Embed Size (px)

DESCRIPTION

Banking

Citation preview

Evaluation of Banking Performance

Ratio Analysis technique is often used for evaluating banking performance.

Broadly speaking, there are two important performance dimensions, namely:

Profitability Risk

Prepared by: Mr. Amir Ikram 2

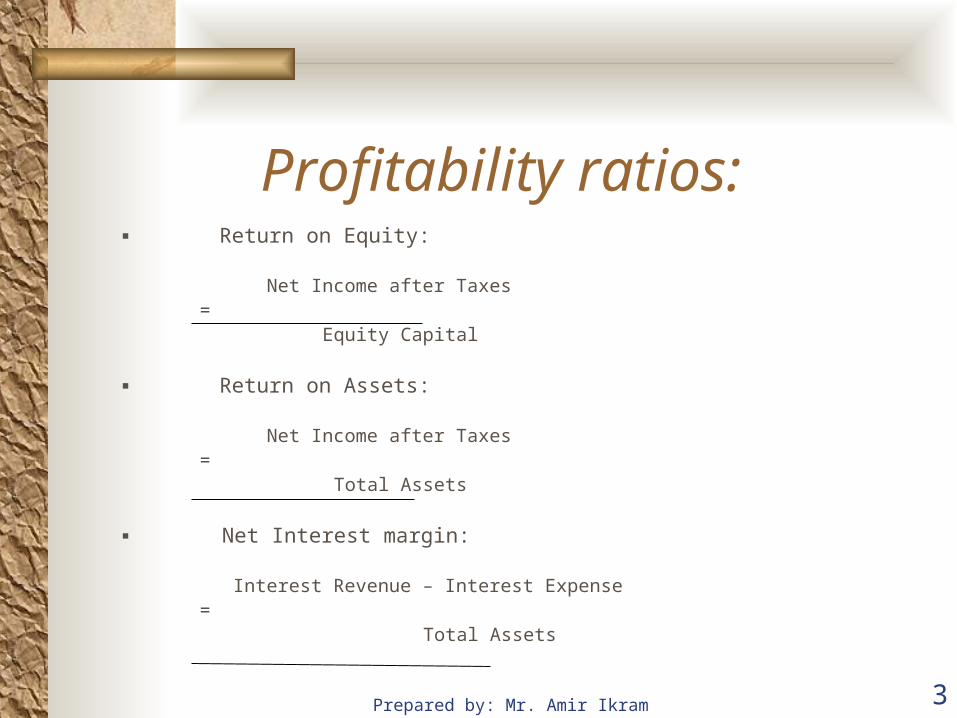

Profitability ratios: Return on Equity: Net Income after Taxes = Equity Capital Return on Assets: Net Income after Taxes = Total Assets Net Interest margin: Interest Revenue – Interest Expense = Total Assets

Prepared by: Mr. Amir Ikram 3

Profitability ratios: Net Non-Interest margin: Non-interest Revenue – Non-interest Expense = Total Assets Net bank operating margin: Total operating Revenues – Total operating Expenses = Total Assets Earning Per share of stock (EPS): Net Income after taxes = Common shares outstanding

Prepared by: Mr. Amir Ikram 4

Risk:Main Risks faced by banks:

Credit Risk Liquidity Risk Market Risk Interest-rate Risk Earning Risk Solvency Risk

Prepared by: Mr. Amir Ikram 5

Risk Analysis:

Credit risk:

“The danger of default by the borrower

to whom the bank has extended credit”

Prepared by: Mr. Amir Ikram 6

Credit risk_Indicators: Non-performing loans = Total loans & leases Net Charge-offs = Total loans & leases Provision for loan losses = Total loans & leases or Equity capital Allowance for loan losses = Total loans & leases or Equity capital

