Embed Size (px)

Citation preview

26 OCT 2011 1

Japan Energy Association Symposium

Challenges to Efficient and Clean Use of Coal in Asian Region

1.Current Status and Future Prospects of

Coal Use in Indonesia

2.Brief Report on Understanding CCS

Potential in Indonesia

Djoko Prasetijo

PT PLN (Persero), Indonesia

WEC Member Committee, Indonesia

Tokyo Keidanren Kaikan

26 October 2011

1

26 OCT 2011 2

Contents:

• Electricity demand forecast

• Large renewable energy: geothermal and hydro power potentials

• Coal: resource, reserve, current use,

• Power development plan to 2020

• Projection of fuel mix for electricity generation to 2020

• Cleaner use of coal

• New framework for international cooperation related with CO2

emission reduction

• Brief report on CCS study in Indonesia

26 OCT 2011 3

Projection of Electricity Demand 2011-2020

Ave growth of electricity demand

8,46% per year

IB : 10,2%

24

TWh

55 TWh

IT :

10,8%

13 TWh

31 TWh

JB : 7,9%

125

TWh241

TWh

2011 2020

26 OCT 2011 4

3,438

2,678

2,745

7,027

56

400

8,420

150

60

290

285

3

695

3,127

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

HEPP

Diesel PP

GTPP

CCPP

Micro HEPP

Geothermal

Coal STPP

IPP (MW) PLN (MW)

Existing Total Capacity 29,400 MW

Existing Generation Capacity (type and ownership)

26 OCT 2011 5

Exploitable Geothermal Potential by WestJEC 2007

Source: Master Plan Study for Geothermal Power Development in the Republic of Indonesia, WestJEC, August 2007

26 OCT 2011 6

Cumulative Geothermal Capacity by the Master Plan

2,000

3,442

4,600

6,000

9,500

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Year

Po

wer

Ou

tpu

t C

ap

acit

y (

MW

)

Rank-N

Rank-L

Rank-C

Rank-B

Rank-A excluding Existing Plan

Existing Plan

Installed

Milestone of the Road Map

Ref: MEMR and JICA, Master Plan Study for Geothermal Power Development in the Republic of Indonesia, 2007

