Embed Size (px)

Citation preview

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 1/31

1

Help session to students with littleor no accounting or finance

background

´Income and Cash Flow Statementsµby Binam Ghimire

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 2/31

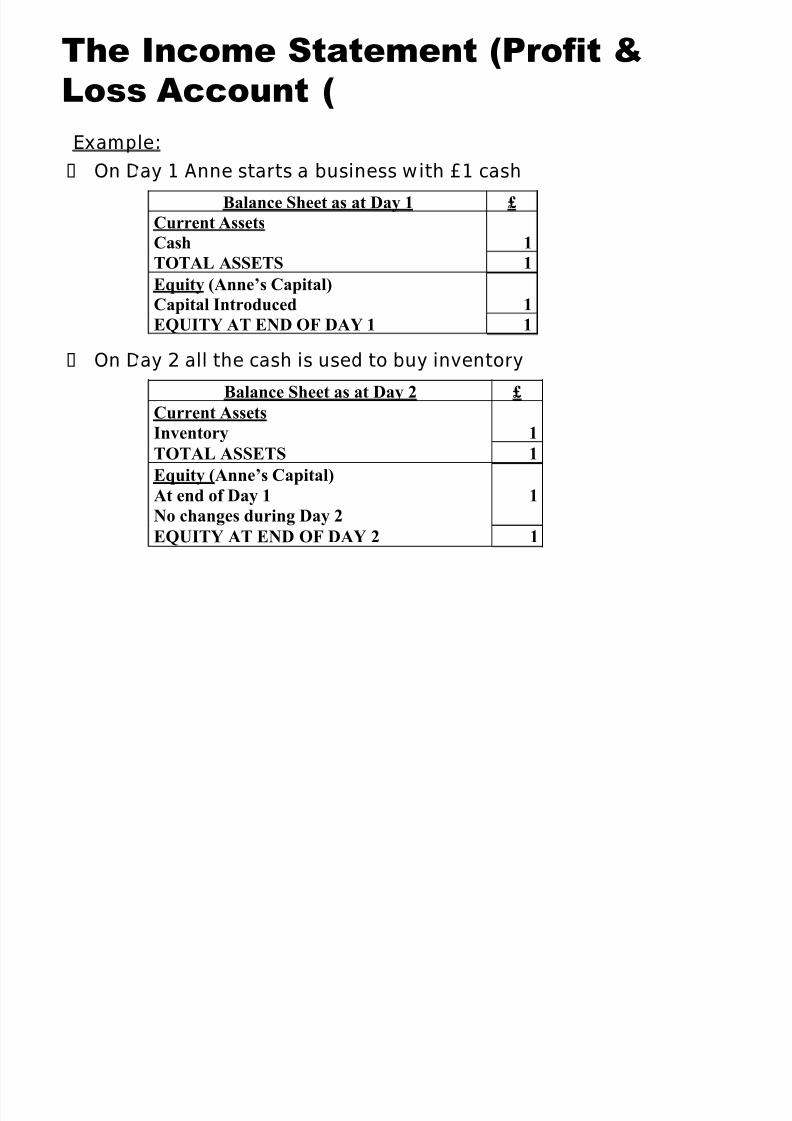

Example:

On Day 1 Anne starts a business with £1 cash

On Day 2 all the cash is used to buy inventory

Balance Sheet as at Day 1 £

Current Assets

Cash 1

TOTAL ASSETS 1

Equity (Anne¶s Capital)

Capital Introduced 1

EQUITY AT END OF DAY 1 1

Balance Sheet as at Day 2 £

Current AssetsInventory 1

TOTAL ASSETS 1

Equity (Anne¶s Capital)

At end of Day 1

No changes during Day 2

1

EQUITY AT END OF DAY 2 1

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 3/31

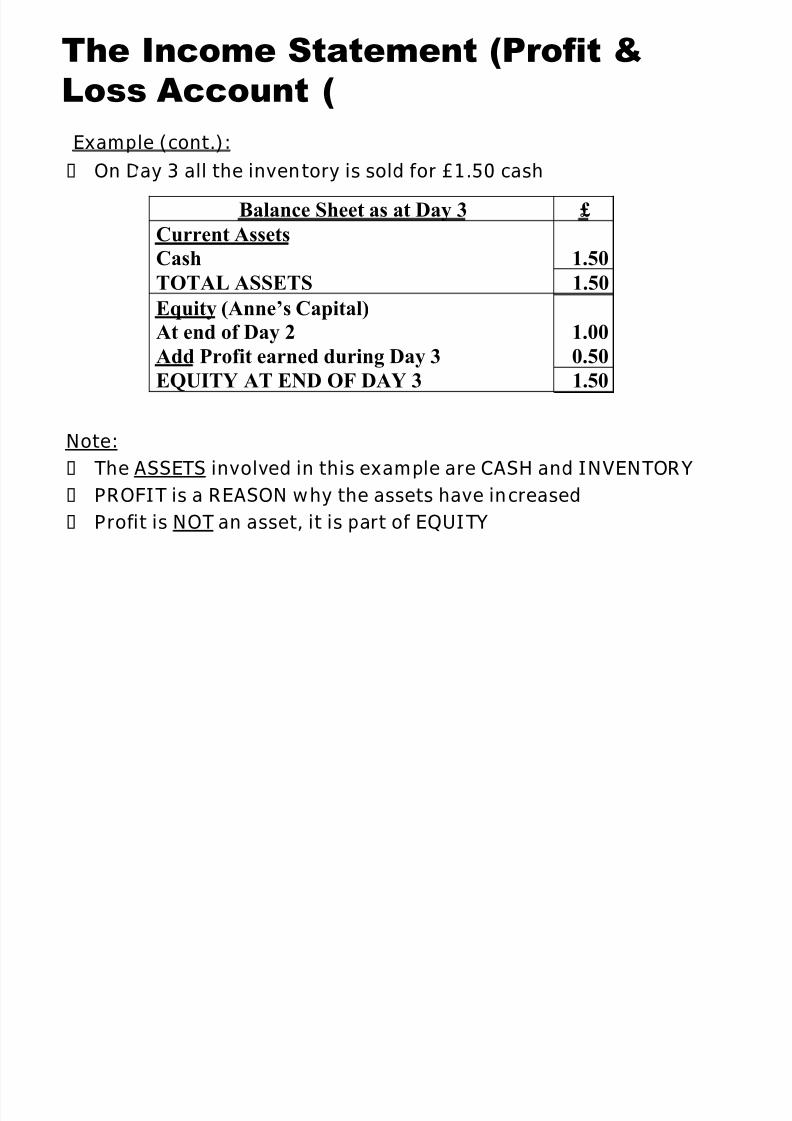

Example (cont.):

On Day 3 all the inventory is sold for £1.50 cash

Note:

The ASSETS involved in this example are CASH and INVENTORY

PROFIT is a REASON why the assets have increased

Profit is NOT an asset, it is part of EQUITY

The Income Statement (Profit &

Loss Account)

Balance Sheet as at Day 3 £

Current Assets

Cash 1.50

TOTAL ASSETS 1.50

Equity (Anne¶s Capital)

At end of Day 2

Add Profit earned during Day 3

1.00

0.50

EQUITY AT END OF DAY 3 1.50

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 4/31

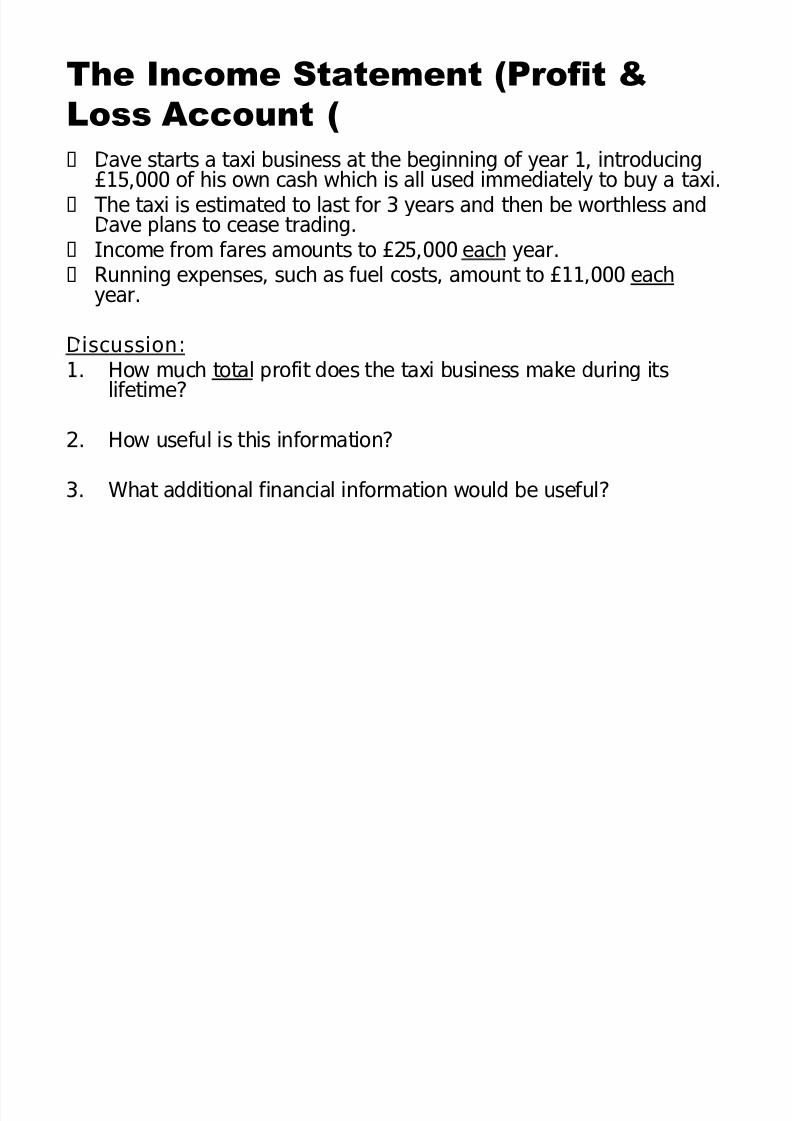

Dave starts a taxi business at the beginning of year 1, introducing£15,000 of his own cash which is all used immediately to buy a taxi.

The taxi is estimated to last for 3 years and then be worthless andDave plans to cease trading.

Income from fares amounts to £25,000 each year.

Running expenses, such as fuel costs, amount to £11,000 eachyear.

Discussion:1. How much total profit does the taxi business make during its

lifetime?

2. How useful is this information?

3. What additional financial information would be useful?

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 5/31

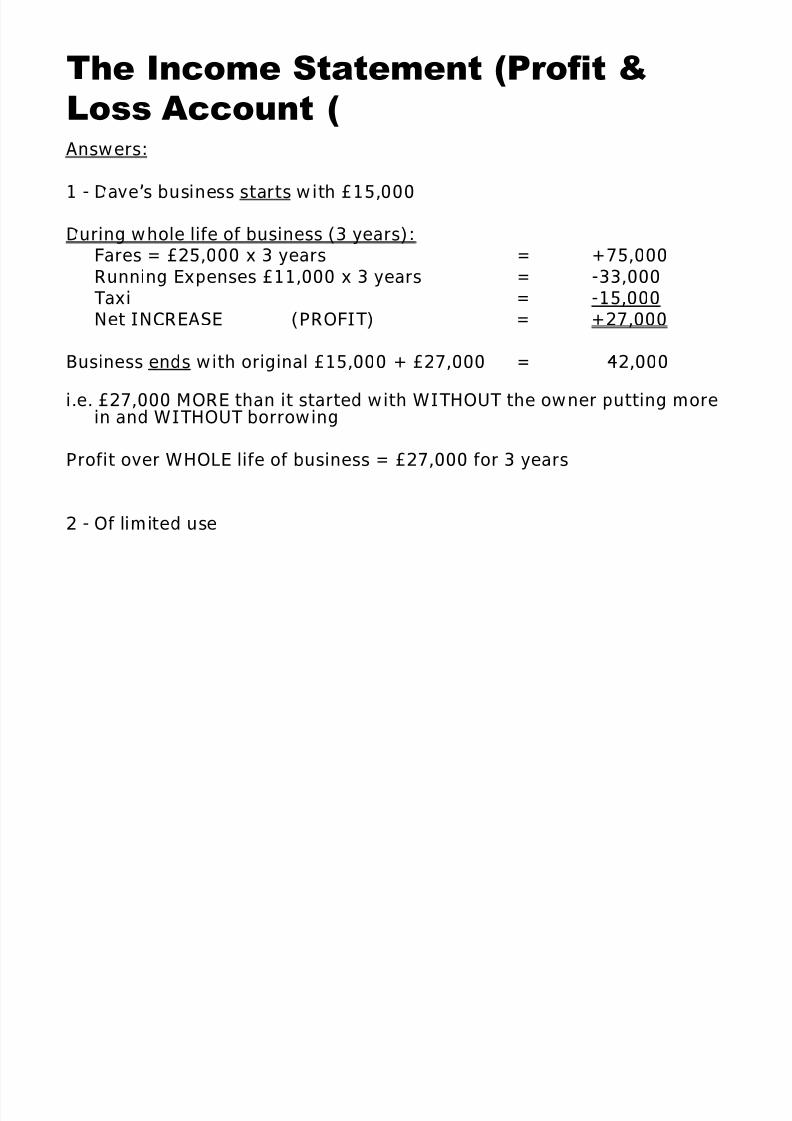

Answers:

