Embed Size (px)

Citation preview

Design/Production: Malmer & Partners, Falkenbergs TryckeriPhoto: Bertil Strandell, Håkan Ludwigson, NASA and others

CONTENTS

1 The SKF Group

2 The SKF Group Divisions

4 Letter from the President

6 Board of Directors’ report

– Environment

10 Awards

11 World bearing market

12 SKF – the knowledge engineering company

18 Industrial Division

20 Automotive Division

22 Electrical Division

24 Service Division

26 Seals Division

28 Steel Division

30 Aerospace and other businesses

32 Financial objectives and dividend policy

33 Financial risk management

34 Sensitivity analysis

34 EMU

FINANCIAL INFORMATION

36 Consolidated income statements

38 Consolidated balance sheets

40 Consolidated statements of cash flow

42 Notes to the consolidated financial statements

55 U.S. GAAP

64 Parent Company income statements

65 Parent Company balance sheets

66 Parent Company statements of cash flow

67 Notes to the financial statements for

the Parent Company

73 Proposed distribution of surplus

73 Auditors’ report

74 Shares and shareholders

76 Board of Directors

78 Management

80 Seven-year review of the SKF Group

81 Words in SKF’s world

82 Financial glossary

83 Three-year review of SKF’s Divisions

Mission

SKF’s mission is to enhance and develop global

leadership in bearings, seals, related products,

systems and services.

The aim is to be the best in the industry at:

• providing customer value

• developing our employees

• creating shareholder value

Drivers

• Profitability

• Quality

• Innovation

• Speed

Values

• Empowerment

• High ethics

• Openness

• Teamwork

KEY DATA 2001 2000 1999

Net Sales, MSEK 43 370 39 848 36 693Operating profit, MSEK 3 634 3 674 2 520Profit before taxes, MSEK 3 120 3 002 1 769Additions to tangible assets, MSEK 1 403 1 388 1 230Earnings per share, SEK 19.04 17.23 9.76Dividend per share, SEK 6.00* 5.25 4.00Cash flow after investments, before financing per share, SEK 37.52 25.30 19.49Return on capital employed, % 14.9 16.2 11.2Equity/assets ratio, % 41.1 37.1 33.5Registered number of employees 38 091 40 401 40 637

* Dividend according to the Board’s proposed distribution of surplus.

1

•SKF is the leading global supplier of products, customer solutions and services in therolling bearing and seals business. SKF also has an increasingly important position inthe market for Linear Motion products, as well as high precision bearings, spindles,spindle services for the machine tool industry, electrical actuators and actuation systems.

• The solutions SKF offers its customers vary from high value-added sophisticated sys-tems with integrated electronic components to the right bearing, seal or actuator thatmeets the demands of a specific application. It also includes programmes that willimprove plant efficiency, and, with the help of advanced technology and maintenancemanagement, increase the customer's competitiveness.

• SKF has 79 manufacturing sites distributed all over the world. With its own sales com-panies in 70 countries, some 7 000 authorized distributors and dealers worldwide, itse-business marketplace and global distribution system, SKF is always close to its cus-tomers for the supply of both products and services.

• This truly global network, combined with the accumulated, deep and thorough knowledge of all the different applications and the expertise of SKF’s highly skilledemployees, places the Group in a unique position to supply all its customers with thebest possible solutions.

• From its very beginnings in 1907, SKF focused intensively on quality, technical development and marketing. It soon became the leading manufacturer in the bearingindustry, and has maintained this position ever since.

• The results of the Group’s efforts in the area of research and development have led to agrowing number of innovations that have created new standards and new products inthe bearing world. In 2001, 171 patent applications were filed by SKF.

• In 2001, SKF presented its by-wire technology to the automotive industry, demonstrat-ing its advantages for future generations of vehicles. By-wire engineering eliminatesthe need of hydraulic systems and offers designers cleaner, lighter, simpler and safersolutions. SKF has already been supplying the aircraft industry with this technologyfor almost two decades.

• Through its US-based oil seals company Chicago Rawhide (CR), SKF is a leadingsupplier of elastomeric seals to the North American market. CR has expanded its activities in recent years into Asia and Europe.

• The Group includes specialty steels operations, i e the manufacture and sale of bearingsteel and other high-quality steel grades.

• The Group has a global ISO 14001 environmental certification. The various Divisionsin the SKF Group have been approved for quality certification in accordance witheither ISO 9000 or QS 9000.

2

Business

Achievements

in 2001

In focus

Industrial Division

• Product development and productionof a wide range of bearings andrelated products.

• Development of special products andsystems for selected customer appli-cations.

• Sales to industrial OEM customers. • Operation of business areas for Rail-

ways, Linear Motion, Machine Toolsand Couplings. This includes productdevelopment, production and salesof high-precision bearings, railwaybearings, spindles and a wide rangeof linear products and couplings.

• Acquisition of Gamfior S.p.A. • Orders received for a new generation

of axle boxes for Siemens’ new trainconcept, ”Desiro”.

• The joint venture in Nankou, Chinareinforced its position as China’sleading supplier of taper roller bear-ing units to the Chinese railway OEMindustry.

• The CARB® toroidal bearing becamethe standard solution in the world’scontinuous slab-casting machines forsteel production.

• Sales to the windmill industry contin-ued to grow strongly.

• Roller Bearing Industries Inc receivedthe SECO award from TTX, the lead-ing freight car leasing company inthe USA, for outstanding quality andcustomer service.

• Launch of Engineering Services inEurope and in the USA.

• Higher frequencies and shorter leadtimes in manufacturing.

• Positive development of e-business.

• To continue to grow the business ofcustomized solutions, systems andsmart products integrating electron-ics etc.

• To reinforce the front line by recruit-ment of sales engineers.

• To lower the capital tied up in inven-tories and improve delivery servicesthrough flexible manufacturing.

• To continue the expansion of spindleservices and repair.

• To grow the business for linear actuators.

• To penetrate the market for SKF’srailway monitoring systems.

• To support the growth strategythrough selected acquisitions.

Electrical Division

• Product development and productionof all deep groove ball bearings with-in SKF.

• Sales of bearings and related products to manufacturers of electricmotors, household appliances, electric components for cars, powertools, office machinery and two-wheelers.

• Joint-venture agreement concludedto build a new factory manufacturingdeep groove ball bearings in China.

• Increased penetration of the marketfor two-wheelers in Asia. Sales grewby some 30%, well above the marketgrowth.

• Launch of new standard seals forsmall deep groove ball bearings.

• Implementation of new technologyfor cleaning rings that is environ-mentally compatible.

• To continue sales of sensor-bearingunits for electric vehicles.

• To increase business based on theDivision’s expertise in numerical simulation and advanced vibrationstudies.

• To develop, in partnership with cus-tomers, bearings for very high-speedapplications, mainly intended forhousehold appliances and auto-motive electrical components.

• To further expand the business inAsia.

Automotive Division

• Product development, productionand sales of bearings and relatedproducts to the global car, lighttruck, heavy truck, bus and vehiclecomponent industries.

• Development of kits for the globalvehicle service market.

• Sales to the vehicle service market in Europe, Brazil and India.

• To continue to expand the range ofvehicle service market parts andservices.

• To introduce the car-diagnostic prod-uct for the vehicle service market,built on SKF’s partnership with Infocar of Sweden.

• To develop supply and partnershiprelations for by-wire applications.

• To continue to develop and sellvalue-added products and serviceswhich benefit both customers andSKF.

• To continue the drive for greater flexibility in manufacturing.

• To continue to drive Zero Defect inall business processes.

• The FILO Drive-by-Wire concept car, developed in collaboration withBertone, was presented to the market.

• Increased flexibility in manufacturing,"Resetting at Formula One Speed".

• Introduction of new value-addedproducts such as the wheel hubbearing units HBU6, with integratedbrake disc rotor; HBU1R, a com-bined unit and integrated aluminumknuckle; and HBU ”Air Bearing”, aunit allowing compressed air to flowthrough the bearing to regulate tyrepressure.

• A newly developed car-diagnosticproduct for the vehicle service market.

• New businesses including bearingson Volvo Cars’ new SUV XC90, theJaguar X-Type, Ford Fiesta, Peugeot307 and the Honda Fit.

• SKF is a technical partner of Ferrari –winner of both the F1 world con-structor’s championship and the F1world driver’s championship in 2001.

3

Service Division

• Providing industrial end-users with afull range of bearings and relatedproducts and services through a net-work of authorized distributors.

• Development of knowledge-basedservice solutions to optimize plantasset efficiency through mechanicalservices, predictive and preventivemaintenance, condition monitoring,decision-support systems and performance-based contracts.

• Logistics services for internal andexternal customers.

• Expanded distributor e-commercewith endorsia.com™ andPTplace.com™.