26 OCT 2011 7

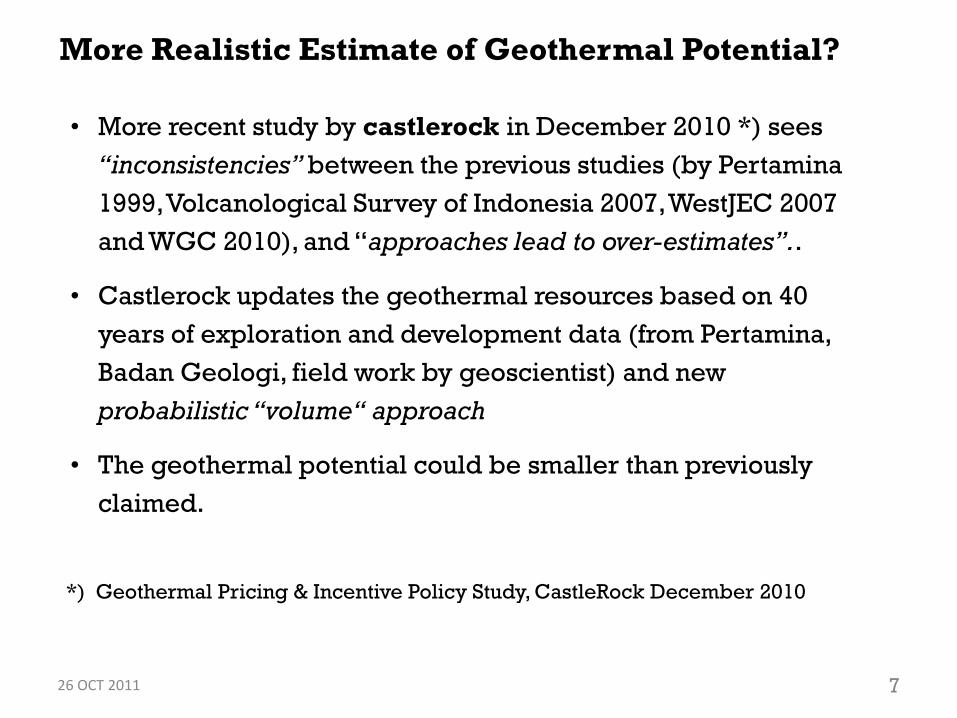

• More recent study by castlerock in December 2010 *) sees

“inconsistencies” between the previous studies (by Pertamina

1999, Volcanological Survey of Indonesia 2007, WestJEC 2007

and WGC 2010), and “approaches lead to over-estimates”..

• Castlerock updates the geothermal resources based on 40

years of exploration and development data (from Pertamina,

Badan Geologi, field work by geoscientist) and new

probabilistic “volume“ approach

• The geothermal potential could be smaller than previously

claimed.

More Realistic Estimate of Geothermal Potential?

*) Geothermal Pricing & Incentive Policy Study, CastleRock December 2010

26 OCT 2011 88

ACEH:

5.000 MW

North Sum:

3.800 MW

South Sum, Jambi,

Bengkulu

& Lampung:

3.100 MW

West Java:

2.860 MW

Central Java

810 MW

West Sum & RIAU:

3.600 MW

East Java

525 MWBali + NTT/NTB

625 MW

West Kal:

4.737 MW

Central+South+East

Kalimantan:

17000 MWNorth Sul +

Gorontalo:

4000 MW

South+South East

Sulawesi:

6.300 MW

Maluku

430 MW

Papua:

22.000 MW

Map of Hydro Power Potential : 75 GW(Ref: Hydro Power Potential Study 1983, Hydro Power Inventory Study 1999)

26 OCT 2011 9

Hydro Power Potential Revisited

• The hydro power potential was reported to be 75 GW In

[1], [2], but after undergoing rigorous environmental and

social screenings in 2010, it is estimated only 26.3 GW [3].

• The 26.3 GW consist existing capacity (of 4.4 GW),

planning & on-going (6 GW), new potential (16 GW).

• The new potentials are classified according to the level of

difficulty in terms of forest type, resettlement, reservoir

area.

• Under realistic scenario, almost 8 GW is available having

almost 33 TWh of energy

Existing studies:

[1] Hydro Power Potential Study HPPS, 1983

[2] Hydro Inventory (HPPS 2) 1999

[3] Master Plan Study of Hydro Power Development in Indonesia, Nippon KOEI, May 2011

26 OCT 2011 10

Hydro Electric Power Plant Development Strategy

PLN to develop very large pump storage plants to meet peaking

demand in Java – Bali and Sumatera power systems : Upper

Cisokan 1000 MW (start construction soon), and Grindulu 1000

MW + Matenggeng 900 MW (study);

Run-off river HEPP (with daily pondage ) recommended due to

environmental consideration.

PLN to develop HEPP with reservoir as peaking generators if

socially & environmentally possible.

Encourage domestic IPP to develop small & medium scale

hydropower ( <10 MW ) making use of feed-in tariff (currently

approx 180 MW have been contracted, and many under

construction).

Hydropower development as a multi purpose project.

26 OCT 2011 11

Indonesia Coal Resources and Reserves

Source: Badan Geologi (Geological Agency), Ministry of Energy and Mineral

Resources, 2009

26 OCT 2011 12

Distribution of Coal Resources

Source: Badan Geologi (Geological Agency), Ministry of Energy and Mineral

Resources, 2009

26 OCT 2011 13

Current Use of Coal for Electricity Generation in 2011

by Rank

Million tons

0

5

10

15

20

25

30

35

2011

Low Rank Medium High

low

medium

Low: < 5100, Medium: 5100-6100, High: >6100 kcal/kg

high

26 OCT 2011 14

Use of Coal in Coal-fired Power Plants to 2020

• Java – Bali interconnected power system

The smallest unit size are 300 MW class, most units now running are of 400

and 600 MW class. A larger plant of 815 MW capacity will soon be on line.

