Embed Size (px)

Citation preview

4

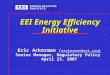

Electricity Is A Great Value

ConsumerPrice Index

Sources: U.S. Department of Labor, Bureau of Labor Statistics (BLS), and U.S. Department of Energy, Energy Information Administration (EIA).

January 2018 © 2018 by the Edison Electric Institute. All rights reserved.

(Percent)

HousingNaturalGas

HealthCare

TransportationFood &Beverage

Gasoline Electricity0

20

40

60

80

100

120

140

160

180

169%

112%

89% 83%88% 80%63% 61%

Increase in cost of selected consumer goods1991–2017 (nominal dollars)

Sources: U.S. Department of Labor, Bureau of Labor Statistics, and U.S. Department of Energy, Energy Information Administration.

10

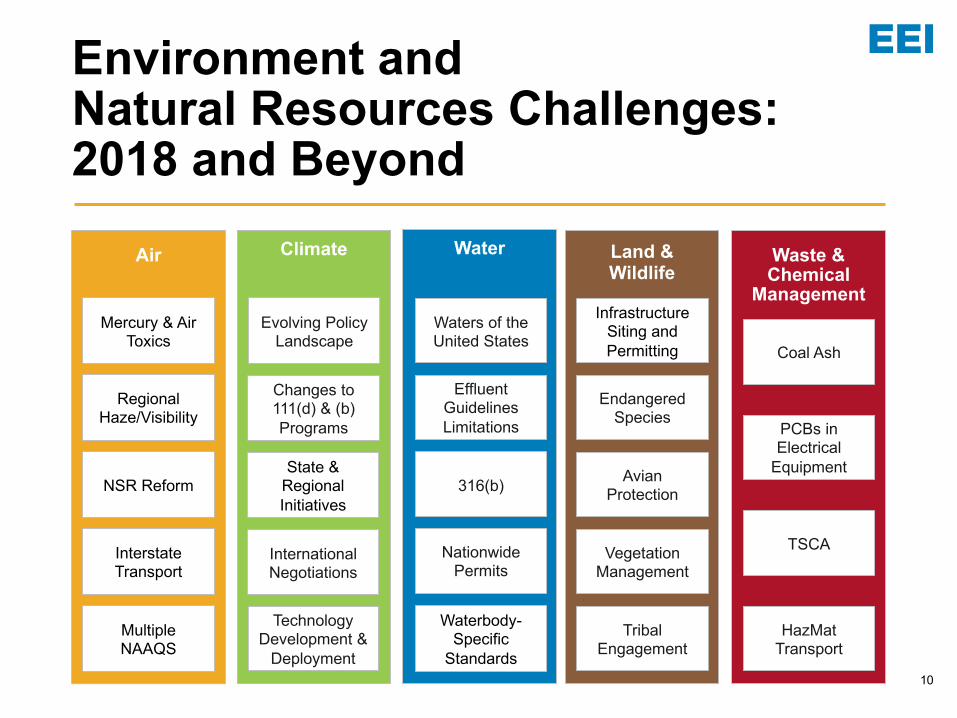

Environment and Natural Resources Challenges: 2018 and Beyond

Air Climate Water Land & Wildlife

Waste & Chemical

Management

Coal Ash

PCBs in Electrical

Equipment

HazMat Transport

Infrastructure Siting and Permitting

Endangered Species

Avian Protection

Vegetation Management

Waters of the United States

Effluent GuidelinesLimitations

316(b)

Nationwide Permits

Evolving Policy Landscape

Changes to 111(d) & (b) Programs

State & Regional Initiatives

International Negotiations

Mercury & Air Toxics

Regional Haze/Visibility

NSR Reform

Interstate Transport

Multiple NAAQS

Waterbody-Specific

Standards

TSCA

Technology Development &

Deployment

Tribal Engagement

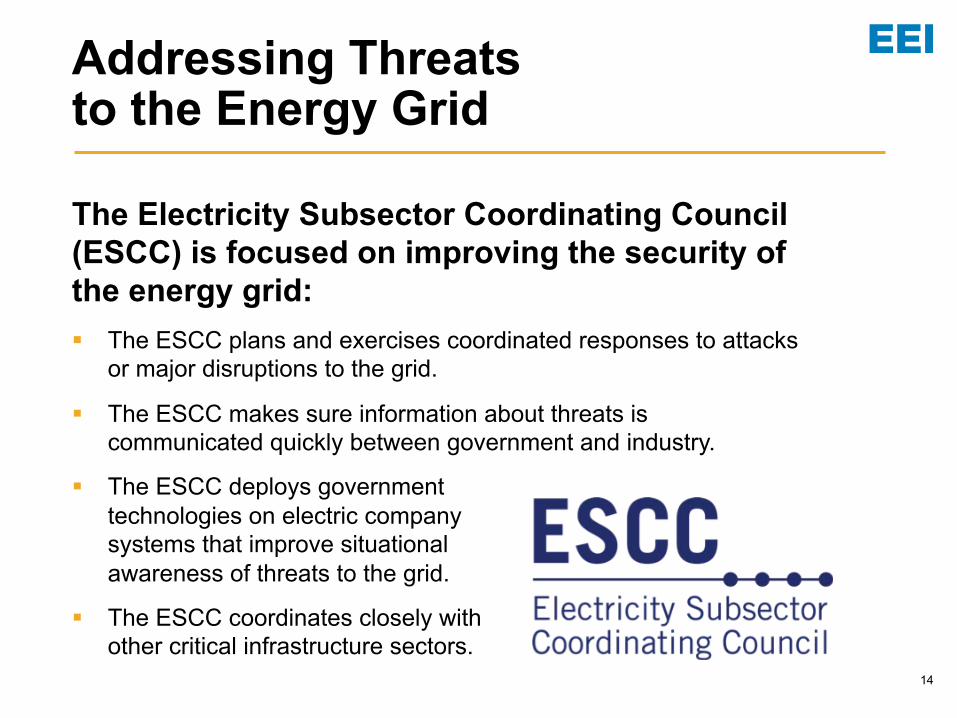

14

The Electricity Subsector Coordinating Council (ESCC) is focused on improving the security of the energy grid:§ The ESCC plans and exercises coordinated responses to attacks

or major disruptions to the grid.

§ The ESCC makes sure information about threats is communicated quickly between government and industry.

§ The ESCC deploys government technologies on electric company systems that improve situational awareness of threats to the grid.

§ The ESCC coordinates closely with other critical infrastructure sectors.

