Embed Size (px)

Citation preview

Tackling the key issues in banking and capital markets*July 2004

the journal

1

the journal • Tackling the key issues in banking and capital markets

Impact of Basel II on the EU economy: Results of thePricewaterhouseCoopers Study for the European Commission

Editor’s comments

Non-performing loan transactions – A review of what is happening in Asia and Europe

Managing security in an insecure new world – Striking the right balance

Practical difficulties of adopting the identification requirements of the EU Savings Directive

Brazil – A review of the effects of inflation on thebanking sector

Lifting the veil on global hedge funds

4

2

Page

12

20

50

30

40

Contents

2

the journal • Tackling the key issues in banking and capital markets

by

Editor’s comments

by Phil Rivett

3

the journal • Tackling the key issues in banking and capital markets

Phil RivettGlobal Leader, Banking and Capital Markets

Tel: 44 20 7212 4686Email: [email protected]

Welcome to the fifth edition of thePricewaterhouseCoopers banking and capital markets journal.

In Europe, there has been much debateabout the possible economic impact ofthe adoption of the new Basel and EUcapital adequacy proposals. In our firstarticle Charles Ilako, Dr Bill Robinsonand Richard Barfield review the findingsfrom a recent study carried out byPricewaterhouseCoopers for the EuropeanCommission into the effect of theseproposals on the economies of Europeand their financial services sectors.

The growth of the hedge fund industryhas been impressive and the opportunitiesit presents have become one of thefocus areas in the banking and capitalmarkets sector. In ‘Lifting the veil onglobal hedge funds’, Mark Casella,Graham Phillips and Robert Welzeldiscuss the globalisation and‘retailisation’ of the hedge fund market.They also map its progress from theexclusive domain of an elite few tobecoming an attractive alternative totraditional asset classes for both banksand their customers.

Continuing our series of articles thatfocus on different parts of the world,

Paulo Miron, Sergio Rogante and Graham Nye discuss the bankingindustry in Brazil. The past 25 years haveseen innovation in the face of significantchallenges experienced by the Brazilianbanks, including a series of inflationaryand hyperinflationary economicenvironments, structural change withinthe sector and the onset of competitionfrom foreign banks.

In ‘Practical difficulties of adopting the identification requirements of the EU Savings Directive’, Sian Herbert, Bob Harland and Laurent de La Mettrieexplain the aims and implications of theSavings Directive and explore some ofthe information and systems’ challenges(and opportunities) financial institutionsare facing in adopting this new law.

How big an issue is security? For manyfinancial services organisations, securitythreats to people, assets and operationsare on the increase. In ‘Managingsecurity in an insecure new world’ Jan Schreuder, Chris Potter and Mark Vosexplore the security issues at hand andsuggest how management shouldanalyse and address these in practiceand highlight the evolving role of theChief Security Officer.

Finally, we consider ongoingdevelopments in the non-performingloans market. Frank Janik, Michael Harrisand Henning Heuerding provide anoverview of how different territories aretackling issues arising from the highlevels of non-performing loans held in the banking sector. They also discuss theopportunities available as activity movesincreasingly towards Europe, whereslower performance in the Germaneconomy and portfolio rebalances arecreating significant interest.

I hope you find the wide range of articlesof interest. Please do continue to provideus with feedback on the topics you wouldlike to see addressed in future editions.Online copies of this, and previouseditions, are available from our website(www.pwc.com/bankingandcapitalmarkets).

Impact of Basel II on the EU economy: Results of the PricewaterhouseCoopers Study for the European Commission

4

the journal • Tackling the key issues in banking and capital markets

by Charles Ilako, Dr Bill Robinson and Richard Barfield

The New Basel Capital Accord (Basel II),and the European Union’s (EU) plannedadoption of Basel II through the Risk-Based Capital Directive (CAD 3),represent a fundamental change in theregulatory framework for banks andinvestment firms, with potentially far-reaching effects on the Europeaneconomy. There has been much debatein Europe about the possible impact on the economy generally, with politicalconcern at both a ministerial andparliamentary level focusing particularlyon the impact on small- and medium-sized enterprises (SMEs). Europe ismuch more dependent on bankintermediation than, say, the UnitedStates, especially in the key small- andmedium-sized company sectors, whichaccount for 99% of all companies and66% of all employment in the EU.

The European Council of Ministers,meeting in Barcelona in March 2002,requested the Commission to assess the impact of the Basel process on ‘all sectors of the European economywith particular attention to SMEs’. The Commission responded byappointing PricewaterhouseCoopers, in partnership with the National Instituteof Economic and Social Research, to carry out this assessment.

The assessment involved three stages,beginning with an analysis of the impactof the proposals on the balance sheetsof banks and investment firms in the EU. They used the results of the thirdquantitative impact survey (QIS 3) dataas the principal source of data. The assessment then considered thepotential impact on profitability and thebehaviour of financial institutions by assessing how changes in capitalrequirements could affect banks in eachof the 15 countries which have quitedifferent market structures. Finally, at the macroeconomic level, the analysisaddressed changes in interest ratesacross all EU countries that could resultfrom Basel II and their combined impacton economic activity by:

• calculating the likely effect onborrowing costs in the economy at large under alternative scenarios in which cost changes were eitherpassed on in loan rates or absorbed in profits; and

• modelling the effect of these EU-wide interest rate changes on the macroeconomy.

The overall assessment1 was that theeffects would be positive for Europe’s

financial institutions, corporates andSMEs. Our analysis, including economicsimulations, suggested that, on balance,across the EU as a whole, the BaselII/CAD 3 proposals slightly reduce overallbank capital requirements. This could, in the longer term, have a small, butsignificant, positive effect (approximately0.1%, compounding to 1% over a period of 10 years) on GDP in the mostfavourable circumstances. Importantly,the new regime is expected tosignificantly enhance risk managementstandards and practices, which shouldlead to a better allocation of capital.

Overall change in regulatorycapital – a relatively small reduction

The Basel Committee and the EuropeanCommission, in revising the approach to regulatory capital, aimed to establisha regime which would create incentivesfor the adoption and development ofsound(er) risk management practices,whilst leaving the overall level of regulatorycapital supporting the financial systembroadly unchanged from the current(Basel I) level. The third quantitativeimpact study indicated that this aim haslargely been achieved, with an expected

5

the journal • Tackling the key issues in banking and capital markets

Charles IlakoLeader, European Financial ServicesRegulatory Practice, Brussels

Tel: 32 2710 7121Email: [email protected]

Richard BarfieldDirector, Valuation & Strategy, UK

Tel: 44 20 7804 6658Email: [email protected]

Dr Bill RobinsonHead UK Business Economist,Valuation & Strategy

Tel: 44 20 7213 5437Email: [email protected]

1 For further details of this report, please visit www.pwc.com/basel

fall of around 5% in regulatory capitallevels in the EU (at the individual countrylevel, though, there is some variationaround this average, see Figure 1 below).This reduction, because it is accompaniedby a more sophisticated approach to riskmeasurement, should not underminefinancial stability.

An enduring matter of contentionthroughout the development of the Basel II proposals has been the BaselCommittee’s intention to include bothexpected and unexpected loan lossesfor the purposes of regulatory capitalcalculations. Banks have argued thatexpected loan losses are alreadycovered by provisions held. Thisargument was finally recognised by

the Basel Committee through the‘Madrid Compromise’ in October 2003.The Commission’s analysis has shownthat the ‘Madrid Compromise’ couldincrease further the capital reduction to approximately an overall 10%, which is believed to constitute areduction of sufficient magnitude topotentially undermine the underlyingobjectives of capital neutrality andfinancial stability. As a consequence,recalibration efforts are now in progressto neutralise this effect.

The impact on individual financialinstitutions will depend on their businessprofiles and their chosen approaches tocalculating regulatory capital requirements.Banks lending primarily to SMEs and

retail customers should find that therelated capital requirements will fall, in some cases materially. Conversely,banks that lend primarily to sovereigns,large corporations and pure investmentbanking businesses see little or noreductions in regulatory capitalrequirements.

Impact on bank behaviour

From the viewpoint of a for-profitfinancial institution, Basel II representsan opportunity to review capital structure(the debt-equity mix) and increaseshareholder value. The more equitybanks are obliged to use, the higher thecost of capital, and hence the moreexpensive will be their loans. On theother hand, more equity means a larger‘cushion’ to insulate depositors from theconsequences of default by borrowers.Since the general thrust of bankingregulation is to impose safety marginsthat make bank failure less likely, therewas some concern that Basel II wouldpush up banks’ costs and hence theprice of loans (especially in the sensitiveSME sector).

The study indicates that the projectedoutput is likely to be quite different. The main impact of Basel II is to givebanks the opportunity to make a moresophisticated analysis of risk and therebyreduce their capital requirements.

Impact of Basel II on the EU economy continued...

6

the journal • Tackling the key issues in banking and capital markets

Austria Belgium France Germany Greece Netherlands Portugal Spain UK15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

-30%

-35%

Credit risk Operational risk Total

Figure 1: Expected change in capital requirements by country

Source: QIS3 country reports, EU Commission and PricewaterhouseCoopers analyses

They can thus reduce their overall costof funds, with beneficial effects on theirprofits and/or on their lending rates.