1 - Daves business starts with £15,000

During whole life of business (3 years):Fares = £25,000 x 3 years = +75,000

Running Expenses £11,000 x 3 years = -33,000Taxi = -15,000Net INCREASE (PROFIT) = +27,000

Business ends with original £15,000 + £27,000 = 42,000

i.e. £27,000 MORE than it started with WITHOUT the owner putting more

in and WITHOUT borrowing

Profit over WHOLE life of business = £27,000 for 3 years

2 - Of limited use

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 6/31

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 7/31

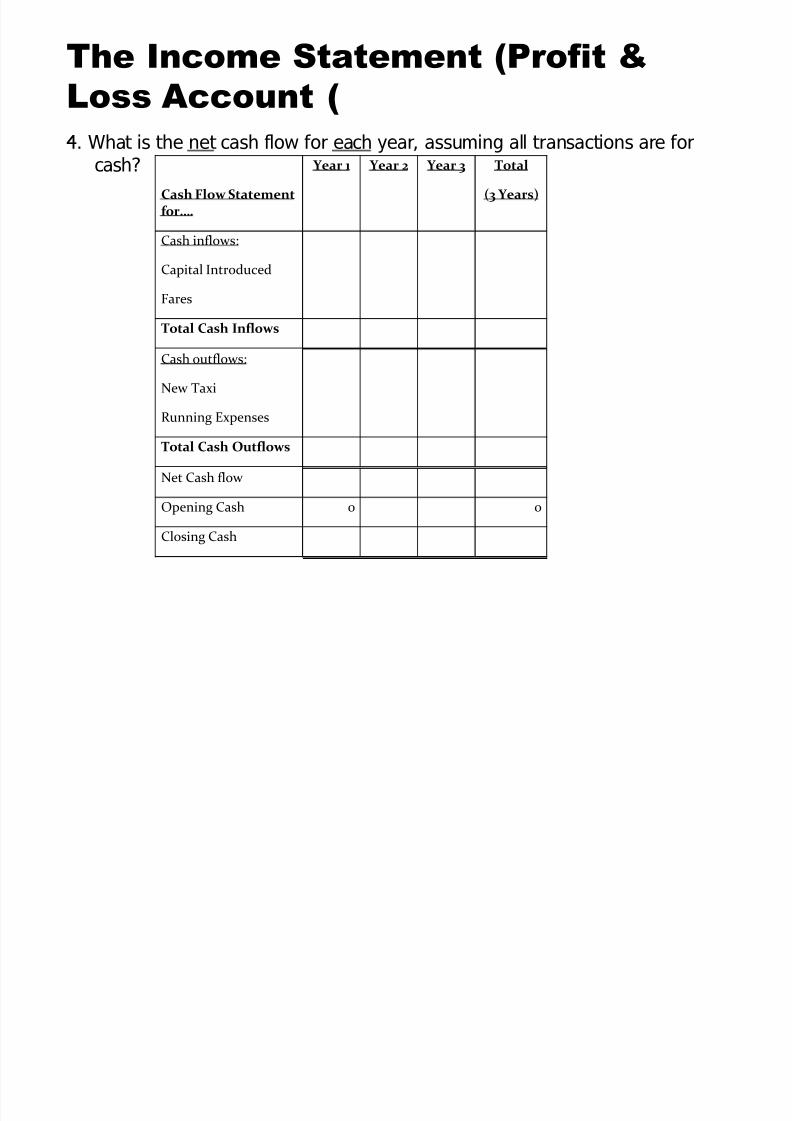

4. What is the net cash flow for each year, assuming all transactions are forcash?

The Income Statement (Profit &

Loss Account)

Cash Flow Statementfor.

Year 1 Year 2 Year 3 Total

(3 Years)

Cash inflows:

Capital IntroducedFares

Total Cash Inflows

Cash outflows:

New Taxi

Running Expenses

Total Cash Outflows

Net Cash flow

Opening Cash 0 0

Closing Cash

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 8/31

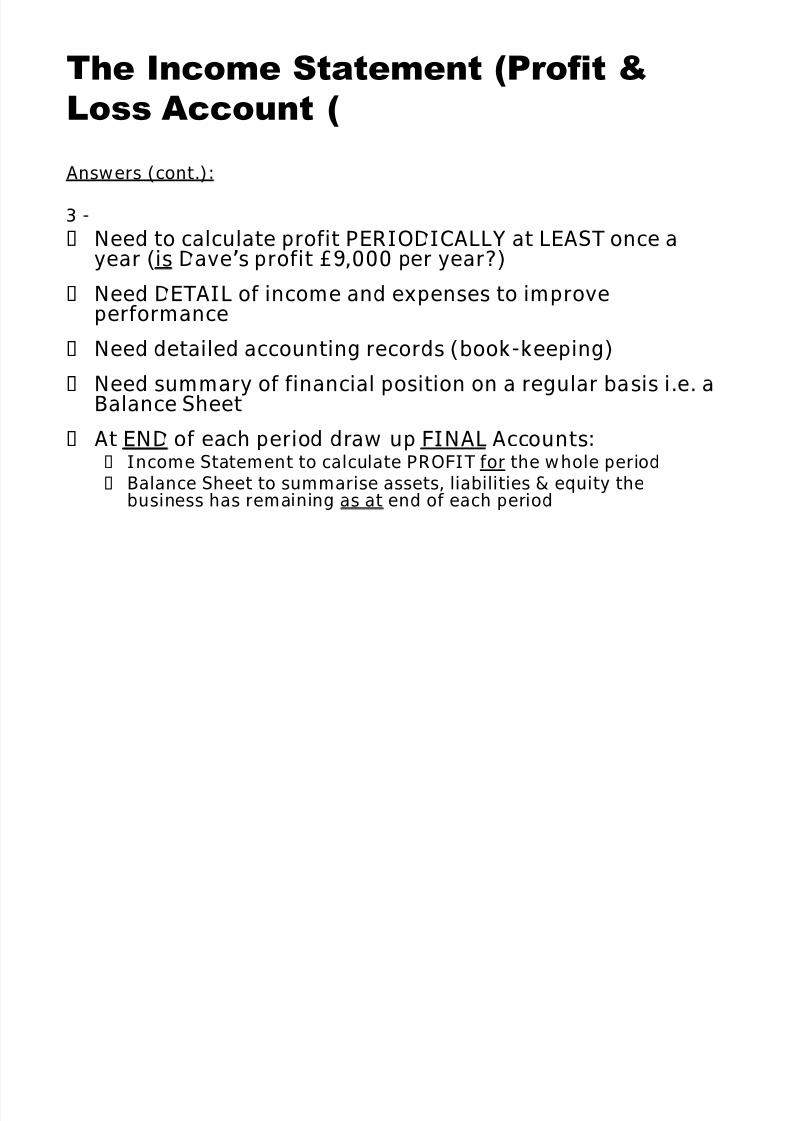

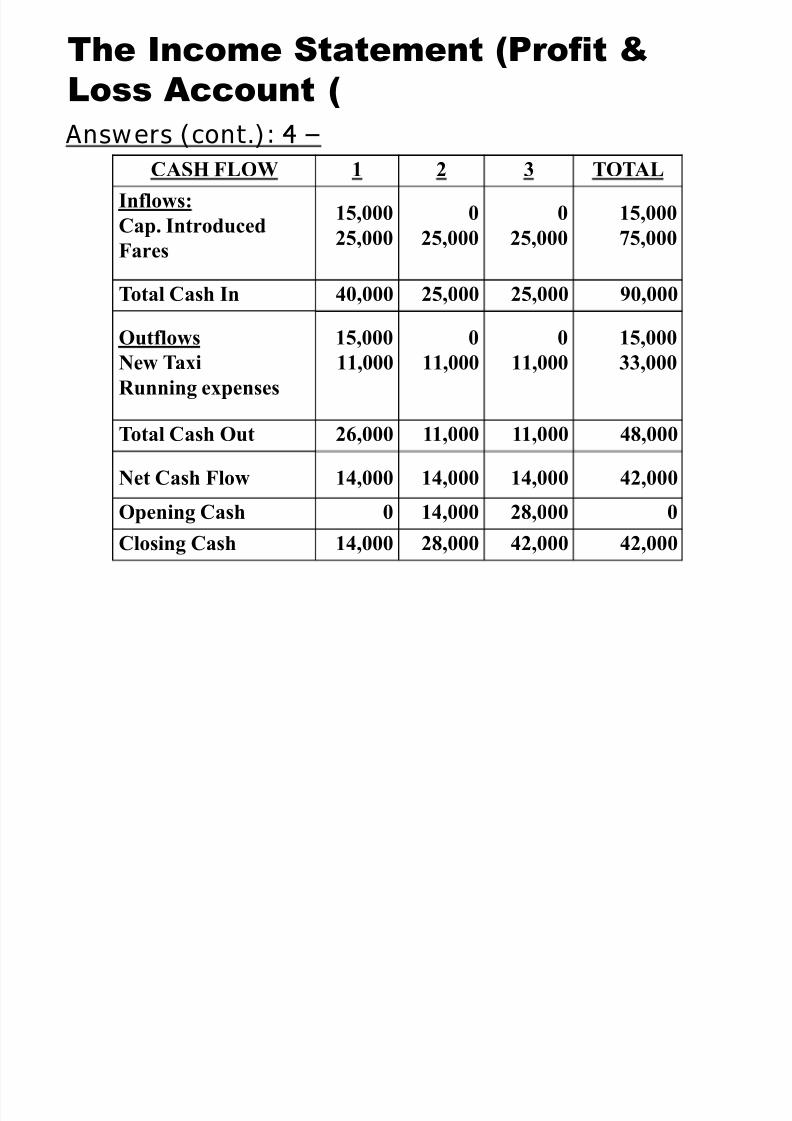

Answers (cont.): 4

The Income Statement (Profit &

Loss Account)

CASH FLOW 1 2 3 TOTAL

Inflows:

Cap. Introduced

Fares

15,000

25,000

0

25,000

0

25,000

15,000

75,000

Total Cash In 40,000 25,000 25,000 90,000

Outflows

New Taxi

Running expenses

15,000

11,000

0

11,000

0

11,000

15,000

33,000

Total Cash Out 26,000 11,000 11,000 48,000

Net Cash Flow 14,000 14,000 14,000 42,000

Opening Cash 0 14,000 28,000 0

Closing Cash 14,000 28,000 42,000 42,000

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 9/31

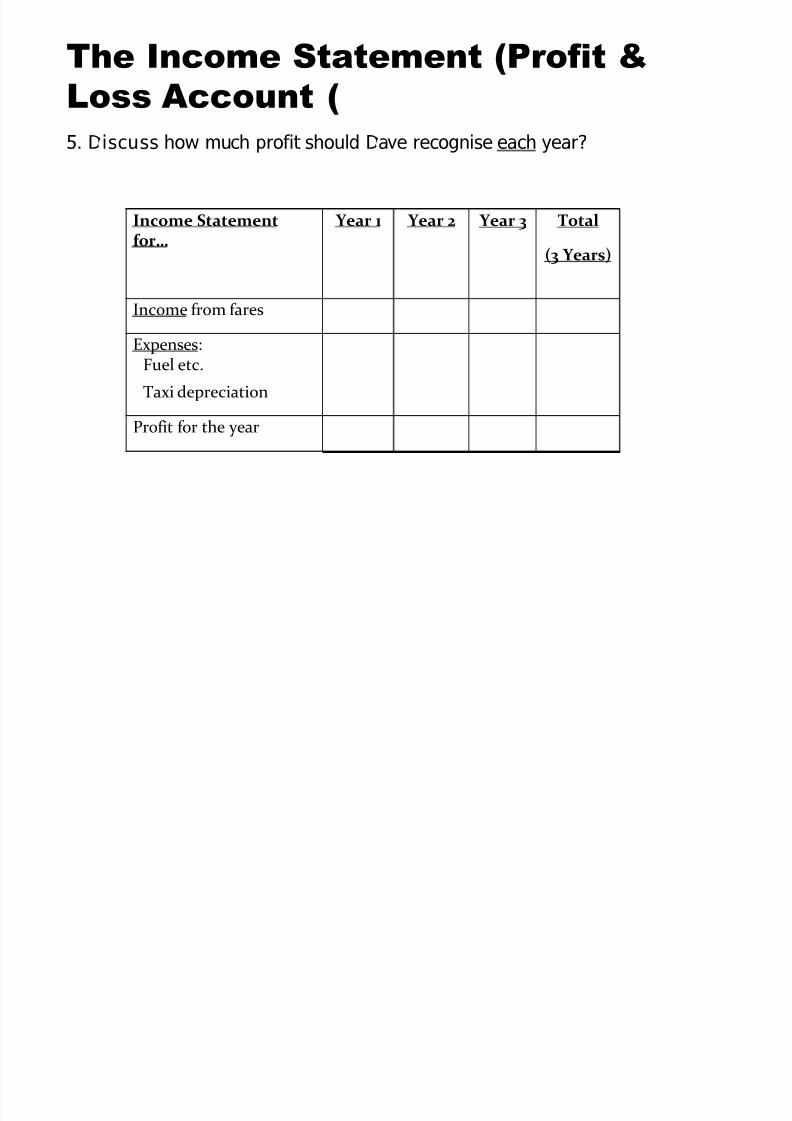

5. Discuss how much profit should Dave recognise each year?

The Income Statement (Profit &

Loss Account)

Income Statementfor

Year 1 Year 2 Year 3 Total

(3 Years)

Income from fares

Expenses:Fuel etc.

Taxi depreciation

Profit for the year

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 10/31

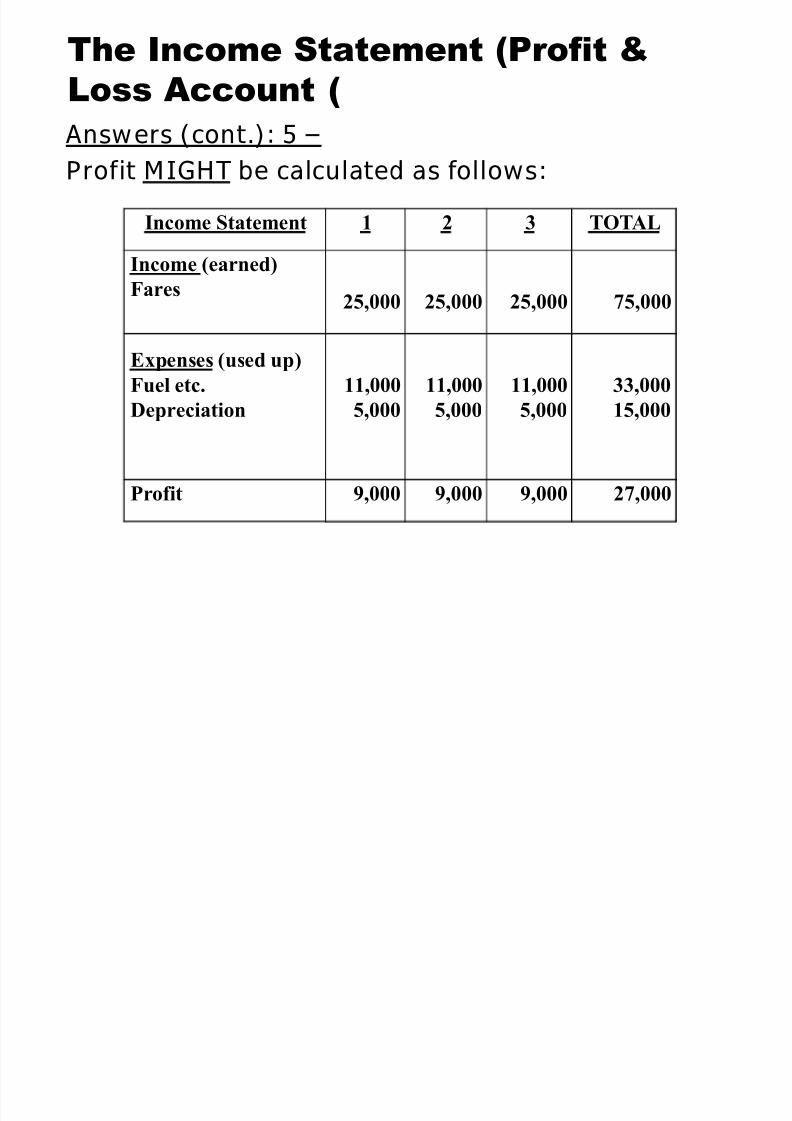

Answers (cont.): 5 Profit MIGHT be calculated as follows:

The Income Statement (Profit &

Loss Account)

Income Statement 1 2 3 TOTAL

Income (earned)

Fares25,000 25,000 25,000 75,000

Expenses (used up)

Fuel etc.

Depreciation

11,000

5,000

11,000

5,000

11,000

5,000

33,000

15,000

Profit 9,000 9,000 9,000 27,000

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 11/31

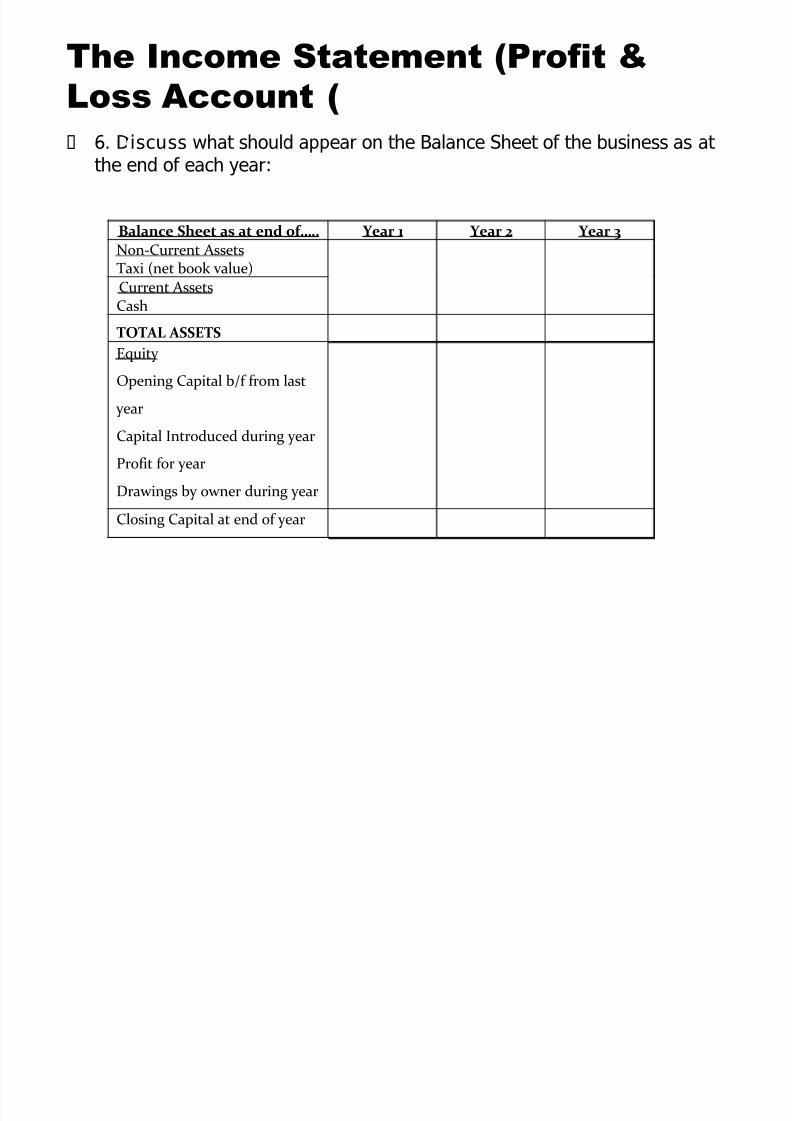

6. Discuss what should appear on the Balance Sheet of the business as at the end of each year:

The Income Statement (Profit &

Loss Account)

Balance Sheet as at end of.. Year 1 Year 2 Year 3

Non-Current AssetsTaxi (net book value)Current AssetsCash

TOTAL ASSETS

Equity

Opening Capital b/f from last

yearCapital Introduced during year

Profit for year

Drawings by owner during year

Closing Capital at end of year

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 12/31

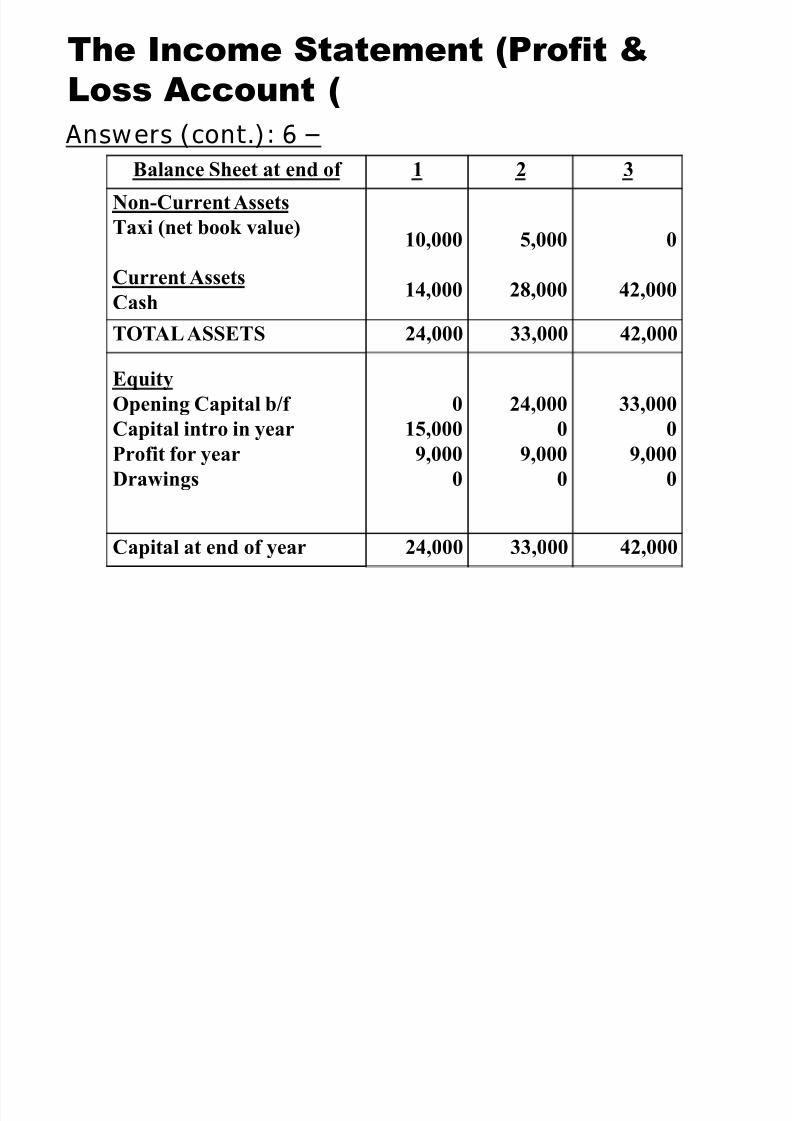

Answers (cont.): 6

The Income Statement (Profit &

Loss Account)

Balance Sheet at end of 1 2 3

Non-Current Assets

Taxi (net book value)