Addressing Threats to the Energy Grid

17

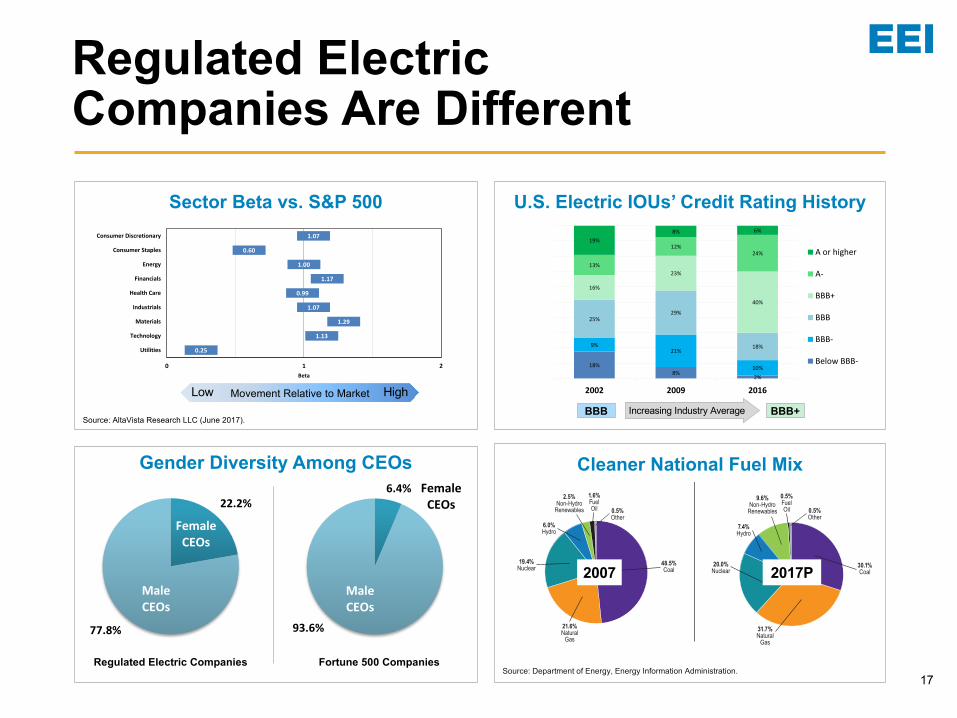

Cleaner National Fuel Mix

The Mix of Resources Used to Generate Electricity Is Changing Dramatically

Source: Department of Energy, Energy Information Administration.

2007 National Energy Resource Mix

2017 National Energy Resource Mix

(preliminary)

21.6%Natural

Gas

19.4%Nuclear

2.5%Non-Hydro

Renewables

6.0%Hydro

48.5%Coal

0.5%Other

1.6%FuelOil

31.7%Natural

Gas

20.0%Nuclear

9.6%Non-Hydro

Renewables

7.4%Hydro

30.1%Coal

0.5%Other

0.5%FuelOil

Sector Beta vs. S&P 500

0.25

1.13

1.29

1.07

0.99

1.17

1.00

0.60

1.07

0 1 2

Utilities

Technology

Materials

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

Beta

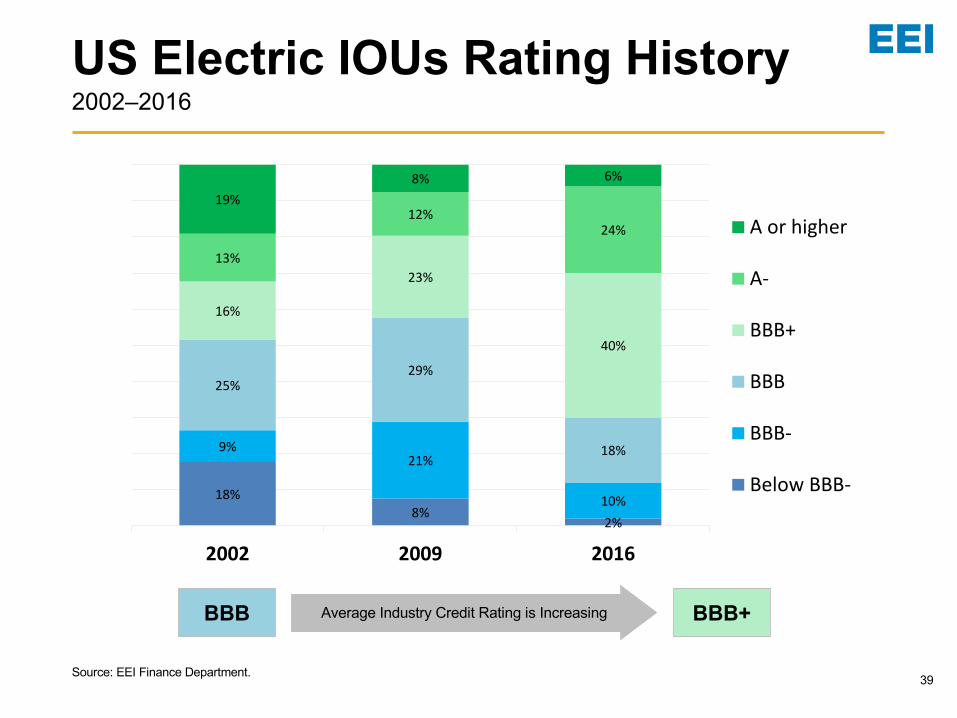

U.S. Electric IOUs’ Credit Rating History

18%8%

2%

9%21%

10%

25%29%

18%

16%

23%

40%

13%

12%24%

19%8% 6%

2002 2009 2016

A or higher

A-

BBB+

BBB

BBB-

Below BBB-

Regulated Electric Companies Are Different

Movement Relative to MarketLow High

Source: AltaVista Research LLC (June 2017).Increasing Industry AverageBBB BBB+

2007 2017P

Source: Department of Energy, Energy Information Administration.

Gender Diversity Among CEOs

22.2%

77.8%

Male CEOs

Female CEOs

6.4%

93.6%

Male CEOs

Female CEOs

Regulated Electric Companies Fortune 500 Companies

18

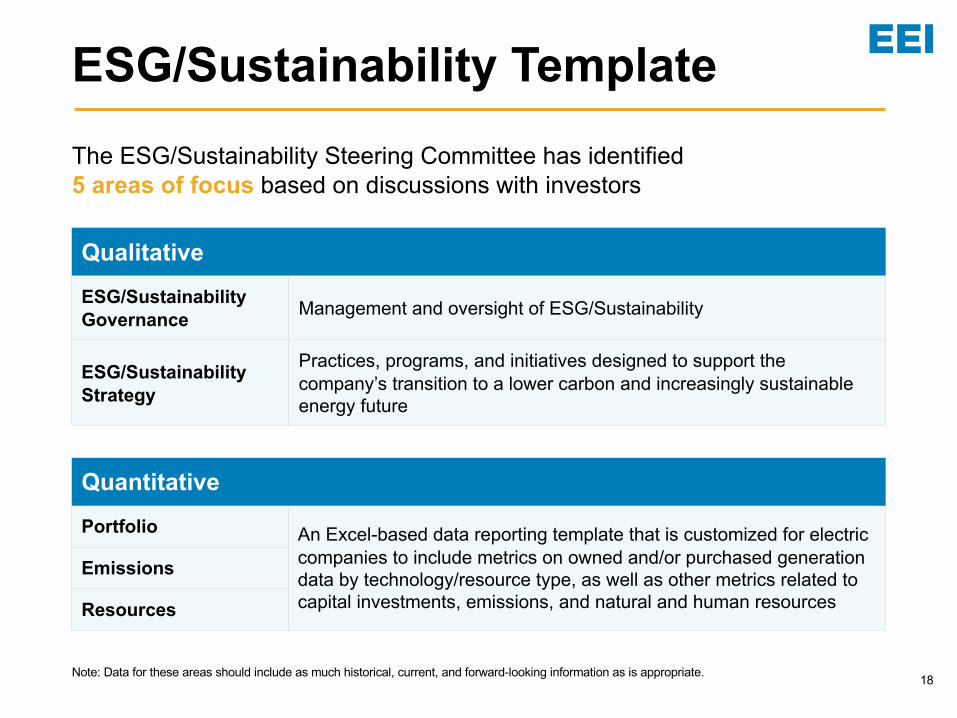

QualitativeESG/Sustainability Governance Management and oversight of ESG/Sustainability