We estimated that a reduction of overallPillar 1 requirements could, on favourableassumptions, translate into an aggregatecapital saving of approximately €80-100 billion across the EU during theimplementation period, which wouldrepresent an increase in annual reportedprofits (post tax) of approximately €10-12 billion in the EU (see Figure 2). Whenthis benefit flows through, it may beshared with customers or retained by thebanks depending on the type of lending,market profitability, customer behaviour,industry structure and marketcompetitiveness in individual countries(see Figure 3). While these factors willvary by market, at a high level ouranalysis indicated the benefits could be shared in the following ways:

• Banks: Finland, Greece and Portugal

• Customers: Austria, France, Germany, Italy andUnited Kingdom

• Either: Belgium, Denmark, Ireland,Luxembourg, Netherlands, Spain or Sweden

7

the journal • Tackling the key issues in banking and capital markets

Austria Belgium France Germany Greece Netherlands Portugal Spain UK

7

€bn

6

5

4

3

2

1

0

-1

Figure 2: Distribution of annual gross economic benefits or costs due toestimated capital changes

Source: QIS3 country reports, Bloomberg and PricewaterhouseCoopers analyses

1 However if low profitability is due to structural reasons, the industry may use Basel II as an opportunity to improve returns.

Banks likely to benefit as they maintain or increase profitability

Little impact on banks or sub-sector customers

Are Basel II capital reductions significant in any market sub-sectors of lending?

Overall, customers may benefit as banks compete for share1

Is the sub-sector profitable (ROE>COE) and the market competitive?

Overall, banks may benefit as they increase returns

Is demand strong? (How rapidly is lending growing?)

Customers may benefit (as banks compete for share or new entrants enter)

Yes

No

Yes

Yes (profitable and competitive)

(profitable but not competitive)

No

No

No

(not profitable but competitive)

Figure 3: Impact analysis

Source: EU/PwC study on the financial and macroeconomic consequences of the draft proposed new capital requirementsfor banks and investment firms in the EU.

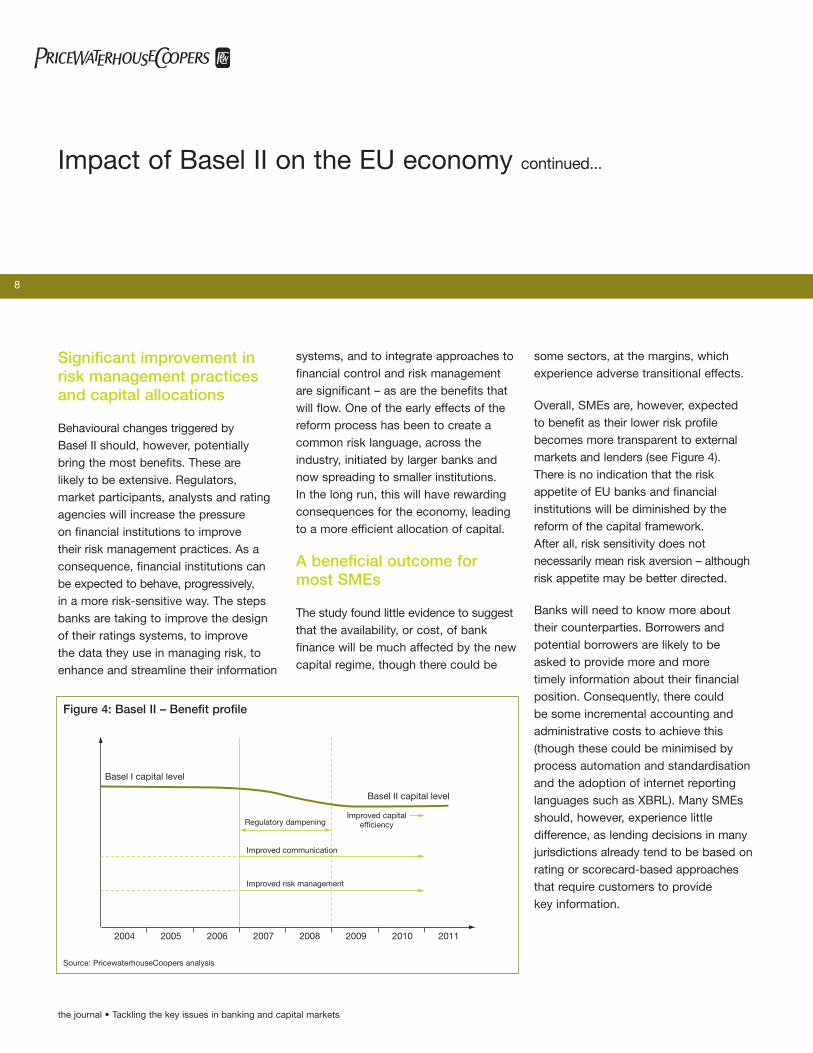

Significant improvement inrisk management practicesand capital allocations

Behavioural changes triggered by Basel II should, however, potentially bring the most benefits. These are likely to be extensive. Regulators, market participants, analysts and ratingagencies will increase the pressure on financial institutions to improve their risk management practices. As aconsequence, financial institutions canbe expected to behave, progressively, in a more risk-sensitive way. The stepsbanks are taking to improve the designof their ratings systems, to improve the data they use in managing risk, toenhance and streamline their information

systems, and to integrate approaches tofinancial control and risk managementare significant – as are the benefits thatwill flow. One of the early effects of thereform process has been to create acommon risk language, across theindustry, initiated by larger banks andnow spreading to smaller institutions. In the long run, this will have rewardingconsequences for the economy, leadingto a more efficient allocation of capital.

A beneficial outcome formost SMEs

The study found little evidence to suggestthat the availability, or cost, of bankfinance will be much affected by the newcapital regime, though there could be

some sectors, at the margins, whichexperience adverse transitional effects.

Overall, SMEs are, however, expected to benefit as their lower risk profilebecomes more transparent to externalmarkets and lenders (see Figure 4). There is no indication that the riskappetite of EU banks and financialinstitutions will be diminished by thereform of the capital framework. After all, risk sensitivity does notnecessarily mean risk aversion – althoughrisk appetite may be better directed.

Banks will need to know more abouttheir counterparties. Borrowers andpotential borrowers are likely to be asked to provide more and more timely information about their financialposition. Consequently, there could be some incremental accounting andadministrative costs to achieve this(though these could be minimised byprocess automation and standardisationand the adoption of internet reportinglanguages such as XBRL). Many SMEsshould, however, experience littledifference, as lending decisions in manyjurisdictions already tend to be based onrating or scorecard-based approachesthat require customers to provide key information.

Impact of Basel II on the EU economy continued...

8

the journal • Tackling the key issues in banking and capital markets

2004 2005 2006 2007 2008 2009 2010 2011

Basel I capital level

Regulatory dampening

Improved communication

Improved risk management

Improved capitalefficiency

Basel II capital level

Figure 4: Basel II – Benefit profile

Source: PricewaterhouseCoopers analysis

Competitive impact on EU financial firms –coordinated nationalimplementation is essential

With one or two possible exceptions, the study did not find evidence tosuggest that EU financial firms will be at a significant competitive disadvantageas a result of the EU applying the newcapital requirements to all banks andinvestment firms. Similarly, the decisionof the US authorities to limit theapplication of Basel II to some 20 institutions is unlikely to be asignificant competitive factor: the vastmajority of US banks are local.

Most competition still takes place withinindividual EU territories – and mostfinancial markets remain defined innational terms – as the full integration ofEurope’s financial services market hasnot yet been achieved. This said, it will be important to have a consistentapplication of the new proposals acrossthe EU. Consequently, it will be importantto ensure safeguards to prevent the manyoptions and areas of supervisorydiscretion included with the Basel IIproposals becoming a source ofcompetitive advantage for rival firms in the EU. The multiple options anddiscretions may have been necessary to accommodate structural differencesbetween countries and to reach

international agreement, but they couldmake the creation of a genuinely levelplaying field in the EU much more difficult.

This concern is strongest with regard to the Pillar 2 elements of the newframework involving supervisoryoversight where there is, as yet, relativelylittle public guidance as to what will berequired of firms. Many institutions worrythat EU regulators may take differentdirections. Discussions with regulatorsduring the course of the study, however,suggested there is keen awareness ofthe issue of competitive equality andmuch effort is being devoted to clarifyingrequirements and to co-ordinating theviews of national supervisors – at theBasel level through the AccordImplementation Group (AIG) and at anEU level through the Groupe de Contact(GdC) and the Committee of EuropeanBanking Supervisors (CEBS).

Procyclicality – unlikely to be a major problem butneeds to be monitored

The issue of procyclicality, or the extent to which risk-sensitive capitalrequirements will exacerbate economiccycles by ramping up capitalrequirements as credit quality worsens,has engendered considerable debate. We believe sufficient steps have beentaken to mitigate the effects of

procyclicality in the current proposals-whether by encouraging stress testing or by flattening risk curves, so thatchanges in creditworthiness do notproduce inordinately large changes incapital requirements.

