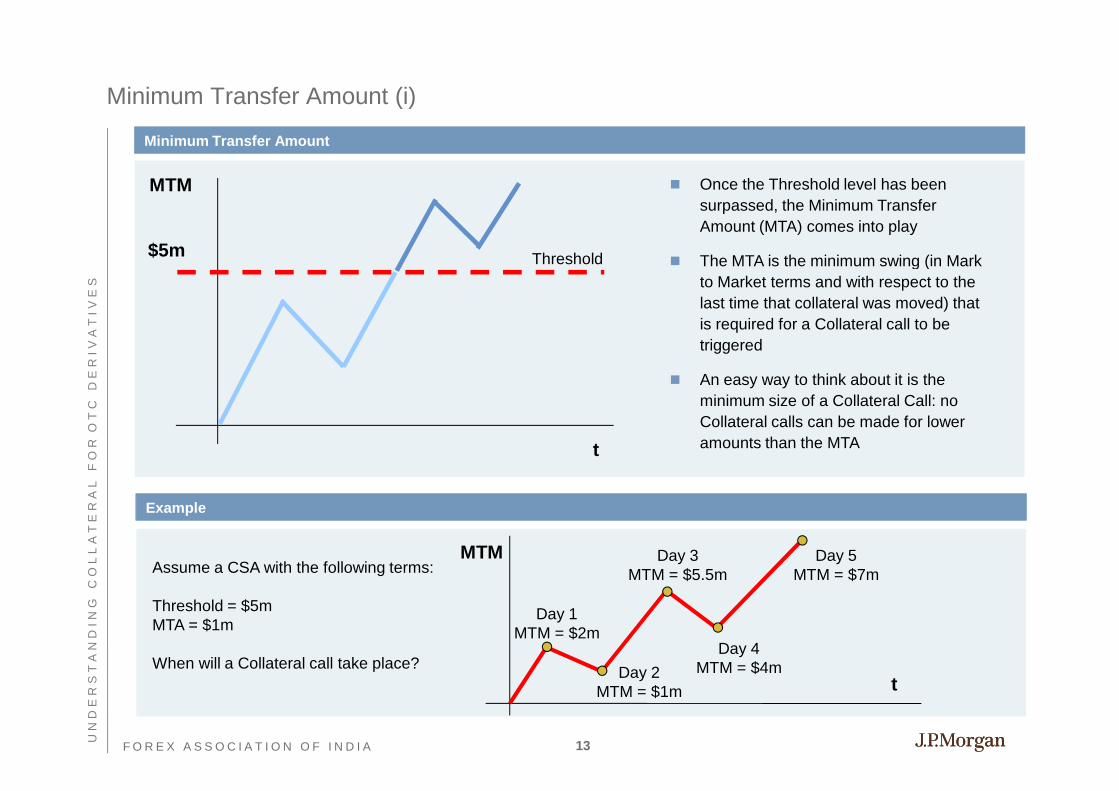

Minimum Transfer Amount (i)

Minimum Transfer Amount

MTM

Threshold

� Once the Threshold level has been surpassed, the Minimum Transfer Amount (MTA) comes into play

� The MTA is the minimum swing (in Mark $5m

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

t

Threshold � The MTA is the minimum swing (in Mark to Market terms and with respect to the last time that collateral was moved) that is required for a Collateral call to be triggered

� An easy way to think about it is the minimum size of a Collateral Call: no Collateral calls can be made for lower amounts than the MTA

Example

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

Assume a CSA with the following terms:

Threshold = $5mMTA = $1m

When will a Collateral call take place?

Day 1MTM = $2m

Day 2MTM = $1m

Day 3MTM = $5.5m

Day 4MTM = $4m

Day 5MTM = $7m

MTM

t

13

Minimum Transfer Amount (ii)

Threshold = $5m , MTA = $0

MTM � A low MTA allows us to react very quickly to small changes in MTM…

� …but the $5m threshold means that we $5m

Collateral

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

t

will never be able to call for the first $5m of exposureWe will never

be able to call for these $5m

Threshold = $0m , MTA = $5

MTM� Until the MTM reaches $5m, both

arrangements yield the same result (no collateral calls)…

$5m

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

t

� … but as soon as the MTM is over that level, we will be able to call for the full exposure…