ESG/Sustainability Strategy

Practices, programs, and initiatives designed to support the company’s transition to a lower carbon and increasingly sustainable energy future

ESG/Sustainability Template

QuantitativePortfolio An Excel-based data reporting template that is customized for electric

companies to include metrics on owned and/or purchased generation data by technology/resource type, as well as other metrics related to capital investments, emissions, and natural and human resources

Emissions

Resources

The ESG/Sustainability Steering Committee has identified 5 areas of focus based on discussions with investors

Note: Data for these areas should include as much historical, current, and forward-looking information as is appropriate.

19

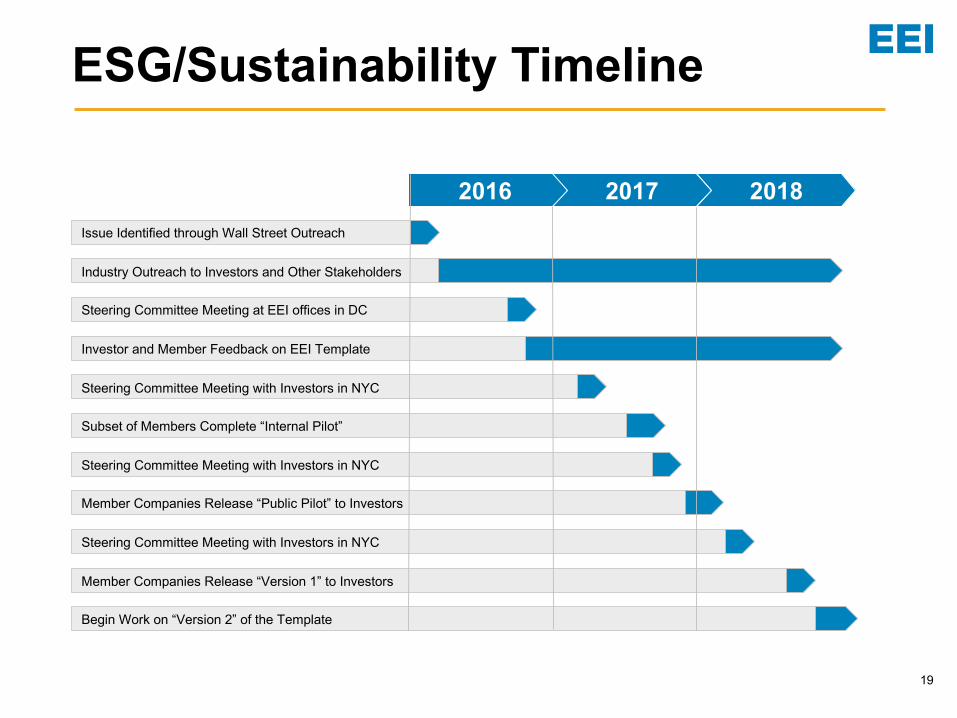

ESG/Sustainability Timeline

Subset of Members Complete “Internal Pilot”

Steering Committee Meeting at EEI offices in DC

Investor and Member Feedback on EEI Template

Industry Outreach to Investors and Other Stakeholders

Issue Identified through Wall Street Outreach

2016 2017 2018

Steering Committee Meeting with Investors in NYC

Steering Committee Meeting with Investors in NYC

Member Companies Release “Public Pilot” to Investors

Member Companies Release “Version 1” to Investors

Begin Work on “Version 2” of the Template

Steering Committee Meeting with Investors in NYC

21

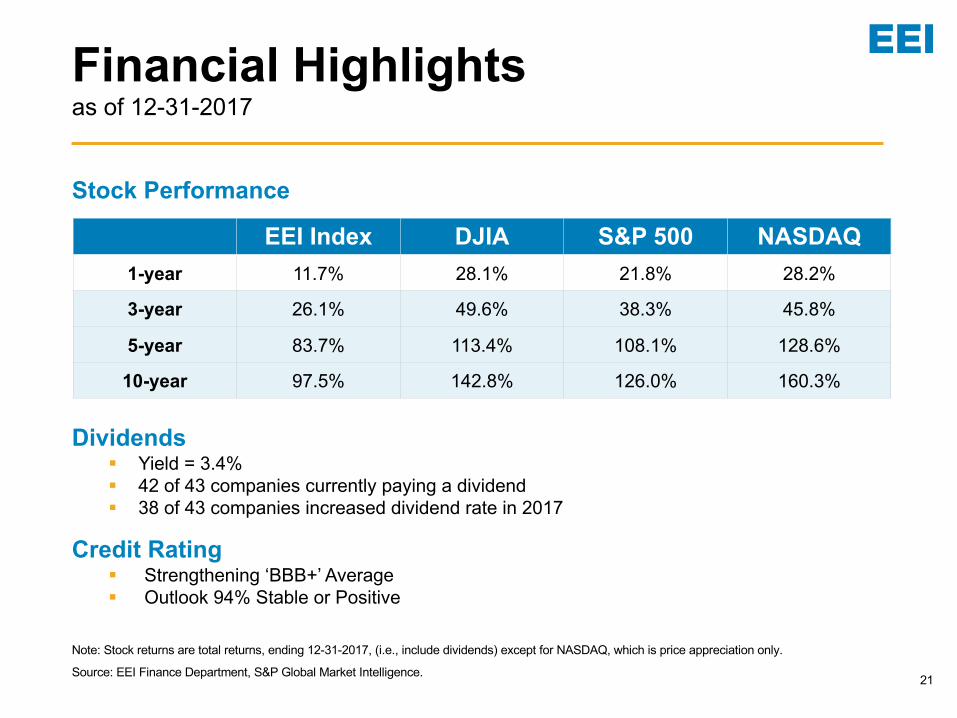

Financial Highlightsas of 12-31-2017

EEI Index DJIA S&P 500 NASDAQ1-year 11.7% 28.1% 21.8% 28.2%

3-year 26.1% 49.6% 38.3% 45.8%

5-year 83.7% 113.4% 108.1% 128.6%

10-year 97.5% 142.8% 126.0% 160.3%

Dividends§ Yield = 3.4%§ 42 of 43 companies currently paying a dividend§ 38 of 43 companies increased dividend rate in 2017

Credit Rating§ Strengthening ‘BBB+’ Average§ Outlook 94% Stable or Positive

Stock Performance

Note: Stock returns are total returns, ending 12-31-2017, (i.e., include dividends) except for NASDAQ, which is price appreciation only.