Basel II should, on balance, reduce herdbehaviour, both in granting and abruptlywithdrawing credit. This has so oftenresulted in lending sprees and creditcrunches. In effect, enhanced riskawareness by the lending institutions,and a more forward-looking approach to granting credit, will be the greatestdefence against procyclicality. Moreformal and well-constructed lending andrisk management processes, togetherwith greater emphasis on the use of fairvalue measures, are less likely to result in abrupt reversals of lending decisions.Prompt correction is more likely to avoidthe need for drastic action at a laterdate. Anecdotal evidence in somecountries indicates that the increaseduse of more formal lending processeshas already led to a dampening of the typical cyclical pattern of bank credit availability.

The Commission and national authoritieswill need to keep this issue under review,during both the initial transition stageand the medium term, and stand readyto amend the framework should thisassessment prove too optimistic.

9

the journal • Tackling the key issues in banking and capital markets

Significant cost and resource requirements

Banks are already spending considerablesums on devising systems in order to comply with the requirements of the new capital regime. Based onPricewaterhouseCoopers’ experienceand on published external surveys, the estimate of the total cost in the EU is between €20 billion and €30 billionduring the period 2002 to 2006 (seeFigure 5). Large banks are forecast tospend some €80-150 million each, while smaller banks are expected toinvest significantly less.

These estimates clearly include elementsof systems development that would have

occurred irrespective of Basel II. It ishard to isolate the element of costs that represents a ‘pure’ regulatory cost,though anecdotal evidence suggests it could be relatively small. It is clear that Basel II has accelerated thedevelopment of more enhanced systemsand processes. Policymakers, however,will need to be mindful of the context inwhich the reform is being implementedas it is one of many competing demandson management time (including theimplementation of International FinancialReporting Standards and meetingincreased corporate governancerequirements, e.g. the Sarbanes-Oxleyprovisions), in an environment wherebank margins in most markets are under pressure.

In addition to financial institutions, the implementation of the new capitalframework will place very significantresource demands on nationalsupervisors. They will have to investsignificant sums on systems, training andrecruitment and in mobilising both thestaff numbers and the technical skills to meet the implementation challenge.Significant concerns exist within theindustry that national supervisors will notbe able to cope with the demands thatBasel will place upon them in terms ofvalidating banks’ internal approaches torisk assessment and quantification andquality and in terms of Pillar 2 supervision.

At the same time, there are concerns in the supervisory community that banksmay be less advanced and less able tomeet supervisors’ requirements than banksthemselves believe. There are differingperceptions of what is ‘fit for purpose’that could be difficult to reconcile.

Overall conclusion – Basel IIand CAD 3 should on balancebe positive for the EUmacroeconomy andprudential structures

From a macroeconomic perspective, the encouragement of risk-sensitivecapital and approaches to supervisionshould impact positively on thebehaviour of financial firms and enhance

Impact of Basel II on the EU economy continued...

10

the journal • Tackling the key issues in banking and capital markets

2003 2004 2005 2006 2007 2008 2009 20102002

Implementation costs/accelerated costs

Basel IIGo live date

€

Maintenance costs

Communication costs

Figure 5: Basel II – Cost profile

Source: PricewaterhouseCoopers analysis

financial stability. More efficientallocation of capital in the economyshould exist without undue adversecompetitive effects or, as far as it ispossible to tell at this stage, excessiveprocyclical effects. The effect on themacroeconomic aggregates and, inparticular, on output, is mildly beneficial.

There are still many unknowns. A numberof key decisions about the final shape of the capital adequacy framework remainto be taken. Much will also depend on the manner in which the framework isimplemented and the extent to whichimplementation is coordinated on an EU-wide basis. Much of the detail of the EU framework will be filled in andcoordinated by the recently constitutedCommittee of European BankingSupervisors, which represents the 15 EU member states.

Overall, however, the analysis of theavailable evidence concludes that, from a macroeconomic perspective,Basel II and CAD 3 should be positive for the EU and for prudential regulationwithin the EU.

11

the journal • Tackling the key issues in banking and capital markets

Lifting the veil on global hedge funds

12

the journal • Tackling the key issues in banking and capital markets

by Mark Casella, Graham Phillips and Robert Welzel

A former backwater of investmentmanagement, hedge funds have becomeone of the most important growth areasin financial services. Growth in businessfor the industry from banks, brokers,derivatives, prime brokerage and custodyand settlement arms is also now beingmirrored by the creation of ‘in house’funds and greater levels of investment of institutions’ own capital into this assetclass. Hedge funds have historicallybeen restricted to the privateparticipation of an elite few. In absolutedollar terms, hedge funds lag behindtraditional mutual funds by a significantamount. However, they are becomingever more mainstream, as institutionalinvestors recognise them as an attractivealternative to traditional asset classes.Increasing awareness of hedge funds’unique attributes and appeal is embodiedby the substantial increase in both thenumber and total value of hedge funds’assets under management. Several yearsof impressive growth have liftedworldwide assets in hedge funds to morethan $750 billion. This has been led bydemand from institutional investors andfavourable regulatory and tax provisionsthat are opening up new markets acrossEurope and Asia as well as relaxingregulatory constraints on investment.

Until recently, regulatory attitude hasbeen ‘buyer beware or touch at yourown risk’. Now squarely out of theshadows and under the microscope ofinvestor interest, hedge funds and otheralternative investments are receivinggreater regulatory attention than everbefore, focusing on their management,reporting and distribution. This attentioncomes not only from regulators and rulemakers such as the Securities andExchange Commission (SEC) in theUnited States and the Financial ServicesAuthority (FSA) in the United Kingdom,where hedge fund markets are welldeveloped, but also from nationalgovernments across Continental Europeand Asia, where the hedge fund marketis now poised for explosive growth.

Banks, insurers, pension funds and other institutional investors continue to increase allocations to alternativeinvestments with expectations of findinginfrastructures capable of satisfying theirrisk and return needs. These participantswill become more important as standard-setters for hedge funds and their internalpractices. Capital markets participants,now seeking to enter what hastraditionally been an industry dominatedby boutiques, will forever change thedynamics between hedge funds and

their investors. Greater transparency and accountability will be demanded offund managers, who will find themselvesanswering to a newer constituency thanthey have been accustomed.

Regulatory attention in the US hasrecently been diverted by the tradingscandals afflicting the mutual fundindustry. However, there will becontinued and intensified interest from global regulators and rule makers in hedge fund structures, reportingpractices and tax issues throughout2004. While financial centres in the US and UK are two of the largest andmost experienced hedge fund markets –setting operational and regulatoryprecedents and best practices,developing regulatory and taxationstructures, and influencing the cross-border flows of global capital – we willalso highlight developments in marketsacross Europe and Asia and theimplications of hedge fund investmentsfor capital markets.

The state of the hedge fund market

In recent years, hedge funds haveceased to be the exclusive domain of the ultra-wealthy and have become

13

the journal • Tackling the key issues in banking and capital markets

Mark CasellaPartner, US Capital Markets

Tel: 1 646 471 2500Email: [email protected]

Robert WelzelSenior Manager, Capital Markets andInvestment Management, Germany

Tel: 49 69 9585 6758Email: [email protected]

Graham PhillipsEuropean Hedge Fund Practice Leader, UK

Tel: 44 20 7213 1719Email: [email protected]

more accessible to a wider audience of investors. Many institutions are nowoffering hedge fund pools or funds-ofhedge-funds1. The entry of assetmanagement companies into theformerly closed world of hedge funds is having a profound effect on practices.This relaxation of access has led todiscussions about registration anddisclosure requirements, a move thatmany have expected for years, especiallyin the highly publicised wake of recenthedge fund meltdowns. In May 2003, the SEC met representatives from thehedge fund industry to determine whatchanges and amendments were neededto existing regulations to make hedgefund investing ‘safer’ for mainstreaminvestors. In the UK, the FSA hasundertaken studies of the hedge fundindustry and short selling2, although nosignificant changes have been proposedto current regulations for the monitoringof hedge fund managers or of thedistribution of hedge fund products.

The hedge fund market has gained evergreater credibility and reach amonginstitutional investors during the past five years. As an increasing number ofinstitutions enter the market, they arechallenged on a number of fronts. At one level, there is the challenge ofretaining top talent, those who used thedownsizing of the sector during the bear

market to strike out on their own and set up funds. Investment professionalsfrustrated by the limitations of ‘long-only’strategies and institutional compliancerequirements were easily wooed by themore dynamic and potentially personallylucrative world of small, private hedgefund management firms. Institutionswhich are adding alternative investmentopportunities to their offerings are beingchallenged by the regulatory/reportingdisconnect between their historicalpractices and the unique operatingenvironment of typical hedge funds.Conflicts between product strategies,going short in one fund while being longin another, will make this institutionalmove into alternative investments farfrom a simple proposition.