� …although we will have to wait for the MTM to move by another $5m to call again

$5m

Collateral

14

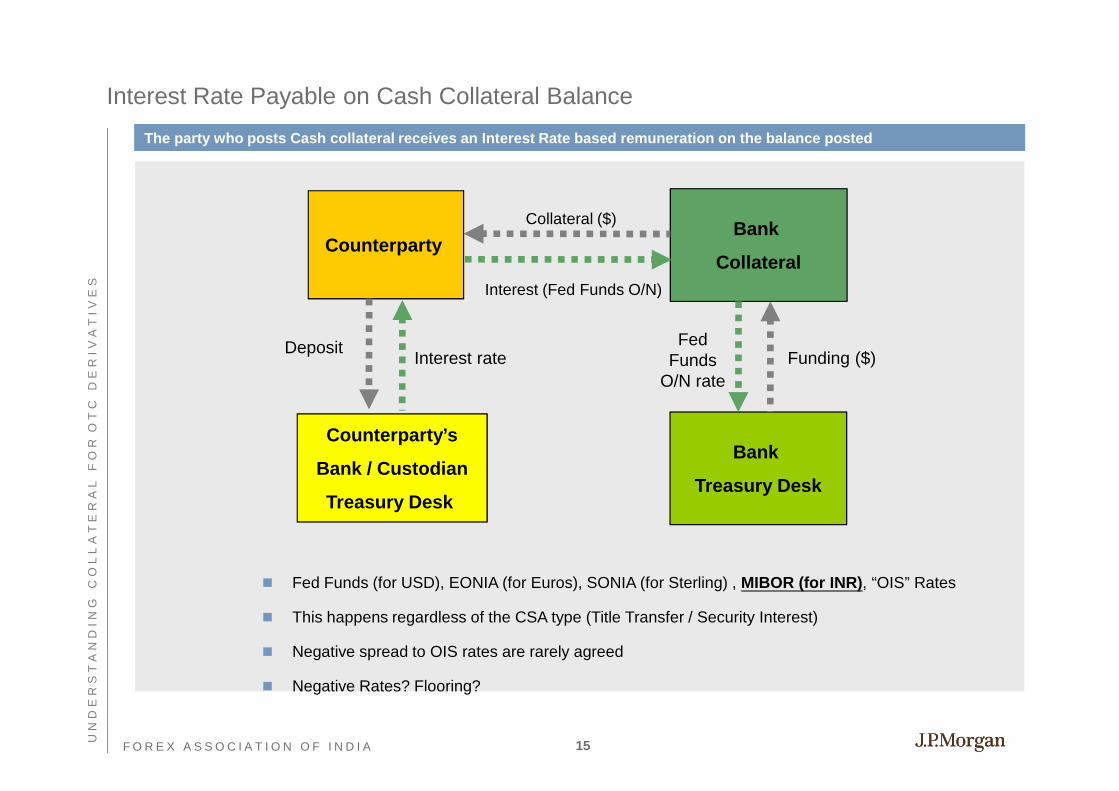

Interest Rate Payable on Cash Collateral Balance

Independent AmountsThe party who posts Cash collateral receives an Int erest Rate based remuneration on the balance posted

Bank

Collateral

Collateral ($)

Counterparty

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

CollateralInterest (Fed Funds O/N)

Counterparty’s

Bank / Custodian

Treasury Desk

Bank

Treasury Desk

Funding ($)Fed

FundsO/N rate

DepositInterest rate

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

� Fed Funds (for USD), EONIA (for Euros), SONIA (for Sterling) , MIBOR (for INR) , “OIS” Rates

� This happens regardless of the CSA type (Title Transfer / Security Interest)

� Negative spread to OIS rates are rarely agreed

� Negative Rates? Flooring?