Current AssetsCash

10,000

14,000

5,000

28,000

0

42,000

TOTAL ASSETS 24,000 33,000 42,000

Equity

Opening Capital b/f

Capital intro in year

Profit for year

Drawings

0

15,000

9,000

0

24,000

0

9,000

0

33,000

0

9,000

0

Capital at end of year 24,000 33,000 42,000

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 13/31

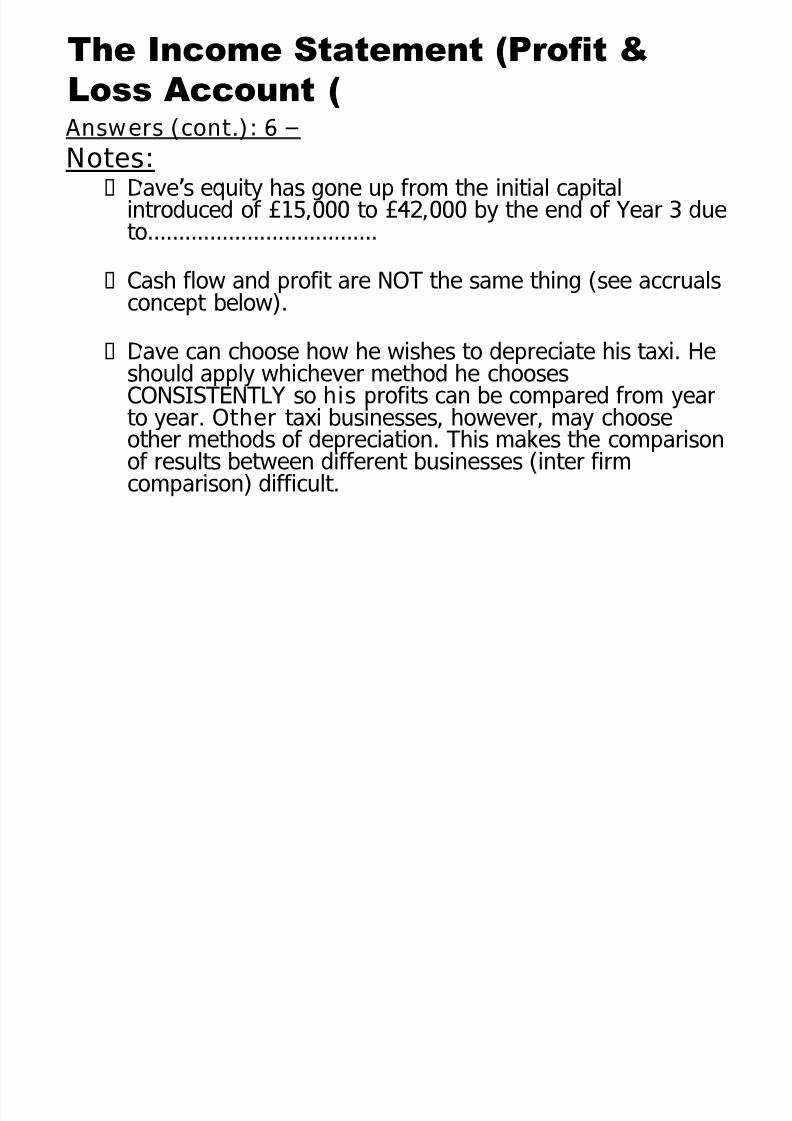

Answers (cont.): 6 Notes: Daves equity has gone up from the initial capital

introduced of £15,000 to £42,000 by the end of Year 3 dueto.

Cash flow and profit are NOT the same thing (see accrualsconcept below).

Dave can choose how he wishes to depreciate his taxi. Heshould apply whichever method he choosesCONSISTENTLY so his profits can be compared from year

to year. Other taxi businesses, however, may chooseother methods of depreciation. This makes the comparisonof results between different businesses (inter firmcomparison) difficult.

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 14/31

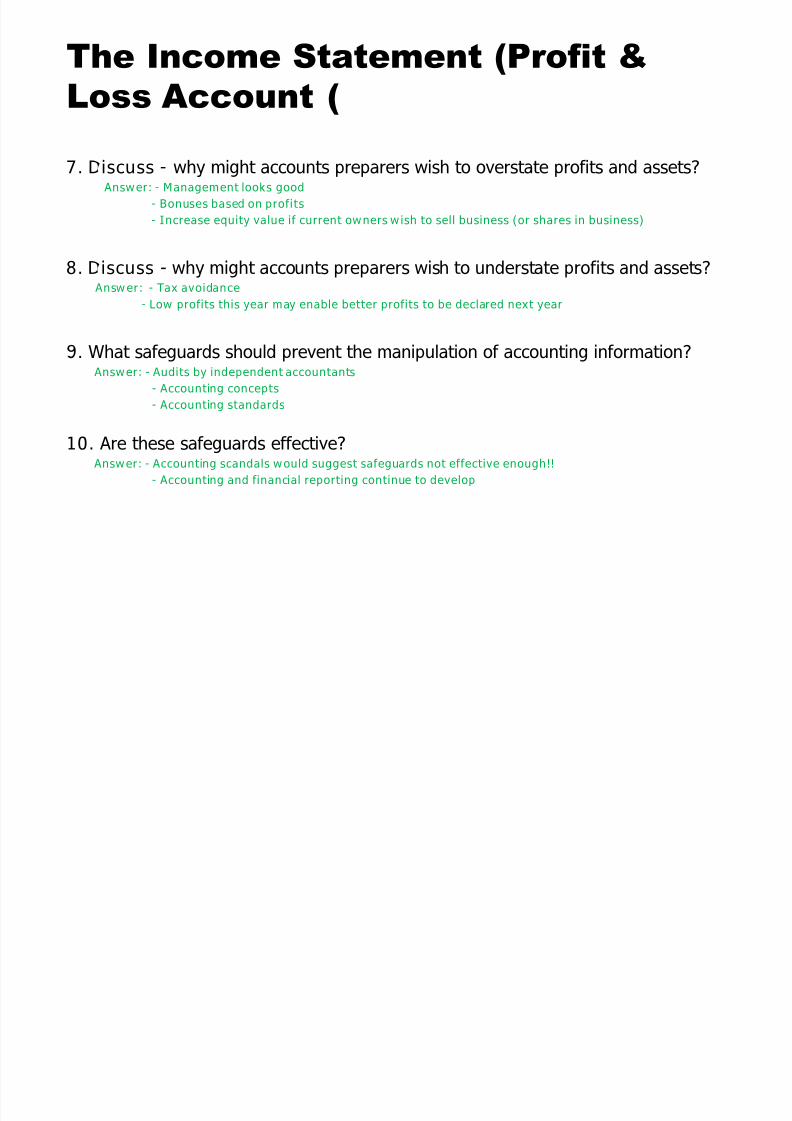

7. Discuss - why might accounts preparers wish to overstate profits and assets? Answer: - Management looks good

- Bonuses based on profits

- Increase equity value if current owners wish to sell business (or shares in business)

8. Discuss - why might accounts preparers wish to understate profits and assets? Answer: - Tax avoidance

- Low profits this year may enable better profits to be declared next year

9. What safeguards should prevent the manipulation of accounting information? Answer: - Audits by independent accountants

- Accounting concepts

- Accounting standards

10. Are these safeguards effective? Answer: - Accounting scandals would suggest safeguards not effective enough!!

- Accounting and financial reporting continue to develop

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 15/31

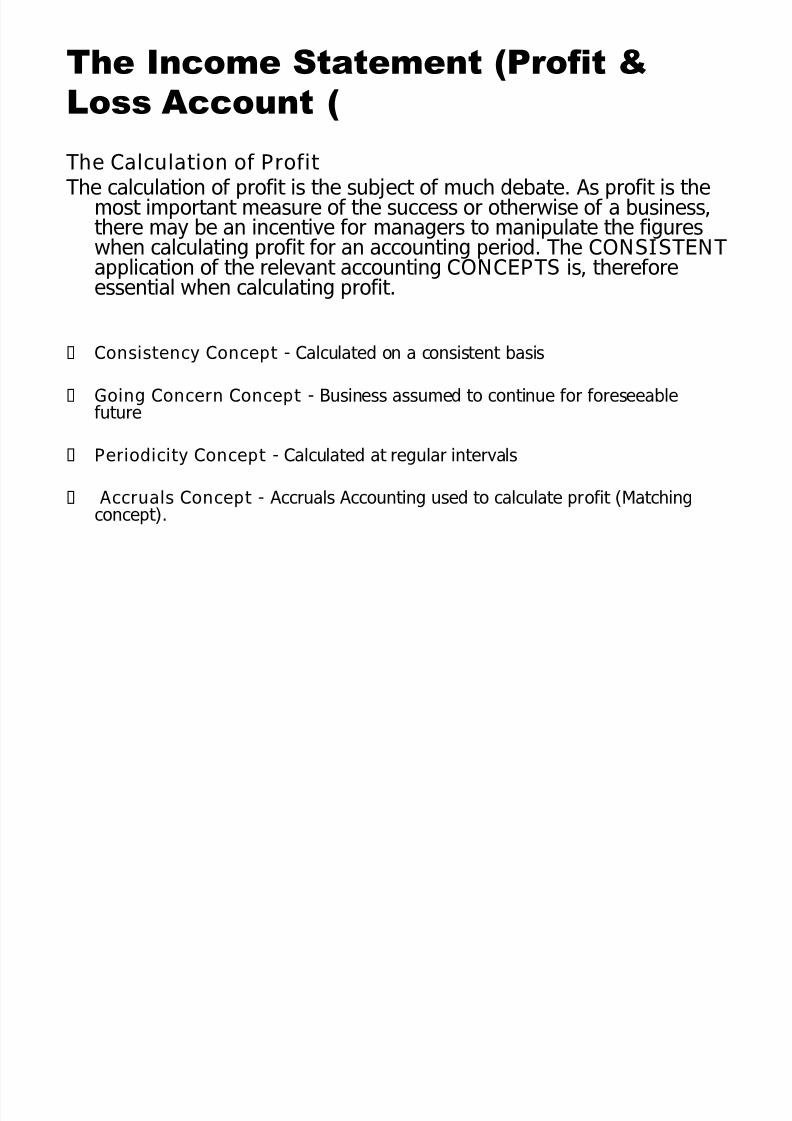

The Calculation of ProfitThe calculation of profit is the subject of much debate. As profit is the

most important measure of the success or otherwise of a business,there may be an incentive for managers to manipulate the figureswhen calculating profit for an accounting period. The CONSISTENT

application of the relevant accounting CONCEPTS is, thereforeessential when calculating profit.

Consistency Concept - Calculated on a consistent basis

Going Concern Concept - Business assumed to continue for foreseeable

future

Periodicity Concept - Calculated at regular intervals

Accruals Concept - Accruals Accounting used to calculate profit (Matchingconcept).

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 16/31

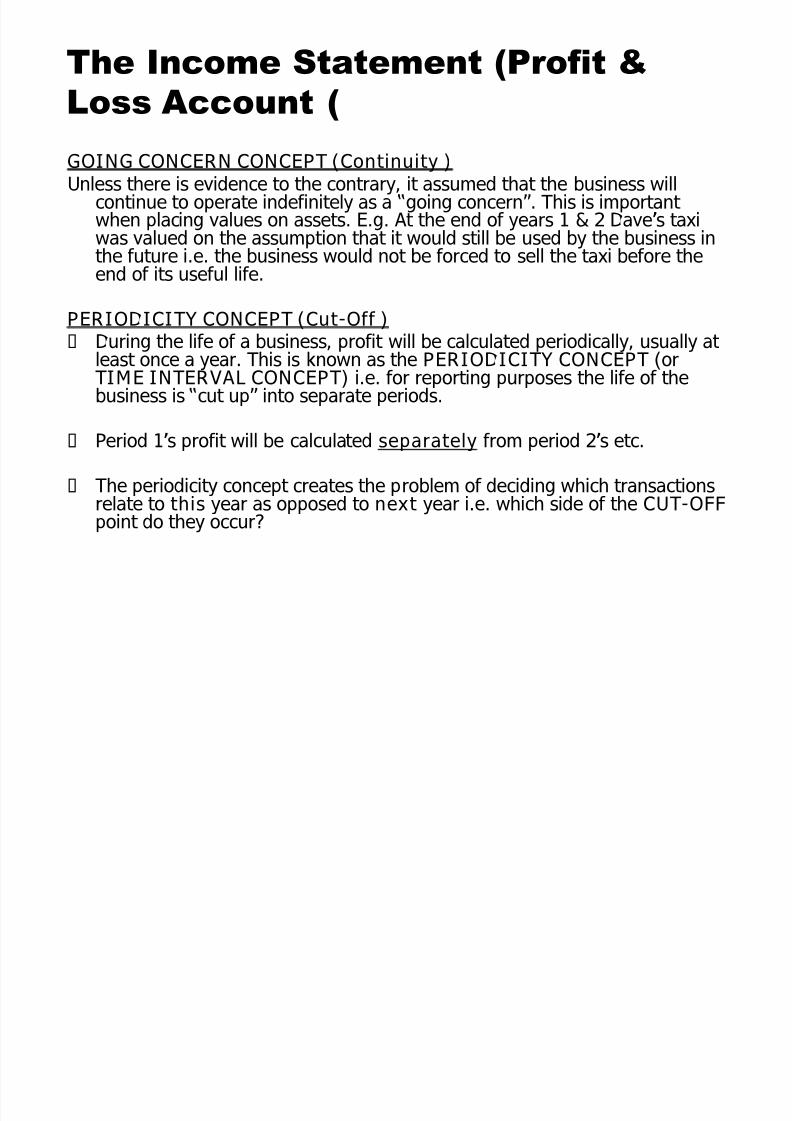

GOING CONCERN CONCEPT (Continuity )Unless there is evidence to the contrary, it assumed that the business will

continue to operate indefinitely as a going concern. This is important when placing values on assets. E.g. At the end of years 1 & 2 Daves taxiwas valued on the assumption that it would still be used by the business inthe future i.e. the business would not be forced to sell the taxi before the

end of its useful life.