• Formed the SKF Reliability Systemsbusiness unit.

• Signed maintenance service contractswith several major new customers.

• Extended the range of precision laseralignment instruments with SKFBeltAlign and SKF ShaftAlign. Intro-duced SKF System Multipoint, a centralized automatic lubricator.

• Opened a new and larger high-techdistribution centre in Singapore.

• Three new customers were added tothe external logistics services busi-ness.

• Acquired Nåiden Teknik AB, a condition-monitoring company.

• Formed an alliance with Vibro-MeterIndustrial and the Marine Division ofMeggitt PLC to develop new on-lineprotection systems with DYMAC.

• Formed an alliance with Goodyear toprovide value-added service for theindustrial power transmission marketin Brazil.

• To continue supporting distributorsthrough efficient logistics andincreased value-added product andservice solutions.

• To continue developing "smart"products, "smart" integrated sys-tems, mechatronic capability, andwireless technology.

• To launch the next generation ofWindows CE®-based, portable condition-monitoring equipment.

• To expand performance-based main-tenance management competence.

• To acquire additional maintenanceservice companies.

• To expand third-party contracts forlogistics operations.

Seals Division

• Product development, production,and sales of seals and sealing sys-tems for the automotive, industrialand electrical markets. The Divisiondevelops and markets seals for usein bearings both for SKF and exter-nal customers.

• Sales of bearings, seals and relatedproducts to the vehicle service mar-ket in North America.

• Development of a fully-automated,single-step magnetization process inthe production of a magnetic impulsering integrated into cassette seals.

• Introduction of SEALPOOL hydraulicsealing products via the SKF Euro-pean Distribution Centre to completethe sealing range for the aftermarket.

• At the Hanover Fair, SKF introducedmaintenance-free hydraulic cylinderkits combining CARB® toroidal bear-ings, plain bearings, rod ends andbushings.

• Launch of a new computerizedselection method for the optimumbearing and seal arrangement forhydraulic cylinders.

• Selected by Ford to supply wheeland axle seals for use by the Forddealer service departments asreplacements parts on Ford passen-ger cars and light-duty trucks inNorth America.

• Major awards received, e g Auto-motive Industries Magazine ”Questfor Excellence Award”.

• To exploit more synergies betweenbearings and seals for all marketsand to develop application-focusedsolutions by integrating the sealsbusiness within other Divisions.

• To continue to drive Zero Defect inall business processes.

Steel Division

• Product development, production,and sales of special steels and steelcomponents to the bearing industryand to other industries with demand-ing applications.

• Continued strong customer interest inthe cost-efficient and environment-ally-compatible air-hardening steelgrades. A third variant of thesegrades was introduced.

• Improved efficiency and economy inthe steel-making process from a newpower-supply equipment installation.

• The restructuring project in the de-partment for cold-worked tubes wascompleted, resulting in shorter leadtimes and increased productivity.

• Several new contracts were conclud-ed with external customers.

• To ensure SKF’s position as theleader in bearing steel and high-quality steel grades.

• To enlarge the European customerbase.

• To strengthen the sales organizationto give all customers better localservice.

• To increase the number of applica-tion engineers.

• To establish the air-hardening steelgrades with a defined number ofcustomers.

• To increase the share of cut andmachined components.

• To take measures for improved productivity and cost reduction.

Aerospace and other businesses

• Development, production and salesof bearings, seals and componentsfor aircraft engines, gearboxes andairframes.

• Services and repair of bearings forthe aerospace industry.

• Development, production and salesof forgings and rings.

• Five-year contract signed with GEAircraft Engines for the supply ofmain-shaft engine bearings.

• Agreement concluded with RollsRoyce to provide all the bearings forthe lift fan for the Joint Strike Fighterto be built by Lockheed-Martin.

• Contract for engine and gearboxbearing repair with Pratt and Whitneyfor their PW4000 programme.

• Launch of a new generation of com-posite rods for airframe applications.

• To establish new partnerships tostrengthen product and servicedevelopment.

• To remain the technical leader withinaero-engine bearings (polymeric,ceramic, sensors), rods (composite,sensors) and fly-by-wire.

• To strengthen SKF’s position withindifferent geographical areas.

• To increase the service performed atSKF´s service units in the USA and inEurope.

4

In spite of the downturn in globaldemand, the SKF Group achieved agood result in 2001. Earnings per

share increased by 10.5% to SEK 19.04.The cash flow was MSEK 4 271,a record high. The operating margindecreased slightly to 8.4%.

The Board of Directors has decided topropose to the Annual General Meetingthat a dividend of SEK 6.00 be paid forthe year. It represents an increase of 14%and reflects the robust performance andsolid financial position of the Group.

Total sales, recorded in local currencies,were fairly flat for the full year. Sales inEurope had good growth at the beginningof last year but decreased in the fourthquarter. In North America, salesdecreased considerably, although in thefourth quarter they were slightly higher,mainly for seasonal reasons. The annualsales in Asia increased and good growthwas noted in the fourth quarter.

The Group’s production levels and thenumber of employees were graduallyreduced during the year to adapt to thelower market demand and to continue thereduction of inventories.

There are signs that a recovery in marketdemand could start already during thecourse of this year. The first quarter,however, is expected to be weak and theproduction volume will be considerablylower than that recorded for the sameperiod last year.

The strategy to reshape the SKF Groupfor long-term profitable growth continuedand major progress was made in a num-ber of areas last year.

The price level was further improvedthrough the strong focus on businesseswith higher customer value and bettermargins.

The work to improve the balance sheetresulted in a major reduction of net bor-rowings, a higher equity/assets ratio andlower cost for the financing of the Group.

SKF’s aftermarket business generatedgood results. The vehicle service busi-ness continued to grow and SKF’s net-work of industrial distributors in Centraland Eastern Europe and Asia was furtherexpanded. The number of long-termmaintenance contracts in the processindustry also increased substantially.

The improvement of SKF’s global logis-tic system and the enhancement of Inter-net trading secured world-class perform-ance in serving customers promptly andefficiently with the maximum of reliability.

Comprehensive efforts were made inbringing new technology and customizedproducts and solutions to the market.Good results were achieved in a numberof application areas in the printing, steel,marine, railway and windmill industries.Important long-term contracts were alsosecured in the automotive and aerospacefield.

The redesigning of SKF’s factories andprocesses for fast and reliable deliveriesof a wide range of high-quality productscontinued. The resetting times for themanufacturing channels were reduced forefficient manufacturing of smaller batch-es with shorter lead times and with lowerinventory levels. The total inventories toannual sales ratio was decreased to 21%at the end of the year, in line with theobjective.

A comprehensive cost reduction and out-sourcing programme was carried out during the year. SKF’s IT activities weretransferred to EDS during the autumn.The use of flexible working hours, short-time work and the reduction of the number of employees contributed to afavourable productivity development.

A number of acquisitions were made inorder to support the growth strategy inselected areas. Adding the Gamfior andMagnetic companies to the business areaSKF Linear Motion and Precision Tech-nologies has created excellent marketpositions in the machine tool spindle andactuator businesses.

The ambition is to make acquisitions thatcan contribute to the growth of profit pershare and add some 2-3% extra sales volume to the Group annually.

As an addition to SKF’s R&D pro-gramme, which aims to improve quality,technical performance and reduce thecosts of its core products, new intelligentproducts and systems with electrical,electronic and software content are beingdeveloped. The engineering capacity inthis field comprises some 300 engineersat present.

The development of drive-by-wire prod-ucts and systems for the next generationof cars and trucks is a good example ofSKF’s new direction. Last year, a conceptcar with SKF’s drive-by-wire technology,developed together with the Italian de-sign company Bertone, was presented tothe market.

Last year, SKF also continued its workon contributing to a sustainable develop-ment in the world. The global ISO 14001certification has been renewed for

5

another three years. New products aimingat reduced energy consumption and newprocesses for cleaner environment werelaunched. The zero-accident programmeresulted in a 35% reduction of the acci-dent rate and 39 manufacturing unitsachieved one year of zero accidents.

The robust performance last year indic-ates that the present target, an operatingmargin of 10% for the Group, is withinreach. It may require somewhat moretime than originally anticipated due tothe prevailing business climate.

Developing the competence of SKF’semployees is a key success factor. Prior-ity is being given to programmes whichfocus on delivering value to customersand also to those which aim to furtherimprove the leadership skills of our managers.

It is also important for the Group to addnew competencies. Consequently, a further reinforcement of the sales andengineering capacity through recruitmentis also being planned.

On behalf of the Board and Group Man-agement, I would like to thank all SKF’semployees most sincerely for their dedi-cated work and strong contribution toanother successful year.