15

Other Parameters in a CSA

Valuation Frequency Independent Amounts Valuation Agent

� The Valuation Frequency is � Upfront collateral amounts that are only applicable to

� The valuation agent is

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S simply how often both parties

will look at the MTM and perform the Collateral Calculations

� If the valuation frequency is weekly or monthly, no Collateral Calls take place in between (Discuss Adhoc rights)

� The valuation frequency does not necessarily have to be equal to frequency of the

that are only applicable to particular trades (i.e. when selling options, for example)

� These are generally negotiated on a case by case basis when trading each product

� Always included in Bank/Dealer Collateral Agreements with Hedge Funds

responsible for making the Collateral requirement calculations

� As per standard, the valuation agent is the “party making the demand”

� A party acting as a sole valuation agent, will typically provide its Counterparty with a (daily) statement

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

equal to frequency of the calls (i.e. the valuation frequency might be daily, for example, but if the MTM does not move by a large enough amount, there will not be a daily collateral call)

Funds (daily) statement regardless of whether they are calling for collateral or not. Otherwise, a statement will typically only be sent when a party is calling

16

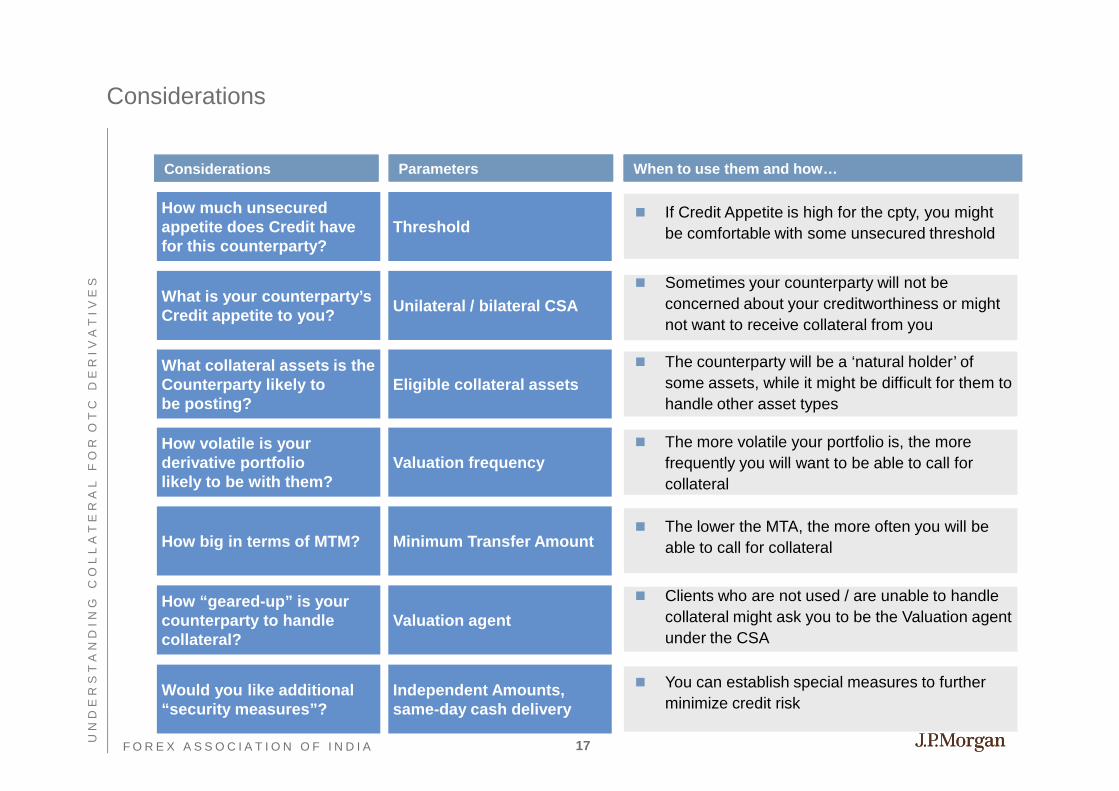

Considerations

Considerations When to use them and how…Parameters

� If Credit Appetite is high for the cpty, you might be comfortable with some unsecured threshold

How much unsecured appetite does Credit havefor this counterparty?

Threshold

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

How volatile is your derivative portfolio likely to be with them?

Valuation frequency

What is your counterparty’sCredit appetite to you?

Unilateral / bilateral CSA� Sometimes your counterparty will not be

concerned about your creditworthiness or might not want to receive collateral from you

� The more volatile your portfolio is, the more frequently you will want to be able to call for collateral

� The lower the MTA, the more often you will be

What collateral assets is theCounterparty likely to be posting?