Prepared by: Mr. Amir Ikram 7

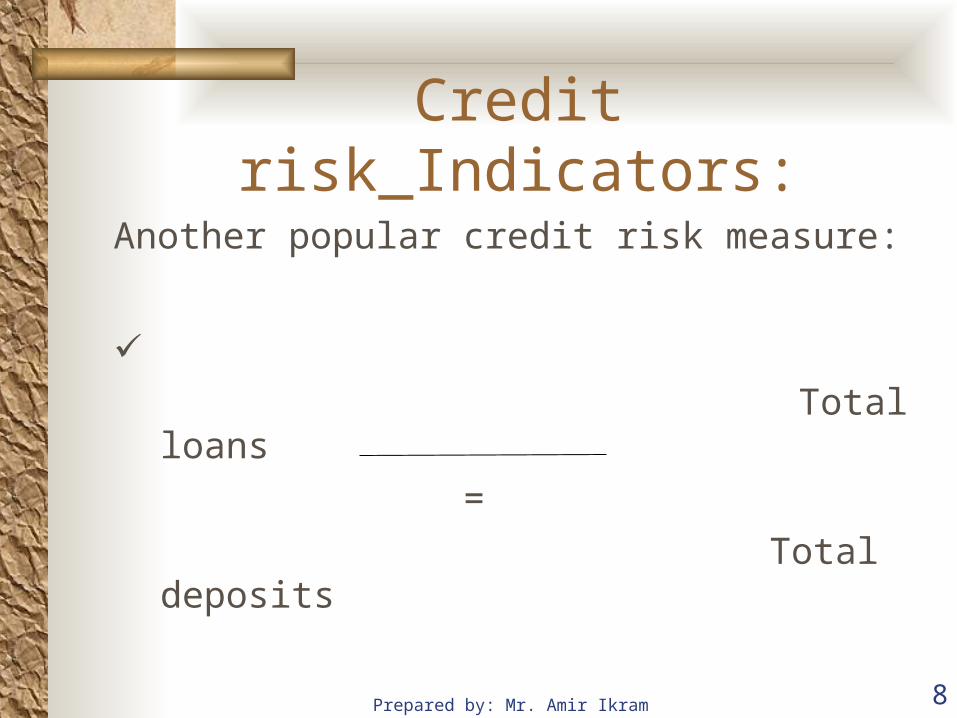

Credit risk_Indicators:Another popular credit risk measure:

Total loans = Total deposits

Prepared by: Mr. Amir Ikram 8

Liquidity risk:

‘The danger of having insufficient cash to meet obligations when due.’

Prepared by: Mr. Amir Ikram 9

Liquidity risk_indicators: Purchased funds = Total Assets

Net loans = Total Assets

The higher the ratio, the greater is the risk.

Prepared by: Mr. Amir Ikram 10

Liquidity risk_indicators: Cash & due from other banks = Total Assets Cash & Govt. Securities = Total Assets

Prepared by: Mr. Amir Ikram 11

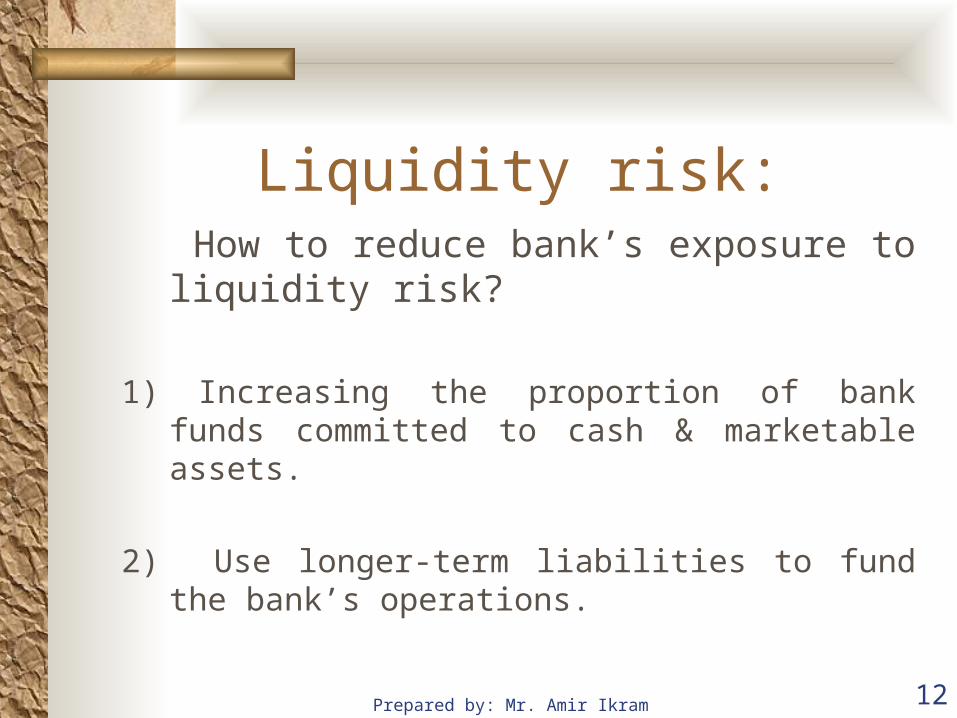

Liquidity risk: How to reduce bank’s exposure to liquidity risk?