The ‘blessing’ of the asset class byincreasing numbers of regulators hasopened the door to a flood of newproducts and opportunities for institutionaland high net worth individuals. The trendin Europe is also one of bringing funds‘onshore’, domiciling them in the countrieswhere they will be distributed andmanaged. This move is largely due toefforts by the European Parliament topass proposals designed to encouragefund managers to base their funds inregulated markets under a EuropeanUnion-wide regulatory regime. Fundmanagers and administrators, however,

should not be beguiled by the vision of a pan-European financial market. The fact remains that there are 25distinct and separate national regulatoryregimes in Europe. This creates complexregulatory difficulties that continue to be a significant barrier in the Europeanmarket. The increasing popularity ofhedge fund investments, however, isforcing national regulators to review thissituation and legislative changes areoccurring in many European territories.

Lifting the veil on global hedge funds continued...

14

the journal • Tackling the key issues in banking and capital markets

For more details about the hedge

fund market in Europe, please see

‘The regulation and distribution of hedge

funds in Europe – Changes and challenges’

at www.pwc.com/hedgefunds

1 A hedge fund with a strategy of investing in multiple other funds to diversify performance risk.2 The sale of shares that are not yet owned in anticipation that they will fall in value before settlement occurs, thus making a profit.

The globalisation of thehedge fund market

European institutional investors havebeen historically risk averse but they are increasingly allocating more of theirportfolios to alternative strategies,including hedge funds, as riskdiversification becomes betterappreciated. For one thing, the euroeliminated many of the diversificationbenefits of cross-border bond investing.In Europe, French and Swiss investorshave been more inclined to invest inhedge funds, though demand fromGerman, Italian, Danish, Dutch and UK investors is now gaining momentum.

Perhaps the greatest immediateopportunity for hedge fund industrygrowth lies in Germany. As of 1 January2004, the German InvestmentModernisation Act permitted assetmanagers to offer hedge funds toinstitutional and high net worth clients inGermany. The pent up demand for theseproducts, which have only been madeavailable to German investors in the pastthrough complicated offshore structures,is expected to spark a rush of interestfrom investment institutions seeking atoehold in the German market. Someexperts predict that German hedge fundinvestments could top the €50 billionmark within five years. Unlike the US,where distribution is restricted to

qualified individual investors, there areno such restrictions written into Germanlaw. These differences in territorial legaland regulatory frameworks furthercomplicate the distribution landscape forfunds seeking to enter the new market.Still an increasing number of institutions,such as DWS, Deutsche Bank, Dresdnerand DIT, are among the German financialinstitutions now offering or planning tooffer hedge fund investments to theircustomers in the near term. It isinteresting to note that, in Germany,individual foreign funds may only bedistributed through private placements,however, funds-of-hedge-funds may bepublicly distributed. In addition, there areno restrictions or minimum thresholdsthat define a ‘qualified’ hedge fundinvestor, opening the way for someinteresting true retail strategies for funds-of-hedge-funds.

Elsewhere in Europe there continues tobe a great deal of hedge fund activity,particularly in London, where many USfunds have established beachheads toaccess better local research and toimprove the reach of their distributionefforts. With a burgeoning infrastructureof specialist accountants, lawyers and prime brokers supporting them,London-based hedge fund managers are well positioned to take advantage of changes by national regulators inEurope. With institutional allocations to

hedge funds nearly doubling in the pastyear, it is widely believed that hedgefund managers with strong infrastructurefor reporting results, managing operationalrisk and satisfying the rigorousrequirements of institutional investors, will benefit the most.

In Italy, institutional hedge fund assetsare expected to triple by 2005, accordingto Hedge Invest, an Italian fund-of-hedge-funds manager. Their assetsunder management grew from €2.2 billionin 2002 to €6.2 billion in 2003 and areexpected to rise to €18 billion by theend of 2005. Recent legislation in Italy dropped the minimum investmentin the class from €1 million to €500,000,providing access to a wider class ofpotential investors.

In Asia, the market is geographicallyfocused on Tokyo, where a number of US and European funds and funds of funds have established a presence to serve the burgeoning market foralternative investment products in theregion. In the Asian markets, there is lessinstitutional investment in hedge fundsthan in the US or Europe but as moreglobal players move into the region andbegin to offer products, this will change.Official reservations against hedge funds,stemming from charges that hedge fundsprofited from and exacerbated theregional currency crisis of 1998, appear

15

the journal • Tackling the key issues in banking and capital markets

to be abating. According to estimatespublished by Eurekahedge, a Singaporeconsulting firm, Asian hedge fund assetsunder management have swelled from $11 billion to $35 billion over the pastfour years.

‘Retailisation’ of the hedgefund market

The creation of more funds-of-hedge-funds, with vastly reduced minimuminvestment levels from the traditionalhedge fund minimum of $1 million in net worth or $200,000 in annual income,is the best indicator of retail investorsgaining access to the potentiallybeneficial attributes of hedge fundinvestments. Retail investors are notablyattracted by the ability to protect capitalin bear markets, a capability accentuatedby the relatively poor performance oflong-only funds recently. Investors alsowant the downside protection that hedgefunds purport to offer.

Mutual fund companies, in particular, aredrawn to these investments. An increasein the number of mutual fund companiesentering the hedge fund market, eitherthrough direct management of hedgefunds or the creation of funds-of-hedge-funds, has profound implications for further regulator involvement,changes in reporting structures and fund governance.

The American mutual fund industry ispressuring the SEC to look more closelyat the practices of the alternativeinvestment world, partially because theirown investments are so closely regulatedand scrutinised, and because they wishto adopt some alternative investmentbest practices. With competition alwayskeen for investment dollars, the mutualfund industry wants to remaincompetitive with the alternativeinvestment world. For example, in theUS, the SEC is focusing on the reportingof the fee structures of the underlyingfunds in funds-of-hedge-funds, and theappointment of an independent board to oversee operations and compliance.Some critics have warned that this willmean a diversion of SEC resources fromthe most popular retail investmentvehicle, mutual funds, to one that is not as significant an asset class astraditional funds, although they receive a great deal of press.

As more investment companies enter thefunds-of-hedge-funds business, one canalso expect some questioning ofmanagers’ conflicts in managing bothlong only and leveraged short funds.Recent SEC recommendations haveattempted to head off these concerns;however, there will be further uncertainty.Discussion is expected to continuethroughout this year.

The marketing of alternative investmentsis an especially sensitive area.Traditionally, hedge funds have not soldtheir investments in any overt way, atleast not on the retail scale that a mutualfund would. Marketing creates claimsand disclaimers. There is currentlysignificant focus on marketing practicesand disclosure standards for ‘retail’hedge funds and funds-of-hedge-funds. The SEC has issued recommendationsfor the presentation of hedge fundbrochures and has asked fund advisersto register with them and then to sendinvestors a statement disclosing conflictsof interest, risk management measuresdeployed by the fund, valuationprocedures used for the securities heldby the fund, and all applicable lock-upperiods for investors. Such a brochure or statement would need to be updatedregularly and made available to investorson an ongoing basis.

While the US hedge fund industry maylead the world in numbers, and arguablyregulatory oversight, the expectation thatother regions will import a US model ismisguided. The notion of establishing a common pan-European regulatoryregime for hedge funds is simply not apriority, and individual funds seeking tooperate and distribute their productsacross the region will have to navigatesome fairly complex issues during theyears to come.

Lifting the veil on global hedge funds continued...

16

the journal • Tackling the key issues in banking and capital markets

Growing in ContinentialEurope too

In the case of Germany, where the mostsignificant changes have recentlyoccurred in the global hedge fundlandscape, participants in the widercapital markets there are confronted with some extremely interesting changes. For instance, insurance companies are now authorised to commit up to 5% of their portfolios into Europeandomiciled hedge fund investments – notoffshore funds. There is likely to becontinued caution shown by institutionsas they dip their toes into alternativeinvestments and expect to see somefunds-of-hedge-funds take great stepsto prove their worthiness as credibleinvestments for historically conservativeinvestment pools.

Another substantial change is the way in which German tax law treatsdistributions of profits earned fromderivatives. For a private investor, anycapital gains from derivatives held by a hedge fund are tax free, whereas aprivate investment directly in a derivativeis taxed. For institutional investors, the tax-free treatment applies only aslong as the gains are not distributed, and as many hedge funds onlyaccumulate and rarely distribute gains,an institutional investor can achievedeferred tax assets by investing in a fund

which is highly invested in derivatives.The implications are that if interest issynthesised through a derivativecontract, it is tax-free for individuals andfor institutions, if it is not distributed.This will be an additional market driverfor investment in credit derivatives, forexample, outside the banking industry,transferring credit risk to non-bankseither through funds and/or theinsurance industry. This general trend ofrisk spreading will be an additional driverof the German fund industry from thetaxation strategy point of view.

Funds-of-hedge-funds

The funds-of-hedge-funds industry ispoised for explosive growth in all majormarkets. As it gains in popularity and asa main vehicle for ‘retailisation’, one canexpect much more scrutiny on how afunds-of-hedge-funds structure affectsthe transparency of the underlyingindividual hedge funds.