Eligible collateral assets� The counterparty will be a ‘natural holder’ of

some assets, while it might be difficult for them to handle other asset types

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

How big in terms of MTM? Minimum Transfer Amount

How “geared-up” is your counterparty to handle collateral?

Valuation agent

Would you like additional“security measures”?

Independent Amounts,same-day cash delivery

� The lower the MTA, the more often you will be able to call for collateral

� Clients who are not used / are unable to handle collateral might ask you to be the Valuation agent under the CSA

� You can establish special measures to further minimize credit risk

17

Agenda

OTC Derivatives Collateral - Introduction and Basics 1

OTC Derivatives Collateral - Legal Concepts and Agreement Parameters 8

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

OTC Derivatives Collateral - Collateral Assets 18

OTC Derivatives Collateral - The Operational Process 21

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

F O R E X A S S O C I A T I O N O F I N D I A 18

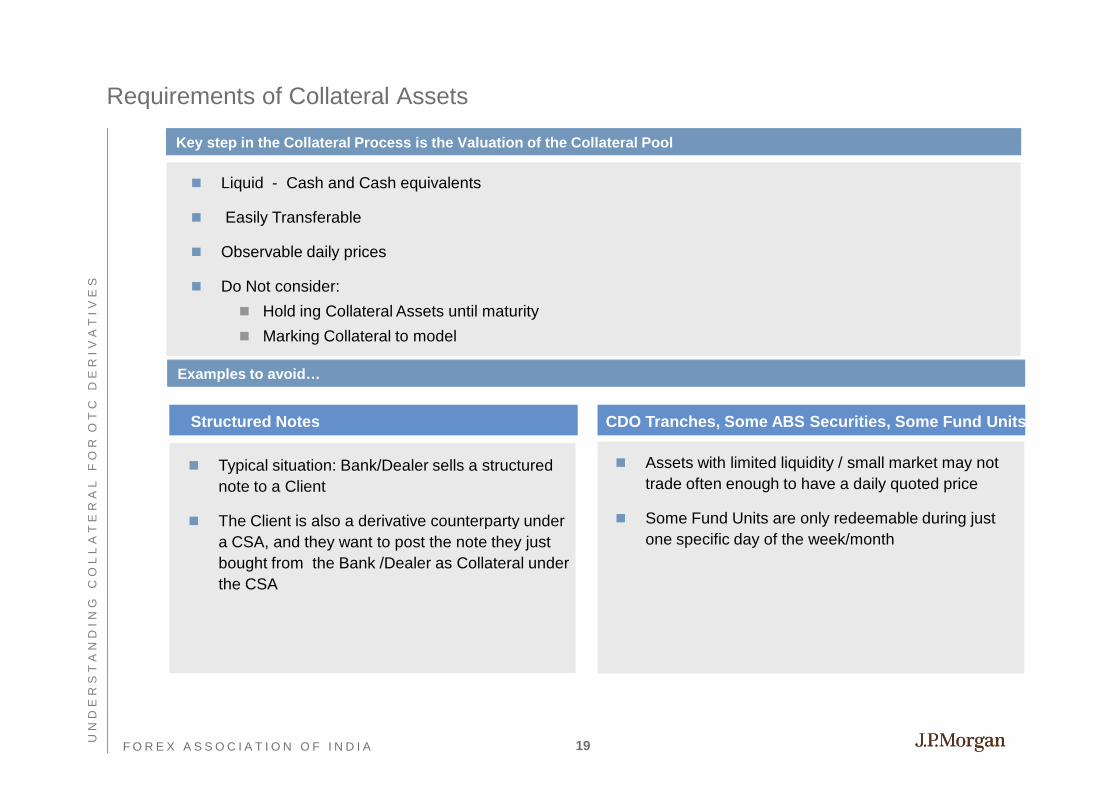

Requirements of Collateral Assets

Key step in the Collateral Process is the Valuation of the Collateral Pool

� Liquid - Cash and Cash equivalents

� Easily Transferable

� Observable daily prices

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

� Do Not consider:

� Hold ing Collateral Assets until maturity

� Marking Collateral to model

Examples to avoid…

Structured Notes CDO Tranches, Some ABS Securities, Some Fund Units

� Typical situation: Bank/Dealer sells a structured note to a Client

� The Client is also a derivative counterparty under

� Assets with limited liquidity / small market may not trade often enough to have a daily quoted price