Göteborg, January 29, 2002

Sune Carlsson President and CEO

The SKF Group’s operating profitin 2001 amounted to MSEK3 634 (3 674). Profit before taxes

rose to MSEK 3 120 (3 002). For theyear 2000, a non-recurring profit ofMSEK 100 was included. The Group’snet sales increased by 8.8%, from MSEK39 848 to MSEK 43 370.

The increase in net sales of 8.8% wasattributable to volume -2.0%, price/mix+1.8%, structure +0.5% and currencyeffects +8.5%.

The new Group strategy, introduced in1998, to change SKF by focusing onprofit before volume, reducing assets,exiting non-core businesses and develop-ing the service and the mechatronic busi-nesses, is now creating results. In spite ofthe drop in volume, SKF managed tomaintain its profit and margin at satisfac-tory levels.

The decline in volume was due toweaker market demand. Total sales,recorded in local currencies were fairlyflat for the full year.

The Group’s production levels and thenumber of employees were graduallyreduced during the year to adapt to thelower market demand and to continue thereduction of inventories. During the year,inventories in percent of annual saleswere reduced from 23.2% to 21.0%.

The number of registered employeeswas reduced during the year by 2 310.

SKF continued to prioritize profitabil-ity. Non-profitable businesses were dis-continued and every effort was made toadd to the range of value-added products.Some of the new products launched on themarket during the year were a new seal-bearing unit, a ceramic-coated, self-lubri-cating plain bearing and a new generationof compact taper roller bearing units forrailways. The drive-by-wire system forcars was also presented to the market.

SKF’s efforts to offer its customerssolutions that contribute to improvingtheir profitability are starting to pay off.A large number of new service contracts

were concluded during the year. Themajority of these contracts were withcustomers within the pulp and paperindustry, but customers in the petro-chemicals, mining, food and textiles segments, are now also signing contractswith SKF.

SKF increased its volumes to the Cent-ral and Eastern European markets. This positive development is the result of thedetermined efforts to establish SKF as aleading supplier to these markets.

In Central and Eastern Europe, SKFhas established a network of its own salescompanies and authorized distributorsthat is the most comprehensive in themarket.

Volumes in China continue to growfollowing five years of steadily increasingbusiness for SKF. A decision was takenduring the year to establish a new jointventure in Shanghai for the manufactureof high-quality deep groove ball bear-ings. Production is expected to start inlate 2002.

The Group also continued to grow inthe Linear business area through theacquisition of the Italian company, Gam-fior, a leading European manufacturer ofmachine tool spindles and ball screws.With this acquisition, SKF has positioneditself as one of the leading global suppli-ers of machine tool spindles as well as aservice provider.

SKF has also acquired the MagneticGroup (in January 2002), a Swiss-based,leading manufacturer of electromechani-cal actuators, motors, and complete actu-ation systems. Magnetic’s product range reinforces SKF’s position in the fast- growing market for electromechanicalactuators, and actuation systems.

SKF’s programme to reduce assets con-tinued and the company manufacturingsteel sheet components in Italy was soldto an Italian company. The Group’s inter-nal IT services were outsourced to EDSand some 700 employees were transferredduring the third quarter to EDS.

’

6

Net sales by customer segment 2001

■ Cars 18%

■ Trucks 5%

■ Vehicle replacement 9%

■ General machinery 13%

■ Specialized industry 8%

■ Customized engineering 7%

■ Electrical industry 4%

■ Aerospace 5%

■ Industrial distribution 31%

Net sales by geographical area 2001

■ Western Europe excl Sweden 47%

■ Sweden 4%

■ Central and Eastern Europe 3%

■ North America 26%

■ Latin America 5%

■ Asia 13%

■ Middle East and Africa 2%

7

To further broaden and strengthen thee-business marketplace endorsia.com™,SKF signed an agreement with Sandvik,Rockwell Automation, INA and Timkenby which these companies share the own-ership and use of the e-business market-place. The five companies are equal own-ers of Endorsia.com International AB.

The same companies, except for Sand-vik, set up a new company for the NorthAmerican market. It is called CoLinx andoperates the portal PTplace.com™ forthe industrial aftermarket.

SKF Logistics Services opened its newAsian distribution centre in Singapore atthe beginning of the year.

The Group’s financial net was MSEK-514 (-672). Earnings per share amount-ed to SEK 19.04 (17.23). The Group’sequity/assets ratio improved further dur-ing the year to 41.1% from 37.1% atyear-end 2000. During the year, MSEK 1 563 of the interest-bearing loans were

amortized. At year-end, the Group’sinterest-bearing loans totalled MSEK 3 541 (4 968) while pension liabilitiesamounted to MSEK 7 044 (6 746). Atyear-end, the Group had financial assetsof MSEK 6 797 (4 557), including short-term financial assets of MSEK 5 387 (3 481).

SKF’s capital expenditure in tangibleassets amounted to MSEK 1 403 (1 388).Depreciation according to plan wasMSEK 1 714 (1 572).

Of the Group’s total capital expendi-ture, MSEK 43 (47) were attributable toenvironmental investments, the aim of

which is to improve SKF’s environmentboth internally and externally.

Expenditure in research and develop-ment amounted to MSEK 871 (710), corresponding to 2.0% (1.8) of annualsales. Development expenditure for ITsolutions and customized designs is notincluded. The number of first-time patentapplications in 2001 was 171. The num-ber in 2000 was 144.

Geographical distribution of net sales, average number of

employees and tangible assets (percent)

26

1422

5 5 3 36 3 2 2 0

13 13 9

51

6063

■ Net sales ■ Average number of employees ■ Tangible assets

AsiaMiddle East and Africa

Central and Eastern Europe

Western EuropeLatin AmericaNorth America

A new solution for a seal/bearingunit for personal water craft hascontributed to a new generationof environmentally friendly high-performance engines for the SKFcustomer Bombardier-ROTAX inAustria.

ENVIRONMENT

SKF’s performance in the fields of en-vironmental care and sustainable devel-opment were recognized in 2001 by theGroup’s inclusion in the FTSE 4 Goodethical investment index, and by approvalfor the second year running by the DowJones Sustainability Group Index.

More units gain ISO 14001

SKF has a multi-site certificate to ISO14001, the international standard forenvironmental management. This certifi-cate covers the Group’s manufacturing,logistics and technical facilities. Six unitsrecently acquired by SKF were approvedto ISO 14001 in 2001, including the newSKF distribution centre in Singapore.The Group environmental certificate nowincludes 76 companies in 21 countries,and demonstrates SKF’s ambition towork to the highest standards in all thecountries in which it operates.

Towards zero accidents

SKF introduced a new health and safetyinitiative, ”Zero Accidents”, in 2000,which completed its first full year ofimplementation in 2001. The initiative isfocused on the attainment of zero work-related (recordable) injuries at all units,rather than the setting of annual targetsfor reduced injury levels.

A total of 39 SKF units completed atleast one year with zero accidents in2001. Employees in these units worked atotal of 3.6 million hours during 2000-2001 without any reported injury.

Environmental permits

The SKF Group has environmental per-mits and consents for all operations inevery country in which it has manufac-turing facilities. This includes the opera-tions at five units in Sweden, comprisingSKF Sverige AB and Ovako Steel ABand subsidiaries. The permits cover

SKF’s production of bearings, steel androlled bars.

The environmental impact of theGroup’s operations is mainly in the areasof waste disposal, emissions to air andwater, and noise. All impacts are con-trolled to ensure strict compliance withnational and local regulations.

SKF Environmental Report 2001

The Environmental Report, which is distributed with the Annual Report, is acomprehensive description of the Group’sactivities related to environmental man-agement, health and safety, and sustain-able development. SKF has adopted theSustainability Reporting Guidelines pub-lished by the Global Reporting Initiative(GRI) for its annual environmentalreport. The 2001 report complies closelywith the guidance on reporting of environmental, health and safety para-meters.

B o a r d o f D i r e c t o r s ’ r e p o r t

8

SKF Österreich at Steyr, Austria uses virtualreality simulators to train their fork-lift drivers.Trainees can learn to respond correctly to dan-gerous situations, without endangering them-selves or their fellow workers while they learn.

9

B o a r d o f D i r e c t o r s ’ r e p o r t

BOARD OF DIRECTORS

Activities of the Board of Directors of AB

SKF in 2001

The Annual General Meeting of AB SKF,held in the spring of 2001, elected eightBoard members. In addition hereto twomembers and two deputy members havebeen appointed by the employees.

The Board held seven meetings in2001. The Board adopted written rules ofprocedure for its internal work. Theserules prescribe i a

• the number of Board meetings andwhen they are to be held,

• the items normally included in theBoard agenda,

• the presentation to the Board ofreports from the external auditors.