In October 2003, the SEC proposedthree new rules under the InvestmentCompany Act of 1940 regarding theability of an investment company toacquire shares of another investmentcompany. The proposal would broadenthe ability of a fund to invest in otherfunds, but the most notable impact maybe the requirement that the expenses ofthe component funds be aggregated and

shown as an additional expense in thefee table of the funds-of-hedge-funds.The pass-through effect of a funds-of-hedge-funds structure on fees, and thelight that is cast on formerly privaterelationships between fund advisers,prime brokers, solicitors and consultants,will cascade down and have a reformingeffect on individual fund practices. This may prove unsettling for many fundmanagers accustomed to working ‘in thedark,’ yet should, in most cases, beoffset by the infusion of new investorsinto their funds.

Returns alone will not be sufficient for an individual hedge fund, or even anestablished fund-of-hedge-funds todistinguish themselves from among a very crowded market of offerings. While returns may have led the charge in terms of attracting assets away fromequities during the market corrections of2000 through to 2002, we believe it willbe the quality of the hedge fundmanager’s reporting, back office, overallinfrastructure, communications andoperational risk management capabilitiesthat will distinguish it from its peers andattract additional institutional interest.

Ongoing due diligence and oversight by investors are becoming increasinglyimportant. With ever stricter requirementson management to show how itdischarges its reporting responsibilities,

17

the journal • Tackling the key issues in banking and capital markets

we would expect controls reporting andcertification arrangements (similar toSAS70 reports in the US or FRAG 21reports in the UK) to be used increasinglyby fund managers.

The effect of funds-of-hedge-funds onindividual fund practices will come intosharp focus as they seek to populatetheir offerings with individual funds that

comply with the mandates of territoryspecific regulations. For example, fundsthat do not comply with Germanregulations stand the risk of beingdesignated ineligible for inclusion in aGerman fund of funds offering. A greatdeal of activity among hedge fundadministrators to identify compliant taxreporting modules for their platforms toreach the chosen markets is occurring.

US funds in a global market – It’s not just Wall Street anymore

As the hedge fund industry continues toexpand in Europe and Asia, many USmanagers are seeking distribution tonon-US investors. This cross-borderfocus raises a number of significanttaxation and regulatory issues.

The impact of the USA Patriot Act and thegeneral security climate in the US hasplaced a large burden of Know-Your-Client(KYC) and anti-money laundering (AML)compliance on hedge fund managers.These strict requirements add to theoverall back office compliance cost andhave had a chilling effect on overseasinvestor solicitation efforts. While US fundmanagers will seek cross-borderinvestors, many will avoid them and becontent to only accept US-domiciledinstitutions and individuals. As registeredinvestment companies enter the market

for funds-of-hedge-funds, with KYC andAML compliance procedures wellestablished it is likely that overseasbusiness will gravitate towards thosecompanies for whom the incrementalcompliance complexity and costs arelowest. While efforts are well underwayto develop a global GAAP, withencouraging progress on IFRS, there canbe a dilemma for US funds trying tocome to grips with local accountingstandards in addition to regulationsduring the transition phase.

US experience with rigorous reportingstandards places those funds in a good position for compliance with new tax regimes, such as thosedeveloping in Germany. Because taxreporting is complicated in the US, it appears that those fund managersshould be able to capture the necessarydata for German tax reporting and, in the end, with some adaptations, maketheir administered funds capable ofreaching the German market.

London has emerged as the beachheadfor US funds seeking a presence inEurope and to capture funds invested intraditional products. While Americanfirms seeking to broaden their cross-border distribution capabilities may havedriven activity in the hedge fund marketin London, a large number of newEuropean hedge fund managers have

Lifting the veil on global hedge funds continued...

18

the journal • Tackling the key issues in banking and capital markets

An article entitled ‘Lifting the veil on

American hedge funds’ appeared in

Investment Management Perspectives,

March 2004 (page 47).

For further details, please visit

www.pwc.com/investmentmanagement

been formed. London has become theepicentre of the alternative investmentbusiness in Europe. Tax advantagesmean Dublin, Jersey and Luxembourghave also seen increasing popularity ashedge fund administration centres.However, we expect to see more localtax authorities reform their treatment ofalternative investments to lure fundsonshore, where they can be more easily regulated.

Conclusion

With financial regulatory reform and the general issue of transparency high onthe agenda, no one should be surprised if hedge funds and the universe ofalternative investments come undercontinuing scrutiny from regulators andlegislators worldwide.

Scrutiny does not mean the hedge fundbusiness is going to wither. This is agrowth industry, with a trend towards‘mainstreaming’ hedge funds into theflow of the traditional financial sector.Funds-of-hedge-funds structures willcontinue to be adopted by banks,insurers and other capital marketsparticipants which seek to offer hedgefund attributes to the retail investor.Institutional investors will continue toembrace asset allocation to hedgefunds, particularly as compliance andrisk management controls become more

transparent and acceptable to their investment committees and theavailability of structured productsenabling leveraged or downsideprotected exposure to hedge fundreturns widens.

The hedge fund industry has an excellentopportunity to adopt control, risk andreporting best practices and self-monitorits operations. The adoption ofcompliance measures will place aburden on smaller funds, which in turnwill rely more heavily on broker-dealersand administrators to assist them inmanaging their back office operations.Larger fund complexes will have anadvantage in satisfying regulatoryrequirements and the compliance burdencould result in pressure on smallerindependent fund managers, with fundsbanding together to share common back office services to gain economiesof scale.

One cannot underestimate the influentialrole of the traditional mutual fundsindustry with regards to how the hedgefund industry will evolve and beregulated. The sharp dichotomy betweenthe transparent and opaque world ofpublic and private funds has increasedpressure on regulators and rule makersto level the playing field. The veil is lifting. As it does, a new era ininvestment management will begin.

The entrance of large players from thecapital markets into hedge funds andother alternative investments willcertainly change the face of hedge fundinvesting forever, removing it from the‘rogue’ category it has laboured underover the past fifty years. It will become a far more mainstream, standardisedinvestment vehicle, one as regulated andcodified as any in the past.

19

the journal • Tackling the key issues in banking and capital markets

Brazil – A review of the effects of inflationon the banking sector

20

the journal • Tackling the key issues in banking and capital markets

by Paulo Miron, Sergio Rogante and Graham Nye

Over the past 25 years, the Brazilianfinancial system has faced the challenge of functioning in an economicenvironment that became inflationary,hyperinflationary and subsequentlyreturned to relatively stable prices. The adaptation of the banking sector to these scenarios introduced peculiarcharacteristics that set the Brazilianfinancial services sector apart from that found in developing nations. These, and the economic changes thatbrought them about, are explored in this article.

Like most, the Brazilian financial systemis based on two subsystems, regulatoryand operating. In Brazil, they areintegrated and interact effectively. The bodies that make up the regulatorysubsystem include the NationalMonetary Council, the Central Bank of Brazil, the Brazilian SecuritiesCommission, the Superintendency forPrivate Insurance and the Secretariat forComplementary Pensions. These bodiesof the Federal Government areresponsible for formulating monetarypolicy, directing the functioning of thesystem within the macroeconomicguidelines and regulating the activities ofinstitutions in the operating subsystem.These bodies are assisted in specific

situations by others, which, whileoperating in nature, also takeresponsibility for specific regulatoryguidelines, such as Banco do Brasil(farm credit), the National Bank forEconomic and Social Development (long-term development) and the Federal Savings Bank (home financing).

The operating subsystem is made up of full-service (bancos múltiplos),commercial and investment banks,savings and loans, leasing companies,securities distributors and brokers,among others. The custody andsettlement of almost all transactions in the banking sector are processed by specialised independent entities; and the agility and dependability withwhich transactions are processed in this operating subsystem deserves note. This environment was further enhancedafter implementation in 2002 of thenational Brazilian Payment System(SPB), resulting in the processing ofsettlements on a virtually real-time basisthus permitting better management ofsystemic risk in the financial system.Given the size of Brazil, in bothgeographic and population terms and the scale of technology applied, the new national payment system is remarkable.

Although the regulatory environment iscomplex, guidelines for the functioningof each of the regulatory units are welldefined. Supervisory procedures andregulations have also improved, reflectingthe strengthening of expertise locally,largely as a result of the application ofbest regulatory practices from abroad.

The beginnings of inflation

Inflation in the Brazilian economy veeredout of control at the start of the 1980s.Inflation indices reached annual levels of nearly 100% and by the mid 1980sreached levels in excess of 200%. At thetime, the economy did not benefit fullyfrom mechanisms that were capable ofreducing the risks inherent in suchcircumstances. Although thesemechanisms (such as the application ofmonetary correction to transactions andthe existence of a significant overnightmarket) already existed, they were notaccessible by all bank customers,especially the less sophisticated. The first consequences of adapting tothis enviroment included a reduction inthe provision of long-term credit bybanks and the collapse of homefinancing, since the maturity of availablefunding was shorter than maturitiestypically required for home loans.