Source: EEI Finance Department, S&P Global Market Intelligence.

22

Industry Capital Expenditures

Actuals

Projections(Aug 2016)

Projections(Aug 2017)

Notes: Total company spending of U.S. Investor-Owned Electric Utilities, consolidated at the parent or appropriate holding company. Projections based on publicly available information and extrapolated for companies reporting fewer than three projected years (0.1% and 2.5% of the industry for 2018 and 2019, respectively).

Source: EEI Finance Department, company reports, S&P Global Market Intelligence (August 2017).

120.8

104.596.5

122.8114.0

109.0

74.1 82.8

77.7 74.378.6

90.3 90.396.1

104.0112.5

$30 B$40 B$50 B$60 B$70 B$80 B$90 B

$100 B$110 B$120 B$130 B

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

23

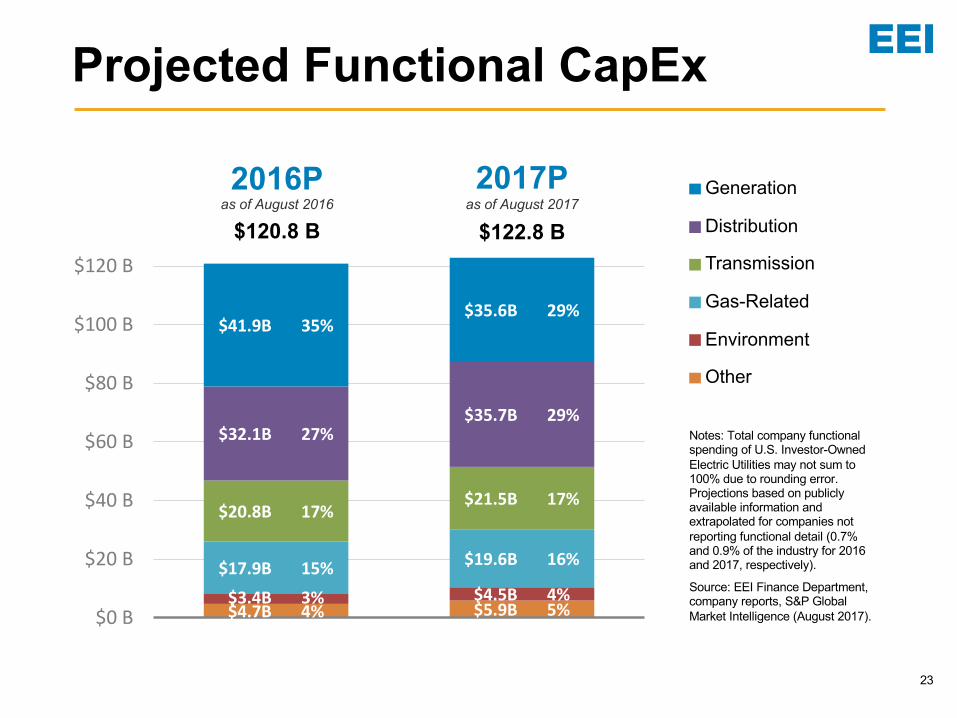

$4.7B 4% $5.9B 5%$3.4B 3% $4.5B 4%$17.9B 15% $19.6B 16%

$20.8B 17% $21.5B 17%

$32.1B 27%$35.7B 29%

$41.9B 35%$35.6B 29%

$0 B

$20 B

$40 B

$60 B

$80 B

$100 B

$120 B

Projected Functional CapEx

$120.8 Bas of August 2016 as of August 2017

$122.8 B

2016P 2017P Generation

Distribution

Transmission

Gas-Related

Environment

Other

Notes: Total company functional spending of U.S. Investor-Owned Electric Utilities may not sum to 100% due to rounding error. Projections based on publicly available information and extrapolated for companies not reporting functional detail (0.7% and 0.9% of the industry for 2016 and 2017, respectively).

Source: EEI Finance Department, company reports, S&P Global Market Intelligence (August 2017).

25

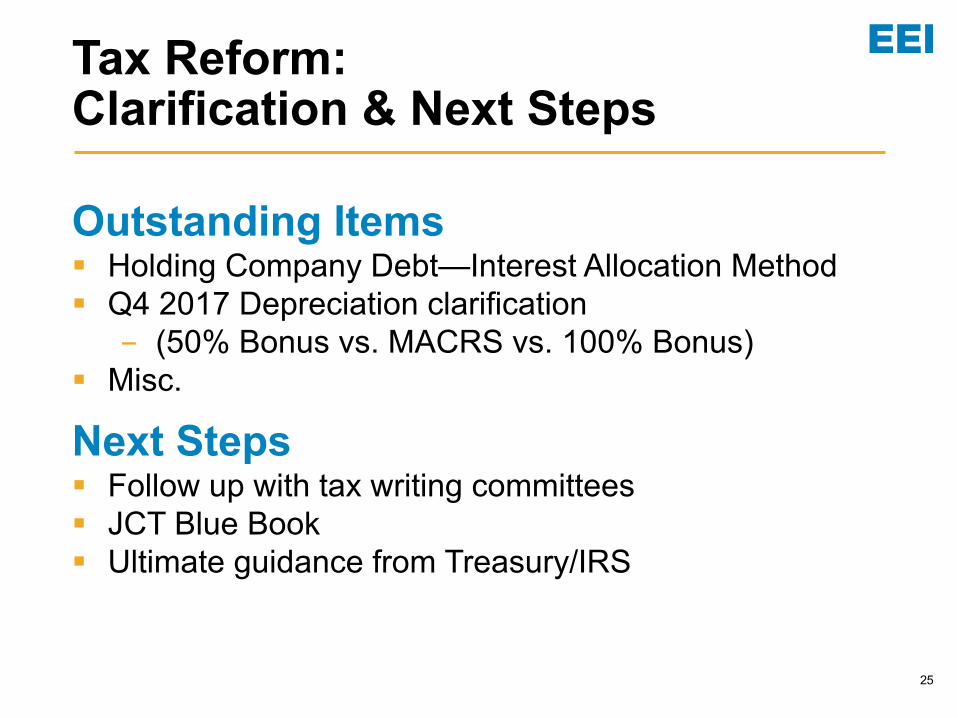

Outstanding Items§ Holding Company Debt—Interest Allocation Method§ Q4 2017 Depreciation clarification - (50% Bonus vs. MACRS vs. 100% Bonus)

§ Misc.

Next Steps§ Follow up with tax writing committees§ JCT Blue Book§ Ultimate guidance from Treasury/IRS

Tax Reform:Clarification & Next Steps

Source: https://www.cnn.com/2018/01/30/politics/2018-house-race-ratings/index.html. Accessed January 30, 2018.