PERIODICITY CONCEPT (Cut-Off ) During the life of a business, profit will be calculated periodically, usually at

least once a year. This is known as the PERIODICITY CONCEPT (orTIME INTERVAL CONCEPT) i.e. for reporting purposes the life of thebusiness is cut up into separate periods.

Period 1s profit will be calculated separately from period 2s etc.

The periodicity concept creates the problem of deciding which transactionsrelate to this year as opposed to next year i.e. which side of the CUT-OFFpoint do they occur?

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 17/31

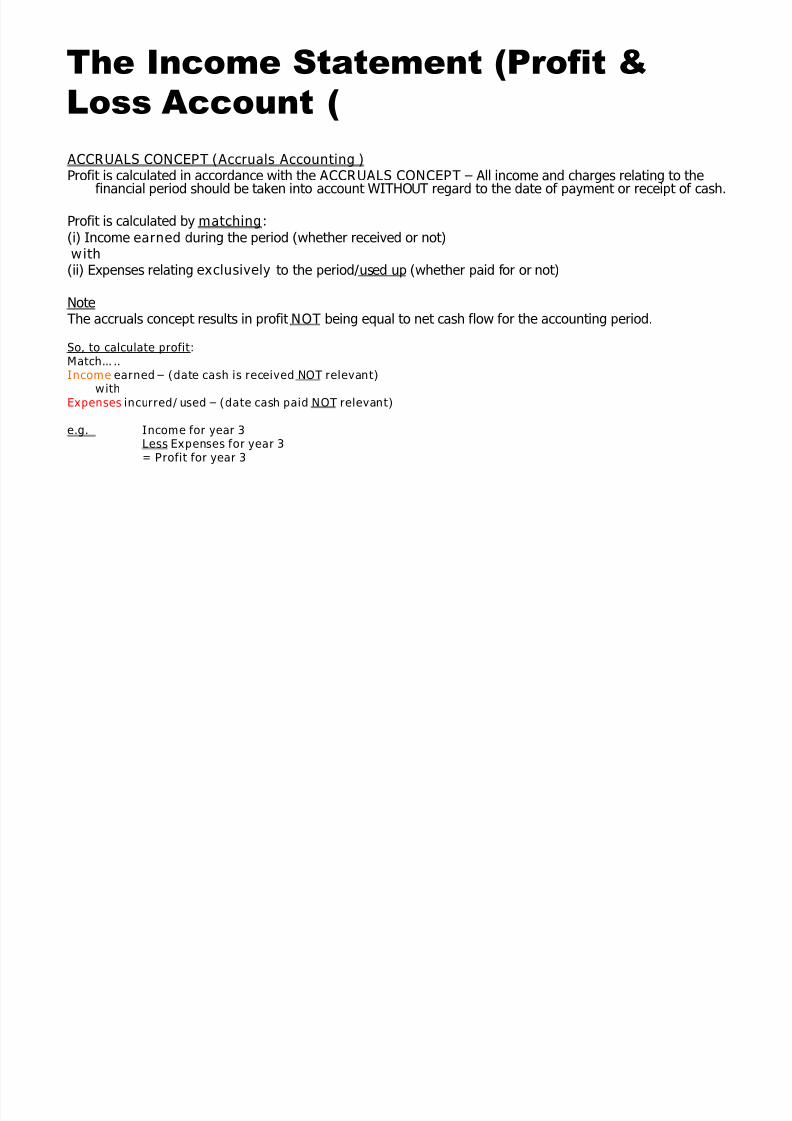

ACCRUALS CONCEPT ( Accruals Accounting )Profit is calculated in accordance with the ACCRUALS CONCEPT All income and charges relating to the

financial period should be taken into account WITHOUT regard to the date of payment or receipt of cash.

Profit is calculated by matching:(i) Income earned during the period (whether received or not)with(ii) Expenses relating exclusively to the period/used up (whether paid for or not)

NoteThe accruals concept results in profit NOT being equal to net cash flow for the accounting period.

So, to calculate profit:Match..Income earned (date cash is received NOT relevant)

withExpenses incurred/used (date cash paid NOT relevant)

e.g. Income for year 3Less Expenses for year 3= Profit for year 3

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 18/31

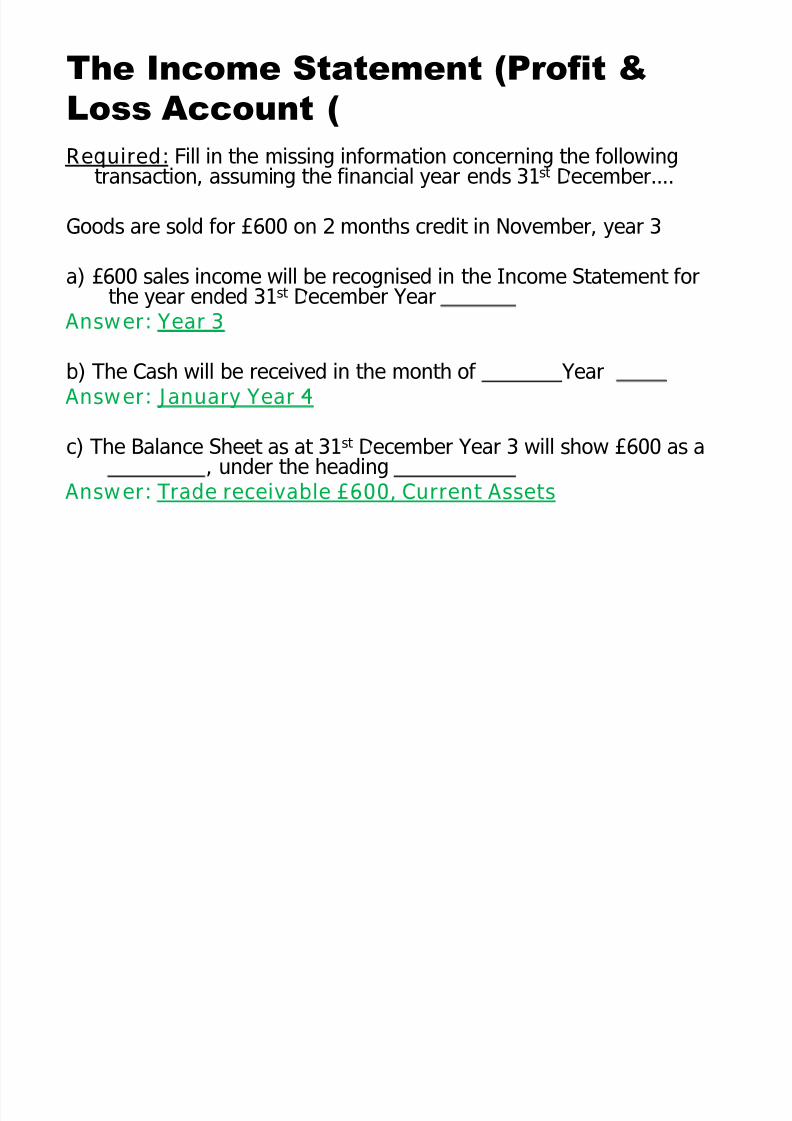

Required: Fill in the missing information concerning the followingtransaction, assuming the financial year ends 31st December.

Goods are sold for £600 on 2 months credit in November, year 3

a) £600 sales income will be recognised in the Income Statement forthe year ended 31st December Year Answer: Year 3

b) The Cash will be received in the month of Year Answer: January Year 4

c) The Balance Sheet as at 31st December Year 3 will show £600 as a, under the heading

Answer: Trade receivable £600, Current Assets

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 19/31

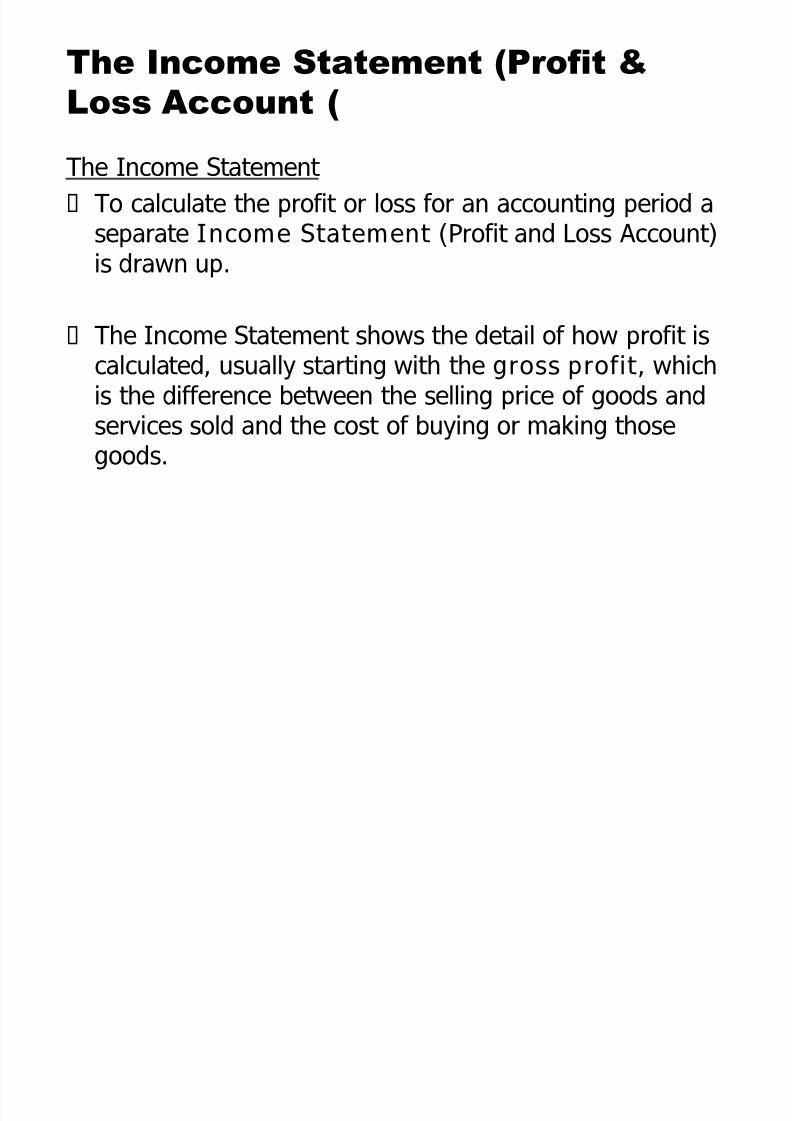

The Income Statement

To calculate the profit or loss for an accounting period aseparate Income Statement (Profit and Loss Account)is drawn up.

The Income Statement shows the detail of how profit iscalculated, usually starting with the gross profit, whichis the difference between the selling price of goods and

services sold and the cost of buying or making thosegoods.

