Embed Size (px)

Citation preview

2nd NATIONAL EXPORT FORUM 2008

Steven C.M. Wong*Institute of Strategic and International Studies (ISIS) Malaysia

* The opinions expressed are solely those of the speaker

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

OUTLINE

Present status

• Short-term outlook

• Medium- to longer-term horizon

• Conclusions

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

PRESENT STATUS• Strong growth in export value since 2001• Manufactured products account for more than 75%, and electrical and electronics about 45%, of total exports • ASEAN countries, particularly Singapore, Thailand, Indonesia and Vietnam, represent a quarter of the total export market• The US is the largest single market (16%), followed by the EU countries (13%) and Mainland China (9%) and Japan (9%)• Fastest growing markets have been those of ASEAN, Northeast Asia and the South• Exports to US, comprising mainly E&E products, have been tapering off and begun to show decline

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

373

334

357

398

481

534

589

601(e)

0 100 200 300 400 500 600 700

2000

2001

2002

2003

2004

2005

2006

2007

RM bn

TOTAL EXPORT VALUE, 2000-2007(e)

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

265.236.4

33.1

32.8

25.9

22.7

22.3

Electrical & electronic products

Palm oil

Chemicals & chem. products

Crude petroleum

Liquified natural gas

Refined petroleum products

Machinery appliances & parts

RM bn

MAJOR EXPORTS, 2007(e)

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

J apan9%

EU13%

US16%

ASEAN25%

Others 12%

China9%

Korea4%

Hong Kong5%

West Asia4%Australia

3%

MAJOR EXPORT MARKETS, 2007(e)

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

ASEAN

US

EU

Japan(RHS)

China(RHS)

Korea(RHS)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000 2001 2002 2003 2004 2005 2006 2007

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

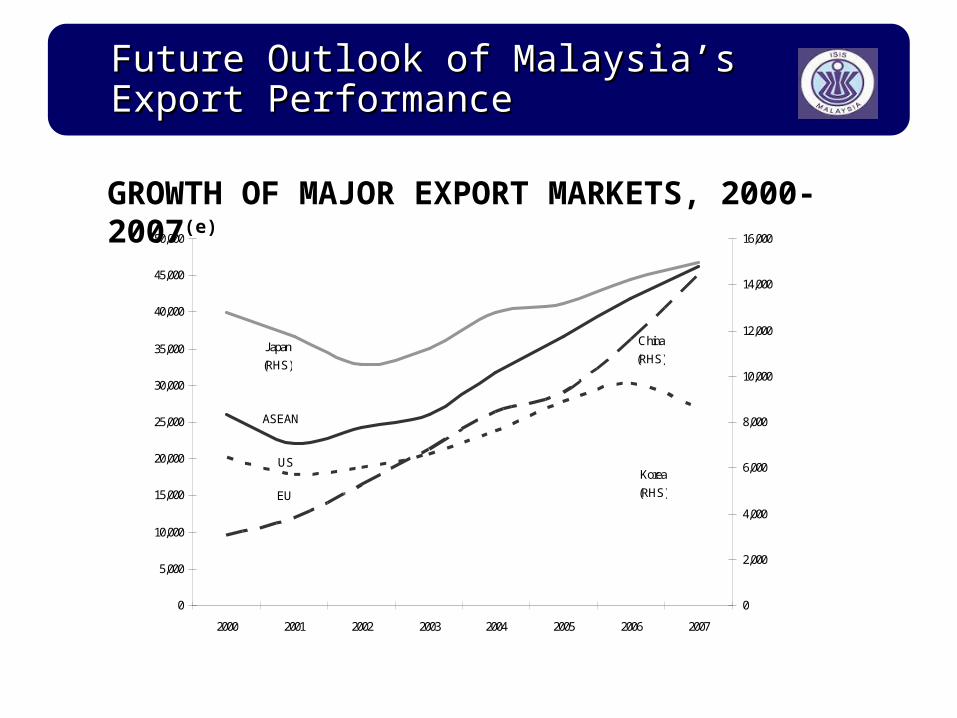

GROWTH OF MAJOR EXPORT MARKETS, 2000-2007(e)

SHORT-TERM OUTLOOK

Exports to the US look increasingly vulnerable, with high risks (not certainty) of an economic recession

• The combined impact on Malaysian exports could be substantial taking into account parts & component (P & C) trade with the US as the final destination market

• Compounding the uncertainty is the price-quantity effect of appreciated Asian currencies on US demand

• De-coupling scenarios only work if domestic absorption is substantially and simultaneously increased in the Rest of the World

• East Asian countries are investing too much and consuming too little Economic integration of East Asia is production-oriented and not consumption-based.