Source: https://www.cnn.com/2018/01/30/politics/2018-senate-race-ratings/index.html. Accessed January 30, 2018.

Source: https://www.washingtonpost.com/news/the-fix/wp/2018/01/29/republican-governors-association-to-cut-all-ties-with-steve-wynn-amid-sexual-misconduct-allegations/?utm_term=.48a326966336. Accessed January 29, 2018.

32

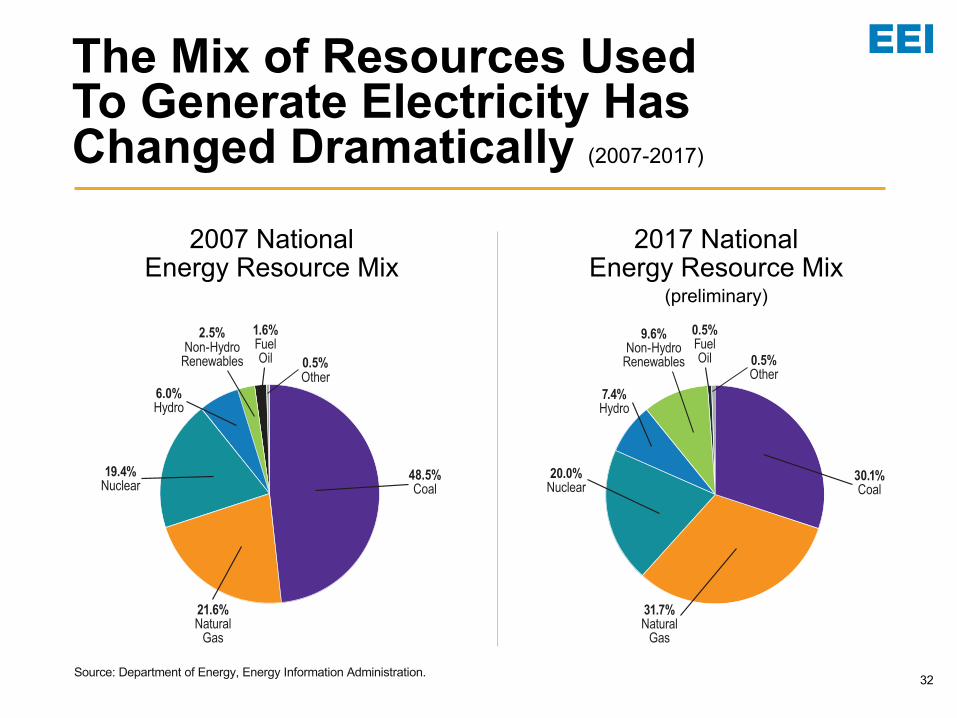

The Mix of Resources Used To Generate Electricity Has Changed Dramatically (2007-2017)

2007 National Energy Resource Mix

2017 National Energy Resource Mix

(preliminary)

21.6%Natural

Gas

19.4%Nuclear

2.5%Non-Hydro

Renewables

6.0%Hydro

48.5%Coal

0.5%Other

1.6%FuelOil

31.7%Natural

Gas

20.0%Nuclear

9.6%Non-Hydro

Renewables

7.4%Hydro

30.1%Coal

0.5%Other

0.5%FuelOil

Source: Department of Energy, Energy Information Administration.

33

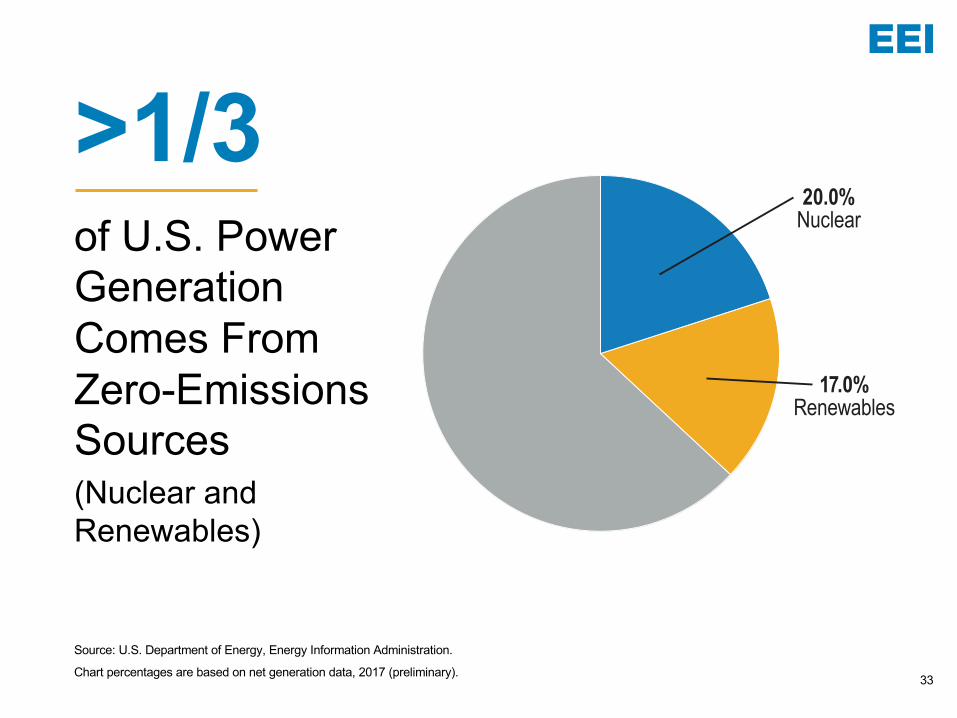

>1/3of U.S. Power Generation Comes From Zero-Emissions Sources (Nuclear and Renewables)

Source: U.S. Department of Energy, Energy Information Administration.

Chart percentages are based on net generation data, 2017 (preliminary).