The Board also issued written instruc-tions as to

• when and how information requiredfor the Board’s assessment of theCompany’s and the Group’s financialposition shall be collected andreported to the Board,

• the allocation of the tasks betweenthe Board and the President,

• the order in which the deputy Presi-dents shall act in the President’sabsence.

The Board has established a Remuner-ation Committee.

Issues dealt with by the Board duringthe year include i a acquisitions anddivestments of companies and the stra-tegic direction of the SKF Group.

Nomination of Board members

The following applied regarding thenomination process of the Board mem-bers who will be proposed by a group ofmajor shareholders for election at theAnnual General Meeting in 2002.

In November/December 2001, theChairman made an assessment of thework of the Board and its members dur-ing the year. He then met with represen-tatives of the Knut and Alice WallenbergFoundation and the Marianne and Mar-cus Wallenberg Foundation (together the”Foundations”) and presented his assess-ment of the need of special Board com-petence and compared such needs withavailable resources in the Board. Thenext step in the nomination process wasthat the Foundations conferred with agroup of major shareholders includingAlecta pensionsförsäkring, ömsesidigt, inthis question.

SKF supplies tailor-made solutions to ABB’s Compact Azipod® units that include thrust bearings, complete with housing on the thrust end. SKF also supplies the bearing on the propeller end of the shaft. On the larger podded propulsion units, SKF’s CARB® toroidal bearings have become the standard.

10

The quality of SKF’s products and services is highly esteemed.

Below is a list of some of the awards received by the Group in 2001.

Quest for Excellence Award

Automotive Industries Magazine, USA

Excellent Supplier Performance

BMW Munich, Germany

Supplier Award

Bosch, Germany

”Camillo” Award

Cecauto, Italy

Approved Supplier - 2001

Dana Spicer Axle Division, USA

Preferred Supplier Award for 2001

Dana Spicer Driveshaft Division, USA

Contribution to the victory in 2001

Superbike World Championship

Ducati Corse, Italy

Quality and Service Award 2000

Ducati Motor Holding, Italy

Good Supplier Performance - 2001

Ejes Tractivos, Mexico

Export - Ar Award

Export.Ar Foundation, Argentina

Q1 Quality Award Renewal 2001

Ford Engine, USA

Certificate of Merit, Best Supplier

Ford Engine Plant Cologne, Germany

Supplier Quality Award - 2001

Ford Essex Engine Plant, USA

Q1 Quality Award

Ford, Mexico

Frost & Sullivan 2001 Market Engineering

Awards in X-by-wire Technologies

Frost & Sullivan, USA

Best Banner 2000

German Industrial Press Association,Germany

Recognition Certificate 100% On-time 2001

GM Service Parts Operations, USA

Partner Award

Iskra Avroelektrika d.d., Slovenia

Top Supplier Performance Award

ITT/Goulds Pumps, Industrial Pump Group, Seneca Falls Operation, USA

Good Supplier Performance - 2001

John Deere, Mexico

Supplier of the Year

John Deere, USA

’JIT - DELIVERIES’

Lucas-TVS Limited, India

Top Five - the best industrial bearing brand in

Brazil

Lund Group, Brazil

The Supplier of the Year 2000

Magneton, Czech Republic

Mazda Zero Defect Award – Recognition of

Outstanding Quality Performance

Mazda, Japan

NAPA Excellence Award for Outstanding 95+

Delivery Performance

NAPA, USA

Approved Supplier

NASA Space Shuttle Program, USA

Outstanding Supplier Award

National Machine, USA

Autop of Mind 2001 - the best automotive

bearing brand in Brazil

Novo Meio, Brazil

Product of the Year 2000 - Silver Award

Plant Engineering Magazine, USA

The Clean Industry Award

PROFEPA (the Federal Attorney forEnvironmental Protection), Mexico

Certified Supplier Status - 2001

Rolls Royce Allison, USA

Bearing Supplier of the Year Award

Siemens Automotive AG, Germany

Approved Supplier List

Stewart & Stevenson Tactical VehicleSystems, USA

Gold performance as call center in Brazil -

CRM Grand Prix 2001

Teleperformance Group, France

Certificate of Achievement

in Import Quality Performance

Toyota, Japan

SECO Award

Trailer Train Company (TTX), USA

Good Supplier Performance - 2001

Tremec, Mexico

Certified Supplier - 2001

Tuthill Pneumatics, USA

100% Supplier Quality Rating

Whirlpool of India Ltd., India

Preferred Supplier

Whirlpool of India Ltd., India

11

The world bearing market

By tradition, the size of the world bear-ing market has been defined by the globalsales of bearings. Measured as such, SKFestimates the market to be worth someSEK 200 billion per year.

The West European market has some-what less than 30% and the North Ameri-can slightly more than 30% of the mar-ket. The third largest market is Japanwith somewhat less than 20% of the mar-ket. Other markets that have a sizeablelocal production of bearings are Brazil,China, India and Russia.

SKF is today the world-leading bear-ing company and the largest supplier tothe markets in Europe, Latin America,Africa and the Middle East. SKF also

leads in Asia (excluding Japan). Theother major international bearing com-panies are INA (including the recentlyacquired FAG) in Europe, Timken andTorrington (which is part of IngersollRand) in the USA, and NSK, NTN andKoyo in Japan.

The bearing business is to a largedegree regional. Most of what is sold inEurope is manufactured in Europe, andmost of what is sold in North America isalso manufactured within that region.The same applies to the business inJapan. This means that SKF’s main competitors vary between the differentregions.

SKF is now making inroads into theservice market and introducing new

concepts to the bearing world. It is notpossible at the moment to determine theexact size of this growing bearing servicemarket, or its boundaries. Companies aretoday focusing more and more on theircore business, and the outsourcing ofmaintenance activities to specialists is agrowing trend in many industries. SKF’ssales of services grew rapidly in 2001.

At the same time, SKF is supplyingthe world market with increasinglysophisticated products, many in whichelectronics are integrated into themechanical components.

Consequently, the SKF Group’s saleswill increasingly reflect the value that isadded and the service offering.

At W.H. Malcolm’s site, Glasgow, Scotland, an SKF Copperhead periodic condition monitoring sys-tem has been in use on a Powerscreen Chieftain 1800 mobile vibration screen since early 2001.

The SKF Copperhead system solution is installed worldwide on vibrating screens and crushersin the mining and mineral processing industries. The system - which is a unique combination ofExplorer bearings and/or CARB®toroidal bearings, and a fault-detection system - eliminatesunplanned downtime, reduces maintenance costs, and extends machine performance.

12

-

To successfully create value forcustomers, demands a deepunderstanding of what cus-

tomers specifically require and needwith regard to products and services.Original equipment manufacturers valuehow SKF’s knowledge can make theirproducts more competitive. For end-users, the aim is to ensure the maximumutilization of their assets in order toincrease their productivity and profit-ability. In the aftermarket, the key factoris to know what kind of products thecustomer needs, and to have these prod-ucts readily available.

The common denominator is know-ledge. Learning and the development ofcompetence is a never-ending processand SKF’s competitive advantage isdirectly linked to the know-how accu-mulated in the Group over decades.

SKF is continuously investing in pro-moting the competence of its employees

SKF’s leadership in the bearing business and the very strong position of its brand in the

bearing world are due to its competence in providing products and services that create

value for the customer.

Anticipating automotive customers’ demands drives SKF engineers to seek new value-added solu-tions, like the wheel hub bearing unit HBU6, shown here. This new and unique bearing design com-bines the weight advantage of a flanged bearing unit with an improved interface to brake disc rotors.

in order to ensure sustainable develop-ment for the company.

Some new, innovative and value-added products and services are present-ed in the text of the different Divisionsand some are described in the following:

SKF SensorMount system

Large SKF spherical roller bearings andCARB® toroidal bearings with taperedbore can now be delivered with an intel-ligent sensor that knows precisely howmuch the internal clearance has beenreduced. The newly patented methodhelps to ensure correct mounting, thusavoiding damage to the shaft/bearinghousing or reduced bearing service lifecaused by mounting errors. Since themounting can be done very simply, thetime for mounting can be reduced andthe bearing function guaranteed.

The information from the integralsensor - factory-fitted to the bearing - isprocessed in a hand-held SKF Sensor-Mount indicator that displays the actualvalue of the interference fit. The maincustomer groups benefiting from theSKF SensorMount system can be foundin the heavy process industries such asthe paper industry, mining and mineralprocessing.

ON0FF

CLR MAX

0,450

TMEM 1500SensorMount Indicator

SKF SensorMount system helps to ensurecorrect mounting of bearings.

13

Condition-monitoring software

The next generation of condition-moni-toring software, called the SKF MachineAnalyst - a support for reliability tech-nology - was released in 2001. The SKFMachine Analyst is the core componentin a suite of complementary softwareapplications with extensive customizedfeatures that give users complete controlover condition-monitoring data, as wellas analysis and reporting.