21

the journal • Tackling the key issues in banking and capital markets

Paulo MironPartner, Banking and CapitalMarkets, Brazil

Tel: 55 11 3674 3788Email: [email protected]

Graham NyePartner, Banking and CapitalMarkets, Brazil

Tel: 55 11 3674 3534Email: [email protected]

Sergio RoganteSenior Manager, Banking andCapital Markets, Brazil

Tel: 55 11 3674 3925Email: [email protected]

The Brazilian banking system wasdivided among four broad groups at the start of the 1980s: federally-ownedbanks, state-owned banks, privateBrazilian-controlled banks and foreign-controlled banks. These groups eachhad separate and diverse interests anddeveloped business strategies that werequite different from one another.

Federally-owned banks for the most part focused on developing andimplementing specific credit policiessuch as farm credit, urban and regionaldevelopment, among others. Banco doBrasil and Caixa Econômica Federal,both large federally-owned banks,developed extensive branch networksthat competed directly with other retailbanks and covered regions andcustomers that were not always of

interest to private sector financialinstitutions. The administrative structuresof these banks were not very efficientbecause employees received employmentbenefits only available in the publicsector, such as tenured positions anddifferentiated retirement schemes.

State-owned banks also developed retailnetworks but these were mostly limitedto their state of origin. They implementedcredit policies that complemented thepolitical interests of the governors ofthese states. Their administrativestructures were generally similar to thoseof federally-owned banks.

Domestically-controlled private banksduring this time comprised of two distinctgroups. The first operated nationwide aspart of a financial conglomerate with a

large national branch network and with a broad range of products and services.The second operated in a more regionalform and served a specific market niche.

Foreign-controlled banks had historicallyheld a relatively small market share in the Brazilian financial market. For themost part, they were organised asrepresentative offices of traditionalinternational institutions that managedlines of financing offered to Braziliancompanies, usually focusing oninternational trade finance. A select few had a retail presence; this waslimited to large urban centres focusingon high net worth individuals, large local corporates and employees ofinternational organisations’ global clients.

Hyperinflation and initialefforts to rationalise costs

In 1986, the implementation of a plan by the government (the Plano Cruzado)to halt the inflationary spiral then incourse put the financial system and the economy as a whole to the test. The main objective of this economic plan was to reduce inflation by anartificial control of prices. The shortperiod of relative stability during 1986,following its implementation, exposedthe fragility of the financial system in an environment with controlled prices. This fragility was attributable to the

Brazil – A review of the effects of inflation on the banking sector continued...

22

the journal • Tackling the key issues in banking and capital markets

0

50

100

150

200

250

1978

40.80%

77.20%

110.30%

95.20% 99.70%

211.00% 223.80%

235.10%

65.00%

1979

%

1980 1981 1982 1983 1984 1985 1986

Domestic General Price Index

Figure 1: Brazilian inflation – Inflationary period

Source: Getulio Vargas Fundation

adaptation of the system to the inflationaryenvironment. Banks had become overlydependent on ‘float’ revenues, that is, theinflationary gains made on the distortedspreads between the interest andindexation on assets, and the cost of theirnon-indexed and non-interest or lowinterest bearing funds. This income grewto as much as 70% of the operatingmargins of banks during the inflationaryperiod that preceded the Plano Cruzado.Without the gains, banks with excessivecost bases – there had been little pressureto control these, since the largest,remuneration of staff, had not beensubject to the levels of indexation thatbanks’ assets had benefited from – had torestructure quickly. Two large banksbecame insolvent due to the loss of theseinflationary gains and were subsequentlyliquidated by the government.

The hyperinflationary period thatfollowed the Plano Cruzado from 1987reduced the banks’ ability to generatedirect float revenues as depositors wereforced to protect themselves againstconstant daily inflation and manage theirliquid funds more effectively by usinginstruments available in the overnightmarket. However, during this period, realinterest rates and spreads increased(compensating the banks for loss of floatrevenues), which further focused banks’activities on lending and deposit takingoperations as an easy source of income.

It became evident that the system wouldface many problems in a stableeconomic environment given banks’dependency on float revenues generatedduring periods of high and hyperinflation(see Figure 2).

One of the side-effects of the inflationaryperiod is that the financial system wasforced to, and had the resourcesavailable to, modernise by developinghigh quality technology-intensiveprocesses. Brazilian banks havedeveloped a reputation for theirtechnological astuteness and many of them use integrated and real-timesystems, especially in their retail andrelated treasury operations. Conversely,the exceptional float revenues alsopermitted the survival of institutions that

had a scale of operations which wasbelow their natural breakeven point andcosts that exceeded accepted levels. As noted earlier, cost control had notbeen a major concern during theinflationary periods due to the distortedlevels of float income.

One of the most significant stepstowards rationalisation of costs in theBrazilian financial sector involved theimplementation of the banco múltiplo or commercial bank concept in 1988.Before this, financial conglomerates wererequired to organise their activities indifferent financial areas using separatelegal entities. The banco múltiploconcept allowed these different activitiesto be grouped in a single business entity, thus reducing operating costs.

23

the journal • Tackling the key issues in banking and capital markets

0

500

1000

1500

2000

2500

3000

1987

415.83%

1037.60%

1782.90%

1476.60%

480.18%

1157.95%

2708.60%

1093.84%

1988

%

1989 1990 1991 1992 1993 1994

Domestic General Price Index

Figure 2: Brazilian inflation – Hyperinflationary period

Source: Getulio Vargas Fundation

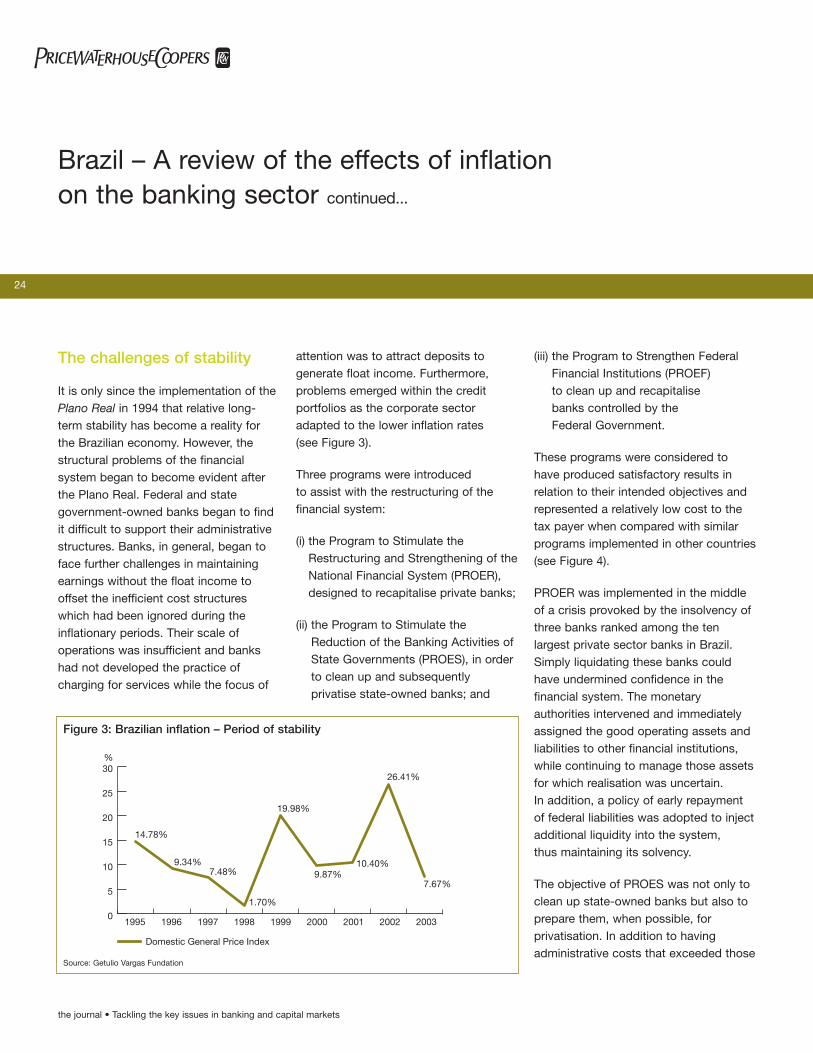

The challenges of stability

It is only since the implementation of thePlano Real in 1994 that relative long-term stability has become a reality forthe Brazilian economy. However, thestructural problems of the financialsystem began to become evident afterthe Plano Real. Federal and stategovernment-owned banks began to findit difficult to support their administrativestructures. Banks, in general, began toface further challenges in maintainingearnings without the float income tooffset the inefficient cost structureswhich had been ignored during theinflationary periods. Their scale ofoperations was insufficient and bankshad not developed the practice ofcharging for services while the focus of

attention was to attract deposits togenerate float income. Furthermore,problems emerged within the creditportfolios as the corporate sectoradapted to the lower inflation rates (see Figure 3).

Three programs were introduced to assist with the restructuring of thefinancial system:

(i) the Program to Stimulate theRestructuring and Strengthening of theNational Financial System (PROER),designed to recapitalise private banks;

(ii) the Program to Stimulate theReduction of the Banking Activities ofState Governments (PROES), in orderto clean up and subsequentlyprivatise state-owned banks; and

(iii) the Program to Strengthen FederalFinancial Institutions (PROEF) to clean up and recapitalise banks controlled by the Federal Government.