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 20/31

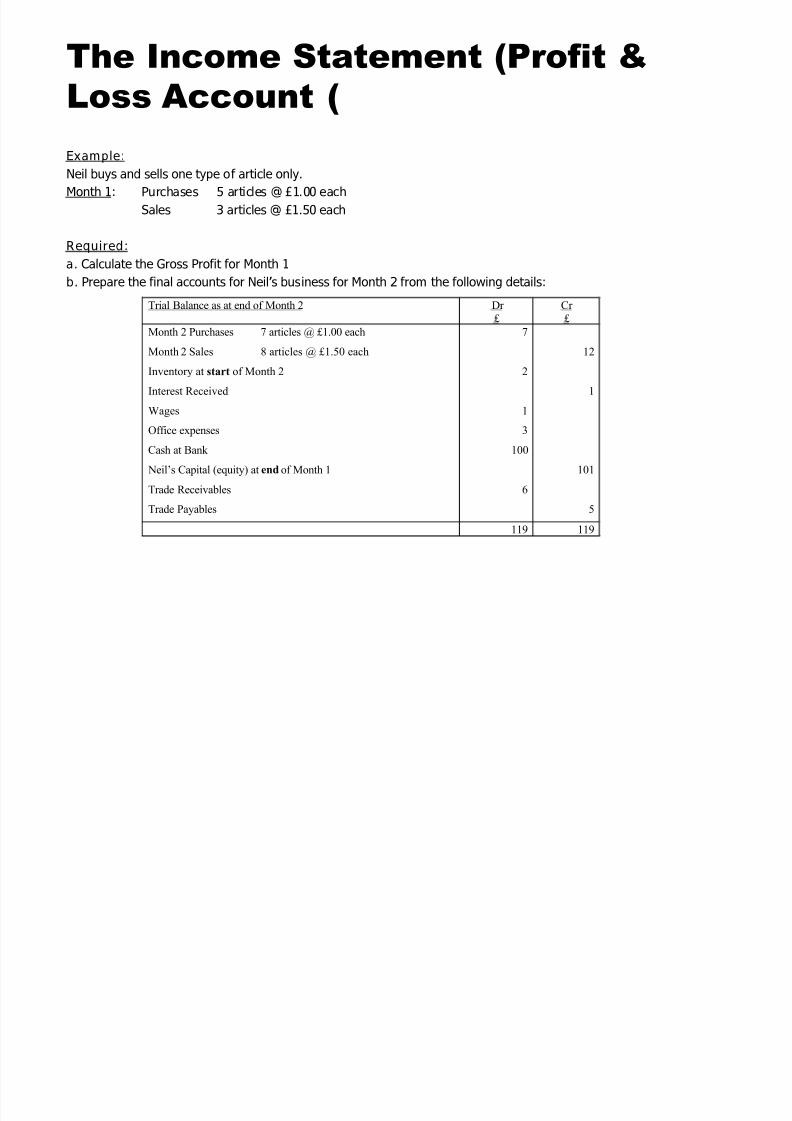

Example:

Neil buys and sells one type of article only.

Month 1: Purchases 5 articles @ £1.00 each

Sales 3 articles @ £1.50 each

Required:

a. Calculate the Gross Profit for Month 1

b. Prepare the final accounts for Neils business for Month 2 from the following details:

The Income Statement (Profit &

Loss Account)

Trial Balance as at end of Month 2 Dr

£

Cr

£

Month 2 Purchases 7 articles @ £1.00 each

Month 2 Sales 8 articles @ £1.50 each

Inventory at start of Month 2

Interest Received

Wages

Office expenses

Cash at Bank

Neil¶s Capital (equity) at end of Month 1

Trade Receivables

Trade Payables

7

2

1

3

100

6

12

1

101

5

119 119

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 21/31

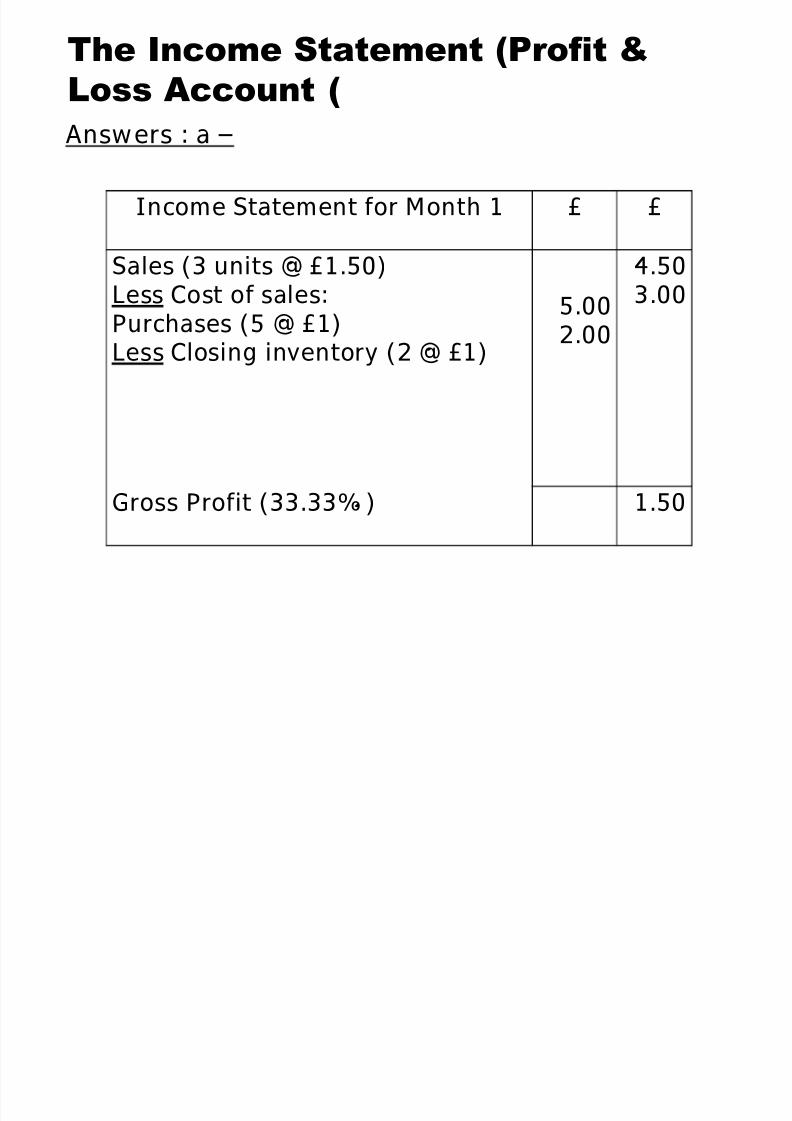

Answers : a

The Income Statement (Profit &

Loss Account)

Income Statement for Month 1 £ £

Sales (3 units @ £1.50)Less Cost of sales:Purchases (5 @ £1)Less Closing inventory (2 @ £1)

5.002.00

4.503.00

Gross Profit (33.33%) 1.50

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 22/31

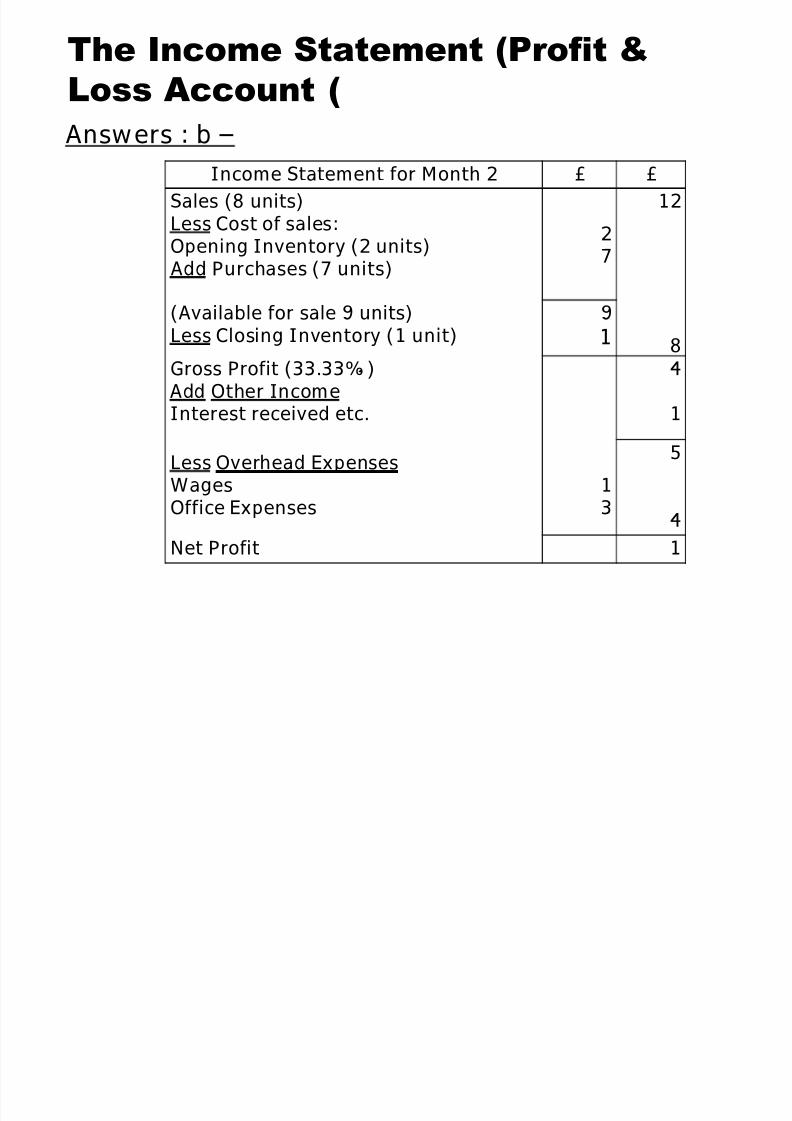

Answers : b

The Income Statement (Profit &

Loss Account)

Income Statement for Month 2 £ £

Sales (8 units)Less Cost of sales:Opening Inventory (2 units)

Add Purchases (7 units)

27

12

(Available for sale 9 units)Less Closing Inventory (1 unit)

9

1 8Gross Profit (33.33%)

Add Other Income

Interest received etc.

4

1

Less Overhead ExpensesWagesOffice Expenses

13

5

4

Net Profit 1

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 23/31

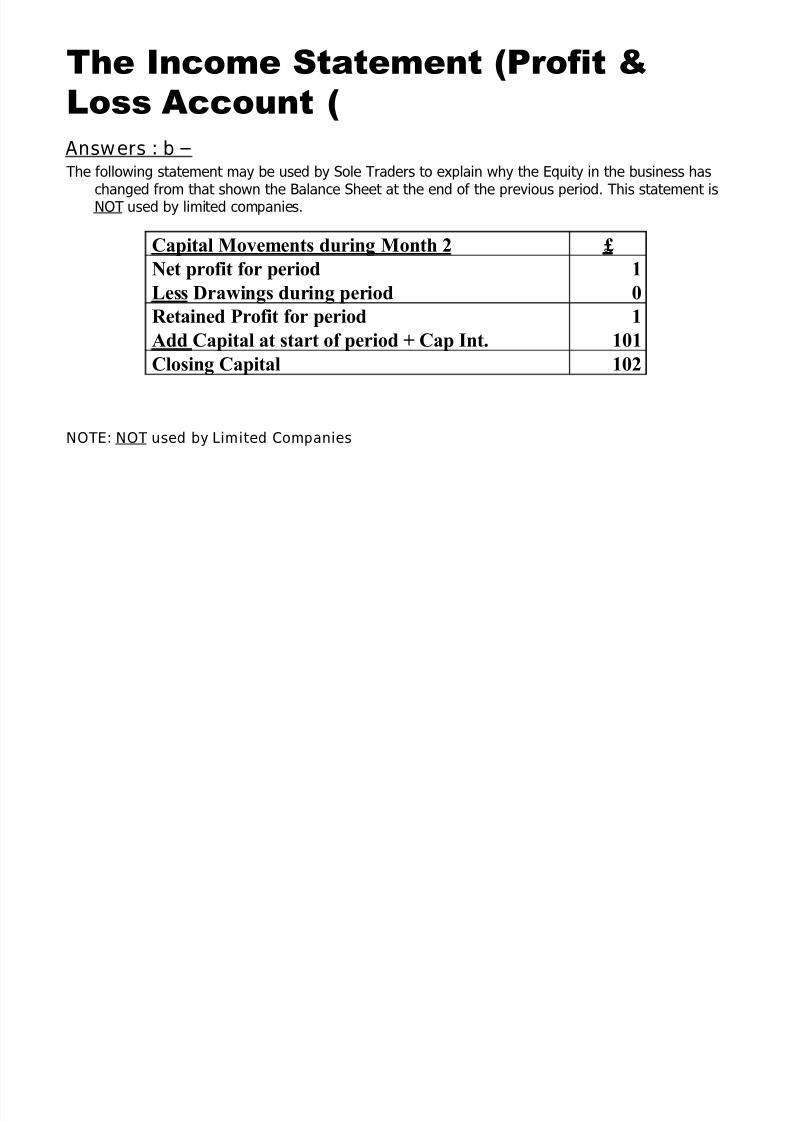

Answers : b The following statement may be used by Sole Traders to explain why the Equity in the business has

changed from that shown the Balance Sheet at the end of the previous period. This statement isNOT used by limited companies.