SKF Machine Analyst is built uponMicrosoft’s® platform (Windows 2000and NT 4.0), and takes full advantage ofthe MS Windows® functionality and features. It can easily and effectively beintegrated with third party plug-ins.

SKF Machine Analyst also offers anumber of time saving features. TheScheduler allows a user to automaticallyschedule key operations. An Alarm Wiz-ard automatically calculates, with mini-mal effort, a reliable set of alarm criteriatailored to specific machinery. Anadvanced report generation function pro-vides Internet ready, HTML output filesfor easy and effective communicationand decision-making throughout theplant.

Decision-support system for selecting

bearing lubricants

Selecting the correct lubricant for anapplication is critical to obtaining thelife expectancy of bearings in operationin the field. SKF’s customers and thecompany’s own application engineersneed fast reference systems that remainupdated in order to continually make thecorrect selection for the many thousandsof applications where SKF’s products areused.

SKF has developed a new method forselecting the correct greases. LubeSelectis an expert system that combines SKF’sdeep understanding of greases and theirlubrication mechanisms.

The SKF Speed Tracker

SKF’s products for in-line skates havebeen developed to include a sensorisedbearing that is combined with a com-plete wireless radio transmission systemplus an electronic wrist-worn display.The system, called the SKF SpeedTracker, gives the skater details of thespeed, the distance covered and the skat-ing time, and also provides a stopwatchand a training programme with targetzones.

New hybrid bearings

A significant breakthrough made by SKFAeroengine, through its partnershipswith key customers, was the develop-ment of a process to manufacture ceram-ic (silicon nitride) rollers in productionquantities. These hybrid roller bearingswith their combination of ceramicrolling elements in traditional bearingconfigurations offer many advantagesand are expected to constitute a signific-ant proportion of SKF Aeroengine’sfuture products.

New knowledge about bearing fatigue

Fatigue phenomena of engineering mate-rials often limit the performance of high-ly loaded bearings made of hardened

bearing steel. A new approach in under-standing the fatigue mechanism, theThermo-Mechanical Response (TMR)technology, has been developed at SKF.TMR is based on a fundamental metal-

The LubeSelect system can be accessed bySKF's application engineers via the SKFIntranet 24 hours a day.

The SKF Speed Tracker provides the inlineskater with information of speed, distance andskating time.

SKF Aeroengine has developed a process to manufacture ceramic rollers in industrial quantities.

14

S K F - t h e k n o w l e d g e e n g i n e e r i n g c o m p a n y

lurgical view of the response of the mate-rial to the operating conditions where, inaddition to the bearing load, the operat-ing temperature, in particular, plays animportant role in the fatigue process.

One application of TMR is in the‘Remaining Life’ model for bearings. Bymonitoring the micro structural changes,using X-ray diffraction, the remaininglife of the bearing can be determined.This approach leads to improved recom-mendations, either for the bearing steeland heat treatment combination or for theapplication conditions of the bearing.

New materials to meet new challenges

Aerospace bearings, used in criticalapplications and often hostile environ-ments, are required to operate at highspeeds and at elevated temperatures forprolonged periods of time. As applica-tions have become more demanding, sohave aeroengine bearing designs andcomponent materials. Research by SKFAeroengine has led to a whole new gen-eration of high-performance bearings,

Pictured is the Pratt & Whitney PW4000 112-inch fan engine, used in the Boeing 777 commercialtransport. The SKF company, MRC Bearings manufactures all five of the main engine bearings,which take thrust loads of up to 500 kN in this critical application.

Ball Bearing

Roller Bearing

Roller Bearing

Roller Bearing

To meet the specific requirements of customers, customer groups or specific applications,

SKF is developing customized solutions for a special product or service. Some examples follow below.

Ball Bearing

Wind energy is a fast-growing and interesting industry for SKF. Market growth is reaching morethan 20% per year, and SKF’s sales to this industry doubled in 2001. The picture shows a numberof wind turbines from Vestas at Vancycle Ridge, Oregon, USA.

coatings, seals and lubricants. Today,researchers at MRC Bearings and SKFAvio are studying the key attributes ofpotential steel alloys for aero-enginebearing applications and their mechani-cal/physical properties, including hothardness, fracture toughness, corrosion

and wear resistance, structural fatiguestrength and rolling contact fatigue life.Research and engineering resources arecommitted to meeting the challenges ofthe aerospace industry today, and toanticipating customer needs well into thefuture.

Wind energy

SKF has cooperated closely with leadingwind turbine manufacturers for severalyears, and supplies a great number ofbearings such as main bearings, bearingsfor the transmissions, generators andblade pitch systems. SKF also supplieshydraulic coupling systems, lubricantsand other items. Specially developedtools, the SKF proprietary computer pro-grams BEAST and Orpheus, for example,are used for improving the design of thewind turbine’s complex dynamic system.

During the year, SKF signed multiple-year contracts with two of the world’slargest manufacturers of wind turbines,the Vestas Group in Denmark andGamesa Eolica in Spain.

15

S K F - t h e k n o w l e d g e e n g i n e e r i n g c o m p a n y

Condition monitoring of NASA Crawler

To move the 8.6-million kilogram NASA Space Shuttle from its 160-metrehigh Vehicle Assembly Building to thelaunch pad four kilometers away at CapeKennedy requires the power of an enormous vehicle, the NASA Crawler.

In 2001, SKF designed and installed,on a demand from NASA, an on-linecondition monitoring system for thecrawler. The system included eight SKFLocal Monitoring Units, 220 accelero-meters and the PRISM4 monitoring soft-ware along with systems engineering,installation supervision and system commissioning.

The NASA contract exemplifies SKF’sexpansion beyond its traditional bearingbusiness and resulted in SKF beingawarded ”Approved Supplier” by theNASA Space Shuttle program.

NASA has chosen an on-line SKF monitoringsystem for its huge Crawler.

16

S K F - t h e k n o w l e d g e e n g i n e e r i n g c o m p a n y

Deepwater piping

A new pipe-laying vessel from Technip-Coflexip, the CSO Deep Blue, is extend-ing the limits of what is possible in deep-water pipelaying. It has the capacity tolay more pipes deeper than any previousvessel from a pair of huge reels. Thedesign of the reels enables pipes to be welded onshore and then continuouslylaid at sea in lengths of up to 12.5 kilo-metres of 400-millimetre pipes or 333kilometres of 60-millimetre pipes. Thebearings and their housing had to bedesigned to allow the rotation of thereels in seas with up to a four-metre sig-nificant wave height, and to withstandextreme static survival load conditions.

SKF’s solution consisted of one spher-ical roller bearing weighing 5.5 tonnesand another 9.5 tonnes – the heaviestspherical roller bearing ever made bySKF. The housings, the largest ever builtby SKF, consisted of one pair, eachweighing 34 tonnes, and another pair,each weighing 26 tonnes. Special greasewas developed to lubricate the bearings.

Kenneth Berkenäs is reading the test resultsfrom the rod seal test equipment at Sealpool'slaboratory in Landskrona, Sweden.

Total system approach - hydraulic

cylinders

The acquisition of Sealpool AB enabledSKF to add an important complement toits Chicago Rawhide range of sealingproducts. The Sealpool hydraulic sealingproducts, with over 2 800 part numbers,were made available through the SKFEuropean Distribution Centre in June2001. During the Hanover Fair, SKFintroduced maintenance-free hydraulic

cylinders based on the systems-solutionapproach combining CARB® toroidalbearings, plain bearings, rod ends andbushings together with Sealpool sealingproducts. This launch has featured acomputerized selection and applicationtool for selecting the optimum bearingand seal arrangement for hydrauliccylinders, and is just one example of the synergies available through moreintegrated bearing and sealing solutions.

The CSO Deep Blue from Technip-Coflexip is equipped with the heaviest bearings and bearinghousings ever built by SKF. The two spherical roller bearings and the four housings have acombined weight of over 130 tonnes.

17

S K F - t h e k n o w l e d g e e n g i n e e r i n g c o m p a n y

Extending the limits of the possible with

NoWear™

Today’s high-speed newsprint papermachines feed out paper at a speed of1.5 km per minute, or more. The fasterthe rolls of a paper machine turn, thehigher the output. With SKF’sNoWear™ solution, machine speed,paper output and productivity haveincreased significantly.

NoWear™ bearings contain a low-friction ceramic coating to prevent

failure. Stora Enso’s German Maxau high-speed newsprint mill has used NoWear™ bearings in the calender/finishing section for some years withincreased productivity as the very suc-cessful result. The year 2001 is consid-ered by SKF as a customer breakthroughyear and orders have been received frommills all around the world.