1) Increasing the proportion of bank funds committed to cash & marketable assets.

2) Use longer-term liabilities to fund the bank’s operations.

Prepared by: Mr. Amir Ikram 12

Market Risk:

“The danger of changing market values of bank assets, liabilities, and equity that may bring about loss.”

Prepared by: Mr. Amir Ikram 13

Market Risk:Main reasons:

Changes in market interest rates Changes in currency prices Shifting public demand for bank services Alteration in central bank policy

Bank’s perception in the eyes of investor.

Prepared by: Mr. Amir Ikram 14

Market Risk_indicators: Book value of Assets = Market value of Assets Book value of Equity Capital = Market value of Equity Capital

Prepared by: Mr. Amir Ikram 15

Market Risk_indicators: Book value of bonds & other fixed assets = Market value of bonds & other fixed assets Market value of common & preferred stock = Common & preferred shares outstanding

Prepared by: Mr. Amir Ikram 16

Interest Rate risk:

“The danger of shifting interest rates may adversely affect a bank’s net income, the value of its assets, or equity.”

Prepared by: Mr. Amir Ikram 17

Interest Rate risk:E.g, if a bank’s flexible-rate assets are greater than its

flexible-rate liabilities, i.e.,Flexible-rate assets/Flexible-rate liabilities > 1

And if interest-rate increases???

Here it will be beneficial for the bank…resulting in increased profit margin.

Prepared by: Mr. Amir Ikram 18

Interest Rate risk:Profit margin will be higher, if

Interest-rate falling Flexible-rate assets < Flexible-rate liabilities

Interest-rate rising Flexible-rate assets > Flexible-rate liabilities

Prepared by: Mr. Amir Ikram 19

Interest-rate risk_indicators: Interest-sensitive Assets = Interest-sensitive Liabilities

Prepared by: Mr. Amir Ikram 20

Interest-rate risk_indicators: Uninsured Deposits = Total Deposits

The higher the ratio, the greater is the risk.

Prepared by: Mr. Amir Ikram 21

Earnings risk:

“The danger that a bank’s rate of return on assets (ROA) or equity (ROE) or its net earnings may fall.”

Prepared by: Mr. Amir Ikram 22

Earnings risk_Indicators:

Standard deviation or Variance of net income (NI). Standard deviation or Variance of the bank’s

return on Assets (ROA) & return on equity (ROE).

The higher the standard deviations, the more risky the bank is.

Prepared by: Mr. Amir Ikram 23

Solvency risk:

“Risk to bank’s long-term survival is called solvency risk. The danger that a bank may

fail due to negative profitability and erosion of its capital.”

Prepared by: Mr. Amir Ikram 24

Solvency risk:Reasons: Excessive number of bad loans Decline in market value to the large portion of

bank’s security portfolio.

Market discipline: Increased chance of failing fall in stock’s market value

high interest rates on borrowings (to attract needed funds).

Prepared by: Mr. Amir Ikram 25

Solvency risk_indicators:

Yield on bank debt issues – Yield on Govt. securities **Govt. securities should be of the same maturity. Greater the difference, the higher is the risk.

Prepared by: Mr. Amir Ikram 26

Solvency risk_indicators: Bank’s Stock price = Annual earnings per share

Net-worth (equity capital) = Total Assets

Decline in ratio Greater risk exposure.

Prepared by: Mr. Amir Ikram 27

Solvency risk_indicators: Purchased funds = Total Liabilities Net-worth (equity capital) = Risky Assets** Risk assets mainly include loans and securities.

Prepared by: Mr. Amir Ikram 28

Other forms of risk:

Inflation Risk Currency or Exchange rate risk Political risk Crime risk

Prepared by: Mr. Amir Ikram 29