NOTE: NOT used by Limited Companies

The Income Statement (Profit &

Loss Account)

Capital Movements during Month 2 £

Net profit for period

Less Drawings during period

1

0

Retained Profit for period

Add Capital at start of period + Cap Int.

1

101

Closing Capital 102

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 24/31

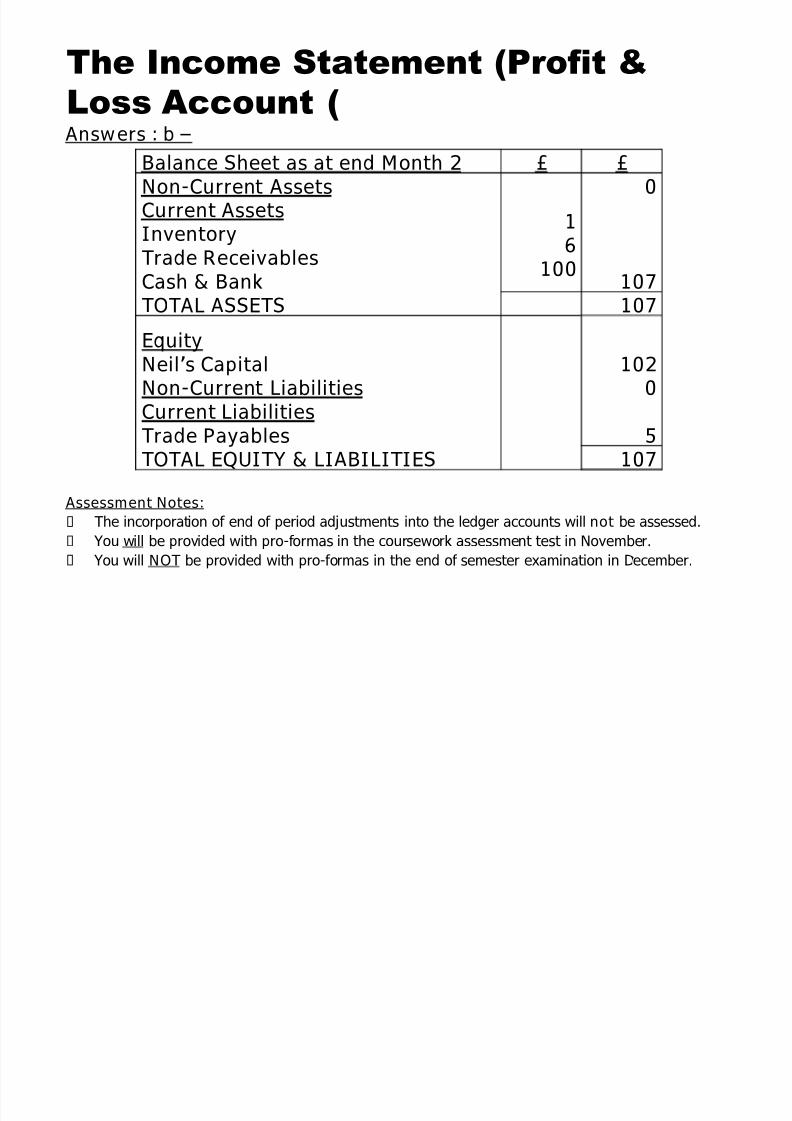

Answers : b

Assessment Notes:

The incorporation of end of period adjustments into the ledger accounts will not be assessed.

You will be provided with pro-formas in the coursework assessment test in November.

You will NOT be provided with pro-formas in the end of semester examination in December.

The Income Statement (Profit &

Loss Account)

Balance Sheet as at end Month 2 £ £Non-Current AssetsCurrent AssetsInventoryTrade Receivables

Cash & Bank

16

100

0

107TOTAL ASSETS 107

EquityNeils CapitalNon-Current Liabilities

Current LiabilitiesTrade Payables

1020

5TOTAL EQUITY & LIABILITIES 107

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 25/31

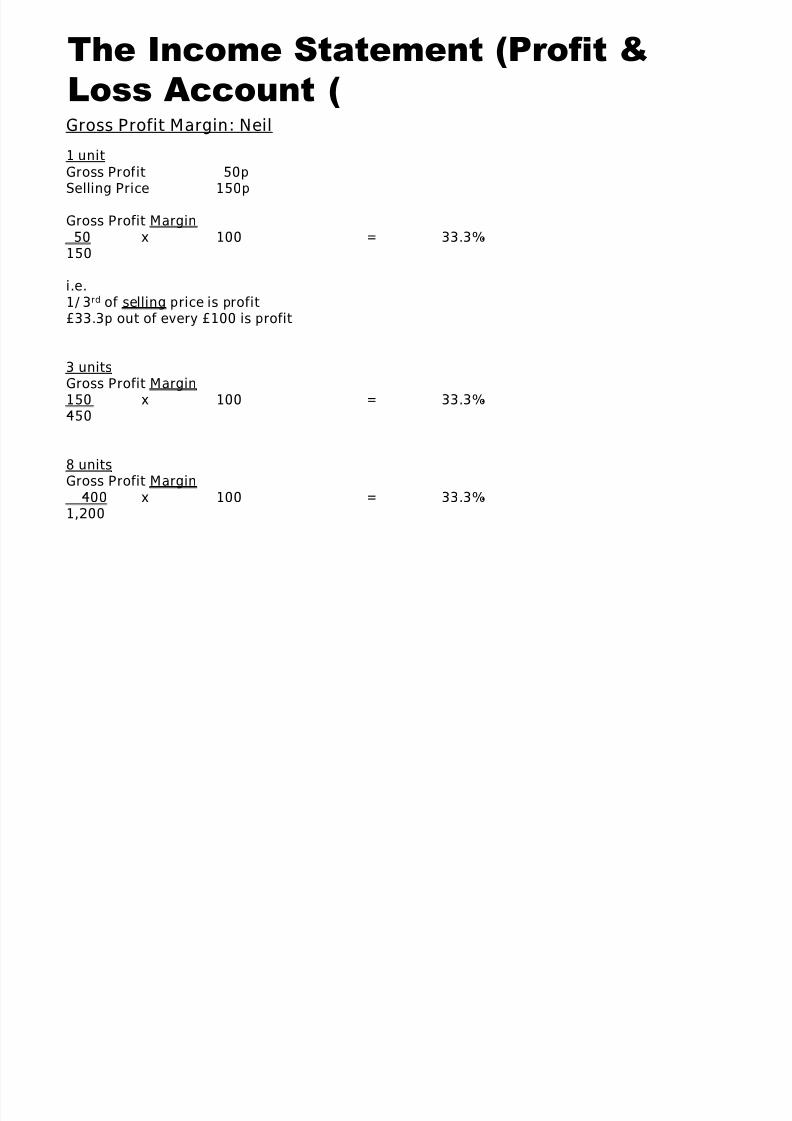

Gross Profit Margin: Neil

1 unitGross Profit 50pSelling Price 150p

Gross Profit Margin50 x 100 = 33.3%

150

i.e.1/3rd of selling price is profit£33.3p out of every £100 is profit

3 unitsGross Profit Margin150 x 100 = 33.3%

450

8 unitsGross Profit Margin

400 x 100 = 33.3%1,200

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 26/31

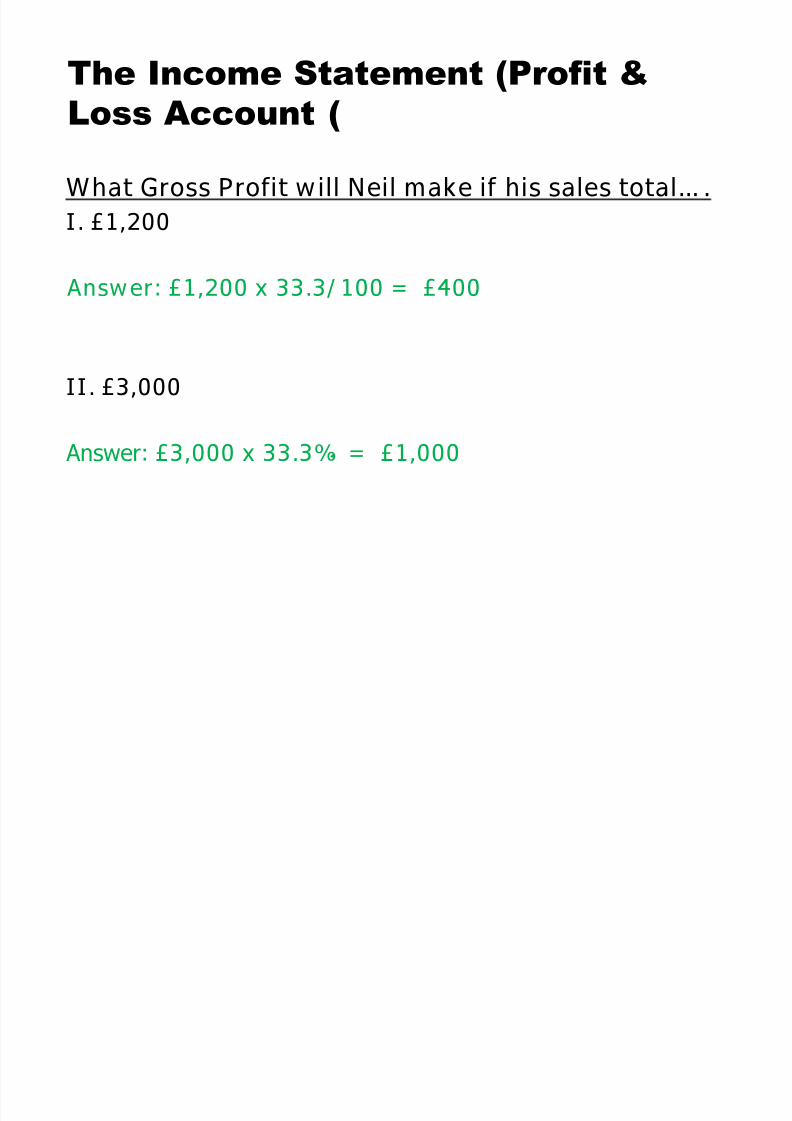

What Gross Profit will Neil make if his sales total.