17.0%Renewables

20.0%Nuclear

34

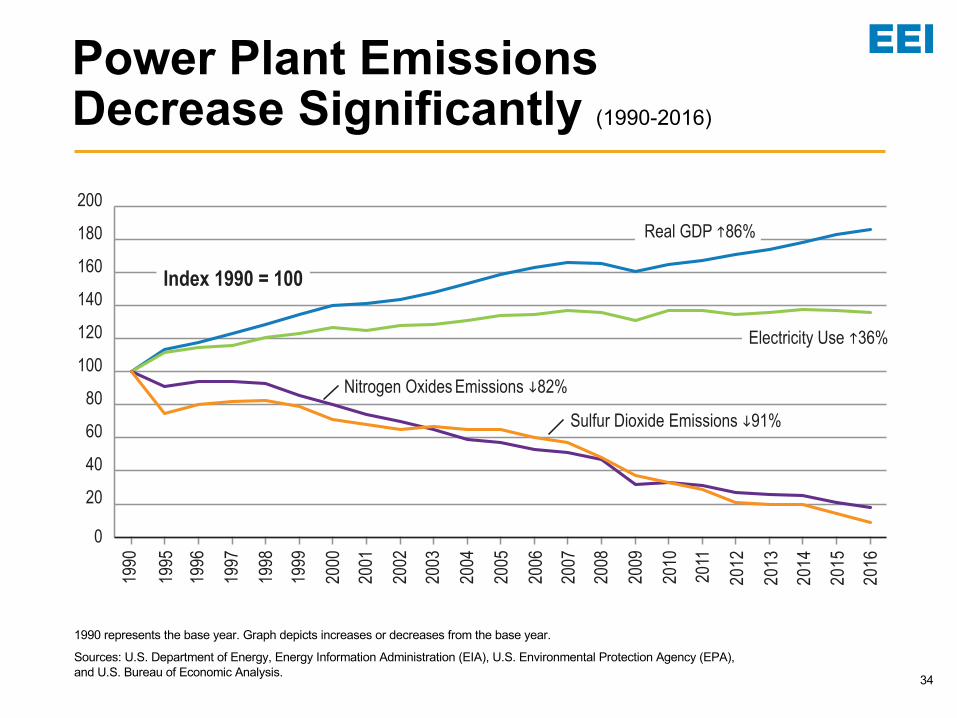

Power Plant Emissions Decrease Significantly (1990-2016)

0

20406080

100120140160180200

Index 1990 = 100

1995

1990

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Real GDP h86%

Electricity Use h36%

Nitrogen Oxides Emissions i82%

2011

2012

2013

2014

2016

Sulfur Dioxide Emissions i91%

1990 represents the base year. Graph depicts increases or decreases from the base year.

Sources: U.S. Department of Energy, Energy Information Administration (EIA), U.S. Environmental Protection Agency (EPA), and U.S. Bureau of Economic Analysis.

April 2017 © 2017 by the Edison Electric Institute. All rights reserved.

2015

1990 represents the base year. Graph depicts increases or decreases from the base year.

Sources: U.S. Department of Energy, Energy Information Administration (EIA), U.S. Environmental Protection Agency (EPA), and U.S. Bureau of Economic Analysis.

35

§ 1/3 of U.S. power generation comes from zero-emissions sources§ As of 2016, industry CO2 emissions were nearly 25 percent below 2005 levels§ Trajectory will continue based on current trends

U.S. Power Sector Carbon Dioxide Emissions Declining (2005-2016)

Source: Developed from U.S. Energy Information Administration, Monthly Energy Review, March 2017.

March 2017 © 2017 by the Edison Electric Institute. All rights reserved.

2005

2006

2007

2008

2009

2011

2012

2013

2015

2016

2014

2010

Million Metric Tons

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

Source: Developed from U.S. Energy Information Administration, Monthly Energy Review, March 2017.

36

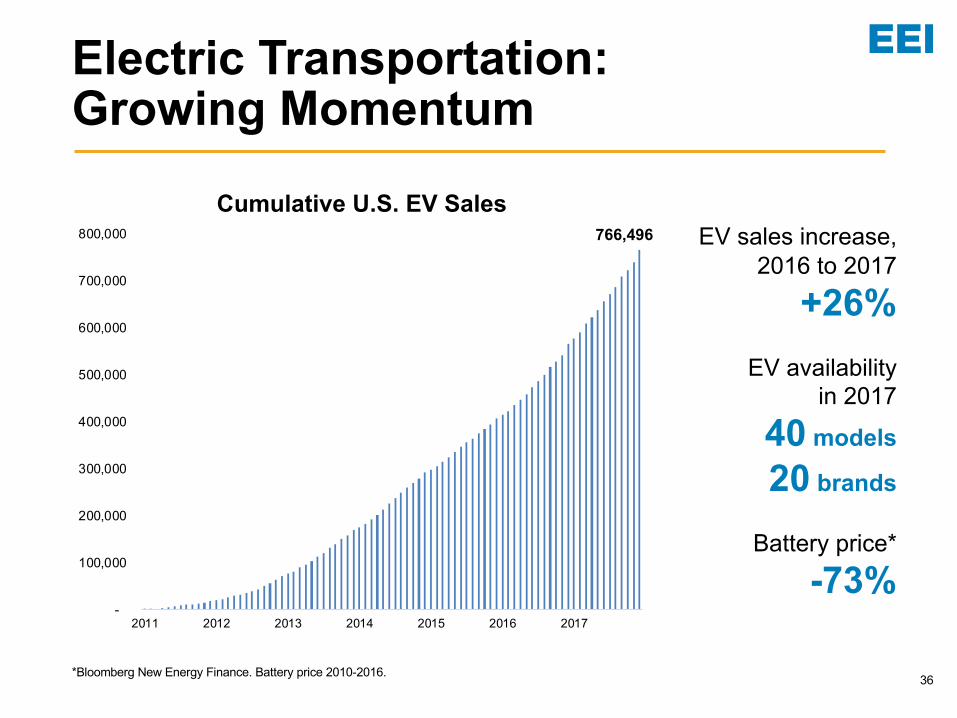

Electric Transportation:Growing Momentum

EV sales increase, 2016 to 2017

+26%EV availability

in 2017

40 models

20 brands

Battery price*

-73%

766,496

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2011 2012 2013 2014 2015 2016 2017

Cumulative U.S. EV Sales

*Bloomberg New Energy Finance. Battery price 2010-2016.