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

SHORT-TERM OUTLOOK

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

Share of Intra-Regional Mfg in

Total Regional MfgExports + Imports

Share of Intra-Regional Mfg in Total Regional Mfg Trade

Exports Imports 1993 2005 1993 2005 1990 2005

East Asia 47.3 54.0 40.0 44.4 46.9 68.9

NAFTA 40.0 40.7 46.9 51.5 34.8 33.7

EU-15 66.2 59.0 66.9 58.2 65.5 59.8

SHORT-TERM OUTLOOK

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

Share of intra-regional inTotal trade

(Exports + Imports)

Share of intra-regional trade

Parts andComponents

FinishedGoods

1993 2005 1993 2005 1990 2005

East Asia 47.3 54.0 51.0 67.1 46.2 47.5

NAFTA 40.0 40.7 45.0 44.3 38.1 39.5

EU-15 66.2 59.0 64.7 56.3 66.5 59.7

SHORT-TERM OUTLOOK

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

• Intra-regional trade is concentrated. Just 30 exports account for 50% of total trade, primarily office machinery, telecommunications, electronics, textiles and clothing.

• Intra-regional trade is parts and components-driven and China-centred. International production sharing has driven intra-regional trade, with Japan, Korea and Taiwan being major suppliers and China being the production platform.

• Studies show before there is a sharp increase of East Asian exports to the US, intra-regional trade rises. An increase in Japanese exports to the region also leads to higher exports to the US.

SHORT-TERM OUTLOOK

Future Outlook of Malaysia’s Future Outlook of Malaysia’s Export PerformanceExport Performance

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

Structural Factors Likely to Affect Malaysian Exports

Producers Consumers Markets• Industrial restructuring• Business outsourcing• Distribution• Technology• Knowledge, design• New entrants• Corporate social responsibility

• Lower consumer choice• Cost conscious• Time sensitive• Quality, performance, value• Information, services• New consumers• Environment, security, politics, etc.

• Imperfect competition• Globalised• Borderless• Convergence• Trade in services• New trade hubs & regimes• Government regulations

MEDIUM- TO LONGER-TERM HORIZON

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

Specific Factors Likely to Affect Malaysian Exports – (1)

• Trade creation from China, India, Vietnam & other rapidly growing economies (+ve)

• Regional economic integration via Asean Economic Community and Plus One (and possibly Plus Three, Plus Six) countries (+ve)

• Displacement effects in third markets as a result of competition from emerging economies (-ve)

• Spill-over/exclusion effects from third-party regional trading arrangements (?)

• Stable exchange rate and macroeconomic regime (+ve)

• Integration of export-sector with domestic economy

MEDIUM- TO LONGER-TERM HORIZON

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

Specific Factors Likely to Affect Malaysian Exports – (2)

• Generating investments in targeted growth areas (IMP3)• Integrating Malaysian companies into regional and global networks (IMP3)• Sustaining the contribution of manufacturing sector to growth (IMP3)• Positioning services as a major source of growth (IMP3)• Facilitating development and application of knowledge-intensive technologies (IMP3)• Developing innovative and creative human capital (IMP3)• Creating a more competitive business-operating environment (IMP3)• Strengthening the role of private sector institutions (IMP3)

MEDIUM- TO LONGER-TERM HORIZON

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

MEDIUM- TO LONGER-TERM HORIZON

Economic Union

Common Market

Free Trade Area

Preferential Trading Arrangement

CustomsUnion

Free Trade Area Plus

Most Favoured Nation

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

MEDIUM- TO LONGER-TERM HORIZON

Regional Trading Arrangements• ASEAN Free Trade Area ~ 2010/2015

• ASEAN - China ~ 2010/2015

• ASEAN - Japan ~ 2012/2017

• ASEAN - Korea ~ 2012/Unstated

• ASEAN Economic Community ~ 2015

• ASEAN – India ~ ?

• ASEAN – Australia/New Zealand ~ ?

• East Asian Free Trade Area ~ ?

• Comprehensive Economic Partnership in East Asia (CEPEA) ~ ?

• European Union ~ ?

Future Outlook of Malaysia’sFuture Outlook of Malaysia’sExport PerformanceExport Performance

• Challenging short-term environment

• Total de-coupling scenario is unlikely

• Exact depth and duration of impact will depend on individual & collective actions

• Longer-term structural changes also require attention

• National and regional supply-side strategies and initiatives are in place and hinge on implementation effectiveness

• The extent to which they respond to demand-side changes, including those of importing country governments, remain to be seen

• Given speed of change, policy action deficits should be felt quickly on national welfare

CONCLUSIONS