There will be 1000 MW class from 2016 onwards.

• Sumatera interconnected power system

Various classes from 50 MW of existing plants to 200 MW class under

construction. Mine mouth CFPP of 300 MW, 400 MW and 600 MW class are

being planned. Those 600 MW mine mouth CFPP are associated with HVDC

transmission project connecting Sumatera and Java.

• Kalimantan, Sulawesi

Most CFPP are under construction, most have unit size of 50 MW and 100

MW.

• Small-scale CFPP (<25 MW)

Many have been planned and under construction in smaller and isolated

power systems when renewable energy are not available locally.

26 OCT 2011 15

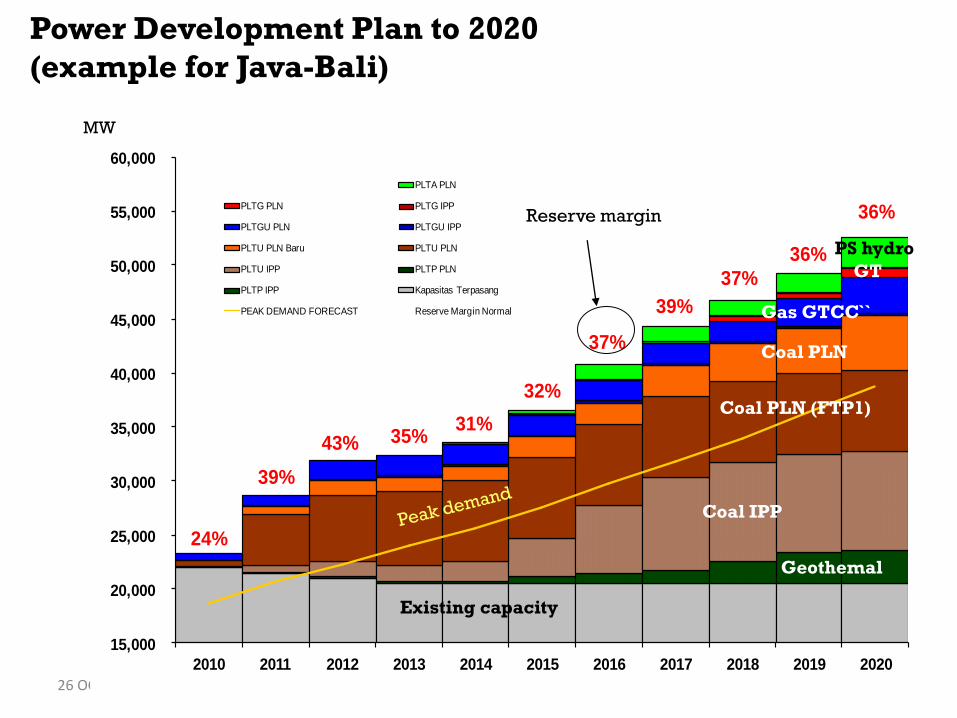

Power Development Plan to 2020

(example for Java-Bali)

24%

39%

43% 35%31%

32%

37%

39%

37%

36%

36%

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

PLTA PLN

PLTG PLN PLTG IPP

PLTGU PLN PLTGU IPP

PLTU PLN Baru PLTU PLN

PLTU IPP PLTP PLN

PLTP IPP Kapasitas Terpasang

PEAK DEMAND FORECAST Reserve Margin Normal

Coal IPP

Geothemal

Existing capacity

PS hydro

GT

Coal PLN (FTP1)

Coal PLN

Gas GTCC``

MW

Reserve margin

26 OCT 2011 16

Fuel Mix of Jawa-Bali 2011-2020 [GWh]