Continuous running with NoWear™ in the cal-ender section at Stora Enso Maxau. KarlheinzSinn, maintenance manager Stora EnsoMaxau, is discussing the importance of a highutilization rate with Thomas Metz, SKF distrib-utor, and Udo Schubert, application engineer.

Victoria Wikström, product manager NoWear™and Rickard Gåhlin, Balzers Sandvik Coating,in discussion over a new bearing range. Thepartnership between SKF and Balzers SandvikCoating AB has been successful in the market-place.

The SKF Group established a new Manufacturing Development Centre(MDC) in Göteborg, Sweden in 2001.The MDC is designed to be a modernworkplace for the future which offers achallenging working environment, andwhich stimulates creativity and interdisci-plinary teamwork. It is divided up into anoffice area and a laboratory where newand rebuilt machines will be evaluated

and tested. This new centre is today homefor some 55 researchers. High-perform-ance machines and equipment have beentransferred from Italy, Austria, the Net-herlands and Sweden. The new centrewill focus on the development of newadvanced technologies. These will thenbe the base for creating new efficient processes enabling SKF to develop andmanufacture products in response to

tomorrow’s market demands. The R&Dincludes the 7entire manufacturing process from the raw material to an as-sembled and packed bearing. Simulationtechnology will be deployed to facilitatea quick reply to customers’ requests,including the optimisation of customerapplications.

New Group Manufacturing Development Centre

18

External sales in 2001 amountedto MSEK 9 852 (8 727), anincrease of 12.9%. Total sales

(sales to external and internal customers)were MSEK 16 027 (14 544). The oper-ating result was MSEK 1 670 (1 665)with an operating margin of 10.4%(11.4).

Despite the slowdown in sales andlower manufacturing volumes, the operat-ing result remained on a satisfactorylevel, comparable to the level in 2000.

Sales in Europe started the year on ahigh level but declined during theautumn. Sales were low throughout theyear in North America. The business inAsia developed well, especially in China.The joint-venture factory for railwaybearings in Nankou achieved a recordoutput for the second year running.

Excellence in product quality, deliveryservice and attention to customers headedthe Division’s agenda last year. The

numerous ”Excellent Supplier” awardsreceived confirm how well these goalswere achieved.

Improved flexibility in manufacturing,the further reduction of lead times,increased production frequencies plusmore robust manufacturing processesallowed the Division to simultaneouslyreduce the capital tied up in inventoriesand improve its delivery service.

In anticipation of slower sales, a reduc-tion in the capacity was already startedduring the fourth quarter of 2000. Thisearly reaction, in combination with flexibleworking-time contracts, enabled SKF to be well prepared to meet with the reducedmarket demand.

The outsourcing of non-critical activ-ities and indirect services is ongoing witha positive effect on the fixed costs. All thelogistic and transport activities at the fac-tory in Steyr, Austria, for example, havebeen outsourced to an external partner.

The work to build up the competenceto become a solution provider continuedand contributed to the improvements insales and price development. Cross- geographical and cross-functional teamsare being formed to focus on specificcustomers’ segments and/or large cus-tomers.

In 1999, a special Wind Energy groupwas set up, comprising people from manufacturing to sales, and with skillsranging from theoretical calculations tofield-testing. A large number of orderscontributed to a doubled growth withinthis segment. For example, SKF secureda major order from the world's biggestwind turbine producer, the Vestas Groupof Denmark. The two-year agreementcovers deliveries of bearings to Vestas’plants worldwide.

A similar approach has been taken formany other industries. A ConCast team isworking with all manufacturers and users

The Industrial Division is responsible for product development and production of a

wide range of bearings (in particular spherical, cylindrical and angular contact bearings)

and related products, and also for sales to industrial OEM customers. The Division

also operates business areas for Railways, Linear Motion, Machine Tools and Couplings.

In addition, the Division develops special products and systems for selected customer

applications to enhance the competitiveness of SKF’s customers.

Christer GybergPresident, Industrial Division

Hu HuiLi at work in the SKF Nankou factorywhere he and his colleagues achieved a recordhigh output in 2001 - more than 40% abovewhat was previously considered a full-capacitylevel - thanks to more efficient and flexibleworking methods.

This channel in the Steyr factory in Austria isan example of SKF’s ambition to increasemanufacturing flexibility. The result was a 50%reduction in the stock of finished goods,thanks to faster resetting and increased fre-quency, and even better service for customers.

Maurizio Marioni at work at the SKF Massafactory in Italy. In 2001, this Y-bearing channelreceived the SKF Gold award for running withzero defects for three years.

19

of continuous casters in the metal industry.During the year, they managed to establishthe CARB® toroidal bearing as the indus-try standard. The Division today offers awide range of tailored products and solu-tions ranging from separate bearings to”intelligent” roller assemblies includingstate-of-the-art sensors and electronicstechnology.

SKF’s team for the printing industrysecured breakthrough orders from theleading Japanese manufacturers of printing machines. SKF’s position as the main supplier to pod manufacturerswithin the marine world area was furtherreinforced.

The integration of sensors and elec-tronics into the products and systems isaccelerating. The first order was received

from the fork-lift truck industry for by-wire steering modules from Raymond inthe USA, and for sensor bearings fromCrown in the USA.

SKF is today the leading full-rangesupplier to the railway industry. Follow-ing close cooperation between Siemensand SKF, orders for SKF’s axle boxeswere received during the year as well asan order for a complete special axle forlow-floor street cars fitted with bearings,wheels, brakes, couplings, earth-returnsystems, and delivered as a ready-to-mount component.

The French manufacturer of cementequipment, FCB Ciment, chose SKF asits partner for the development of theoptimal bearing arrangements for theirnew, flexible cement grinder, ”Horomill”.

8 11

5

8 72

713 1

90

14 5

44

16 0

279

852

0

500

1 000

1 500

2 000

010099

1 02

9 1 67

0

1 66

5

0

100

200

300

400

500

010099

382

299

429

0

3 000

6 000

9 000

12 000

010099

10 3

30

10 2

46

10 5

55

0

5 000

10 000

15 000

20 000

010099

■ External sales

■ Total sales

■ General machinery 40%

■ Specialized industry 32%

■ Customized engineering 16%

■ Electrical industry 1%

■ Industrial distribution 9%

■ Cars 1%

■ Trucks 1%

Sales, MSEK* Operating

result, MSEK*

Additions to

tangible

assets, MSEK*

Registered

number of

employees*

External sales by customer segment 2001

Mounting an SKF spherical roller bearing on the main shaft of a wind turbine at the VestasWind Systems A/S, Denmark. SKF is the main supplier of bearings for Vestas wind turbines.The wind energy market grew strongly throughout 2001 and SKF sales doubled the same year.

During the year, the Division laun-ched a new Engineering ConsultancyBusiness Unit, which offers advancedengineering support to customers. In the startup phase, SKF focused on thesegments of industrial gearboxes and thefast growing wind turbine industry.

Linear Motion and Precision Techno-logies enjoyed increased sales to thefood, health care, medical and ergonomicsegments, while sales in the electronics-related segments and the machine toolindustry slowed down. The negative trendwas offset, however, by the developmentof new products and a growing serviceand repair business.

Two new companies were added to thebusiness area Linear Motion and Preci-sion Technologies. The first was GamfiorS.p.A. in Italy, a leading manufacturer ofhigh-precision motorized spindles, andhigh-precision ball screws for machinetools. Magnetic Elektromotoren AG inSwitzerland, was acquired at the begin-ning of 2002. The company develops,manufactures and markets electrical actu-ation products and systems for medical,industrial, health care, ergonomics andbuilding automation applications.

Major new functions were introducedin e-business. US customers can checkavailability, delivery status and the priceof their items via the marketplace,PTplace.comTM. The endorsia.comTM Lin-ear Webshop allows customers to easilyconfigure special products, for example,with automatic order-processing linkeddirectly to the manufacturing units.

*Previously published amounts have been restated to conform to current Group structure.

20

External sales in 2001 amountedto MSEK 9 719 (8 932), anincrease of 8.8%. Total sales

(sales to external and internal customers)were MSEK 11 155 (10 162). The oper-ating result was MSEK 305 (338) withan operating margin of 2.7% (3.3).

The result was on too low a level andwas slightly weaker than for the previousyear due to lower volumes in the truckbusiness.

Sales to the car and light truck indus-try in Europe started to develop positive-ly for the year but weakened as the yearprogressed. In North America, the levelwas lower than last year due to the reduc-tion in production and inventories ofvehicles.

The heavy truck market in Europedeclined. In North America, sales fellsharply for the second year running.

Sales in India, mainly of wheel hubbearing units, increased substantially tothe car segment, in spite of a relativelyflat level of car production in the country.Truck production in India and SKF’ssales to this segment declined during theyear.