37

6.4%

93.6%

Male CEOs

Female CEOs

22.2%

77.8%

Male CEOs

Female CEOs

Gender Diversity at Regulated Electric Companies

Pat Vincent-Collawn (EEI Chairman)Chairman, President and CEOPNM Resources

Lynn Good (EEI Vice Chairman)Chairman, President and CEODuke Energy

Patricia KamplingChairman, President and CEOAlliant Energy Corporation

Patricia Poppe President and CEOCMS Energy

Mary KippPresident and CEOEl Paso Electric Company

Mary Powell President and CEOGreen Mountain Power

Connie LauPresident and CEOHawaiian Electric Industries

Linda Aspey President and CEOITC Holdings Corp

Geisha WilliamsPresident and CEOPG&E Corporation

Maria PopePresident and CEOPortland General Electric Company

Kimberly Harris President and CEOPuget Sound Energy

Debra ReedChairman, President and CEOSempra Energy

Regulated Electric Companies

Fortune 500 Companies

Female Leadership in the Electric Industry

38

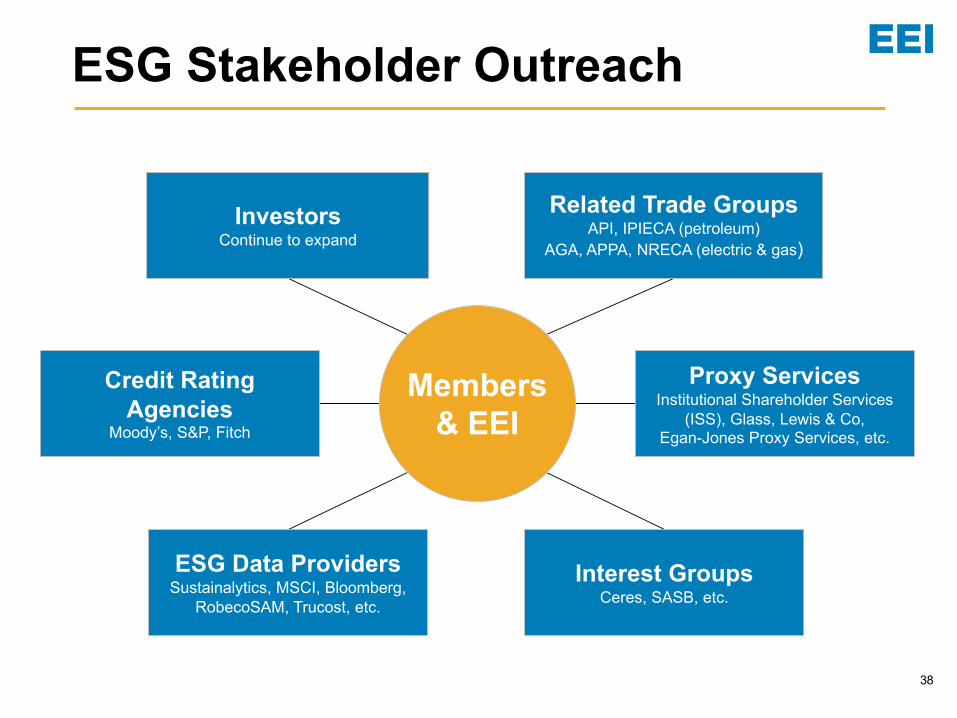

ESG Stakeholder Outreach

InvestorsContinue to expand

Related Trade GroupsAPI, IPIECA (petroleum)

AGA, APPA, NRECA (electric & gas)

Proxy ServicesInstitutional Shareholder Services

(ISS), Glass, Lewis & Co,

Egan-Jones Proxy Services, etc.

Credit Rating Agencies

Moody’s, S&P, Fitch

ESG Data ProvidersSustainalytics, MSCI, Bloomberg,

RobecoSAM, Trucost, etc.

Interest GroupsCeres, SASB, etc.

Members& EEI

39

US Electric IOUs Rating History

18%8%

2%

9%21%

10%

25%29%

18%

16%

23%

40%

13%

12%24%

19%8% 6%

2002 2009 2016

A or higher

A-

BBB+

BBB

BBB-

Below BBB-

Source: EEI Finance Department.

2002–2016

Average Industry Credit Rating is IncreasingBBB BBB+

40

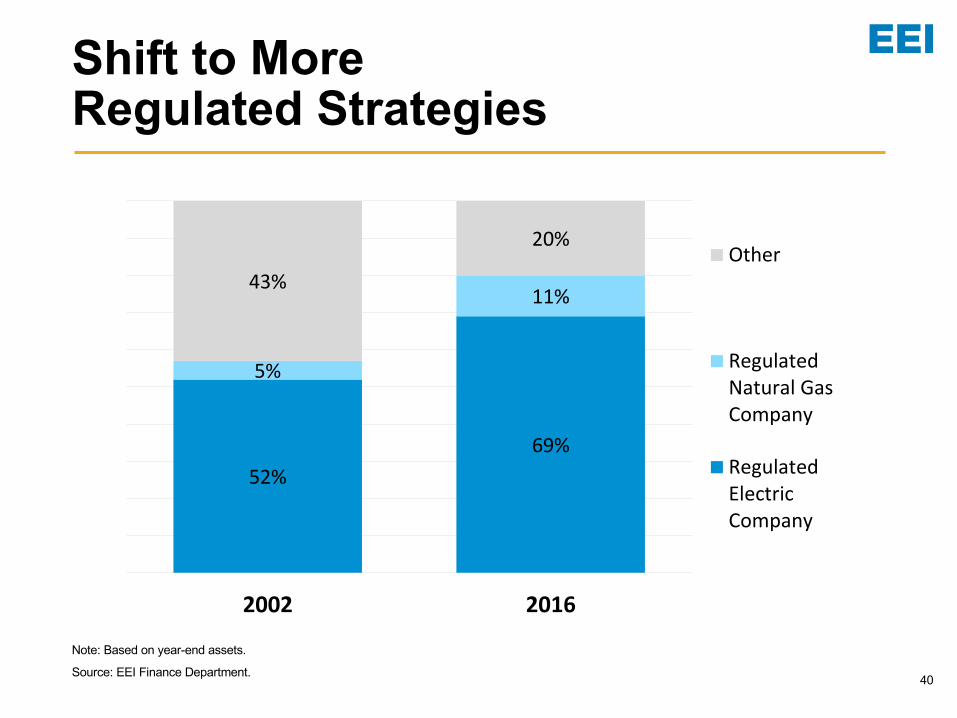

Shift to More Regulated Strategies

52%69%

5%

11%43%

20%

2002 2016

Other

RegulatedNatural GasCompany

RegulatedElectricCompany

Note: Based on year-end assets.

Source: EEI Finance Department.

41

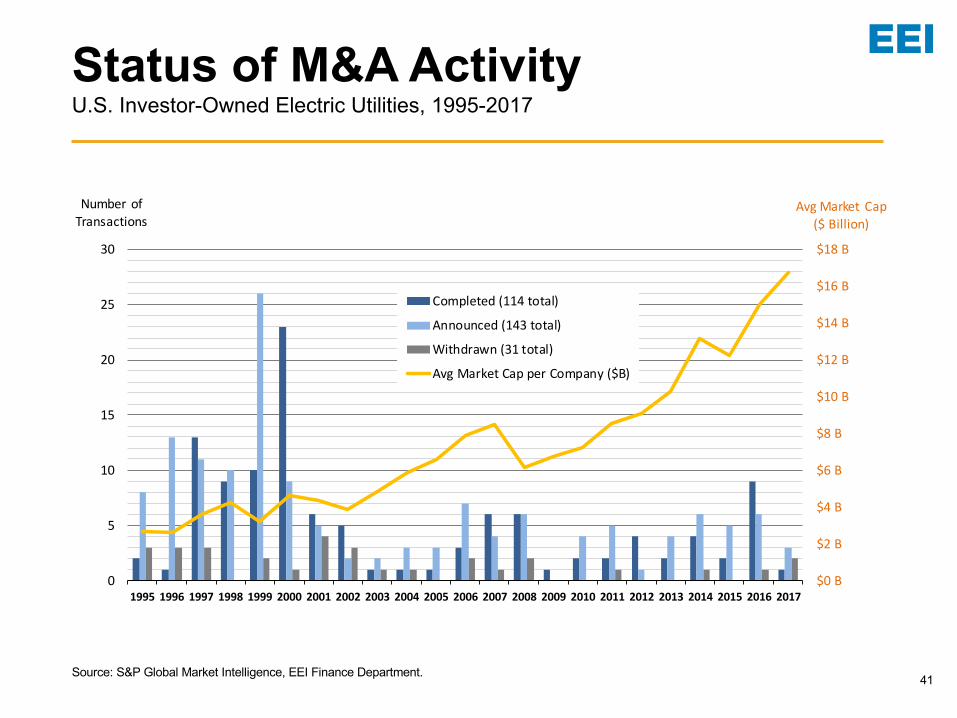

Status of M&A ActivityU.S. Investor-Owned Electric Utilities, 1995-2017

$0 B

$2 B

$4 B

$6 B

$8 B

$10 B

$12 B

$14 B

$16 B

$18 B

0

5

10

15

20

25

30

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Avg Market Cap($ Billion)

Number of Transactions

Completed (114 total)

Announced (143 total)

Withdrawn (31 total)

Avg Market Cap per Company ($B)

Source: S&P Global Market Intelligence, EEI Finance Department.