These programs were considered tohave produced satisfactory results inrelation to their intended objectives andrepresented a relatively low cost to thetax payer when compared with similarprograms implemented in other countries(see Figure 4).

PROER was implemented in the middleof a crisis provoked by the insolvency ofthree banks ranked among the tenlargest private sector banks in Brazil.Simply liquidating these banks couldhave undermined confidence in thefinancial system. The monetaryauthorities intervened and immediatelyassigned the good operating assets andliabilities to other financial institutions,while continuing to manage those assetsfor which realisation was uncertain. In addition, a policy of early repaymentof federal liabilities was adopted to injectadditional liquidity into the system, thus maintaining its solvency.

The objective of PROES was not only toclean up state-owned banks but also toprepare them, when possible, forprivatisation. In addition to havingadministrative costs that exceeded those

Brazil – A review of the effects of inflation on the banking sector continued...

24

the journal • Tackling the key issues in banking and capital markets

0

5

10

15

20

25

30

1995

14.78%

9.34%7.48%

1.70%

19.98%

9.87%10.40%

26.41%

7.67%

1996

%

1997 1998 1999 2000 2001 2002 2003

Domestic General Price Index

Figure 3: Brazilian inflation – Period of stability

Source: Getulio Vargas Fundation

of private sector institutions, these bankswere also used by state governments tofinance their debt and for other politicalpurposes. Accordingly, loan delinquencyratios were higher than the average in the Brazilian market. The PROESstimulated the ‘federalisation’ of thesebanks, that is, majority ownership wastransferred to the federal government. A process that included restructuringand recapitalisation was then initiated,ready for privatisation.

PROEF was instituted to clean up andcapitalise the four main federallycontrolled banks: Banco do Brasil, CaixaEconômica Federal, Banco do Nordeste,

and Banco da Amazônia. These banksheld a significant volume of loans thatwere unlikely to be realised or for whichreturns were insufficient as a result of thedevelopment policies of the federalgovernment. The approach in this caseinvolved the transfer of these credits tothe National Treasury, as well as theexchange of other non-liquid assets forones with more liquidity and returnscompatible with market levels.

Facing international crises

The Asian Crisis in 1997 presented anotherchallenge for the Brazilian financial system.Immediately prior to the crisis, the domesticeconomy was being prepared for a gradualreduction in basic interest rates, while thebanking system developed new service-related business strategies. Some privatesector banks, especially those with smallerscale operations, began to borrow payingfloating rates, while lending these samefunds at fixed rates. However, the AsianCrisis resulted in local interest ratesincreasing significantly and unexpectedly.The Central Bank of Brazil acted byidentifying institutions with problems andrequiring action from shareholders orfacilitating the transfer of control to thestate before the situation worsened.

This facilitated the entry of new players –international banks – into the Brazilianbanking system. These institutions, whichhad previously limited interests in Brazil,entered the Brazilian banking system bytaking part in privatisation processes oracquiring medium-sized private sectorbanks caught up in the after-effects of theAsian crisis. Accordingly, of the eighteenlargest deals involving acquisitions,associations or privatisations in theBrazilian banking market between 1997and 2002, nine involved an internationalfinancial institution as buyer (see Figures5 and 6 overleaf).

25

the journal • Tackling the key issues in banking and capital markets

Figure 4: Comparison between countries

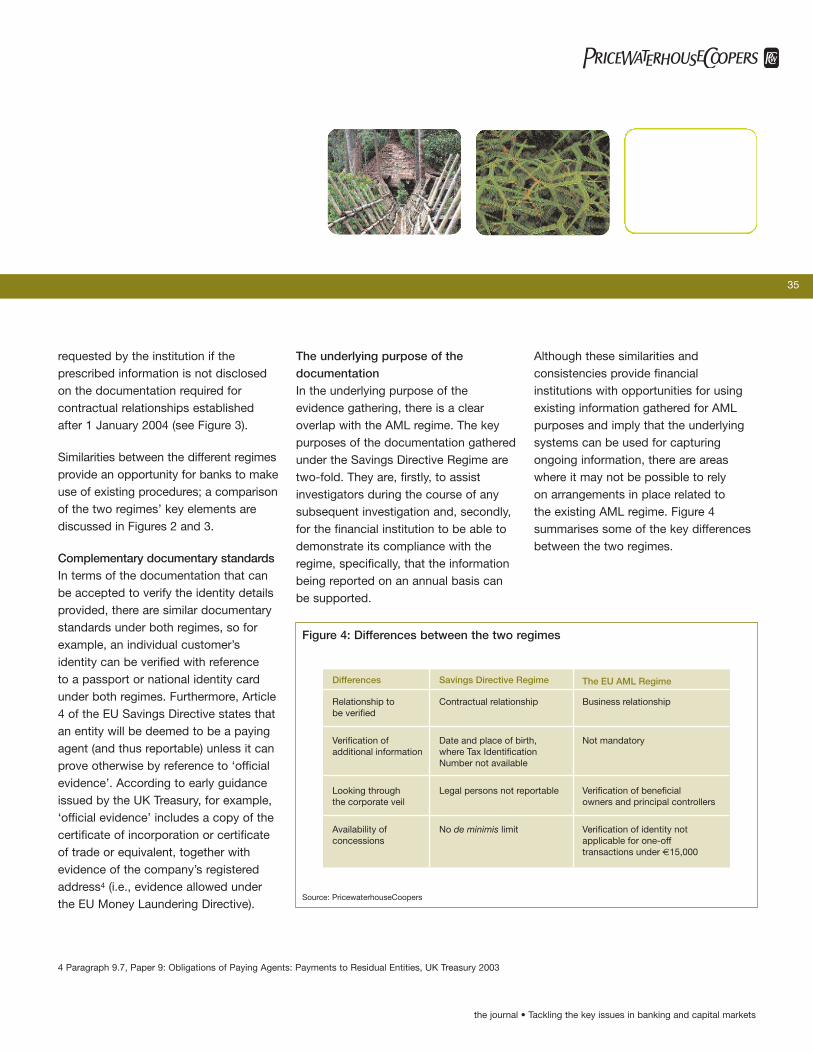

Source: Rojas-Suarez, Liliana, and Weisbroad, Steven R, ‘Banking Crises in Latin America: Experience and Issues’ BID (1995);Brazil: Central Bank of Brazil

Year Country Fiscal cost/GDP

1982 Argentina 13.00%

1985 Chile 19.60%

1985 Colombia 6.00%

1988 – 1992 Norway 4.50%

1991 – 1993 Finland 8.20%

1991 – 1993 Sweden 4.50%

1991 United States 5.10%

1994 Venezuela 13.00%

1995 – 1997 Brazil 1.40%

Brazil then faced the so-called ‘BrazilianCrisis’ during 1999. The practical effect of this attack on its currency, the Real, resulted in its devaluation byapproximately 70% during the month of January 1999. This did not, however,result in serious consequences for thebanking sector, because many of thelarger banks had anticipated thedevaluation and entered into appropriatehedging arrangements. The CentralBank of Brazil provided the liquidity tothe market while attempting to preservethe value of Brazil’s currency throughintervention in the derivatives marketsselling dollars. Only two small bankscollapsed in this period as a result of thesuccess of the initiative.

Consolidation andperspectives

The profile of the Brazilian banking sectoris currently concentrated (the 20 largestbanks hold approximately 80% of totalassets in the system). The dominantbanks include the two largest federally-owned banks and the three largestdomestic private sector banks (whichoccupy the first five positions by assets)and five large international banks. In theshort term, there is no expectation ofsignificant change to this position.

Brazil – A review of the effects of inflation on the banking sector continued...

26

the journal • Tackling the key issues in banking and capital markets

Private sector banks 41%

International banks8%

Government-owned banks51%

Figure 5: Market shares in the Brazilian financial system – 1993

Source: Central Bank of Brazil

Private sector banks 37%

International banks27%

Government-owned banks36%

Figure 6: Market shares in the Brazilian financial system – 2002

Source: Central Bank of Brazil

Although the sector has become moreconcentrated, some institutions withinthe largest 20 have not yet acquired thescale of business necessary to achievethe sector’s average level of profitability.In addition, the macroeconomicenvironment still holds challenges thathave yet to be dealt with by the sector.Brazil still has the second highest realinterest rate in the world after Turkey.Lowering the basic interest rate is aparticularly difficult challenge in Brazil,due to the fact that decreases in rates,while benefiting the government from acost perspective, seriously increase therisk of hot money exiting the economyand downward pressure on the value ofthe Real. The Government’s economistshave nevertheless indicated that interestrates should fall gradually over 2004. Infact, the Brazilian economy’s inter-bankinterest rate has already fallenapproximately 10 percentage pointssince July 2003 to its present level of16.0% per annum. Furthermore,competition for banks and other lendersremains intense since, outside of theGovernment, there are relatively fewcorporates and other borrowersconsidered sound enough from a creditperspective and the consumer financemarket is in its infancy (in relative terms).These factors point to a continuedsqueeze of bank spreads.