Sales in Brazil developed positively inthe first half of the year, but as a result ofthe energy crisis in the summer the mar-ket decreased, and growth in the secondhalf of the year was not as strong.

SKF was very successful in gainingcontracts for the supply of bearings for a

number of important car models such asFord’s new Fiesta and Jaguar’s X-Type. Inthe heavy truck segment, SKF started tosupply new unitized wheel end bearingsin Europe to Scania for the front axle andin North America to Hendrickson for atrailer axle.

SKF supplies the Car of the Year inEurope - the Peugeot 307 - and the Carof the Year in Japan - the Honda Fit - andwill be the major bearing supplier for theVolvo Cars’ SUV XC90, which will gointo production in 2002.

The vehicle service market developedvery positively during the year owing toboth the addition of new and improvedproducts and to an expanded distributornetwork. An agreement with the Swedishsoftware company Infocar was concludedto develop and market a unique dia-gnostic software for repair and servicesfor cars. A cooperation was initiated with

Tenneco, TRW and Valeo to developimproved services for the European mar-ket. The focus is on training, technicalsupport services and logistics, particular-ly in transportation.

The FILO Drive-by-Wire concept car,developed jointly by SKF and the designcompany Bertone, was presented at theGeneva Motor Show. The car is the firstand only car featuring brake-by-wire,steer-by-wire, clutch-by-wire andgearshift-by-wire functions, all of whichwere developed by SKF. The brake-by-wire system was the result of SKF’s part-nership with Brembo, which wasannounced last year. There has been sig-nificant interest in SKF’s patented tech-nology in this area and discussions arebeing held with a number of manufactur-ers. SKF was selected by GM as thedrive-by-wire partner for their new versa-tile fuel cell concept car – Autonomy –

The Automotive Division is responsible for product development, production and

sales of bearings and related products to the global car, light truck, heavy truck,

bus and vehicle component industries and for sales to the vehicle service market in

Europe, Brazil and India. The product range includes wheel hub bearing units, taper

roller bearings, special automotive products and the specific kits for the vehicle

service market.

In the SKF factory in Cajamar, Brazil, produc-tivity increased by 30% in 2001 in the channelproducing taper roller bearings. This was achieved by combining SKF Reliability Systems’ technology and methodology withoperator-managed maintenance.

Fabrizio Sola at work at a new wheel hub bear-ing unit channel in Airasca, Italy. This channelis using new technology that provides fasterresetting and increased productivity.

Tom JohnstonePresident, Automotive Division

21

which was shown at the North AmericanInternational Motor Show in January2002.

During the year, 2000 people attended”The Value Leadership programme”. Theaim of the training is to further developvalue-added solutions for customers.

During the year, SKF launched a num-ber of new value-added wheel hub bear-ing units. The HBU6 is a unique wheelhub bearing design that combines theweight advantage of a flanged hub bear-ing unit with an improved interface to thebrake disc rotor. This hub unit can haveeither a normal steel disc rotor or a car-bon composite rotor. The HBU1R is anew innovative solution, which allows forsignificant weight saving by using a pro-

prietary closing technique to enable theunit to be fitted into a lightweight alu-minum knuckle. SKF also developed anew wheel hub bearing unit, HBU ”AirBearing”, for active tyre-pressure man-agement. It enables air to pass throughthe bearing to the wheel and tyre assem-bly. This new unit is a crucial element inthe development of the new MichelinWabco air-management system.

During the year, SKF and the Timkencompany formed a joint venture in Brazil,named International Component SupplyLtda, to produce forged and turned bear-ing rings. SKF also reached an agree-ment with SNR on the exchange and useof patents for the sealing of wheel hubbearing units.

Flexibility in production was verymuch in focus for SKF during the year.One example was an aggressive pro-gramme called ”Resetting at FormulaOne Speed”. The intention was todramatically reduce set-up times, therebyimproving the response to customerdemands and reducing capital tied up inthe business. One example of flexibilityis the new wheel hub bearing unit line inthe Airasca plant in Italy, where the adop-tion of simple modular equipment notonly enabled the line to produce moredemanding and tighter tolerances for theproduct but also to accommodate a number of different products on the samechannel.

The use of e-business was also infocus during the year, particularly in theaftermarket where the websitewww.vsm.skf.com was further developed,allowing customers to identify productsquickly and easily from a vehicle makeand model, and to find an authorizedSKF dealer of these products.

8 55

2

8 93

2

9 62

7

10 1

62

11 1

559

719

0

100

200

300

400

010099

172

30533

8

0

100

200

300

400

500

010099

329 42

6

379

0

2 000

4 000

6 000

8 000

010099

7 84

3

7 39

4

7 86

0

0

5 000

10 000

15 000

010099

■ External sales

■ Total sales

■ Cars 61%

■ Trucks 18%

■ Vehicle replacement 19%

■ General machinery 1%

■ Industrial distribution 1%

Sales, MSEK* Operating

result, MSEK*

Additions to

tangible

assets, MSEK*

Registered

number of

employees*

External sales by customer segment 2001

The SKF-Bertone FILO concept car is the first vehicle demonstrating thefreedom offered by drive-by-wire technology in the interior design. Steer-ing, brake, clutch and gearshift are all by-wire developments by SKF.Brake-by-wire has been developed in partnership with Brembo.

*Previously published amounts have been restated to conform to current Group structure.

22

External sales in 2001 amountedto MSEK 1 726 (1 575), anincrease of 9.6%. Total sales

(sales to external and internal customers)were MSEK 6 246 (6 268). The operatingresult was MSEK 372 (504) with anoperating margin of 6.0% (8.0).

Substantial falls in volume in Europeand the USA had a negative impact onthe Division’s results.

In Europe, sales were affected by theweakening of the economy and the two-wheeler segment suffered most. Saleswere more stable in the electrical seg-ment, owing to new businesses.

Sales in Asia increased strongly in2001 thanks to the introduction ofadvanced technical solutions. The training of customers and the offering of advanced calculation and simulationsoftware played an important role in thegrowing business in this market.

A joint-venture agreement was con-cluded with Shanghai Bearing (Group)Co. Ltd. to build a deep groove ball bearing factory in Shanghai to serve thefast-growing Chinese market with high-quality products.

One of the products introduced in2001 was a new standard range of smalldeep groove ball bearings. It has seals of

a new design that allow for better dustexclusion, grease retention and low friction, advantages that will benefit theenvironment and reduce energy con-sumption. In addition, a new bearingsolution, mainly for automotive, electri-cal and household-appliance applications,has been developed to cope with extremeconditions as regards speed and tempera-ture.

Sales of sensor-bearing units for elec-tric motor control, forklift steering, etc.,developed well. The business in Europeis expanding rapidly, and the Divisionalso gained an order from India for bear-ings for electric vehicle applications.

The Electrical Division is responsible for the product development and the production of

all deep groove ball bearings within SKF, as well as for sales to manufacturers of electric

motors, household appliances, electrical components for cars, power tools, office

machinery and two-wheelers. Of the Division’s total sales, 75% are made through other

Divisions.

This deep groove ball bearing channel in the Cassino factory in Italyimproved its productivity substantially during 2001, achieving a recordlevel of 2 800 bearings per hour.

Working closely with the customer Vorwerk in Germany, SKF developed a special type of high-speed ball bearing in 2001 for Vorwerk’s Kobold vacuumcleaner. The picture shows an assembly line at Vorwerk.

Giuseppe DonatoPresident, Electrical Division

23

1 47

5

1 57

5

6 06

6

6 26

8

6 24

61

726

0

200

400

600

010099

246 37

2

504

0

100

200

300

010099

203 221

193

0

2 000

4 000

6 000

8 000

010099

6 44

9

5 66

7

6 00

2

0

2 000

4 000

6 000

8 000

010099

■ External sales

■ Total sales

■ Electrical industry 71%

■ Two-wheelers 22%

■ General machinery 2%

■ Customized engineering 1%

■ Cars 2%

■ Vehicle replacement 2%

Sales, MSEK* Operating

result, MSEK*

Additions to

tangible

assets, MSEK*

Registered

number of

employees*

External sales by customer segment 2001

During the year, SKF implemented anew, environmentally-compatible clean-ing technology for bearing rings. Thismeans less pollution in the factories,which is of benefit for both working conditions and the global environment.

SKF sold its Italian-based productionof sheet-metal components such as cagesand shields to an Italian company specializing in sheet-metal pressing.

SKF is a technical partner for the two-wheeler racing teams of Ducati, Aprilia,Betamotor and Caltex Yamaha Indonesia.SKF engineers are working side by sidewith the racing teams’ technicians todevelop advanced solutions for increasedperformance and weight reduction.