I. £1,200

Answer: £1,200 x 33.3/100 = £400

II. £3,000

Answer: £3,000 x 33.3% = £1,000

The Income Statement (Profit &

Loss Account)

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 27/31

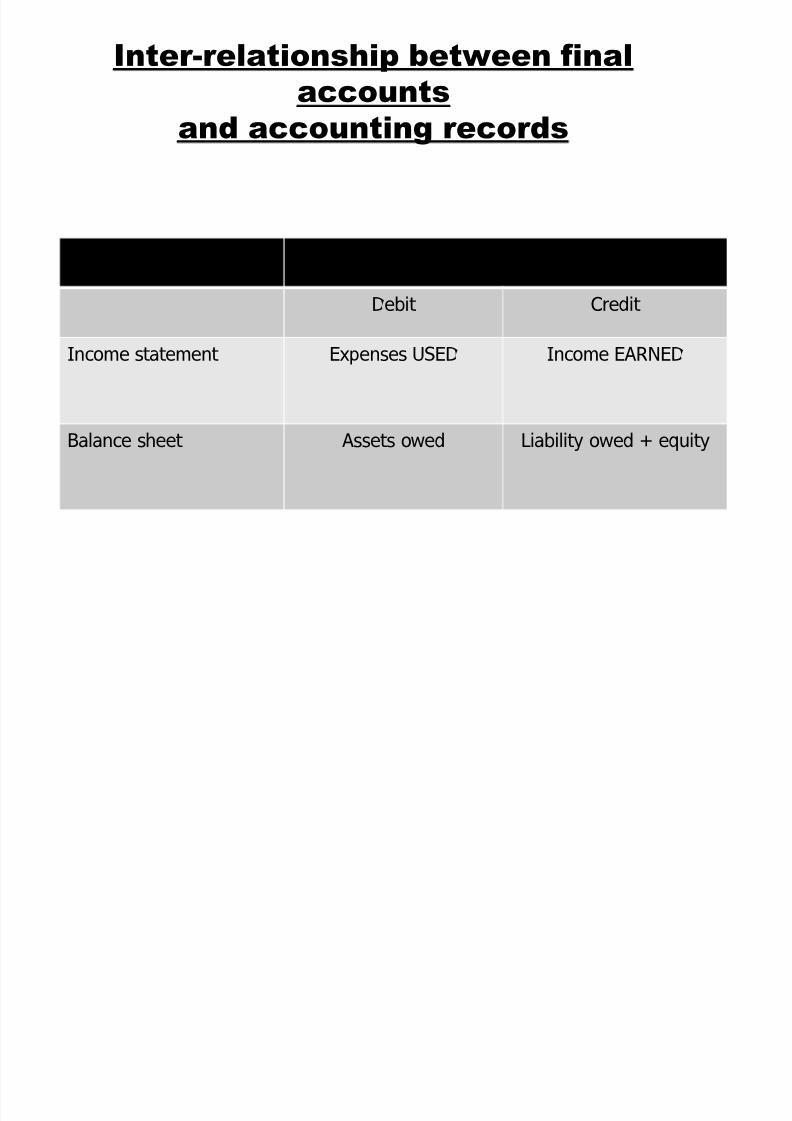

Inter-relationship between final

accounts

and accounting records

Final accounts Double entry rules

Debit Credit

Income statement Expenses USED Income EARNED

Balance sheet Assets owed Liability owed + equity

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 28/31

Inter-relationship between final

accounts

and accounting records

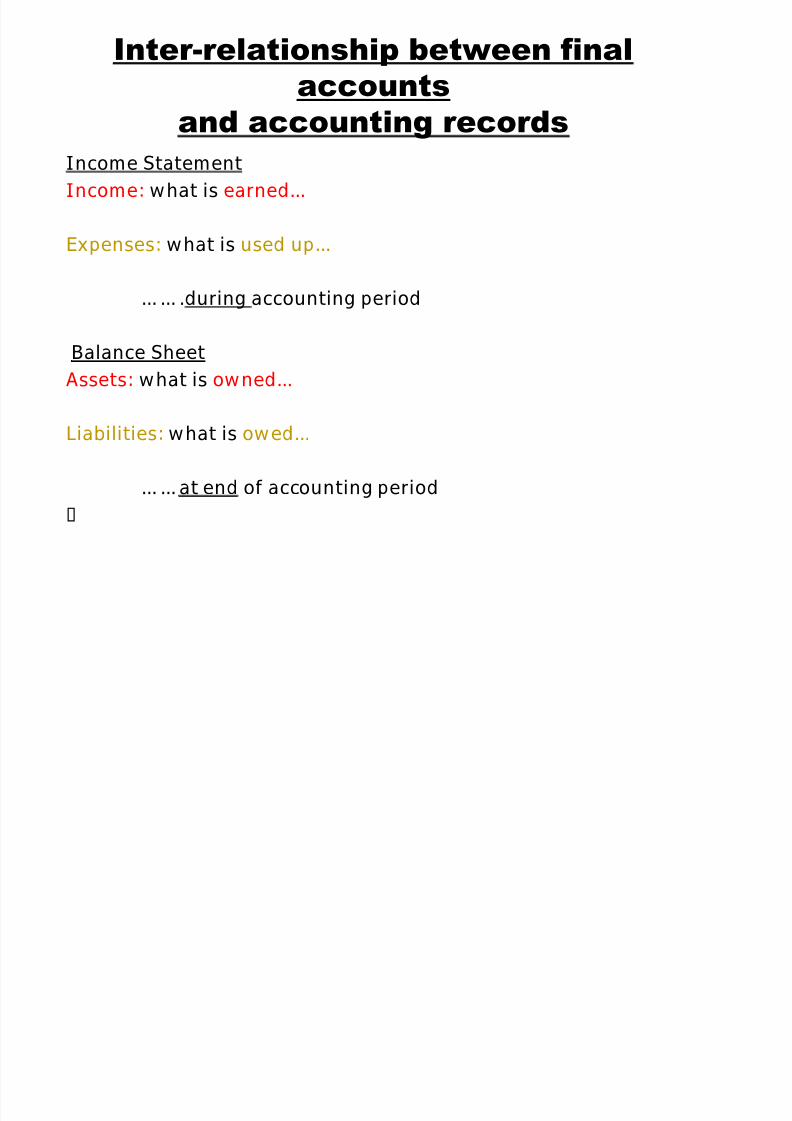

Income Statement

Income: what is earned

Expenses: what is used up

.during accounting period

Balance Sheet

Assets: what is owned

Liabilities: what is owed

at end of accounting period

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 29/31

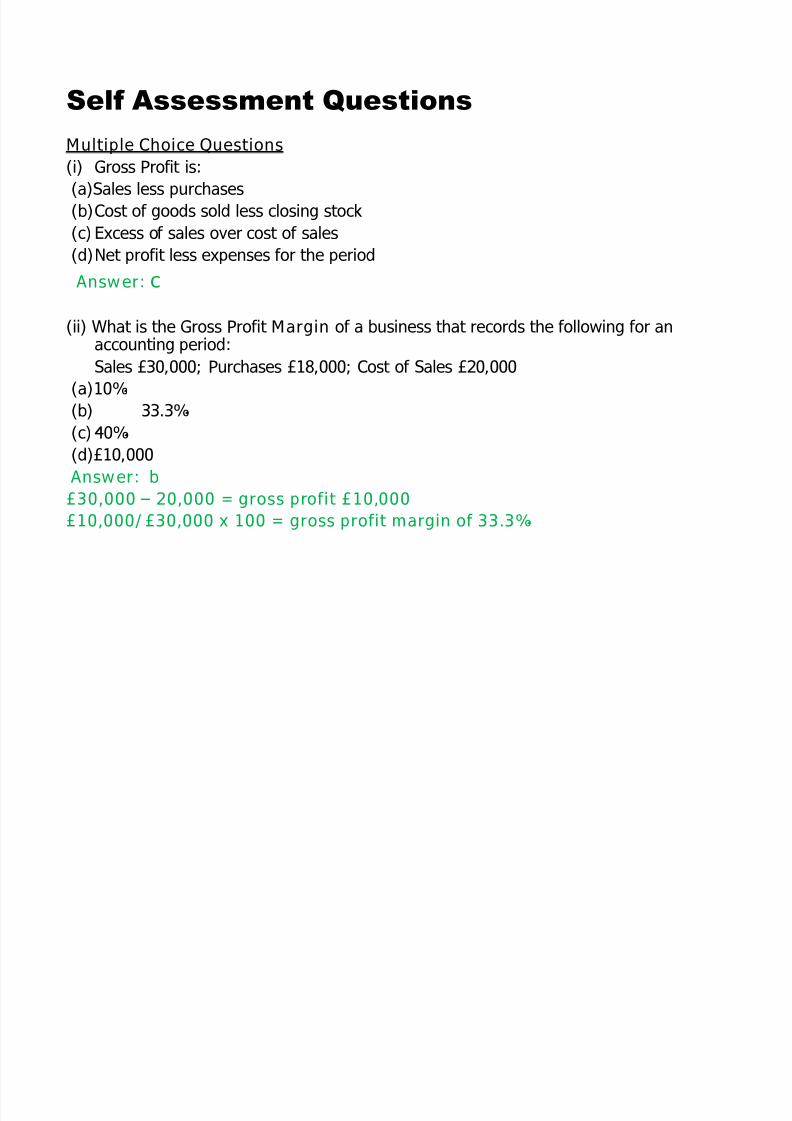

Multiple Choice Questions(i) Gross Profit is:

(a)Sales less purchases

(b)Cost of goods sold less closing stock

(c) Excess of sales over cost of sales

(d)Net profit less expenses for the period

Answer: c

(ii) What is the Gross Profit Margin of a business that records the following for anaccounting period:

Sales £30,000; Purchases £18,000; Cost of Sales £20,000

(a)10%

(b) 33.3%(c)40%

(d)£10,000

Answer: b

£30,000 20,000 = gross profit £10,000

£10,000/£30,000 x 100 = gross profit margin of 33.3%

Self Assessment Questions

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 30/31

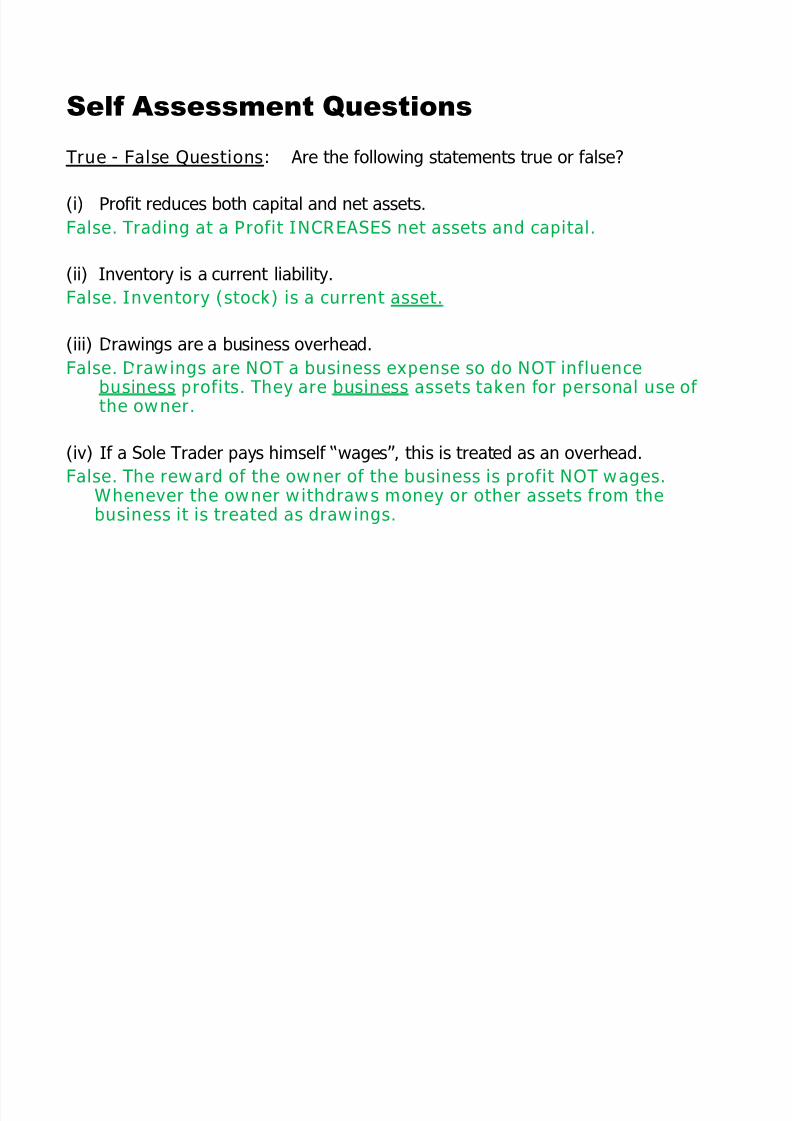

True - False Questions: Are the following statements true or false?

(i) Profit reduces both capital and net assets.

False. Trading at a Profit INCREASES net assets and capital.

(ii) Inventory is a current liability.False. Inventory (stock) is a current asset.

(iii) Drawings are a business overhead.

False. Drawings are NOT a business expense so do NOT influencebusiness profits. They are business assets taken for personal use ofthe owner.

(iv) If a Sole Trader pays himself wages, this is treated as an overhead.

False. The reward of the owner of the business is profit NOT wages.Whenever the owner withdraws money or other assets from thebusiness it is treated as drawings.

Self Assessment Questions

8/3/2019 2 Income N CashFlow Statements Help Session1

http://slidepdf.com/reader/full/2-income-n-cashflow-statements-help-session1 31/31

31

Thank You

Note : Images were downloaded between 28th April to 2nd May 2011

Examples are from Atrill and McLaney, 2011 and others. detail references can be provided on request