Geothermal

HSD MFO

-

50,000

100,000

150,000

200,000

250,000

300,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Air Panas Bumi Batubara Gas LNG MFO (Oil) HSD (Oil)

coal

gas

geothermal

hydro

HSD

LNG

26 OCT 2011 17

Fuel Mix of Western Indonesia 2011-2020 [GWh]

HSD MFO

coal

gas

geothermal

HSD

MFO

-

10.000

20.000

30.000

40.000

50.000

60.000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Pro

du

ks

i en

erg

i (G

Wh

)

Hydro Geot. Batubara Gas LNG HSD MFO

LNG

coal

gas

geothermal

hydro

HSD

MFO

26 OCT 2011 18

Fuel Mix of Eastern Indonesia 2011-2020 [GWh]

Geothermal

Hydro

LNG

HSD MFO

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Pro

du

ksi

en

erg

i (G

Wh

)

Hydro Geot. Batubara Gas LNG HSD MFO Surya/Hybrid

coal

gas

geothermal

hydro

HSD

MFO

26 OCT 2011 19

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

GW

h

Impor Biomass Surya/Hybrid HSD MFO LNG Gas Batubara Geothermal Hydro

Hydro

HSD

Gas

LNG

coal

geothermal

Hydro

oil

Projection of Fuel Mix to 2020 (national)

26 OCT 2011 20

Coal Consumption for Electricity Generation to 2020

million tons

0

20

40

60

80

100

120

140

2006 2008 2010 2012 2014 2016 2018 2020

Historical Projection 126

42

30

26 OCT 2011 21

Projection of Coal Use for Electricity Generation

by Rank

Million Tons

0

20

40

60

80

100

120

140

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Low Rank Medium High

Low rank

126

42

26 OCT 2011 22

CO2 emission from electricity sector

0

50

100

150

200

250

300

2011 2013 2015 2017 2019

Total Emission Emission from Coal

Million Tons CO2

• Emission will increase

from 125 million tons in

2011 to 275 million tons

in 2020

• Most emission will come

from coal combustion

(almost 90%)

• For Java Bali: Grid

emission factor will

reduce from 0.78 kg

CO2/kWh in 2011 to

0.75 kg/kWh in 2020.

26 OCT 2011 23

Cleaner Use of Low Rank Coal

• Indonesia‟s power sector can be mistakenly regarded as more

concern about growth and use of indigenous coal than concern

about global climate challenge.

• However, Indonesia would actually do better than just „grow first –

cleanup later’ , it is seen from the fact that Indonesia have plan to

develop large scale geothermal and small-medium-large scale

hydro power, as well as clean coal technology.

• PLN in its 10-year power development plan to 2020 set a policy

that only SC/USC coal plants will be developed in Java for better

efficiency and lower CO2 emissions.

• Gov of Indonesia (MEMR) and gov of Japan (JICA) are carrying

out a project study “Promotion of Clean Coal Technology (CCT)

inn Indonesia” from April 2011 to be completed by May 2012. The

CCT study team consists of Chubu Electric, JPower and Jcoal, with

MEMR and PLN as counterpart team.

26 OCT 2011 24

Roadmap of CCT in Indonesia *)

• After assessing relevant factors (technical availability, low rank

coal availability, economic viability, technical challenges in

introducing CCT and contribution to GHG emission reduction),

the CCT study concludes that the CCT technology that can be

adopted by Indonesia are USC and IGCC.

• USC is commercially matured, already proven and well

performed in many countries, can use low rank coal having

above average ash melting point, has economic merit to SubC

and SC, produces lower CO2 emissions.

• IGCC is a promising technology, yet not commercially matured,

can use low rank coal with low ash melting point, its project cost

is expected to drop and make it economical compared to SC and

USC, lower CO2 emission than SC and USC.

*) Source: The Project for Promotion of Clean Coal Technology (CCT) in Indonesia, Interim

Report, October 2011, Jakarta, JICA Study Team.