As a technical partner for several two-wheeler racing teams, SKF is developing special technicalsolutions contributing to the success of the motorbikes.

*Previously published amounts have been restated to conform to current Group structure.

24

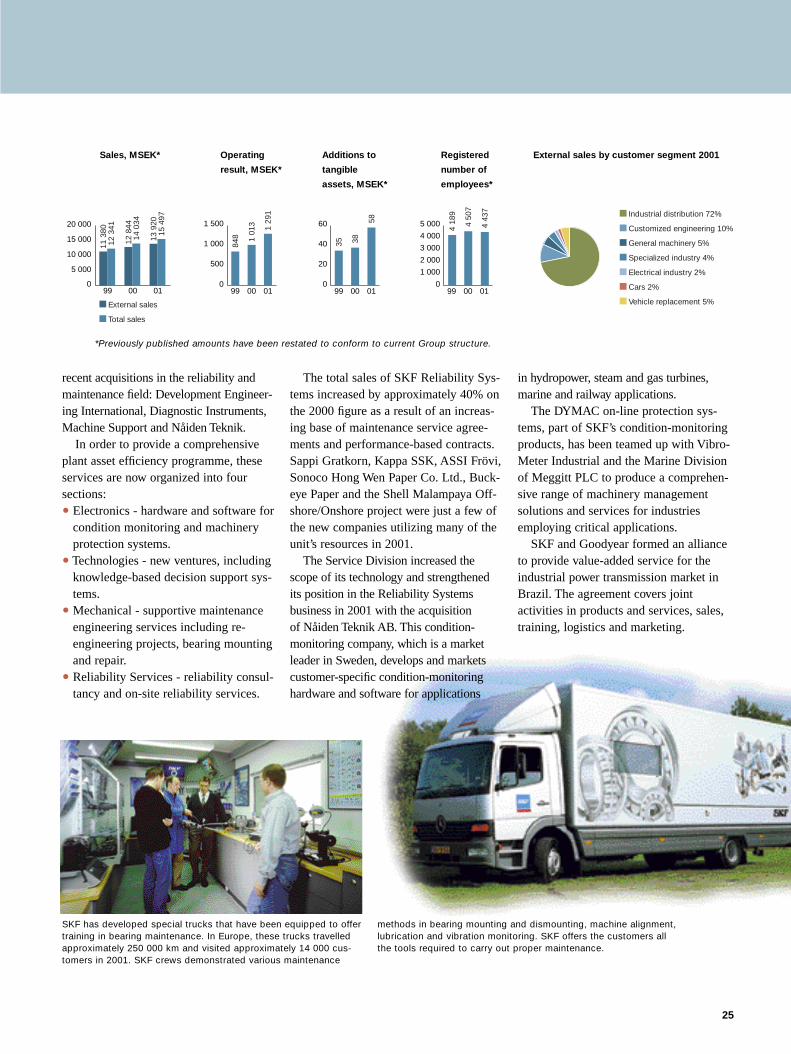

External sales in 2001 amountedto MSEK 13 920 (12 844), anincrease of 8.4%. Total sales

(sales to external and internal customers)were MSEK 15 497 (14 034). The oper-ating result was MSEK 1 291 (1 013)with an operating margin of 8.3% (7.2).

Efficient logistics, cost-effective opera-tions, and revenues from acquired com-panies, together with price increases andthe currency effect, contributed to animproved result.

Sales were strong in Western Europeduring the first half of the year, but thenweakened in the second half. In NorthAmerica, sales remained weak, buttowards the end of the year sales werehigher, mainly for seasonal reasons. Cen-

tral and Eastern Europe grew stronglywhilst the Middle East and Africa wereweaker than 2000. In Asia, there wasagain some solid growth, particularly inChina and South East Asia, whereasLatin America sales remained on the2000 level, but with demand weakeningduring the year.

Industrial Distribution

The core of the Division’s sales is com-posed of the business done primarilythrough its global network of authorizeddistributors and dealers. This highly efficient supply chain handles the dailyneeds of end-user customers requiringbearings and other products for mainten-ance and repair operations (MRO).

Greater efficiency in the supply chainwas achieved during the year through theexpanded use of endorsia.com™ andPTplace.com™ web-based marketplaces.These all-in-one service networks featurebranded industrial goods and endorsedmanufacturer know-how. Users can accessprice and availability, check order status,gain product knowledge, and place orders.

Order lines at the rate of approximate-ly one million per year are placedthrough endorsia.com™ andPTplace.com™. E-business in 2001 hasgrown tenfold since 2000. The globalimplementation continues and some 650distributor companies in 44 countries arenow registered.

Logistics Services

SKF Logistics Services operates a globaltime-phased delivery network, which provides excellent delivery servicearound the world. This is utilized by bothinternal SKF operations and a growingnumber of external customers.

SKF enhanced its global network inAsia with the move into a new and largerhigh-tech distribution centre in Singa-pore. A fully integrated tracking and tracing capability was also added to thenetwork during the year, enabling cus-tomers to keep track of their goods up tofinal delivery.

SKF Logistics Services gained threenew external customers in 2001. JohnsonPump contracted SKF to handle deliver-ies in Europe and its overseas cargos andairfreight activities. AvestaPolarit Weld-ing also turned to SKF Logistic Servicesto manage the company’s central stockkeeping and goods flow in Europe. ForJungheinrich, SKF set up and is runningtheir new Asia Pacific Parts Centre inSingapore.

Reliability Systems

During the year, the Service Divisionorganized its maintenance service opera-tions to form a new business unit called”SKF Reliability Systems”. The new unitincludes SKF Condition Monitoring,Dymac, SKF Decision Support Systems,and the SKF Industrial Service Centresaround the world. Also included are SKF’s

The Service Division is responsible for sales to the industrial aftermarket via a network of

some 7 000 authorized distributors and dealers. The Division also supports industrial

customers with knowledge-based service solutions to optimize plant asset efficiency

through its SKF Reliability Systems business unit which offers mechanical services,

predictive and preventive maintenance, condition monitoring, decision-support systems

and performance-based contracts. SKF Logistics Services, which is part of the Division,

deals with logistics and distribution both for the SKF Group and external customers.

Phil KnightsPresident, Service Division

Located in Havlickuv Brod and Brno in theCzech Repulic, the distributor Mateza utilizesendorsia.com™ e-commerce to manage its SKFbusiness activities. Besides supplying the com-plete range of SKF and CR products, it alsoprovides complementary products such as beltsand chains to meet customer needs.

recent acquisitions in the reliability andmaintenance field: Development Engineer-ing International, Diagnostic Instruments,Machine Support and Nåiden Teknik.

In order to provide a comprehensiveplant asset efficiency programme, theseservices are now organized into four sections:

• Electronics - hardware and software forcondition monitoring and machineryprotection systems.

• Technologies - new ventures, includingknowledge-based decision support sys-tems.

• Mechanical - supportive maintenanceengineering services including re-engineering projects, bearing mountingand repair.

• Reliability Services - reliability consul-tancy and on-site reliability services.

The total sales of SKF Reliability Sys-tems increased by approximately 40% onthe 2000 figure as a result of an increas-ing base of maintenance service agree-ments and performance-based contracts.Sappi Gratkorn, Kappa SSK, ASSI Frövi,Sonoco Hong Wen Paper Co. Ltd., Buck-eye Paper and the Shell Malampaya Off-shore/Onshore project were just a few ofthe new companies utilizing many of theunit’s resources in 2001.

The Service Division increased thescope of its technology and strengthenedits position in the Reliability Systems business in 2001 with the acquisition of Nåiden Teknik AB. This condition-monitoring company, which is a marketleader in Sweden, develops and marketscustomer-specific condition-monitoringhardware and software for applications

in hydropower, steam and gas turbines,marine and railway applications.

The DYMAC on-line protection sys-tems, part of SKF’s condition-monitoring products, has been teamed up with Vibro-Meter Industrial and the Marine Divisionof Meggitt PLC to produce a comprehen-sive range of machinery managementsolutions and services for industriesemploying critical applications.

SKF and Goodyear formed an allianceto provide value-added service for theindustrial power transmission market inBrazil. The agreement covers joint activities in products and services, sales,training, logistics and marketing.

25

11 3

80

12 8

44

12 3

41

14 0

34

15 4

9713

920

0

500

1 000

1 500

010099

848

1 29

1

1 01

3

0

20

40

60

010099

35

58

38

0

1 000

2 000

3 000

4 000

5 000

010099

4 18

9

4 43

7

4 50

7

0

5 000

10 000

15 000

20 000

010099

■ External sales

■ Total sales

■ Industrial distribution 72%

■ Customized engineering 10%

■ General machinery 5%

■ Specialized industry 4%

■ Electrical industry 2%

■ Cars 2%