� Some Fund Units are only redeemable during just

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

� The Client is also a derivative counterparty under a CSA, and they want to post the note they just bought from the Bank /Dealer as Collateral under the CSA

one specific day of the week/month

19

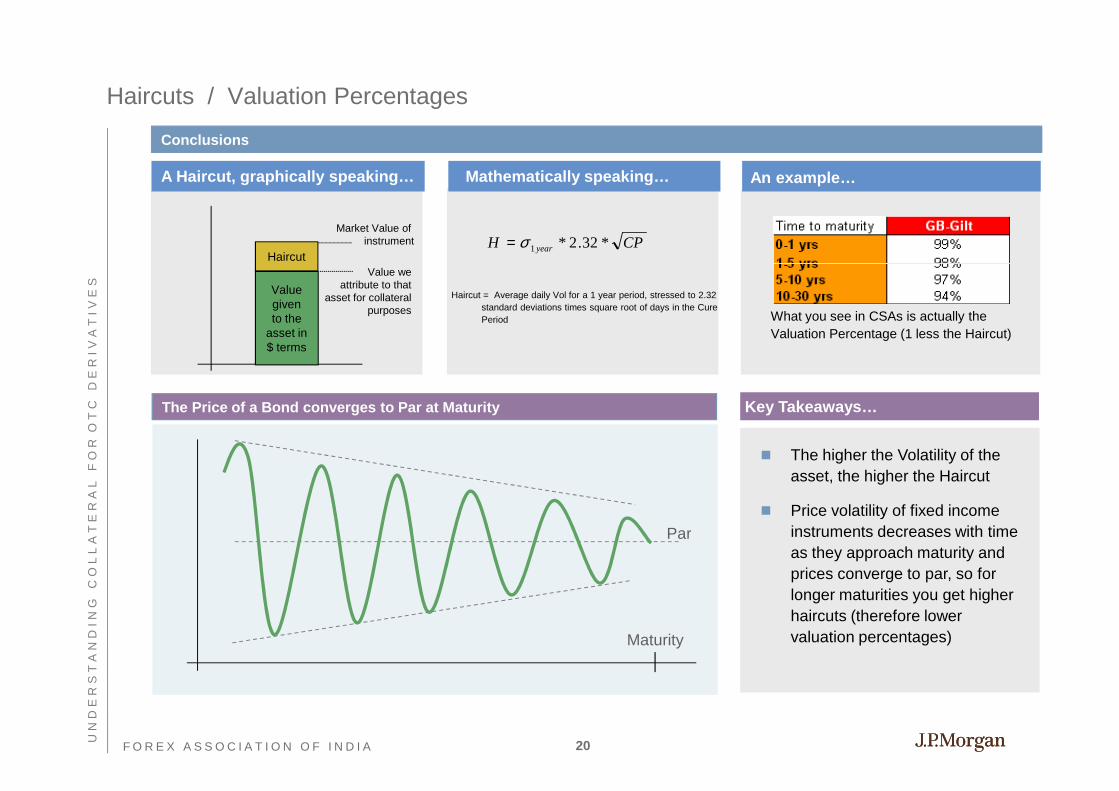

Haircuts / Valuation Percentages

A Haircut, graphically speaking… Mathematically speaking… An example…

Conclusions

Haircut

Market Value of instrument CPH year *32.2*1σ=

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

The Price of a Bond converges to Par at Maturity

Haircut = Average daily Vol for a 1 year period, stressed to 2.32 standard deviations times square root of days in the Cure Period

Par

Key Takeaways…

� The higher the Volatility of the asset, the higher the Haircut

� Price volatility of fixed income instruments decreases with time

Valuegivento the

asset in$ terms

Value weattribute to that

asset for collateralpurposes What you see in CSAs is actually the

Valuation Percentage (1 less the Haircut)

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

Par instruments decreases with time as they approach maturity and prices converge to par, so for longer maturities you get higher haircuts (therefore lower valuation percentages)Maturity