26 OCT 2011 25

Roadmap of CCT in Indonesia *)

*) Source: The Project for Promotion of Clean Coal Technology (CCT) in Indonesia, Interim

Report, October 2011, Jakarta, JICA Study Team, with modification

2011 2015 2020 2025

SC, = 30-40%

USC, 43%

IGCC

45-48%

IPP

(USC 2x1000 MW)

Indramayu #1

(USC 1000 MW)

Indramayu #2

(USC 1000 MW)

Bekasi

(USC 2x600 MW)

2000–3000 MW

per year

IGCC 1000 MW Class

26 OCT 2011 26

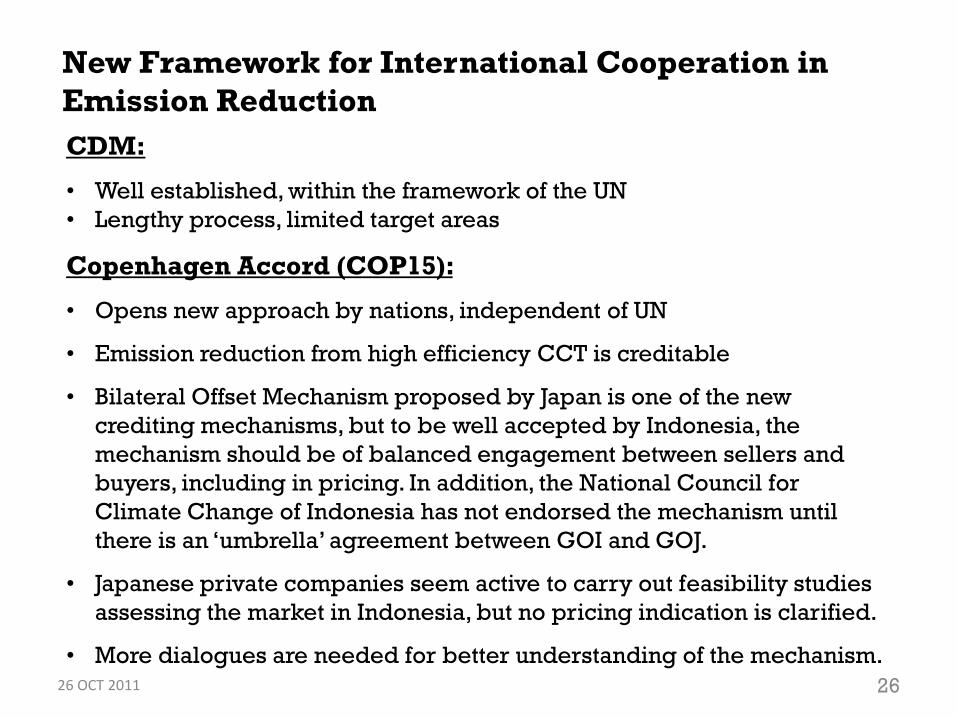

New Framework for International Cooperation in

Emission Reduction

CDM:

• Well established, within the framework of the UN

• Lengthy process, limited target areas

Copenhagen Accord (COP15):

• Opens new approach by nations, independent of UN

• Emission reduction from high efficiency CCT is creditable

• Bilateral Offset Mechanism proposed by Japan is one of the new

crediting mechanisms, but to be well accepted by Indonesia, the

mechanism should be of balanced engagement between sellers and

buyers, including in pricing. In addition, the National Council for

Climate Change of Indonesia has not endorsed the mechanism until

there is an „umbrella‟ agreement between GOI and GOJ.

• Japanese private companies seem active to carry out feasibility studies

assessing the market in Indonesia, but no pricing indication is clarified.

• More dialogues are needed for better understanding of the mechanism.

26 OCT 2011 27

Hydro

Reduction of CO2 Emissions (National)

The objective is to increase the role of low carbon technology (and zero

carbon technology) into long term energy path in order to have

sustainable energy development as instrument of mitigation action, not

just in meting supply and demand..