One of the alternatives for banks foreseenby the industry is the redirecting of fundsthat are presently invested in the moneymarket, mainly in federal governmentsecurities, to corporate and consumerloan portfolios that provide higherreturns. The share of loan portfolios intotal financial assets in Brazil is still small(approximately 25% as of December2003) and the capital ratios of Brazilianbanks would allow this realignment (theaverage capital adequacy ratio of the 20 largest Brazilian banks is around 21% measured by reference to the Basel Accord (see Figure 7 overleaf)).Large banks have, therefore, begun toplace more emphasis on their consumerloan businesses and the generation of commission business from services.This segment was previously served bysmaller financial institutions. By focusinggrowth on their consumer loan business, the larger banks are also targeting thelarge number of individuals who havetraditionally not done business withbanks. Lower inflation rates havebenefited the country’s huge segment of society which has operated in a cash-only economy: banks are now targetingthis sector as the poor become morebankable and in their search for greaterbusiness volume and market share.

27

the journal • Tackling the key issues in banking and capital markets

Highlights of Brazil: 2003-2004

For more details of our annualpublication, please visitwww.pwc.com/soacat or [email protected] [email protected]

Brazil – A review of the effects of inflation on the banking sector continued...

28

the journal • Tackling the key issues in banking and capital markets

Figure 7: Top 20 banks in Brazil by total assets (US$)

Source: Central Bank of Brazil

Bank Capital Total assets Deposits Equity Number of Number of (Capital(in thousands (in thousands (in thousands branches employees ratio)

of dollars) of dollars) of dollars)

1 Banco do Brasil Brazil – Public 79.635 38.067 4.212 3.296 97.258 13.65%

2 Caixa Econômica Federal Brazil – Public 52.074 28.036 1.997 2.046 100.498 19.24%

3 Bradesco Brazil – Private 50.922 20.157 4.691 3.060 70.716 19.85%

4 Itaú Brazil – Private 38.048 12.963 4.426 2.258 49.487 20.22%

5 Unibanco Brazil – Private 22.018 9.021 2.545 912 24.096 18.60%

6 Santander Spain 19.737 6.305 2.663 1.026 21.458 18.08%

7 ABN Amro Real The Netherlands 18.842 9.258 2.908 1.145 29.750 19.55%

8 Safra Brazil – Private 11.772 3.003 1.085 82 4.344 15.59%

9 Nossa Caixa Brazil – Public 9.528 6.571 631 505 13.822 28.67%

10 HSBC United Kingdom 9.088 5.236 657 928 20.792 14.39%

11 Votorantim Brazil – Private 8.638 3.046 825 4 320 22.12%

12 Citibank USA 7.042 426 1.138 45 2.099 20.85%

13 BankBoston USA 6.733 1.142 883 60 3.837 21.33%

14 BNB Brazil – Public 4.414 957 455 175 6.472 22.55%

15 Banrisul Brazil – Public 4.083 2.653 277 380 8.648 16.69%

16 Credit Suisse Switzerland 3.185 541 235 2 12 56.59%

17 Pactual Brazil – Private 2.353 360 191 4 332 20.48%

18 JP Morgan Chase USA 2.186 313 465 5 298 16.74%

19 Alfa Brazil – Private 2.131 544 346 9 765 21.82%

20 Santos Brazil – Private 2.124 606 189 4 323 12.59%

29

the journal • Tackling the key issues in banking and capital markets

Ironically, the effects of the ‘inflationary’years have resulted in the sector beingtechnologically advanced but, bycomparison internationally, narrower in the nature and breadth of bankingservices offered and from whichrevenues are generated.

The Brazilian financial system ascurrently structured has provided itsparticipants with excellent returns. The average return on net income for the ten largest financial conglomerateswas 23% in 2003. Economic stability,falling interest rates and consequentrealigning of resources towards higher risk portfolios point to a potentialreduction in these returns for theindustry. This, in turn, will be offset asthe overall market for bankablecustomers and the nature of both basicand sophisticated services offered bybanks continues to grow.

Practical difficulties of adoptingthe identification requirements of the EU Savings Directive

30

the journal • Tackling the key issues in banking and capital markets

by Sian Herbert, Bob Harland and Laurent de La Mettrie

Over the last 15-20 years, there has beenincreasing tension between the majoronshore economies and the offshorefinancial centres (both the traditionalisland tax havens and the onshorejurisdictions that place a substantialpremium on banking secrecy) over theextent to which national tax revenueswere being eroded through the use ofoffshore investments and structures.

As national economies experiencedsignificant pressure to reduce rates of direct taxes, so have the majoronshore economies focused increasinglyupon the loss of tax revenue throughfunds held offshore. The use of heavypenalties for tax evasion and complexanti-tax avoidance measures have been invoked by most national taxauthorities with varying degrees ofsuccess. However, in the absence ofcomprehensive information on investorprofiles and concrete information on thesums involved, the tax authorities oftenappear to be groping in the dark.

Achieving a political consensus on themost appropriate way to handle thissituation has not been an easy task, with anumber of prominent financial institutionsand governments collectively recognising

the wider economic implications of taxevasion (and its frequent links to criminalactivities) but acknowledging at anindividual level the profitability of manyaspects of offshore finance.

The predicament has been highlighted inthe differing approaches to the questionof how to counter tax evasion that theUnited States and the EU have adopted.

The United States introduced its QualifiedIntermediary (QI) regime in 2001. Althoughthere were protests in relation to theglobal reach of the regime, there was alsowidespread acceptance of the economicreality of the United States’ ability to:

(a) secure acceptance of the concept of the QI regime in most countries;

(b) require institutions to provide data oninvestments held on behalf of relevantcustomers;

(c) require minimum standards for Know-Your-Customer (KYC) requirements at both national and institutionallevels; and

(d) ensure compliance with the regime on an ongoing basis at relatively littlecost to the United States’ authorities.

The EU’s approach to the problem has developed over a longer timespanreflecting the political reality of theeconomies of some EU member statesprofiting historically from assisting the residents of other member states to shelter or defer their domestic tax liabilities.

By June 2000, there was acceptanceamongst the EU member states of the need for effective taxation of cross-border savings by individuals.Three years of debate within the EU and some key non-member statesresulted in the Council of the EuropeanUnion agreeing to adopt a new lawdealing with the taxation and reporting of savings income in the form of interestpayments (the ‘Savings Directive’ or ‘Directive’) on 3 June 2003. The term‘interest payments’ is broadly definedand, for example, includes dividends onbond funds and the income element ofthe proceeds of the encashment or saleof units in an accumulation fund.

The aim of the Directive is to enablesavings income in the form of interestpayments made in one member state toBeneficial Owners1 to be made subjectto effective taxation in accordance with

31

the journal • Tackling the key issues in banking and capital markets

Sian HerbertDirector, UK Anti-Money Laundering Team

Tel: 44 20 7212 4351Email: [email protected]

Laurent de La MettriePartner, Tax and Legal Services,Luxembourg

Tel: 352 49 48 48 32 04Email: [email protected]

Bob HarlandPartner, Tax and Legal Services, UK

Tel: 44 20 7213 1954Email: [email protected]

1 Individuals resident for tax purposes in another member state.

the national laws of the latter memberstate. It does this by requiring financialinstitutions that make payments ofinterest cross-border to submitparticulars of the payee and the interestpayment to the tax authorities of theterritory in which the institution is based.This information is then passed to thetax authorities where the recipients areconsidered to be resident underarrangements for the exchange ofinformation. A number of territories havethe option of charging a withholding taxas an alternative to the exchange of information2.

It is apparent from the experience of a number of financial institutions whichare seeking to apply both the reportingand withholding regimes that thesystems’ implications of compliance with both are considerable. The relativelyshort timescale that is available tosecure operational readiness is posing a significant burden on those responsiblefor systems development andimplementation, as well as productdevelopment and marketing.

The territorial application of the Directiveis not just limited to the existing EUmember states: it also embraces themember states’ dependent territories e.g.Jersey, The Cayman Islands, Netherlands

Antilles, as well as Switzerland,Liechtenstein, Andorra, San Marinoand Monaco. Although extensive, theterritorial scope is clearly less than thatachieved by the United States with its QI regime. The Directive imposes,however, significant new requirements on all financial institutions involved in thepayment of interest to beneficial ownersin the EU, irrespective of the location ofthe institution’s headquarters.

The implementation of the Directive hasconsiderable implications for mostfinancial institutions that provide servicesand products to individuals, particularlyfor institutions with operations in thosejurisdictions that have elected to apply a withholding tax.

The work involved in preparing for theoperation of the Directive is extensiveand the scale of the task often onlybecomes clear as projects get underway.Issues identified include:

• The Directive may impact not onlymost aspects of private banking andretail fund management, but also morespecialised areas of businesses suchas private equity and hedge funds;

• The basic data on investments requiredfor the day-to-day application of theDirective is not readily available and

systems need to be put in place toensure that reports of interest paymentscan be compiled and reviewed;

• The interpretation of the Directivevaries between most territoriesaffected by it, leading to the risk of omissions and the need for coordination of advice from all relevant jurisdictions beforeimplementing systems changes; and