20

Agenda

OTC Derivatives Collateral - Introduction and Basics 1

OTC Derivatives Collateral - Legal Concepts and Agreement Parameters 8

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

OTC Derivatives Collateral - The Operational Proces s 21

OTC Derivatives Collateral - Collateral Assets 18

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O

T C

D

E R

I V

A T

I V

E S

F O R E X A S S O C I A T I O N O F I N D I A 21

OTC Collateral

The Operational ProcessU

N D

E R

S T

A N

D I

N G

C

O L

L A

T E

R A

L

F O

R O

T C

D

E R

I V

A T

I V

E S

OTC Derivatives

Portfolio valuation

Collateral valuation

Collateral requirement calculation

Communication VerificationMovement of

collateral

T T T+1 T+1 T+1 T+2

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 22

T T T+1 T+1 T+1 T+2Portfolio valuation

� Gather Close of Business (CoB) mark-to-market information for each trade covered by the collateral agreement

� All OTC derivatives covered by the ISDA Master Agreement should be included, as failure to include certain types of

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S � All OTC derivatives covered by the ISDA Master Agreement should be included, as failure to include certain types of

product can expose either party to increased risk - avoid the temptation to exclude short term products

� FX Spot?

� Trades approaching maturity / settlement on T+1 or T+2 ?

� Trades novating to central clearing? Discuss CCIL Forward Segment

� Calculate the aggregate market value of the entire portfolio

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 23

T T T+1 T+1 T+1 T+2Collateral valuation

� Calculate the collateral value of the assets currently posted

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

� FX timing for Cash if different from the CSA Base Currency

� Securities Collateral is valued dirty (including accrued coupon) before the appropriate haircut per the agreement is

applied

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 24

T T T+1 T+1 T+1 T+2Collateral requirement calculation

� Apply collateral parameters contained within the Credit Support Annex, such as thresholds, upfront amounts etc. to

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S determine the MTM exposure to be collateralised

� The collateral value of assets held / posted is then compared to the exposure amount

� A collateral requirement figure will be calculated. If this figure is greater than the minimum transfer amount, collateral

of sufficient value to cover the requirement (after the application of the appropriate haircut) must be transferred

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 25

T T T+1 T+1 T+1 T+2Communication

� The collateral call information is communicated between parties

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S � On occasion both parties might present a demand

� A breakdown of the market values of the individual trades constituting the portfolio is provided to facilitate

reconciliation, should the valuations prepared by the two parties differ

� Communication is typically via email with follow up telephone calls from Operations to Operations

� Avoid Sales or Relationship coverage involvement

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 26

T T T+1 T+1 T+1 T+2Reconciliation

� Should discrepancies exist between the two parties collateral requirement calculations, the reconciliation process

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S must begin

� The portfolio will be reviewed for obvious discrepancies such as different trade populations, significant differences in

valuations of specific trades etc.

� Industry efforts to proactively reconcile the portfolio daily

� If the parties are unable to agree upon the valuations of certain trades, the dispute resolution mechanism which is

outlined in the Credit Support Annex will be activated

� The key concept of the “Undisputed Amount” “Oils the wheels” of the CSA , provides ongoing feedback and level

of comfort

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A

of comfort

� Robust processes to internally escalate disputes or non response

27

T T T+1 T+1 T+1 T+2Movement of collateral

� Parties agree par values of the specific assets which they are going to deliver or return. These should not be altered

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S once agreed

� Standard Settlement Instructions (SSIs) are usually established however this can be a cause for operational delay

and risk for new agreements or those that remain inactive under a Threshold for a long time

� Trades included in MTM Exposure as of CoB T may be maturing on T+1 or T+2 Discuss?

� Avoid side arrangements to settle underlying trades out of proceeds of Collateral posted

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 28

T T T+1 T+1 T+1 T+2Movement of collateral (cont’d)

� Collateral Operations confirm that the instructed delivery of assets has settled successfully

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

� Asia time zone - if the delivery was for example in USD you may not become aware of failure to deliver until T+3

� Robust processes to internally escalate fails (Collateral Transfers and Underlying Trade settlements)

� Collateral holdings are updated in Collateral Systems and will be integrated in the calculations for a new statement

U N

D E

R S

T A

N D

I N

G

C O

L L

A T

E R

A L

F

O R

O T

C

D E

R I

V A

T I

V E

S

F O R E X A S S O C I A T I O N O F I N D I A 29