Domestic effort

HSD

Gas

LNG

coal

geothermal

Hydro

oil

BAU 26%

41% With international support

Off-set

CO2 emission

2020

26 OCT 2011 28

Hydro

Conclusions

• PLN welcomes all kinds of RE, but the RE that can contribute significantly to

the fuel mix for electricity generation are geothermal and hydro power;

• PLN would like to see those large scale geothermal and hydro power

developed a.s.a.p, however, their development apparently would need

longer lead time;

• Having sizable coal resources, it is natural if Indonesia plan to use more

coal in the fuel mix of electricity generation.

• The type of coal that would used more in electricity generation Indonesia

is low rank coal, due to plentiful availability in Kalimantan and Sumatera

and more economical, thus securing more stable supply, whilst most high

rank coal would be exported to global market.

• Yet Indonesia is committed to adopt cleaner coal technology. PLN plans

only USC CFPP in Java, and adopting IGCC as soon as it is commercially

matured, hopefully not in too distant future.

• Some Indonesians are not very familiar with Bilateral Offset Mechanism as

a crediting scheme, more dialogues are needed.

26 OCT 2011 29

1. Introduction.

2. CO2 Emission Sources in Indonesia: (i) Oil and Gas Industry, and (ii)

Power Sector.

3. Capture Technology.

4. Transportation Technology.

5. Methodology for Sites Selection: (i) Non-EOR, and (ii) NOR.

6. Geological Potential Storage .

7. CCS Regulatory Framework and Enabling Policies.

8. Conclusions and Recommendations.

Understanding CCS Potential in Indonesia

British Embassy

Jakarta

KOMITE NASIONAL

INDONESIA

PT PLN (PERSERO)

http://www.worldenergy.org/work_programme/technical_programme/technical_c

ommittees/cleaner_fossil_fuel_systems/default.asp

26 OCT 2011 30

A study into the potential for Indonesia to implement CCS has been

undertaken by the CCS Study Working Group. The Working Group comprises

the Agency for Oil and Gas Research Development (LEMIGAS) of the Ministry

of Energy and Mineral Resources of Indonesia, Indonesian National

Committee – World Energy Council (KNI-WEC), PT PLN (Persero) – Indonesia

State Electricity Corporation, Ministry of Enviroment of Indonesia, Royal Dutch

Shell and UK Embassy.

The purpose of this study is to develop an understanding of the requirements

associated with deploying Carbon Capture and Geological Storage in

Indonesia by addressing technical, commercial and regulatory aspects of

CCS deployment to further stimulate the on-going dialogue on potential

application of such technology in Indonesia.

This assessment of carbon capture and storage feasibility in Indonesia

focuses on a number of factors. These factors include both technical aspects

(e.g. geological storage potential, CO2 capture from industrial sources) and

non-technical issues (e.g. regulatory framework on CCS implementation,

business opportunity).

The Purpose of the Study

26 OCT 2011 31

The Main Part of the Study - CO2 Emission Sources

4 Power Plants & 1 Gas Processing Plant

CCS Capture Options

GUU

U

Plant

2

(2008-2018): 6.2 x 1062

GUU

GUU

U

Plant

2

- : 6.2 x 10 2

Bangko

Tengah

Coal power

plant

Muara Jawa

Coal power

plant

Subang

Gas

processing

plant

Indramayu

Coal power

plant

Muara Tawar

2,3,4

Natural gas

power plant

26 OCT 2011 32

Long oil exploration and

production history has left a

legacy of depleted oil and

gas fields, providing:

• geological stability

• well- characterised

reservoirs

• low population density

• existing infrastructures

• reduction of exploration

cost

Geological Potential Storage

26 OCT 2011 33

CO2

Sources

Geological Potential

Storage Location

Pipeline

Distance

(Km)

Estimated Avoided

Cost (US$/tCO2)

Indramayu

1000 MW

Steam Coal Power Plant

South Sumatra region

(onshore)655

62.1

(versus 1000 MW

plant without

capture)

Muara Tawar

750 MW

NGCC Power Plant

North Jawa sea

(offshore)15

71.4

(versus NGCC

without capture)

Bangko Tengah

600 MW

Steam Coal Power Plant

South Sumatra region

(onshore)60

56.2

(versus 600 MW plant

without capture)