42

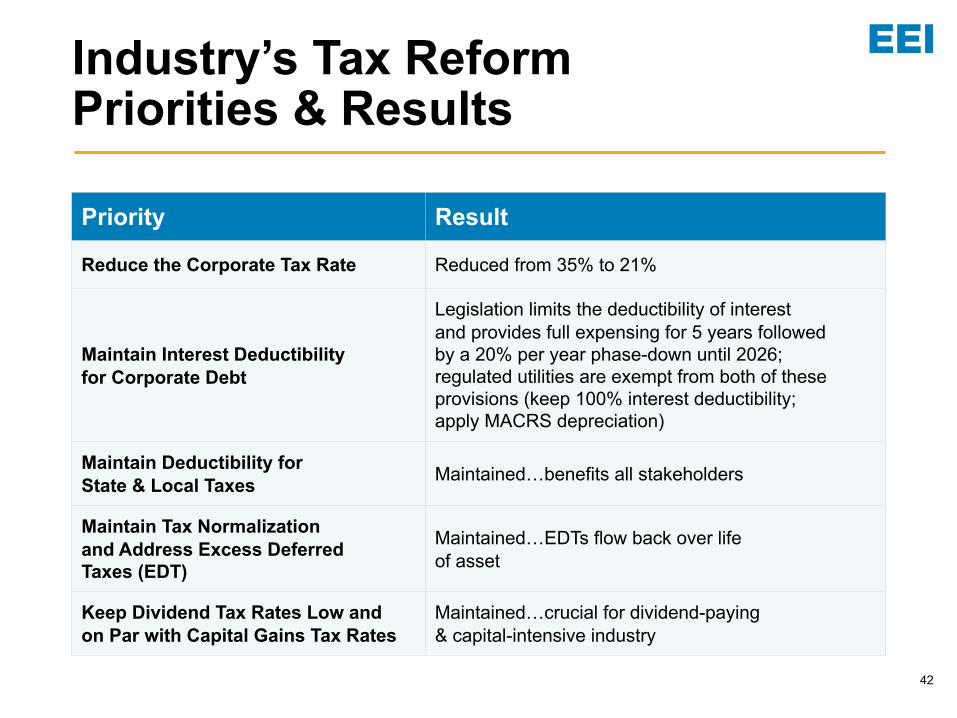

Industry’s Tax Reform Priorities & Results

Priority Result

Reduce the Corporate Tax Rate Reduced from 35% to 21%

Maintain Interest Deductibility for Corporate Debt

Legislation limits the deductibility of interest and provides full expensing for 5 years followed by a 20% per year phase-down until 2026; regulated utilities are exempt from both of these provisions (keep 100% interest deductibility; apply MACRS depreciation)

Maintain Deductibility for State & Local Taxes

Maintained…benefits all stakeholders

Maintain Tax Normalization and Address Excess Deferred Taxes (EDT)

Maintained…EDTs flow back over life of asset

Keep Dividend Tax Rates Low and on Par with Capital Gains Tax Rates

Maintained…crucial for dividend-paying & capital-intensive industry

43

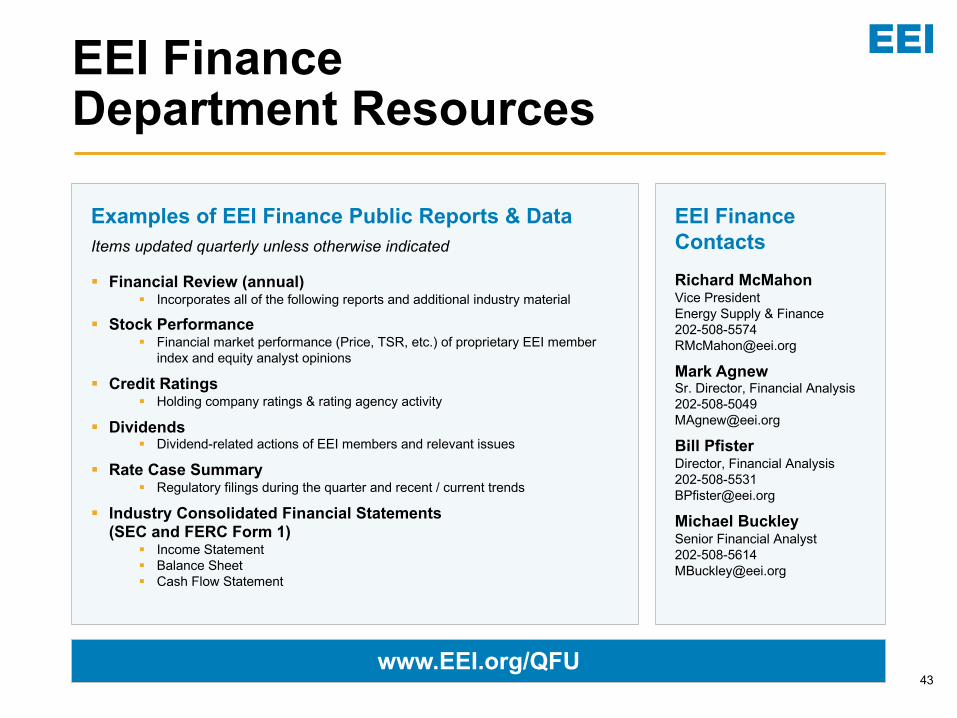

EEI Finance Contacts

Richard McMahonVice PresidentEnergy Supply & Finance [email protected]

Mark AgnewSr. Director, Financial [email protected]

Bill PfisterDirector, Financial [email protected]

Michael BuckleySenior Financial [email protected]

www.EEI.org/QFU

EEI Finance Department Resources

Examples of EEI Finance Public Reports & DataItems updated quarterly unless otherwise indicated

§ Financial Review (annual)§ Incorporates all of the following reports and additional industry material

§ Stock Performance§ Financial market performance (Price, TSR, etc.) of proprietary EEI member

index and equity analyst opinions

§ Credit Ratings§ Holding company ratings & rating agency activity

§ Dividends§ Dividend-related actions of EEI members and relevant issues

§ Rate Case Summary§ Regulatory filings during the quarter and recent / current trends

§ Industry Consolidated Financial Statements (SEC and FERC Form 1)

§ Income Statement§ Balance Sheet§ Cash Flow Statement