Muara Jawa

100 MW

Steam Coal Power Plant

East Kalimantan

region

(onshore)

60

76.3

(versus 100 MW plant

without capture)

Subang Field

Natural Gas Processing Plant

North Jawa sea

(offshore)79.7

10.7

(cost of compressing)

CO2 Sources, Geological Potential Storage

Locations & Estimated Avoided Costs

26 OCT 2011 34

Cost of Various Components of a CCS System

CCS System Components Cost Range Remarks

Capture

From a coal or gas

fired power plant

15 – 75 US$/tCO2

net captured

Net costs of captured CO2 compared to the

same plant without capture

From hydrogen &

ammonia

production or gas

processing

5 – 55 US$/tCO2

net captured

Applies to high-purity sources requiring

simple drying and compression.

From other

industrial sources

25 – 115 US$/tCO2

net captured

Range reflects use of a number of different

technologies and fuels.

Transportation Via pipeline or ship1 – 8 US$/tCO2

transported

Per 250 km pipeline or shipping for mass

flow rates of 5 (high end) to 40 (low end)

MtCO2/yr.

Storage

Geological storage*0.5 – 8 US$/tCO2

net injected

Excluding potential revenues from EOR or

Enhanced Coal Bed Methane (ECBM).

Geological storage:

monitoring &

verification

0.1 – 0.3 US$/tCO2

injected

This covers pre-injection, injection, and post

injection monitoring, and depends on the

regulatory requirements.

Ocean storage5 – 30 US$/tCO2

net injected

Including offshore transportation of

100-500 km, excluding monitoring and

verification.

* Over the long-term, there may be additional costs for remediation and liabilities; Source: Carbon

Dioxide Capture and Storage, Summary for Policymakers and Technical Summary, IPCC, 2006.

26 OCT 2011 35

Indonesia has several promising options for CCS application considering

its variety of CO2 sources and availability of geological storage

International funding and support in collaborative approach will be

required to render at least fully integrated industrial-scale CCS

demonstration project in developing countries in providing financial

assistance together with the government with appropriate policies,

measures and/or instruments.

Concerns such as long-term liability and project boundaries, as well as

developing robust regulatory framework will need to be addressed

among others through proper demonstration projects

Assessment of potential sites and confirmation of the geological storage of

CO2

Assessment of reasonable routes to geological CO2 storage

An estimate of cost impacts of essential capture-ready measures, such as

modifications to plant design and changes in ongoing running costs*)

Environmental considerations, reviewing and highlighting any potential

impacts associated with capture-ready plants and retrofitting

Conclusions

26 OCT 2011 37

Coal price

US$/ton50 70 90 110 130 150

LCOE (US$/MWh)

USC 1000 ( = 40%)

SubC 600 ( = 36%)

DR=10% utk solid line

DR= 5% utk dashed line

USC 1000 + CCS ( = 28%)

26 OCT 2011 38

Optimization Results:

Configuration of Power Generation (by Technology)

0

20000

40000

60000

80000

100000

120000

140000

160000B

ase

lin

e

Sce

na

rio

1

Sce

na

rio

2

Sce

na

rio

3

Ba

se

lin

e

Sce

na

rio

1

Sce

na

rio

2

Sce

na

rio

3

Ba

se

lin

e

Sce

na

rio

1

Sce

na

rio

2

Sce

na

rio

3

Ba

se

lin

e

Sce

na

rio

1

Sce

na

rio

2

Sce

na

rio

3

PLTP PLTN PLTU PLTU USC PLTU+CCS PLTU AUSC IGCC

IGCC+CCS PLTGU GAS PLTGU LNG PLTG PLTD PLTA PS

2020

2011

2030

2040

US

CA

US

CS

ub

C

NP

P

LN

G

USC+CCS

MW

IGCC+CCS

$0 $25 $50 $75 $0 $25 $50 $75 $0 $25 $50 $75 $0 $25 $50 $75